law practice management class #7 – malpractice and professional liability insurance

TRANSCRIPT

Law Practice Law Practice ManagementManagement

Class #7 – Class #7 – Malpractice and Malpractice and Professional Liability InsuranceProfessional Liability Insurance

Insurance?Insurance?

• Only a fool goes “bare” in today’s litigious Only a fool goes “bare” in today’s litigious societysociety

• Professional liability does not depend on Professional liability does not depend on whether or not you collected a feewhether or not you collected a fee

• You You WILLWILL be sued at some point in your legal be sued at some point in your legal careercareer

• In order to participate in a “lawyer referral In order to participate in a “lawyer referral service” in FL must have professional liability service” in FL must have professional liability insurance in an amount not less than $100,000 insurance in an amount not less than $100,000 per claim or occurrence Rule 4-7.10(a)(4) per claim or occurrence Rule 4-7.10(a)(4)

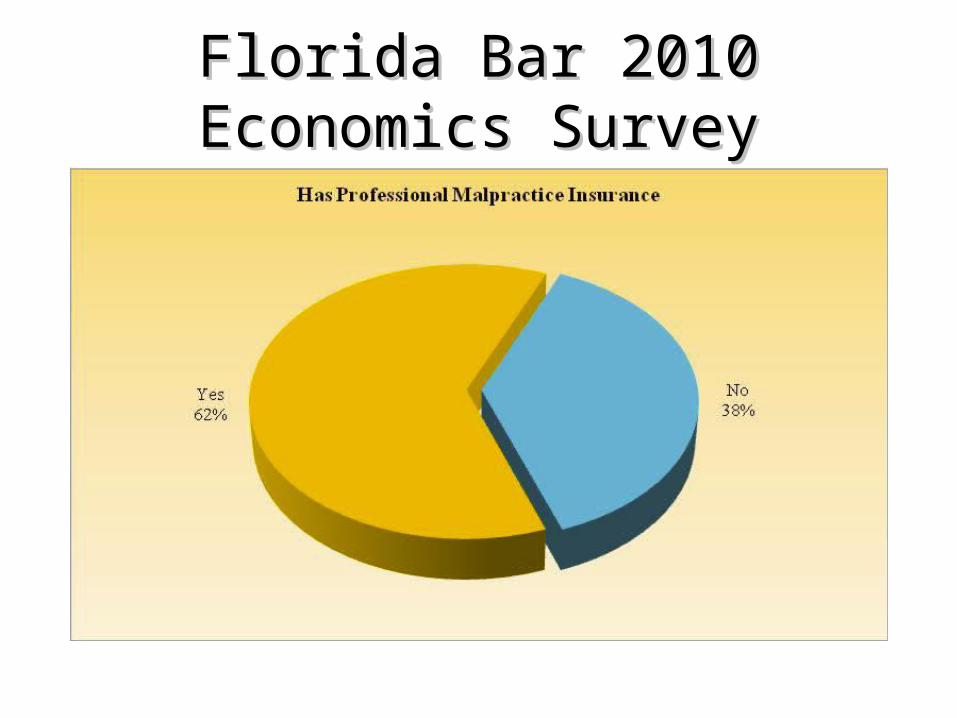

Florida Bar 2010 Economics Florida Bar 2010 Economics SurveySurvey

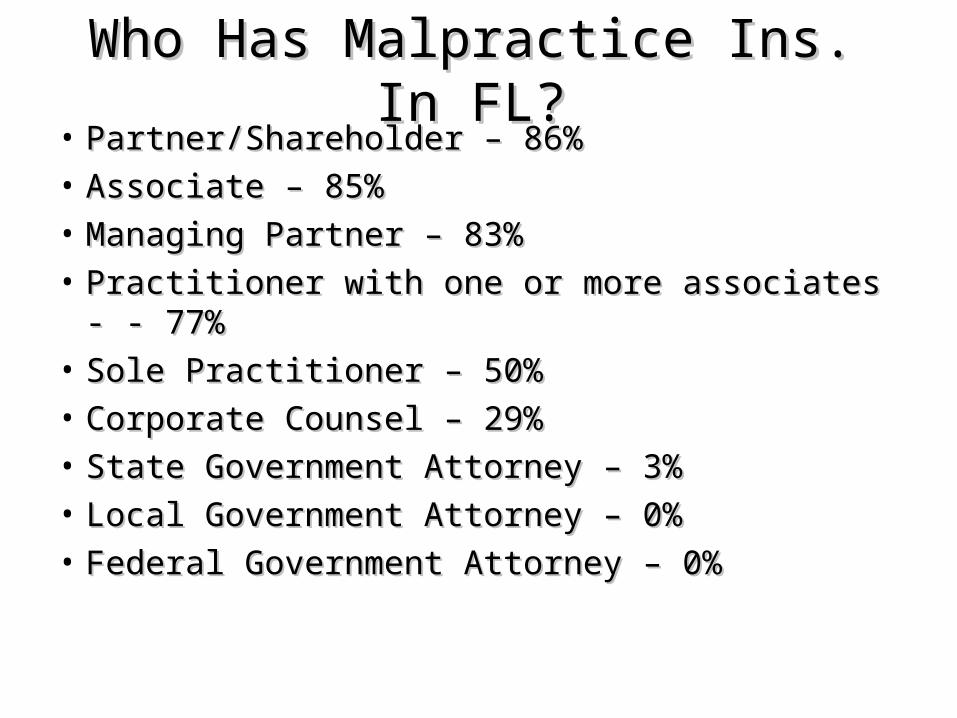

Who Has Malpractice Ins. In FL?Who Has Malpractice Ins. In FL?• Partner/Shareholder – 86%Partner/Shareholder – 86%• Associate – 85%Associate – 85%• Managing Partner – 83%Managing Partner – 83%• Practitioner with one or more associates - - 77%Practitioner with one or more associates - - 77%• Sole Practitioner – 50%Sole Practitioner – 50%• Corporate Counsel – 29%Corporate Counsel – 29%• State Government Attorney – 3%State Government Attorney – 3%• Local Government Attorney – 0%Local Government Attorney – 0%• Federal Government Attorney – 0%Federal Government Attorney – 0%

Malpractice insurance carriersMalpractice insurance carriers

• ABA maintains a ABA maintains a list of carriers writing writing legal malpractice policies in FL and other legal malpractice policies in FL and other statesstates

• Shop aroundShop around– Coverage as important as priceCoverage as important as price– Working with independent broker can be best Working with independent broker can be best

way to find best carrier for your needsway to find best carrier for your needs

Malpractice insurance issuesMalpractice insurance issues

• Beware of “Gaps” in coverageBeware of “Gaps” in coverage– Claims (or claims made) policies – coverage Claims (or claims made) policies – coverage

is based on date of claim, not occurrence is based on date of claim, not occurrence (most common type of policy today)(most common type of policy today)

– Occurrence policies – coverage is based on Occurrence policies – coverage is based on occurrence that led to claim, not date of claimoccurrence that led to claim, not date of claim

• Difference between these types of policies Difference between these types of policies can result in gap even if you had can result in gap even if you had insurance continuouslyinsurance continuously

