market focus - group.pictet

TRANSCRIPT

Unless stated otherwise in the document, all data are as of 04.11.2021Please read important disclosure information at the end of the document

This document should not be copied or forwarded; it is reserved for the exclusive use of the recipient

In other words

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and is not for distribution to retail investors

8 November 2021Market Focus

Markets continue to move higher, and as we write, the Fed has managed to communicate tapering in an announcement that was met by another record close for the S&P500: so far not a tantrum in sight.

Can this continue? We think it can. While economic momentum may have peaked and momentum in earnings is also expected to normalise following such a powerful recovery, growth remains strong, and earnings resilient. If a taper tantrum has been avoided, it is the matter of inflation and how the Fed handles that which continues to preoccupy markets: how sticky will prove the more protracted-than-expected nature of this otherwise ‘transitory’ phenomenon that has resulted from supply-chain bottlenecks, higher commodity prices and which is now becoming evident in wages? The word “transitory” has become a sullied term now that the Fed has acknowledged the more persistent nature of inflation – but it remains applicable: the hunt is on for an untainted equivalent…

Key as we go forward will be how markets anticipate and digest the prospect of peaking and decelerating economic and earnings growth – even if both are still expected to remain healthy. This while those anagrams we love to hate, “FOMO” and “TINA” have continued to drive investors up the wall of worry. However over the past week or so we have seen several short-term macro headwinds fade, while negative real yields remain supportive of an equity market that has already priced rate rises next year in anticipation of upcoming policy tightening. Should we continue to see evidence of improving participation in the labour market while inflation expectations remain “well-anchored”, it remains our view that such a market environment can allow the favourable seasonal trends to prevail into the end of the year.

Contents

Global Equity Quantitative Monitor 2

Market Update 3

“Another word for ‘transitory’ - anyone?”

Figure 1: PTS Equity Regional Matrix*

Global equity quantitative monitor

Source: FactSet; Markit, Copyright © 2020 S&P Global Market Intelligence; Pictet Trading Strategy; as of 1/11/2021. *Criteria are explained in the endnotes

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investors

*Our top down’ Equity Regional Matrix gives us an overview of the prevailing market conditions in equity markets, drawing on macroeconomic data, trend analysis on leading indices, and sentiment. For further information on each

parameter, see the endnotes.

Since our last update at the end of September, Europe's score in our equity regional matrix (the top-down indicator that gives us a regional view*) remains a ‘very bullish’ 33%. Sentiment is little changed (a somewhat ‘neutral’ -13%) while the economics score has improved (17%). Trend has strengthened to 86% (from 74%), while the region’s valuation score remains neutral (-2%). While the ECB’s Governing Council has announced a moderate reduction in the pace of emergency asset purchases it remains very cautious in tone, Christine Lagarde pushing back against market rate hike expectations brought forward to 2022. At 4.1% y-o-y in October, Eurozone inflation is at its highest level since July 2008. The ECB acknowledged that inflation was going to “last longer than initially expected”, yet still expects it to fall in 2022. Euro area GDP expanded 2.2% in Q3, after +2.1% in Q2, and while slowing, at 54.3 the Eurozone composite PMI remains above the pre-pandemic long-run average of 53.0. Supply shortages and transportation problems remain, yet the labour market outlook has also been improving, job growth edging up in both manufacturing and services. We expect momentum in the Eurozone to continue to pick up, attracting with it investors seeking out value plays exposed to the cycle, and we also like green infrastructure, and European luxury.

The US’ regional score remains steady at a bullish 20% (little changed off 19%). Trend has recovered back to 82% (from 69%, although a valuation score of -75% continues to reflect a market that is ‘extended’ on a historical basis. Liquidity remains at 100% while the economics score has improved (from 33% to 50%) and sentiment has inched higher (now at -26% from -28%). While US GDP rose only 2.0% q-o-q SAAR, and September employment grew by only

235,000, reflecting slowing growth after a solid recovery in the first half of the year, October saw the addition of another 351,000. A rebound in the 10-year US Treasury yield has supported the reflation trades and we think the names and sectors exposed to the cycle should still do well into the end of the year – with opportunity to seek out entry points among industrials (and we would not overlook infrastructure).

Japan’s regional score in our matrix has climbed on up from a bullish 27% to a ‘very bullish’ 45%. Trend has dropped from 88% to 10% yet we see an impressive switch in sentiment from -94% to 59% while the valuation score remains “attractive” at 73%, and liquidity is at 100%. Fumio Kishida’s election win was welcomed by markets as encouraging on the fiscal front. Furthermore, and contrary to the other global central banks, BoJminutes reiterated the possibility of more easing. We continue to prefer the country’s exporters as beneficiaries of the global recovery (the weaker yen a tailwind) as well as quality cyclicals in the region.

Emerging market equities have held a steady rating in our matrix over the past month (to -34% from -35%). The outlook for EM equities continues to be challenged by international trade dislocations the trend-score falling further to -64% from -92%. Regarding China, following the recent sell-off, on a short-term tactical basis some opportunity could be presenting itself following the recent selloff. However, we remain cognisant of regulatory changes and corporate liquidity events (i.e. Evergrande) and would continue to take a more selective, tactical approach to EM for now.

2Banque Pictet & Cie SA | Trading Strategy

As we write, the S&P500 index is on track for its fifth straight week of gains; having climbed a wall of worry off the 1 October low. A series of concerns piled up over the summer around risks associated with monetary policy normalisation, as well as the resurgent / persistent Delta variant, the US debt ceiling, the energy crisis, inflation concerns, and slowing economic growth in China (and peaking globally). The low visibility around these risks resulted in a summer shake out in terms of sentiment. However with the extreme euphoria of the initial recovery removed, our own indicators have been reflecting a return in risk-appetite and improving breadth, in a manner that suggests markets are likely to remain risk-on for the holiday season.

Market update

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investors

Figure 2: PTS risk barometer

Source: Bloomberg Finance L.P; Pictet Trading Strategy; as of 24/10/2021.

Love it or hate it – is this rally unstoppable?

Clearly in this low-rate environment our friends TINA (the notion that “there is no alternative” to equities in the current low-yield environment) and FOMO (“fear of missing out”) have a part to play, and earlier this month when we re-visited our positioning indicators (see the letter again here or on request) we discussed how risk appetite was improving despite the weaker sentiment in a manner that suggested that investors were indeed reluctantly dragging themselves up a wall of worry. However several risks have also recently been removed from the macro picture. Covid prevails – but markets are increasingly willing to look through it; growth may be peaking – but should remain at higher levels; earnings have proved more resilient than expected, and the Fed has just pulled off a policy change without spooking markets (so far). Newsflow into the weekend was also encouraging – with a strong payrolls report, news of a possible breakthrough Covid pill, and the passage of the physical infrastructure part of Biden’s fiscal spending plan through the House; and this week the US opens up at last to international travel.

