journal of islamic banking and finance july – sept 2017 1 · journal of islamic banking and...

TRANSCRIPT

Journal of Islamic Banking and Finance July – Sept 2017 1

2 Journal of Islamic Banking and Finance July – Sept 2017

Journal of Islamic Banking and Finance July – Sept 2017 3

In The Name of Allah,

The most Beneficent, The most Merciful

“O Believers: devour not Riba, doubled and redoubled;

and fear Allah, in the hope that you may get prosperity.”

Sura Ale-Imran (verse No. 130)

-------------------------------------------------------------------

The articles published in this Journal contain references from the

sacred verses of Holy Qur’an and Traditions of the prophet (p.b.u.h) printed for the understanding and the benefit of our

readers. Please maintain their due sanctity and ensure that the pages on which these are printed should be disposed of in the

proper Islamic manner

4 Journal of Islamic Banking and Finance July – Sept 2017

Journal of Islamic Banking and Finance

Volume 34 July – Sept 2017 No.3 Founding Chairman Muazzam Ali (Late) Former –Vice Chairman Dar Al-Maal Al-Islami Trust, Geneva, Switzerland

Chairman Basheer Ahmed Chowdry Shariah Advisor Uzair Ashraf Usmani

Editorial Board

Ahmed Ali Siddiqui Mufti Bilal Qazi S. A. Q. Haqqani Dr. Hasan uz Zaman Dr. Mohammad Uzair Altaf Noor Ali (ACA)

Editor Aftab Ahmad Siddiqi

Associate Editor Seemin Shafi Salman Ahmed Shaikh

Manager Publication Mohammad Farhan

Published by: International Association of Islamic Banks Karachi, Pakistan. Ph: +92 (021) 35837315 Fax: +92 (021) 35837315 Email: ia _ ib @ yahoo.com

[email protected] Website: www.islamicbanking.asia

Follow us on Facebook: http://www.facebook.com/JIBFK

http://external.worldbankimflib.org/uhtbin/cgisirsi/x/0/0/5/?searchdata1=37177{ckey}

Registration No. 0154 Printed at M/S Maaz Prints, Karachi

Academic Advisory Board

Dr. Mohammad Kabir Hassan Professor of Economics & Finance University of New Orleans, USA.

Dr. M. Ishaq Bhatti Associate Professor of Finance and Financial Economics, LA TROBE University, Australia.

Dr. Riham Rizk, Associate Professor in Accounting Durham University Business School, UK Dr. Zubair Hasan, Professor Emeritus INCEIF Global University of Islamic Finance, Malaysia.

Dr. Rodney Wilson Professor Emeritus, INCEIF, Lorong Universiti A Malaysia/France.

Dr. S. Nazim Ali, Professor and Director, Center for Islamic Economics and Finance, Hamad Bin Khalifa University, Doha, Qatar.

Dr. Mohd. Ma’sum Billah Professor IEI, King Abdul Aziz University, Kingdom of Saudi Arabia.

Dr. Mehboob ul Hassan Professor, Department of Economics, (CBA) King Saud University, Saudi Arabia. Dr, R. Ibrahim Adebayo Department of Religions, University of Ilorin, Nigeria.

Dr. Huud Shittu Department of Religion and Philosophy, Faculty of Art University of Jos – Plateau State, Nigeria.

Dr. Manzoor Ahmed Al-Azhari, Associate Professor (Islamic Law) Ph.D, Legal Policy, Fac. Shariah & Law. Alazhar University, Egypt. Post Doc. Fac. of Law, Univ.of Oxford, UK.

Dr. Waheed Akhtar Assistant Professor, Comsats Institute of Information Technology (CIIT), Lahore, Pakistan.

Dr. Muhammad Zubair Usmani Jamia Daraluloom Karachi.

Journal of Islamic Banking and Finance July – Sept 2017 5

Journal of Islamic Banking and Finance

Volume 34 July - Sept 2017 No. 3

C O N T E N T S 1. Editor’s Note ---------------------------------------------------------------------------------07 2. Analysis of Minor Proposals Outside the Mainstream ------------------------------11

Islamic Finance in Pakistan By Salman Ahmed Shaikh

3. Medical Takaful (Insurance) Reform Models and Structures ---------------------22 By Prof. Dr. Mohd Ma'Sum Billah

4. Combination Of Contracts In Sovereign Sukuk Structure -------------------------39 in Indonesia And A Proposed Sharī’a Parameters By Muhammad Iman

5. Working Model of an Islamic Bank: -----------------------------------------------------56 How different it is from conventional banking By Muhammad Ali Shaikh 6. Understanding on Islamic Banking: The Perception and -------------------------68

Thoughtfulness of Customers about Islamic Banking in the Context of Balochistan

By Jameel Ahmed, Safia Bano & Lubaina Dawood 7. Risk Management and Performance of Islamic Banks: ------------------------------81

Using the Income of Mudharaba and Musharaka as a Moderator By Vatmetou Mokhtar Maouloud, Ghazi Zouari & Anwar Hasan Abdullah Othman

8. Profitability of Islamic Banks: Case of Malaysia -----------------------------------90 By Huma Nawaz & Prof. Dr. BarjoyaiBardai

9. Book Review: The Bottom Billion --------------------------------------------------------104

10. Country Model: Luxembourg---------------- ---------------------------------------------106

12. Islamic Banking Indicators ---------------------------------------------------------------108

6 Journal of Islamic Banking and Finance July – Sept 2017

Journal of Islamic Banking and Finance July – Sept 2017 7

Editor’s Note Islamic banking and finance is well and truly making its mark in diverse regions.

At the same time, it is facing challenges in assimilating into regions where the environment is not as much conducive as it should be for a level playing field. Several countries in East Asia and Europe have accorded tax neutrality to Islamic banking and finance products. However, still a lot needs to be done in order for Islamic banking and finance products to penetrate into markets in North America, Central Asia, South America and countries in Europe other than in the Western part of Europe. To achieve tax neutrality, awareness among regulatory, monetary and fiscal authorities is necessary.

Islamic banking and finance primarily provides Shari’ah compliant financial products and services to the faith-conscious Muslims who want to avoid non-compliance with the injunctions of their faith. At the same time, Islamic banking and finance products have an equally strong congruence with products which have ethical and social undertones. For instance, Islamic banking and finance products do not charge fixed interest on the simple loan of money. They provide asset backed financing and earn rents and profits from the sale and lease of asset whose ownership is borne by the Islamic financial institution. Islamic banking and finance products also avoid transactions with socially and morally undesirable activities, such as financing weapons, night clubs, casinos and activities which exhibit vulgarity.

Islamic banking and finance products are equally competitive if a level playing field is provided to Islamic banking and finance products. They can enrich the financial market by catering to the faith conscious and socially conscious clients by providing faith compliant ethical products and services which are also priced competitively. But, for this to happen, it is necessary that the regulators provide a level playing field which can improve the financial market depth, inclusiveness, competition and efficiency.

Islamic banking and finance providers need to expand their coverage geographically. This can be expedited if new institutions are provided with incentives to enter into the market. At the same time, conventional banks existing in the markets can also extend their services in the Islamic banking and finance segment to cater to a broad range of clients with different needs. The growth in Islamic banking and finance is exemplary. However, it still forms a very small percentage of global financial assets. It is important to provide a level playing field to Islamic banking and finance products by removing extra taxes, duties and registration charges. This can enable the Islamic banks to withstand the price competition from large conventional banks and provide Shari’ah compliant and yet competitive products to the clients.

8 Journal of Islamic Banking and Finance July – Sept 2017

In financing provided by international development finance institutions and multilateral financing between governments, the Sukuk structure can be effectively utilized for development finance of real estate infrastructure, high-cost equipment and facilities. The recent success in the use of Sukuk by even the non-Muslim majority countries provides credence to the view that Islamic finance is broad in its appeal and scope to different clients as well as to their different needs. If development finance is structured using Islamic finance structures, then necessary mobilization of funds can be ensured to obtain finance for meeting sustainable development goals. This could be vital for underdeveloped Muslim majority countries. Furthermore, it will enable Islamic finance to exhibit its potential in contributing to economic development more directly and boost its economic stature and appeal beyond being a faith-compliant financial system alone.

This issue of Journal of Islamic Banking & Finance documents scholarly contributions from authors around the globe. Contributions in this current issue discuss the theoretical underpinnings of an Islamic economy, contemporary issues in Islamic finance and performance based empirical studies on Islamic banking and finance. Below, we introduce the research contributions with their key findings that are selected for inclusion in this issue.

The paper “Analysis of Minor Proposals outside the Mainstream Islamic Finance in Pakistan” by Salman Ahmed Shaikh discusses the minor proposals which are outside the mainstream Islamic finance in Pakistan. Some of the minor proposals like two-tier Mudarabah are not used widely because of lack of preparation, government incentives and initiatives at the practical level in the current scenario. In the presence of practiced Islamic banking and its growing penetration, accessibility and growth, Islamic banking should be preferred over conventional banking and finance products if one wants to be compliant with Islamic injunctions.

