market highlights -...

TRANSCRIPT

Pulse

Monthly Real Estate Monitor

Market Highlights

September 2015

AUGUST 2015

Office space demand

improved across all

cities barring

Ahmedabad, Chennai

and Kolkata

Retail space leasing

increased in Chennai,

Hyderabad, Kolkata

and Mumbai

Residential demand

continued to increase in

Hyderabad

Get city Pulse by clicking below

Pulse

Monthly Real Estate Monitor

September 2015

Favourable Neutral Unfavourable

Legend: Market Sentiment

Commercial Real Estate

up across Major Cities

Average transacted office lease sizes across Mumbai, Bangalore,

Chennai and Pune have increased from the uncertain times seen in

1Q14 – prior to the general elections. Following elections in May

2014, however, market sentiment improved gradually, while Mumbai,

for example, witnessed 65% appreciation in average deal sizes

between 2Q14 and 2Q15.

The number of transactions has also increased considerably across

all these cities. Pune leads with an impressive 89% y-o-y growth in

transacted space per lease deal, followed by Bangalore at 78% and

Chennai at 67%. Good days are returning for office real estate and

tenants will remain in an expansionary mode. Occupiers are not only

leasing larger office space, but they also expect all the space to be on

the same floor. Developers are constructing bigger floor plates to

meet the evolving demand.

Ashutosh Limaye, National Director- Research, JLL India

-------------------------------------------------------------------------------------------- For further reading please refer to following link:

http://www.joneslanglasalleblog.com/realestatecompass/real-estate/2015/08/commercial-

real-estate-residential-major-indian-cities///

India’s economy, defying weakness in

developed countries and elsewhere in

emerging Asia, expanded 7% in the April—

June quarter, making it one of the world’s

fastest-growing as China downshifts. Asia’s third-largest economy also continued

to distinguish itself by being fuelled not by

investments or exports but by consumer

spending, which grew 7.4% y-o-y. Indians are

still opening their pocketbooks despite a

withering of demand in other large

economies, which has sapped trade and

production growth around the globe.

Investment sentiments

improving

A sea-facing triplex penthouse of 17,000 sq. ft.

carpet area in South Mumbai's Napean Sea

Road locality is being sold for INR 2 billion,

the biggest for a residential apartment in India

The Centre named 98 cities for the Narendra Modi

government's flagship Smart Cities project, with Uttar Pradesh

bagging the most in August.

To develop Rajarhat-New Town as a green and

smart city, the Housing Infrastructure

Development Corporation (HIDCO) will set up

two new utility buildings in the township that will

be developed as green buildings

Next

DELHI

KOLKATA

CHENNAI

BANGALORE

HYDERABAD

PUNE MUMBAI

AHMEDABAD

For more information about our research, contact

Ashutosh Limaye

National Director, Research and REIS +91 98211 07054 [email protected]

Sujash Bera

Manager, Research +91 98305 43922 [email protected]

Research Dynamics 2015

Pulse reports from JLL are frequent updates on real estate market dynamics.

