market infrastructure developments impacting asian bond - citibank

TRANSCRIPT

Securities and Fund Services

Market Infrastructure Developments Impacting Asian Bond MarketsInsights | Institutional Clients April 2013

210mm

China

Hong Kong

Australia

JapanKorea

Taiwan

PhilippinesVietnam

SingaporeMalaysia

Indonesia

Thailand

India

Bond Markets in Asia Pacific

Contents

Asian Bond Markets 2

Asia Pacific Market Infrastructure Developments - Bonds

APAC Major Markets 7

ASEAN Markets 11

Major Registration Markets 16

Acronym Glossary 20

Contact Us 21

1 Citi Securities and Fund Services

Citi Securities and Fund Services

Asian Bond MarketsThe need to further develop the Asian bond markets has been a consistent theme ever since the 2008 global financial crisis. The Asia Pacific bond markets weathered the financial crisis well, and there was no dramatic decline in bond issuance. Indeed, bond markets in Asia continued to grow rapidly, with the size of local currency bond market increasing to USD25.5 trillion as of December 2012, recording growth of 11.0% year-on-year. This was supported by a combination of growth in both the corporate and government bond sectors.

Governments and central banks in the region have also been encouraging the expansion of the bond markets, which has led to growth in the domestic sovereign debt market.

The Asian corporate bond market, which underwent significant changes in the aftermath of 1998 Asia financial crisis, acted as a cushion for corporate financing during the global crisis. The markets operated as a balancing-act against fluctuating sentiment in global markets as well as slowing banking credit. Foreign participation in the bond markets was encouraged. Interest rate and liquidity risk exposures, as well as promoting borrowing in local currency have been great policy successes, especially in the emerging markets during the past decade. This has fostered the development of domestic bond markets. Governments and central banks in the region have also been encouraging the expansion of the bond markets, which has led to growth in the domestic sovereign debt market.

All these changes have led to a renewed awareness of the need to develop domestic financial and capital markets during periods of turmoil in the international financial markets. Policymakers in Asia have played a major role in developing efficient and liquid bond markets in Asia, as well as enabling better utilization of Asian savings for Asian investments. The policies implemented contribute to the mitigation of currency and maturity mismatches in financing and aim to establish a national and regional market infrastructure for bond market development.

Bond market development is significant not only as a way of reducing the region’s traditional reliance on capital flows, but also for its contribution to the expansion of domestic demand and as a driver of regional financial integration. As a result of the global financial crisis, there is more government cooperation.

The following are some key examples of recent developments in the Asian bond markets:

Asia RegionASEAN + 3 Bond Market Forum (ABMF)While significant developments have taken place in the local currency bond markets, intra-regional financial flows are still limited. In order to increase the use of regional savings/reserves to encourage a more active intra-regional bond market, the issuance and trading of local currency bonds is essential because it will channel regional resources to intra-regional investments, and will eventually lead to sustainable and balanced economic growth in the region.

The Association of Southeast Asian Nations (ASEAN), along with China, Japan and Korea established the ASEAN+3 Bond Market Forum (ABMF) in September 2010 as a common platform to foster standardization of market practices and harmonization of regulations relating to cross-border transactions in the region. ABMF reports its activities to the Task Force 3 (TF3) of the Asian Bond Markets Initiative (ABMI) under the institutional framework of ASEAN+3 Finance Ministers Meeting (AFMM+3). ABMF consists of two sub-forums: Sub-Forum 1 (SF1) researched, collated and compared regulations and market practices in the region, while Sub-Forum 2 (SF2) looked to harmonize transaction procedures across bonds market infrastructures in ASEAN+3 markets. National members and international experts (Citi is one of the international experts for ABMF) participated in the ABMF SF1 and conducted a survey on regional bond markets, and the legal and regulatory infrastructures in ASEAN+3 with support from the Asian Development Bank (ADB).

210mm

3

Market Infrastructure Developments Impacting Asian Bond Markets

Key output of the organization, which collaborated with the ADB, is the ASEAN+3 Bond Market Guide publication (http://asianbondsonline.adb.org/publications/adb/2012/asean+3_bond_market_guide.pdf).

The publication raised awareness and detailed how each market is structured, with the aim to encourage more cross-border bond issuance and investment in the region’s local currency bond markets. The report covers comparative analyses, as well as bond market guides for ASEAN+3 members.

Summary of findings

1 Over-the-Counter (OTC) Market: Bonds could be listed on the stock exchanges in many markets, but most of the instruments are traded on the OTC markets.

2 Bondholder Representative and/or Trustee: The concepts of bondholder representative, trustee and commissioned bank are gaining popularity and are evolving. For example, the new Commercial Code in the Republic of Korea, which came into effect in 2012, is redefining the role of commissioned banks.

3 There is an opportunity to propose a common self-regulatory framework for qualified market players in the future, so as to improve properly regulated and exempted private placement markets.

4 Two general approaches are observed in the markets when it comes to public offerings: (1) full disclosure with specific exemptions, and (2) a clearly defined disclosure regime.

The key objectives for ABMF Phase 2 will be to facilitate cross-border inter-regional initiatives of issuance and investment of bonds, and it might focus on private placements or exempted markets from full-disclosure requirements across jurisdictions. This might create a professional, organized and well-documented common regional private placement marketplace populated by qualified investors, and where the self-regulation concept would come in as part of discussions about effective governance.

Islamic Bonds (Sukuk)The value of Islamic financial assets have expanded from USD150 billion in the mid-1990s to USD1.3 trillion in 2011 globally, and reached

USD1.6 trillion as of the end of 2012. Indeed, Islamic finance is one of the fastest growing sectors within the global financial services industry, expanding at a rate of 10% to 15% per year with signs of consistent future growth. The market has increased since the Islamic Development Bank (IDB) opened in 1975 to finance economic development and foster social progress in compliance with Shariah principles, or Islamic law. Sukuk are one of the most prominent instruments used in Islamic finance, and have been commonly issued for raising funds in domestic and international capital markets.

Given the strategic importance and influence of investors from the Middle East, Islamic finance is increasingly in demand by investors. In recent years, several countries in East Asia, mostly those with large Muslim populations, have developed Shariah-compliant products and markets. Markets such as Malaysia and Indonesia had increasing demands for Islamic bonds after they launched their regulatory framework for the issuance of sukuk.

Malaysia continues to be the hub for Islamic financial services, while other countries are also launching their own regulatory framework for the issuance of Islamic bonds or sukuk in their respective bond markets, if they are not already in place. In essence, the risk exposure of investors for sukuk is not materially different from a conventional bond. If material difference exists, it is usually disclosed in the offering documents.

Pan-Asian CSD AllianceAs part of the continuing journey in deepening and strengthening the financial markets in Asia, to facilitate the Asian bond market development and to enhance the attractiveness of Asian debt securities to foreign investors, the Hong Kong Monetary Authority (HKMA) along with a group of central banks and central securities depositories (CSDs) in Asia, formed an alliance in June 2010 with Euroclear Bank and developed a common platform model. The Common Platform Model enables Asian CSDs to improve the cross-border post-trade infrastructure in Asia, to adopt harmonized procedures, shared technology in processing debt securities in a pragmatic and gradual approach, and to establish an intra-regional bond issuance program.

Islamic finance is one of the fastest growing sectors within the global financial services industry, expanding at a rate of 10% to 15% per year with signs of consistent future growth.

210mm

4

Citi Securities and Fund Services

Hong KongHong Kong is one of the most liberal debt markets in the world. International investors are free to invest in debt instruments locally, and there are no restrictions on foreign borrowers tapping the domestic debt market to finance their business. As of the end of 2012, it had an active and liquid private sector bond market of USD102.88 billion, accounting for around 38% of total outstanding Hong Kong dollar debt instruments while offshore RMB (CNH) debt instruments accounted for approximately 46%.

January 2007 marked a milestone development for Hong Kong’s debt market, when the Chinese government gave the green light to mainland financial institutions to issue RMB bonds in Hong Kong. The Hong Kong market of RMB bonds (known as dim-sum bonds) is the largest outside Mainland China. In 2012, 78 issuers raised a total of RMB 110 billion, which was three times the amount raised in 2010. Over the years, the range of issuers in the RMB bond market in Hong Kong has diversified from predominantly the government and banks in Mainland China to multinational companies (e.g. McDonald’s, Volkswagen) and international financial institutions (e.g. Asian Development Bank) and even non-bank institutions in Mainland China (e.g. Baosteel). Demand for dim sum bonds in Hong Kong continues to be strong from investors and central banks who want to diversify their investments or currency reserves into RMB, and to enjoy the benefits of a favorable tax and regulatory regime in Hong Kong. For example, dim sum bonds in Hong Kong are not subject to any withholding tax.

