issues in classificationestv.in/idtc/gstaudit/pdf/livewebcastonissuesin... · contracts for supply...

TRANSCRIPT

ISSUES IN CLASSIFICATION

By:A. Saiprasad

Advocate

Classification

Why is Classification Important?

How is Classification in GST different from erstwhile laws

Services – Whether classification was required before since single rate?

Services – Different Rates & SAC Code

Supplies of Goods treated as Services

Transfer of right to use goods/ right in goods

July 8, 2018 © Indirect Taxes Committee, ICAI 2

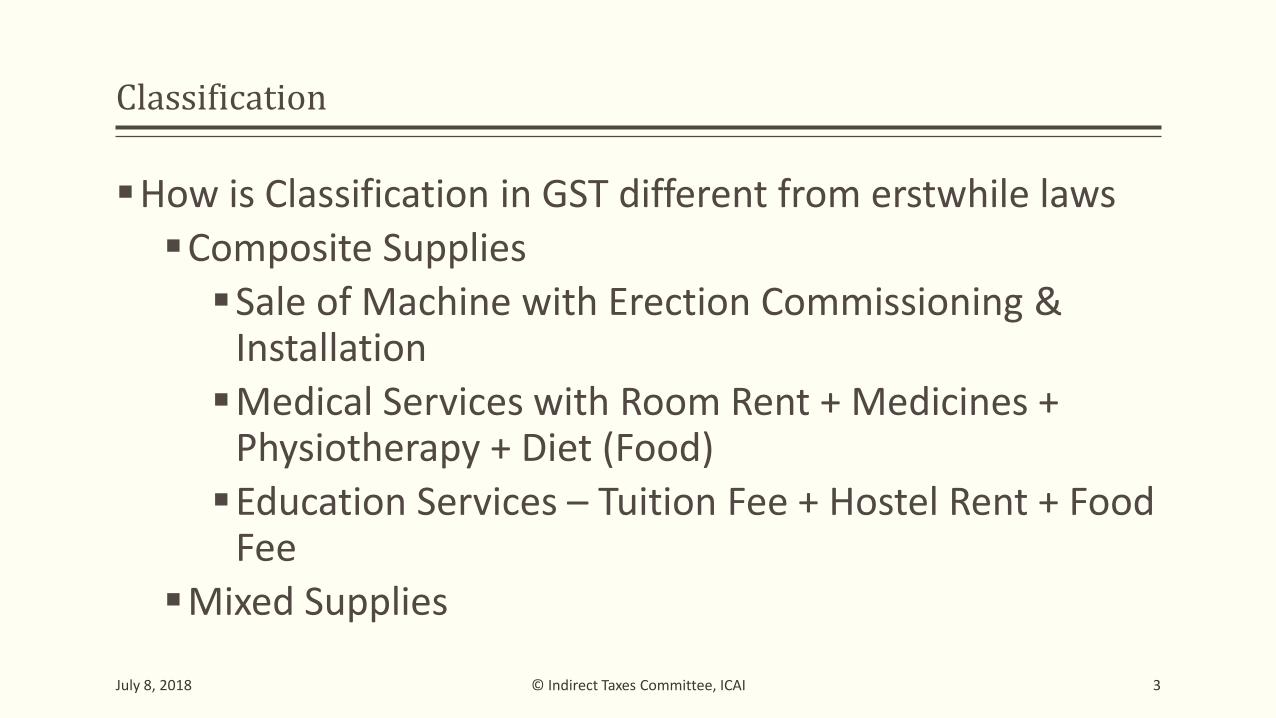

Classification

How is Classification in GST different from erstwhile laws

Composite Supplies

Sale of Machine with Erection Commissioning & Installation

Medical Services with Room Rent + Medicines + Physiotherapy + Diet (Food)

Education Services – Tuition Fee + Hostel Rent + Food Fee

Mixed Supplies

July 8, 2018 © Indirect Taxes Committee, ICAI 3

Classification

Understanding Nature of Transaction Important

Construction Service V. Works Contract Service

Commission Agent/ Commodity Broker Vs. Buyers and Sellers of the Commodity

Restaurant Service V. Outdoor Catering Service V. Convention Centre Service

Restaurant Service with tariff V. Restaurant Service without tariff

Availment of Credit

Convention Service – Food & Renting of HallJuly 8, 2018 © Indirect Taxes Committee, ICAI 4

Classification

Understanding Nature of Transaction Important

Printing - Where Content belongs to printer/ person other than printer

Books/ Annual Reports V. Envelopes, Tissues, Printed Boxes

Classification and Person Liable to Pay Tax

GTA – 5% Vs. 12%

Supply of Goods or Service?