www.joneslanglasalle.co.in

Cities

Office

Rental

Value

Retail

Rental

Value

Residential

Capital

values

AHMEDABAD

DELHI

MUMBAI

PUNE

BANGALORE

CHENNAI

HYDERABAD

KOLKATA

Legend

Growing Stabilise Stagnate Falling

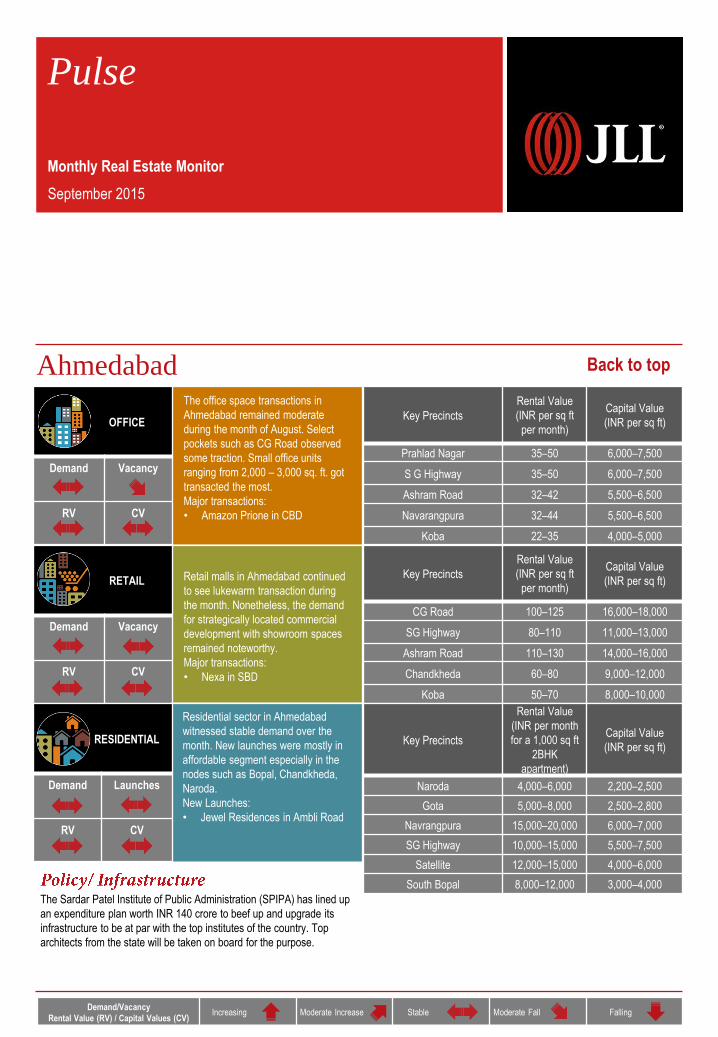

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Ahmedabad

The Sardar Patel Institute of Public Administration (SPIPA) has lined up

an expenditure plan worth INR 140 crore to beef up and upgrade its

infrastructure to be at par with the top institutes of the country. Top

architects from the state will be taken on board for the purpose.

The office space transactions in

Ahmedabad remained moderate

during the month of August. Select

pockets such as CG Road observed

some traction. Small office units

ranging from 2,000 – 3,000 sq. ft. got

transacted the most.

Major transactions:

• Amazon Prione in CBD

Retail malls in Ahmedabad continued

to see lukewarm transaction during

the month. Nonetheless, the demand

for strategically located commercial

development with showroom spaces

remained noteworthy.

Major transactions:

• Nexa in SBD

Residential sector in Ahmedabad

witnessed stable demand over the

month. New launches were mostly in

affordable segment especially in the

nodes such as Bopal, Chandkheda,

Naroda.

New Launches:

• Jewel Residences in Ambli Road

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Prahlad Nagar 35–50 6,000–7,500

S G Highway 35–50 6,000–7,500

Ashram Road 32–42 5,500–6,500

Navarangpura 32–44 5,500–6,500

Koba 22–35 4,000–5,000

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

CG Road 100–125 16,000–18,000

SG Highway 80–110 11,000–13,000

Ashram Road 110–130 14,000–16,000

Chandkheda 60–80 9,000–12,000

Koba 50–70 8,000–10,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Naroda 4,000–6,000 2,200–2,500

Gota 5,000–8,000 2,500–2,800

Navrangpura 15,000–20,000 6,000–7,000

SG Highway 10,000–15,000 5,500–7,500

Satellite 12,000–15,000 4,000–6,000

South Bopal 8,000–12,000 3,000–4,000

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Bangalore

The Bangalore Metro Rail Corporation Limited (BMRCL) revised the plan

for the part of phase-II metro rail project at Jayadeva hospital junction. As

per the new plan Jayadeva flyover will get demolished to build two levels

of metro lines above the flyover at maximum height of 22 m for the

Gottigere and Nagavara line above the ground level and also 14 buildings

out of 98 will be razed under this plan. BMRCL allocated INR 245 Billon

for this two line metro rail which is of 72km length.

