journal 25 200903

DESCRIPTION

The Journal on financial transformation, edited by The Capital Markets Company (Capco), produced by Cypres. Capco is a leading global provider of integrated consulting, technology, and transformation services dedicated solely to the financial services industry. Recipient of the APEX Awards for Publication Excellence 2002 & 2008TRANSCRIPT

journal 03

/20

09

/#2

5

the journal of financial transformation

www.capco.com

Amsterdam T +31 20 561 6260

Antwerp T +32 3 740 10 00

Bangalore T +91 80 4199 7200

Frankfurt T +49 69 9760 9000

Geneva T +41 22 819 1774

London T +44 20 7426 1500

New York T +1 212 284 8600

Paris T +33 1 77 72 64 40

San Francisco T +1 415 445 0968

Toronto T +1 416 923 4570

the journal of fi

nancial transformation

03/20

09/#

25

Recipient of the APEX Awards for Publication Excellence 2002-2008

Cass-Capco Institute Paper Series on Risk

www.capco.com

Amsterdam T +31 20 561 6260

Antwerp T +32 3 740 10 00

Bangalore T +91 80 4199 7200

Frankfurt T +49 69 9760 9000

Geneva T +41 22 819 1774

London T +44 20 7426 1500

New York T +1 212 284 8600

Paris T +33 1 77 72 64 40

San Francisco T +1 415 445 0968

Toronto T +1 416 923 4570

the journal of fi

nancial transformation

03/20

09/#

25

Editor

Shahin Shojai, Global Head of Strategic Research, Capco

Advisory Editors

Dai Bedford, Partner, Capco

Nick Jackson, Partner, Capco

Keith MacDonald, Partner, Capco

Editorial Board

Franklin Allen, Nippon Life Professor of Finance, The Wharton School,

University of PennsylvaniaJoe Anastasio, Partner, Capco

Philippe d’Arvisenet, Group Chief Economist, BNP Paribas

Rudi Bogni, former Chief Executive Officer, UBS Private Banking

Bruno Bonati, Strategic Consultant, Bruno Bonati Consulting

David Clark, NED on the board of financial institutions and a former senior

advisor to the FSA

Géry Daeninck, former CEO, Robeco

Stephen C. Daffron, Global Head, Operations, Institutional Trading & Investment

Banking, Morgan Stanley

Douglas W. Diamond, Merton H. Miller Distinguished Service Professor of Finance,

Graduate School of Business, University of Chicago

Elroy Dimson, BGI Professor of Investment Management, London Business School

Nicholas Economides, Professor of Economics, Leonard N. Stern School of

Business, New York University

José Luis Escrivá, Group Chief Economist, Grupo BBVA

George Feiger, Executive Vice President and Head of Wealth Management,

Zions Bancorporation

Gregorio de Felice, Group Chief Economist, Banca Intesa

Hans Geiger, Professor of Banking, Swiss Banking Institute, University of Zurich

Wilfried Hauck, Chief Executive Officer, Allianz Dresdner Asset Management

International GmbH

Pierre Hillion, de Picciotto Chaired Professor of Alternative Investments and

Shell Professor of Finance, INSEAD

Thomas Kloet, Senior Executive Vice-President & Chief Operating Officer,

Fimat USA, Inc.

Mitchel Lenson, former Group Head of IT and Operations, Deutsche Bank Group

David Lester, Chief Information Officer, The London Stock Exchange

Donald A. Marchand, Professor of Strategy and Information Management,

IMD and Chairman and President of enterpriseIQ®

Colin Mayer, Peter Moores Dean, Saïd Business School, Oxford University

Robert J. McGrail, Executive Managing Director, Domestic and International Core

Services, and CEO & President, Fixed Income Clearing Corporation

John Owen, CEO, Library House

Steve Perry, Executive Vice President, Visa Europe

Derek Sach, Managing Director, Specialized Lending Services, The Royal Bank

of Scotland

John Taysom, Founder & Joint CEO, The Reuters Greenhouse Fund

Graham Vickery, Head of Information Economy Unit, OECD

Norbert Walter, Group Chief Economist, Deutsche Bank Group

TABlE of conTEnTs

PArT 1

8 opinion — Delta hedging a two-fixed-income-securities portfolio under gamma and vega constraints: the example of mortgage servicing rightsCarlos E. Ortiz, Charles A. Stone, Anne Zissu

12 opinion — reducing the poor’s investment risk: introducing bearer money market mutual sharesRobert E. Wright

15 opinion — financial risk and political risk in mature and emerging financial marketsWenjiang Jiang, Zhenyu Wu

19 Estimating the iceberg: how much fraud is there in the U.K.?David J. Hand, Gordon Blunt

31 Enhanced credit default models for heterogeneous sME segmentsMaria Elena DeGiuli, Dean Fantazzini, Silvia Figini, Paolo Giudici

41 The impact of demographics on economic policy: a huge risk often ignoredTimothy J. Keogh, Stephen Jay Silver, D. Sykes Wilford

51 risk and return measures for a non-Gaussian worldMichael R. Powers, Thomas Y. Powers

55 Medium-term macroeconomic determinants of exchange rate volatilityClaudio Morana

65 risk adjustment of bank stocks in the face of terrorDirk Schiereck, Felix Zeidler

75 Macroeconomic risk — sources and distributions according to a DsGE model of the E.U.David Meenagh, Patrick Minford, Michael Wickens

PArT 2

88 opinion — risk management in the evolving investment management industryPhilip Best, Mark Reeves

91 opinion — Bridging the gap — arbitrage free valuation of derivatives in AlMPeter den Iseger, Joeri Potters

95 Does individual performance affect entrepreneurial mobility? Empirical evidence from the financial analysis marketBoris Groysberg, Ashish Nanda, M Julia Prats

107 A new approach for an integrated credit and market risk measurement of interest rate swap portfoliosJohn Hatgioannides, George Petropoulos

113 risk drivers in historical simulation: scaled percentage changes versus first differencesSu Xu, Stephen D. Young

123 The impact of hedge fund family membership on performance and market shareNicole M. Boyson

131 Public sector support of the banking industryAlistair Milne

145 Evaluating the integrity of consumer payment systemsValerie Dias

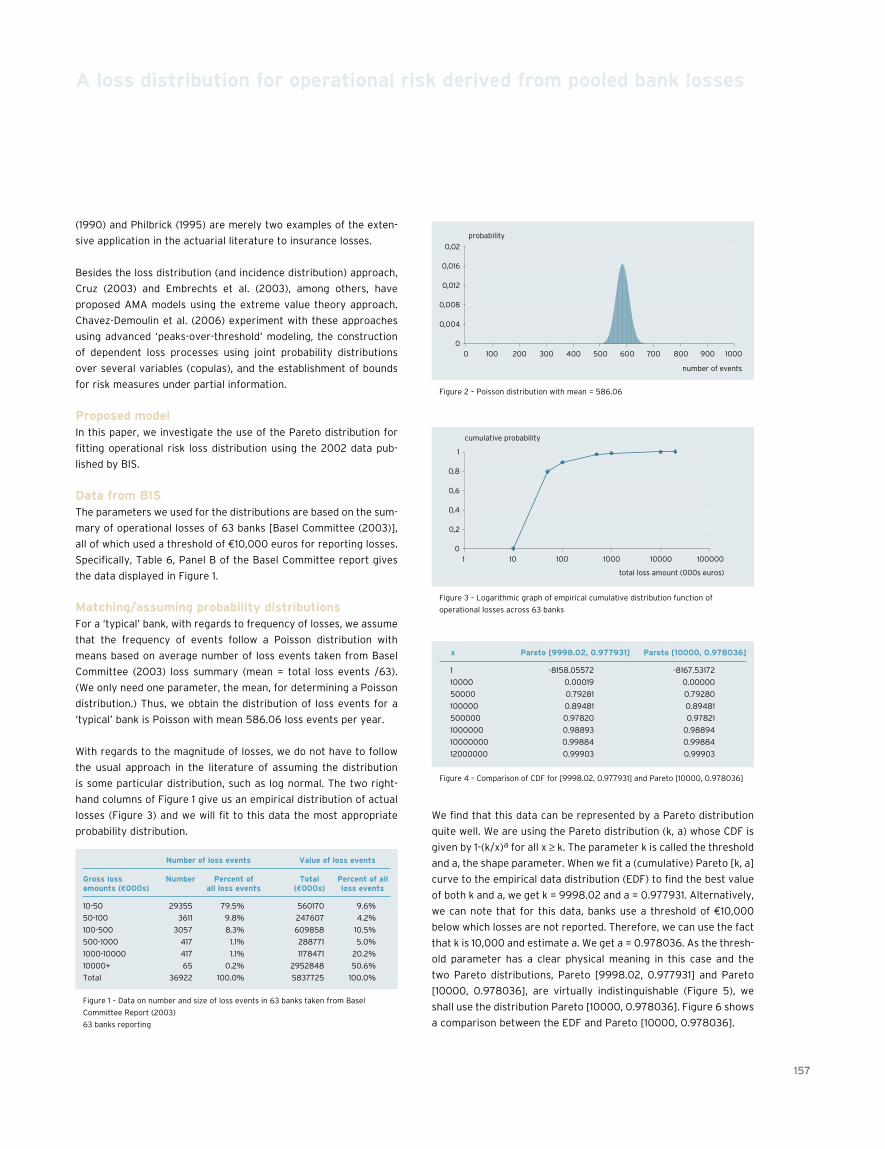

155 A loss distribution for operational risk derived from pooled bank lossesManMohan S. Sodhi, Wayne Holland

No one can deny that the extent and ferocity of the events of the past year or so have been unexpected. We all

