latin america: outlook and challenges - cemla · latin america: outlook and challenges alejandro...

TRANSCRIPT

International Monetary Fund Washington, DC. May 15, 2013

Latin America: Outlook and Challenges

Alejandro Werner Director

Western Hemisphere Department

Developments and Outlook

Policy Challenges and Priorities

Growth moderating toward potential, with little spare capacity

(pick up in Brazil after deceleration)

Sources: National authorities and IMF staff estimates. ¹ Includes data for Argentina, Brazil, Chile, Colombia, Costa Rica, Ecuador, Mexico, Paraguay, Peru and Venezuela.

Selected Latin America: Real GDP Growth (12-month percent change, seasonally adjusted, quarterly)

-4

-2

0

2

4

6

2006

20

07

2008

20

09

2010

20

11

2012

20

13

median

Sources: IMF, World Economic Outlook; and IMF staff estimates. 1 10–90 percentile range for all Latin American countries (excludes the Caribbean).

Latin America: Output Gaps (Percent of potential GDP)

10–90 percentile range -20

-15 -10

-5 0 5

10 15

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

25–75 percentil

median

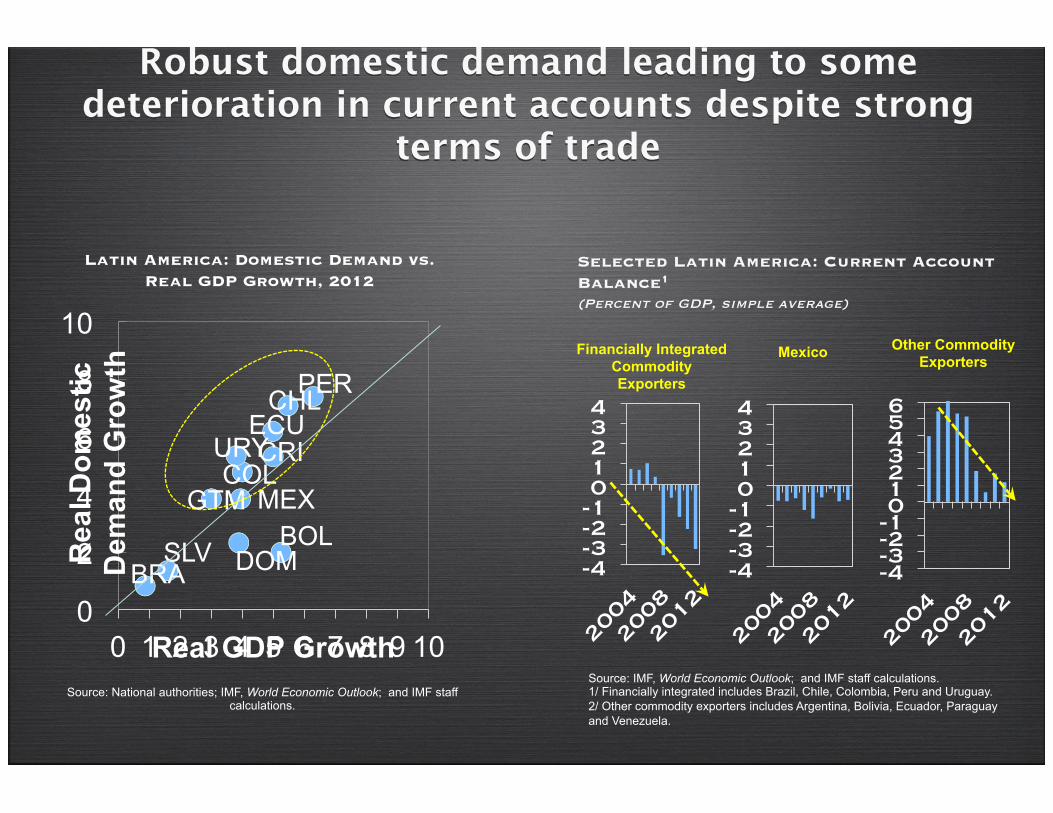

Robust domestic demand leading to some deterioration in current accounts despite strong

terms of trade

Selected Latin America: Current Account Balance1

(Percent of GDP, simple average)

Latin America: Domestic Demand vs. Real GDP Growth, 2012

Source: National authorities; IMF, World Economic Outlook; and IMF staff calculations.

-4 -3 -2 -1 0 1 2 3 4

-4 -3 -2 -1 0 1 2 3 4 5 6

Mexico Other Commodity Exporters

Financially Integrated Commodity Exporters

BOL BRA

CHL

COL CRI

DOM

ECU

SLV

GTM MEX

PER

URY

0

2

4

6

8

10

0 1 2 3 4 5 6 7 8 9 10

Rea

l Dom

estic

D

eman

d G

row

th

Real GDP Growth

-4 -3 -2 -1 0 1 2 3 4

Source: IMF, World Economic Outlook; and IMF staff calculations. 1/ Financially integrated includes Brazil, Chile, Colombia, Peru and Uruguay. 2/ Other commodity exporters includes Argentina, Bolivia, Ecuador, Paraguay and Venezuela.

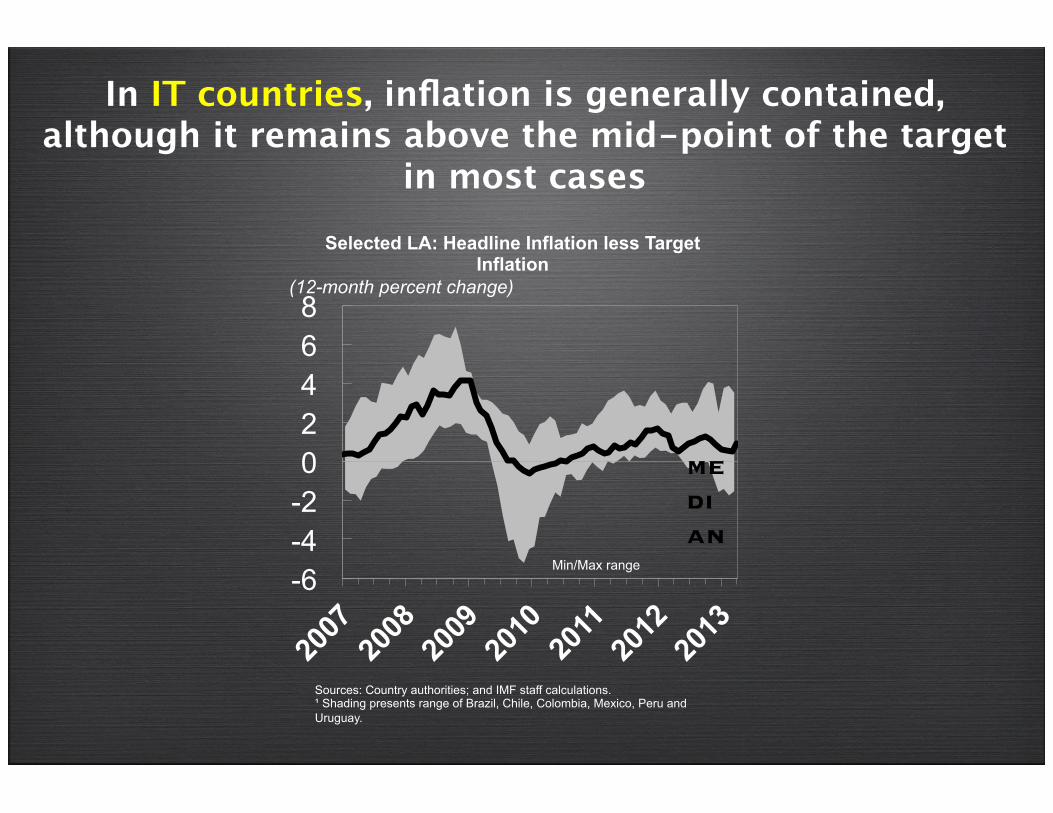

In IT countries, inflation is generally contained, although it remains above the mid-point of the target

in most cases Selected LA: Headline Inflation less Target

Inflation (12-month percent change)

Sources: Country authorities; and IMF staff calculations. ¹ Shading presents range of Brazil, Chile, Colombia, Mexico, Peru and Uruguay.

