ipsas at 20: origins and challenges or a walk down … · · 2017-07-20ipsas at 20: origins and...

TRANSCRIPT

cipfa.org

IPSAS at 20: Origins and ChallengesorA Walk Down Memory Lane…

Ian BallChair, Audit Committee for Financial Statements of the NZ GovernmentChair, CIPFA International

Winterthur, 3 July, 2017

cipfa.org

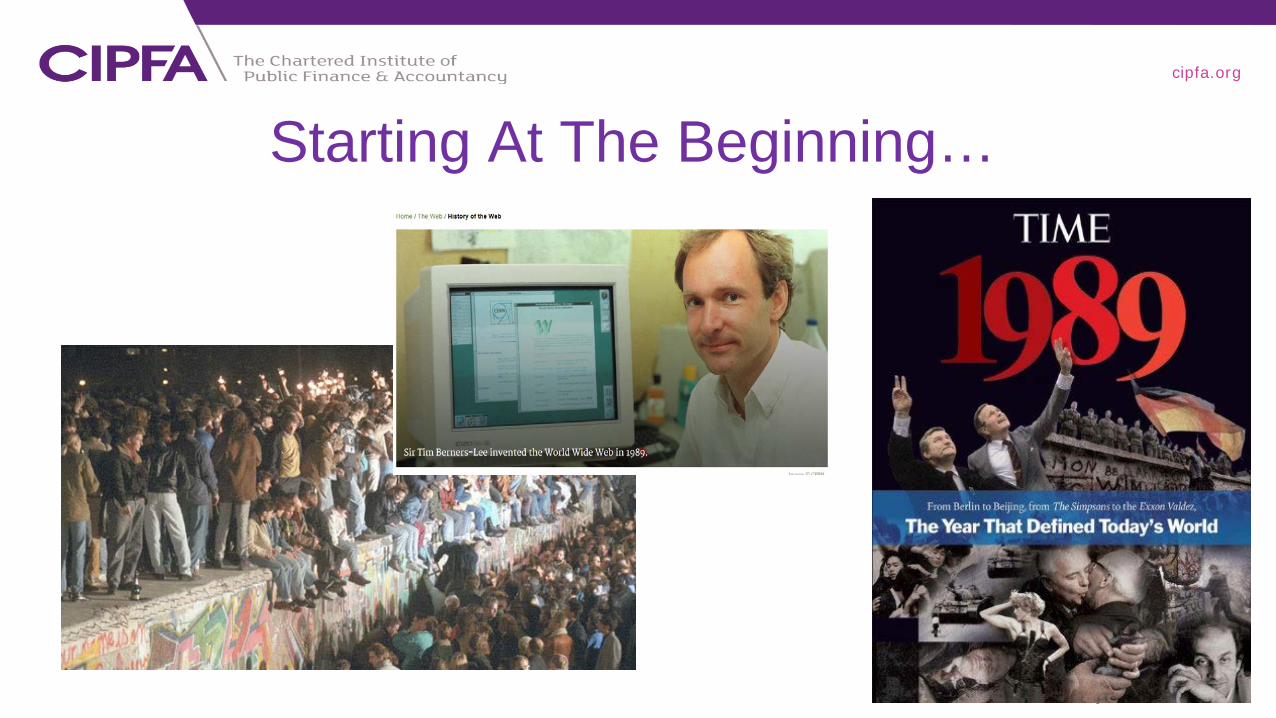

Starting At The Beginning…

cipfa.org

But also…

cipfa.org

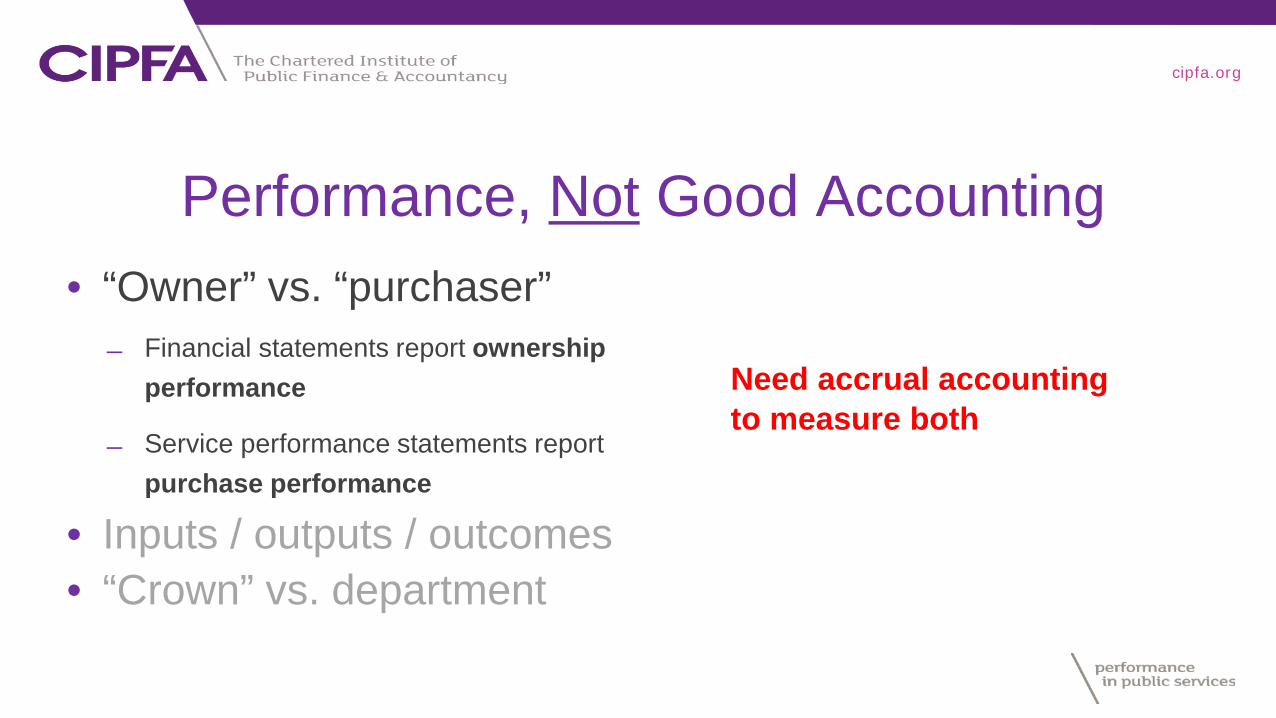

Performance, Not Good Accounting• “Owner” vs. “purchaser”

