market embeddedness and corporate instability: the ecology of

TRANSCRIPT

Market Embeddedness and Corporate Instability:The Ecology of Inter-industrial Networks

Ilan Talmud and Gustavo S. Mesch

Department of Sociology and Anthropology, University of Haifa, Mount Carmel, Haifa 31905, Israel

This paper studies the effect of inter-industrial control on the survival of Israeli firms. Itexamines how relationsbetweenenvironments modify relationswithin environments.More specifically, this paper studies how the social organization of the competition at theaggregate level (industry) affects outcomes at the individual (firm) level. Using trade dataand national accounts statistics, we specify and test the hypothesis that an industry’scorporate instability is negatively associated with its social capital (comprised from itsmarket embeddedness and political embeddedness). Our findings show that industry’scorporate instability within industries is associated with the industry’s structural embedded-ness in the network of input–output transactions, the degree of control it has over itsexternal transactions, and its political leverage.r 1997 Academic Press

MARKET EMBEDDEDNESS IN THE SOCIAL STRUCTUREOF THE COMPETITION

This paper studies the effect of inter-industrial dependency on the survival ofIsraeli firms.1 The first part of this paper presents the analytical research problem,using models of social capital and structural models of exchange. The secondsection reviews the differences between two approaches to social capital, derivingseveral testable hypotheses considering the effect of industry’s social capital.Then structural determinants of industry’s corporate instability are estimated.Finally, we discuss the findings and their implications for research on the relationsbetween environments and business organizations.

The first author thanks the Koret Foundation for financing the project. Both authors are grateful toYitshak Haberfeld, Shin-Kap Han, Michael Harrison, Robert Faulkner, Vered Krauss, Haya Stier, andtwo anonymous reviewers for their valuable comments and suggestions. We appreciate the technicalassistance provided by Bina Ben-Dor and Daphna Caspi.

Address reprint requests to Ilan Talmud, Department of Sociology and Anthropology, University ofHaifa, Mount Carmel, Haifa 31905, Israel. E-mail: [email protected].

1 This paper reports findings of the first stage of a larger project. The method used here is acomparative static approach to instability between two years, 1976 and 1986. We hope to analyze inthe second stage, firms’ survival using a dynamic model (i.e. event-history analysis)

SOCIAL SCIENCE RESEARCH26, 419–441 (1997)ARTICLE NO. S0970601

419

0049-089X/97 $25.00Copyrightr 1997 by Academic Press

All rights of reproduction in any form reserved.

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

No. of Pages—23 First page no.—419 Last page no.—441

1. SOCIAL CAPITAL AS A STRUCTURAL SOURCEOF MARKET INEQUALITIES

A. Economic Treatment of Market Imperfection and Rent

Despite the fact that contemporary economics of industrial organization dealswith structured inequality between producers, its baseline is still the theory ofperfect competition.

According to the paradigm of perfect competition, supply and demand arefreely negotiated. Moreover, this theory holds that to the extent to which themarket is perfect, buyers and sellers are numerous, small, and anonymous, andcommodities can be divided infinitely. As a result, trade is assumed to beperformed under conditions of equity on individual dyadic base, no single agenthas a noticeable influence over price by his or her conduct, and there are no exit orentry barriers for producers. Market outcomes, then, are a product of individuals’gaming behavior. One consequences of this individualistic perspective of eco-nomic theory is a theoretical disregard with the conduct ofobservablemarket.

As a consequence of this idealist and individualist bias, only a few leadingeconomists paid systematic theoretical attention to rent-creation and rent-seekingbehavior.2 Rent is defined as an economic profit that is earned when competition isnot free or markets are imperfect (such as under monopoly). Moreover, even thoseeconomists who pay tribute to the phenomenon assume an ideal reality of perfectcompetition, where there are no socially structured inequalities. Hence, imperfectcompetition and rent creation are considered as ‘‘deviant cases.’’ The existence ofmonopoly is explained as a function of scale economy, production advangate, orintellectual property right. The economic theory usually does not discuss casesstemming from structural rigidities and social capital.3 Consequently, rent, whichis the outcome of market power, is assumed to be a temporary situation (Sorenson,1996). Neo-classical theorists, have thus failed to perceive that the real marketoperates under intrinsic structural barriers to ‘‘free’’ competition in the form ofsocial capital and political institutions, which are inherent forces of the economicrivalry.

B. The Sociology of Competition, Social Capital, and Rent

By contrast to the individualist ‘‘baseline’’ approach of neo-classical theory,sociologists treat the market, like any other social areana, as socially structured.Consequently, in sociology, social capital is regarded as pervasive and inevitable.Social capital is any aspect of social organization that provides comparativeadvantage to one actor or more.4 Rent, which is an outcome of the operation of

2 Prominent exceptions are Alfred Marshall, Krueger (1974), and Bhagwati (1982). See Sorenson(1996) for a recent extension of the theory of rent into the field of social stratification.

3 Moreover, contemporary economic theory maintains that even under a monopoly control, marketposition can be ‘‘contestable’’ (Baumol, Panzar, and Willig, 1986), as another potential producer couldoffer the holder of the monopoly the discounted value of its monopoly return.

4 This definition is slightly different from Coleman’s (1994: 1970).

420 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

social capital, is depicted as ‘‘any advantage or surplus created by nature or socialstructure over a certain period of time’’ (Sorenson, 1996, p. 1344). Rent, then, istightly connected to the social structure of the competition and to economicagents’ social capital. Individual may rationally invest in social capital, aiming tomaximize or maintain an established advantageous market position, using allsorts of social investments. As a result, surplus in revenues, derived from socialcapital (over and beyond what is expected from ‘‘market equilibrium price’’), issometimes depicted as a result of ‘‘directly unproductive, profit-seeking behav-ior’’ (Bhagwati, 1982).

Weber describes the market as a social arena, where a price is determined by astruggle between parties. Yet, the struggle between parties is influenced by ‘‘aplurality of potential exchange partners,’’ seeking opportunities and power. ForWeber, market outcomes are consequences of actors’ rational considerations andpower. In other words, the process of competition—that ends up in an exchange(Swedberg, 1994, p. 265)—is a function of a direct power struggle betweenparties and indirect influence of potential competitors, buyers and suppliers. Thesocial organization of the competition sets up the opportunity space for each party.Weber asserts that economic power is a function of an organization capacity todictate prices to both exchange partners and competitors (Weber, 1978, pp.941–943). Collusions, tacit agreements, and oligopolistic structures providefirms, by squeezing profits from a third party (either the supplier or the consumer),with the capacity to operate even at high costs (Baker and Faulkner, 1993).

Additionally, Weber treated politics as an independent source of power. Inmany cases, political embeddedness of the market, institutional regulation andgovernment-sanctioned restrictions on competition permeate the economy, thusaugmenting barriers to entry (Levacic, 1987, pp. 118–138).

This Weberian insight was further elaborated by the sociological treatment ofrational choice and by the structural analysis of markets. First, models of powerand exchange stipulate the conditions under which actors control outcomes insystems of exchange. More specifically, models of social exchange have shownthat power and social capital are related to availability of direct and indirectresources (Emerson, 1972; Cook et al., 1983; Markovsky et al., 1988).

Second, models of resource dependence have argued that discretionary powerand organizational control are a function of resource spread over trade partners(Pfeffer and Salancik, 1978).

Third, in a similar way to models of resource dependence and to theories ofsocial exchange, network analysis inquires into the impact of relationship struc-ture on interdependencies and inequalities among actors (see Burt and Talmud,1993). More particularly, in this framework, relationship structure modifies thedegree to which an actor controls his or her transactions (Emerson, 1972; Cook etal., 1983; Marsden, 1981; 1983; Burt, 1983; Stokman et al., 1985; Stearns andMizruchi, 1986; Burt, 1988a; Markovsky, Willer and Patton, 1988; Burt andCarlton, 1989).