Hong Kong also remains as issuers’ country of choice for dim sum bond issuance, as it has the largest pool of RMB liquidity outside of Mainland China. Hong Kong is also playing a unique role in the internationalization of the RMB. During the early part of 2012, the Hong Kong Monetary Authority (HKMA) and the UK Treasury announced the launch of a joint private-sector forum to enhance cooperation

between Hong Kong and London on the development of offshore RMB business. On April 18, 2012, the first dim sum bond was sold in London. Hong Kong has also developed a highly efficient and reliable RMB clearing platform, the RMB Real Time Gross Settlement (RTGS) system, to support banks from all over the world in developing various kinds of offshore RMB business.

• The RMB RTGS system in Hong Kong is linked up with China National Advanced Payment System (CNAPS), the large-value RMB payment system in Mainland China.

• From June 2012, the operating hours of the RMB RTGS system was extended to 15 hours, serving from 08:30 to 23:30 (Hong Kong time). This facilitates financial institutions in different time zones to settle offshore RMB payments through the Hong Kong infrastructure.

• At the end of October 2012, there were a total of 202 banks participating in the RMB clearing platform in Hong Kong, of which 179 were branches and subsidiaries of foreign banks or mainland banks with an overseas presence. This has formed a global payment network covering more than 30 countries in six continents, capable of handling renminbi transactions between Mainland China and overseas and among different offshore markets.

ChinaThe China regulator recently allowed more international investors to buy bonds on the nation’s largest debt market, the Interbank RMB Bond Market and purchase higher-yielding notes for the first time, as the world’s second-biggest economy develops its capital markets. In addition to Hong Kong-based RMB clearing banks, financial institutions and assets managers, the China Securities Regulatory Commission allowed participants in the Qualified Foreign Institutional Investor (QFII) program to buy bonds on the Interbank RMB Bond Market. Previously, the QFIIs were restricted to buy exchange-listed debt,

Demand for dim sum bonds in Hong Kong continues to be strong from investors and central banks who want to diversify their investments or currency reserves into RMB, and to enjoy the benefits of a favorable tax and regulatory regime in Hong Kong. For example, dim sum bonds in Hong Kong are not subject to any withholding tax.

210mm

5

Market Infrastructure Developments Impacting Asian Bond Markets

Citi has been actively monitoring and assisting the market infrastructures in many of these developments. We have compiled a quick summary of key market infrastructure changes impacting bonds to help keep you abreast of these developments in Asia Pacific. We hope that you will find this snapshot useful and informative.

The China bond market is made up of the inter-bank bond market and the exchange-listed bond market. The inter-bank bond markets is an OTC market and accounts for about 97% of outstanding bond value, as well as 99% of bond trading volume.

which accounts for less than 3 percent of the interbank equivalent. There was RMB22.3 trillion (USD3.6 trillion) worth of bonds or securities traded over-the-counter (OTC) among commercial banks and other financial companies via the interbank RMB bond market, as compared with just RMB579.5 million worth of bonds on the exchange-listed market. The China bond market is made up of the inter-bank bond market and the exchange-listed bond market. The inter-bank bond markets is an OTC market and accounts for about 97% of outstanding bond value, as well as 99% of bond trading volume. The market was established in 1997 and has recorded an impressive average annual growth rate of more than 50% since 2005. The main products in the inter-bank bond market include cash bonds, government bonds, central bank papers, policy bank bonds, short-term papers, medium-term notes (MTNs), corporate bonds, local municipal bonds, asset-backed securities, collateral repurchases (repos), out-right repos, bond lending and the like. Currently, policy bank bonds, central bank paper and MTNs are the three most actively traded bonds in the inter-bank bond market. Currently, the interbank bond market has more than 10,000 members covering all types of financial institutions such as commercial banks, securities companies, insurance companies and various kinds of investment companies, such as mutual fund managers and pension funds. Among these, commercial banks are the most active participants.

The inter-bank bond market facilitates two trading modes: bilateral negotiations and market makers. The OTC bond market officially introduced the market maker mechanism in

2001 to improve market liquidity and enhance efficiency. At present, more than 25 market makers provide bid-offer quotes for underlying bonds that cover all types and terms.

China Foreign Exchange Trade System (CFETS) and the National Inter-Bank Funding Center have been operating the unified trading platform for the interbank bond market in China. CFETS has been operating the inter-bank bond market since 1997, and is now developed into a unique OTC electronic bond-trading platform in China with comprehensive functions of trade, post-trading service, risk management and information services (e.g. quotes and prices). There is a straight-through processing set-up between CFETS and the China Central Depository and Clearing Corporation Ltd (CCDCC) and the Shanghai Clearing House through which transaction data is transferred to the settlement system automatically.

210mm

6

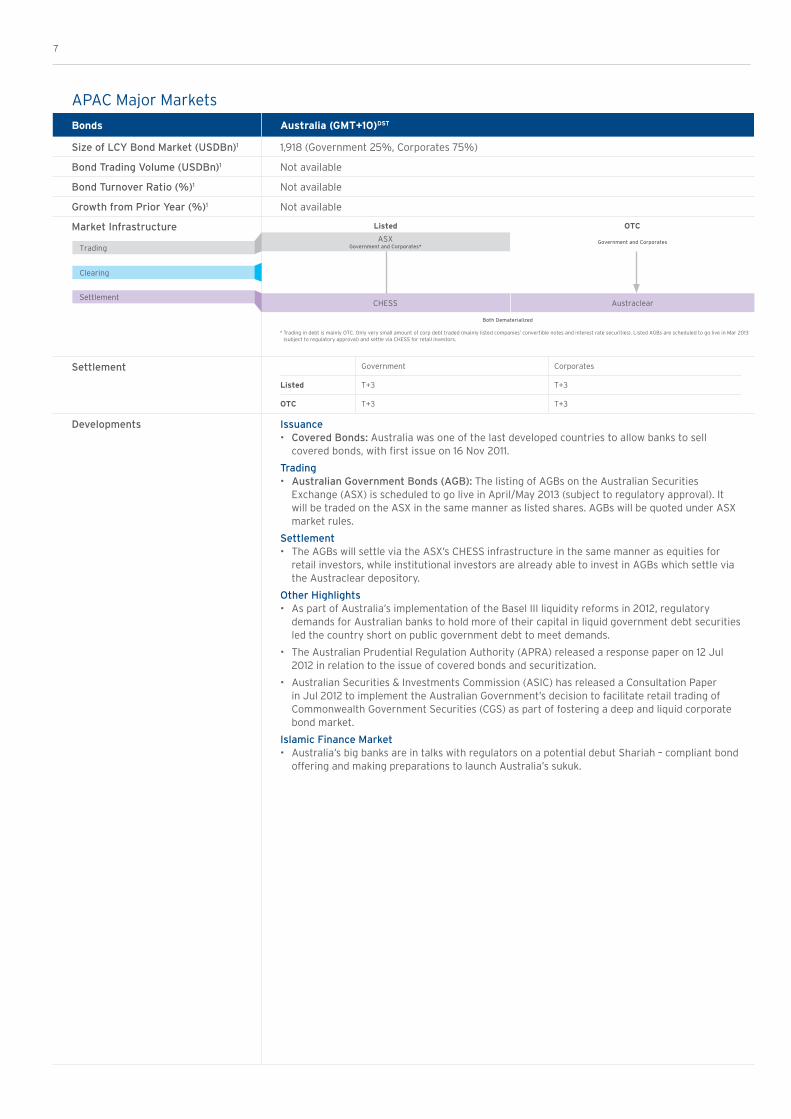

APAC Major MarketsBonds Australia (GMT+10)DST

Size of LCY Bond Market (USDBn)1 1,918 (Government 25%, Corporates 75%)

Bond Trading Volume (USDBn)1 Not available

Bond Turnover Ratio (%)1 Not available

Growth from Prior Year (%)1 Not available

Market Infrastructure Listed OTC

ASXGovernment and Corporates*

Government and Corporates

CHESS Austraclear

Both Dematerialized

* Trading in debt is mainly OTC. Only very small amount of corp debt traded (mainly listed companies’ convertible notes and interest rate securities). Listed AGBs are scheduled to go live in Mar 2013 (subject to regulatory approval) and settle via CHESS for retail investors.