Financial statements report ownership performance

Service performance statements report purchase performance

• Inputs / outputs / outcomes• “Crown” vs. department

Need accrual accounting to measure both

cipfa.org

How The Economist Saw It…

cipfa.org

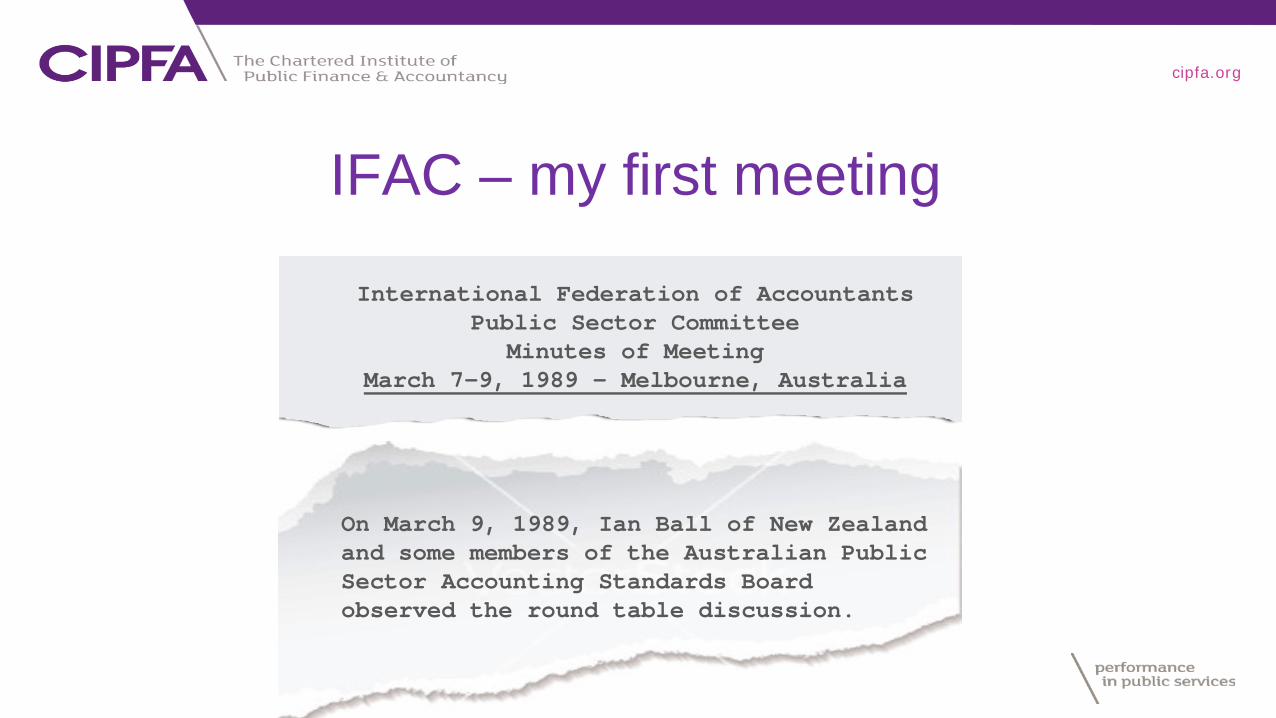

International Federation of AccountantsPublic Sector Committee

Minutes of MeetingMarch 7-9, 1989 – Melbourne, Australia

IFAC – my first meeting

On March 9, 1989, Ian Ball of New Zealand and some members of the Australian Public Sector Accounting Standards Board observed the round table discussion.

cipfa.org

Evidence and Experience

• Success came early, and continued• Same benefits could “accrue” elsewhere• Demonstration effect – it can be done…• Insurance for the NZ reforms

cipfa.org

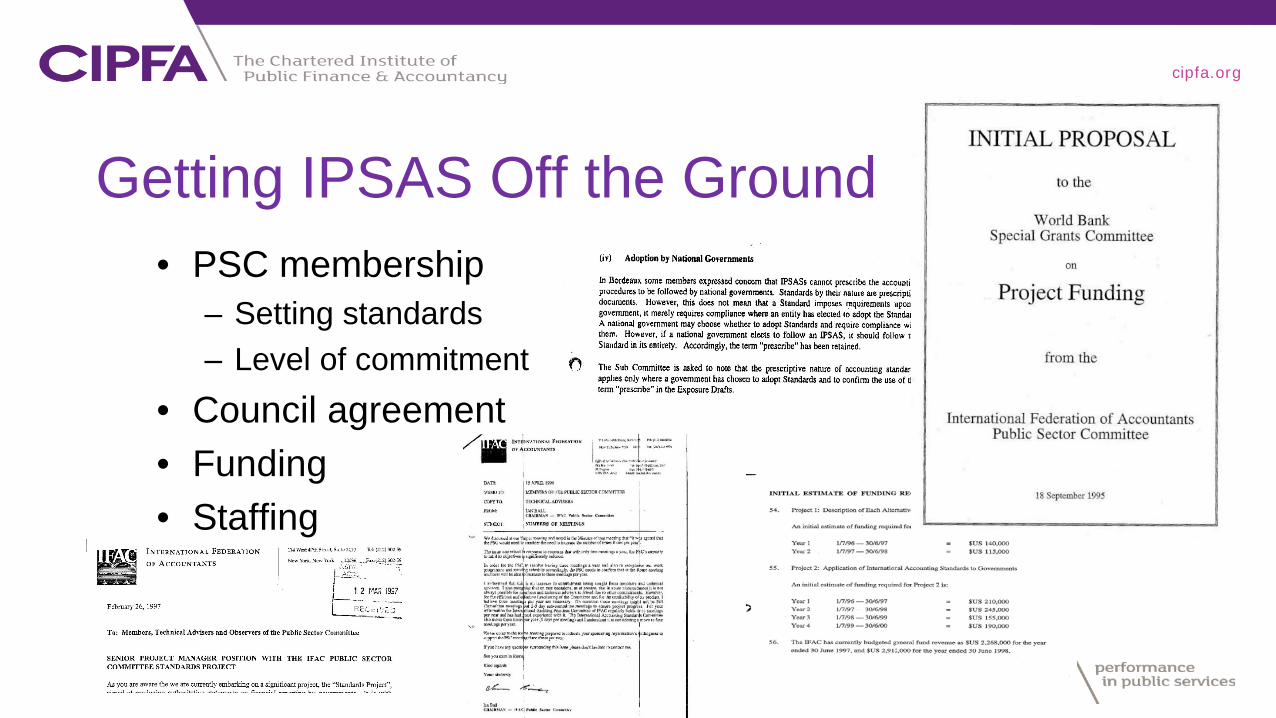

Getting IPSAS Off the Ground• PSC membership

– Setting standards– Level of commitment

• Council agreement• Funding• Staffing

cipfa.org

Secondary issues:• IASC copyright permissions• Translations• INTOSAI CAS• Consultative Group

