march 2014 techtarget it priorities survey technology...

TRANSCRIPT

$$$

¤

£%%

TECHTARGET IT PRIORITIES SURVEY

TECHNOLOGY PRIORITIES FOR 2014In TechTarget’s annual IT Priorities Survey, 5,241 worldwide respondents, including 1,368 in the U.S. and Canada, weighed in on their most pressing technology concerns and top areas for investment.

March 2014

REGULATORY COMPLIANCE

Data Complexity and the Demand for GRC

D

IT SECURITY

Network Security: The Next Big Thing

D

A LOOK AHEAD

Beyond Virtualization: Cloud and Automation

D

STORAGE STRATEGY

Reshaping Storage Infrastructure

D

SURVEY OVERVIEW

The IT Master Plan for 2014

D

2 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

SURVEY OVERVIEW

THE IT MASTER PLAN FOR 2014What’s on tap for 2014? Heavy doses of business intelligence, mobility and Windows 8. BY MARK SCHLACK

THE SLOW CRAWL out of recession will be more like a power walk in 2014 for U.S. IT managers, putting them ahead of their European counterparts’ still-hesitant climb out of recession and behind the sprinting Asian, African and Latin American markets, according to TechTarget’s annual survey of IT priorities.

As for what IT departments are going to invest in, 2014 is a tale of overlapping waves of change. For almost 10 years, the wave of consolidation that ultimately brought with it virtualization and cloud services has dominated IT depart-ments. Now, that wave is interacting with growth-driven trends in business intelligence and mobility. In turn, both waves need improvements in security and network infra-structure to succeed.

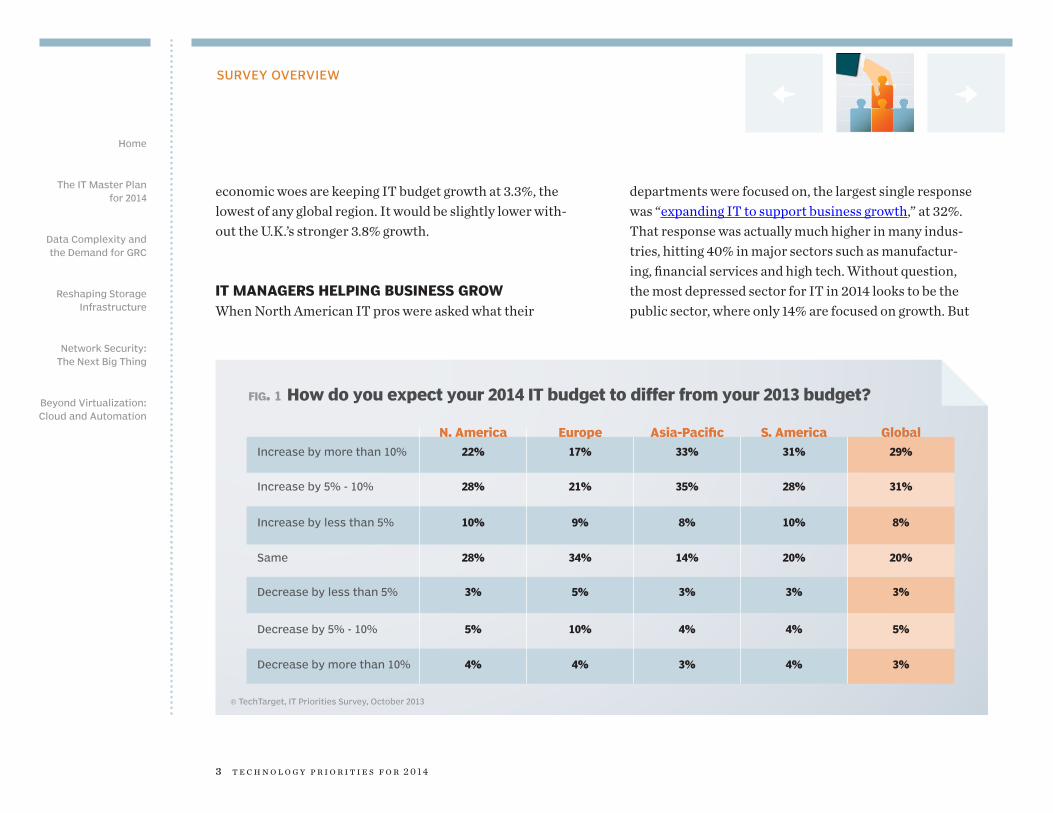

Amid all of that, IT shops are going through the normal Windows upgrade cycle with both desktop and server ver-sions. What will surprise some is the relatively high first-year level of Windows 8 adoption (see FIGURE 1, page 3).