Good connectivity with good

infrastructure and availability of Grade

A office projects were the main key

factors to keep the demand intact in

the Outer Ring Road over the month.

However, less space availability for

leasing in this sub-market pushed the

rents upwards.

Major transactions:

• Citrix at Inner Ring Road

Retail demand improved significantly

over the month.

Major transactions:

• Farzi Café, Made in Punjab and

Ducati, all at UB City Mall

• Nandos at Indira Nagar

Launches in August remained healthy

with the city witnessing good volume

of high end projects.

Key Launches:

• Sobha Clovelly at

Padmanabhanagar

• Godrej Gold County at Tumkur

Road

• VKC Chourasia Sapphire at

Mahadevapura

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

CBD 80–130 10,000–22,000

Old Airport Road 60–75 7,000–12,000

Outer Ring Road (Eastern) 52–65 6,000–8,500

Old Madras Road 48–65 5,200–7,000

Electronic City 28–34 3,000–3,800

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Koramangala 90–160 9,000–18,000

Indiranagar 90–180 12,000–18,000

New BEL Road 60–80 6,000–12,000

Commercial Street 175–250 16,000–20,000

Jayanagar 100–170 8,000–18,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Old Madras Road 15,000–25,000 5,000–8,000

Indiranagar 25,000–35,000 10,000–25,000

Bellary Road 12,000–18,000 4,500–11,000

Hosur Road 10,000–14,000 4,000–6,000

Whitefield 18,000–25,000 5,000–9,000

Tumkur Road 8,000–12,000 3,600–5,500

Kanakapura Road 10,000–17,000 4,200–6,500

Mysore Road 8,000–10,000 3,500–5,000

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Chennai

Chennai court passed a new order stating that the landlord is entitled to

receive only one month's agreed rent by way of advance and any

amount paid in excess of agreed rent shall be refunded or adjusted

towards rent.

The growth of banking and health care

was the trend that continued even

during this month

Major transactions:

• World Bank in OMR Perungudi

• Lyca Health in Nungambakkam

• Caterpillar in OMR Taramani

Most of the reputed retailers preferred

high streets for expanding their

footprints in Chennai.

Major transactions:

• Anjappar and Concorde Motors at

OMR

• Shree Mithai at Nungambakkam

Chennai witnessed moderate increase

in number of launches in key micro

markets.

Key launches

• Express Exclusive at Royapettah

• Abhinandan at Perambur Barracks

Road by Landmark Constructions

• Colorberry at Padur by Color

Homes

• TVH Crossway at Karapakkam

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Mount Road 60–85 9,000–16,500

RK Salai 65–85 10,000–15,000

Pre-toll OMR 40–70 5,000–6,500

Post-toll OMR 30–40 3,000–6,000

Guindy 45–65 6,500–9,000

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

T. Nagar 120–180 12,000–15,000

Nungambakkam 130–150 13,000–16,000

Velachery 90–125 10,000–12,000

Pre-toll OMR 80–100 8,000–11,000

Anna Nagar 120–150 11,000–13,000

LB Road (Adyar) 100–140 10,500–13,500

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Adyar 20,000–30,000 18,000–22,000

Medavakkam 11,000–14,000 4,000–6,000

Tambaram 8,000–15,000 4,000–6,000

Anna Nagar 18,000–25,000 10,000–15,000

Porur 7,000–12,000 4,200–6,200

Sholinganallur 9,000–12,000 4,500–6,000

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Delhi NCR

• Indo-Chinese JV, Cico-YFC awarded contract for construction of 6.8

km link of Metro from Noida City Centre to Sector-62 in Noida.

• Work on Delhi-Jaipur highway to be completed by March, 2016

• Circle rates enhanced by 5-10% across various categories in Noida

• Lutyens Bungalow Zone in Delhi to be shrunk by 5 sq. km as areas

such as Bengali Market, Jor Bagh, Sundar Nagar, Golf Links to be

taken out of the LBZ regulations

Demand continued to remain healthy

as occupiers were active in fulfilling

their space requirements. Some

moderate to large space requirements

would become active going forward.

