islamic banking and finance in the philippines · islamic banking and finance in the philippines...

TRANSCRIPT

ISLAMIC BANKING AND FINANCE IN THE PHILIPPINES

Presentation at the Microinsurance Learning Session Diamond Hotel, 4 July 2014

Atty. Arifa A. Ala Director, BSP

OUTLINE OF PRESENTATION

• Background on Islamic Banking and Finance

• Status of Islamic Banking in the Philippines

• Major Challenges to the Development of Islamic

Banking and Finance in the Philippines

• How to Promote Islamic Banking and Finance

• Initiatives on Islamic Banking

• The Philippine Financial System

• Opportunities from Developing Islamic Banking and

Finance

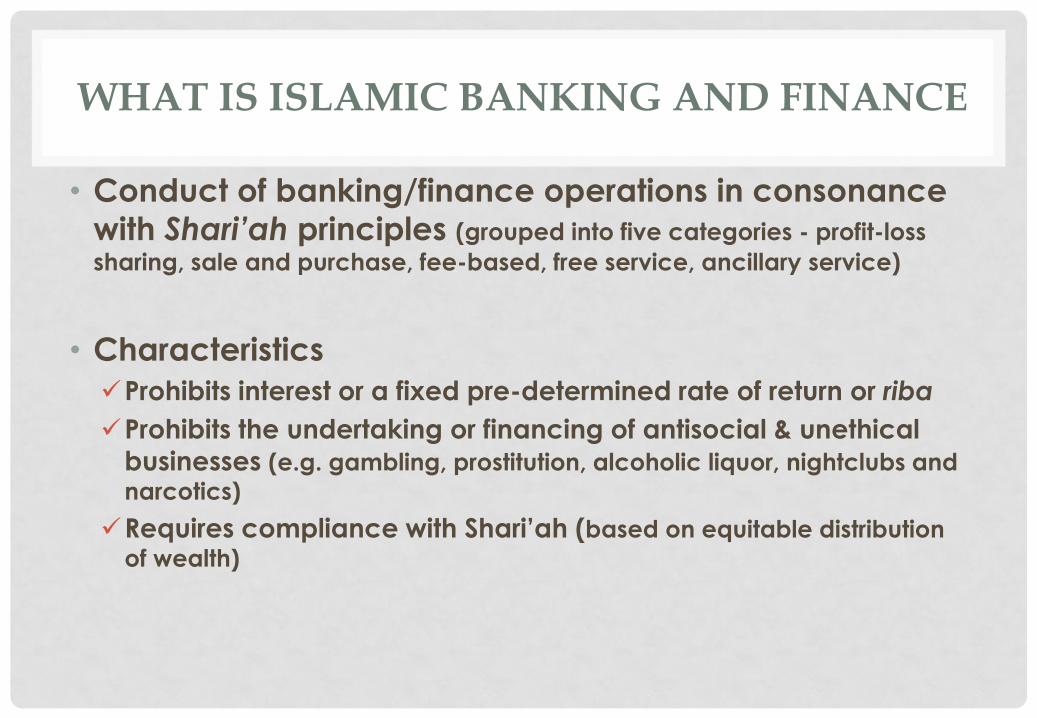

WHAT IS ISLAMIC BANKING AND FINANCE

• Conduct of banking/finance operations in consonance

with Shari’ah principles (grouped into five categories - profit-loss

sharing, sale and purchase, fee-based, free service, ancillary service)

• Characteristics

Prohibits interest or a fixed pre-determined rate of return or riba

Prohibits the undertaking or financing of antisocial & unethical

businesses (e.g. gambling, prostitution, alcoholic liquor, nightclubs and

narcotics)

Requires compliance with Shari’ah (based on equitable distribution

of wealth)

STATUS OF ISLAMIC BANKING

Only one Islamic bank - Al-Amanah

Islamic Investment Bank of the Philippines Established in 1973

Does not operate as full-fledge Islamic bank

Fully-owned by the Development Bank of the

Philippines

Operates 9 branches, 8 are located in strategic cities

in Mindanao

1. Lack of a clear legal and regulatory framework

for Islamic banking and finance Laws are not able to anticipate the need for a system engaging

many Islamic banking players

R.A. No. 6848 is limited to Al-Amanah Bank

Tax laws/regulations create tax disparities (Islamic finance

products are subject to more taxes; become more costly)