-6 -4 -2 0 2 4 6 8

median

Min/Max range

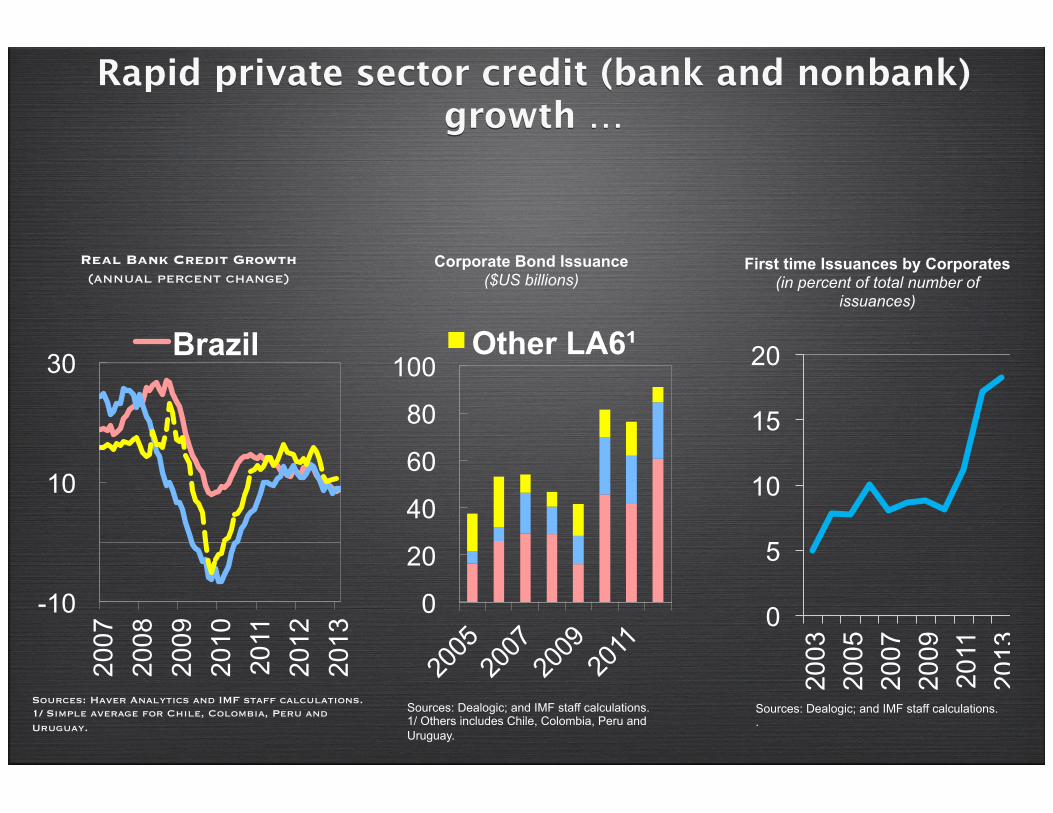

Rapid private sector credit (bank and nonbank) growth …

Real Bank Credit Growth (annual percent change)

Sources: Haver Analytics and IMF staff calculations. 1/ Simple average for Chile, Colombia, Peru and Uruguay.

0

20

40

60

80

100 Other LA6¹

Corporate Bond Issuance ($US billions)

Sources: Dealogic; and IMF staff calculations. 1/ Others includes Chile, Colombia, Peru and Uruguay.

2007

20

08

2009

20

10

2011

20

12

2013

-10

10

30 Brazil

0

5

10

15

20

2003

20

05

2007

20

09

2011

20

13

First time Issuances by Corporates (in percent of total number of

issuances)

Sources: Dealogic; and IMF staff calculations. .

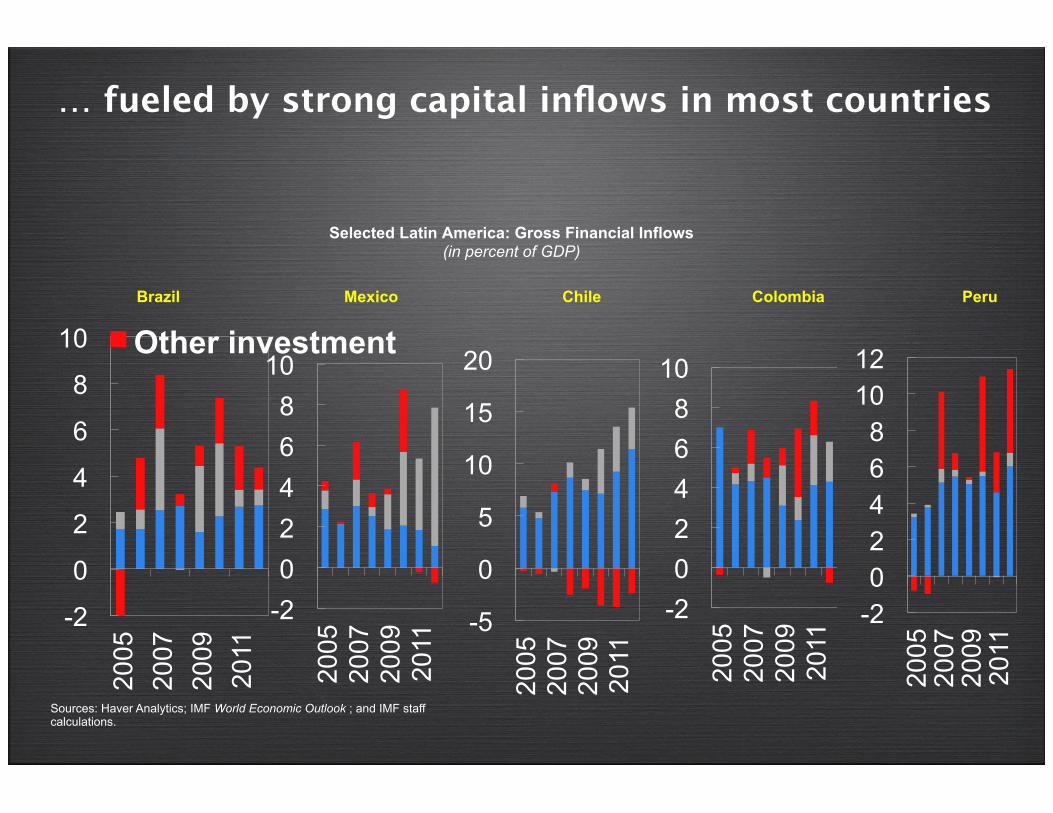

… fueled by strong capital inflows in most countries

Selected Latin America: Gross Financial Inflows (in percent of GDP)

Sources: Haver Analytics; IMF World Economic Outlook ; and IMF staff calculations.

