management’s discussion and analysis - torex gold · this management’s discussion and analysis...

TRANSCRIPT

1

Legal*10184613.1

Management’s Discussion and Analysis For the Three Months Ended March 31, 2016

TOREX GOLD RESOURCES INC.MANAGEMENT’S DISCUSSION AND ANALYSIS

FOR THE QUARTER ENDED MARCH 31, 2016

TABLE OF CONTENTS

Company Overview and Strategy ....................................................................................................... 2Highlights............................................................................................................................................ 2Overview of the First Quarter 2016 Financial Results ........................................................................ 4Objectives for 2016............................................................................................................................. 4Morelos Gold Property ....................................................................................................................... 5

El Limón Guajes Mine Update ........................................................................................................ 62016 Life of Mine Plan.................................................................................................................... 9Morelos Gold Property Exploration Update................................................................................... 12Media Luna Project Update............................................................................................................ 12

Debt Financing.................................................................................................................................... 12Results of Operations ......................................................................................................................... 14Summary of Quarterly Results............................................................................................................ 15Liquidity and Capital Resources .......................................................................................................... 16Economic Trends and Liquidity and Capital Resources Outlook ......................................................... 18Off-Balance Sheet Arrangements ....................................................................................................... 18Financial Risk Management................................................................................................................ 19Transactions with Related Parties....................................................................................................... 21Outstanding Share Data...................................................................................................................... 21Critical Accounting Policies and Estimates.......................................................................................... 21Risks and Uncertainties ...................................................................................................................... 22Internal Control Over Financial Reporting .......................................................................................... 24Qualified Persons................................................................................................................................ 24Cautionary Note Regarding Forward-Looking Statements ................................................................. 25

This management’s discussion and analysis of the financial condition and results of operations (“MD&A”)for Torex Gold Resources Inc. (“Torex” or the “Company”) was prepared as at May 11, 2016 and is intendedto supplement and complement the Company’s condensed consolidated interim financial statements andrelated notes for the quarter ended March 31, 2016. The condensed consolidated interim financialstatements have been prepared in accordance with International Financial Reporting Standards (“IFRS”).All dollar figures included therein and in the following MD&A are stated in United States dollars (“U.S.dollar”) unless otherwise stated. Additional information relating to the Company, including its annualinformation form and other Company filings, can also be viewed on the Company’s website atwww.torexgold.com or on SEDAR at www.sedar.com.

For further details regarding the El Limón Guajes (“ELG”) mine (the “ELG Mine”) and the Media Luna Project(the “Media Luna Project”), please refer to the updated ELG mine plan and the Media Luna ProjectPreliminary Economic Assessment (the “PEA”), dated effective August 17, 2015, and titled “NI 43-101Technical Report - El Limón Guajes Mine Plan and Media Luna Preliminary Economic Assessment, GuerreroState, Mexico” (the “Technical Report”). The updated 2015 mine plan for the ELG Mine was undertaken in

1

connection with the PEA for the Media Luna Project, which are both located on the Morelos gold property(the “Morelos Gold Property”). The PEA considers the potential economic viability of developing the MediaLuna resource by making use of the infrastructure, social capital, and secure work area which has beendeveloped for the ELG Mine. As such, the Technical Report was completed to include the updated mineplan for the ELG Mine and the PEA for the Media Luna Project in accordance with National Instrument43-101 (“NI 43-101”). The current Technical Report is available on the Company’s website atwww.torexgold.com and was filed on SEDAR at www.sedar.com on September 3, 2015. The mine plan forthe ELG Mine was subsequently updated further (See “Morelos Gold Property - 2016 Life of Mine Plan”).

2

COMPANY OVERVIEW AND STRATEGY

The Company is a growth-oriented Canadian-based resource company engaged in the exploration,development and operation of the Morelos Gold Property. The Morelos Gold Property includes a large landpackage of approximately 29,000 hectares and contains, among other things, two assets, the ELG Mine,which is in the production stage effective April 1, 2016, and the Media Luna Project, which is in an advancedstage of exploration, for which the Company issued a PEA in 2015.

The Company’s strategy is to grow the production from the Morelos Gold Property. In March 2016, theCompany announced that the ELG Mine had reached commercial production status ahead of schedule. TheMedia Luna Project, 7 km from the ELG processing plant, provides prospects for future production growth,and exploration targets below the El Limón pit provide the opportunity to extend the ELG Mine life. Thereare many other exploration targets on the Morelos Gold Property, however exploration activities have beencurtailed in order to focus on the ELG Mine and the development of Media Luna.

HIGHLIGHTS

ELG Mine Achieved Commercial Production

• On March 30, 2016, the Company announced that the ELG Mine had achieved commercial productionahead of schedule and under budget, reaching an average of more than 60% of plant design throughputof 14,000 tonnes per day (“tpd”) for 30 days. For accounting purposes, the transition to the productionphase will be reflected commencing April 1, 2016.

• The plant produced 38,161 ounces of gold during the first quarter and produced 19,900 ounces of goldin April 2016.

• Plant throughput was ahead of plan, averaging 9,100 tpd during the first quarter. In the latter half ofApril, throughput averaged more than 12,800 tpd, or 91% of design capacity, at an average gold recoveryof 85%.

• The current record daily production level of 16,300 tpd was achieved on May 9, 2016, and again onMay 10. This exceeded nameplate design capacity of 14,000 tpd by 16%.

• Gold recovery levels during the first quarter ranged from 63.0% to 90.7%, averaging above 80% forMarch 2016, compared to life of mine design levels of 87.4%.

• The tailings filtration plant is delivering the expected product for dry stack disposal, and throughputhas been steadily increasing to match the cadence set by the grinding circuit.

Mining

• At the end of the first quarter, the Company had approximately 1.0 million tonnes of ore stockpiled.• Commissioning of both the El Limón crusher and RopeCon commenced in March 2016 and was

completed in April. • The resettlement of the Real del Limón village was started during the first quarter and was completed

in April 2016.

Temporary Suspension of Operations • In April 2016, the Company suspended operations at the ELG Mine for a period of 10 days due to an

illegal blockade.

• The Company refuted the unjustified claims made and refused to make payments to those engaging inthe illegal blockade. After an intervention by the Government of the State of Guerrero, the blockadewas lifted on April 14, 2016.

• During the temporary suspension, a number of maintenance, fine tuning, and commissioning activitieswere completed. These included the replacement of the SAG mill liners, chute adjustments, pipingimprovements, filter cloth replacement and the final commissioning of the RopeCon.

ELG Life of Mine Plan Update

• In May 2016, the Company completed a Life of Mine (“LOM”) plan update for the ELG Mine on astandalone basis. As previously reported, the Company was investigating the location of post-mineralization dike intrusions, and the potential effect of these intrusions on the resource estimate.The updated LOM plan incorporates the results of this recent work. The LOM is now projected to be8.5 years, a decrease from the previous estimate of 10 years, and the projected gold production for thefirst seven years of the LOM is expected to be comparable to the first seven years of the previousstandalone life of mine plan. Refer to “Morelos Gold Property - 2016 Life of Mine Plan” below.

Financial Position

• The Company ended the first quarter with cash on hand of $30.5 million, with an additional $34.6 millionin restricted cash.

• Current cash and restricted cash balances, along with proceeds from gold sales and recoveries of ValueAdded Tax (“VAT”), are expected to be sufficient to fund operations and settle outstanding liabilities asthe plant ramps up to design capacity of 14,000 tpd.

• Proceeds from gold sales during the first quarter of 2016 were $38.9 million1 from the sale of31,518 ounces of gold at an average realized price of $1,234 per ounce. Gold sold subsequent to quarter-end was 29,185 ounces as at May 11, 2016.

• Refunds of VAT of $9.9 million were received during the first quarter of 2016, with a further $1.2 millionreceived in April. The Company expects to recover an additional $28.1 million within the next twelvemonths.

3

1 Includes proceeds from deliveries under derivative contracts entered into in connection with the Company’s CreditAgreement as discussed in “Debt Financing”.

• Efforts to secure a VAT loan, as a contingency plan for possible delays in the collection of VAT refunds,are advancing and loan documents are under review. The loan is expected to close in the second quarterof 2016 and is expected to provide funds for up to 80% of the outstanding VAT receivables at the timethe loan is executed.

• During the first quarter, the Company utilized $6.2 million of its $17.4 million Finance Lease Arrangementwith Parilease SAS, to finance certain mining equipment.

4

OVERVIEW OF THE FIRST QUARTER 2016 FINANCIAL RESULTS

The net loss for the quarter ended March 31, 2016 totaled $37.8 million compared to $10.7 million for thequarter ended March 31, 2015. This increase in net loss is primarily due to the recognition of unrealizedlosses on the Company’s gold derivative contracts outstanding at March 31, 2016 of $34.3 million as a resultof the increase in gold prices during the first quarter of 2016. The Company also recognized a foreignexchange loss of $1.6 million during the first quarter of 2016 primarily as a result of fluctuations in the valueof the Mexican peso relative to the U.S. dollar. These were partly offset by a reduction in exploration andevaluation expenditures during the period, which totalled $0.8 million for the three months endedMarch 31, 2016, compared to $3.7 million in the prior year period.

