local scpd students please come to stanford to take the ... 09 week 7... · 17-1 handout #17a...

TRANSCRIPT

17-1

Handout #17ADerivative Security Markets

Risk Management of Transaction Exposure

http://stanford2009.pageout.net

MWF 3:15-4:30 Gates B01Final Exam MS&E 247S

Fri Aug 14 2009 12:15PM-3:15PM Gates B01 (alternate time)Or Saturday Aug 15 2009 7PM-10PM Gates B01 (official time)

Remote SCPD participants will also take the exam on Friday, 8/14Please Submit Exam Proctor’s Name, Contact info as SCPD requires.

C.c. the info to [email protected], preferably a week before the exam.Local SCPD students please come to Stanford to take the exam. Light refreshments will

be served.

17-2

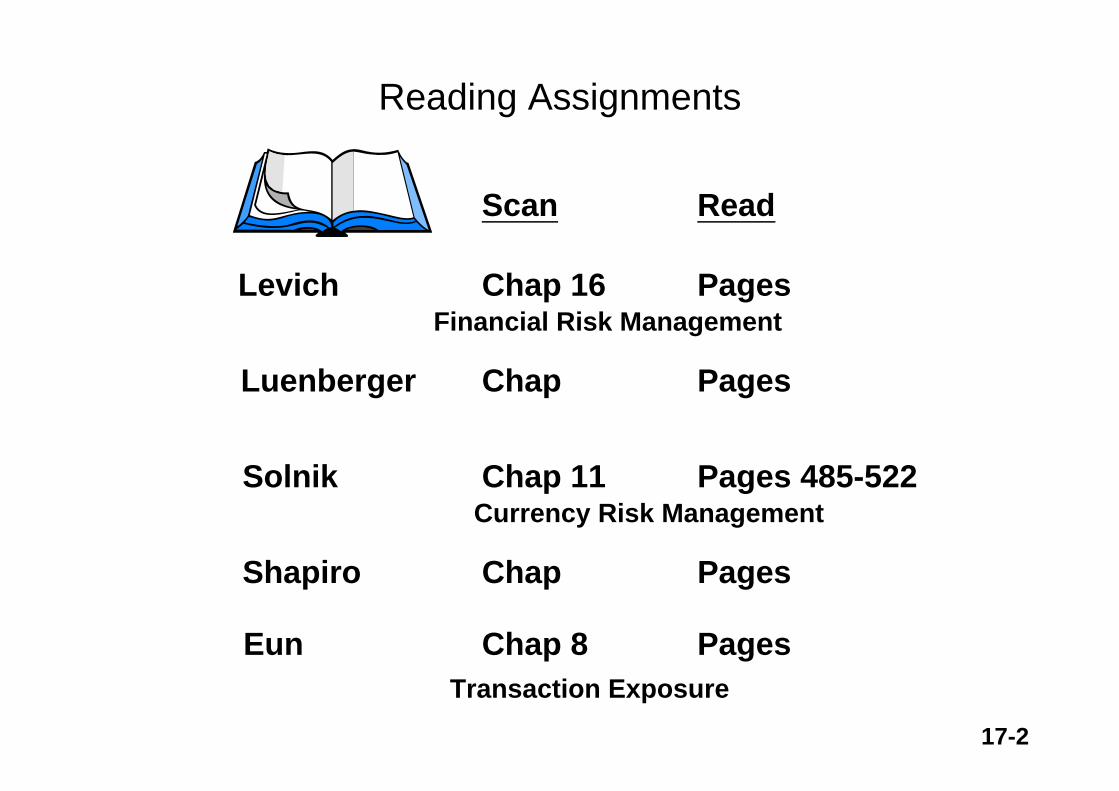

Levich

Luenberger

Solnik

Shapiro

Eun

Reading Assignments

Chap 16

Chap

Chap 11

Chap 8

Scan Read

Pages

Transaction Exposure

Pages 485-522

Pages

Chap Pages

Financial Risk Management

Pages

Currency Risk Management

17-3

Derivative Security MarketsRisk Management of

Transaction Exposure

MS&E 247S International InvestmentsYee-Tien Fu

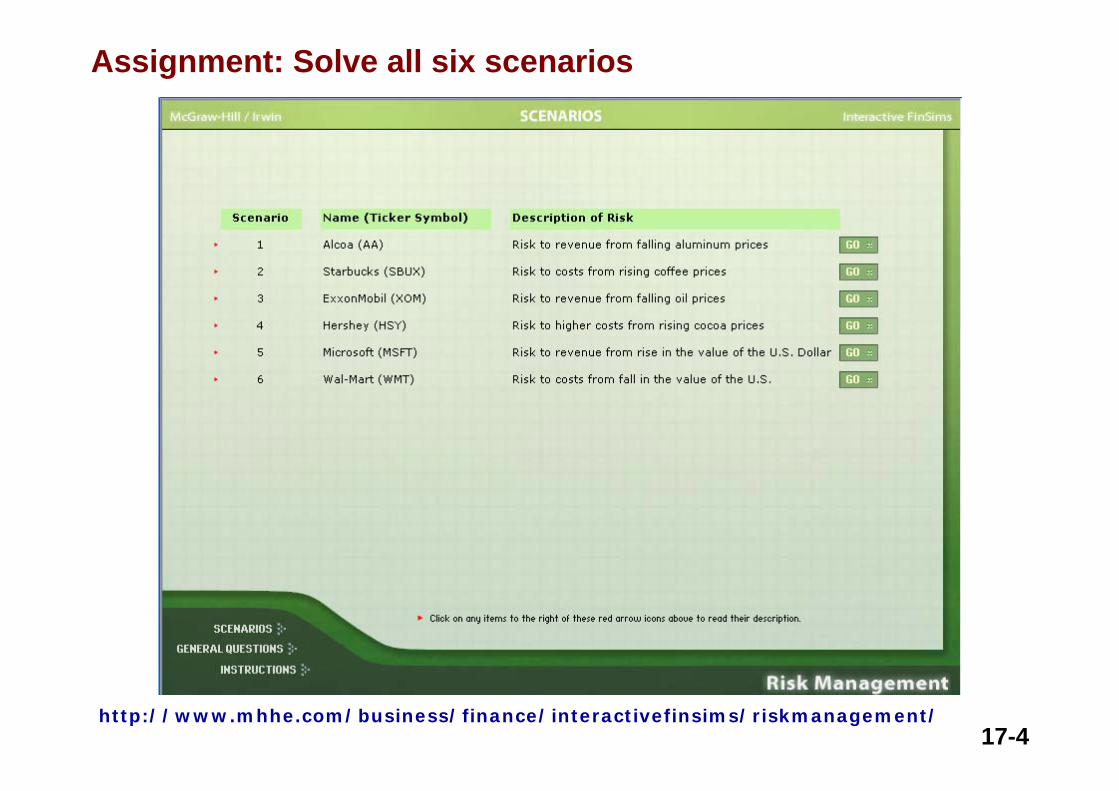

17-4http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

Assignment: Solve all six scenarios

17-5http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

17-6http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

17-7http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

17-8http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

17-9http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

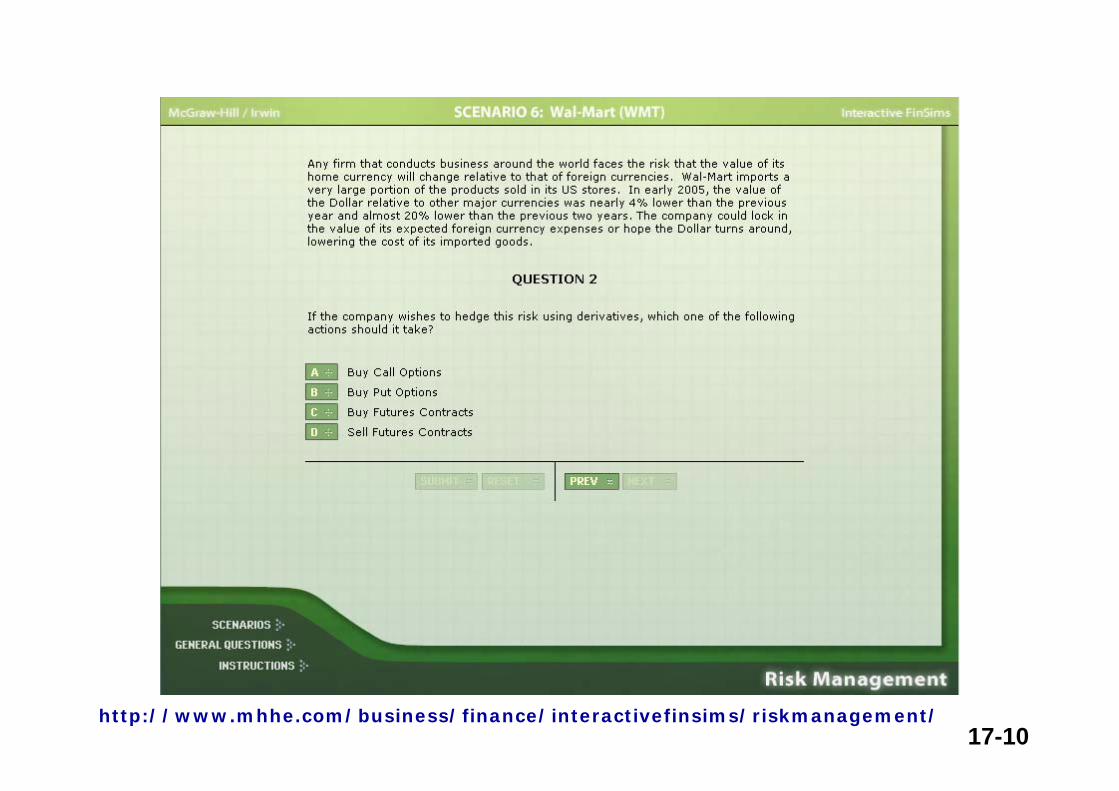

17-10http://www.mhhe.com/business/finance/interactivefinsims/riskmanagement/

17-11

INTERNATIONALFINANCIAL

MANAGEMENT

EUN / RESNICK

Fourth Edition

17-12

Chapter Objective:

This chapter discusses various methods available for the management of transaction exposure facing multinational firms.

8Chapter Eight

Risk Management of Transaction Exposure

17-13

Chapter Outline

• Forward Market Hedge• Money Market Hedge• Options Market Hedge• Cross-Hedging Minor Currency Exposure• Hedging Contingent Exposure• Hedging Recurrent Exposure with Swap Contracts• The Boeing Example• The Progressive Corporate Taxes

17-14

Chapter Outline (continued)

• Hedging Through Invoice Currency• Hedging via Lead and Lag• Exposure Netting• Should the Firm Hedge?• What Risk Management Products do Firms

Use?

17-15

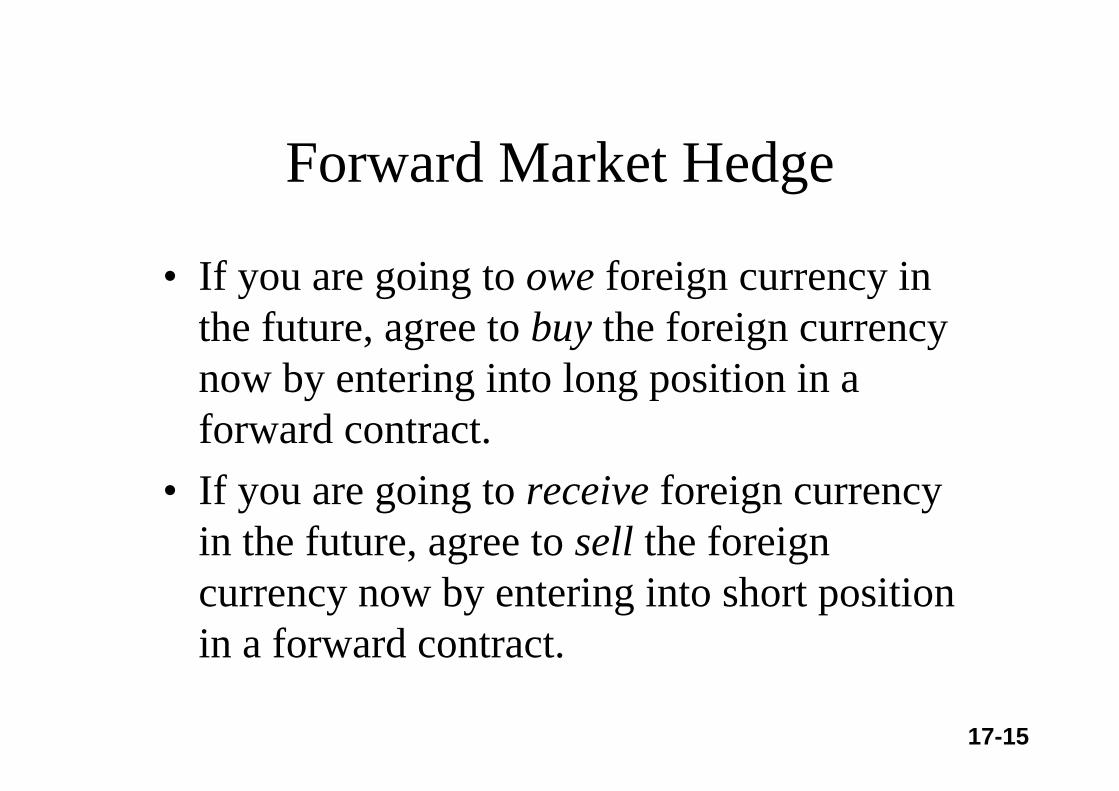

Forward Market Hedge

• If you are going to owe foreign currency in the future, agree to buy the foreign currency now by entering into long position in a forward contract.

• If you are going to receive foreign currency in the future, agree to sell the foreign currency now by entering into short position in a forward contract.