Brazil Mexico Chile Colombia Peru

-5

0

5

10

15

20

2005

20

07

2009

20

11 -2

0 2 4 6 8

10 20

05

2007

20

09

2011

-2 0 2 4 6 8

10

2005

20

07

2009

20

11 -2

0 2 4 6 8

10 12

2005

20

07

2009

20

11 -2

0

2

4

6

8

10

2005

20

07

2009

20

11

Other investment

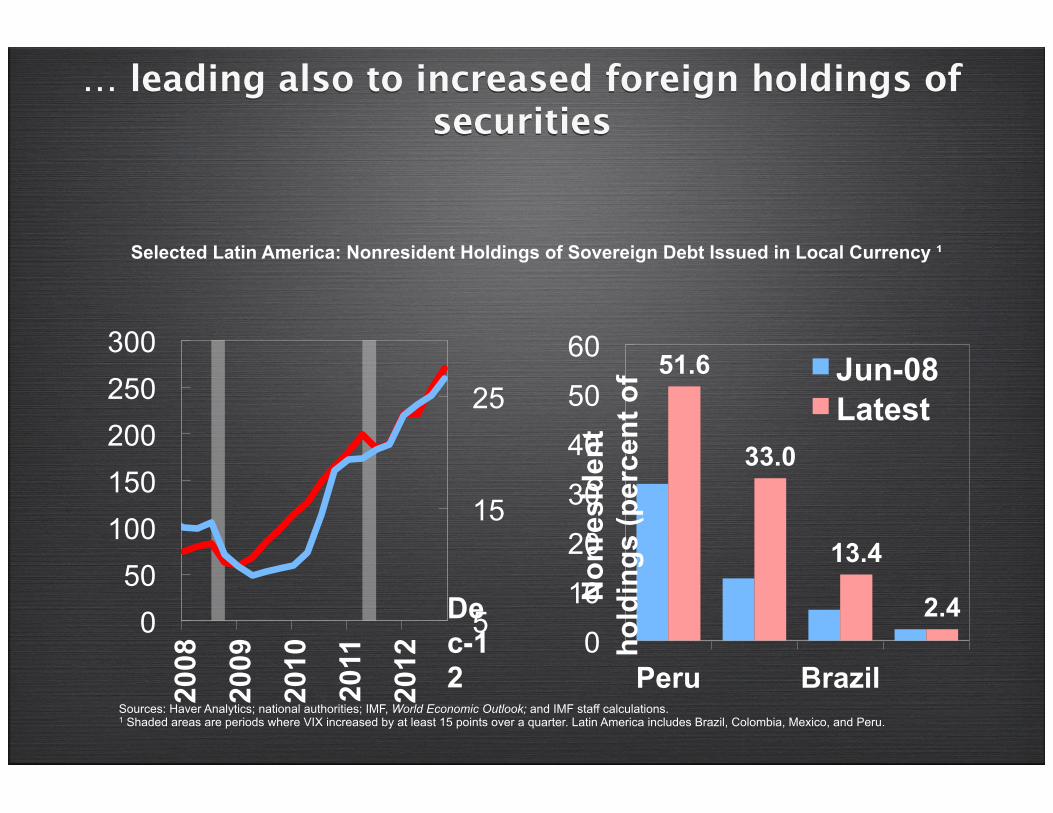

… leading also to increased foreign holdings of securities

5

15

25

0 50

100 150 200 250 300

2008

2009

2010

2011

2012

Dec-12

51.6

33.0

13.4

2.4 0

10

20

30

40

50

60

Peru Brazil

Non

resi

dent

ho

ldin

gs (p

erce

nt o

f Jun-08 Latest

Selected Latin America: Nonresident Holdings of Sovereign Debt Issued in Local Currency ¹

Sources: Haver Analytics; national authorities; IMF, World Economic Outlook; and IMF staff calculations. 1 Shaded areas are periods where VIX increased by at least 15 points over a quarter. Latin America includes Brazil, Colombia, Mexico, and Peru.

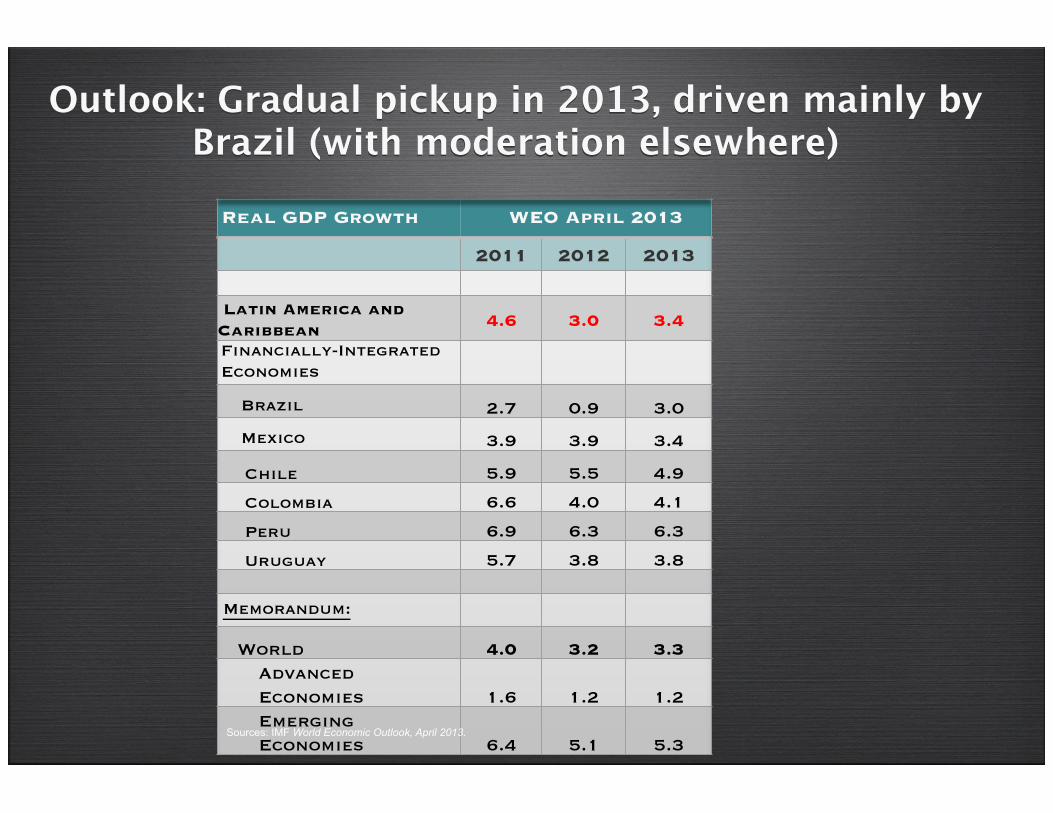

Real GDP Growth WEO April 2013

2011 2012 2013

Latin America and Caribbean 4.6 3.0 3.4

Financially-Integrated Economies

Brazil 2.7 0.9 3.0

Mexico 3.9 3.9 3.4

Chile 5.9 5.5 4.9

Colombia 6.6 4.0 4.1

Peru 6.9 6.3 6.3

Uruguay 5.7 3.8 3.8

Memorandum:

World 4.0 3.2 3.3 Advanced Economies 1.6 1.2 1.2 Emerging Economies 6.4 5.1 5.3

Outlook: Gradual pickup in 2013, driven mainly by Brazil (with moderation elsewhere)

Sources: IMF World Economic Outlook, April 2013.

