journal of technical analysis (jota). issue 10 (1981, february)

TRANSCRIPT

LIBRARY MARKET TECHNICIANS ASSN.

70 Pine St, New Y&k. N. Y. 10005

Market Technicians Association

JOURNAL Issue 10 February 1981

MARKET TECHNICIANS ASSOCIATION JOURNAL

Issue 10

February 1981

i

Published by : Market Technicians Association 70 Pine Street

New York, New York 10005

Copyright 1981 by Market Technicians Association

-l-

-

i

intentionally blank

-2-

Market Technicians Association Journal

Editor : Anthony W. Tabell Delafield , Harvey, Tabell 909 State Road Princeton, New Jersey 08540

Associate Editor : Shary Anaya D elafield , Harvey , T abell

i

Thanks to the following MTA members and subscribers for their part in the creation of this issue:

Richard W. Arms Abraham W. Cohen Frederic H. Dickson Ann C. Fahnestock Steven C. Leuthold William P. Livesey Arthur A. Merrill Jack Y . Narayan Richard C. Orr Kenneth G. Tower

-3-

EDITORIAL

-

THE MTA JOURNAL

INDICATOR SYNERGY Richard C . Orr , Ph.D. Jack Y . Narayan , Ph. D .

13

The familiar “model, ” or combination of market indicators, is a predictive technique that has been utilized by many technicians. It has long been theorized that this combination produces a syn- ergistic effect, i.e. , the combination produces better results than the best of the individual indicators. The authors in this article demonstrate mathematically why this should be the case, drawing on the actual results obtained from two widely-used indicators. The appendix to the article provides a non-technical discussion of the Chi-squared technique of assessing significance. This technique is often of great value in testing stock market indicators.

Dick Orr , an MTA member, is an associate professor of mathematics at the State University of New York, Oswego, and a consultant to Pershing & Co. His co-author, Jack Narayan, is also a S .U.N .Y. professor.

SIGNIFICANCE : WHAT IS IT?? Arthur A. Merrill

Arthur Merrill is a charter member of the Market Technicians Association and was the 1977: winner of its Award for Distin- guished Contribution to Technical Analysis. One of his fortes for many years has been the advocacy of standards of statis- tical significance, and his ability to explain the derivation of those standards in easily understandable terms. This article is one more piece of evidence of that ability.

THE BEARISH SENTIMENT INDEX UPDATED Abraham W. Cohen

Abraham W. Cohen, a long-time MTA member, is the originator and foremost interpretor of the Investment Advisory Services Sentiment Indices. In this article he updates the bearish senti- ment indicator and discusses recent work that has been done by himself and others in the use of the indicator.

21

25

-

-4-

Issue No, 10 February, 1981

THE STOCK MARKET AS INFLATION HEDGE -- MYTH OR REALITY 29 Steven C. Leuthold

Analysts have for years debated the pros and cons of the stock market as an inflation hedge. Steven C . .Leuthold, author of the recently-published book The Myths of Inflation and Investing, from which this aritcle is excerpted and updated, comes down firmly in the opposing camp. Drawing on 109 years of stock- market history, Leuthold argues that both rapid inflation and rapid deflation tend to produce poor stock markets, and that the market does best during periods of price stability.

Leuthold, an MTA member, is vice president and director of Funds, Incorporated, and a special consultant to Piper, Jaffray, & Hopwood. He is also the author of Index Funds The Risks and Pitfalls, the definitive critique of the indexing concept.

OVERBOUGHT CAN BE BULLISH Kenneth G. Tower

The lo-day advance-decline line is one of the most widely- followed of all technical indicators. It is conventionally interpreted as a simple oscillator with extremely low levels being bullish and high levels bearish.

i

Kenneth Tower, on the technical staff of Delafield, Harvey, Tabell, has done some extensive research which suggests that “overbought” conditions on this indicator, whatever they may mean for the short term, tend, paradoxically, to be bullish for the intermediate or longer term.

45

NEW DAILY TECHNICAL MARKET INDICATORS Frederic H. Dickson William P. Livesey

51

There are many manipulations of stock price data which are basically simple in concept but which would be impossible to undertake with- out the availability of computer data bases. A prime example of such a manipulation are breadth indices based on advances and/or declines over periods of longer than one day. Such an indicator, with a half- dozen years of its history, is explored in this article by Fred Dickson, a long-time MTA member, and William P . Livesey of CompuServe, Inc.

Index (Continued)

DOW VOLUME AT ALL LEVELS Richard W. Arms

65

Dick Arms of Greeley Securities is widely known to MTA members as the originator of the Short-term Trading Index. His research is, however, eclectic, as this article shows. In it he explores the significance of volume occurring at various price levels in point- ing out support and resistance zones.

INSTITUTIONAL FLOW OF FUNDS IN THE STOCK MARKET Ann C. Fahnestock

69

Much is made of “institutional dominance” in the stock market, but precious little work has been done on actually quantifying institutional flow of funds. Ann Fahnestock explores the 15- year history of purchases and sales by major institutions and suggests some relationships between this activity and market direction.

Miss Fahnestock has been a member of the Market Technicians Association from its early years and has served as secretary, editor of the Newsletter, and as a member of the Board of Governors.

i

Book Review

CRISIS INVESTING

75 Anthony W . Tabell

Douglas R. Casey Stratford Press

-

-6-

MARKET TECHNICIANS ASSOCIATION

MEMBERSHIP and SUBSCRIPTION INFORMATION

REGULAR MEMBERSHIP - $50 per year plus $10 one-time application fee.

Receives the Journal, the monthly MTA Newsletter, invitations to all meetings, voting member status and a discount on the Annual Seminar Fee. Eligibility requires that the emphasis of the applicant’s professional work involve technical analysis.

SUBSCRIBER STATUS - $50 per year plus $10 one-time application fee.

Receives the Journal and the MTA Newsletter, which contains shorter articles on technical analysis, and the subscriber receives special announcements of the MTA meetings open to The New York Society of Security Analysts and/or the public, plus a discount on the Annual Seminar Fee.

ANNUAL SUBSCRIPTION TO THE MTA JOURNAL - $35 per year.

SINGLE ISSUES OF THE MTA JOURNAL (including back issues)

i

are available for $15 to regular members or subscribers $15 to non-members and non-subscribers

The Market Technicians Association Journal is scheduled to be published three times each fiscal year, in approximately November, February, and May.

An Annual Seminar is held each spring.

Inquiries for Regular Membership or Subscriber Status should be directed to:

Fred R. Gruber, V.P. United Jersey Bank 210 Main Street Hackensack, New Jersey 07602

-7- -.

i

intentionally blank

-8-

Editorial

THERE HADN’T OUGHTA BE A LAW

This is a journal for market technicians. The time is February, 1981. Editorials are supposed to comment on subjects of current interest. Under this particular confluence of circumstances, whatever our preferences, we would be burying our heads in the sand were we to fill this space with an editorial comment which did not mention the name “Joseph Granville. (’ Accordingly, a few thoughts on the subject.

There will be, in this commentary, at least, no thunderous pronouncements. It was, apparently, such portentiousness that set the whole thing off in the first place. It is our view that, at this stage, calmness and circumspection should best be the order of the day, and this advice is gratuitously offered to Joe Granville, as well as to members of the MTA.

Reaction, so far, has been on various levels and is, of course, interesting. Disbelievers in technical analysis were incredulous that a pronouncement by a market technician could have the kind of effect that it did. Daniel Seligman in Fortune, a critic, but a normally urbane one, totally blew his cool. Granville, Seligman positively stated, had nothing whatever to do with what happened on January ‘7. The $40 billion of NYSE loss on that day was clearly due to the fact that the Secretary of the Treasury had held a press conference and said the sort of thing that Treasury Secretaries say at press conferences. This is the sort of mindset that would blame the Johnstown flood on a leaky toilet in A ltoona.

From technicians we spoke to, the response was mixed, and --- let’s be honest and admit it, fellows --- not without a twinge of jealousy. “The Roar of the Grease Paint and the Smell of the Crowd” is a powerful anodyne. Who among us, his proscriptions ignored by the idiots whom he must advise, does not secretly yearn for the day when pearls dropping

-9-

from his lips can swing capital markets $40 billion in one direction or another? It is a heady feeling, but, like most temptations, best put behind one.

Perhaps the most common post-January-7 comment, however, was some form of that fine old American panacea, “There oughta be a law. ” This is the one reaction which, in our view? .is just about totally wrong. There should be no law, or, if there is to be one, its drafting should be approached with the extremest of caution, and the full extent of its possible consequences rigorously examined. Those investors who plunk down their hard-earned cash to subscribe to Joe Granville’s service and who choose to act on recommendations in that service are, let it be remembered, deploying their own money. The attitude which says that people are too stupid to manage their own affairs and require some sort of Big Brother to tell them how to do it properly, is one which has gotten us into enough trouble in enough areas already. We are right to be wary of it.

i

Here, we think, is the subtle danger that confronts us as a result of the events of early January. For whatever reason --- Granville’s prior record, his efforts at publicity, or the tone in which his pre- dictions were couched --- the size of the resultant market swing was huge. What is worrisome is that size serving as an excuse for calling down on the heads of the profession those who would like to see research in general, and perhaps technical research in particular, more ordered and regulated by authorities outside the profession than is already the case. Such regulation, it seems to us, is dangerously likely to be carried on by people unsuited for the task and whose preparation is apt to consist of such exercises as reading Eugene Fama’s Ph.D. dis- sertation. If Joe Granville proves to be the catalyst for this sort of effort, it will be this sin, and this sin alone, that earns him the deserved opprobrium of the profession.

Other issues are, of course, raised. The second paragraph of the MTA Code of Ethics says:

“The analyst shall not make statements which he knows or has reason to believe are inaccurate or misleading. He shall, in particular, be careful to avoid leading his audience to believe that his technically-derived views of future stock price behavior reflect foreknowledge rather than estimates and projections sub- ject to re-examination and, as circumstances may dictate, to change. l1

-

-lO-

There will be no comment in this space as to whether or not the collected works of Joseph Granville meet or fail to meet this standard. It is assuredly not the function of the Journal to decide this issue, and, in any case, the MTA, as a professional organization, can enforce a code of ethics only upon its own members. Official wrestling with the question would be a suitable task only for a membership committee

which would have to pass on Granville’s application for membership, should he choose to make one.

It seems appropriate for the MTA, at this stage, only to reiterate

that Code of Ethics, redouble its effort to enforce it among the member- ship, and make sure that all activities under its sponsorship are appropriate for an organization which adheres to such a code. Efforts at a certification program, conducted by the profession itself, are already underway, and ‘these efforts are worthy of support. The MTA has, in this case, the opportunity to lead, not by condemnation, but by example. This is an opportunity which should be seized.

-ll-

intentionally blank

-1%

INDICATOR SYNERGY

RICHARD C. ORR, PH.D.

and

JACK Y. NARAYAN, PH.D.

