journal of business studies - university of rajshahi

TRANSCRIPT

Vol. 9July-December 2016

JBS-ISSN 2303-9884

JOURNAL OFBUSINESS STUDIES

FACULTY OF BUSINESS STUDIESUniversity of Rajshahi

Vol. 9, July-December 2016

JBS-ISSN 2303-9884

Journal of Business Studies

Faculty of Business StudiesUniversity of Rajshahi

www.ru.ac.bd/business

Published by : Faculty of Business Studies Dean’s Complex (2nd Floor) University of Rajshahi Rajshahi - 6205, Banglasesh Tel # -0721-711129 Email: [email protected] Web: www.ru.ac.bd/business

Printed by : Sarkar Printing Ranibazar, Rajshahi-6100 Tel : 0721-770608

Price : Tk. 300.00

University of Rajshahi(Vol. 9, July-December 2016)

Journal of Business Studies

Editorial Board

Professor Dr. Md. Shibley Sadique

Dean, Faculty of Business Studies

University of Rajshahi

Chief Editor

Professor Dr. Md. Zafor Sadique

Dept. of Management Studies

University of Rajshahi

Member

Professor Dr. Md. Ohidul Islam

Dept. of Management Studies

University of Rajshahi

Member

Professor Dr. Md. Humayun Kabir

Dept. of Accounting & Information Systems

University of Rajshahi

Member

Dr. Md. Anwarul Haque

Dept. of Accounting & Information Systems

University of Rajshahi

Member

Professor Dr. Mohammad Zahid Hossain

Dept. of Finance

University of Rajshahi

Member

Dr. Abu Sadeque Md. Kamruzzaman

Dept. of Finance

University of Rajshahi

Member

Professor A.K.M. Mostafizur Rahman Al-Arif

Dept. of Marketing

University of Rajshahi

Member

Professor Dr. Md. Salim Reza

Dept. of Marketing

University of Rajshahi

Member

Professor Abdul Quddus

Dept. Banking and Insurance

University of Rajshahi

Member

N.B. Views expressed in the articles published in this Journal are of the author(s).

Therefore, neither the Chief Editor nor any Member of the Editorial Board bears

any responsibility of the views expressed in the papers.

Editorial Foreword

Welcome to Vol.9, July-December 2016 issue, of Journal of Business

Studies, an issue which consolidates the January-July 2015, July-

December 2015 and January-July 2016 volumes. This consolidation is

deemed necessary to bridge the accumulated time lag from 2015 to the

present. Indeed it is a much anticipated and long overdue issue. The

editorial board is excited to present this issue which carries a varied range

of submissions; one we trust that will tantalize the minds of the readers of

this journal.

With its broad scope area of coverage inter alia extending from

economics, finance, accounting, management and tourism, this journal is

dedicated to a challenge rather than to a topic or an intersection of topics

per se. This challenge is to address current issues that relates to the field of

business in Bangladesh in particular and the world in general and to

incrementally add to the body of knowledge which is already in existence.

The Journal of Business Studies aims first, to contribute in its role as a

University journal by allowing all the academics, researchers and post-

graduate students of Rajshahi University the opportunity to get their work

peer-refereed and published on an open-access platform. It serves as the

starting point in the journey of getting these articles to be published in

indexed journals. In the foreseeable future, it is the aspiration of this

editorial board to get this journal indexed and accepted worldwide.

Second, the journal aims to encourage and facilitate inter-disciplinary

research on issues that relate to business across the departments within the

Faculty. It is universally acknowledged that “Business Studies” is a

subject which relates to various issues and our aim is to draw on these

academic debates and solicit contributions from a wide variety of

disciplines. Inter-disciplinary research have gained great momentum in the

world of academia, that theories and models are transcending from

disciplines and creating a niche in a ground breaking manner in areas

where it was never considered plausible. The plethora of possibilities is

vast with inter-disciplinary research andin tandem with the current

research practices. Therefore, it is an opportune time for researchers in

Rajshahi University to work collaboratively and address those knowledge

gaps that seeks to be filled.This issue embraces this diversity as you will

notice from the range of papers that it contains.

Moving to the current issue, it contains ten (10) peer-refereed articles

which seek to shed some light on contemporary research questions in the

field of business in Bangladesh. There are a series of empirically proven

research articles which will give you an insight of what is happening in the

related areas. Some of these articles are exploratory in nature and sets the

first step to the development of a more rigorous investigation and thought

provoking journey. I hope to see more extended works in the areas that

have been highlighted in this issue and publication of the same in refereed

journals.

We all know that a journal needs commitment, not only from editors but

also from editorial boards, reviewers and the contributors. Without the

support of my editorial team, Icannot imagine this feat being possible.

Special thanks, also, goes to the reviewers for supporting the editorial

board with their commitment in turning around the articles within a short

span of time and providing their invaluable input to improvise the work by

the contributors. I also thank the contributors for their trust, patience and

timely revisions.

Professor Dr. Md. Shibley Sadique

Chief Editor

Journal of Business Studies &

Dean, Faculty of Business Studies

University of Rajshahi

Contents

1. Agricultural Commercialization in Bangladesh: Are Smallholder

Farmers Market Oriented?

Md. Ataul Gani Osmani

Md. Elias Hossain

01

2. Factors Affecting the Choices for Off-farm Activities in

Bangladesh: A study on Rajshahi District

Dr. A S M Kamruzzaman

26

3. The Economics of Price Volatility in Commodity Futures

Markets: A Survey

Mahmud Hossain Riazi

45

4. Impact of Market Size and Foreign Trade on FDI Inflow in

Bangladesh: A VEC Approach

Rakibul Islam

75

5. Visitors’ Perception towards Tour Destinations: A Study on

Padma Garden

Rudrendu Ray

Md. Abdul Alim Dr. Md Enayet Hossain

95

6. Determinants of Share Prices in Bangladesh: Evidence from

Pharmaceuticals Industry

Ajit Kumar Ghose Md. Solaiman Chowdhury

117

7. Influence of Cognitive and Affective Image on a Recreational

Park: An Empirical Study

Md. Ikbal Hossain

Rebeka Sultana Rekha

Dr. Md. Enayet Hossain

133

8. Performance Evaluation of Selected NCBs and PCBs in

Bangladesh: An Empirical Study

Dr. Mohammad Zahid Hossain Md. Fazle Fattah Hossain

161

9. Succession Plan in Second or Subsequent Generation Family

Owned Firms in Bangladesh- a Study on Rajshahi Division

Md. Shariful Islam

Professor Dr. Md. Amzad Hossain

199

10. Impact of Remittances to the Economic Development of

Bangladesh

Md. Omar Faruque Udayshankar Sarkar

213

Journal of Business Studies, Vol. 9, 2016 1

JBS-ISSN 2303-9884

Agricultural Commercialization in Bangladesh: Are

Smallholder Farmers Market Oriented? Md. Ataul Gani Osmani 1

Md. Elias Hossain 2

Abstract

Agricultural commercialization is a viable mechanism to strengthen the thrust of

improving agriculture. This paper investigates the status of smallholder farmers

of Bangladesh in promoting agricultural commercialization. Using field survey

data from 100 smallholder farmers of Rajshahi district, households‟ market

orientation index is calculated to measure their market orientation status. A One-

way ANOVA analysis is performed to check whether the smallholders are using

more traded inputs in production as they move from low to high level of market

orientation. Moreover, a multiple regression analysis is applied to identify the

factors determining smallholders‟ market orientation. Results show that

smallholder farmers in the study area are not subsistence oriented as, on the

average, 65% of their produced commodities are sold in the market, and that the

sample farmers are moderately market oriented with average market orientation

index 0.59, indicating that they allocate 59% of their cultivable land to

marketable crops. The results of the study indicate that market orientated farmers

are progressively using traded inputs to increase total production and are

significantly influenced by exogenous determinants like farm size, use of

improved seeds, access to extension services and total value of produced cash

crops. These findings suggest that enhancing direct motivation, enforcing farmer-

market contacts and promoting market orientated crop technologies may

facilitate the move of smallholder farmers from subsistence to commercialized

agriculture. Keywords: Commercialization, market orientation, smallholder farmers, traded

inputs, Bangladesh

(I) Introduction

gricultural commercialization is an effective way to transform

agriculture from subsistence to market oriented agricultural

1 Lecturer, Department of Economics, Varendra University, Rajshahi,

Email: [email protected] 2 Professor, Department of Economics, University of Rajshahi,