IT MORE UPBEAT THAN LAST YEARThe last two years saw a pretty firm pattern, with 58% of respondents reporting budget increases, but this year that rose to 60%. At the same time, the number of people cutting budgets dropped from 19% last year to 12% this year.

Overall, respondents report budget growth of 5.1%, com-pared with 2.8% in 2013. As has been the pattern, Asia and other parts of the world with a significant number of de-veloping nations showed the greatest increases. But North America also showed robust growth this year of 4.6%, up from only 1.4% last year.

For the first time, TechTarget did extensive surveying in Latin America, and growth there is among the most vibrant in the world: 6.5% on average, with 65% of respondents re-porting an increasing budget and 30% reporting an increase of more than 10%. Growth is especially strong in the tech sectors, media, agribusiness and financial services.

The global laggard is Europe, where well-publicized

3 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

SURVEY OVERVIEW

economic woes are keeping IT budget growth at 3.3%, the lowest of any global region. It would be slightly lower with-out the U.K.’s stronger 3.8% growth.

IT MANAGERS HELPING BUSINESS GROWWhen North American IT pros were asked what their

departments were focused on, the largest single response was “expanding IT to support business growth,” at 32%. That response was actually much higher in many indus-tries, hitting 40% in major sectors such as manufactur-ing, financial services and high tech. Without question, the most depressed sector for IT in 2014 looks to be the public sector, where only 14% are focused on growth. But

fig. 1 How do you expect your 2014 IT budget to differ from your 2013 budget?

N. America Europe Asia-Pacific S. America Global

Increase by more than 10% 22% 17% 33% 31% 29%

Increase by 5% - 10% 28% 21% 35% 28% 31%

Increase by less than 5% 10% 9% 8% 10% 8%

Same 28% 34% 14% 20% 20%

Decrease by less than 5% 3% 5% 3% 3% 3%

Decrease by 5% - 10% 5% 10% 4% 4% 5%

Decrease by more than 10% 4% 4% 3% 4% 3%

© TechTarget, IT Priorities Survey, October 2013

4 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

SURVEY OVERVIEW

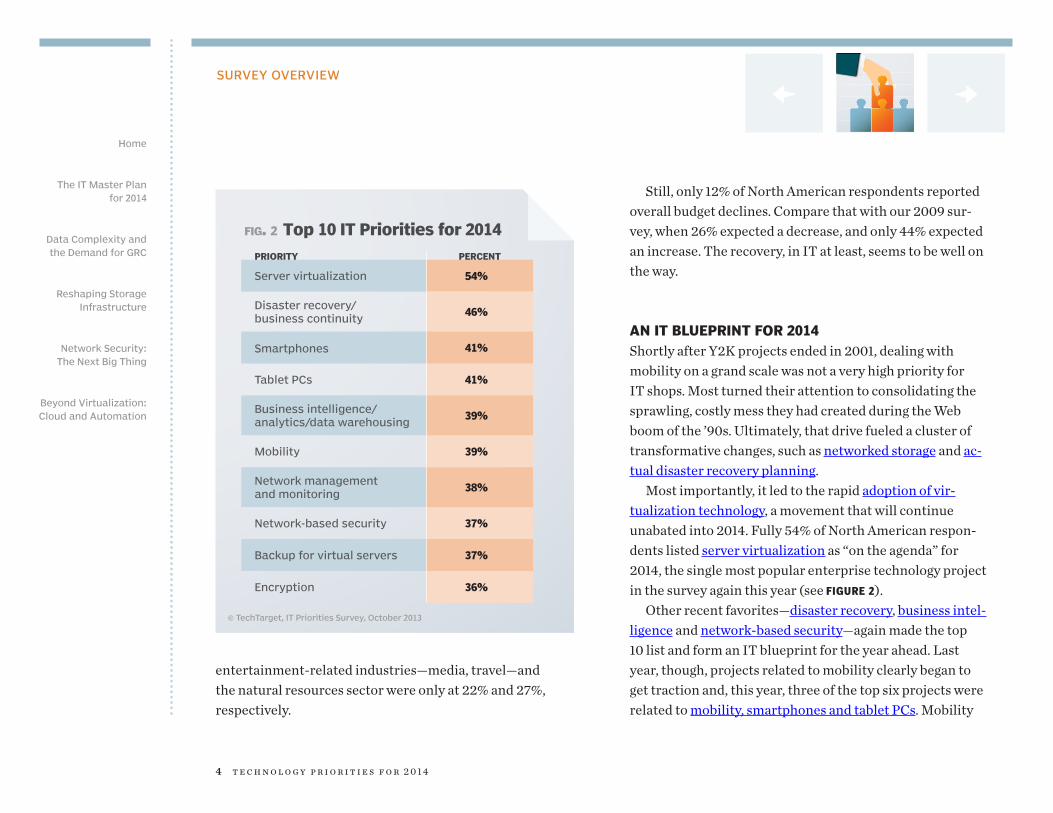

entertainment-related industries—media, travel—and the natural resources sector were only at 22% and 27%, respectively.