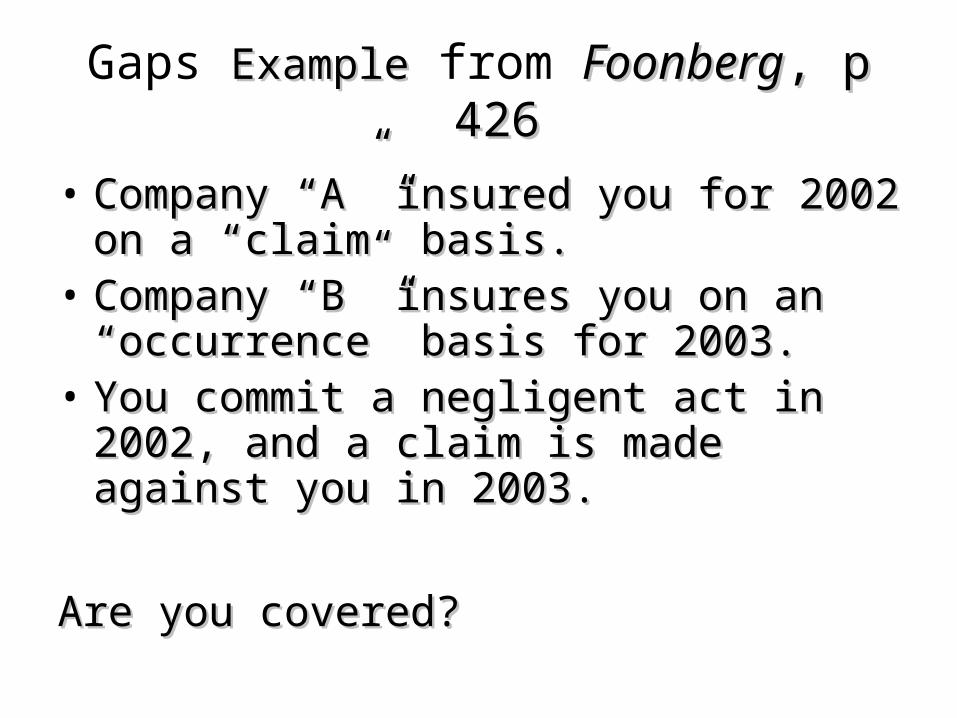

Gaps ExampleExample from FoonbergFoonberg, p 426, p 426

• Company “A” insured you for 2002 on a Company “A” insured you for 2002 on a “claim” basis.“claim” basis.

• Company “B” insures you on an Company “B” insures you on an “occurrence” basis for 2003.“occurrence” basis for 2003.

• You commit a negligent act in 2002, and a You commit a negligent act in 2002, and a claim is made against you in 2003.claim is made against you in 2003.

Are you covered?Are you covered?

““No”No”

• Company “A” will not cover you because Company “A” will not cover you because the “claim” wasn’t made during the policy the “claim” wasn’t made during the policy period 2002period 2002

• Company “B” will not cover you because Company “B” will not cover you because the “occurrence” didn’t occur during its the “occurrence” didn’t occur during its policy period, 2003. policy period, 2003.

Although you had policies in effect at all Although you had policies in effect at all times, you have no coverage.times, you have no coverage.

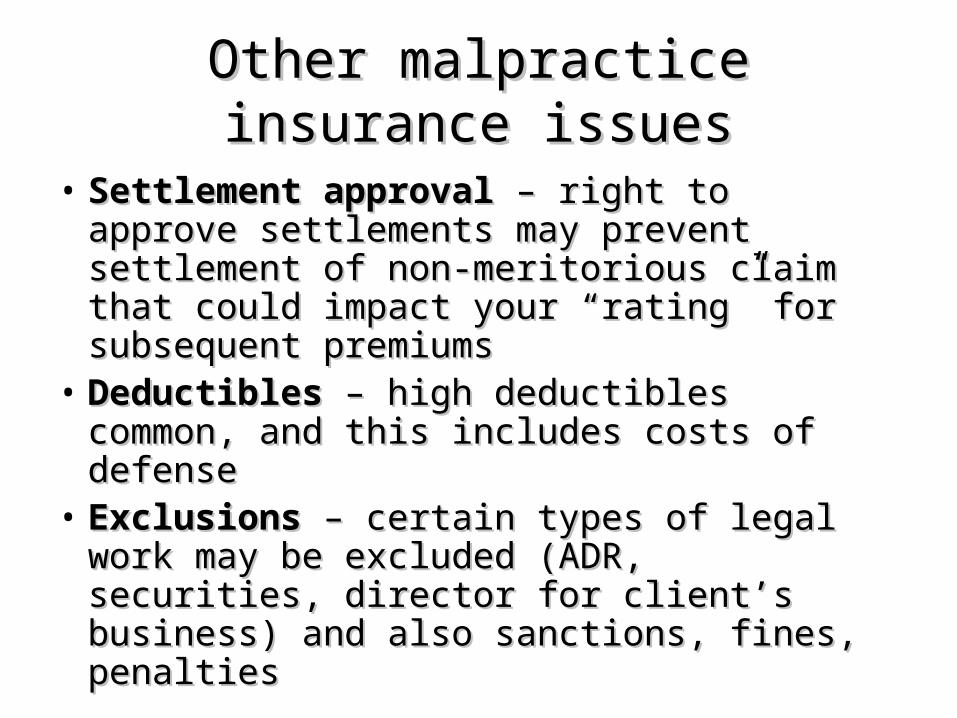

Other malpractice insurance issuesOther malpractice insurance issues

• Settlement approvalSettlement approval – right to approve – right to approve settlements may prevent settlement of settlements may prevent settlement of non-meritorious claim that could impact non-meritorious claim that could impact your “rating” for subsequent premiumsyour “rating” for subsequent premiums

