managingtheriskofthe“betting-against-beta” anomaly ... · (“betting-against-beta” (bab))...

TRANSCRIPT

Managing the risk of the “betting-against-beta”

anomaly: does it pay to bet against beta?1

Pedro Barroso2 Paulo Maio3

First version: November 2016

1We are grateful to Kenneth French and Lasse Pedersen for providing stock marketreturn data.

2University of New South Wales. E-mail: [email protected] School of Economics, Department of Finance and Statistics. E-mail: paulof-

Abstract

We study the risk dynamics of the betting-against-beta anomaly. The strategy

shows strong and predictable time variation in risk and no risk-return trade-off. A

risk-managed strategy exploiting this achieves an annualized Sharpe ratio of 1.28

with a very high information ratio of 0.94 with respect to the original strategy.

Similar strategies for the market, size, value, profitability, and investment factors

achieve a much smaller information ratio of 0.15 on average. The large economic

benefits of risk-scaling are similar to those of momentum and set these two anoma-

lies apart from other equity factors. Decomposing risk into a market and a specific

component we find the specific component drives our results.

JEL classification: G11; G12; G17.

Keywords: Betting-against-beta, BAB, time-varying risk, realized volatility, mo-

mentum, risk factors, scaled factors, market anomalies.

1. Introduction

The capital asset pricing model (CAPM) of Sharpe (1964), Lintner (1965),

and Treynor (1965) provides the first theoretically motivated measure of the risk-

iness of each asset and the expected return it should command in equilibrium.

It is arguably the most taught asset pricing model and is widely used in corpo-

rate finance, portfolio performance measurement and investment valuation (see e.g.

Fama and French (2004) and Damodaran (2012)). However, we know from early

empirical tests of the model that low (high) beta stocks have consistently positive

(negative) risk-adjusted returns, a result known as the beta anomaly (Black et al.

(1972)). Recently, Frazzini and Pedersen (2014) propose an investment strategy

(“betting-against-beta” (BAB)) that exploits this anomaly by buying low-beta

stocks and shorting high-beta stocks. They report a Sharpe ratio for the strategy

of 0.78, about double that of the US equity market.

Besides US equities, Frazzini and Pedersen (2014) show that BAB achieves

abnormal returns in international equities, bonds, and currencies. Asness et al.

(2014b) and Baker et al. (2014) find similar results examining industry portfolios

and macro level country selection. Furthermore, in contrast to other anomalies

in equities, the profits of exploiting the beta anomaly seem robust to transaction

costs (Asness et al. (2014b)).

So the beta anomaly allows an impressive investment performance, at least

from an unconditional perspective. But Cederburg and O’Doherty (2016) find

that if one fully accounts for the time-varying systematic risk of the strategy its

alpha already becomes insignificant. We propose an alternative approach to the

conditional performance of the strategy and examine its time-varying volatility

1

instead.

There is an extensive literature documenting the time varying risk of the stock

market (e.g. Schwert (1989), Bollerslev (1987)) and the potential benefits of timing

its volatility (Fleming et al. (2001)). Barroso and Santa-Clara (2015) extend this

discussion to the space of long-short equity factor investing by showing the benefits

of managing the risk of momentum. More recently Moreira and Muir (2016) find

similar benefits of volatility timing for other equity factors.

We find that volatility has an important economic value to condition expo-

sure to the BAB strategy. In our sample, the Sharpe ratio of the BAB strategy

increases from 0.91 to 1.28 with risk-management. The information ratio of the

risk-managed strategy is 0.94 when compared to its original version, a result simi-

lar to that of momentum (0.93). The Fama-French 5-factor alpha of the strategy

increases from an annualized 5.48% to 15.97%. Similar to momentum, the benefits

come from strong predictability in risk and the absence of a risk-return trade-off.

In fact, we find months with extreme high risk for the strategy are followed by

lower returns on average.

Our results contrast with those of Cederburg and O’Doherty (2016). They

find that conditional on time-varying beta BAB is less of a puzzle. We find the

strategy also has strongly time-varying volatility and that using this to manage

its risk makes BAB a much deeper puzzle.

We decompose the risk of the strategy into specific and market risk to assess

the origins of the gains. We find that market risk plays a relatively minor role in

our results. The specific component is the one showing interesting predictability.

Our study is closely related to the literature on the conditional behaviour of the

beta anomaly. Cohen et al. (2005) find that consistent with the presence of money

2

illusion in the stock market, the required real discount rate on low-beta stocks

increases disproportionately with inflation. As a result the low-beta anomaly is

concentrated in periods with moderate to high inflation. Antoniou et al. (2015)

show that beta commands a reasonable risk premium in pessimistic periods and

show that the anomaly is mainly present at times of optimism. They suggest that

optimism attracts unsophisticated and overconfident investors to the market that

result in the mispricing of beta. Huang et al. (2015) examine a measure of excess

co-movement in the BAB portfolio as a proxy for arbitrage activity. They find

that periods of high activity predict short-term returns positively but also more

pronounced subsequent reversals. We add to this literature by examining the case

for timing the volatility of the strategy.

Our paper is also related to the recent literature on timing the volatility of

alternative equity factors. Moreira and Muir (2016) provide a comprehensive study

of such benefits but they do not examine BAB in the current version of their paper.

Therefore, to the best of our knowledge, our study is the first to document the

large economic benefits of managing the risk of BAB and its startling similarity

with those found for momentum.

This paper is structured as follows. Section 2. compares the performance of

BAB with that of other equity factors. Section 3. shows the performance of risk-

managed factor portfolios. Section 4. assesses the predictability of risk for the

strategy and the existence of a risk-return trade-off. In section 5. we examine a

decomposition of the risk of the strategy into its market and specific components.

Section 6. concludes.

3

2. Factor investing and betting-against-beta

In this section we describe the equity factors used in this study, provide de-

scriptive statistics of their investment performance, and examine the risk-adjusted

performance of betting-against-beta (BAB).

We use the BAB returns for US stocks obtained from AQR’s data library

(https : //www.aqr.com/library/data − sets). The strategy consists on buying

low-beta stocks and shorting high-beta stocks choosing weights such that the ex-

ante beta of the strategy is zero. This implies having more than one dollar in the

long leg and less than one dollar in the short leg. The difference is funded by a

short position in the risk-free rate asset (T-bills) such that the overall portfolio

has zero cost. Frazzini and Pedersen (2014) provide a complete description of the

construction of the strategy’s portfolio.

We compare the returns of BAB with those of the Fama and French (1993)

three factors (FF3 model). The FF3 factors are: i) the excess return of the market

over the risk-free rate (market factor or ‘RM’); ii) the return of small firms in

excess of large firms (size factor or ‘SMB’); iii) the return of high book-to-market

stocks in excess of low book-to-market stocks (value factor or ‘HML’). For com-

pleteness we add to these the two newly proposed factors in Fama and French

(2015) (FF5 model): operating profitability (‘RMW’ for robust-minus-weak) and

investment (‘CMA’ for conservative-minus-aggressive). These two factors capture,

respectively, the average positive excess returns of firms with high profitability and

of those with low investments (as measured by asset growth). Taken together these

factors reflect the sources of predictability for the cross section of equity returns

found in the size (Banz (1981)), value (Basu (1983), Bondt and Thaler (1985),

4

Rosenberg et al. (1985)), profitability (Novy-Marx (2013), Hou et al. (2014)), and

investment (Hou et al. (2014)) variables.