During the quarter, the Company collected proceeds of $38.9 million from gold sales (including realizedgains of $0.2 million from deliveries under derivative contracts entered into in connection with theCompany’s Credit Agreement as discussed in “Debt Financing”), as well as $9.9 million in refunds of VATreceivables (excluding interest of $0.1 million). The Company also utilized $6.2 million under its FinanceLease Agreement to finance certain mining equipment. Further, the Company withdrew $4.0 million and$6.0 million from the Sponsor Reserve Account (as defined in “Debt Financing”) to fund corporateexpenditures and expenditures for the ELG Mine, respectively. As a result, the Company’s restricted cashtotalled $34.6 million as at March 31, 2016, while cash and cash equivalents amounted to $30.5 million.The Company had $1,106.2 million in total assets at the end of the first quarter of 2016, compared with$1,121.1 million in assets as at December 31, 2015.

For a discussion of trends which may impact the Company, see “Economic Trends and Liquidity and CapitalResources Outlook.”

OBJECTIVES FOR 2016

The following highlights the Company’s primary objectives for 2016:

Safety and Health:• No fatalities.• A lost time injury frequency of no more than 2 lost time injuries per million hours worked

(contractors and employees combined).

Environment• No reportable spills of 1,000 litres or more to the river or the reservoir.

Production:• 2016 Production: Sell 275,000 ELG Mine gold ounces.• Setting up 2017 Production: Strip 17 million tonnes of waste in 2016.

Cost Control:• Cash cost of less than $550 per equivalent gold ounce.• All-in sustaining cost of less than $775 per equivalent gold ounce.

Milestones:• Achieve commercial production in the second quarter of 2016.• Complete commissioning of the El Limón crusher and RopeCon in the second quarter of 2016.• Complete the resettlement of the Real del Limón village in the second quarter of 2016.• Complete the commissioning of the truck shop for the ELG Mine in the second quarter of 2016.• Obtain the permits for an exploration tunnel for the Media Luna Project.

5

MORELOS GOLD PROPERTY

Overview

The Morelos Gold Property is in the Guerrero Gold Belt in southern Mexico, 180 kilometres to the southwestof Mexico City and approximately 50 kilometres southwest of Iguala. The Guerrero Gold Belt contains anumber of gold deposits and prospects, including Goldcorp Inc.’s Los Filos Mine, located approximately14 kilometres southeast of the ELG Mine of the Morelos Gold Property.

The Morelos Gold Property consists of seven mineral concessions covering a total area of approximately29,000 hectares. The 29,000 hectare land package is bisected by the Balsas River and the drilling areas thatthe Company has defined are generally referenced as “North” or “South” of the Balsas River. Drilling areaslocated north of the Balsas River include the ELG Mine, Guajes South and Pacifico. Additional prospectiveareas in the north include Todos Santos (north portion), Corona, Tecate, Azcala, Modelo, Querenque andEl Limón Deep. Drilling areas located south of the Balsas River include Media Luna, El Cristo, Naranjoand La Fe.

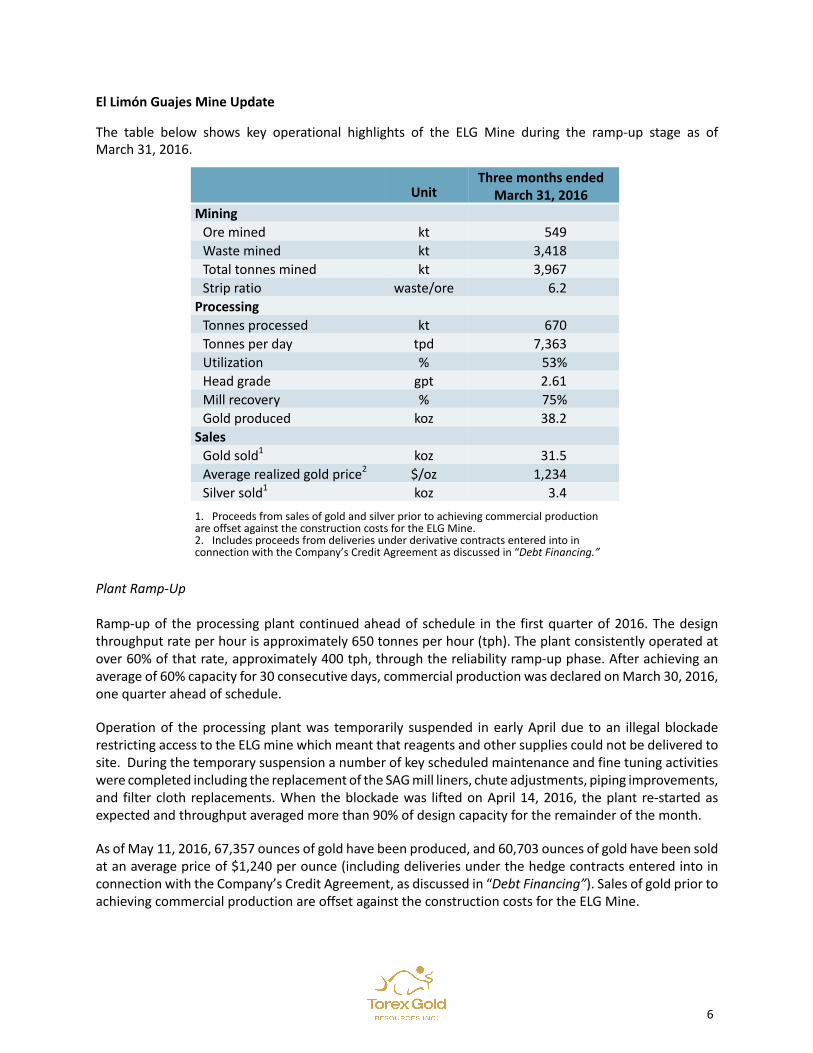

El Limón Guajes Mine Update

The table below shows key operational highlights of the ELG Mine during the ramp-up stage as ofMarch 31, 2016.

UnitThree months ended

March 31, 2016Mining

Ore mined kt 549Waste mined kt 3,418Total tonnes mined kt 3,967Strip ratio waste/ore 6.2

ProcessingTonnes processed kt 670Tonnes per day tpd 7,363Utilization % 53%Head grade gpt 2.61Mill recovery % 75%Gold produced koz 38.2

SalesGold sold1 koz 31.5Average realized gold price2 $/oz 1,234Silver sold1 koz 3.4

1. Proceeds from sales of gold and silver prior to achieving commercial productionare offset against the construction costs for the ELG Mine. 2. Includes proceeds from deliveries under derivative contracts entered into inconnection with the Company’s Credit Agreement as discussed in “Debt Financing.”

Plant Ramp-Up

Ramp-up of the processing plant continued ahead of schedule in the first quarter of 2016. The designthroughput rate per hour is approximately 650 tonnes per hour (tph). The plant consistently operated atover 60% of that rate, approximately 400 tph, through the reliability ramp-up phase. After achieving anaverage of 60% capacity for 30 consecutive days, commercial production was declared on March 30, 2016,one quarter ahead of schedule.

Operation of the processing plant was temporarily suspended in early April due to an illegal blockaderestricting access to the ELG mine which meant that reagents and other supplies could not be delivered tosite. During the temporary suspension a number of key scheduled maintenance and fine tuning activitieswere completed including the replacement of the SAG mill liners, chute adjustments, piping improvements,and filter cloth replacements. When the blockade was lifted on April 14, 2016, the plant re-started asexpected and throughput averaged more than 90% of design capacity for the remainder of the month.

As of May 11, 2016, 67,357 ounces of gold have been produced, and 60,703 ounces of gold have been soldat an average price of $1,240 per ounce (including deliveries under the hedge contracts entered into inconnection with the Company’s Credit Agreement, as discussed in “Debt Financing”). Sales of gold prior toachieving commercial production are offset against the construction costs for the ELG Mine.

6

Initially, the ramp-up at the processing plant started with 6 of 11 leach tanks available, and 5 of the 7 tailingfilters in operation. During the first quarter, production volumes increased, and the remaining leach tanksand tailing filters were placed into service. The tailings filtration plant is delivering the expected productfor dry stack disposal and tailings filtration throughput has been steadily increasing as processes and filtercloth selection are optimized.

Leached copper initially presented a challenge to efficient gold elution and electrowinning steps during theearly ramp-up stage with copper levels in solution reaching 1000 parts per million (ppm). Adjusting the freecyanide concentration and the introduction of a cold wash cycle have resulted in the copper levels returningto design background levels. Evaluation efforts are in progress to determine if mitigation actions need tocontinue.