On the Covid front, the global picture in terms of case data has been deteriorating once again – as the world heads into the northern-hemisphere winter. Yet mobility continues its steady recovery, with workplace, retail and recreation space presence improving – most western economies generally preferring to rely on the protection provided by vaccinations over the prospect of further lockdowns –while markets appear increasingly comfortable to look through the risk (although there remains that posed by the risk of zero-tolerance policy in China hampering global activity). As we write, cases are peaking in the UK, while still ticking up in the US, euro area and Japan:

3Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Source: www.ourworldindata.org; Pictet as of 3.11.2021

Figure 3: Daily cases (LHS) and fatalities (RHS) US Europe and Japan per 10k inhabitants

Figure 4: Share of population fully vaccinated (%)

Source: WHO; Johns Hopkins; National Health Administrations; Bloomberg Finance L.P; Pictet as of 3.11.2021

Figure 5: Mobility in advanced (LHS) and emerging (RHS) economies: workplace presence less residential*

Source: Google LLC*Google COVID-19 Community Mobility Reports; Pictet as of 03.11.2021

4Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

On the policy front, the Fed’s dogged policy communication over the past several months appears to have paid off, markets content with last week’s tapering announcement that was teased well in advance which has allowed Powell to avoid a tantrum ahead of the decision around his re-nomination. As was widely expected the FOMC committee (unanimously) agreed to reduce the Fed’s monthly bond purchases by 15bn per month in November and December, starting mid-November (and expects "similar" monthly reductions going forward). All eyes are now trained on rate policy –around which we expect more patient communication from a Fed providing (undetailed) reassurance that it is ready to move according to how economic and labour market conditions evolve accordingly. Risk continues to lie in inflation proving more persistent than expected and the slack in the labour market less than the Fed appears to believe – which could result in acceleration in QE and the Fed’s rate hike timetable. Either way, wage growth could take on a crucial role in coming months to shape expectations for the interest-rate liftoff (post meeting, the Fed funds futures market is pricing 0.58% by December 2022 and 1.14% by December 2023).

While US GDP rising only 2.0% q-o-q SAAR reflects slowing growth after a solid recovery in the first half of the year, it remains healthy. The Q3 earnings season has proved stronger than expected, allaying worst-case fears around the margin pressures brought about by supply chain issues (even if reference to the same is ubiquitous across guidance and pressures are likely to persist for several months more). The test for markets will be how they manage to digest the inevitable peak in both growth and earnings momentum following such an impressive recovery and as base effects fade. However Q3 results have easily surpassed consensus estimates – and the evident resilience brings with it some reassurance that the idiosyncratic supply chain issues are weighing less on margins than initially feared (much of the surprise in operating margins as the stronger demand has enabled companies to pass on cost inflation). As we write, 84% of the S&P500 have reported third quarter results, and while EPS growth has fallen significantly from Q2 levels (when the base effects in annual growth were felt most), so far 82% have beaten consensus EPS, while 76% have beaten on revenues, with an average surprise of 10.5% (on EPS) and 2.95% (on sales); energy and technology contributing the most:

Figure 6: US Q3 EPS and sales beat and surprise data (as of 3.11.2021)

Source: FactSet; Pictet Trading Strategy, as of 03.11.2021

5Banque Pictet & Cie SA | Trading Strategy

Taking a step back, it is however worth remembering that since the two oil shocks of 1973 and 1979 and the peaking inflation of that era, we have been living in a disinflationary world, the liberal policies of Thatcher and Reagan and the tightening of money supply encouraging the downward trend. Technology and globalization at the end of the 1990’s helped this new paradigm bed in (the huge degree of quantitative easing deployed since 2008 resulting in only a modest rise in inflationary pressure). Moreover, and while it is widely acknowledged that the inflationary pressures currently in play may indeed be proving more persistent that originally anticipated, consensus remains that for the most part the kinks that are contributing to the spike in inflation will eventually straighten themselves out. Moreover, and in pursuit of its maximum employment and price stability goals, the Fed continues to be patient - Powell repeating in the press conference following last week’s Fed meeting that “a different and more stringent test for the economic conditions that would need to be met before raising the federal funds rate” and that there was still some way to go - particularly in relation to labour force participation. And while he acknowledged that he sees inflation persisting into next year, he continues to insist that the Fed is not behind the curve - while reiterating that policy could be adapted as appropriate (albeit without giving any detail).

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Dissecting inflation

Inflation remains the big risk preoccupying markets. Having been subdued for so long, the post-pandemic imbalances driven by supply-chain bottlenecks and unmet demand brought about by the faster-than-expected and asynchronous reopening of global economies following the Covidcrisis have now sent US PPI to levels not seen since the 1980s and inflation expectations to their highest levels since 2014. Moreover and while we still think that inflation is mostly cost-push inflation, we still need to watch the labour market and the price pressures now materialising in higher services costs and wages. While such pressures might still be considered ‘transitory’ to the extent that they relate back to the exogenous shock of Covid lockdowns and ‘power-surge’ recoveries, the risk is that the outlook for higher inflation is indeed even more protracted than currently anticipated (both by market participants and central banks) – triggering a spike in inflation expectations and spooking the market accordingly.

Multidecade downtrend inflation but significant

short-term spike

Figure 7: US CPI &PPI

Source: FactSet; Pictet Trading Strategy, as of 03.11.2021

Figure 8: US CPI going back to 1979

Source: FactSet; Pictet Trading Strategy, as of 03.11.2021

6Banque Pictet & Cie SA | Trading Strategy

What the current short-term inflation picture means for markets in our view hinges on whether we have seen a top in the US ISM manufacturing index - and if the Fed is obliged to act sooner than expected we could be looking at a scenario whereby economic activity is slowing while inflation is rising (the worst combination according to our recent crude study). However we think the US economy will prove to be in better shape than it might at first appear, and that, although the ISM manufacturing index may have reached a local peak, it is likely to remain at a high level in the months to come. This while there appears to be broad consensus that while more protracted than initially anticipated, inflation is likely to stabilise once the idiosyncratic factors associated with the reopening have normalised.

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

So how have we got here?

At figure 9 we show the one-year change in the Bloomberg Commodity Index, and below it the correlation between Chinese PPI (a measure of the costs of goods at factory gates) and US CPI. This gives us a crude timeline illustration of the rise in inflation worldwide. We have broken it down into four phases: (1) Worldwide lockdowns result in drawdowns across markets and asset classes (and inflation falling); (2) central banks and governments respond with colossal emergency monetary and fiscal support measures, commodity prices start to bounce back (on hopes the ‘virus will pass while the support will stay’ and the prospect of medical breakthroughs) and CPI starts to pick up from close to zero territory; (3) China emerges from lockdowns with the US and Europe following, while the vaccine breakthrough sparks a sharp rise in commodity prices as confidence in economic reopening soars - triggering strong global demand for raw materials (Chinese factories suffer skyrocketing input prices - as illustrated by the Chinese PPI measure in black in the bottom chart). Rising input costs in China (historically, correlated with US CPI) together with higher commodities prices and supply chain issues start to send US prices higher as well, US CPI reaching pre-pracademic levels while showing little sign of abating; and (4) more recently, and despite a normalization in commodity prices (lateral consolidation), inflation remains high in the US, with a 5.4% YoY increase:

Figure 9: Bloomberg commodity spot index (YoY % change; top) and China PPI and US CPI (YoY % bottom)

Source: FactSet; Pictet Trading Strategy, as of 03.11.2021

7Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

So given the prevailing backdrop, what are our current favourite themes?