Existing laws do not provide for necessary infrastructures such

as lender of last resort, deposit insurance system and

secondary markets

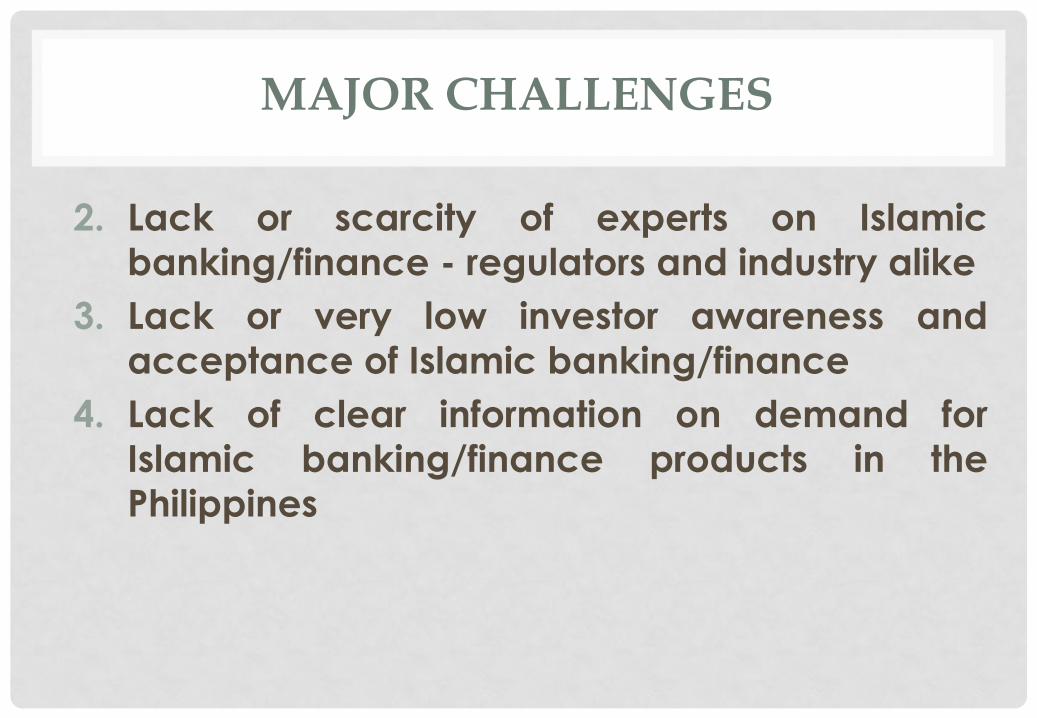

MAJOR CHALLENGES

2. Lack or scarcity of experts on Islamic

banking/finance - regulators and industry alike

3. Lack or very low investor awareness and

acceptance of Islamic banking/finance

4. Lack of clear information on demand for

Islamic banking/finance products in the

Philippines

MAJOR CHALLENGES

HOW TO PROMOTE ISLAMIC BANKING & FINANCE

How to promote IBF?