Still, only 12% of North American respondents reported overall budget declines. Compare that with our 2009 sur-vey, when 26% expected a decrease, and only 44% expected an increase. The recovery, in IT at least, seems to be well on the way.

AN IT BLUEPRINT FOR 2014Shortly after Y2K projects ended in 2001, dealing with mobility on a grand scale was not a very high priority for IT shops. Most turned their attention to consolidating the sprawling, costly mess they had created during the Web boom of the ’90s. Ultimately, that drive fueled a cluster of transformative changes, such as networked storage and ac-tual disaster recovery planning.

Most importantly, it led to the rapid adoption of vir-tualization technology, a movement that will continue unabated into 2014. Fully 54% of North American respon-dents listed server virtualization as “on the agenda” for 2014, the single most popular enterprise technology project in the survey again this year (see FIGURE 2).

Other recent favorites—disaster recovery, business intel-ligence and network-based security—again made the top 10 list and form an IT blueprint for the year ahead. Last year, though, projects related to mobility clearly began to get traction and, this year, three of the top six projects were related to mobility, smartphones and tablet PCs. Mobility

fig. 2 Top 10 IT Priorities for 2014

priority percent

Server virtualization 54%

Disaster recovery/ business continuity

46%

Smartphones 41%

Tablet PCs 41%

Business intelligence/ analytics/data warehousing

39%

Mobility 39%

Network management and monitoring

38%

Network-based security 37%

Backup for virtual servers 37%

Encryption 36%

© TechTarget, IT Priorities Survey, October 2013

5 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

is here to stay as a top IT priority at many companies, with 39% citing some kind of broad mobility initiative for 2014.

Along with those projects, IT is building the manage-ment structure to make smartphones and tablets safe for enterprise computing. This year, 34% cited mobile device management or mobile endpoint security projects, in line with last year’s results. Mobile security, in general, is a focus for 32% of respondents. That puts it on a par with data cen-ter consolidation—in other words, a major focus.

Putting those mobile devices to use is also a point of em-phasis, with mobile applications a project focus in 2014 for 35% of respondents.

MOBILITY + VIRTUALIZATION = CLOUDServer virtualization has led to a series of other changes as IT shops try to adapt other parts of the infrastructure to the virtual-machine world. Thirty-one percent of our respondents will be doing a storage virtualization project next year. It’s the third year in a row that at least that many respondents listed a storage virtualization project.

Networking changes are beginning to show up as well, with 24% listing some form of network virtualization as a 2014 priority.

But the bigger change is the adoption of larger chunks of cloud-based services. In North America, 29% of respon-dents will be using external cloud infrastructure in 2014. By far, that translates to Infrastructure as a Service (IaaS) and/or Software as a Service (SaaS). Of those using exter-nal cloud, 51% are using cloud infrastructure services, 49% SaaS and about 25% both.

And they are using cloud infrastructure in surprising quantities. On the server front, respondents using IaaS services estimate that they will put 28% of their server and storage capacity in the cloud.

Back in the data center proper, the normal upgrade cy-cles continue. Windows Server 2012 upgrades will be on the agenda at 34% of shops. When it comes to the desktop, the big turn away from Windows XP is going in two directions. Windows 7 upgrades are going on at 34% of shops, but Win-dows 8 also got the nod at 19%. There is little duplication between these two groups: 24% of Windows 7 migrators are also doing Windows 8, but only 12% of Windows 8 users are also doing Windows 7. In all, 49% of shops are going to one or another of Microsoft’s post-XP operating systems. n

MARK SCHLACK is senior vice president of editorial at TechTarget. Write to him at [email protected].

SURVEY OVERVIEW

6 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

REGULATORY COMPLIANCE

DATA COMPLEXITY AND THE DEMAND FOR GRCOrganizations have turned to GRC programs to avoid regulatory issues and keep data secure. But can these programs also benefit the bottom line? BY BEN COLE

REMAINING REGULATORY-COMPLIANT and keeping data secure has become increasingly difficult in the digital age, and companies have started taking a targeted approach: Eighty-two percent of respondents to TechTarget’s annual IT Pri-orities Survey reported that in 2014 their organization will already have, or is planning to implement, a formal gover-nance, risk and compliance (GRC) program.

Increased regulations, expanded IT security threats and a rapidly growing data footprint force a proactive approach to maintaining GRC, said Derek Gascon, executive direc-tor of the Compliance, Governance and Oversight Council (CGOC).