cipfa.org

Invaluable New Zealand Support• The Treasury

– Dr Graham Scott, Secretary to the Treasury• New Zealand Society of Accountants

– April Mackenzie, Director, Accounting and Professional Standards

– Kevin Simpkins, Technical Adviser • Public Sector Performance (NZ) Ltd

– Tony Dale, Principal

cipfa.org

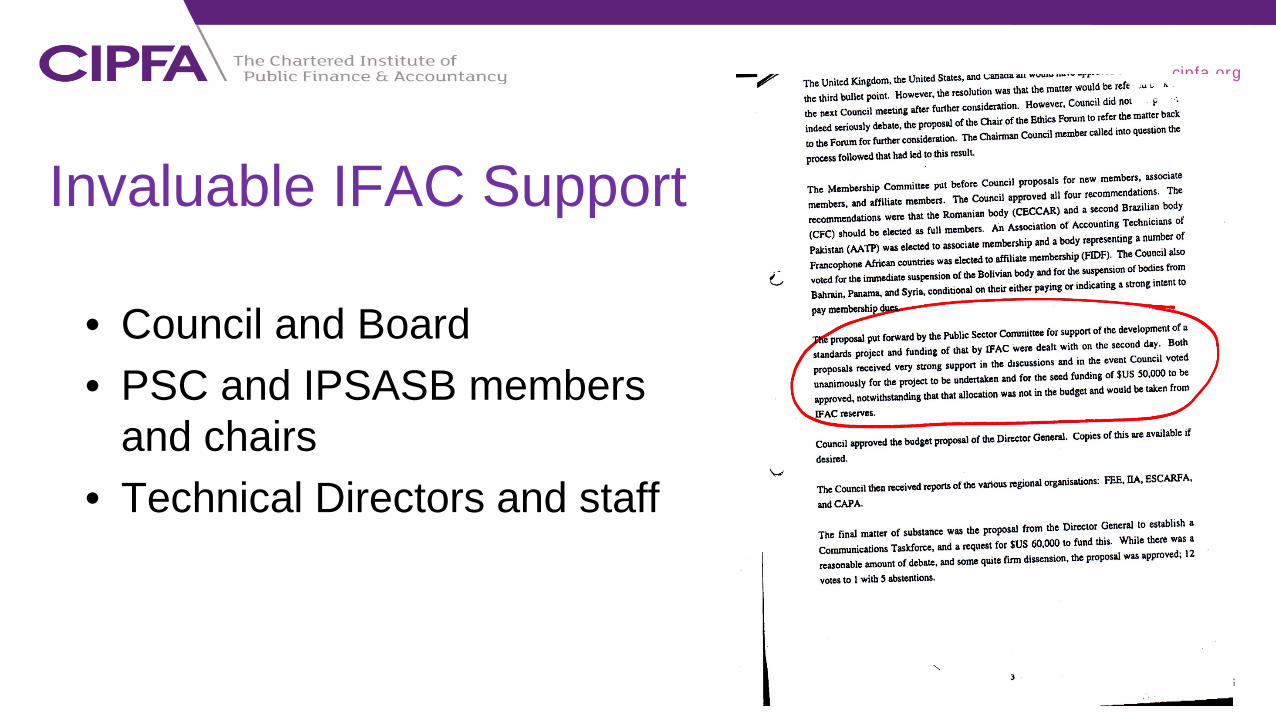

Invaluable IFAC Support

• Council and Board• PSC and IPSASB members

and chairs• Technical Directors and staff

cipfa.org

Original Objectives

cipfa.org

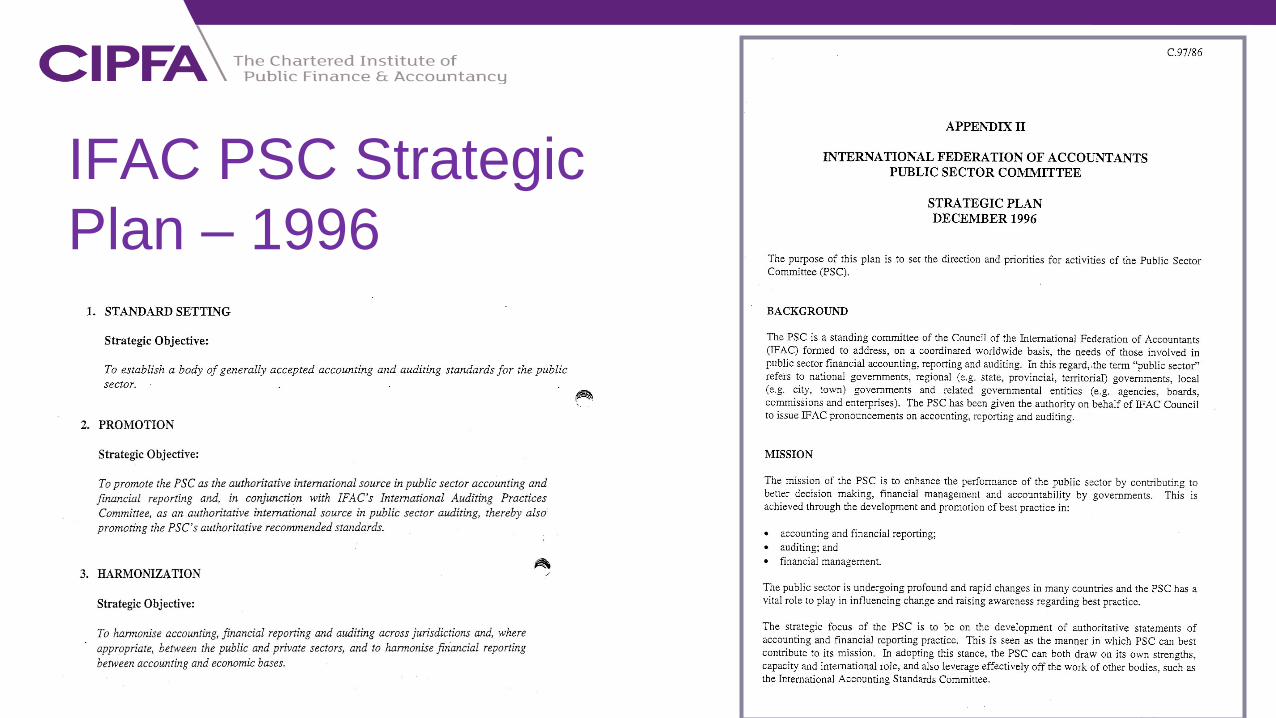

IFAC PSC Strategic Plan – 1996

cipfa.org

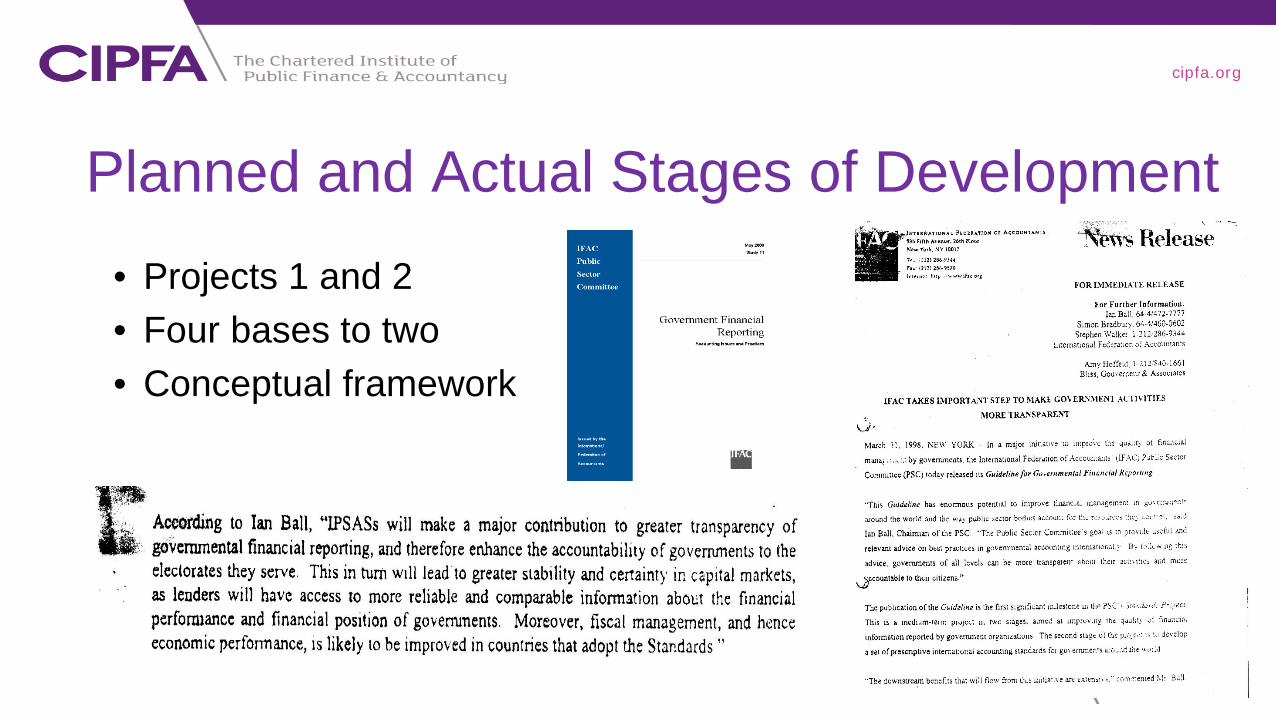

Planned and Actual Stages of Development• Projects 1 and 2• Four bases to two• Conceptual framework

