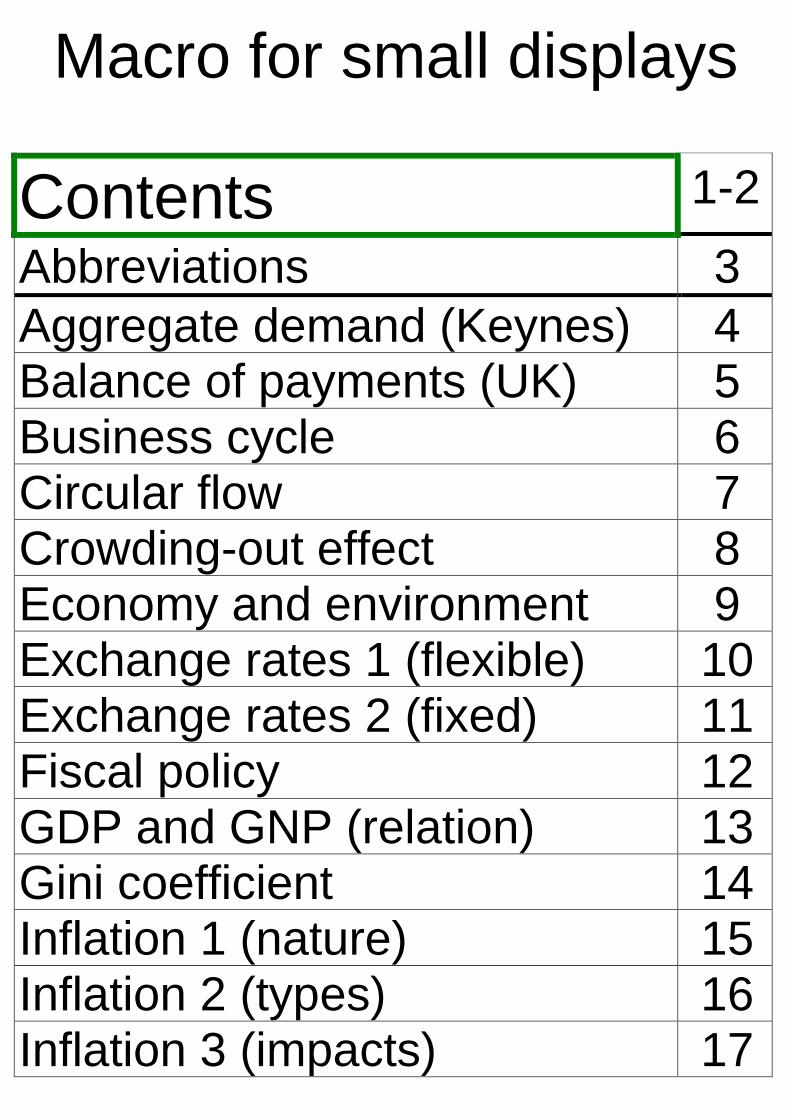

macro for small displays contents 1-2 abbreviations 3 ... · circular flow 7 crowding-out effect...

TRANSCRIPT

Macro for small displays

Contents 1-2

Abbreviations 3Aggregate demand (Keynes) 4Balance of payments (UK) 5Business cycle 6Circular flow 7Crowding-out effect 8Economy and environment 9Exchange rates 1 (flexible) 10Exchange rates 2 (fixed) 11Fiscal policy 12GDP and GNP (relation) 13Gini coefficient 14Inflation 1 (nature) 15Inflation 2 (types) 16Inflation 3 (impacts) 17

Investment demand 18Labour force 19Laffer curve 20Liquidity trap 21Lorenz curve 1 (nature, form) 22Lorenz curve 2 (redistribution) 23Monetary policy 24Money market 25Multiplier and accelerator 26Multiplier and AD 27Objectives and policies 28Paradox of thrift 29Phillips curve 30Poverty (vicious circle) 31Quantity theory of money 32Unemployment 1 (types) 33Unemployment 2 (impacts) 34Wealth (virtuous circle) 35

2012-11-01

Abbreviations

AD Aggegate demandAS Aggregate supplyC ConsumptionD DemandG Government spendingGDP Gross domestic productGNP Gross national productI Investmenti or r Interest ratesM ImportsQ Quantityr or i Interest ratesS SavingsT TaxesX ExportsY National income

2012-11-01

planned AD

Y

I + G

Aggregate demand (Keynes)

C

AD = Y

- AD = C + I + G- C = a + bY- I and G are not dependent on Y.- Y* = Equilibrium national income

AD

Y*

45o

2012-11-01

2012-11-01

Balance of payments (UK)

Trade in goods

Trade in services

Total income

Current transfers

Current balance

Errors/Omissions

Financial account

Capital account

Economic activity

Time

3

Business cycle

1

2

Recovery

Boom

Recession

Depression

4

Phase Danger

1

2

3

4

Inflation

Unemployment

2012-11-01

2012-11-01

Circular flow

HouseholdsFirms

Income

Consumer expenditure (C)

Factors of production

+ Injections I,G,X - Withdrawels S,T,M

Goods and services

Private spending

2012-11-01

Crowding-out effect

Market for loans

Interest rate

Loans

An increase in government bor-rowing causes a reduction in pri-vate spending (C or I) due to anincrease in interest rates.