Major transactions:

• Bank of Tokyo & Mitsubishi and

Oracle, both in SBD

• Navig8 Shipping Management in

MG Road-Gurgaon

Demand continued to remain weak as

vacancy is low in good-performing

malls.

Major transactions:

• H&M, Hush Puppies, Monisha

Jaising, Creyate and Mothercare,

all in Prime South

• Indian Terrain and Paislei, both in

Ghaziabad-Suburbs

Sales remained slow as buyers

remained fence-sitters and were taking

time before their buying decisions.

Price discounts and various pricing

techniques were on offer by developers

to push project sales.

New Launches:

• Godrej 101 in Gurgaon

• Panchsheel Premium 24 and

Panchsheel Pebbles in Ghaziabad

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Barakhamba Road 170–400 28,000–35,000

Jasola 110–170 17,000–21,000

DLF Cybercity 95–100 NA

MG Road 115–140 17,000–19,000

Golf Course Road 90–110 12,500–15,000

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

South Delhi 180–330 24,000–32,000

West and North Delhi 140–230 15,000–23,000

Gurgaon–MG Road 140–270 17,500–23,000

Rest of Gurgaon 60–100 8,000–14,000

Noida 130–220 14,000–25,000

Ghaziabad 90–150 10,500–16,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Golf Course Road 27,000–32,000 13,000–19,000

Sohna Road 17,000–20,000 5,800–7,500

Golf Course Extension Road 19,000–22,000 8,500–11,000

Dwarka Expressway NA 5,500–7,500

Noida–Greater Noida

Expressway 13,000–15,000 4,300–6,500

Noida City 12,000–14,500 4,700–6,000

Indirapuram 11,000–12,000 4,500–5,300

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Hyderabad

• INR 25 billion natural gas pipeline is proposed to be developed to

link East and South connecting Paradip in Odisha and Hyderabad in

Telangana.

• The government is soon slated to launch the first phase of T- Hub,

an incubation hub for start-ups to encourage start-up initiatives in the

city.

The city’s western sub market

remained active with most of the

leases. Government policies to draw

investment would soon show results

as there would likely be increased

interest among investors.

Major transactions:

• CDK Global at Hitec City.

• Indeed at Kondapur

Demands remained strong with some

large transactions happening in the

CBD and SBD sub markets. Luxury

brand Zara opened its first store at a

mall in Prime suburb while Cinepolis

expanded in the city with operation of

another 5 screens.

Major transactions:

• Crocodile, Wildcraft and Lenskart

in the High Streets of CBD

Hyderabad Residential sector

witnessed moderate rise in the

demand numbers during the month.

New Launches:

• Jayabheri Temple Tree and

Jaybheri The Peak near Express

Highway - ORR crossing off

Gachibowli.

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Begumpet 45–50 5,300–6,500

Banjara Hills 45–55 6,000–8,000

Hitec City 45–53 5,200–6,500

Gachibowli 38–43 5,000–6,000

Uppal 30–38 4,000–5,000

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Banjara Hills - Jubilee Hills 110–165 11,000–16,500

Secunderabad 110–120 11,000–12,000

Hitec City 110–130 11,000–13,000

Kukatpally 100–110 10,000–11,500

Himayatnagar 150–160 15,000–16,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Banjara Hills 20,000–25,000 8,500–15,000

Begumpet 14,750–20,000 4,500–5,500

Kondapur 11,500–17,500 3,500–5,700

Gachibowli 10,500–16,000 3,300–5,000

Tellapur 8,000–13,000 2,800–3,700

Kukatpally 9,500–15,000 4,000–5,000

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Kolkata

In a bid to develop Rajarhat New Town as a green and smart city, the

Housing Infrastructure Development Corporation (HIDCO) will set up two

new utility buildings in the township that will be developed as green

buildings. Once set up, the two buildings will be the first green buildings

developed beforehand with ready built-up space for accommodating

government offices.