Further, network models of market operation describe how social capital,

421MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

defined by parameters of imperfect competition, shapes the ability of a rent-maximizing, rational actor to influence price and accumulate resources (Burt,1983; 1988a; 1992; Burt and Carlton, 1989).

C. Social Capital as Market Advantage

As an extension of both resource dependence and models of social exchange,Burt shows that entrepreneurial opportunity increases with disconnection be-tween network clusters (Burt, 1992, esp. Chaps. 1, 2). This theory is consistentwith Kirzner’s theory of real-world market process and myopia (Kirzner, 1973;1979). Moreover, Burt implements his theory of ‘‘structural holes’’ in a variety ofcontexts, including the national business market, precisely operationalizing a keystructural dimension of imperfect competition. Burt asserts that dependence is afunction of alternative (direct and indirect) opportunities. Structural alternativeopportunities for resources are captured by: (1) how resource segments areorganized and (2) the manner in which trade partners are connected (Burt, 1982;1983; 1988a; 1989; 1992). Thus, it is not just the strength of relations, but also the(direct and indirect) structure of those relations that define market power. Socialcapital, therefore, is a direct function of market imperfection. Rent creation,therefore, is intimately related to an actor’s social capital, derived by its positionin a transaction network.

2. TWO PERSPECTIVES ON SOCIAL CAPITAL: THE IMPACTOF SPARSE VERSUS DENSE NETWORKS

Different schools have emphasized various dimensions of social capital:cultural capital and symbolic capital, on the one hand (Bourdieu, 1987) versusnets’ closure, actor’s exchange alternative, and collective goods, on the other(Coleman, 1988; 1994). One of the consequences of this heterogeneous use is thatin the sociological literature, social capital is vaguely specified.

By contrast, in this study we define social capital more narrowly, followingBurt (1982; 1983; 1992), as a function of actor’s structural location in the(imperfect) competition. An analytical benefit of this definition is that it isconsistent with the logic behind both the rational choice approach to competition,and with the economics of market power. Next, we address the following issue:What kind of social capital is advantageous? (See Fig. 1.)

A. Rent As A Result of A Sparse Network

Recent literature on social capital and competitive advantage has stressed therole of weak ties and sparse social networks in determining performance in verydifferent settings and levels (Burt, 1992). For examples, job seekers with sparsenetworks find new jobs through weak ties more quickly than those connected tostrong, dense ties (Granovetter, 1973; 1974). Similarly, it was found that firmsspreading their ties with unconnected market segments are more profitable thanthose connecting to ‘‘redundant ties’’ (Burt, 1988a; Burt and Carlton, 1989;

422 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

Talmud, 1992; 1994). Coleman (1994, pp. 172–178) suggested that dense net-work may inhibit economic innovation. In the marketplace and inside organiza-tions, players develop ways to manage their dependence, while protecting theiradvantage in strategic positions (Galaskiewicz, 1985; Baker, 1990; Garguillo,1993). Burt found that managers with non-dense networks are ‘‘fast movers’’ inthe organizational promotion ladder (Burt, 1992, Chap. 4), and Lin and hisassociates showed that holders of high status acquire prestigious positions viaweak ties (Lin, Ensel, and Vaughn, 1981; Lin, 1982; Lin and Dumin, 1986).5

Additionally, two primary networks concepts: prominence (Burt, 1983b) andcentrality-as-betweenness (Freeman, 1979) implicitly assume that ego’s power isa function of his or her association with sparse network clusters.

B. Control As A Result of A Dense Network

In contrast, other studies on social capital and rent creation have foundsignificant impact ofstrong tiesand dense networksin creating opportunities.Coleman stresses the major benefit of closure in social nets (Coleman, 1988). Thisline of thought was corroborated in many studies. For example, people occupyingunsecured positions, especially under conditions of severe scarcity, use strong tiesto find a job (Granovetter, 1982). Similarly, Krackhardt found that trust andpolitical moves within a business firm are facilitated via ‘‘philos’’ relations(Krackhardt, 1992). In a similar way, Lin and his associates found that first job in

5 This mechanism is valid also in the inter-personal arena: families who have unconnected friendshave more autonomy in their role performance (Bott, 1957). Weimann found a structural advantage ofweak ties and marginal individuals in the process of communication flow (Weimann, 1982, 1983).

FIG. 1. Two approaches to social capital.

423MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

the university system is typically found through strong ties (Lin, Ensel, andVaughn, 1981; Lin, 1982; Lin and Dumin 1986). Also, the adoption of a newproduct and the reception of technical innovation are usually affected by cohesivenetworks and communication flow through strong ties (Katz and Lazarsfeld,1955; Menzel and Katz, 1955; Rogers, 1963; Rogers and Kincaid, 1981; but seeBurt, 1987). New business information and opportunities are enhanced throughcohesive contacts (Aldrich and Zimmer, 1986; Gilad and Kaish, and Ronen,1989). Other examples are relevant here: product prices are fixed through tightsocial networks (Faulkner, 1983; Faulkner and Anderson, 1987; Baker andFaulkner, 1993); and securities’ price fluctuations are moderated to the extent thatthe dealers have ‘‘clique’’ relations among them (Baker, 1984). By contrast, Tamshowed that strong mentorship ties do not produce economic advantage amongAmerican lawyers (Tam, 1996). The effect of strong ties seems to be a conditionalone. For example, it is evident that, while male managers are promoted viaentrepreneurial networks which are composed mainly of non-redundant ties,female middle managers are typically promoted through strong ties with astrategic ally (Burt, 1992, Chap. 4). At another level, Burt (1992) and Han (1993)revealed that, contrary to the logic behind the theory of resource dependence.Those American firms having high recourse dependence on the governmentsurvive at higher rates. These analytically related findings—on female insidemanagement and on state-dependent firms—are highly meaningful because theyindicate that to the extent that an economic domian is under ‘‘uncertainty,’’6

embedding economic transactions in strong relations, or constructing the eco-nomic deal in terms of strong ties, could serve as remedies for survival.

The literature on vertical integration also supports the ‘‘strong tie’’ perspective.To the degree that transaction costs are excessive, and to the extent thatuncertainty plays an important role in the transaction, embedding relations in ahierarchical organization can be a beneficial strategy for gaining an advantageousposition in the market (Hennart, 1988; Williamson, 1994).7 In fact, forming closenetworks ties can be an alternative strategy for strictly vertically integratedhierarchy (Powell, 1990). The network form of organizing lowers monitoringcosts and, at the same time, enable the firms a more flexible exit in times ofchanging preferences (Powell, 1990; Uzzi, 1996). Network form of inter-organizational embeddedness is particularly suitable strategy for purposes suchas: maintaining access to reliable and non-standard information, trade in repeated

6 The reality of management and the operation of political organs such as states involve politicaldimensions that augments uncertainty (DiMaggio and Powell, 1990). It is very difficult to assess whois a ‘‘good manager’’; this is the reason why the ‘‘ceiling glass’’ effect takes place for womenmanagers. Similarly, as governments do not compete with one another over local suppliers, andbecause it is reasonable to assume that in the institutional sector the terms for vying are less clear andcompetitive, firms’ operation in a highly politically-embedded domains stems from negotiatedinstitutional environment.

7 Transaction-cost economics focuses mainly on dyadic interface between organizations, whilenetwork theory conceptualizes leverage and control as generated by a triad structure of the trade. Bothperspectives, nonetheless, emphasize the relationship management of the actors.

424 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

transactions, while also preserving other opportunities at hand (Geertz, 1978;Powell, 1990; Uzzi, 1996).