New Policy Challenges

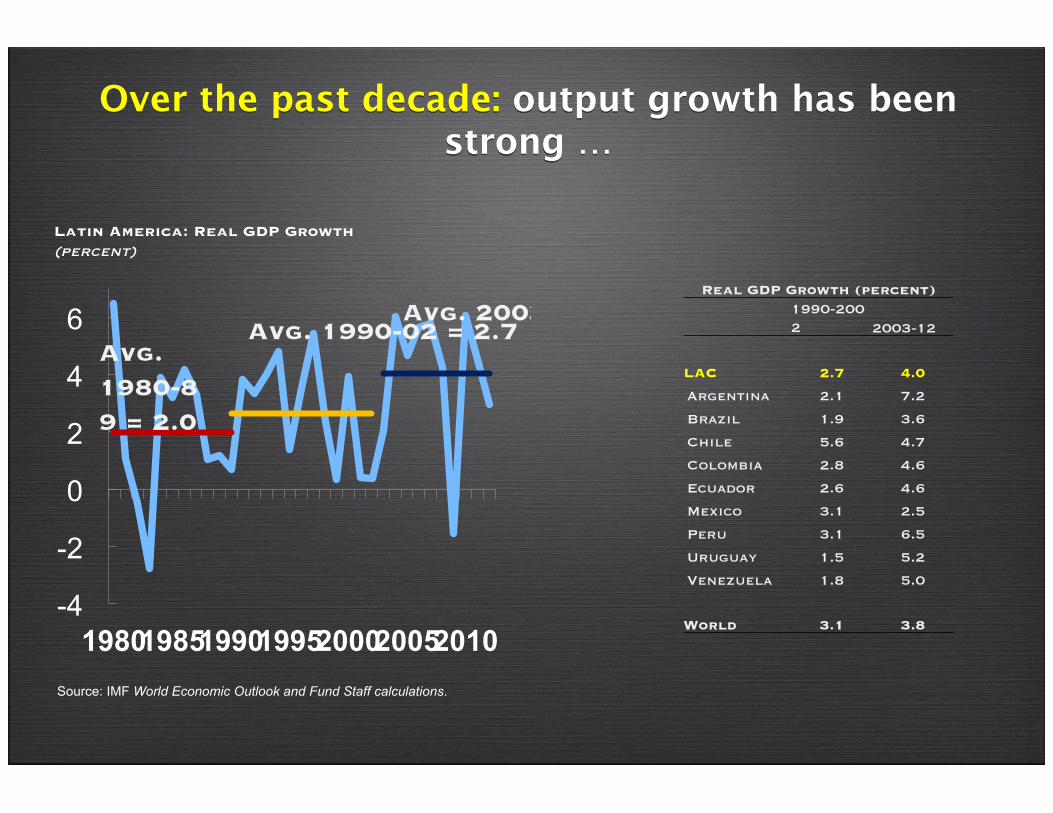

Over the past decade: output growth has been strong …

Source: IMF World Economic Outlook and Fund Staff calculations.

-4

-2

0

2

4

6

1980 1985 1990 1995 2000 2005 2010

Avg. 1980-89 = 2.0

Avg. 2003-12 = 4.0 Avg. 1990-02 = 2.7

Latin America: Real GDP Growth (percent)

Real GDP Growth (percent)

1990-2002 2003-12

LAC 2.7 4.0

Argentina 2.1 7.2

Brazil 1.9 3.6

Chile 5.6 4.7

Colombia 2.8 4.6

Ecuador 2.6 4.6

Mexico 3.1 2.5

Peru 3.1 6.5

Uruguay 1.5 5.2

Venezuela 1.8 5.0

World 3.1 3.8

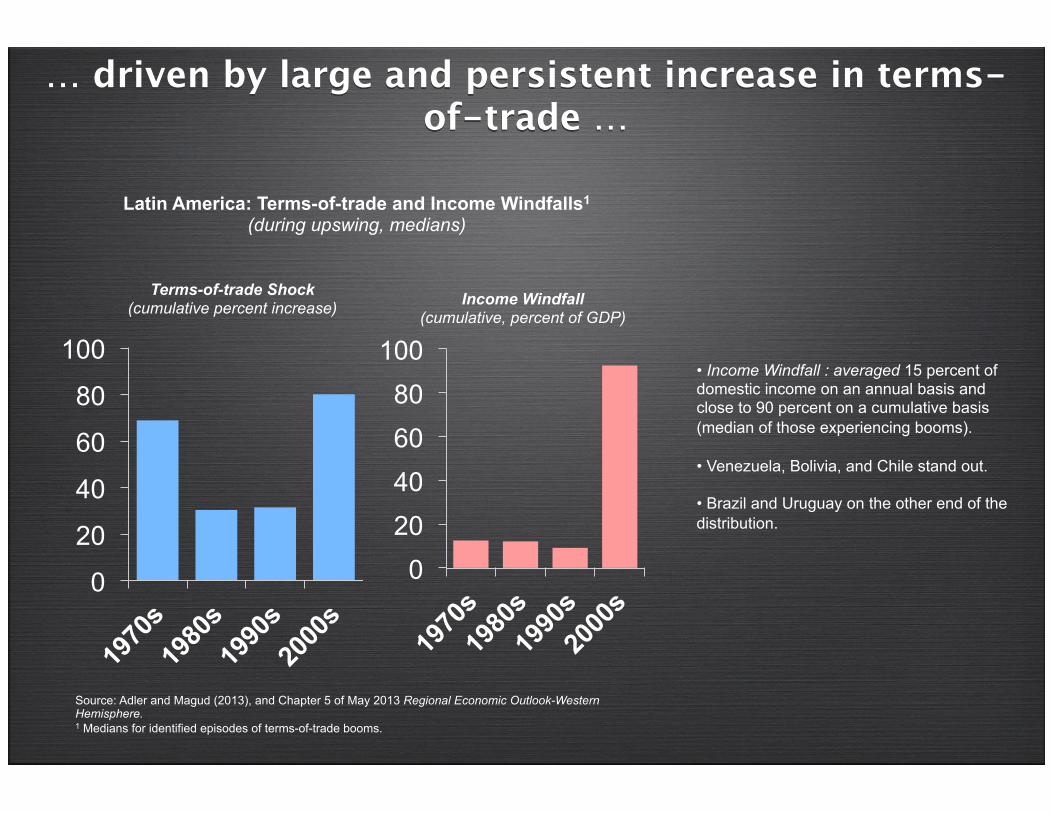

… driven by large and persistent increase in terms-of-trade …

• Income Windfall : averaged 15 percent of domestic income on an annual basis and close to 90 percent on a cumulative basis (median of those experiencing booms). • Venezuela, Bolivia, and Chile stand out.

• Brazil and Uruguay on the other end of the distribution.

0

20

40

60

80

100

0 20 40 60 80

100

Terms-of-trade Shock (cumulative percent increase)

Latin America: Terms-of-trade and Income Windfalls1

(during upswing, medians)

Income Windfall (cumulative, percent of GDP)

Source: Adler and Magud (2013), and Chapter 5 of May 2013 Regional Economic Outlook-Western Hemisphere. 1 Medians for identified episodes of terms-of-trade booms.