Email: [email protected]

A

2 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

production. Commercialization of agriculture increases the ability of the

agriculture dependent developing countries to bolster economic growth

and development (Pingali and Rosegrant, 1995; Timmer, 1997). It is

generally driven by forces like globalization, urbanization, migration, state

of rising per capita income, etc. It also involves a gradual but definite

movement out of subsistence production system to increasingly market

oriented production system with progressive use of purchased (traded)

inputs (Pingali, 2001). Specifically, agricultural commercialization is a

complex and dynamic process involving various linkages between the

farm and industry, where the key agents are the farmers, traders and

processors (Thapliya, 2006). However, the core problem of promoting

agricultural commercialization in Bangladesh is the lack of effective value

chain linkages among the key agents such as input providers, farmers,

traders, processors and service providers (Azad, 2015). In Bangladesh,

market orientation of high valued crops, which generally refers to fish,

livestock products, fruits, spices and vegetables, is one of the potential

avenues of agricultural commercialization (Azad, 2015). Although the

opportunities of commercialization for these high value crops are seized

upon due to growing domestic and global demand, it requires more

advanced post harvest technologies, as high valued agricultural products

are generally more perishable than the traditional staples (Azad, 2015). It

is estimated that post harvest losses are more than 40% for highly

perishable fruits and vegetables in Bangladesh, while in food grains these

losses are estimated as 20-25%.

Agricultural commercialization requires access to agricultural markets,

and access to emerging high-income agricultural markets is seen to be

skewed in favor of large-scale farmers (Balint, 2003). In Bangladesh, most

of the farmers are smallholders and market orientation of them is hindered

by a number of difficulties such as poor quality and high cost of inputs,

high transportation costs, high market charges and unreliable market

information (Sharma et al., 2012). Thus, it is necessary to link smallholder

farmers strongly with market in order to expand demand for agricultural

products and set opportunities for income generation in rural economy

(Pingali, 1997). Market orientation of the smallholder farmers enhances

their purchasing power for food, while enabling re-allocation of their

incomes to high valued non-food agribusiness sectors and off-farm

Journal of Business Studies, Vol. 9, 2016 3

JBS-ISSN 2303-9884

enterprises (Davis, 2006). In this context, the government and non-

government organizations (NGOs) in Bangladesh are recently trying to

transform and diversify smallholder agriculture in Bangladesh as it is

prescribed in the policy forums that the development of agriculture sector

is only possible through transformation of subsistence agriculture to

agribusiness or commercialization (Azad, 2015). National Agricultural

Technology Project (NATP), Integrating Smallholders into Expanding

Markets (ISEM) project (2011-2012) and Strengthening Low-cost

Technology Market Systems (SLCTMS) (2011) are the few examples of the efforts to transform Bangladesh agriculture towards commercialization.

Agriculture has continued to play important role in the economy of

Bangladesh as it contributes 16.77% to the GDP and provides employment

for about 47% of the labor force of the country (BBS, 2013). Moreover,

about 67% of total population lives in rural areas (World Bank, 2013) and

within the rural economy, smallholder farmers are the main performers of

agriculture sector in Bangladesh (SFB, 2015). Although these smallholder

farmers have not yet fully utilized agriculture for its multiple functions,

they are now practicing market oriented agriculture that slightly includes

them with the formal market system and the related income mediated

benefits (Razzaque and Hossain, 2007).

Considering the issue of market orientation of smallholder farmers, several

questions have arisen, which remained unanswered in the context of

Bangladesh: (a) to what extent are smallholder farmers market oriented?

(b) are market oriented farmers progressively using purchased inputs in

their production? (c) and what are the factors that mostly determine the

level of market orientation of smallholder farmers in Bangladesh? This

paper is designed to respond to these questions by assessing the state of

market orientation of the smallholder farmers, the pattern of using inputs

by them, and identifying the factors that influence smallholders to be

market oriented.

The paper has the following structure. Section Two provides a brief

review of literature. Section Three deals with the methodology and data

required for the study. Section Four presents the results and discussions

based on the results, while Section Five concludes with some suggestions.

4 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

(II) Literature Review

There are both theoretical and empirical studies that have examined the

process of agricultural commercialization. However, the actual meaning of

the concept of agricultural commercialization is seldom clearly defined

(Pingali and Rosegrant, 1995; Von Braun and Kennedy, 1994). Hinderink

and sterkenburg (1987) observed from an analysis of the relevant literature

that agricultural commercialization is interpreted in different ways and is

measured in various criteria with the consequence that different aspects of

the phenomenon are taken into account. Some researchers including

Pingali and Rosegrant (1995) and Pingali et al. (2005) agreed that

agricultural commercialization leads to more specialization both at a

regional and household level, and at the same time to more diversification

at national level. As the process of structural transformation takes root, it

can be occurred through increasing participation in the rural market

economy to earn higher income, accumulate asset, and thereby the

smallholder households may be lifted out of poverty and food insecurity

through it (Gabre-Madhin and Haggblade, 2004; Haggblade & Hazell,

2010). Thus, the key feature of agricultural transformation is the transition

of smallholder farming from subsistence to commercialized farming in the

process of economic development (Johnston and Mellor, 1961; Johnston,

1970).

There is an on-going debate on the role of smallholder farmers in

economic development. Although smallholder farmers cannot cope with

current trends in market demands (IFPRI, 2005), they are important

players in agricultural growth with their significant shares in agricultural

resources, activities and outputs, as they can efficiently use their land and

cheaper family or local labor in production and directly benefit from

income and food supply growth (Hazell et al., 2007; Pingali, 2010).

Narayanan and Gulati (2002) characterized smallholder farmers as

practicing a mix of commercial and subsistence farming. Another study

defined smallholder farmers as farmers with limited resource endowments,

relative to other farmers in the sector (Dixon et al., 2003). The most

common approach to define small farms is based on the size of

landholding or livestock numbers (Nagayets, 2005; Chamberlin, 2008).

The concept of smallholder farmers in Bangladesh is defined as farmers

Journal of Business Studies, Vol. 9, 2016 5

JBS-ISSN 2303-9884

with 0.05 to 2.49 acres of cultivable land (GoB, 2008; Sharma et al.,

2012). Thus, the smallholder farmers in Bangladesh are resource poor in

terms of land holding. However, they may improve their livelihood status

through significant market orientation or commercialization, as market

orientation of smallholder farmers leads to gradual decline in real food

prices due to increased competition and lower costs in food marketing and

processing (Jayne et al., 1995). For example, smallholder farmers in

Bangladesh are enjoying better welfare outcomes in terms of more food

and goods as they move through lower to upper level of

commercialization (Osmani, et al., 2015).

Agricultural commercialization mainly entails increased integration of

farmers into the exchange economy and participation in input and output

markets (von Braun and Kennedy, 1994; Pingali and Rosegrant, 1995;

Jaleta et al., 2009). There exists little distinction between market

orientation and market participation as the former means production

decision based on market signals while the latter means the percentage

sales of output (Gebremedhin and Jaleta, 2010; 2012). However,

examining the trend of market orientation is a method of accessing the

farmers‟ participation in the output market so that the objective of

agricultural commercialization can be justified (Adenegan et al., 2013).

Thus, in order to draw policy implications to enhance agricultural

commercialization, it is important to analyze the trend of market

orientation and its determinants (Gebremedhin and Jaleta, 2010). Several

studies have also verified that the degree of market orientation is a major

determinant of competitive advantage (Fritz, 1996; Selnes et al., 1996).

Moreover, commercialized or market oriented farms depend more on

markets to collect their required inputs (improved seed, inorganic

fertilizer, crop protection chemicals etc.) instead of their own produced

inputs (Leavy and Poulton, 2007).

Although market orientation has taken its place in marketing thinking and

business operations of manufacturing firms, it is also important for the

development of agricultural firms (Helfert et al., 2001). It is shown in

some empirical research findings that market orientation is positively

related to aspects such as profitability (Narver and Slater, 1990), new

diversified product (Atuahene-Gima, 1995) and sales growth with

6 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

increased sales revenue (Greenley, 1995, Jaworski and Kohli, 1993).