“There is so much new data they have to deal with,” Gas-con said. “Organizations are realizing the amount of infor-mation they are generating has to be managed in a way that they can more easily produce it when necessary, and also be able to protect it throughout the lifecycle.”

But with compliance already broadly deployed, new

programs may be on the decline: Twenty-four percent of respondents said their organizations would implement a compliance program in 2014, down from 36% of the respon-dents in last year’s survey.

Many companies balance numerous GRC projects, but this often creates disconnects among interdepartmental efforts, said Michael Rasmussen, chief GRC pundit at GRC 20/20 Research LLC in Waterford, Wis. Large organiza-tions might have multiple GRC platforms for certain de-partments, but still struggle with spreadsheets, documents and emails because other parts of the company still have paper-intensive processes.

While it makes sense that more than 80% of respondents say they have a GRC program in place, Rasmussen guesses that a majority of these are department-based.

“If the question were, ‘Do you have an enterprise GRC program that integrates the views of enterprise risk, audit, corporate compliance, legal, IT security, health and safety?’

7 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

REGULATORY COMPLIANCE

then you [would] find the percentage to be significantly less,” Rasmussen said.

The inter-operational approach to GRC programs is hugely beneficial in that many risks—especially those that are regulatory-related—affect multiple departments. A companywide approach to GRC can save multiple resources if the organization’s risk management efforts are not com-pletely independent from one another.

“A failure in finance can impact IT, and a failure in IT can impact finance,” said Renee Murphy, a senior analyst at Cambridge, Mass.-based Forrester Research Inc. “You can’t make corporate-level decisions, board-level decisions with-out understanding that relationship.”

This enterprise-wide approach to GRC programs re-quires a similar strategy for information management, Gas-con said, and forces organizations to take a more holistic view of the data they generate and how they govern it.

It’s not just the data that falls under governance and compliance mandates, either: Everyday business data should be managed throughout its lifecycle as well, Gascon said. While not specifically targeting GRC, encouraging this type of data management culture ultimately benefits com-pliance programs, he added.

“It creates a culture within the organization that every-body needs to take care of the information they are working with and follow the guidelines that are out there,” Gascon said.

THE BUSINESS BENEFITS OF GRCImplementing a companywide GRC program is definitely not easy, and is potentially costly to a business’ bottom line and reputation. Take, for example, the Target breach during the 2013 holiday season as proof of how customer loyalty—and profits—can drop dramatically due to a risk-related oversight, Murphy said. “If you are really forward-thinking and understand that GRC is a net positive for your organization, l think you are ahead of the game,” she said.

One big obstacle to GRC program implementation is due to the negative connotations still associated with compliance mandates. Employees often immediately think of audits or litigation when they hear GRC, Gascon said.

But as data and how it’s managed become more of a pri-ority, companies can realize the business benefits of for-mal compliance and GRC programs beyond their original purpose.

“People should see the real value that comes from put-ting that kind of rigor in place and following those pro-cesses,” Gascon said. “Going forward, we’re starting to see organizations realize governance programs as actually a start to taking advantage of the data that they have.” n

BEN COLE is site editor for SearchCompliance.com. Contact him at [email protected].

8 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

STORAGE STRATEGY

RESHAPING STORAGE INFRASTRUCTURETechTarget’s IT Priorities survey shows wide interest in cloud services despite recent missteps by some prominent providers. BY RICH CASTAGNA

IT SHOPS WILL devote a significant portion of their resources to storage and storage-related infrastructure projects in 2014, according to TechTarget’s IT Priorities Survey. While storage alone isn’t necessarily at the top of IT directors’ to-do lists, key initiatives involving cloud services, disaster recovery and data protection are poised to reshape or re-build the data storage infrastructure in many companies.

ECONOMIC OUTLOOK MOSTLY POSITIVE FOR ITLast year, 45% of the IT pros who responded to our survey expected their overall IT budgets to increase, versus 15% who were preparing for diminishing budgets. The 2014 pic-ture is even rosier, as 54% expect to have bigger IT budgets, 24% don’t foresee any changes and only 11% will have to make do with less.

The lingering effects of the Great Recession are still hampering some companies, although we’re seeing some

improvement. Eleven percent of respondents said they’re still mired in recessionary economics (versus 17% last year), while 42% noted that they’re recovering, but slowly (same as last year).

PLANS CALL FOR CLOUD STORAGE AND DISASTER RECOVERYDespite all the talk of software-defined storage and soft-ware-defined just about everything else, more than half of our respondents (51%) indicated that their companies’ IT budgets would include increased spending for hardware.

Even more are looking to cloud technologies, with 55% projecting increased cloud spending in 2014. Storage will play a significant part for those companies, as 34% plan to tap into external cloud services to add storage capacity. Interest in Storage as a Service cuts across companies of all sizes, with a slight tilt toward midsize and small firms.