went from having minor fears about an economic slowdown in Western economies, with the East somewhat shielded

and a manageable crisis within the financial sector, to a situation where many are talking about a potential global

depression and nationalization of most of the world’s major financial institutions. Everyday we are faced with even

more worrying news. Yet despite the uncertainty, now is when we need a clear head and ideas about what must be

done to survive, and possibly even prosper.

When this paper series with Cass Business School was established in early 2007, we were convinced that many in

the financial services sector underestimated the risks inherent in many of the instruments and transactions they

were counterparty to, and that more financial discipline was needed to benefit from the array of innovations taking

place. We highlighted a number of these concerns in the inaugural issue of the paper series and feel vindicated by

the events that have transpired since.

The establishment of this paper series exemplifies the reason we founded Capco in the first place, namely to help the

industry in ways that were not previously possible. To help the industry recognize that fascinating formulas don’t

necessarily represent accuracy, that operational risk is endemic, and that we have all got a long way to go before

we come to grips with the risks each institution faces and the most effective ways of managing them.

This second edition of the Cass-Capco Institute Paper Series on Risk covers the whole spectrum of financial sector

risks. A number of papers focus on how risk could be better understood, measured, and managed. The paper series

comes to life during our annual conference on April 6th at the Cass Business School, where we hope to see many

of you.

The challenges facing our industry have never been greater. That is why publications such as this are essential. We

need to take a critical view of what went wrong, objectively identify where the shortfalls are, and ensure that we

correct them for the future. These are the objectives of this issue, and have always been the ambitions of Capco

and its partners.

It is only through a better understanding of the past that we can make a brighter future. We hope that we have also

been able to contribute in our own way to that journey. Obviously, we still have a long way to go before we achieve

what we set out to do when we established Capco. But we shall stand shoulder to shoulder with our clients in ensur-

ing that our industry achieves the levels of efficiency that we are certain it deserves. Our hope is that you will also

join us in helping shape the future of our industry.

Good reading and good luck.

Yours,

Rob Heyvaert,

Founder and CEO, Capco

Dear reader,

After 40 years of growing confidence about our understanding of risk, many are now questioning the basic

fundamentals of how it should be measured, let alone managed. Ever since the options pricing model was

developed, so-called financial experts have been engineering exciting new instruments for the financial markets.

As the complexity and variety of these instruments grew so did the thirst of the investment community for them.

This helped create a vicious circle of demand and hubris. The last 40 years were the hubris years.

It was not only in the financial markets that hubris over our understanding of the functioning of the models

prevailed. Economists genuinely believed that they understood how economies operate and had developed models

that could influence them. Economists at the IMF sincerely thought that they understood how economic tools could

be applied and were certain of their implications.

The events of the past two years have forced everyone to take a step back and reassess their models. Everyone

has now realized that the world of economics is far too complex for anyone to be able to influence; that financial

risk is dependent on far too many variables to be correctly measured; and that the certainty with which financial

and economic experts spoke had no relationship to reality.

We were aware of the risks that were inherent within the global financial system when we first established the

Cass-Capco Institute Paper Series on Risk, and hoped that better dialogue between the world of finance and

academia would help mitigate them. However, we had no idea that our timing was so perfect, that we were fast

approaching the end of the hubris era.

We were not alone in getting caught out by the speed with which many of the stars of the world of economics and

finance lost their reputations. Many authors in this issue had no idea when thinking about their articles that they

would be so pertinent at the time of publication.

The papers in this edition highlight many of the problems that exist within the models used and provide insights

into how they can be mitigated in the future. The topics covered are broad, ensuring that we discuss as many

economic areas as possible.

We hope you enjoy reading these articles and that you also make your own contribution by submitting articles to

future issues of the Journal.

On behalf of the board of editors

The end of hubris

Part 1

Delta hedging a two-fixed-income-securities portfolio under gamma and vega constraints: the example of mortgage servicing rights

Reducing the poor’s investment risk: introducing bearer money market mutual shares

Financial risk and political risk in mature and emerging financial markets

Estimating the iceberg: how much fraud is there in the U.K.?

Enhanced credit default models for heterogeneous SME segments

The impact of demographics on economic policy: a huge risk often ignored

Risk and return measures for a non-Gaussian world

Medium-term macroeconomic determinants of exchange rate volatility

Risk adjustment of bank stocks in the face of terror

Macroeconomic risk — sources and distributions according to a DSGE model of the E.U.

Since July 2007, we have witnessed a growing number of mortgages

going into default and eventually being foreclosed. Mortgage servic-

ing rights are fees collected by institutions managing mortgages. The

yearly fees correspond to a percentage of the outstanding balance

of individual mortgages. Typically, an institution collects between 25

and 50 basis points per year (.25%-.5% of the outstanding balance

each year). The servicing is a compensation that institutions receive

for services that include the collection of the monthly payments, for

making sure that the monthly payments are paid on time, and, when

necessary, for foreclosing the property when a mortgagor defaults

on the property. Banks have been confronted with major losses

related to mortgage-backed securities and to the heavy reduction in

the volume of mortgage servicing rights.

Ortiz et al. (2008) develop a dynamical hedge ratio for portfolios of

mortgage servicing rights (MSR) and U.S. Treasury securities, such

that it is readjusted for changes in market rates and prepayment

rates. They develop a delta-hedge ratio rebalancing function for

three different portfolios, compare the three dynamic hedge ratios,

and rank them with respect to the gamma hedge ratio.

In this paper we develop a general model to obtain the optimal delta

hedge for a portfolio of two-fixed-income-securities (a1, a2), each

a function of the market interest rate y, such that when the value

of each of the individual securities changes up or down, because

of changes in market rates y, the total value of the portfolio is

unchanged. We develop the delta hedge under the constraint of a

zero-gamma in order to avoid costs related to the rebalancing of

such portfolio.

We first describe in details mortgage servicing rights (MSR), then

we develop the model, and finally discuss how our model can be

applied to MSR.

Mortgage servicing rightsBecause MSRs correspond to a percentage of the mortgages’

outstanding balance their characteristics are the same as those of

interest only (IOs). IO securities have values that are both affected

by interest rates and prepayment rates. It is interesting to analyze

the price/yield relationship of an IO security in order to understand

MSRs.

Figure 1 shows the projected scheduled principal (at the very bot-

tom), the unscheduled principal, the interest, and servicing (top)

to be paid over time for a 5.5%-FNMA pass-through security. The

pass-through security is backed by a pool of mortgages with a cur-

rent balance of U.S.$52 million, a weighted average maturity of

28.8 years, and a weighted average coupon rate of 6.243%. The

cash flows are based on a projected PSA of 50, which corresponds

to an annual prepayment rate of 3% (cpr = 3%).

Because the graph in Figure 2 is compressed, it is important, when

comparing it to Figure 1, to read the numbers on the vertical axis.

Figure 2 shows what happens to the different projected cash flows

for a projected 1000 PSA (60% annual prepayment rate). Clearly,

the total principal being repaid overtime remains the same (same

area under the curve) under the two different prepayment scenari-

os, however, both the interest and servicing are being significantly

reduced for faster prepayment rate. When principal is refinanced,

no more interest is paid by mortgagors and banks cannot collect

servicing fees for mortgages that do not exist anymore.

Prepayment rates are a function of interest rates. When interest

rates decrease, prepayment rate increases and vice versa. Figure

3 graphs the projected cash flows of an IO security over time, for

different prepayment scenarios.

Figure 3 is taken from Bloomberg and shows the cash flows of a 9%

FHS IO under four different PSA scenarios. CPR stands for constant

prepayment rate. A CPR of 5% indicates that mortgage principal

is being prepaid at an annual rate of 5%. The prepayment model

developed by the Public Securities Association (PSA) is also widely

used for a basis of quoting prices on mortgage-backed securities.