There is evidence of research examining the importance of market

orientation within food industry and related sectors (Harris and Piercy,

1999). More recently market orientation of smallholder farmers has been

examined for different context in different countries (Gebremedhin and

Jaleta, 2012; Goshu et al., 2012; Adenegan et al., 2013).

Agricultural commercialization of smallholder farmers is not researched

intensively in the context of Bangladesh. It is found that

commercialization of smallholder farming in Bangladesh is still not high

enough and the farmers are still producing under the state of subsistence

agriculture (Mahelet, 2007). These farmers receive low welfare outcomes

of commercialization because of market imperfections and high

transaction costs (De Janvry et al.1991). Thus, the smallholder farmers are

not able to take part in the market for reaping the possible benefits of

commercialization unless the mentioned difficulties are removed and

better environment is created (Wegner and Zwart, 2011).

(III) Methodology

Study Area Selection and Data Collection

The present study is related to commercialization of agriculture, and is

based on primary data collected from Durgapur Upazila under Rajshahi

district of Bangladesh. The rationale behind selecting this area is that

Rajshahi is an agriculture based area. Rice is the dominant crop in the area

produced simultaneously with other minor crops such as wheat, potato,

vegetables, jute, maize, oilseeds, pulse, onion, garlic etc. Farming is the

principle occupation of most of the population and their livelihood mostly

depend on agricultural activities. In this area, farming is characterized by

low level of production technology and small size of farm holding. About

79.85% people of the Upazila are farmers and rest 20.15% people are

involved with non-agricultural activities. The present study has been

carried out in three unions, chosen randomly, from Durgapur Upazila of

Rajshahi district namely, Noapara, Deluabari, and Jhaluka. The total

population in Noapara, Deluabari, and Jhaluka are 25041, 25860 and

23028, respectively. Most of the people of these unions earn their

livelihoods from agriculture and most of the farmers are smallholders. The

Journal of Business Studies, Vol. 9, 2016 7

JBS-ISSN 2303-9884

randomly selected villages, two from each union, are Nondigram,

Kashipur, Vobanipur, Bera, Coupukoria, and Shaheber.

This study is focused on the selected smallholder farmers who are mainly

engaged in agriculture for their livelihood and the data is collected from

randomly selected farmers from the above six villages through a structured

questionnaire. The study focuses on the 2013 production year and

therefore, relied on recalled information. Multistage random sampling

technique is adopted to choose sample farmers from the study area. For

analyzing agricultural commercialization in Bangladesh, the sample has

been selected in such a way that it covers all necessary data required for

the analysis. During the sampling, firstly, the researchers selected three

unions randomly and in the next stage, two villages from each union are

selected randomly. Next, a list of all smallholder farmers is collected from

the agriculture extension office of Durgapur Upazila, and 100 respondents

were selected from the six villages of three sample unions using the simple

random sampling method.

Empirical Methodology

The methodology of the study includes quantitative techniques to obtain

the study objectives of measuring the level of market orientation,

examination of the use of purchased inputs, and estimating the factors

responsible for market orientation in the study area. That is, the methods

include a description of the techniques which are used for analysis and the

empirical design of the study. The study techniques involve descriptive

and econometric analyses. The descriptive analysis involved the use of

statistical tools like frequency tables, percentages and ratios to describe

different socio-economic characteristics, particularly related to market

orientation of the smallholder farmers. Moreover, One-way ANOVA

technique is applied to inspect the progressive use of purchased inputs in

production. To see how the factors affect the level of market orientation, a

multiple regression analysis is used as well.

There are many studies on farm market orientation and progressive

substitution of non-traded inputs for purchased inputs. These studies

defined market orientation in agriculture as a production decision issue

and the degree of allocation of resources (land, labor and capital) to

8 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

production of agricultural products that are meant for exchange or sale

(Hinderink and Sterkenburg, 1987; Immink and Aarcon, 1993). Hence, in

studying the commercialization of agriculture in Bangladesh, the present

study tries to assess the level or extent of market orientation of

smallholder farmers by calculating market orientation index following

Gebremedhin and Jaleta (2010) and Goshu et al. (2012). According to

Gebremedhin and Jaleta (2010) and Goshu et al. (2012), a smallholder

farmer is said to be market oriented if his production plan follows market

signals and he produces commodities that are more marketable. As there

exists a semi or moderate commercial system in Bangladesh (Osmani and

Hossain, 2015), production decision is significantly influenced by both

market signal and home consumption level (Gebremedhin and Jaleta,

2010), noted that all crops produced by a moderately commercialized

farmers may not be marketable in the same proportion. Thus, households

could differ in their market orientation depending on their resource

allocation (land, labor and capital) to the more marketable commodities.

Based on the proportion of total amount sold to total production at farming

system level, firstly, a crop specific marketability index is computed for

each crop produced at farming system level as follows:

N

i

ki

N

i

ki

k

Y

X

CMI

1

1 ; XY kiki and 10 CMIk (1)

Where CMI k is the crop specific marketability index defined as the

proportion of crop k sold ( X ki) to the total amount produced (Y ki )

aggregated over the total households in a farming system. CMI k takes a

value between 0 and 1, indicating that crops mainly produced for markets

have CMI k values closer to 1. After computing CMI k , household‟s market

orientation index in land allocation, MOIi , is computed from the land

allocation pattern of the household weighted by the marketability index of

each crop ( CMI k ) as follows:

Journal of Business Studies, Vol. 9, 2016 9

JBS-ISSN 2303-9884

L

LCMI

MOI Ti

k

k

ikk

i1 ; L

Ti > 0 and 0 < 1MOIi (2)

Where, MOIi is market orientation index for household i, Lik is amount

of land allocated to crop k and LTi is the total crop land operated by

household i. This also indicates that with a value of MOIi closer to 1, the

ith household allocates higher proportion of land to more marketable crops

and thus, the household is more market oriented.

Although earlier studies on smallholder market orientation have

considered output market only, a sustainable market orientation requires

integration into input markets as well (Pingali and Rosegrant, 1995). In the

crop mix of the households, market orientation may be justified by the

relative importance of more marketable crops and profit motive of the

households (Pingali and Rosegrant, 1995; Pingali, 2001). According to

Gebremedhin and Jaleta (2010) the realization of profit through market

revenues also requires increased production efficiency using modern

inputs and technologies. Having the background of market orientation, we

adopted a statistical model of One-way ANOVA to inspect whether there

is a rising trend in using purchased inputs in agricultural production by

smallholder farmers working at different levels of market orientation. The

reason is that in the recent years, per capita land holding has rapidly been

reduced and the production system has been converted from organic

system to chemical based system. In order to maximize production, most

of the ignorant farmers of remote rural areas are using purchased inputs

haphazardly such as, improved seeds, chemical fertilizer, insecticides, etc.

Finally, following Gebremedhin and Jaleta (2010), market orientation

index (market orientation) is modeled as a function of different socio-

economic factors to see how the factors affect the level of market

orientation. The functional form is as follows:

)3( )(XfMOI ii

10 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

Where, MOIi = Market Orientation Index, and Xi = Socio-economic

factors that affect the level of market orientation. In the study, market

orientation index is taken as dependent variable following the earlier study

of Gebremedhin and Jaleta (2010). Thus, for the determinants of

household market orientation a multiple regression model is employed,

since the dependent variable is a continuous one. It is found that age,

education, experience of farmer, farm size, fertilizer cost, seed quality,

ownership of oxen, non-farm income, value of produced food crops, value

of produced cash crops etc. affect the degree of market orientation or

commercialization of smallholder farmers (Goshu et al., 2012;

Gebremedhin and Jaleta, 2010). Therefore, a specified regression model is

formulated as follows:

)4( 110109988776655443322110uXXXXXXXXXXMOI i

Where, MOIi is the market orientation index or the level of market

orientation; β0, β1,..,β10 are parameters to be estimated; X1, X2,....., X 9 , 10X

are the explanatory variables that affect the level of market orientation,

and ui is the stochastic error term. The regression Equation (4) shows a

linear relationship between dependent variable and explanatory variables

and the equation is estimated using Ordinary Least Squares (OLS)

method. The explanatory variables that are used in the regression are

shown in Table 1.