Settlement Government Corporates

Listed T+3 T+3

OTC T+3 T+3

Developments Issuance• Covered Bonds: Australia was one of the last developed countries to allow banks to sell

covered bonds, with first issue on 16 Nov 2011.

Trading • Australian Government Bonds (AGB): The listing of AGBs on the Australian Securities

Exchange (ASX) is scheduled to go live in April/May 2013 (subject to regulatory approval). It will be traded on the ASX in the same manner as listed shares. AGBs will be quoted under ASX market rules.

Settlement • The AGBs will settle via the ASX’s CHESS infrastructure in the same manner as equities for

retail investors, while institutional investors are already able to invest in AGBs which settle via the Austraclear depository.

Other Highlights • As part of Australia’s implementation of the Basel III liquidity reforms in 2012, regulatory

demands for Australian banks to hold more of their capital in liquid government debt securities led the country short on public government debt to meet demands.

• The Australian Prudential Regulation Authority (APRA) released a response paper on 12 Jul 2012 in relation to the issue of covered bonds and securitization.

• Australian Securities & Investments Commission (ASIC) has released a Consultation Paper in Jul 2012 to implement the Australian Government’s decision to facilitate retail trading of Commonwealth Government Securities (CGS) as part of fostering a deep and liquid corporate bond market.

Islamic Finance Market • Australia’s big banks are in talks with regulators on a potential debut Shariah – compliant bond

offering and making preparations to launch Australia’s sukuk.

7

Trading

Clearing

Settlement

210mm 210mm

APAC Major MarketsBonds Hong Kong (GMT+8)

Size of LCY Bond Market (USDBn)1 178 (Government 53%, Corporates 47%)(Dim Sum Bond 45)

Bond Trading Volume (USDBn)1 165

Bond Turnover Ratio (%)1 Government (165%), Corporates (14%)

Growth from Prior Year (%)1 Government (-94%), Corporates (14%)

Market Infrastructure

Settlement Government Corporates

Listed T+2 T+2

OTC T+0 to T+2 (negotiable) T+0 to T+2 (negotiable)

Developments Issuance• Dim Sum Bond: RMB denominated bonds have developed rapidly since 2010 in response to the

growth in demand for RMB.

• On 14 Jun 2012, the Central Government issued offshore RMB sovereign bonds for the fourth time since the first issue in 2009, which was listed and traded on the SEHK on 3rd Jul 2012.

• As of the end of 2012, there were 47 bonds denominated in RMB listed on the SEHK.

Trading• Since 19 Aug 2010, HKEx supported the trading and clearing of products denominated in RMB.

Settlement• Pan Asian Bond Platform: HKMA, Bank Negara Malaysia (BNM) and Euroclear Bank developed

a common platform model to provide cross-border repurchase services, allowing banks to use bonds held through the platform as collateral for short-term funding in RMB, USD or EUR. A pilot platform for the cross-border investment and settlement of debt securities became operational on 30 Mar 2012.

Other Highlights • The People’s Bank of China (PBOC) has permitted some overseas insurance companies based

in China the right to invest in the China interbank bond market.

• On 12 Sep 2012, HKEx Information Services Limited (HKEx-IS) obtained approval from Chinese authorities to establish a financial information services business subsidiary in Shanghai to enable the delivery of broader HKEx market data products to Mainland information vendors, and subsequently to investors. This will also facilitate Mainland connectivity, and prompted Mainland investors to invest in securities and derivative products offshore.

• On 12 Oct 2012, the first dual counter (DC) security, the RQFII Exchange Traded Fund (ETF) was listed. One major benefit of a DC security for investors is the convenience of being able to trade in either one of the two currencies, while the benefits for issuers include a wider base of potential investors. Offering investors a choice of trading a security in RMB or HKD will further enhance HKEx’s position as a leading international market and Hong Kong’s increasingly important role as an offshore RMB centre.

Islamic Finance Market • The Hong Kong government launched a consultation on the legal and tax framework required

to support the development of Islamic financing in the region.

• In May 2012, the HKMA adopted a four part approach to boost the Islamic bond market, including 1) improving related financial infrastructures, 2) enhancing the international profile of Hong Kong, 3) promoting product development and 4) raising market awareness. Hong Kong also signed a Memorandum of Understanding (MOU) with Bank Negara Malaysia.

• Pan Asian Bond Platform aims to strengthen the cross-border issuance of, and foreign investment in local bonds in Hong Kong and Malaysia, which will spur trading of sukuk and dim sum bonds, as Hong Kong aims to become China’s hub for Islamic finance and offshore RMB transactions.

• The government has proposed a long-awaited amendment to the Inland Revenue Ordinance and the Stamp Duty Ordinance to give special tax treatment to four common types of sukuk traded globally: ijarah (asset-backed bonds), musharakah (bonds held by multiple parties), mudarabah (bonds held by one party) and the murabahah (in which there is a receivable debt on the sale of goods) to encourage firms to issue Islamic bonds in Hong Kong. The government will submit a bill for lawmakers’ approval during hearings in Oct 2013.

Listed (5%) OTC (95%)

SEHKGovernment and Corporates

Government and Corporates

HKSCC

CCASS CMU

Both Dematerialized

A bond can be transferred between CMU and CCASS for clearing and settlement (if it is an eligible listed instrument in both CMU and CCASS).

8

Trading

Clearing

Settlement

210mm

APAC Major MarketsBonds Japan (GMT+9)

Size of LCY Bond Market (USDBn)1 11,663 (JGB 92%, Corporates 8%)

Bond Trading Volume (USDBn)1 11,672

Bond Turnover Ratio (%)1 JGB (109%), Corporates (8%)

Growth from Prior Year (%)1 JGB (-2%), Corporates (4%)

Market Infrastructure

Settlement Government Corporates

OTC T+2* T+3

* Domestic trades only; offshore and cross-border trades are T+3 or negotiable

Developments Issuance • JGBs and Extra Budget: Japanese government bonds (JGBs) are the main bonds issued.

Reconstruction JGBs have been issued from fiscal year 2011 to finance the bulk of the spending on rebuilding from the Mar 2011 earthquake.

• 10-year inflation-indexed JGBs issuance is likely to be resumed after suspension from 2008, with some new product design.

Trading• OTC-only Market: always traded on an OTC basis, bilaterally between market participants.

• JBT as Trading Platform: 60% of the OTC bond trades are executed at the Japan Bond Trading Co. Ltd. (JBT), also known as the brokers’ broker (BB) in the market.

Clearing• Bilateral Netting: Except for JGBCC assumed trades, there is no centralized clearing process

for bilateral settlements; bilateral netting by trading parties is the market practice.

• JGBCC: the CCP acts as the clearing house for the OTC trades, currently utilized by broker/dealer community only.

Settlement• More JGBCC Coverage Expected: JGB clearing to be fully centralized at single clearinghouse,

Japan Government Bond Clearing Corporation (JGBCC) by participating domestic banks, trust banks and brokers in the first half of 2014 to reduce settlement and default risks.

• Domestic JGB Settlement Cycle Reduction: Japan Securities Dealers Association (JSDA) shortened the domestic JGB settlement cycle reduction from T+3 to T+2 in 2012, and there is continuous discussion on further shortening from T+2 to T+1.

Other Highlights• Tokyo Pro-Bond Market: Previously established as a joint venture, but it now became an

in-house market in TSE. It offers flexible and timely issuance of bonds, and provides more convenience to issuers, investors, securities companies and other market participants both in Japan and overseas.

• Revenue Bond: Effective 1 Apr 2012, revenue bond became Japanese Bond Income Exemption Scheme (J-BIEM) eligible instruments for non-resident investors, to allow tax exemption on interest arising from profit-linked bonds. It is specifically to be issued in the areas affected by the Mar 2011 Japan earthquake.

Islamic Finance Market • Tax regulations amended in 2011 to offer tax exemptions to sukuk, to bring more investment

opportunities for Islamic investors to the Japanese market.

• JASDEC started to handle J-Sukuk in its Corporate Bonds Book-entry System in April 2012.

9

OTC trades only

JGBCC

JASDECCorporates

BOJJGBs

Both Dematerialized

* All trading are OTC. Listing only remains on Tokyo Stock Exchange (TSE), but no trading.