Gold recovery levels varied through February and March trending higher overall as the plant response todiffering concentrations of reagents was tested. Design level recoveries are 87.4%. Recovery levels averaged81% for March but reached as high as 90.7% in the last week of March. Recovery levels averaged 85% inApril following the re-start of operations.

Commercial Production

With the construction of the ELG Mine close to completion and the ramp-up of the plant progressing aheadof schedule, the Company announced on March 30, 2016, that commercial production had been achieved,one quarter ahead of schedule.

Commercial production signals the transition for a project from the development phase into the productionphase. Although commercial production was announced in March 2016, for accounting purposes, thistransition will be reflected as of April 1, 2016 and the Company will begin recognizing revenue and operatingcosts, including depreciation, and reporting operating measures such as total cash costs and all-in sustainingcosts, as defined by standards published by the World Gold Council.

Mining

Mining recommenced as planned at the Guajes pit in January 2016. At El Limón, activities focused on pitpre-stripping and the completion of the haul road to the El Limón crusher which was completed ahead ofschedule. At March 31, 2016, there were 1.0 million tonnes of ore stockpiled, consisting of 0.6 milliontonnes from Guajes and 0.4 million tonnes from North Nose.

Construction Progress

Engineering, procurement, and construction management (“EPCM”) activities by M3 Engineering &Technology Corporation (“M3”) continued during the first quarter of 2016. Overall construction progresswas at approximately 99.5% at the end of March. After March 31, 2016, remaining EPCM activities focusedon project close-out and transitioning final responsibilities.

7

Milestones achieved in 2016 to date include the following:• The mine haul road to the El Limón crusher was completed.• Commissioning of the El Limón crusher and RopeCon commenced in March and were completed

in April 2016.• The resettlement of the Real del Limón village was completed in April 2016.

Estimated Expenditures for the ELG Mine

Total project costs for the ELG Mine were approximately $790 million. Total cash spent to March 31, 2016was $743.5 million.

The following summarizes the cash spent on the development of the ELG Mine as at March 31, 2016:• $145.9 million had been spent on Mine Capital, which includes costs for the acquisition of mining

equipment, the development of haul roads and pre-production stripping of the open pits. • $516.4 million had been spent on Process Plant Capital, which includes costs in connection with the

acquisition of process plant equipment, materials and labour to erect the process plant and relatedinfrastructure and EPCM fees to oversee the construction period, and the resettlement of two villages.

• $81.2 million had been spent on Owner’s Costs, which includes costs in connection with the Company’sproject team, insurance, and certain land lease costs.

Safety

From the start of construction to the end of March 31, 2016, 15.3 million hours have been worked on theELG Mine, with a total of eight lost time accidents. In March 2016, a contractor was fatally injured in a singlevehicle accident, while commuting to the worksite. While this is not an ‘on the job’ accident, the Companyhas taken appropriate actions to assist the family, and continues to actively promote safe practices bothon and off the job.

Community

In April 2016, the Company temporarily suspended operations at the ELG Mine due to an illegal blockadeinitiated by three families and the Citizen’s Committee demanding unjustified payments for allegedenvironmental damages. The Company refuted the claims made and refused to make payments to thoseengaging in the illegal blockade. The blockade was lifted on April 14, 2016. The State Government, whichwas involved in the mediation with the blockaders, agreed to lead the studies to assess whether the claimsmade are attributable to the Company’s activities. Reports and studies to date, both by the Governmentand the Company, support the Company’s position that the Company remains in compliance with itsenvironmental approvals.

The Company remains committed to continuing to work with communities to maintain an environmentthat ensures the uninterrupted operation of the mine.

8

Security

In February 2016, the Company signed an agreement with the Ministry of Public Safety of the StateGovernment of Guerrero (the “Ministry”), endorsed by the Federal Government, for the provision ofpermanent police and military presence in the areas adjacent to the Company's Morelos Gold Property. Inthe first stage under this agreement, the Ministry has established two check points with permanent policeand military presence which, along with regular patrols, will improve security for the communities in theareas adjacent to the ELG Mine. The Media Luna Project will receive some security benefits from this pilotprogram, with more comprehensive coverage planned for later in this program and in future programs. TheCompany will support the program with infrastructure including lodging for the police and military forces,and additional support in the form of transportation and vehicle maintenance. The program came intoeffect immediately upon the signing of the agreement, and may be renewed on a yearly basis by agreementof the parties.

The Company also continues to provide private security at the ELG Mine and satellite installations such asthe permanent camp.

9

2016 Life of Mine Plan

In May 2016, the Company completed a Life of Mine (“LOM”) plan update for ELG on a standalone basis.As previously reported, the Company was investigating the location of post-mineralization dike intrusions,and the potential effect of these intrusions on the resource estimate. The updated LOM plan incorporatesthe results of this recent work. The LOM is now projected to be 8.5 years, a decrease from the previousestimate of 10 years, and the projected gold production over the first 7 years of the LOM is expected to becomparable to the first 7 years of the previous standalone life of mine plan. See table below “EstimatedGold Sales by Year”.

While there is some depletion recognized in the new reserve estimate, the majority of the decrease comesas a result of new interpretations regarding the mineralization of dikes that cross cut the deposit. In theprevious resource estimate all intrusive dikes were considered to be mineralized. The age dating work donefor Media Luna has indicated that intrusive dikes came at different times and have slightly differentcompositions. The dikes that came before the mineralizing event could carry gold, but those that cameafter the mineralizing event were barren.

Utilizing this new knowledge of the composition of the various intrusive events, all ELG core was re-loggedto identify which dikes were post mineralization. A small drill program was also conducted to test the newinterpretation. The tonnes contained in the post mineralizing event dikes were then removed from theresource estimate, resulting in the decrease in reserves.

Another interesting interpretation that came from the re-logging effort, was that the El Limón deposit sitson top of an intrusive sill (the “Sill”). The chemical conditions that allowed the gold to deposit above theSill also exist below the Sill. Four of six holes that pierced the Sill produced grades and thicknesses that havethe potential to be economic. This area will be investigated with a drill program in the near future and hasupside potential for the operation. Another area with upside potential is the deeper mineralization thatextends at depth underneath the existing final pit shell for the El Limón pit. Options to develop a ramp intothis area are being identified now. If some or all of the mineralization can support mineral resourceestimation and eventual conversion to mineral reserves, there may be potential to extend the operatingmine life for El Limón. The Media Luna Project also provides options to keep the processing plant operatingwell into the future. These near term exploration programs will provide additional information that willhelp form the decisions to be made on how best to extend the mine life.

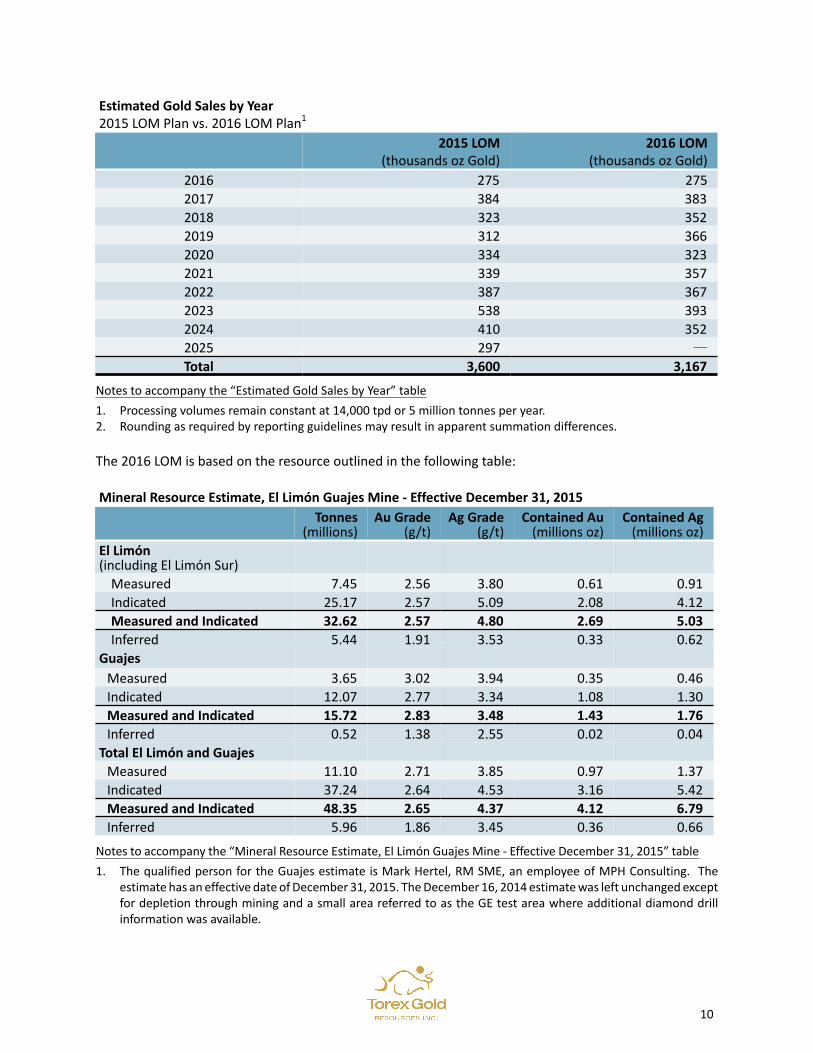

Estimated Gold Sales by Year2015 LOM Plan vs. 2016 LOM Plan1

2015 LOM(thousands oz Gold)

2016 LOM(thousands oz Gold)

2016 275 2752017 384 3832018 323 3522019 312 3662020 334 3232021 339 3572022 387 3672023 538 3932024 410 3522025 297 —Total 3,600 3,167

Notes to accompany the “Estimated Gold Sales by Year” table

1. Processing volumes remain constant at 14,000 tpd or 5 million tonnes per year.2. Rounding as required by reporting guidelines may result in apparent summation differences.