Playing inflation

As discussed above, the market narrative continues to focus on rising prices and whether the prevailing inflationary pressures will prove transitory or more persistent. The US consumer price index rose 0.4% in September, more than the consensus forecast (0.3%), suggesting that inflation risks remain tilted to the upside, especially if pandemic related supply issues persist. Sector differences are also likely to persist as pricing pressures do not have the same impact on corporate results. In the past, consumer & retail, industrials, basic materials, energy and financials have been among the beneficiaries of rising inflation (while technology, utilities, insurance, and food/consumer are less resilient). See our recent letter on this topic here and our preferred themes summarised below:

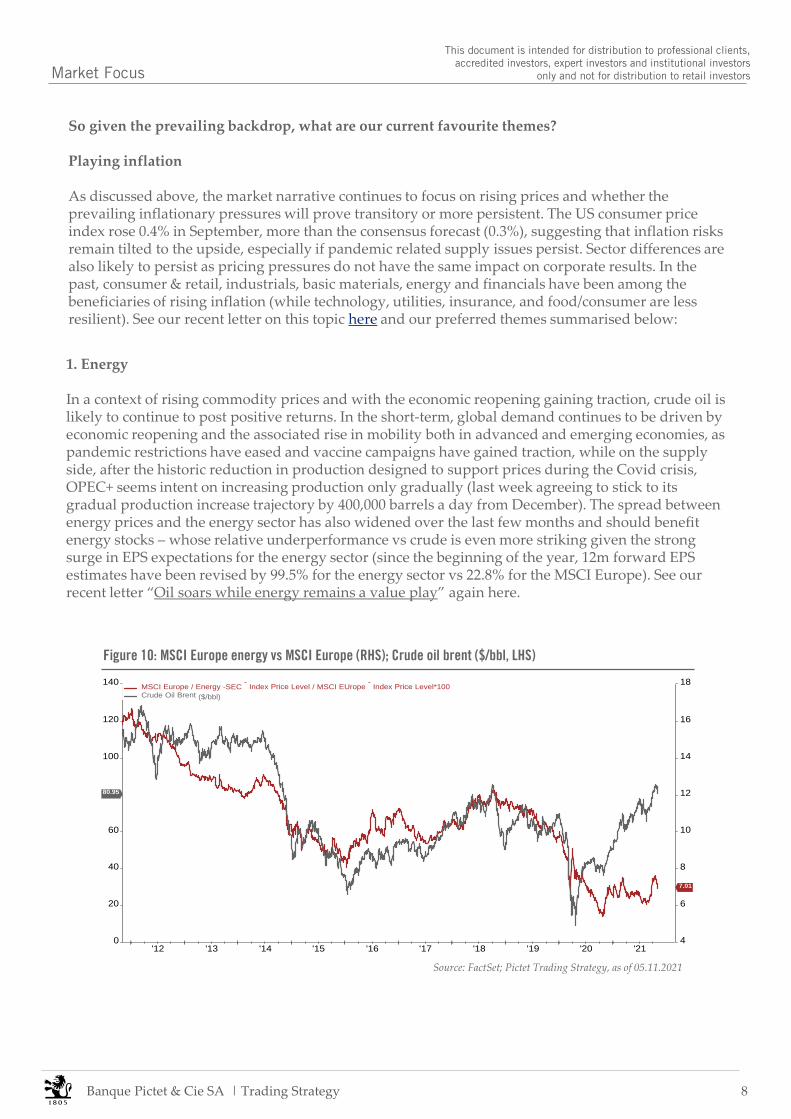

1. Energy

In a context of rising commodity prices and with the economic reopening gaining traction, crude oil is likely to continue to post positive returns. In the short-term, global demand continues to be driven by economic reopening and the associated rise in mobility both in advanced and emerging economies, as pandemic restrictions have eased and vaccine campaigns have gained traction, while on the supply side, after the historic reduction in production designed to support prices during the Covid crisis, OPEC+ seems intent on increasing production only gradually (last week agreeing to stick to its gradual production increase trajectory by 400,000 barrels a day from December). The spread between energy prices and the energy sector has also widened over the last few months and should benefit energy stocks – whose relative underperformance vs crude is even more striking given the strong surge in EPS expectations for the energy sector (since the beginning of the year, 12m forward EPS estimates have been revised by 99.5% for the energy sector vs 22.8% for the MSCI Europe). See our recent letter “Oil soars while energy remains a value play” again here.

Figure 10: MSCI Europe energy vs MSCI Europe (RHS); Crude oil brent ($/bbl, LHS)

Source: FactSet; Pictet Trading Strategy, as of 05.11.2021

'12 '13 '14 '15 '16 '17 '18 '19 '20 '214

6

8

10

12

14

16

18

0

20

40

60

80

100

120

140

80.95

7.01

MSCI Europe / Energy -SEC - Index Price Level / MSCI EUrope - Index Price Level*100Crude Oil Brent ($/bbl)

8Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Figure 11: MSCI Europe energy valuation discount 50% vs the market

Source: FactSet; Pictet Trading Strategy, as of 05.11.2021

2. Financials

With rising yields and a more reflationary global environment, financial stocks should also do well. Recent reports from US and EU banks have also so far been solid, showing core banking activities are picking up (see our letter on Q3 banks earnings again here or on request). A steepening yield curve and positive seasonal trends for the sector should also be tailwinds for the banks. Moreover, and while financials could suffer from the prospect of decelerating economic growth, they are little impacted by the rising costs or supply chain bottlenecks that are currently of greater concern to the market. Following last week’s taper announcement the US 10-year Treasury yield has fallen back below 1.5% towards its 200-DMA; a support that we expect to hold with the yield continuing to rise steadily towards the next technical hurdle at 1.8650% (the 50% Fibonacci retracement of the entire bearish sequence):

0

0.5

1

1.5

2MSCI Europe / Energy -SEC - Price to Earnings Ratio / MSCI Europe - Price to Earnings Ratio

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 20210

5

10

15

20

25

30

35MSCI Europe / Energy -SEC - Price to Earnings Ratio

Figure 12: The 10-Year US Treasury yield

Oct-18 Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

0.50

1.00

1.50

2.00

2.50

3.00

0% 0.5008

60% 1.1448

20% 1.5432

00% 1.8652

80% 2.1872

0.00% 3.2296

(3)

(4)

(2)

(1)

(5)?

US Benchmark Bond - 10 Year - Price 200-d sma US Benchmark Bond - 10 Year - MA-50D

Source: FactSet; Pictet Trading Strategy; as of 08/11/2021. *Criteria are explained in the endnotes. The target price presented in the chart is based upon chart analysis. This is not the product of any Pictet financial research unit.

9Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

3. Metals & mining

Concerns around slowing growth in China and the negative news flow around the Evergrande saga brought about some underperformance in the metals & mining sector in October. However, global reopening and the rise in base metals are likely to act as a strong tailwind for the entire basic resources industry. The performance of materials companies is also historically highly correlated with the direction of inflation expectations and should benefit from the reflation environment. Moreover, the sector is also a way to play the growth recovery at an attractive price. The recent divergence between the price of base metals (as measured by the Bloomberg Commodity Base Metal Index) and global metals & mining stocks encourages our view that the sector could pick up, rebounding to catch up with the move in metals prices in the coming weeks. For more see our recent letter “Mine the GAAP!’ again here or on request.

Figure 13: Base metals and the iShares MSCI Global Metals and Mining ETF

Source: Bloomberg Finance L.P; Pictet Trading Strategy; as of 13/10/2021

4. Inflation contagion – the more wage-sensitive names could suffer more

Moving away from the sector story, wage inflation is probably one of the least-cyclical components of inflation - their effect on corporate profitability is anything but transitory, and a compare between the relative performance of two theoretical equally-weighted baskets made up of the top/bottom decile of S&P500 names according wage sensitivity (revenue/employee ratio) illustrates how investors may have already started to take note – the theoretical performance of the two baskets having already started to diverge (see figure 14). Since September, the less wage-sensitive companies have started to outperform, while the more wage-sensitive basket has lagged and again see our recent letter on inflation here). 5. And we can’t ignore the silver-lining that is the fiscal spending frenzy

While the central banks were quick to meet the Covid crisis by turning the liquidity taps on full, governments were not far behind with emergency social spending measures and/or furlough schemes. They have also acknowledged the strategic opportunity presented by the crisis to deploy more considered long-term investment, the two big examples of course being President Biden’s ambitious infrastructure and special spending plans in the US, and the NextGenerationEU fund’s

10Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Figure 14: High vs low labour costs (top/bottom decile) vs S&P500 equally weighted

Source: Bloomberg Finance L.P; Pictet Trading Strategy; as of 3/11/2021.

loans, grants and incentives. While policies may differ on a regional basis - as do the politics and local priorities - the sums involved are seismic, with much strategically associated with the need to move the dial on climate change and build a “greener” economy, and while infrastructure and clean energy sectors are indeed secular calls, they continue to benefit in particular from the prevailing short-term fiscal tailwinds and the narratives around them. Furthermore, with global leaders recently meeting for the G20 and COP26 summits, green technology in particular has once again been pushed to the top of the political agenda. So in terms of macro-theme investing we would continue to keep an eye on themes such as urban renovation, renewables, energy efficiency and digitalisation - as well as materials and infrastructure, and mining stocks as a play on the demand for industrial metals on the physical infrastructure side. For more see our recent letter on themes here or on request.

Figure 15: US infrastructure stocks have outperformed YTD

Source: FactSet; Pictet Trading Strategy, as of 05.11.2021Jan Feb Mar Apr May Jun Jul Aug Sep Oct

95

100

105

110

115

120

125

130

135

140

121.18

125.41

135.05

Global X U.S. Infrastructure Development ETF - PriceS&P 500 - PriceS&P 500 / Materials - SEC - Price

11Banque Pictet & Cie SA | Trading Strategy

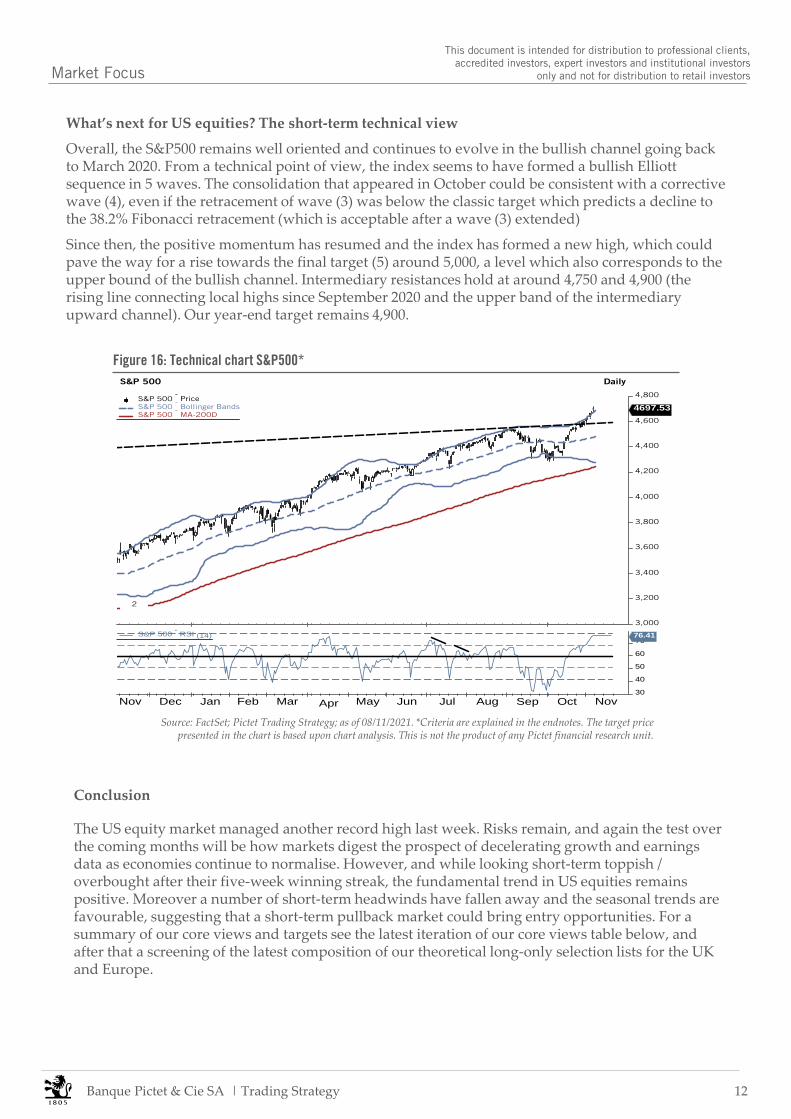

What’s next for US equities? The short-term technical view

Overall, the S&P500 remains well oriented and continues to evolve in the bullish channel going back to March 2020. From a technical point of view, the index seems to have formed a bullish Elliott sequence in 5 waves. The consolidation that appeared in October could be consistent with a corrective wave (4), even if the retracement of wave (3) was below the classic target which predicts a decline to the 38.2% Fibonacci retracement (which is acceptable after a wave (3) extended)

Since then, the positive momentum has resumed and the index has formed a new high, which could pave the way for a rise towards the final target (5) around 5,000, a level which also corresponds to the upper bound of the bullish channel. Intermediary resistances hold at around 4,750 and 4,900 (the rising line connecting local highs since September 2020 and the upper band of the intermediary upward channel). Our year-end target remains 4,900.