A 100 PSA corresponds to a 6% cpr, a 200 PSA corresponds to a

12% cpr, and a 500 PSA corresponds to a 30% cpr. In the Figure,

PSA ranges from 0% to 395%. When PSA rate is high, more of the

outstanding balance is being prepaid, so less IO or MSR is available

as a percentage of outstanding remaining balance. This can be

Delta hedging a two-fixed-income-securities portfolio under gamma and vega constraints: the example of mortgage servicing rights Carlos E. Ortiz, Chairman, Department of Computer Science and Mathematics, Arcadia University

Charles A. Stone, Associate Professor, Department of Economics, Brooklyn College, City

University of New York

Anne Zissu, Chair of Department of Business, CityTech, City University of New York, and Research

Fellow, Department of Financial Engineering, The Polytechnic Institute of New York University

8 – The journal of financial transformation

observed for example under PSA 395, the lowest curve in Figure 3.

On the other hand, for low PSA, the outstanding balance remains

at a greater level, and the derived cash flows stay higher (see top

curve for extreme scenario of 0 PSA).

It is important that the reader understands that the value of an IO,

or of a MSR, is the present value of the cash flows received over

time. Clearly, the lower the cash flows are (due to high prepayment

rates), the lower the value is. On the other hand, the higher the cash

flows are, due to high market interest rates and therefore low pre-

payment rates, the higher the value is. This is true only over a range

of interest rates (prepayment effect). At some point, however, the

discount effect takes over the prepayment effect, and the value of

IOs or MSRs will start to decrease. We show the typical value of an

IO or MSR as a function of interest rates in Figure 4.

The value of an IO security or a MSR increases when interest rates

(y) increase as long as the prepayment effect is greater than the

discount effect. When the discount effect takes over, we observe

the value decreasing for increases in interest rates. Both IOs and

MSRs are very interesting types of securities. Most fixed income

securities decrease in value when yields increase. IOs and MSRs do

the opposite for a wide range of yields.

s-curve prepayment functionIt is important to understand the prepayment behavior in order to

value MSR. Periodically, investment banks submit to Bloomberg

their expected PSA level for corresponding changes in yield.

Figure 5 shows the data submitted by twelve investment banks

on their expected PSA levels for corresponding changes in yields

ranging from -300 bps to +300 bps, for the same 5.5% FNMA

pass-through security we described in the beginning of the paper

with Figures 1 and 2. It is interesting to observe how different

these projections can be. For a decrease of 300 bps, the projected

PSA ranges from 884 to 3125 (a corresponding cpr ranging from

53% to 187.6%).

9

Figure 1 Figure 3

Figure 2 Figure 4

10 – The journal of financial transformation

Figure 6 plots for different changes in yield, the corresponding

expected PSA level for each investment bank that submitted

information to Bloomberg on October 2008 for a specific pool of

securitized mortgages. The changes in yield are represented on the

horizontal axis, with expected PSA levels on the vertical axis. The

curve represents the median for the twelve banks that submitted

the data. One can see that the prepayment curve, as a function of

changes in yield, has an S-shape. The S-shape prepayment function

is common to all banks, but each differs in projecting its magnitude/

steepness.

The S-curve shows a steeper slope around the initial market rate

(at 0% change in yield), with prepayment rate increasing as mar-

ket rates continue to drop, until a burnout effect is reached, and

the curve flattens, meaning that prepayment rate is no longer

increasing as it did in the middle range of market rates decrease.

The S-curve also flattens in the high range of market rates. What

happens is that prepayment rate decreases with increase in market

rates until it reaches a minimum beyond which no further decrease

in prepayment rates is observed. The natural level of prepayment

rate is reached, that is, the prepayment rate that is independent of

market rates, but is a function of mortgagers’ personal events.

We next, express the relationship between prepayment rate (we

use cpr for prepayment rate instead of PSA) and the change in

basis points. The prepayment rate, cpr, is mainly a function of the

difference between the new mortgage rate y in the market and the

contracted mortgage rate r. cpr = a ÷ [1 + eb(y-r)].

We now develop a general model for a two-fixed-income-security

portfolio that is delta and gamma hedged against interest rate

changes.

Model for portfolio optimizationWe have a portfolio of two securities (a1, a2). Each security's value

is a function of the market interest rate y. We want to find the opti-

mal share of each security in the portfolio such that: Σi=k→2 αiai = K

(1), where αi is the weight of security ai. In order for the value K of

the portfolio, at a specific yield y, to be hedged against any move-

ments in interest rate we need to find the optimal weights for each

security in the portfolio, such that when there is a change in market

rates the sum of the change in value of each security times its cor-

responding weight in the portfolio is equal to zero.

We next, develop a general model and apply it to the particular case

of portfolios of mortgage servicing rights (MSRs). Consider two

functions ai(y), i = 1,2 and two coefficients αi, i = 1,2. We want the

following to hold: Σi=1→2 αiai(y) = K (2).

The values of the functions ai(y) are given for every value of y and

we want to find the values of αi that will satisfy equation (2), and

other conditions of ‘stability’ that we will describe later.

notation: For any ƒ(y) let us denote by ƒ(n)(y) the n-th derivative

of ƒ.

When the αi’s are assumed to be constant, the objective is to find

for a fixed y0, hence for any given value of the ai(y0), values of the

constants αi, such that: Σi=1→2 αiai(y0) = K (3).

[Σi=1→2 αiai(y0)]1 = [Σi=1→2 αiai(1)(y0)] = 0 (4), where the second con-

dition represents the constraint that the total sum of the αiai(y0)

will not change for small changes in y from the initial value y0.

More generally, to obtain an optimal portfolio we need to find the

values of the αi for i = 1,2 such that for small changes in y from

the original y0, the value of Σi=1→2 αiai(y) will not change from the

original value of Σi=1→2 αiai(y0) = K.

Figure 5

Figure 6

11

For a fixed y0 there exists a unique solution that optimizes the port-

folio of two fixed income securities if: a1(y0)a2(1)(y0) – a1

(1)(y0)a2(y0)

≠ 0. As expected, this condition depends only on the values of the

functions a1, a2 and their derivatives at point y0. The values for α1

and α2, the optimal weights for the two securities that constitute a

delta-gamma hedged portfolio, are:

α1 = [Ka2(1)(y0)] ÷ [a1(y0)a2

(1)(y0) – a1(1)(y0)a2(y0)]

α2 = [-Ka1(1)(y0)] ÷ [a1(y0)a2

(1)(y0) – a1(1)(y0)a2(y0)]

If: a1(y0)a2(1)(y0) – a1

(1)(y0)a2(y0)] = 0

Then we have no solutions or there exist infinitely many solutions.

Examples of no solutionsIt is not unusual to have a portfolio of fixed-income securities that

increases in value when market rates decline and decreases in

value when market rates rise. We could have, for example, a portfo-

lio composed of a 30-year 8% coupon bond with a 10-year Treasury

note. This is a case when it is impossible to delta hedge the portfolio

under gamma and vega constraints.

The case of mortgage servicing rightsA delta-hedged portfolio could have a combination of bonds and MSR.

We next present the valuation approach developed by Stone and

Zissu (2005) that incorporates the prepayment function (S-curve).

Valuation of Msr

The cash flow of a MSR portfolio at time t is equal to the servicing

rate s times the outstanding pool in the previous period: MSRt =

(s)m0(1 – cpr)t-1Bt-1 (5), where m0 is the number of mortgages in

the initial pool at time zero, B0 is the original balance of individual

mortgage at time zero, r is the mortgage coupon rate, cpr is the

prepayment rate, m0(1-cpr)t is the number of mortgages left in pool

at time (t), Bt is the outstanding balance of individual mortgage at

time (t), and s is the servicing rate.

V(MSR) = (s)m0 [Σ(1 – cpr)t-1Bt-1] ÷ [(1+y)t] (6), with t = 1,…..n (through

the entire paper)

Equation (6) values a MSR portfolio by adding each discounted cash

flow generated by the portfolio to the present, where n is the time

at which the mortgages mature, and y is the yield to maturity.

After replacing the prepayment function in equation (6) we obtain

the MSR function as:

V(MSR) = (s)m0 [Σ(1 – (a/(1+expb(y-r)))t-1Bt-1] ÷ [(1+y)t] (6a)

Valuation of a bond

The valuation of a bond with yearly coupon and face value received

at maturity is represented in equation (4): V(B) = c Σ1/(1+y)t + Face/

(1+y)t (7), where V(B) is the value of a bond, c is the coupon, Face

is the face value, n is the time at which the bond matures, and y is

the yield to maturity.