C. A Suggested Integration

It seems that there is no such thing as a universal optimal network structure(dense or sparse). Coleman asserts that ‘‘social relationships that constitute socialcapital for one kind of productive activity may be impediments for another’’(Coleman, 1994, p. 177). We argue that each form of control (dense networkversus sparse network) is beneficial only under certain conditions. Indeed, itseems that different conditions modify distinct networks’ strategies. Both Ibarra(1992) and Krackhardt (1992) argued and showed that a combination of au-tonomy and cohesive networks are used, depending on the structural context ofadvantage and constraint. Similarly, studying entrepreneurial success in a networkorganization, Gabbay has found that corporate turnover is predicted both bystructural autonomy and network density (Gabbay, 1997). Gabbay asserts that thesuccessful manager has a dual advantage: non-redundant business opportunitiesare provided to him or her by non-connectivity among alters, while trust andcohesion are provided by strong ties with some other colleagues. Gabbay foundevidence that network density (indicating average strength of relations) andstructural autonomy are two different dimensions of successful entrepreneurialopportunity structure (Gabbay, 1997).

In a similar way, Uzzi found in his study of the New York apparel industry thatorganizational failure increases to the degree that the focal firm’s network tends tobe comprised of either all arm-length ties (i.e. ‘‘under-embedded,’’ disconnected,non-redundant contractors), or all embedded ties (i.e., ‘‘over-embedded,’’ dense,semi-integrated contractors). Uzzi found out that organizational survival ispositively associated with a ‘‘mix model’’ network, which provides a combinedadvantage. On the one hand, market embeddedness provide benefits such as: trust,joint problem-solving arrangement, complex adaptation, reduced bargaining andmonitoring costs. On the other hand, arms-lengths contacts facilitate the firmswith new and novel information outside the immediate ties (Uzzi, 1996; 1997). Insum, the conditional approach to social control argue that the logic behindnetwork form is contingent.

3. EXAMINING INSTABILITY IN NETWORK MODELS

It is evident that the effect of corporate social capital on corporate turnover isconditional. Despite the dramatic stabilityacrossmarkets, Burt (1992) and Han(1992) found a relatively high volatility of firmswithin markets which wasaffected by industry’s network position. Yet, similar to the above-mentionedGabbay’s assertion (Gabbay, 1997), they established that different structures ofdependencies determine the level and direction of corporate survival. They foundthat organizational instability increases with inter-industrial dependence on otherbusiness. In contrast, high dependance on the government decreases firms’instability (Burt, 1992, Chap. 6; Han, 1992).

425MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

A. Basic Premise

Following this structural tradition, the present study examines the manner inwhich the social organization of market competition affects firm’s survival. Weuse data industry level-of-analysis to predict its corporate instability between twotime points.

Our general postulate is that there is a direct positive association between theextent to which an industry controls its transactions, and the level of its stability.8

In other words, the greater the degree to which an industry controls its trade, thehigher the likelihood of an occurrence of corporate stability within it. Next, weattempt to specify and examine the structural modes under which an industrycontrols its trade.

B. Hypotheses Specification

H1.An industry is stable to the extent that its organization of ties is efficient. Anefficient organization of ties indicates a non-redundency in an industry’s transac-tions and can serve as a structural leverage for rent appropriation and profitsqueezing behavior (Burt, 1992; Talmud, 1992; 1994).

H2. Ceteris paribus, an industry is stable to the extent that the transactionsdensity among its trading partners is high. According to the dense networkliterature (e.g. Lin, Ensel, and Vaughn, 1981; Gabbay, 1997), control is a functionof strong ties and may provide a substantial cohesion as a buffer against unstableenvironment.

H3. An industry is unstable to the extent that its alters increase their densitybetween 1976 to 1986. Such an increase indicates a higher ability of alters tocontrol the focal industry’s behavior by their intensified interconnection. Theopposite logic suggests that loosing control between alters may provide the focalindustry with more leverage and autonomy.

H4. An industry is stable to the extent that its firms are politically owned. Inlight of resource mobilization literature and institutional theories of organizations,then, this proxy reflects an industry’s ability to gain material support from thepolitical sphere. It is a positive function of an industry’s access to the core of thepolity (Tilly, 1978; Laumann and Knoke, 1987).9

8 ‘‘Control’’ refers to what Alfred Marshall calls ‘‘the external economy’’ of the firm, and not to its‘‘internal economy.’’ Parallel thinking is found in resource dependence theory (Pfeffer and Salancik,1978) and transaction costs economics (Williamson, 1985). In network models of markets, the termsignifies the control over external relations, which is a function of inter-industry buying and sellingactivities and the degree to which each industry is organized (Burt, 1983: 224–235).

9 A recent study on the lobbying power of fifteen Israeli manufacturing industries has shown thatchange in protectionist policy (tariff setting) is influenced by the extent of the public sector’sownership in an industry (Kahane, 1992). This variable predicts both net industrial profitability anddirect subsidies granted to producers by the state (Talmud, 1992). We combined ownership ofestablishments by the government and ownership by the Histadrut (Labor Federation) because theyhave both served the same political and financial functions, and they demonstrated a similarmanagerial and business performance. This is also consistent with institutional theory. See anelaborate discussion in Talmud, 1992.

426 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

H5. An industry is stable to the degree it is oligopolistic. Oligopoly hamperscompetition by providing a profit-squeezing capacity (or unproductive rent-seeking behavior) by utilizing switching cost, capital requirements, regulations,barriers to entry a new technology, etc. (Caves, 1976; 1982; Porter, 1980: chapter5; Jacquemin, 1987; Shapiro, 1989).

C. Method

1. Data.A. The data used for this analysis are the input–output tables of theIsraeli industries, for the years 1977 and 1986, accounting for 41 industries.10 Aninput–output table describes the Israeli detailed intermediary transactions ofcommodities and other material traded in factor or input markets. Each input–output industry is an aggregation of structurally equivalent economic establish-ments, operating in the same environment and using a homogeneous technology.Thus, the specified resource flows at the industry level are aggregate outcomes ofindividual interactions of firms operating within that industry. These tablesdescribe the inter-industrial transactions in a given fiscal year. In other words, aninput–output table describes the amounts of money each industry spent (as abuyer) on purchases from every other Israeli industry, and the sums of funds eachindustry received (as a seller) from every other industry. The table represents thenetwork of resource flows between and within industrial branches. It describes thedirect and indirect inter-industrial linkage of the Israeli economy. The rowi in thetable represents the industry’s sales, whereas the columnj specifies the industry’spurchases. (See Fig. 2.)

B. In addition, we usedIndustry and Craft Surveydata (State of Israel, 1981)to calculate the public sector’s size for the 25 manufacturing industries. TheIndustry and Craft Survey are performed by the Israeli Central Bureau ofStatistics, furnishing a highly reliable data set on manufacturing industries’production attributes.

C. Data on industry’ corporate instability were obtained from Dunn andBradstreat’s trade publications for all Israeli corporations for the years 1976 andin 1986. After adjusting different industrial classification in the I/O tables and inDunn and Bradstreat’s publications, we calculated dropout rate for each industry.More specifically, we formed a list of the 10 largest firms (according to sales) forevery industry, once for 1976, and once for 1986.11

10 The input-output table accounts for 43 industries since 1977 (State of Israel, 1977), due to theUnited Nation’s directive. The tables comprised business outcomes from structurally-equivalent profitcenters, regardless of legal boundaries. Yet, Repairs and Maintenance industry and General Commerceindustry are two residual classification categories. These two industries are too heterogenous becomprised of structurally equivalent players. Previous analyses (Talmud, 1992; 1994) have confirmedthat these industries are outliers in any analysis.

11 A few words on data choice are needed here. We selected the years 1976 to 1986 simply becausethere are no input-output data on the Israeli market at this level of aggregation prior to or followingthose years. For the firms, we chose to focus our attention on the first biggest ten in each industry,because it fits the size of the Israeli economy. A similar analysis conducted on the American market

427MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

2. Variables. Dependent variable:Dropouts is the number of firms that wereremoved from the list of the top 10 in each industry between 1976 to 1986.12 Itindicates the extent to which variations in competitive pressures differentiallyeliminate ‘‘looser’’ corporations from the top 10 list, and the degree to whichinstability within the main industrial players is observed, at least among thebiggest 430 firms (10 biggest firms in each 43 industries).13

(Han, 1993) picked up the first twenty firms, a choice which—for some Israeli industries—seemsmeaningless. Alternative cut off points, including standardization of the list size to the entire numberof firms operating in an industry are relevant, but, unfortunately, unrealistic due to data limitation. Wechose to define dominance in the market based on rank of sales. We had theoretical and empiricalreasons for this choice. Theoretically, sales is the most prevalent dimension for various proxies ofintra-market power (see Jacquemin, 1987, pp. 48–65). Other dimensions of dominance (numbers ofemployees, production capacity, export) have more biases. Empirically, sales was the only consistentmeasure, lacking missing data, across all population of firms and industries.