• DeductiblesDeductibles – high deductibles common, – high deductibles common, and this includes costs of defenseand this includes costs of defense

• ExclusionsExclusions – certain types of legal work – certain types of legal work may be excluded (ADR, securities, director may be excluded (ADR, securities, director for client’s business) and also sanctions, for client’s business) and also sanctions, fines, penaltiesfines, penalties

Other malpractice insurance issuesOther malpractice insurance issues

• Sufficient CoverageSufficient Coverage– How much at stake in your most significant How much at stake in your most significant

matter? Need to cover potential lossmatter? Need to cover potential loss– Consider raising rates on high-end (or high-Consider raising rates on high-end (or high-

risk) matters to cover premiums for increased risk) matters to cover premiums for increased coverage. Coverage protects coverage. Coverage protects you and your you and your clientclient..

Malpractice insurance for new Malpractice insurance for new lawyerslawyers

• Can be very affordableCan be very affordable– Loss-leader:Loss-leader: Carrier wants to get you as a Carrier wants to get you as a

regular and loyal customer early on, knowing regular and loyal customer early on, knowing they can raise premiums as your career they can raise premiums as your career progresses and ultimately make more money progresses and ultimately make more money on you.on you.

– Lower risk of claim:Lower risk of claim: Most policies are Most policies are “claims-made” and new lawyers don’t have a “claims-made” and new lawyers don’t have a long history or large base of clients who could long history or large base of clients who could make a claim. make a claim.

ADR clauses in fee agreementsADR clauses in fee agreements

• Clauses in fee agreements for mediation Clauses in fee agreements for mediation or arbitration of fee disputes reduce or arbitration of fee disputes reduce malpractice claimsmalpractice claims

• Many malpractice claims brought as Many malpractice claims brought as counter-claims to suits for fees – merely counter-claims to suits for fees – merely attempt to obtain leverage to reduce or attempt to obtain leverage to reduce or eliminate fee that is owed eliminate fee that is owed

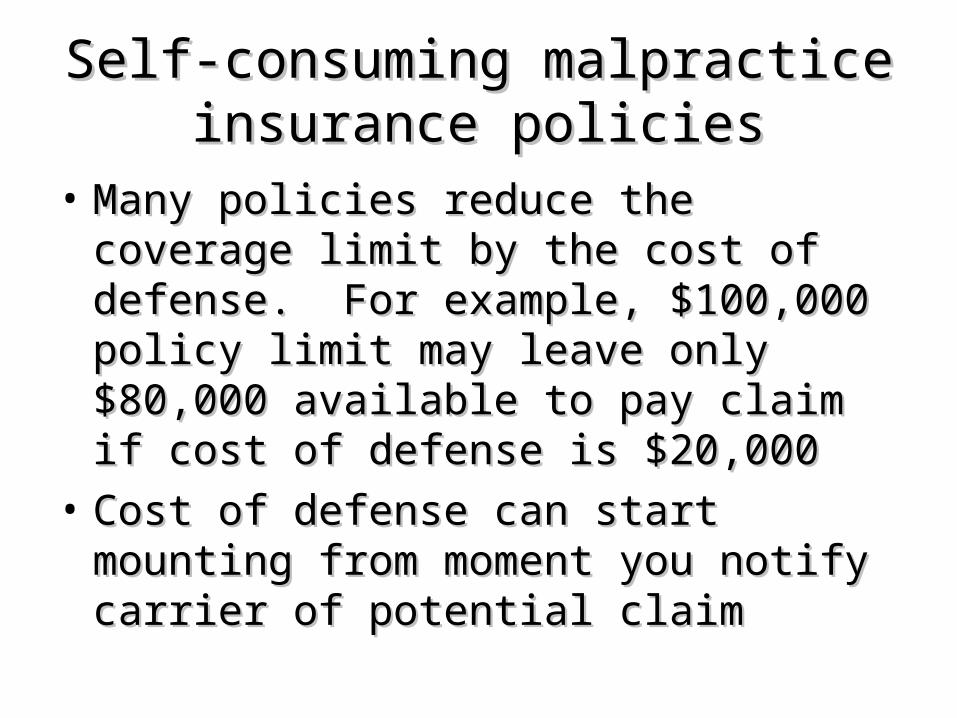

Self-consuming malpractice Self-consuming malpractice insurance policiesinsurance policies