If we now relabel equation (6a) and equation (7) as a1 and a2 respec-

tively, and replace them in the equations we derived previously for

the optimal α1 and α2 respectively, we obtain a portfolio of bonds

and of MSR that is delta- and gamma-hedged against small changes

in interest rates and corresponding changes in prepayment rates.

conclusionWith an estimated $10 trillion in outstanding mortgages, MSR gen-

erate a significant source of income for banks. This is a significant

market with risks that need to be addressed. If not managed prop-

erly, banks will have important losses to report. Prepayment risk

and interest rate risks need to be carefully evaluated when creating

a portfolio of fixed income securities. We have developed a gen-

eral portfolio of two-fixed-income securities, each with the optimal

weight, in order for the portfolio to be delta- and gamma-hedged

against small changes in interest rates. We have shown how this

model can be applied to portfolios’ MSR.

references• Bierwag, G. O., 1987, “Duration analysis: managing interest rate risk,” Ballinger

Publishing Company, Cambridge, MA

• Boudoukh, J., M. Richardson, R. Stanton, and R. F. Whitelaw, 1995, “A new strategy for

dynamically hedging mortgage-backed securities,” Journal of Derivatives, 2, 60-77

• Ederington, L. H., and W. Guan, 2007, “Higher order Greeks,” Journal of Derivatives,

14:3, 7-34

• Eisenbeis, R. A., S. W. Frame, and L. D. Wall, 2006 “An analysis of the systemic risks

posed by Fannie Mae and Freddie Mac and an evaluation of the policy options for

reducing those risks,” Federal Reserve Bank of Atlanta, Working Paper Series, Working

Paper 2006-2

• Goodman, L. S., and J. Ho Jeffrey, 1997, “Mortgage hedge ratios: which one works

best?” Journal of Fixed Income, 7:3, pp 23-34

• Mato, M. A. M., 2005, “Classic and modern measures of risk in fixed-income portfolio

optimization,” Journal of Risk Finance, 6:5, 416-423

• Office of Thrift Supervision, 2007, “Hedging mortgage servicing rights,” Examination

Book, 750.46-750.52, July

• Posner K., and D. Brown, 2005, “Fannie Mae, Freddie Mac, and the road to redemp-

tion,” Morgan Stanley, Mortgage Finance, July 6

• Ortiz, C. E., C. A. Stone, and A. Zissu, 2008, “Delta hedging of mortgage servicing port-

folios under gamma constraints,” Journal of Risk Finance, 9:4

• Ortiz, C. E., C. A. Stone, and A. Zissu, 2008, “Delta hedging a multi-fixed-income-securi-

ties portfolio under gamma and vega constraints,” Journal of Risk Finance, forthcoming

• Stone, C. A. and A. Zissu, 2005, The securitization markets handbook: structure and

dynamics of mortgage- and asset-backed securities, Bloomberg Press

• Yu. S. K., and A. N. Krasnopolskaya, 2006, “Selection of a fixed-income portfolio,”

Automation And Remote Control, 67:4, 598 – 605

12 – The journal of financial transformation

reducing the poor’s investment risk: introducing bearer money market mutual sharesRobert E. Wright, Clinical Associate Professor of Economics, Department of Economics, Stern School of Business, New York University

Now that micro-credit in general and the Grameen Bank in particular

have finally received their due recognition [Yunus and Jolis (1998)],

policymakers and international financiers can begin to focus on the

other side of the poor’s balance sheet, their assets or savings. As de

Soto (2000) and others have pointed out, property rights in many

countries remain precarious and formal protection of physical and

intellectual property costly. In many places, not even the local curren-

cy can be trusted to hold its value for any significant length of time.

Billions of people therefore have little ability or incentive to save.

Outsiders cannot impose democracy or property rights protections

[Baumol et al. (2007)] and, as Stiglitz (2002), Easterly (2006), and

others have argued, the IMF and World Bank can do precious little

to thwart bouts of inflation, exchange crises, and financial panics in

developing countries. Outsiders can, however, provide the world’s

poor with a safe, low transaction cost, and remunerative savings out-

let. For several generations, poor people in many places throughout

the globe have saved by buying U.S. Federal Reserve notes and the

fiat currencies of other major economic powers. Although subject to

physical risk (theft, burning, and so forth) and exchange rate fluctua-

tions, such notes typically held their purchasing power much better

than local notes or bank deposits denominated in local currencies. As

the dollar weakens over the next few decades, as most expect it to

do as the U.S. economy loses ground relative to Europe, a revitalized

Japan, and the BRIC nations, its allure as a savings vehicle will fade.

International financiers can fill the vacuum with a simple product,

bearer money market mutual shares (B3MS), almost guaranteed to

appreciate against all the world’s fiat monies.

reducing the poor’s investment risk: introducing bearer money market mutual sharesHelping budding entrepreneurs to obtain loans, even for just a

few dollars, is beyond noble. It is growth-inducing. Where oligarchs

or the grabbing hand of government [Shleifer and Vishny (1998)]

are not overpowering, micro-credit can summon forth productive

work where before was only despair [Aghion and Morduch (2005),

Khandker (1998), Yunnis and Jolis (1998)]. Micro-insurance is also

gaining traction [Mijuk (2007)]. But what becomes of the entre-

preneur who thrives and begins to accumulate assets? The small

businessperson who, for any number of valid reasons, may not want

to continue plowing profits back into her business? Who fears pur-

chasing conspicuous physical assets lest they be seized by the state

or brigands? Who wishes to avoid investing in financial assets issued

by shaky, inept, or corrupt local intermediaries or denominated in a

local currency of dubious value over the desired holding period, be it

a week, month, year, or decade?

For the past several generations and up to the present, millions of

such people worldwide have invested in U.S. Federal Reserve notes

or the physical media of exchange of other major nations. Although

subject to some physical risk of theft, loss, burning, and the like, the

high value to bulk of such notes renders them ideal for saving for a

personal rainy day or hedging against a local economic meltdown.

Returns in terms of local purchasing power are not guaranteed, but

Federal Reserve notes are perfectly safe from default risk and highly

liquid, sometimes even more liquid than local notes or deposits. Their

widespread use as personal savings and business working capital

attests to the financial savvy of people worldwide [Allison (1998)].

The U.S. dollar has often been the best available savings option

for the world’s poor. Physical currencies are not, however, optimal

investment instruments and the long-run outlook for dollar-denomi-

nated assets of all stripes is weak. Although the dollar long tended to

appreciate vis-à-vis local currencies, short-term depreciations which

temporarily reduce the purchasing power of Federal Reserve notes

held by the poor are frequent and notoriously difficult to predict

[Chinn and Frankel (1994)]. Moreover, in the future, the dollar may

tend to depreciate as the U.S. economy loses ground relative to a

united Europe, a resurgent Japan, and the growth of the BRIC (Brazil,

Russia, India, China) economies [Vietor (2007)]. In fact, numerous

central banks are already beginning to rethink their peg to the dollar

and emerging market entrepreneurs will not be far behind [Slater

and Phillips (2007)]. The poor could respond to a sustained deprecia-

tion of the dollar by substituting physical yen, euro, or other curren-

cies in their portfolios but they would still face the risk of adverse

exchange rate movements, to wit the appreciation of their local

currencies. And of course no fiat currency pays interest or is immune

from counterfeiting. Holding another country’s paper currency as an

investment instrument is ingenious but hardly foolproof.

International financiers could supply the world’s poor with a similar

but ultimately superior instrument, a liquid, low-cost, constantly

appreciating bearer instrument with almost no default or counterfeit

risk and low levels of physical risk. And they have economic reasons

for doing so because the profit potential, especially for an aggressive

first-mover, is enormous. Estimates vary but the consensus is that

60 to 70 percent of all Federal Reserve notes outstanding, about

U.S.$800 billion in 3Q 2008, circulate outside of the U.S. proper

[Allison and Pianalto (1997), Lambert and Stanton (2001)]. Supplying

the world with liquid bearer savings instruments is, in other words,

approximately a U.S.$500 billion business and growing.

Savers in emerging markets would prize a private instrument

13

more highly than dollars, euro, yen, or other fiat currencies if the

returns of holding the private instrument were relatively higher and

steadier and if it were as safe and liquid as fiat notes, less easily

counterfeited, and less subject to physical risk. Such an instrument

currently does not exist, but bearer shares issued by a money mar-

ket mutual fund (B3MS) in an intelligent way could fit the bill. B3MS

could provide the poor worldwide with a low-transaction cost yet

remunerative alternative to fiat currencies while simultaneously

generating considerable seigniorage profits for the fund(s) that

provide the best product.