Trading

Clearing

Settlement

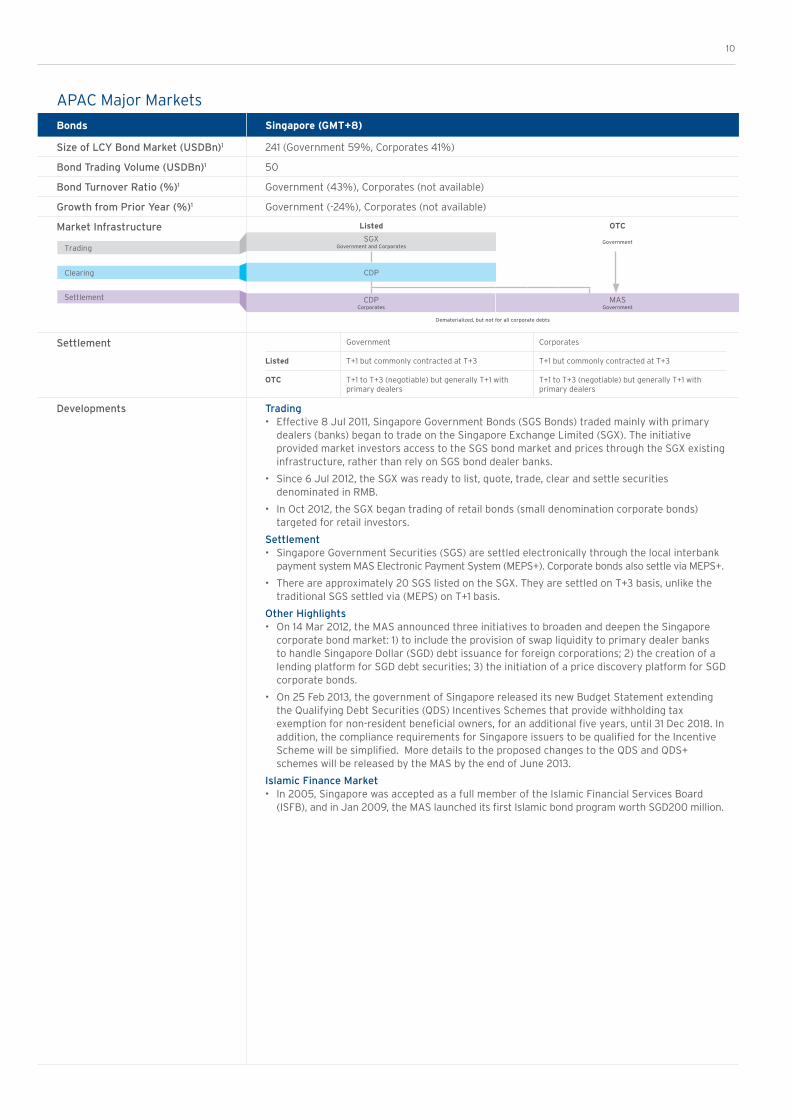

APAC Major MarketsBonds Singapore (GMT+8)

Size of LCY Bond Market (USDBn)1 241 (Government 59%, Corporates 41%)

Bond Trading Volume (USDBn)1 50

Bond Turnover Ratio (%)1 Government (43%), Corporates (not available)

Growth from Prior Year (%)1 Government (-24%), Corporates (not available)

Market Infrastructure

Settlement Government Corporates

Listed T+1 but commonly contracted at T+3 T+1 but commonly contracted at T+3

OTC T+1 to T+3 (negotiable) but generally T+1 with primary dealers

T+1 to T+3 (negotiable) but generally T+1 with primary dealers

Developments Trading• Effective 8 Jul 2011, Singapore Government Bonds (SGS Bonds) traded mainly with primary

dealers (banks) began to trade on the Singapore Exchange Limited (SGX). The initiative provided market investors access to the SGS bond market and prices through the SGX existing infrastructure, rather than rely on SGS bond dealer banks.

• Since 6 Jul 2012, the SGX was ready to list, quote, trade, clear and settle securities denominated in RMB.

• In Oct 2012, the SGX began trading of retail bonds (small denomination corporate bonds) targeted for retail investors.

Settlement • Singapore Government Securities (SGS) are settled electronically through the local interbank

payment system MAS Electronic Payment System (MEPS+). Corporate bonds also settle via MEPS+.

• There are approximately 20 SGS listed on the SGX. They are settled on T+3 basis, unlike the traditional SGS settled via (MEPS) on T+1 basis.

Other Highlights • On 14 Mar 2012, the MAS announced three initiatives to broaden and deepen the Singapore

corporate bond market: 1) to include the provision of swap liquidity to primary dealer banks to handle Singapore Dollar (SGD) debt issuance for foreign corporations; 2) the creation of a lending platform for SGD debt securities; 3) the initiation of a price discovery platform for SGD corporate bonds.

• On 25 Feb 2013, the government of Singapore released its new Budget Statement extending the Qualifying Debt Securities (QDS) Incentives Schemes that provide withholding tax exemption for non-resident beneficial owners, for an additional five years, until 31 Dec 2018. In addition, the compliance requirements for Singapore issuers to be qualified for the Incentive Scheme will be simplified. More details to the proposed changes to the QDS and QDS+ schemes will be released by the MAS by the end of June 2013.

Islamic Finance Market • In 2005, Singapore was accepted as a full member of the Islamic Financial Services Board

(ISFB), and in Jan 2009, the MAS launched its first Islamic bond program worth SGD200 million.

Listed OTC

SGXGovernment and Corporates

Government

CDP

CDPCorporates

MASGovernment

Dematerialized, but not for all corporate debts

10

Trading

Clearing

Settlement

1 1

ASEAN MarketsBonds Indonesia (GMT+7)

Size of LCY Bond Market (USDBn)1 111 (Government 83%, Corporates 17%)

Bond Trading Volume (USDBn)1 26

Bond Turnover Ratio (%)1 Government (29%), Corporates (12%)

Growth from Prior Year (%)1 Government (-1%), Corporates (42%)

Market Infrastructure Listed OTC

IDXGovernment and Corporates

Government

KPEIGovernment and Corporates

KSEI BI

Dematerialized

Settlement Government Corporates

Listed T+2 T+2

OTC T+2 (negotiable) T+2 (negotiable)

Developments Issuance• OTC trading of government bonds began in 2003.

• Sertifikat Bank Indonesia (SBI): Prior to Mar 2011, the Government issued treasury bills with a three month tenor. SBI was the main tool used by BI for open-market operations to control the liquidity of the banking system and the most actively traded money market instrument in Indonesia.

Trading• The holding period before investors can sell SBI to the secondary market was extended to six

months in May 2011.

• Although IDX provides facility to trade debt instruments in its Jakarta Automated Trading System (JATS), it is not used and instead, market participants usually trade and settle debt instruments off the exchange.

Clearing • ECLEARs — The Indonesian Clearing and Guarantee Corporation (KPEI) is the only Clearing

House in the Indonesian capital market. Its clearing system is called E-CLEARS (Electronic Clearing System). KPEI has established a STP linkage from brokers to the Clearing House in 2012.

Settlement • Settlement of Shariah government bonds is done through the Bank Indonesia Scripless Securities

Settlement System (BI-S4), a settlement system for government debt instruments.

Other Highlights • Bapepam-LK revised the regulation to have fund managers use bond pricing published by the

Indonesia Bonds Pricing Agency (PHEI), as the mandatory pricing source for fixed income.

• The Indonesian Bonds Pricing Agency (PHEI) began its plan to publish the fair market value (price) of Indonesian government bonds in foreign currency denomination (Indonesian Global Bonds) in Mar 2012.

• Bapepam-LK and the Indonesia Stock Exchange (IDX) plan to establish an Investor Protection Fund (IPF) in 2013 to help players on the capital market and investors in the event a broker becomes insolvent.

• Onshore commercial banks that participate in the trading of government debt instruments such as government bonds and treasury bills, are in discussion to possibly be eligible to become members of the Indonesia Stock Exchange (IDX).

• Indonesia’s central bank began buying RMB denominated bonds issued in mainland China, joining a growing number of countries moving to add the Chinese currency to their foreign-exchange reserves.

Islamic Finance Market • In Dec 2010, Bank Indonesia formed a committee with Shariah scholars to speed up the approval

process for new products. Indonesian Islamic bond sales are believed to recover from the slowest half in three years as the government finances transport and power projects, which ensure stable cash flows.