cipfa.org

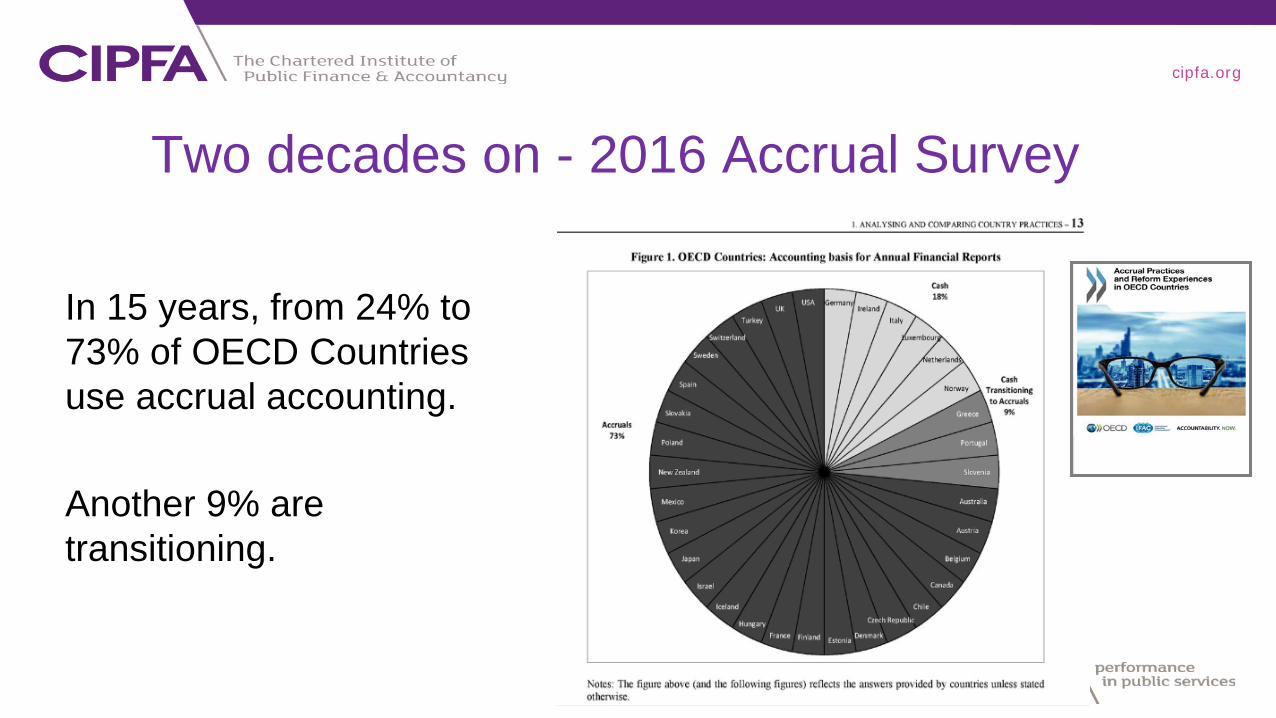

Two decades on - 2016 Accrual Survey

In 15 years, from 24% to 73% of OECD Countries use accrual accounting.

Another 9% are transitioning.

cipfa.org

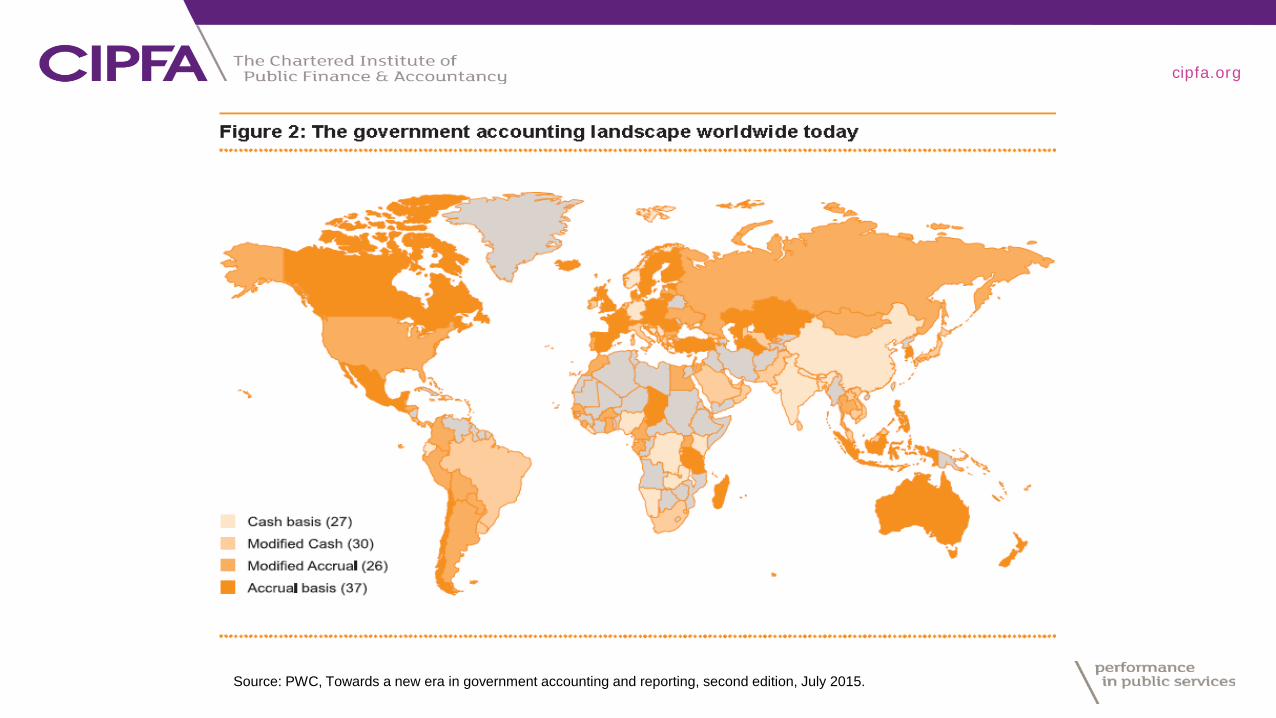

Source: PWC, Towards a new era in government accounting and reporting, second edition, July 2015.

cipfa.org

Source: PWC, Towards a new era in government accounting and reporting, second edition, July 2015.

cipfa.org

IPSAS – the benchmarkIMF IPSAS are the only international accounting standards designed for the

public sector (2014)

EC IPSAS is currently the only internationally recognized set of public sector accounting standards (2013)

World Bank As the only available international financial reporting standards for governments that are based on generally accepted accounting principles, IPSAS can contribute to greater quality, consistency, and comparability of government financial information within and between jurisdictions. (2004)

FEE International standards (IPSAS) already exist. They are the only recognized set of international standards. (2014)

IFAC High-quality and timely accrual-based financial reporting in the public sector can be achieved through the adoption of globally-accepted, high quality reporting standards developed specifically for the public sector, i.e., IPSASs. (2014)

IIF The IIF supports the implementation of international public sector accounting standards (IPSAS) for governments due to their importance for global growth and stability. (2013)