The 2016 LOM is based on the resource outlined in the following table:

Mineral Resource Estimate, El Limón Guajes Mine - Effective December 31, 2015Tonnes

(millions)Au Grade

(g/t)Ag Grade

(g/t)Contained Au

(millions oz)Contained Ag

(millions oz)El Limón (including El Limón Sur)

Measured 7.45 2.56 3.80 0.61 0.91Indicated 25.17 2.57 5.09 2.08 4.12Measured and Indicated 32.62 2.57 4.80 2.69 5.03Inferred 5.44 1.91 3.53 0.33 0.62

GuajesMeasured 3.65 3.02 3.94 0.35 0.46Indicated 12.07 2.77 3.34 1.08 1.30Measured and Indicated 15.72 2.83 3.48 1.43 1.76Inferred 0.52 1.38 2.55 0.02 0.04

Total El Limón and GuajesMeasured 11.10 2.71 3.85 0.97 1.37Indicated 37.24 2.64 4.53 3.16 5.42Measured and Indicated 48.35 2.65 4.37 4.12 6.79Inferred 5.96 1.86 3.45 0.36 0.66

Notes to accompany the “Mineral Resource Estimate, El Limón Guajes Mine - Effective December 31, 2015” table

1. The qualified person for the Guajes estimate is Mark Hertel, RM SME, an employee of MPH Consulting. Theestimate has an effective date of December 31, 2015. The December 16, 2014 estimate was left unchanged exceptfor depletion through mining and a small area referred to as the GE test area where additional diamond drillinformation was available.

10

2. The qualified person for the El Limón estimate is Edward J. C. Orbock III, RM SME, an Amec Foster Wheeleremployee. The estimate has an effective date of December 31, 2015.

3. The qualified person for the El Limón Sur area within the El Limón estimate is Mark Hertel, RM SME, an employeeof MPH Consulting. The estimate for the El Limón Sur area has an effective date of August 6, 2014.

4. Mineral Resources are reported above a 0.5 g/t Au cut-off grade.5. Mineral Resources are reported as undiluted; grades are contained grades. 6. Mineral Resources are reported within a conceptual open pit shell.7. Mineral Resources are reported using a long-term gold price of $1,380/oz, silver price of $21.00/oz.8. The metal prices used for the Mineral Resources estimates are based on Amec Foster Wheeler’s internal guidelines

which are based on long-term consensus prices. The assumed mining method is open pit, mining costs used are$2.60 per tonne, processing costs at $16.90 per tonne. General and administrative costs are estimated at $6.20per tonne processed.

9. Metallurgical recoveries average 87% for gold and 32% for silver.10. Assumed pit slopes range from 33 to 49 degrees.11. Rounding as required by reporting guidelines may result in apparent summation differences between tonnes,

grade, and contained metal content.12. Mineral Resources are reported using topography with mining progress as of December 31, 2015. Mining progress

applies to both El Limón and Guajes Mineral Resources. 13. The Measured and Indicated Mineral Resources are inclusive of those Mineral Resources modified to produce

the Mineral Reserves, with the exclusion of stockpiled ore which is not included within the Mineral Resource tableabove.

14. Mineral Resources were developed in accordance with CIM (2014) guidelines.

Based on the LOM, the mineral reserve estimates for the ELG Mine at the end of 2015 were as follows:

Mineral Reserve Estimate, El Limón Guajes Mine - Effective December 31, 2015

Reserve CategoryTonnes

(millions)Au Grade

(g/t)Ag Grade

(g/t)Contained Au

(millions oz)Contained Ag

(millions oz)El Limón (including El Limón Sur)

Proven 6.33 2.65 3.50 0.54 0.71Probable 20.33 2.60 4.58 1.70 2.99Proven and Probable 26.66 2.61 4.32 2.24 3.71

GuajesProven 3.56 2.85 3.75 0.33 0.43Probable 11.72 2.60 3.15 0.98 1.19Total 15.28 2.66 3.29 1.31 1.62

Mine stockpiles Proven 1.17 2.17 3.37 0.08 0.13

Total El Limón and GuajesProven 11.07 2.66 3.57 0.95 1.27Probable 32.05 2.60 4.06 2.68 4.18Total 43.11 2.62 3.93 3.63 5.45

Notes to accompany the “Mineral Resource Estimate, El Limón Guajes Mine - Effective December 31, 2015” table

1. The qualified person for the El Limón and Guajes mineral reserve estimate is Victor Barua, AUSIMM member,Manager, Technical Services of Torex Gold Resources Inc.

11

2. Mineral Reserves are reported based on open pit mining within designed pits above in situ cut-off grades thatare 0.80 g/t Au for all ore types excluding Breccia ore. Breccia ore cut-off is set at 1.30 g/t Au. Mineral Reservesincorporate an estimate for dilution and mining losses. The cut-off grades and pit designs are considered for themetal price of $1,200/oz gold and $15/oz silver.

3. The table above includes stockpiled ore as at December 31, 2015.4. Mineral Reserves were developed in accordance with CIM (2014) guidelines.5. Rounding as required by reporting guidelines may result in apparent summation differences between tonnes,

grade, and contained metal content.

12

Morelos Gold Property Exploration Update

Although the Morelos Gold Property contains additional exploration potential, the Company’s efforts arecurrently focused on the operation of the ELG Mine and development of the Media Luna Project. Explorationactivities were curtailed during the first quarter of 2016.

Media Luna Project Update

The Media Luna deposit occurs primarily at the contact between Morelos formation carbonate rocks andthe El Limón granodiorite. The sedimentary rocks and their contact with the main granodiorite stock dip tothe south west at about 35 degrees. Extensive skarn alteration and mineralization formed at this contactand exhibits the same dip. Later intrusive dikes and Sills cut the deposit and its host rocks and are moreabundant in the northwestern portion of the current resource area. The mineralized zone is widely exposedat the surface in steep cliffs along the northeastern margin of the area.

Drilling shows that the large magnetic anomalies in the area are explained by the presence of massivemagnetite and magnetic pyrrhotite, which are typically associated with gold-silver-copper mineralization.In more detail, gold-silver-copper mineralization typically occurs together with sulfide minerals and a latestage of skarn alteration. A significant area of the magnetic anomalies remains untested and skarn alterationand associated gold-silver-copper mineralization remains open in several directions.

Work on the Media Luna Project during the first quarter of 2016 continued to be limited to preparation forthe underground exploration program. This work included continued environmental studies and landacquisition to support the permit application. The goal of the work is to have permits in hand and readyfor execution when the Company chooses to undertake this work as recommended in the Technical Report.

Management Change

Effective May 31, 2016, Mr. Alejandro Kakarieka, Vice President of Exploration, will be leaving the Companyto pursue other interests. Mr. Kakarieka will continue working with Torex on a consulting basis. The Companythanks Alejandro for his five years with Torex where he led the exploration team which discovered theMedia Luna deposit.

DEBT FINANCING

Loan Facility

In August 2014, the Company, through its subsidiary Minera Media Luna, S.A. de C.V. (“MML”), signed acredit agreement (the “Credit Agreement”) with BMO Harris N.A., BNP Paribas, Commonwealth Bank ofAustralia, ING Bank N.V., Société Générale, and The Bank of Nova Scotia (the “Lenders”) and other definitivedocumentation giving effect to a $375 million senior secured project finance loan (the “Loan Facility”). The

Loan Facility is comprised of two separate facilities, a project finance facility of $300 million (the “PFF”) anda cost overrun facility of $75 million (the “COF”). Advances under the PFF bear interest at a rate of LIBOR+ 4.25% to 4.75% and advances under the COF bear interest at the same rate plus 1%. The Loan Facility hasa maturity date of September 30, 2022.