Journal of Business Studies, Vol. 9, 2016 11

JBS-ISSN 2303-9884

(IV) Results and Discussion

This section provides the results of the estimations towards attaining the

objectives set for this study. To this end, descriptive statistics of collected

data from the questionnaire survey are presented at first. The results from

estimation of households‟ market orientation index are presented in the

next section. After that results from the One-way ANOVA analysis are

presented. Finally, the estimation results of the multiple regression model,

showing the influence of the key socio-economic factors on the level of

market orientation, are discussed.

Table 1: Specification of the Explanatory Variables for Multiple Regression

Models

Variable Name Type Measurement Expected

Sign

Farm size ( X 1 ) Continuous Amount of household‟s land under

cultivation (Bigha) +

Farming Experience

( 2X ) Continuous

Number of years engaged in crop

production (years) +

Education level

( 3X ) Continuous

Formal education of the household

head (years of schooling) +

Cost of Chemical

fertilizer ( 4X ) Continuous

Total value of fertilizer used in the

last production year (Tk.) +

Use of improved

seeds ( 5X ) Continuous % land used improved seeds +

Access to extension

Services ( 6X ) Dummy If access then 1, otherwise o +

Income from

livestock ( 7X ) Continuous

Total value of livestock sold in the

production year (Tk) -

Non-farm income

( 8X ) Continuous

Total income earned from non-farm

activities in the production year -

Value of cash crops

( X 9 ) Continuous Total market value of produced

cash crop (Tk.) +

Value of food crops

( 10X ) Continuous

Total market value of produced food

crops in the production year (Tk.) +

12 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

Descriptive Statistics

Analyses of the demographic and socio-economic characteristics revealed that substantial difference exists among the sample smallholder farmers of the study area. Although farm size, farming experience, education level, cost of chemical fertilizer, use of improved seeds, access to extension services, income from livestock, non-farm income, value of cash crops and value of food crops were hypothesized to be the common factors affecting commercialization, significant variations across farmers with respect to information of these variables were found. Moreover, to check whether all variables used in this study really tap into one construct from the questionnaire, we used Cronbach‟s Alpha Test of Reliability. It is an important concept in the evaluation of assessments and questionnaires which measures the internal consistency or reliability of the variables (Tavakol and Dennick, 2011). The coefficient Alpha (α) in this test ranges from 0 to 1, that is, if all variables are perfectly reliable and measure the same thing (true score), then α is equal to 1 and if there is no true score but only error in the items, then α is equal to 0. In this study, the coefficient Alpha (α) is found as 0.781 which is considered “good level of reliability” as far as social science research is concerned (Cronbach, 1951; Nunnally & Bernstien, 1994). The descriptive statistics of the variables used in the present study are shown in Table 2.

Table 2: Socio-economic Characteristics of Smallholder Farmers

Variables Mean Std. Dev. Min. Max.

Farm size (bigha) 4.01 1.824892 0.65 7

Farming Experience (years) 25.68 11.62623 4 45

Education level (years of schooling) 5.4 5.270463 0 20

Cost of Chemical fertilizer (Tk.) 6467.41 3256.146 1578 17180

Use of improved seeds (% of

cultivated land) 84.48 31.12005 0 100

Income from livestock (Tk.) 20204 25788.87 0 110000

Non-farm income (Tk.) 37252 61529.35 0 400000

Value of cash crops (Tk.) 46126.5 56299.27 0 284000

Value of food crops (Tk.) 57983.3 44550.57 5600 252000

Note: Tk. indicates Bangladeshi currency, taka

Source: Authors‟ calculations according to data from Osmani and Hossain (2013)

Journal of Business Studies, Vol. 9, 2016 13

JBS-ISSN 2303-9884

From the table it is found that the average farm size of a sample farmer is

4.01 bigha indicating that most of the farmers in the study area are

smallholders. It is also found that all farmers in the study area do not have

same experience. Table 2 shows that the average experience of the sample

farmers is 25.68 years, where minimum experience is 4 years and

maximum experience is 45 years. The average level of education of

farmers in the study area is 5.4 years of schooling with minimum of no

education and maximum of 20 years of schooling. Chemical fertilizer is an

important input for agricultural production in the study area. The average

cost of chemical fertilizer of the sample farmers is Tk.6467.41 in a crop

year. From the above table, it is observed that in 2013-14 production

season, about 84.48% of cultivated land of the sample farmers was under

the use of improved seeds. It is also seen that average annual income from

livestock asset is Tk.20244, whereas average annual non-farm income is

Tk. 37252. Farmers in the study area produce mainly food and cash crops.

It is found that the average value of produced food crops of the sample

farmers is Tk.57983.3 and that of cash crop is Tk.46126.5.

Level of Market Orientation of Smallholder Farmers

In explaining the level of market orientation of smallholder farmers in

Durgapur Upazila, we adopted a household market orientation index. As

indicated earlier, households‟ commercialization behavior can be reflected

by their land allocation pattern and the crop marketability index is used as

an indicator of the households‟ market orientation. The market orientation

index is computed for specific crops produced in 2013 production season.

The findings of market orientation index reflect that the land allocation

decision of households is designed for profit maximization. Specifically,

on average, smallholder farmers in the study area allocate 59% of their

cultivable land to the production of marketable crops and as the average

market orientation index is about 0.59, indicating a moderate market

orientation of smallholder farmers in the study area (Table 3). The

computed results from crop marketability index and household market

orientation index are presented in Table 3.

14 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

Table 3: Level of Market Orientation of Smallholder Farmers

with Crop Specific Marketability Index (CMI)

Indicators Rice Jute Potato Wheat Maize Mustard Pulse Onion Total

Total

Production

(„000‟Tk.)

4541.25 200.5 3239.8 274.99 760.51 186.98 194.48 790.9 10189.4

Total sales

(„000‟ Tk.) 1983.58 198.4 2528.04 123.69 750.51 146.48 156.5 743.9 6631.1

CMI 0.44 0.99 0.78 0.45 0.99 0.78 0.80 0.94 0.65

Household Market Orientation Index (MOI)

Indicators Obs. Mean Std. Dev. Min Max

MOI 100 0.59 0.24 0.06 0.96

Source: Authors‟ calculations according to data from Osmani and Hossain

(2013)

Analysis of crop specific marketability index indicates that 65% of total

production is sold by the households in the study area. Thus, the

households are considered moderately commercialized as their percentage

of crop sales is well above the midpoint but less than the threshold level

75%. According to Goletti (2005) and Ohen et al. (2013), farmers (small

or large) are said to be commercial if they sell more than 75% of their total

production. However, the crop specific marketability index also revealed

that jute and maize are jointly the most marketable crops in the study area.

Moreover, rice and wheat are the dominant forms of crops produced by

almost every smallholder farmer in the study area. The crop specific

marketability index calculates that only 44% of produced rice and 56% of

produced wheat are sold by the smallholder farmers in the output market

as shown in the above table. This indicates that rice and wheat farmers are

less commercialized as these crops are mainly produced in Bangladesh to

meet the farmers‟ consumption needs. Potato is another food crop

produced by the smallholder farmers where marketability index is

computed as 0.78, which indicates that potato producers are

commercialized. Table 3 also shows that crop marketability indices are

Journal of Business Studies, Vol. 9, 2016 15

JBS-ISSN 2303-9884

0.78, 0.80 and 0.94 for mustard, pulse and onion, respectively, although

farmers are less interested in production of these types.

Intensity of Market Orientation by use of Purchased Inputs

According to Gebremedhin and Jaleta (2010), market orientation is

strongly translated into crop output and input market participation.

Moreover, market orientation is geared through the progressive need to

purchased external inputs into production process. Results in Table 4

indicate that purchased input use pattern is an important determinant of

agricultural commercialization in the study area. This is evident from the

analysis of One-way ANOVA examining the relationship between the

levels of market orientation and purchased (traded) input use pattern. In

doing this statistical test, the farm households are categorized into three

groups depending on the value of MOI, such as ≤0.50, ≥0.50 to <0.75, and

≥0.75, and improved seeds, chemical fertilizer and pesticides are taken as

the intensity representatives of market orientation by the use of purchased

inputs. Moreover, as most of the respondents (about 85%) are Boro rice

producers, we only considered input cost of Boro rice production showing

the rising trend of average cost.

Table 4: Intensity of Market Orientation by use of Purchased Inputs

Representatives of Purchased

Inputs

Level of Market Orientation Prob.> F

≤0.50 ≥0.50 to

<0.75

≥0.75.