17-16

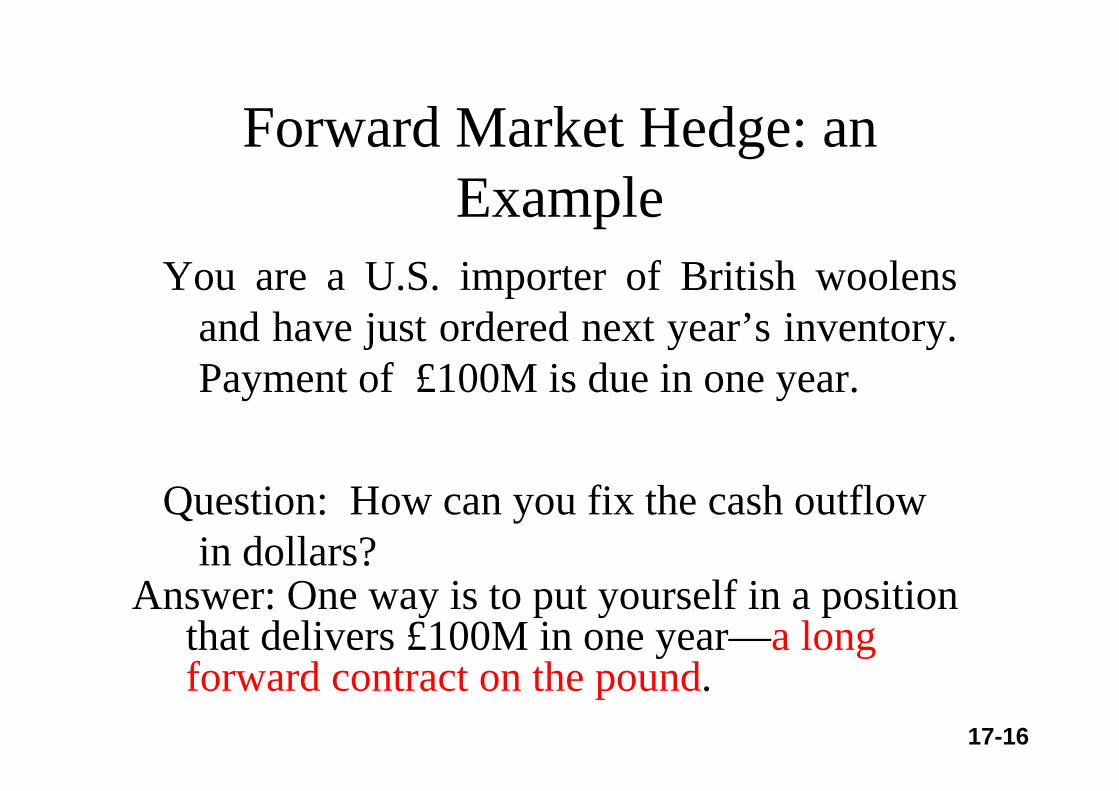

Forward Market Hedge: an Example

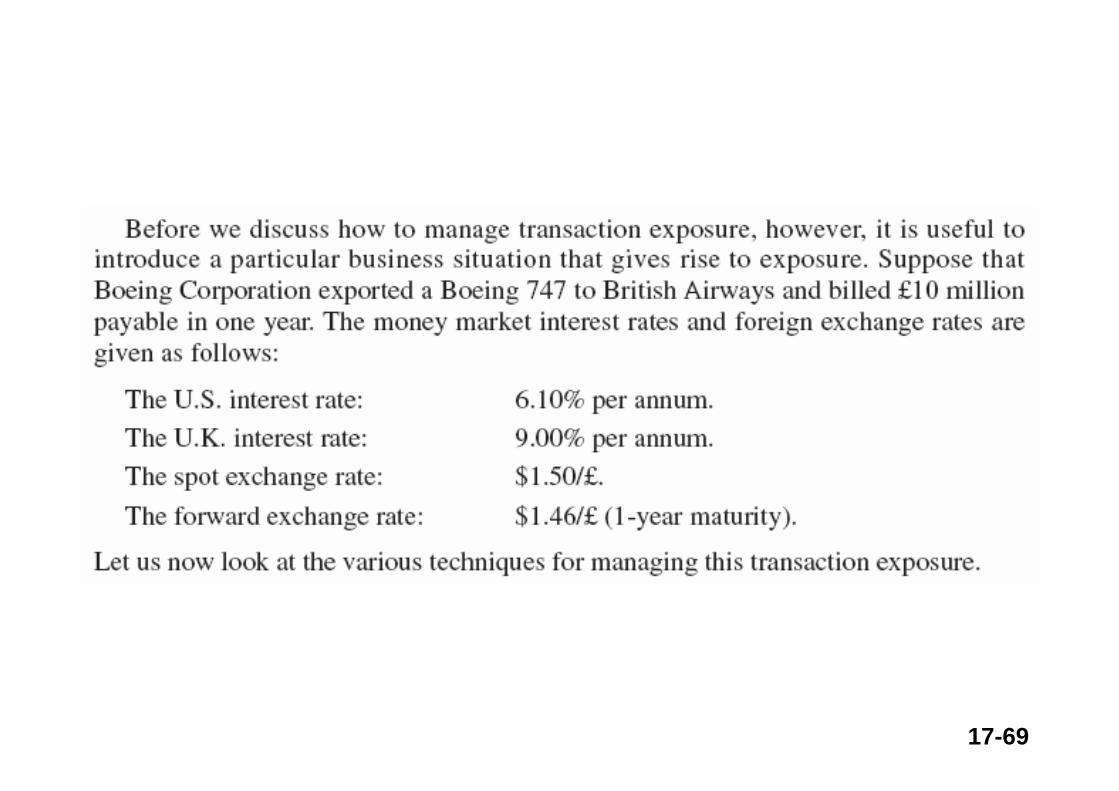

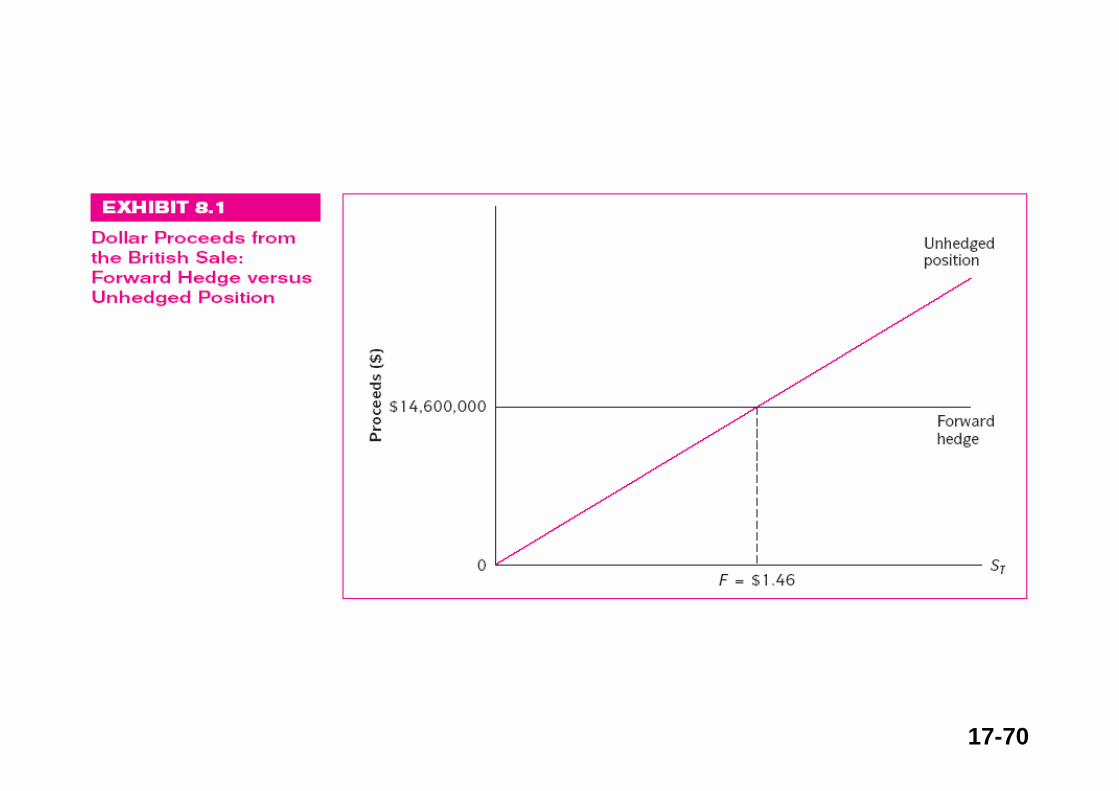

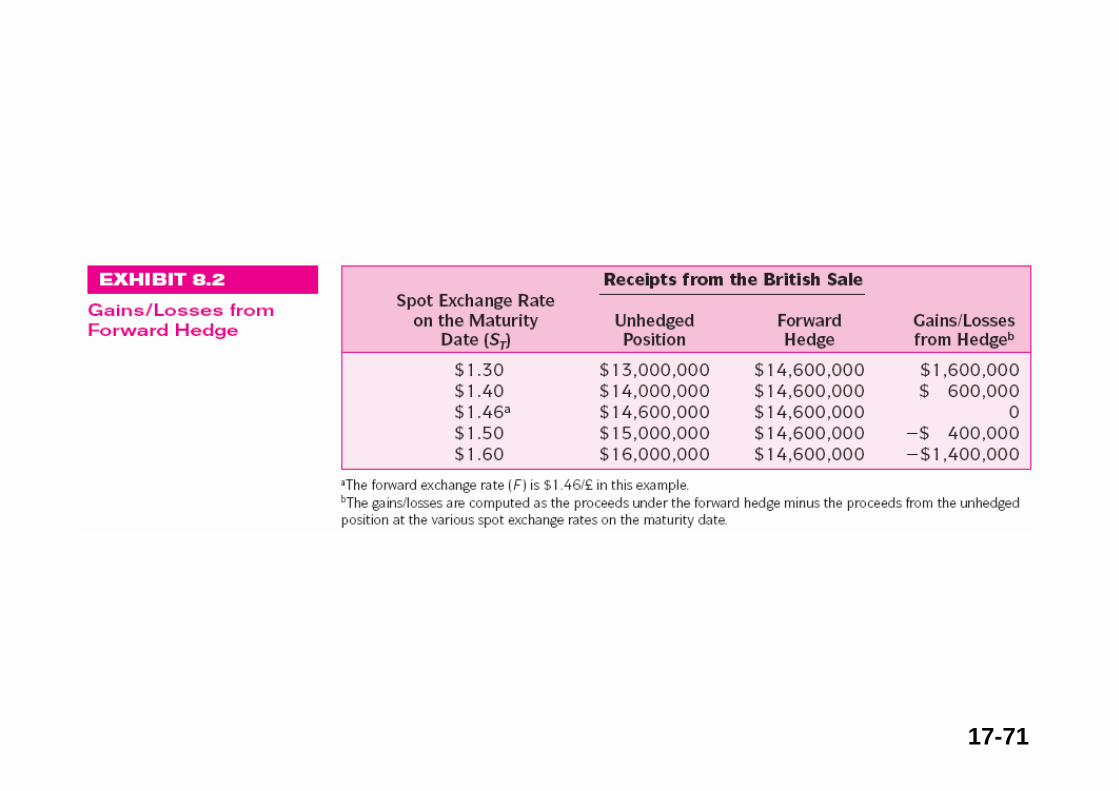

You are a U.S. importer of British woolens and have just ordered next year’s inventory. Payment of £100M is due in one year.

Question: How can you fix the cash outflow in dollars?

Answer: One way is to put yourself in a position that delivers £100M in one year—a long forward contract on the pound.

17-17

Forward Market Hedge

$1.50/£Value of £1 in $

in one year

Suppose the forward exchange rate is $1.50/£.

If he does not hedge the £100m payable, in one year his gain (loss) on the unhedged position is shown in green.

$0

$1.20/£ $1.80/£

–$30m

$30m

Unhedged payable

The importer will be better off if the pound depreciates: he

still buys £100m but at an exchange rate of only $1.20/£

he saves $30 million relative to $1.50/£

But he will be worse off if the pound appreciates.

17-18

Forward Market Hedge

$1.50/£Value of £1 in $

in one year$1.80/£

If he agrees to buy £100m in one year at $1.50/£ his gain (loss) on the forward are shown in blue.

$0

$30m

$1.20/£

–$30m

Long forward

If you agree to buy £100 million at a price of $1.50 per pound, you will lose

$30 million if the price of a pound is only $1.20.

If you agree to buy £100 million at a price of $1.50 per pound, you will make $30 million if the price of a pound reaches $1.80.

17-19

Forward Market Hedge

$1.50/£Value of £1 in $

in one year$1.80/£

The red line shows the payoff of the hedged payable. Note that gains on one position are offset by losses on the other position.

$0

$30 m

$1.20/£

–$30 m

Long forward

Unhedged payable

Hedged payable

17-20

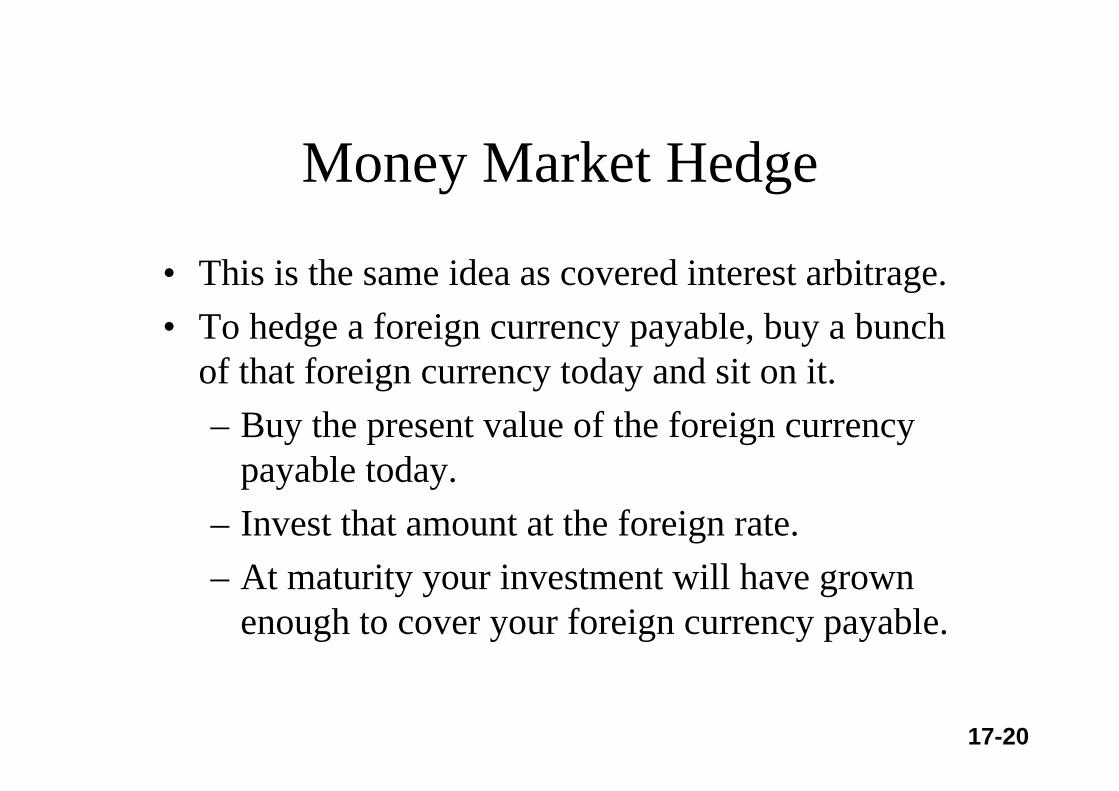

Money Market Hedge

• This is the same idea as covered interest arbitrage.• To hedge a foreign currency payable, buy a bunch

of that foreign currency today and sit on it.– Buy the present value of the foreign currency

payable today.– Invest that amount at the foreign rate.– At maturity your investment will have grown

enough to cover your foreign currency payable.

