island village montessori charter school, inc. table … rpts... · island village montessori...

TRANSCRIPT

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.

TABLE OF CONTENTS PAGE Independent Auditor’s Report 1-2 Management’s Discussion and Analysis 3-7 Governmental Fund (General Fund) Balance Sheet 8 Statement of Net Position 9 Reconciliation of the Governmental Fund (General Fund) Balance Sheet to the Statement of Net Position

10

Statement of Governmental Fund (General Fund) Revenues, Expenditures and Changes in Fund Balance

11

Statement of Activities 12 Statement of Revenues, Expenditures, and Changes in Fund Balance-Budget (GAAP Basis) and Actual-All Governmental Fund Types

13-14 Reconciliation of Statement of Revenues, Expenditures And Changes in Fund Balance of Governmental Fund (General Fund) to the Statement of Activities

15 Notes to Financial Statements 16-23 Report on Internal Control Over Financial Reporting And on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards

24-25 Management Letter 26-27

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. MANAGEMENT’S DISCUSSION AND ANALYSIS

JUNE 30, 2016 Our discussion and analysis of Island Village Montessori Charter School, Inc.’s (“the School”) financial program provides an overview of the School’s financial activities for the year ended June 30, 2016. Because the information contained in this discussion is intended to highlight significant transactions, it should be read in conjunction with the School’s financial statements, which begin on page 8. For financial statement purposes the School is considered a component unit of the District School Board of Sarasota County, which is a primary government entity for financial reporting. The School used the option to present the governmental standards and fund statement on the same page. The Statement of Net Position and the Statement of Activities report provide information on the activities of the School. The fund financial statements reflect financing activities of the School by providing information on inflows and outflows of spendable resources. NON FINANCIAL HIGHLIGHTS The School’s enrollment at the end of the fiscal year ended June 30, 2016 was 700 students. This was approximately five students greater than budgeted. The School expects to have an enrollment of 750 students for the school year 2016-2017. OVERVIEW OF THE FINANCIAL STATEMENTS Government-wide Financial Statements The government-wide financial statements are designed to provide readers with a broad overview of the School’s financial position. Included in these statements are all assets and liabilities using the accrual basis of accounting. All of the current year’s revenues and expenses are recorded when earned or incurred. The Statement of Net Position presents information on all of the School’s assets and liabilities, with the difference between the two reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the School is improving or deteriorating. The Statement of Activities presents information showing how the government’s net position changed during the most recent fiscal year. All changes in net position are reported when the underlying event giving rise to the change occurs, regardless of the timing of the related cash flows. Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives.

3

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. MANAGEMENT’S DISCUSSION AND ANALYSIS

JUNE 30, 2016 OVERVIEW OF FINANCIAL STATEMENTS (Cont’d.) Fund Financial Statements (Cont’d.) Governmental Funds – All of the School’s basic services are reported in governmental funds, which focus on how money flows into and out of those funds and the balances left at year-end that are available for spending. These funds are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of the School’s governmental activities and the basic services it provides. Notes to Financial statements The Notes to the Financial Statements provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The Notes to the Financial Statements can be found on pages 16-23 of this report. GOVERNMENT-WIDE FINANCIAL ANALYSIS As noted earlier, net position may serve over time as a useful indicator of the School’s financial position. The School’s assets exceeded liabilities by $2,447,019 at June 30, 2016. This is an increase of $1,015,507 over the prior year.

NET ASSETS

JUNE 30, 2016 JUNE 30, 2015

Current and Other Assets $ 1,468,978 $ 897,379 Capital Assets 5,382,498 4,773,219 Total Assets $ 6,851,476 5,670,598

Long-Term Liabilities 4,089,000 3,962,498 Other Liabilities 315,457 276,588 Total Liabilities $ 4,404,457 $ 4,239,086

Investment in Capital Assets 1,293,498 810,721 Unrestricted 1,153,521 620,791 Total Net Position $ 2,447,019 $ 1,431,512

Revenues from governmental activities totaled $6,514,492 for the year ended June 30, 2016. The main source of revenue is from Florida Education Finance Program (FEFP). This revenue represented approximately 89.6% of total revenue compared to 90.6% in the prior year.

4

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. MANAGEMENT’S DISCUSSION AND ANALYSIS

JUNE 30, 2016 GOVERNMENT-WIDE FINANCIAL ANALYSIS (Cont’d.)