“Medical Takaful (Insurance) Reform Models and Structures” paper is written by Mohd Ma’Sum Billah, is an attempt in this paper to analyze possible reformed models and structures of medical insurance appropriate for the Kingdom's environment. In establishing the idea, some experiences will be analyzed as a reference from the existing practices of the Kingdom of Saudi Arabia and also the Malaysian practices of medical takaful as the pioneer of the scheme.

The paper “Combination of Contracts in Sovereign Sukuk Structure in Indonesia and a Proposed Sharī’ah Parameters” by Muhammad Iman Sastra Mihajat discusses how to deal with the use of combinations of contracts in Sukuk issuance. The paper reveals that majority of contracts in Sukuk market (corporate and sovereign) are using double and multiple of contracts in their ‘aqad’ structure. However, based on hadith of the Prophet, it is prohibited to combine more than one contract in single transaction. Therefore, the paper cites some Muslim scholars who have questioned the level of compliance with Shari’ah law in Sukuk issuance. The paper concludes that not all combinations of contracts are prohibited as long as they follow the Shari’ah parameter guidelines.

Journal of Islamic Banking and Finance July – Sept 2017 9

In his article “Working Model of an Islamic Bank: How different it is from

conventional banking” Muhammad Ali Shaikh, teaching subjects of financial management and Islamic finance at leading business schools in Karachi, has given a very comprehensive list of differences between conventional and Islamic banking. He, very rightly, argues that since the two are diametrically different, not only should the products they offer be different, but so should the presentation of their accounts. The difficulties or handicaps must be removed so that the IB products are truly Shariah compliant. Organized and coordinated research in product development and joint market penetration strategies, he says, will help increase overall market share and acceptability and will benefit the IB industry as a whole.

“Understanding Islamic Banking: The Perception and Thoughtfulness of Customers about Islamic Banking in the Context of Balochistan” contributed by Jameel Ahmed and Safia Bano both Assistant Professors, University of Balochistan, Quetta and Lubaina Dawood Lecturer, Sardar Bahadur Khan Women’s University, Quetta attempt to examine the basic knowledge about Shariah principles on which Islamic banking is based and to analyze the clarity of different modes of financing and offerings of Islamic banks among the customers. This inquiry is qualitative in nature and attempts to explore how people in Balochistan feel regarding Islamic banking. In the final analysis they find that a great deal more information and knowledge needs to be transmitted to the market and customers even though their desire to bank with Islamic banks is existant, their knowledge is imperfect.

The paper “Risk Management and Performance of Islamic Banks: Using the Income of Mudharabah & Musharakah as a Moderator” by Dr. Vatimetou Mokhtar, Ghazi Zouari and Anwar Hasan Abdullah Othman employed unbalanced panel data regression analysis on 16 Islamic banks from different countries over the period 2012 to 2015. Their results showed that the income of PLS products had a moderating effect particularly on the relationships between performance and liquidity risk, and operational risk. However, it had no moderating effect on the relationship between performance and market risk.

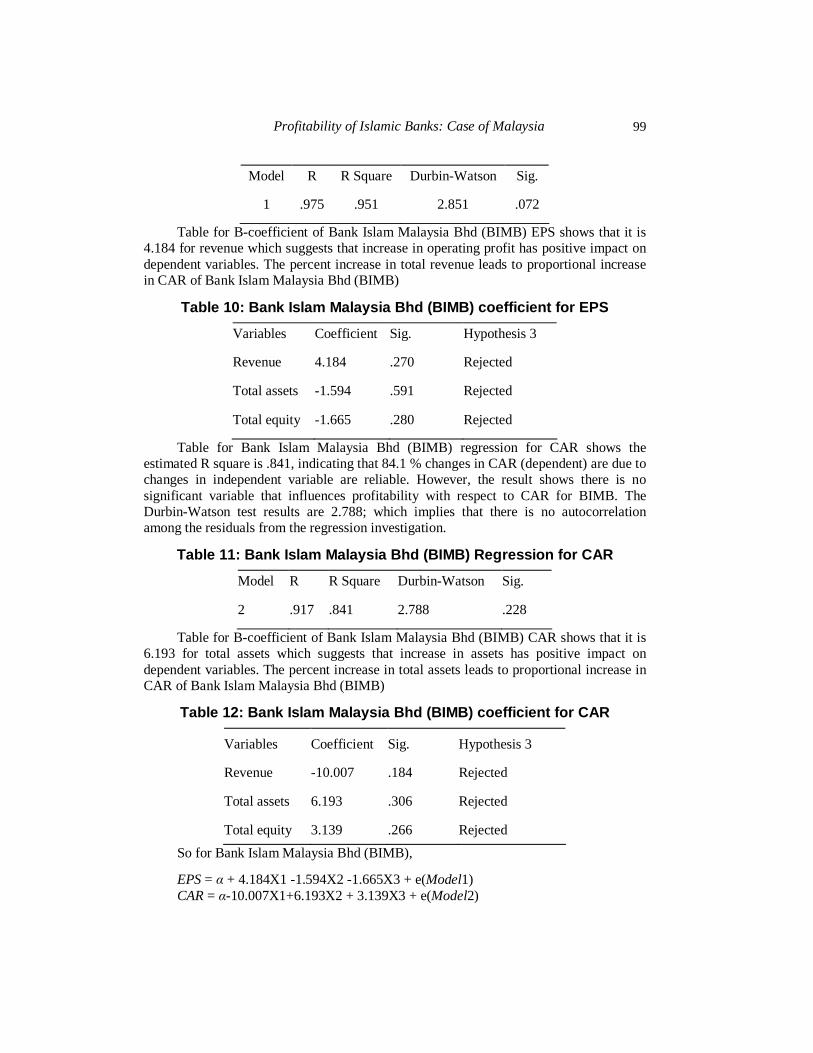

Huma Nawaz, doctoral student at Al Madinah International University, Malaysia, supervised by Professor Dr. Barjoyai Bardai of same university, has documented her research in the article “Profitability of Islamic Banks: Case of Malaysia”. Her study is focused on two Malaysian Islamic banks and how they compare on performance efficiency between them and what variables determine such profitability. The researcher has based her study on banks financial ratios over the period of 2010 to 2015 and used Linear Regression Model and Correlation analysis to arrive at her conclusion.

10 Journal of Islamic Banking and Finance July – Sept 2017

Readers Comments Dr. Adebayo, R. Ibrahim, Associate Professor, University of Ilorin, Nigeria.

E-mail: [email protected]

“The journal is gaining more popularity and it is being cited by many in the academia because of rich information contained therein. The journal has become a household material in the hand of scholars in Islamic banking and finance. I therefore commend the efforts of the association in this direction. May Allah continue to enrich you more in wisdom, wealth and health”.

Disclaimer

The authors themselves are responsible for the views and opinions expressed by them in their articles published in this Journal.

The opinions, suggestions from our worthy readers are welcome, may be

communicated on

E-mail: [email protected], Facebook: http://www.facebook.com/JIBFK,

Website: www.islamicbanking.asia

Journal of Islamic Banking and Finance July – Sept 2017 11

Analysis of Minor Proposals outside the Mainstream Islamic Finance in Pakistan

By Salman Ahmed Shaikh*

Abstract This paper is a humble attempt to discuss the minor proposals which are outside the mainstream Islamic finance in Pakistan. Some of the minor proposals like two-tier Mudarabah are not used widely because of lack of preparation, government incentives and initiatives at the practical level in the current scenario. Some other proposals like rationalizing bank interest through non-textual arguments (other than in Qur’an and Hadith) are not in compliance with Islamic source texts (Qur’an and Hadith). Furthermore, some minor proposals have misapplied the Islamic contracts, such as Qard-e-Hasan as in Time Multiple Counter Loan. There are several features in conventional banking and finance which contradict with Islamic injunctions directly without any ambiguity. Islamic banking first and foremost attempts to be interest-free as well as avoid other non-permissible elements in Islamic contract law and rules of sale. In the presence of practiced Islamic banking and its growing penetration, accessibility and growth, Islamic banking should be preferred over conventional banking and finance products if one wants to be compliant with Islamic injunctions. Islamic banking alone might not be the only solution to meet all sorts of economic and social objectives. The simultaneous growth of Islamic social finance in the form of Waqf and institutionalization of Zakat and Qard-e-Hasan based microfinancecan contribute in completing the access to Islamic finance to people of different economic standings. Now, people of all socio-economic sections can be served through either commercial Islamic banking and/or through Islamic social finance institutions. Thus, Islamic finance itself as a combination of commercial and social finance institutions is fast appearing to be a comprehensive and

* Author: Salman Ahmed Shaikh is Ph.D scholar in Economics.

E-mail: [email protected]

12 Journal of Islamic Banking and Finance July – Sept 2017

complete alternate financial system for the faith conscious clients. As a result, there is no need to rationalize conventional interest based banking in part or in total.