The familiar “model, ” or combination of market indicators, is a predictive technique that has been utilized by many technicians. It has long been theorized that this combination produces a syner- gistic effect, i.e., the combination produces better results than the best of the individual indicators. The authors in this article demonstrate mathematically why this should be the case, drawing on the actual results obtained from two widely-used indicators. The appendix to the article provides a non-technical discussion of the Chi-squared technique of assessing significance. This technique is often of great value in testing stock market indicators.

i

Dick Orr, an MTA member, is an associate professor of mathematics at the State University of New York, Oswego, and a consultant to Pershing & Co. His co-author, Jack Narayan, is also a S. U.N. Y. professor.

INTRODUCTION

Market indicators measure a variety of disparate rhythms of the market such as breadth, momentum, cycles, trends, and sentiment. Market technicians generally use a combination of indicators from a number of these categories, rather than relying only on a single “favorite” indi- cator. Two approaches which immediately come to mind are the informal combination of indicators based upon the considerable experience of the technician (e.g. Stan Weinstein of The Professional Tape Reader) and the formal combination of indicators to obtain the “weight of the evidence” (e. g. Art Merrill of Technical Trends). This effort to maintain a balance between various categories of indicators is curcial. For example, momen- tum indicators all tend, roughly, to measure a common characteristic of the market, albeit in different ways. While there is an advantage to the

-13-

use of more than one momentum indicator, one must keep momentum in proper perspective. It is only one facet of the market. As the market approaches a top, one’s stable of momentum indicators may be very bullish, in which case they may be giving an incorrect “signal.” At the same time, another category of indicators may be warning that the market is severely overbought, while yet another may show that sentiment is too bullish. The real power of these indicators, then, lies in their interaction.

The purpose of this paper is to demonstrate by means of a simple model the synergy generated by the simultaneous use of two indicators. The model by no means represents the state of the art in market timing, but is merely a device by which we will explore the added power obtained by the joint use of indicators. We wish to express our appreciation to Tony Tabell of Delafield , Harvey, Tabell for his generous assistance in obtain- ing up /down volume and DJIA historical data.

DESCRIPTION OF THE VARIABLES TO BE USED

Market behavior will be measured by using the daily close of the DJIA in the following manner. On a given day, the market will be considered bullish if, from that time forward, it rises at least 10 percent before cor- recting 5 percent. The market will be considered bearish if it falls at least 10 percent before rallying 5 percent. Should the market move less than 10 percent in a given direction before moving 5 percent in the other direction, it will be considered neutral. No time limit is prescribed. How- ever, historically these moves take weeks or months, not years.

One of the indicators we will use is the well-known percentage of all NYSE stocks above their lo-week moving average, published by Abe Cohen in Investors Intelligence. When the percentaye figure rises above 70 percent the market is considered overbought, but it may go higher. Hence, no action is recommended until the percentage figure again drops below the

8 70 percent level. At this point a bearish signal is given. Similarly, when the percentage figure drops below and then rises above the 30 percent level, a bullish signal is given. If the figure is either below 30 percent or above 70 percent, we will consider it to be neutral. As this data is compiled weekly, the state of this indicator is assumed to hold for an entire week.

The other indicator we will use employs an exponentially smoothed average of NYSE up volume minus down volume such that the data has a 16-day “half-life. ” A 25-day moving average of up volume minus down volume would probably serve the same purpose. The current value of this ex- ponentially smoothed average is compared with the value 10, 20, and 30 trading days earlier. If the current value is larger than all three of the previous values, then the indicator is considered bullish, while it is con- sidered bearish if the current value is smaller than all three previous values. Any other combination gives a neutral reading for this indicator.

-14-

DESCRIPTION OF THE EXPERIMENT

As we have now characterized, on a daily basis,the state of each of the two indicators; as well as the state of the market, we are ready to formulate hypotheses and test them. Our testing procedure will involve the selec- tion of a random sample of 144 of the 3,000 trading days from April 22, 1968 through April 15, 1986. We are sampling without replacement which means that no day will be represented more than once in the sample. The sampling will be accomplished by the use of a table of random numbers.1 The date corresponding to each of these numbers will then be determined and the state of both indicators as well as the market will be recorded in tabular form. From this first table, we will create three contingency tables to measure the interaction of the indicators, both individually and jointly, against the market. We will then calculate the %” (Chi-squared) value for each contingency table. The significance of XL and its compu- tation are described in an appendix to this paper. Eeyond this, we hope to gain an insight into the reliability of these indicators individually and jointly by simply observing the distributions in the several tables. The states of the indicators and the market will be denoted as follows: U for a bullish state, N for a neutral state and D for a bearish state. In the case of the joint use of indicators, we will hypothesize that if both indica- tors are in state U , then the market should be in state U abnormally often. If both indicators are in state D, or if the net volume indicator is in state N while the NYSE percent indicator is in state U, then the market should be in state D a disproportionate percentage of the time. This dissimilarity takes into account the old adage that “stocks will fall of their own weight. *’ If the NYSE percentage has moved above 30 percent and net volume either remains neutral or falls to neutral, we would expect this to be bearish more often than not. We will further hypothesize that any combination of indicator states other than the three described above will tend to produce a market state of N.

RESULTS OF THE EXPERIMENT AND CONCLUSIONS i

.- The experiment produced the following results. listed next to the frequencies.

Net Vol. NYSE Market

D

D

D

N

N

N

U

U

U

D

N

U

D

N

U

D

N

U

D N

5 7

2 15

1 1

2 9

5 19

9 6

0 0

3 18

3 9

Our original hypotheses are

U

1

5

1

2

2

4

0

3

12

Hypothesis

D

N

N

N

N

D

N

N

U

-15-

The contingency tables produced by this table are:

i

Table 1

Market

D N U

Table 2

Market

DN U

Table 3

Market

m DN U __

L 3c = 7.3

= 27.7

For a detailed explanation of the calculation of x’ values the reader is reminded to see the appendix. The larger the value of x/i the more dependent the market state is on the state of the indicator(s) listed on the left of the table. In Table 1, a s value of 7.3 is not very signifi- cant, but the p- values for the other two tables are very significant. Beyond this analysis, however, the reader will immediately notice a dra- matic improvement in Table 3 of the ratio of good predictions (down the main diagonal) to the bad predictions (which are circled) when compared to Table 1 and Table 2. This technique shows real promise in its applica- tion to the formal combination of various market indicators. While we have restricted our attention to only two indicators, this technique may be generalized to handle combinations of a larger number of indicators. 2

-16-

FOOTNOTES

1 These tables are readily available. See, for example, the Handbook of Tables for Probability and Statistics, published by the Chemical Rubber Company.

2 The interested reader with a background in statistics should see Feinberg , The Analysis of Cross-Classified Categorical Date, M.I.T. Press.

i

-17-

APPENDIX

CALCULATION AND INTERPRETATION

OF

CONTINGENCY TABLES

We will use Table 3 from before as our model. This table together with all row sums and column sums should be displayed.

The entries in the table below the diagonal lines are the expected frequencies assuming that the joint indicators and the market are independent of one another. These are calculated by taking the appropriate row total times the appropriate column total and dividing by the grand total. For example, the third row, second column of the table has an observed frequency of 9 and an expected frequency of (24) (84) /144 = 14.0. The XL function for a contin- gency table is given by the formula

-18-

= (Observed - Expected) 2

each cell Expected

so the contribution of the cell we just considered to the total for 2

would be (9.0 - 14.0)2 = 1 *

x

14.0 . .

IL If we list in tabular form each of the nine cells’ contributions to we have

Market

N U

1.7 .4

2.2 1.5

1.8 9.8

= 27.7

Notice that the main diagonal contributes 20.0 of the total, and that in each case the observed frequency is higher than the expected frequency. In order to determine the significance of this, we must look up XL in a set of tables. To do this, we must calculate the number of degrees of freedom for this test, given by the formula

i Degrees of Freedom = (# of rows - 1) (# of columns - 1)

We therefore look up z- = 27.7 with ( 3- 1) ( 3-1) = 4 degrees of freedom and discover that this value is significant at the .Ol level. * The joint indi- cators are not independent of the market and, in fact, have abnormally high concentration along the main diagonal of the table.

*For a brief description of levels of significance, see Orr, The Timely Demise of the Random Walk, Journal, February, 1980.

-19-

intentionally blank

-2o-

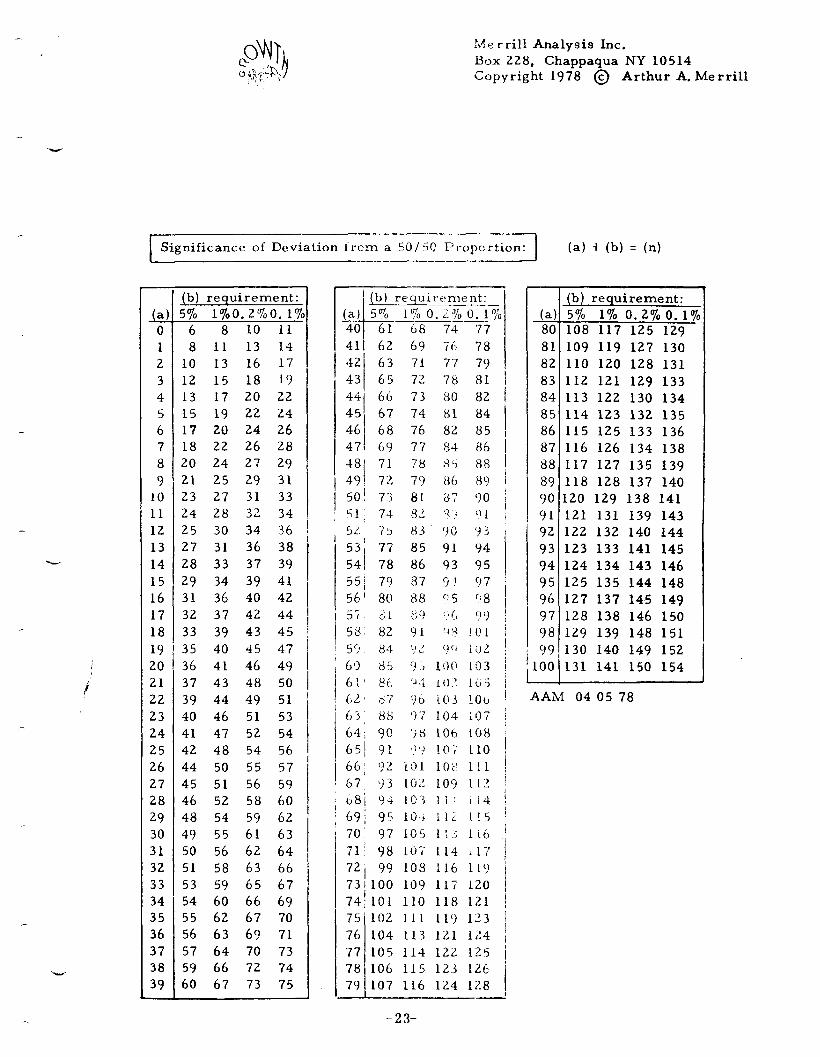

SIGNIFICANCE: WHAT IS IT??

i

ARTHUR A. MERRILL Merrill Analysis Inc.

Arthur Merrill is a charter member of the Market Technicians Association and was the 1977 winner of its Award for Distin- guished Contribution to Techncial Analysis. One of his fortes for many years has been the advocacy of standards of statis- tical significance , and his ability to expZain the derivation of those standards in easily understandable terms. This article is one more piece of evidence of that ability.