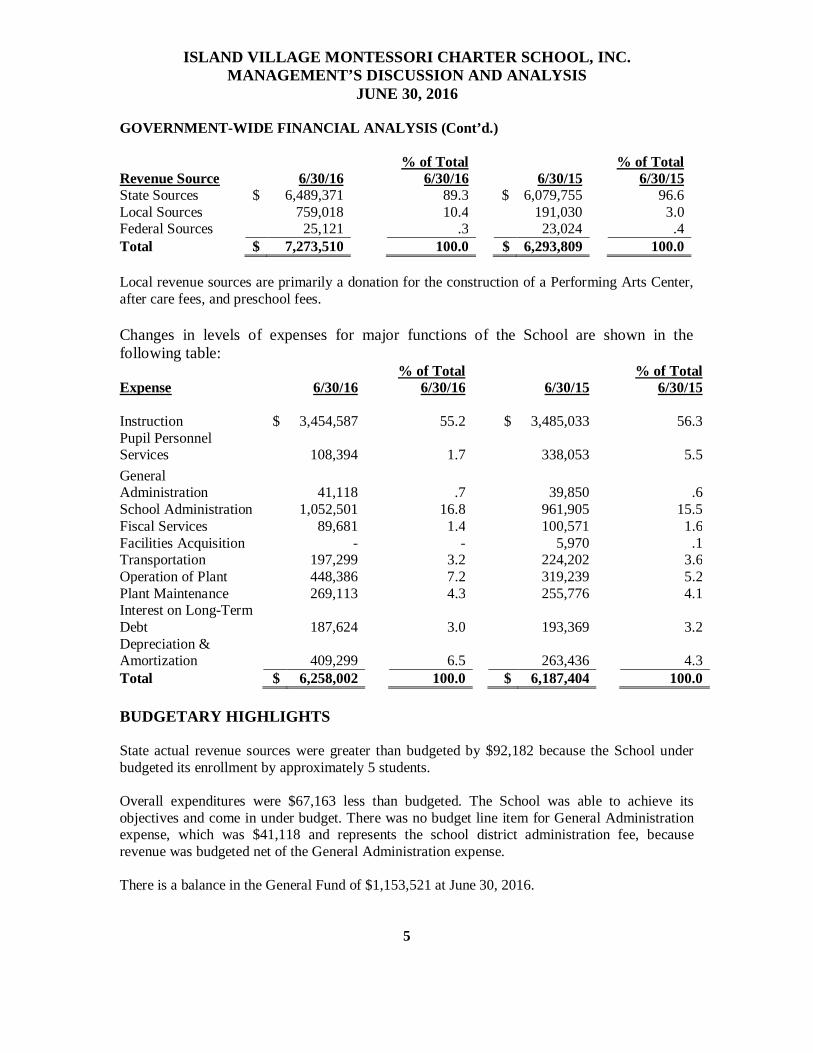

Revenue Source

6/30/16

% of Total 6/30/16

6/30/15

% of Total 6/30/15

State Sources $ 6,489,371 89.3 $ 6,079,755 96.6 Local Sources 759,018 10.4 191,030 3.0 Federal Sources 25,121 .3 23,024 .4 Total $ 7,273,510 100.0 $ 6,293,809 100.0

Local revenue sources are primarily a donation for the construction of a Performing Arts Center, after care fees, and preschool fees. Changes in levels of expenses for major functions of the School are shown in the following table: % of Total % of Total Expense 6/30/16 6/30/16 6/30/15 6/30/15 Instruction $ 3,454,587 55.2 $ 3,485,033 56.3 Pupil Personnel Services

108,394

1.7

338,053

5.5

General Administration

41,118

.7

39,850

.6

School Administration 1,052,501 16.8 961,905 15.5 Fiscal Services 89,681 1.4 100,571 1.6 Facilities Acquisition - - 5,970 .1 Transportation 197,299 3.2 224,202 3.6 Operation of Plant 448,386 7.2 319,239 5.2 Plant Maintenance 269,113 4.3 255,776 4.1 Interest on Long-Term Debt

187,624

3.0

193,369

3.2

Depreciation & Amortization

409,299

6.5

263,436

4.3

Total $ 6,258,002 100.0 $ 6,187,404 100.0

BUDGETARY HIGHLIGHTS State actual revenue sources were greater than budgeted by $92,182 because the School under budgeted its enrollment by approximately 5 students. Overall expenditures were $67,163 less than budgeted. The School was able to achieve its objectives and come in under budget. There was no budget line item for General Administration expense, which was $41,118 and represents the school district administration fee, because revenue was budgeted net of the General Administration expense. There is a balance in the General Fund of $1,153,521 at June 30, 2016.