Keywords Riba, Islamic Banking, Insurance, Takaful

1. Introduction Ever since the establishment of Pakistan, there was a great zeal to introduce Islamic

institutions in the socio-economic milieu to realize the vision for which the independence struggle was carried out. Muhammad Ali Jinnah, the First Governor General of the country stated in his address at the inauguration of State Bank of Pakistan: “The adoption of Western economic theory and practice will not help us in achieving our goal of creating a happy and contented people. We must work our destiny in our own way and present to the world an economic system based on true Islamic concept of equality of manhood and social justice. We will thereby be fulfilling our mission as Muslims and giving to humanity the message of peace which alone can save and secure the welfare, happiness and prosperity of mankind.”

Later on, the political turmoil did not give adequate attention to this vision. However, given the increased focus in the 1970s around the Muslim world to develop an Islamic financial system for Muslims, the positive effects were also felt in Pakistan. The 1973 constitution of Pakistan in Section 38(f) stated that Riba should be eliminated as early as possible. However, lack of political will in the subsequent governments has still remained as a hurdle in the way of completely replacing the interest based banking system with an Islamic one. Nonetheless, Islamic banking has begun its journey. At the same time, outside the mainstream Islamic finance, there have been some minor proposals proposed by certain quarters. This paper gives an account of these minor proposals to explicate why these proposals are not part of the mainstream Islamic finance. This paper is divided into 3 sections. After a brief background introduction in Section 1, Section 2 provides a critical account of some minor proposals which have been put forward in Pakistan. Section 3 discusses how the mainstream Islamic finance has streamlined the development of Islamic finance products by giving primary emphasis to compliance with Islamic injunctions (Qur’an and Sunnah) and by keeping in line with market dynamics and needs of faith conscious clients and stakeholders in the current scenario.

2. Minor Financial Proposals Outside the Mainstream Islamic Finance Besides the mainstream Islamic banking that operates in Pakistan under the careful

supervision of Shari’ah Advisors, some other proposals had also been put forward by other writers. In this paper, we analyze these proposals and alternate perspectives and see as to why they did not become the mainstream view due to Shari’ah related or other practical difficulties.

2.1 Two Tier Mudarabah Framework Uzair (1978) envisaged two tiers of Mudarabah partnership, one between

depositors and bankers and the other between bankers and investors. These parties may share the profit according to a pre-arranged ratio. These ratios may be regulated by the

Journal of Islamic Banking and Finance July – Sept 2017 13

market or the central bank and may be used by the latter as an alternative instrument of credit control. This framework has remained outside of mainstream Islamic finance not because of its socio-economic merit or its lack of affinity with Islamicprinciples. Rather, this proposal had been favored by early academicians. Shaikh Mufti Taqi Usmani has repeatedly emphasized the preference of Mudarabah and Musharakah over other modes of financing from the socioeconomic, income distribution and Maqasid-e-Shari’ah perspective. Mufti Taqi Usmani (2004) in his book “Introduction to Islamic Finance” stated at least 5 times that Mudarabah and Musharakah are ideal modes of financing on page 12, 17, 72, 107 and 164 respectively.

The reason why these modesof financing had not been used often in practice owes to practical difficulties such as non-standardization of accounting, tax disadvantage to equity over debt finance, the weak motivation of commercial stakeholders and the agency problems. Some authors have emphasized agency problems in Mudarabah, such as Bacha (1997), Khalil et al. (2002), Dar and Presley (2000), Warde (1999) and Rosly and Zaini (2008). Nonetheless, the lack of this proposal’s practical use is not due to its nonconformity with Shari’ah principles.

2.2 Narrowing the Scope of Riba Prohibition in Contemporary Finance In the early period since the establishment of Pakistan, there were some

intellectuals who had given some non-traditional views on Riba. For instance, Rehman (1964) gives this definition of Riba: “An exorbitant increment whereby the capital sum is doubled several-fold, against a fixed extension of the term of payment of the debt.” Rehman (1964) and Saeed (1996) argued that only the exorbitant rates of interest charged on consumption loans from the poor borrowers by rich lenders were condemned by Islam. However, this view has been effectively and comprehensively dealt with both in academics and then subsequently in the legal sphere.

Early writers in Islamic Economics like Mawdudi (1961) defined Riba as follows: “Excess money which is obtained on determinate conditions and at a fixed rate for the principal loaned out in consideration of the period for which the money has been lent”. The Pakistan Council of Islamic Ideology (1980, p.1) clearly reflected a consensus view when it concluded in its 1980 report on the elimination of interest from the Pakistan economy: “The term riba encompasses interest in all its manifestations irrespective of whether it relates to loans for consumption purposes or for productive purposes, whether the loans are of a personal nature or of a commercial type, whether the borrower is a government, a private individual or a concern, and whether the rate of interest is low or high.” Subsequently, the Historic Judgment on Interest settled the debate both in academics as well as in legal sphere.

On the other hand, some authors attempt to contextualize the scope of Riba. One suggestion put forward is that government national saving schemes for retired employees are allowable since government gives the premium on principal on its own and can change the premium by its own desire. This understanding is based on the misconception that government borrows funds for investment purposes and gives the residual from the returns on investment projects to the borrowers. As per this understanding, issuing prize bond is also a source of finance adopted by the governments to finance investment

Analysis of Minor Proposals Outside the Mainstream …….

14 Journal of Islamic Banking and Finance July – Sept 2017

projects. Since governments pay premium or prize unilaterally, that is why it is not akin to interest prohibited in Qur’an. Though it is undesirable, the needy persons can benefit from this scheme.

In response to this view, we should note the fact that Pakistan pays around half of all the tax it collects in the form of debt servicing. If the payment of interest is regarded as completely permissible, then the government could opt for more debts. These domestic borrowings by the government are mostly used for non-development expenditures. Development expenditure is a very small portion of government’s total expenditure. The government has run a fiscal deficit in almost every year since its independence. The possibility of project based and development infrastructure finance is promised by the instrument of Sukuk structure in Islamic finance.

For the individuals who are risk averse and who want relatively regular incomes, Islamic asset management companies have designed tailor-made income funds, cash funds and capital protection funds. There are at least 19 Islamic income funds operating in Pakistan to date. There are 5 full-fledged Islamic banks and at least 17 conventional banks with Islamic banking windows. The total branch network of Islamic banking in Pakistan alone has reached 2,300 in number. In the developed world, even more structures and variety is available. It would be a worthwhile effort to make people know about these products, especially when Islamic finance is being offered in all major countries of Asia, Africa and Europe and is set to grow further.

Entering into an interest based transaction is a voluntary contract between two parties who can enter into a contract with their free will. In contemporary finance, most of the borrowers are organized businesses operating as corporations. In Pakistan, around 70 percent of the financing provided by banks is concentrated with corporate clients. These clients are corporations established with equity first and most of them have their shares publicly held. Other than 5 fully-fledged Islamic banks and 17 banks with Islamic banking operations, these corporations also have access to capital markets for obtaining equity finance through the issuance of shares.

The reason why equity based modes of financing are not widely practiced in Pakistan owes to the fact that these corporations are comfortable in obtaining bank finance and to pay a fixed interest rather than sharing their high return on equity with banks. As a whole, most of these corporations overall have a higher return on equity than the average interest rates which they pay to the banks. The insistence of bigger and profitable corporations on debt based finance and their reluctance on using equity based modes of financing is one of the great hindrances in fostering equity based financial intermediation. That is why it makes a lot of sense that they are as much part of the status quo in fighting the interest based debt finance as the conventional financial institutions themselves.

As a matter of fact, bank interest had been declared un-Islamic by the Supreme Court of Pakistan since a long time ago. Mufti Taqi Usmani has given a detailed account of the case and verdict in his book ‘Historic Judgement on Interest’. Amidst the ruling of prohibition of bank interest by the Supreme Court of Pakistan and wide access to Islamic banking, granting unqualified freedom to borrowing on interest basis voluntarily is not a justifiable stance.

Journal of Islamic Banking and Finance July – Sept 2017 15

Conventional banks provide loans as debts rather than providing finance on the

basis of equity participation. Their receivables are the debts and the interest on these debts. It does not matter whether the debts are provided for the purchase of real assets or lent in the form of money. It makes no consequential difference whatsoever to the cash flow commitments decided between bank as lender and the client as a borrower. If the nature of finance provided creates debt, then banks cannot demand a premium over and above the principal amount of debt as per Islamic injunctions. What conventional banks charge is a proportional predetermined increase over the principal amount quoted as a percent of the principal amount. We can take a very simple example to illustrate the point. If the borrower obtains a loan of Rs 100,000 for two years at a rate of 10% and earns Rs 200,000 in the first year and incurs a loss of Rs 50,000 in the second year, then the amount payable to the bank in the form of interest is Rs 10,000 in each year. The proposal to not charge interest in the period of loss does not change the contractual relationship of debt based lending. It also does not justify the pre-determined Rs 10,000 taken as interest no matter whether the profit is Rs 100, Rs 10,000 or Rs 1,000,000.