Retreading of Tyres

Supply of Retreaded tyres where old tyres belong to Supplier

Bus Body Building on Chasis Received from Supplier

Manufacturing Service on physical inputs owned by others (SAC 9988) or

Supply of Bus (HSN 8707)

Whether value is the sole factor in determining type of supplyJuly 8, 2018 © Indirect Taxes Committee, ICAI

5

ISSUE - I

Issue: In Re: EMC Ltd., 2018 (13) GSTL (AAR - WB)

Contracts for supply of Tower Packages split up into two separate sets of contracts.

One for supply of materials at ex-factory price (First Contract), and

Other for supply of allied services (Second Contract)

Survey and erection of towers, testing and commissioning of transmission lines etc.,which also includes inland/local transportation, in-transit insurance, loading/unloadingfor delivery of materials and storage at the contractee’s site

Contractee agrees to pay GST, except on inland/local transportation, in-transit insurance andloading/unloading

Applicant raises separate freight bills on the Contractee.

Whether freight bills classificable as GTA Service?

© Indirect Taxes Committee, ICAI 6July 8, 2018

ISSUE - II

Issue: In Re: Rashmi Hospitality Services Private Limited

Applicant providing catering service to recipient who have statutory canteens

Catering service liable to tax @ 18%

Service recipient of Applicant seeking GST @ 5% based on C.B.E.C. Circular No. 28/02/2018-GST, dated 8-1-2018

Whether services classifiable under Sl. No.7(i) or 7(v) of N.No.11/17 CT (R)

© Indirect Taxes Committee, ICAI 7July 8, 2018

ISSUE - II

Indian Coffee Workers’ Co-op. Society Ltd. v. CCE & ST, Allahabad 2014 (34) S.T.R. 546 (All.)

C.B.E.C. Circular No. 28/02/2018-GST, dated 8-1-2018:

The educational institutions have mess facility for providing food to their students and staff.

Such facility is either run by the institution/students themselves or is outsourced to a third person.

Supply of food or drink provided by a mess or canteen is taxable at 5% without Input Tax Credit [Serial No. 7(i) of notification No. 11/2017-CT (Rate) as amended vide notification No. 46/2017-C.T. (Rate), dated 14-11-2017 refers].

It is immaterial whether the service is provided by the educational institution itself or the institution outsources the activity to an outside contractor.

© Indirect Taxes Committee, ICAI 8July 8, 2018

ISSUE - III

Issue: In Re: VPSSR Facilities, 2018 (13) GSTL 116 (AAR - Del)

Whether cleaning service provided to railways are classifiable under 9997 – Cleaning service or exempt under entry no. 3/ 3A of N.No.12/17 CT (R)?

Whether Cleaning is a pure service for the purpose of entry no.3 of N.No.12/17 CT (R)?

Whether Railways is CG for the purpose of entry no.3/ 3A of N.No.12/17 CT (R)?

Whether Cleaning service provided to railway is a function entrusted to municipality under Article 243 W of Constitution of India r/w XII Sch to the Constitution?

Section 3(8) of General Clauses Act, 1897 – CG means President

Sch XII - Public health, sanitation conservancy and solid waste management.

© Indirect Taxes Committee, ICAI 9July 8, 2018

ISSUE - IV

Issue: In Re: Switching Avo Electro Power Ltd., 2018 (13) GSTL 84 (AAR - WB)

Whether Supply of UPS along with Batteries is a Composite Supply or Mixed Supply?

UPS supplied with inbuilt battery

UPS and battery supplied separately Single Contract - Single Price/ Separate Prices in One Invoice

Separate Contracts - Separate Price

AAR holds – “Goods are naturally bundled in a supply contract if the contract is indivisible”. Reasoning squarely opposed to the text and illustration of Composite Supply

© Indirect Taxes Committee, ICAI 10July 8, 2018

ISSUE - IV

Note 3 to Section XVI of the Tariff Act

defines a Composite Machine as

Consisting of two or more machines fitted together to form a whole.

Such machines, as well as other machines designed for the purpose of performing two ormore complementary or alternative functions, are to be classified as if consisting only of thatcomponent or as being that machine, which performs the principal function

Rule 3(b) of General Interpretative Rules

© Indirect Taxes Committee, ICAI 11July 8, 2018

Rule 3(b) – Mixed Supply?

the material or component which gives them their essential character,

shall be classified as if they consisted of

which cannot be classified by reference to Rule 3 (a),

goods put up in sets for retail sale,

Mixtures, composite goods consisting of different materials or made up of different components, and

12© Indirect Taxes Committee, ICAIJuly 8, 2018

Rule 3(b) – Mixed Supply?

Meaning of ‘set of articles’ (SOA) More than one item, each complementing the other while retaining their individual

identity all the time

If a set consists of drawing instruments – 90.17, pencil – 96.09 and pencil sharpner –82.14, put up in a leather case – 42.01 – Classification?