17-21

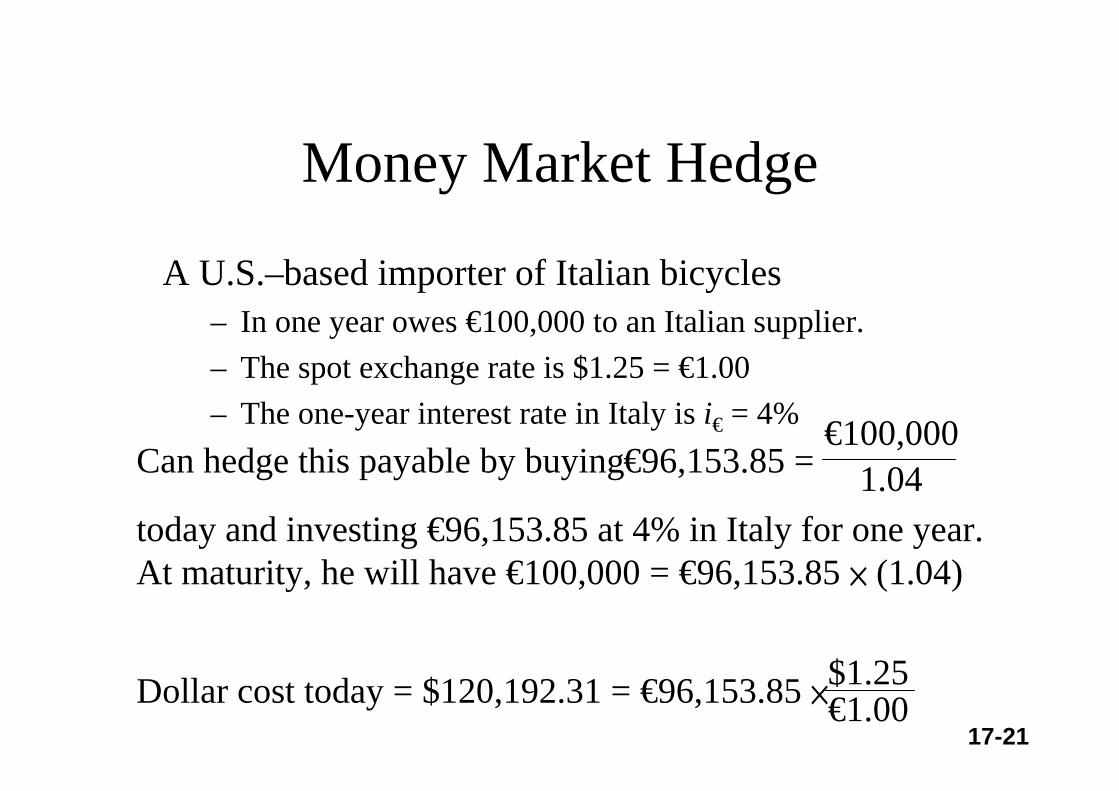

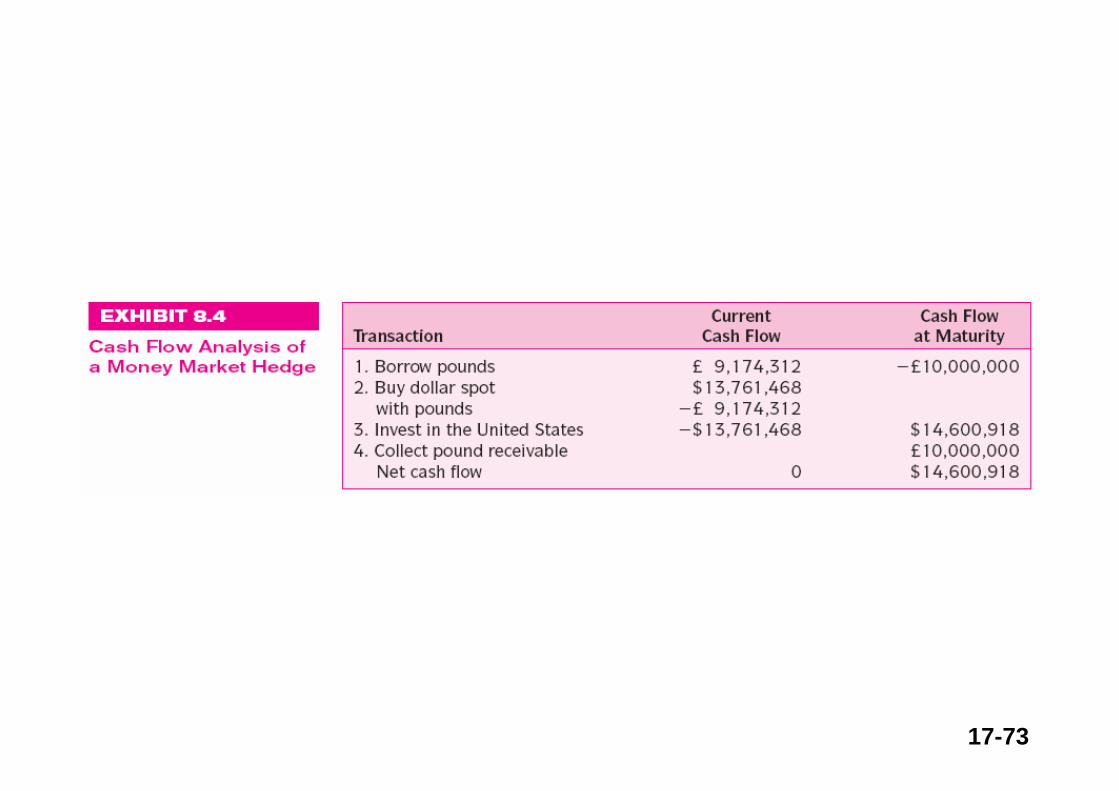

Money Market Hedge

A U.S.–based importer of Italian bicycles– In one year owes €100,000 to an Italian supplier.– The spot exchange rate is $1.25 = €1.00– The one-year interest rate in Italy is i€ = 4%

$1.25€1.00Dollar cost today = $120,192.31 = €96,153.85 ×

€100,0001.04€96,153.85 = Can hedge this payable by buying

today and investing €96,153.85 at 4% in Italy for one year.At maturity, he will have €100,000 = €96,153.85 × (1.04)

17-22

Money Market Hedge

$123,798.08 = $120,192.31 ×(1.03)

• With this money market hedge, we have redenominated a one-year €100,000 payable into a $120,192.31 payable due today.

• If the U.S. interest rate is i$ = 3% we could borrow the $120,192.31 today and owe in one year

$123,798.08 =€100,000(1+ i€)T (1+ i$)T×S($/€)×

Generalizewith i’s and T:

17-23

Money Market Hedge: Step OneSuppose you want to hedge a payable in the

amount of £y with a maturity of T:i. Borrow $x at t = 0 on a loan at a rate of i$ per year.

$x = S($/£)× £y(1+ i£)T

0 T

$x –$x(1 + i$)TRepay the loan in T years

17-24

Money Market Hedge: Step Two

at the prevailing spot rate.

£y(1+ i£)Tii. Exchange the borrowed $x for

Invest at i£ for the maturity of the payable.£y(1+ i£)T

At maturity, you will owe a $x(1 + i$)T.Your British investments will have grown to £y. This amount will service your payable and you will have no exposure to the pound.

17-25

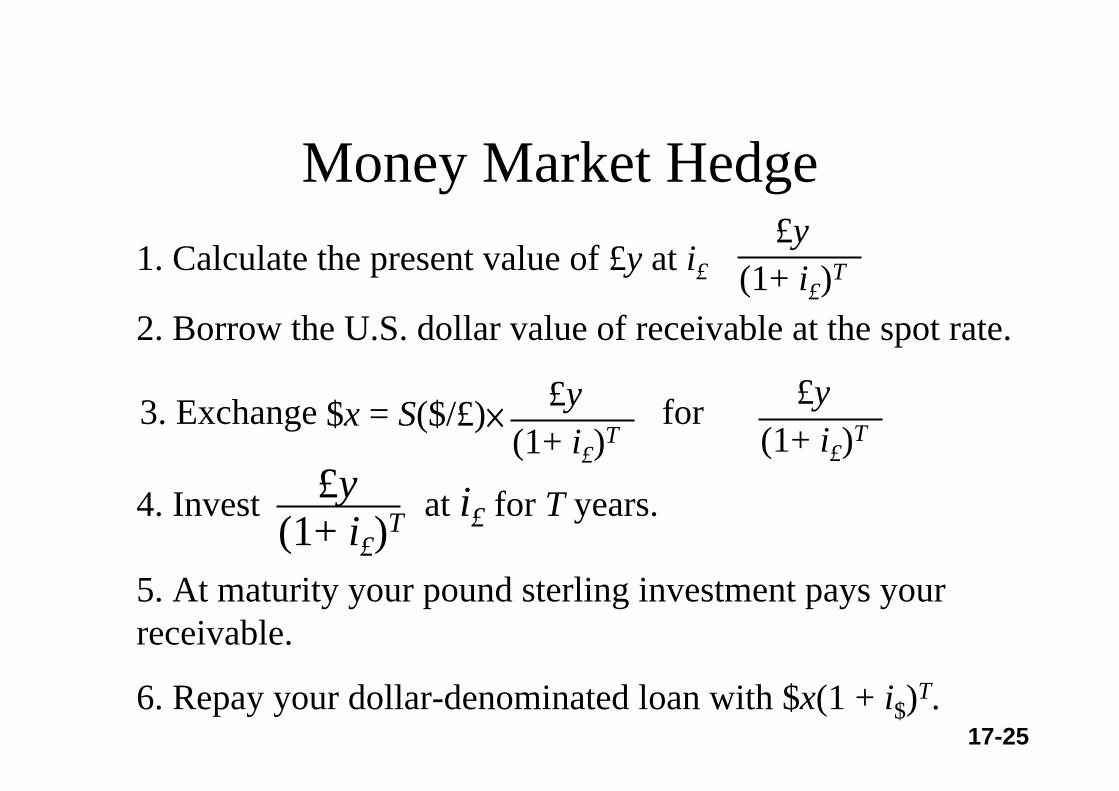

Money Market Hedge1. Calculate the present value of £y at i£

£y(1+ i£)T

2. Borrow the U.S. dollar value of receivable at the spot rate.

$x = S($/£)× £y(1+ i£)T

3. Exchange for £y(1+ i£)T

4. Invest at i£ for T years.£y(1+ i£)T

5. At maturity your pound sterling investment pays your receivable.

6. Repay your dollar-denominated loan with $x(1 + i$)T.

17-26

Options Market Hedge

• Options provide a flexible hedge against the downside, while preserving the upside potential.

• To hedge a foreign currency payable buy calls on the currency.– If the currency appreciates, your call option lets

you buy the currency at the exercise price of the call.

• To hedge a foreign currency receivable buy puts on the currency.– If the currency depreciates, your put option lets

you sell the currency for the exercise price.

17-27

Options Market Hedge

$1.50/£Value of £1 in $

in one year

Suppose the forward exchange rate is $1.50/£.

If an importer who owes £100m does not hedge the payable, in one year his gain (loss) on the unhedged position is shown in green.

$0

$1.20/£ $1.80/£

–$30m

$30m

Unhedged payable

The importer will be better off if the pound depreciates: he

still buys £100m but at an exchange rate of only $1.20/£

he saves $30 million relative to $1.50/£

But he will be worse off if the pound appreciates.

17-28

Options Markets HedgeProfit

loss

–$5m$1.55/£

Long call on £100m Suppose our

importer buys a call option on £100m with an exercise price of $1.50 per pound.

He pays $.05 per pound for the call.

$1.50/£

Value of £1 in $ in one year

17-29

Value of £1 in $ in one year

Options Markets HedgeProfit

loss

–$5m

$1.45 /£

Long call on £100m

The payoff of the portfolio of a call and a payable is shown in red.

He can still profit from decreases in the exchange rate below $1.45/£ but has a hedge against unfavorable increases in the exchange rate.

$1.50/£ Unhedged payable

$1.20/£

$25m

17-30

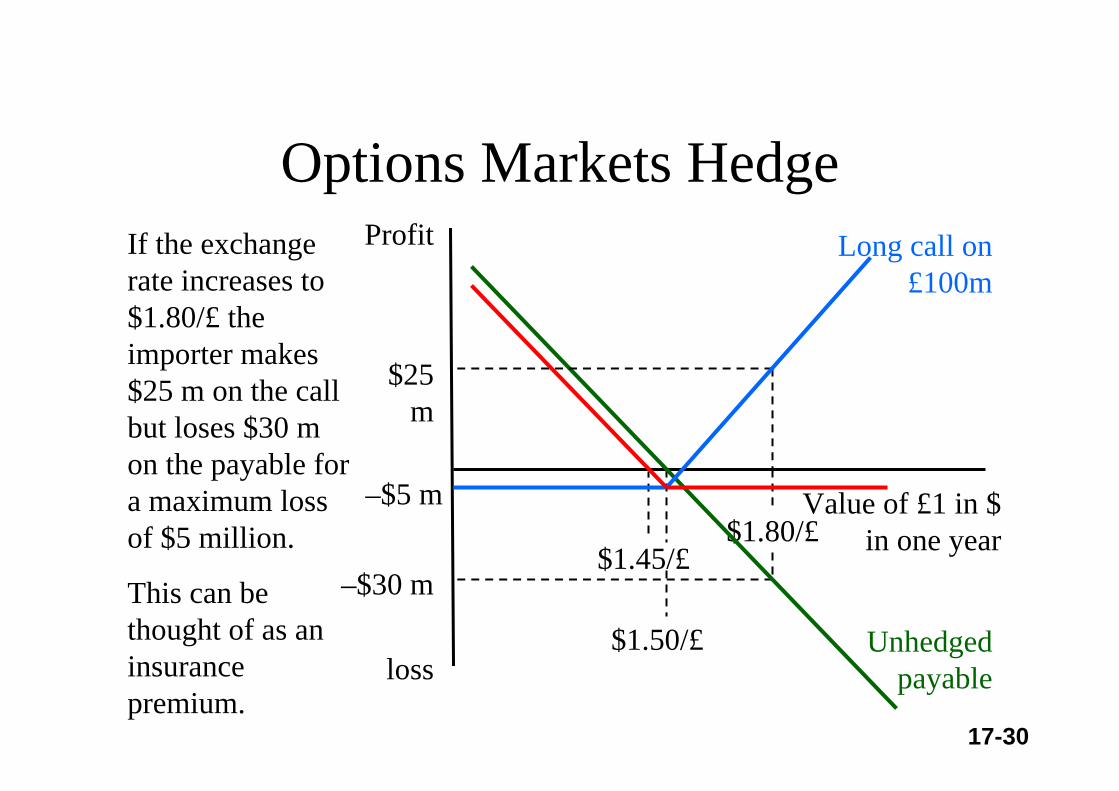

–$30 m

$1.80/£Value of £1 in $

in one year

Options Markets HedgeProfit

loss

–$5 m

$1.45/£

Long call on £100m

If the exchange rate increases to $1.80/£ the importer makes $25 m on the call but loses $30 m on the payable for a maximum loss of $5 million.