Overall demand of the city started

witnessing positive demand traction.

Occupier enquiries increased across

all submarkets other than SBD.

Major transactions:

• Bentley at Rajarhat

Transaction activity continued to

increase during August. Acropolis Mall

at Kasba would commence operation

in the coming 1—2 months.

Major transactions:

• Chili’s opened its second outlet

• Airtel opened stores in multiple

locations within city limits.

• Axis Bank opened its outlet in

Prime Others.

Residential demand in the city

continued to be stable in the mid-end

and upper-mid end category. New

Launches:

• Starwood by Aspira Group and

Arch Group near Chinar Park

• Merlin Maximus at Sodepur

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Park Street 110–135 13,000–20,000

Topsia 70–90 7,500–10,000

Kasba 75–90 8,000–11,000

Salt Lake Sector V 40–45 4,000–4,800

New Town and Rajarhat 32–36 3,200–4,100

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Elgin Road 300–350 24,000–28,000

Park Street (high street) 325–375 25,000–31,000

Prince Anwar Shah Road 150–200 15,000–18,000

Salt Lake 185–225 15,000–20,000

New Town and Rajarhat 60–80 6,500–8,000

Gariahat (high street) 200–250 16,000–22,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Alipore 50,000–70,000 15,000–22,000

Prince Anwar Shah Road 20,000–35,000 7,000–14,000

EM Bypass (Topsia) 15,000–25,000 6,000–10,000

Lake Town 10,000–16,000 4,000–7,500

New Town (AA- I, II & III) 9,000–15,000 3,500–6,000

Rajarhat 7,000–14,000 3,000–4,500

Behala 7,000–14,000 3,000–5,500

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Mumbai

The Chief Minister of Maharashtra approved the two new Metro lines, a

16.5-km line from Andheri (East) to Dahisar (East) and an 18.6-km line

from Dahisar to DN Nagar. The Andheri (East) to Dahisar (East) line

would be part of a 27-km Dahisar-Andheri-Bandra (East) Metro, while

the Dahisar-DN Nagar line would be part of the larger 40-km Dahisar-

Charkop-Bandra-Mankhurd Metro.

The month of August witnessed robust

transaction activity in Mumbai office

market. Important to mention, most of

them were lease renewals in the

submarkets such as SBD Central &

Eastern Suburbs. Rents remained

unaltered during the month.

Major transactions:

• MNC IT/ITeS firm renewed at

Eastern Suburbs

With limited space available in quality

malls within Mumbai's city limits, many

brands expressed their interest in

occupying space in existing or

upcoming malls in the far-off suburbs.

Major transactions:

• Anita Dongre in a high street in

Prime South

• Brio hospitality, Lifestyle and

Louis Philippe, all at Suburbs

Mumbai residential market continued

to witness fall in demand on the back

of sluggish market sentiments. New

launches also recorded a fall in the

month of August.

New Launches:

• Lodha Codename August Moon at

Upper Worli

• Arihant Anaika at Taloja

• Avant Heritage at JVLR

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Lower Parel 160–200 17,000–22,000

BKC 240–330 26,500–34,000

Andheri - Kurla Road 100–145 10,000–15,500

Goregaon-Malad 85–125 9,000–12,500

Wagle Estate 50–65 5,200–6,900

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Lower Parel 260–390 22,000–32,300

Malad 160–250 12,500–20,000

Ghatkopar 130–220 10,100–18,300

Mulund 125–200 9,500–15,500

Thane 100–185 8,000–14,500

Navi Mumbai 75–150 7,000–12,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Lower Parel 65,000–1,10,000 25,000–40,000

Wadala 36,000–60,000 15,000–23,000

Andheri 32,000–55,000 12,500–21,500

Ghatkopar 30,000–46,000 11,500–17,000

Ghodbunder Road 12,000–25,000 6.000–9,500

Kharghar 10,000–18,000 6,000–9,000

Back to top

OFFICE

Demand Vacancy

RV

CV

RETAIL

Demand Vacancy

RV

CV

RESIDENTIAL

Demand Launches

RV

CV

Demand/Vacancy

Rental Value (RV) / Capital Values (CV) Increasing Moderate Increase Stable Moderate Fall Falling

Pulse

Monthly Real Estate Monitor

September 2015

Pune

No new infrastructure update is available for August.