A money market mutual fund could sell physical bearer shares in

itself in exchange for major or local currencies, immediately investing

them in safe, short-term government and corporate notes denomi-

nated in dollars, euro, yen, and a basket of other currencies. Rather

than crediting earned interest to an investor’s account as money

market mutual funds traditionally have done, a B3MS fund would

simply keep reinvesting its profits. The market value (and net asset

value, or NAV) of each bearer share would therefore increase, just

as stock prices increase when corporations retain profits instead of

paying them out as dividends. Just as traditional mutual fund shares

‘appreciate’ against the dollar (euro, etc.), so too would B3MS appre-

ciate against (buy more of) all of the world’s fiat currencies.

For example, a budding young entrepreneur in Ethiopia might pur-

chase 100 B3MS for 9,000 Birr (roughly, U.S.$90) today, but in a

year’s time he will be able to obtain, say, 9,200 Birr for his shares,

either by redeeming them at the fund or, more likely, by selling

them to another investor who is willing to give more Birr for the

shares because their NAV would have increased due to a year’s

accrued interest. If a fund emerges with a strong product and a

long lead time before competitors appear, it may be able to avoid

ever having to redeem its shares because the secondary market for

them could grow sufficiently deep that local investors would always

find someone to take them off their hands. The shares could begin

to pass from hand-to-hand like cash (albeit at slowly increasing

local values) and domestic financial institutions could deal in them,

perhaps even offering euro B3MS accounts and loans analogous to

eurodollar accounts and eurocredit loans.

If this sounds like eighteenth and nineteenth century banking

systems in Scotland and America, where banks issued bearer

liabilities in the form of non-legal tender convertible notes, it should

because the general principle is identical [Bodenhorn (2000, 2003),

Checkland (1975), Perkins (1994)]. But unlike banks, the assets of

which are notoriously difficult for outsiders to value and hence are

subject to runs in the absence of deposit insurance [Diamond and

Dybvig (1983), Jacklin and Bhattacharya (1988)], money market

mutual funds invest transparently and safely and their liabilities

are effectively marked-to-market. Money market mutual funds are

therefore never run upon in any economically significant sense.

The worst that can happen, barring a global catastrophe, is that the

NAV of their shares declines below par, but even that is a rare event

[Collins and Mack (1994), Macey and Miller (1992)]. Particularly in

developing economies, mutual funds are superior to deposit insur-

ance, which induces banks to take on tremendous and potentially

destabilizing risks [White (1995)].

If B3MS issuance would benefit both the fund managers and the

shareholders, why has the product not yet emerged? One could just

as well ask why were exchange traded funds (ETFs) not introduced

until the early 1990s? Why did mutual funds not proliferate until after

World War II? Why was life insurance the reserve of a tiny handful

of people until the 1840s? The answers remain unclear [Eaker and

Right (2006), Murphy (2005), Roe (1991)]. Perhaps no one has yet

developed the idea or perhaps international financiers fear factors

that could prevent B3MS issuers from earning a reasonable profit.

Some potential issuers may fear the wrath of government. Local

governments, for example, may not like residents selling their cur-

rencies for B3MS. That may be, but governments have already shown

that they can do little about it. Dollars and other foreign physical

currencies already circulate in large numbers. Most countries realize

that they cannot control what residents use for cash and may wel-

come the substitution of private instruments for dollars, which are

a palpable symbol of U.S. hegemony and on an increasingly shaky

economic footing. In other words, most governments realize they are

already losing seigniorage and would rather lose it to an international

mutual company than to the American government. In fact, since

the U.S. government has the most to lose it represents the biggest

threat to any fund issuing B3MS. Thankfully, offshore havens abound

and the U.S. government would be hard pressed to take a principled

stand against a private competitor. Another potential problem is that

the world’s poor may eschew B3MS for cultural reasons or from mere

ignorance. The nature of the shares will certainly need explanation

but much of the public education can be handled via websites and

at the points of issuance and tender. As Prahalad (2006) and oth-

ers have shown, the poor are astute value hunters. They will quickly

learn the virtues of new savings instruments as they do other new

products. Cultural barriers will be minimal in most places but some

Muslims may object to holding B3MS because the fund issuing them

invests in debt. The shares themselves, however, are equity instru-

ments and no explicit interest is paid, so many Muslims will likely

accept them [Obaidullah (2004), Vogel and Hayes (1998)].

Other potential problems are technical. If the fund gains signifi-

cant market share it will be enormous and may come to influence

the world’s money markets. The fund’s managers will have to pay

much closer attention to foreign exchange markets than tradi-

tional money market mutual fund managers do and may well find

it expedient to hedge exchange rate risks using futures markets or

other derivatives. Optimal trading strategies are not clear a priori

so undoubtedly mistakes will be made. The managers must have

incentives to earn low and safe returns and disincentives to taking

on risks that could endanger the fund’s principal [Wright (2008)].

Fund managers must also devise physical shares that are relatively

immune from counterfeiting and the risks of physical destruction,

carefully balancing the costs and benefits of different technologies.

Paper is a relatively cheap and well-established material but is

perhaps too easily counterfeited and destroyed. Shares made from

plastic, metal, or composite materials, although more expensive to

produce, may prove superior because they would be more robust

physically and could incorporate stronger security and convenience

features including visual, sub-visual, tactile, sonic, and electronic

authentication devices. Although the B3MS concept probably can-

not be patented, the technologies incorporated into its physical

shares could be, providing a barrier to entry likely strong enough

to dissuade free riders (numerous competing funds issuing B3MS)

until the initial entrant(s) have gained significant market share.

As Baumol et al. (2007) show, such barriers are often crucial con-

siderations for innovative entrepreneurs. It may seem strange to

invest in the technology of physical media of exchange in the early

twenty-first century. The simple fact of the matter is that breath-

less predictions of an e-money revolution have proven to be hot air

[Palley (2002)]. At best, an e-money evolution is underway but it

will take decades and perhaps centuries to play out, particularly in

the poorer parts of the world. Even in the U.S., Japan, and Europe,

most people continue to find physical notes an indispensable way

of making some types of payments. Because they are almost always

issued by governments or small non-profits, physical notes are far

behind the technological frontier. Consider, for example, the lawsuit

regarding the unsuitability of Federal Reserve Notes for the visually

impaired (http://www.dcd.uscourts.gov/opinions/2006/2002-CV-

0864~12:3:41~12-1-2006-a.pdf). A private, for-profit issuer would

have tremendous incentives to bring their physical bearer obliga-

tions to the bleeding edge.

The micro-finance revolution is a great first step toward breaking

the cycle of political violence, oppression, and predation that rel-

egates billions of human beings to lives of desperate poverty. But

the world’s poor face other risks as well. The entrepreneurial poor

also need liquid, safe, and reliable savings instruments, the value of

which are free of local political and economic disturbances. An idea

born of centuries of experience with bank note issuance and money

market mutual funds, B3MS could emerge as just such instruments.

Alone, they are no panacea to widespread poverty, but combined

with micro-finance and micro-insurance, bottom of the pyramid

strategies [Prahaland (2006)], and other ‘ground up’ initiatives

[Easterly (2006)], they could become an important component of

the risk management strategies of the world’s poorest and most

vulnerable entrepreneurs.

references• Aghion, B., and J. Morduch, 2005, The economics of microfinance, MIT Press,

Cambridge, MA

• Allison, T. E. 1998, “Testimony of Theodore E. Allison: overall impact of euro ban-

knotes on the demand for U.S. currency,” Before the Subcommittee on Domestic and

International Monetary Policy, Committee on Banking and Financial Services, U.S. House

of Representatives, October 8

• Allison, T. E., and R. S. Pianalto, 1997, “The issuance of series-1996 $100 Federal

Reserve notes: goals, strategy, and likely results,” Federal Reserve Bulletin, July

• Baumol, W. J., R. E. Litan, and C. J. Schramm, 2007, Good capitalism, bad capitalism and

the economics of growth and prosperity, Yale University Press, New Haven

• Bodenhorn, H., 2000, A history of banking in Antebellum America: financial markets and

economic development in an era of nation-building, Cambridge University Press, New

York

• Bodenhorn, H., 2003, State banking in early America: a new economic history, Oxford

University Press, New York

• Checkland, S. G., 1975, Scottish banking: a history, 1695-1973, Collins, Glasgow

• Chinn, M., and J. Frankel, 1994, “Patterns in exchange rate forecasts for twenty-five cur-

rencies,” Journal of Money, Credit and Banking, 26:4, 759-70

• Collins, S., and P. Mack, 1994, “Avoiding runs in money market mutual funds: have regu-

latory reforms reduced the potential for a crash?” Finance and Economics Discussion