This can be thought of as an insurance premium.

$1.50/£ Unhedged payable

$25 m

17-31

Options Markets HedgeIMPORTERS who OWE foreign currency in the future should BUY CALL OPTIONS.– If the price of the currency

goes up, his call will lock in an upper limit on the dollar cost of his imports.

– If the price of the currency goes down, he will have the option to buy the foreign currency at a lower price.

EXPORTERS with accounts receivable denominated in foreign currency should BUY PUT OPTIONS.– If the price of the currency goes

down, puts will lock in a lower limit on the dollar value of his exports.

– If the price of the currency goes up, he will have the option to sell the foreign currency at a higher price.

17-32

Hedging Exports with Put Options

• Show the portfolio payoff of an exporter who is owed £1 million in one year.

• The current one-year forward rate is £1 = $2.• Instead of entering into a short forward

contract, he buys a put option written on £1 million with a maturity of one year and a strike price of £1 = $2. – The cost of this option is $0.05 per pound.

17-33

S($/£)360

–$2m

$2

Long

receiv

able Long put

$1,950,000

–$50k

Options Market Hedge:Exporter buys a put option to protect the dollar value of his receivable.

–$50k

$2.05

Hedge

d rece

ivable

17-34

S($/£)360

$2

The exporter who buys a put option to protect the dollar value of his receivable

–$50k

$2.05

Hedge

d rece

ivable

has essentially purchased a call.

17-35

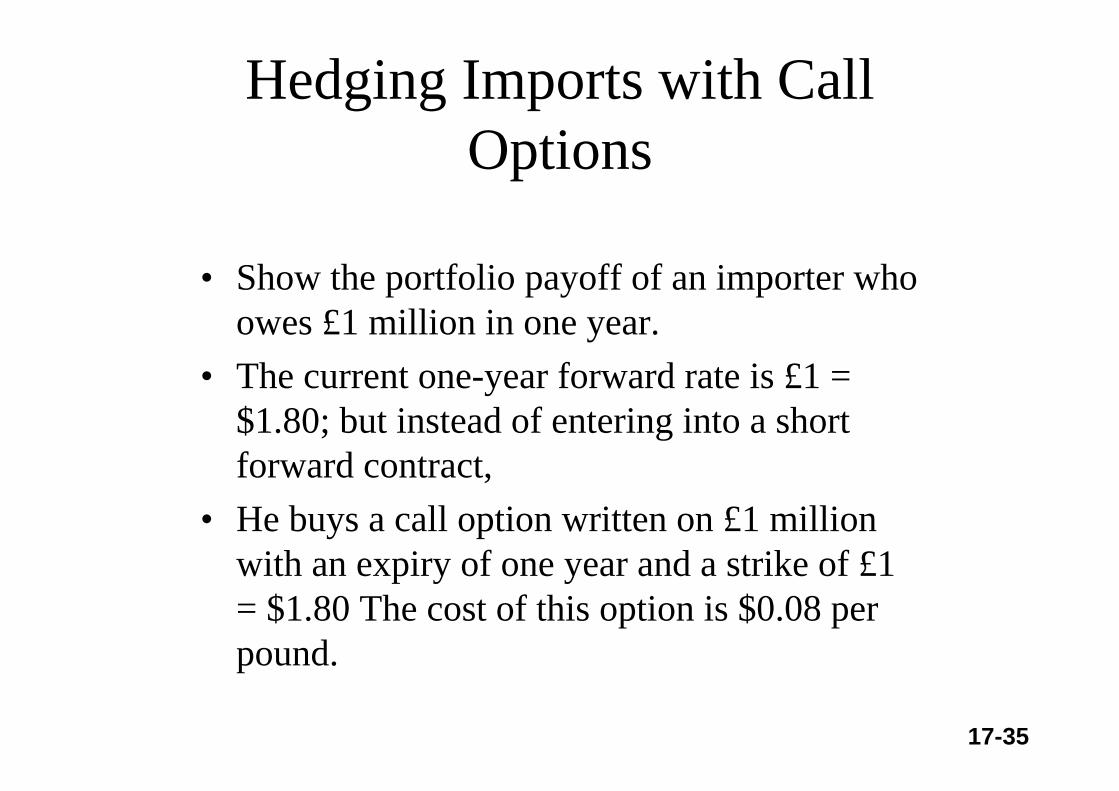

Hedging Imports with Call Options

• Show the portfolio payoff of an importer who owes £1 million in one year.

• The current one-year forward rate is £1 = $1.80; but instead of entering into a short forward contract,

• He buys a call option written on £1 million with an expiry of one year and a strike of £1 = $1.80 The cost of this option is $0.08 per pound.

17-36

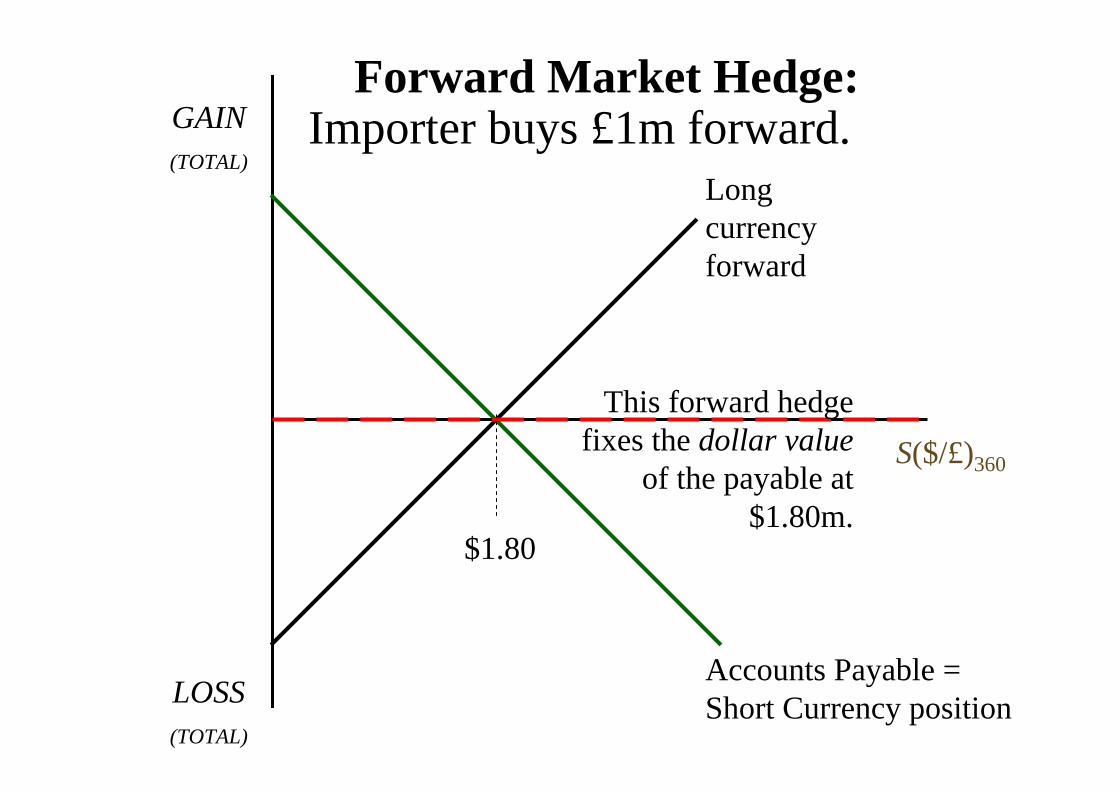

LOSS(TOTAL)

GAIN(TOTAL)

S($/£)360

Long currency forward

Accounts Payable = Short Currency position

Forward Market Hedge:Importer buys £1m forward.

This forward hedge fixes the dollar value

of the payable at $1.80m.

$1.80

17-37

$1.8m

S($/£)360

$1.80

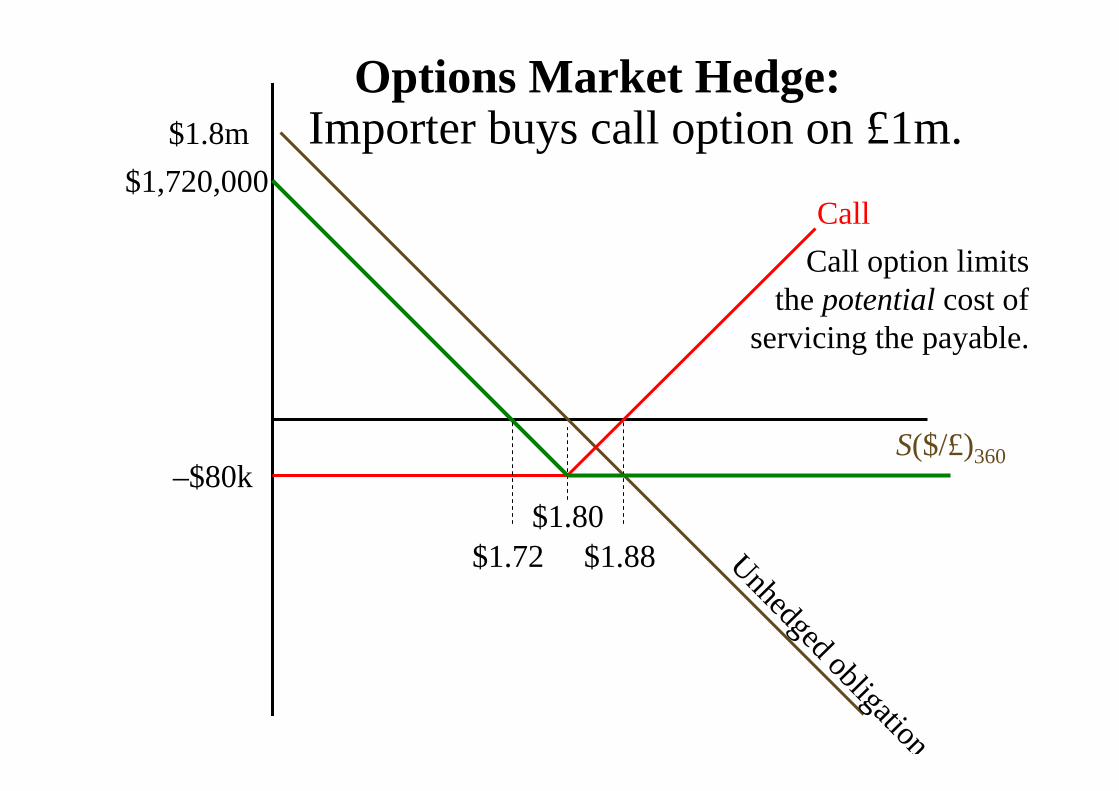

Unhedged obligationCall

–$80k

$1.88

$1,720,000

$1.72

Call option limits the potential cost of

servicing the payable.

Options Market Hedge:Importer buys call option on £1m.

17-38

S($/£)360

$1.80

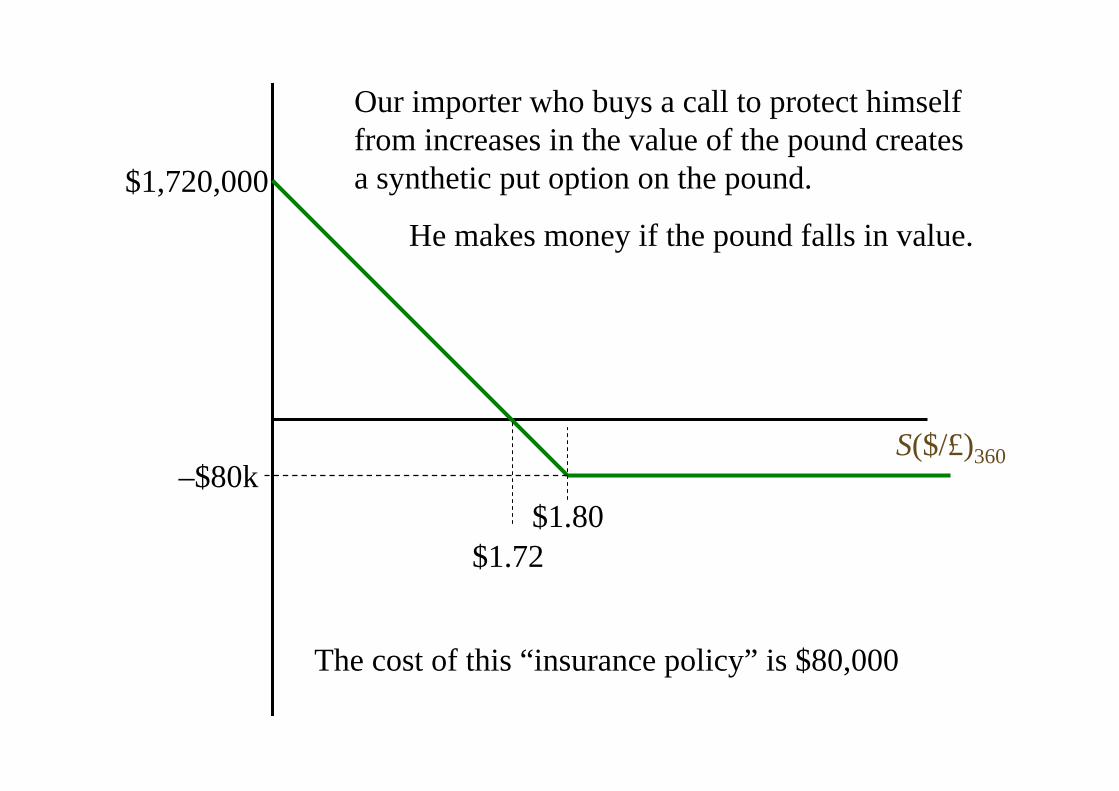

$1,720,000

$1.72

Our importer who buys a call to protect himself from increases in the value of the pound creates a synthetic put option on the pound.