The “witchcraft” appellation can be dispelled by the use of just two words: Significant Evidence.

The second word is easy. We all support our conclusions with evidence. But do we always check significance ? the suspicion of luck

Are the examples we cite sufficient to dispel ? As John Heywood put it in 1577, “One swallowe prouveth

not that summer is neare. ”

To check for significance, some knowledge of- statistics is needed. But don’t be alarmed; the problem may have an easy solution. Many of our conclusions are simple two-way: after this breakout. ”

“The price of this stock will probably be higher two weeks “The Dow will probably close higher next Friday. ” The

result is two way: Up-Down, or Right-Wrong. The statistician’s buzz word for this type is “binomial,” and tables giving the answers are quite easy to use.

The tables in this paper deal with the problem when the basic probabilities are about even money. The problem is more complicated if the odds are biased one way or the other; if, for example, we are forecasting a rise in an upward trend. There are methods, but we don’t discuss them here.

But suppose the odds are about even. lette red and black is another.

Matching coins is a good parallel. Rou- Serious workers who use evidence like to see

odds of 20-to-1 against simple luck before calling the results “probably signifi- cant . ” If the evidence shows loo-to-l, it’s called “significant;” 1000~to-1 is

-21-

called “highly significant. ” The first is called the “95% confidence level.” The second, the “99% confidence level, ” the third, the “99.9% confidence level. ‘I

The 20-to-1 doesn’t mean a test with 20 successes and 1 failure. It is reached when a test has six successes and no failure, or eight successes and one fail- ure . You will see this when you use the following table. The loo-to-1 can be reached by a test with eight successes and no failures. The table gives the required ratios for various test sizes. It’s easy to use:

The Problem

In a situation with two solutions, with an expected 50/50 outcome (heads and tails, red and black in roulette, stock market rises and declines, etc. ) are the results of a test significantly different from 50/50?

Solution

Call the two outcomes (such as number of reds, number of blacks) (a) and (b) . Let (a) be the smaller of the two. Find this number in the left hand column of the tabulation. If (b) exceeds the corresponding number in the 5% column, the difference from 50/50 is probably significant; the odds of it happening by chance are one in twenty. If (b) exceeds the number in the 1% column, the difference can be considered significant ; the odds are one in a hundred. If (b) exceeds the numbers in the 0.2% (one in five hundred) or 0.1% (one in a thousand), the difference is highly significant. Note that the actual numbers must be used for (a) and (b) , not the percentages.

Example

In the last 83 years, on the trading day before the 4th of July holiday, the stock market went up 65 times and declined 18 times. Is this significant? On the day following the holiday, the market rose 50 times and declined 33 times. Significant ?

For the day before the holiday, (a) = 18 and (b) = 65. Find 18 in the left hand column; 65 far exceeds the 33, 39, 43, and 45 in the table, sothe record demon- strates a-highly significant bullish bias on that day.

For the day following the holiday, (a) = 33 and (b) = 50. Find 33 in the left hand column. The minimum requirement for (b) is 53; 50 falls short; no signifi- - cant bias is demonstrated.

Source

Some of the figures were developed from a 50% probability table by Russell Langley (in Practical Statistics Simply Explained, Dover 1971)) for which he used binomial tables. Some of the figures I calculated using a formula for Chi- squared with the Yates correction. This table was distributed at our 1978 seminar.

-22-

.‘\de rrill Analysis Inc.

Box 228, Chappaqua NY 10514 Copyright 1978 @ Arthur A. Merrill

-- Significance of Deviation frcm a SO/ 5(! Fropcrtion:

7 (a) + lb) = (n)

-

(a) 0 1 2

3

4

5

6

7

8

9 10 11

12

13

14

15

16

17

18

19 20 21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39 -

(b) requirement:

5% l%O. 2%0. 1% 6 8 10 11

8 11 13 14

10 13 16 17

12 15 18 19

13 17 20 22

15 19 22 24

17 20 24 26

18 22 26 28

20 24 27 29

21 25 29 31

23 27 31 33

24 28 32 34

25 30 34 36

27 31 36 38

28 33 37 39

29 34 39 41

31 36 40 42

32 37 42 44

33 39 43 45

35 40 45 47

36 41 46 49

37 43 48 50

39 44 49 51

40 46 51 53

41 47 52 54

42 48 54 56

44 50 55 57

45 51 56 59

46 52 58 60

48 54 59 62

49 55 61 63

50 56 62 64

51 58 63 66

53 59 65 67

54 60 66 69

55 62 67 70

56 63 69 71

57 64 70 73

59 66 72 74

60 67 73 75

’ (b) requircbment:

-+-

(a) 5% IX 0.2% 0.1%

40 6168 74 ‘7 7

411 62 69 -ii, 78

421 63 ‘71 77

431

79

65 72 78 81

44’ 66 73 80 a2

45 67 74 81 84

46

471

68 76 82 85

69 77 84 86

48’

49. I

71 ? 8 $5 a5 72 79 86 89

50! 73 a1 87 30

51 74 32 9, .J

f)O

“1

j

,

(b) requirement:

(a) 5% 1% 0.2% 0.1% 80 108 117 125 129

81 109 119 127 130

82 110 120 128 131

83 112 121 129 133

a4 113 122 130 134

85 114 123 132 135

86 115 125 133 136

87 116 126 134 138

88 117 127 135 139

89 118 128 137 140

90 120 129 138 141

91 121 131 139 143

92 122 132 140 144

93 123 133 141 145

94 124 134 143 146

95 125 135 144 148

96 127 137 14,5 149

97 128 138 146 150

98 129 139 148 151

99 130 140 149 152

100 131 141 150 154

97 105 1 it,

71 j 98 107 114 117

72i 99 108 116 ll?

731100 109 11; 120

741101 110 118 121

-23-

intentionally blank

-24-

THE BEARISH SENTIMENT INDEX UPDATED

ABRAHAM W. COHEN Investors Intelligence

Abraham W. Cohen, a long-time MTA member, is the originator and foremost interpretor of the Investment Advisory Services Sentiment Indices. In this article he updates the bearish senti- ment indicator and discusses recent work that has been done by himself and others in the use of the indicator.

An explanation of the construction and interpretation of the Bearish Senti- ment Index appeared in the first issue of the Market Technicians Journal. A very brief review of this material will be of value to those to whom this index may be entirely new.

The Bearish Sentiment Index is based on the opinions of about 100 invest-

i ment advisory services as to the present and future trend of the stock market. The great majority of these services are technically oriented. Their opinions, taken weekly, are classified in three categories, bullish, bearish, and those expecting a correction or consolidation. The third cate- gory consists of “waiting” bulls. These three classes are then expressed in percentages - % of bulls, % of bears, etc.

For the purpose of interpretation, the bearish % is most important and is the only percentage that is charted and compared to the action of the Dow- Jones Industrial Average. The reason for this is that a bearish advisory service is usually unequivocal in its opinion whereas a bullish advisory service often hedges its opinion. A bearish advisory service tells you to sell your stocks, to go short, to buy puts. There is no mistaking that such advice is bearish.

Since most services are trend followers, they tend to turn less bearish as the Dow-Jones Industrial Averages rises, and become more bearish as this average falls. Investment Advisory Services will be least bearish at market

-25-

I -, ,............ ;t a 6 : 2

Ffi

. . . . . (’ .r P L E a + i . . . . . 3 2 i -

.i.i./.l.l.i.I.!.l. . . . . .I. . . _ .I_ . . .

tops and most bearish at market bottoms. The Bearish Sentiment Index can, therefore, be used as an indicator of Contrary Opinion. The consensus of opinion is always wrong at extremes -- when too many agree to the same pro- position.

Originally the parameters of this index were about 10% and 60%. When only about 10% of the advisory services were bearish, it was time to look for a market top; when about 60% of the services were bearish it was time to look for a market bottom. However, in the last few years, these parameters may have changed to adjust to the narrower fluctuations in the Dow-Jones Indus- trial Average.

Arthur Merrill, the leading statistician among market technicians, suggests parameters of 18.4% and 42.9%, i.e., a Bear market should be looked for when the bearish % falls below 18.4% and a Bull market when it rises above 42.9%. Merrill also issues reports on the indicators “which had the best performance in a twelve-year test.” His report of January 13, 1981, puts the Bearish Sentiment Index at the top of the list. (Arthur Merrill is the editor and pub- lisher of Merrill Analysis, Box 228, Chappaqua, New York 10514)

Ned Davis, another leading market technician, while still editor of the “J. C . Bradford Market Timing Letter, v in its issue of June, 1980, made a detailed study of the extremes in the Bearish Sentiment Index since 1965 and correlated these figures with what happened in the Dow-Jones Industrial Index. He found that “in 40 out of 43 cases, the market proceeded to move exactly oppo- site to the predictions of the ‘experts’ when they were at extreme positions.” (Ned Davis is now co-editor with Martin Zweig of “Traders Hotline,” 747 Third Avenue, New York,, New York 10017)

A detailed study of the Sentiment Index by John C. Boland appeared in the September 1, 1980 issue of Barron’s. Mr. Boland uses a unique method of interpreting the index. He subtracts the % of Bears from the % of Bulls.

i “When the bulls have the upper hand, the resulting figure is positive. When the bears are more numerous the figure is negative. That provides a measure of bullish-bearish sentiment. l1 His study shows that the consensus opinion of investment advisors has been much more often wrong than right, and he con- cludes that, although advisor sentiment has a “sad history,” it isn’t a foolproof key to forecasting market moves. It should be pointed out that Mr. Boland places equal weight on both the bullish and bearish percentages, whereas Investors Intelligence relies solely on the Bearish %. However, he also concludes that “advisor sentiment retains one important value. A move that doesn’t draw the advisors along has traditionally had a way to go. ”