• The government offered as much as USD1 billion worth of dollar-denominated Islamic bonds in the second half of 2012 to finance its budget deficit.

Trading

Clearing

Settlement

12

ASEAN MarketsBonds Malaysia (GMT+8)

Size of LCY Bond Market (USDBn)1 327 (Government 60%, Corporates 40%)

Bond Trading Volume (USDBn)1 117

Bond Turnover Ratio (%)1 Government (54%), Corporates (10%)

Growth from Prior Year (%)1 Government (3%), Corporates (-5%)

Market Infrastructure

Settlement Government Corporates

Listed T+3 T+3

OTC T+2 (negotiable) T+2 (negotiable)

Developments Issuance• A pilot platform for the cross-border investment and settlement of debt securities became

operational on 30 Mar 2012. It strengthened the cross-border issuance of, and foreign investment in local bonds in Malaysia and other domestic markets in Asia connected via the pilot platform. It allowed investors in Malaysia to buy RMB-denominated bonds in Hong Kong, and Hong Kong investors to gain access to sukuk via Euroclear.

• In Jan 2013, Bursa Malaysia launched the much anticipated first retail Exchange-Traded Bonds/Sukuk (ETBS). This is open to the public to provide retail investors with the option to acquire bonds that provide interest and certain stability, and it also provides investors with a more tradable alternative in an asset class of investments apart from equities.

Trading• Electronic Trading Platform (ETP) facilities launched on 10 Mar 2008 for the trading and

reporting of government and corporate bonds, and all secondary market activities allowed dealers to easily match bids with offers, negotiate deals and access historical data through a common computerized network.

Other Highlights • The Bond Info Hub is a one-stop center detailing all bond related information in Malaysia. In Jul

2011, the Securities Commission issued revised guidelines for private debt securities and sukuk in line with the broader objectives of the Capital Market Masterplan 2. The revised guidelines include: 1) streamline the approval process and time-to-market for the issuance of corporate bonds and sukuk, 2) remove the mandatory rating requirement for selected issues or offers, 3) provide greater disclosure of relevant information for debenture holders.

Islamic Finance Market • Malaysia is the Islamic capital market center. Approximately 70% of Malaysia’s domestic debt

issuance is in the form of sukuk, making it the world’s largest Islamic bond market with over 60% of global sukuk issuance originating from Malaysia.

• Bank Negara Malaysia issued its first Sukuk ljarah Notes in Feb 2006.

• Exempted investors from paying taxes on capital gains made on Shariah-compliant debt denominated in currencies other than the ringgit through 2014.

• On 7 Sep 2012, the Securities Commission Malaysia (SC) launched the Malaysian retail bonds and sukuk framework that provided retail investors direct access to invest in bonds and sukuk.

• On 27 Sep 2012, Bursa Malaysia introduced rules to facilitate listing and trading of exchange traded bonds and sukuks on the Exchange.

Trading

Clearing

Settlement

Listed OTC

MYXGovernment and Corporates

Government

BSC

BMD Bank Negara

Dematerialized Immobilized

13

ASEAN MarketsBonds Philippines (GMT+8)

Size of LCY Bond Market (USDBn)1 100 (Government 87%, Corporates 13%)

Bond Trading Volume (USDBn)1 53

Bond Turnover Ratio (%)1 Government (65%), Corporates (not available)

Growth from Prior Year (%)1 Government (55%), Corporates (not available)

Market Infrastructure

Settlement

Developments Issuance • Government bonds are issued.

• Benchmark Bonds: As part of the country’s debt consolidation program, the government issued benchmark bonds in exchange for old bonds, thereby creating very liquid bonds up to ten years.

• Peso-Denominated Global Bonds: The US Securities and Exchange Commission-registered bonds, the first deal of its kind from Asia, are peso-denominated and are traded onshore but settled offshore. These bonds are a part of the government’s proactive management of external liabilities, particularly with respect to reducing its vulnerability to foreign currency risk.

Clearing• Direct delivery from is required by local regulators. There is no CCP for fixed income yet.

Settlement• Corporates settle directly between broker/dealer & buyer/seller.

• Government securities are settled through the Registry of Scripless Securities (Ross), usually on the same day and on a semi-DVP basis

Other Highlights • Tax: Under the Tax Code of 1997, income tax exemption is granted to sovereign entities from

bond investments in the Philippines. On 7 Nov 2012, the Bureau of Internal Revenue (BIR) issued Revenue Regulation to reiterate and clarify existing rules on the tax treatment of financial instruments and related transactions.

• Dollar-linked Promissory Notes are peso-denominated coupon bonds where cash flows are adjusted to the USD/PHP exchange rate at the time of payment.

• The Philippines market is predominantly composed of government securities (81% of the market’s total outstanding).

• The private sector commercial paper market is small, presenting many obstacles to foreign investors. However, the development of the euro-peso bond market for foreign issuers has generated interest.

• The country is looking to the capital markets to help finance its infrastructure funding needs. The government is working with the World Bank and its private sector arm, the International Finance Corporation, to create instruments that matched funds to infrastructure requirements as well as tapping private infrastructure funds.

Trading

Clearing

Settlement

Government Corporates

Listed T+1 T+1

OTC T+1 T+1

T+1 (market conversion for domestic transactions T+1, parties can still agree on T+0 basis).

Listed OTC

PDEXGovernment and Corporates

Government and Corporates

BTR-RoSSGovernment

PDTCCorporates

Dematerialized

14

ASEAN MarketsBonds Thailand (GMT+7)

Size of LCY Bond Market (USDBn)1 279 (Government 79%, Corporates 21%)

Bond Trading Volume (USDBn)1 150

Bond Turnover Ratio (%)1 Government (68%), Corporates (7%)

Growth from Prior Year (%)1 Government (21%), Corporates (122%)

Market Infrastructure

Settlement Government Corporates

Listed T+2 T+2

OTC T+2 (negotiable) T+2 (negotiable)

Developments Issuance • Since May 2011, the cities of Bangkok and Pattaya and other selected local governments were

allowed to raise funds through bond issues. However, the central government will not guarantee these issues. The SEC will supervise the bond issues and a credit rating will be required. The Finance Ministry and the Interior Ministry are working together on this regulation and regulatory framework needs to be finalized.

• In July 2011, the Ministry of Finance issued inflation-linked bonds (ILBs) that protect the principal against inflation.

• The Thai Ministry of Finance has permitted seven foreign entities to issue baht-denominated bonds or debentures in Thailand by 30 Sep 2012. Citi is one of the permitted entities with an authorized issue amount of 10,000 million Baht.

Trading• The Bond Electronic Exchange (BEX) was established by the Stock Exchange of Thailand (SET)

and started trading on 26 Nov 2003. Securities eligible for trading on SET’s BEX were bonds issued by SET-listed and MAI-listed companies. Prior to that, all bonds were traded OTC.

Settlement • In 1999, Citi was instrumental in setting up the book-entry system for government bonds with

the Bank of Thailand (BoT). Citi continues to actively participate in the Thailand Securities Depository’s Working Committees to implement real-time depository records and straight-through processing.

• The BoT is currently working on a project to improve efficiency in the settlement system for the government to facilitate real time delivery versus payment (DVP).

Other Highlights • Government bonds are the most actively traded securities, accounting for approximately 80%

total trade.

• On 22 Aug 2012, SEC launched SMEs Bond to promote fundraising channel for small and medium-sized businesses.

• From 1 Oct 2012, there are new symbols for government debentures that are registered with the Thai Bond Market Association (ThaiBMA). The new symbols helped market participants to better distinguish the types of the government debentures.

Islamic Finance Market

• On 15 May 2012, the Islamic Bank of Thailand sent a request for proposals (RFP) to a group of banks to submit proposals for baht-denominated sukuk.

• A state-run Thai Islamic bank plans to issue an Islamic bond soon, but no specific date has been identified.

Trading

Clearing

Settlement

Listed OTC

BEXGovernment and Corporates

Government and Corporates

TCH

TSD

Immobilized

BEX enhances the bond’s secondary market. Prior to BEX, bonds were traded in OTC.