He makes money if the pound falls in value.

–$80k

The cost of this “insurance policy” is $80,000

17-39

Taking it to the Next Level

• Suppose our importer can absorb “small” amounts of exchange rate risk, but his competitive position will suffer with big movements in the exchange rate.– Large dollar depreciations increase the cost of

his imports– Large dollar appreciations increase the foreign

currency cost of his competitors exports, costing him customers as his competitors renew their focus on the domestic market.

17-40

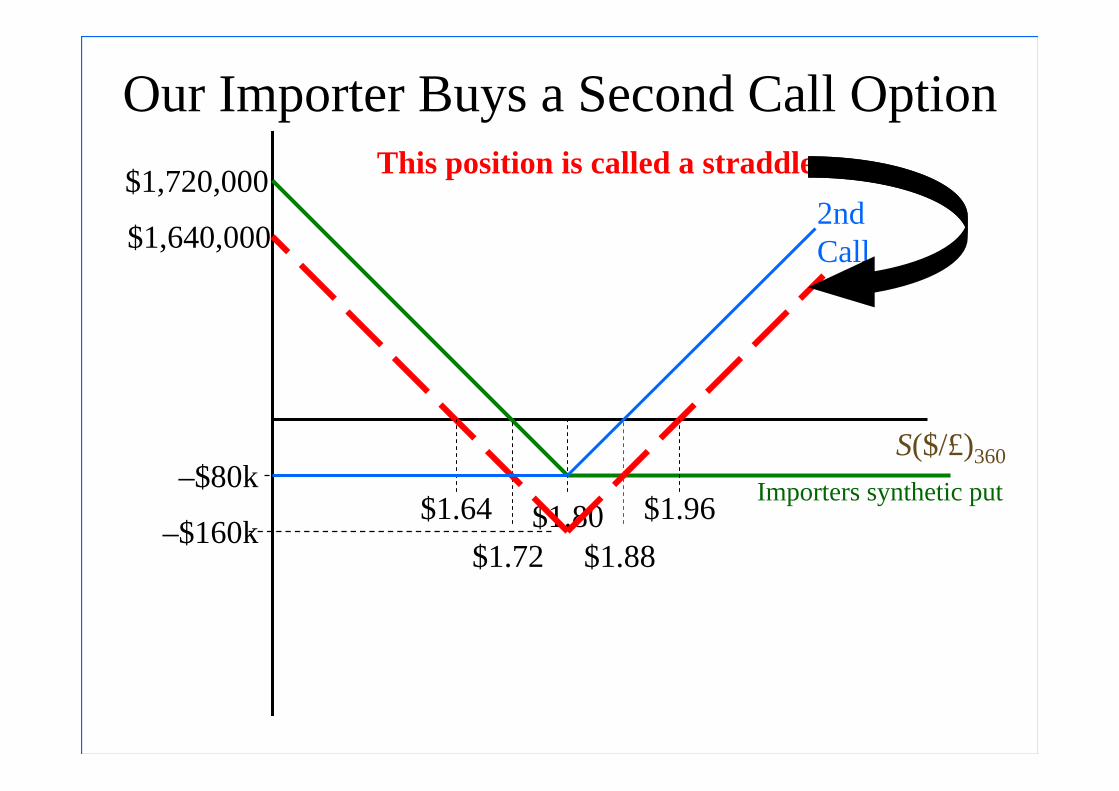

Our Importer Buys a Second Call Option

S($/£)360

$1.80

$1,720,000

$1.72

–$80k

This position is called a straddle

$1.64 $1.96

$1,640,000

–$160k

2ndCall

$1.88

Importers synthetic put

17-41

S($/£)360

$1.80

$1,720,000

$1.72

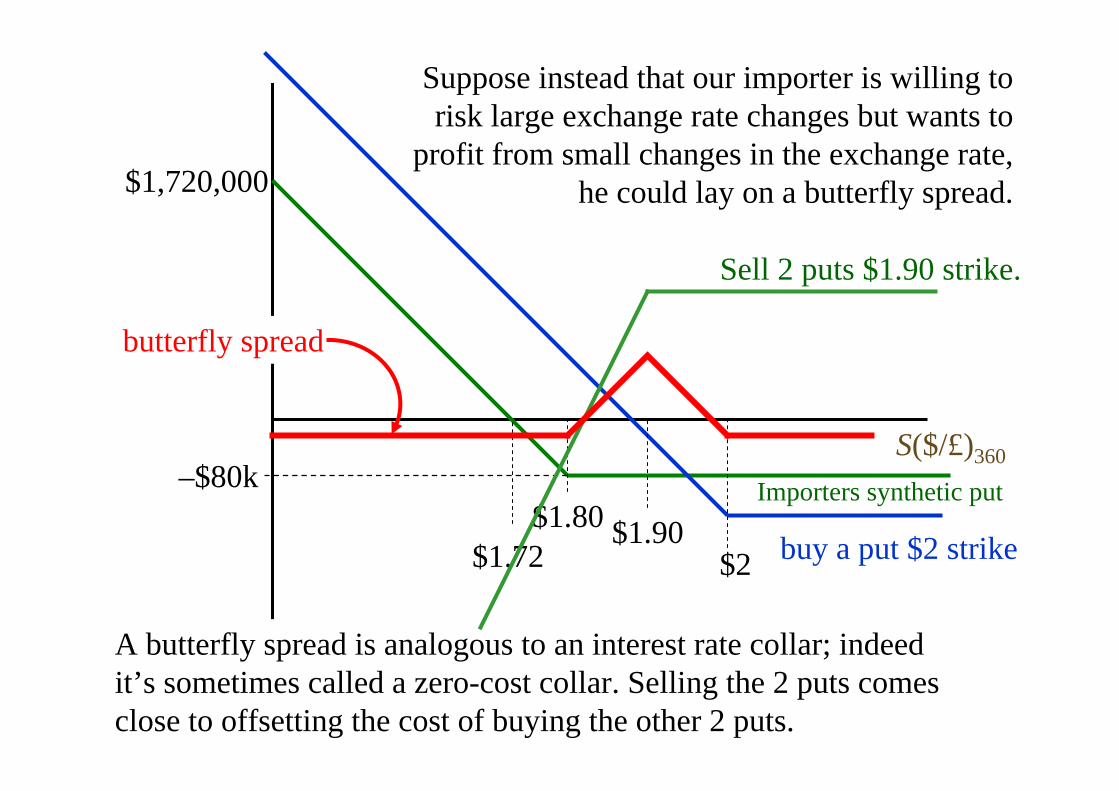

Suppose instead that our importer is willing to risk large exchange rate changes but wants to

profit from small changes in the exchange rate, he could lay on a butterfly spread.

–$80k

A butterfly spread is analogous to an interest rate collar; indeed it’s sometimes called a zero-cost collar. Selling the 2 puts comes close to offsetting the cost of buying the other 2 puts.

$2 buy a put $2 strike

butterfly spread

Sell 2 puts $1.90 strike.

$1.90Importers synthetic put

17-42

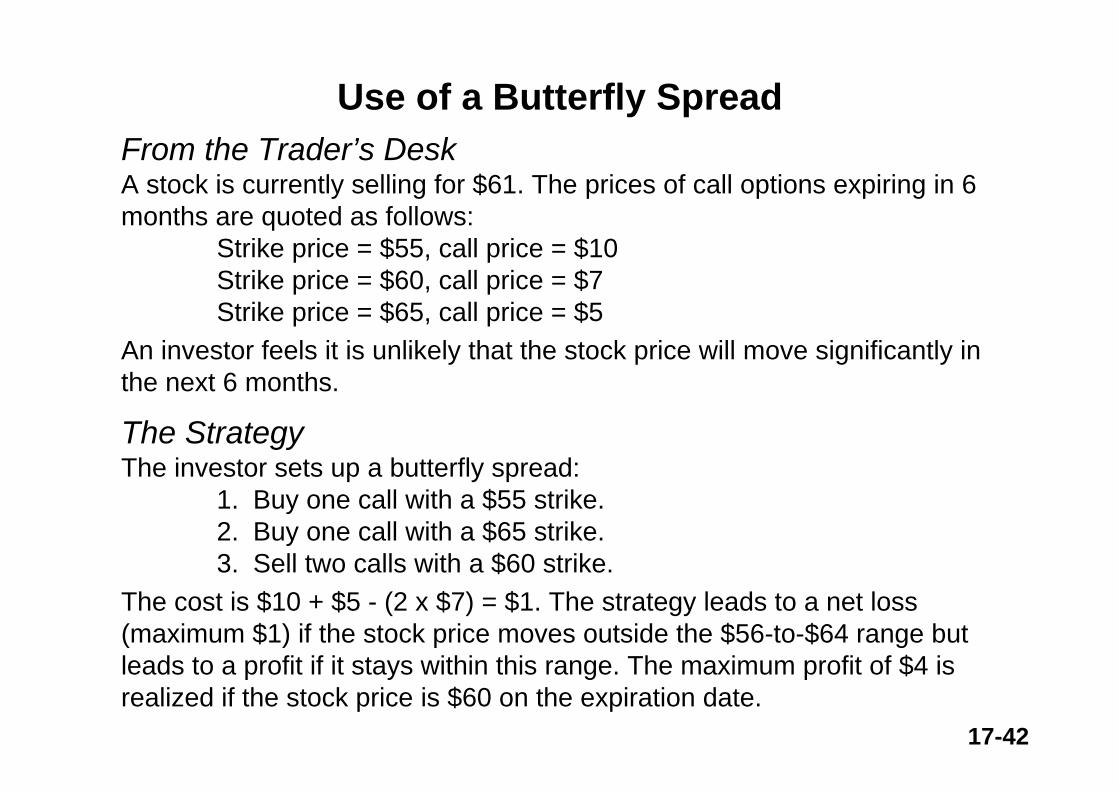

Use of a Butterfly SpreadFrom the Trader’s DeskA stock is currently selling for $61. The prices of call options expiring in 6 months are quoted as follows:

Strike price = $55, call price = $10Strike price = $60, call price = $7Strike price = $65, call price = $5

An investor feels it is unlikely that the stock price will move significantly in the next 6 months.

The StrategyThe investor sets up a butterfly spread:

1. Buy one call with a $55 strike.2. Buy one call with a $65 strike.3. Sell two calls with a $60 strike.

The cost is $10 + $5 - (2 x $7) = $1. The strategy leads to a net loss (maximum $1) if the stock price moves outside the $56-to-$64 range but leads to a profit if it stays within this range. The maximum profit of $4 is realized if the stock price is $60 on the expiration date.

17-43

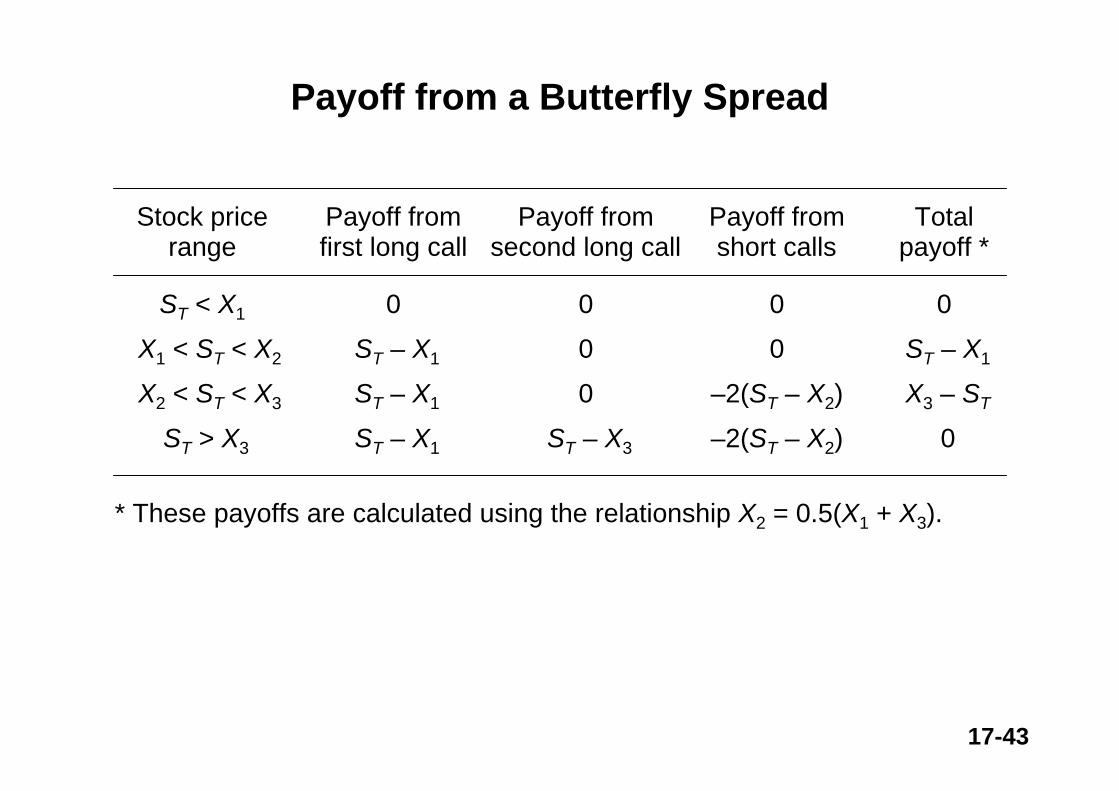

Payoff from a Butterfly Spread

Stock price Payoff from Payoff from Payoff from Totalrange first long call second long call short calls payoff *

ST < X1 0 0 0 0

X1 < ST < X2 ST – X1 0 0 ST – X1

X2 < ST < X3 ST – X1 0 –2(ST – X2) X3 – ST

ST > X3 ST – X1 ST – X3 –2(ST – X2) 0

* These payoffs are calculated using the relationship X2 = 0.5(X1 + X3).

17-44

Butterfly Spread Using Call Options

X1 X3

Profit

STX2

17-45

Butterfly Spread Using Put Options

X1 X3

Profit

STX2

17-46

Options

• A motivated financial engineer can create almost any risk-return profile that a company might wish to consider.

• Straddles and butterfly spreads are quite common.

• Notice that the butterfly spread costs our importer quite a bit less than a naïve strategy of buying call options.

17-47

17-48

Cross-Hedging Minor Currency Exposure

• The major currencies are the: U.S. dollar, Canadian dollar, British pound, Euro, Swiss franc, Mexican peso, and Japanese yen.