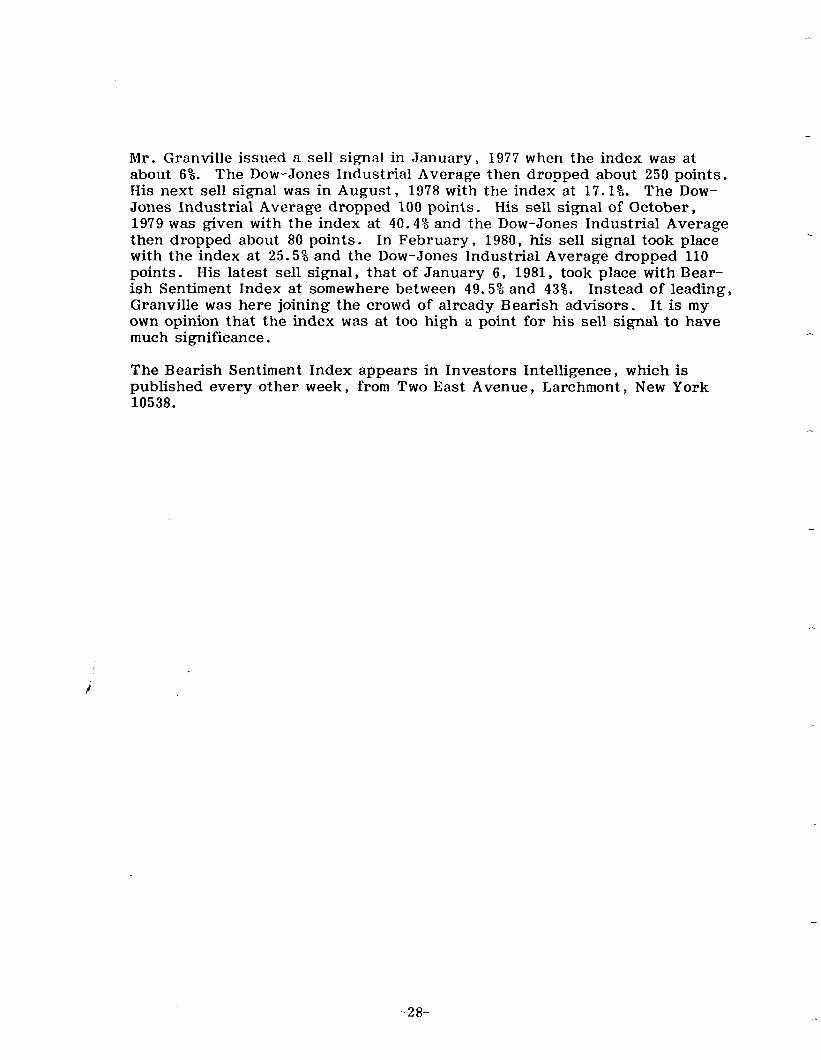

No article can be complete today without some comment on Joseph Granville’s latest sell signal. Mr. Granville, in his market letter, has often stated that the Bearish Sentiment Index is one of the indicators to which he pays attention. Correlating his sell signals with the Bearish Sentiment Index may prove inter- esting and revealing.

- 27-

Mr. Granville issued a sell signal in January, 1977 when the index was at about 6%. The Dow-Jones Industrial Average then dropped about 250 points. His next sell signal was in August, 1978 with the index at 17.1%. The Dow- Jones Industrial Average dropped 100 points. His sell signal of October, 1979 was given with the index at 40.4% and the Dow-Jones Industrial Average then dropped about 80 points. In February, 1980, his sell signal took place with the index at 25.5% and the Dow-Jones Industrial Average dropped 110 points. His latest sell signal, that of January 6, 1981, took place with Bear- ish Sentiment Index at somewhere between 49.5% and 43%. Instead of leading, Granville was here joining the crowd of already Bearish advisors. It is my own opinion that the index was at too high a point for his sell signal to have much significance.

The Bearish Sentiment Index appears in Investors Intelligence, which is published every other week, from Two East Avenue, Larchmont , New York 10538.

i

-28- . .

THESTOCK MARKET AS INFLATION HEDGE --

MYTH OR REALITY

STEVEN C. LEUTHOLD Vice President & Director

Funds, Inc.

Analysts have for years debated the pros and cons of the stock market as an inflation hed.qe. Steven C. Leuthold, author of the recently-published book The Myths of Inflation and Inv&ting. from which this article is excerpted and updated, comes down firmly in the opposing camp. Drawing on 109 years of stock- market his tory, Leuthold argues that both rapid inflation and rapid deflation tend to produce poor stock markets, and that the market does best during periods of price stability.

Leuthold, an MTA member, is vice president and director of Funds, incorporated, and a special consultant to Piper, Jaffray, & Hopwood. He is also the author of Index Funds The Risks and Pitfalls, the definitive critique of the indexing concept.

i

There exists the widespread belief that the stock market provides a hedge against price inflation. Close examination of the historical record tends to indicate, by and large, this is not the case. The stock market tends to perform poorly both in highly inflationary and highly deflationary periods. The best environment for the stock market tends to be stability. As long as inflation or deflation does not exceed 3 percent, there is no adverse effect on stock prices.

INVESTMENT PERFORMANCE IN A HIGH-INFLATION ENVIRONMENT

Taking a closer look, what has been the stock market’s comparative record in years when inflation was 4 percent or more?

Contrary to the almost universally accepted dogma of the 1950’s and 1960’s, which held that common stocks were the best inflation hedge, history clearly reveals the market provided no protection at all when inflation was at or

-29-

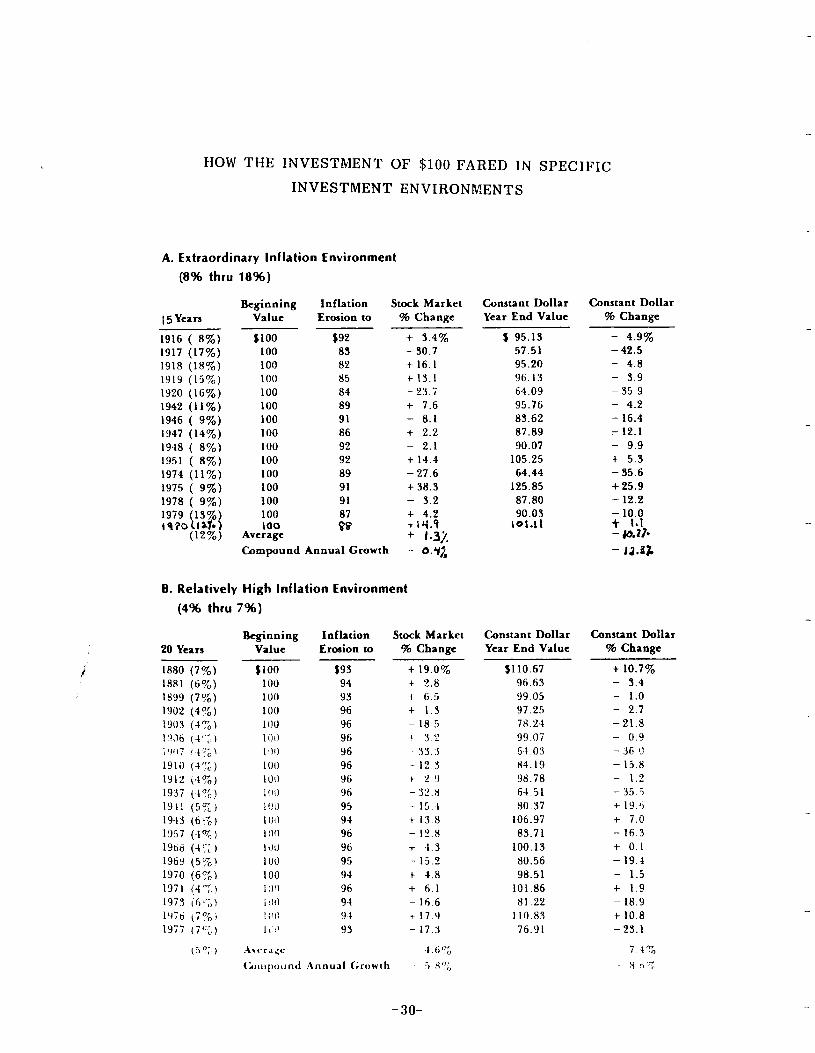

HOW THE INVESTMENT OF $100 FARED IN SPECIFIC

INVESTMENT ENVIRONMENTS

A. Extraordinary Inflation Environment

(8% thru 18%)

Beginning Inflation Stock Market

15 Years Value Erosion to % Change

1916 ( 8%) $100 $92 + 3.4%

1917 (17%) 100 83 - 30.7

1918 (18%) 100 82 + 16.1

1919 (15%) 100 85 t 13.1

1920 (16%) 100 84 - 23.7

1942 (11%) 100 89 + 7.6

1946 ( 9%) 100 91 - 8.1

lY47 (14%) 100 86 + 2.2

1948 ( 8%) 100 92 - 2.1

1951 ( 8%) 100 92 + 14.4 1974 (11%) 100 89 - 27.6

1975 ( 9%) 100 91 + 38.3

1978 ( 9%) 100 91 - 3.2

100 + 4.2 LOO T lri.9

Average + 1.3% Compound Annual Growth - o.r2

B. Relatively High Inflation Environment

(4% thru 7%)

20 Years

1880 (7%) 1881 (6%)

1899 (7%) 1902 (4?‘,)

I’)03 (4T,, Imj (i“;. 1 ;‘,I17 !it-o\

1910 (4”;)

1912 (4%) 1937 (-406)

1911 (5%) 19-43 (6fo)

1357 (4%)

1968 (-II‘: ) 196Y (5%)

1970 (647,) 1971 (47,)

1973 ifi’;,) 19;ti (7?&, 1977 (7’:. ) u

(Ti*;,)

Beginning Inflation Stock Market

Value Erosion to % Change

$100 $93 + 19.0% 100 94 + 2.8 100 93 t G.5

100 96 + 1.3 1w 96 - 18.5

1111) 96 1 3.”

1’)O Y6 33..1 IO0 96 - 12.3

101) ‘36 + 2Y illI) 96 - 32.kl

II!0 95 - 15. I 100 94 + 13.8 1110 96 - 12.8

II)0 96 + 4,s lU0 95 - 15.2

100 94 + -4.8 !:I(? 96 + 6.1 ia)0 9-4 - 16 6 !:l:: 94 + 17.Y It :’ YS - 17.3

;\tC.r2jC .I (i ‘,V&

(;nqwuncl Annual (irowth 5 H “I

Constant Dollar Constant Dollar

Year End Value % Change

$ 95.13

57.51 95.20 96.13

64.09

95.76 83.62 87.89

90.07

105.25 64.44

125.85

87.80 90.03

LOl.11

Constant Dollar

Year End Value

$110.67

96.63 YY.05

97.25 78.24

9Y.07

G-4.03

84.19 98.78 64.51

so.37

106.97 83.71

100.13

80.56 98.51

101.86 81.22

110.83 76.91

- 4.9%

- 42.5 - 4.8

- 3.9 - 35.9

- 4.2 - 16.4 - 12.1

- 9.9

+ 5.3 - 35.6 •t 25.9

- 12.2

Constant Dollar

% Change

+ 10.7% - 3.4 - 1.0

- 2.7

-21.8 - 0.9 -JG 1::

- 13.8 - 1.2 - 35.5

+ lY.‘j

+ 7.0 - 16.3

+ 0.1

- 19.i - 1.5

+ 1.9

- 18.9 + 10.8

- 23.1

-3o-

above 4 percent. It is interesting to note that when it was generally accepted that stocks were an inflation hedge, inflation only equaled or exceeded 4 per- cent in four widely-spaced years -- 1951, 1957, 1968, and 1969.

During the past 109 years there have been 35 years with annual inflation rates of 4 percent or higher. In only eight of these years did the stock market manage to keep pace with or rise more than the inflation rate (excluding divi- dends) . In those 109 years, including 1979, there have been nine years when inflation blazed at levels of 10 percent or higher. 1980 was the only one of those nine years in which the stock market outperformed the inflation rate (See tables). In the years of extraordinary inflation, shown in Table A, the market was up nine years and down six, but the compound annual growth rate for the period was minus 9.4 percent, while in constant dollars the compound annual rate eroded to minus 12.3 percent. In the periods of relatively high inflation -- 4 percent to 7 percent, shown in Table B , -- the market was up 11 years and down nine, but again finished with a negative compound annual growth rate -- minus 5.8 percent, while in constant dollars the loss mounted to an 8.6 percent compound annual rate.