Interest rate

Spending (C,I)

Supply

D1D2

2012-11-01

Factors of production

Economy and environment

NatureNature Households Firms

Goods and servicesWaste

See also: Graham Dawson, Macroeconomics,Harlow 2006, 553

2012-11-01

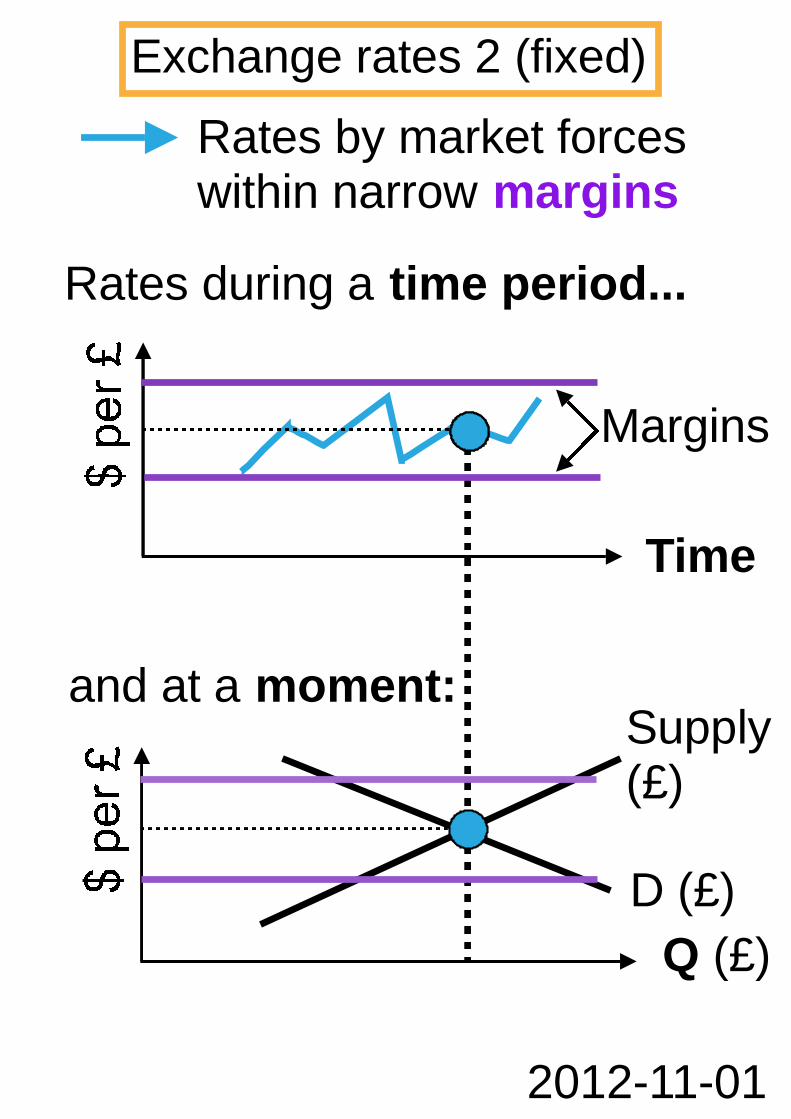

Supply(£)

Rates by market forces

Exchange rates 1 (flexible)

and at a moment:

Time

Q (£)

Rates during a time period...

D (£)

2012-11-01

Supply(£)

Rates by market forceswithin narrow margins

Exchange rates 2 (fixed)

and at a moment:

Time

Q (£)

Rates during a time period...