We also use the Carhart (1997) 4-factor model (C4 model) that combines mo-

mentum with the FF3 factors. The return of momentum in a given month t is

defined as the difference in value-weighted returns between the portfolio of previous

winners and the portfolio of previous losers. The previous winners are the stocks

in the top decile according to cumulative return from months t− 12 to t− 2 while

the previous losers are those in the bottom decile. Only stocks listed in NYSE are

used to compute the cut-off points of the deciles. This avoids having some of the

deciles dominated by many small caps. The month t− 1 is skipped to avoid con-

founding with the short-term reversal effect in monthly returns (Jegadeesh (1990),

Jegadeesh and Titman (1995)). Momentum returns capture the tendency of recent

winners, as defined by their returns in the previous 3 to 12 months, to continue

outperforming recent losers (Levy (1967), Jegadeesh and Titman (1993)).

The returns of the momentum portfolios and the FF5 factors are from Kenneth

French’s data library.1 We have both daily and monthly returns available for all

factors from July 1963 to December 2015. We use realized volatilities computed

from one month and 6 months of data to perform the risk-scaling so our first

risk-managed returns start in January 1964 and end in December 2015.

[Insert table 1 near here]

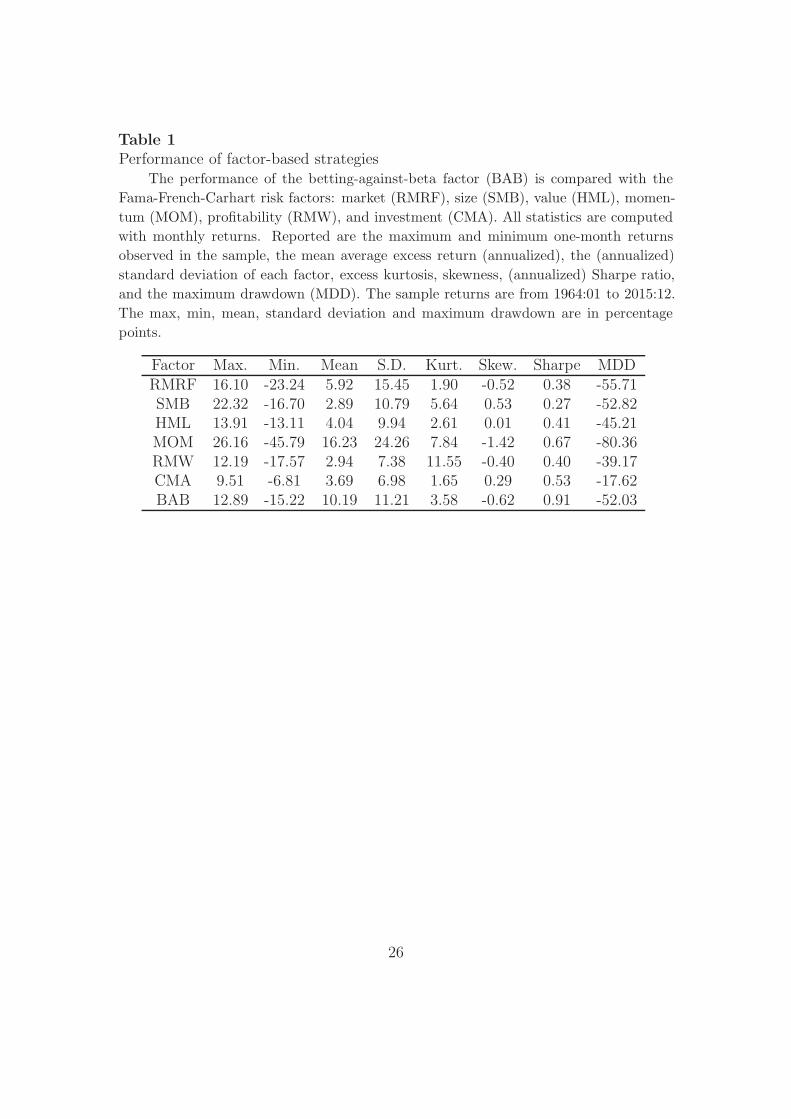

Table 1 shows the descriptive statistics of each factor-based investment strategy.

Compared with the market, size, value, momentum, profitability, and investment

factors, BAB has the highest Sharpe ratio. Its annualized Sharpe ratio is of 0.91,

1http : //mba.tuck.dartmouth.edu/pages/faculty/ken.french/datalibrary.html

5

more than double the 0.38 of the market with is already a central puzzle in financial

economics (Mehra and Prescott (1985)). It is also higher than the Sharpe ratio

of momentum (0.67) which is often regarded has the major asset pricing anomaly.

This illustrates the extent of the empirical failure of the CAPM. Black et al. (1972)

find that the security market line (SML) is flatter than what should hold accord-

ing to the CAPM. Frazzini and Pedersen (2014) show that a strategy exploiting

this apparent mispricing has an economic performance even more impressive than

momentum.

The strategy’s high Sharpe ratio comes with a considerable higher order risk

though with an excess kurtosis of 3.58 combined with a skewness of -0.62, both

higher in absolute terms than the market that has 1.90 and -0.52 respectively. This

higher order risk is small though when compared to the very high excess kurtosis

of momentum (7.84) and respective negative skewness (-1.42).

In spite of the impressive long run performance of the strategy it is also ex-

posed to substantial downside risk. Its maximum drawdown of -52.03 is close in

magnitude to that of the market (-55.71) which has a much higher standard de-

viation (15.45% versus 11.21%). Still, both the higher order risk and the (closely

related) maximum drawdown are smaller than those of momentum. So BAB of-

fers a higher Sharpe ratio and it is not as exposed to crashes as momentum (see

Daniel and Moskowitz (2016), Barroso and Santa-Clara (2015) for a discussion of

the crash risk of momentum).

Table 2 examines the ability of other risk factors to explain the returns of BAB.

The second column shows the alpha of the strategy with respect to the different

risk models. Columns 3 to 8 show the factor loadings of the strategy.

The market factor does not explain the returns of BAB. The strategy has a

6

high annualized alpha of 10.54% with a t-statistic of 6.57. The beta of the strategy

is very close to zero (-0.06). This shows that the strategy, which is constructed to

have an ex-ante beta of zero, on average achieves this goal ex-post.

Jointly the size and value factors explain approximately 20% of the CAPM-

alpha of the strategy. This is mainly due to the value factor. The BAB strategy in

all specifications that include the value factor shows a significant exposure to that

factor. The strategy is also exposed to the momentum, profitability and investment

factors. Taken together we see that available stock market risk models explain up

to 48% of the CAPM-alpha of the strategy (1−5.48/10.54). This happens because

on average low beta firms also show some loading on value, profitability and (low)

investment factors.

This suggests that a substantial part of the empirical failure of the CAPM can

be traced to failing to capture the multi-dimensional nature of risk that features

in latter models.2. But this ability of other factors to explain approximately half

of the anomaly’s risk-adjusted returns still leaves a considerable amount to be

explained. The alpha of approximately 5.5 to 6 percentage points a year and

respective t-statistics (3.49 in the C4 model and 3.48 in the FF5 model) are clearly

economically and statistically significant.