PERIODS OF MODERATE INFLATION OR STABILITY

What has been the historic stock market behavior in periods of moderate infla- tion -- 2 percent to 3 percent ? Consider the data shown in Table C.

If you had invested only in the 21 years when inflation was in the 2 percent to 3 percent range, you would have had 7.1 percent compound annual rate of return (excluding dividends). Even after factoring out inflation (in constant dollars), the return would have been 4.6 percent. The market declined more than 15 percent only one year - 1966- in this environment; and there were only eight years out of 21 when the market returns were negative.

i In summary, inflation at these lower levels would seem to have no adverse effect on the stock market. However, the investment record, although good, falls significantly short of the market performance found in the environment of price stability if viewed in terms of constant dollars.

The stock market appears to react most favorably in periods of relative price stability, when inflation is 1 percent or less, or when deflation is 1 percent or less. Those periods are summarized in Table D. In only eight of the 30 years in which these conditions existed was there a losing market, and only in 1893 did the decline exceed 15 percent.

The compound annual growth rate for these years was 8 percent (about 13 percent when dividends are included) with a one year high of 44 percent in 1954. Even in constant dollars, the growth rate was an impressive 7.7 percent. Unfortunately, the last years in which these stable conditions existed were 1961, 1962, 1963, and 1964.

-31-

----.’ THE INVESTMENT OF $100 FARED IN SPECIFIC HUW

INVESTMENT ENVIRONMENTS

C. Moderate inflation Environment

(2% thru 3%)

21 Years Inflation Erosion to

Stock hlarket 96 Change

Constant Dollar Scar End Value

1 w! (2 7; ) f ! (3 ! ! S9R IA97 (2%) 10:) 98

1558 (2%) 100 98

1890 (2%) 100 98

1897 (2%) 1 cm 98 1900 (2%) 1 on 98 1901 (2%) 100 98

1923 (2%) 100 98 1925 (3%) 100 97

1934 (3%) 100 97

1935 (3%) 100 97

1944 (2%) 100 98

1945 (2%) 100 98

1952 (2%) 100 98

1956 (2%) 100 98 1958 (3%) 100 97

1960 (2%) 100 98

1965 (2%) 100 98

1966 (3%) 100 97

1967 (3%) 100 97

1972 (3%) 100 97

- 2.05;.

- 6.5 - 2.4

- 13.6 + 12.9

+ 14.1 + 15.8

- 2.4 + 22.8

- 1.1

+ 37.0 + 12.1 + 26.7

+ 8.4

+ 2.3 + 34.0

- 9.3 + 10.9

- 19.0 + 15.2

+ 14.6

5 95.16

91.63 95.65

84.67 110.64 111.82

113.48

95.65 119.12

95.93 132.89

109.86 124.17

106.23

100.25 129.98

88.89 108.68

78.57 111.74

111.16

Constant Dollar % Change

- 4.8%

- 8.4 - 4.3

- 15.3 + 10.6

+ 11.8 + 13.5

- 4.3 + 19.1

- 4.1

+ 32.9 + 9.9 + 24.2

-I- 6.2

+ 0.3 + 30.0

- 11.1 + 8.7

-21.4 + 11.7

+ 11.2

(2%) Average + 8.1% + 5.5%

Compound Annual Growth + 7.1% + 4.6%

E. Moderate Deflation Environment

(2% thru 4%)

13 Years

Bqinning Inflation

Value Erosion IO % Change

Conscant Dol!ar Consant Dollar Year End Value % Change

SIOO

100 100

100 100

100

100 100

100 ::10

1W

100 100

$102 102

104 102

102 102

102 102

102 If17

102 103 IO?

5 88.74 105.26

94.12 145.86

93.13

122.20 110.67

105.26 120.56 14 1.42

128.63 73.23

130.66

(2%) Average i 9.80/;, + 12.3%

Compound Annual Growth + 7.8% + 10.3%

-32-

- 11.3yo

t 5.3 - 3.9

+ 45.9 - 6.9 + -9 9 .-L._

+ 10.7 i 5 .3 - L,I, 6

f -11.4 t 2R.R

-26.8

+ 30.7

HOW THE INVESTMENT OF $100 FARED IN SPECIFIC

INVESTMENT ENVIRONMENTS

D. Stable Environment

(1% or Less Inflation/Deflation)

Inflation/

SO Years Deflation

1872 1% D 1892 1% D 1893 -O- 1895 -o-

1896 -O-

1898 1% 1 1904 -O-

1905 -O-

1909 -O-

1911 -O- 1913 1% D 1914 1% I 1915 1% 1 1924 -O- 1926 1% I 1928 1% 1 1929 -O- 1956 -O-

1939 1% D 1940 1% 1 1949 1% D 1950 1% 1 1953 1% I 1954 1% 1 1955 -O- 1959 1% 1 1961 1% 1 1962 1% I 1963 1% 1 1964 1% 1

i

10 Years

1875 ( 5%) $100 $105

lA76 ( 5%) 100 105

1878 ( 6%) 100 106

1884 ( 6%) 100 106

1894 ( 8%) 100 108

1921 (11%) 100 111

1922 ( 6%) 100 106

1931 ( 9%) 100 109

1932 (10%) 100 110

1933 ( 5%) 100 105

( 7%)

-0.

Adjustment Beginning Inflation/ Stock Market Constant Dollar Constant Dollar

Value Deflation 96 Change Year End Value 96 Change

$100 $101 + 6.9% $107.97 + 8.0% 100 101 + 1.4 102.41 + 2.4

100 100 - 19.8 80.20 - 19.8

100 100 + 1.0 101.00 + 1.0

100 100 - 2.3 97.70 - 2.3

100 99 t 18.6 117.41 + 17.4

100 100 t 25.6 125.60 + 25.6 100 100 + 16.0 116.00 + 16.0

100 100 + 14.3 114.30 + 14.9

100 100 + 1.0 101 .oo -I- 1.0

100 101 - 14.2 86.66 - 13.3 100 99 - 9.0 90.09 - 9.9

100 99 + 31.6 130.28 + 30.3 100 100 + 18.6 118.60 + 18.6

100 99 t 5.1 104.05 + 4.1

100 99 t 28.Y 127.51 + 27.5

100 100 - IO.3 89.70 - 10.3

100 100 + 28.9 128.90 t 28.9 100 101 - 3.0 97.99 - 2.0

100 99 - 12.7 86.43 - 13.6 100 101 t 12.9 114.03 + 14.0

100 99 t 17.6 116.42 + 16.4

100 99 - 3.8 95.24 - 4.8

100 99 t 44.0 142.56 t 42.6

100 100 t 20.8 120.80 + 20.8

100 99 + 16.4 115.24 + 15.2

100 99 t 18.7 117.51 + 17.5

100 99 - 10.8 88.31 - 11.7

100 99 t 17.0 115.83 + 15.8 100 99 + 14.6 113.45 + 13.5

Average t 9.1% + 8.8%

Compound Annual Growth t 8.0% + 7.7%

F. Extraordinary Deflation Environment

(5% thru 11%)

Beginning

Value

Deflation Adjustment

Stock Market % Change

Constant Dollar

Year End Value

- 4.2% 5100.59

- 18.0 86.10

+ 6.3 112.68

- 18.7 86.18

- 2.8 104.98

+ 7.3 119.10

+ 20.1 127.31

- 46.6 58.21 - 19.4 88.66

+ 49.5 156.98

Average - 2.7%

Compodnd Annual Growth - 5.9%

Constant Dollar % Change

+ 0.6% - 13.9

+ 12.7

- 3.8 + 5.0 + 19.1

-I- 27.3

-41.8 - 11.3 + 57.0

+ 5.1%

+ 1.9%

-33-

DEFLATIONARY ENVIRONMENTS

Years of moderate deflation appear to be favorable for the market. In the 13 years of moderate deflation (prices declining between 2 percent and 4 percent), as shown in Table E , the market advanced in nine years and declined in four. A person who confined investing to only those years would have experienced a 7.8 percent compound annual growth rate, not much lower than in the years of relative price stability. In constant dollar terms, he would have done even better because on an inflation-adjusted basis the growth rate was 10.3 per- cent compounded annually. However ,. the sample here is relatively small -- only 13 years -- and also ancient, with only three instances since the turn of the century. Therefore it is difficult to say with confidence that moderate deflation is the best env-iornment for the market.

In the 10 years of extraordinary deflation, as shown in Table F, when prices fell between 5 percent and 11 percent, investment experience was generally not good. Only 1922, when the market was up 20.1 percent, and 1933, when the market was up 49.4 percent, were good years. An investor who limited his investing to this kind of environment would have experienced a 5.9 percent compound annual loss, although, because of the high levels of deflation, his result on a constant dollar basis was actually a 1.9 percent gain.

Thus, the best environment for investing in the stock market seems to be years of relative price stability, with some eiidence that this is followed closely by years of moderate deflation. Investing in years of extraordinary inflation, relatively high inflation or extraordinary deflation brought poor results.

But can you make money in the stock market with all this knowledge?

CAN WE PREDICT INFLATION?

From a practical standpoint, the catch, of course, is knowing at the beginning i of a particular year what the inflation or deflation rate for that year will be.

One approach would be to assume that next year’s inflation or deflation rate will approximate this year’s. Unfortunately, this does not work well at all. There is very little year-to-year inflation or deflation stability. AnaIyzing the historic data, through 1979, we find that the odds of a particular year’s infla- tion/deflation environment being repeated in the following year are less than 50-50.

If This Year’s Environment Is : The Odds Next Year’s Environment Will be the Same Are:

Extraordinary Deflation 38% Moderate Deflation 16 Price Stability 35 Moderate Inflation 23 High Inflation 17 Extraordinary Inflation 45

-34-

So, even though the research indicates there is a correlation between annual stock market movements and the annual rate of inflation or deflation, this information, although helpful to the investor, does not qualify as an invest- ment panacea. It is not a magic key to successful investment strategy because it depends on one’s ability to predict inflation or deflation levels one year in advance. And predicting next year’s inflation or deflation, especially when inflation is currently high, could be as difficult as predicting next year’s stock market.

Most people will be surprised to learn the inflation rate during the span of this study. Most would probably guess it has been about 3 percent per year, but in fact it has been but half that. Equally surprising may be that during this 109year period there were 38 years when there was no inflation, includ- ing 31 years of deflation. Unfortunately, that still left us with 71 years of inflation of one degree or another, and thus, with a problem for the stock market investor.

In 12 of the 109 years, inflation exceeded 8 percent, and in only two of those years, 1975 and 1980, did the stock market beat inflation. In three of the 12 years, the market was horrible.