• Everything else is a minor currency, like the Thai bhat.

• It is difficult, expensive, or impossible to use financial contracts to hedge exposure to minor currencies.

17-49

Cross-Hedging Minor Currency Exposure

• Cross-Hedging involves hedging a position in one asset by taking a position in another asset.

• The effectiveness of cross-hedging depends upon how well the assets are correlated.– An example would be a U.S. importer with

liabilities in Swedish krona hedging with long or short forward contracts on the euro. If the krona is expensive when the euro is expensive, or even if the krona is cheap when the euro is expensive it can be a good hedge. But they need to co-vary in a predictable way.

17-50

Hedging Contingent Exposure

• If only certain contingencies give rise to exposure, then options can be effective insurance.

• For example, if your firm is bidding on a hydroelectric dam project in Canada, you will need to hedge the Canadian-U.S. dollar exchange rate only if your bid wins the contract. Your firm can hedge this contingent risk with options.

17-51

17-52

17-53

17-54

17-55

Hedging Recurrent Exposure with Swaps

• Recall that swap contracts can be viewed as a portfolio of forward contracts.

• Firms that have recurrent exposure can very likely hedge their exchange risk at a lower cost with swaps than with a program of hedging each exposure as it comes along.

• It is also the case that swaps are available in longer-terms than futures and forwards.

17-56

17-57

17-58

Hedging through Invoice Currency

• The firm can shift, share, or diversify:– shift exchange rate risk

• by invoicing foreign sales in home currency

– share exchange rate risk• by pro-rating the currency of the invoice between

foreign and home currencies

– diversify exchange rate risk• by using a market basket index

17-59

Hedging via Lead and Lag

• If a currency is appreciating, pay those bills denominated in that currency early; let customers in that country pay late as long as they are paying in that currency.

• If a currency is depreciating, give incentives to customers who owe you in that currency to pay early; pay your obligations denominated in that currency as late as your contracts will allow.

17-60

Exposure Netting

• A multinational firm should not consider deals in isolation, but should focus on hedging the firm as a portfolio of currency positions.– As an example, consider a U.S.-based

multinational with Korean won receivables and Japanese yen payables. Since the won and the yen tend to move in similar directions against the U.S. dollar, the firm can just wait until these accounts come due and just buy yen with won.

– Even if it’s not a perfect hedge, it may be too expensive or impractical to hedge each currency separately.

17-61

Exposure Netting

• Many multinational firms use a reinvoice center. Which is a financial subsidiary that nets out the intrafirm transactions.

• Once the residual exposure is determined, then the firm implements hedging.

17-62

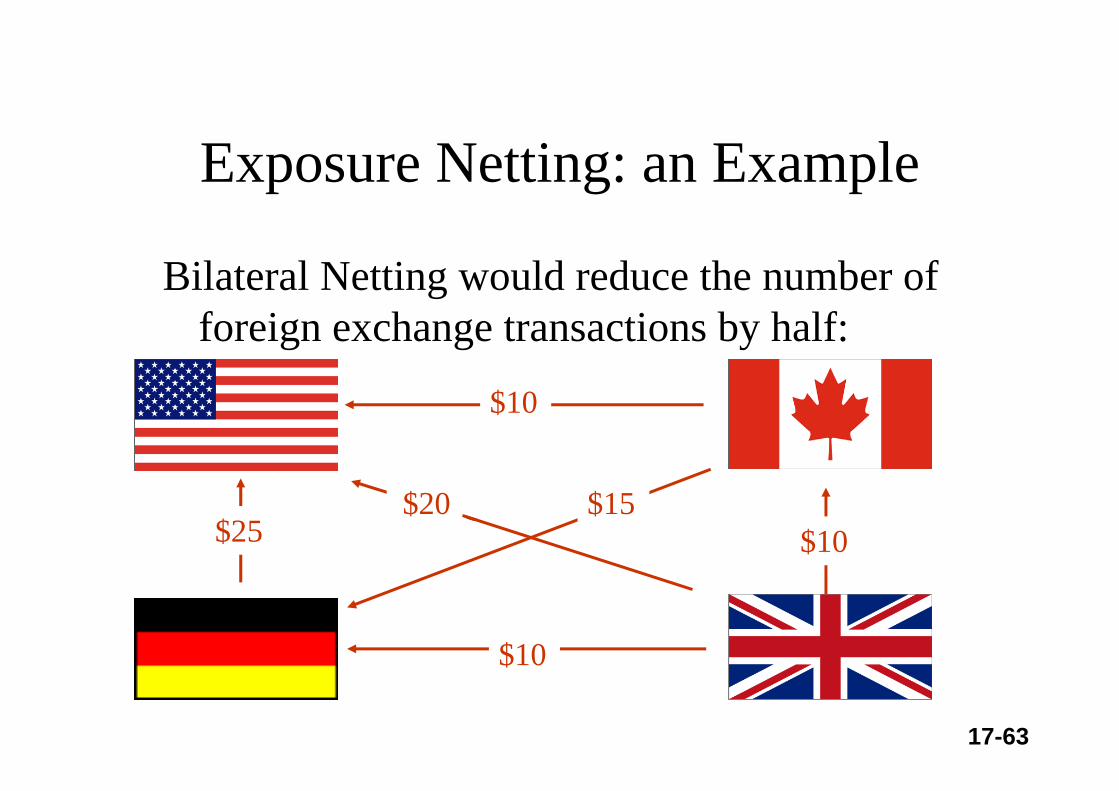

Exposure Netting: an Example

Consider a U.S. MNC with three subsidiaries and the following foreign exchange transactions:

$10 $35 $40$30

$20

$25 $60

$40$10

$30

$20$30

17-63

Exposure Netting: an Example

Bilateral Netting would reduce the number of foreign exchange transactions by half:

$10 $35 $40$30

$20

$40

$30

$20$30

$20$30$10

$40$30$10

$30$20

$60

$10 $35$25

$60

$40$20

$25 $10

$25 $10$15

$10

17-64

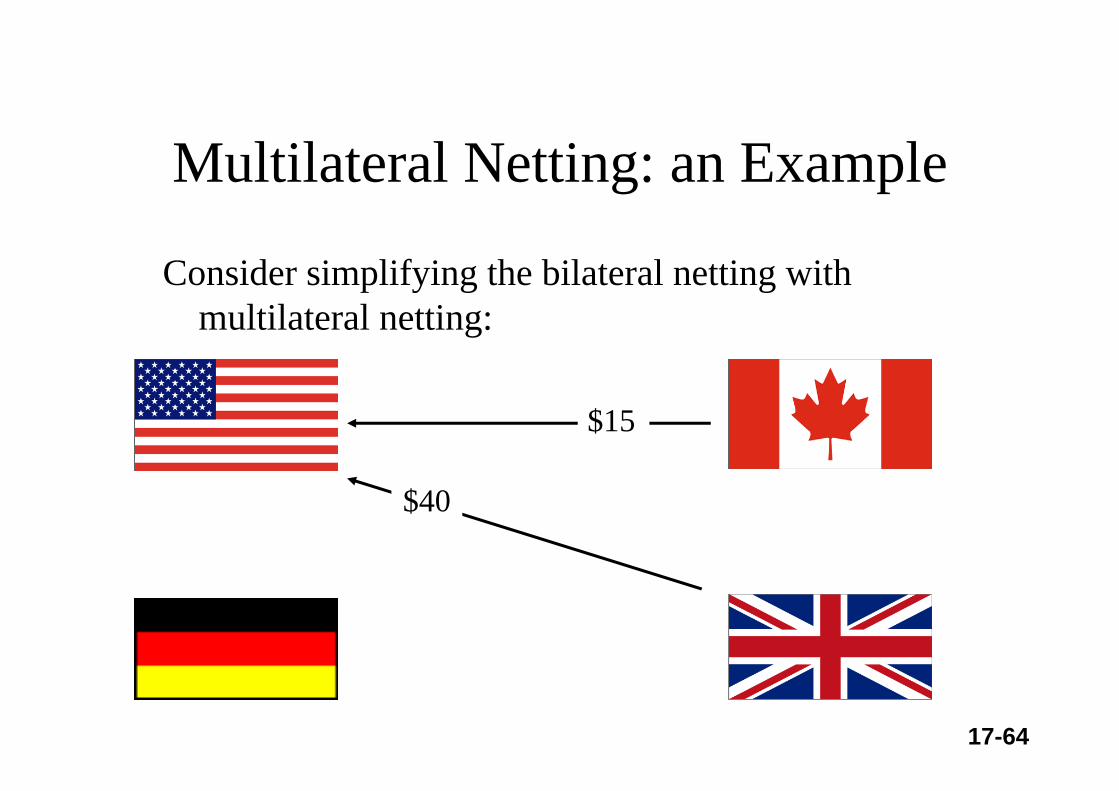

Multilateral Netting: an Example

Consider simplifying the bilateral netting with multilateral netting:

$25 $10$20

$10

$10$10

$15 $10

$10

$30 $15 $10

$10

$40$15

$15 $40$40

$15

17-65

Should the Firm Hedge?

• Not everyone agrees that a firm should hedge:– Hedging by the firm may not add to

shareholder wealth if the shareholders can manage exposure themselves.

– Hedging may not reduce the non-diversifiable risk of the firm. Therefore shareholders who hold a diversified portfolio are not helped when management hedges.

17-66

Should the Firm Hedge?

• In the presence of market imperfections, the firm should hedge.– Information Asymmetry

• The managers may have better information than the shareholders.

– Differential Transactions Costs• The firm may be able to hedge at better prices than

the shareholders.– Default Costs

• Hedging may reduce the firms cost of capital if it reduces the probability of default.

17-67

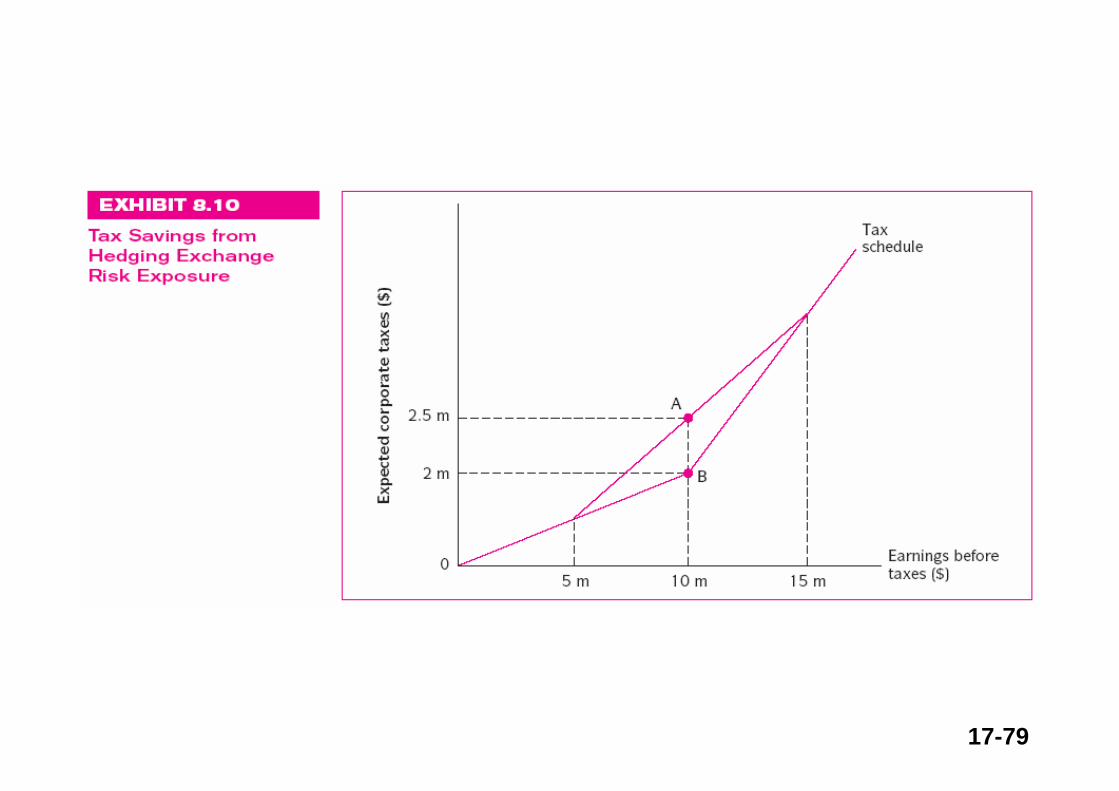

Should the Firm Hedge?

• Taxes can be a large market imperfection.– Corporations that face progressive tax rates

may find that they pay less in taxes if they can manage earnings by hedging than if they have “boom and bust” cycles in their earnings stream.

17-68

What Risk Management Products do Firms Use?

• Most U.S. firms meet their exchange risk management needs with forward, swap, and options contracts.

• The greater the degree of international involvement, the greater the firm’s use of foreign exchange risk management.