Average cost of improved

seeds (Tk.) 270.35 476.60 710.77 0.0001***

Average cost of chemical

fertilizer (Tk.) 1978.20 3487.34 5235 0.0001***

Average cost of pesticides

(Tk.) 625.43 1104.32 1657.75 0.0001***

Total Number of Observation 25 47 28 100

Note: *** 1% significance level

Source: Authors‟ calculations according to data from Osmani and

Hossain (2013)

16 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

Table 4 shows the intensity of market orientation of smallholder farmers

by the use of purchased inputs in the production of agricultural

commodities. The results presented in the table showed that the use of

purchased inputs has consistent increasing pattern along the level of

market orientation, from low to high. The One-way ANOVA test results

confirm that the variation in average costs of improved seeds, chemical

fertilizer and pesticides by farm households at different levels of market

orientation is statistically significant at 1% significance level.

Determinants of Market Orientation

A multiple regression model is estimated to examine the factors affecting

farmers‟ market orientation in the study area and the regression model is

estimated by Ordinary Least Squares (OLS) method. In this regression

analysis, farmers‟ market orientation index is used as the dependent

variable to determine farmers‟ preparedness for participation in the market

through efficient allocation of their small landholdings. Table 5 presents

the results of the OLS estimation of factors affecting smallholder farmers‟

market orientation in Durgapur Upazila of Rajshahi district, Bangladesh.

The R-squared value indicates that 49% of the variation in the market

orientation index is explained by the explanatory variables. As the study is

based on the primary data, there is a probability of occurring

heteroscedasticity and multicolinearity problems in the estimation process

of OLS. However, the robust action was taken to remedy the problem of

heteroscedasticity. Moreover, the VIF test is performed to see if the model

suffers from the problem of multicollinearity and incorrect specification.

This test reveals that the model is free from such problems as the average

VIF value for the explanatory variables included in OLS estimation is

1.45.

Journal of Business Studies, Vol. 9, 2016 17

JBS-ISSN 2303-9884

Table 5: OLS Estimation Results for Determinants of Market Orientation

Variable Coefficient Robust

Std. Err. T P>|t|

Farm size ( X 1 ) 0.028** 0.013 2.09 0.040

Farming Experience ( 2X ) 0.002 0.002 1.23 0.221

Education level ( 3X ) 0.002 0.004 0.52 0.605

Cost of Chemical fertilizer

( 4X ) 3.45e-06 6.46e-06 0.53 0.595

Use of improved seeds

( 5X ) 0.002*** 0.001 2.86 0.005

Access to extension Services

( 6X ) 0.099** 0.047 2.11 0.038

Income from livestock ( 7X ) -6.38e-08 7.43e-07 -0.09 0.932

Non-farm income ( 8X ) -3.50e-07 3.44e-07 -1.02 0.312

Value of cash crops ( X 9 ) 1.30e-

04*** 3.37e-07 3.86 0.000

Value of food crops ( 10X ) 1.93e-07 4.76e-07 0.41 0.686

Constant 0.146 0.079 1.84 0.069

F( 10, 89) = 11.92; Prob. > F = 0.0000; R-squared =0.4867; Root MSE

=0.17835

Note: *** and ** indicate 1% and 5% significance levels, respectively

Source: Authors‟ calculations according to data from Osmani and

Hossain (2013)

Table 5 shows the results from the OLS estimation of the determinants of

market orientation of smallholder farmers. The result indicates that that

the extent of market orientation by smallholder farmers is significantly

determined by farm size, use of improved seeds, access to extension

services and value of produced cash crops. That is, these variables have

stronger numerical effects on market orientation. Other explanatory

variables have no significant impact on market orientation of the small

holder farmers. It is found that there is a strong significant and positive

relationship between farm size and market orientation in the study area i.e.

(β = 0.028; P = 0.040). This indicates that if farmers‟ farm size is

18 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

increased by one bigha, market orientation index will be increased by

0.028 at 5% significance level. The fact might be that farm households

with large farm size could allocate their land for cash crop production

giving them better position to participate in the output market. The

regression result also revealed that use of improved seeds has a significant

and positive impact (β = 0.002; P = 0.005) on the market orientation

index. It explains that at 1% significance level, farm households‟ market

orientation increases by 0.20% if they use 1% more land for cultivation by

using improved seeds. This is so because use of improved seeds renders

higher production and improved seeds are supposed to be effective to

produce high quality crops resulting from high demand and possible

higher selling price for the crop.

Agricultural extension services appeared effective in inducing market

orientation for Bangladeshi smallholder farmers. The result of table 5

shows that farmers‟ access to extension services are (β = 0.0993; P =

0.038) related significantly and positively with the market orientation in

the study area. This explains that if agricultural extension services are

locally available to the smallholder farmers then their market orientation is

expected to rise by 0.099. The result may be attributed to the effective

monitoring and teaching approach of the extension agents and expert

persons in the study area. Finally, the amount of total cash crop production

(β = 1.30e-06; P = 0.000) is also strongly and positively related with

market orientation of smallholder farmers in the study area. This explains

that as value of cash crop production increases by 1 Tk., the extent of

market orientation increases by 0.00013.

(V) Conclusion

Commercialization is a new paradigm in Bangladesh agriculture.

Generally, Bangladeshi smallholder farmers have integrated into the

market system with their surplus production. This also leads to progressive

substitution of non-traded inputs in favor of purchased inputs in crop

production. Thus, this study puts emphasis on the analysis of the

potentiality of Bangladeshi smallholder farmers in enhancing farmers‟

involvement in commercial agriculture. The calculation of household

market orientation index reveals that on the average, farm households

allocate 59% of their cultivable land to the production of marketed crops.

Journal of Business Studies, Vol. 9, 2016 19

JBS-ISSN 2303-9884

This is because of the gradual substitution of complex farming system in

the study area by specialized farmers for specific high value crops in

which every farm decision depends on the market signals. It is also

important to note that as farmers in the study area are moderately market

orientated, they progressively use traded inputs like improved seeds,

chemical fertilizer and pesticides in production. One-way ANOVA test

finds that farm households are overwhelmingly using purchased inputs in

production as they move from lower to higher level of market orientation.

However, one of the key limiting factors in production is that although

farmers are somewhat market oriented, the production system is not yet

fully mechanized. Moreover, ownership or availability of factors is not

likely to be complementary to external inputs for the smallholder farmers

in the study area. Thus, for proper interventions to promote input market

orientation in terms of using more land for cultivation by using traded

inputs may need to address the problem of availability of complementary

inputs.

Moreover, the result of OLS estimation shows that market orientation of

smallholder farmers increases as the farmers with relatively larger farm

size are using more improved seeds and have well accessed to extension

services for production of cash crops. Specifically, these findings suggest

that a holistic approaches should be taken that would enforce farmer-

market contracts and fair input prices, adequate extension services for all

marginal and smallholder farmers and encourage farmers to produce and

trade market oriented crops, such as onion, pulse, maize, jute and potato.

Along these lines, there is a need to promote market oriented crop

technologies and further research on endogenous determinants of market

orientation also deserves better attention.

20 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

References

Adenegan, K.O., Olorunsomo, S.O. and Nwauwa, L.O.E., (2013),

“Determinants of Market Orientation among Smallholders Cassava

Farmers in Nigeria”, Global Journal of Management and Business

Research Finance, Volume 13, Issue 6, Version 1.0.

Atuahene-Gima, K., (1995), “An exploratory analysis of the impact of

market orientation on new product performance: A contingency

approach”, J. Prod. Innovat. Manag., 12: 275-293.

Azad, S.A.K., (2015), “High-Value Agriculture Products in Bangladesh:

An Empirical Study on Agro-Business Opportunities and

Constraints”, Dhaka University Institutional Repository, A Ph. D.

Thesis submitted to the Department of Marketing, University of

Dhaka.

BBS, (2013), “Macroeconomic indicators”, Bangladesh Bureau of

Statistics, Ministry of Finance, Government of the People‟s

Republic of Bangladesh.

BBS, (2011), “Bangladesh Population Census”, Bangladesh Bureau of

Statistics, Ministry of Finance, Government of the People‟s

Republic of Bangladesh.