TWELVE YEARS WHEN INFLATION TOPPED 8 %

Inflation Year Stock Market Change

9” 0, 1978 - 3% 9 1946 -8 9 1975 +38

11 1942 +7 11 1974 -28 12 1980 +15 13 1979 +4 14 1947 +2 15 1919 +13 16 1920 -24 17 1917 -31 18 1918 +16

Contrary to what might be expected, the shift from an inflationary environment to a deflationary one need not be gradual. It can be quite abrupt. For example, in 1919 the country suffered through 15 percent inflation, and in 1920 it had 16 percent inflation, but in 1921 it had 11 percent deflation. Similarly, in 1947 the country had 14 percent inflation followed by 8 percent inflation in 1948, and then 1 percent deflation in 1949.

-35-

1%

1872 + 6.9%

1898 +18.6 1914 - 9.0

1915 +31.6 1926 + 5.1 1928 +28.8

1940 -12.7 1950 +17.6 1953 - 3.8

1954 +44.0

1959 +16.4 1961 +18.7

1962 -10.8 1963 + 17.0 1964 +14.6

7%

YEARS OF INFLATION 1872- 1980

Includes Annual Stock Market Performance Excluding Dividends

Annual Inflation Rate

2%

1882 - 2.9% 1887 - 6.5 1888 - 2.4

1890 -13.6 1897 +12.9

1900 +14.1 1901 +15.8

1923 - 2.4 1944 +12.1

1945 +26.7 1952 + 8.4

1956 + 2.3 1960 - 9.3

1965 +10.9

3% 4%

1925 + 22.8% 1934 - 1.1

1935 +37.0 1958 +34.0

1966 -19.0 1967 +15.2 1972 +14.6

1902 + 1.3% 1903 -18.5

1906 + 3.2 1907 -33.3

1910 -12.3 1912 + 2.9

1937 -32.8 1957 -128 1968 + 4.3

1971 + 61

5% 6%

1941 -15.4% 1881 + 2.8% 1969 -15.2 1943 +13.8

1970 + 4.8

1973 -16.6

1976 +17.9

8% 9% 10% 11% 12% 13% 14% 81 Over

1880 +19.0X 1916 + 3.4% 1946 - 8.1% - 1942 + 7.6% 'f@ 1979 + 4.2% 1947 + 2.2% (14)

1899 + 6.5 1948 - 2.1 1975 +38.3 1974 -27.6 df..t]. 1919 +13.1 (15)

1977 -17.3 1951 +14.4 1978 - 3.2 1920 - 23.7 (16) 1917 -30.7 (17)

1918 +16.1 (18)

11%

!321 - 7.3?+#

5%

1875 - 4.2% 1876 -180

1933 +495

YEARS OF DEFLATION 1872-1980

Includes Annual Stock Market Performance Excluding Dividends

Annual Inflation Rate

10%

1932 -194%

4%

1877 - 9.5%

9% 8% 1931 -466% 1894 - 2.9%

3% 2%

1908 + 37.3%

1930 -28.9 1873 -130% 1874 + 3.2

1879 +-I30 1883 - 87 1885 +198

1886 + 8.5 1889 + 32 1891 cl82

1927 +?63

1938 +291

7% 6% -- -

- 1578 + 6.39'0 iif:.: -137 ;3? 1 c Z!j 1 --

1% 0%

1892 + 14% 1893 -198?b 1913 -14.2 ie95 + 1.0

1939 - 3.0 1896 - 2.3 1949 +i2.9 190-l +256

1905 +160

1909 +14.3 1911 + 1.0 1,V.l +18c. 1919 -103

1936 +x9 1355 +20?3

-36-

SUMMARY TABLE

The Six Environments and the Stock Market

Average Annual Compound Stock Annual Price Growth* Change (Negative)

UP Market Years

+ 0.3% - 1.4% 8

Down

Market Years

Average

Gain Average loss

- 15.9%

Years

14

20

21

Environment

Extraordinary inflation (8%-18%)

Relatively High Inflation

(4%-7%)

Moderate Inflation (2%-3%)

Stability (1% Inflation-

1% Deflation)

Moderate Deflation

(2%-4%)

Extraordinary Deflation (5%-11%)

The Entire Period

The Stock Market

+12.4%* 6

+ 7.5

+17.5

- 4.6 - 5.8 11 9 -18.1

8 - 7.2 + 8.1 + 7.1 13

30

13

10

+ 91 + 8.0 21

9

+17.1 9

+ 20.8 4

+ 8.0 6

- 9.5

+ 9.8 + 7.8 -15.0

.- 8.3 - 2.7 - 5.9 4

108 + 4.4% + 2.6% 66 + 15.0% 42 -14.1%

l Annual percentage gains and declines for all years included in each en-

vironment geometrically linked and presented in terms of annual com-

pound positive or (negative) growth rates. Excludes dividends.

-37-

THE MARKET AS INFLATION HEDGE

What then of those who say the stock market is a long-term hedge against inflation. The evidence cited by the believers usually consists of present- ing long-term stock market investment results of say, 25 years, 50 years or more, and comparing this with the long-term inflation rate.

Because the stock market gained more than was lost to inflation during this period, the conclusion is that stocks are a hedge against inflation.

This is, at best, a questionable conclusion. In all of the time periods cited, stock market growth rates most closely correlate with book value growth, earnings growth and dividends growth. The stock market gains during these periods are recognition of these fundamental growth factors. These are the prime movers, not inflation. If the long-term growth of these fundamental factors ceases or slows down, the stock market will follow suit, no matter that inflation continues to surge ahead.

“A ha , It the diehard stock market /inflation advocate might say “won’t in- flation itself cause earnings, book value and dividends to grow at a simi- lar rate?”

It’s the old chicken and egg argument. Sometimes, it will, but certainly not all the time, escpecially when inflation is running 5 percent or more per year. A look at recent experience might be of interest. From Dec- ember 31, 1968, through December 31, 1977, only book value growth managed to stay within hailing distance of the increase in consumer prices as measured by the Consumer Price Index. Earnings growth and dividend growth lagged far behind inflation.

Consider the following :

f Dec. 31, 1968 Dec. 31, 1977 Increase

Dow-Jones Industrials Earnings $ 57.89 $ 89.10 53.9% Dividends 31.34 45.10 43.9 Book Value 521 838 60.8

Consumer Price Index 106.4 186.1 74.9%

In summary, inflation has been a recurring but not constant phenomenon in the U . S . economy and, conventional wisdom notwithstanding, it has not been a good environment for stock market investing. In the last 10 years, the Consumer Price Index rose 117 percent and during the same period, the Dow-Jones Industrial Average rose only 15%. As a matter of fact, the stock market return has managed to exceed the high annual inflation rates (8 Percent Plus) in only three years since 1872. Therefore, the stock market does not appear to be a good inflation hedge. The best time to profit in the stock market is during periods of price stability of even mild deflation.

-38-

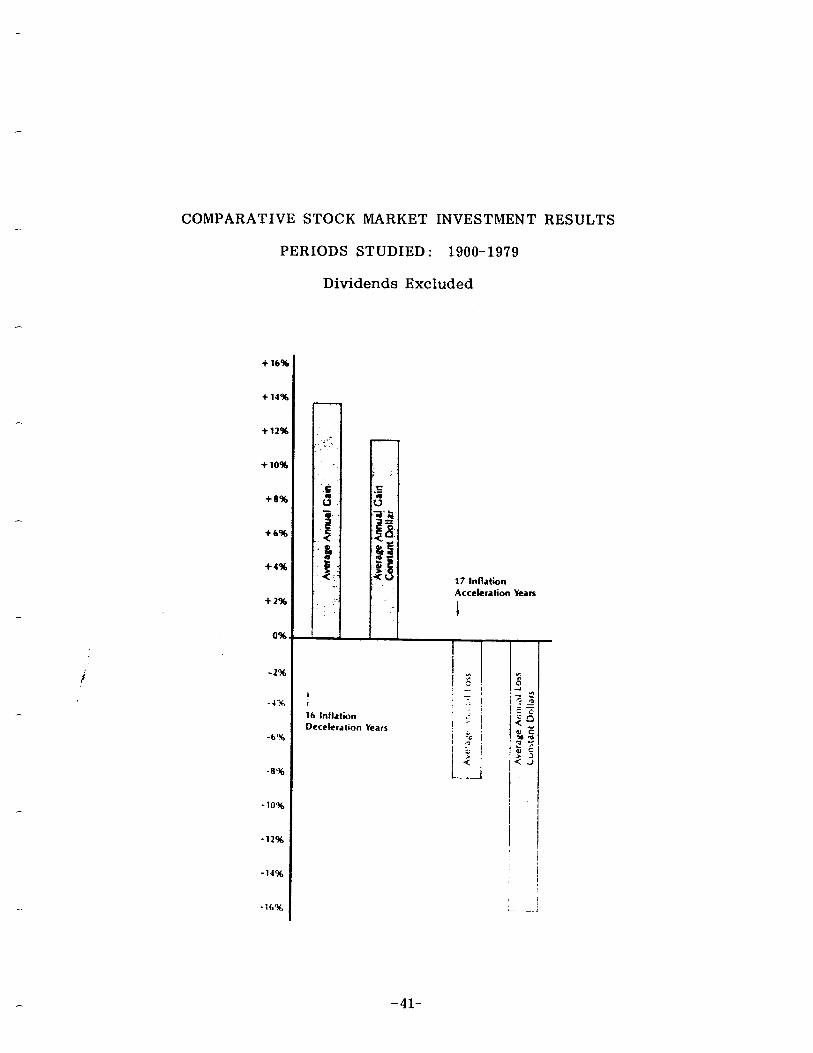

THE EFFECT OF ACCELERATING AND DECELERATING INFLATION

When economic history and stock market performance are rubbed together, the evidence is overhwelming that the stock market performs below average during periods of more than 4 percent inflation, while in periods of rela- tive price stability or perhaps even mild inflation, market performance is significantly above average . .

But what happens to the stock market when inflation is accelerating or decelerating?

To provide some insights into this question, we’ve isolated all years from 1900 to 1980 in which inflation was 4 percent and above and in which infla- tion had accelerated at least 2 percent from the prior year. We also tracked the stock market performance for these same years. The table below pre- sents the results of the 17 years when inflation was accelerating. The Cowles Commission Index and the Dow-Jones Industrial Average were once again used as the stock market proxy.

Year

1902 1906 1910 1912 1916 1917

i 1937 1941 1942 1946 1947 1951 1957 1973 1974 1978 1979

Seventeen Inflation Acceleration Years: 1900-1980

Preceding Net Change Inflation Year Stock in Constant Dollar Level Inflation Change Market (Inflation Adjusted)

40 9 2 % +2% + 1.3% - 2.7% 4 +4 + 3.2 - 0.8 4 +4 -12.3 -16.3 4 - +4 + 2.9 - 1.1 8 1 +7 + 3.4 - 4.6

17 8 +9 -30.7 -47.7 4 +4 -32.8 -36.8 5 1 +4 -15.4 -20.4

11 5 +6 + 7.6 - 3.4 9 2 +7 - 8.1 -17.1

14 9 +5 + 2.2 -11.8 8 1 +7 +14.4 + 6.4 4 2 +2 -12.8 -16.8 6 3 +3 -16.6 -22.6

11 6 +5 -27.6 -38.6 9 7 +2 - 3.2 -12.2

13 9 +4 + 4.2 - 8.8

-39-

Summary: 17 years Nominal Dollars Constant Dollars

Up Years 8 1 Down Years 9 l6 All 17 Years

Median Annual Performance -3.2% -12.2% Average Annual Performance -7.1% -15.0% Hypothetical Annual

Compound Loss ( 17 Years Linked) -8.2% -16.4%

The table shows several interesting things. First, even though the actual up years and down years are almost balanced (eight up, nine down), the losing years were really big losers, declining an average 20 percent. Also, the years of market advance were marginal at best, averaging 5 percent. The biggest nominal winner was 1951, which had 14.4 percent gain.