If we look at the product structures in both conventional and Islamic banking, only Islamic banks become the owner of the assets and bear the risks related to the ownership. Conventional banks do not take ownership or bear any risk related to the assets. They start charging interest as soon as the loan is sanctioned and not from the date of transfer of an asset in usable condition. They continue to charge interest even when the asset is not in usable condition. If the client wants to obtain a loan for purchasing an asset from a conventional bank, the only thing that changes is that the loan would be considered as more secure for the bank as it has a ready collateral available for effecting repayment, in case of eventual default. From all perspective of cash flow commitments, contractual rights, responsibilities, accounting, recording, regulation and documentation, the bank remains the lender only. If during the mortgage finance term, the client wants to give back the asset or property in use to the bank/financier, it is not possible because mortgage finance is simply not a rental agreement. The installments have no connection with market rents for the same or similar assets or properties. For financing different years of finance, the same amount of property will have different installment structure, i.e. higher installments for a shorter duration of the lease and lower installments for a longer duration of the lease. This is because the bank wants to recover all its costs alongwith interest from the cumulative sum of installments. Nowhere, a conventional bank even mentions that it is entering into a rental agreement in the documentation, accounting books, financial statements or even in marketing supplements or brochures.

2.3 Time Multiple Counter Loan This model was presented by Shaikh Mahmud Ahmad. Ahmad (1989) builds his

model on the premise that ‘time is an ingredient of a loan as the value of loan itself’. Specifically, what the proposal practically implies is that if a person needs a loan for any purpose from a bank for a certain period of time, he should also give a loan to that bank in an amount such that the ‘values’ of the two loans are equal. For example, if a person needs a loan of Rs. 1,000 for one year, he should give a loan of, say, Rs. 100 for ten years to the bank. At the expiry of the stated period, both parties will repay their loans in original. This is the essence of Time-Multiple Counter-Loan (TMCL) based interest-free banking.

Analysis of Minor Proposals Outside the Mainstream …….

16 Journal of Islamic Banking and Finance July – Sept 2017

This model has some issues from the perspective of Shari’ah as well as from the perspective of its practical implications. With respect to Shari’ah, two contracts cannot be executed contingent to each other. Also, from the Shari’ah perspective, time is not a commodity. A commodity can have different prices in different states of the time. However, time itself cannot be factored in price in monetary loans.

From the practical standpoint, savers and borrowers have different financial situations and needs. Savers have surplus money when they lend or invest the surplus money. They do not require a monetary loan in reciprocation. Thus, by lending Rs 1,000 for one year and getting a loan of Rs 100 for 10 years, the values are not even balanced even in a purely zero-interest economy.

In a positive inflation rate economy, the value of the medium of exchange will decrease overtime. To counter that, some authors suggested inflation-adjusted loans. Nonetheless, OIC Fiqh Academy has ruled out this proposal. If this proposal of indexing loans with inflation benchmark is suggested at the macroeconomic level in financial intermediation, then this is not practical. The bank is an intermediary between those who have surplus funds and those who need funds and itearns profits through the difference in interest rates on deposit and financing side. Indexing loans with inflation will not yield any return for the intermediary (the bank) in the two-tier loan based banking. Secondly, inflation is measured by an index which has an urban bias as Consumer Price Index (CPI) inflation is calculated by looking only at the prices in the urban areas. It has a period bias since in indexing; the choice of base year makes the calculations very different. It also has a representation bias as inflation in urban areas is not a true representative of inflation in all areas, especially if rural areas comprise two-thirds of the population in some developing countries. Plus, inflation is just a measure and there are at least four varieties of inflation measures used by Pakistan Bureau of Statistics (Consumer Price Index, Wholesale Price Index, Sensitive Price Index and Producer Price Index). The results depend on the methodology; the particular commodities in the index which change from time to time and not everyone have the same basket of goods relevant to them. Thirdly, cost-push inflation is driven by supply shocks resulting in higher oil, gas and electricity prices. Therefore, in this case, deterioration in real purchasing power is caused by factors, not in the control of the borrower. He cannot be held liable to compensate in a matter in which he was not responsible.

3. Why Current Islamic Finance is Mainstream in Pakistan Upon reflection, it seems that time value of money is the basis of interest. As per

Islamic principles, it seems that time value of money is the problem for the investor to avoid keeping his/her money idle and to avoid forgoing the use of money that may bring positive value to his/her investment. However, it does not mean that the investor can demand an arbitrary increase as the cost of using money without taking the risk of a productive enterprise. As per Islamic principles, a financial investor has to undertake the risk of the productive enterprise by becoming self-entrepreneur or an investing entrepreneur as an equity partner in others’ business to have any justifiable compensation out of the production process. In short term finance, there are some Islamic debt based modes of finance which ensure distinct asset ownership of the financier in order to enable

Journal of Islamic Banking and Finance July – Sept 2017 17

the charging of rents or profits on an asset sale. In a conventional debt based financing, this feature is absent and the interest is charged no matter whether the asset exists and no matter whether it is available in usable condition or not.

In Pakistan, the first full-fledged Islamic bank was established in 2002 with the name of Meezan Bank. Currently, Islamic banking in Pakistan is an established industry with 11.7% and 13.2% market share in total banking assets and deposits respectively as at March 31, 2017. The industry experts are further aiming at a 20 percent market share for Islamic banking in the overall banking industry by 2020. There are 5 full-fledged Islamic banks operating in the country along with 17 conventional banks with Islamic banking branches. The market share of Islamic banking assets has grown from a meager 0.5% in 2002 to 11.7% in 2017. By year-end 2016, the total Islamic banking assets in Pakistan stood at Rs 1.88 trillion ($17.95 billion) while the total Islamic banking deposits stood at Rs 1.57 trillion ($15 billion). With increased participation of conventional banks in Islamic banking industry, the branch network has surpassed the mark of 2,300 branches by year-end 2016. With the launch of innovative products like Running Musharakah, now the Islamic banking is catering to the working capital needs of the corporate sector. This has also helped the industry to make effective use of equity based modes of financing and reduce the share of debt based modes of financing.

One can argue that the economic substance of Islamic banks is also no different in terms of economic outcome as argued by Siddiqi (2014), Shaikh (2013), Kayed (2012), Choudhury (2012), Siddiqi (2007), Haniffa & Hudaib (2010), El-Gamal (2005& 2007) and Hassan and Bashir (2003) to name a few scholars in Islamic economics literature. Nevertheless, except for El-Gamal, the other scholars in the idealist camp are critical of Islamic banking not for its legitimacy of product offerings, but with regards to their limited product offerings to achieve the redistribution objectives. This criticism is widely known and appears even from within. The respected scholar Mufti Muhammad Taqi Usmani (2009) in his essay ‘New Steps in Islamic Finance’ writes:

“…One must not forget that these instruments are not modes of financing in their origin. They are in fact some forms of trade that have been modified to serve the purpose of financing at the initial stage as secondary and transitory measures. Since they are modified versions of certain forms of trade, they are subject to strict conditions and cannot be used as alternatives for interest based transactions in all respects. And since they are secondary and transitory measures, they cannot be taken as the final goal of Islamic Finance on which Islamic Financial Institutions should sit content for all times to come. It is a matter of concern for a student of Islamic finance, like me, that both these points are increasingly neglected by the players in the field, and especially by the newcomers in the industry.”

Furthermore, in his book, ‘Introduction to Islamic Finance’, the respected scholar, Mufti Muhammad Tami USANi (2004) writes:

“It should never be overlooked that, originally, Murabaha is not a mode of financing. It is only a device to escape from “interest” and not an

Analysis of Minor Proposals Outside the Mainstream …….

18 Journal of Islamic Banking and Finance July – Sept 2017

ideal instrument for carrying out the real economic objectives of Islam. Therefore, this instrument should be used as a transitory step taken in the process of the Islamization of the economy, and its use should be restricted only to those cases where Mudarabah or Musharakah is not practicable.” (p. 72)

The realist camp scholars argue that these redistribution objectives will be taken care of by Islamic social finance institutions which include Zakat, Wirssat, Islamic microfinance and Waqf while Islamic banks will continue to serve the short term recurrent finance needs of businesses and middle to urban class households and for which mostly the debt based Islamic modes of financing are the suitable options. In Malaysia and Indonesia, Islamic microfinance, Zakat and Waqf institutions have been used as social finance vehicles in the overall Islamic finance architecture very successfully. In Pakistan also, the institutions like Akhuwat have shown how Qard-e-Hasan can be used to help the downtrodden on a large scale. Mufti Muhammad Taqi Usmani (2004) has been a strong proponent for introducing equity based financing and regards them as more preferable in order to achieve Islamic egalitarian and redistributive objectives even through the Islamic banking institutions. But, the idealism from a financial and development perspective does not determine legitimacy and illegitimacy of the other alternatives which may lack in contributing significantly to the redistributive ideals, but which nevertheless provide a practical solution to avoid Riba and its ramifications. In his book, ‘Ghair Soodi Bainkari [Interest Free Banking], the respected scholar, Mufti Muhammad Taqi Usmani (2007) has clarified that the criticism on underachievement of the ideal redistributive objective in current practice is different from the status of legitimacy of Islamic banking which by and large has to use Islamic debt based modes of financing. But, it does not help in improving the chance to use equity financing any better if an unqualified legitimacy is accorded to interest based borrowing by the borrowers, especially when the large majority of them are the corporate clients and well-to-do professionals. Banks do not finance anyone except in the top income quintile of income distribution by having collateral and income based lending criteria.