D (£)

Margins

2012-11-01

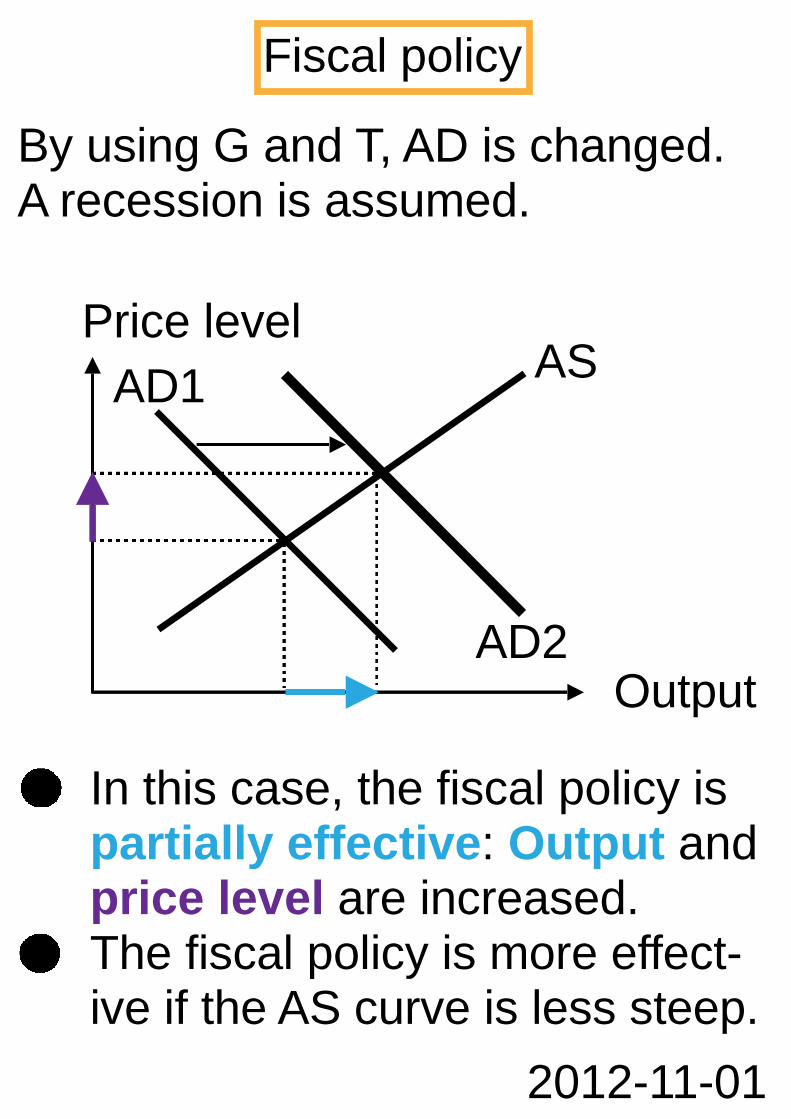

AD1

Output

Price level

By using G and T, AD is changed.A recession is assumed.

Fiscal policy

AS

In this case, the fiscal policy ispartially effective: Output andprice level are increased.The fiscal policy is more effect-ive if the AS curve is less steep.

AD2

C

NI = Net income from abroad(from labour, from investments)If NI > 0, then GDP < GNP(more income from abroadthan to abroad)If NI < 0, then GDP > GNP(less income from abroad thanto abroad)

GDP and GNP (relation)

I

G

X - M

NI

2012-11-01

Gini coefficient =Area between diagonal and LCArea ABC

LC = Lorenz curve

2012-11-01- 0 < Gini coeff. < 1

Gini coefficient

Persons (cumulative %)

100

- 100

A B

C

LC

- The Gini coefficient is a measureof (in)equality in income.