15

ASEAN MarketsBonds Vietnam (GMT+7)

Size of LCY Bond Market (USDBn)1 25 (Government 96%, Corporates 4%)

Bond Trading Volume (USDBn)1 Not available

Bond Turnover Ratio (%)1 Not available

Growth from Prior Year (%)1 Not available

Market Infrastructure

Settlement Government Corporates

Listed or UpCom T+1 T+1

OTC No standard process (negotiable) No standard process (negotiable)

Developments Issuance• Decree 01 came into effect on 20 Feb 2011. The decree specifies which organizations are allowed

to issue government guaranteed bonds, the purposes for which government guaranteed bonds can be issued, and provides additional clarity on the role of the State Bank of Vietnam in international government bond issues.

• On 14 Oct 2011, Decree 90 on corporate bond issuance was issued to unify previously separate regulations on domestic and international issuance into one decree.

• The Ministry of Finance (MOF) has issued a new Circular effective from 20 Jan 2013 providing guidance on corporate bond issuance, in accordance with the Decree 90 on bond issuance.

Trading• HNX Government Bond Trading Platform: In Sep 2009, the HNX launched a specialized market

to trade government bonds, local government bonds, and other government-guaranteed securities.

• New systems - the HNX is in the midst of plans to facilitate the development of Vietnam’s bond market, of which a variety of new systems are to be installed in the first half of 2013.

• In May 2012, the exchange allowed of transactions such as the launch of electronic procurment, yield curves, and a bond index on treasury bonds.

• The HNX has successfully built an e-procurment system that launched in 2012 to promote the bond market.

• On 6 Mar 2013, HNX launched the new Government Bond Trading System Version 2 to facilitate increasing demand for bond trading by market participants.

• Effective 18 Mar 2013, HNX has a new decision that regulates trading of government bonds, government guaranteed bonds, municipal bonds and treasury bills.

Other Highlights • On 1 Mar 2012, the new tax rules came into effect for the Vietnam market. The withholding tax on

interest received from fixed income investments was reduced to 5% from 10%.

• In Jul 2012, the HNX, VSD and some government bond issuers signed a multilateral memorandum with an aim to enhance the operations of government bond issuance, registration, listing and settlement in the local market.

• On 6 Aug 2012, the HNX launched an electronic auction system for government bonds, government-guaranteed bonds and municipal bonds, which helps shorten the timeframe of auction approval and bidding results.

Trading

Clearing

Settlement

Listed OTC

HNXGovernment and Corporates

HOSEGovernment and Corporates

Corporates

VSD

Immobilized

16

Major Registration MarketsBonds China (GMT+8)

Size of LCY Bond Market (USDBn)1 3,811 (Government 73%, Corporates 27%)

Bond Trading Volume (USDBn)1 3,248

Bond Turnover Ratio (%)1 Government (75%), Corporates (98%)

Growth from Prior Year (%)1 Government (29%), Corporates (15%)

Market Infrastructure Listed OTC

SSEGovernment and Corporates

SZSEGovernment and Corporates

Government and Corporates

CSDCC CCDC

Dematerialized

Settlement Government Corporates

Listed T+0/T+1 T+0/T+1

OTC T+0/T+1 T+0/T+1

Developments Issuance• On 20 Oct 2011, the Ministry of Finance launched a trial program allowing some of its

provincial and municipal governments to issue bonds directly in their own name.

• On 8 Jun 2012, the China Securities Regulatory Commission (CSRC) approved high yield bonds issuance, part of a push to broaden the range of financing routes for smaller and medium-sized companies.

Settlement• Starting from 2 Jul 2012, the CSDCC began to charge settlement fees for corporate bonds

and specific net management plans.

• As of 16 Jul 2012, the Shenzhen Stock Exchange (SZSE) adjusted the settlement cycle from T+1 DVP to T+0 for corporate bonds, T+1 for cash in a netting mode.

• The SZSE published the “Implementation Rules on bond trading in SZSE” (the Rules) which went into effect on 10 Dec 2012. The rules included the trading method and time for both listed bonds and bond repurchases products, including block trading, information disclosure, etc.

Other Highlights

• On 30 Sep 2011, the Shanghai Stock Exchange (SSE) announced it has been working with the CSDCC on repos for convertible bonds. The SSE planned to allow repos for convertible bonds after the technical preparation is completed. However, QFIIs are not allowed to participate in the bond repos.

• In Feb 2012, China Securities Index Co., Ltd launched the China Securities Index Co., Ltd. (CSI) bond valuation, which provided a benchmark to gauge fair market value for bond investors.

• China intends to expand its capital markets and open them more widely to foreign investors by 2015. Its goal is to be amongst the top three capital markets by 2015, up from its place as the fifth biggest capital market in 2010. Plans include encouraging foreign companies to issue renminbi-denominated bonds and list on the SSE.

• In Apr 2012, the China Banking Regulatory Commission (CBRC) tightened controls on banks’ bond underwriting by requiring the banks to treat corporate bonds that they underwrite as credit lines and include them in their loan books.

• On 5 Jul 2012, the China Securities Regulatory Commission (CSRC) allowed QFIIs to invest in fixed income products in the China interbank bond market. However, it is still pending detailed implementation rules from the People Bank of China (PBOC).

• On 14 Jan 2013, the Chairman of the China Securities Regulatory Commission (CSRC) at the Asia Financial Forum held in Hong Kong commented that China may gradually increase investment quotas for both QFII and RQFII by as much as 10 times the current level. Individual investors may also be allowed to participate in schemes aimed at managing cross-border capital flow.

Trading

Clearing

Settlement

17

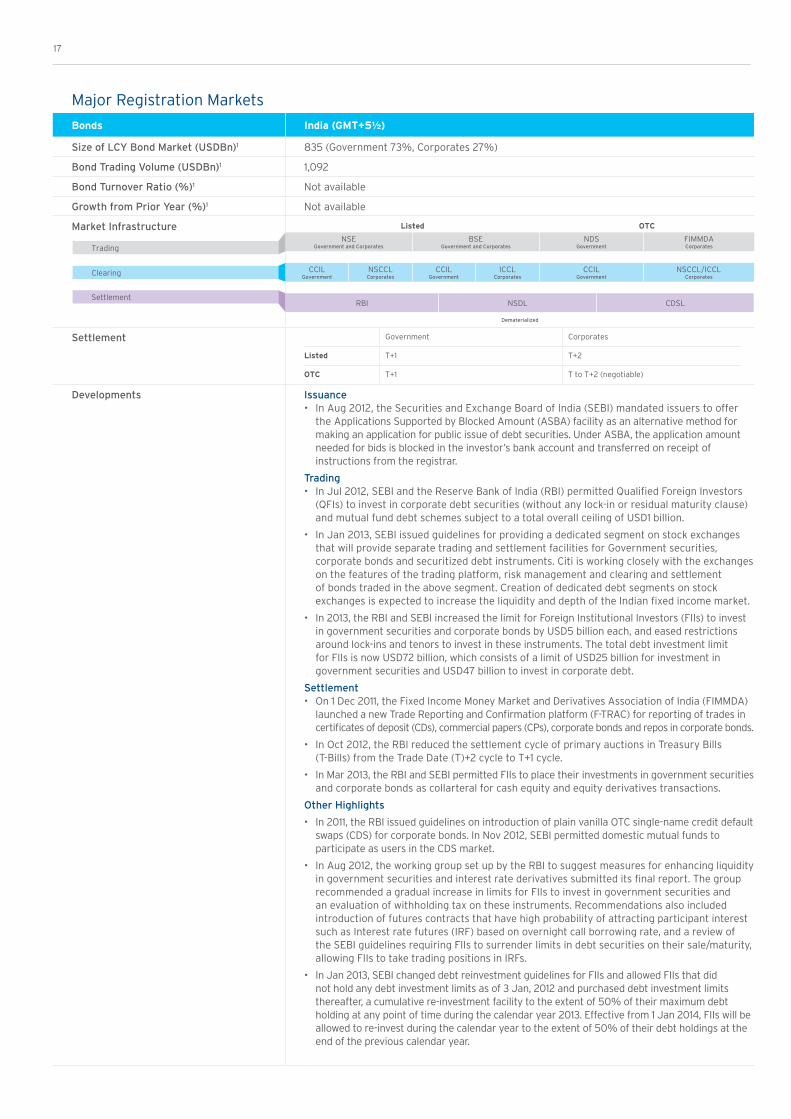

Major Registration MarketsBonds India (GMT+5½)

Size of LCY Bond Market (USDBn)1 835 (Government 73%, Corporates 27%)

Bond Trading Volume (USDBn)1 1,092

Bond Turnover Ratio (%)1 Not available

Growth from Prior Year (%)1 Not available

Market Infrastructure

Settlement Government Corporates

Listed T+1 T+2

OTC T+1 T to T+2 (negotiable)

Developments Issuance• In Aug 2012, the Securities and Exchange Board of India (SEBI) mandated issuers to offer

the Applications Supported by Blocked Amount (ASBA) facility as an alternative method for making an application for public issue of debt securities. Under ASBA, the application amount needed for bids is blocked in the investor’s bank account and transferred on receipt of instructions from the registrar.