9 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

STORAGE STRATEGY

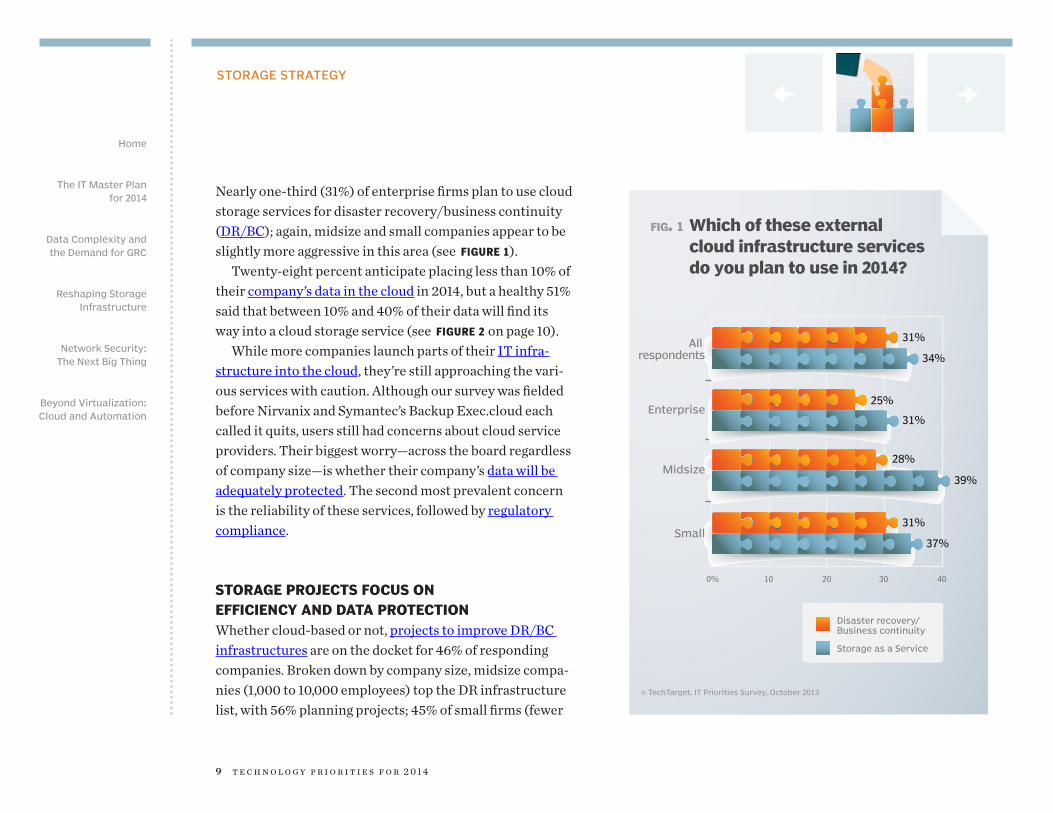

Nearly one-third (31%) of enterprise firms plan to use cloud storage services for disaster recovery/business continuity (DR/BC); again, midsize and small companies appear to be slightly more aggressive in this area (see FIGURE 1).

Twenty-eight percent anticipate placing less than 10% of their company’s data in the cloud in 2014, but a healthy 51% said that between 10% and 40% of their data will find its way into a cloud storage service (see FIGURE 2 on page 10).

While more companies launch parts of their IT infra-structure into the cloud, they’re still approaching the vari-ous services with caution. Although our survey was fielded before Nirvanix and Symantec’s Backup Exec.cloud each called it quits, users still had concerns about cloud service providers. Their biggest worry—across the board regardless of company size—is whether their company’s data will be adequately protected. The second most prevalent concern is the reliability of these services, followed by regulatory compliance.

STORAGE PROJECTS FOCUS ON EFFICIENCY AND DATA PROTECTIONWhether cloud-based or not, projects to improve DR/BC infrastructures are on the docket for 46% of responding companies. Broken down by company size, midsize compa-nies (1,000 to 10,000 employees) top the DR infrastructure list, with 56% planning projects; 45% of small firms (fewer

0% 10 20 30 40

© TechTarget, IT Priorities Survey, October 2013

Disaster recovery/Business continuity

Storage as a Service

All respondents

31%

31%

34%

25%Enterprise

Midsize

Small31%

37%

39%

28%

fig. 1 Which of these external cloud infrastructure services do you plan to use in 2014?

10 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

STORAGE STRATEGY

than 1,000 employees) and 42% of enterprises (more than 10,000 employees) will be involved with DR in 2014. The more modest numbers at the lower and higher ends of the spectrum suggest that small companies may not have the

means to pursue DR projects, while big companies likely have at least some DR infrastructure in place.