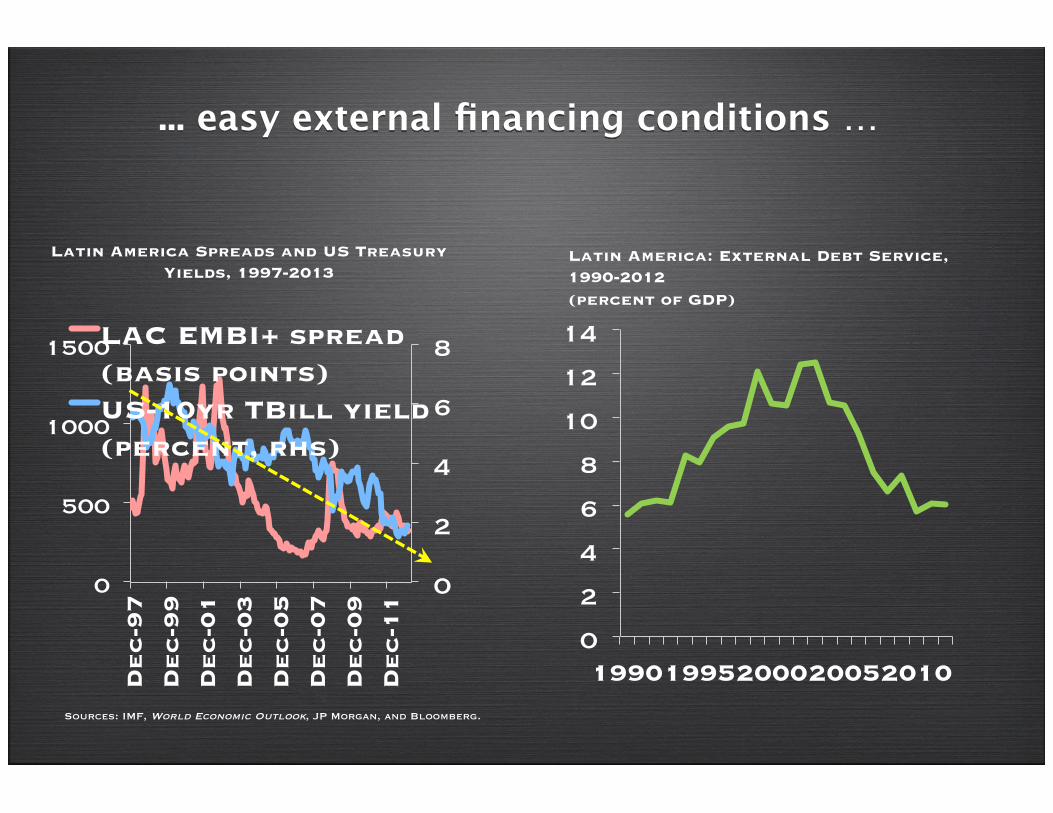

... easy external financing conditions …

0

2

4

6

8

0

500

1000

1500

De

c-9

7

De

c-9

9

De

c-0

1

De

c-0

3

De

c-0

5

De

c-0

7

De

c-0

9

De

c-1

1

LAC EMBI+ spread (basis points) US-10yr TBill yield (percent, rhs)

Latin America Spreads and US Treasury Yields, 1997-2013

Sources: IMF, World Economic Outlook, JP Morgan, and Bloomberg.

0

2

4

6

8

10

12

14

1990 1995 2000 2005 2010

Latin America: External Debt Service, 1990-2012 (percent of GDP)

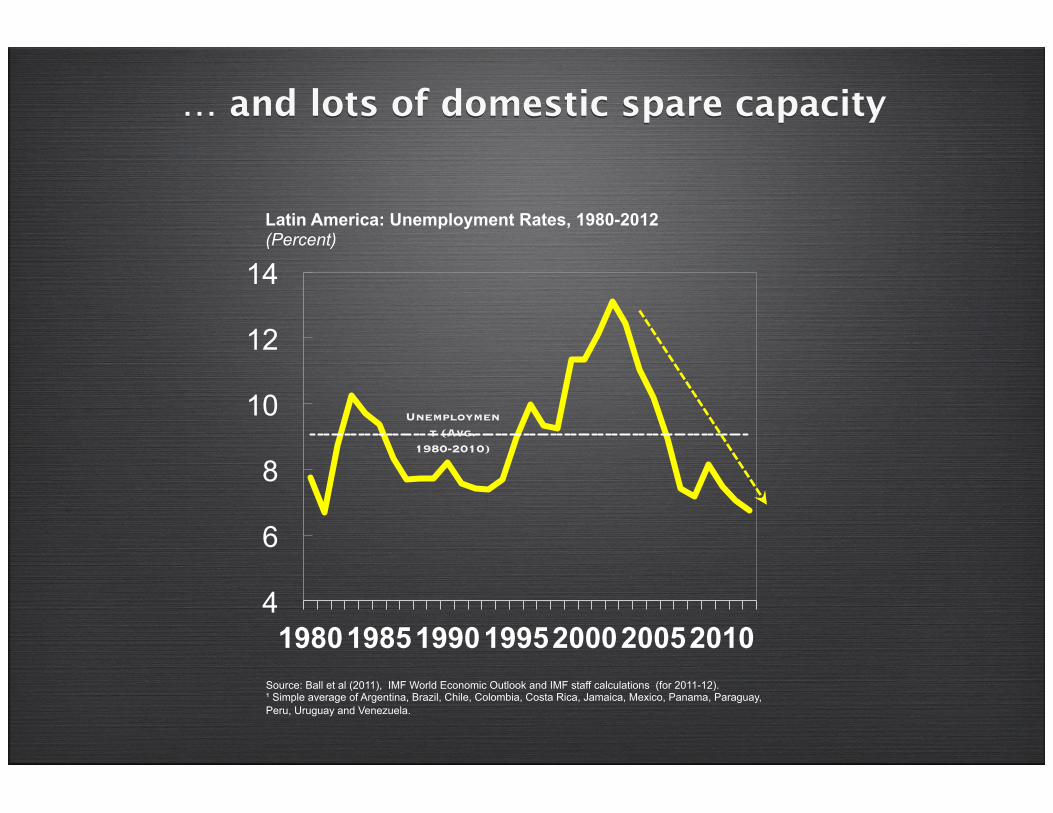

… and lots of domestic spare capacity

4

6

8

10

12

14

1980 1985 1990 1995 2000 2005 2010 Source: Ball et al (2011), IMF World Economic Outlook and IMF staff calculations (for 2011-12). ¹ Simple average of Argentina, Brazil, Chile, Colombia, Costa Rica, Jamaica, Mexico, Panama, Paraguay, Peru, Uruguay and Venezuela.

Latin America: Unemployment Rates, 1980-2012 (Percent)

Unemployment (Avg.

1980-2010)

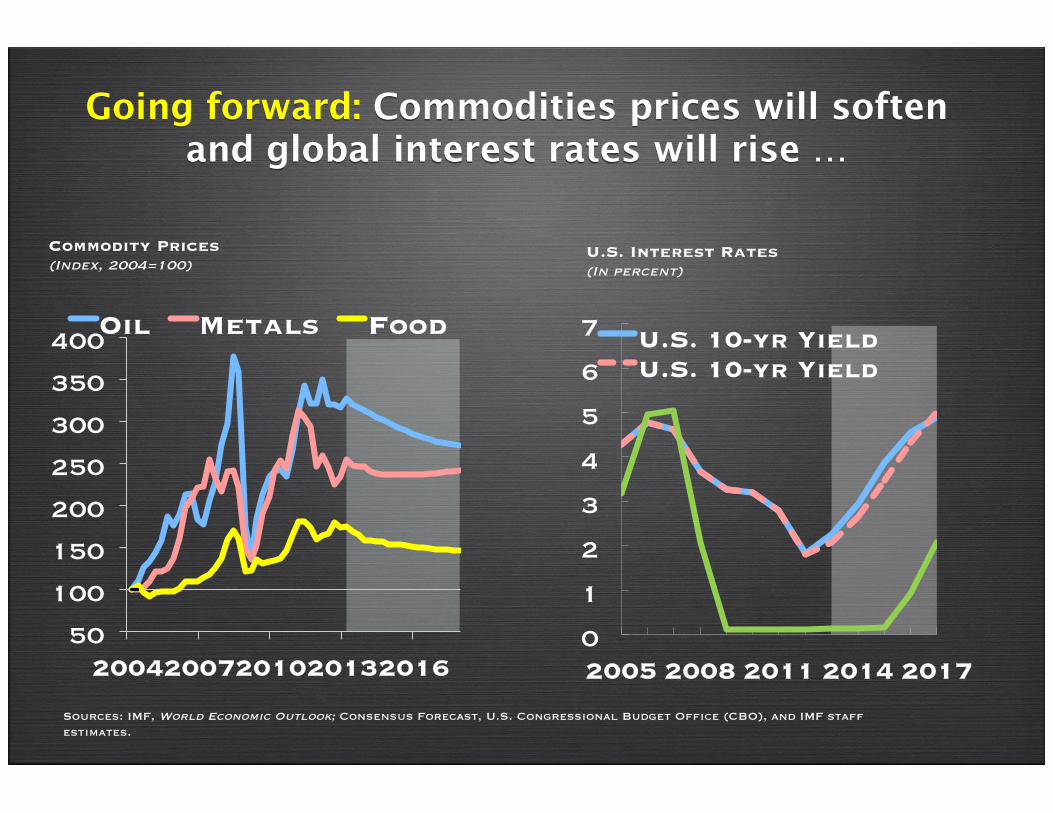

Going forward: Commodities prices will soften and global interest rates will rise …

