lifo n fifo

TRANSCRIPT

Fundamentals of AccountingINVENTORY VALUATION

InventoryInventory is the one of the largest current asset of a retail store or of a whole business merchandise. The sale of this inventory is the main source of revenue.

Inventory contains materials/Products in three forms of conditions

Raw MaterialsThe materials needed to make anything are called raw materials.The initial condition of any material is its raw form.Some work is needed to make a raw material into something useful

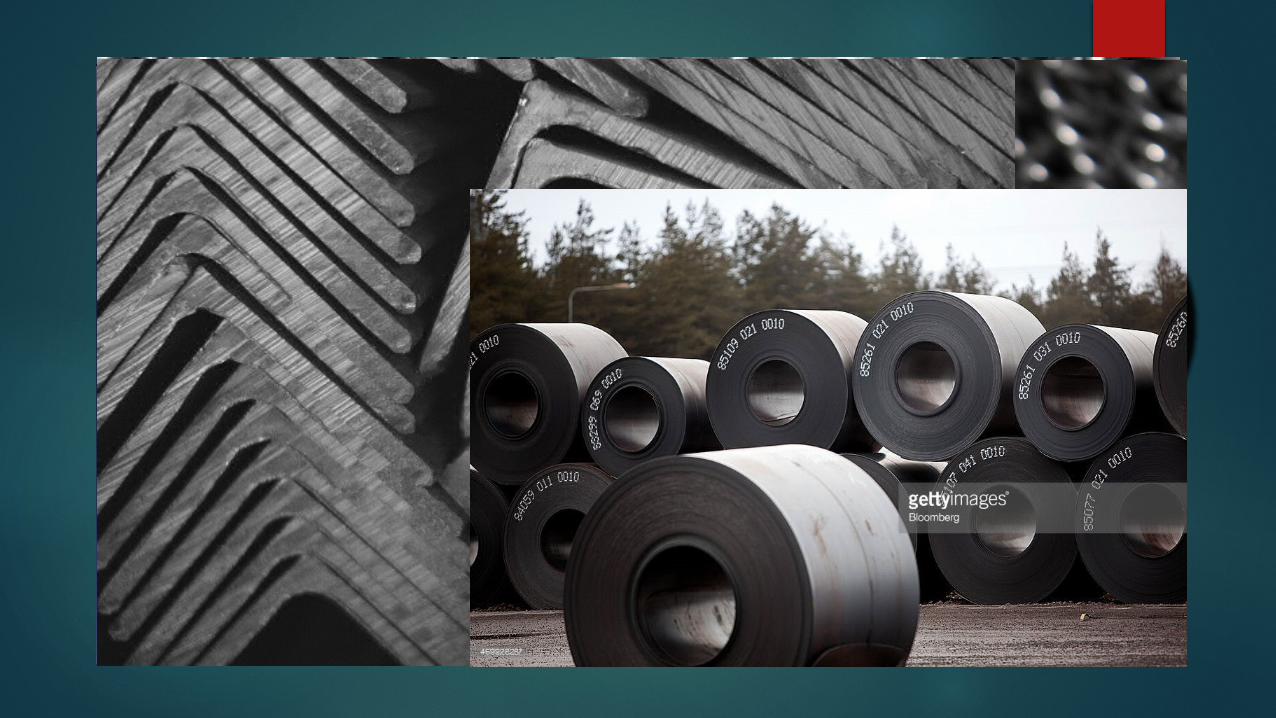

Consider we were making something using steel

Steel in raw form

WIP (Work in process)The process of making raw materials into some useful things

Steel is melted to reshape it into something useful

Finished GoodThe finished product formed after doing some work on raw material.The price of finished product is considerably high from raw material

We can make numerous useful products using same raw material

LIFO Last in First out

In LIFO the last formed products were sold earlier then first products

Products

Sold

Advantages of LIFOIn times of rising prices LIFO is beneficial because in LIFO the last purchased products (which were expensive than older) were sold Earlier. So the first products will be sell at greater profit.

Purchased

Selling Price = 100

80

80

80

Profit2020 20

Selling Price = 150

130130

Selling Price = 200

180

70 120

To overcome it the products last purchased were sold with lower profit The advantage of lower profit is that you don’t have to pay more income-taxes

But in this way income-taxes increasesThe more the profit the more the income-tax has to pay

You can also sell first products at same profit and lower price. So in this way you can variate your price. It also happies customers.

Sold at 110

20 20

Sold at 60

LIFO is also beneficial in (Non-Expiring) products.

For example

The price of Rice increases as it gets older

Also in Non-Muslim countries the price of Wine increases as it gets older.

So if we’re using LIFO the cost of old rice and wine keeps rising until we sold them.

FIFO First in First out

In FIFO the first formed products were sold earlier than last formed products

Products

Sold

Advantages of FIFOThe main advantage of FIFO is that the products were less likely to expire. Because in FIFO the oldest product is sold earlier

When you’re using FIFO your inventory is showing latest prices of the products because the old products were already sold.

If Inflation (Increase in market prices) occurs. FIFO decreases the impact of inflation on the company

Purchased

200030005000

Market Price = 2000Market Price = 3000Market Price = 5000

Profit3000

Market Price = 6000

6000

30001000Instead of Market Price = 7000

Inventory Valuation is recorded in balance sheet

Purchased Sold BalanceDate Unit

sUnit Cost

Total Cost Unit

sUnits

Unit Cost

Unit Cost

Total CostTotal Cost

5 Feb 2 1000 2000

2 1000 2000

7 Feb 7 1200 8400

27

10001200 10400

10 Feb 1 1000 1000 17

10001200 9400

12 Feb 1 1000 1000 07

10001200 8400

FIFO

Purchased Sold BalanceDate Unit

sUnit Cost

Total Cost Unit

sUnits

Unit Cost

Unit Cost

Total CostTotal Cost

5 Feb 2 1000 2000

2 1000 2000

7 Feb 7 1200 8400

27

10001200 10400

10 Feb 1 1200 1200 26

10001200 9200

12 Feb 2 1200 2400 24

10001200 6800

LIFO

Purchased Sold BalanceDate Unit

sUnit Cost

Total Cost Unit

sUnits

Unit Cost

Unit Cost

Total CostTotal Cost

5 Feb 2 1000 2000

2 1000 2000

7 Feb 3 1200 3600

5 1120 5600

10 Feb 1 1120 1120 4 1120 4480

Average

2000+3600=5600

2+3=5 5600/5=11

20

The End