Provide level playing field

Build pool of experts on Islamic

Banking and Finance

Establish clear legal and regulatory

framework

Build broader customer and asset

base; increase investor awareness and acceptance

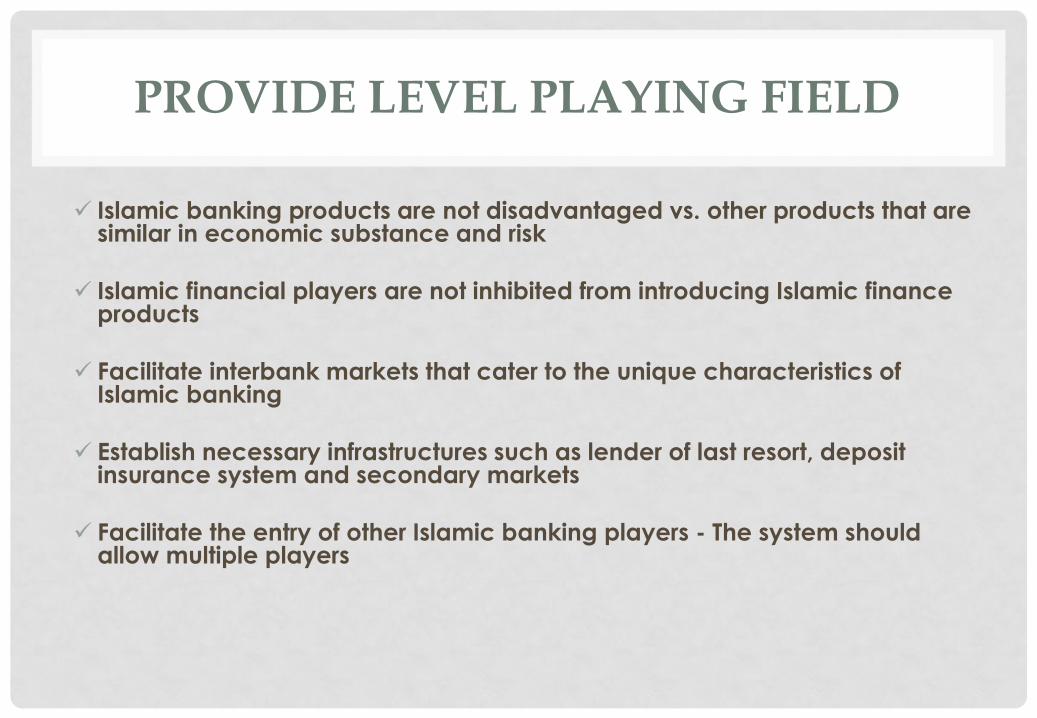

Islamic banking products are not disadvantaged vs. other products that are similar in economic substance and risk

Islamic financial players are not inhibited from introducing Islamic finance products

Facilitate interbank markets that cater to the unique characteristics of Islamic banking

Establish necessary infrastructures such as lender of last resort, deposit insurance system and secondary markets

Facilitate the entry of other Islamic banking players - The system should allow multiple players

PROVIDE LEVEL PLAYING FIELD

INITIATIVES ON ISLAMIC BANKING & FINANCE

Addressing lack of clear and regulatory framework for IBF

- Coordination with other appropriate government agencies (SEC, PDIC, DoF, Insurance Commission) to

address the lack of a clear legal and regulatory framework on Islamic banking and finance

Addressing lack of facilities that cater to the unique characteristics of Islamic Banks

- Proposed amendments to the New Central Bank Act to enable BSP to provide financial facilities to Islamic Banks, taking into consideration the peculiar characteristics of

Islamic Banking

Capacity building and increasing awareness on IBF -

Hosting/supporting workshops on Islamic banking and finance

Provide personnel with necessary trainings on Islamic banking and finance

Supporting initiatives to enable Al-Amanah Bank to

operate as full-fledge Islamic Bank

What we do

PHILIPPINE BANKING SYSTEM

Total Head Office Other Offices

Universal and Commercial Banks 5,514 36 5,478

Thrift Banks 1/ 1,856 70 1,786

Rural and Cooperative Banks 2,650 561 2,089

Total, as of March 2014 10,020 667 9,353

MAJOR GEOGRAPHICAL DISTRIBUTION OF BANKS AND ATM UNITS

11

0

2,000

4,000

6,000

8,000

10,000

12,000

Banking Offices ATMs

Luzon Visayas Mindanao Of which in ARMM

REGIONAL DISTRIBUTION OF BANKING OFFICES

12

NCR

Ilocos

Cag. Val C. Luzon CALABARZON MIMAROPA

Bicol

W. Vis.

Central Vis.