12 Surely, there could be raised some hypothetical alternative reasons to dropouts. Yet, in the realityof the Israeli oligipolistic market of the 1970s and 1980s, corporate merges and acquisition practicewas virtually absent. Similarly, organizational death of one of the ‘‘BIG 10’’ did not occur (unlike thebottom of the list). This reality, especially regarding mergers and acquisition activity, was dramaticallychanged since the 1990s, where globalized financial markets along with restructured stock marketpractices were introduced. However we want to remind the reader that the data used in this research isfor changes between 1976–1986. Additionally, out of our total 430 corporations, two companies,nested in two different industries, changed their positions between 1976 to 1986 from their originalSIC industry into another. These two firms reappear in 1986 as dropouts in their original industries,1986, and as new entrants in their destination industries. The firms changed their strategic profileprecisely because of competitive pressures.

13 The use of additional five alternative measures of industrial stability will be discussed below.

FIG. 2. Industries as dealers in a transaction matrix.

428 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

Independent variables:Contact Efficiency is the proportion of non-redundantcontacts out of the total contacts made by an industry. Non-redundancy is theopposite of dependence between industry’s transactions. Contact Efficiencyindicates an efficient organization of ties in dealing with other industries, showingthe degree to which an industry is strategic.14 Formally, non-redundancy measureof range is defined as

Non-redundancy5 oi31 2 o

q

PjqMjq 4,i Þ j

j Þq

q Þ i

, (1)

where the summation is across all of industryi’s N contacts and where (1)Piq isthe proportion ofi’s industry network effort (in terms of shipments, money andenergy) invested in the relationship with industryq. Piq then, expresses theinteraction with industryq, divided by the total of industryi’s contacts with otherindustries,

Piq 5 (Ziq 1 Zqi) ⁄oj

(Zij 1 Zji), i Þ j. (2)

(2) miq is the marginal strength of relations from contactj to q. It expresses theratio between the interaction ofj with q, quantity divided by the strongest ofj’srelations with any other industry,

Mjq 5 (Zjq 1 Zq j)/MAX ( Zjk 1 Zkj), j Þ k, (3)

where MAX (Zjk 1 Zkj) is the largest of industryj’s relations with any otherindustry.mjq varies between zero to unity. This measure expresses the degree towhich an industryi has many independent ties. Dependence betweeni and jsignifies a high overlap betweeni contacts toj contacts. Range is the additiveinverse of industry ties dependence. More specifically, this measure estimates thedegree of whichq is a large proportion ofj’s contacts, andi has contact withj.This overlap is subtracted from unity, and the measure sums the results acrossj’scontactsi. Finally, Contact Efficiency is the ratio

Number of non-redundant ties

Number of total contacts. (4)

14 Non-redundancy and prominence are linked. A prominent industry is sought by many uncon-nected clusters of industry. Range, therefore, is a component of prominence (see Burt, 1983b, 1989,for a comprehensive review). This link is especially valid in relatively sparse networks which are alsocomposed of asymmetric relations, such as a transaction matrix between input-output industries.While Burt’s measure of non-redundancy can be used as a proxy for total range (or effectiveness),contact efficiency is the ratio of an industry’s non-redundant ties to its total contacts (Burt, 1983).Though network effectiveness (non-redundancy) and network efficiency have non-linear relations (seeBurt, 1992, Chap. 1), previous studies on Israeli industrial profitability and political support revealedthat contact efficiency is the most powerful and robust predictor of both industry market power andindustry political leverage (Talmud, 1992; 1994).

429MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv3/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 rich

Proportional Density is a proxy for local cluster’s cohesion in t1 (1976). Itmeasures the degree of transaction density among the trading partners of anindustry. It estimates the extent to which alters or contact pairs have some kind ofconnection with one another. This proportional measure of density varies fromzero (no relations between alters) to 1 (every pair of alters are in contact).Whereas network density measures the average marginal strength of relations(relative to the strongest), proportional density indicates the extent to whichrelations between the focal industry and its trade partners are both direct (betweenan industry and its alter) and indirect (between alters).

1oi

oj

diq2 ⁄N(N21), i Þ q (5)

Ddensity is the difference between proportional density in 1986 to the level ofproportional density of 1976.

Share is the proportion of the four largest firms’ sales in relation to the totalindustry’s output, and is a accepted index of industrial concentration for aneconomy comprised mainly of oligopolistic competition (Caves, 1976; 1982;Jacquemin, 1987).15

Political Ownership is the proportion of legal possession of economic establish-ments by political organs in an industry. It is a proxy for the magnitude of politicalties that managers of an industry have to the political structure. The degree ofpolitical ownership approximates the managers’ ability to mobilize resources fortheir industry’s benefit (Tilly, 1985). Previous studies showed that politicalownership had a strong positive effect on tariff protection, subsidies, and a directnet effect on profitability (Kahane, 1992; Talmud, 1992; 1994).

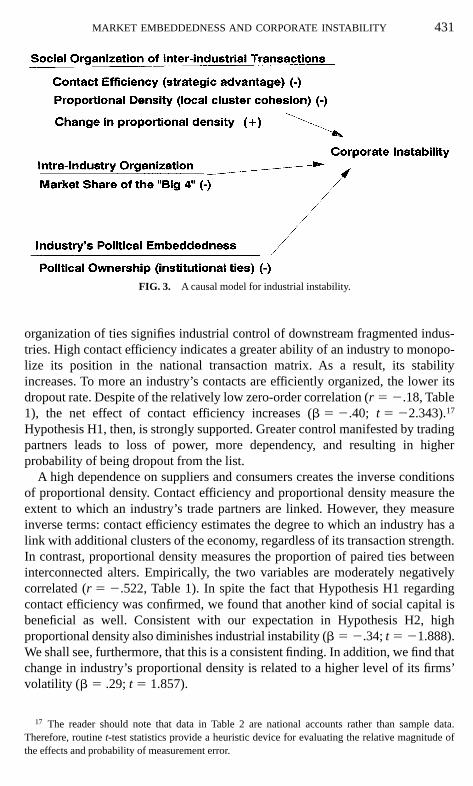

Manufacturing Industries is a dummy variable used to control the presumedslower adjustment rate of manufacturing firms to enter and to exit industrialactivities. It reflects also the higher tendency of this sector to depend on largebatches and capital-intensive technology, leading to an increase of the ‘‘optimalestablishment size,’’ and thereby elevating the barriers to entry to and exit fromthe industry. (See Fig. 3.)

3. Findings.Dropout rates of Israeli industries between 1976 to 1986 wereregressed on their network characteristics, using unrestrictive OLS models.Descriptive statistics and a pairwise correlation matrix are presented in Table 1.The Ordinary Least Squares results are shown in Table 2.16 Table 2 shows that theway in which transactions are conducted is the most significant factor: contact-efficient industries have a notably more advantageous position. Dealing withunlinked industries provides a strategic advantage. An industry is strategic to theextent that it is sought by different fractions of the national economy. An efficient

15 Other measures of intra-industry relations, such as Herfindahl’s index or Thail index of absoluteor relative entropy, are more biased, and are useful to estimate market power in a more detailedindustrial classification system (see a review in Jacquemin, 1987, pp. 48–65).