17-69

17-70

17-71

17-72

17-73

17-74

17-75

17-76

17-77

17-78

17-79

17-80

17-81

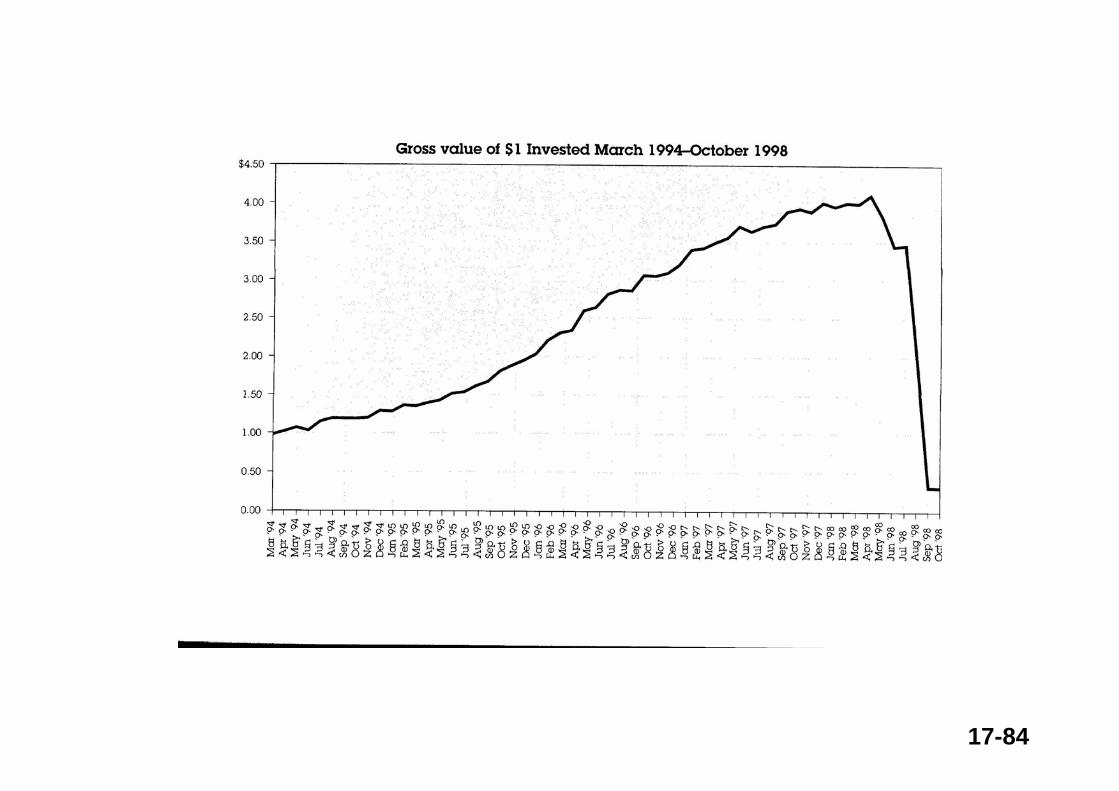

LTCM began trading in 1994, after completing a road show that, despite the Ph.D.-touting partners' disdainful condescension of potential investors who couldn't rise to their intellectual level, netted a whopping $1.25 billion. The fund would seek to earn a tiny spread on thousands of trades, "as if it were vacuuming nickels that others couldn't see," in the words of one of its Nobel laureate partners, Myron Scholes. And nickels it found. In its first two years, LTCM earned $1.6 billion, profits that exceeded 40 percent even after the partners' hefty cuts. By the spring of 1996, it was holding $140 billion in assets. But the end was soon in sight, and Lowenstein's detailed account of each successively worse month of 1998, culminating in a disastrous August and the partners' subsequent panicked moves, is riveting.

17-82

LTCM began operating in 1994, set up by John Meriwether formally head of the bond-arbitrage group at Solomon Brothers. He put together a star-studded cast that included the (1997) Nobel prize winners in economics. Their basic strategy was something called convergence arbitrage. In essence this strategy says buy two bonds that you think will track one another. Go long on the cheap one and short on the other; you make money if the spread narrows. In theory you are protected from changing prices as long as the two vary in the same way. To make the big bucks LTCM was after they took a gigantic number of highly leveraged arbitrage positions all over the world. To get high leverage you borrow for the position, like buying a stock on margin. LTCM got really high leverage by avoiding something called the "haircut," which is an extra margin of collateral banks usually demand, but forgave LTCM. Why would banks then do such a thing? Because they were blinded by the glitter of the cast, and in some cases the banks themselves were investors in LTCM.

17-83

By 1997 convergence arbitrage opportunities in bonds began to dry up, everyone was doing it. So LTCM applied their strategy to stocks. Find two stocks that will track one another and go long and short with borrowed money. This is not easy. Stocks are less amenable to mathematical analysis than bonds, and after all these were the bond guys from Solomon, they were out of their depth. You might ask how can you borrow most of your stock position when the Federal Reserve requires 50% margin (Regulation T). Answer: don't really buy the stocks, instead buy derivative contracts that simulate stocks, an end run around Regulation T. Even with all this leverage LTCM would claim that the fund was no more risky than the stock market, meaning a stock index. In 1998 the markets went against LTCM, with the "flight to quality" (US government bonds) as investors panicked. The fund suffered from what reliability engineers call "common mode error." Spreads got wider not narrower across the board, and LTCM'scapital base began to shrink as their positions lost money. At a certain point they would have to start liquidating positions, and the market impact of such large scale selling would cascade across their portfolio. The fund would "blow up."

17-84

17-85

Long-Term Capital Management, L.P. (LTCM) was in the business of engaging in trading strategies to exploit market pricing discrepancies. Because the firm employed strategies designed to make money over long horizons--from six months to two years or more--it adopted a long--term financing structure designed to allow it to withstand short-term market fluctuations. In many of its trades, the firm was in effect a seller of liquidity. LTCM generally sought to hedge the risk--exposure components of its positions that were not expected to add incremental value to portfolio performance and to increase the value-added component of its risk exposures by borrowing to increase the size of its positions. The fund's positions were diversified across many markets. This case is set in September 1997, when, after three and a half years of high investment returns, LTCM's fund capital had grown to $6.7 billion. Because of the limitations imposed by available market liquidity, LTCM was considering whether it was a prudent and opportune moment to return capital to investors.

Long-Term Capital Management, L.P. (A)

17-86

Setting:Connecticut; Finance; 1997-1998

Subjects Covered:Arbitrage, Capital markets, Efficient markets, Financial institutions, Investment management, Risk management.

Learning Objective:To discuss a broad range of issues relating to arbitrage, marketefficiency, implementation of investment strategies, liquidity shocks, risk management, financial intermediation, investment management, hedge funds, incentives, systemic risk, and regulation.

17-87

Long-Term Capital Management, L.P. (LTCM) was in the business of engaging in trading strategies to exploit market pricing discrepancies. Because the firm employed strategies designed to make money over long horizons--from six months to two years or more--it adopted a long--term financing structure designed to allow it to withstand short-term market fluctuations. In many of its trades, the firm was in effect a seller of liquidity. LTCM generally sought to hedge the risk--exposure components of its positions that were not expected to add incremental value to portfolio performance and to increase the value-added component of its risk exposures by borrowing to increase the size of its positions. The fund's positions were diversified across many markets. This case is set in late August 1998. LTCM's fund was down nearly 40% since the beginning of 1998, with most of this loss having occurred in recent weeks. LTCM was evaluating the fund's liquidity and considering alternative courses of action. Possible choices included attempting a rapid reduction of many of the fund's positions and trying to raise additional capital.

Long-Term Capital Management, L.P. (C)

17-88

Setting:Connecticut; Finance; 1997-1998

Subjects Covered:Arbitrage, Capital markets, Efficient markets, Financial institutions, Investment management, Risk management.

Learning Objective:To discuss a broad range of issues relating to arbitrage, marketefficiency, implementation of investment strategies, liquidity shocks, risk management, financial intermediation, investment management, hedge funds, incentives, systemic risk, and regulation.

17-89

International Financial Risk Management

How Leeson Broke Barings

17-90

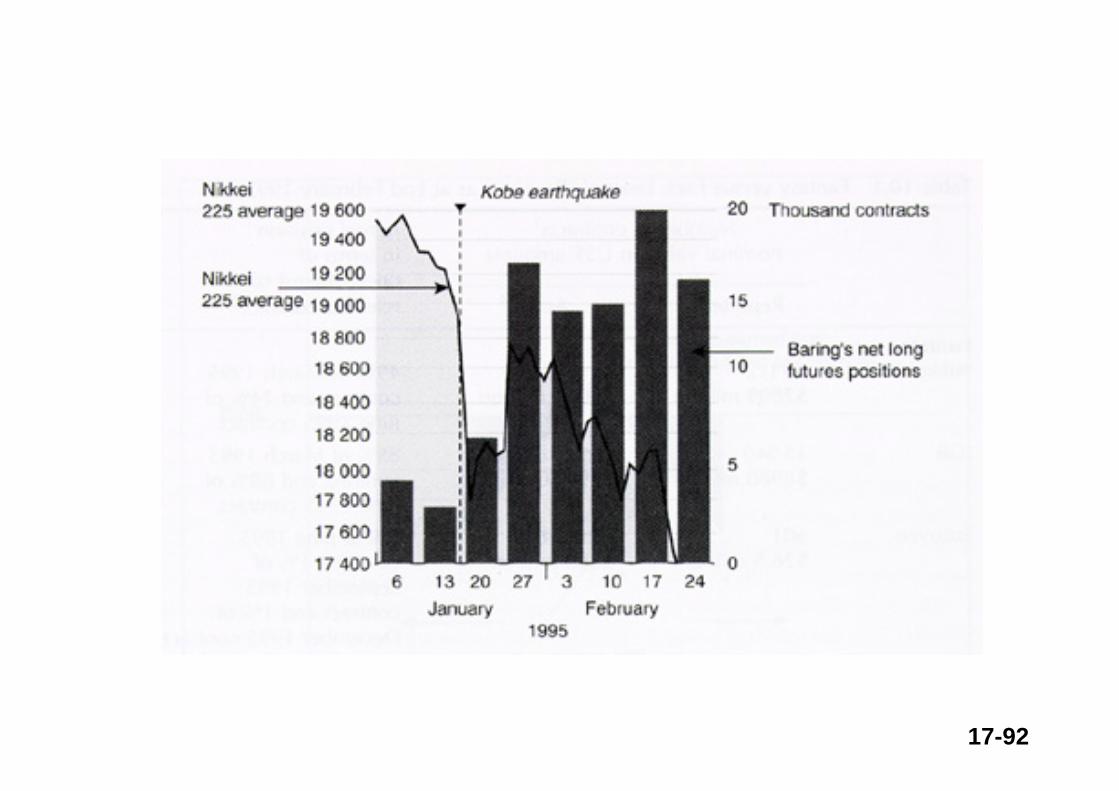

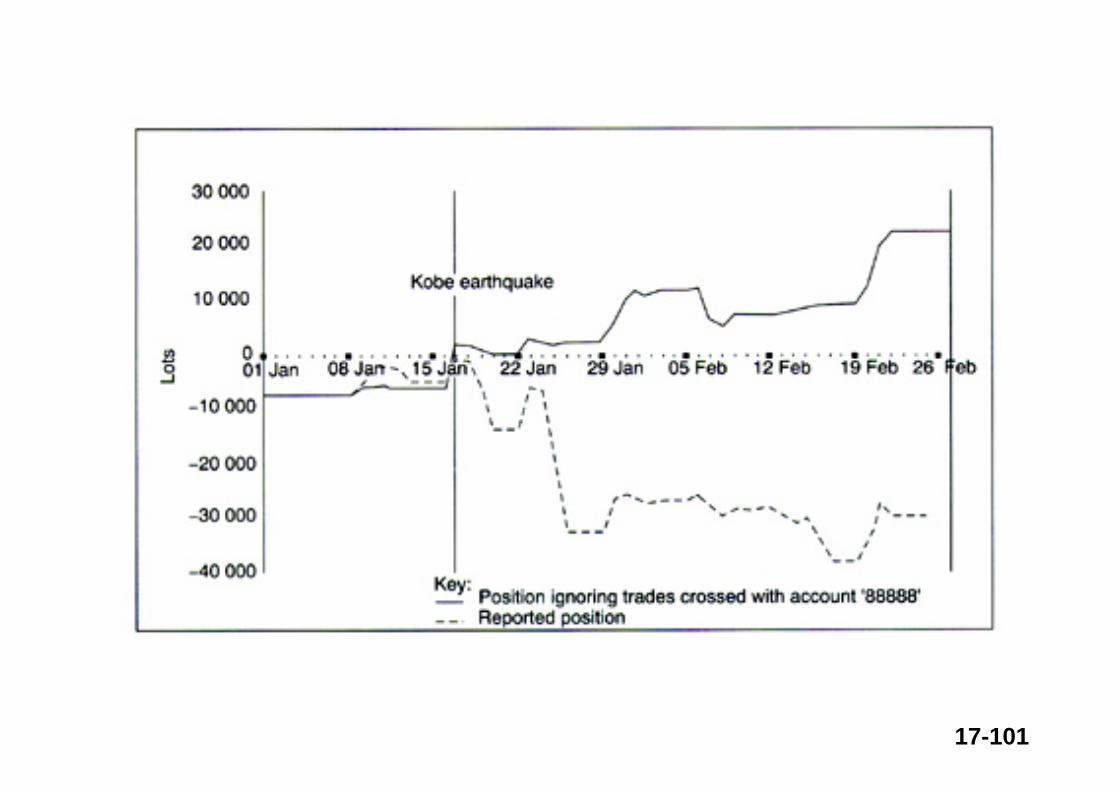

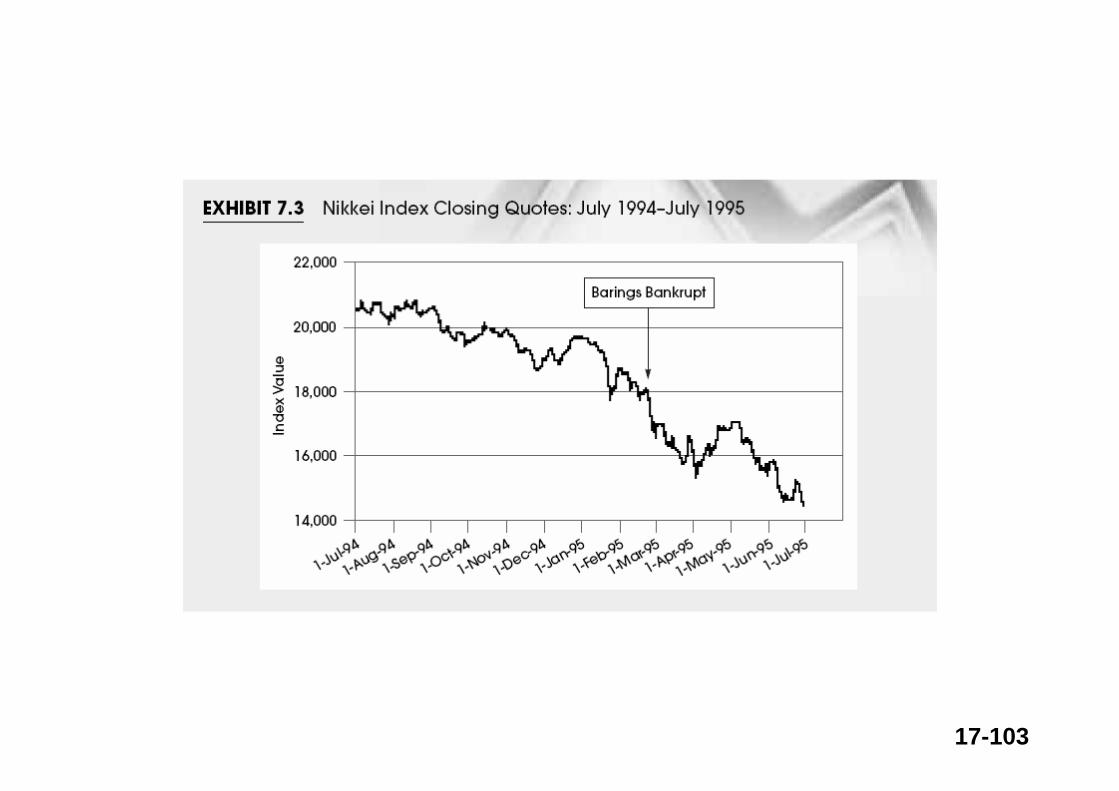

The activities of Nick Leeson on the Japanese and Singapore futures exchanges, which led to the downfall of his employer, Barings, are well-documented.