At the very least, Islamic banks take ownership of the asset for which they provide finance, bear the risks alongwith mitigating these risks as a custodian of depositors’ funds, charge rent after the asset is transferred in usable condition and charge these rents only until the asset remains in their ownership and is being possessed by the client in usable condition. They do not charge late payment penalties as income. In practice, it is found that late payment surcharge is seldom charged and it is used in the contract to avoid the very real moral hazard problem and the eventuality of customers willfully defaulting on loans. As a result, the non-performing loan to financing ratio in Islamic banking has remained much lower than conventional banks in Pakistan (3.9% in Islamic versus 9.9% for the industry). Hanif (2014) argues that IFIs cannot claim interest on their balances with other banks and mandatory cash reserve maintained with a central bank. Islamic banks cannot invest in interest based government securities, interest based bonds. They cannot claim time value of money from defaulters and they have to bear risks in the sale.

Journal of Islamic Banking and Finance July – Sept 2017 19

Scholars like Khan (2014) think that critics of practiced Islamic banking do not

appreciate how important debt financing is for value creation in an economy and especially for inclusive growth and economic development through making financial services accessible for asset acquisition. Chapra (2007) argues that even if debt financing is predominantly used in Islamic banking practice, asset backed financing does not allow the debt to exceed the growth of the real economy. He argues that the introduction of such a discipline would ensure greater stability as well as efficiency and equity in the financial system.

Globally, Pakistan is widely acknowledged for its more conservative and cautious approach to Islamic banking and finance whereby, Islamic banking in Pakistan does not use Bai Inah, Organized Tawarruq and secondary market trading of Murabaha based Sukuk. Thus, it is not appropriate to disregard these differences and latest developments as substantial knowingly or due to lack of information.

Conclusion This paper is a humble attempt to discuss the minor proposals which are outside the

mainstream Islamic finance in Pakistan. Some of the minor proposals like two-tier Mudarabah are not used widely because of lack of preparation and government incentives at the practical level. Some other proposals like rationalizing bank interest through non-textual arguments (other than in Qur’an and Hadith) are not in compliance with Islamic source texts (Qur’an and Hadith). Furthermore, some minor proposals have misapplied the Islamic contracts, such as Qard-e-Hasan as in Time Multiple Counter Loan.

There are several features in conventional banking and finance which contradict with Islamic injunctions directly without any ambiguity. Islamic banking first and foremost attempts to be interest-free as well as avoid other non-permissible elements in Islamic contract law and rules of sale. In the presence of practiced Islamic banking and its growing penetration, accessibility and growth, Islamic banking should be preferred over conventional banking and finance products. The meticulous efforts of Islamic scholars, regulators, academia and industry players have contributed in instigating interest-free finance.

Islamic banking alone might not be the only solution to meet all sorts of economic and social objectives. This has increasingly been realized in the academia and the simultaneous growth of Islamic social finance in the form of Waqf and institutionalization of Zakat and Qard-e-Hasan based micro-finance has contributed in completing the access to Islamic finance to people of different economic standings. Now, people of all socio-economic sections can be served through either commercial Islamic banking and/or through Islamic social finance institutions. Thus, Islamic finance itself as a combination of commercial and social finance institutions is fast appearing to be a comprehensive and complete alternate financial system for faith conscious clients. As a result, there is no need to rationalize conventional interest based banking in part or in total.

Analysis of Minor Proposals Outside the Mainstream …….

20 Journal of Islamic Banking and Finance July – Sept 2017

References Ahmad, S. M. (1989). “Towards Interest-Free Banking”. Institute of Islamic Culture:

Lahore.

Bacha, I.O. (1997). “Adopting Mudarabah Financing to Contemporary Realities: A Proposed Financing Structure”, The Journal Of Accounting, Commerce & Finance, 1(1): 26 – 54.

Chapra, M. U. (2007). “The Case Against Interest: Is It Compelling?”, Thunderbird International Business Review, 49(2), pp. 161 – 186.

Choudhury, M. A. (2012). “The ‘Impossibility’ Theorems of Islamic Economics”, International Journal of Islamic and Middle Eastern Finance and Management, 5(3): 179 – 202.

Council of Islamic Ideology (1980). “Report of the Council of Islamic Ideology on the Elimination of Interest from the Economy”, CII, Pakistan.

Dar, H. A. & Presley, J. R. (2000). “Lack of Profit Loss Sharing in Islamic Banking:Management and Control Imbalances”, International Journal of Islamic Financial Services, 2(2): 1 – 9.

El-Gamal, M. A. (2005). “Limits and Dangers of Shari’ah Arbitrage”, in S. Nazim Ali, Islamic Finance: Current Legal and Regulatory Issues, Cambridge, Massachusetts: Islamic Finance Project, Islamic Legal Studies, Harvard Law School, pp. 117 – 131.

El‐Gamal, M. A. (2007). “Mutuality as an Antidote to Rent‐seeking Shari’ah Arbitrage in Islamic Finance”, Thunderbird International Business Review, 49(2): 187 – 202.

Hanif, M. (2014). “Differences and Similarities in Islamic and Conventional Banking”, International Journal of Business and Social Science, 2(2): 166 – 175.

Haniffa, R.& Hudaib, M. (2010). “Islamic Finance: From Sacred Intentions to Secular Goals?”, Journal of Islamic Accounting and Business Research, 1(2): 85 – 91.

Hassan, M. K.& Bashir, A.H. (2003). “Determinants of Islamic Banking Profitability”, ERF Paper, 10: 3 – 31.

Kayed, R. N. (2012). “The Entrepreneurial Role of Profit & Loss Sharing Modes of Finance: Theory & Practice”, International Journal of Islamic and Middle Eastern Finance and Management, 5(3): 203 – 228.

Khalil, A. F. A.; Rickwood, C. & Murinde, V. (2002). “Evidence on Agency-Contractual Problems in Mudarabah Financing Operations by Islamic Banks”. Islamic Banking and Finance: New Perspectives on Profit Sharing and Risk, 57.

Khan, T. (2014). “Comment on: Islamic Economics: Where From, Where To?”,Journal of King Abdul Aziz University: Islamic Economics, 27(2): 95 – 103.

Journal of Islamic Banking and Finance July – Sept 2017 21

Maududi, S. A (1961). “Sood” (Interest). Islamic Publications, Lahore.

Rahman, F. (1964). “Riba and Interest”. Islamic Studies, 3(1): 1 – 43.

Rosly, S. A. & Zaini, M. A. M. (2008). “Risk-return Analysis of Islamic Banks’ Investment Deposits and Shareholders’ Fund”, Managerial Finance, 34(10): 695 – 707.

Saeed, A. (1996). “Islamic Banking and Interest: A Study of the Prohibition of Riba and its Contemporary Interpretation”, Brill: Leiden.

Shaikh, S. A. (2013). “Islamic Banking in Pakistan: A Critical Analysis”,Journal of Islamic Economics, Banking and Finance, 9(2): 45 – 62.

Siddiqi, M. N. (2014). “Islamic Economics: Where From, Where To?”,Journal of King Abdul Aziz University: Islamic Economics, 27(2): 59 – 68.

Siddiqui, S. A. (2007). “Establishing the Need and Suggesting a Strategy to Develop Profit and Loss Sharing Islamic Banking”. In IIU Malaysia Conference on Islamic Banking and Finance at Kuala Lumpur.

Usmani, M. T. (2004). “Historic Judgement on Interest”, Karachi: Idaratul-Ma'arif.

Usmani, M. T. (2004). “An Introduction to Islamic Finance”, Karachi: Maktaba Ma’ariful Quran.

Usmani, Muhammad Taqi. (2007). “Ghair Soodi Bainkari” [Interest Free Banking], Karachi:Maktaba Ma’ariful Quran.

Uzair, M. (1978). “Interest Free Banking”, Royal Book Company: Karachi.

Warde, I. (1999). “Islamic Finance in Global Economy”, Edinburgh: Edinburgh University Press.

Analysis of Minor Proposals Outside the Mainstream …….