16 Coefficient variance inflation (VIF), as a direct index of the extent to which collinearity harmsestimates’ precision (Fox, 1991, pp. 252–259), is low, varying between 1.0008 to 1.29.

430 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

organization of ties signifies industrial control of downstream fragmented indus-tries. High contact efficiency indicates a greater ability of an industry to monopo-lize its position in the national transaction matrix. As a result, its stabilityincreases. To more an industry’s contacts are efficiently organized, the lower itsdropout rate. Despite of the relatively low zero-order correlation (r 5 2.18, Table1), the net effect of contact efficiency increases (b 5 2.40; t 5 22.343).17

Hypothesis H1, then, is strongly supported. Greater control manifested by tradingpartners leads to loss of power, more dependency, and resulting in higherprobability of being dropout from the list.

A high dependence on suppliers and consumers creates the inverse conditionsof proportional density. Contact efficiency and proportional density measure theextent to which an industry’s trade partners are linked. However, they measureinverse terms: contact efficiency estimates the degree to which an industry has alink with additional clusters of the economy, regardless of its transaction strength.In contrast, proportional density measures the proportion of paired ties betweeninterconnected alters. Empirically, the two variables are moderately negativelycorrelated (r 5 2.522, Table 1). In spite the fact that Hypothesis H1 regardingcontact efficiency was confirmed, we found that another kind of social capital isbeneficial as well. Consistent with our expectation in Hypothesis H2, highproportional density also diminishes industrial instability (b 5 2.34;t 5 21.888).We shall see, furthermore, that this is a consistent finding. In addition, we find thatchange in industry’s proportional density is related to a higher level of its firms’volatility (b 5 .29; t 5 1.857).

17 The reader should note that data in Table 2 are national accounts rather than sample data.Therefore, routinet-test statistics provide a heuristic device for evaluating the relative magnitude ofthe effects and probability of measurement error.

FIG. 3. A causal model for industrial instability.

431MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

Table 3 examines the extent to which industry’s structural embeddedness (inthe national transactions network) and its political embeddedness (in the manage-ment of the economy) affect industrial instability. Previous studies have shownthat both dimensions of industrial embeddedness are strongly associated with twomeaningful dimensions of rent appropriation. In these studies, inequality betweenproducers in profitability and in state direct subsidies was explained by variationsin contact efficiency and in political ownership (Talmud, 1992; 1994). Becausedata on political ownership were available for only 25 manufacturing industries,

TABLE 1Descriptive Statistics and Zero-Order Correlation Matrix

Mean (SD) (1) (2) (3) (4) (5)

Dropouts5.366 (2.709) (1)Share.631 (.351) (2) .1129Proportional Density.413 (.136) (3) 2.1989 .0426Ddensity2.001 (.053) (4) .3416 .1166 2.3004Contact Efficiency.881 (.046) (5) 2.1811 2.0417 2.5225** .1766Political Ownership*.122 (.094) (6) 2.263 2.284 2.237 2.317 .154

Note. Nof cases, 41; 1-tailed Signif, **, .001; * N of cases, 25; see data description in text.

TABLE 2OLS Estimates of Israeli Industrial Instability

1976–1986

Contact Efficiency 2.40**(22.343)

Proportional Density 2.34*(21.888)

Manufacturing industries (dummy) .10(.620)

Ddensity .29*(1.857)

Share .04(.234)

R2 5 .26

Note. N 5 41. Standardized effects.t value inparentheses.

* Significant atp , .05.** Significant atp , .01.

*** Significant at p , .001.

432 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

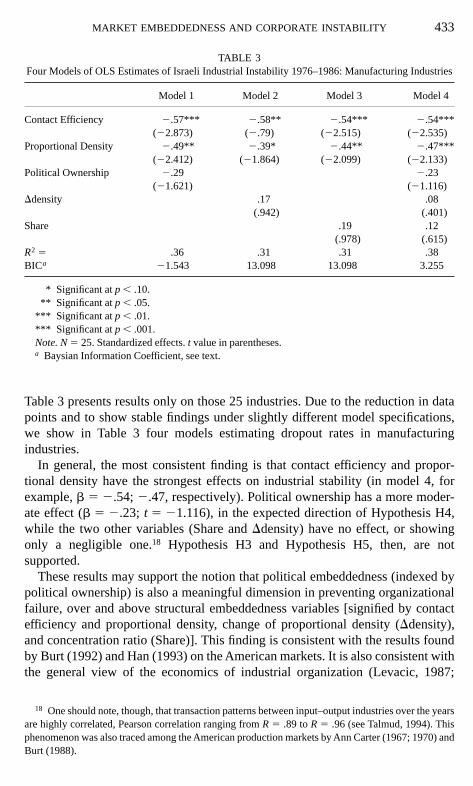

Table 3 presents results only on those 25 industries. Due to the reduction in datapoints and to show stable findings under slightly different model specifications,we show in Table 3 four models estimating dropout rates in manufacturingindustries.

In general, the most consistent finding is that contact efficiency and propor-tional density have the strongest effects on industrial stability (in model 4, forexample,b 5 2.54; 2.47, respectively). Political ownership has a more moder-ate effect (b 5 2.23; t 5 21.116), in the expected direction of Hypothesis H4,while the two other variables (Share andDdensity) have no effect, or showingonly a negligible one.18 Hypothesis H3 and Hypothesis H5, then, are notsupported.

These results may support the notion that political embeddedness (indexed bypolitical ownership) is also a meaningful dimension in preventing organizationalfailure, over and above structural embeddedness variables [signified by contactefficiency and proportional density, change of proportional density (Ddensity),and concentration ratio (Share)]. This finding is consistent with the results foundby Burt (1992) and Han (1993) on the American markets. It is also consistent withthe general view of the economics of industrial organization (Levacic, 1987;

18 One should note, though, that transaction patterns between input–output industries over the yearsare highly correlated, Pearson correlation ranging fromR 5 .89 toR 5 .96 (see Talmud, 1994). Thisphenomenon was also traced among the American production markets by Ann Carter (1967; 1970) andBurt (1988).

TABLE 3Four Models of OLS Estimates of Israeli Industrial Instability 1976–1986: Manufacturing Industries

Model 1 Model 2 Model 3 Model 4

Contact Efficiency 2.57*** 2.58** 2.54*** 2.54***(22.873) (2.79) (22.515) (22.535)

Proportional Density 2.49** 2.39* 2.44** 2.47***(22.412) (21.864) (22.099) (22.133)

Political Ownership 2.29 2.23(21.621) (21.116)

Ddensity .17 .08(.942) (.401)

Share .19 .12(.978) (.615)

R2 5 .36 .31 .31 .38BICa 21.543 13.098 13.098 3.255

* Significant atp , .10.** Significant atp , .05.

*** Significant at p , .01.*** Significant at p , .001.Note. N5 25. Standardized effects.t value in parentheses.a Baysian Information Coefficient, see text.

433MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

Caves, 1982) and with the logic behind the sociological institutional theory(DiMaggio and Powell, 1990).

Table 3 reports also the Bayesian Information Coefficient (BIC) as a goodness-of-fit statistics for the different regression models. The BIC has recently beengeneralized for a variety of other statistical procedure besides the standard use ofit in the evaluation of long-linear models (Raftery, 1995; see an application inKraus and Maestracci, 1997). BIC indicates the relative likelihood that a modelfits a given data set. It provides a statistical comparison between various modelspecifications as a function of the number of cases, explained variance, and thenumber of independent variables in the equation. For the ordinary least square(OLS) models, BIC is calculated as

BICi 5 N[ln (1 2 Ri2)] 1 pi[ln (N)], (6)

whereN is the number of cases andp is number of independent variables in theOLS regression modeli. When models are compared, the model with the mostnegative BIC value is the most likely to best fit the data.19

Comparing the four models in Table 3, it is clear that model 1, comprised fromthree independent variables (Contact Efficiency,Ddensity, and Political Owner-ship), has the most negative BIC value and is the best fitting model.