5

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. MANAGEMENT’S DISCUSSION AND ANALYSIS

JUNE 30, 2016 DEBT ADMINISTRATION Long Term Debt On June 23, 2016 the original Industrial Development Revenue Bonds, Series 2007 were refunded to the City of Venice and the original note payable and two additional notes payable were paid off through the issuance of an Educational Facilities Revenue Refunding Bond, Series 2016. The new Revenue Bond is for $3,850,000 and was purchased by Wells Fargo Bank. The balance outstanding on this loan at June 30, 2016 is $3,850,000. The School had a loan for the purchase of a campus in 2012. The loan was financed through BB&T Bank in the amount of $1,593,750. Interest on the loan is 4.75% and the balance was paid off out of the proceeds of the new bonds. The School also has a line of credit in the amount of $400,000 with the Wells Fargo bank, which was not used. The School purchased a property in March 2013, which was financed through a loan from BB&T Bank. The balance was also paid off out of the revenue bond proceeds. A donor to the School financed the Performing Arts Center for $838,042 with the understanding that $250,000 would be paid back to him over a 30 year period. Interest and principal payments are $1,000 per month and the note bears interest of 2.6% per annum. CAPITAL ASSETS The School’s investment in capital assets at June 30, 2016 was $5,382,498 (net of depreciation). The investment includes land and improvements, building, furniture, fixtures and equipment and Vehicles. The following is a summary of capital assets balances at June 30, 2016:

Land and Improvements $ 829,116 Building 5,609,412 Furniture, Fixtures & Equipment 1,495,242 Vehicles 20,471 7,954,241 Less Accumulated Depreciation 2,571,743 $ 5,382,498

PROSPECTS FOR THE FUTURE The School continues to receive funds from State sources in the form of Florida Education Finance Program Fees (FEFP). The fees are evaluated in October and February and are based on student enrollment.

The School received a “B” rating from the Department of Education, so the Administration invested in additional software and staff to achieve an “A” rating for the 2016-2017 school year.

The Administration believes that higher test scores will be achieved because of

investments in reading and math computer based programs. 6

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. MANAGEMENT’S DISCUSSION AND ANALYSIS

JUNE 30, 2016

PROSPECTS FOR THE FUTURE (Cont’d.)

The School should surpass its budgeted amount of 750 students for the 2016-2017 school year.

The Administration believes that the School will continue to progress and contribute to the educational needs of Sarasota County.

The School will operate through 11th grade for the 2016-2017 school year.

REQUESTS FOR INFORMATION The Management Discussion and Analysis provides a general overview of the finances of the School. Requests for additional information should be addressed to Jennifer Ocana, Executive Director, at 2001 Pinebrook Road, Venice, Florida 34292.

7

GovernmentalFunds

ASSETS Cash $1,188,470 Accounts receivable 5,340 Prepayments 151,534 Mortgage costs,net 123,634Total Assets $1,468,978

LIABILITIES

Accrued payroll and benefits $182,562 Accounts Payable 132,895Total Liabilities 315,457

FUND BALANCE Nonspendable 151,534 Unassigned 1,001,987Total fund balances 1,153,521

Total Liabilities and Fund Balance $1,468,978

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.Governmental Fund Balance Sheet

June 30, 2016

The accompanying notes are an integral part of this statement8

Account Governmental Business-typeASSETS Number Activities Activities TotalCash and Cash Equivalents 1110 1,188,470 1,188,470 Accounts Receivable, Net 1130 5,340 5,340 Deferred Charges:Prepaid Items 1230 151,534 151,534 Mortgage Costs, net 123,634 123,634 Capital Assets: Land 1310 829,116 829,116 Buildings & Fixed Equipment 1330 5,609,412 5,609,412 Less Accumulated Depreciation 1329 (1,591,381) (1,591,381) Furniture, Fixtures and equipment 1340 1,495,242 1,495,242 Less Accumulated Depreciation 1349 (959,891) (959,891) Motor Vehicles 1350 20,471 20,471 Less Accumulated Depreciation 1359 (20,471) (20,471) Total Assets 6,851,476 6,851,476

LIABILITIESSalaries and Wages Payable 2110 182,562 182,562 Payroll Deductions and Withholdings 2170Accounts Payable 2120 132,895 132,895 Noncurrent Liabilities: Portion Due Within One Year:Notes Payable 2320 4,089,000 4,089,000 Liability for Compensated Absences 2330Total Liabilities 4,404,457 4,404,457

NET POSITIONInvested in Capital Assets, Net of Related Debt 1,293,498 1,293,498 Restricted For: Categorical Carryover Programs 2710Debt Service 2750Unrestricted 1,153,521 1,153,521 Total Net Position 2,447,019 2,447,019

Primary Government

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.STATEMENT OF NET POSITIONFor the Year ended June 30, 2016