cipfa.org

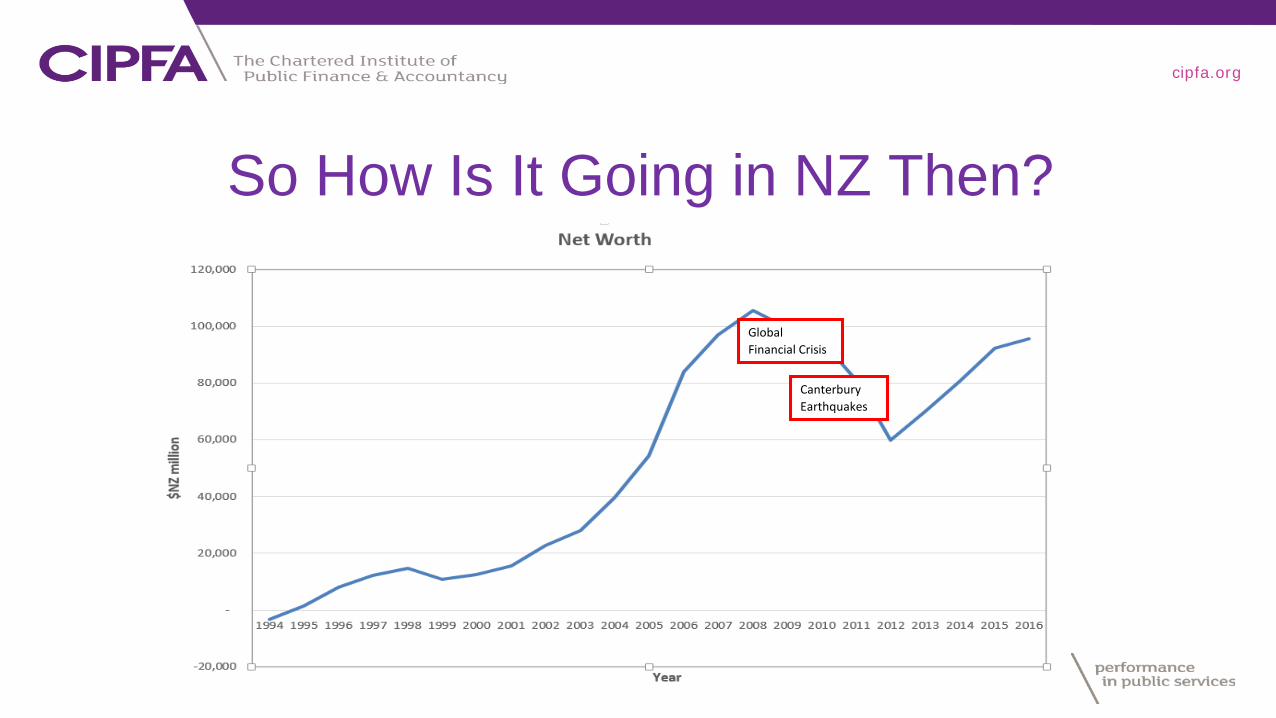

So How Is It Going in NZ Then?

cipfa.org

So How Is It Going in NZ Then?