It is worth noting that Hypothesis H5 was not supported. One reason for thatcould be the highly oligipolistic nature of the Israeli economyacrossindustries,thereby minimizing variation in concentration ratio between industries. Thisphenomenon is also manifested in other developed and small countries such as theNetherlands, Japan, and South Korea.

One can claim that it is possible to capture corporate instability by othermeasures of industrial change. Consequently, we attempted to refine our operation-alization of corporate instability by introducing five alternative measures ofcorporate change:20 (1) Spearman’s Rho, which specifies the extent to which theorder of a firm’s rank in an industry (as ordered by sale volume) varies from 1976to 1986, (2) Kendall Taub, similarly measuring how many ranks a firm movesfrom 1976 to 1986, (3) a turnover rate, measuring the proportion between firmsdropping out the list from 1976 to 1986 to new entrants to the list in 1986 (Han,1993), (4) a regeneration index (following McNeil and Thompson, 1971, Tables2, 8), indicating the rate of industrial stability. (It is measured by the rate of‘‘stayer’’ firms in an industry to ‘‘movers’’ and ‘‘newcomers.’’21), and (5) an

19 A more restrictive requisite to conclude that one model fits better than the other is that the BICvalues of two (or more) models will differ in the order of 10 (Raftery, 1995). The difference betweenmodels 1, on the one hand, and models 2 and 3, on the other one, also fits this more restrictivecondition.

20 We would like to thank Robert Faulkner and an anonymous referee for raising this point.21 More precisely, the regeneration index is specified as the number of firms present in an industry’s

top 10 lists in both 1976 and 1986, divided by the firms present both times plus those present in 1986only (McNeil and Thompson, 1971, Table 8).

434 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

additional aggregate index of stability, specified as

Relative Range Stability5Îoi

(1976 Rank2 1986 Rank)2

number of ranks, (7)

wherei expresses a firm nested in one of the 43 industries.22Then, we repeated thefive OLS analyses shown above for each of the five indices. Nonetheless, wefound that none of these alternative operationalizations of corporate stability ispredicted by inter-industrial linkage. Overall, the only predictive variable of theexplained variance in these 25 analyses (five analyses for each dependentvariable) was the industrial concentration index. In general, inter-industriallinkage variables did not significantly contribute to the explaining power of themodel over and above industrial concentration.23 We therefore presented here theresults of the model, predicting variations of the more meaningful dependentvariable, namely: corporate dropout.

4. DISCUSSION

A. Two Conditions of Social Capital

This study has examined the ways in which relationsbetweenenvironmentsmodify relationswithin environments. More specifically, this study has demon-strated how environments and real market players are structurally embedded. Wealso showed that the social organization at the aggregate level (industry) affectsoutcomes at the individual (firm) level. We demonstrated that structural embedded-ness in the national transaction matrix and political embeddedness in the nationaleconomy play an important role in shaping corporate likelihood of durability.Corporate social capital, then, is a function of the industry’s structural location.

In other words, this study reveals that the structure of inter-industrial relationslays out the dependence characteristics among individual trade partners, hencedetermining firms’ capacity to survive under imperfect competition.

In concrete network terms, proportional density and contact efficiency are twodifferent, co-exiting, conditions of control over the external transactions of thefirm. High contact efficiency and high proportional density differentiate betweenthe marginal actor and the central player and they influence the firms’ stability.24

Contact efficiency and proportional density signifies two contrasting conditions ofsocial capital: the first condition indicates an overall efficiency in an industry’s

22 We thank one of our reviewers for this point.23 Tables are available upon requests from the authors. Our task here is limited to the inquiry of the

role of inter-industrial forces in shaping corporate instability. We do not wish to develop here a generaltheory of industrial organization and operation, linking intra- to inter-industrial forces. We merelyconclude, therefore, that for the proposed study, our dependent variable is the best alternative amongthe six operationalizations of industrial instability. We speculate that this could be so, preciselybecause it captures more extreme events of change in corporate ranking, namely: dropouts.

24 We didn’t find any impact of their interaction effects. The tests were performed using Allison’smethod (Allison, 1977).

435MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

transaction network, while the second circumstance can be interpreted as anindustry’s local effectiveness in the organization of economic ties. It seems thatindustries utilize two seemingly contradictory relational methods to gain anadvantage in the marketplace: efficiency and effectiveness. Yet, the preciserelations between cluster’s cohesion and ties’ efficiency, and their link withconcrete business strategy cannot be assessed using this highly aggregated dataset.

Industry’s social capital, then, is composed of at least three, presumablytenuous, dimensions: relatively an efficient organization of inter-industrial ties,relatively high cohesion in trade cluster, and strong linkage to institutionalizedpolitical sphere. This reasoning is consistent with Uzzi’s finding, derived from amicro level analyses, that ‘‘a firm’s structural location, although not fullyconstraining, can significantly blind it to the important effects of the largernetwork structure.’’ Additionally, ‘‘a paradox appears: optimal networks are notcomposed of either all embedded ties or arm’s-length ties but integrate the two’’(Uzzi, 1996, p. 694). Gabbay (1997) and Uzzi (1996; forthcoming) claims thateach kind of controlled embeddedness ‘‘yield positive returns up to a certainpoint,’’ and ‘‘embedded networks offer a competitive form of organizing, butpossess their own pitfalls.’’

Our interpretation, then, is consistent with Gabbay (1997) and Uzzi (1996;forthcoming). Competitive pressures create complex, dissimilar, and distinctnetworks forms, rather than a singly optimal embeddedness strategy. Yet, theseresults still leave us with a theoretical puzzle for future research regarding theprecise specification of the boundary conditions under which each form ofembeddedness is functional for the corporate organization.

B. A Few Issues for the Future

1. Conditional relevance of social capital.A general theoretical puzzle stemsfrom this study (as well as from the related inquiries of Burt, 1992; Han, 1992;Gabbay, 1997; and Uzzi 1996): It seems that ‘‘mix model’’ of embeddingeconomic relations is very beneficial. Yet, the theoretical question remains: underwhat general practical circumstances ‘‘over-embeddedness’’ [to borrow Uzzi’sterminology (1996)] of strong ties and closed networks is an asset and what arethe situations under which it is a liability? What are the conditions under which‘‘under-embeddedness’’ of unconnected market segments may prove beneficial?We have a partial answer to this question. We speculate that in the generaloperation of competition between producers, weak ties are beneficial. Yet, in allthose circumstances where trust, uncertainty, synergy, and long-term projects areinvolved, strong ties and cohesion are significantly important. Based on ourhighly aggregated data, however, we cannot precisely determine the rationality orthe fitness of social capital to the immediate economic context25 (though Gabbay(1997) and especially Uzzi (1996) elaborate and show the conditional rational).

25 See Hannan (1970) on problems of aggregation and disaggregation.

436 TALMUD AND MESCH

SSR601@xyserv3/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 rich

Further studies on the creation and operation of social capital under differentstructural conditions is highly required.

2. Cross-level analysis.Another way to scrutinize competitive process is torelate market structure, as specified by network models of competitive advantage,to individual firms’ structural attributes, using techniques such as cross-levelanalyses or Hierarchical Linear Models (Byrk and Raudenbush, 1988; Hox andKreft, 1994). Using this analytical strategy, the researcher may decomposevariations in organizational failure into inter-industry and intra-industry compo-nents.

3. Two levels of ‘‘residual analysis.’’Two important research agendas stem herefrom ‘‘residual analyses.’’ The first one is mainly interested in agency, while thesecond revolves around issues of structure. The first raises questions for futureresearch on business strategy, while the second addresses the nature of variousenvironments.

A. At the firm level-of-analysis: (1) Given our ability to predict the averageindustrial instability from network parameters of competitive advantage, what arethe organizational characteristics of the ‘‘losers’’ or the ‘‘winners’’ within eachindustry (i.e., those below and above the average prediction)? (2) How, forexample, do inter-industrial relationships differentially modify the ‘‘top 10,’’ onthe one hand, and small, peripheral firms, on the other (within each industry)?