The accompanying notes are an integral part of this statement9

Fund Balance- Governmental Funds 1,153,521

Capital assets used in governmental activities are not financial resources and therefore are not reported in the governmental funds

Governmental capital assets 7,954,241 Less accumulated depreciation (2,571,743)

5,382,498

Long-Term Liabilities not due and payable in the current period and therefore are not reported in the governmental funds

Mortgages Payable (4,089,000) (4,089,000)

Net Position of Governmental activities 2,447,019

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.Reconciliation of the Governmental Fund (General Fund)

Balance Sheet To The Statement of Net PositionJune 30, 2016

The accompanying notes are an integral part of this statement10

Governmental SpecialFunds Revenue Total

EXPENSES Instruction 3,429,466 25,121 3,454,587 Pupil Personnel Services 108,394 108,394 General Administration 41,118 41,118 School Administration 1,052,501 1,052,501 Fiscal Services 89,681 89,681 Operation of Plant 448,386 448,386 Maintenance of Plant 269,113 269,113 Transportation 197,299 197,299 Debt Service 417,898 417,898 Capital Outlay 1,018,579 1,018,579

TOTAL EXPENSES 7,072,435 25,121 7,097,556

PROGRAM REVENUES Florida Education Finance Program (FEFP) 5,976,057 5,976,057 Capital grants and contributions 513,061 513,061 Charges for services 50,369 50,369 Total program revenues 6,539,487 6,539,487 GENERAL REVENUES: Other federal sources 25,121 25,121 Other state sources 253 253 Other local sources 708,649 708,649 Total general revenues 708,902 734,023 Other Financing Sources Proceeds from long term borrowing 4,100,000 4,100,000 Payment on notes payable (3,743,224) (3,743,224) Total Other financing Sources 356,776 356,776 Excess of Revenues over expenses 532,730 532,730

Fund balance, beginning of year 620,791 620,791 Fund balance, end of year 1,153,521 - 1,153,521

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.Statement of Governmental Fund (General Fund) Revenues, Expenditures and

Changes in Fund BalanceYear ended June 30, 2016

The accompanying notes are an integral part of this statement11

Net (Expense) Revenueand Changes in Net Position

Operating CapitalCharges for Grants and Grants and Governmental

FUNCTIONS Expenses Services Contributions Contributions ActivitiesGovernmental activities: Instruction 3,454,587 50,369 25,121 (3,379,097) Pupil Personnel services 108,394 253 (108,394) General Administration 41,118 (41,118) School Administration 1,052,501 (1,052,501) Fiscal Services 89,681 513,061 423,380 Transportation 197,299 197,299 Operation of Plant 448,386 (448,386) Maintenance of Plant 269,113 (269,113) Interest on long term debt 187,624 (187,624) Unallocated Depreciation Expense * 409,299 (409,299) Total governmental activities 6,258,002 50,369 25,374 513,061 (5,669,198)

General RevenuesState through local school district 5,976,057 Miscellaneous revenues 708,647 Total General revenues 6,684,704 Change in net position 1,015,506 Net position , beginning 1,431,513 Net position, ended 2,447,019

Program Revenues

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2016

The accompanying notes are an integral part of this statement12

Governmental Funds Special Revenue TOTALOriginal Original Original

and Final and Final and FinalBudget Actual Variance Budget Actual Variance Budget Actual Variance

EXPENDITURES: Instruction 3,559,038 3,429,466 (129,572) 24,000 25,121 1,121 3,583,038 3,454,587 (128,451) Pupil Personnel Services 98,388 108,394 10,006 98,388 108,394 10,006 General Administration 41,118 41,118 41,118 41,118 School Administration 957,207 1,052,501 95,294 957,207 1,052,501 95,294 Fiscal Services 82,121 89,681 7,560 82,121 89,681 7,560 Operation of Plant 454,420 448,386 (6,034) 454,420 448,386 (6,034) Maintenance of Plant 313,898 269,113 (44,785) 313,898 269,113 (44,785) Transportation 220,385 197,299 (23,086) 220,385 197,299 (23,086) Debt Service 419,262 417,898 (1,364) 419,262 417,898 (1,364) Capital Outlay 1,036,000 1,018,579 (17,421) 1,036,000 1,018,579 (17,421)

7,140,719 7,072,435 (68,284) 24,000 25,121 1,121 7,164,719 7,097,556 (67,163)

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.Statement of Revenues, Expenditures and ChangesIn Fund Balance-Budget (GAAP Basis) and Actual