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Source: FactSet; Pictet Trading Strategy; as of 08/11/2021. *Criteria are explained in the endnotes. The target price presented in the chart is based upon chart analysis. This is not the product of any Pictet financial research unit.

Figure 16: Technical chart S&P500*

3,000

3,200

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

2

4697.53

S&P 500 Daily

S&P 500-Price

S&P 500-Bollinger Bands

S&P 500-MA-200D

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov30

40

50

60

7076.41S&P 500 - RSI (14)

Conclusion

The US equity market managed another record high last week. Risks remain, and again the test over the coming months will be how markets digest the prospect of decelerating growth and earnings data as economies continue to normalise. However, and while looking short-term toppish / overbought after their five-week winning streak, the fundamental trend in US equities remains positive. Moreover a number of short-term headwinds have fallen away and the seasonal trends are favourable, suggesting that a short-term pullback market could bring entry opportunities. For a summary of our core views and targets see the latest iteration of our core views table below, and after that a screening of the latest composition of our theoretical long-only selection lists for the UK and Europe.

12Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Source: FactSet; Pictet Trading Strategy; as of 08/11/2021 *The target prices presented are based upon chart analysis. This is not the product of any Pictet financial research unit.

Figure 17: PTS core views November 2021*

13Banque Pictet & Cie SA | Trading Strategy

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investors

Source: FactSet; Markit, Bloomberg Finance L.P.; Copyright © 2020 S&P Global Market Intelligence; Pictet Trading Strategy; as of 2/11/2021. *Criteria are explained in the endnotes.

Market Focus

Figure 18: PTS EU long-only selection as at 02.11.2021 - quantitative grades*

Weight in Global Grade: 25% 10% 10% 15% 10% 10% 10% 10% 100%

Ticker Name Sector Growth EPS Sales Value Quality Credit MFS a t Sent. RS Global

gle fp SOCIETE GENERALE SA Banks 73 88 48 69 51 53 91 36 96 65

rdsa na ROYAL DUTCH SHELL PLC-A SHS Oil, Gas & Consumable Fuels 71 87 43 69 49 63 60 51 92 63

engi fp ENGIE Multi-Utilities 64 75 42 68 48 49 89 57 34 62

glen ln GLENCORE PLC Metals & Mining 67 80 57 63 51 50 89 32 95 62

stm im STMICROELECTRONICS NV Semiconductors & Semiconductor 74 72 74 26 56 62 74 46 72 61

tte fp TOTALENERGIES SE Oil, Gas & Consumable Fuels 71 84 50 66 49 64 18 66 80 61

air fp AIRBUS SE Aerospace & Defense 74 82 31 39 64 58 68 45 82 59

jd/ ln JD SPORTS FASHION PLC Specialty Retail 67 73 86 47 43 49 48 45 61 58

isp im INTESA SANPAOLO Banks 62 73 36 61 53 28 96 49 79 58

pum gy PUMA SE Textiles, Apparel & Luxury Goo 53 67 77 24 52 55 85 57 55 56

amun fp AMUNDI SA Capital Markets 59 54 63 56 56 65 45 42 54 56

CCH LN COCA-COLA HBC AG-DI Beverages 55 55 63 47 53 44 65 60 53 55

stla im STELLANTIS NV Automobiles 59 82 46 65 54 46 27 38 90 54

bnp fp BNP PARIBAS Banks 55 64 34 59 50 59 33 68 88 53

asml na ASML HOLDING NV Semiconductors & Semiconductor 73 66 75 10 63 70 24 35 95 53

viv fp VIVENDI SE Media 71 81 35 52 45 46 1 66 94 53

alv gy ALLIANZ SE-REG Insurance 53 56 41 66 49 76 18 48 50 52

azn ln ASTRAZENECA PLC Pharmaceuticals 50 49 75 33 56 48 63 53 32 52

su fp SCHNEIDER ELECTRIC SE Electrical Equipment 60 62 46 30 54 63 45 46 59 51

fgr fp EIFFAGE Construction & Engineering 56 65 48 68 48 33 29 45 57 51

pst im POSTE ITALIANE SPA Insurance 58 50 37 63 42 24 66 48 81 51

cs fp AXA SA Insurance 35 46 30 75 49 59 44 72 83 50

sie gy SIEMENS AG-REG Industrial Conglomerates 47 56 44 39 49 54 74 46 54 50

ker fp KERING Textiles, Apparel & Luxury Goo 60 52 61 31 56 61 24 48 40 50

tep fp TELEPERFORMANCE Professional Services 65 63 67 25 52 37 32 47 58 50

vow3 gy VOLKSWAGEN AG-PREF Automobiles 40 46 41 79 46 52 48 43 73 49

novn sw NOVARTIS AG-REG Pharmaceuticals 40 41 50 49 55 61 61 39 23 48

sika sw SIKA AG-REG Chemicals 55 41 55 20 54 56 33 74 56 48

volvb ss VOLVO AB-B SHS Machinery 49 45 36 59 50 60 21 55 35 48

srt3 gy SARTORIUS AG-VORZUG Health Care Equipment & Suppli 63 49 86 10 48 39 55 26 76 48

or fp L'OREAL Personal Products 49 53 59 20 53 66 44 43 57 47

dte gy DEUTSCHE TELEKOM AG-REG Diversified Telecommunication 42 41 55 67 39 32 24 64 46 46

nesn sw NESTLE SA-REG Food Products 49 40 39 31 52 59 47 52 32 46

ifx gy INFINEON TECHNOLOGIES AG Semiconductors & Semiconductor 47 59 71 21 53 44 18 52 72 45

heia na HEINEKEN NV Beverages 46 53 36 33 54 35 34 56 38 43

rwe gy RWE AG Multi-Utilities 31 47 31 49 58 56 21 61 19 43

ezj ln EASYJET PLC Airlines 28 24 32 40 39 25 91 52 65 39

lonn sw LONZA GROUP AG-REG Life Sciences Tools & Services 41 28 40 12 52 54 25 40 52 36

PHIA NA KONINKLIJKE PHILIPS NV Health Care Equipment & Suppli 23 21 32 41 45 49 29 41 18 34

Short-termTechnical

ParametersLong-term

14Banque Pictet & Cie SA | Trading Strategy

Our long-only selection lists aim to provide investors with long equity ideas within our European and US large cap coverage. The selection is made with reference to our quantitative screening tool, technical analysis, qualitative attributes, and the prevailing market environment. They are updated weekly and available on request.