Commodity Prices (Index, 2004=100)

Sources: IMF, World Economic Outlook; Consensus Forecast, U.S. Congressional Budget Office (CBO), and IMF staff estimates.

0

1

2

3

4

5

6

7

2005 2008 2011 2014 2017

U.S. 10-yr Yield U.S. 10-yr Yield

U.S. Interest Rates (In percent)

50

100

150

200

250

300

350

400

2004 2007 2010 2013 2016

Oil Metals Food

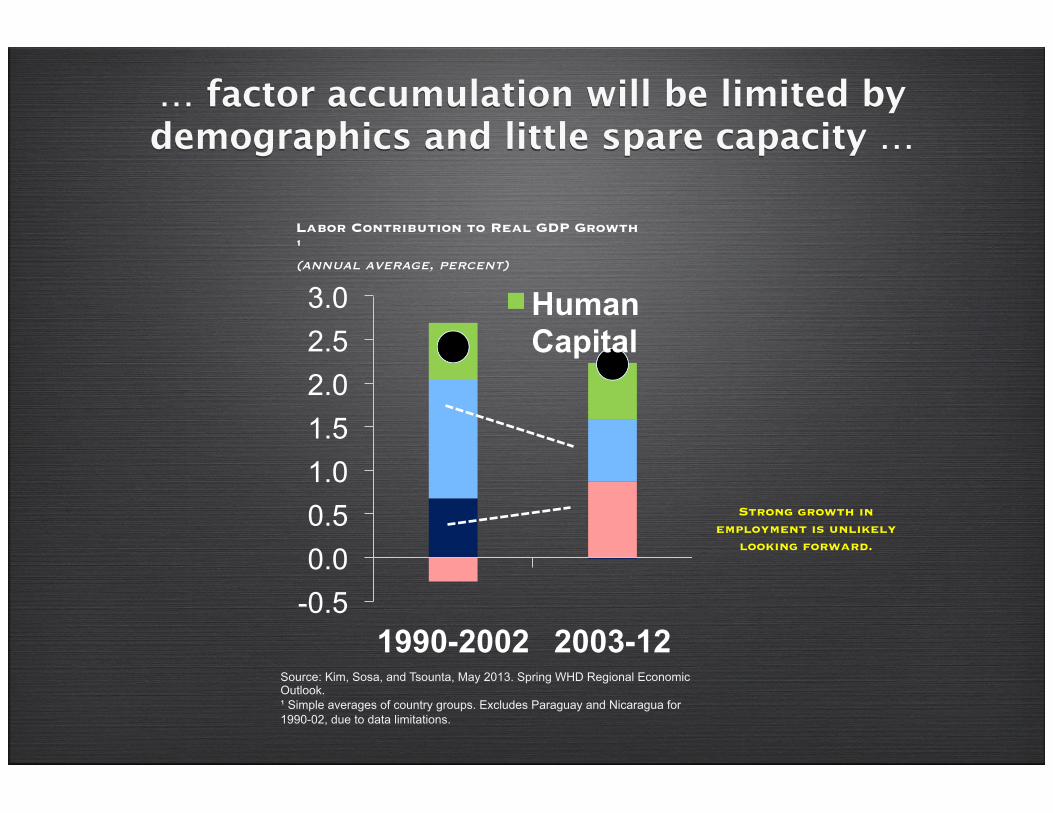

… factor accumulation will be limited by demographics and little spare capacity …

-0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0

1990-2002 2003-12

Human Capital

Source: Kim, Sosa, and Tsounta, May 2013. Spring WHD Regional Economic Outlook. ¹ Simple averages of country groups. Excludes Paraguay and Nicaragua for 1990-02, due to data limitations.

Labor Contribution to Real GDP Growth 1 (annual average, percent)

Strong growth in employment is unlikely

looking forward.

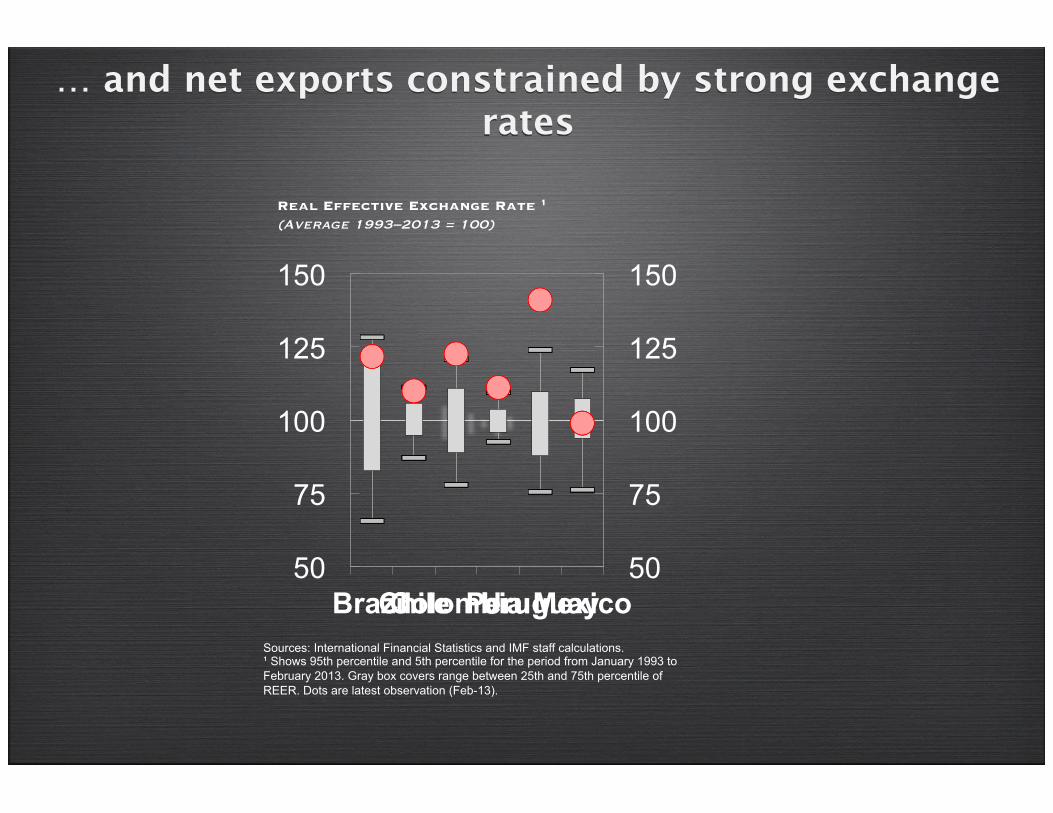

… and net exports constrained by strong exchange rates

Real Effective Exchange Rate 1 (Average 1993–2013 = 100)

Sources: International Financial Statistics and IMF staff calculations. ¹ Shows 95th percentile and 5th percentile for the period from January 1993 to February 2013. Gray box covers range between 25th and 75th percentile of REER. Dots are latest observation (Feb-13).