In March 2015, the Credit Agreement was amended. Included in the amendment was the deferral of thestarting date for the Loan Facility’s scheduled repayments, as well as amendments to the amounts ofscheduled repayments. The amendment also addressed potential impacts that a delay in the anticipatedcommencement of production may have on certain requirements under the Loan Facility. While theCompany anticipated that first gold production would occur in the fourth quarter of 2015, certain of theamendments to the Credit Agreement were based on more conservative assumptions relating to productionschedule, capital expenditures and production ramp-up. As such, the Company placed $30.9 million in areserve account (the “Sponsor Reserve Account”) to fund the conservative assumptions. The Company isable, in the absence of the conservative assumptions occurring, to withdraw funds from the account undercertain conditions.

The amendment included adjustments to accommodate the financing impacts of a change in the plannedschedule, as well as additional conservatism in the event that the schedule for the first gold pour was tobe delayed until the first quarter of fiscal 2016.

In connection with the Loan Facility, the Company entered into commitments to deliver 204,360 ounces ofgold over an 18-month period commencing in January 2016 to the Lenders, at an average flat forward goldprice of $1,241 per ounce. The gold hedges provide price protection for the Company’s debt obligationsand represent approximately 6% of the Company’s expected total gold production from the ELG Mine. TheCompany has also executed the required foreign exchange currency hedges which cover 75% of theCompany’s non-U.S. dollar denominated capital expenditures for the ELG Mine from November 2014 tothe second quarter of 2017. An operating expenditures foreign exchange currency hedge to cover exposurefor 75%, 50% and 25% annually, on a three year rolling basis, of the Company’s non-U.S. dollar denominatedoperating expenditures for the ELG Mine, will be required during production pursuant to the CreditAgreement. The hedges are secured on an equal basis with the Loan Facility and documented in the formof International Swaps and Derivatives Association Agreements.

A copy of the Credit Agreement and amendment of the Credit Agreement were filed on August 21, 2014and March 31, 2015, respectively, and are available on SEDAR at www.sedar.com.

The Loan Facility has been fully drawn down, and the amount outstanding as at March 31, 2016 was$375.0 million. The proceeds of the Loan Facility were used to fund the development of the ELG Mine. TheLoan Facility is presented in the Statement of Financial Position at amortized cost, net of deferred financingcosts, and totalled $363.9 million as at March 31, 2016.

Further, during the first quarter of 2016, the Company met the conditions required to withdraw funds fromthe Sponsor Reserve Account, and withdrew $4.0 million. In March 2016, the Company also utilized$6.0 million from the Sponsor Reserve Account to fund expenditures for the ELG Mine.

Equipment Loan

On December 23, 2015, the Company executed a $7.6 million 4-year loan agreement with BNP Paribas (the“Equipment Loan”). The Equipment Loan, secured by certain mining vehicles that are owned by the

13

Company, is due to mature on December 31, 2019, is repayable in quarterly installments starting March31, 2016, and bears interest at a rate of LIBOR + 3.75%. The loan is carried at amortized cost on the Statementof Financial Position, net of deferred finance charges, and totalled $6.7 million as at March 31, 2016.

Finance Lease Agreement

Further, on December 31, 2015, the Company executed the Finance Lease Arrangement which provides upto $17.4 million in lease financing for mining equipment. As of March 31, 2016, the Company has utilized$6.2 million under the Finance Lease Arrangement. Advances under the Finance Lease Arrangement bearinterest at a rate of LIBOR + 4.0%, and are repayable in quarterly rent installments starting June 30, 2016.The loan is carried at amortized cost on the Statement of Financial Position, net of deferred finance charges,and totalled $6.1 million as at March 31, 2016.

14

RESULTS OF OPERATIONS

The Company is in the exploration stage at the Media Luna Project and in the ramp-up stage at the ELGMine. The expenditures directly attributable to the development of the ELG Mine have been capitalizeduntil reaching commercial production, which was announced on March 30, 2016, while evaluationexpenditures related to the Media Luna Project, exploration expenses, and other corporate activities willcontinue to be expensed. The Company commenced selling gold from the ELG Mine in February 2016, andproceeds from gold sales were offset against the costs capitalized for the ELG Mine prior to commercialproduction.

For the three months ended March 31, 2016 compared to the three months ended March 31, 2015

The net loss for the three months ended March 31, 2016 was $37.8 million ($0.05 per common share)compared to $10.7 million ($0.01 per common share) for the quarter ended March 31, 2015.

General and administrative costs totaled $2.9 million for the quarter ended March 31, 2016, in line withthose incurred in the quarter ended March 31, 2015. Although salary expenses and share basedcompensation expenses were higher in the current period, the increase was partly offset by lower consultingfees related to corporate administration. Further, as the majority of general and administrative costs areincurred in Canadian dollars, the devaluation of the Canadian dollar resulted in a lower U.S. dollar equivalent.

For the quarter ended March 31, 2016, exploration and evaluation expenditures totaled $0.8 million,compared to $3.7 million in the comparable period in 2015. The decrease year-over-year reflects a reductionin exploration activities in 2016 compared to 2015. No drilling activities were undertaken in the first quarterof 2016, compared to 5,063 metres in the prior year quarter, as part of a diamond drill program ofapproximately 11,900 meters to support an updated inferred mineral resource for the Media Luna Project.Evaluation expenditures in the first quarter of 2015 also included expenditures in relation to the PEA forthe Media Luna Project, the results of which were released in September 2015.

The Company recognized a foreign exchange loss of $1.6 million for the quarter ended March 31, 2016,compared to a gain of $1.1 million for the quarter ended March 31, 2015. As the Company holds a portionof its cash balances, accounts receivable and accounts payable in Mexican pesos or Canadian dollars, theforeign exchange gains and losses fluctuate with the value of these currencies relative to the U.S. dollar,the Company’s functional currency. A weakening Mexican peso and Canadian dollar result in a foreign

exchange loss on non-U.S. dollar denominated monetary assets, which results in a foreign exchange gainon non-U.S. dollar denominated monetary liabilities.

As described in “Debt Financing”, the Company entered into gold derivative contracts pursuant to the CreditAgreement. During the three months ended March 31, 2016, the Company recognized a realized gain of$0.2 million with respect to the gold derivative contracts settled in the quarter. Contracts that remainoutstanding at the end of the reporting period are marked-to-market as they are considered non-designatedhedges. Based on the forward prices for gold at March 31, 2016, the Company recognized an asset of $0.5million as at March 31, 2016 (December 31, 2015 - $34.4 million). As a result, the Company recognized anunrealized loss of $33.9 million for the quarter ended March 31, 2016 compared to $1.7 million for thequarter ended March 31, 2015, reflecting the increase in gold prices in the first quarter of 2016.

With respect to the currency derivative contracts, the Company recognized a realized loss of $4.2 millionin the quarter ended March 31, 2016 in relation to contracts settled during the period. Similar to the goldcontracts, currency contracts that remain outstanding as at March 31, 2016 are marked-to-market at eachreporting period. The resulting liability as at March 31, 2016 totalled $1.9 million, compared to $5.6 millionas at December 31, 2015, reflecting fewer contracts outstanding.

The Company recognized a deferred income tax recovery of $1.9 million in the quarter ended March 31,2016, compared to a deferred tax expense of $0.3 million for the quarter ended March 31, 2015. Deferredincome tax recovery or expense reflects the change in the deferred income tax liability relating to theMexican mining royalty for the decommissioning liability of the ELG Mine and the Company’s unrealizedgain or loss on the gold derivative contracts, deferred withholding taxes, as well as the impact the foreignexchange rate fluctuations have on the tax base of the Company’s exploration and evaluation tax pools. Forthe three months ended March 31, 2016, the change in deferred tax liability was primarily due to thedecrease in the marked-to-mark gold derivative asset.

15

SUMMARY OF QUARTERLY RESULTS

Quarterly Results for the Eight Most Recently Completed Quarters

in millions, exceptper share amounts

2016 2015 2014

Mar 31 Dec 31 Sept 30 Jun 30 Mar 31 Dec 31 Sept 30 Jun 30

Operatingrevenues

$ — $ — $ — $ — $ — $ — $ — $ —

General & administrative 2.9 3.8 2.8 2.7 2.9 4.5 3.0 3.6

Exploration and evaluation 0.8 1.6 1.7 2.7 3.7 5.5 1.8 0.6

Net loss (gain) $ 37.8 (0.1) $ 4.8 $ 9.2 $ 10.7 $ 15.7 $ 1.1 $ 6.2

Basic and diluted loss per share $ 0.05 $ 0.00 $ 0.01 $ 0.01 $ 0.01 $ 0.02 $ 0.00 $ 0.01

The net loss (gain) in all quarters includes costs for exploration, evaluation, corporate general andadministrative cost, unrealized gains and losses on derivative contracts, and foreign exchange gains andlosses. The net loss (gain) also includes derivative gains and losses and financing costs starting in the fourthquarter of 2014.