B. At the industry level-of-analysis: (3) Given our capacity to draw a linkbetween inter-industrial relations and industrial stability, what are the structuralcharacteristics of ‘‘loser’’ and ‘‘winner’’ industries (i.e., those firms situatedbelow and above the regression line)?

4. Political embeddedness with the state and between producers.Further, thisstudy corroborates the general notion that political embeddedness is also keydimension of market operation, over and above structural embeddedness. Yetother questions have also to be examined at both the macro and micro levels. Theyinclude the effect of other indices of political capital (as derived by actors’location in the political organization of economy) on survival. These prospectiveresearch questions should include the ways in which the politics of markets—informal political networks, tacit collusions, trade unions, privatization andglobalization efforts, institutional regularities, latent financial aid, and tariffprotection—influence the survival of the firm.

REFERENCES

Aldrich, H., and Zimmer, C. (1986). ‘‘Entreprenuership through social networks,’’in The Art andScience of Entreprenuership (D. L. Sexton, and R. W. Smilor, Eds.), Ballinger, Cambridge, MA.

Allison, P. (1977). ‘‘Testing for interaction in multiple regression,’’American Journal of Sociology83,144–155.

Baker, W. E. (1984). ‘‘The social structure of a national securities market,’’ American Journal ofSociology89,775–811.

Baker, W. E. (1990). ‘‘Market Networks and Corporate Behavior,’’American Journal of Sociology96,589–625.

437MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv3/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 rich

Baker, W., and Faulkner, R. (1993). ‘‘The social organization of conspiracy in the heavy electricalequipment industry,’’American Sociological Review58,837–860.

Baumol, W. J., Panzar, J. C., and Willig, R. D. (1986). ‘‘On the theory of perfectly contestablemarkets,’’ in New Developments in the Analysis of Market Structure (J. Stiglitz and A.Mathewson, Eds.), pp. 339–365, MacMillian, Cambridge, MA.

Bhagwati, J. (1982). ‘‘Directly, unproductive profit seeking (DUP) activities,’’ Journal of PoliticalEconomy90,988–1002.

Bourdiue, P. (1987). ‘‘Social space and symbolic power,’’in In Other Words: Essays Towards aReflective Sociology, Polity Press, Oxford.

Bott, E. (1957). Family and Social Networks, Free Press, New York.Burt, R. S. (1982). Toward A Structural Theory of Action: Network Models of Social Structure,

Perception and Action, Academic Press, New York.Burt, R. S. (1983a). Corporate Profits and Cooptation, Academic Press, New York.Burt, R. S. (1983b). ‘‘Range,’’in Applied Network Analysis: A Methodological Introduction (R. S.

Burt and M. J. Minor, Eds.), pp. 176–194, Sage Publications, Beverly Hills.Burt, R. S. (1987). ‘‘Social Contagion and Innovation: Cohesion Versus Structural Equivalence,’’

American Journal of Sociology92,1287–1335.Burt, R. S. (1988). ‘‘The Stability of the American Markets,’’ American Journal of Sociology94,

356–95.Burt, R. S. (1991). STRUCTURE 4.2, Program of Structural Analysis, Center for the Social Sciences,

Columbia University, New York.Burt, R. S. (1992). Structural Holes: The Social Structure of Competition, Harvard Univ. Press,

Cambridge, MA.Burt, R. S. and Carlton, D. (1989). ‘‘Another look at the network boundaries of American markets,’’

American Journal of Sociology95,723–753.Burt, R. S. and Talmud, I. (1993). ‘‘Market niche,’’ Social Networks15,133–149.Byrk, A. and Raudenbush, S. (1988). ‘‘Methodology for cross-level organizational research,’’in

Research in Organizational Behavior, JAI Press, CT.Carroll, G. R. (1984). ‘‘Organizational ecology,’’Annual Review of Sociology10,71–93.Carroll, G. R. (1985). ‘‘Concentration and specialization: Dynamics of niche width in populations of

organizations,’’American Journal of Sociology90,1262–1283.Carter, A. (1967). ‘‘Changes in the structure of the American economy, 1947 to 1958 and 1962,’’

Review of Economics and Statistics49,209–224.Carter, A. (1970). Structural Change in the American Economy, Harvard Univ. Press, Boston.Caves, R. (1976). ‘‘The determinants of market structure: Design for research,’’in Market, Corporate

Behaviour and the State: International Aspects of Industrial Organization (A. P. Jacquemin andH. W. de Jong, Eds.), Vol.1, pp. 3–17, Martinus Nijhoff, The Hague.

Caves, R. (1982). American Industry: Structure, Conduct, Performance, Prentice-Hall, EngelwoodCliffs, NJ.

Coleman, J. (1988). ‘‘Social capital in the creation of human capital,’’American Journal of Sociology94,S95–S120.

Coleman, J. (1994). ‘‘A rational choice perspective on economic sociology,’’in Handbook ofEconomic Sociology, (N. Smelser and R. Swedberg, Eds.), pp. 166–181, Russell Sage andPrinceton Univ. Press, New York.

Cook, K. S., Emerson, R. E., Gillmore, M. R., and Yamagishi, T. (1983). ‘‘The distribution of power inexchange networks: Theory and experimental results,’’ American Journal of Sociology89,275–305.

DiMaggio, P. J., and Powell, W. W. (1990). ‘‘Introduction,’’in The New Institutionalism inOrganizational Analysis (W. W. Powell and P. J. DiMaggio, Eds.), pp. 1–38, Univ. of ChicagoPress, Chicago.

Emerson, R. (1972). ‘‘Exchange theory, part II: Exchange relations and network structure,’’inSociological Theories in Progress (J. Berger, M. Zelditch Jr., and B. Anderson, Eds.), HoughtonMifflin, New York.

438 TALMUD AND MESCH

SSR601@xyserv2/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 donn

Faulkner, R. (1983). Music on Demand, Transactions, New Brunswick, NJ.Faulkner, R., and Anderson, A. (1987). ‘‘Short-term projects and emergent career: Evidence from

hallywood,’’American Journal of Sociology92,879–909.Fligstein, N., and Brantly, P. (1992). ‘‘Bank control, owner control, or organizational dynamics: Who

control the large modern corporation?’’American Journal of Sociology98,280–307.Freeman, L. (1979). ‘‘Centrality in social networks: Conceptual clarification,’’ Social Networks1,

215–239.Fox, John (1991). Regression Diagnostics, Sage, London.Gabbay, S. (1997). Social Capital in Creation of Financial Capital, Stipes, Champaign, IL.Garguilo, M. (1993). ‘‘Two-step leverage: Managing constraint in organizational politics,’’ Adminis-

trative Science Quarterly38,1–19.Galaskiewicz, J. (1985). The Social Organization of an Urban Grants Economy, Academic Press, New

York.Geertz, C. (1978). ‘‘The bazaar economy: Information and search in peasant marketing,’’ American

Economic Review68,28–32.Gilad, N., Kaish, S., and Ronen, J. (1989). ‘‘Information, search, and entrepreneurship: A pilot study,’’

The Journal of Behavioral Economics18(3), 217–231.Granovetter, M. (1973). ‘‘The strength of weak ties,’’ American Journal of Sociology78(6),

1360–1361.Granovetter, M. (1974). Getting a Job, Harvard Univ. Press, Cambridge, MA.Granovetter, M. (1982). ‘‘The strength of weak ties: A network theory revisited,’’in Sociological

Theory (R. Collins, Ed.), pp. 201–233, Jossey-Bass, San Francisco.Han, S.-K. (1992), ‘‘Churning firms in stable markets,’’ Social Science Research21,406–418.Hannan, M. T. (1970). Problems of Aggregation and Disaggregation in Sociological Research,

Institute for Research in Social Science, University of North Carolina, Chapel Hill.Hannan, M., and Freeman, J. (1989). Organizational Ecology, Harvard Univ. Press, Cambridge, MA.Hennart, Jean-Francois (1988). ‘‘Upstream vertical integration in the aliminium and tin industries,’’

Journal of Economic Behavior and Organization9, 281–299.Hox, Joop J., and Kreft, I. (1994). ‘‘Multilevel analysis methods,’’Social Methods and Research22(3),

283–299.Ibarra, H. (1992). ‘‘Structural alignments, individual strategies, and managerial action,’’in Networks

and Organization (N. Nohria and R. Ecceles, Eds.), pp. 165–188, Harvard Business School Press,Cambridge, MA.

Jacquemin, A. (1987). The New Industrial Organization, MIT Press, Cambridge, MA.Kahane, L. H. (1992). The Political Economy of Israeli Protectionism: An Empirical Analysis, Public

Choice.Katz, E., and Lazasrfeld, P. F. (1955). Personal Influence, Free Press, Glencoe, Ill.Katz, D., and Kahn, L. (1978). The Social Psychology of Organizations, 2nd ed., Wiley, New York.Kirzner, I. (1973). Competition and Entreprenuership, Univ. of Chicago Press, Chicago.Kirzner, I. (1979). Perception, Opportunity, and Profit, Univ. of Chicago Press, Chicago.Krackhardt, D. (1992). ‘‘The strength of strong ties,’’in Networks and Organization (N. Nohria and R.

Ecceles, Eds), pp. 216–239, Harvard Business School Press, Cambridge, MA.Kraus, V., and Maestracci, P. (1997). ‘‘Do social classes determine income inequality? The Israeli

case,’’ unpublished manuscript, Department of Sociology, University of Haifa, Israel.Krueger, A. (1974). ‘‘The political economy of rent-seeking society,’’ American Economic Review

64(3), 291–303.Laumann, E. O., and Knoke, D. (1988). The Organizational State: Social Choice in National Policy

Domains, Univ. of Wisconsin Press, Madison.Levacic, R. (1987). Economic Policy Making, Brighton, Wheatsheaf.Lin, N. (1982). ‘‘Social resources and instrumental action,’’in Social Structure and Network Analysis

(P. V. Marsden and N. Lin, Eds.), pp. 131–145, Sage, Beverly Hills.Lin, N. and Dumin, M. (1986). ‘‘Access to occupation through social ties,’’ Social Networks8,

365–385.

439MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv3/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 rich

Lin, N., Ensel, W. M., and Vaughn, J. (1981). ‘‘Social resources and the strength of ties,’’ AmericanSociological Review46,393–405.

Markovsky, B., Willer, D. and Patton, T. (1988). ‘‘Power relations in exchange networks,’’ AmericanSociological Review53,220–236.

Marsden, P. V. (1981). ‘‘Introducing influence processes into a system of collective decisions,’’American Journal of Sociology86,220–236.

Marsden, P. V. (1983). ‘‘Restricted access in networks and models of power,’’ American Journal ofSociology88,686–717.

McNeil, K., and Thompson, J. D. (1971). ‘‘The regeneration of social organization,’’ AmericanSociological Review36,624–637.

Menzel, H., and Katz, E. (1955). ‘‘Social relations and innovation in the medical profession: Theepidemiology of a new drug,’’ Public Opinion Quarterly19,337–352.

Mizruchi, M. S. (1992). The Structure of Corporate Political Action, Harvard Univ. Press, Cambridge.Mizruchi, M. S., and Koenig, T. (1988). ‘‘Economic concentration and corporate political behavior: A

cross-industry comparison,’’ Social Science Research17,287–305.Mizruchi, M. S., and Schwartz, M. Eds. (1987). Intercorporate Relations: The Structural Analysis of

Business, Cambridge Univ. Press, New York.Mizruchi, M. S., and Stearns, L. B. (1988). ‘‘A longitudinal study of the formation of interlocking

directorates,’’Administrative Science Quarterly33,194–210.Pfeffer, J., and Salancik, G. R. (1978). The External Control of Organizations: A Resource Depen-

dence Perspective, Harper and Row, New York.Porter, Michael (1980). Competitive Strategy, Free Press, New York.Powell, W. W. (1990). ‘‘Neither markets nor hierarchy: Network forms of organization,’’in Research

in Organizational Behavior (B. Stan, Ed.), Vol.12,pp. 295–336, JAI Press, Greenwich, CT.Raftery, A. E. (1995). ‘‘Bayesian model selection in social research,’’in Sociological Methodology,

American Sociological Association, Washington, DC.Rogers, E. (1962). The Diffusion of Innovations, Free Press, New York.Rogers, E. and Kincaid, L. (1981). Communication Networks, Free Press, New York.Sorenson, Aage (1996). ‘‘The structural basis of social inequality,’’ American Journal of Sociology

101(5), 1333–65.Shapiro, R. (1989). ‘‘Theories of oligopoly behavior,’’in Handbook of Industrial Organization (R.

Schmalensee and R. Willig, Eds.), Vol. 1, pp. 229–414, North Holland, Elsevier Science,Amsterdam.

State of Israel, Central Bureau of Statistics (1977). Special Reports on Input Output Tables, SpecialSeries 710, Jerusalem.

State of Israel, Central Bureau of Statistics (1972–1992) Statistical Abstracts of Israel, Bureau ofStatistics, Jerusalem, Vols. 23–40.

State of Israel, Central Bureau of Statistics (1981). Industry and Craft Survey, Bureau of Statistics,Jerusalem.

Stearns, L. B., and Mizruchi, M. S. (1986) ‘‘Broken-tie reconstitution and the functions of interorgani-zational interlocks: A reexamination,’’Administrative Science Quarterly31,522–538.

Stokman, F., Ziegler, R., and Scott, J. (Eds.) (1985). Networks of Corporate Power: A ComparativeAnalysis of Ten Countries, Polity Press, London.

Swedberg, R. (1994). ‘‘Markets as social structure,’’in Handbook of Economic Sociology (N. Smelserand R. Swedberg, Eds.), pp. 255–282, Russell Sage and Princeton Univ. Press, New York.

Talmud, I. (1992). ‘‘Industry market power, industry political power, and state support: The case ofisraeli industry,’’in Research in Politics and Society, (G. Moore and J. A. Whitt, Eds.), Vol. 4, pp.35–62, JAI Press, CT.

Talmud, I. (1994). ‘‘Relations and profits: Imperfect competition and its outcome,’’ Social ScienceResearch23,109–135.

Tilly, Charles (1985). From Mobilization to Revolution, Addison–Wesley, MA.Uzzi, B. (1996). ‘‘Social structure and competition in interfirm networks: The paradox of embedded-

ness,’’Administrative Science Quarterly42,35–62.

440 TALMUD AND MESCH

SSR601@xyserv3/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 rich

Uzzi, B. (1997). ‘‘The sources and consequences of embeddedness for the economic performance oforganizations: The network effect,’’American Sociological Review61(4), 647–698.

Van Rossem, R. (1996). ‘‘The world system paradigm as general theory of development: Across-national test,’’American Sociological Review61,508–527.

Weber, M. (1978).in Economy and Society (G. Roth and C. Wittich, Eds.), 2Vol., Univ. of CaliforniaPress, Berkeley.

Weimann, G. (1982). ‘‘On the importance of marginality: One more step into the two-step flow ofcommunication,’’American Sociological Review47,764–773.

Weimann, G. (1983). ‘‘The strength of weak conversational ties in the flow of information andinfluence,’’ Social Networks5, 245–267.

Williamson, O. (1994). ‘‘Transaction cost economics and organization theory,’’in Handbook ofEconomic Sociology (N. Smelser and R. Swedberg, Eds.), pp. 77–107, Russell Sage andPrinceton Univ. Press, New York.

441MARKET EMBEDDEDNESS AND CORPORATE INSTABILITY

SSR601@xyserv3/disk4/CLS_jrnlkz/GRP_ssrj/JOB_ssrj97ps/DIV_232z01 rich