22 Journal of Islamic Banking and Finance July – Sept 2017

Medical Takaful (Insurance) Reform Models and Structures

By

Mohd Ma’Sum Billah, PhD*

Abstract Living with healthy life is among the prime natural concern of everyone regardless of one's status or background. A proper health–care requires money and today, it is one of the most expensive components of expenditure, which is not affordable to everyone thus, medical takaful1 (insurance) may be a solution. In view of creating a healthy society, several developing countries make the medical insurance compulsory. In the Kingdom of Saudi Arabia on the other hand, the health insurance has not been made mandatory yet on everyone living in the Kingdom, the native or the expatriate. The law of the Kingdom in general, is a Shari’ah (Islamic law) while its recognized insurance model is based on the cooperative (ta’awuni) principles2. In creating a healthier society by encouraging everyone to care about health, the medical takaful may be an effective step to be taken in to consideration thus, its reform is an emergence factor by allowing choices in package within the supreme law of the Kingdom. An attempt is thus made in this paper to analyze possible reformed models and structures of medical insurance appropriate for the Kingdom's environment. In establishing the idea, some experiences will be analyzed as a reference from the existing practices of the Kingdom of Saudi Arabia and also the Malaysian practices of medical takaful as the pioneer of the scheme.

Keywords: shari'ah, medical, healthcare, insurance

JEL Classification Code: G22, I13, Z4

* Professor of finance & insurance, Islamic Economics Institute, King Abdul Aziz

University, Kingdom of Saudi Arabia, blog: www.drmasumbillah.blogspot.com 1 Takaful is a Shari'ah alternative to Insurance. Some countries it (Takaful) terms as Islamic

Insurance. 2 Al-Qur’an (5:2).

Journal of Islamic Banking and Finance July – Sept 2017 23

Facts and Phenomena Health-care is among the prime concern of life. Everyone is equal as to one's

physical pain and suffering in no issue of one's socio-economic, legal or religious status or origin. A proper health–care requires money as at today. The rich may afford to care about health subject to own available resources, but not the poor, except as depending on own limited resources or common facility or cooperation from others in some exceptional cases. Medical insurance scheme may be a prompt solution to health-care for everyone. Medical insurance is made compulsory in many developing countries to ensure a healthy life for each citizen besides one’s education and economic wellbeing.

In the Kingdom of Saudi Arabia, the health insurance has not been taken as a mandatory level yet. Several insurance companies offer the health insurance product and services in the kingdom, but out of total 32,515,171 population in Saudi Arabia3 only 3.11 million4 (15 %) of the total 20,915,171 native Saudis5, while 7.85 million (67%) of the total 11,600,0006 expatriates have coverage7.

Based on the above data it is understood that, there are about 85% of the native Saudis uncovered by medical insurance, which might be due the following reasons:

Medical coverage for every employee along with one's dependents are undertaken by the respective employer of the Kingdom as a part of employment benefit.

The employee serves the elite corporate group of the Kingdom are along with one's dependents are covered with lavish medical benefits undertaken by the respective employer as the employment package.

The Kingdom provides free medical facilities for the rural people through the establishment of the polyclinic scheme.

Many elite groups of Saudi exercise their option to be treated in overseas hospitals using one's own financing capacity or any arrangement at choice.

Saudi students study in abroad are covered by the respective education package with standard medical facilities in the hospitals abroad.

In the Kingdom, there are many individuals or families influenced by the Fatwa and Shari'ah views against insurance thus, contributes to the declination of participation in the Medical insurance scheme.

3 Worldmeters, 2017, UN estimates as at February 11, 2017 4 As per report of the Council of Cooperative Health Insurance (CCHI), ARAB NEWS

(Saturday 19 December 2015) 5 Worldmeters, op.cit. 6 Saudi Gazette, November 28, 2016 7 the Council of the Cooperative Health Insurance (CCHI), op. cit.

Medical Takaful (Insurance) Reform Models and Structures

24 Journal of Islamic Banking and Finance July – Sept 2017

Moreover, there are about 33% of expatriates living in the Kingdom are still uncovered by the medical insurance perhaps due to the following reasons:

Medical coverage is a part of employment package undertaken by the respective employer.

Diplomats along with their dependents are covered with required medical facilities by the respective employer government as a part of the employment package.

Foreign business owners or investors living in the Kingdom by holding the business visa, do exercise their choices in their health-care plan at own cost, either to be treated locally or aboard with insurance package or otherwise arrangement are totally on the individual's selection.

Expatriate children study in the kingdom are either covered by the respective guardian's health-care arrangement or by the students' health-care scheme provided by the institution concern.

Residents living in the kingdom with the refugee status are covered by the special public health-care scheme of the Kingdom or with any arrangement by NGOs or private initiative.

There are number of Illegal Immigrants (with no Iqamah) living in the Kingdom whose health-care is arranged on their own respective initiative.

The non-coverage of health-care by the medical insurance scheme may result in numerous risks as follows:

Individual and Family Risks: Physical risk due to unattended health-care.

Financial burden in bearing the medical cost on own.

Emotional damage resulting from unhealthy life.

Socio-Cultural Risks: Unhealthiness due to unattended diseases.

Unhealthy life is a social liability.

Poor physical condition may result in less creativity.

National Risks: In the absence of the medical insurance scheme may result in excessive final

burden for the public health undertaken by the government.

Less appreciation of the medical insurance scheme may place the government with humanitarian liability for unable to attend everyone living in the kingdom with reasonable public health-care.

Journal of Islamic Banking and Finance July – Sept 2017 25

Poor health-care may result in less productivity and thus effect the socio-

economic growth.

Therefore, to encourage a significant participation in the health-care scheme, the importance, policies, perception, products and services of health insurance may be required to be designed with more attractive existence by an appropriate reform in models with structures. Such reform may encourage everyone to participate in creating a healthier society by undertaking and appreciating medical insurance policy as part of day to day life. It is importantly noted here that, in the Kingdom of Saudi Arabia, the law of its land is a Shari’ah (Islamic law) while its present recognized insurance model is based on the Shari’ah justified cooperative principles (ta’awuny)8. By complying the spirit of law and culture of the Kingdom several alternative models with structures within the Maqasi al-Shari’ah are suggested in this paper aiming at encouraging everyone to participate in and benefit from the reformed medical insurance policy by exercising an option as to packages. In view of justifying the objective of the research, as a pioneer with Shari’ah compliant of medical insurance scheme the Malaysian experience will be analyzed besides the current practices of the Kingdom of Saudi Arabia.

Shari’ah Compliant Medical insurance Scheme: An Experience Based on a conceptual survey it has been discovered that, in the contemporary

socio-economic environment, a Shari’ah compliant medical insurance was introduced by Takaful Malaysia sometimes in 90s as among the pioneers.9 The scheme provides coverage for thirty-six types of critical illness. Through this plan, the policyholder will obtain the sufficient amount of money to cover the required cost for the medical treatment. This plan also provide the opportunity to the policyholder to choose any kind of treatment that one may intend to get10.

As per practices in Malaysia, A health insurance plan is open for participation by any individual between the ages of 18 to 55 years old and free from those 36 critical illnesses. Thus, the duration of participation depends on the package chosen. They are three packages, 10 years, 15 years and 20 years.

There are numerous products of Islamic insurance including health-care scheme offered in the market. Some of them are not available in the conventional insurance providers. Generally, Islamic insurance is categorized into two, namely: life insurance and General insurance. However, this paper attempts to provide possible practical model of Islamic health-care insurance product justified under the Shari'ah principles of cooperation. Islamic life insurance11 plan generally is a long-term based on al-Mudharabah (profit and loss sharing) contract. Basically, Islamic life insurance plan is designed to serve and provide coverage for both individual and corporate sector. It also provides mutual aid or financial assistance among its participants from the Islamic life 8 Al-Qur’an (5:2). 9 Takaful my Health Protector Simply A Better Choice for Your Health, Takaful Malaysia, at P.1 10 http://www.insuranceinfo.com.my/choose_your_takaful/things_to_note/medical_health_tak

aful.php?intPrefLangID=1&#content1 11 As practiced in some ASEAN countries (Malaysia, Brunei and Indonesia) in particular.

Medical Takaful (Insurance) Reform Models and Structures

26 Journal of Islamic Banking and Finance July – Sept 2017

insurance Fund should any of its members be inflicted by a tragedy. Among the products under Islamic life insurance plan include:

Islamic life insurance Plan

Islamic life insurance Plan for Education

Employees insurance Plan

Ma'asyi insurance Plan

Health insurance Plan (Health-care insurance).12

Thus, the Health-Care insurance plan enables the individual to take preventive action from the critical illness. Under Islamic life insurance plan, the contribution paid by the participant is credited into two separate accounts namely; the Participant's Accounts (PA) and the Participant's Special Accounts (PSA). The purposes of these two types of accounts are, a proportion of the contribution will be credited into the PA only for savings and investment. While the balance of installment is credited into the PSA account and is considered as tabarru (donation) for the risk management, which is not necessarily to be fixed, but flexible with mutual arrangement.13 A health-care insurance plan is a sub-product of life insurance, which may provide two packages with option. Package one where the account is treated on a dual benefits with two accounts namely risk coverage account while the other is a saving account with investment return based on the principle of al-Mudarabah. The other option is on single tier basis to provide only the health-care coverage by having no investment return available14.