• Many policies reduce the coverage limit by Many policies reduce the coverage limit by the cost of defense. For example, the cost of defense. For example, $100,000 policy limit may leave only $100,000 policy limit may leave only $80,000 available to pay claim if cost of $80,000 available to pay claim if cost of defense is $20,000defense is $20,000

• Cost of defense can start mounting from Cost of defense can start mounting from moment you notify carrier of potential moment you notify carrier of potential claimclaim

Liability from malpractice of lawyers Liability from malpractice of lawyers in your office/suitein your office/suite

• Many lawyers sued for acts of other lawyers with Many lawyers sued for acts of other lawyers with whom they have no formal relationship (other whom they have no formal relationship (other than proximity in same office suite)than proximity in same office suite)

• Client perceptionClient perception (if reasonable), not actual (if reasonable), not actual legal ties, may be the determining factorlegal ties, may be the determining factor

• Jury may determine if that perception is Jury may determine if that perception is reasonablereasonable

• You must insist that all other lawyers in You must insist that all other lawyers in suite/office have adequate coverage. Your suite/office have adequate coverage. Your carrier may ask for proof. carrier may ask for proof.

4 Phases of Malpractice Claim4 Phases of Malpractice Claimfrom Lawyers Mutual Ins Co of Kentuckyfrom Lawyers Mutual Ins Co of Kentucky

1. Discovery of Malpractice. Discovery of Malpractice

– Served with Complaint from ClientServed with Complaint from Client– Discovered Before Client is AwareDiscovered Before Client is Aware

2. Notification of Client and Ins Carrier2. Notification of Client and Ins Carrier– Don’t Delay, Coverage May be Lost on Policy Don’t Delay, Coverage May be Lost on Policy

Renewal DateRenewal Date– Start with Carrier, Then ClientStart with Carrier, Then Client

3.3.Claims Repair (Mitigate Loss to Client)Claims Repair (Mitigate Loss to Client)

4.4.Adjudication (Negotiation, ADR, Trial)Adjudication (Negotiation, ADR, Trial)

Umbrella coverageUmbrella coverage

• Can be Can be best valuebest value available available• Picks up coverage where underlying Picks up coverage where underlying

policies leave offpolicies leave off• Often cheaper to have $300,000 Often cheaper to have $300,000

malpractice policy and $1,000,000 malpractice policy and $1,000,000 umbrella than buy $1,000,000 malpractice umbrella than buy $1,000,000 malpractice policypolicy

• Will apply to areas other than malpractice Will apply to areas other than malpractice (auto, homeowners, etc.)(auto, homeowners, etc.)

Other insurance issuesOther insurance issues

• Non-owned autosNon-owned autos– Employee running an errand for you in their Employee running an errand for you in their

personal vehiclepersonal vehicle

• Non-owned assetsNon-owned assets– Employee using their own computer or cell Employee using their own computer or cell

phone at your officephone at your office

• Office furniture, etc.Office furniture, etc.– Look for “replacement value” coverage. Look for “replacement value” coverage.

Depreciated value of furniture and equipment Depreciated value of furniture and equipment will result in very low claim recoverywill result in very low claim recovery