50

75

100

125

150

50

75

100

125

150

Brazil Chile Colombia Peru Uruguay Mexico

0

5

BR

A

CH

L

CO

L

ME

X

PE

R

UR

Y

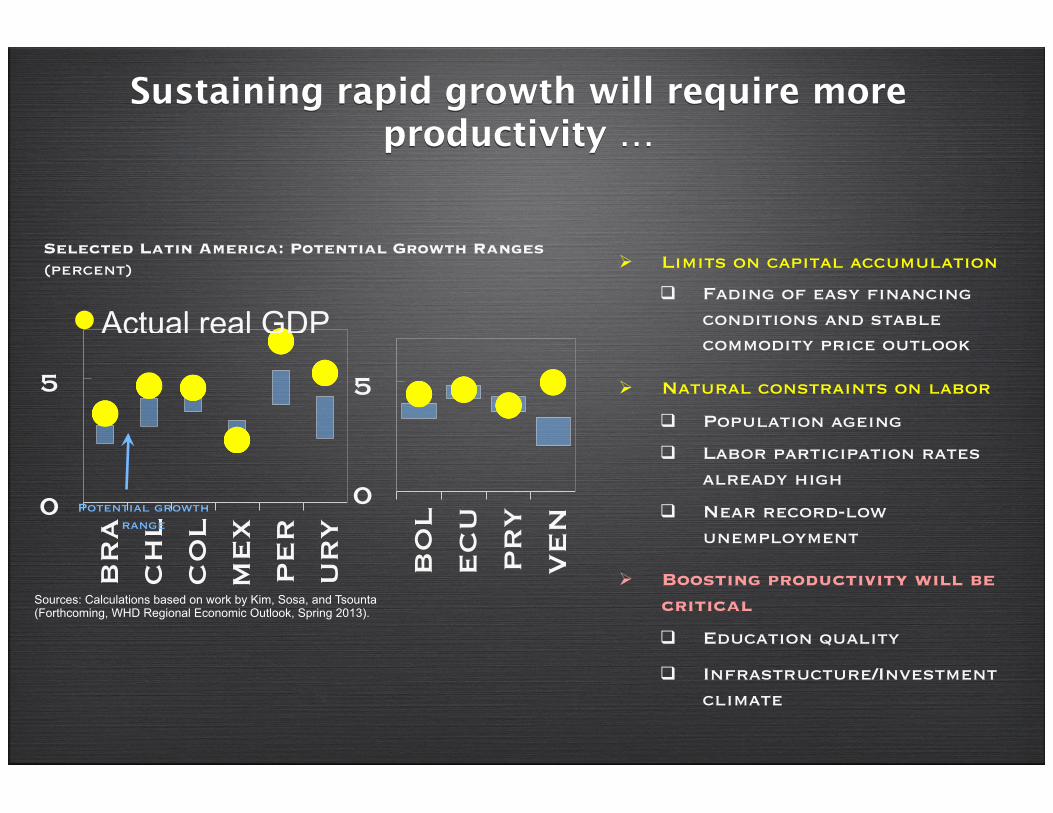

Actual real GDP

Selected Latin America: Potential Growth Ranges (percent)

0

5 B

OL

EC

U

PR

Y

VE

N

Sustaining rapid growth will require more productivity …

Ø Limits on capital accumulation

q Fading of easy financing conditions and stable commodity price outlook

Ø Natural constraints on labor

q Population ageing

q Labor participation rates already high

q Near record-low unemployment

Ø Boosting productivity will be critical

q Education quality

q Infrastructure/Investment climate

Sources: Calculations based on work by Kim, Sosa, and Tsounta (Forthcoming, WHD Regional Economic Outlook, Spring 2013).

Potential growth range

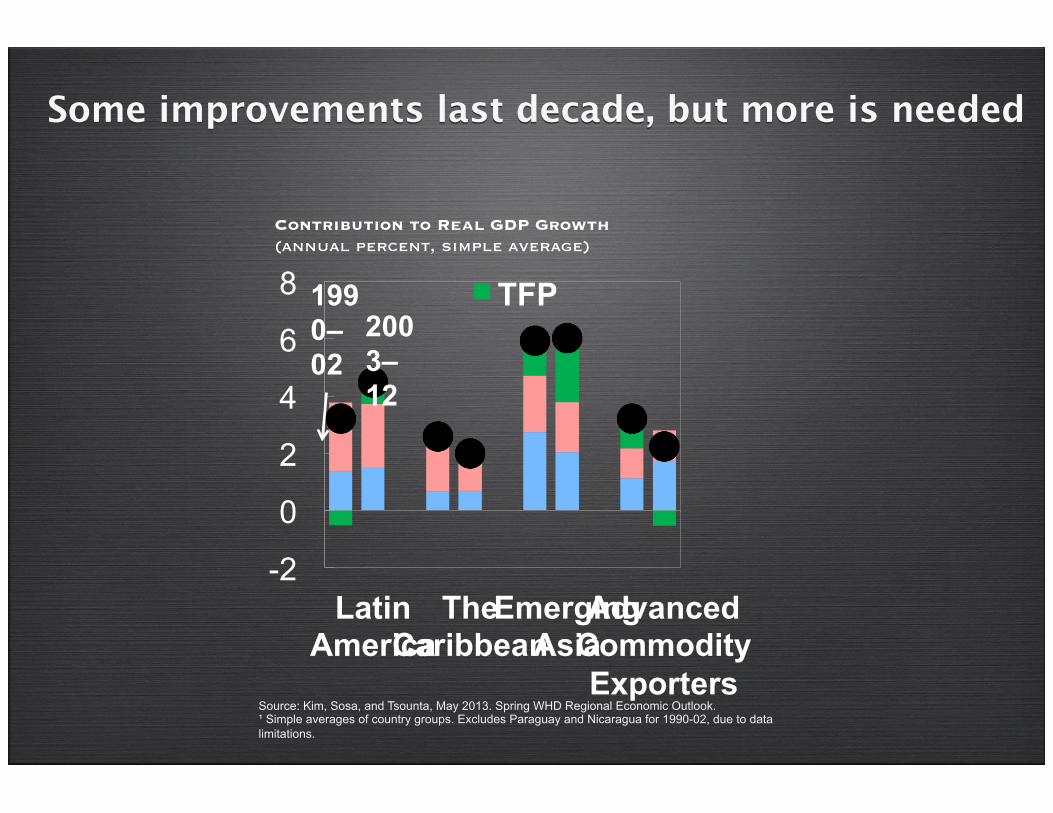

Some improvements last decade, but more is needed

Contribution to Real GDP Growth (annual percent, simple average)

-2

0

2

4

6

8

Latin America

The Caribbean

Emerging Asia

Advanced Commodity Exporters

TFP 2003–12

1990–02

Source: Kim, Sosa, and Tsounta, May 2013. Spring WHD Regional Economic Outlook. ¹ Simple averages of country groups. Excludes Paraguay and Nicaragua for 1990-02, due to data limitations.