Balint, B.E., (2003), “Determinants of Commercial Orientation and

Sustainability of Agricultural Production of the Individual Farms

in Romania”, PhD Dissertation, University of Bonn, Germany.

Chamberlin, J., (2008), “It‟s a Small World After All, Defining

Smallholder Agriculture in Ghana”, paper presented at

International Food Policy Research Institute (IFPRI), IFPRI

Discussion Paper 00823.

Cronbach, L.F., (1951), “Coefficient alpha and the internal structure of

tests”, Psychometricka, 16, 297-334.

De Janvry, A., Fafchamps, M. and Sadoulet. E. (1991), “Peasant

Household Behavior with Missing Markets: Some Paradoxes

Explained,” The Economic Journal, 101(409):1400-1417.

Journal of Business Studies, Vol. 9, 2016 21

JBS-ISSN 2303-9884

Davis, J.R., (2006), “How can the poor benefit from the growing markets

for high value agricultural products?”, Research Report, Natural

Resources Institute, Kent, UK.

Dixon, J., Taniguchi, K. and Wattenbach, H., Eds., (2003), “Approaches

to assessing the impact of globalization on African smallholders:

Household and village economy modeling”, Proceedings of a

working session on Globalization and the African Smallholder

Study, Food and Agriculture Organization of the United Nations.

Fritz, W., (1996), “Market Orientation and Corporate Success: Findings

from Germany”, European Journal of Marketing, Vol 30(8): 59-

74.

Gabre-Madhin, E.Z., and Haggblade, S., (2004), “Successes in African

Agriculture: Results of an Expert Survey.” World Development 32

(5): 745–766.

Gebremedhin, B. and Jaleta, M., (2010), “Commercialization of

Smallholders: Is Market Participation Enough?” Joint 3rd

African

Association of Agricultural Economists (AAAE) and 48th

Agricultural Economists Association of South Africa (AEASA)

Conference, Cape Town, South Africa.

Gebremedhin, B. and Jaleta, M., (2012), “Market orientation and market

participation of smallholders in Ethiopia: Implications for

commercial transformation”, Proceeding of International

Association of Agricultural Economists (IAAE) Triennial

Conference. Foz do lguacu, Brazil.

Goletti, F., (2005), “Agricultural Commercialization, Value Chains and

Poverty Reduction, Making Markets World Better for the

Poor”, Discussion Paper no.7, Hanoi: Asian Development

Bank.

Goshu, D., Kassa, B. and Ketema, M., (2012), “Measuring Smallholder

Commercialization Decision and Interaction in Ethiopia”, Journal

of Economics and Sustainable Development. ISSN 2222-1700

(Paper) ISSN 2222-2855 (Online), Vol.3, No.13.

22 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

GoB (Government of Bangladesh), (2008). Handbook of Agricultural

Statistics, December 2007, Ministry of Agriculture, Government of

the People‟s Republic of Bangladesh, Dhaka.

Greenley, G.E., (1995), “Market orientation and company performance:

Empirical evidence from UK companies”, Brit. J. Manage., 6: 1-13.

Haggblade, S., & Hazell, P.B.R., (2010), “Successes in African

Agriculture: Lessons for the Future”, Baltimore: Johns Hopkins

University Press.

Hazell, P., Poulton, C., Wiggins, S. and Dorward, A., (2007), “The Future

of Small Farms for Poverty Reduction and Growth”, 2020

Discussion Paper No. 42. IFPRI, Washington, D.C.

Harris, L.C. and Piercy, N.F., (1999), “Management behavior and barriers

to market orientation in retailing companies”, Journal of Services

Marketing, 13(2): 113-131.

Helfert, G., Ritter, T. and Walter, A., (2001), “How does market

orientation affect business relationships?”, Proceeding of the 17th

IMP Conference, Oslo, September 9-11, pp: 1-26.

Hinderink, J. and Sterkenbur, J.J., (1987), “Agricultural

Commercialization and Government Policy in Africa”, KPI

Limited, New York.

Immink, M.D.C and Alarcon, J.A., (1993), “Household Income, Food

Availability, and Commercial Crop Production by Smallholders

Farmers in the Western Hifghlands of Guatemala”, Economic

Development and Cultural Change, 41: 319-342

IFPRI (International Food Policy Research Institute), (2005), “The future

of small farms: Proceedings of a research workshop”, Wye, UK,

June 26-29, Washington, DC.

Jaleta, M., Gebremedhin, B. and Hoekstra, D., (2009), “Smallholder

commercialization: Processes, determinants and impact. ILRI

Discussion Papers, No. 18. Improving Productivity and Market

Success (IPMS) of Ethiopian Farmers Project. International

Livestock Research Institute (ILRI), Nairobi, Kenya.

Journal of Business Studies, Vol. 9, 2016 23

JBS-ISSN 2303-9884

Jayne, T.S., Mukumbu, M., Duncan, J., Lundberg, M., Aldridge, Staatz, J.,

Howard, J.K., Nakaponda, B., Ferris, J., Keita, F. and

Sananankoua, A.K., (1995), “Trends in real food prices in six Sub-

Sahara African countries”, Policy synthesis Number 2 East

Lansing: Michigan State University.

Johnston, B.F., & Mellor, J.W., (1961), “The Role of Agriculture in

Economic Development”, American Economic Review 51 (4):

566–593.

Johnston, B.F., (1970), “Agriculture and Structural Transformation in

Developing Countries: A Survey of Research”, Journal of

Economic Literature 8 (2): 369–404.

Jaworski, B.J. and Kohli, A.K., (1993), “Market Orientation: antecedents

and consequences”, Journal of Marketing, Vol. 57(3): 53-70.

Leavy, J. and Poulton, C., (2007), “Commercializations in Agriculture”,

Future Agricultures Consortium, working paper 003.

Mahelet, G.F (2007), Factors Affecting Commercialization of Smallholder

Farmers in Ethiopia, Ministry of Finance and Economic

Development (MoFED) GTP, Volume I: Maintext (2010).

Narver, J.C. and Slater, S.F., (1990), “The effect of marketing orientation

on business profitability”, Journal of Marketing, Vol. 4(1): 20-36.

Nagayets, O., (2005), “Small Farms: Current Status and Key Trends”,

Information Brief Prepared for the Future of Small Farms Research

Workshop, Wye College.

Narayanan, S., and Gulati. A., (2002), “Globalization and the

smallholders: A review of issues, approaches, and implications.

Markets and Structural Studies Division”, International Food

Policy Research Institute, Discussion Paper No. 50. Washington,

D.C.

Nunnally, J.C. and Bernstien, I.H., (1994), “Psychometric theory 3”, New

York: McGraw-Hill.

24 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

Ohen, S.B., Etuk, E.A., Onoja, J.A., (2013), “Analysis of Market

Participation by Rice Farmers in Southern Nigeria”, Journal of

Economics and Sustainable Development, vol. 4, no. 7, pp. 6-11.

Osmani, M.A.G. and Hossain, E., (2013), “Household survey-2013:

Commercialization of smallholder farmers and its welfare

outcome”, Department of Economics, University of Rajshahi,

Rajshahi-6205, Bangladesh.

Osmani, M.A.G., Islam, M.K., Ghosh, B.C. and Hossain, M.E., (2014),

“Commercialization of Smallholder Farmers and Its Welfare

Outcomes: Evidence from Durgapur Upazila of Rajshahi District,

Bangladesh” Journal of World Economic Research, Vol. 3, No. 6,

2014, pp. 119-126.

Osmani, M.A.G. and Hossain, E., (2015), “Market Participation Decision

of Smallholder Farmers and its Determinants in Bangladesh”,

Economics of Agriculture, Vol. (62), No. 1 (163-179).

Pingali, P.L. and Rosegrant, M.W., (1995), “Agricultural

commercialization and diversification: Process and polices”, Food

Policy, 20(3):171-185.

Pingali, P.L., (1997), “From Subsistence to Commercial Production

Systems: The Transformation of Asian Agriculture”, American

Journal of Agricultural Economics, 79(2): 628-634.

Pingali, P.L., (2001), “Environmental consequences of agricultural

commercialization in Asia” Environment and Development

Economics, null, pp 483-502.

Pingali, P., Khwaja, Y. and Meijer, M., (2005), “Commercializing small

farmers: Reducing transaction costs”, FAO/ESA Working Paper

No. 05-08. Food and Agriculture Organization of the United

Nations, Rome, Italy.