Barings collapsed because it could not meet the enormous trading obligations, which Leeson established in the name of the bank. When it went into receivership on February 27, 1995, Barings, via Leeson, had outstanding notional futures positions on Japanese equities and interest rates of US$27 billion: US$7 billion on the Nikkei 225 equity contract and US$20 billion on Japanese government bond (JGB) and Euroyen contracts. Leeson also sold 70,892 Nikkei put and call options with a nominal value of $6.68 billion. The nominal size of these positions is breathtaking; their enormity is all the more astounding when compared with the banks reported capital of about $615 million.

17-91

The size of the positions can also be underlined by the fact that in January and February 1995, Barings Tokyo and London transferred US$835 million to its Singapore office to enable the latter the meet of its margin obligations on the Singapore International Monetary Exchange (SIMEX).

17-92

17-93

17-94

17-95

http://www.aw-bc.com/scp/0321197488/assets/downloads/ch7.pdf

17-96

Nicholas (“Nick”) William Leeson was relaxing at a luxuryresort in Malaysia when he heard that Barings Bank PLC,Britain’s oldest bank, had lost $1.2 billion (£860 million) andwas in administration (i.e., Chapter 11 bankruptcy). He wasshocked, but Leeson should not have been: it was his massivespeculative losses on the futures market over a briefthree-year period that wiped out the net worth of this venerable bank.

Leeson worked at the Singapore branch of Barings BankPLC, the blue-blooded British merchant bank founded in1763 that catered to royalty and was at the pinnacle of theLondon financial world. Among its many accomplishmentsover the centuries, Barings financed both the Louisiana Purchase in 1803 and the Napoleonic Wars. But the road to success was not always smooth. The bank endured both warsand depressions, and it overcame near-bankruptcy in 1890,surviving only because it was bailed out at the last minuteby the Bank of England. In spite of these sporadic periods ofturmoil, Barings was always one of the most well-placed

17-97

and highly regarded players in London’s financial hub. Howironic that this centuries-old bank would be toppled by oneman operating out of Barings’ remote Singapore affiliate.Leeson was the chief trader for Barings’ Singapore affiliate,dealing mainly in futures contracts on both the Nikkei 225index and 10-year Japanese government bonds. Due to hishuge trading profits, Leeson earned a reputation amongBarings’ management in London, Tokyo, and Singapore as astar performer, and he was given virtually free rein. Manyof Barings Bank’s top management believed that Leesonpossessed an innate feel for the markets, but the story ofthis rogue trader reveals that he had nothing of the sort.How, one wonders, could Barings’ management have beenso seriously mistaken and for so long?

This chapter addresses two main questions about theBarings collapse: why did the bank give Leeson so muchdiscretionary authority to trade, allowing him to operatewithout any effective trading restraints by managers andinternal control systems; and what trading strategy didLeeson employ to lose so much in such a short time?

17-98

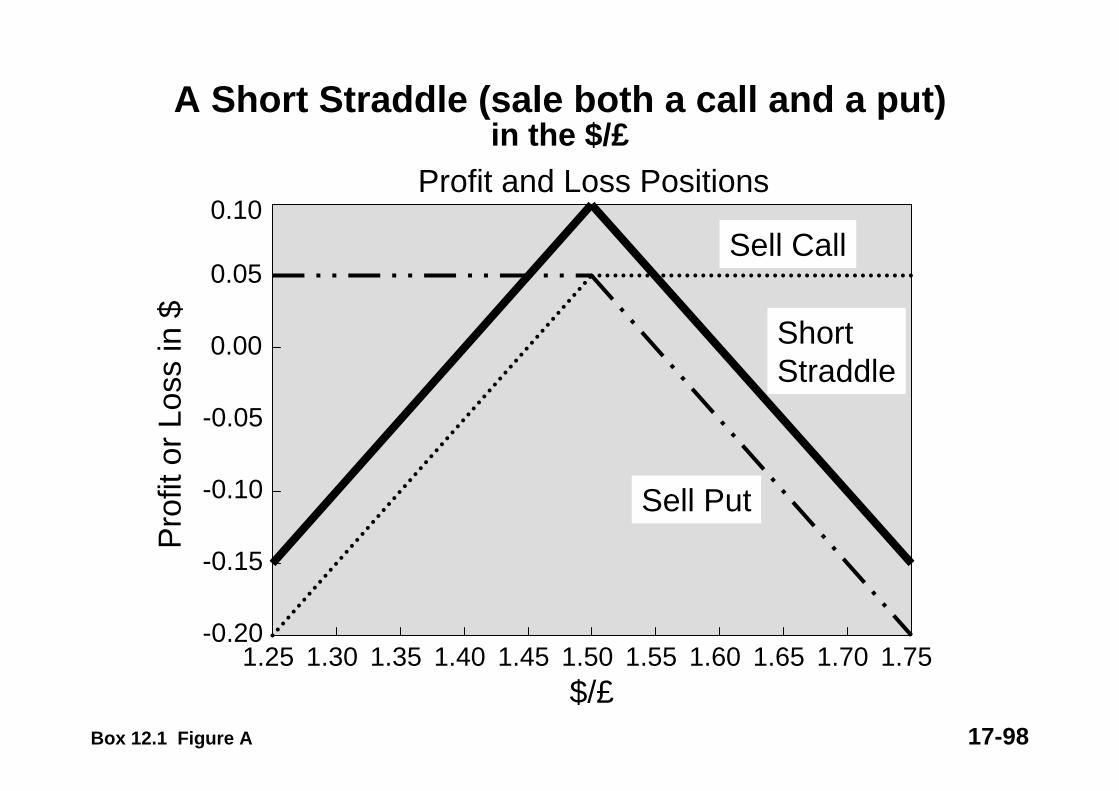

A Short Straddle (sale both a call and a put) in the $/£

0.10

0.05

0.00

-0.05

-0.10

-0.15

-0.201.25 1.30 1.35 1.40 1.45 1.50 1.55 1.60 1.65 1.70 1.75

Pro

fit o

r Los

s in

$

$/£

Profit and Loss Positions

Sell Call

Sell Put

ShortStraddle

Box 12.1 Figure A

17-99

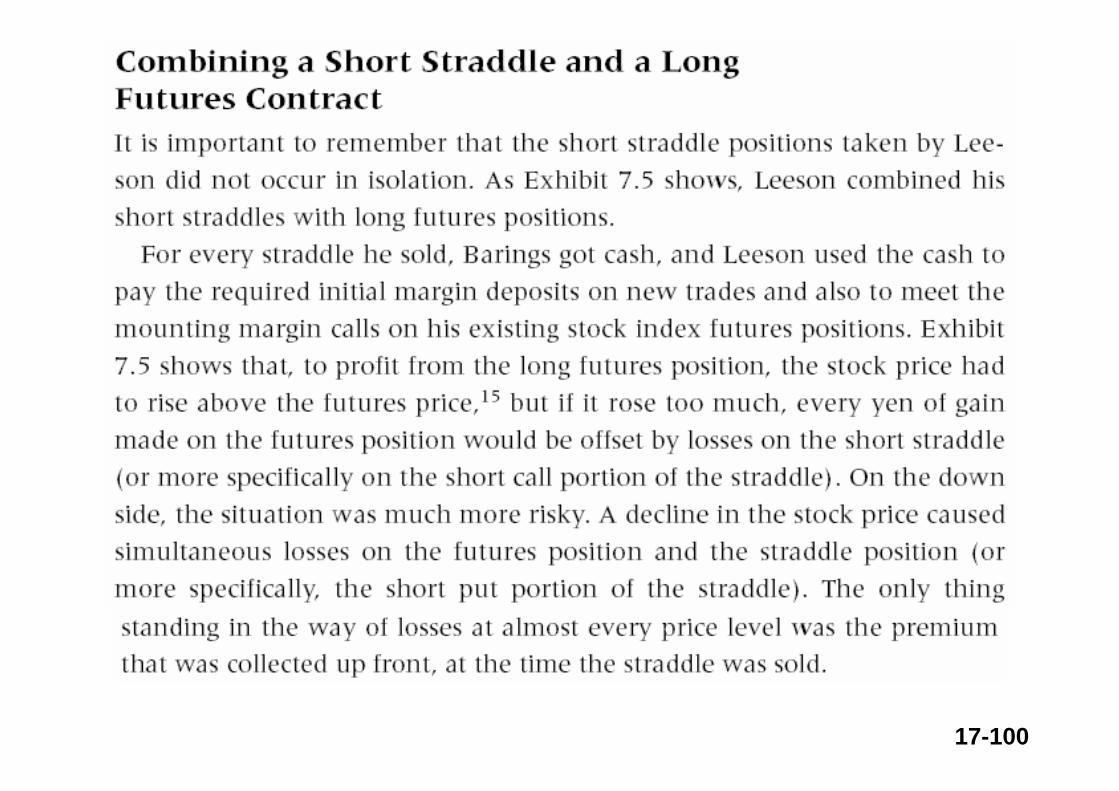

17-100

17-101

17-102

17-103

17-104

17-105

17-106

Topics in Financial Contract DesignEpisode--Italian Asset Swap Volumes Soar on Buyback PlansVolumes in the basis-swap spread market doubled last week as traders entered swaps in response to the Italian treasury's announcement that it "does not rule out buybacks." Traders said the increase in volume was exceptional given that so many investors are on holiday at this time of year.Traders and investors were entering trades designed to profit if the treasury initiates a buyback program and the bonds increase in value as they become scarcer and outperform the swaps curve. A trader,said in a typical trade the investor owns the 30-year Italian government bond and enters a swap in which it pays the 6% couponand receives 10.5 basis points over six-month Euribor. "Since traders started entering the position last Monday the spread has narrowed to 8 bps over Euribor," he added. The trader thinks the spread could narrow to 6.5 bps over Euribor within the next month if conditions in the equity and emerging markets improve. A trader at a major European bank predicts this could go to Euribor flat over the next six months. The typical notional size of the trades is EUR50 million(USD43.65 million) and the maturity is 30 years. (IFR Issue 1217)

17-107

(a) Suppose there is an Italian swap curve along with a yield curve obtained from Italian government bonds (sovereign curve). Suppose this latter is upward sloping. Discuss how the two curves might shift relative to each other if the Italian government buys back some bonds.

(b) Is it important which bonds are bought back? Discuss.(c) Show the cash flows of a 5-year Italian government

coupon bonds (paying 6%) and the cash flows of a fixed-payer interest-rate swap.

(d) What is the reason behind the existence of the 10.15 bpspread?

(e) What happens to this spread when government buys back bonds? Show your conclusions using cash flow diagrams.

17-108

Episode--Foreigners buying Australian dollar instruments issued in Australia have to pay withholding taxes on interest earnings. This withholding tax can be exploited in tax-arbitrage portfolios using swaps and bonds. First let us consider an episode from the markets related to this issue.Under Australia's withholding tax regime, resident issuers have been relegated to second cousin status compared with nonresident issuers in both the domestic and international markets. Something has to change.In the domestic market, bond offerings from resident issuers incur the 10% withholding tax. Domestic offerings from nonresident issuers, commonly known as Kangaroo bonds, do not incur withholding tax because the income is sourced from overseas. This raises the spectre of international issuers crowding out local issuers from their own markets.

17-109

In the international arena, punitive tax rules restricting coupon washing have reduced foreign investor interest in Commonwealth government securities and semi-government bonds. This has facilitated the growth of global Australian dollar offerings by Triple A rated issuers such as Fannie Mae, which offer foreign investors an attractive tax-free alternative.The impact of the tax regime is aptly demonstrated in the secondary market. Exchangeable issues in the international markets from both Queensland Treasury Corporation and Treasury Corporation of NSW are presently trading through comparable domestic issues. These exchangeable issues are exempt from withholding tax.If Australia wishes to develop into an international financial centre, domestic borrowers must have unfettered access to the international capital markets—which means compliance costs and uncertainty over tax treatment must be minimized. Moreover, for the Australian domestic debt markets to continue to develop, the inequitable tax treatment between domestic and foreign issues must be corrected. (IFR, Issue 1206)

17-110

We now consider a series of questions dealing with this problem. First, take a 4-year straight coupon bond issued by a local government that pays interest annually. We let the coupon rate be denoted by c%. Next, consider an Aussie dollar Eurobond issued at the same time by a Spanish company. The Eurobond has a coupon rate d%. The Spanish company will use the funds domestically in Spain. Finally, you know that interest rate swaps or FRAsin Aussie$ are not subject to any tax,

(a) Would a foreign investor have to pay the withholding tax on the Eurobond? Why or why not?

(b) Suppose the Aussie$ IRSs are trading at a swap rate of d + 10bp. Design a 4-year interest rate swap that will benefit from tax arbitrage. Display the relevant cash flows.

(c) If the swap notional is denoted by N, how much would the tax arbitrage yield?(d) Can you benefit from the same tax-arbitrage using a strip of FRAs in Aussie$?(e) Which arbitrage portfolio would you prefer, swaps or FRAs? For what reasons?(f) Where do you think it is more profitable for the Spanish company to issue bonds

under these conditions, in Australian domestic markets or in Euromarkets? Explain.

17-111

Errata: Real Option CalculationBy YTF

M (1,728) – (1 + .08) (B) = 928M (1,200) – (1 + .08) (B) = 400• M=1, B=741• 1 * 1,440 – 741 = 699M (1,200) – (1 + .08) (B) = 400M (833) – (1 + .08) (B) = 33• M = 1, B=741• 1 * 1,000 – 741 = 259M (833) – (1 + .08) (B) = 33M (579) M (579) –– (1 + .08) (B) = 0(1 + .08) (B) = 0• M = 0.13, B = 70• 0.13 * 694 – 70 = 20

M (1,440) – (1 + .08) (B) = 699M (1,000) – (1 + .08) (B) = 259• M = 1, B = 686• 1 * 1,200 – 686 = 514M (1,000) – (1 + .08) (B) = 259M (694) – (1 + .08) (B) = 21• M = .777, B = 479• .777 * 833 – 479 = 169M (1,200) – (1 + .08) (B) = 114M (833) M (833) –– (1 + .08) (B) = 0(1 + .08) (B) = 0• M = .31, B = 239• .31 * 1,000 – 239 = 71

From Event Tree Strategic Decision with flexibilityStrategic Decision with flexibility