When viewed in terms of constant dollars, taking into consideration the dollar erosion from each year’s inflation rate, 1951 was the single winning year in the 17 years examined, and that was only a 6.4 percent gain. Over- all, relative investment performance for these inflation acceleration years is miserable when measured in nominal or constant dollars.

The largest nominal loss in inflation acceleration years was 32.8 percent in 1937 when inflation increased from zero the previous year to 4 percent. The second biggest nominal loss was 30.7 percent in 1917 when the inflation rate more than doubled from 8 percent in 1916 to 17 percent in 1917. More recent- ly, when inflation almost doubled -- from 6 percent in 1973 to 11 percent in 1974 -- the market lost 27.6 percent.

Rapidly accelerating inflation, particularly if it is from a level of 4 percent or more, is a hostile environment for the stock market investor. If the in- vestor can strongly support a conclusion that a current inflation level of 4 percent or higher will increase by 2 percent or more in the next 12 months, he should realize he probably has two strikes against him.

Essentially the same procedure has been followed in examining years from 1900 to date when inflation was decelerating. Inflation deceleration years are identified as years in which inflation declined at least 2 percent from a preceding significant inflation year (4 percent and above). Sixteen years fit this definition. Note that some high inflation years, such as 1919 (15 percent) and 1975 (9 percent), also qualify as inflation deceleration years in that inflation, though still high, was coming down.

We find that 16 years fit our selected criteria, and 14 of these recorded gains in nominal dollars ranging from 38 percent in 1975 and 37 percent in 1908 to 6 percent in 1971. Only 1913 (minus 14 percent) was a signifi- cant losing year. More importantly perhaps, in constant dollars there were only three losing years out of the 16. All in all, these look like pretty good odds.

- 40-

i

COMPARATIVE STOCK MARKET INVESTMENT RESULTS

PERIODS STUDIED : 1900-19’79

Dividends Excluded

+ 1691

+ 14%

+6%

-2%

-4%

-8%

-10%

-12%

-14%

-16%

t 16 Inflhon

Deceleration years

17 Inflation Acceleration Yearn

1

I

- -2

-41-

Inflation Deceleration Years 1900- 1980

Year Inflation

Level

1900 + 2% 1904 0 1908 - 3 1911 0 1913 - 1 1919 +15 1921 -11 1938 -2 1943 +6 1944 +2 1948 +8 1949 -1 1952 +2 1971 +4 1975 +9 1976 +6

Preceding Year Inflation

Summary : 16 Years

70 3- 4 4 4 4

18 16

4 11

6 14

8 8 6

11 9

Change

- 5% - 4 -7 - 4

I- IJ3 -27 -6 -5 -4 -6 -7 -6 -2 -2 -3

Stock Market

+14.1% +25.6 +37.3 + 1.0 -14.2 +13.1 + 7.3 +28.1 +13.8 +12.1 - 2.1 +12.9 + 8.4 + 6.1 +38.3 +17.6

Nominal Dollars

: Up Years

i Down Years All 16 Years

Median Annual Performance Average Annual Performance Hypothetical Annual

Compound Gain ( 16 Years Linked)

14 2

+13.0% +13.7%

+12.9%

Net Change in Constant Dollar (Inflation Adjusted)

+12.1% +25.6 +40.3 + 1.0 -13.2 - 1.9 +18.3 +30.1 + 7.8 +10.1 -10.1 +13.9 + 6.4 + 2.1 +29.3 +11.6

Constant Dollars

13 3

+10.9% +11.5%

+10.9%

Thus, periods of decelerating inflation appear to be very positive investment environments. And, even though the actual level of inflation may still be high by historic standards, the more important factor is the declining trend. Investor recognition of inflation deceleration from levels of 4 percent and above would appear to be a significant factor, improving the odds of investment success.

-42-

Year

-1872 1873 1874 1875 1876 1877 1878 1879

1880 1881 1882 1883 1884 1885 1886 1887 1888 1889

1890 1891 1892 1893 1894 1895 1896 1897

1898 1899

l

1900 1901 1902 1903

Inflation (+ ) % Change Deflation (- 1 stock Market

+ 1% -2 -2 -5 -5 - 4 -6 -2

+ 7 +6 +2 -2 -6 -2 -2 +2 +2 -2

+2 -2 -1

0 -8

0 0

+2

+1 +7

+ 6.9% -13.0 + 3.2 - 4.2 -18.0 - 9.5 + 6.3 + 43.0

+ 19.0 + 2.8 - 2.9 - 8.7 -18.7 +19.8 + 8.5 - 6.5 - 2.4 + 3.2

-13.6 + 18.2 + 1.4 -19.8 - 2.8 + 1.0 - 2.3 +12.9

+ 18.6 + 6.5

i 1904 1905 1906 1907 1908 1909

+2 +14.1 + 2 +15.8 +4 + 1.3 +4 -18.5

0 + 25.6 0 + 16.0

+4 + 3.2 +4 - 33.3 - 3 + 37.3

0 + 14.3

1910 +4 -12.3 1911 0 + 1.0 19l2 +4 + 2.9 WI3 -1 -14.2 19l4 +1 - 9.0 19l5 + .l +31.6 1916 +8 + 3.4 1917 +I7 - 30.7 19l8 + 18 +lLl WI9 +15 + 13.1

1920 +16 - 23.7 1921 -11 + 7.3 1922 -6 + 20.1 1923 +2 - 2.4 1924 0 +18.6 1925 +3 + 22.8

PRIMARY DATA TABLE

Year 1916 1927 1928 1929

1930 1931 1932 1933 1934 1935 1936 1937 1938 1939

1940 1941 1942 1943 1944 1945 1946 1947 1948 1949

1950 1951

Inflation (+ ) Deflation (-)

+1 -2 + 1

0

-3 -9 -10 -5 + 3 +j

0 +4 -2 -1

+ 1 + 5 +11 +6 + 2 + 2 +9 +14 +8 - 1

1952 1953 1954 1955 1956 1957 1958 1959

+ 1 +8 +2 +1 +1

0 + 2 +4 +3 + 1

+ 2 +l +1 +1 + 1 + 2 + 3 + 3 +4 + 5

96 Change Stock Market

+ 5.1 + 26.3 + 28.8 -10.3

- 28.9 - 46.6 -19.4

* +49.5 - 1.1 + 37.0 + 28.9 -32.8 . n + 28.1 - 3.0

-12.7 -15.4 + 7.6 +13.8 +12.1 + 26.7 - 8.1 + 2.2 - 2.1 +12.9

+17.6 +14.4 + 8.4 - 3.8 + 44.0 + 20.8 + 2.3 -12.8 + 34.0 +16.4

1960 1961

1962 1963 1%4 1%5 1966 1967 1968 1969

- 9.3 + 18.7 - 10.8 +17.0 +14.6 + 10.9 -19.0

+15.2,

+ 4.3 -15.2

1970 +6 + 4.8 1971 +4 + 6.1 1972 + 3 +14.6 1973 +6 -16.6 1974 +11 - 27.6 1975 +9 + 38.3 1976 +6 +17.9 1977 + 7 -17.3 1978 + 9 - 3.2 1979 b¶m

+13 + 4.2 + II. +I%?

-43-

intentionally blank

-44-

OVERBOUGHT CAN BE BULLISH

KENNETH G. TOWER Delafield , Harvey, Tabell

The IO-day advance-decline line is one of the most widely- followed of all technical indicators. It is conventionally interpreted as a simple oscillator with extremely low levels being bullish and high levels bearish.

Kenneth Tower, on the technical staff of DeZafieZd, Harvey, Tabell, has done some extensive research which suggests that “overbought” conditions on this indicator, whatever they may mean for the short term, tend, paradoxically, to be bullish for the intermediate or longer term.

Appearing in a great variety of stock market publications, the lo-day advance-decline oscillator, usually expressed as a simple lo-day total of advances minus declines, invariably receives a glance from all but the most casual investor. Most market technicians perceive its wild swings as a measure of contrary opinion. Indeed, this interpretation is encour- aged by the often-used term of “overbought-oversold indicator. ” Thus, when the oscillator reaches a particularly low level, the reader anticipates a halt in a market decline, while a high reading is supposed to suggest a downside reversal. Paradoxically, however, an extremely high reading, while it may be suggestive of short-term weakness, can have strongly bullish implications for the intermediate term.

Since 1949, a 7.5 percent filter isolates 37 market rallies. 29 of these have been accompanied by extremely high, (“overbought”) readings. These readings occurred an average of 29 days after and 8.0 percent above an important low in the S & P 500 (see Table I).

-45-

ALL MkRKET !S8F’ 500) MOVES OF GREATER THAN 7.5% SINCE JAN 1949 (KT2S55)

DATE OF LOW LOW

FOLLOWING HIGH

JUN 13 1449 13.55 19.40 JUL 17 1950 16.5s 22.81 JUN 29 1951 20.95 25.55 SEP 14 1957

195; 22.71 45.53

OCT 11 40.80 43.87. MAY 23 1955 44.10 49.74 FEL( 12 1957 42.39 49.13 OCT 22 1957 33.09 50.71 SEP 22 1959 ss.14 50.39 MAR s 1950 53.47 59.07 OCT 25 1950 52.30 72.54 JUN 26 1952 52.32 59.78 OCT 23 1952 53.49 90.27 JUN 2s 1955 31.60 94.05 OCT 7 1956 73.20 97.59 MAR 5 1963 37.72 103.37 FEB 25 1969 97.98 106.15 JUL 29 19.59 89.48 93.33 MAY 25 1970 59.29 78.52 JUL 7 1970 71.23 104.77 AUG 9 1071 93.53 101.34 NOV 23 1971 PO.?5 120.24 JUL 5 1973 101.28 109.35 AUG 22 1973 lOc).53 111.44 DEC 5 I?73 ?3.15 99.so FEB 12 1??4 90.9-l 99.74 HAY 29 1?74 85.59 93.10

’ SEP 13 1774 55.20 70.14 OCT 3 1974 52.23 75.21

c DEC 5 1974 55.01 95.51 SEF’ 15 1?7ti 32.09 107.33 NOV 10 1975 Y8.81 107.45 MAR 5 1978 E5.90 105.99 NOV 14 1978 92.49 111 ,27 NOV 7 1979 09.87 118.44 MAR 27 l?PO 98 *22 140.52 DEC 11 1930 1?.7.36 138.12