Pingali, P.L., (2010), “Agriculture Renaissance: Making “Agriculture for

Development” Work in the 21st Century”, Handbook Agric. Econ.

4:3867-3894. Elsevier.

Journal of Business Studies, Vol. 9, 2016 25

JBS-ISSN 2303-9884

Razzaque, M.A., Hossain, M.G., (2007), “Country Report on the State of

Plant Genetic Resources for Food and Agriculture”, Ministry of

Agriculture Bangladesh.

Sharma, V.P., Jain, D. and Sourovi, D., (2012), “Managing agricultural

commercialization for inclusive growth in South Asia”, Agriculture

Policy Series, Briefing Paper No. 6/2012, GDN, New Delhi, India.

Selnes, F., Jaworski, B.J. and Kohli, A.K., (1996), “Market Orientation in

United States and Scandinavian Companies: A cross-cultural

study”, Scandinavian Journal of Management, Vol 12(2): 139-157.

SFB (Syngenta Foundation Bangladesh), (2015), “Improving the

Livelihood of Smallholder Farmers”, available at:

www.syngentafoundation.org/index.cfm?pageID=579.

Thapliya, J.N., (2006), “Constraints and Approaches for Developing

Market Access and Vertical Linkages in High Value Agriculture”,

A Policy Paper (16) prepared for Economic Policy Network and

Asian Development Bank, Confederation of Nepalese Industries

(CNI) 303 Bagmati Chambers, Teku, Kathmandu, Nerpal.

Timmer, C.P., (1997), “Farmers and Markets: The Political Economy of

New Paradigms”, American Journal of Agricultural Economics,

79(2): 621-627.

Tavakol, M. and Dennick, R., (2011), “Making sense of Cronbach‟s

alpha”, International Journal of Medical Education, Vol. 2:53-55.

von Braun, J. and Kennedy, E. (Eds.), (1994), “Agricultural

Commercialization, Economic Development, and Nutrition”, Johns

Hopkins University Press, Baltimore.

von Braun, J., (1995), “Agricultural commercialization: impacts on

income and nutrition and implications for policy”, Food Policy, 20

(3): 187 – 202.

Wegner, L. and Zwart, G., (2011), “Who will Feed the World? The

Production Challenge”, Oxfam Research Report, www.oxfam.org.

World Bank, (2013), “World Development Indicators: Rural environment

and land use”, World Bank, Washington, DC.

Journal of Business Studies, Vol. 9, 2016 26

JBS-ISSN 2303-9884

Factors Affecting the Choices for Off-farm Activities in

Bangladesh: A Study of Rajshahi District

Dr. A S M Kamruzzaman

Abstract

People living in rural and semi-urban areas in Bangladesh are taking

heterogeneous income generating off-farm activities to reduce poverty. But the

participation in any employment activity or sector depends on both motivational

and ability factors. The capacity of individuals or households to participate in

such activities is not uniform. Poverty, inequality and human skills affect the

capacity of individuals or households to engage in their preferred high

remunerative off-farm activities. This paper has identified some demographic and

socio-economic ability factors of rural individuals and households to engage in

some selected off-farm activities in the study area. These factors were found to

have affected significantly the decisions of households to choose or participate in

some sample off-farm activities. Age of entrepreneur, family size, whether the

head of the family or not, education, training, past experience, social network,

loan diversion for other purposes, household land ownership, percentage of off-

farm income in total household income, percentage of equity and debt fund

invested in business, distance between the local bank branch and the residence of

an entrepreneur, and distance between the local market and the residence of an

entrepreneur were found as significant factors to affect the choices for a

particular off-farm activity in the study. The multinomial logistic regression

analysis was used for modeling the choices of off-farm activities. A randomly

selected, cross-sectional, sample survey data of 300 borrowers from the SECP

program of RAKUB, purposively selected under five categories of sample off-

farm activities, had been used in this study.

Keywords: Rural livelihood diversification, ability factors of rural entrepreneurs,

natural, human, social and financial capital

(I) Introduction

ural and semi-urban people are taking heterogeneous income

generating activities besides their main occupations to reduce the

Associate Professor, Department of Finance, University of Rajshahi

Email : [email protected]

R

Journal of Business Studies, Vol. 9, 2016 27

JBS-ISSN 2303-9884

overall risk of livelihood, or to take opportunities for higher remunerative

jobs than less remunerative traditional agriculture (Davis and Bezemer

2004). In developing countries, the resource-poor farmers are usually risk-

averse and, therefore, they will allocate less time to more risky jobs or,

alternatively, they will be willing to accept lower wages in the less-risky

environment. Rural farmers may participate in off-farm activities only to

reduce the overall risk of their incomes or to increase their total returns

(NRI, 2000)1.

Participation in any employment sector depends on both motivational and

ability factors. The first is the incentive or motivation – perhaps higher

return or less risk than alternatives. The second is the capacity of an

individual or household– perhaps certain skills or making necessary

financial commitment. It is often the poorest households who have the

highest motivation to diversify their livelihoods and also have the highest

constraints to diversify. Poverty, inequality in income and wealth, and

human skills affect the ability of an individual or household to engage in

the preferred activity or sector.

Although the choice and the participation in any rural off-farm activity for

self-employment depend on the motivation and the ability factors, the

capacity of households or individuals is not uniform. The analysis of 100

farm-households (Reardon et al 2000) shows a rough pattern of the

capacity of rural households : a positive relationship between non-farm

income share (and level) and total household income or Land-holding in

much of Africa; a negative relationship in much of Latin America, and a

very mixed set of results in Asia. They argue that the positive relationship

and the U-curve relationship (mixed results) reflect high entry barriers for

poor households to engage in nonfarm self-employment activities in

Africa and Asia.

Factors determining access to high remunerative nonfarm jobs can be of

individual, household, region or place, and project specific. Ellis and

Hussein (1998) in their study identified health and nutrition, household

1 Policy and Research on the Rural Non-Farm Economy: A Review of Conceptual, Methodological

and Practical Issues, Draft paper, NRI RNFE Project Team, November 2000.

28 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

composition, access to finance, education, social capital and infrastructure

as determining factors to have access in nonfarm jobs. These factors are

considered as assets, or factors of production, or capital representing the

capacity of household to diversify income or livelihood. In some

livelihood literature (i.e. Barrett and Reardon 2000; Ellis 2000; and

Carney 1998) factors affecting the choice, or the access of households

were classified as: natural capital (access to land or common property

resources); social capital (networks and organizations); human capital

(health and educational status); financial capital; and physical capital (hard

infrastructure, shelter and production equipments).

As population pressure increases and rapid unplanned urbanization takes

place, it has become more difficult for the rural poor to rely only on

agriculture or natural-resource-based activities. Even for many,

livelihoods have become less secure and sources of incomes have more

varied. The alternative to reduce overall risk of livelihoods or to diversity

incomes, and to take opportunities to relatively high remunerative jobs

will require some ability factors of individuals or households suitable to

have better access in it. Therefore, it is important to understand who have

access to alternative or supplementary activities that can bring sustained

and significant improvements in incomes or welfare for the individuals or

households concerned. A clear understanding of the entry-barriers faced

by different groups within the society, or even individuals within a

household is, therefore, very useful and important to academics,

institutions providing micro or SME finance, and particularly for policy

makers. Specially, financial institutions which are providing micro or

SME finance in different activity-based projects to alleviate poverty or to

develop entrepreneurial base for SME, may be benefited from this study

being better informed about the groups of entrepreneurs suitable for

heterogeneous off-farm activities.

(II) Objective of the study

This study attempts to identify the ability factors of rural households that

affect their choices for heterogeneous off-farm activities to diversify

incomes. The study has explored the capacity of individuals or households

to engage in off-farm activities crossing varying levels of entry barriers

with various forms capital (human, financial, social etc). Therefore, the

Journal of Business Studies, Vol. 9, 2016 29

JBS-ISSN 2303-9884

study has segregated the socio-economic, demographic and other factors

of rural households that determine the access to the preferred high

remunerative off-farm activities.