This document is intended for distribution to professional clients, accredited investors, expert investors and institutional investors

only and not for distribution to retail investorsMarket Focus

Figure 19: PTS US long-only selection as at 02.11.2021 - quantitative grades*

Weight in Global Grade: 25% 10% 10% 15% 10% 10% 10% 10% 100%

Ticker Name Sector Growth EPS Sales Value Quality Credit MF

Sent. RS Global

goog us ALPHABET INC-CL C Interactive Media & Services 79 75 83 20 61 88 65 36 87 64

c us CITIGROUP INC Banks 65 74 41 65 56 64 82 48 74 63

lng us CHENIERE ENERGY INC Oil, Gas & Consumable Fuels 68 82 83 52 31 34 82 32 93 59

bac us BANK OF AMERICA CORP Banks 71 74 47 44 57 78 22 41 91 56

adbe us ADOBE INC Software 62 44 72 9 66 75 74 52 56 55

clh us CLEAN HARBORS INC Commercial Services & Supplies 68 64 58 32 57 36 96 21 89 55

abt us ABBOTT LABORATORIES Health Care Equipment & Suppli 66 63 72 31 55 64 44 35 39 54

msft us MICROSOFT CORP Software 68 57 78 15 62 75 50 28 71 54

fcx us FREEPORT-MCMORAN INC Metals & Mining 61 84 47 44 56 49 47 41 91 54

qcom us QUALCOMM INC Semiconductors & Semiconductor 68 68 65 44 67 57 9 32 24 53

usb us US BANCORP Banks 51 58 47 53 57 77 51 34 70 53

aapl us APPLE INC Technology Hardware, Storage & 68 64 69 15 64 61 49 30 50 53

unh us UNITEDHEALTH GROUP INC Health Care Providers & Servic 56 44 66 39 47 65 82 26 63 53

nflx us NETFLIX INC Entertainment 78 68 76 26 49 42 20 38 62 53

amzn us AMAZON.COM INC Internet & Direct Marketing Re 64 46 70 30 54 66 36 42 23 52

MCD US MCDONALD'S CORP Hotels, Restaurants & Leisure 59 65 58 33 55 54 48 32 29 51

ma us MASTERCARD INC - A IT Services 63 51 67 15 62 56 62 29 26 51

ko us COCA-COLA CO/THE Beverages 55 50 43 38 63 51 78 27 31 51

blk us BLACKROCK INC Capital Markets 47 43 69 29 57 72 19 68 70 49

slb us SCHLUMBERGER LTD Energy Equipment & Services 69 74 22 46 50 48 11 38 94 48

wmt us WALMART INC Food & Staples Retailing 51 50 52 40 53 66 49 26 23 48

exas us EXACT SCIENCES CORP Biotechnology 26 34 72 41 29 46 92 84 5 48

pypl us PAYPAL HOLDINGS INC IT Services 60 44 72 9 60 64 48 26 48 48

fb us META PLATFORMS INC Interactive Media & Services 57 39 74 35 56 69 9 31 30 47

cmg us CHIPOTLE MEXICAN GRILL INC Hotels, Restaurants & Leisure 63 60 71 13 50 45 24 45 67 47

tel us TE CONNECTIVITY LTD Electronic Equipment, Instrume 35 33 49 29 55 67 90 41 70 47

zts us ZOETIS INC Pharmaceuticals 60 45 66 16 56 42 48 30 50 46

atvi us ACTIVISION BLIZZARD INC Entertainment 54 38 49 34 65 76 5 38 17 46

eqix us EQUINIX INC Equity Real Estate Investment 43 34 60 21 30 33 70 74 30 44

xray us DENTSPLY SIRONA INC Health Care Equipment & Suppli 51 56 41 39 50 48 10 44 44 44

mdlz us MONDELEZ INTERNATIONAL INC-A Food Products 37 29 42 39 53 39 78 29 30 42

fis us FIDELITY NATIONAL INFO SERV IT Services 32 42 51 40 43 49 67 28 10 42

nke us NIKE INC -CL B Textiles, Apparel & Luxury Goo 42 27 49 20 66 71 34 34 49 42

jci us JOHNSON CONTROLS INTERNATION Building Products 38 43 29 40 54 54 38 37 81 41

nee us NEXTERA ENERGY INC Electric Utilities 31 41 44 20 31 40 91 35 31 39

wltw us WILLIS TOWERS WATSON PLC Insurance 48 26 33 44 61 37 5 37 51 39

alk us ALASKA AIR GROUP INC Airlines 41 47 46 45 56 34 12 20 62 39

Short-termTechnical

ParametersLong-term

Source: FactSet; Markit, Bloomberg Finance L.P.; Copyright © 2020 S&P Global Market Intelligence; Pictet Trading Strategy; as of 2/11/2021. *Criteria are explained in the endnotes.

15Banque Pictet & Cie SA | Trading Strategy

Endnotes: References for publications of Banque Pictet & Cie SA – Trading Strategy

This document is intended for distribution to accredited investors, expert investors and institutional investors only and not for distribution to retail investors

Model performance data is not a reliable indicator of future returns. Model performance calculation has a number of limitations and the results do not represent the results of actual trading using client assets. The data provided is gross of fees and other commissions. Fees and charges will apply and will reduce the final return. No representation is being made that the model portfolios illustrated will or are likely to achieve results similar to those shown and there are often sharp differences between model performance results and actual results achieved.

The Equity quantitative gradesGrowth Grade: The Growth Grade is a proprietary formula made up of earnings revisions momentum, past earnings growth, earnings stability, and current and long-term earnings growth. A grade above 55 is considered bullish on a 3-month basis, bearish below 45 and neutral between 55 and 45.EPS Grade: The EPS Grade is a proprietary formula consisting of current and forward EPS growth, change and surprise data. An EPS grade above 60 or below 40 is considered predictive for future out/under performance.Sales Grade: The Sales Grade is a proprietary formula made up of current and next year’s sales momentum, past sales growth, sales stability, and current and long-term sales growth. A grade above 55 is considered bullish on a 3-month basis, bearish below 45, and neutral between 55 and 45.Value Grade: The Value Grade is a proprietary formula made up of estimated P/E, P/B, P/S and P/CF ratios. 40% of the grade is based on historical values and 60% on current market data. A grade above 55 suggests a stock is cheap, below 45 expensive, and neutral between 55 and 45.Quality Grade: The Quality Gating is a proprietary formula that focuses on the balance sheet (i.e. change in accruals, change in free cash flows and profitability). A grade above 55 suggests a stock with a good balance sheet.Credit Grade: The Credit Grade focusses on the passive side of the balance sheet. It is divided into three sub-components to assess both short and long-term solvency. A grade above 55 suggests a strong capital structure, while a grade below 45 suggests a weak one.Money Flow Grade: The Money Flow Grade is a proprietary formula that gives the accumulation/distribution based on the volume flows of a stock. A grade above 55 indicates good money flow and a grade below 45 suggests weak money flow.Smart Sentiment Grade: The Smart Sentiment grade is a contrarian indicator based on investor positioning measures such as the days to cover ratio, the put call ratio, and the short interest ratio. A weak grade suggests ‘too much’ optimism.Relative Strength (RS) Grade: The RS grade measures the price momentum of a stock over its 1-year price performance.Global Grade: The Global Grade is a weighted average of the Growth, EPS Sales, Value, Quality, Credit, Money Flow and Smart Sentiment Grades.

