lehigh accounting programs

TRANSCRIPT

Department of Accounting

Lehigh Accounting Programs&

State-Law Education Requirements for the CPA Exam & CPA Licensure by

New York, New Jersey and Pennsylvania

2

Topics we will cover today…

1. Statutory educational requirements of NY, NJ and PA to…

– Sit for the CPA exam

– Obtain a CPA license

2. Degree requirements for Lehigh’s accounting major

3. Lehigh’s Recent First-Time Pass Rates by Exam Section

– Recommended elective courses

4. Planning to meet the 150-hour requirement

5. Advice from students currently taking parts of the exam

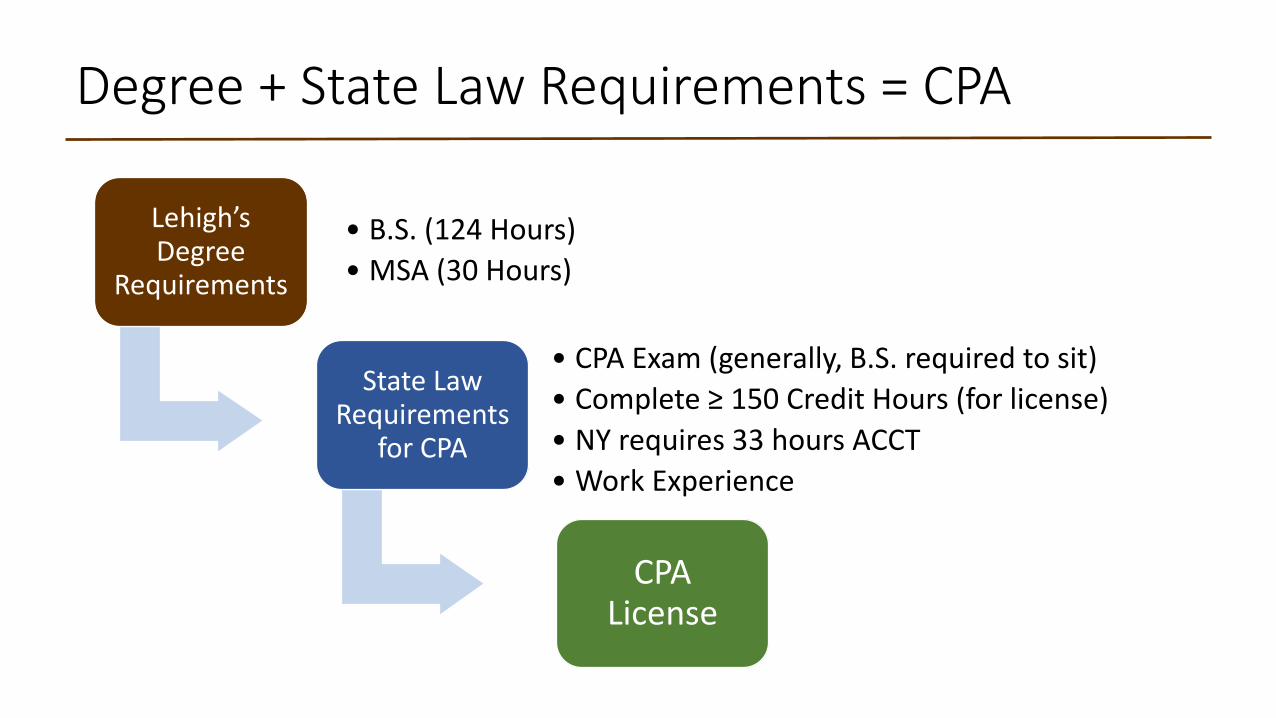

Degree + State Law Requirements = CPA

Lehigh’s Degree

Requirements

• B.S. (124 Hours)

• MSA (30 Hours)

State Law Requirements

for CPA

• CPA Exam (generally, B.S. required to sit)

• Complete ≥ 150 Credit Hours (for license)

• NY requires 33 hours ACCT

• Work Experience

CPA License

Minimum Education to Sit For CPA Exam

New York New Jersey Pennsylvania120 sit rule: At least 120 SH of course work, including 1 course in each of the following areas:

Financial accounting & reporting (upper level)

Cost or management accounting

Taxation

Auditing & attestation (upper level)

Bachelor’s or higher degree

At least 120 SH of college credit, including:

– At least 24 SH in accounting courses and

– At least 24 SH in general business courses (other than accounting)

Bachelor’s or higher degree

At least 24 SH in accounting and auditing, business law, finance or tax subjects of a content satisfactory to the board.

Helpful Source: https://nasba.org/exams/cpaexam/ (then scroll down for menu of states)

Minimum Education for CPA License

New York New Jersey PennsylvaniaBachelor’s degreeCompletion of 150 SH including: 33 SH in ACCT with at least 1

course in each of the four areas shown above, and

36 SH in general business courses

Must include the study of: Business or accounting

communications, Ethics & professional

responsibilities, and Accounting research

Bachelor’s or higher degree

At least 150 SH of college credit, including:– At least 24 SH in

accounting courses and– At least 24 SH in general

business courses (other than accounting))

Bachelor’s or higher degree

Completion of 150 SH including at least 24 SH of accounting and auditing, business law, finance or tax subjects.