Canterbury Earthquakes

Global Financial Crisis

cipfa.org

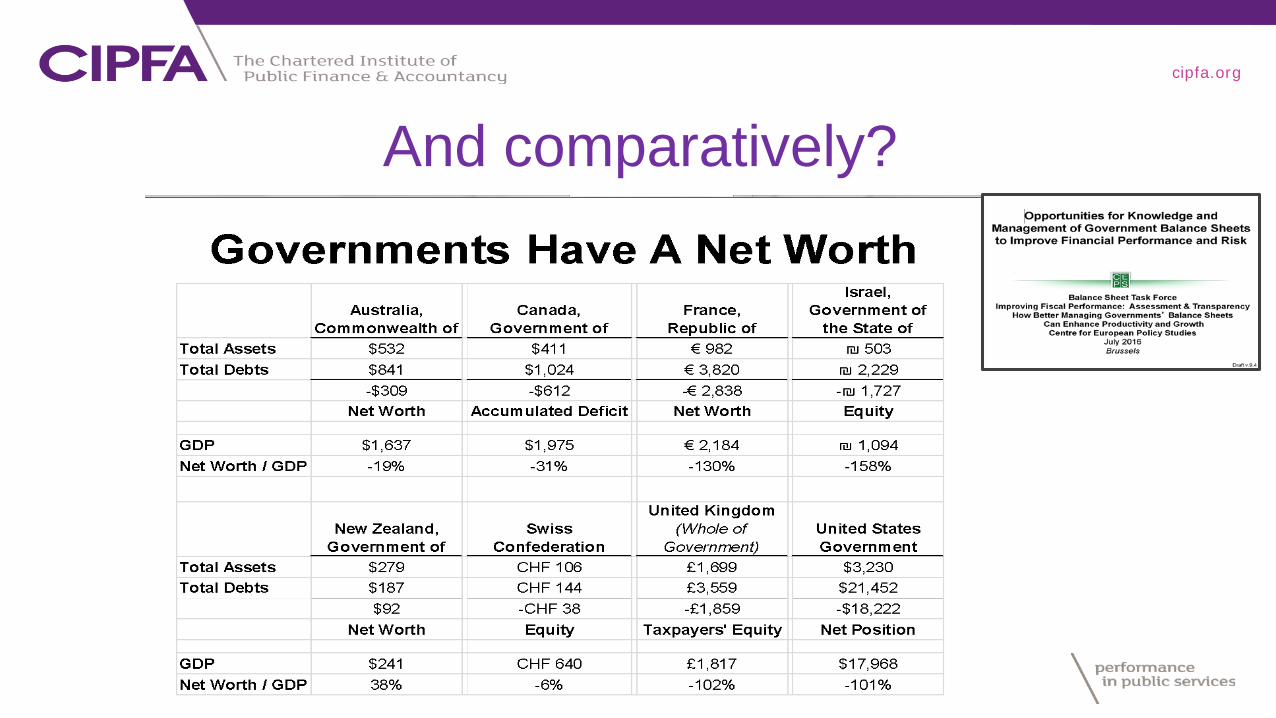

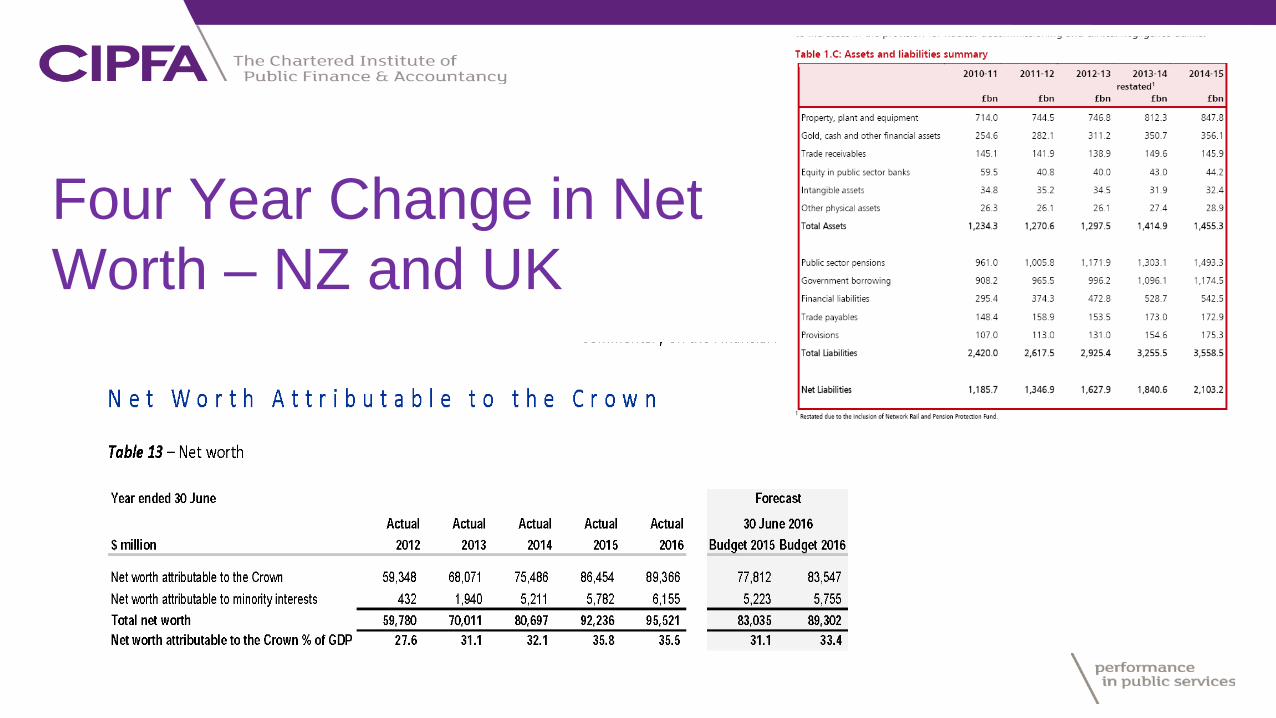

And comparatively?