All Governmental Fund TypesFor the Fiscal Year Ended June 30, 2016

The accompanying notes are an integral part of this statement13

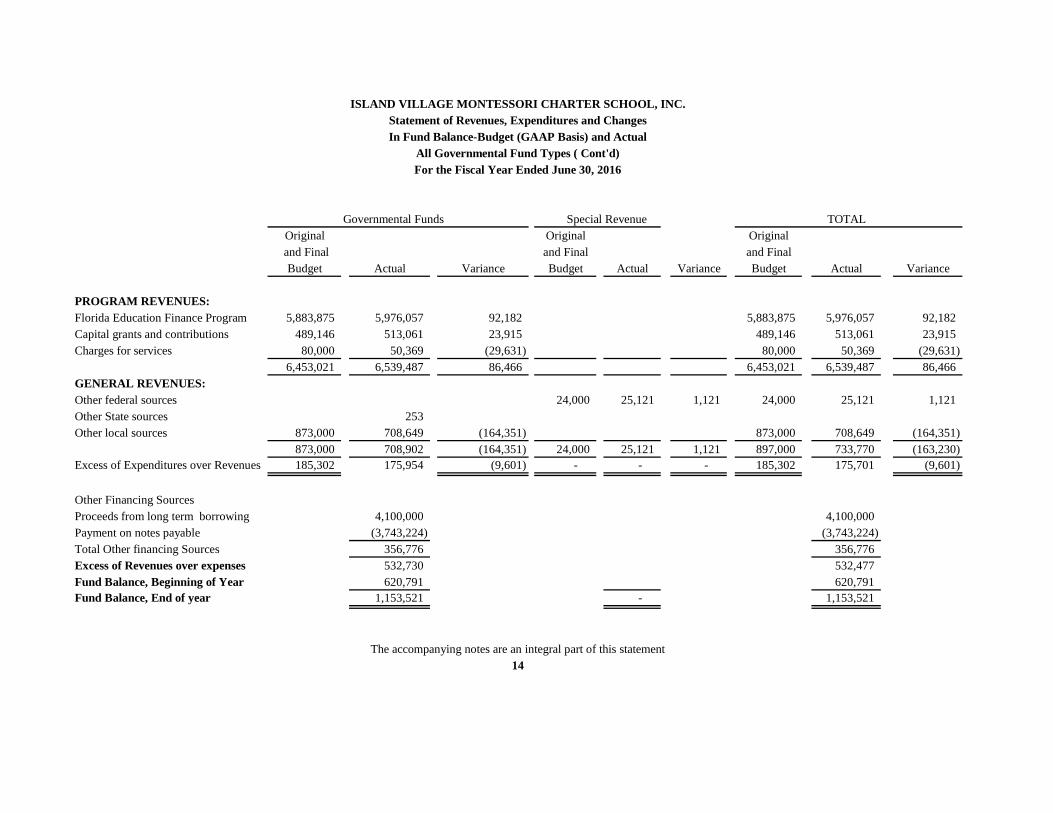

Governmental Funds Special Revenue TOTALOriginal Original Original

and Final and Final and FinalBudget Actual Variance Budget Actual Variance Budget Actual Variance

PROGRAM REVENUES:Florida Education Finance Program 5,883,875 5,976,057 92,182 5,883,875 5,976,057 92,182 Capital grants and contributions 489,146 513,061 23,915 489,146 513,061 23,915 Charges for services 80,000 50,369 (29,631) 80,000 50,369 (29,631)

6,453,021 6,539,487 86,466 6,453,021 6,539,487 86,466 GENERAL REVENUES:Other federal sources 24,000 25,121 1,121 24,000 25,121 1,121 Other State sources 253 Other local sources 873,000 708,649 (164,351) 873,000 708,649 (164,351)

873,000 708,902 (164,351) 24,000 25,121 1,121 897,000 733,770 (163,230) Excess of Expenditures over Revenues 185,302 175,954 (9,601) - - - 185,302 175,701 (9,601)

Other Financing SourcesProceeds from long term borrowing 4,100,000 4,100,000 Payment on notes payable (3,743,224) (3,743,224) Total Other financing Sources 356,776 356,776 Excess of Revenues over expenses 532,730 532,477 Fund Balance, Beginning of Year 620,791 620,791 Fund Balance, End of year 1,153,521 - 1,153,521

The accompanying notes are an integral part of this statement14

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.Statement of Revenues, Expenditures and ChangesIn Fund Balance-Budget (GAAP Basis) and Actual

All Governmental Fund Types ( Cont'd)For the Fiscal Year Ended June 30, 2016

Net Changes in Fund Balances- Governmental Funds 532,730

Amounts reported for governmental activities in thestatement of net position are different because:

Governmental Funds report capital outlays as expenditures.However, in the Statement of Activities, the cost of thoseassets is depreciated over their estimated useful lives.