Scope of Coverage As per the practices of Bupa Arabia in the Kingdom of Saudi Arabia (KSA), a

health-care insurance plan in the covers among those of followings:

Variable overall cover with limitation

Fully paid In-patient and out-patient, including cover for General Practitioner and Specialist consultation.

Extensive network of hospitals and clinics coverage

Single room to Standard suite accommodation for in-patients

Maternity cover with benefits including neonatal care, maternity complications and treatment of premature babies

12 Brochure, Health-Care Takaful Plan, Takaful Malaysia 13 Yusof, M. F.,(1999), The Concept and Working System of insurance, Institute of Islamic

Banking & Insurance, London, 19. 14 As practiced by most of the Islamic Insurance providers in Malaysia.

Journal of Islamic Banking and Finance July – Sept 2017 27

Dental cover

Optical cover

Cover for cancer

Cover for diabetes

Cover for heart ailments

Life-threatening emergency treatment out of network in KSA

Emergency evacuation through International SOS Assistance when outside of KSA

Emergency treatment outside of KSA

Elective treatment outside of network inside or outside of KSA.15

Whereas in Malaysia, the health-care takaful covers among the followings:

Critical illness diagnosis

Death

Accidents

Funeral expenses

Hospitalization (Day allowances)

Cash withdrawal

Permanent Disablement.

Benefits in the Existing Health insurance Plan In the Kingdom of Saudi Arabia, the benefit under a health-care insurance plan is

ruled out under article 18 of the Kingdom of Saudi Arabia Cooperative Health Insurance Council Secretariat General as follows:

1. Diagnosis and treatment by service providers, provided that the beneficiary pays the agreed upon deductible, if any.

2. The cost of necessary and emergency medical treatment paid directly by the beneficiary, provided that the insurance company fails to urgently provide such service to the beneficiary or unjustifiably refuses to provide the service. The person bearing the expenses shall be indemnified in accordance with the limits provided

15 International health plan, Bupa Arabia (KSA).

Medical Takaful (Insurance) Reform Models and Structures

28 Journal of Islamic Banking and Finance July – Sept 2017

for in the policy and the limits paid by the company to a service provider of a similar level16.

Policyholder in Malaysian practices, may have an option to choose either of the following two packages of benefits:17

Package A (coverage with saving)

Package B (coverage without saving)

Package A This package provides saving besides protecting participants from thirty-six critical

illness. Furthermore, the participant also is entitled to obtain profit sharing from the al-Mudharabah principles. However, it also depends to their age, gender, duration and level of healthiness.

For instance, let takes 20 years old participant and 40 years old participant.

20 Years old participant The risk is low

Therefore, the proportion to PSA is low and proportion for PA is high

Let say 80% in PA and 20% in PSA

40 Years old participant The risk is high

Therefore, the proportion for PSA is high and proportion for PA is high

Let say 60% in PSA and 40%in PA.

Package B This package offers protection only against thirty-six types of critical illness with a

low rate of contribution apart from profit sharing based on al–Mudharabah principle. Normally, this package is depending on the participant’s age and based on the duration of coverage. Most of participant who choose this package will contribute more proportion to the ASP account. For instance 80% of the contribution will go into ASP and the balance 20% will go into AP18.

16 Article 18, Kingdom of Saudi Arabia Cooperative Health Insurance Council Secretariat

General, Implementing Regulation of the Cooperative Health Insurance Law Approved in Session (93) Dated 11/3/1435H Approved by Ministerial Order (9/35/1/DH) Dated 13/4/1435H

17 See Takaful myHealth Protector, Takaful Malaysia. 18 This Plan does not cover pre-existing illness and pre existing symptom and all illness which

commence with a period of 30 days from certificate effective date.

Journal of Islamic Banking and Finance July – Sept 2017 29

Types of critical illness covered by Health-Care takaful: A Malaysian experience19

1. Heart attack 19.Motor Neuron Disease

2. Stroke 20.AIDS Due to Blood Transfusion

3.Coronary Artery Disease Requiring Surgery

21.Parkinson’s Disease

4.Cancer 22.Chronic Liver Disease

5. Kidney failure 23.Chronic Lung Disease

6.Fulminant Hepatitis 24. Head Injury Due to Accident Cause of Major Head Trauma.

7.Major Organ Transplantation 25.Aplastic Anemia

8.Paralysis 26.Muscular Dystrophy

9. Multiple Sclerosis 27.Benign Brain Tumor

10. Pulmonary Arterial Hypertension 28.Encephalitis

11.Blindness 29.Poliomyelitis

12. Heart Valve Surgery 30.Brain Surgery

13.Deafness 31.Bacterial Meningitis

14. Surgery to the Aorta 32.Others Serious Coronary Artery Disease

15.Loss of Speech 33.Apalic Syndrome

16. Major burns 34.AIDS Due from occupation

17.Alzheimer’s Disease 35.Full Blown AIDS

18.Coma 36.Terminal illness

Examples of Shari’ah Compliant Medical Scheme As practices among the takaful operators, the premium paid by the participants is

credited into two separate accounts namely; Participant's Accounts (PA) and the Participant's Special Accounts (PSA). An agreed portion of the contribution is credited into the PA for saving and duly investment while the balance is credited into the PSA account and be considered as tabarru’ (donation) for the risk coverage. The ratio of the account treatment is subjective depending on the actuarial policy and the choice of the participant as to the nature of coverage. Thus, some hypothetical experiences (examples) are shared as follows:

19 See Takaful myHealth Protector, Takaful Malaysia.

Medical Takaful (Insurance) Reform Models and Structures

30 Journal of Islamic Banking and Finance July – Sept 2017

Example 1:

The distribution of contribution between Participant’s Account (PA) and Participant's Special Accounts (PSA) is made by applying several criteria as follows.20 Age - Age is regarded as an important criterion. This is because the older a

person is the higher is the risk of being diagnosed with an illness. The higher risk result in more proportion of the installment placed under PSA compared to a younger person with lesser risk.

Gender- According to studies done previously, life expectation of female is longer than male. This means the risk is lower for female. So female participants will be eligible for more proportion of installment to be placed in PA compared to male.

Duration- When a young person signs up for Health insurance, then the coverage period is longer compared to older person. The longer coverage period or duration results in more proportion placed under PA.

Health- Health condition of the participants is also considered in placing the installments. If the participant is diagnosed with illness the risk is higher which means higher proportion placed under PSA.

Package A Health insurance provides two packages for its customers. The first one is Package

A, which provides saving for the participant in addition to the coverage for the listed illness.21 The participant can enjoy with the share of profits over the saving account (PA) according to the principles of al-Mudharabah. Several coverage is provided under packages.

20 Takaful Malaysia, Health-Care Insurance Plan, Appendix (Package A) 21 Takaful Malaysia, Health-Care Insurance Plan, Appendix (Package A)

Journal of Islamic Banking and Finance July – Sept 2017 31

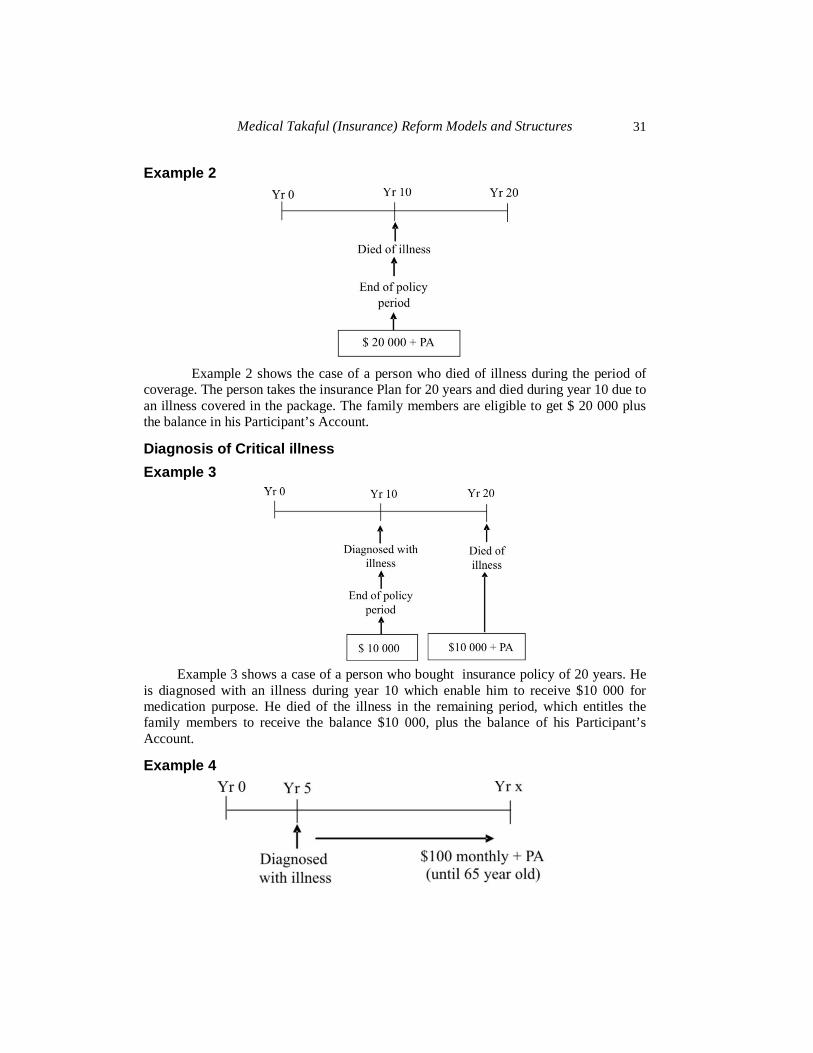

Example 2

Example 2 shows the case of a person who died of illness during the period of coverage. The person takes the insurance Plan for 20 years and died during year 10 due to an illness covered in the package. The family members are eligible to get $ 20 000 plus the balance in his Participant’s Account.