More on New York…

New YorkBachelor’s degree…

Must include the study of: Business or accounting

communications, Ethics & professional

responsibilities, and Accounting research

These topics must be included in the curriculum, either as stand-alone courses or integrated into other courses. Lehigh’s accounting program integrates these topics into other courses (e.g., accounting research is covered in ACCT 307 and ACCT 316).

Students should retain electronic copies of all course syllabi as documentation of topics covered in their coursework.

Master’s degree: New York law stipulates that receipt of Master’s degree in accounting from an AACSB accredited accounting program will be deemed as meeting New York's 150 semester hour education requirements for licensure.

Undergraduate Major in Accounting

SophomorePrerequisites

ACCT 151 – Intro FinancialACCT 152 – Intro Managerial

+ AccountingCore

(Junior Year)

ACCT 315 – Intermediate Financial IACCT 324 – Cost AccountingACCT 316 – Intermediate Financial IIACCT 311 – Accounting Information Systems

+ ConcentrationSelect 1 of 3

“tracks”(Senior Year)

Public AccountingACCT 307: TaxACCT 317: Advanced FinancialACCT 320: Auditing

Financial Services & CorpFIN 323: InvestmentsFIN 328: Corp Financial PolicyACCT 318: Financial Stmt Analysis

Information SystemsACCT 320: AuditingACCT 330: Data AnalyticsOne BIS 300-level course

ACCT Hours 27 21 24

NY Exam Lacking Tax & Auditing Lacking Tax

NY License + 6 ACCT & 150 overall+ 12 ACCT (incl. Tax & Auditing) &

150 overall+ 9 ACCT (incl. Tax) & 150

overall

Elective ACCT courses at Lehigh

Courses that NY will count as “accounting” semester hours

• ACCT 309—Advanced Federal Income Tax (every spring semester)

• ACCT 318—Financial Statement Analysis (every spring semester)

• ACCT 330 —Accounting Data Analytics (S 2019, F 2019, F 2020)

• Option to take 400-level MACC course

Courses that NY will count toward 150, but not as “accounting”

• ACCT 098—Segal Distinguished Speaker Series (every fall)

2017 First-Time Pass Rate by Exam Section

AUD BEC FAR REG

AACSB-Acct

Overall (all 1st time) 58.6% 70.7% 56.0% 56.9%

1st time within 1-year of Graduation 57.4% 70.2% 57.2% 56.1%

LEHIGH

Overall (all 1st time) 80.4% 94.4% 66.7% 61.5%

1st time within 1-year of Graduation 90.0% 94.3% 73.9% 76.0%

2018 First-Time Pass Rate by Exam Section

AUD BEC FAR REG

AACSB-Acct

Overall (all 1st time) 61.0% 76.9% 57.7% 63.9%

LEHIGH

Overall (all 1st time) 79.6% 95.3% 80.4% 68.7%

What is REG?

Uniform CPA Examination Blueprint(Effective Date: Jan. 1, 2019)Regulation (REG)Content area allocation WeightI. Ethics, Professional Responsibilities and Federal Tax

Procedures (10–20%)II. Business Law (10–20%)III. Federal Taxation of Property Transactions (12–22%)IV. Federal Taxation of Individuals (15–25%)V. Federal Taxation of Entities (28–38%)

https://www.aicpa.org/content/dam/aicpa/becomeacpa/cpaexam/examinationcontent/downloadabledocuments/cpa-exam-blueprints-effective-jan-2019.pdf

Overall, REG is roughly 85% TAX

15% Business Law

Consider taking ACCT 309

Business Law courses at Lehigh

LAW 201 Legal Environment of Business (3 Credits)—CBE Core Requirement

This course examines the legal relationships between business and government, business and society, and the individual and society. A significant focus of the course is on the structure of the U.S. legal system, the role of the courts in the legal system, and contract law as the principal mechanism for the private allocation of resources and risk allocation. The course also focuses on business ethics with particular emphasis on corporate social responsibility. Junior standing is required.Prerequisites: (ECO 001)

LAW 202 Business Law (3 Credits)—CBE Elective

The law of agency, business organizations, secured transactions, bankruptcy and negotiable instruments.Prerequisites: (LAW 201)

What Business Law topics are on the CPA exam?

A. Agency1. Authority of principals and agents2. Duties and liabilities of agents and principals

B. Contracts1. Formation2. Performance3. Discharge, breach and remedies

C. Debtor-creditor relationships1. Rights, duties & liabilities of debtors, creditors and guarantors2. Bankruptcy & insolvency3. Secured transactions

D. Government regulation of business1. Federal securities regulation2. Other federal laws & regulations

E. Business Structure1. Selection and formation of business entity and related operations and termination2. Rights, duties, legal obligations and authority of owners and management

Overall, REG is roughly 85% TAX

15% Business Law

Most relevant topics are covered in

LAW 202

Resources for State Rules, Exam Application, etc.

• NASBA.org

• Candidate Bulletin 2020

• https://nasba.org/app/uploads/2020/01/Candidate-Bulletin-2020_January-2020v5.pdf

What Questions Do You Have?