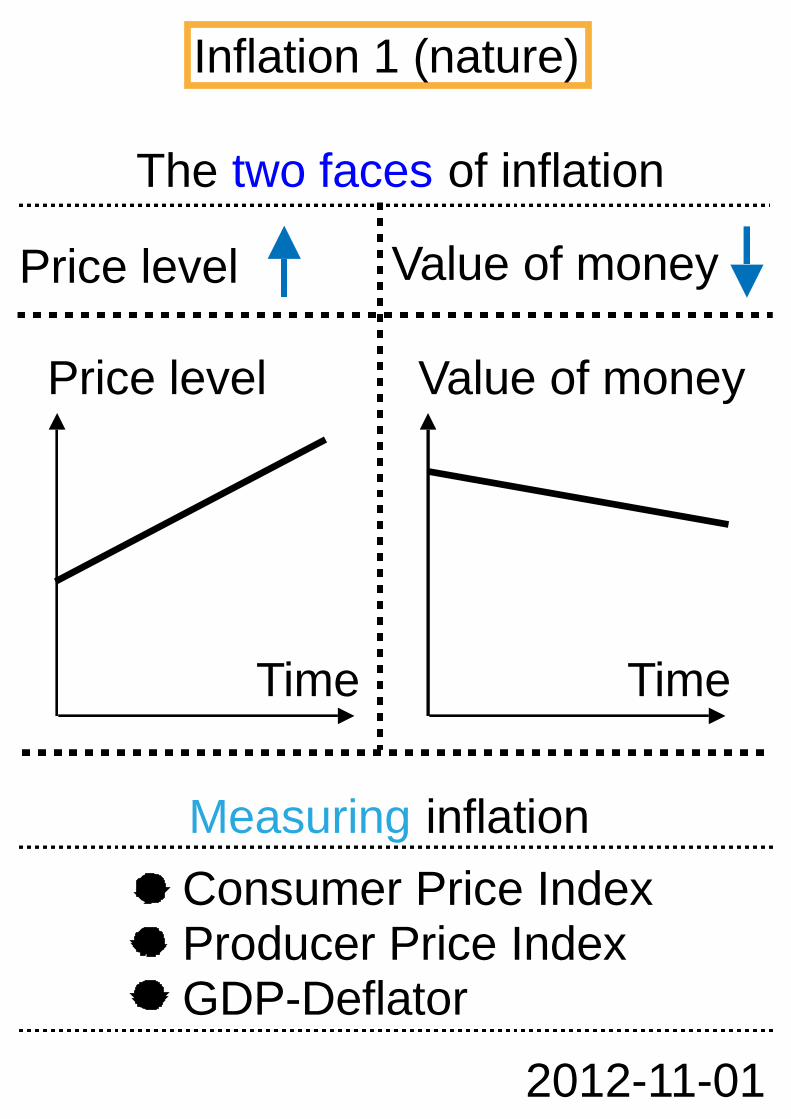

The two faces of inflation

Measuring inflation

- Consumer Price Index- Producer Price Index- GDP-Deflator

Inflation 1 (nature)

Value of moneyPrice level

Price level

Time

Value of money

Time

2012-11-01

Types of inflation

Price level

Inflation 2 (types)

Demand-pull

Example:Consumption

Cost-push

Example:Wages

GDP

AS1

AS2Price level

GDP

AS

ADAD1

AD2

2012-11-01

General impacts

If inflation is anticipated:Cost for avoiding theimpacts (time and effort)

2012-11-01

Inflation 3 (impacts)

Uncertainty

Speculation

Special impacts

If inflation is not antici-pated:Redistribution of incomeand wealth from lenders toborrowers

1

2

i

Investment demand

I D curve Change in i Shifting of D

D+

I

D

I

D

ID

I

D

I

ii

Negativerelationshipbetween i and I(ceteris paribus)

Movementalong D (ceterisparibus):

If i , then IIf i , then I

D

-

Determinants:Growth (+)Recession (-)Optimism (+)Pessimism (-)

Unemployed

1 leaving labour force

Labour force

The labour force consists of em-ployed and unemployed persons.

Employed

32

getting employed again

5

1

2

3

4

4

5

changing the job

getting unemployed

entering labour force

2012-11-01

2012-11-01

In most cases, the peak will not beat the tax rate of 50 %. Neverthe-less, total tax revenue will be low ifthe tax rate is very low or very high.