Demand for office space in Pune

remained buoyant with transactions

dominated by IT/ITeS firms. As a

result, vacancy rate witnessed

marginal dip. Western part of the city

and Hinjewadi continued to remain

favourable among occupiers.

Major transactions:

• Tata Technologies in Suburbs

• InfoBeans in SBD

Leasing activity in malls remained

sluggish. With no new completions

recorded, Pune’s organised retail

stock remains unchanged. Rents and

capital values remained stable over

the month.

Pune Residential sector witnessed

stable demand during the month.

Projects such as Purvankara

Silversand and Kalapataru Crescendo

were at pre-launch stage.

New launches:

• New tower inside Godrej Prana in

South East submarket

• Marvel Fria II in North East

submarket

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

Hadapsar 55–70 6,500–8,000

Kharadi 55–70 6,500–7,500

Hinjewadi 38–48 5,000–7,000

Viman Nagar 55–75 6,500–8,500

SB Road 70–85 7,000–12,000

Key Precincts

Rental Value

(INR per sq ft

per month)

Capital Value

(INR per sq ft)

MG Road 100–160 15,000–21,000

Bund Garden Road 90–130 13,000–17,000

FC Road 100–150 15,000–20,000

JM Road 100–150 15,000–20,000

DP Road 90–130 12,000–16,000

SB Road 80–140 13,000-16,000

Key Precincts

Rental Value

(INR per month

for a 1,000 sq ft

2BHK

apartment)

Capital Value

(INR per sq ft)

Wakad 10,000–13,000 5,000–6,500

Hinjewadi 9,000–11,000 4,800–6,500

Kharadi 11,000–15,000 5,000–7,200

Hadapsar 13,000–18,000 5,500–7,500

Undri 8,000–12,000 4,000–5,500

Pimri-Chinchwad 8,000–15,000 4,500–6,000

Back to top

For more information about our research, contact

Ashutosh Limaye

National Director, Research and REIS

+91 98211 07054 [email protected]

Sujash Bera

Manager, Research

+91 98305 43922 [email protected]

Research Dynamics 2015

Pulse reports from JLL are frequent updates on real estate market dynamics.

Jones Lang LaSalle (NYSE:JLL) is a professional services and investment management firm offering specialized real estate services to clients

seeking increased value by owning, occupying and investing in real estate. With annual revenue of $4 billion, JLL operates in 70 countries from

more than 1,000 locations worldwide. On behalf of its clients, the firm provides management and real estate outsourcing services to a property

portfolio of 3.0 billion square feet. Its investment management business, LaSalle Investment Management, has $47.6 billion of real estate

assets under management.

JLL has over 50 years of experience in Asia Pacific, with over 27,500 employees operating in 80 offices in 15 countries across the region. The

firm was named ‘Best Property Consultancy’ in three Asia Pacific countries at the International Property Awards Asia Pacific 2013, and won

nine Asia Pacific Awards in the Euromoney Real Estate Awards 2013.

For further information, please visit our website, www.jll.com

JLL is India’s premier and largest professional services firm specializing in real estate. With an extensive geographic footprint across 11 cities

(Ahmedabad, Delhi, Mumbai, Bangalore, Pune, Chennai, Hyderabad, Kolkata, Kochi, Chandigarh and Coimbatore) and a staff strength of over

6800, the firm provides investors, developers, local corporates and multinational companies with a comprehensive range of services including

research, analytics, consultancy, transactions, project and development services, integrated facility management, property and asset

management, sustainability, industrial, capital markets, residential, hotels, health care, senior living, education and retail advisory.

The firm was named the Best Property Consultancy in India (5 Star Winner) at the International Property Awards – Asia Pacific for 2012-13.

For further information, please visit www.joneslanglasalle.co.in