Trading• In Jul 2012, SEBI and the Reserve Bank of India (RBI) permitted Qualified Foreign Investors

(QFIs) to invest in corporate debt securities (without any lock-in or residual maturity clause) and mutual fund debt schemes subject to a total overall ceiling of USD1 billion.

• In Jan 2013, SEBI issued guidelines for providing a dedicated segment on stock exchanges that will provide separate trading and settlement facilities for Government securities, corporate bonds and securitized debt instruments. Citi is working closely with the exchanges on the features of the trading platform, risk management and clearing and settlement of bonds traded in the above segment. Creation of dedicated debt segments on stock exchanges is expected to increase the liquidity and depth of the Indian fixed income market.

• In 2013, the RBI and SEBI increased the limit for Foreign Institutional Investors (FIIs) to invest in government securities and corporate bonds by USD5 billion each, and eased restrictions around lock-ins and tenors to invest in these instruments. The total debt investment limit for FIIs is now USD72 billion, which consists of a limit of USD25 billion for investment in government securities and USD47 billion to invest in corporate debt.

Settlement• On 1 Dec 2011, the Fixed Income Money Market and Derivatives Association of India (FIMMDA)

launched a new Trade Reporting and Confirmation platform (F-TRAC) for reporting of trades in certificates of deposit (CDs), commercial papers (CPs), corporate bonds and repos in corporate bonds.

• In Oct 2012, the RBI reduced the settlement cycle of primary auctions in Treasury Bills (T-Bills) from the Trade Date (T)+2 cycle to T+1 cycle.

• In Mar 2013, the RBI and SEBI permitted FIIs to place their investments in government securities and corporate bonds as collarteral for cash equity and equity derivatives transactions.

Other Highlights

• In 2011, the RBI issued guidelines on introduction of plain vanilla OTC single-name credit default swaps (CDS) for corporate bonds. In Nov 2012, SEBI permitted domestic mutual funds to participate as users in the CDS market.

• In Aug 2012, the working group set up by the RBI to suggest measures for enhancing liquidity in government securities and interest rate derivatives submitted its final report. The group recommended a gradual increase in limits for FIIs to invest in government securities and an evaluation of withholding tax on these instruments. Recommendations also included introduction of futures contracts that have high probability of attracting participant interest such as Interest rate futures (IRF) based on overnight call borrowing rate, and a review of the SEBI guidelines requiring FIIs to surrender limits in debt securities on their sale/maturity, allowing FIIs to take trading positions in IRFs.

• In Jan 2013, SEBI changed debt reinvestment guidelines for FIIs and allowed FIIs that did not hold any debt investment limits as of 3 Jan, 2012 and purchased debt investment limits thereafter, a cumulative re-investment facility to the extent of 50% of their maximum debt holding at any point of time during the calendar year 2013. Effective from 1 Jan 2014, FIIs will be allowed to re-invest during the calendar year to the extent of 50% of their debt holdings at the end of the previous calendar year.

Trading

Clearing

Settlement

Listed OTC

NSEGovernment and Corporates

BSEGovernment and Corporates

NDSGovernment

FIMMDACorporates

CCILGovernment

NSCCLCorporates

CCILGovernment

ICCLCorporates

CCILGovernment

NSCCL/ICCLCorporates

RBI NSDL CDSL

Dematerialized

18

Major Registration MarketsBonds Korea (GMT+9)

Size of LCY Bond Market (USDBn)1 1,471 (Government 39%, Corporates 61%)

Bond Trading Volume (USDBn)1 702

Bond Turnover Ratio (%)1 Government (101%), Corporates (15%)

Growth from Prior Year (%)1 Government (-4%), Corporates (-9%)

Market Infrastructure

Settlement

Developments Issuance • Since Jan 2006, the Republic of Korea began issuing 20-year government bonds to satisfy

requests from pension funds and insurance companies.

• Corporate bond issuance surged 30.5% in 2011, as local firms sought funds to repay debts maturing in early 2012.

• Dim Sum Bond: First issued in Korea on 11 Aug 2011.

• Kimchi Bond: To restrain foreign loans from growing rapidly, the Bank of Korea in Oct 2011 announced that financial firms are banned from buying kimchi bonds, which are foreign currency-denominated bonds issued in South Korea.

• Covered Bond: Effective 30 Jun 2011, the Financial Supervisory Service (FSS) announced new guidelines for issuance of covered bonds by banks. The Korean Housing Finance Corporation (KHFC) is the only entity in Korea to issue covered bonds. The issuance format is attractive to Korean banks primarily because of their ability to get off-balance sheet treatment.

• Since Sep 2012, 30-year government bonds have first been issued to support long term demand of National Finance.

Trading• The KRX operates the Electronic Trading System (ETS) for trading between primary dealers.

• Since 31 Jan 2011, the Ministry of Strategy and Finance (MOSF) started to provide Korea Government Bonds data in English.

• On Mar 2011, Korea launched its preliminary primary dealer system with the aim of enhancing market-making and promoting development of its treasury bond market.

• KRX will allow US Treasury bills, notes and bonds to be used for margin deposits from 18 Mar, 2013. This will enhance convenience whilst aligning the market to global standards.

Other Highlights • Effective 25 Jul 2011, the Bank of Korea restricted foreign exchange agencies’ investments

in foreign currency denominated bonds issued domestically for Korean won financing to control the country’s short-term foreign currency debt to avoid any capital outflow when the market is unstable.

• Effective Jan 2012, tax on foreign currency bonds for non-resident investors were implemented. Non-residents or local entities of foreign corporations will no longer benefit from tax exemption on interest from foreign currency bonds in Korea, issued on and after 1 Jan 2012 by the Korean government, local authority, or a domestic corporation.

• Korea’s corporate bond market is well developed among other Asian counterparts.

• The market revamped the settlement process to introduce continuous net settlement, advancing the start of settlement, new buy-in rules, among other changes.

• Tax on foreign currency bonds for non-resident investors implemented for issuance in Korea on and after 1 Jan 2012.

Trading

Clearing

Settlement

Government Corporates

KRX Listed T+1 T

OTC T+1 to T+30 (negotiable) T+1 to T+30 (negotiable)

The settlement cycle for bond is T+1 (government bonds in the KRX-Stock Market Division), T (other bonds in the KRX-Stock Market Division), or it could be negotiable between T+1~T+30 (in the OTC market).

Listed (10%) OTC (90%)

KRXGovernment and Corporates

Corporates

KRX KSD

KSD

Dematerialized and small portion are physically held

19

Listed OTC

GTSMGovernment and Corporates

Government and Corporates

TDCCCorporates

CBCGovernment

Some corporate bonds (physical bonds) are not deposited at TDCC, so the bond market as a whole is not immobilized or dematerialized

Major Registration MarketsBonds Taiwan (GMT+8)

Size of LCY Bond Market (USDBn)1 250 (Government 70%, Corporates 30%)

Bond Trading Volume (USDBn)1 155

Bond Turnover Ratio (%)1 Not available

Growth from Prior Year (%)1 Not available

Market Infrastructure

Settlement

Developments Issuance• The country’s bond issuance activity had been low in the recent years due to inflation, and

the proportion of financial institutions’ bonds has declined, while corporate bond issuance has increased.

• Formosa Bond: The first formosa bond was issued in Nov 2006. Formosa bonds are foreign currency-denominated bonds sold by foreign institutions in Taiwan to the local market. In Jun 2010, Citigroup Inc. issued the largest formosa bond and was also the first US financial institution issuer in the formosa bond market.

• Dim Sum Bond: In July 2012, the Financial Supervisory Commission (FSC) and the Central Bank of China (CBC) announced to allow domestic public companies to float dim sum bonds in Hong Kong, but the raised funds cannot be remitted back to Taiwan.