0 %

Tax rate

Laffer curve

= peak, at the tax rate of 50 %

100 %50 %

2012-11-01

r very low monetary policy ineffective

Liquidity trap

1

r

AD (C+I+G+...)InvestmentMoney market

Money

r

I

planned AD

Y

D

2

Y*1=Y*2

AD1=AD2

Supply

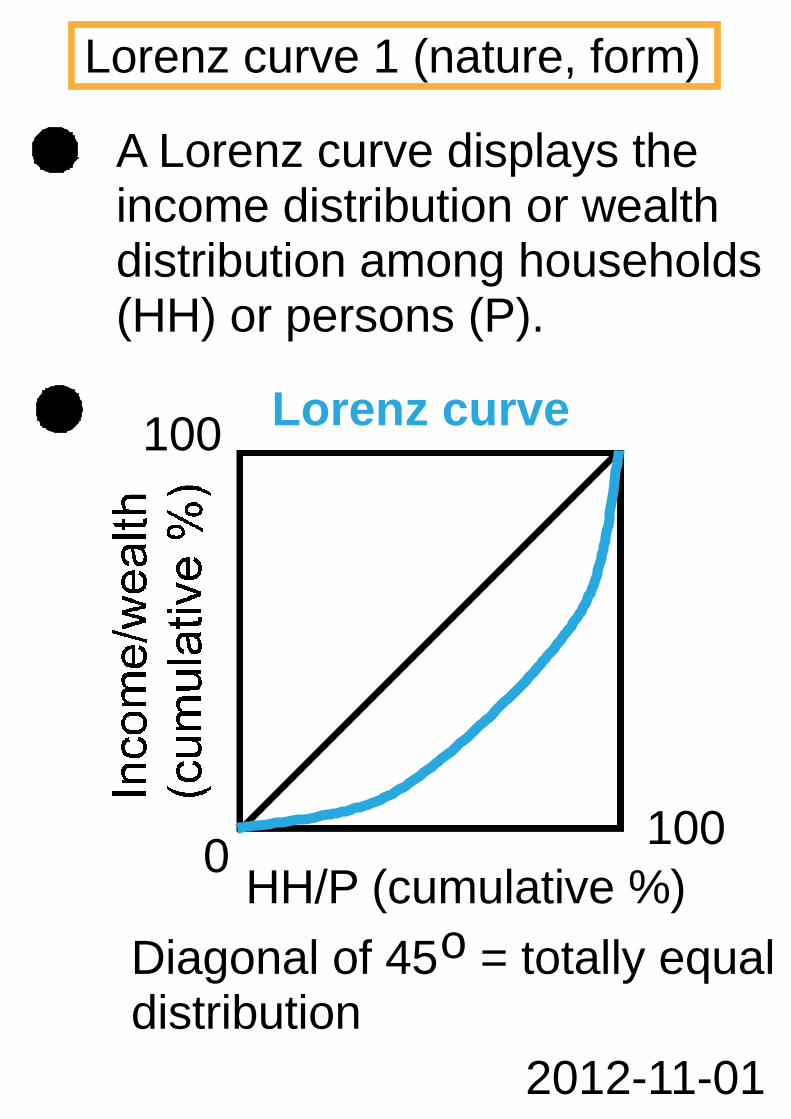

A Lorenz curve displays theincome distribution or wealthdistribution among households(HH) or persons (P).

2012-11-01

Lorenz curve 1 (nature, form)

HH/P (cumulative %)0

100

100Lorenz curve

Diagonal of 45o = totally equaldistribution

If a government redistributesincome from rich to poor, e.g. byprogressive taxes, the Lorenzcurve shifts inwards (to the left).

2012-11-01

LC1

Lorenz curve 2 (redistribution)

Persons (cumulative %)0

100

100Lorenz curve (LC)

LC2

2012-11-01

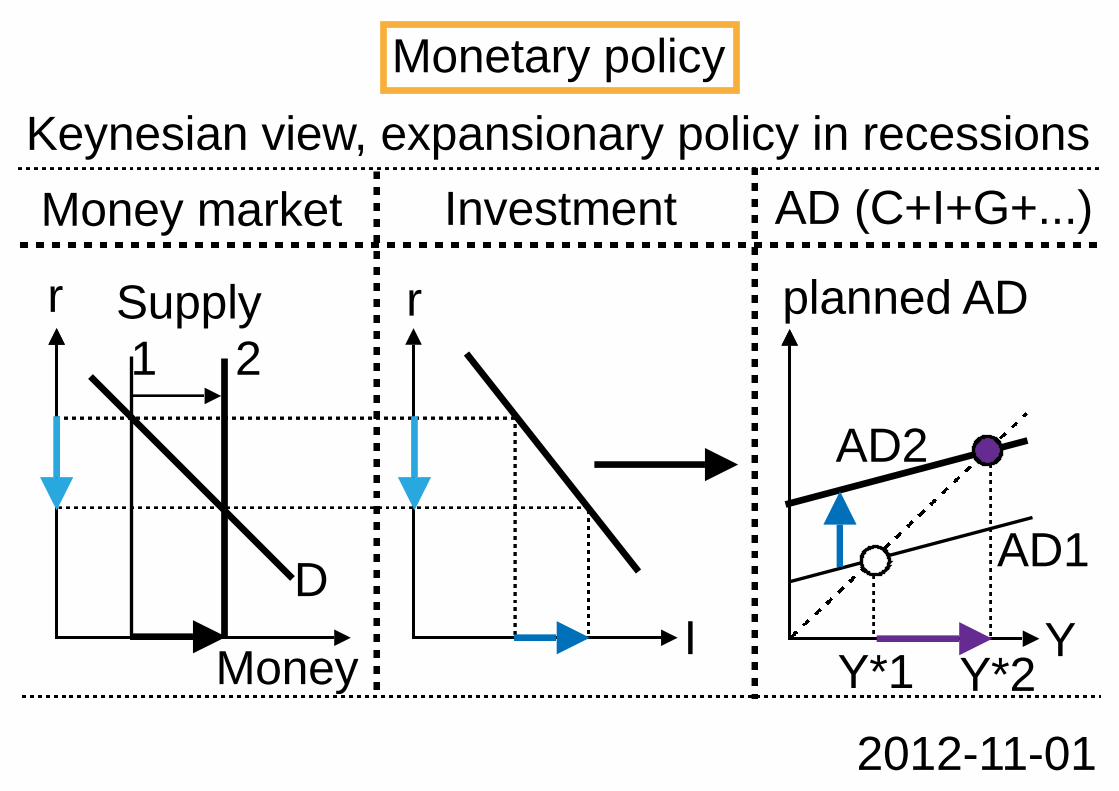

Keynesian view, expansionary policy in recessions

Monetary policy

1

r

AD (C+I+G+...)InvestmentMoney market

Money

r

I

planned AD

Y

AD2

D

2

Y*2Y*1

AD1

Supply

2012-11-01

Money supply is determinedby the central bank.