(III) Methods of Analysis

Logistic regression method has been used for modeling the choices of

households for some selected sample off-farm activities. Since the forms

of choices or the categories of the dependent variable are more than two or

multi-categorical, the multinomial logistic regression analysis is used to

predict the probability of being in the specific sample category of the

dependent variable for a set of independent variables or factors. A

sequential description on the estimation model, data and variables are

presented below in this section:

Estimation model

The logistic regression models the logit-transformed probability as a linear

relationship with the predictor variables. Let X1, X2, X3, . . . . . . Xn be a set

of predictors or independent variables and Z be the logit for the dependent

variable, then the logistic regression model can be written as follows:

Z = logit (P) = Log (P/1-P) = b 0 + b 1 X 1 + b 2 X 2 + . . . . . . . + b n X n

or

Z = ln [odds (event)] = ln [prob (event) / prob (nonevent)] = ln [prob (event) /

1-prob (event)]

= b 0 + b 1 X 1 + b 2 X 2 + . . . . . . . + b n X n

In terms of probabilities, the above regression equation can be translated

as follows:

P = Exp (b0 + b1 x1 + b2 x2 +. . + bk xk) / 1+ Exp (b0 + b1 x1 + b2 x2 + . . + bk xk)

Where b 0 is the constant and there are n independent (X) variables. Beta

coefficients are used to predict the log odds (logit) of the dependent

variable. To convert the log odds (which is Z, which is the logit) back into

an odds ratio, the natural logarithmic base e is raised to the Zth power:

30 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

odds (event) = exp (Z). Exp (Z) is the log odds of the dependent, or the

estimate of the odds of event.

Logistic regression estimates parameter values for b0, b1, b2 …..bn through

the Maximum Likelihood Estimation (MLE).

Data, Sample and Statistical tool

A cross-sectional sample survey data of 300 borrowers from the SECP

program of RAKUB, randomly collected from eleven than areas of

Rajshahi district, under purposively selected five categories of sample off-

farm activities popular in the sample area has been used in the analysis.

The SPSS package (11.5 Version) was used to analyze the data. The

sample design of the study is presented below:

Table 1: Sample design

Off-farm Activities

Sample Area Animal

raising Poultry Fishery Nursery Others Total

Mohonpur 5 10 15 16 10 56

Tanore 13 6 14 6 12 51

Godadari 4 4 5 0 6 19

Bagmara 4 8 5 0 4 21

Durgapur 7 8 4 2 8 29

Rajshahi 9 12 11 2 5 39

Charghat 5 9 10 7 4 35

Putia 14 9 6 6 15 50

Total 61 66 70 39 64 300

Variables

The list of the variables containing their descriptions and units of

measurements are presented below:

Journal of Business Studies, Vol. 9, 2016 31

JBS-ISSN 2303-9884

Dependent variable

Name Definition and measurement

Y choice Choice of off-farm activity

(1 = Animal raising, 2 = Poultry, 3 = Fishery, 4 = Nursery,

5 = Others)

Explanatory variables

Name Definition and measurement

AGE Age (years)

GEN Gender (0 = Female, 1 = Male)

EDU Educational level ( 1 = Primary, 2 = Secondary, 3 = Higher

Secondary,

4 = Graduation & above, 5 = No Schooling )

PEX Past experience (0 = No, 1 = Yes )

TRNG Training (0 = No, 1 = Yes)

HOF Household head (0 = Others, 1 = Himself)

NOFM Size of the family (number of family members)

LAND Household land ownership (1 = Landless and marginal farmer (0

--1.49) acres, 2 = Small and Medium farmer (1.5 -- 4.99) acres, 3 =

Large farmer (5.00+) acres.)

EQINV Equity investment in the project (TK)

REQTD Ratio of equity to debt investment (Equity/Loan)

THIN Household income (TK)

ROFFIN Ratio of household off-farm income (Off-farm income/Total

income)

ASSET Household assets of the borrower (TK)

LSNET Level of social network (0 = No participation, 1 = Participate in

one organization, 2 = Participate in two organizations, 3 =

Participate in three or more organizations)

WLDIV Whether the borrower had loan diversion motive (0 = Yes, 1 = No)

DTBR Distance from a borrower’s residence to local branch (Km)

DTBZ Distance from a borrower’s residence to local market (Km)

32 Journal of Business Studies, Vol. 9, 2016

JBS-ISSN 2303-9884

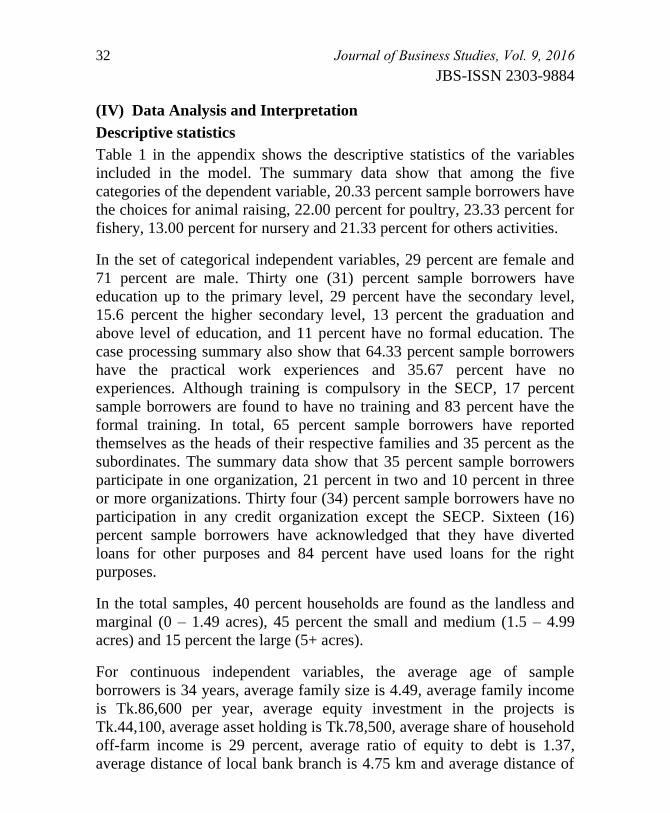

(IV) Data Analysis and Interpretation

Descriptive statistics

Table 1 in the appendix shows the descriptive statistics of the variables

included in the model. The summary data show that among the five

categories of the dependent variable, 20.33 percent sample borrowers have

the choices for animal raising, 22.00 percent for poultry, 23.33 percent for

fishery, 13.00 percent for nursery and 21.33 percent for others activities.

In the set of categorical independent variables, 29 percent are female and

71 percent are male. Thirty one (31) percent sample borrowers have

education up to the primary level, 29 percent have the secondary level,

15.6 percent the higher secondary level, 13 percent the graduation and

above level of education, and 11 percent have no formal education. The

case processing summary also show that 64.33 percent sample borrowers

have the practical work experiences and 35.67 percent have no

experiences. Although training is compulsory in the SECP, 17 percent

sample borrowers are found to have no training and 83 percent have the

formal training. In total, 65 percent sample borrowers have reported

themselves as the heads of their respective families and 35 percent as the

subordinates. The summary data show that 35 percent sample borrowers

participate in one organization, 21 percent in two and 10 percent in three

or more organizations. Thirty four (34) percent sample borrowers have no

participation in any credit organization except the SECP. Sixteen (16)

percent sample borrowers have acknowledged that they have diverted

loans for other purposes and 84 percent have used loans for the right

purposes.

In the total samples, 40 percent households are found as the landless and

marginal (0 – 1.49 acres), 45 percent the small and medium (1.5 – 4.99

acres) and 15 percent the large (5+ acres).

For continuous independent variables, the average age of sample

borrowers is 34 years, average family size is 4.49, average family income

is Tk.86,600 per year, average equity investment in the projects is

Tk.44,100, average asset holding is Tk.78,500, average share of household

off-farm income is 29 percent, average ratio of equity to debt is 1.37,

average distance of local bank branch is 4.75 km and average distance of

Journal of Business Studies, Vol. 9, 2016 33

JBS-ISSN 2303-9884

local market from home is 1.38 km. Total 300 cases were processed in the

analysis and there were no missing cases.

Model Fitting Information

Table 2 shows the model fitting information of the regression analysis

which indicates whether this model gives adequate predictions compared

to the null model or the intercept only. The null model gives the initial test

for the model in which the coefficients for all the explanatory variables are

zero.

Table 2: Model fitting information

Model -2 Log

Likelihood Chi-Square df Sig.

Intercept Only 954.824