The Regional MATRIX gradesThe Regional Matrix grades range from -100% to +100%. We consider a grade above 50% to be very bullish, a grade above 25% to be bullish, and a grade between 0% and 25% to be neutral. A grade between 0% and -45% we consider bearish and a grade below -45% very bearish.Regional Grade: The Regional Grade (-100 to +100) is an indicator of a structural bull market or not. It is calculated by combining and applying weight to each of the other grades that make up the Regional Matrix (Trend, Overbought/Oversold, Valuation, Liquidity, Economics, and Sentiment). If we believe equities to be in a structural bull market, we use 15 years of data to assess Valuation.Trend Grade: The Trend Grade (-100% to +100%) is based on a moving averages model adjusted according to the overbought/oversold conditions of the region’s main indices.Valuation Grade: The Valuation Grade (-100% to 100%) is based on the percentile rank of the regional Index stocks’ P/E ratios since 1995 (current year estimated).Economics Grade: The Economics Grade (-100% to 100%) is based on a combination of manufacturing and non-manufacturing PMIs and the Citigroup Surprise Indices. The Citigroup Economic Surprise Indices are an objective and quantitative measure of economic news and are defined as weighted historical standard deviations of data surprises (actual releases vs. Bloomberg survey median). A positive reading of the Economic Surprise Index suggests that economic releases have on balance beaten the consensus.Sentiment Grade: The Sentiment Grade (-100% to 100%) is based on various contrarian and non-contrarian indicators. Reversal date in the Trend: If the trend has reversed, we give the reversal date and indicate the direction of the reversal.Factor trends: We look at the performance of 5 theoretical long-short selections, each built around one of our quantitative grades (i.e. growth (EPS momentum), price momentum (RS), quality, sentiment and value), and each long the top decile and short the bottom decile of stocks within the respective region in our equity universe in terms of exposure to each specific score. Model Long Only & Absolute return regional Allocation: The Regional Allocation shows the advised net exposure in total and per region. It is calculated by multiplying the MSCI regional weight by the Regional Grade (we use the structural bull market regional grade).Trading Strategy Exposure: The Trading Strategy Exposure shows the actual net exposure in total and per region, based on our trades.Short-Term: 1 to 4 weeks / Medium Term: 1 to 3 months / Long Term: more than 3 months.PTS: Pictet Trading Strategy.Buy/Long: Stock is expected to achieve a total return that exceeds the relevant market index over the next 3 to 6 months.Sell/Short: Stock is expected to underperform the relevant market index over the next 3 to 6 months.Hold/Neutral: Stock is expected to be in line with total return of the relevant market index over the next 3 to 6 months.

Technical Analysis: The technical analysis used in this presentation combines traditional technical tools: graphical analysis (trend lines, support lines, continuation and reversal patterns) which determines the tendency, mathematical indicators (moving averages, RSI, MACD) used as numeric filters and Elliot wave theory which allows us to build a scenario with target levels and invalidation points.

Elliott Wave Theory: According to Elliott Wave Theory, markets move in impulse waves – with five sub-waves (numbered 1-5 or I-V) following the direction of the main trend, followed by three corrective sub-waves (A-B-C) (example to the right). These waves follow a set of specific rules and are linked to each other by target and retracement ratios based on the Fibonacci sequence, and the characteristics of each wave form an integral part of the reflection of the mass psychology it embodies.

A

B61.8% * A

C 61.8% 1-5

1

3

4

5

2 61.8%

1.618% * 1

38.2%

0.618% * 3

ABC

ABC

Elliott Wave Theory

16Banque Pictet & Cie SA | Trading Strategy

Disclosure Information

General disclaimer This marketing communication is produced by the Trading and Sales division of Banque Pictet & Cie SA (hereafter “Pictet”), a Swiss bank under the supervision of the Swiss Financial Market Supervisory Authority FINMA. This document is not a product of any Pictet Financial Research Unit therefore it is not subject to the “Directives on the Independence of Financial Research” of the Swiss Bankers Association. This marketing communication has not been prepared in accordance with the legal and regulatory requirements to promote the independence of research.This document is neither an investment advice nor an advertising material of financial instruments, products or services. The information, tools and material presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe any securities or other financial instruments. In researching the past market history of prices and trading volumes, the persons who prepared this document (hereafter the “authors”) apply special technical methods and formulas to identify and project price trends, including Technical Analysis.

This document does not constitute the investment policy of Pictet and/or the investment policy of Pictet Canada L.P, Bank Pictet & Cie (Asia) Ltd, Pictet Global Markets (UK) Limited or Pictet & Cie (Europe) SA (hereafter collectively “affiliates”) but merely the different assumptions, views and analytical methods of the authors. Pictet and/or any of its affiliates may have issued other documents that are inconsistent with, and reach different conclusions from the information and opinions presented in this document.

The value and income of any of the securities or financial instrument mentioned in this document can fall as well rise. Indeed, they may be affected by many factors. Past performance should not be taken as an indication or guarantee of future performance and no representation or warranty, expressed or implied, is made by Pictet and/or any of its affiliates regarding future performance. Pictet and/or any of its affiliates accept no liability for any loss or damage arising from the use of this document.

Information and opinions contained in this document may be subject to frequent changes and are set for indicative purpose only. Pictet and/or any of its affiliates have no obligation to update, modify or amend this document or to otherwise notify a reader thereof in the event that any matter stated herein becomes inaccurate. Information and opinions presented by Pictet have been obtained from sources believed to be reliable, and, although all reasonable care has been taken, Pictet and/or any of its affiliates are not able to make any representations as to its accuracy or completeness. Information usually attributed to a unique specific source is quoted whenever such source is available. Otherwise, the information may have been gathered from public news dissemination services.

It does not take into account the specific investment objectives, the financial situation and the particular needs of any person who may receive this report and invest in any financial instrument. Therefore, investors should seek financial advice regarding the suitability of investing in any securities or investment strategies discussed in this report. Pictet and/or any of its affiliates make no representation and give no advice in respect of any tax, legal or accounting matters in any applicable jurisdiction.

This document may contain a series of trading tips, the reader should note that the model portfolio (if any) set out in this document is not a portfolio management product, it may not be updated and Pictet and/or any of its affiliates may discontinue the publication or distribution of the model portfolio at any time. The reader should not replicate part or all of, or rely on, the model portfolio to construct its own investment portfolio.

The trademarks, logos and images set out in this document are used only for the purpose of this publication.

Vendor disclaimersAny index used in this document is the intellectual property of its relevant owner (hereafter “the owner”). The owner has not been involved in any way in the creation of any reported information and does not give any warranty and excludes any liability whatsoever (whether in negligence or otherwise) – including without limitation for the accuracy, adequateness, correctness, completeness, timeliness, and fitness for any purpose – with respect to any reported information or in relation to any errors, omissions or interruptions in the relevant index or its data.

Any dissemination or further distribution of any such information pertaining to the owner is prohibited.