Money

Supply

Interest rate

Money market

Demand

Motives for demand:- Transactions- Precaution- SpeculationThe first two motives dependon income, the third dependson the interest rate.

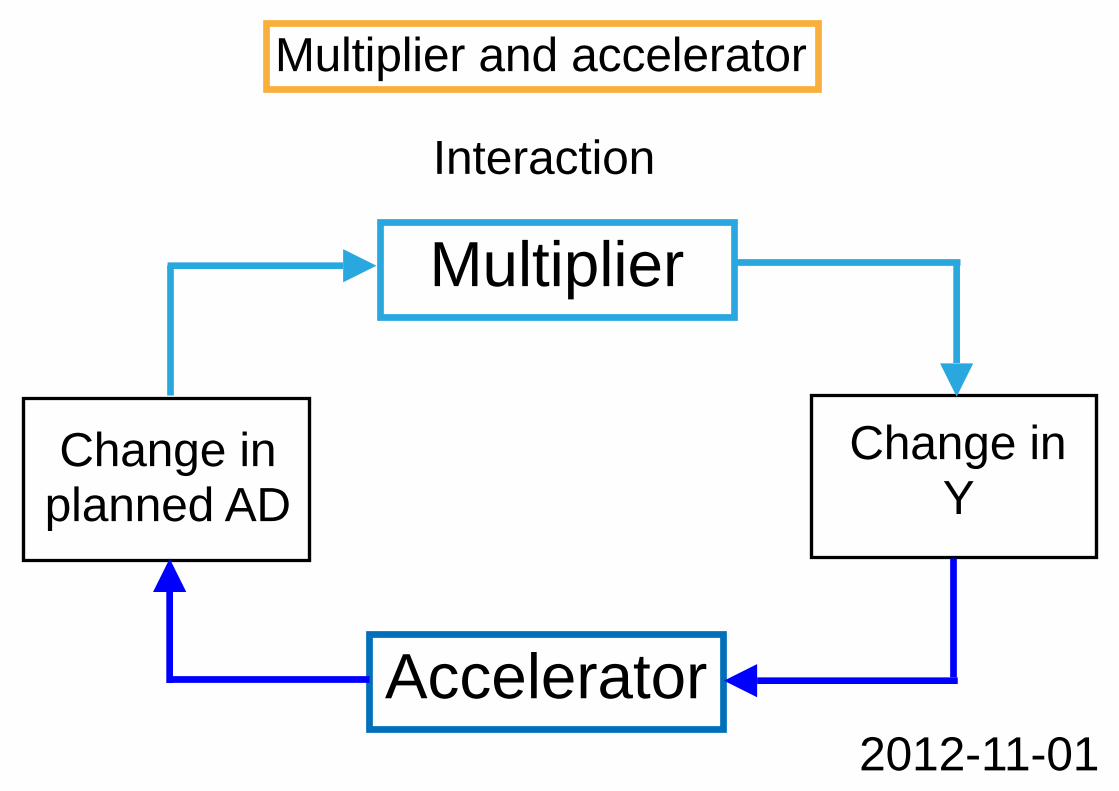

Multiplier and accelerator

Accelerator

Multiplier

Change inplanned AD

Change inY

Interaction

2012-11-01

planned AD

Y

Multiplier and AD

AD = Y

AD1

45o

2012-11-01

Multiplier

Changein AD

Change in Y

Change in AD=

AD2

Y1 Y2Change in Y

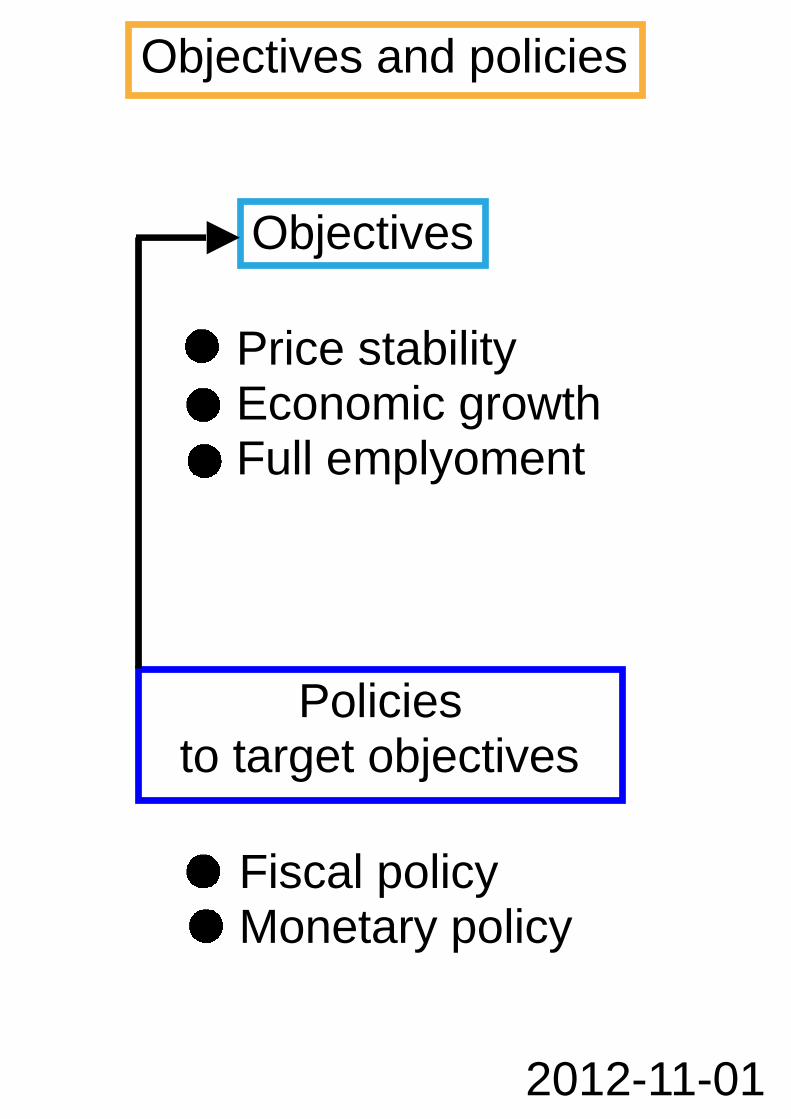