Series, Board of Governors of the Federal Reserve System, No 94-14

• De Soto, H., 2000, The mystery of capital: why capitalism triumphs in the west and fails

everywhere else, Basic Books, New York

• Diamond, D., and P. Dybvig, 1983, “Bank runs, deposit insurance, and liquidity,” Journal

of Political Economy. 91:3, 401-419

• Eaker, M., and J. Right, 2006, “Exchange-traded funds,” Working Paper

• Easterly, W., 2006, The white man’s burden: why the west’s efforts to aid the rest have

done so much ill and so little good, Penguin Press, New York

• Jacklin, C., and S. Bhattacharya, 1988, “Distinguishing panics and information-based

bank runs: welfare and policy implications,” Journal of Political Economy, 96:3, 568-592

• Khandker, S., 1998, Fighting poverty with microcredit: experience in Bangladesh, Oxford

University Press, New York

• Lambert, M., and K. Stanton, 2001, “Opportunities and challenges of the U.S. dollar as an

increasingly global currency: a Federal Reserve perspective,” Federal Reserve Bulletin,

September

• Macey, J., and G. Miller, 1992, “Nondeposit deposits and the future of bank regulation,”

Michigan Law Review, 91, 237-273

• Mijuk, G., 2007, “Insurers tap world’s poor as new clients,” Wall Street Journal, July 11,

B4A

• Murphy, S., 2005, “Security in an uncertain world: life insurance and the emergence of

modern America,” Ph.D. dissertation, University of Virginia, 2005

• Obaidullah, M., 2004, Islamic financial markets: toward greater ethics and efficiency,

Genuine Publications & Media Pvt. Ltd., Delhi

• Palley, T., 2002, “The E-money revolution: challenges and implications for monetary

policy,” Journal of Post-Keynesian Economics, 24:2, 217-33.

• Perkins, E., 1994, American public finance and financial services, 1700-1815, Ohio State

University Press, Columbus

• Prahalad, C. K., 2006, The fortune at the bottom of the pyramid: eradicating poverty

through profits, Wharton School Publishing, Philadelphia

• Roe, M., 1991, “Political elements in the creation of a mutual fund industry,” University

of Pennsylvania Law Review, 39:6, 1469-1511

• Shleifer, A., and R. Vishny, 1998, The grabbing hand: government pathologies and their

cures, Harvard University Press, Cambridge, MA

• Slater, J., and M. M. Phillips, 2007, “Will weakness in dollar bust some couples?

Currency divorces loom as nations may move to head off inflation.” Wall Street Journal,

May 22, C1

• Stiglitz, J., 2002, Globalization and its discontents, W. W. Norton, New York

• Vietor, R. H. K., 2007, How countries compete: strategy, structure, and government in

the global economy, Harvard Business School Press, Boston

• Vogel, F., and S. Hayes, 1998, Islamic law and finance: religion, risk, and return, Kluwer

International, Boston

• White, E., 1995, “Deposit Insurance,” Working Paper

• Wright, R. E., 2008, “How to incentivise the financial system,” Central Banking, 19:2, 65-68

• Yunus, M., and A. Jolis, 1998, Banker to the poor: micro-lending and the battle against

world poverty, Public Affairs, New York

14 – The journal of financial transformation

15

financial risk and political risk in mature and emerging financial marketsWenjiang Jiang, Professor, School of Mathematical Sciences, Yunnan Normal University, China

Zhenyu Wu, Associate Professor, Edwards School of Business, University of Saskatchewan, Canada

While the importance of managing financial risk in industrialized

countries has been realized for many years, financial integration

brings fresh attention to the risk management issues in emerging

financial markets. Since the first era of globalization, emerging mar-

kets have been playing increasingly important roles in the global

economy. As the pace of international investments in emerging

markets increases, the effects of policy change and political risk

on asset prices become more critical to international investors.

Consequently, this subject has attracted increasing attention in

recent years, and one of the typical examples is the impact of gov-

ernment policies on the Chinese financial markets.

Furthermore, the increasing popularity of globalization has made

interactions among international financial markets more significant.

For example, the collapse of prices on NASDAQ in 2000 impacted

major financial markets in various countries. Thus, investigating the

price behaviors of financial securities in a financial market affected

by the changes in others is also of interest.

It is widely believed that developing a model which is sufficiently

robust for measuring risk in both mature and emerging financial

markets is of importance for both academic researchers and prac-

titioners. Jiang et al. (2008) propose a time-series model (JWC

model hereafter), which outperforms traditional GARCH (general-

ized autoregressive conditionally heteroskedastic) models. This is

mainly because the JWC model relaxes some assumptions made

in GARCH models and allows more flexibility to characterize price

behaviors, which enables risk to be measured more accurately.

In this article, we investigate the validity and robustness of the

JWC model in financial markets at different stages of development.

After demonstrating the effects of the falling prices on NASDAQ in

2000 on major U.S. markets, we illustrate the influences of policy

changes in China on behaviors of market indices. Therefore, results

presented in this study do not only add to the academic literature

on risk management, but also provide important implications for

policy makers and international investors.

Parameter estimation To measure risk and to characterize price behaviors in financial

markets, Jiang et al. (2008) develop a time-series model based

on quantile distributions. The JWC model outperforms traditional

GARCH models mainly because of the advantages of quantile distri-

butions, which take into account multiple features of risk, such as

location, scalar, tail order, and tail balance, and provide flexibility

for risk measurement [Jiang (2000), Deng and Jiang (2004), Jiang

et al. (2008)].

According to the JWC model, Xt ≡ log P(t)/P(t-1) = δ1/αt log Utβt/

(1 - Utβt)(1/αt) + μ (1)

where αt = ƒ(Xt-1,···, Xt-p, αt-1,···, αt-q) (2)

and βt = g(Xt-1,···, Xt-r, βt-1,···, βt-s) (3)

X(t) denotes the log return of a security in day t, P(t) is the adjusted

close price on that day, α is the tail order which determines the

volatility of the security price, β is the tail balance adjuster which

indicates the probability of making profit, μ describes the location,

and δ measures the scaling. To measure risk based on historical

price behaviors observed, the classic maximum likelihood estima-

tion (MLE) is adopted by Jiang et al. (2008), while we will use the

Q-Q estimation in the examples presented below.

As pointed out in Jiang (2000) and Jiang et al. (2008), the

quantile distribution has an explicit density function, which then

guarantees a closed-form likelihood function for the quantile

function-based JWC model. Therefore, the likelihood inference is

as straightforward as it is in the classic GARCH models presented

in the extant research, and some initial values, such as α0 and β0,

need to be predetermined when the JWC model is applied. The

strategy chosen by Jiang et al. (2008) for getting these initial

values is to choose a relatively stable period, view the time series

as if they are an i.i.d. sequence from the probability law of quantile

distribution, and then estimate the parameter values. While the

MLE is generally adopted for estimating parameter values, the

existence of an explicit quantile function in the JWC model allows

us to use a more robust estimation method, the Q-Q estimation

first proposed by Jiang (2000). This method is a simulation-

based estimation scheme, and it provides reliable estimation in

the presence of a closed-form quantile function in the theoretical

distribution. Technically, the Q-Q method is solely based on the

advantages of the quantile models, and is a mechanism directly

matching quantile functions of theoretical and empirical distribu-

tions by searching the set of parameters that minimize the ‘dis-

tance’ between them.

Suppose that a distribution class F(x; θ), θ∈Θ is parameterized

by the vector θ. A member of F(x; θ) with unknown θ generates a

series of observations Y1, Y2, ···, Yn. We also assume that F(x; θ) can

be simulated for any given θ. The Q-Q estimation method infers θ

from Y1, Y2,···, Yn by solving the optimization problem minθ∈Θ

ƒ[R1(Y), ···, Rl(Y); θ, T1(X),···, Tl(X)] (4), where f(·) is an appropriate

score function, with the most common choice being the L1 or L2

norm. X≡(X1,···, Xm) is simply a set of simulated sample of F(x; θ)

for a given θ, Fm (·, X) denotes the empirical distribution function

based on X, and (q1, q2,···, ql) denotes the set of probabilities for

which the quantiles are obtained. R1(Y),···, Rl(Y) and T1(X(θ)), ···,

1 We also estimate the parameter values from May 23, 2000 to December 20, 2002.

Due to space limitations, however, we only present those from December 30, 1999 to

May 22, 2000. 16 – The journal of financial transformation

Tl(X(θ)), are empirical quantiles of Y=(Y1,···, Yn) and X=(X1,···, Xm),

respectively, where Ri(Y) = Fn-1(pi;Y) and Tj(X) = Fm

-1 (pj;X).