cipfa.org

Four Year Change in Net Worth – NZ and UK

cipfa.org

cipfa.org

Context of the PFM World - 2017

• Growth• Debt• Tax

– Cooperation– Competition

• Uncertainty• Globalization

cipfa.org

Context of the PFM World - 2017

• Growth• Debt• Tax

– Competition– Cooperation

• Uncertainty• Globalization

cipfa.org

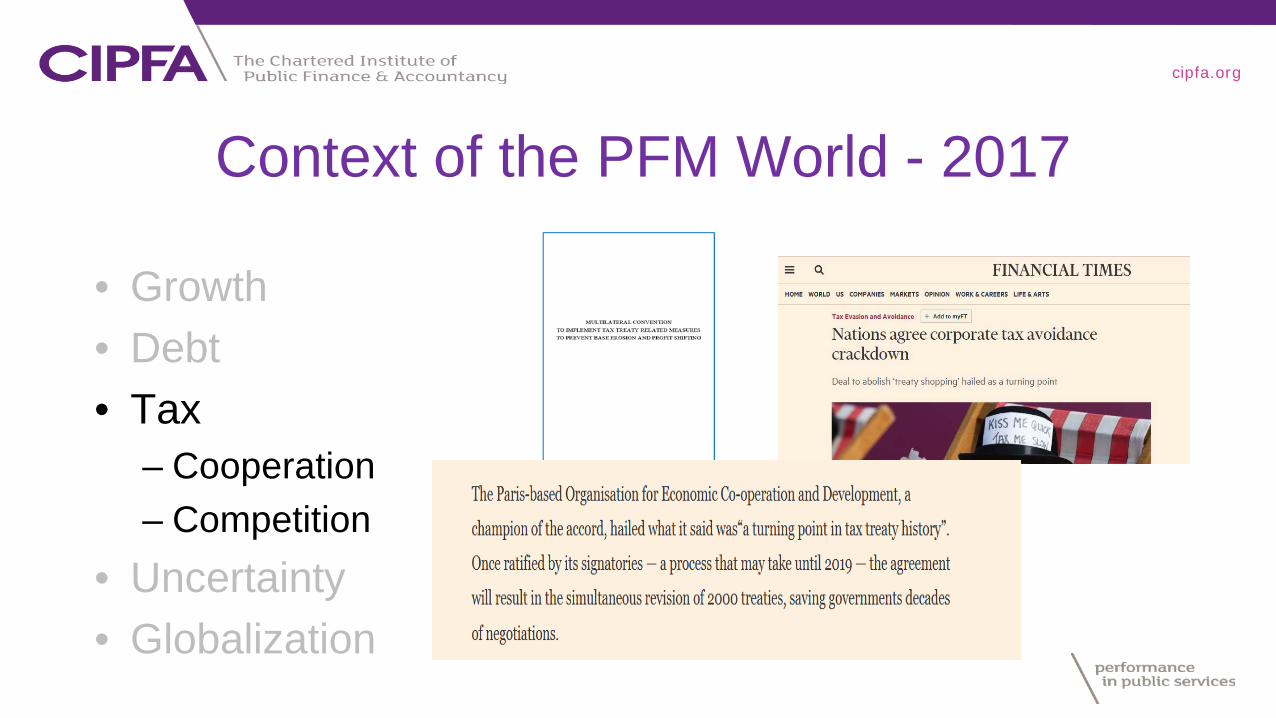

Context of the PFM World - 2017

• Growth• Debt• Tax

– Competition– Cooperation

• Uncertainty• Globalization

cipfa.org

Context of the PFM World - 2017

• Growth• Debt• Tax

– Cooperation– Competition

• Uncertainty• Globalization

cipfa.org

Context of the PFM World - 2017

• Growth• Debt• Tax

– Cooperation– Competition

• Uncertainty• Globalization

cipfa.org

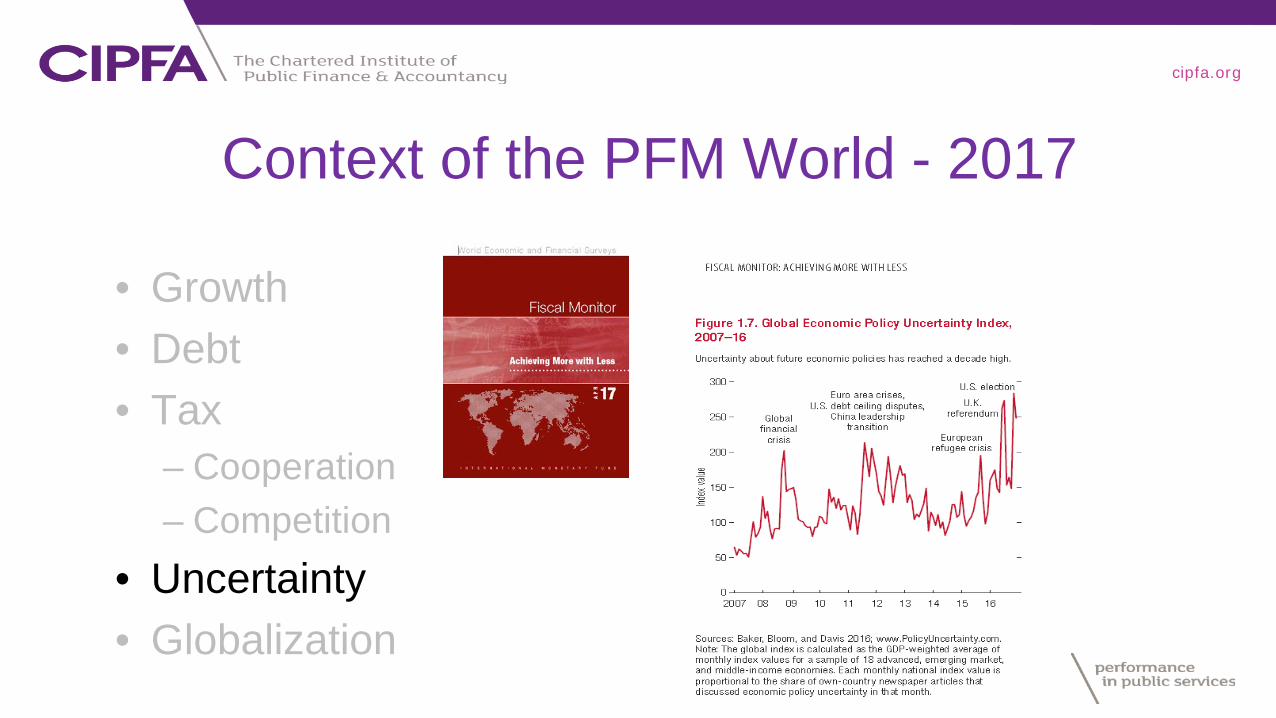

Context of the PFM World - 2017

• Growth• Debt• Tax