Objectives

Policiesto target objectives

2012-11-01

Objectives and policies

- Price stability- Economic growth- Full emplyoment

- Fiscal policy- Monetary policy

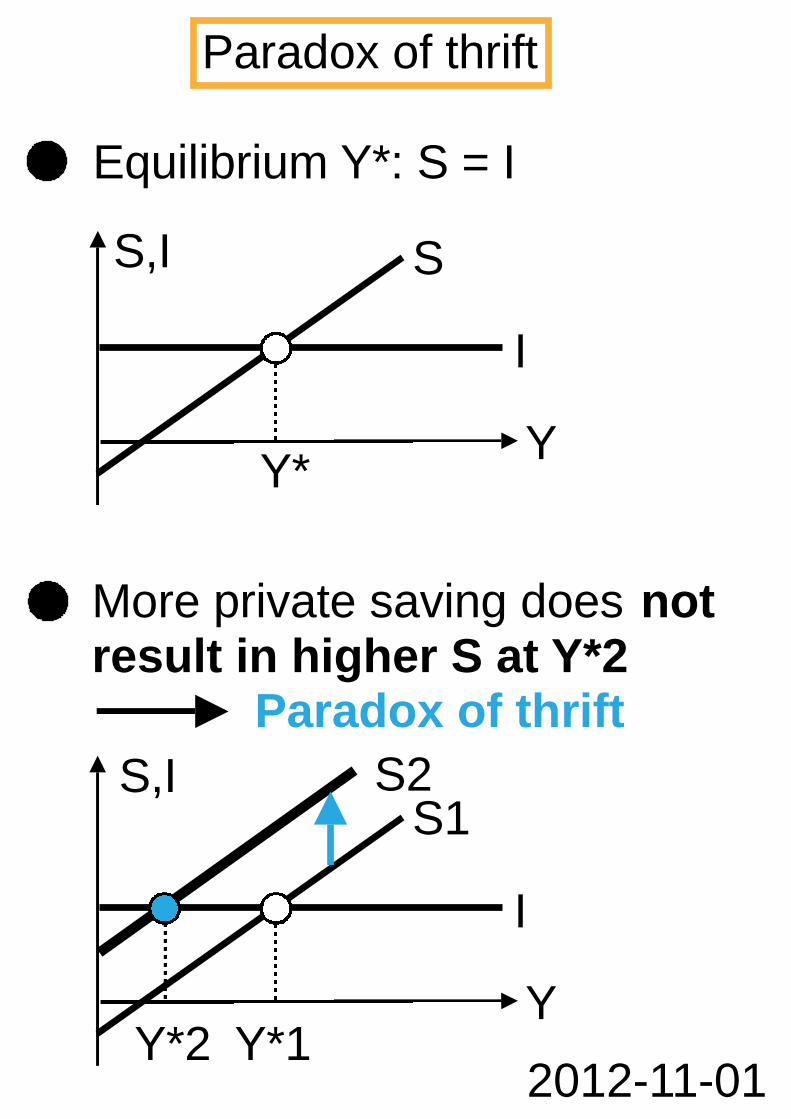

Equilibrium Y*: S = I

S,I

2012-11-01

Paradox of thrift

S

I

Y*Y

S1

I

Y*1Y

More private saving does notresult in higher S at Y*2

Paradox of thrift

S2

Y*2

S,I

Inflation (%)

2012-11-01

Phillips curve

Unemploy-ment (%)X

Y

The Phillips curve describes anegative relationship betweeninflation and unemployment.

- Since the 1970s this relation-ship has not been constant anymore. The curve is shiftedsometimes.

X = unemployment /Y= inflation

Low incomes

Low savingand investment

Source: Samuelson/Nordhaus:Economics, 18th ed, 583

Poverty (vicious circle)

Low capitalaccumulation

Low productivity

2012-11-01

2012-11-01

Classical and monetarist view:Monetary policy just changesthe price level (and not othervariables).

M * V = P * Q- M = Money supply- V = Velocity of circulation- P = Price level- Q = Output

Quantity theory of money

If V (pattern of payments) andQ (full employment) areconstant, then it can be said:A rise in M results in aproportional increase in P, e.g.more money, more inflation.

2012-11-01

Unemployment 1(types)

Seasonal unemployment:regular during the year

Frictional unemployment:when joining the labour forceor changing the job

Structural unemployment:due to changes in technology

Cyclical unemployment:during recessions

2012-11-01

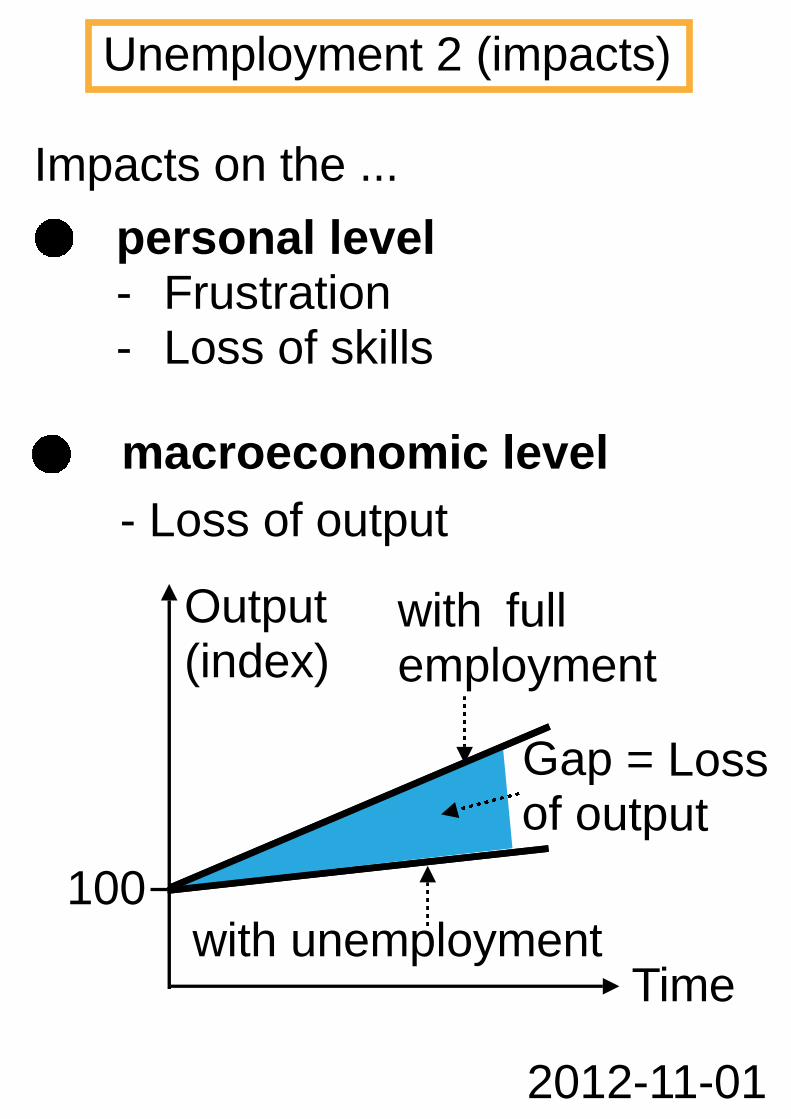

- Loss of output

100

Output(index)

personal level- Frustration- Loss of skills

Impacts on the ...

Unemployment 2 (impacts)

macroeconomic level

with fullemployment

with unemployment

Gap = Lossof output

Time

High incomes

High savingand investment

Wealth (virtuous circle)

High capitalaccumulation

High productivity

2012-11-01