The reason for using quantiles to construct the score function is

that empirical quantiles are robust estimators of the theoretical

ones. Consequently, the Q-Q method is expected to yield reli-

able estimators, and it is confirmed by our experimental testing

on some common distributions. For quantile modeling, since the

theoretical quantiles are explicitly specified as q(u; θ), the optimi-

zation problem (4) can be rewritten as: minθ∈Θ ƒ[R1(Y), ···, Rl(Y);

q(p1; θ),···, q(pl; θ)] (5)

Jiang (2000) uses sample forms of f(·) such as minθ∈Θ ∑i=1→l

wi|Ri(Y) – F-1(Pi)|, and minθ∈Θ ∑i=1→l wi[Ri(Y) – F-1(Pi)]2, where wl,···,

wl are properly chosen weights.

financial risk: evidence from the U.s. marketsWith increasing globalization interactions among financial markets

within a country and among different countries have been attract-

ing more attention. Investing in international financial markets is

an effective way of diversifying risk [Erb et al. (1996)]. A typical

example is the fall of the NASDAQ market in 2000 and its effects

on the other major financial markets in the U.S.

The observations presented in Figures 1 and 2 are based on S&P500

and Dow Jones Industrial Average indices within the period of 100

trading days from December 30, 1999 to May 22, 20001. We follow

Jiang et al. (2008), and use the information from January 5, 1998

to December 29, 1999 and JWC(1,1,1,1) to estimate the initial values

of parameters θ0=(a0, a1, b1, c0, c1, d1, δ, μ). The estimated results

show that the average δt of the Dow Jones Industrial Average index

over the observation period with 100 trading days was 0.001, while

that of the S&P500 index was 0.005. The average μt of the Dow

Jones Industrial Average index over that period was 0.007, while

that of the S&P500 index was -0.011.

Figure 1 illustrates the indices, log returns, and αt and βt series of

the Dow Jones Industrial Average index within this period, while

Figure 2 illustrates those of the S&P500 index during the same

period. According to these two figures, we find that the risk carried

by αt of the S&P500 index was not as stable as that of the Dow

Jones Industrial Average index. In addition, at the time of the fall

of the NASDAQ index, the profile of βt of the S&P500 index showed

a more dramatic change than that of the Dow Jones Industrial

Average index. In other words, at that time, S&P500 was a better

candidate of short-term investment than the Dow Jones Industrial

Average index was. One of the possible reasons is that the Dow

Jones Industrial Average index consists of 30 of the largest and

most widely held public companies in the U.S., and the effects of

the NASDAQ collapse on these companies were not as significant

as those included in the S&P500 index.

Political risk: evidence from the chinese marketsPioneering studies [such as Ekern (1971), Aliber (1975), Bunn and

Mustafaoglu (1978), and Dooley and Isard (1980)] have considered

political risk as one of the most important factors in the field of

international investments. As globalization has become more popu-

lar, the literature on political risk has been significantly enriched,

with the typical research focusing on international asset markets

[Stockman and Dellas (1986), Gemmill (1992), Bailey and Chung

(1995), Perotti and van Oijen (2001), Kim and Mei (2001)], corporate

governance in international investments [Phillips-Patrick (1989a,

b), Ellstrand et al. (2002), Keillor et al. (2005), and foreign direct

investments [Ma et al. (2003), Mudambi and Navarra (2003), Busse

and Khefeker (2007)].

Recently, factors in emerging markets have attracted increas-Figure 1 – Behavior of the Dow Jones Industrial Average Index, from January 5, 1998

to December 20, 2002

Figure 2 – Behavior of the S&P 500 Index, from January 5, 1998 to December 20, 2002

3500

3000

25000 20 40 60 80 100

Stock prices

0.1

0

-0.10 20 40 60 80 100

Log returns

1.37

1.36

1.350 20 40 60 80 100

Estimated αt profile

10

5

00 20 40 60 80 100

Estimated βt profile

ˆ

ˆ

6

4

2

0

155015001450140013501300

1.1991.1981.1971.1961.1951.194

0.1

0.05

0

-0.05

-0.1

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

Estimated βt profile

Estimated αt profile

Log returns

Stock prices

ˆ

ˆ

172 We also estimate the parameter values from September 6, 2001 to December 31,

2002. Due to space limitations, however, we only present those from April 12 to

September 5, 2001.

ing attention from financial researchers and practitioners.

Representatives of the relevant studies on political risk in emerg-

ing markets include Bailey and Chung (1995), Diamonte et al. (1996),

Clark and Tunaru, (2001), Perotti and van Oijen (2001), Bilson et al.

(2002), and Harms (2002). As claimed by Erb et al. (1996), political

risk is one of the four dimensions of the risk considered in global

investments.

In recent years, the Chinese market has been widely acknowledged

to be one of the most influential emerging markets in the world, and

therefore investigating the impacts of political risk and government

policies on asset market behaviors in China is very important. In this

section, we present the impacts of reducing state-owned shares in

2001 on indices of Shanghai Stock Exchange (SSE) and Shenzhen

Stock Exchange (SZSE) during the period of 100 trading days from

April 12, 2001 to September 5, 20012 as shown in Figures 3 and 4.

The two indices in Chinese stock markets are Shanghai Composite

Index and Shenzhen Composite Index, respectively. Estimating

parameters θ0=(a0, a1, b1, c0, c1, d1, δ, μ) using the information from

June 26, 2000 to April 11, 2001 and JWC(1,1,1,1), we find that the

average δt of the Shanghai Composite index over the observation

period was 0.013, while that of the Shenzhen Composite index was

0.002. The average μt of the Shanghai Composite index over that

period was 0.004, while that of the Shenzhen Composite index was

0.007.

Figure 3 illustrates the indices, log returns, and αt and βt series of

the Shanghai Composite index within the observation period with

100 trading days, and Figure 4 illustrates those of the Shenzhen

Composite index during that period. The Figures show that after the

policy of reducing state-owned shares was in effect, both indices

dropped significantly and consistently. According to the profiles of

αt and βt over the observation period illustrated, the risk carried by

αt of the Shenzhen Composite index after the policy was changed

was much more dramatic than that of the Shanghai Composite

index. As shown by the βt profiles of these two indices, in the

meantime, the Shenzhen Composite index was a better candidate

for short-term investments than the Shanghai Composite Index

after the policy was in effect. This may be caused by the fact that

most of the companies on the Shenzhen Stock Exchange are rela-

tively small- and medium-sized, while those on the Shanghai Stock

Exchange are relatively large. In other words, political risk has been

shown to have more significant effects on small- and medium-sized

companies.

conclusionWith the increasing global financial integration, international invest-

ments become more important. Consequently, measuring risk in the

various types of markets accurately plays a crucial role in modern

financial management. This study focuses on the application of the

newly-proposed JWC time-series model for measuring risk in both

mature and emerging markets, and shows that the JWC model is

valid and robust for financial markets at different stages of devel-

opment. Illustrating the effects of the fall in the NASDAQ market on

the U.S. financial markets and the influences of policy changes on

the Chinese markets, respectively, we address the financial risk in

mature markets and political risk in emerging markets. Behaviors

of four major market indices, the Dow Jones Industrial Average,

the S&P 500, Shanghai Composite Index, and Shenzhen Composite

Index, are used to highlight these effects. The Q-Q estimation meth-

od is adopted to implement the JWC model. We believe that this

study not only provides a parameter estimation method for mea-

suring risk accurately in financial markets, but it also has important

policy applications in international investments and financial fore-

casting. Further studies, such as portfolio optimization and asset

allocation based on the JWC model, will also be of interest.