Diagnosis of Critical illness Example 3

Example 3 shows a case of a person who bought insurance policy of 20 years. He is diagnosed with an illness during year 10 which enable him to receive $10 000 for medication purpose. He died of the illness in the remaining period, which entitles the family members to receive the balance $10 000, plus the balance of his Participant’s Account.

Example 4

Medical Takaful (Insurance) Reform Models and Structures

32 Journal of Islamic Banking and Finance July – Sept 2017

Example 4 relates to a case of a permanent disablement. When a person is permanently disabled due to illness then they are entitled to receive $100 monthly plus Participant’s Account balance until the person reaches 65 years old. Besides, permanent disablement coverage also depends on the percentage of part of body which is disabled.

Accident If the participant is involved in an accident then he is eligible to get $ 40 000.This

is only if it is not caused by any illness.

Hospital Allowance If a participant is diagnosed with an illness that requires hospital stay, then the person will be entitled for $100 daily as long as he stays in the hospital. Example of illness is such as dengue.

Cash Withdrawal In case of emergency, participants can withdraw their money according to the

proportion determined earlier. Participants can withdraw 50% of the total Participants Account balance after 2 years and 70% of the total Participants Account balance after 5 years.

Package B Package B is planned more toward charity. The installment is divided according to

age groups. The premium gets higher as the age increases22. All other plans are same with Package A except for critical illness plan which is different.

Example 5

Diagnosis of critical illness

Example 5 shows that in Package B, when the participant is diagnosed with an illness, the total amount which is $ 20 000 plus AP is given. As we can see this is contrast to Package A. 22 Takaful Malaysia, Health-Care Insurance Plan, Appendix (Package B)

Journal of Islamic Banking and Finance July – Sept 2017 33

Medical Takaful (Insurance) : The Reformed Models with Structures There are eight different medical takaful models within the Maqasid al-Shari'ah

namely:

1. Ta'awuni (Cooperative) Model 2. Wakalah (Agency) Model 3. Waqf (Endowment) Model 4. Tabarru' (Philanthropy) Model 5. Hibah (Gift) Model 6. Composite(Tabarru' & Mudharabah) Model 7. Humanitarian Health-care through Zakat Model 8. Health-care through i-Crowd Funding Model The Structure in Nutshell are as follows:

.

CoP

Operational Reserve

Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Operational Reserve Claim Reserve Re-insurance IBNR / RBNS Unearned Premium

Distribution Claims No Claim Benefit

(Subjective)

Agreed Coverage (on Claim)

No Claim Benefit (Discount / Income / Both)

5

1

Surplus Operator / Insurer

(Shareholders)

2

3

4

.

WKL

Wakalah Reserve

Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Wakalah Reserve Claim Reserve Re-insurance

IBNR / RBNS Unearned Premium

Distribution Claims No Claim Benefit

(as agreed)

Agreed Coverage (on Claim)

No Claim Benefit (Discount / Income / Both)

5

1

Surplus Zakat / IT Policyholders (Subj)

Operator / Insurer

(Shareholders)

2

3

4

Medical Takaful (Insurance) Reform Models and Structures

34 Journal of Islamic Banking and Finance July – Sept 2017

.

TRS

Trustee Reserve Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Trustee Reserve Claim Reserve Re-insurance IBNR / RBNS Unearned Premium

Distribution Claims No Claim Benefit

Agreed Coverage (on Claim)

No Claim Benefit (Discount on Renewal)

5

1

Surplus Operator / Insurer

(Shareholders)

2

3

4

.

DON

Tabarru’ Reserve

Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Tabarru’ Reserve Claim Reserve

Re-insurance IBNR / RBNS Unearned Premium

Distribution Claims No Claim Benefit

Agreed Coverage (on Claim)

No Claim Benefit (Discount on Renewal)

5

1

Surplus Operator / Insurer

(Shareholders)

2

3

4

Journal of Islamic Banking and Finance July – Sept 2017 35

.

GFT

Hibah Reserve Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Hibah Reserve Claim Reserve Re-insurance IBNR / RBNS Unearned Premium

Distribution Claims No Claim Benefit

(Subjective)

Agreed Coverage (on Claim)

No Claim Benefit (Discount / Profit / Both)

5

1

Surplus Operator / Insurer

(Shareholders)

Policyholders (Subjective)

2

3

4

.

Co

MP

Management Reserve

Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Management Reserve Claim Reserve Re-insurance IBNR / RBNS Unearned Premium Investment Reserve

Distribution Claims No Claim Benefit

Agreed Coverage (on Claim)

No Claim Benefit (Investment Return)

6

Surplus Zakat / IT Policyholders Operator / Insurer

(Shareholders)

2

4

5

Investment3

1

Medical Takaful (Insurance) Reform Models and Structures

36 Journal of Islamic Banking and Finance July – Sept 2017

.

HHI

Trustee Reserve Management Operation Marketing Establishment

RM A/C (as per actuarial rate)

Trustee Reserve Claim Reserve Re-insurance IBNR / RBNS Unearned Premium

Distribution Claims No Claim Benefit

Agreed Coverage (on Claim)

No Claim Benefit (Discount / Income / Both)

5

Surplus Operator / Insurer

(Shareholders)

Policyholders (Subjective)

2

3

4

Insured (insurable interest)

Fuqara (poor)

Masakeen (needy)

Ibni Sabeel

(including Hjji & travelers)

Types of Scheme

Group Family Individual

1

.

Nation-wide Free Quality Health-care

Government is able to Cut its (Billion) Public Health-care Cost / Budget annually

Comprehensive (Inpatient & Outpatient) Test Medicine Funeral Package (Subjective)

Any of the Followings:

GLC NGO Trustee

All Public Hospitals All Public Clinics All Public Support Groups (Laboratory etc) Required Health-care Providers to be Established

Native Saudis (all levels) Expatriates (all levels) Residents (regardless of Status) Visitors (Hajj, Umrah, Ziyarah)

Justification:

al-Qur’an 09:60 Needy Test Humanitarian Test.

The Health Care Budget for 2017 is SAR 120,419,691.000.00

(2017 Budget, KSA, P. 22)

Journal of Islamic Banking and Finance July – Sept 2017 37

Recommendations

Medical takaful is undoubtedly an essential component of day to day life to care about own health within the ability and afford. Thus, the following recommendation is made in view of treating health-care insurance as a life routine.

9. Public awareness has to be made on the importance and ideas of health-care insurance.

10. Health insurance operators are to increase their market share. There are numerous insurance operators in any jurisdiction of the world and no exception in the Kingdom of Saudi Arabia. Thus, in order to strengthen the operators’ competitive position, they should conduct aggressive promotional activities. Health insurance is already a growing phenomenon among the people of different levels, because of its offered benefits. This promotion is needed in order for the information to reach out for people from all walks of life.

11. The government and the industry with a joint-effort, may take an effective initiative to reduce the misconception regarding the image of the scheme. This can be done by reducing the problems of misunderstanding of the coverage provided. This has become a big issue especially when the participants complain through the media. The executives should carefully monitor the registration process so that, the participants understand the terms and conditions.

12. The term (duration) of policy may be increased. The participation period in Malaysia for example is; only limited to 10, 15 and 20 years. The period should be increased to 25 or 30 years. This is because, if a participant gets a Health insurance plan when he or she is 20 years old then the coverage is only until the person reaches the age of 40. Usually the risk of getting illness is lesser for those bellow 40 years old.

Conclusion Human being exists in this world in a state of uncertainly as we are lack of the

knowledge of the future happening. There would be no risk if we know what will happen in the future. Without risk there will be no need for protection. In reality, we can only anticipate the future based on our past experience. From the economic point of view, uncertainty relates to the fear of having to face the possibility of huge losses. Insurance emerges as a protection from this kind of mischief. Medical takaful thus, is a monetary coverage against any critical illness. It is thus, submitted that, health-care insurance is one of the strategic plans that the operators have designed to help one monetarily who unexpectedly ought to have been diagnosed with illness thus, no contradiction with the Shari’ah or cooperative principles per se.

References 1. Ali, A. Y., 2001, the Holy Quran.