[Insert table 2 near here]

3. Scaled factor strategies

Barroso and Santa-Clara (2015) construct a risk-scaled version of momentum.

2It also suggests a possible reason for the particularly high Sharpe ratio of the strategy: it isanalogous to a linear combination of weakly correlated stock market factors

7

We extend this to other factors and examine the resulting economic performance

for an unconstrained investor. We compute the realized variance RVF,t from daily

returns in the previous 21 sessions for each month and factor. Let {rd}Dd=1

be the

daily returns and {dt}Tt=1 the time series of the dates of the last trading sessions

of each month. Then the realized variance of factor F in month t is:

RVF,t =

20∑

j=0

r2F,dt−j. (1)

Then we use the realized volatility σ̂F,t =√

RVF,t to scale the returns in order

to achieve a given target σtarget. Implicitly σ̂F,t is used as the forecast of σF,t+1.

All of the original factors used are zero-cost portfolios, so their scaled versions are

still zero-cost and self financing strategies that we can scale without constraints.

The scaled portfolio weight in the original factor at time t is:

Wt =σtarget

σ̂F,t

(2)

And so the risk-scaled factors are defined as F ∗

t+1 = Ft+1Wt. The choice of

volatility target is arbitrary but influences directly the maximum, minimum, mean

and the standard deviation of returns as well as the maximum drawdown of the

scaled portfolio. However this choice is irrelevant for scale-invariant measures

of portfolio performance such as the Sharpe ratio, (left) skewness, and excess

kurtosis. As in Barroso and Santa-Clara (2015) we pick a target corresponding to

an annualized volatility of 12%. This choice of target has the desirable property of

producing scaled factor portfolios with approximately the same ex-post volatility

of the (unscaled) US stock market. Picking the same target for all portfolios

facilitates comparison of those performance measures that are sensible to scaling.

8

Other volatility models could produce more accurate estimates of risk with

increased potential for risk-scaling. We refrain from that pursuit in this paper

and chose to focus instead on this somehow coarse measure of volatility. This also

serves as an implicit control mechanism when assessing the existence of robust

economic benefits in risk-scaling.3

[Insert table 3 near here]

Table 3 shows the performance of the scaled factors. Risk-scaling has economic

gains for investors following (almost) all factor strategies. For the market, the

risk-scaled factor has an information ratio of 0.20 with respect to the unscaled

factor. This gain confirms the result of Fleming et al. (2001) who document the

economic benefits of timing the volatility of the market. Their documented gains

from market timing using volatility contrast with the difficulty of similar strategies

trying to use predictability in returns (Goyal and Welch (2008)).

The benefits are not restricted to the market factor as 6 out of the 7 portfolios

show positive information ratios. The exception is the size premium for which the

scaled factor has a negative information ratio. Moskowitz (2003) show that the

size premium increases with volatility and recessions in a way consistent with a

risk-based explanation. Our results are consistent with theirs for the size factor.

By far the most impressive gains are found for the momentum and BAB factors.

Comparing with table 1 the Sharpe ratio of momentum increases from 0.67 to 1.08

(a 0.41 gain) and that of BAB increases from 0.91 to 1.28 (a 0.37 gain). The

information ratio of the scaled strategies with respect to their original versions

are very large for these two factors: 0.93 for MOM* and 0.94 for BAB*. These

3As a robustness test we also use the usual workhorse of volatility modelling, the GARCH(1,1).We present those results in table 6.

9

high information ratios reflect the fact that the risk-scaled portfolios are highly

correlated with the original factors but much more profitable. For the FF5 factors

the information ratio is on average 0.15, momentum and BAB have information

ratios about 6 times larger. Our results for momentum confirm the findings of

Barroso and Santa-Clara (2015). Moreira and Muir (2016) recently examine the

benefits of risk management in a set of factors that includes the FF5 but do not

consider BAB. Therefore, to the best of our knowledge, we are the first to document

that BAB shares this puzzling feature with momentum: the two strategies have

particularly expressive economic benefits from risk management, gains that set

them both apart from the FF5 factors.

[Insert table 4 near here]

Table 4 shows the risk-adjusted performance of BAB*. The strategy has a very

high CAPM-alpha of 21.10% per year. The risk model with the best fit for the strat-

egy is the C4 that explains 25% of its CAPM-alpha ((21.10%-15.83%)/21.10%).

This is a smaller proportion than the almost half explained in table 2. So risk-

managed BAB offers more diversification benefits than BAB for diversified in-

vestors exposed to other equity factors. The smallest annualized alpha is a very

high 15.83% (with the C4 model) and the adjusted r-squares of the regressions

are all smaller than in table 2. This confirms that BAB* is of value for diversified

investors and more so than BAB.

[Insert figure 1 near here]

Figure 1 shows the cumulative returns of momentum, betting-against-beta and

their respective risk-managed versions. As the strategies considered are zero-cost

10

portfolios their returns are excess returns. In order to have gross returns we add

to each strategy the gross return of an investment in the risk-free rate. So each

moment in time the portfolio puts all wealth in the risk-free rate and combines

this with a long-short portfolio. 4

In a pure CAPM world none of the strategies in figure 1 should have any

drift but empirically they have had an impressive economic performance. One

US dollar invested in momentum in July 1963 grows to 9, 990 by the end of the

sample. For the betting-against beta strategy the investment grows to a more

modest amount of 1, 675 dollars but with much less risk than the momentum

strategy. The scaled strategies have similar ex post standard deviation (17.37 for

MOM* versus 16.84 for BAB*) but very different end results: the investment in

risk-managed momentum grows to 87, 843 but in the beta anomaly to 364, 121.

For comparison a similar investment in the US stock market grows to 139 US

dollars by the end of the sample. This illustrates with an investment approach

the extent of the puzzle in the performance of these strategies, particularly the

benefits derived from managing their risk. A related debate is whether investors

could attain these performances in a realistic setting with transactions costs and

other frictions (see for example Lesmond et al. (2004) and Asness et al. (2014a)

for different interpretations of the evidence).

We do not address this debate directly but one possible interpretation of our

results is that the economic performance of these strategies, without frictions,

seems too puzzling to accept any explanation that does not incorporate them.

4For example, for momentum the original strategy puts a notional amount in the long leg ofWealtht and in the short leg of −Wealtht. For the risk-managed version the notional amountwould be WtWealtht and −WtWealtht in the long and short legs respectively. For BAB theamounts in the long and short leg are different in order to target a beta of zero but they areoffset by positions in the T-bills.

11

From an asset pricing perspective it is relevant to distinguish between correct

prices driven by risk loadings from mispricings that are hard to arbitrage. The

sizeable benefits of risk-management for BAB deepen the puzzle of the anomaly

and provide further indirect evidence of its relation to explanations relying on

arbitrage and frictions.

3.1. Robustness test: GARCH (1,1)

We assess the robustness of our results with respect to the horizon used to

compute the realized variance and using the GARCH(1,1) instead to estimate

variance.

Table 5 shows the performance of scaled factors using 6 months to estimate

variance instead of just one. First we note that for this particular window the

result of the economic value of timing the volatility of the market is not robust.

[Insert table 5 near here]

The information ratio for risk-managed momentum is 0.98, so the benefits for

this strategy are robust to this alternative period to compute variance. For BAB,

with a Sharpe ratio of 1.17 and an information ratio of 0.76 with respect to the

original strategy, we conclude that the benefits of risk-management are robust to

using an alternative window.

We also use GARCH(1,1) from monthly returns of each strategy to compute

risk-managed strategies. In order to assess the benefits of risk-management in

a realistic OOS environment we only use volatility estimates obtained from a

GARCH(1,1) model estimated in real time. We use the initial 120 months of

data to infer the parameters of the initial model and use them to make a forecast

12

for month 121. The following month we expand the sample with a new observation

and re-estimate the model. We keep re-iterating the procedure until the end of the

sample. Table 6 shows the economic performance of the risk-managed portfolios.

For comparison table 7 shows the performance of the original strategies for this

different sample period.

[Insert tables 6 and 7 near here]

In this setting the benefits of risk-management for the market are not robust

with a negative information ratio of -0.18. For momentum the benefits are robust

with a gain in Sharpe ratio from 0.57 to 0.71 and a substantial reduction in the

maximum drawdown from -80.36% to just -31.88%. For BAB the results are quite

robust. The information ratio of BAB* is 0.65, even higher than the 0.43 of MOM*.

So in this particular exercise the benefits of risk-management for BAB are stronger

than for MOM.

4. Risk and return of BAB

We examine the predictability of the risk of BAB and its relation with expected

returns.

First we examine the predictability of risk. Figure 2 shows the time series of

the (annualized) monthly realized variances computed from daily returns.

[Insert figure 2 near here]

The plot illustrates the typical patterns of volatility known from Bollerslev

(1987), Schwert (1989) and many others. Namely, volatility varies over time in a

13

persistent manner. The realized volatility of the strategy varies significantly from a

minimum of 1.75% in April 1965 to a maximum of 83% reached in May 2002. The

series is also highly non-normal with a kurtosis of 35.44 and a very high positive

skewness of 4.52 indicating that the sample contains extreme high risk outliers.

To examine the predictability of risk we run the regression:

1

ˆσi,t+1

= ρ0 + ρ11

σ̂i,t

+ εt+1. (3)

We focus on the inverse of realized volatility for two reasons. First, the risk-

managed strategy puts a weight on BAB proportional to this quantity so it is

the variable of direct interest to understand the source of the gains. Second, the

sample of the inverse of volatilities is much closer to normal. It has a kurtosis of

2.99 and a skewness of -0.11, this allows for a much better inference reducing the

large weight of outliers in the fit.

Table 8 shows the results of regression 3. Given the similar gains of risk manage-

ments for BAB and momentum we focus on these two strategies for the remainder

of the paper.

[Insert table 8 near here]

The table shows that both series have similar levels of predictability. The slope

coefficient is positive and it has a t-statistic of 23.88 for BAB and 25.31 for MOM.

This shows that safe months tend to follow safe months. Most of the variation in

the dependent variable is explained by its lagged value (R2 of 60.79% for BAB and

56.11% for MOM).

But in sample predictability can be misleading and so we also compute the out-

of-sample (OOS) R2 of the regression. For that purpose we use an initial window S

14

of 120 months ro run the first in-sample regression and use this to make a forecast

for month S + 1 that we compare with the ex-post realized value of the variable.

The following month we use an expanding window to estimate the regression and

re-iterate the procedure until the end of the sample. The OOS R2 for a factor i is

estimated as:

R2

i,OOS = 1−

T−1∑t=S

(ρ̂0,t + ρ̂1,t1̂/σi,t − ̂1/σi,t+1

T−1∑t=S

(1̂/σi,t − ̂1/σi,t+1)2, (4)

where 1̂/σi,t is the historical average up to time t and both α̂t and ρ̂t are

estimated with information available only up to time t. A positive OOS R2 shows

that on average the forecast from the regression outperforms that obtained from

the historical average.

We find the OOS R2 for BAB is not only positive but also very close to its

in-sample counterpart. This shows that the regression shows strong robustness out-

of-sample – a stark contrast with similar regressions for the equity premium that

typically achieve negative OOS R2’s (Goyal and Welch (2008)). The predictability

of the (inverse of) realized volatility for BAB is quite similar to the one documented

for momentum.

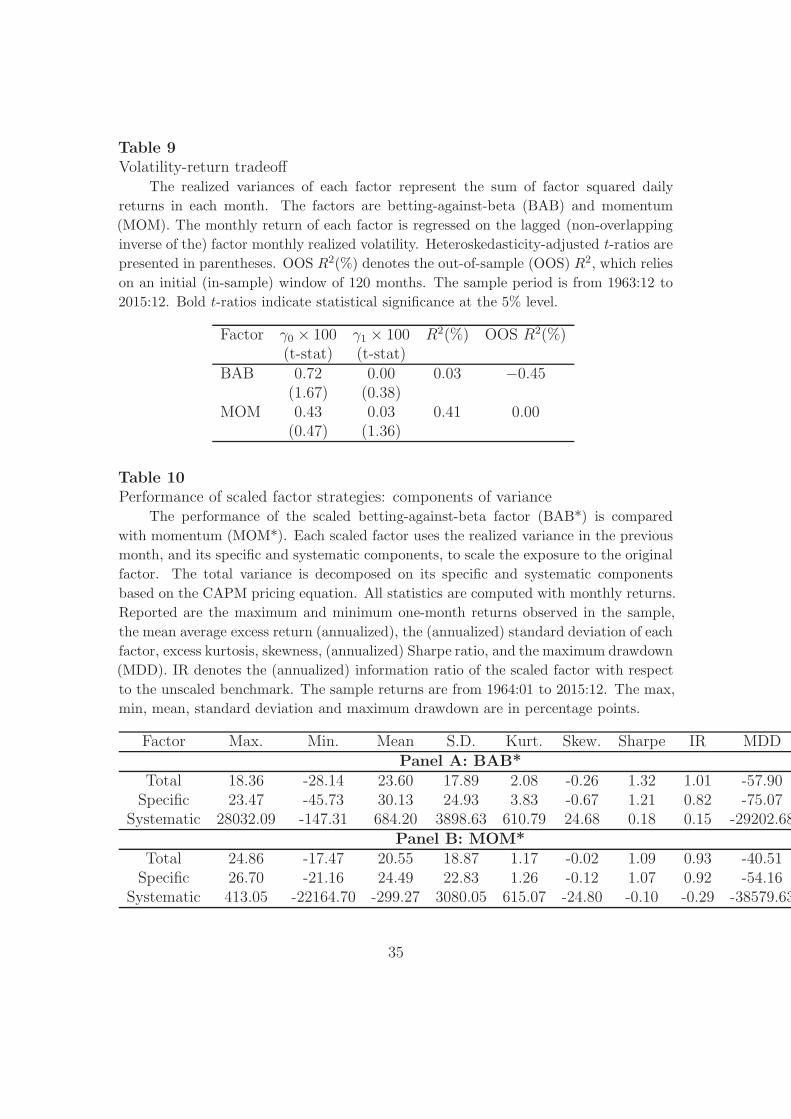

[Insert table 9 near here]

We next examine if this predictability in risk is related with expected returns.

For this purpose we regress the returns of each strategy on its lagged (inverse of)

realized volatility.

15

ri,t+1 = γ0 + γ1(1/σ̂i,t) + ηt+1. (5)

The existence of a risk-return trade-off should be captured by a statistically

significant negative γ1 meaning that months with less risk for the strategy also

predict smaller returns. The results in table 9 show there is no evidence of any

predictability of risk for the returns of BAB (or momentum). In fact the point

estimates for both strategies are positive, although not statistically significant.

[Insert figure 3 near here]

In figure 3 we further examine the relation between risk and return for the

strategies. For each strategy, we sort all months into quintiles according to realized

volatility. Then, for each quintile, we take the subset of months subsequent to

those in that quintile and compute the average return, standard deviation, and

Sharpe ratio over that subset. The results for momentum confirm the pattern in

Barroso and Santa-Clara (2015) that higher risk predicts both lower returns and

higher risk for the strategy, so the Sharpe ratio of the strategy is much higher

following quintiles 1 to 3 than in the two top quintiles. The results for BAB

show a similar pattern. In panel A the returns following a month in quintile 5

are lower (4.84%) on average than for other quintiles (11.53%). The relation is

not monotonous and the underperformance of BAB in terms of expected returns

is concentrated in months of particularly high risk. On the other hand, panel B

shows that subsequent risk rises monotonically with lagged risk. The annualized

volatility is 5.13% after a month in quintile 1 and it is 19.06% after a month in

quintile 5. As a result the Sharpe ratio is much smaller after months in the top

quintile (0.25) versus months after the lowest quintile (1.83). Both effects combine

16

such that BAB has a quite weak performance as a factor subsequent to months of

very high risk.

[Insert figure 4 near here]

Figure 4 shows the weights of BAB* and MOM*. On average BAB* has a

higher weight than MOM*. This happens because both strategies target the same

volatility but original BAB has a much lower standard deviation than MOM.5 As

the choice of target volatility is arbitrary this difference in the average weight is not

very informative. We note though that the two series have a strong and statistically

significant correlation of 0.63 (at the 1%) level. So an hypothetical unconstrained

arbitrageur following both strategies simultaneously would see speculative capital

being absorbed and freed-up from these two uses at the same time. This suggests

a possible limit to arbitrage for risk-management.

5. Anatomy of BAB risk

Grundy and Martin (2001) show that the beta of momentum with respect to

the market varies substantially over time. Cederburg and O’Doherty (2016) argue

that the conditional beta of BAB explains its premium. Motivated by this we

examine if time-varying systematic risk can account for the similar gains of risk

management for BAB and MOM and the performance of BAB in particular.

[Insert figure 5 near here]

5A version of BAB* re-scaled to have a similar average weight as MOM* would also show avery similar standard deviation in weights, so the apparent wilder swings of the weights in BABare only due to a level effect.

17

Figure 5 shows the plot of the time series of monthly betas of BAB and MOM

with respect to the market. The results for momentum confirm Grundy and Martin

(2001). The beta of MOM ranges between -2.86 and 2.57. We find that BAB also

has some time-varying market risk. In spite of being deliberately constructed to be

market neutral, its beta ranges between -1.57 and 0.30 and it shows some persis-

tence. Still the beta of BAB shows relatively little time-variation when compared

to momentum.

We use the CAPM to decompose the risk of BAB and MOM into a market and

a specific component:

RVF,t = β2

tRVRM,t + σ2

ε,t. (6)

The realized variances are estimated from daily returns in each month. 6 We

find that on average 37% of the risk of BAB is systematic, so the market neutral

strategy has a substantial market risk component. To assert the origin of the

gains, we examine the performance of a risk-managed strategy using each of the

risk components separately.

[Insert table 10 near here]

Table 10 shows the performance of risk-scaled BAB and momentum with total

risk, specific risk, and market risk respectively. The Sharpe ratio of BAB scaled

with specific risk is 1.21, close to the one using total risk (1.32). By contrast,

the strategy using the systematic risk has a very low Sharpe ratio of 0.18 and

6To ensure the decomposition holds exactly, we use in this section the variance formula. Thisde-means returns each month instead of just summing the squares of returns as in equation1. This does not change any of the results substantially and avoids the possibility of getting anegative specific risk.

18

a extreme value for standard deviation (3898.63), excess kurtosis (610.79), and

skewness (24.68). The results for momentum are similar to those of BAB. They

both show that the gains of risk-management come from using the informational

content in the specific component of risk.

We also examine the predictability of the inverse of each component of risk.

Table 11 shows the results of an auto-regression for each of those components

(which correspond to the weights in the strategies examined in table 10).

[Insert table 11 near here]

For BAB the specific part of risk is highly persistent with a slope coefficient

of 0.68 and a t-statistic of 20.30. The regression shows a good fit both in-sample

and OOS with R-squares of 46.13% and 47.46% respectively. The predictability

of the specific component is almost as high as that of total risk. For the sys-

tematic component there is no predictability. The slope coefficient is zero and

so is the R-squared. The results for momentum are similar and confirm those of

Barroso and Santa-Clara (2015). For both strategies the predictable part of risk

is the specific component.

6. Conclusion

Approximately half of the risk-adjusted returns of betting-against-beta with

respect to the market are explained by the Carhart (1997) or the Fama and French

(2015) factor models. While the remainder risk-adjusted performance is still a

puzzle in its own right, managing the risk of the strategy makes it much larger.

The risk-managed strategy has a high information ratio of 0.94, similar to that of

19

momentum. The scaled BAB has a higher alpha with respect to the market and

less of it (only 25%) is explained by equity risk factors. So managing the risk of

BAB creates and economic value orthogonal to those equity factors and even the

original BAB itself.

Risk is highly predictable for BAB, similar to that of momentum. There is also

no evidence of a risk-return trade-off for the strategy. If anything there seems to

be the opposite of a trade-off: BAB generally performs worse after months of high

risk in the strategy. This bad performance is concentrated in periods of extreme

risk for the strategy suggesting a regime switch in high volatility states.

Time-varying systematic risk has been proposed as an explanation of the pre-

mium of BAB (Cederburg and O’Doherty (2016)). We find evidence confirming

the existence of this time-varying systematic risk but also find that it conveys rela-

tively little information about the conditional performance of the strategy. Decom-

posing the risk of BAB into market and specific risk we find that the predictable

part is the specific one. Also, the performance of a strategy scaled by specific risk

only is very similar to one using total risk. So we conclude that specific risk is

causing the gains of risk management.

Generally, our results show that risk-managed BAB is a deeper puzzle than its

original version. The informational content of its own lagged volatility to condition

exposure to the strategy is very large, similar to momentum and much higher than

that found for the other equity factors examined.

The results are robust to using a different window to compute volatilities or a

GARCH(1,1) model to estimate it.

20

References

Antoniou, C., Doukas, J. A., and Subrahmanyam, A. (2015). Investor sentiment,

beta, and the cost of equity capital. Management Science, 62(2):347–367.

Asness, C. S., Frazzini, A., Israel, R., and Moskowitz, T. J. (2014a). Fact, fiction

and momentum investing. Journal of Portfolio Management, Fall.

Asness, C. S., Frazzini, A., and Pedersen, L. H. (2014b). Low-risk investing without

industry bets. Financial Analysts Journal, 70(4):24–41.

Baker, M., Bradley, B., and Taliaferro, R. (2014). The low-risk anomaly: A decom-

position into micro and macro effects. Financial Analysts Journal, 70(2):43–58.

Banz, R. W. (1981). The relationship between return and market value of common

stocks. Journal of financial economics, 9(1):3–18.

Barroso, P. and Santa-Clara, P. (2015). Momentum has its moments. Journal of

Financial Economics, 116(1):111–120.

Basu, S. (1983). The relationship between earnings’ yield, market value and return

for nyse common stocks: Further evidence. Journal of financial economics,

12(1):129–156.

Black, F., Jensen, M. C., and Scholes, M. S. (1972). The capital asset pricing

model: Some empirical tests. In Jensen, M., editor, Studies in the Theory of

Capital Markets. Praeger Publishers Inc.

21

Bollerslev, T. (1987). A conditionally heteroskedastic time series model for specu-

lative prices and rates of return. The review of economics and statistics, pages

542–547.

Bondt, W. F. and Thaler, R. (1985). Does the stock market overreact? The

Journal of finance, 40(3):793–805.

Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal

of finance, 52(1):57–82.

Cederburg, S. and O’Doherty, M. S. (2016). Does it pay to bet against beta?

on the conditional performance of the beta anomaly. The Journal of finance,

71(2):737–774.

Cohen, R. B., Polk, C., and Vuolteenaho, T. (2005). Money illusion in the stock

market: The modigliani-cohn hypothesis. The Quarterly journal of economics,

120(2):639–668.

Damodaran, A. (2012). Investment valuation: Tools and techniques for determin-

ing the value of any asset, volume 666. John Wiley & Sons.

Daniel, K. D. and Moskowitz, T. J. (2016). Momentum crashes. Journal of

Financial Economics, 122(2):221–247.

Fama, E. F. and French, K. R. (1993). Common risk factors in the returns on

stocks and bonds. Journal of financial economics, 33(1):3–56.

Fama, E. F. and French, K. R. (2004). The capital asset pricing model: Theory

and evidence. The Journal of Economic Perspectives, 18(3):25–46.

22

Fama, E. F. and French, K. R. (2015). A five-factor asset pricing model. Journal

of Financial Economics, 116(1):1–22.

Fleming, J., Kirby, C., and Ostdiek, B. (2001). The economic value of volatility

timing. The Journal of Finance, 56(1):329–352.

Frazzini, A. and Pedersen, L. H. (2014). Betting against beta. Journal of Financial

Economics, 111(1):1–25.

Goyal, A. and Welch, I. (2008). A comprehensive look at the empirical performance

of equity premium prediction. Review of Financial Studies, 21(4):1455–1508.

Grundy, B. D. and Martin, J. S. M. (2001). Understanding the nature of the risks

and the source of the rewards to momentum investing. Review of Financial

studies, 14(1):29–78.

Hou, K., Xue, C., and Zhang, L. (2014). Digesting anomalies: An investment

approach. Review of Financial Studies.

Huang, S., Lou, D., and Polk, C. (2015). The booms and busts of beta arbitrage.

Available at SSRN 2666910.

Jegadeesh, N. (1990). Evidence of predictable behavior of security returns. The

Journal of Finance, 45(3):881–898.

Jegadeesh, N. and Titman, S. (1993). Returns to buying winners and selling losers:

Implications for stock market efficiency. The Journal of finance, 48(1):65–91.

Jegadeesh, N. and Titman, S. (1995). Short-horizon return reversals and the bid-

ask spread. Journal of Financial Intermediation, 4(2):116–132.

23

Lesmond, D. A., Schill, M. J., and Zhou, C. (2004). The illusory nature of mo-

mentum profits. Journal of financial economics, 71(2):349–380.

Levy, R. A. (1967). Relative strength as a criterion for investment selection. The

Journal of Finance, 22(4):595–610.

Lintner, J. (1965). The valuation of risk assets and the selection of risky invest-

ments in stock portfolios and capital budgets. The review of economics and

statistics, pages 13–37.

Mehra, R. and Prescott, E. C. (1985). The equity premium: A puzzle. Journal of

monetary Economics, 15(2):145–161.

Moreira, A. and Muir, T. (2016). Volatility managed portfolios. The journal of

finance, forthcomming.

Moskowitz, T. J. (2003). An analysis of covariance risk and pricing anomalies.

Review of Financial Studies, 16(2):417–457.

Novy-Marx, R. (2013). The other side of value: The gross profitability premium.

Journal of Financial Economics, 108(1):1–28.

Rosenberg, B., Reid, K., and Lanstein, R. (1985). Persuasive evidence of market

inefficiency. The Journal of Portfolio Management, 11(3):9–16.

Schwert, G. W. (1989). Why does stock market volatility change over time? The

journal of finance, 44(5):1115–1153.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under

conditions of risk. The journal of finance, 19(3):425–442.

24

Treynor, J. L. (1965). How to rate management of investment funds. Harvard

business review, 43(1):63–75.

25

Table 1Performance of factor-based strategies

The performance of the betting-against-beta factor (BAB) is compared with the

Fama-French-Carhart risk factors: market (RMRF), size (SMB), value (HML), momen-

tum (MOM), profitability (RMW), and investment (CMA). All statistics are computed

with monthly returns. Reported are the maximum and minimum one-month returns

observed in the sample, the mean average excess return (annualized), the (annualized)

standard deviation of each factor, excess kurtosis, skewness, (annualized) Sharpe ratio,

and the maximum drawdown (MDD). The sample returns are from 1964:01 to 2015:12.

The max, min, mean, standard deviation and maximum drawdown are in percentage

points.

Factor Max. Min. Mean S.D. Kurt. Skew. Sharpe MDDRMRF 16.10 -23.24 5.92 15.45 1.90 -0.52 0.38 -55.71SMB 22.32 -16.70 2.89 10.79 5.64 0.53 0.27 -52.82HML 13.91 -13.11 4.04 9.94 2.61 0.01 0.41 -45.21MOM 26.16 -45.79 16.23 24.26 7.84 -1.42 0.67 -80.36RMW 12.19 -17.57 2.94 7.38 11.55 -0.40 0.40 -39.17CMA 9.51 -6.81 3.69 6.98 1.65 0.29 0.53 -17.62BAB 12.89 -15.22 10.19 11.21 3.58 -0.62 0.91 -52.03

26

Table 2Alphas for BAB

This table presents the alphas and factor loadings from time-series regressions of

the betting-against-beta factor (BAB). The factor models are the CAPM, Fama-French

three-factor model (FF3), Carhart’s four-factor model (C4), and the Fama-French five-

factor model (FF5). The factors are the market (RM), size (SMB), value (HML), mo-

mentum (MOM), profitability (RMW), and investment (CMA). The sample is 1964:01

to 2015:12. For each regression, the first row presents the coefficient estimates and the

second row reports Heteroskedasticity-adjusted t-ratios (in parentheses). α is the an-

nualized intercept. R2 denotes the adjusted coefficient of determination. Bold t-ratios

indicate statistical significance at the 5% level.

Model α(%) βRM βSMB βHML βMOM βRMW βCMA R2(%)CAPM 10.54 −0.06 0.51

(6.57) (−1.25)FF3 8.26 0.03 −0.01 0.44 14.31

(5.27) (0.56) (−0.10) (6.46)C4 5.97 0.07 0.00 0.50 0.11 19.64

(3.49) (1.40) (0.01) (7.06) (4.10)FF5 5.48 0.08 0.11 0.28 0.46 0.38 22.00

(3.48) (1.76) (2.17) (3.06) (5.90) (3.21)

27

Table 3Performance of scaled factor strategies

The performance of the scaled betting-against-beta factor (BAB*) is compared with

the Fama-French-Carhart scaled risk factors: market (RMRF*), size (SMB*), value

(HML*), momentum (MOM*), profitability (RMW*), and investment (CMA*). Each

scaled factor uses the realized variance in the previous month to scale the exposure to

the original factor. All statistics are computed with monthly returns. Reported are the

maximum and minimum one-month returns observed in the sample, the mean average

excess return (annualized), the (annualized) standard deviation of each factor, excess

kurtosis, skewness, (annualized) Sharpe ratio, and the maximum drawdown (MDD).

IR denotes the (annualized) information ratio of the scaled factor with respect to the

unscaled benchmark. The sample returns are from 1964:01 to 2015:12. The max, min,

mean, standard deviation and maximum drawdown are in percentage points.

Factor Max. Min. Mean S.D. Kurt. Skew. Sharpe IR MDDRMRF* 13.94 -18.66 6.30 14.63 1.14 -0.27 0.43 0.20 -52.82SMB* 23.60 -22.94 4.21 18.86 1.85 -0.10 0.22 -0.04 -84.68HML* 22.84 -22.78 8.41 18.67 1.19 0.15 0.45 0.20 -57.42MOM* 20.74 -15.43 18.79 17.37 0.82 -0.17 1.08 0.93 -37.33RMW* 18.26 -17.15 8.65 17.14 0.49 0.03 0.50 0.31 -57.97CMA* 18.22 -13.84 8.15 16.24 0.07 0.17 0.50 0.07 -44.02BAB* 17.59 -28.54 21.48 16.84 2.70 -0.41 1.28 0.94 -56.75

28

Table 4Alphas for scaled BAB

This table presents the alphas and factor loadings from time-series regressions of

the scaled betting-against-beta factor (BAB*). BAB* uses the realized variance in the

previous month to scale the exposure to the original factor. The factor models are the

CAPM, Fama-French three-factor model (FF3), Carhart’s four-factor model (C4), and

the Fama-French five-factor model (FF5). The factors are the market (RM), size (SMB),

value (HML), momentum (MOM), profitability (RMW), and investment (CMA). The

sample is 1964:01 to 2015:12. For each regression, the first row presents the coefficient

estimates and the second row reports Heteroskedasticity-adjusted t-ratios (in parenthe-

ses). α is the annualized intercept. R2 denotes the adjusted coefficient of determination.

Bold t-ratios indicate statistical significance at the 5% level.

Model α(%) βRM βSMB βHML βMOM βRMW βCMA R2(%)CAPM 21.10 0.06 0.19

(8.75) (0.90)FF3 18.22 0.16 0.03 0.55 9.22

(7.68) (2.33) (0.45) (7.66)C4 15.83 0.20 0.04 0.61 0.12 11.75

(6.42) (2.87) (0.54) (8.39) (4.04)FF5 15.97 0.22 0.10 0.35 0.30 0.44 11.14

(6.34) (2.93) (1.33) (3.66) (2.96) (2.83)

29

60 65 70 75 80 85 90 95 00 05 10 15 2010

0

101

102

103

104

105

106

Cumulative returns

MOMBABMOM*BAB*

Fig. 1. The cumulative returns of BAB, MOM and its risk-managed versionsusing the previous month realized volatility. The returns are from 1964:01 to2015:12 and include the return of the risk-free rate asset plus the excess return ofthe respective zero-cost portfolio.

30

Table 5Performance of scaled factor strategies: alternative variance measures

The performance of the scaled betting-against-beta factor (BAB*) is compared with

the Fama-French-Carhart scaled risk factors: market (RMRF*), size (SMB*), value

(HML*), momentum (MOM*), profitability (RMW*), and investment (CMA*). Each

scaled factor uses the realized variance in the previous six months to scale the exposure to

the original factor. All statistics are computed with monthly returns. Reported are the

maximum and minimum one-month returns observed in the sample, the mean average

excess return (annualized), the (annualized) standard deviation of each factor, excess

kurtosis, skewness, (annualized) Sharpe ratio, and the maximum drawdown (MDD).

IR denotes the (annualized) information ratio of the scaled factor with respect to the

unscaled benchmark. The sample returns are from 1964:01 to 2015:12. The max, min,

mean, standard deviation and maximum drawdown are in percentage points.

Factor Max. Min. Mean S.D. Kurt. Skew. Sharpe IR MDDRMRF* 11.39 -20.35 4.99 13.99 1.64 -0.57 0.36 0.00 -57.36SMB* 21.79 -21.52 4.34 17.96 1.50 0.11 0.24 -0.02 -82.76HML* 23.13 -17.50 7.41 17.78 0.92 0.12 0.42 0.12 -55.81MOM* 21.74 -17.06 18.67 17.04 1.18 -0.15 1.10 0.98 -28.28RMW* 15.82 -24.01 7.63 16.65 1.10 -0.19 0.46 0.23 -62.33CMA* 13.77 -14.23 8.38 15.63 -0.07 0.16 0.54 0.14 -37.14BAB* 18.25 -22.79 19.16 16.38 1.63 -0.43 1.17 0.76 -57.14

31

Table 6Performance of scaled factor strategies: GARCH(1,1)

The performance of the scaled betting-against-beta factor (BAB*) is compared with

the Fama-French-Carhart scaled risk factors: market (RMRF*), size (SMB*), value

(HML*), momentum (MOM*), profitability (RMW*), and investment (CMA*). Each

scaled factor uses the volatility forecast obtained from a GARCH(1,1) model to scale

the exposure to the original factor. All statistics are computed with monthly returns.

Reported are the maximum and minimum one-month returns observed in the sample,

the mean average excess return (annualized), the (annualized) standard deviation of each

factor, excess kurtosis, skewness, (annualized) Sharpe ratio, and the maximum drawdown

(MDD). IR denotes the (annualized) information ratio of the scaled factor with respect

to the unscaled benchmark. The sample returns are from 1963:07 to 2015:12, while the

first volatility forecast and scaled factor observation occurs for 1973:07. The max, min,

mean, standard deviation and maximum drawdown are in percentage points.

Factor Max. Min. Mean S.D. Kurt. Skew. Sharpe IR MDDRMRF* 9.14 -18.52 4.49 12.24 2.25 -0.75 0.37 -0.18 -42.77SMB* 16.83 -13.35 3.01 11.96 1.75 0.14 0.25 0.02 -62.68HML* 12.87 -11.67 3.79 12.23 0.73 -0.13 0.31 -0.18 -48.07MOM* 12.94 -27.62 9.99 13.99 6.31 -1.22 0.71 0.43 -31.88RMW* 9.54 -18.18 5.91 12.64 1.78 -0.45 0.47 0.19 -57.12CMA* 9.53 -9.80 6.76 11.75 -0.13 0.04 0.58 0.01 -31.88BAB* 14.49 -18.18 14.58 13.18 2.37 -0.71 1.11 0.65 -54.01

32

Table 7Performance of factor-based strategies: 1973:07–2015:12

The performance of the betting-against-beta factor (BAB) is compared with the

Fama-French-Carhart risk factors: market (RMRF), size (SMB), value (HML), momen-

tum (MOM), profitability (RMW), and investment (CMA). All statistics are computed

with monthly returns. Reported are the maximum and minimum one-month returns

observed in the sample, the mean average excess return (annualized), the (annualized)

standard deviation of each factor, excess kurtosis, skewness, (annualized) Sharpe ratio,

and the maximum drawdown (MDD). The sample returns are from 1973:07 to 2015:12.