Expenditures for capital assets 1,018,579 Less current year depreciation (409,299)

609,280

Some expenses reported in the Statement of Activities do not require the use of current financial resources and therefore are not reported as expenditures in the Governmental Funds.

Payments of Notes payable 3,973,498 Proceeds from notes payable (4,100,000)

(126,504)

Change in Net Position of Governmental Activities 1,015,506

The accompanying notes are an integral part of this statement15

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC.Reconciliation of the Statement of Revenues,Expenditures and Changes in Fund Balances

of Governmental Fund (General Fund) To TheStatement of Activities

June 30, 2016

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Reporting Entity Island Village Montessori Charter School, Inc. (“the School”) was established as a nonprofit organization in January 2001 under the laws of the State of Florida and is the reporting entity. The School operates as a Charter School pursuant to a Charter School Contract (the Contract) with the School District of Sarasota County, Florida. Under the Contract the School provides a Montessori education to children from kindergarten through 12th grade. However, the school operated through 10th grade for the 2015-2016 school year and added 11th grade for the 2016-2017 school year. For financial statement purposes the School is considered a component unit of the School District of Sarasota County, which is a primary government entity for financial reporting. The School District of Sarasota County received 5% of the Florida Education Finance Program (FEFP) revenue as an administrative fee for the first 250 students decreasing to 2.5%. The Contract is effective through June 2025. The Contract requires the School District to provide the School’s primary source of funding based upon the number of full-time equivalent students (FTES) registered at the School. The School is a tax exempt organization under 501(C)(3) of the Internal Revenue Code. The School’s financial statements are prepared in accordance with generally accepted accounting principles (GAAP). The Government Accounting Standards Board (GASB) is responsible for establishing GAAP for school districts through its pronouncements (statements and interpretations). The more significant accounting policies established in GAAP and used by the School are discussed below. Basic Financial Statements The School’s basic financial statements are the Statements of Net Position and the Statement of Activities. All the activities of the School are classified as governmental type activities. There are no business type activities of the School. All the School’s governmental type activities are included in the general fund. There are no other major funds. In the Statement of Net position, the governmental activities column is reported on a full accrual, economic resource basis, which recognizes all long-term assets and receivables as well as long-term debt obligations. The School’s net position are reported in three parts – invested in capital assets, net of related debt; restricted for categorical carryover programs, debt service; and unrestricted net position. The Statement of Activities reports both the gross and net cost of each of the School’s functions. The functions are also supported by government revenues such as Florida Education Finance Program (FEFP), Capital Outlay Funds and Federal Grants. The Statement of Activities reduces gross expenses (including depreciation) by related program revenues, operating and capital grants. Program revenues must be directly associated with the function (after care and youth services, etc.). Operating grants include operating-specific and discretionary (either operating or capital) grants while the capital grants column reflects capital-specific grants.

16

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont’d.) Fund Financial Statements Fund financial statements are provided for governmental funds. The operations of the funds are accounted for with a separate set of self-balancing accounts that comprise its assets, liabilities, equity, revenues and expenditures. Major individual governmental funds are reported as separate columns in the fund financial statements:

General Fund – is the School’s primary operating fund. It accounts for all financial resources of the School, except those required to be accounted for in another fund. Special Revenue Fund – accounts for specific revenue, such as federal grants that are legally restricted to expenditures for particular purposes.

Basis of Accounting Basic of accounting refers to the point at which revenues or expenditures/expenses are recognized in the accounting and reported in the financial statements. It relates to the timing of the measurements made regardless of the measurement focus applied. Accrual The governmental type activities in the financial statements are presented on the accrual basis of accounting. Revenues are recognized when earned and expenses are recognized when incurred. When both restricted and unrestricted resources are available for use, it is the policy of the School to use restricted resources first, the unrestricted resources as they are needed. Measurement Focus The accounting and financial reporting treatment is determined by applicable measurement focus and basis of accounting. Measurement focus indicates the type of resources being measured such as current financial resources (current assets less current liabilities) or economic resources (all assets and liabilities). The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting. With this measurement focus, all assets and all liabilities associated with the operation of these funds are included on the balance sheet and operating statements present increases (i.e. revenues) and decreases (i.e. expenses) in net assets.