% CHG

43.17 35.75 27.19

100.93 la,73 12;79 15.90 55.75

9 .52 P.50

33.89 14.25 58.75 15.27 33.32 13.54 -3.35

9.39 13.32 47.09

3.35 33.35

8.45 10.35

3.29 9.68 P.39 7.53

20.75 47.07 31.35

3.75 23.12 20.39 13.59 43.07 a.45

SIGtdAL LAG iN X FR@H % CHG TO - DATE DAYS sap 500 BOTTOM HIGH

Jl! L 13 21 14.73 JLfL 27 8 17.50 AUG 2 23 22.32 @CT 21 25 24.19 FEE 24 03 45.32

NO CONFI%MATION SIGNAL NO CONFIRHATION SIGNAL

NOV 29 25 41.72 NO CO&FIRHATION SIGNAL

AUG 17 113 55.34 NOV 10 11 55.13 JUL 10 9 57.20 NOV . 7 10 53’,71 JUL 13 10 85.59 JAN 12 55 83.91 AF’K’ 3 24 94.95

NO CClNFIRtiATION SIGNAL OCT 21 59 97.20

NO CONFiRHATION SIGNAL

JUL 23 9 77.72 AUG 24 11 100.40 KJEC 7 9 95.87 JUL 19 9 105.55 SEF’ 5 10 105.15

NO CONFIRMATION SIGNAL FEB 27 10 96.40

NO CONFIRMATIO>! SIGNAL NO CONFIRMATION SIGNAL

OCT 14 7 72.74 JAN 5 19 71.07 JAN 5 75 92.58 NOV 24 10 102.41 H AR 2 0 10 90.82 JAN 5 35 99.13 DEC 5 20 108.00 AFR 11 10 103.79 DEC 25 10 135.57

9.08 31.25 4.92 30.34 8*37 15.83 5.52 38.53

11.08 7.83 -

7.03 4’ cr.52

5.30 7*32 9.33 9.75 4+89

14.53 8.24

2.15 29.41 -

4.51 53.75

9.00 15.30 14’.13

3.53 1.15

9.11 34.80 7.35 0.94 7.44 24.13 5.20 i 3.10 4.50 5.98

5.00

15.80 9 .32

12.78 3.54 4.5 1 7.18 8.14 5.57 7.23

THERE WERE 37 RALLIES OF :: 7.5% AND 29 OF THOSE WERE CONFIRMES THE AVERAGE % CHAN4E OF THE CI?NFIKMCD RALLIES WAS 23.9% ON AVERAGE. THE CONFI~HATION SIGNAL CAtlE 26.0 tlkYS kFTER THE LOW THE AVERAGE LiISl?iNr_‘E AECiVE THE LOU IS 7.99? . THE AVERAGE Z CHANGE OF THE RALLIES WHICH YERE NOT CONFIRHED WAS 10.5% THE AVEKAGE Nl!hP’C_R Clt- DAYS FEOH SIGNAL TO HIGP t!AS ?‘j9 DAYS THE AVEKAGE % CP:INGE FfiOtl SIGNAL TO HIGFI WAS 19.30% $10000 INVESTED ON EACH SIGNAL AND SOLD AT THE NEXT HIGH BECAME $1195470.0~

3.46

3.40 34.53 16.47

4.03 17.&O 12.25

9.57 35.39

1.13

-46-

i

Throughout this discourse, I will be referring to advances minus declines/ total issues traded. This allows for a direct comparison of 1949 to the present, a comparison which, if based solely on advances minus declines, would be distorted by the increase in issues traded over the past 30 years (For example, a recent trading day with 1,000 advancing stocks is considerably less noteworthy in a market trading 2,000 issues than a similar day in 1949 when there were only 1,500 issues traded. ) .

In order to properly utilize this indicator, it is necessary to recognize its limitations. It is primarily useful only as a buy signal. There have been 241 days since 1949 when the indicator was above -177. On 184 or 76% of those days, the market was higher 50 days later. For all dates the market was higher 50 days later only 62% of the time. Chi-squared for this relationship is 20.66, suggesting less than 1 chance in 1000 that it occurred randomly. There are no comparable figures corresponding to particularly low levels.

The analysis in Table I suggests one application of this indicator. It is assumed that a buy signal is given after both of the following conditions have been met. The market must have declined at least 7.5%, and the lo- day oscillator must surpass .177. Results are measured to the following high. Using these guidelines, an investor would have participated in 29 of the 37 rallies greater than 7.5%, since 1949. The average percentage change from buy signal to high was 19.30 percent. The average length of time from buy signal to high was 159 days, an annualized rate of 31.90 percent. Furthermore, note that the rallies which do not contain a confirm- ing signal average only 10.5 percent while those that do average 28.8 per- cent. Indeed, lack of confirmation can be suggestive in that rallies with no confirming signal tend to be concentrated in periods of declining lows (bear markets). In each case where there is a non-confirmed rally, the subsequent low is lower than the previous one (except for the 1970 double bottom at approximately 70).

Similarly, all 9 of the confirmed rallies which measured less than 10 percent, trough to peak, have led to, lower lows. The rally which began from the December 11, 1980 low of 127.36 and was followed 10 days later by a con- firmation signal has appreciated, through January 6, 1981, a scant 8.45 percent. Should this prove to be the total extent of the move, it would be among the smallest rallies on record and would suggest the possibility of an imminent decline.

Another simple test is shown in Table II. It involves purchasing the DJIA on each crossing of . 177, regardless of when it occurrs and closing out the position 25 days later. Sixty-seven percent of the sixty-three signals were profitable with an average gain per trade of 1.8 percent. This equals a compounded annual rate of 18 percent.

-47-

DATES WHEN THE 1G DAY OSCILLATOR ROSE ABOVE ,177 AND THE SUFSEGUENT 25 DAY % CHANGE PREPARED BY DELAFIELDt HfvRVEYf TAEELL (KART66)

DATE DJIA DJIAt 25 X CHG

tlAR 8 1949 JUL 13 1949 SEP 13 194Y 34N 9 1950 JUL 27 l’?;O SEP 15 1950 NOV 20 1950 DEC 28 1950 FEB 6 1951 APR 14 1951 AUG 2 1951 SEP 10 1951 DEC 6 1951 NOV -‘6 195.’ AUG ;O 195; OCT 21 1953 JAN 15 1954 SEP 15 1954 NOW 12 1954 MAR 28 1955 FEB 14 1955 JAN 7 1958 HAR 11 1958 APR 21 1958 FEB 24 1959 AUG 17 1960 NOV 10 1960 JAN 12 1961 JUL 10 1962 AUG 20 1952 NOV 7 1962 JAN 8 1963 JAN 13 1965 JUL 13 1965 JAN 12 1967 JUN 19 1967 APR 8 1968 OCT 21 1969 JUN 9 1970 JUL 20 1970 AUG 26 1970 OCT 6 1970 DEC 3G 1970 AUG 24 1971 DEC 7 1971 JUL 19 1973 SEP T’S 1973 JAN 4 1974 FE8 27 1974 OCT 14 1974 JAN 6 1975 UAR 11 1975 JAN 5 1976

JUN 21 1976 NOV 24 1976 NOV 15 1977 APR 17 1978 AUG 3 1978 JAN 5 10-79 iIfl E C 6 i979 JAN 17 1980 UAY 27 1980 DEC 26 1980

176.09 176.71 173.24 181.59 181.01 186.36 194.68 203.53 206.37 216.87 235185 230.83 231.53 231.20 235.34 247.36 254.62 252.75 156.18 255.08 261.89 273.89 275.35 275.13 256.23 270.34 182.44 293.79 275.32 257.67 273.74 281.37 286.72 291.07 350.63 357.42 377.10 397.32 412.Pl 422.78 485.66 515.10 449.87 442.35 455.92 444.35 450.72 461.06 602.91 602.9.4 616.54 592.1s 612.01 617.78 628.50 651.86 586.01 601.90 612.86 588.k2 615.75 645.20 569.88 676.62 886.85 882.93 876.97 894.26 829.95 851.56 884.54 901.29 884.42 907.82 846.88 807.29 700.16 711.66 733.91 759.58 760.47 760.68 782.45 777.38 802.54 874.79 904.13 883.83 857.40 910.81 906.68 864.46 901.04 968.54 880.23 820.40 863.42 858.03 673.50 624.92 637.20 708.39 770.89 815.71 877.83 957.19

1007.45 984.13 950.96 1004.65 841.78 813.93 773.82 855.34 886.87 907.74 830.73 822.33 835.07 863.57 863.57 868.77 791.55 872.27 966.311 932.15

* SIGNIFIES AN INTERVENING SIGNAL CkUSECl AN EXTENIlED HOLDING PERIOD

THE TOTAL c’ERCENTAGE CHANGE IS 106.859 THERE WERE J 3 s I G N A L ‘4 OF THESC 4:. i)F: 67% WFRE PROFITASI-E ON AVERACE ?? IlAYS WERE sFEf!r fN rlik tlAi?hET EACH SIGNIlL A’.JtF:fiCiEIl k 1.7% GAIN $10000 IM.C’ESTED UN C-ASIA 5IZtJf’; F’:C,‘HL: S ‘273-‘0.;<

0.35 4.82

* 2.38 * 4.55

5.09 2.21

-0.14 5.11

-0.73 -0.04

4.18 -0.04

1.54 4.02

-6.41 2.79 1.52 1.94 5.36 2.39 6.06

* -1.67 -2.54

2.29 0.00

-5.49 0.94 3.72 2.71

-4i02 4.78 1.01

-0.44 1.97 2.60 1.89 2.65

-4.67 1.64 3.50 3.03

-0.65 * 8.99

-2.2s 6.23

-4.66 * 7.49

-6.80 -0.62 -7.21 11.17

5.81 9.04

-2.31 5.65

-3.42 8 10.53

2.35 -1.01

3.41 0.60

* 10.20 -3.53

It can be seen that a high reading on the lo-day oscillator of advances minus declines has startling implications for the intermediate-term trend of the market. Dividing the difference of advances minus declines by total issues traded neutralizes the effects of the rising secular trend in total issues, resulting in a consistent range of values. An analysis of these figures provides a consistent measurement of market psychology even through such diverse periods as the “pleasantly-dull” 50’s, “go- go” ‘60’s, and “viscious” ‘70’s. There would appear to be no reason why it should not prove equally valuable in the “who knows” ‘80’s.

i

-49-

intentionally blank

-5o-

NEW DAILY TECHNICAL MARKET INDICATORS

FREDERIC H. DICKSON Goldman Sachs & Co.

and

WILLIAM P. LIVESEY CompuServe , Inc.

There are many manipulations of stock price data which are basically simple in concept but which would be impossible to undertake with- out the availability of computer data bases. A prime example of such a manipulation are breadth indices based on advances and/or declines over periods of longer than one day. Such an indicator, with a half- dozen years of its history, is explored in this article by Fred Dickson, a long-time MTA member, and William P. Livesey of Compuserve, Inc.

INTRODUCTION

The advent of computer-based stock market data services has provided the professional technical market analyst with an amazing array of quantitative

i tools which can be used to develop new indicators or test existing theories. The purpose of this paper is to present an example of an intermediate-term timing indicator which could be readily derived only with the use of such a data base.

NEW DATA SERIES

Since November, 1980, CompuServe Inc. has made available via time-sharing several series of technical market data derived from a daily screening of its stock price data base. Among these series are the following items for each of the major exchanges (NYSE, AMEX, and OTC) :