jeffrey l. chastain - jefferies · jeffrey l. chastain ... fleet strategy, growth into new market...

TRANSCRIPT

Jefferies 2015 Energy ConferenceNovember 12, 2015

Jeffrey L. ChastainVice President Investor Relations and Corporate Communications

2

Forward Looking Statement

This presentation contains “forward‐looking statements” about Noble’s business, financialperformance, contracts and prospects. Statements regarding contract backlog, costs,benefits, opportunities, financial performance, anticipated timing and cost of newbuildrigs, fleet strategy, growth into new market segments, bidding activity, rig demand,contract commencements, dayrates, impact of future regulations, contract duration, fleetcondition, capabilities or performance, industry fundamentals, shareholder value, timingor number of share repurchases, as well as any other statements that are not historicalfacts in this release, are forward‐looking statements that involve certain risks,uncertainties and assumptions. These include but are not limited to actions by regulatoryauthorities or other third parties, market conditions, financial results and performance,ability to repay debt and timing thereof, actions by customers and other third parties,factors affecting the level of activity in the oil and gas industry, supply and demand ofdrilling rigs, factors affecting the duration of contracts, the actual amount of downtime,factors that reduce applicable dayrates, violations of anti‐corruption laws, hurricanes andother weather conditions, delays, costs and difficulties related to the construction ofnewbuild rigs, the future price of oil and gas and other factors detailed in the Company’smost recent Form 10‐K, Form 10‐Q’s and other filings with the Securities and ExchangeCommission. Should one or more of these risks or uncertainties materialize, or shouldunderlying assumptions prove incorrect, actual results may vary materially from thoseindicated. The Company disclaims any duty to update the information presented here.

3

Best Positioned Offshore Driller

Premium Fleet

Strong Operations Execution

Solid Balance Sheet and Liquidity

Sustainable Cash Allocation Strategy

Managing Cyclical Weakness

Company Overview

9 Drillships 8 UDW, DP 8 added to fleet since 2011

4

8 Semisubmersibles 3 UDW, DP 5 conv. moored, UDW, DW

15 Jackups 6 added since 2012 3 added since 2007 1 under construction

Average Fleet Age – 11 years

Source: Noble as of November 2015

Current Status:Contracted: 9 6 14Idle: 0 1 1Stacked: 0 1 0

Source: Noble as of November 2015

Company OverviewGlobal Drilling Presence with Established Deep and Shallow Water Experience

5

Global Fleet CompositionCorporate Headquarters - UK

U.S. Operations

46

3

1

18

1

1 1

1 1

1

11

1

Company OverviewRevenues Diversified by Region and Rig Type

6Source: Noble as of September 30, 2015

Revenues by Rig Type

YTD September 30, 2015Total Revenues

$2.5 Billion

Revenues by Region

7

54%

31%

15%

1. Shell

2. Freeport-McMoRan

3. Saudi Aramco

4. Anadarko

Revenue Split by Customer

Top Customers

Source: Noble as of September 30, 2015

Company OverviewDiverse Base of Quality Customers

YTD September 30, 2015

Strong Operations Execution

8

Strong Operations ExecutionReduction in Fleet Downtime

9

10.5%

7.4%

3.9%4.4% 4.6%

3.0%

5.0%

7.0%

9.0%

11.0%

Percent of Total Downtime per Quarter

Strong Operations ExecutionSuccessful Cost Management Efforts

10

$139.4

$135.2

$121.3 $116.9

$106.7

$117.8

$100

$110

$120

$130

$140

$150

Drivers

Reduction in: Labor Costs Idle Rig Costs Operations Support

Costs Insurance Costs

$112.3 -

Contract Drilling Costs Per Available Day($ Thousands)

Strong Operations ExecutionMargin Preservation

11

52.4%

50.4%

58.7% 58.6% 58.9%

45.0%

50.0%

55.0%

60.0%

65.0%

Contract Drilling Margin per Quarter

(1)

(1) Adjusted for Noble Homer Ferrington arbitration award

Strong Operations Execution

12

Two Important Keys Driving Improved Operations Execution:

Noble NEXT Center

Long-Term Focus onSubsea Operations

Solid Balance Sheet and Liquidity

13

37%

40% 40% 40%

37% 37%

35%

36%

37%

38%

39%

40%

41%

14

($ Millions)

Solid Balance Sheet and Liquidity

Target Range 35% to 40%

Debt/Total CapitalizationManageable Debt Maturities

Solid Balance Sheet and Liquidity

15

$2.0

$1.8

$2.7

$2.9$2.8

$3.0

$1.5

$2.0

$2.5

$3.0

Liquidity Improvement Supported by Strong Operations

($ Billions)

Liquidity Components:Cash (@ 9/30/15) $165

5-year RCF $2,445(1)

1-year RCF $225(2)