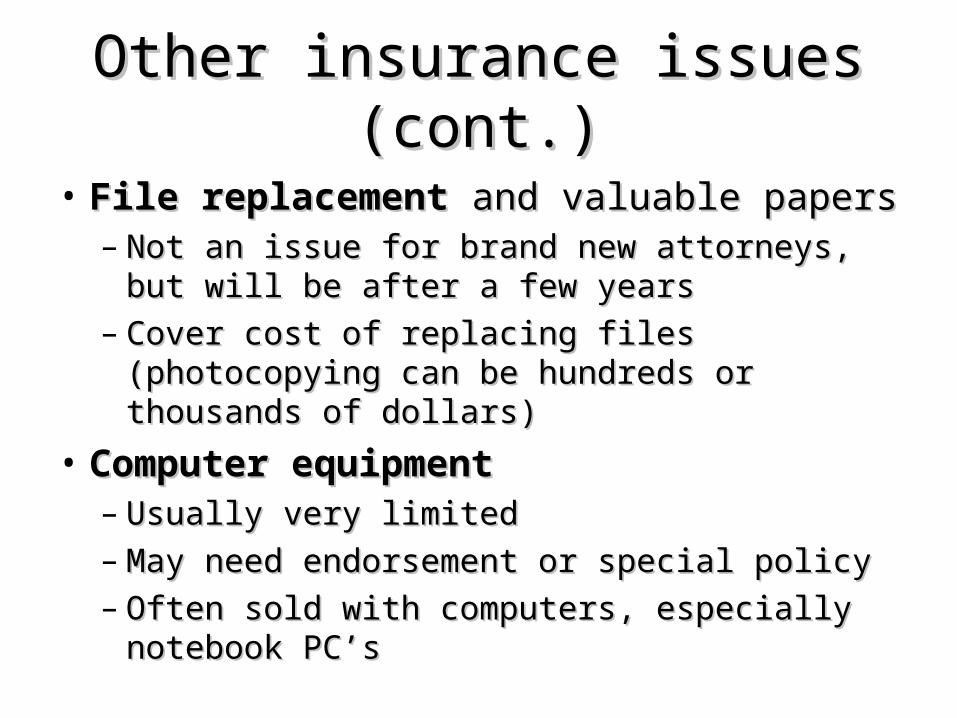

Other insurance issues (cont.)Other insurance issues (cont.)

• File replacementFile replacement and valuable papers and valuable papers– Not an issue for brand new attorneys, but will Not an issue for brand new attorneys, but will

be after a few yearsbe after a few years– Cover cost of replacing files (photocopying Cover cost of replacing files (photocopying

can be hundreds or thousands of dollars)can be hundreds or thousands of dollars)

• Computer equipmentComputer equipment– Usually very limitedUsually very limited– May need endorsement or special policyMay need endorsement or special policy– Often sold with computers, especially Often sold with computers, especially

notebook PC’snotebook PC’s

Other insurance issues (cont.)Other insurance issues (cont.)

• Employment practices liabilityEmployment practices liability– New areaNew area– Covers violation of employment lawsCovers violation of employment laws

• Workers’ CompWorkers’ Comp– Need this as soon as you hire your first Need this as soon as you hire your first

employeeemployee– May be a state-owned or state-chartered May be a state-owned or state-chartered

company that provides low-cost coverage for company that provides low-cost coverage for new businesses new businesses

Other insurance issues (cont.)Other insurance issues (cont.)

• Fiduciary liabilityFiduciary liability– If you act as a trustee of fiduciaryIf you act as a trustee of fiduciary– May be a rider to your malpractice policyMay be a rider to your malpractice policy

• ““Office block” insuranceOffice block” insurance– Package deal that includes many types of Package deal that includes many types of

coverage such as premises liability, theft, coverage such as premises liability, theft, worker’s comp, etc.worker’s comp, etc.

• Trust account theftTrust account theft (employee bonding) (employee bonding)– Covers theft of trust (client) funds by an Covers theft of trust (client) funds by an

employeeemployee

Other insurance issues (cont.)Other insurance issues (cont.)

• Disability, Office Overhead, Business Disability, Office Overhead, Business IncomeIncome– Buy all you can affordBuy all you can afford– May be more essential than life insuranceMay be more essential than life insurance

• Life insurance protects others if you dieLife insurance protects others if you die• Disability insurance protects you if you liveDisability insurance protects you if you live

– Look for group rates through bar associationLook for group rates through bar association

Other insurance issues (cont.)Other insurance issues (cont.)

• Life insuranceLife insurance– Renewable term may be best option when Renewable term may be best option when

starting outstarting out• Rates are low when your cash flow is meager – Rates are low when your cash flow is meager –

Good matchGood match

• Arbitrator/Mediator insuranceArbitrator/Mediator insurance– If you act as mediator or arbitrator, make sure If you act as mediator or arbitrator, make sure

your malpractice policy covers these activitiesyour malpractice policy covers these activities– May need rider or special policyMay need rider or special policy

Other insurance issues (cont.)Other insurance issues (cont.)

• Discounts for new, part-time, semi-retired Discounts for new, part-time, semi-retired lawyers on malpractice insurancelawyers on malpractice insurance– Rates often based on billable hoursRates often based on billable hours– Can be substantially lower than full-time ratesCan be substantially lower than full-time rates

ProblemProblem

• What type of professional liability What type of professional liability insurance should you have?insurance should you have?

• How much coverage do you need?How much coverage do you need?