– Cooperation– Competition

• Uncertainty• Globalization

cipfa.org

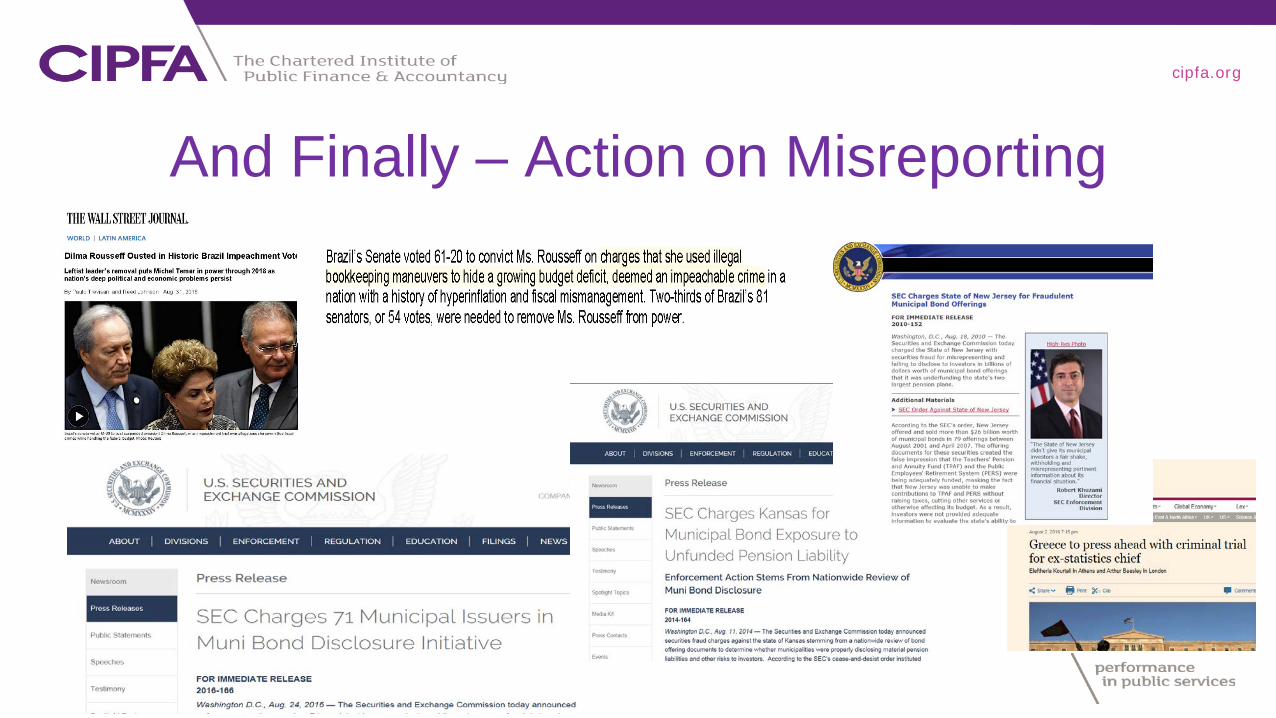

And Finally – Action on Misreporting

cipfa.org

Current and Future Challenges

• Setting standards – technical program• Convergence – Countries, IFRS and SNA/GFS

– Institutional pressures to diverge

• Usefulness (coming full circle)– Performance management (core to PFM)– Fiscal management

• Establishing a role in fiscal policy• Authority – can IPSAS be mandatory?• Governance – who is independent?

For example, a government’s policies will not be sustainable if they significantly reduce its net worth.

cipfa.org

IPSAS at 20: Origins and ChallengesorA Walk Down Memory Lane…

Ian BallChair, Audit Committee for Financial Statements of the NZ GovernmentChair, CIPFA International

Winterthur, 3 July, 2017