(1) Matures January 2020(2) Matures January 2016

Sustainable Cash Allocation Strategy

16

Positive FCF and Sustainable Cash Allocation Strategy

Dividend

Share Repurchase

Debt Retirement

Premium Fleet Expansion

17

Managing Cyclical Weakness

18

19

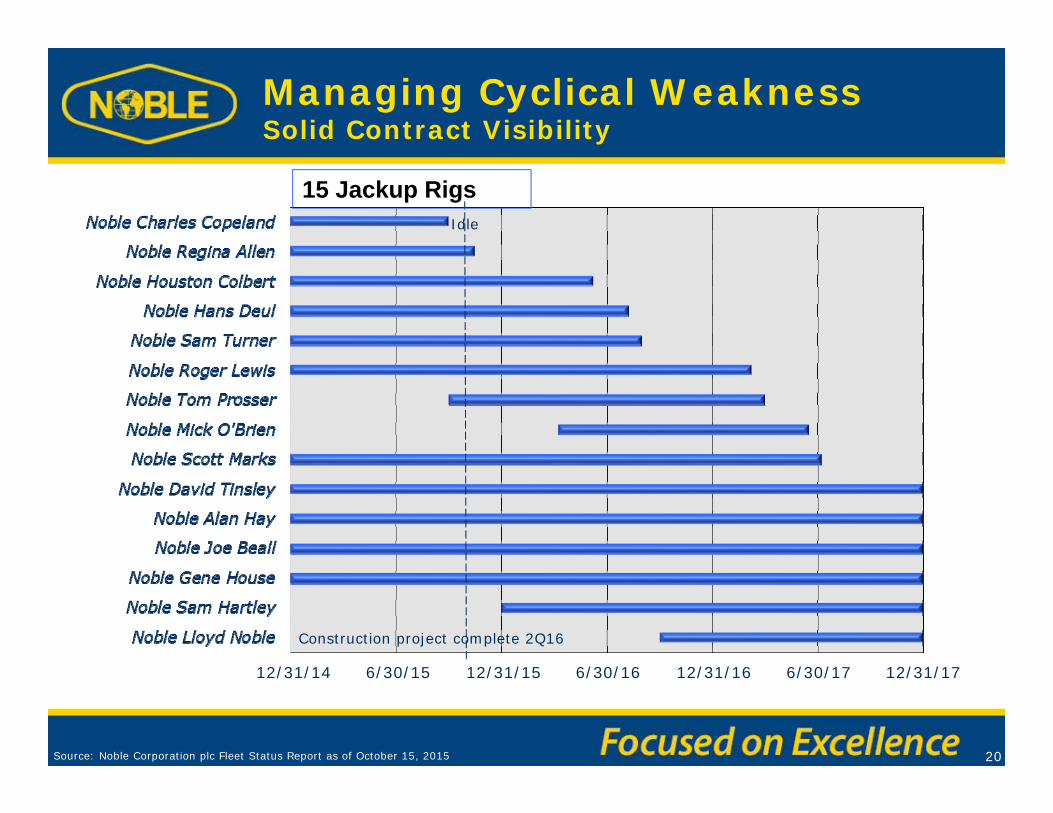

Managing Cyclical WeaknessSolid Contract Visibility

• 8 rigs contracted into 2017 or later, including 3 rigs contracted beyond 2020

12/31/176/30/176/30/15 12/31/15 6/30/16 12/31/1612/31/14

Cold stacked

Idle

17 Floating Rigs

Source: Noble Corporation plc Fleet Status Report as of October 15, 2015

20

Managing Cyclical WeaknessSolid Contract Visibility

12/31/176/30/176/30/15 12/31/15 6/30/16 12/31/1612/31/14

Construction project complete 2Q16

15 Jackup Rigs

Source: Noble Corporation plc Fleet Status Report as of October 15, 2015

Idle

21

80% Committed

58% Committed

Jackup Rigs

2015

2016

74% Committed

76% Committed

Floating Rigs

2015

2016

Percentage of Available Operating Days

Source: Noble as of September 30, 2015

Managing Cyclical WeaknessSolid Contract Coverage

35% Committed

48% Committed

2017

2017

Managing Cyclical WeaknessBacklog Provides Excellent Visibility

22

$0.7

$2.5

$1.6

$1.0

$2.3

$0

$1

$2

$3

$4

20

15

20

16

20

17

20

18

20

19

-2

02

3

Shell60.4%

Freeport-McMoRan

11.2%

Saudi Aramco7.5%

Statoil7.9%

Anadarko3.7%

Other9.3%

Note: Backlog includes between 25-50% performance bonus realization on rigs with bonus provisions.

Estimated Annual Contribution Backlog by Client

Backlog at September 30, 2015: $8.1 Billion

Source: Noble

23

$2.1

$1.2

$2.1$1.9

$.450$.340

$0

$1

$2

$3

2011 2012 2013 2014 2015 2016

($ Billions)

3 3 22 4

Annual Capex(1)2011-2014 Avg. - $2.0 billion

(1) Totals prior to 2015 adjusted for spin-off of Paragon Offshore

Source: Noble

Managing Cyclical WeaknessDeclining Capex

(P)

$.585

3Q15 Guidance

Down $135mm

$.800

Newbuild CapexNoble Lloyd Noble

Delivery

(P)

Extending a 95-Year Legacy

Operational PerformanceFinancial DisciplinePosition for Advantage

24

Noble Corporation plcDevonshire House1 Mayfair PlaceLondon W1J 8AJEnglandwww.noblecorp.com

Investor contacts:Jeffrey L. Chastain Vice President Investor Relations281-276-6383

John S. BreedDirector Investor Relations281-276-6729

Enterprise Value (as of 11/9/15)Exchange ListingShares Outstanding (ex. Treasury Shares)52-Week Average Daily Trading Volume Debt Rating

$8.3hp billionNYSE: NE

241.9 million9.1 millionBBB/Baa3