Figure 3 – Behavior of Shanghai Composite Index, from June 26, 2000 to December

31, 2002

Figure 4 – Behavior of Shenzhen Composite Index, from June 26, 2000 to December

31, 2002

6

4

2

0

0.7685

0.768

0.7675

0.767

1.167

5.1985

5.1986

5.1987

5000

4500

4000

3500

155015001450140013501300

0.1

0.05

0

-0.05

-0.1

0.040.02

0-0.02-0.04-0.06

6

5

4

3

2

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

Estimated βt profile

Estimated βt profile

Estimated αt profile

Estimated αt profile

Log returns

Log returns

Stock prices

Stock prices

ˆ

ˆ

ˆ

ˆ

18 – The journal of financial transformation

references• Aliber, R. Z., 1975, “Exchange risk, political risk, and investor demand for external cur-

rency deposits,” Journal of Money, Credit & Banking, 7, 161-179

• Bailey, W., and Y. Peter Chung, 1995, “Exchange rate fluctuations, political risk, and

stock returns: some evidence from an emerging market,” Journal of Financial &

Quantitative Analysis, 30, 541-561

• Bilson, C. M., T. J. Brailsford, and V. C. Hooper, 2002, “The explanatory power of politi-

cal risk in emerging markets,” International Review of Financial Analysis, 11, 1-27

• Bunn, D.W. and M. M. Mustafaoglu, 1978, "Forecasting political risk,” Management

Science, 24, 1557-1567

• Busse, M., and C. Khfeker, 2007, “Political risk and the internationalization of firms: an

empirical study of Canadian-based export and FDI firms,” European Journal of Political

Economy 23, 397-415

• Clark, E., and R. Tunaru, 2001, "Emerging markets: investing with political risk,”

Multinational Finance Journal, 5, 155-175

• Deng, S. J. and W. J. Jiang, 2004, “Quantile-based probabilistic models with an applica-

tion in modelling electricity prices,” in Modelling prices in competitive electricity mar-

kets, Bunn, D., (ed), John Wiley & Sons, Inc.

• Diamonte, R. L., J. M. Liew, and R. J. Stevens, 1996, "Political risk in emerging and

developed markets,” Financial Analysts Journal, 52, 71-76

• Dooley, M. P., and P. Isard, 1980, “Capital controls, political risk, and deviations from

interest-rate parity,” Journal of Political Economy, 88, 370-384

• Ekern, S., 1971, “Taxation, political risk and portfolio selection,” Economica, 38, 421-430

• Ellstrand, A. E., L. Tihanyi, and J. L. Johnson, 2002, "Board structure and international

political risk,” Academy of Management Journal, 45, 769-777

• Erb, C. B., C. R. Harvey, and T. E. Viskanta, 1996, "Political risk, economic risk, and

financial risk,” Financial Analysts Journal, 52, 29-46

• Gemmill, G., 1992, “Political risk and market efficiency: tests based in British stock and

options markets in the 1987 election,” Journal of Banking & Finance, 16, 211-231

• Harms, P., 2002, “Political risk and equity investment in developing countries,” Applied

Economics Letters 9, 377-380

• Jiang, W., 2000, “Some simulation-based models towards mathematical finance," Ph.D.

Dissertation, University of Aarhus

• Jiang, W., Z. Wu, and G. Chen, 2008, “A new quantile function based model for model-

ing price behaviors in financial markets,” Statistics and Its Interface, forthcoming

• Keillor, B. D., T. J. Wilkinson, and D. Owens, 2005, “Threats to international operations:

dealing with political risk at the firm level,” Journal of Business Research 58, 629-635

• Kim, H. Y., and J. P. Mei, 2001, "What makes the stock market jump? An analysis of

political risk on Hong Kong stock returns,” Journal of International Money & Finance,

20, 1003-1016

• Ma, Y., H-L. Sun, and A. P. Tang, 2003, "The stock return effect of political risk event

on foreign joint ventures: evidence from the Tiananmen Square incident,” Global

Finance Journal, 14, 49-64

• Mudambi, R., and P. Navarra, 2003, “Political tradition, political risk and foreign direct

investment in Italy,” Management International Review, 43, 247-265

• Perotti, E. C., and P. van Oijen, 2001, "Privatization, political risk and stock market

development in emerging economies,” Journal of International Money & Finance, 20,

43-69

• Phillips-Patrick, F. J., 1989a, “Political risk and organizational form,” Journal of Law &

Economics, 34, 675-693

• Phillips-Patrick, F. J., 1989b, “The effect of asset and ownership structure on political

risk,” Journal of Banking & Finance, 13, 651-671

• Stockman, A. C., and H. Dellas, 1986, “Asset markets, tariffs, and political risk,” Journal

of International Economics, 21, 199-213

191 The work of David Hand described here was partially supported by a Royal Society

Wolfson Research Merit Award. This work was part of the ThinkCrime project on

Statistical and machine learning tools for plastic card and other personal fraud detec-

tion, funded by the EPSRC under grant number EP/C532589/1.

Part 1

Estimating the iceberg: how much fraud is there in the U.K.?

AbstractMeasuring the amount of fraud is a particularly intractable estima-

tion problem. Difficulties arise from basic definitions, from the fact

that fraud is illicit and deliberately concealed, and from its dynamic

and reactive nature. No wonder, then, that estimates of fraud in the

U.K. vary by an order of magnitude. In this paper, we look at these

problems, assess the quality of various figures which have been

published, examine what data sources are available, and consider

proposals for improving the estimates.

David J. HandProfessor of Statistics, Department of Mathematics,

Imperial College, and Institute for Mathematical Sciences, Imperial College1

Gordon BluntDirector, Gordon Blunt Analytics Ltd

Newspapers and other media frequently carry stories about fraud.

Often these are about specific cases, but sometimes they are general

articles, either about particular kinds of fraud (i.e., benefits fraud,

credit card fraud, tax fraud, insurance fraud, procurement fraud),

or about the extent of fraud. While communications media have

the nominal aim of keeping us informed, it is well known that this

reporting is not without its biases. There is, for example, the familiar

tendency to report news preferentially if it is bad. In the context

of fraud this has several consequences. It means that many news

stories have frightening or threatening overtones: the risk of falling

victim of identity theft, the discovery that a batch of medicines or car

parts are fake, the funding of terrorist activities from low level credit

card fraud, and so on. It also means that there may be a tendency

for numbers to be inflated. A report that 10% of drugs on the market

are counterfeit is much more worrying, and likely to receive wider

circulation than one reporting only 0.1%. To steal an old economics

adage, we might say that there is a tendency for bad numbers to

drive out good. This paper is about the difficulty of obtaining accu-

rate estimates for the amount of fraud in the U.K.

Reporting bias is just one of the difficulties. Others, which we dis-

cuss in more detail below, include:

n The definition of fraud — statisticians know only too well the

problems arising from imprecise, ambiguous, or differing defini-

tions. In the case of fraud it is not simply that insufficient care

has been taken in defining what is meant by ‘fraud,’ it is also that

in some situations people may disagree on whether an activity is

fraudulent or legitimate. For example, some people might regard

certain ‘complementary medicines’ as legitimate, while others

might regard them as fraudulent. Moreover, an activity may or

may not be fraud depending on the context in which it is carried

out. And even in apparently straightforward cases there can be

ambiguity about costs. For example, if goods are obtained by

fraudulent means, should the loss be the cost of producing the

goods, the price they would be sold for, the retail value, or the

wholesale value, and should VAT be included?

n The fact that some, possibly much, fraud, goes unreported —

this particular problem is the one we have chosen to highlight in

the title. Missing data and nonresponse are, of course, problems

with which statisticians have considerable familiarity.

n In an increasingly complex society, there are increasing

opportunities for fraud — our ancestors did not have to worry

about credit card fraud, ATM theft, insurance scams, and certain-

ly not about more exotic activities such as phishing, pharming, or

419 fraud. Such frauds ride on the back of technologies designed

to make things more convenient, and generally to provide us with

richer opportunities, but which can be corrupted for dishonest or

unethical use. As the Office of Fair Trading survey of mass mar-

keted scams [OFT (2006)] put it: “Mass marketed consumer fraud

is a feature of the new globalized economy. It is a huge problem:

international in scope, its reach and organization.”

n fraud prevention tools themselves represent an advancing

technology [Bolton and Hand (2002), Weston et al. (2008),

Juszczak et al. (2008), Whitrow et al. (2008)] — but fraudsters

and law enforcement agencies leapfrog over each other: fraud

is a reactive phenomenon, with fraudsters responding to law

enforcement activity, as well as the other way round. This means

that the fraud environment is in a state of constant flux which

in turn means that any estimates of the size of the problem are

likely to be out of date by the time they are published.

n Difficulty in measuring the complete cost of fraud — although

this paper is concerned with the amount of fraud, and it measures

this in monetary terms, it almost certainly does not measure the

complete costs attributable to fraud. For example, the need to

deter fraud by developing detection and prevention systems and

employing police and regulators involves a cost, and there is a

cost of pursuing fraudsters through the courts. Moreover, there

is a hidden loss arising from the deterrent effect that awareness

of fraud causes on trade — for example, an unwillingness to use a

credit card on the Internet. This is one reason why, for example,

banks may not advertise the amount of fraud that they suffer.

Unfortunately, this understandable unwillingness to divulge or

publicize fraud further complicates efforts to estimate its extent.

n There are also many types of fraud for which estimating or

even defining the cost in monetary terms is extremely dif-

ficult — for example, a student who cheats in an examination or

plagiarizes some coursework may unjustifiably take a job. There