Looking exclusively at primary storage initiatives, stor-age virtualization projects (31%) top the list, as they did

0%

10

20

30

40

Lessthan 1%*

1% to4.9%

5% to9.9%

10% to19.9%

20% to39.9%

40% to59.9%*

60% to79.9%

80% to99.9%*

100%*

*Missing data indicates 0% in that category.

© TechTarget, IT Priorities Survey, October 2013

Small

Midsize

Enterprise

fig. 2 What percent of your storage capacity will be in the cloud in 2014?

1 1 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

STORAGE STRATEGY

last year. Storage virtualization has seemingly been on the verge of wider implementation for several years, so maybe as server virtualization matures, more attention is shifting to the storage side of the shop.

Cloud storage—external or internal—is also high on IT managers’ 2014 to-do lists; 30% said it would be a deploy-ment priority in 2014, which is a big jump from last year’s 18%. And while some of those projects are likely inspired

0%

10

20

30

40

50

DR/BC Backup forvirtual servers

© TechTarget, IT Priorities Survey, October 2013

Small

Midsize

Enterprise

Deduplicationfor backup

Cloudbackup

Laptop/Mobilebackup

New tapetechnologies

fig. 3 Which of these backup storage initiatives will your company deploy in 2014?

12 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

STORAGE STRATEGY

by spiraling capacity requirements, storage managers are also looking to make better use of their on-premises stor-age resources, with 24% looking to implement compres-sion, data deduplication or some other data reduction technology.

The next four items on the storage project priority list are all closely bunched: storage for big data (19%), solid-state storage (18%), storage for virtual desktops (18%) and scale-out NAS (17%). Company size has a lot to do with how much attention will be focused on each of these technical areas. For instance, enterprise-scale companies are more likely to pursue big data projects (28%), more midsize orga-nizations are preparing to deploy storage for virtual desk-tops (28%), and solid-state storage is now affordable and

ubiquitous enough for companies of all sizes.Backup projects for 2014 are led, as noted earlier, by DR/

BC efforts. Not far behind on the priority list is backup for virtual servers (37%). There are far more solid alternatives for backing up virtual machines (VMs) than there were just a few years ago, but VM backup remains a priority at many companies because the virtual server environment—and all the data it’s creating—is growing at a rate that outpaces backup efforts in some organizations (see FIGURE 3 on page 11).

Deploying dedupe for backup operations is on the agenda for 30% of respondents, another indication that although the technology has been available for 10 years, many com-panies have yet to fit it into their backup environments.

Tape continues to fade from the backup scene, with only 7% considering new tape technologies for 2014. But on a more encouraging note, 20% of our respondents said they have plans to implement backup of mobile devices. n

RICH CASTAGNA is vice president of editorial in the Storage Media Group at TechTarget. Write to him at [email protected].

VM backup remains a priority at many companies because the virtual server environment is growing at a rate that outpaces backup efforts.

1 3 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

IT SECURITY

NETWORK SECURITY: THE NEXT BIG THINGThe top security initiatives for 2014 include network security, data loss prevention and encryption. BY ROBERT RICHARDSON

TECHTARGET’S MOST RECENT IT Priorities Survey shows that 2014 priorities include a healthy dollop of security concerns, but the top security initiatives were perhaps not quite what you’d expect.

New deployments in network security lead the to-do list: Forty-five percent of respondents said they’d add new capacity in this area, with data loss prevention (DLP) follow-ing at 39%. Behind network security and DLP, top project priorities were threat detection and management, as well as identity and access management, both at 35%, followed by encryption at 34%.

Tyler Shields, a senior analyst of security and risk man-agement at Forrester Research Inc., said that network security also led research performed at that company. “It doesn’t surprise me in the least, because that’s what people understand. I’m surprised that DLP is as high as it is, be-cause it’s extremely difficult.”

Shields said he liked seeing encryption as a top priority

because, “If you think about what you’re really trying to se-cure as a company, at the end of the day, the most effective way to secure your data is to make sure that only you can read it. The hard part is managing how encryption works,

but there are some pretty cool technologies out now that keep things searchable and usable, so that’s probably what’s pushing encryption up right now.”

And, he said, “It’s also people saying, ‘Oh my god, the NSA has been looking at my stuff.’ Of course, they’ve been looking at your stuff for 20 years, but all of a sudden you’re realizing it. There’s a bit of a bubble there, but there are also

“ [The NSA has] been looking at your stuff for 20 years, but all of a sudden you’re realizing it.”

—TYLER SHIELDS, senior analyst, Forrester Research Inc.

14 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

IT SECURITY

some new technologies there that are pushing that forward as well.”