E. Vis.

Zam. Pen. N. Mind. Davao

SOCCSKSARGEN Caraga CAR ARMM

REGIONAL DISTRIBUTION OF BANKING OFFICES BY TYPE OF BANKS

13

0

20

0

40

0

60

0

80

0

10

00

12

00

14

00

16

00

18

00

20

00

22

00

24

00

26

00

28

00

30

00

NCR

Ilocos

Cag. Val

C. Luzon

CALABARZON

MIMAROPA

Bicol

W. Vis.

Central Vis.

E. Vis.

Zam. Pen.

N. Mind.

Davao

SOCCSKSARGEN

Caraga

CAR

ARMM

RCBs TBs UKBs

14 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

NCR

Ilocos

Cag. Val

C. Luzon

CALABARZON

MIMAROPA

Bicol

CAR

W. Vis.

Central Vis.

E. Vis.

Zam. Pen.

N. Mind.

Davao

SOCCSKSARGEN

Caraga

ARMM

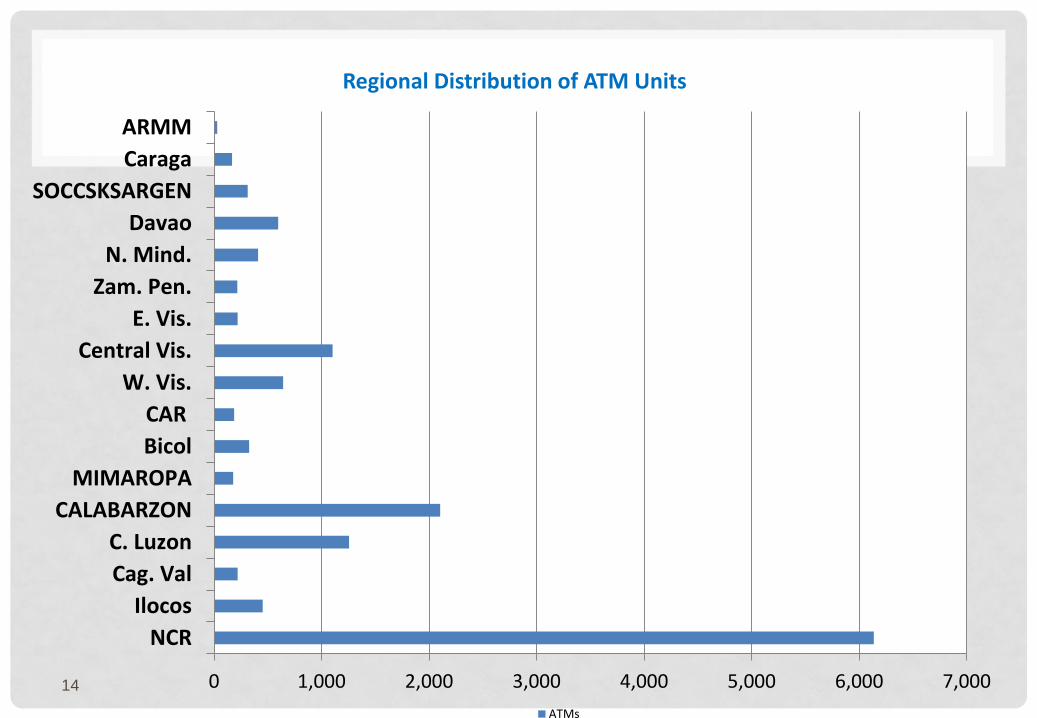

Regional Distribution of ATM Units

ATMs

PHILIPPINE FINANCIAL SYSTEM

• There is significant untapped market opportunity for

banks in the Philippines

• Only about 30% of Filipino adults have deposit accounts at a

financial institution

• Conventional banking has been slow in covering the

Autonomous Region in Muslim Mindanao. With just 20 banks and

28 ATMs present, only 8% of the municipalities of the ARMM have

a banking presence

• Banks have 34% of their physical presence in the

National Capital Region (where only 13% of the

population resides and poverty is low)

OPPORTUNITIES

• Developing Islamic Banking and Finance in the

Philippines can promote inclusive finance

• It may also trigger inflows of foreign investments which

can in turn be deployed in building necessary

infrastructures

• ASEAN Integration

• Liberalization of entry of foreign banks in the country