17

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont’d.) Measurement Focus (Cont’d.) Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. With this measurement focus, only current assets and current liabilities generally are included on the balance sheet. Operating statements of these funds present increases (i.e. revenues and other financing sources) and decreases (i.e. expenditures and other financial uses) in net current assets. Under the modified accrual basis of accounting, revenues are recognized when they become measurable and available to finance expenditures of the fiscal period. For this purpose, the School considers revenues to be available if they are collected within sixty days of the end of the current fiscal period. Expenditures are generally recognized under the modified accrual basis of accounting when the related liability is incurred. Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles include the use of estimates that affect the financial statements. Accordingly, actual results could differ from those estimates. Concentration of Credit Risk Financial instruments that subject the School to concentrations of credit risk include cash and deposits. While the School attempts to limit its financial exposure, its cash balances may at times exceed federally insured limits. The School has not experienced any losses on such balances. Cash deposits are held at banks qualified as public depositories under Florida law. Fair Value Measurements The Fair Value Measurements Topic of the FASB Accounting Standards Codification defines fair value, establishes a consistent framework for measuring fair value and expands disclosure requirements for fair value measurements. The School measures the fair value of assets and liabilities as the price that would be received to sell an asset or paid to transfer a liability in the principal or most advantageous market in an orderly transaction between market participants at the measurement date. The fair value hierarchy distinguishes between independent observable inputs and unobservable inputs used to measure fair value as follows:

18

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont’d.) Fair Value Measurements (Cont’d.) Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date. Level 2: Inputs other than quoted Market prices included within Level1 that are observable for an asset or liability, either directly or indirectly. Level 3: Unobservable inputs for an asset or liability. Level 3 inputs should be used to measure fair value to the extent that observable Level 1 or 2 inputs are not available. Financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The assessment of the significance of a particular input to the fair value measurement requires judgment, and may affect the valuation of assets and liabilities and their placement within the fair value hierarchy levels. Contributed Services The School does not recognize any support, revenue or expense from services contributed by individual volunteers because they do not meet the criteria for measurement. Budgetary Basis of Accounting Budgets are presented on the modified accrual basis of accounting. During the fiscal year expenditures were controlled at the object level (i.e. salaries, purchased services, and capital outlay). Capital Assets Capital assets purchased or acquired with an original cost of $500 or more are reported at historical cost. Contributed assets are reported at fair market value as of the date received. Additions, improvements and other capital outlays that significantly extend the useful life of an asset are capitalized. Other costs incurred for repairs and maintenance are expensed as incurred. Depreciation on all assets is provided on the straight-line basis over the following estimated useful lives: Land Improvements 25 Years

Buildings 20-50 Years Furniture, Fixtures and Equipment 5-10 Years Motor Vehicle 5 Years Debt Issuance Costs

Bond Issue and loan costs are deferred and amortized over the life of the Bonds using the straight-line method which approximates the interest method.

19

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont’d.)

Revenue Sources Revenues for operations are received primarily from the School District of Sarasota County pursuant to the funding provisions included in the School’s Charter. In accordance with the funding provisions of the Charter and Section 1002.33, Florida Statutes, the School will report the number of full-time equivalent (FTE) students and related data to the School District of Sarasota County. Funding for the School is adjusted during the year to reflect the revised calculations by the Florida Department of Education under the Florida Education Finance Program and the actual weighted full-time equivalent students reported by the School during the designated full-time equivalent student survey periods. In addition, the School receives an annual allocation of charter school capital outlay funds. Fund Balance Classifications GASB requires the fund balance amounts to be properly reported within one of the fund balance categories listed below:

a) Nonspendable fund balance includes amounts that are not in a spendable form such as inventories, prepaid expenses, long-term loans and notes receivable, and property held for resale (unless the proceeds are restricted, committed or assigned). There was a nonspendable fund balance at year end.

b) Restricted fund balance includes amounts that can be spent only for the specific

purposes stipulated by external resource providers, constitutionally, or through enabling legislation. There was no restricted fund balance at year end.

c) Committed fund balance includes amounts that can be used only for the specific

purposes determined by a formal action of the School’s highest level decision making authority. There was no committed fund balance at year end.

d) Assigned fund balance includes amounts intended to be used by the School’s

Management for specific purposes but which does not meet the criteria to be classified as restricted or committed. There was no assigned fund balance at year end.

e) Unassigned fund balance includes amounts that are available for any purpose. These

amounts are reported only in the general fund. There was an unassigned fund balance at year end.

Order of Fund Balance Spending Policy The School’s policy is to apply expenditures against nonspendable fund balance followed in order by restricted fund balance, committed fund balance, assigned fund balance, and lastly unassigned fund balance at the end of the fiscal year. The School’s Board of Directors can deviate from this policy if it is in the best interest of the School.