Cryptography expert Bruce Schneier, however, doesn’t see encryption being much driven by NSA-related con-cerns. “My guess is that the ‘[Edward] Snowden effect’ is minimal and more pronounced in individuals and non-U.S. corporations,” he said in an email conversation.

At the somewhat more abstract level of embracing over-arching security programs, 83% said they either already have or will implement a formal governance, risk and com-pliance program.

In terms of the larger trends that are reshaping IT,

one-quarter of respondents said that they’ll have 40% or more of their overall storage capacity in the cloud next year (no doubt pushing encryption up the list) and three-quarters (74%) said they’ll be giving their employees more mobile devices next year.

The respondents were spread fairly evenly around the world. Fully one-fifth of respondents said that they spend most of their time working on security and security-related matters. n

ROBERT RICHARDSON is editorial director of the Security Media Group at TechTarget. Write to him at [email protected].

1 5 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

A LOOK AHEAD

BEYOND VIRTUALIZATION: CLOUD AND AUTOMATIONOur survey shines light on the future of the IT department, as well as IT’s fears moving forward. But how does IT enhance its business? BY STEPHEN J. BIGELOW

KNOWING WHICH TECHNOLOGIES are on the way out and where you should ramp up IT efforts in 2014 could mean the difference between profit and loss. But navigating the ever-changing IT space is a daunting challenge—with your business hanging in the balance.

IT GOALS FOR 2014Any adjustment to IT—and its role in everyday business operations—must start by reviewing and establishing a new set of goals. Thirty-seven percent of respondents plan to ex-pand IT to support business growth. Organizations depend on computing as a critical business resource; as the scope of employees, partners and users grows to global propor-tions, IT must have appropriate computing levels in place to handle the load.

Even when growth is not the top priority, there are al-ways opportunities to enhance the business with key IT

projects, and 23% of IT professionals reported selective spending in some technological areas. This may include ini-tiatives like data protection, strategic upgrades to network infrastructure, deploying a virtualization or consolidation project, or some other targeted technology that offers a measurable business benefit.

Organizations now realize that even the most talented and well-paid IT employees can’t help the business when they are preoccupied with mundane data center tasks like server provisioning, monitoring and other day-to-day “fire-fighting.” This has brought new attention to the importance of data center automation, and 20% of survey respondents plan to increase the use of automation in the business, which frees IT to focus its attention on more strategic projects.

“Firefighting is going to happen,” said Chris Steffen, director of IT at Boulder, Colo.-based Magpul Industries Corp. “Having a centralized suite of management tools makes firefighting much easier.”

16 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

A LOOK AHEAD

IT BUDGETS INCREASE IN 2014The last recession cycle has been difficult for businesses and IT departments. Lower budgets have curtailed every-thing from IT staffing to equipment purchases to software updates. As the economy eases out of recession, IT spend-ing is creeping up. Where 59% of respondents reported a budget increase in 2013, 65% expect a budget increase in 2014. More than 1,500 respondents reported where the budget increases will be spent.

The biggest emphasis of 2014 budget increases will be on tangible goods, with 59% of IT professionals planning to purchase new software. This usually involves software up-grades for existing products along with new software tools (such as cloud management or IT automation tools to sup-port the business).

“Companies see the push for automation as an opportu-nity to consolidate, reduce costs and increase automation,” said Pete Sclafani, CIO at 6connect Inc., a software-defined network software provider based in San Francisco. “But these new tools must integrate with each other using multi-tenant/Web service APIs [application programming inter-faces]—and hopefully [will] not require legacy approaches based on proprietary hardware.”

At the same time, 52% of respondents plan to purchase new hardware to expand computing capacity and increase energy efficiency.

Increased IT budgets will also have an impact on data

center operations, and 35% of IT professionals expect to spend more on maintenance, which can range from soft-ware licensing to routine hardware services to infrastruc-ture projects like electrical subsystem and mechanical air conditioning work. Organizations may need to catch up on some maintenance issues ignored during leaner budget years. Another 31% of organizations may add IT staff in 2014 to meet the overall goals of business growth and tar-geted IT projects.

Next year’s budgets also reflect a shift in IT from a busi-ness expense to a business utility—especially in the use of computing services—and 38% of respondents expect to grow spending in public and private cloud services.

Cloud technologies are important elements in IT auto-mation (e.g., self-provisioning and chargeback) and greater IT staff efficiency. When data centers simply cannot grow any more or offsite computing resources are needed to sup-port the business, outsourcing can provide effective alter-natives to in-house IT; 18% of respondents plan to increase the use of outsourcing providers in 2014. Sclafani also noted

“ Companies see the push for automation as an opportunity to consolidate, reduce costs and increase automation.”

—PETE SCLAFANI, CIO, 6connect Inc.

1 7 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

A LOOK AHEAD

that automation in other aspects of the infrastructure—such as network switching and routing—are on the horizon for data centers.