Desktop Computer with CPU, Monitor & Keyboard (SOA) V. Laptop

Meaning of ‘Essential Character’ Software Loaded on a Computer – Classification S/w or Hardware?

Book with CD and Software with Manual – Classification?

Software loaded on a CD – Classification?

Mobile handset with additional features

Pen Stand fitted with clock/ Vehicle lock with alarm

13© Indirect Taxes Committee, ICAIJuly 8, 2018

ISSUE - V

Issue: In Re: Giriraj Renewables Private Limited

Whether EPC Contract of Solar Power Plant a Works Contract or a Composite Supply u/s 2(30)?

Whether principal supply i.e. solar generating system liable to 5% GST as per N.No.1/17?

Commissioner of Central Excise, Ahmedabad v. Solid and Correct Engineering Works [(2010) 5 SCC 122 = 2010 (252) E.L.T. 481

Meaning of Immovable Property

Whether it is supply of goods or service?

© Indirect Taxes Committee, ICAI 14July 8, 2018

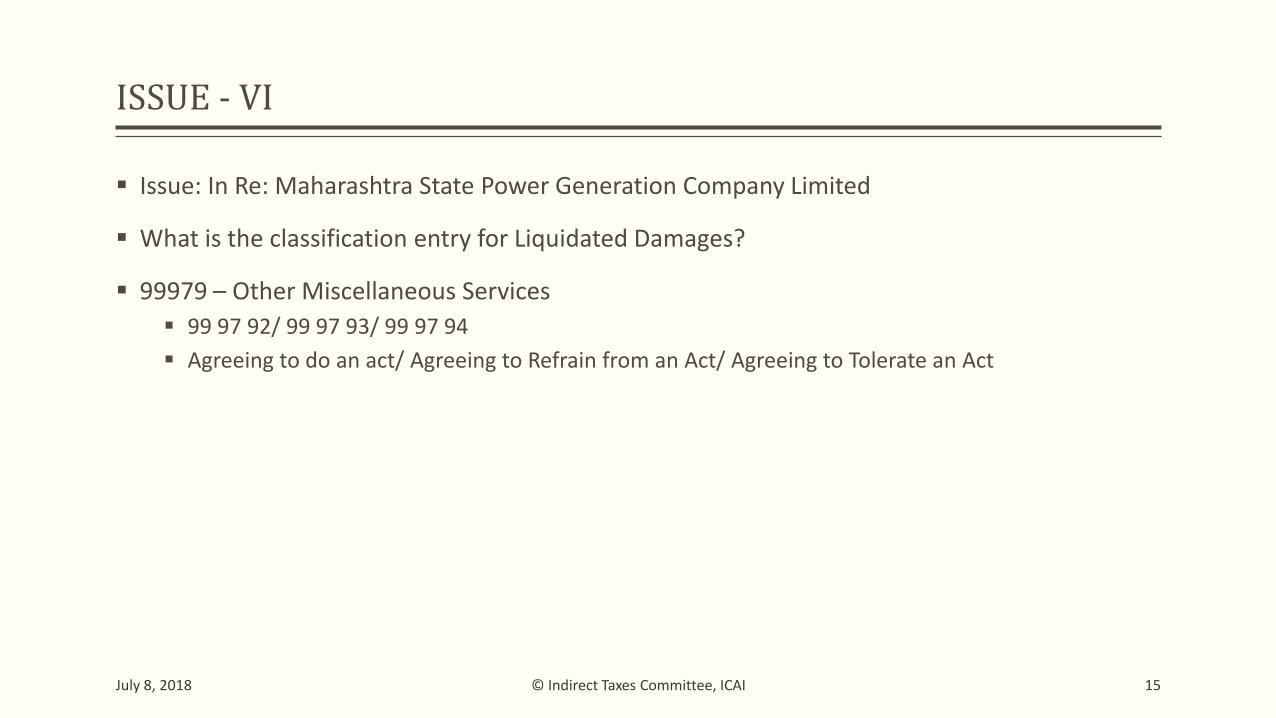

ISSUE - VI

Issue: In Re: Maharashtra State Power Generation Company Limited

What is the classification entry for Liquidated Damages?

99979 – Other Miscellaneous Services

99 97 92/ 99 97 93/ 99 97 94

Agreeing to do an act/ Agreeing to Refrain from an Act/ Agreeing to Tolerate an Act

© Indirect Taxes Committee, ICAI 15July 8, 2018

Indirect Taxes Committee of ICAI at [email protected] and Register on www.idtc.icai.org for updates and resource material from ICAI

16© Indirect Taxes Committee, ICAIJuly 8, 2018