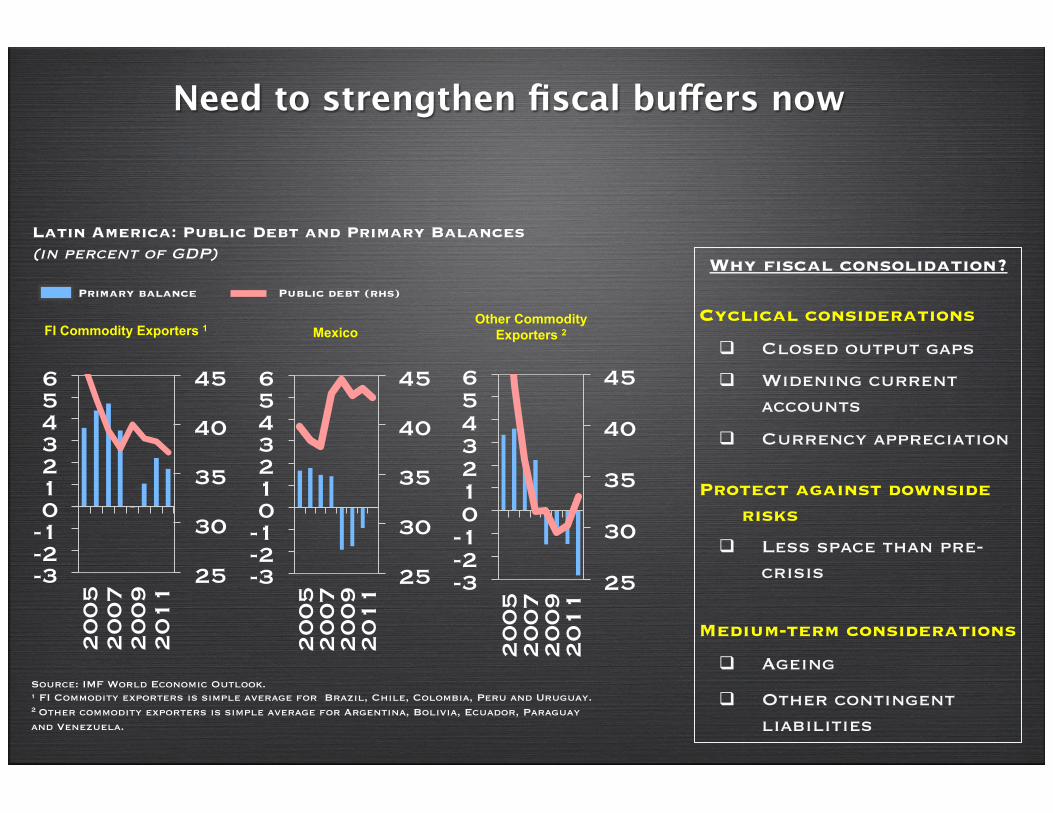

Need to strengthen fiscal buffers now

Why fiscal consolidation?

Cyclical considerations

q Closed output gaps

q Widening current accounts

q Currency appreciation

Protect against downside risks

q Less space than pre-crisis

Medium-term considerations

q Ageing

q Other contingent liabilities

Latin America: Public Debt and Primary Balances (in percent of GDP)

Source: IMF World Economic Outlook. ¹ FI Commodity exporters is simple average for Brazil, Chile, Colombia, Peru and Uruguay. 2 Other commodity exporters is simple average for Argentina, Bolivia, Ecuador, Paraguay and Venezuela.

FI Commodity Exporters 1 Mexico Other Commodity

Exporters 2

Primary balance Public debt (rhs)

25

30

35

40

45

-3 -2 -1 0 1 2 3 4 5 6

20

05

20

07

20

09

20

11 25

30

35

40

45

-3 -2 -1 0 1 2 3 4 5 6

20

05

20

07

20

09

20

11 25

30

35

40

45

-3 -2 -1 0 1 2 3 4 5 6

20

05

20

07

20

09

20

11

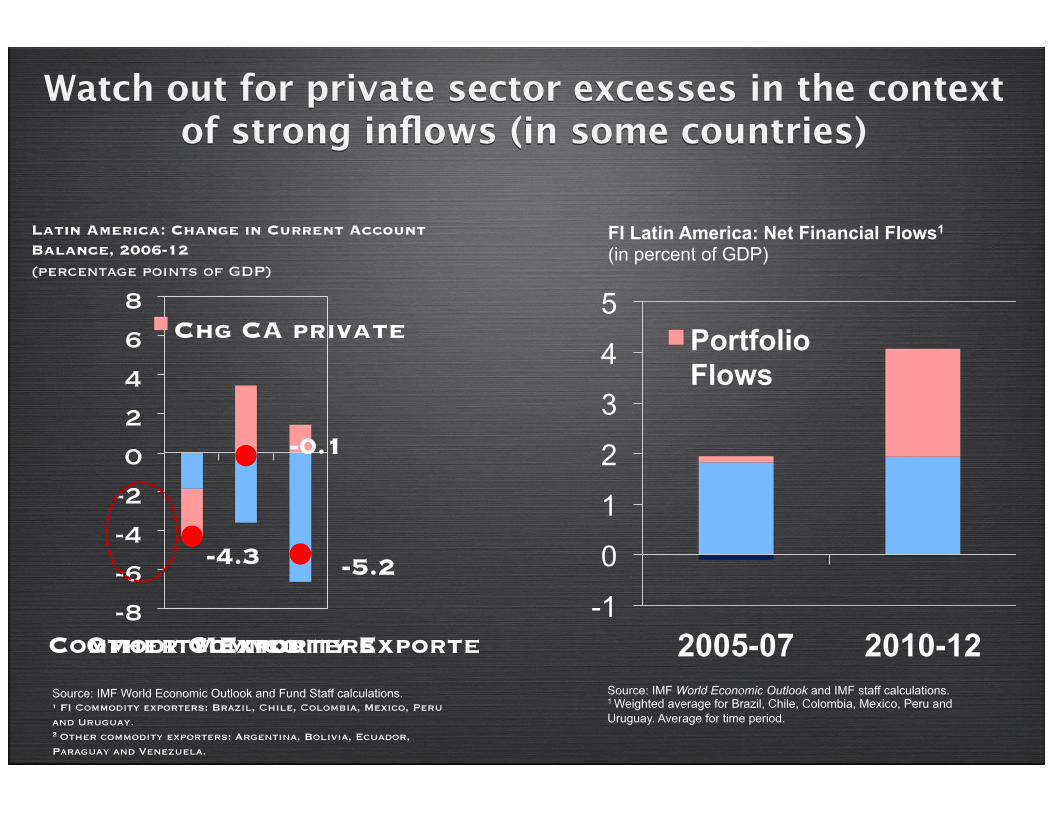

Watch out for private sector excesses in the context of strong inflows (in some countries)

-4.3

-0.1

-5.2

-8 -6 -4 -2 0 2 4 6 8

FI Commodity Exporters Mexico Other Commodity Exporters

Chg CA private

Latin America: Change in Current Account Balance, 2006-12 (percentage points of GDP)

Source: IMF World Economic Outlook and Fund Staff calculations. ¹ FI Commodity exporters: Brazil, Chile, Colombia, Mexico, Peru and Uruguay. 2 Other commodity exporters: Argentina, Bolivia, Ecuador, Paraguay and Venezuela.

-1

0

1

2

3

4

5

2005-07 2010-12

Portfolio Flows

FI Latin America: Net Financial Flows1

(in percent of GDP)

Source: IMF World Economic Outlook and IMF staff calculations. 1 Weighted average for Brazil, Chile, Colombia, Mexico, Peru and Uruguay. Average for time period.

International Monetary Fund Washington, DC. May 15, 2013.

Latin America: Key Takeaways Strong growth, moderating to potential

Widening current accounts, rapid credit and asset price growth (vulnerabilities building) Going forward:

ü Strengthen fiscal consolidation

ü Watch out for private sector excesses

ü Reforms to boost productivity and savings