Trading• Foreign Institutional Investor (FINI)’s aggregate investment in the following instruments

must not exceed 30% of total net-remitted-in capital:

1) Government bonds (regardless of tenors);

2) Money market instruments (only bills with remaining maturity of 90 days or less are allowed);

3) Money market funds;

4) Premiums paid and net settlement amount for certain derivative products

• The FSC expanded the scope of foreign brokerage business to allow the selling of foreign bonds with a bond rating of BB (or higher) to professional investors.

Settlement• Central government bonds are issued in the book-entry form.

Other Highlights • Effective Jan 2012, government bond repos settled via repo slip instead of actual transfer

requires delivery of payment certificate along with the repo slip to terminate the repo transaction at expiration.

• Revised ruling by the FSC allows banks to accept bonds issued by the China government, as well as other foreign central governments or time deposits issued by the world’s top 1,000 banks (ranked by asset or capital) as qualified collateral for NTD credit extension.

Trading

Clearing

Settlement

Government Corporates

Listed T+2 T+2

OTC T+2 T+2

In general up to T+2 for both government and corporate bonds (between arrangements of counterparties). Formosa bond: settled on T+3 or more.

Acronym GlossaryABS Asset-Backed Securities

ADIs Authorized Deposit-Taking Institutions

APRA Australian Prudential Regulation Authority

ASX Australian Securities Exchange

BEX Bond Electronic Exchange

BOJ Bank of Japan

BMD Bursa Malaysia Depository (BMD)

BNM Bank Negara Malaysia

BSC Bursa Securities Clearing

BSE Bombay Stock Exchange

BTR Bureau of Treasury

CBC Central Bank of the Republic of China (Taiwan)

C-BEST Central Depository Book-Entry Settlement System

CCASS Central Clearing and Settlement System

CCIL Clearing Corporation of India Limited

CCP Central Counterparty Clearing

CDB Central Development Bank

CDP Central Depository (Pte) Ltd

CDS Credit Default Swaps

CDSL Central Depository Services (India) Limited

CGSDTCC China Government Securities Depository Trust & Clearing Co. Ltd

CGSS Central Government Securities Settlement System

CSDCC China Securities Depository and Clearing Corporation

CMU Central Money Markets Unit

CPI Consumer Price Index

CSD Central Securities Depository

CSRC China Securities Regulatory Commission

CSSO Clearing and Settlement System Ordinance

DVP Delivery Versus Payment

EBTS Electronic Bond Trading System

EFBNs Exchange Fund Bills and Notes

EFBs Exchange Fund Bills

EFNs Exchange Fund Notes

ETFs Exchange-Traded Funds

ETP Electronic Trading Platform

ETS Electronic Trading System

FIIs Foreign Institutional Investors

FINI Foreign Institutional Investor

FILP Fiscal Investment and Loan Program

FIMMDA Fixed Income Money Market and Derivatives Association

FSA Financial Services Agency

FSC Financial Services Commission

GBP Government Bond Programme

GMT Greenwich Mean Time

GTSM GreTai Securities Market

HKMA Hong Kong Monetary Authority

HKSCC Hong Kong Securities Clearing Company

HNX Hanoi Stock Exchange

HOSE Ho Chi Minh Stock Exchange

ICCL Indian Clearing Corporation Limited

IDX Indonesia Stock Exchange

JASDEC Japan Securities Depository Center Inc.

JBT Japan Bond Trading Co. Ltd.

J-BIEM Japanese Bond Income Exemption Scheme

JGB Japanese Government Bond

JGBCC Japan Government Bond Clearing Corporation

JSDA Japan Securities Dealers Association

KRX Korea Exchange

KSD Korea Securities Depository

LCY Local Currency

LLB Inflation Link Bond

LSE London Stock Exchange

MAI Market for Alternative Investment

MAS Monetary Authority of Singapore

MBS Mortgage-Backed Securities

MDBs Multilateral Development Banks

MGS Malaysian Government Securities

MOF Ministry of Finance

MOSF Ministry of Strategy and Finance

MPF Mandatory Provident Fund

MYX Bursa Malaysia Bhd

NBMC National Bond Market Committee

NSCCL National Securities Clearing Corporation

NSDL National Securities Depository Limited

NSE National Stock Exchange

OTC Over the Counter

PDEX Philippine Dealing & Exchange

PDO Public Debt Office

PDTC Philippine Depository & Trust Corp.

PTI Post Trade Integration

QFIIs Qualified Foreign Institutional Investors

RBA Reserve Bank of Australia

RBI Reserve Bank of India

RMB Renminbi

SBV State Bank of Vietnam

SC Securities Commission

SCA Securities Commission Act

SEBI Securities and Exchange Board of India

SEC Securities Exchange Commission

SEHK Hong Kong Stock Exchange

SET Stock Exchange of Thailand

SFC Securities Futures Commission

SGS Singapore Government Securities

SGX Singapore Exchange Limited

SOE State-Owned Enterprises

SRO Self-Regulatory Organization

SSE Shanghai Stock Exchange

SSTS Scripless Securities Trading System

STP Straight Through Processing

SZSE Shenzhen Stock Exchange

TCH Thailand Clearing House

TDCC Taiwan Depository Clearing Corporation

ThaiBMA Thai Bond Market Association

TSD Thailand Securities Depository Co. Ltd

TSE Tokyo Stock Exchange

VSD Vietnam Securities Depository

Market Infrastructure Developments Impacting Asian Bond Markets 20

Citi Securities and Fund Services21

Contact Us

VIETNAM

Ha Thu NguyenSecurities Country Manager +84 (43) [email protected]

AUSTRALIA

Martin CarpenterSecurities Country Manager +61 (2) [email protected]

CHINA

Kevin Sc WongSecurities Country Manager +86 (21) 2896-6705 [email protected]

HONG KONG

Cindy T ChenSecurities Country Manager +852 [email protected]

INDIA

Debopama SenSecurities Country Manager +91 (22) [email protected]

INDONESIA

Daniel WijonoSecurities Country Manager +62 (21) [email protected]

JAPAN

Yasuhiro YanakawaSecurities Country Manager +81 (3) [email protected]

KOREA

Hee-Jin Kim Securities Country Manager +82 (2) [email protected]

MALAYSIA

Benedict LerSecurities Country Manager +60 (3) [email protected]

PHILIPPINES

Theresa ReyesSecurities Country Manager +63 (2) [email protected]

SINGAPORE

Alvin GohSecurities Country Manager +65 6657-5008 [email protected]

TAIWAN

Hsiao-Chi WangSecurities Country Manager +886 2 8726 [email protected]

THAILAND

Dol WatanasriSecurities Country Manager +66 (2) 788 [email protected]

Asia Pacific Jeffrey WilliamsRegional Head, Direct Custody & Clearing Asia Pacific+852 3419-8826 [email protected]

Rudy IngkiriwangRegional Head, Asia Network Management+65 [email protected]

Judy Yip ToMarket Advocacy, Asia Pacific+852 [email protected]

Footnote1. Size of LCY Bond Market data for Australia is as of Dec 2012 from the Reserve Bank of Australia. Data for Taiwan is as of Dec

2012 from GreTai Securities Market (GTSM) and the Central Bank of Republic of China (Taiwan CBC). India government bond data is as of Dec 2012 from the Ministry of Finance and corporate bond info is from Securities and Exchange Board of India. India government bonds data is from Clearing Corporation of India Limited, and corporate bonds data is from Securities and Exchange Board of India. All other data is as of Dec 2012.

2. Bonds trading volume data is from AsiaBondsOnline. Data used are Dec 2012, except HK and Taiwan data is as of Sep 2012.3. Bonds Turnover ratio data is from AsiaBondsOnline. Data used are Dec 2012, except HK data is as of Sep 2012. 4. Growth from prior year data is from AsiaBondsOnline. Data used are Dec 2012, except HK data is as of Sep 2012.

DisclosureIRIS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the “promotion or marketing” of any transaction contemplated hereby (“ Transaction”). Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor. Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting a s a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the information contained herein and the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b) there may be legal tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with respect to any Transaction, and not withstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest. Citi has enacted policies and procedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances.

© 2013 Citibank N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our own environmental footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position Statement, the first US financial institution to do so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy clean technology and other carbon-emission reduction activities; (c) committing to an absolute reduction in GHG emission of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of carbon neutral power for our operations over the last three years; (e) establishing in 2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of electric power projects; (f) producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

Efficiency, renewable energy and mitigation

Citi Securities and Fund Services transactionservices.citi.com

CTA4112 April 2013