The Company’s policy is to expense all mineral property exploration and evaluation costs when incurredand to capitalize its development expenditures. Exploration expenditures, include drilling, sampleprocessing, road maintenance, water consumption, security, and personnel costs. In 2016, no drillingprograms were undertaken, as the Company’s focus remained on the ramp-up and operation of the ELGMine. In 2015, exploration and evaluation expenditures were highest in the first and second quarters, asthe Company completed two drilling programs, one of which totalled approximately 11,900 metres tosupport an updated inferred resource for Media Luna, which was released in September 2015 in conjunctionwith the Media Luna Project PEA. The second program related to a 1,733-metre in-fill drilling program inthe El Limón East area within the El Limón resource. In 2014, exploration and evaluation expenses werelower in the second and third quarters of 2014, as the Company suspended the drilling program at the ELGMine and the Media Luna Project from April to October 2014.

Corporate general and administrative expenses, which include depreciation on corporate assets, remainedrelatively consistent for the eight most recent quarters. In general, performance based bonuses for theCompany’s executive team and corporate employees are accrued in the last quarter of every year.

Share-based compensation expense and salaries and benefits varied during the eight most recent quarters.Share purchase options generally vest over a two-year term with one third of the options vestingimmediately and one third vesting on each of the two subsequent anniversary dates. The related expenseis based on the vesting dates, with one third of the expense recorded immediately, one third of the expenseamortized equally over the first year, and one third of the expense amortized equally over two years.Restricted share units are expensed from the issue date over the vesting period. As a result, quarterly sharebased compensation expense was the greatest during the quarters in which options were granted. Sharebased compensation expenses were higher in 2014 than in 2015 as fewer options and restricted share unitswere issued in 2015 than in 2014. The decrease in the number of share based awards in 2015 comparedto 2014 is due to the fact that long-term incentive awards for directors and certain executives were notgranted in 2015, and are expected to be issued in 2016. The related expense will be recognized over thevesting period.

Further, the majority of expenses related to salaries, benefits and share-based compensation aredenominated in Canadian dollars. A weakening of the Canadian dollar has resulted in lower U.S. dollarequivalent amounts year-over-year.

In October 2014, in connection with the Loan Facility, the Company entered into gold and currency hedgecontracts, which are marked-to-market at every reporting period as they are considered non-designatedhedges. The gain or loss relating to these contracts fluctuates with the price of gold and the Mexican pesoexchange rate relative to the U.S. dollar, respectively.

The Company holds cash balances in both Canadian dollars and Mexican pesos in addition to its U.S. dollarholdings. The Company also has VAT receivables denominated in Mexican pesos. The foreign exchange gainsand losses for the eight quarters fluctuate with the movement of the Canadian dollar and Mexican pesoexchange rate relative to the U.S. dollar.

16

LIQUIDITY AND CAPITAL RESOURCES

As noted in “Results of Operations”, the Company commenced selling gold from the ELG Mine in February2016, and announced that the ELG Mine had achieved commercial production on March 30, 2016. Inaddition to proceeds from gold sales, sources of funding include VAT refunds, funds in the Sponsor ReserveAccount, debt, such as the Finance Lease Arrangement, as well as proceeds from stock option exercises.

The total assets of the Company as at March 31, 2016 were $1,106.2 million (December 31, 2015 -$1,121.0 million), which includes $30.5 million in cash and cash equivalents (December 31, 2015 -$46.1 million), excluding restricted cash of $34.6 million (December 31, 2015 - $44.6 million). The Companyhad working capital of $3.7 million as at March 31, 2016, compared to $56.7 million at December 31, 2015.

Cash flow used in operating activities, including changes in non-cash working capital, for the quarter endedMarch 31, 2016 totaled $8.8 million, compared to $0.8 million for the quarter ended March 31, 2015. Theincrease in cash flows used in operations is primarily a result of the realized loss on the derivative currencycontracts of $4.2 million and the purchase of materials and supplies inventory as the ELG Mine ramps upto full production. This was partly offset by lower exploration and evaluation costs and general andadministrative expenses.

Investing activities resulted in cash outflows of $6.4 million for the quarter ended March 31, 2016, comparedwith cash outflows of $103.6 million for the quarter ended March 31, 2015. In both periods, the outflowsinclude the purchase of equipment and the capitalization of expenditures directly related to thedevelopment of the ELG Mine, as well as capitalized borrowing costs of $5.6 million in the three monthsended March 31, 2016 (March 31, 2015 - $2.1 million). Cash flows generated from investing activities inthe three months ended March 31, 2016 include proceeds from pre-production gold sales, which totalled$38.7 million (excluding proceeds from deliveries under derivative contracts), collections of $9.9 million inVAT refunds, excluding interest, partly offsetting the increase in VAT paid of $8.3 million relating toconstruction activities. In comparison, in the first quarter of 2015, the Company had no gold sales as theELG Mine was still in the construction phase. VAT collections in the first quarter of 2015 of $11.1 millionwere almost entirely offset by VAT paid in that quarter.

Financing activities resulted in cash outflows of $1.0 million for the quarter ended March 31, 2016,compared with net inflows of $109.5 million for the quarter ended March 31, 2015. Cash flows fromfinancing activities in the first quarter of 2016 relate primarily to the first rent installment of $0.5 millionon the Company’s Equipment Loan. In comparison, the first quarter of 2015 included $110.0 million indraws from the Loan Facility.

As discussed under “Debt Financing,” an amendment to the Loan Facility was completed in March 2015,pursuant to which the Company funded the Sponsor Reserve Account, which was reflected as an investingcash outflow of $30.1 million. With the Company producing its first gold on schedule in the fourth quarterof 2015, some of the concerns relating to the progress of the project were alleviated. In February 2016, theCompany met the conditions required to withdraw from the Sponsor Reserve Account, and $4.0 millionwas released to fund future corporate expenditures. In March 2016, $6.0 million was used from the SponsorReserve Account to fund ELG Mine exenditures. These withdrawals from the Sponsor Reserve Account werereflected in investing activities in the three months ended March 31, 2016.

Furthermore, the Loan Facility is subject to an Interim and Final Completion Test (“ICT” and “FCT”) requiringthe Company to meet certain operational, legal and financial criteria. The deadline for completion of the

17

ICT and FCT is September 30, 2016 and March 31, 2018, respectively. Inability to achieve either the ICT orFCT constitutes an event of default under the Loan Facility, unless a waiver or amendment to the Facility isobtained. The Company is also restricted from repatriating funds from MML until the FCT has been achieved,which the Company believes will occur in mid-2017.

As at March 31, 2016, the Company’s contractual obligations included a head office lease agreement, officeequipment leases, long-term land lease agreements with the Rio Balsas, the Real del Limón, and the ValerioTrujano Ejidos and the individual owners of land parcels within certain of those Ejido boundaries, a five-year exploration access agreement with the Puente Sur Balsas Ejido, and contractual commitments relatedto the ongoing construction of the ELG Mine. All of the long-term land lease agreements and the explorationagreement can be terminated at the Company’s discretion at any time without penalty. The five-yearexploration access agreement includes access to the new discoveries at the Media Luna Project. Theseagreements are not included in the contractual commitments reported below. In addition, the Companyhas entered into several exploration-related agreements, all of which are cancellable within a year at theCompany’s discretion. The Company has entered into development-related agreements for the ELG Minethat extend through 2016.

Contractual Commitments (in thousands)

Contractual Obligations Payments Due by Period

TotalLess than

1 year 1-3 years 4-5 yearsGreater than

5 years

Long-term leases $ 695 $ 129 $ 486 $ 80 $ —

ELG Mine commitments 61,813 61,796 17 — —

Debt 388,282 2,988 67,059 164,973 153,262

Total $ 450,790 $ 64,913 $ 67,562 $ 165,053 $ 153,262

18

ECONOMIC TRENDS AND LIQUIDITY AND CAPITAL RESOURCES OUTLOOK

As at March 31, 2016, the total amount spent on the development of the ELG Mine was $744 million. Theremaining costs to complete are expected to be funded through the Company’s existing cash resources,proceeds from gold sales, funds from the collection of VAT receivables, undrawn amounts under the FinanceLease Arrangement, restricted cash reserves, and other financing options, if necessary.

The average trading price of a troy ounce of gold for the quarter ended March 31, 2016 was $1,183,compared to $1,219 for the quarter ended March 31, 2015, representing a decrease of 3% year over year.The market price of gold continues to exhibit significant volatility. Proceeds from gold sales will be impactedby fluctuations in the price of gold.