20

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 2 – CAPITAL ASSETS Capital assets activity for the year ended June 30, 2016, were as follows: Balance

Beginning

Additions

Disposals Balance

Ending Land $ 829,116 $ - $ - $ 829,116 Buildings 4,727,858 881,554 - 5,609,412 Furniture, Fixtures and Equipment

1,358,218

137,024

-

1,495,242

Motor Vehicle 20,471 - - 20,471 6,935,663 1,018,578 - 7,954,241 Less Accumulated Depreciation

2,162,444

409,299

-

2,571,743

CAPITAL ASSETS $ 4,773,219 $ 609,279 $ - $ 5,382,498 Depreciation expense of $409,299 was charged to administrative and general expenses during the year ended June 30, 2016. Beginning balances were restated to reflect actual amounts. NOTE 3 – COMPENSATED ABSENCES Employees of the School are entitled to paid vacation and sick days depending on length of services. The School’s policy is to recognize the cost of vacation days when earned by the employee. The value of unused vacation days was determined to be immaterial therefore no accrual has been made. NOTE 4 – LONG TERM LIABILITIES Long Term liability activity for the year ended June 30, 2016 was as follows:

Beginning Balance

Additions

Re-ductions

Ending Balance

Due Within One Year

Loan Payable $ 2,372,936 $ - $ 2,372,936 $ - $ - Note Payable 1,362,119 - 1,362,119 - - Note Payable 227,443 - 227,443 - - Note–Wells Fargo - 3,850,000 - 3,850,000 192,839 Note–Jack Urfer - 250,000 11,000 239,000 5,700

$ 3,962,498 $ 4,100,000 3,973,498 $ 4,089,000 $ 198,539

21

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 4 – LONG TERM LIABILITIES (Cont’d.) Debt Maturity Debt service requirements at June 30, 2016 were as follows:

YEAR ENDED JUNE 30

PRINCIPAL INTEREST 2017 198,539 102,876 2018 221,936 105,790 2019 228,219 99,508 2020 234,679 93,347 2021 241,322 86,404 2022-2031 2,964,305 502,841 $ 4,089,000 $ 990,766

Educational Revenue Bonds On June 23, 2016, the City of Venice issued Educational Facilities Revenue Refunding Bonds in the amount of $3,850,000 for Island Village Montessori Charter School, Inc. Project 2016 to enable the school to do the following:

Refund the City of Venice’s outstanding Industrial Development Revenue Bonds, Series 2007.

Refinance the School’s obligations under two promissory notes dated May 21, 2012 and March 5, 2013 held by Branch Banking and Trust Company.

Pay certain costs of issuance of the Series 2016 Bonds. The Bonds were purchase by Wells Fargo Bank. The school has a promissory note with the bank in the amount of $3,850,000. Monthly Principal and interest payments are to be made on this loan commencing on August 1, 2016. Monthly debt service payments are $26,311 and the note bears interest at 2.8% per annum. The note matures on August 1, 2031 and is collateralized by the school property. The note payable to the original purchaser of the Industrial Development Revenue Bonds, Series 2007, was paid off as a result of this refinancing agreement. The balance paid off was $2,241,723. Notes Payable On June 1, 2016 two promissory notes were paid off through the refinancing of the revenue Bonds. The notes were for $1,276,279 and $ 214,223 respectively.

22

ISLAND VILLAGE MONTESSORI CHARTER SCHOOL, INC. NOTES TO FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

NOTE 4 – LONG TERM LIABILITIES (Cont’d.) During the year the School received a donation of $838,042, which is being used for the construction of a performing arts center. The School has to pay back $250,000 of these funds to the benefactor and has entered into a promissory note for the same amount. The School pays $1,000 per month and the note bears interest at 2.6% per annum. The note matures on September 20, 2045. NOTE 5 – COMMITMENTS AND CONTINGENCIES Risk Management The School is exposed to various risks of loss related to theft, damage to, and destruction of assets, errors and omissions; injuries to employees; and natural disasters. The School purchases commercial insurance for all material risks of loss to which the School is exposed, including general liability, property, auto and workers compensation. A review of the last five years reveals that settled claims have not exceeded insurance coverage. The School receives funding from the State of Florida based on the number of full time equivalent (FTE) students who attend the Charter School. The data is compiled by the School and is subject to audit by the State and if errors are found this could result in amounts having to be repaid to the State or decrease in future allocations. Management believes that the amounts that would have to be remitted to the State due to errors in their FTE count would not be material to the financial position of the School.

NOTE 6 – SUBSEQUENT EVENTS Management has evaluated events that occurred subsequent to the year end for potential recognition or disclosure in the financial statements, through the date on which the financial statements were available to be issued. The date when the financial statements were available to be issued was September 13, 2016. Management’s evaluation did not reveal any subsequent events that would have a material effect on the financial statements.

23