WHEN IT BUDGETS ARE CUTUnfortunately, not every IT budget will increase in 2014: Thirteen percent of survey respondents are faced with the prospect of maintaining current service levels with flat bud-gets, while another 7% must reduce IT spending.

Some businesses are still mired in the aftermath of the last recession, while others may have already completed major IT initiatives and may not require previous funding for the coming fiscal year. Regardless of the reason, lower budgets will put enormous pressure on IT, and 335 sur-vey respondents reported how budget cuts will affect IT spending.

Hardware is first on the chopping block, as 61% of re-spondents faced with lower budgets will curtail hardware spending. Capital expenses like this are easiest to cut, and technologies like virtualization make it possible to increase utilization and extend the working life of existing systems.

By comparison, only 44% of respondents noted that budget cuts will affect software purchases. Software ap-plications and tools are the foundation of any business, and it’s much harder to continue running the business without current software.

Meanwhile, IT budget cuts demand the most innovative thinking and lead to groundbreaking projects. For example, the astounding growth of server virtualization and con-solidation was largely driven by budget reductions caused by the latest recession (which some organizations are still grappling with today).

Lean budgets will also shave maintenance and staffing efforts. Consider that 39% of respondents with smaller budgets will seek to reduce IT staffing. This may be a matter of foregoing new hires or leaving job requisitions unfilled, but may also include staff reductions. Businesses will de-pend on higher levels of IT automation tools to help address reduced IT staffing. Otherwise, organizations risk compro-mising service levels for both internal and external users.

“This highlights the need to identify automation solu-tions with flexible deployment models for pricing flexibility and operational robustness,” Sclafani said.

Survey results also showed that 37% of IT planners facing smaller IT budgets will cut back on maintenance, forestall-ing software upgrades and potentially relying on previous consolidation projects to reduce hardware dependencies, and will turn to alternative computing resources like cloud; both initiatives reduce the data center server count and supporting systems. However, Magpul Industries’ Steffen pointed out that those maintenance cutbacks can be more challenging in today’s climate of subscription-based soft-ware products, as many require an annual fee to continue

1 8 t e c h n o l o g y p r i o r i t i e s f o r 2 0 1 4

Home

The IT Master Plan for 2014

Data Complexity and the Demand for GRC

Reshaping Storage Infrastructure

Network Security: The Next Big Thing

Beyond Virtualization: Cloud and Automation

A LOOK AHEAD

using them.Survey data reported 34% of budget-strapped organi-

zations will reduce outsourcing efforts, likely because of broader business conditions that require reductions in monthly operating expenses. In many cases, some out-sourced workloads can be brought back in-house and run on excess computing capacity in the local data center. How-ever, only 7% of respondents would consider reducing their cloud investment, though cloud is still a fairly new technol-ogy with limited adoption anyway.

“Do IT managers and C-table execs see the value of their cloud spend, or do they not have the tools to calculate the TCO [total cost of ownership] of their cloud spend?” Steffen asked.

Regardless of your purchasing intentions for 2014, suc-cessful IT goes far beyond line items and purchase req-uisitions. IT professionals can now draw on an extensive array of innovative computing technologies, management tools and utility computing alternatives to meet the orga-nization’s needs. Unlike decades past, making the right IT choices for 2014 takes a keen knowledge of business goals and regulatory needs, a thorough understanding of the available options, and development of a long-term strategic plan that allows IT to meet those goals. n

STEPHEN J. BIGELOW is a senior technology editor at TechTarget. Write to him at [email protected].

Technology Priorities for 2014 is a SearchCIO.com e-publication.

Mark Schlack, Senior Vice President of Editorial

Rachel Lebeaux, Managing Editor

Christina Torode, Editorial Director

Stephen J. Bigelow, Rich Castagna, Ben Cole,

Robert Richardson, Contributing Editors

Lindsay Chase, Production Editor

Linda Koury, Director of Online Design

Neva Maniscalco, Graphic Designer

FOR SALES INQUIRIES, PLEASE CONTACT

Amalie Keerl, Director of Product Management [email protected]

TechTarget 275 Grove Street, Newton, MA 02466

www.techtarget.com

© 2014 TechTarget Inc. No part of this publication may be transmitted or repro-duced in any form or by any means without written permission from the pub-lisher. TechTarget reprints are available through The YGS Group.

About TechTarget: TechTarget publishes media for information technology professionals. More than 100 focused websites enable quick access to a deep store of news, advice and analysis about the technologies, products and pro-cesses crucial to your job. Our live and virtual events give you direct access to independent expert commentary and advice. At IT Knowledge Exchange, our social community, you can get advice and share solutions with peers and experts.

COVER ART: NEVA MANISCALCO