The average exchange rate of the Mexican peso relative to the U.S. dollar for the quarter ended March 31,2016 was 18.07 pesos, compared to 14.95 pesos for the quarter ended March 31, 2015, representing adevaluation of 21% year over year. The Mexican peso continues to exhibit significant volatility. The valueof the Mexican peso relative to the U.S. dollar will impact the valuation and financial models of the ELGMine, as well as the value of monetary assets and liabilities denominated in Mexican pesos.

OFF-BALANCE SHEET ARRANGEMENTS

The Company does not have any off-balance sheet arrangements.

FINANCIAL RISK MANAGEMENT

The Company examines the various financial risks to which it is exposed and assesses the impact andlikelihood of those risks. These risks include credit risk, liquidity risk, foreign currency risk and interestrate risk.

Credit risk

Credit risk is the risk of a loss associated with a counterparty’s inability to fulfill its contractual paymentobligations. The Company’s financial assets are primarily composed of cash and cash equivalents, restrictedcash, derivative contracts and VAT receivables. To mitigate exposure to credit risk, the Company has adoptedstrict investment policies, which prohibit any equity or money market investments. All of the Company’scash, cash equivalents, restricted cash and derivative contracts are with reputable financial institutions,and as such, the Company does not consider its credit risk on these balances to be significant as at March 31,2016.

Liquidity risk

Liquidity risk is the risk that the Company will not have sufficient cash resources to meet its financialobligations as they come due. The Company has a history of operating losses during the exploration anddevelopment stages and has traditionally obtained cash from its financing activities and as a result theCompany’s liquidity may be adversely affected if the Company’s access to the capital market is hindered,whether as a result of a downturn in stock market conditions generally or related to matters specific to theCompany. In the opinion of management, the Company’s working capital balance, collection from VATreceivables, proceeds from gold sales, undrawn amounts on the Finance Lease Arrangement, and funds inthe Sponsor Reserve Account will be sufficient to sustain operations and corporate activities.

The Company’s approach to managing liquidity risk is to ensure that it will have sufficient liquidity to meetliabilities when due. At March 31, 2016, the Company had cash balances of $30.5 million (excludingrestricted cash of $34.6 million) (March 31, 2015 – cash balance of $46.1 million, excluding restricted cashof $44.6 million). The Company maintains its cash in fully liquid business accounts.

During the three months ended March 31, 2016, the Company drew down a total of $6.2 million from itsFinance Lease Arrangement to finance certain mining equipment. As at March 31, 2016, the amountsoutstanding under the Loan Facility, Equipment Loan, and Finance Lease Arrangement totalled$375.0 million, $7.1 million and $6.2 million, respectively.

As discussed in “Liquidity and Capital Resources”, under the terms of the Credit Agreement, the Companyis restricted from repatriating funds from MML until the FCT has been achieved, which the Company expectswill occur in mid-2017. In addition, there can be no assurance that the Company will be able to recover allor parts of the amount remaining in the Sponsor Reserve Account.

Cash flows that are expected to fund the ELG Mine and settle current liabilities are dependent on, amongother things, proceeds from gold sales and recovery of the Company’s VAT receivables. The Company isexposed to liquidity and credit risk with respect to its VAT receivables if the Mexican tax authorities areunable or unwilling to make payments in a timely manner in accordance with Company’s monthly filings.Timing of collection on VAT receivables is uncertain as VAT refund procedures require a significant amountof information and follow-up. As at March 31, 2016, the Company expects to recover $28.1 million overthe next twelve months and a further $21.2 million thereafter. Significant delays in the collection of VAT

19

receivables may affect the Company's ability to fund the operation of the ELG Mine and settlement of theCompany’s current liabilities. The Company’s approach to managing liquidity risk with respect to its VATreceivables is to file its refund requests on a timely basis, monitor actual and projected collections of itsVAT receivables, and cooperate with the Mexican tax authorities in providing information as required.Although the Company expects a full recovery, there remains risk on the amount and timing of collectionof the Company’s VAT receivables, which may affect the Company’s liquidity and ability to fund otherpriorities.

The Company regularly evaluates its cash position to ensure preservation and security of capital as well asmaintenance of liquidity.

Commodity Price Risk

Gold prices have fluctuated widely in recent years and the market price of gold has decreased significantlysince 2013. There is no assurance that, even as commercial quantities of gold may be produced in thefuture, a profitable market will exist for them. Under requirements from the Loan Facility, the Companyentered into commitments to deliver 204,360 ounces of gold over an 18-month period commencing inJanuary 2016 to the Lenders, at an average flat forward gold price of $1,241 per ounce. As at March 31,2016, there remained 187,022 ounces to be delivered under these derivative contracts. A 10% appreciationor depreciation of gold prices would result in an increase or decrease of $23.1 million (using the spot rateas at March 31, 2016 of $1,237 per ounce) in the Company’s mark to market asset relating to the derivativegold contracts.

Foreign Currency Risk

The Company is exposed to financial risk related to foreign exchange rates. The Company operates in Canadaand Mexico and has foreign currency exposure to non-U.S dollar denominated transactions. The Companyexpects a significant amount of exploration, project development, operating and decommissioningexpenditures associated with the Morelos Gold Property to be paid in Mexican pesos and U.S. dollars. Asignificant change in the currency exchange rates between the Canadian dollar and Mexican peso comparedto the U.S. dollar is expected to have an effect on the Company’s results of operations in the future periods.

As at March 31, 2016, the Company had cash and cash equivalents, amounts receivable, VAT receivables,accounts payable and accrued liabilities and income tax payable that are in Mexican pesos and in Canadiandollars. As at March 31, 2016, a 10% appreciation or depreciation of the Mexican peso and Canadian dollarrelative to the U.S. dollar would have resulted in a decrease or increase of $4.1 million and $0.7 million inthe Company’s net loss for the period, respectively.

Under requirements from the Loan Facility, the Company has hedged its exposure to foreign currencyexchange fluctuations through the execution of foreign exchange currency contracts which cover 75% ofthe Company’s non-U.S. dollar denominated capital expenditures from November 2014 to the secondquarter of 2017. An operating expenditures foreign exchange currency contract to cover exposure for 75%,50% and 25% annually, on a three year rolling basis, of the Company’s non-U.S. dollar denominated operatingexpenditures for the ELG Mine, will be required following during production. As at March 31, 2016, a 10%appreciation or depreciation of the Mexican peso relative to the U.S. dollar would have resulted in a decreaseor increase of $0.6 million (using the spot rate as at March 31, 2016 of 17.4015 Mexico peso per U.S. dollar)in the Company’s net loss for the period.

20

Interest Rate Risk

Interest rate risk is the risk that the future cash flows of a financial instrument or its fair value will fluctuatebecause of changes in market interest rates. Amounts outstanding under the PFF of the Loan Facility bearinterest at a rate of LIBOR + 4.25% to 4.75% and advances under the COF bear interest at the same rate+ 1% until project completion, while amounts outstanding under the Equipment Loan and Finance LeaseAgreement bear interest at a rate of LIBOR + 3.75% and LIBOR + 4.0%, respectively. As at March 31, 2016,a 100 basis point change in the LIBOR rate would result in a $3.9 million change per annum in interestexpense. The Company has not entered into any agreements to hedge against unfavourable changes ininterest rates.

The Company deposits cash in fully liquid business bank accounts with reputable financial institutions. Assuch, the Company does not consider its interest rate risk exposure to be significant at March 31, 2016 withrespect to its cash and cash equivalent positions.

21

TRANSACTIONS WITH RELATED PARTIES

Certain key management personnel of the Company purchased refined gold from the Company’s first goldpour at the prevailing gold market prices. Total sales to key management personnel for the three monthsended March 31, 2016 amounted to $51 thousand.

OUTSTANDING SHARE DATA

Table 4: Outstanding Share Data at May 11, 2016

NumberCommon shares 786,961,118Share purchase options 1 21,473,324

Restricted share units 2 2,302,941

1. Each share purchase option is exercisable into one common share of the Company.2. Each restricted share unit is redeemable into one common share of the Company.

For the quarter ended March 31, 2016, the Company granted 703,876 stock options, issued 1,514,200common shares as a result of 10,528,300 stock option exercises, of which 10,508,300 were exercised underthe Company’s stock option plan’s cashless exercise option, resulting in the issuance of 1,494,200 shares.The remaining 20,000 shares were issued pursuant to regular stock option exercises.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in accordance with IFRS requires management to make estimatesand judgments that affect the reported amounts of assets and liabilities at the date of the financialstatements and reported amounts of expenses during the reporting period. Actual results could differ fromthese estimates. Revisions to accounting estimates are recognized in the period in which the estimate isrevised and the revision affects both the current and future periods.

The areas which require management to make significant judgments in applying the Company’s accountingpolicies to determine carrying values in these unaudited consolidated interim financial statements are thesame as those applied to the audited consolidated financial statements as at and for the year endedDecember 31, 2015.