The max, min, mean, standard deviation and maximum drawdown are in percentage

points.

Factor Max. Min. Mean S.D. Kurt. Skew. Sharpe MDDRMRF 16.10 -23.24 6.71 15.94 2.00 -0.56 0.42 -54.36SMB 22.32 -16.70 2.94 10.78 6.96 0.59 0.27 -52.82HML 13.91 -13.11 3.94 10.36 2.59 0.00 0.38 -45.21MOM 26.16 -45.79 14.53 25.39 7.69 -1.44 0.57 -80.36RMW 12.19 -17.57 3.33 7.76 11.45 -0.45 0.43 -39.17CMA 9.51 -6.81 4.11 6.87 1.83 0.38 0.60 -17.30BAB 12.89 -15.22 10.90 11.92 3.22 -0.67 0.91 -52.03

Table 8Autoregression of monthly realized volatilities

The realized variances of each factor represent the sum of factor squared daily returns

in each month. The factors are betting-against-beta (BAB) and momentum (MOM).

The AR(1) process regresses the (non-overlapping inverse of the) factor monthly realized

volatility on its own lagged value. Heteroskedasticity-adjusted t-ratios are presented in

parentheses. OOS R2(%) denotes the out-of-sample (OOS) R2, which relies on an initial

(in-sample) window of 120 months. The sample period is from 1963:12 to 2015:12. Bold

t-ratios indicate statistical significance at the 5% level.

Factor ρ0 ρ1 R2(%) OOS R2(%)(t-stat) (t-stat)

BAB 12.96 0.78 60.79 63.36(7.49) (23.88)

MOM 7.16 0.75 56.11 60.41(9.12) (25.31)

33

60 65 70 75 80 85 90 95 00 05 10 15 200

10

20

30

40

50

60

70

80

90

Fig. 2. Realized volatility of BABThis figure plots the time-series of the annualized realized volatility (in %) associated

with the BAB factor computed from daily returns each month. The sample is 1964:01

to 2015:12.

34

Table 9Volatility-return tradeoff

The realized variances of each factor represent the sum of factor squared daily

returns in each month. The factors are betting-against-beta (BAB) and momentum

(MOM). The monthly return of each factor is regressed on the lagged (non-overlapping

inverse of the) factor monthly realized volatility. Heteroskedasticity-adjusted t-ratios are

presented in parentheses. OOS R2(%) denotes the out-of-sample (OOS) R2, which relies

on an initial (in-sample) window of 120 months. The sample period is from 1963:12 to

2015:12. Bold t-ratios indicate statistical significance at the 5% level.

Factor γ0 × 100 γ1 × 100 R2(%) OOS R2(%)(t-stat) (t-stat)

BAB 0.72 0.00 0.03 −0.45(1.67) (0.38)

MOM 0.43 0.03 0.41 0.00(0.47) (1.36)

Table 10Performance of scaled factor strategies: components of variance

The performance of the scaled betting-against-beta factor (BAB*) is compared

with momentum (MOM*). Each scaled factor uses the realized variance in the previous

month, and its specific and systematic components, to scale the exposure to the original

factor. The total variance is decomposed on its specific and systematic components

based on the CAPM pricing equation. All statistics are computed with monthly returns.

Reported are the maximum and minimum one-month returns observed in the sample,

the mean average excess return (annualized), the (annualized) standard deviation of each

factor, excess kurtosis, skewness, (annualized) Sharpe ratio, and the maximum drawdown

(MDD). IR denotes the (annualized) information ratio of the scaled factor with respect

to the unscaled benchmark. The sample returns are from 1964:01 to 2015:12. The max,

min, mean, standard deviation and maximum drawdown are in percentage points.

Factor Max. Min. Mean S.D. Kurt. Skew. Sharpe IR MDDPanel A: BAB*

Total 18.36 -28.14 23.60 17.89 2.08 -0.26 1.32 1.01 -57.90Specific 23.47 -45.73 30.13 24.93 3.83 -0.67 1.21 0.82 -75.07

Systematic 28032.09 -147.31 684.20 3898.63 610.79 24.68 0.18 0.15 -29202.68Panel B: MOM*

Total 24.86 -17.47 20.55 18.87 1.17 -0.02 1.09 0.93 -40.51Specific 26.70 -21.16 24.49 22.83 1.26 -0.12 1.07 0.92 -54.16

Systematic 413.05 -22164.70 -299.27 3080.05 615.07 -24.80 -0.10 -0.29 -38579.63

35

1 2 3 4 5−10

0

10

20

30Panel A: Mean(%)

MOMBAB

1 2 3 4 50

20

40

60Panel B: Volatility(%)

MOMBAB

1 2 3 4 5−1

0

1

2Panel C: Sharpe ratio

MOMBAB

Fig. 3. Conditional performance of BAB and MOMThe returns of each factor are sorted on quintiles based on the realized volatility in the

previous month. The figure presents the following annualized average return, volatility,

and Sharpe ratio. The sample is 1964:01 to 2015:12.

36

60 65 70 75 80 85 90 95 00 05 10 15 200

1

2

3

4

5

6

7

MOM*BAB*

Fig. 4. Weights of scaled BAB and MOMThis figure plots the time-series of the weights associated with the scaled BAB and MOM

factors. The sample is 1964:01 to 2015:12.

37

60 65 70 75 80 85 90 95 00 05 10 15 20−3

−2

−1

0

1

2

3

MOM*BAB*

Fig. 5. Betas for BAB and MOMThis figure plots the time-series for the realized market beta associated with the BAB

and MOM factors. The sample is 1964:01 to 2015:12.

38

Table 11Autoregression of the components of realized volatilities

The realized variances of each factor represent the sum of factor squared daily

returns in each month. The total variance is decomposed on its specific and systematic

components based on the CAPM pricing equation. The factors are betting-against-

beta (BAB) and momentum (MOM). The AR(1) process regresses the (non-overlapping

inverse of the) factor monthly realized volatility (or each of its components) on its own

lagged value. Heteroskedasticity-adjusted t-ratios are presented in parentheses. OOS

R2(%) denotes the out-of-sample (OOS) R2, which relies on an initial (in-sample) window

of 120 months. The sample period is from 1963:12 to 2015:12. Bold t-ratios indicate

statistical significance at the 5% level.

Volatility ρ0 ρ1 R2(%) OOS R2(%)(t-stat) (t-stat)

Panel A: BABTotal 16.72 0.74 54.82 57.06

(8.09) (20.89)Spec. 26.96 0.68 46.13 47.46

(10.17) (20.30)Syst. 930.83 −0.00 0.00 −0.15

(1.54) (−0.01)Panel B: MOM

Total 9.38 0.70 49.05 55.19(9.75) (21.48)

Spec. 11.81 0.68 46.11 50.42(10.81) (22.45)

Syst. 210.73 −0.00 0.00 −0.50(6.62) (−0.11)

39