Please click on the following link in order to read the vendor-disclaimer for each index used in our publication: www.group.pictet/trading/disclosure-vendor-disclosure

Conflicts of interest A part of the compensation of the authors may be, directly or indirectly, related to the specific performance of recommendations or views expressed in this document. Authors are also paid a salary plus bonus based on the overall revenue generated by Pictet which may include a portion generated by the Trading and Sales division. Pictet, its affiliates or any of its employees are not subject to the prohibition on dealing in any financial instrument mentioned at any time before this document is distributed. For the companies mentioned in this document Pictet, its affiliates, or any of its employees involved and not involved in the preparation of this document may from time to time have long/short positions or holdings in the securities or other related investments. Nevertheless, the position of Pictet or any of its affiliates does not exceed the threshold of 0.5 percent of the total issued share capital of the issuer. Otherwise, a statement to that effect will be disclosed. The authors responsible for this document, nor any related household members, are not officers, nor directors, nor advisory board members of any covered company. Pictet, its affiliates or any of its employees may use the above mentioned strategy for their own activity. Pictet or any of its affiliates did not, for any company mentioned in this document: (a) Manage or co-manage a public offering in the past 12 months, (b) Participate in any issues of securities in the last 3 years. Pictet, any of its affiliates or authors have not received compensation from any covered company in the last 12 months and do not expect to receive or intend to seek compensation for investment banking services in the next 3 months. Pictet may act from time to time as a market maker for any security mentioned in this document.

This document is intended for distribution to accredited investors, expert investors and institutional investors only and not for distribution to retail investors

17Banque Pictet & Cie SA | Trading Strategy

Pictet and its affiliates provide a vast array of financial services other than investment banking. The reader should assume that Pictet and its affiliates receive compensation for those services. Moreover, the companies mentioned in this document could currently be or could have been during the last 12 months a client of Pictet or any of its affiliates. The sales and trading department of Pictet is engaged in selling and trading in securities which relates to this document. Pictet, its affiliates and its authors adhere to professional standards and abide by a formal code of ethics that puts the interests of its client ahead of their own. Pictet is not aware of any other possible conflict of interest, not already disclosed above, that may affect the objectivity of this document.

Report distributionThis document is not directed at, or intended for distribution to, or publication for use by, any person or entity that is citizen or resident of, or located in, any locality, state or other jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or would subject Pictet or any of its affiliates to licensing or other requirements within such jurisdiction. This document is directed to persons having professional experience in matters relating to investments. Services referred herein are not available to retail clients. This material may not be published or reproduced, in all or in part, without the prior consent of Pictet.

In the USA and in Canada: In the United States, distribution by Pictet is permitted as provided by the exemption under article 15a-6 of the Securities Exchange Act of 1934, and is intended exclusively for major US institutional investors, as defined by the same article. All major US institutional investors may effect a transaction in accordance with the above mentioned article with Pictet Overseas Inc., a US registered broker-dealer.

Please click on the following link in order to read full disclosure information for distribution from Pictet Overseas or from Pictet Canada: Pictet Overseas Inc. & Pictet Canada L.P. disclosure information : www.group.pictet/trading/disclosure-pictet-canada-lp-pictet-overseas-inc

In the UK: This document is distributed by Pictet & Cie (Europe) S.A. London Branch. Pictet & Cie (Europe) S.A. London Branch is authorised and regulated by the Commission de Surveillance du Secteur Financier. Deemed authorised by the Prudential Regulation Authority. Subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority . This document has not been prepared in accordance with legal requirements designed to promote the independence of research. It has to be considered as non-independent research and a marketing communication. This document may constitute an investment recommendation under the UK version of European Union Market Abuse Directive (2014/57/EU) and the UK version of the European Union Market Abuse Regulation (Regulation 596/2014). This document is intended only for UK Clients who meet the UK version of The Markets in Instruments Directive (MiFID) client categorisation requirements of Professional clients or Eligible counterparties. This material is not intended for Retail Clients.

In Luxembourg and the European Economic Area: This document is distributed by Pictet & Cie (Europe) SA. Pictet & Cie (Europe) SA is a bank organized and existing under the laws of the Grand Duchy of Luxembourg and is regulated by the Commission de Surveillance de Secteur Financier (“CSSF”). This document has not been prepared in accordance with legal requirements designed to promote the independence of research. It has to be considered as non-independent research and a marketing communication. This document may constitute an investment recommendation under the European Union Market Abuse Directive (2014/57/EU) and the European Union Market Abuse Regulation (Regulation 596/2014). This document is intended only for Luxembourg and EEA Clients who meet The Markets in Instruments Directive (MiFID) client categorisation requirements of Professional clients or Eligible counterparties. This material is not intended for Retail Clients.

In Singapore: This document is distributed by the Pictet Trading & Sales department of Bank Pictet & Cie (Asia) Ltd (“BPCAL”) in Singapore, and is not directed to, or intended for distribution, publication to or use by, persons who are not accredited investors, expert investors or institutional investors as defined in section 4A of the Securities and Futures Act (Cap. 289 of Singapore) (“SFA”) or any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject BPCAL and any of its affiliates or related corporations to any prospectus or registration requirements. BPCAL has obtained an exemption from the Monetary Authority of Singapore (“MAS”) under section 100(2) of the Financial Advisers Act (“FAA”) for the provision of financial advisory services to High Net Worth Individuals (as defined in the MAS Guidelines on Exemption for Specialized Units Serving High Net Worth Individuals FAA-G07) (the “Exemption”) and is exempted from the requirements of sections 25, 27, 28 and 36 of the FAA, the MAS Notice on Recommendations on Investment Products (FAA-N16), MAS Notice on Appointment and Use of Introducers by Financial Advisers (FAA-N02), MAS Notice on Information to Clients and Product Information Disclosure (FAA-N03) and MAS Notice on Minimum Entry and Examination Requirements for Representatives of Licensed Financial Advisers and Exempt Financial Advisers (FAA-N13). Please contact BPCAL in Singapore in respect of any matters arising from or in connection with this document.

This document is only meant as a marketing tool and is not a product of any independent financial research unit. The information, tools and material presented in this document are provided for information purposes only and are not to be used or considered as an offer, an invitation to offer or solicitation to buy, sell or subscribe for any securities, commodities, derivatives, (in respect of Singapore only) futures, or other financial instruments (collectively referred to as “Investments”) or to enter into any legal relations, nor as advice or recommendation with respect to any Investments. This document contains a series of trading tips. The model portfolio set out in this document is not a portfolio management product, it may not be updated and BPCAL may discontinue the publication of the model portfolio at any time. An investor should not replicate part or all of, or rely on the model portfolio to construct its own investment portfolio. Please click on the following link in order to read full disclosure information for distribution from Bank Pictet & Cie (Asia) Ltd: Bank Pictet & Cie (Asia) Ltd (“BPCAL”) : www.group.pictet/trading/disclosure-trading-strategy-asia

Additional information is available upon request.

Tel: +41 58 323 1250; [email protected]

This document is intended for distribution to accredited investors, expert investors and institutional investors only and not for distribution to retail investors

18Banque Pictet & Cie SA | Trading Strategy