RISKS AND UNCERTAINTIES

The most significant risks and uncertainties the Company faces are: the Company’s reliance on its principalassets, the ELG Mine and the Media Luna Project that form part of its 100% owned Morelos Gold Property;key issues relating to the development and exploitation of the ELG Mine, including matters pertaining tothe substantial capital requirements to complete the ELG Mine and conduct further exploration of otherproperties, operating risks safety and security of operations. Risks inherent in mineral exploration, minedevelopment and mining operations include the negative operating cash flow of the Company, risksassociated with the potential construction and start-up of a new mine, including the ability to reach fullproduction, open pit mine risks, risks of interruptions to construction or operating activities as a result ofcontractor, labour, or community demands, protests or blockades, political and country risk, foreigntaxation, the timing and receipt of the Company’s anticipated refunds of value-added taxes, recent increasesin demand for and cost of mining contract services and equipment, availability of all applicable permits andlicenses and adequate infrastructure, risks associated with land title, reliability of mineral resource andreserve estimates, environmental risks and hazards, the absence of history of mineral production by theCompany, dependence on key executives and employees, competition within the industry, exchange ratefluctuations, the absence of any hedging policy by the Company, litigation and insurance risks, volatility ofthe market price of the common shares of the Company, limitations under the Loan Facility, EquipmentLoan and Finance Lease Agreement, liquidity of parent company, potential conflicts of interest with directorsand officers, dilution risk, risks associated with compliance with anti-corruption laws and enforcement oflegal rights under the laws of Mexico and Canada, no certainty of economically viable mining operations,volatility and fluctuations in gold prices, and the volatility of global markets, the impact of which is to causevolatility in the Company’s stock price and may have a resulting effect on the Company’s ability to obtainand secure financing if required. For a detailed description of risks and uncertainties refer to the Company’smost recent annual information form, which is available on SEDAR at www.sedar.com. See also “CautionaryNote Regarding Forward-Looking Statements.”

Reliability of Resource and Reserve Estimates

The Company completed an updated LOM plan for the ELG Mine in May 2016, the details of which areincluded herein. There can be no assurance that the estimates in the Company’s life of mine plan will beconsistent with future economic factors or actual results and performance. A decline in net cash flow mayalso require the Company to record an impairment charge against the carrying value of its net assets.

The mineral resources contained in this MD&A are estimated quantities of measured, indicated and inferredmineral resources. The mineral reserves contained in this MD&A are estimated quantities of proven andprobable mineral reserves that can be mined legally and economically and processed by extracting theirmineral content under current conditions and conditions anticipated in the future. The Company determinesthe amount of its mineral resources and mineral reserves according to the regulatory requirements thatapply and following established mining standards.

There are numerous uncertainties inherent in estimating mineral resources and mineral reserves, includingmany factors beyond the Company’s control. Such estimation is a subjective process and the accuracy ofany mineral resource or mineral reserve estimate is a function of the quantity and quality of available data,the assumptions made and judgments used in engineering and geological interpretation. Mineral resourceand mineral reserve estimates are also uncertain because they are based on limited sampling and not theentire ore body. In addition, there can be no assurance that gold or silver recoveries in small scale laboratorytests will be duplicated in larger scale tests under on-site conditions or during production. There is no

22

assurance that the estimated amount of mineral reserves will be recovered or that such minerals will berecovered at costs that the Company assumed in determining such mineral reserves.

As the Company gains more knowledge and understanding of an ore body through on-going explorationand mining activity, the mineral resource and mineral reserve estimates may change significantly, eitherpositively or negatively. In particular, results of drilling, metallurgical testing, production, the evaluation ofmine plans and fluctuations in gold or silver prices subsequent to the date of any estimate may requirerevisions of such estimate. Any material reductions in mineral resource or mineral reserve estimates or ofthe Company’s ability to extract the mineral reserves could have a material adverse effect on the Company’sresults of operations and financial condition.

Security Risks in the State of Guerrero

As noted previously, the ELG Mine and the Media Luna Project are located in the State of Guerrero, Mexico.Criminal activities in the region, or the perception that activities are likely, may disrupt the Company’soperations, hamper the Company’s ability to hire and keep qualified personnel and impair the Company’saccess to sources of capital.

Social acceptance remains strong and supportive of the ELG Mine, however, throughout the constructionperiod, there were blockades that were normally short-lived. The blockades were not supported by thecommunity at large and were quickly resolved with the assistance of mediation by the state government.In April 2016, there was an illegal blockade of the ELG Mine that lasted two weeks. This was lifted followingmediation by the Company and the intervention of the state government.

Of larger significance to the construction workforce was the violence initiated by the municipal police inSeptember 2014 in the City of Iguala against protesting students about 60 km from the ELG Mine site.Municipal police fired on protesting college students, killing six and then abducting another 43. Thosestudents have not been seen since. The incident resulted in national and international outcry and the federalgovernment responded by taking over the policing of the City of Iguala and some other municipalities inGuerrero.

In February 2015, the Company received information that 12 community members, from the vicinity of theELG Mine, had gone missing from the public highway to Cocula, in the State of Guerrero, and possibly fromthe public waterways. It was encouraging to see the rapid progress made by the army and community policein recovering ten of the missing community members. Within the following two weeks the other two missingcommunity members were returned to their families. The army has continued to maintain a presence inthe area. The Company shut down construction on February 7, 2015 to give the army and community policethe opportunity to conduct their operations without the complexity of project generated road traffic. Theconstruction activities were restarted on February 13, 2015.

Over the long-term, the increased presence of the federal police, state police, and army is expected toenhance the security profile of the state, but in the short term, the situation described above was unsettlingfor contract construction workers that come from other parts of the country to work on the ELG Mine.While there has been no change in the specific security environment at the ELG Mine site, some contractworkers chose to leave to work on projects in other areas. With the calm in the area over the past months,this is no longer the case and workers are more comfortable working in the area.

23

In February 2016, the Company signed an agreement with the Ministry of Public Safety of the StateGovernment of Guerrero, endorsed by the Federal Government, under which the Ministry has establishedcheck points with permanent police and military presence, along with regular patrols of the areassurrounding the Morelos Gold Property. In return, the Company provides infrastructure including lodgingfor the police and military forces, and additional support in the form of transportation and vehiclemaintenance. The program may be renewed on a yearly basis by agreement of the parties.

24

INTERNAL CONTROL OVER FINANCIAL REPORTING

The President and Chief Executive Officer and Chief Financial Officer of the Company are responsible fordesigning internal controls over financial reporting or causing them to be designed under their supervisionin order to provide reasonable assurance regarding the reliability of financial reporting and the preparationof financial statements for external purposes in accordance with IFRS. The Company’s internal controlframework was designed based on the Internal Control - Integrated Framework (2013) issued by theCommittee of Sponsoring Organizations of the Treadway Commission (“COSO”).

There was no change in the Company’s internal controls over financial reporting that occurred during thefirst quarter of 2016 that has materially affected, or is reasonably likely to materially affect, the Company’sinternal controls over financial reporting.

Disclosure Controls and Procedures

Disclosure controls and procedures have been designed to provide reasonable assurance that all relevantinformation required to be disclosed by the Company is accumulated and communicated to seniormanagement as appropriate to allow timely decisions regarding required disclosure. The Company’sPresident and Chief Executive Officer and Chief Financial Officer have concluded, based on their evaluationof the design of the disclosure controls and procedures that as of March 31, 2016, the Company’s disclosurecontrols and procedures provide reasonable assurance that material information is made known to themby others within the Company are appropriately designed.

Limitations of Controls and Procedures

The Company’s management, including the President and Chief Executive Officer and Chief Financial Officer,believe that any internal controls over financial reporting and disclosure controls and procedures, no matterhow well designed, can have inherent limitations. Therefore, even those systems determined to be effectivecan provide only reasonable assurance that the objectives of the control system are met.

QUALIFIED PERSONS

The qualified person for the Guajes estimate is Mark Hertel, RM SME, an employee of MPH Consulting.The estimate has an effective date of December 31, 2015.

The qualified person for the El Limón (excluding El Limón Sur) estimate is Edward J. C. Orbock III, RM SME,an Amec Foster Wheeler employee. The estimate has an effective date of December 31, 2015.

The qualified person for the El Limón Sur area within El Limón estimate is Mark Hertel, RM SME, anemployee of MPH Consulting. The estimate for the El Limón Sur area has an effective date of August 6, 2014.

The qualified person for the El Limón and Guajes mineral reserve estimate and estimated gold sales byyear is Victor Barua, AUSIMM member, Manager, Technical Services of Torex Gold Resources Inc. The

estimate for the El Limón and Guajes mineral reserve estimate and estimated gold sales by year have aneffective date of December 31, 2015.

Other scientific and technical information contained in this MD&A has been reviewed and approved byDawson Proudfoot, P.Eng., Vice President, Engineering of Torex Gold Resources Inc. and a Qualified Personunder NI 43-101.

25

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS