ipd index guide - european commissionec.europa.eu/finance/consultations/2012/benchmarks/docs/... ·...

TRANSCRIPT

IPD Index GuideEdition Eight

2012

1 IPD.com/IndexSchedule

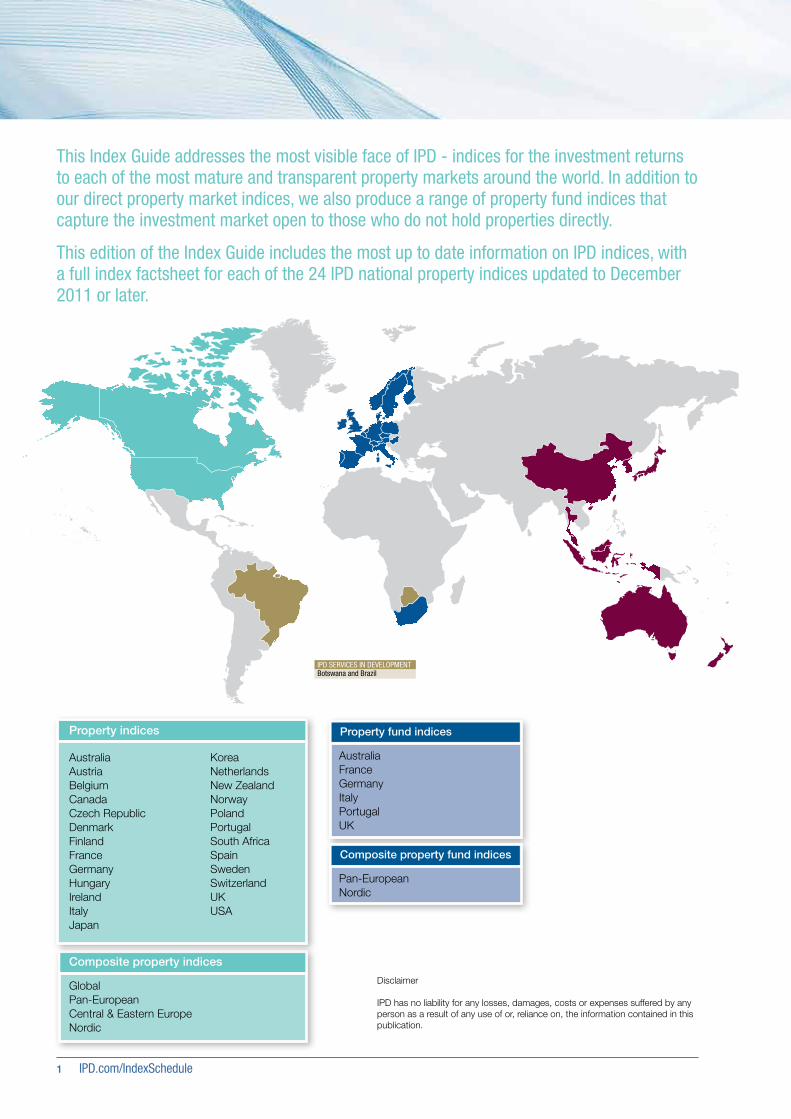

IPD SERVICES IN DEVELOPMENTBotswana and Brazil

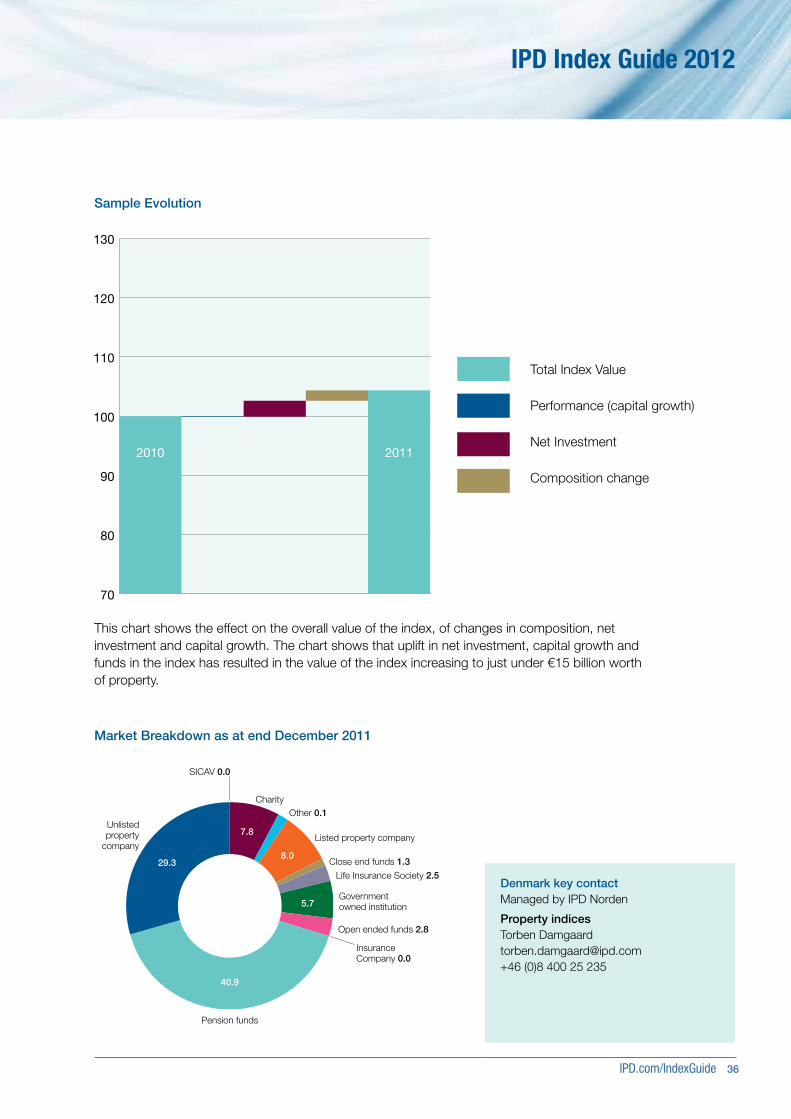

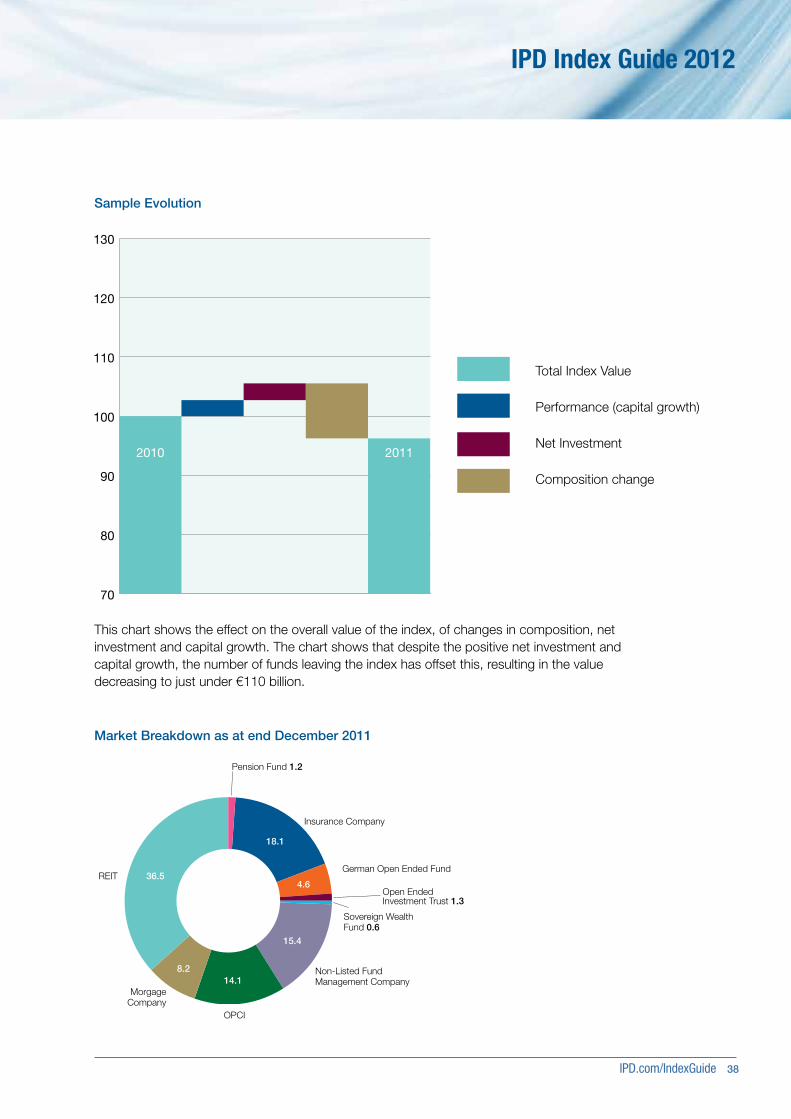

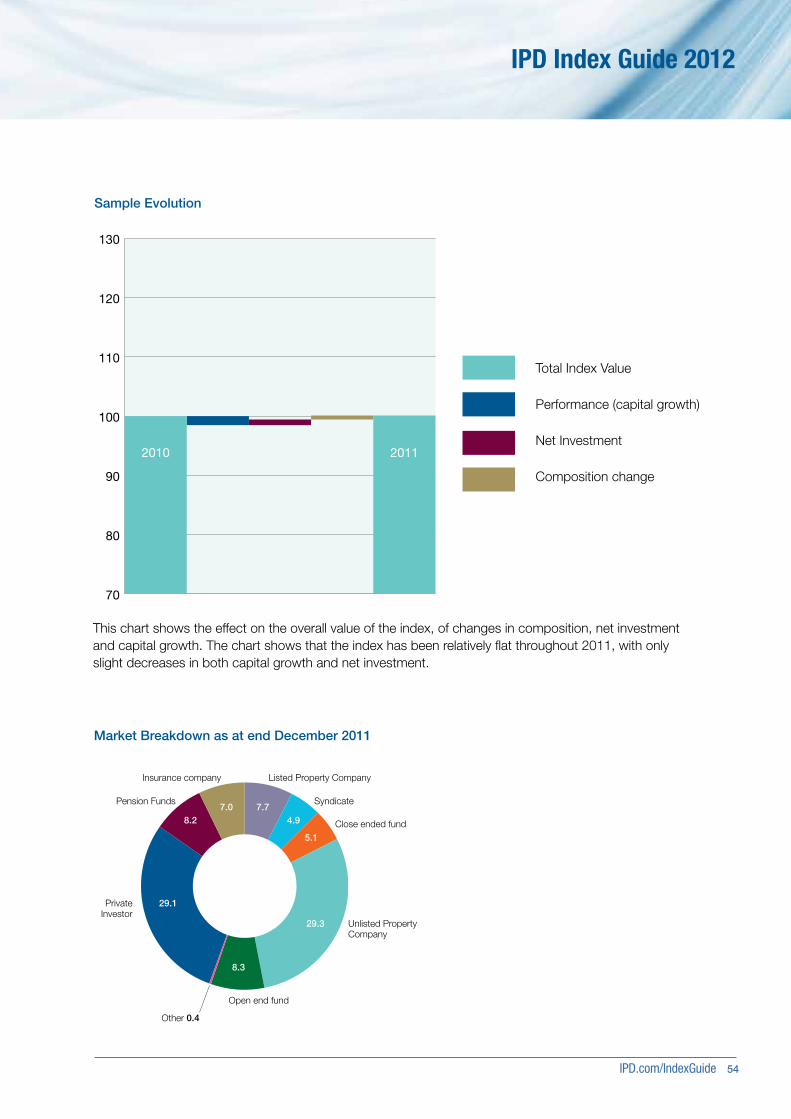

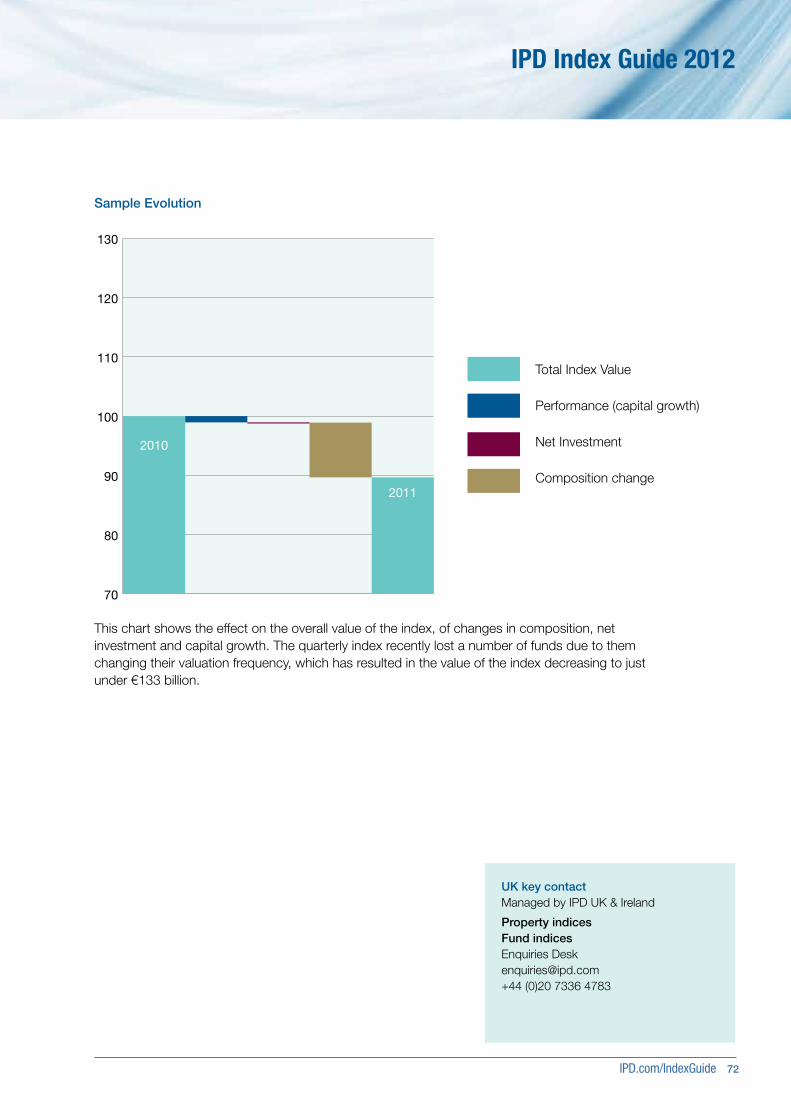

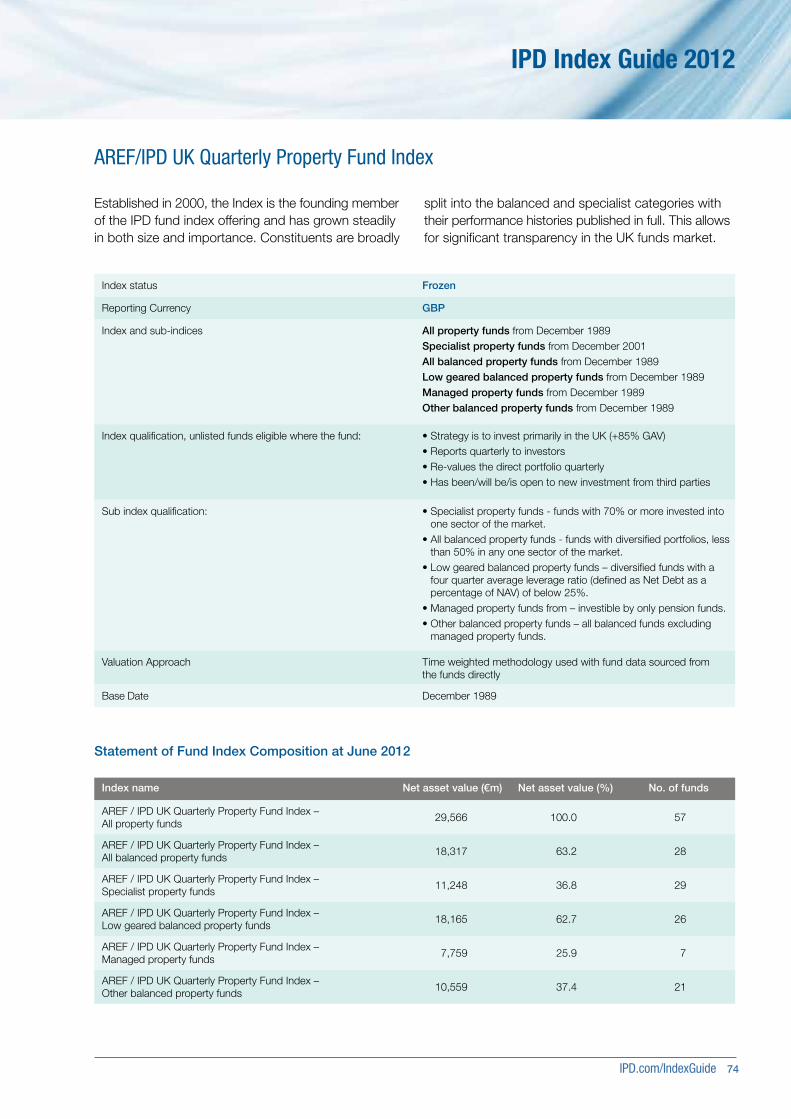

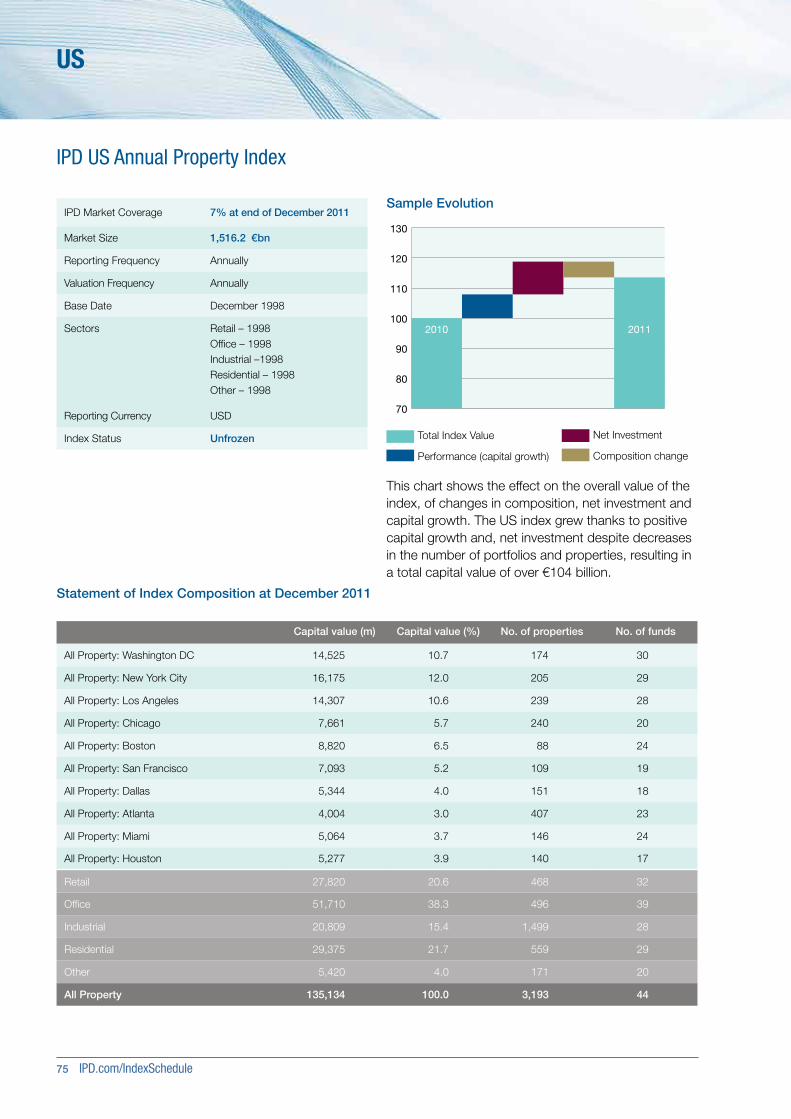

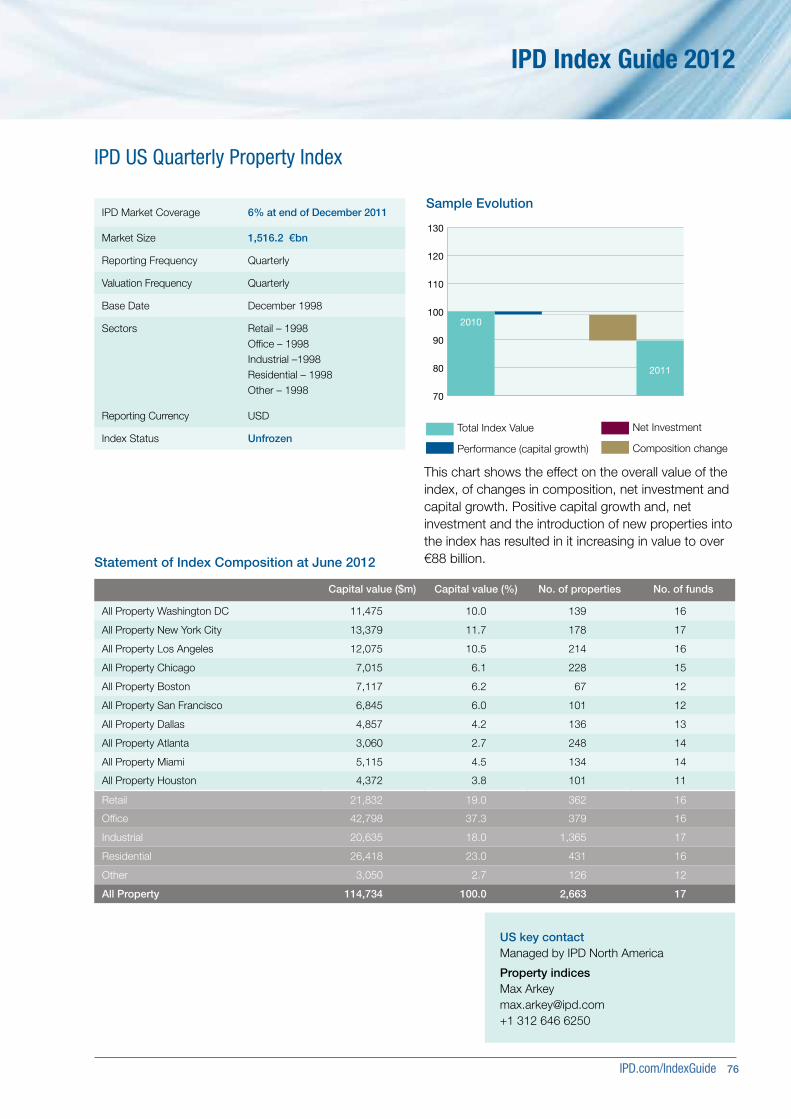

This Index Guide addresses the most visible face of IPD - indices for the investment returns to each of the most mature and transparent property markets around the world. In addition to our direct property market indices, we also produce a range of property fund indices that capture the investment market open to those who do not hold properties directly.

This edition of the Index Guide includes the most up to date information on IPD indices, with a full index factsheet for each of the 24 IPD national property indices updated to December 2011 or later.

Property fund indices

Composite property fund indices

AustraliaFranceGermanyItalyPortugalUK

Pan-EuropeanNordic

GlobalPan-EuropeanCentral & Eastern EuropeNordic

Property indices

Composite property indices

AustraliaAustriaBelgiumCanadaCzech RepublicDenmarkFinlandFranceGermanyHungaryIrelandItalyJapan

KoreaNetherlandsNew ZealandNorwayPolandPortugalSouth AfricaSpainSwedenSwitzerlandUKUSA

Disclaimer

IPD has no liability for any losses, damages, costs or expenses suffered by any person as a result of any use of or, reliance on, the information contained in this publication.

IPD.com/IndexGuide 2

IPD Index Guide 2012

ContentsIPD Property Indices ........................................................................................................3

IPD Property Fund Indices ...............................................................................................5

IPD Indices for European and Global markets .................................................................7

Property Indices .........................................................................................................7Property Fund Indices ................................................................................................8

Index Governance ............................................................................................................9

Indices in development .................................................................................................10

IPD Transaction Linked Indices .................................................................................10

Indices for Derivatives ...................................................................................................12

Computing IPD’s Performance Measures ......................................................................13

Key IPD calculations ................................................................................................13

Computation formulae – Direct property indices ......................................................14

Computation formulae – Property fund indices ........................................................15

Time-weighting ........................................................................................................16

Other index compilation rules ..................................................................................17

Further Information .......................................................................................................18

Index status .............................................................................................................18

IPD property market information ..............................................................................18

Fund market information .........................................................................................19

Acquiring Index Licences ..............................................................................................20

Frequently Asked Questions ..........................................................................................21Index factsheets ............................................................................................................23

Australia .............................................................................................................23Austria ................................................................................................................27Belgium ..............................................................................................................29Canada ..............................................................................................................31Czech Republic ..................................................................................................33Denmark ............................................................................................................35France ................................................................................................................37Germany ............................................................................................................41Hungary .............................................................................................................44Ireland ................................................................................................................45Italy ....................................................................................................................47Japan .................................................................................................................51Korea .................................................................................................................52Netherlands ........................................................................................................53New Zealand ......................................................................................................57Poland ................................................................................................................58Portugal ..............................................................................................................59Spain ..................................................................................................................63Sweden ..............................................................................................................65Switzerland .........................................................................................................67UK ......................................................................................................................69US ......................................................................................................................75

Copyright notice

IPD owns the copyright and all other intellectual property rights in the IPD Index Guide (“The Guide”). You may use The Guide and its contents for your internal business purposes, including making photocopies and extracting insubstantial portions to be used in your own internal documents and in client services on an insubstantial and ad hoc basis. You shall ensure that any reproduction of all or part of The Guide includes the following notice: “source: IPD Ltd © 2012” All rights reserved. IPD has no liability to any person for any losses, damages, costs or expenses suffered as a result of any use of or reliance on any of the informa-tion which may be attributed to it. The Guide (or any part of it) may not be republished without the prior written approval of IPD.

3 IPD.com/IndexSchedule

IPD property indices are calculated at the property level, excluding the impact of debt, fund management fees, taxation and cash on property portfolios.

Our aim is to assemble and maintain consistent, comprehensive financial and descriptive records of real estate assets held in each market. This ensures that property returns can be fairly and precisely reported, and compared across asset classes and national boundaries.

We provide a large number of standard and bespoke benchmarks, as well as research, to support the real estate fund management strategies of property investors worldwide. These are not covered in this Index Guide.

Our main endeavour is to strip away the fund level overlays of cash and debt management, providing a fair and all inclusive comparison of the underlying direct property markets, reporting the undistorted total returns.

To date such indices have been produced for 17 European markets and 7 other global markets. We collaborate with an index providing partner, KTI in Finland, which has enabled the compilation of the IPD Pan-European Annual Property Index (est. 2004), and the launch of the IPD Global Annual Property Index (est.2008).

IPD indices provide the definitive statement of investment returns to many property markets. They measure total returns for all directly held real estate assets (All Property) and the four main market sectors - Retail, Office, Industrial and Residential - wherever they are held in professionally managed portfolios.

Indices can normally be further disaggregated into detailed sub-sectors, regions, size bands etc. IPD indices are definitive because they make use of the largest and most detailed databases on the financial returns of actual buildings held in professionally managed portfolios, and are built upon identical and demanding data capture, computation and reporting regimes.

Chart 1: IPD property index returns in EUR (€) as at end-2011

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

To

tal r

etur

n %

pa

Global

Pan-European

Nordic

CEE

Australia

Austria

Belgium

Canada

Czech Republic

Denmark

Finland (KTI)

France

Germany

Hungary

Ireland

Italy

Japan

Korea

Netherlands

New Zealand

Norway

Poland

Portugal

South Africa

Spain

Sweden

Switzerland

UK

USA

IPD Property Indices

IPD.com/IndexGuide 4

IPD Index Guide 2012

Comparability with other major asset classes, identifying trends in key market sectors and assessing property performance in different countries. For this reason, IPD indices have been specifically developed to be as consistent as possible with those used in mainstream investment analysis.

Frequency of annual results, with some countries also having biannual, quarterly and monthly indices, dependent upon the frequency of local market valuation practices.

Long term reporting with IPD data time series of a significant length. IPD indices can be used as a basis for risk analysis, forecasting and financial derivatives. They are published as soon as possible after the end of each reporting period using monthly time weighted returns.

Availability of headline results freely available from ipd.com, reflecting our objective to bring transparency and better information to the world’s property investment markets.

Standardised performance measures for each national and composite market, supplemented by further measures specifically applicable to that market.

All growth and index calculations are value weighted, i.e. each property contributes to the result in proportion to its capital value, and compounded monthly to report time weighted measures for quarterly, biannual and longer periods.

All IPD index performance measures are nominal, i.e. they do not take inflation into account. However, it is possible to calculate real total return, income return and capital growth by deflating these measures by inflation.

Open market valuations to provide the most comprehensive and authoritative coverage possible. All valuations used in IPD indices have been produced by property professionals for investment purposes, to a standard definition of capital value in each national market.

Property market returns covering ‘standing investments’, i.e. completed and letable properties, excluding properties that are purchased, sold or in the course of development during the measurement period. This ensures that IPD indices only reflect market returns and are not influenced by abnormal profits or losses which may be generated through active management. Exclusive use of standing investments also ensures consistency with indices available for other types of investment assets.

Directly owned properties from the organisations that contribute data to IPD, and not those that are held indirectly through investment vehicles, such as Property Unit Trusts. This ensures IPD indices reflect the underlying performance of assets, independent of any borrowing or financial management regime. They do not include any bonds, cash or derivative, or REIT share holdings.

Full transparency making it possible to conduct extensive analysis of the properties and mechanisms driving the underlying published return figures.IPD indices are compiled from records of individual properties; they are completely transparent in terms of samples used and calculations applied. Reporting confidentiality procedures are strictly governed so that no individual fund/property results are inadvertently divulged. Minimum requirements for release of any aggregated data is five assets across three ownerships.

5 IPD.com/IndexSchedule

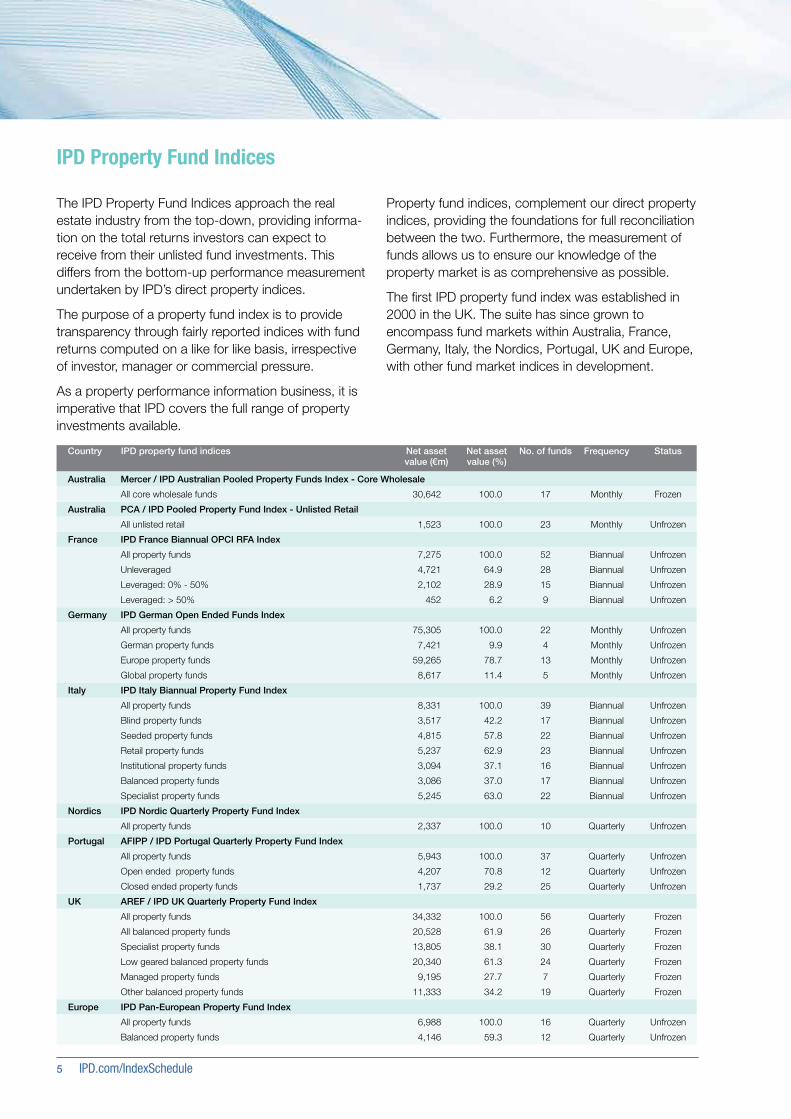

The IPD Property Fund Indices approach the real estate industry from the top-down, providing informa-tion on the total returns investors can expect to receive from their unlisted fund investments. This differs from the bottom-up performance measurement undertaken by IPD’s direct property indices.

The purpose of a property fund index is to provide transparency through fairly reported indices with fund returns computed on a like for like basis, irrespective of investor, manager or commercial pressure.

As a property performance information business, it is imperative that IPD covers the full range of property investments available.

Country IPD property fund indices Net asset value (€m)

Net asset value (%)

No. of funds Frequency Status

Australia Mercer / IPD Australian Pooled Property Funds Index - Core Wholesale

All core wholesale funds 30,642 100.0 17 Monthly Frozen

Australia PCA / IPD Pooled Property Fund Index - Unlisted Retail

All unlisted retail 1,523 100.0 23 Monthly Unfrozen

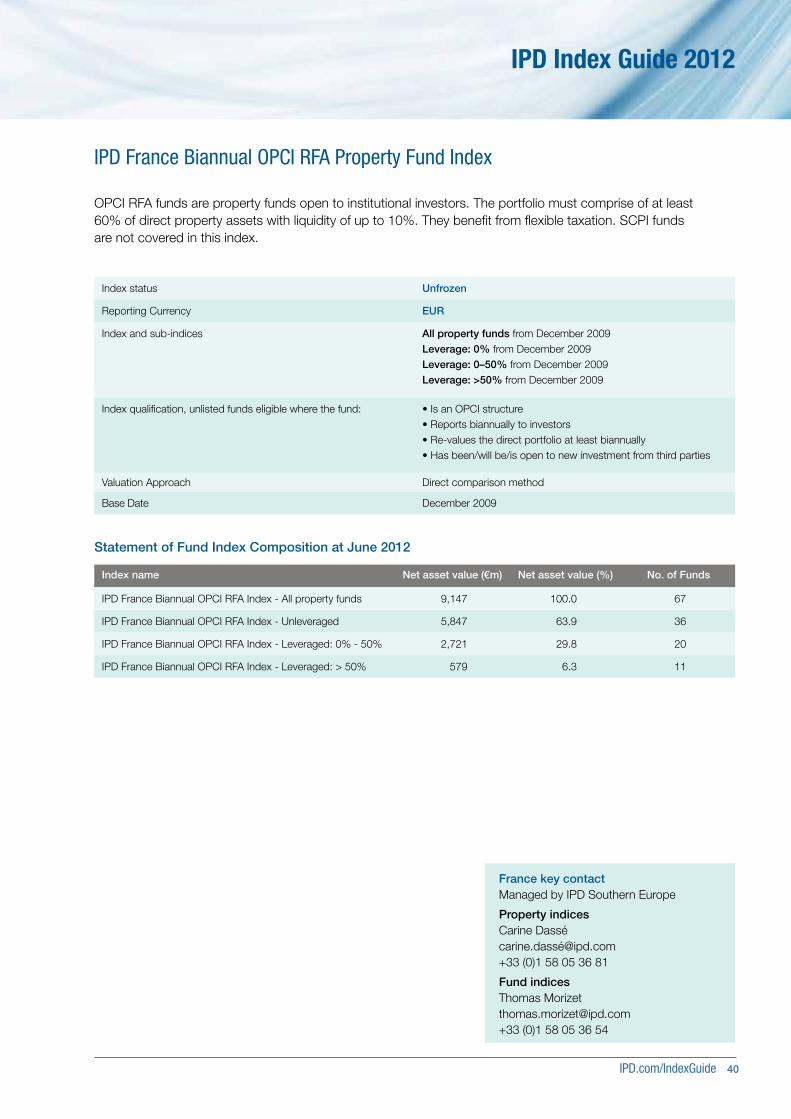

France IPD France Biannual OPCI RFA Index

All property funds 7,275 100.0 52 Biannual Unfrozen

Unleveraged 4,721 64.9 28 Biannual Unfrozen

Leveraged: 0% - 50% 2,102 28.9 15 Biannual Unfrozen

Leveraged: > 50% 452 6.2 9 Biannual Unfrozen

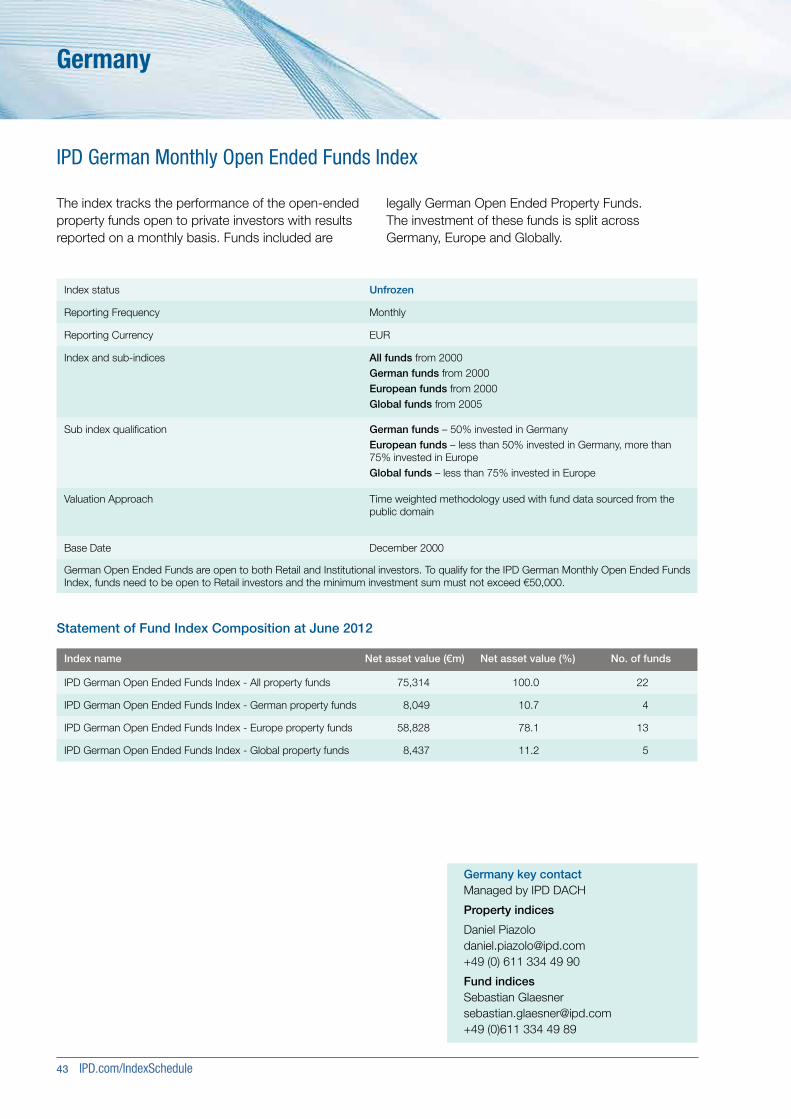

Germany IPD German Open Ended Funds Index

All property funds 75,305 100.0 22 Monthly Unfrozen

German property funds 7,421 9.9 4 Monthly Unfrozen

Europe property funds 59,265 78.7 13 Monthly Unfrozen

Global property funds 8,617 11.4 5 Monthly Unfrozen

Italy IPD Italy Biannual Property Fund Index

All property funds 8,331 100.0 39 Biannual Unfrozen

Blind property funds 3,517 42.2 17 Biannual Unfrozen

Seeded property funds 4,815 57.8 22 Biannual Unfrozen

Retail property funds 5,237 62.9 23 Biannual Unfrozen

Institutional property funds 3,094 37.1 16 Biannual Unfrozen

Balanced property funds 3,086 37.0 17 Biannual Unfrozen

Specialist property funds 5,245 63.0 22 Biannual Unfrozen

Nordics IPD Nordic Quarterly Property Fund Index

All property funds 2,337 100.0 10 Quarterly Unfrozen

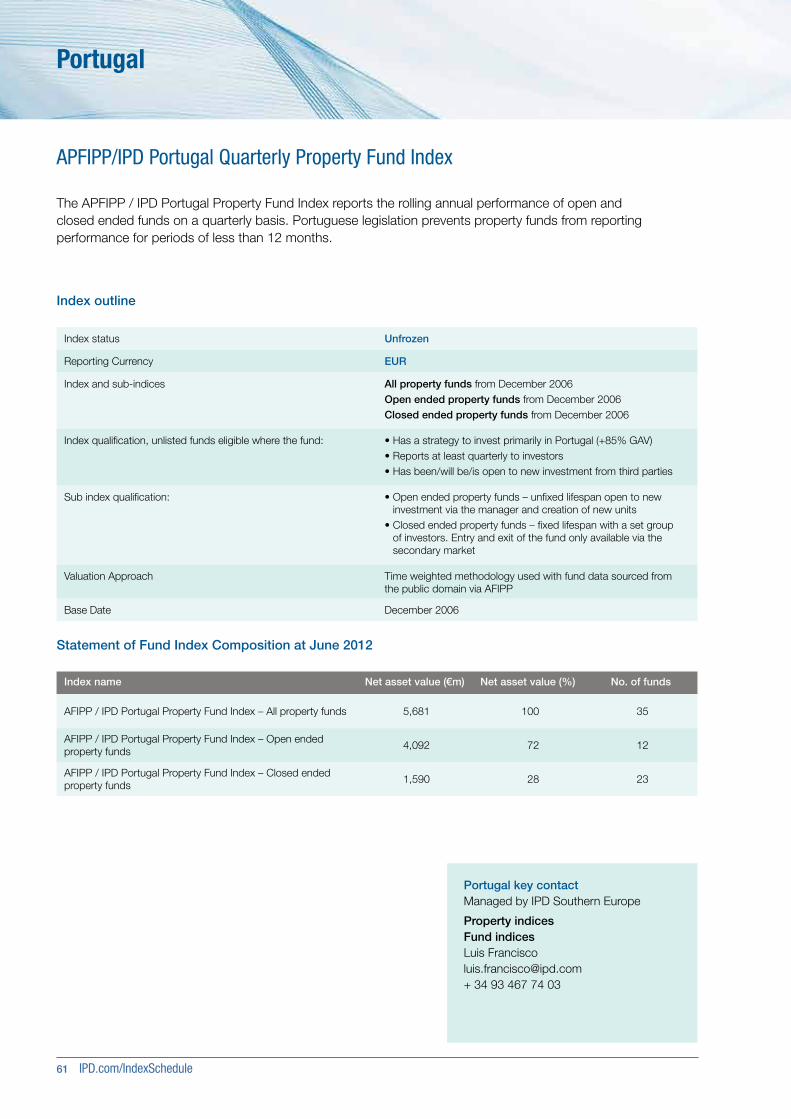

Portugal AFIPP / IPD Portugal Quarterly Property Fund Index

All property funds 5,943 100.0 37 Quarterly Unfrozen

Open ended property funds 4,207 70.8 12 Quarterly Unfrozen

Closed ended property funds 1,737 29.2 25 Quarterly Unfrozen

UK AREF / IPD UK Quarterly Property Fund Index

All property funds 34,332 100.0 56 Quarterly Frozen

All balanced property funds 20,528 61.9 26 Quarterly Frozen

Specialist property funds 13,805 38.1 30 Quarterly Frozen

Low geared balanced property funds 20,340 61.3 24 Quarterly Frozen

Managed property funds 9,195 27.7 7 Quarterly Frozen

Other balanced property funds 11,333 34.2 19 Quarterly Frozen

Europe IPD Pan-European Property Fund Index

All property funds 6,988 100.0 16 Quarterly Unfrozen

Balanced property funds 4,146 59.3 12 Quarterly Unfrozen

Property fund indices, complement our direct property indices, providing the foundations for full reconciliation between the two. Furthermore, the measurement of funds allows us to ensure our knowledge of the property market is as comprehensive as possible.

The first IPD property fund index was established in 2000 in the UK. The suite has since grown to encompass fund markets within Australia, France, Germany, Italy, the Nordics, Portugal, UK and Europe, with other fund market indices in development.

IPD Property Fund Indices

IPD.com/IndexGuide 6

IPD Index Guide 2012

Performance is tracked as close to local market reporting timeframes as possible, with index publication frequencies of monthly, quarterly, biannual and annual.

Property fund indices provide funds with the opportunity to demonstrate their transparency and manager expertise as their fund information is published alongside their peers. Where fund specific returns are unavailable, IPD lists those managers that have contributed, in an effort to stimulate transparency. It should be noted that not all markets allow for the disclosure of fund specific returns, at which point only headline aggregate results are published.

Availability of headline results on ipd.com, with additional data freely available to data contributors. Bespoke requests can also be accommodated.

Data usage in reports and presentations, provided results are correctly sourced to the IPD index. Index contributors are entitled to use property fund indices for benchmarking, however, non-contributors must obtain prior agreement from IPD in the form of a license.

IPD property funds database contains descriptive and financial information for each fund. Data is standardised to allow comparability and gathered directly from the funds and third party industry bodies.

Index qualification is based on a fund being, or intending to be, open to third parties. Further inclusion criteria and rules are applied in accordance with local market specifics. A fund must provide consistent and continuous data, to an acceptable standard and in accordance with local index rules.

Sub indices follow a standard headline index of All Funds, and can be broken into sub indices in relation to local market specifics such as sector investment (balanced or specialist funds), structure (open-ended or closed-ended funds) and leverage (low or high geared funds). Samples may also be divided by region.

Currency outputs allow the user to monitor the effect of currency fluctuations. Fund data is collected in the fund’s local reporting currency. Once in the system, all figures are then converted into GBP, based on that month’s exchange rate, and then converted again into EUR, USD, JPY and Local (today’s exchange rate applied historically to all data).

Alternatively, local currency allows the user to see fund performance without the impact of currency movements.

7 IPD.com/IndexSchedule

Property Indices

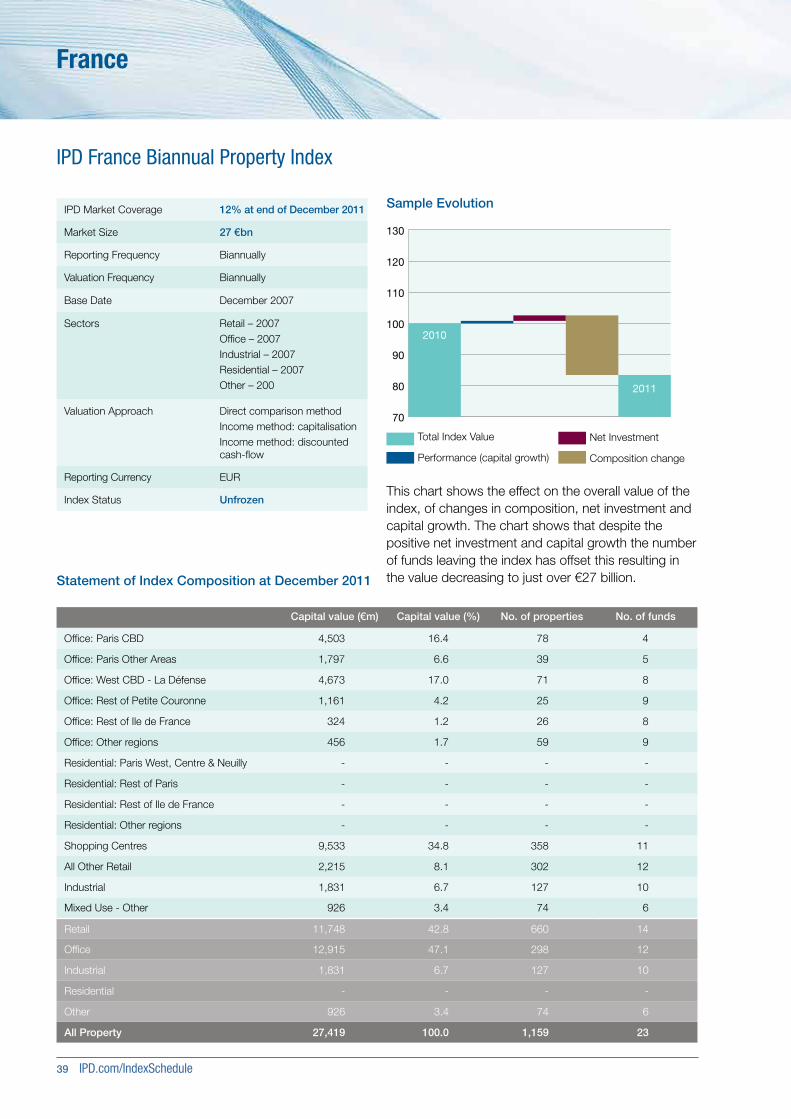

IPD publishes indices in 17 European markets, and 7 non-European markets. Most IPD indices are annual, with quarterly indices available for Ireland, Netherlands, UK and the US. Annual indices are reported quarterly in Australia, New Zealand and Canada. Biannual indices and indicators are available for France, Italy and South Africa. Monthly indices are available for the UK and Japan.

IPD Indices for European and Global markets

No. of funds

No. of properties

Capital value

Total market size estimate

IPD coverage

Status Frequency

(€bn) ($bn) (€bn) ($bn) (%)

Australia 70 1,670 103.8 134.8 182.5 236.9 56.9 Unfrozen Quarterly

Austria 16 595 6.7 8.6 22.8 29.6 29.2 Unfrozen Annual

Belgium 35 376 8.2 10.7 47.6 61.8 17.3 Consultative Annual

Canada 42 2,141 72.0 93.5 139.8 181.5 51.5 Unfrozen Quarterly

Czech Republic 22 120 2.9 3.7 11.2 14.5 25.9 Consultative Annual

Denmark 20 1,033 14.7 19.0 34.4 44.7 42.6 Unfrozen Annual

Finland (KTI) 21 2,272 21.3 27.6 42.9 55.7 49.6 Unfrozen Annual

France 112 6,932 109.5 142.1 236.3 306.8 46.3 Frozen Annual, Biannual

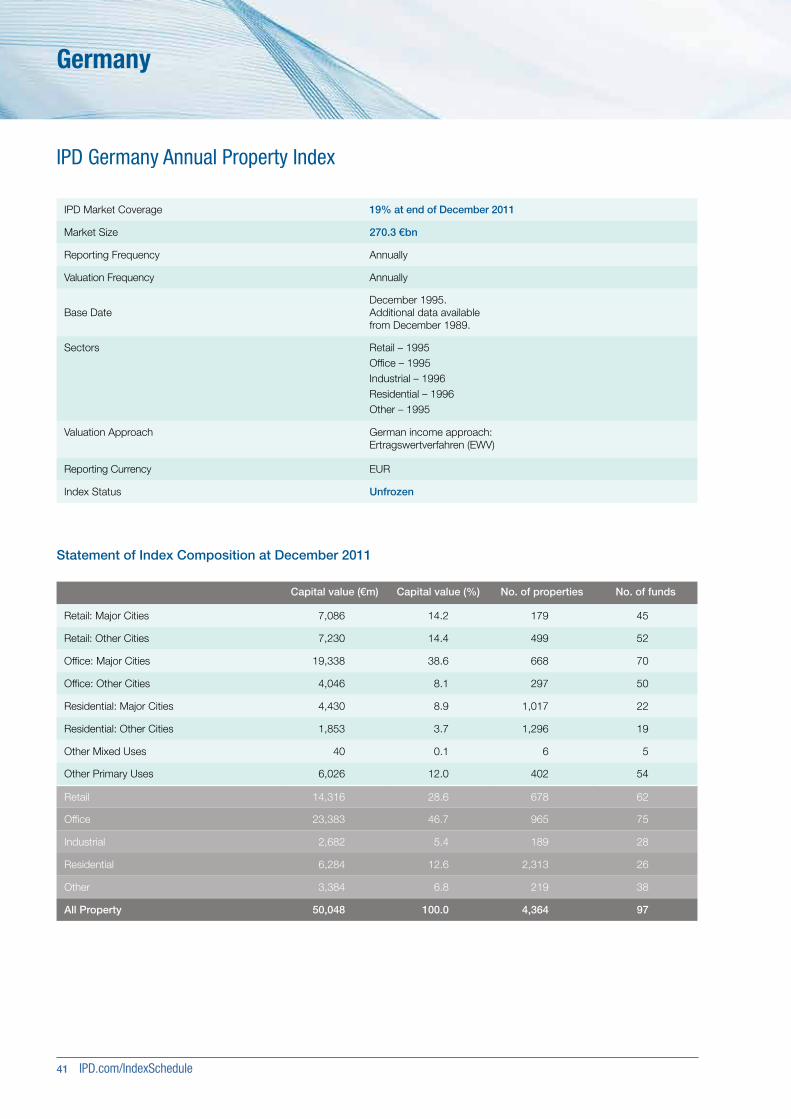

Germany 97 4,364 50.0 65.0 270.3 350.9 18.5 Unfrozen Annual

Hungary 20 107 2.2 2.8 9.1 11.9 23.7 Consultative Annual

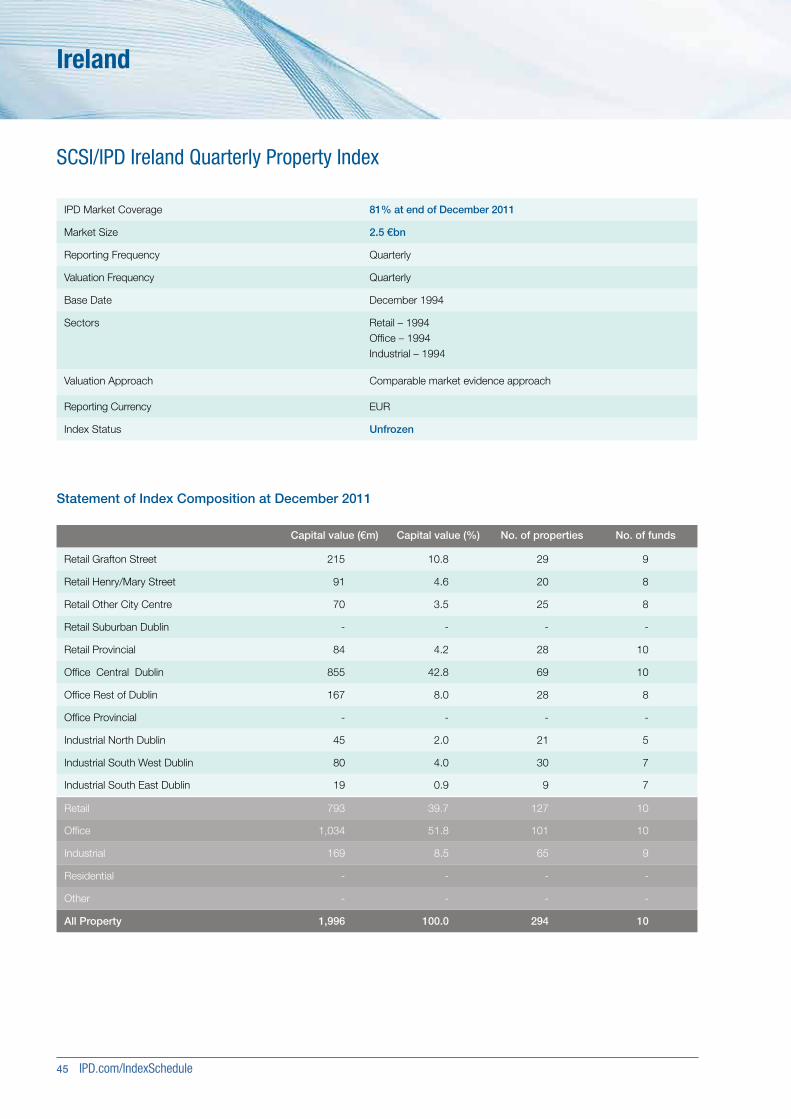

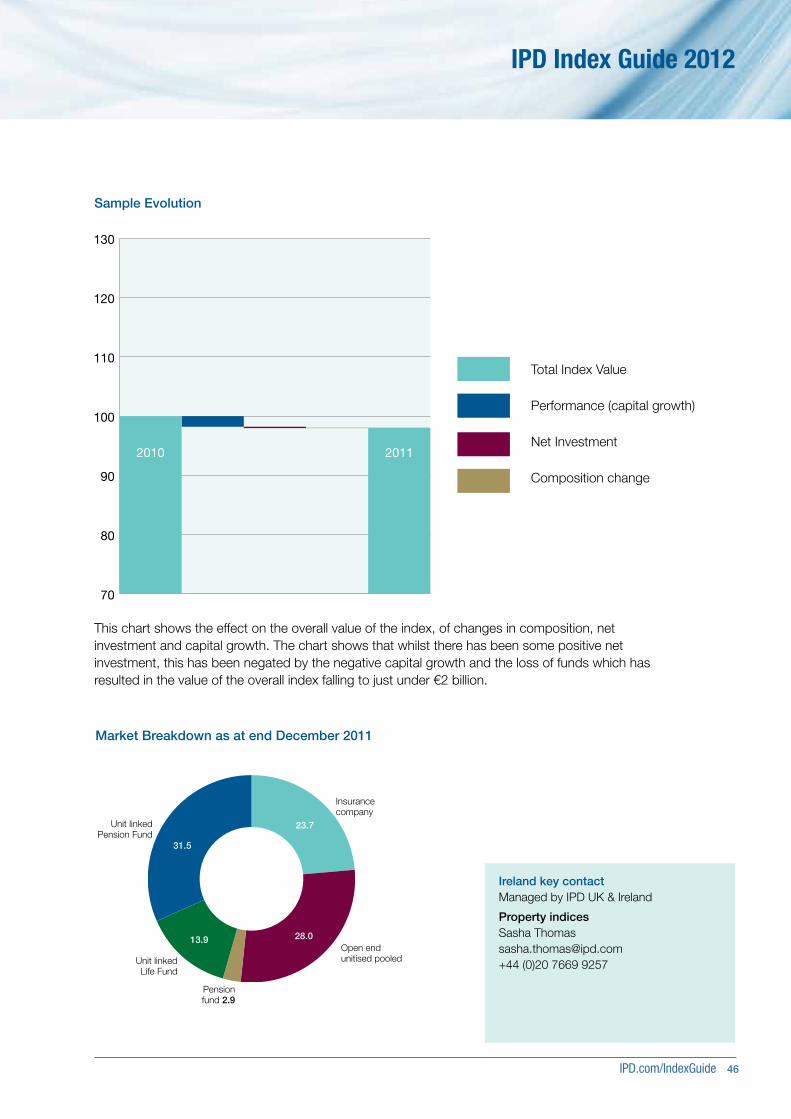

Ireland 12 328 2.3 3.0 2.5 3.3 90.1 Unfrozen Quarterly

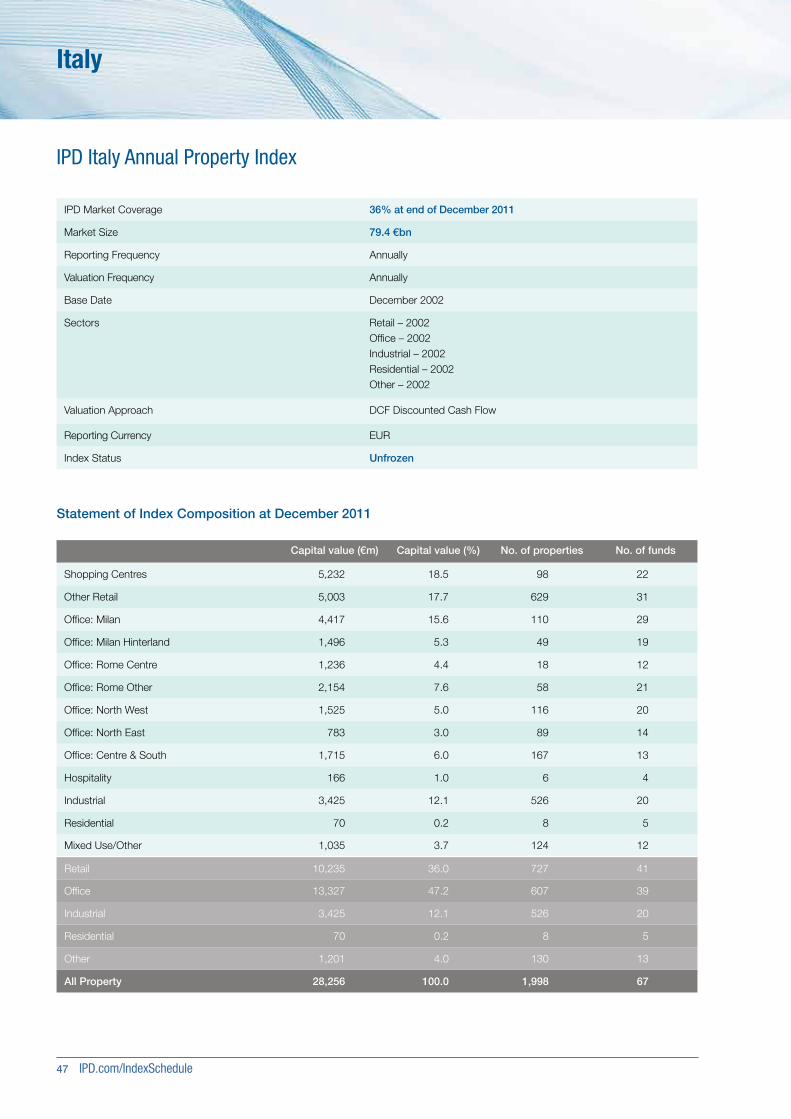

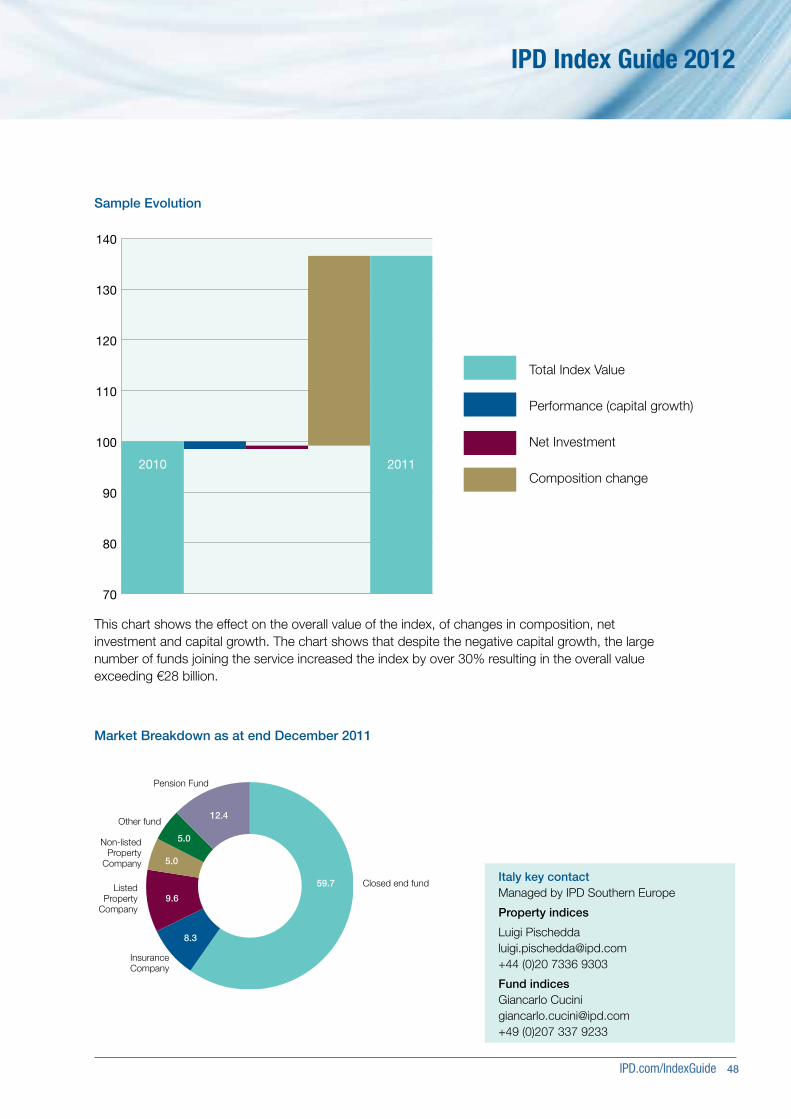

Italy 67 1,998 28.3 36.7 79.5 103.2 35.6 Unfrozen Annual, Biannual

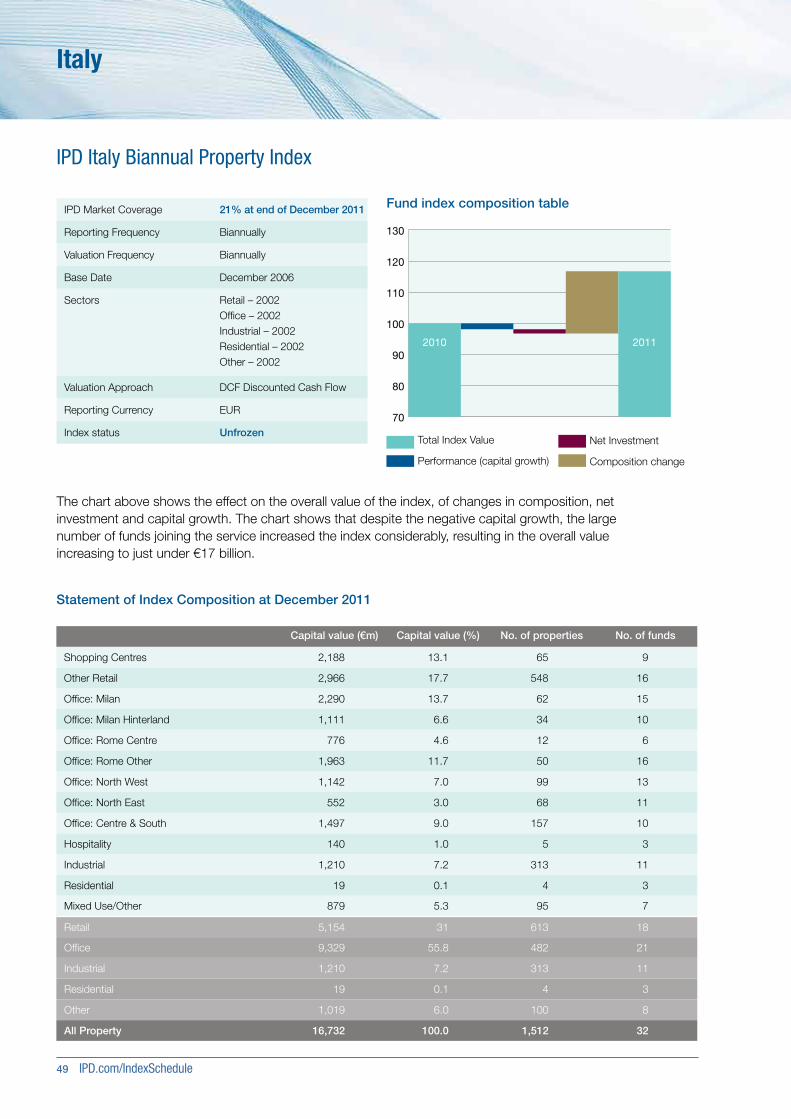

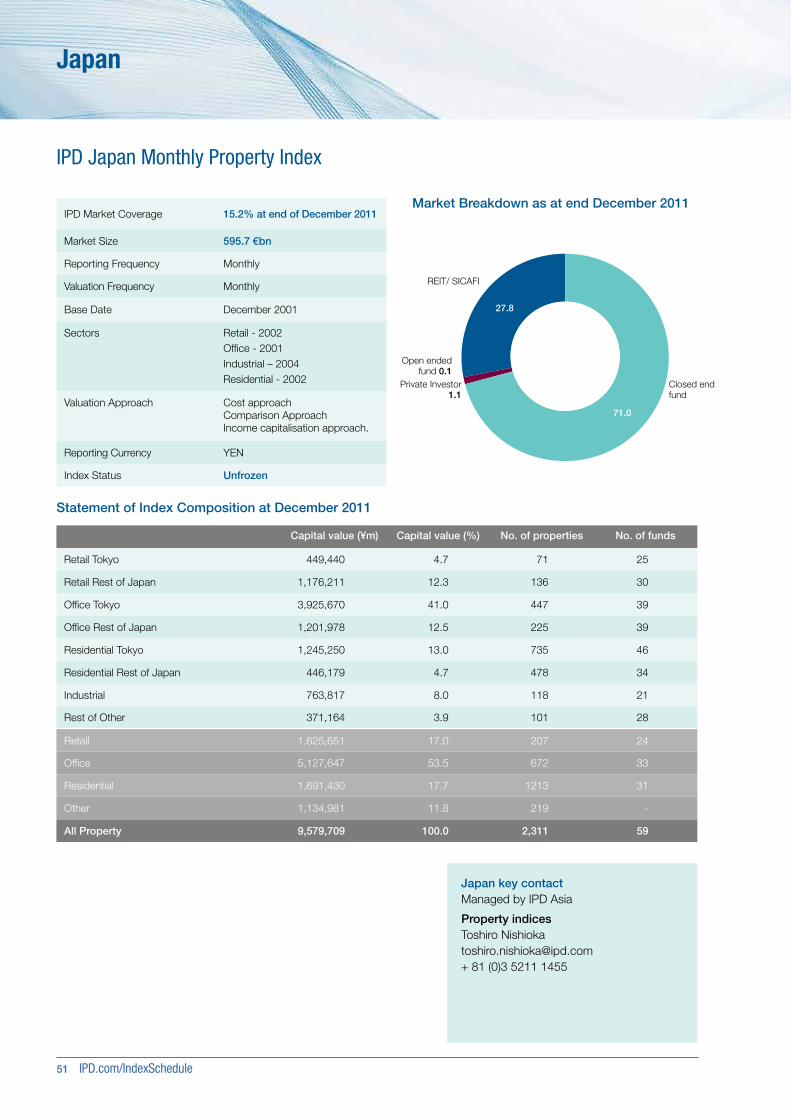

Japan 57 2,131 90.7 117.7 595.7 773.3 15.2 Unfrozen Monthly

Korea 27 120 9.4 12.2 38.1 49.5 24.7 Consultative Annual

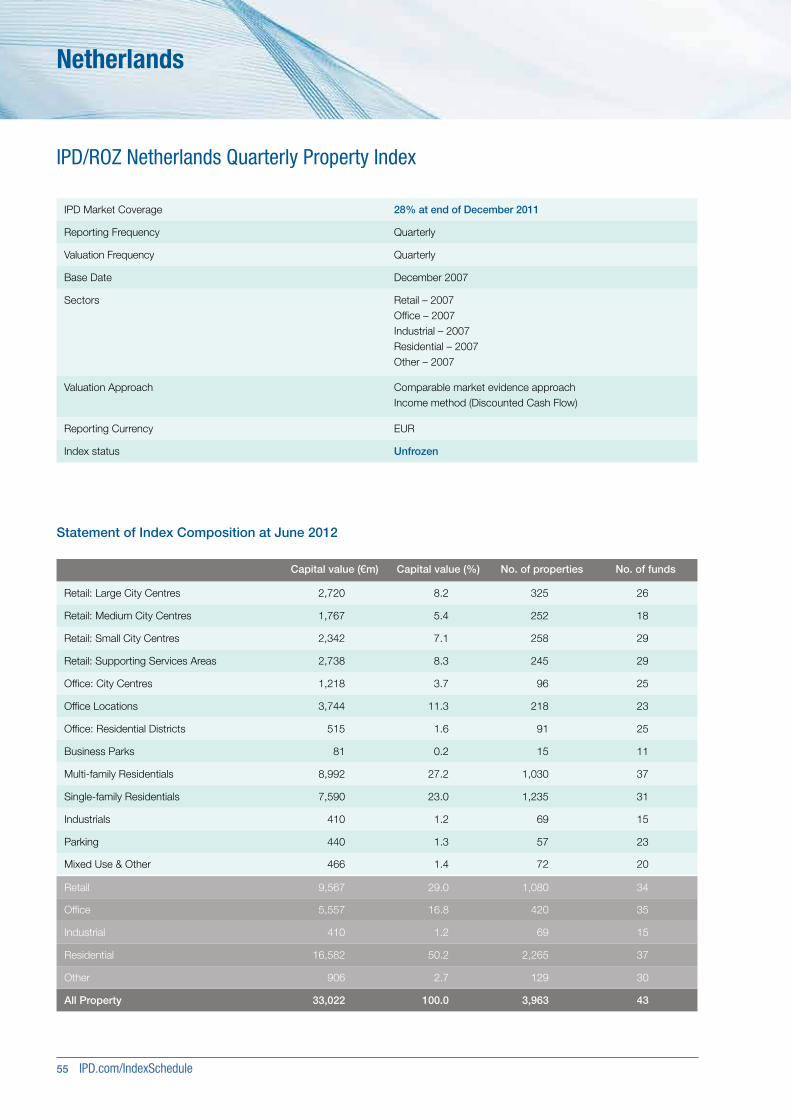

Netherlands 59 4,620 38.9 50.5 117.2 152.2 33.2 Frozen Annual, Quarterly

New Zealand 26 585 6.4 8.3 9.6 12.5 66.1 Unfrozen Quarterly

Norway 14 569 16.2 21.0 40.2 52.2 40.2 Unfrozen Annual

Poland 27 232 5.4 7.1 16.2 21.1 33.5 Consultative Annual

Portugal 41 998 9.9 12.8 15.1 19.6 65.5 Unfrozen Annual

South Africa 22 2,017 19.5 25.4 30.9 40.1 63.3 Unfrozen Annual, Biannual Indicator

Spain 50 523 17.8 23.1 41.0 53.2 43.4 Unfrozen Annual

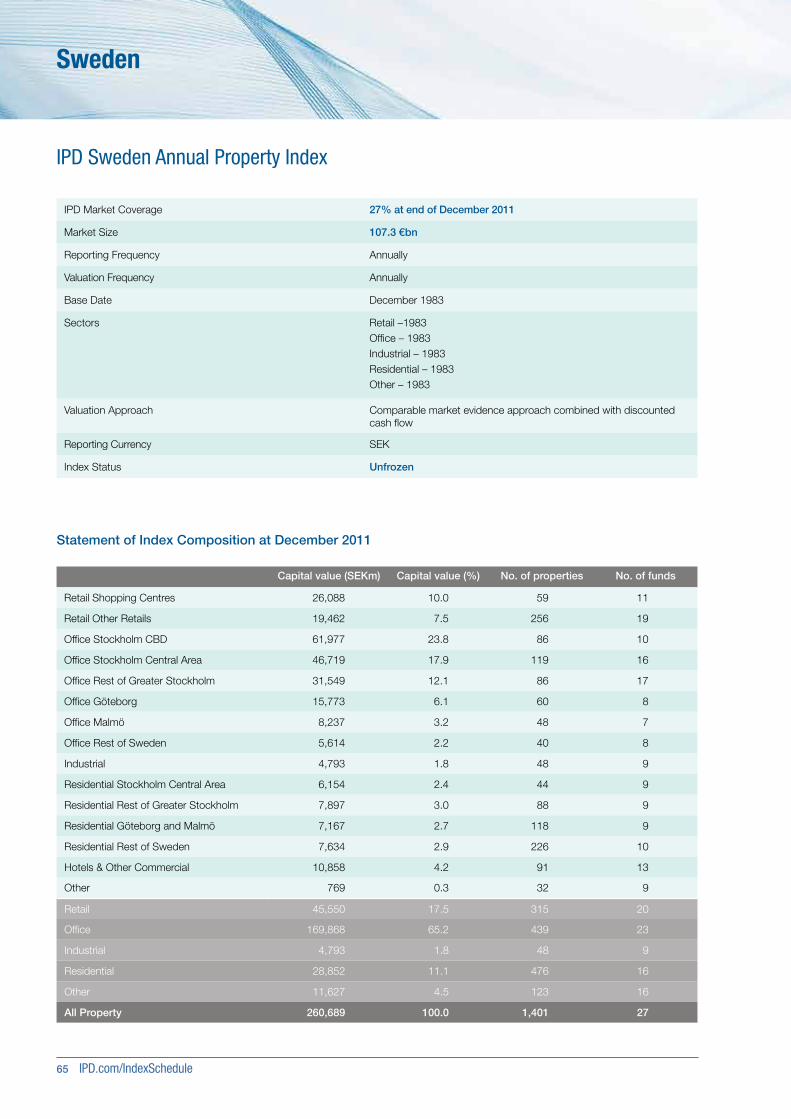

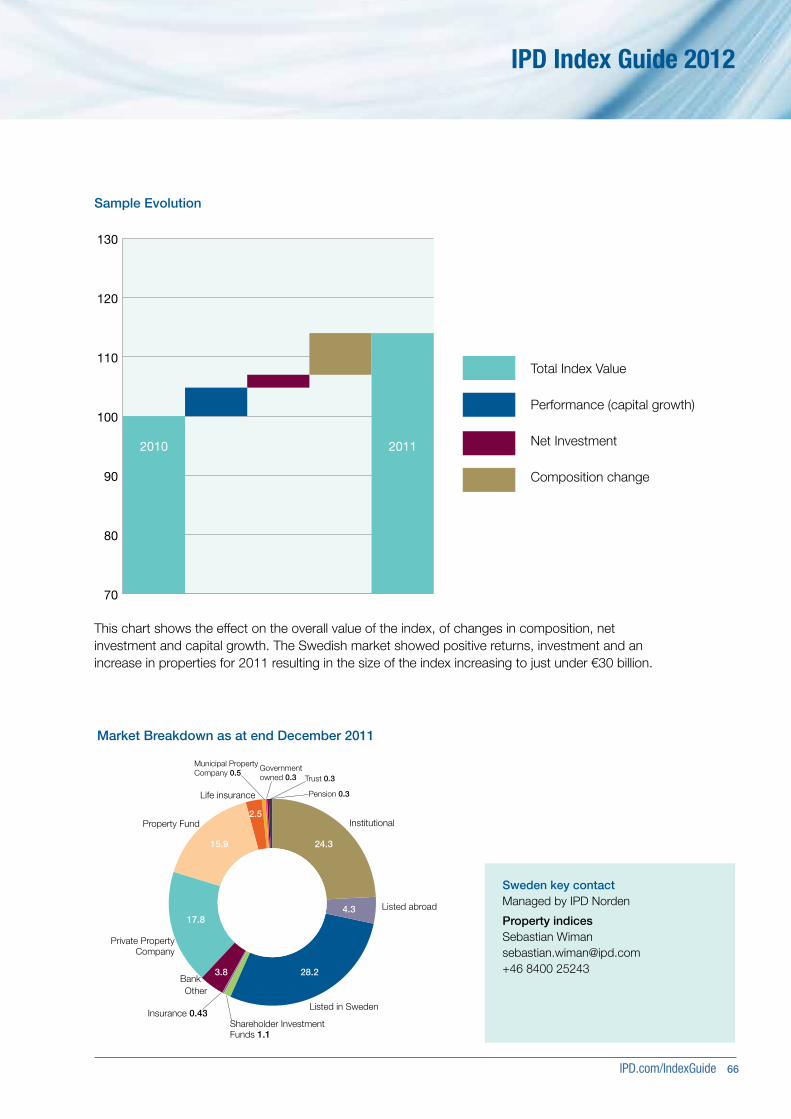

Sweden 27 1,401 29.3 38.0 107.3 139.3 27.3 Unfrozen Annual

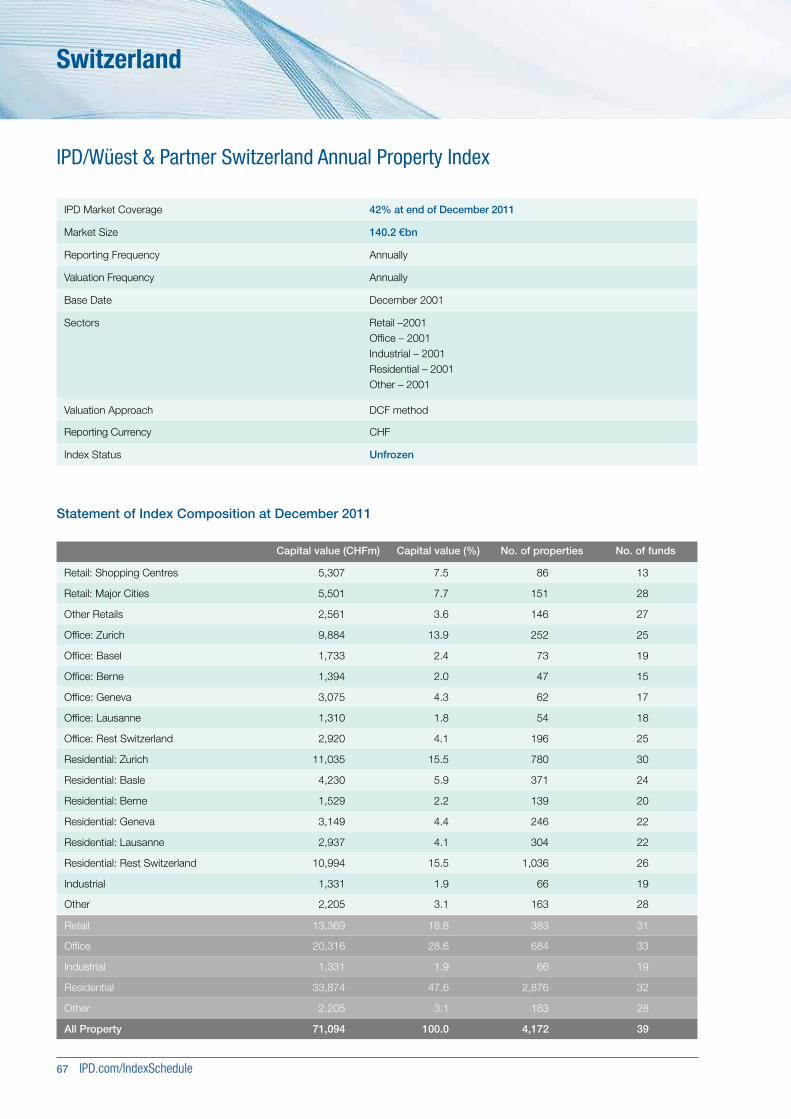

Switzerland 39 4,172 58.6 76.0 140.2 182.0 41.8 Unfrozen Annual

UK 304 20,456 177.4 230.3 284.1 368.8 62.5 Frozen Annual, Quarterly, Monthly

United States 44 3,193 104.1 135.1 1,516.2 1,968.2 6.9 Unfrozen Annual, Quarterly

IPD CEE 35 558 13.9 18.0 79.4 103.1 17.5 Unfrozen Annual

IPD Nordic 82 5,275 83.4 108.3 224.0 290.8 36.2 Unfrozen Annual

IPD Eurozone 510 23,006 292.7 380.0 875.2 1,136.1 33.4 Unfrozen Annual

IPD Pan-European 983 51,096 599.3 778.0 1,518.1 1,970.7 39.5 Unfrozen Annual

IPD Global 1,245 62,368 998.9 1,296.7 4,021.4 5,220.2 24.8 Unfrozen Annual

Databank profiles and estimated market sizes as at December 2011

The table below summarises the IPD index sizes and coverage ratios as at December 2011.

In addition to single country property indices, IPD also collates composite indices. These are formed by taking all properties located across the specific countries. The most well known composite property indices are our Pan-European and Global indices. We also produce indices for the Nordics and Central and Eastern Europe.

IPD.com/IndexGuide 8

IPD Index Guide 2012

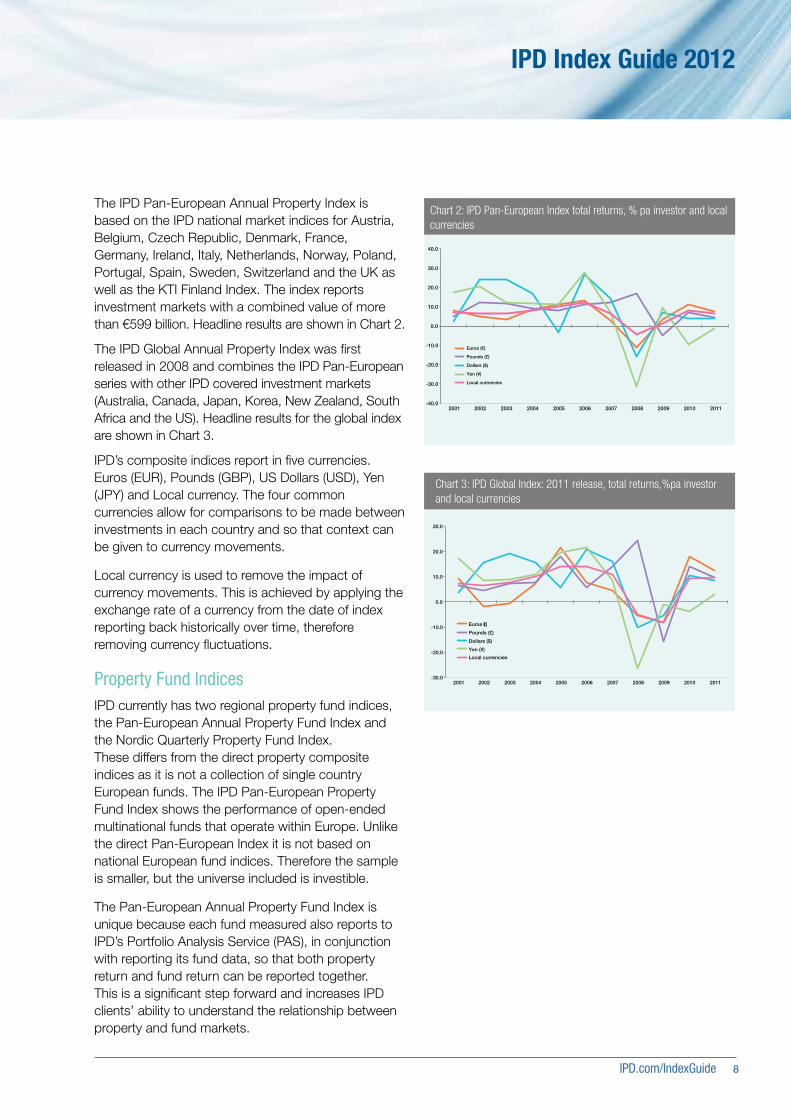

The IPD Pan-European Annual Property Index is based on the IPD national market indices for Austria, Belgium, Czech Republic, Denmark, France, Germany, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Spain, Sweden, Switzerland and the UK as well as the KTI Finland Index. The index reports investment markets with a combined value of more than €599 billion. Headline results are shown in Chart 2.

The IPD Global Annual Property Index was first released in 2008 and combines the IPD Pan-European series with other IPD covered investment markets (Australia, Canada, Japan, Korea, New Zealand, South Africa and the US). Headline results for the global index are shown in Chart 3.

IPD’s composite indices report in five currencies. Euros (EUR), Pounds (GBP), US Dollars (USD), Yen (JPY) and Local currency. The four common currencies allow for comparisons to be made between investments in each country and so that context can be given to currency movements.

Local currency is used to remove the impact of currency movements. This is achieved by applying the exchange rate of a currency from the date of index reporting back historically over time, therefore removing currency fluctuations.

Property Fund IndicesIPD currently has two regional property fund indices, the Pan-European Annual Property Fund Index and the Nordic Quarterly Property Fund Index. These differs from the direct property composite indices as it is not a collection of single country European funds. The IPD Pan-European Property Fund Index shows the performance of open-ended multinational funds that operate within Europe. Unlike the direct Pan-European Index it is not based on national European fund indices. Therefore the sample is smaller, but the universe included is investible.

The Pan-European Annual Property Fund Index is unique because each fund measured also reports to IPD’s Portfolio Analysis Service (PAS), in conjunction with reporting its fund data, so that both property return and fund return can be reported together. This is a significant step forward and increases IPD clients’ ability to understand the relationship between property and fund markets.

Chart 2: IPD Pan-European Index total returns, % pa investor and local currencies

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Euros (€)

Pounds (£)

Dollars ($)

Yen (¥)

Local currencies

Chart 3: IPD Global Index: 2011 release, total returns,%pa investor and local currencies

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Euros (€)

Pounds (£)

Dollars ($)

Yen (¥)

Local currencies

9 IPD.com/IndexSchedule

IPD’s Index Rules cover composition, calculation, content and presentation.

More specific extensions or elaborations are in place for some indices where circumstances require, e.g. UK monthly, Pan-European, Global and Fund indices.

New indices for national markets are titled ‘Consultative’ in their initial releases to highlight the immature nature of their development.

Indicators exist where IPD is able to release mid-year performance data for a market on a sample which is not comparable with that of the annual index.

The composition and construction rules for IPD indices are reviewed regularly by independent, non-executive bodies, referred to as Index Consultative Groups.

Members are drawn from the property investment industry, major universities, research and property consultants, trade associations and investment consulting organisations. These groups exist at national and global levels and meet two or three times each year in most regions.

Data quality, data capture and computation control processes are overseen by IPD’s Business Assurance Unit. The mandate for the unit, which reports directly to an independent Business Audit Committee, is to define quality procedures, audit dataflow and reporting operations for all IPD services. This regime is a result of a major external audit in 2001.

Since 2006, the UK data process audit was extended to encompass client data origination, with randomly selected funds audited on their primary data generation and supply procedures.

Assets are only included in an IPD database if the portfolios within which they are held are reported to IPD in their entirety – including (for benchmarking purposes) all transactions, developments and indirect interests in real estate. Samples from investment portfolios are not accepted.

Index Governance

IPD’s validation process checks each fund for client data errors, errors from data entry and/or data processes. Types of validation issues include:

• Responses outside specified ranges,

• Logical validity of responses in relation to each other (cross checks),

• Missing financial records, or data in essential fields

• Exceptional growth/performance.

IPD.com/IndexGuide 10

IPD Index Guide 2012

Indices in Development

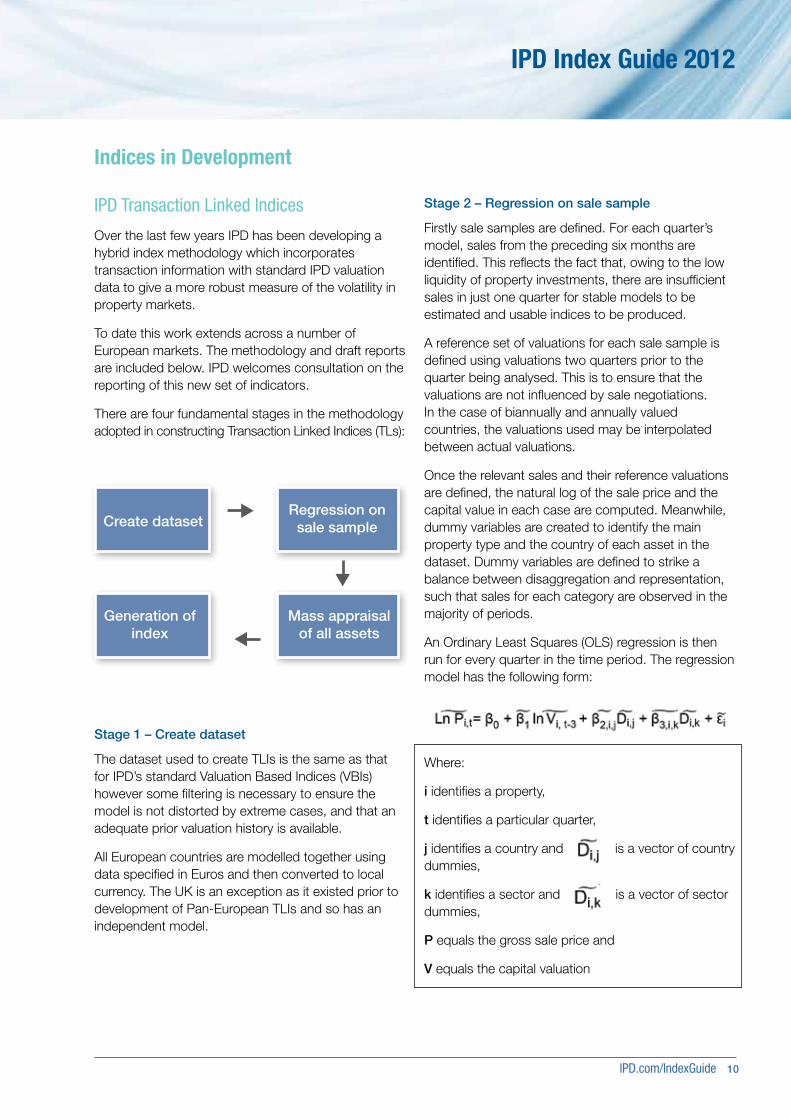

IPD Transaction Linked Indices

Over the last few years IPD has been developing a hybrid index methodology which incorporates transaction information with standard IPD valuation data to give a more robust measure of the volatility in property markets.

To date this work extends across a number of European markets. The methodology and draft reports are included below. IPD welcomes consultation on the reporting of this new set of indicators.

There are four fundamental stages in the methodology adopted in constructing Transaction Linked Indices (TLs):

Stage 1 – Create dataset

The dataset used to create TLIs is the same as that for IPD’s standard Valuation Based Indices (VBIs) however some filtering is necessary to ensure the model is not distorted by extreme cases, and that an adequate prior valuation history is available.

All European countries are modelled together using data specified in Euros and then converted to local currency. The UK is an exception as it existed prior to development of Pan-European TLIs and so has an independent model.

Stage 2 – Regression on sale sample

Firstly sale samples are defined. For each quarter’s model, sales from the preceding six months are identified. This reflects the fact that, owing to the low liquidity of property investments, there are insufficient sales in just one quarter for stable models to be estimated and usable indices to be produced.

A reference set of valuations for each sale sample is defined using valuations two quarters prior to the quarter being analysed. This is to ensure that the valuations are not influenced by sale negotiations. In the case of biannually and annually valued countries, the valuations used may be interpolated between actual valuations.

Once the relevant sales and their reference valuations are defined, the natural log of the sale price and the capital value in each case are computed. Meanwhile, dummy variables are created to identify the main property type and the country of each asset in the dataset. Dummy variables are defined to strike a balance between disaggregation and representation, such that sales for each category are observed in the majority of periods.

An Ordinary Least Squares (OLS) regression is then run for every quarter in the time period. The regression model has the following form:

Where:

i identifies a property,

t identifies a particular quarter,

j identifies a country and is a vector of country dummies,

k identifies a sector and is a vector of sector dummies,

P equals the gross sale price and

V equals the capital valuation

e

s

Create datasetRegression on

sale sample

Generation ofindex

Mass appraisalof all assets

11 IPD.com/IndexSchedule

Stage 3 – Mass appraisal of all assets

The coefficients from regressions can be used to predict sale prices for assets that were not traded. Two predictions are made for properties held in each quarter.

First, a start price is predicted using coefficients from the regression on the sale sample for the preceding period.

Second, an end price is predicted from output for the regression on the sale sample for the current period.

So, for Q4, predicted start prices are derived from the regression on Q2-Q3 sales and predicted end prices are derived using the regression on Q3-Q4 sales.

These predicted prices are in log form rather than cash terms and it is the latter that is required for generating indices. The predicted log prices are transformed in the following manner to correct for bias:

Where: O2 is the mean squared error of the regression generating the predicted price

Stage 4 – Generation of index

The transformed start and end prices can then each be summed for all assets within a particular country or sector. The change between these two totals (in % terms) will represent a value-weighted capital return figure derived from transaction evidence. These rates of change can be chain-linked with those from the surrounding quarters in order to form a time-series for that country or sector.

IPD.com/IndexGuide 12

IPD Index Guide 2012

Indices for Derivatives

IPD indices are used as the basis of real estate derivative contracts. For investors looking to trade in commercial property indices, there are three main types of instruments:

• Total return swaps

• Futures

• Structured notes

The main differences between these instruments concern the exchange of principal and the need for ISDA documentation.

Property derivatives come with a number of advantages over conventional real estate assets:

• Lower transaction costs (0.5% compared to 6.0%)

• Rapid liquidity

• Diversification

• Current sentiment pricing

• The ability to facilitate benefit from a falling market.

When property derivatives were launched in 2004, there was a steady build up in interest as a buoyant market looked for new ways of exploiting their property sector knowledge. Interest primarily took the form of total return swaps on IPD UK indices, with later interest building in both the French and German indices.

Soon thereafter, a series of test trades were executed on Italian, Swiss, Japanese, Spanish, Canadian and Australian IPD indices. The majority of UK trades have been on the All Property Index, but there have been a significant number of trades on selected sector and sub-sector indices.

Since February 2009, it has been possible to trade futures based on the IPD UK Total Return Index on the Eurex international derivatives exchange. Futures are standardised contracts, each traded for a set value and term. Eurex nets derivatives exposure and provides central counterparty clearing, significantly mitigating counter-party risk.

In Q2 2011 sector futures contracts were launched, and sub-sector contracts are planned. The volume of open-interest is available from Eurex.

The emergence of the property derivatives market not only aids managers, with potentially more efficient portfolio management techniques, but also opens up a new range of strategies.

Perhaps the most obvious use of derivatives for property portfolio managers is the hedging of risk and the fast, efficient rebalancing of portfolios. This concept can be used by both managers of multi-asset portfolios and managers of property portfolios.

Total return swaps allow investors to leverage their position to property by holding less cash than the notional size of the contract, whilst structured notes can also be structured with embedded leverage. This is especially attractive in market conditions, such as those currently being experienced, where debt can be expensive and difficult to obtain from banks.

The ability to short property exposure through a derivative allows managers to hedge risk in their portfolios. All Property swaps can be used to hedge market risk on a portfolio of assets, or just some part of that risk for specific assets. Sector (Retail, Office and Industrial) or subsector (e.g. shopping centres, retail warehouses etc) swaps can be sold to hedge out more specific market risks.

The ability to exit or enter at specific times in the direct property market depends upon often difficult and illiquid market circumstances. Derivatives can offer a means of bridging periods in which direct transactions cannot be speedily completed - for instance, when there are no available purchasers or there is a lack of available stock in a certain sector.

Portfolio managers can also use derivatives to offset market sector performance and risk (beta), and concentrate on asset outperformance and risk (alpha). They can then focus on delivering excess performance from the directly held assets.

13 IPD.com/IndexSchedule

Computing IPD’s Performance Measures

IPD indices use monthly time-weighted returns, including the KTI Finland Annual Index which is approved as fully compliant with IPD standards.

A number of IPD indices are frozen historically, meaning that published returns are never restated. Therefore the addition of new funds to these databases does not involve retrospective restatement, even where historical data for those funds is available.

In all other IPD indices, historical restatement is undertaken whenever it gives a more comprehensive and accurate report of past market performance.

Indices currently frozen historically are:

• IPD France Annual Property Index

• IPD Netherlands Annual Property Index

• IPD UK Annual Property Index

• IPD UK Quarterly Property Index

• AREF / IPD UK Pooled Property Fund Index

• IPD UK Monthly Property Index

This position is continuously under review. As indices grow in size and coverage, the possibility of index freezing is reconsidered.

Key IPD calculations

All IPD performance measures, including indices, are value-weighted within a single measurement period (i.e. one month) based on open market valuations of each of the real estate assets directly held within contributing portfolios. Capital employed is defined as the value of assets held at the beginning of the computation period plus purchase, development and other capital expenditure during the period. Capital employed is the denominator of the total return equation.

Calculation of principal single period measures

Total return is calculated as the change in capital value, less any capital expenditure incurred, plus net income, expressed as a percentage of capital employed over the period concerned.

Income return is calculated as net income expressed as a percentage of capital employed over the period concerned.

Capital growth is calculated as the change in capital value, less any capital expenditure incurred, expressed as a percentage of capital employed over the period concerned.

Standard Property Fund Index measures:

• Total return

• Leverage ratio

• Distribution yield

• Net asset value

Subject to index maturity, the above measures are also available for each fund within the index. Each fund’s contribution to the index, longer term performance and current asset allocation is detailed in the publication.

IPD.com/IndexGuide 14

IPD Index Guide 2012

The basis for IPD’s annual and quarterly performance measures is time-weighted. Annual measures are the result of compounding 12-month’s figures and annual figures are shown only when 12-month’s figures are available. The measure gives an equal weight to each month.

To calculate quarterly and annual returns, it is necessary first to construct an index from the monthly values.

The 12-month return, for example, is then calculated as the percentage change in the index (Xt) over the relevant 12 months.

12-month Total Return = [ (X (t + 12) / Xt ) -1 ] * 100

Note: Multi-period capital growth and income return may not sum perfectly to total return due to the cross product that occurs when capital and income returns are combined within compounded total returns.

Computation formulae – Direct property indices

Total return

With respect to a single month total return is defined as:

Income return

Capital growth

Where:

TRt is the total return in month t

CVt is the capital value at the end of month t

CExpt is the capital expenditure (includes purchases & developments) in month t

CRptt is the capital receipts (includes sales) in month t

Nlt is the day-dated rent receivable during month t, net of property management costs, ground rent and other irrecoverable expenditure

15 IPD.com/IndexSchedule

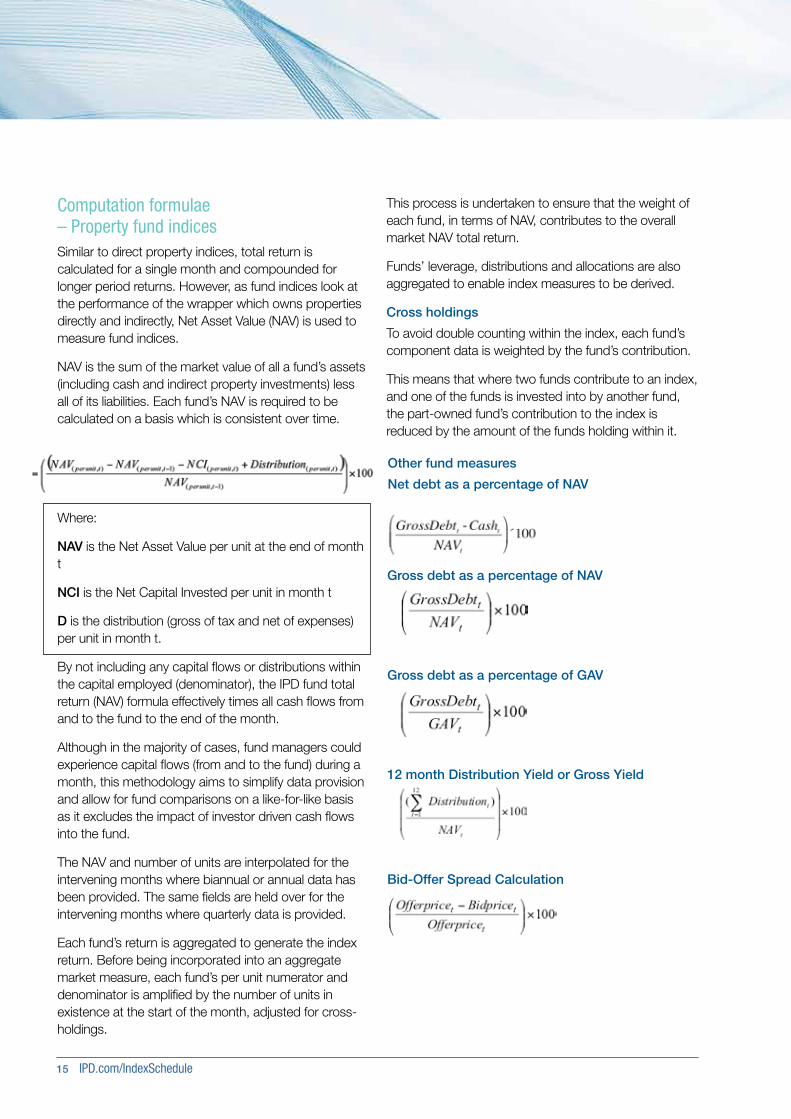

Computation formulae – Property fund indicesSimilar to direct property indices, total return is calculated for a single month and compounded for longer period returns. However, as fund indices look at the performance of the wrapper which owns properties directly and indirectly, Net Asset Value (NAV) is used to measure fund indices.

NAV is the sum of the market value of all a fund’s assets (including cash and indirect property investments) less all of its liabilities. Each fund’s NAV is required to be calculated on a basis which is consistent over time.

Where:

NAV is the Net Asset Value per unit at the end of month t

NCI is the Net Capital Invested per unit in month t

D is the distribution (gross of tax and net of expenses) per unit in month t.

By not including any capital flows or distributions within the capital employed (denominator), the IPD fund total return (NAV) formula effectively times all cash flows from and to the fund to the end of the month.

Although in the majority of cases, fund managers could experience capital flows (from and to the fund) during a month, this methodology aims to simplify data provision and allow for fund comparisons on a like-for-like basis as it excludes the impact of investor driven cash flows into the fund.

The NAV and number of units are interpolated for the intervening months where biannual or annual data has been provided. The same fields are held over for the intervening months where quarterly data is provided.

Each fund’s return is aggregated to generate the index return. Before being incorporated into an aggregate market measure, each fund’s per unit numerator and denominator is amplified by the number of units in existence at the start of the month, adjusted for cross-holdings.

Other fund measures

Net debt as a percentage of NAV

Gross debt as a percentage of NAV

Gross debt as a percentage of GAV

12 month Distribution Yield or Gross Yield

Bid-Offer Spread Calculation

This process is undertaken to ensure that the weight of each fund, in terms of NAV, contributes to the overall market NAV total return.

Funds’ leverage, distributions and allocations are also aggregated to enable index measures to be derived.

Cross holdings

To avoid double counting within the index, each fund’s component data is weighted by the fund’s contribution.

This means that where two funds contribute to an index, and one of the funds is invested into by another fund, the part-owned fund’s contribution to the index is reduced by the amount of the funds holding within it.

IPD.com/IndexGuide 16

IPD Index Guide 2012

Time-weighting

Monthly computation of IPD performance measures

The return calculation period and minimum measurement period for IPD performance measures, including all indices, is one calendar month. Returns for longer periods, such as quarters and years, are calculated by chain-linking individual monthly returns. All IPD annual, biannual and quarterly indices worldwide are calculated using this time-weighted basis, ensuring consistency of methodology from country to country.

Within each monthly measurement period, the total return is the sum of the capital and income components, although it should be noted that multi-period capital growth and income return do not sum perfectly to total return. This is due to the cross product that occurs when capital and income returns are combined within compounded total returns.

Converting local currency indices into common currencies

The start and end month capital values, monthly net income, capital expenditure and receipt figures used in these time weighted calculations are all converted into common currencies at the month end.

Currency conversion has an impact on local market returns as changes in values from one month to the next are partly the result of fluctuations in currency exchange rates in addition to local property market factors.

The composite IPD Pan-European Property Index return, when computed and reported in local currencies, is calculated by converting all markets to the same currency, but at a fixed rate over time to remove the impact of exchange rate movement.

Constructing monthly data

Valuation data

If monthly valuations are available, as is the case for the IPD UK Monthly Property Index, these are used for calculating total return, capital growth and income return indices.

Where monthly valuations are not available, but the valuation dates of contributing properties are synchronised to a common date, IPD inserts estimated monthly valuations which are derived by interpolating between actual values. In services where the valuation dates of contributing properties are spread throughout the year, IPD can apply one of two methodologies.

• The first is to simply hold values flat from one valuation date to the next. While this introduces an inertial tendency into published results, it avoids the need for regular restatement that would otherwise result.

• The second is to interpolate historically between true valuations and use evidence in most recent measurement periods to mix adjust across the entire sample. While avoiding the inertial tendency in reported figures, this does introduce systematic restatement of previously published returns.

While IPD would prefer indices to be built on services with a common valuation date, this is not always possible. In Canada the first methodology is currently used, whilst in Australia and New Zealand, the second methodology is now employed.

Use of monthly and quarterly data for estimation in countries where IPD publishes a monthly index, the majority of properties are interpolated non-linearly between successive actual valuations, shaping the intervening notional values to match the known movements of the market over the period for that particular property type and region. Valuations are indexed between the two known end values on the basis of the capital and rental value movements within the market.

Cashflow items

Monthly cashflows, if available, are recorded in the actual months in which they occur. If cashflow data can only be provided on a quarterly or annual basis, it is apportioned equally over the period to which it relates.

Interpolation process in detail

To calculate annual returns from monthly data, it is necessary to have valuations at the end of each month. Where properties are valued less frequently, IPD computes estimated capital and rental values.

17 IPD.com/IndexSchedule

Other index compilation rules

Frozen index series

Property indices in France, Netherlands and the UK are frozen historically. This means the historical time series is not restated with new information after publication. The frozen history does not apply to all performance measures or sub-sectors however.

Total return, income return and capital growth series are frozen at sector and All Property level. New portfolios are added from time to time, but without their histories. The histories of any funds that are sold off, or otherwise cease to contribute their data to IPD, remain in the indices historically. If portfolios are either split or merged, the history remains in the indices in the original form and continues in their new split or merged versions.

At present, all other IPD indices are unfrozen and subject to historical restatement, if and when additional portfolios are added to their constituent databanks. Indices are not frozen historically if it is felt that additional information from additional portfolios would create a more accurate picture of the market.

Alterations to frozen index historical results

If, in consultation with international partners, consultative groups and other relevant organisations / individuals, IPD decides that a change in computation method will be beneficial these will normally be restated historically for the sake of presenting a consistent, continuous series.

Likewise, if it is agreed after consultation that a change to the method of computation or composition of the series would be beneficial to the users of an index, a restatement of historic index returns may result.

The frozen index series may also be restated if a significant error in data recording or computation is discovered. IPD makes every effort to avoid this situation, and these indices are frozen against minor data amendments.

Frozen fund index series

The AREF/IPD UK Pooled Property Fund Index and Mercer/IPD Australian Pooled Property Fund Index - Core Wholesale are frozen. By frozen, IPD means that the aggregate index series derived from the fund data are frozen after each release. Any retrospective fund data amendments do not affect the frozen time series. This includes the index medians and descriptive data.

However, where individual fund returns are published these are always live. Required data amendments are accommodated so that the IPD fund returns match the fund returns made available elsewhere.

Review of index composition

A review of index composition occurs when the contribution from a single firm of valuers rises above 25% by value of the capital employed in an index. Similarly, such a review occurs when any one investor contributes in excess of 50% by value to either the overall index or any of the published sectors therein. This review must include consultation with the investor in question, and seek written permission to publish results in which they dominate.

Portfolio types permitted in indices

Properties from all fund and portfolio types are eligible for inclusion in IPD indices, irrespective of their liabilities and investment disciplines. This includes unitised, securitised and partnership vehicles, as long as they meet required valuation standards and provide full asset level information in accordance with IPD internal rules and data definitions.

Joint ventures and private investments are not permitted for inclusion within a fund index.

Addition of new portfolios

New portfolios or funds will be added to index samples once the index is considered stable. All additions and withdrawals are communicated, provided they have a material impact on size and structure of the index. For example, if a fund were to leave the IPD UK Annual Property Index, communication would be made available on IPD’s website at least of three months in advance.

IPD.com/IndexGuide 18

IPD Index Guide 2012

Minimum market coverage

The publication of new IPD indices will be delayed if the total value of capital employed is less than 20% of the best available estimate of the total value of the market they are intended to track.

This estimate will reflect the ungeared value of all directly held properties in each of the professionally managed portfolios whose mandate is primarily focused on the market in question. Where relevant, the interests of known multinational investors will be included.

The exception to this is when the national market is so large that a robust sample is attained with less than 20% of the market covered.

Delays to publication of indices

As the compiler of the index, IPD retains the right to delay the calculation and publication of index results, or to suspend or discontinue the publication of index results, if it believes that there are circumstances preventing the correct and consistent calculation of an index.

Further InformationIndex status

Consultative index

An index is given ‘Consultative’ status during the early stages of its development. This highlights to users that the index is likely to grow in size over time and thus historical results are likely to be restated to a greater extent than established indices. Consultative status is used to encourage users, contributors and potential contributors to engage with IPD about the future of the index.

Indicator

An indicator is a guide to market performance that is released between two annual index releases. These indicator results are produced on a smaller sample than index results and have no history. Once the latest annual index is published, the interim period indicator results are no longer valid as they have been replaced with robust full annual index results.

IPD property market informationDatabases for detailed analysis

In addition to property indices for each country in which it operates, IPD also produces a range of publications and research reports investigating market investment performance in detail. IPD indices are transparent because the databases make it possible to analyse these markets using more detailed breakdowns of property type and location, and many additional measures of capital and income performance - all on a completely consistent basis.

This consistent ‘market performance’ approach is used in:

• IPD Annual Indices

• IPD Biannual Indices

• IPD Quarterly Indices

• IPD Monthly Indices

• IPD Market Digests - in depth market reports

• IPD Key Centres Publications - standard local market publications.

Inclusion of standing investment properties

Index results and all IPD standard research publications are based on standing investment properties. These must be revalued at least once during the reporting period, and exclude the effect of buying, selling and development. In the time-weighted methodology, standing investments are not only properties with a valuation at the start and finish of the measurement period; other properties may contribute to standing investment returns for a part of the period if they have a valuation after (or before) an excluding event. A property will qualify for inclusion between any pair of actual valuations.

Other exclusions from market measures

Index figures exclude properties where terms of ownership, or specific events such as major capital expenditure, mean that changes in value throughout the year may have been influenced by non-market factors.

19 IPD.com/IndexSchedule

These rules are designed to make an index a measure of the return to be expected from held investments without active management, and therefore a fair basis for comparison across asset classes and between markets.

Some properties, such as occupational properties, are excluded from market measures in all periods. Others, such as those affected by refurbishment or improvement spending, are excluded only for those months in which the spending has occurred. A property is excluded from market measures where:

• monthly net expenditure amounts to 10% or more of capital value

• it has a zero or negative capital value

• it is predominantly owner occupied

• there is a change of ownership share

• it is held on a short leasehold with less than 25 years term remaining

• it is a fixed rent property where market rental value is more than five times the current rent

• it has been subject to unique events such as fire damage or flooding.

Fund market information

The aim of a fund index is to report the status of the market to the industry. Further breakdowns and analysis of the national and multinational fund indices are available and bespoke requests can be explored.

The status of properties is not of concern for a fund index. A fund can contribute for any time period while it meets the inclusion criteria. However, as with the inclusion of standing investments, a fund can only contribute to the medians of an index where it has provided a return for that reporting period.

IPD.com/IndexGuide 20

IPD Index Guide 2012

Acquiring index licences

Requirements for trading derivatives

No derivative or other financial product may be linked to IPD data for the purpose of determining the product’s capital value, income yield or any other material outcome without acquiring a licence from IPD. The licence will be based on a standard IPD licence template and will detail precisely what data will be used, for what commercial or other purpose, and on what terms. Licences are available to any party willing to accept the terms of licence.

Since February 2009, Europe’s first property futures are tradable at Eurex. The property futures are annual contracts based on the All Property total returns of the IPD UK Annual Property Index for individual calendar years.

Requirements for redistributing IPD statistics

No sale, resale, distribution, transmission or other form of re-publication of IPD data may be made without IPD’s prior written consent. No commercial use may be made of IPD data or any of its published statistics other than:

• internally within an organisation

• in specifically pre-agreed published research reports whose content has been submitted to IPD for prior approval

• in advice to clients which draws selectively on IPD data.

In each such case, any quotation of IPD figures should be clearly attributed. All IPD data is the exclusive property of IPD or its licensors, and is protected by copyright, database rights and other intellectual property laws.

Requirements for using IPD data for portfolio benchmarking

IPD’s benchmarks and other related statistics are the intellectual property of IPD and may be used by subscribers without a licence for internal research purposes only. Companies wishing to use IPD statistics to report performance publicly must apply for a licence to utilise the information in any formal documentation or to publish the figures within widely circulated reports.

An IPD licence can be obtained in one of two ways:

• If a fund subscribes to the Portfolio Analysis Service it gains the right to publish the portfolio’s result and its benchmark in any medium. A licence to use and republish IPD statistics is implicit for subscribers of this service.

• If a client wishes to remain outside the Portfolio Analysis Service, then IPD may grant a licence to use a relevant IPD series as a benchmark. The cost of a license will depend on the size of the portfolio, but will be no less than the cost of being measured and fully benchmarked by IPD.

Fund index licenses

If a fund wishes to use an IPD Property Fund Index as a benchmark, but is not a contributor to that index, a license must be obtained. Licenses are issued on a fund by fund basis. Contributing funds may access and view the content but may not otherwise - without limitation - copy, distribute, sell, publish, or commercially exploit any of the content included within a Property Fund Index without IPD’s prior written permission.

21 IPD.com/IndexSchedule

Frequently Asked Questions

1. Is there a minimum size for a property to be included in IPD indices and benchmarks, in terms of either value or lettable area?

There is no minimum size, as all assets held within client portfolios are included in IPD outputs.

2. Is there a minimum frequency with which included properties must be valued?

In order to be included in a monthly, quarterly or biannual index, properties must be valued on a monthly, quarterly or biannual basis respectively.To be included in an annual index, properties must be valued at least once a year, although not necessarily at year end.

3. Who is allowed to carry out valuations which contribute to IPD indices?

IPD requests that external valuations are provided wherever possible. However, internal valuations are also permitted, but must meet the definition of market value which is applied by IPD in each national market, e.g. in accordance with the RICS Red Book.

4. Is there a technical committee that monitors the credibility of IPD indices?

In the UK, IPD is advised by its Index Consultative Group, which meets twice a year. This reviews the composition and construction rules for UK monthly, quarterly and annual indices on a regular basis. It is an independent, non-executive body whose members are drawn from the property investment industry, universities, major research and chartered surveying firms and index publication and investment measurement organisations. A parallel Portfolio Analysis Service Consultative Group advises on the benchmarking techniques and measurement procedures used by IPD.

Similar groups advise on IPD’s indices in other national markets, although the distinction between Index and Portfolio Analysis is not usually made due to a typically smaller client pool from which to draw membership.

5. What stage of development completion must a building reach before it is included in an IPD index?

No developments are included in IPD indices, due to their potentially idiosyncratic performance.

IPD considers that a building ceases to be a development either six months after practical completion, or when it is 75% let, whichever is sooner. However, these properties are recorded by IPD and appear in the owner’s PAS reports and benchmark results.

6. Does IPD query unusual data supplied by its participants, such as large losses or gains?

Any extreme changes in data inputs from period to period are queried with participating clients. Clients are required to sign off their reports before their data is included in indices and benchmarks.

7. How are refurbishments, partial sales and vacancies dealt with?

Significant refurbishment and partial sales are not reflected in the indices, from which they are excluded. Minor refurbishments are treated as normal expenditure. Vacant properties are included in indices, with their valuation and income stream (likely to be zero) reflecting that vacancy.

8. How do actual transaction prices affect the indices?

Properties which are bought into or sold from contributing portfolios do not contribute to IPD indices in the period when they are transacted. They are however included in benchmarks.

9. Why are time-weighted returns used rather than money-weighted? That is to say, chain-linked monthly returns even for quarterly, biannual and annual indices?

Time-weighted returns are comparable with other assets where time-weighted return calculations are the norm, and conform with international standards, in particular the Global Investment Performance Standard (GIPS). The trend towards more frequent valuations requires IPD to be able to provide measurement over almost any period on a comparable basis. This can only be achieved by using a consistent building block of monthly cashflows.

This also means that IPD uses identical calculation methods for all outputs worldwide, greatly expanding the potential for international comparison.

IPD.com/IndexGuide 22

IPD Index Guide 2012

10. IPD often refers to sectors and segments within an index. What is the difference?

The IPD standard sectors are broad types of property use - Retail, Office, Industrial, Residential and Other. Segments, also referred to as sub-sectors, are any further disaggregation of these sectors into more specific property types or regions, eg. shopping centre is a segment of All Retail, distribution warehouse is a segment of All Industrial etc.

11. Why is residential property included in some indices, but not others?

Property types included within an index are dependent on the assets held by the Portfolio Analysis Service clients in that country. Therefore, if residential property is favoured by institutional investors in a given market, it will be represented within that country’s index in the same proportion to the value of residential properties held within the constituent portfolios.

12. Does IPD hold data beyond that published in their indices?

Yes. The base date of an index is set at the point where the majority of funds are able to provide data, or where the minimum market coverage has been reached. If funds have submitted data prior to the index base date, and or there is additional market data considered unsuitable for an index, IPD can make this available. However, before this data is made available, IPD will ensure the user is aware of its boundaries.

13. What is a property fund?

Broadly speaking a pooled fund is a professionally managed fund that allows third party access to direct and indirect property (including derivatives and fund of funds). The majority of the fund must be held in physical property. The fund must have been, currently be, or intending to be open for third party investment.

14. How can a fund join a property fund index?

A fund must complete a Data Collection Form, which will determine if the fund is eligible and ensure all necessary data fields are provided. A newly completed Data Collection Form must be submitted one month prior to the end of the reporting period and then again at the update time.

15. How should net asset value (NAV) be calculated and provided to IPD?

A fund’s NAV is the sum of the value of all its assets (including cash, derivatives and indirect property investments) less all its liabilities.

Providing they are calculated on a consistent basis over time, funds are, at present, asked to submit NAVs drawn up under whichever accounting convention they use to prepare their annual accounts (or the equivalent). In practice this usually means either local Generally Accepted Accounting Principles (Local GAAP) or International Financial Reporting Standards (IFRS). NAVs calculated under IFRS are reported after marking fixed rate debt to market value: those calculated under local GAAP are not.

16. Are the property fund index returns net or gross of fees?

The returns are net of fees and management costs. Where fee information is provided to IPD we do have the capability to produce returns gross of fees.

17. What is the value of being a property fund index contributor?

Funds contributing to a property fund index may use the index return as a benchmark, free of charge. Headline data, historic time series and fund specific returns are available to all contributors.

Fund indices are the second most downloaded index of the 100+ IPD Indices; therefore each fund receives a considerable amount of exposure. This exposure can be utilised by prospective investors, while current investors benefit from transparency.

23 IPD.com/IndexSchedule

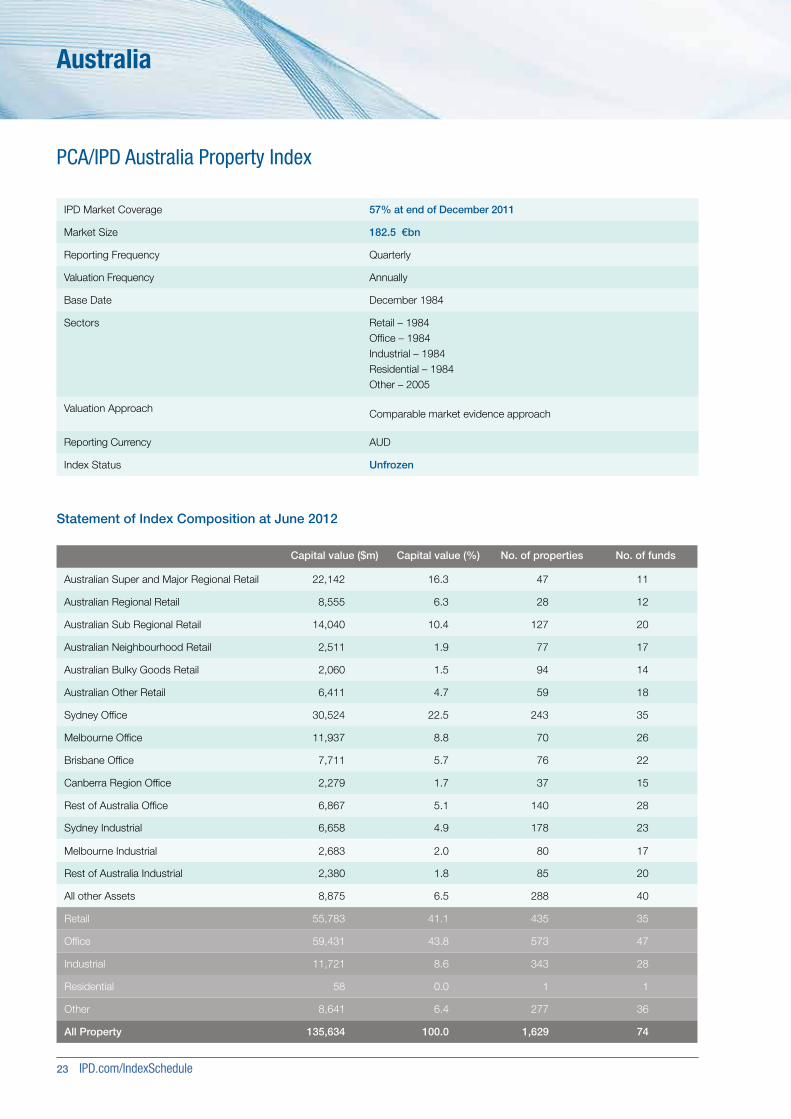

Australia

PCA/IPD Australia Property Index

Capital value ($m) Capital value (%) No. of properties No. of funds

Australian Super and Major Regional Retail 22,142 16.3 47 11

Australian Regional Retail 8,555 6.3 28 12

Australian Sub Regional Retail 14,040 10.4 127 20

Australian Neighbourhood Retail 2,511 1.9 77 17

Australian Bulky Goods Retail 2,060 1.5 94 14

Australian Other Retail 6,411 4.7 59 18

Sydney Office 30,524 22.5 243 35

Melbourne Office 11,937 8.8 70 26

Brisbane Office 7,711 5.7 76 22

Canberra Region Office 2,279 1.7 37 15

Rest of Australia Office 6,867 5.1 140 28

Sydney Industrial 6,658 4.9 178 23

Melbourne Industrial 2,683 2.0 80 17

Rest of Australia Industrial 2,380 1.8 85 20

All other Assets 8,875 6.5 288 40

Retail 55,783 41.1 435 35

Office 59,431 43.8 573 47

Industrial 11,721 8.6 343 28

Residential 58 0.0 1 1

Other 8,641 6.4 277 36

All Property 135,634 100.0 1,629 74

Statement of Index Composition at June 2012

IPD Market Coverage 57% at end of December 2011

Market Size 182.5 €bn

Reporting Frequency Quarterly

Valuation Frequency Annually

Base Date December 1984

Sectors Retail – 1984Office – 1984Industrial – 1984Residential – 1984Other – 2005

Valuation Approach Comparable market evidence approach

Reporting Currency AUD

Index Status Unfrozen

IPD.com/IndexGuide 24

IPD Index Guide 2012

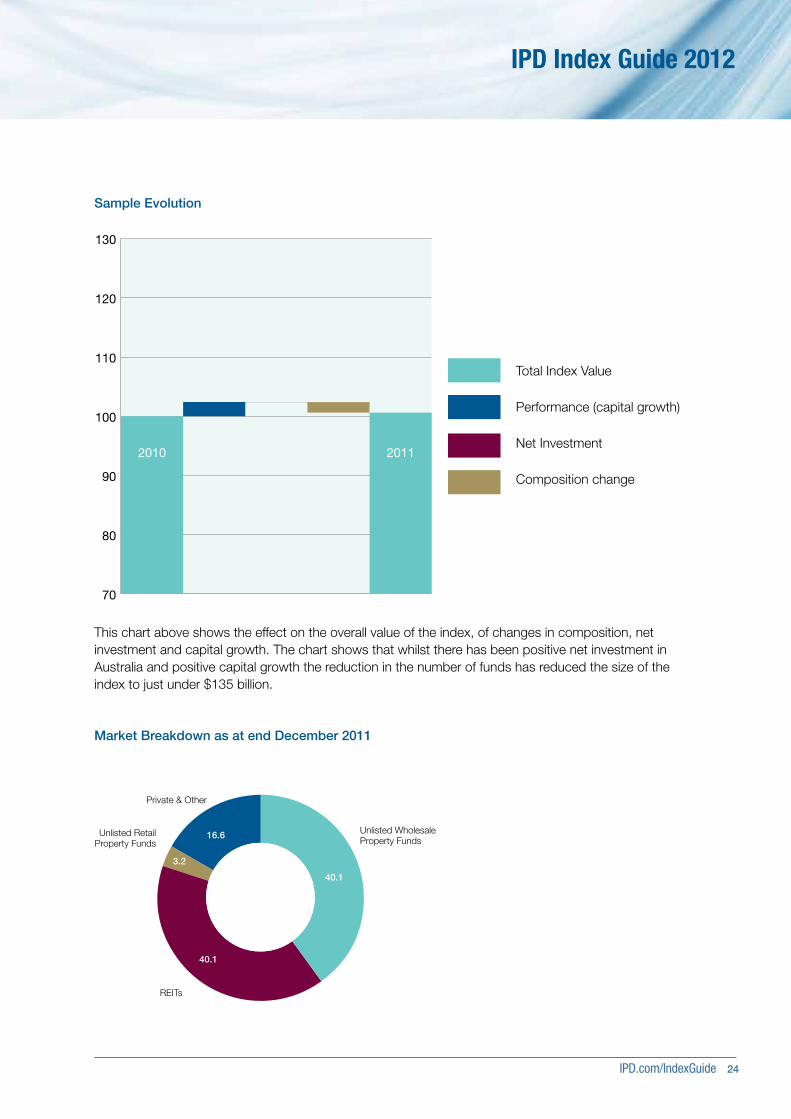

Market Breakdown as at end December 2011

40.1

40.1

3.2

16.6

REITs

Unlisted Retail Property Funds

Private & Other

Unlisted Wholesale Property Funds

70

80

90

100

110

120

130

2010 2011

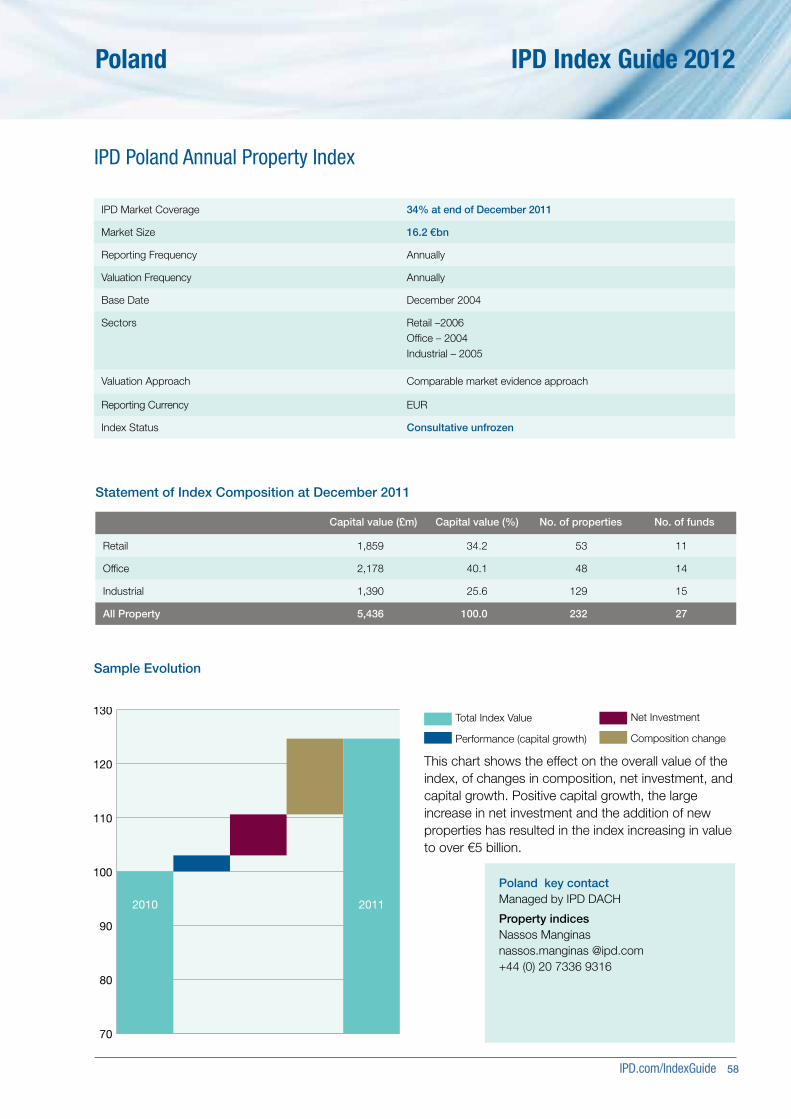

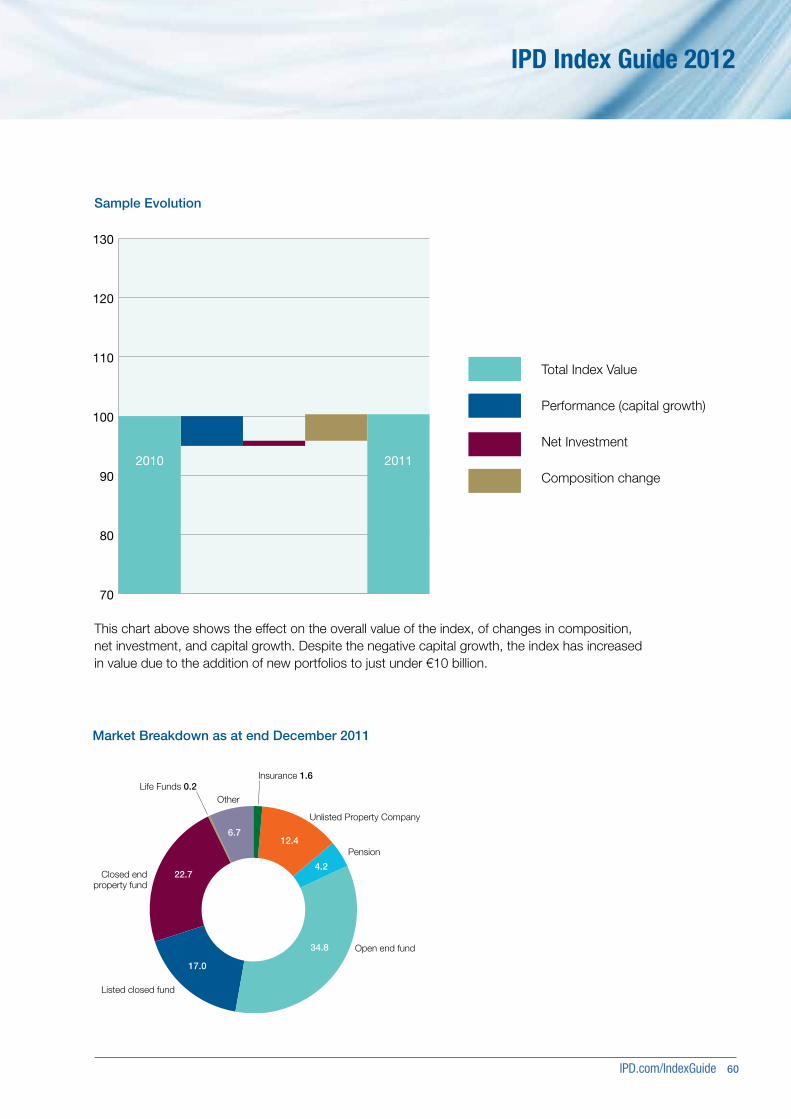

Sample Evolution

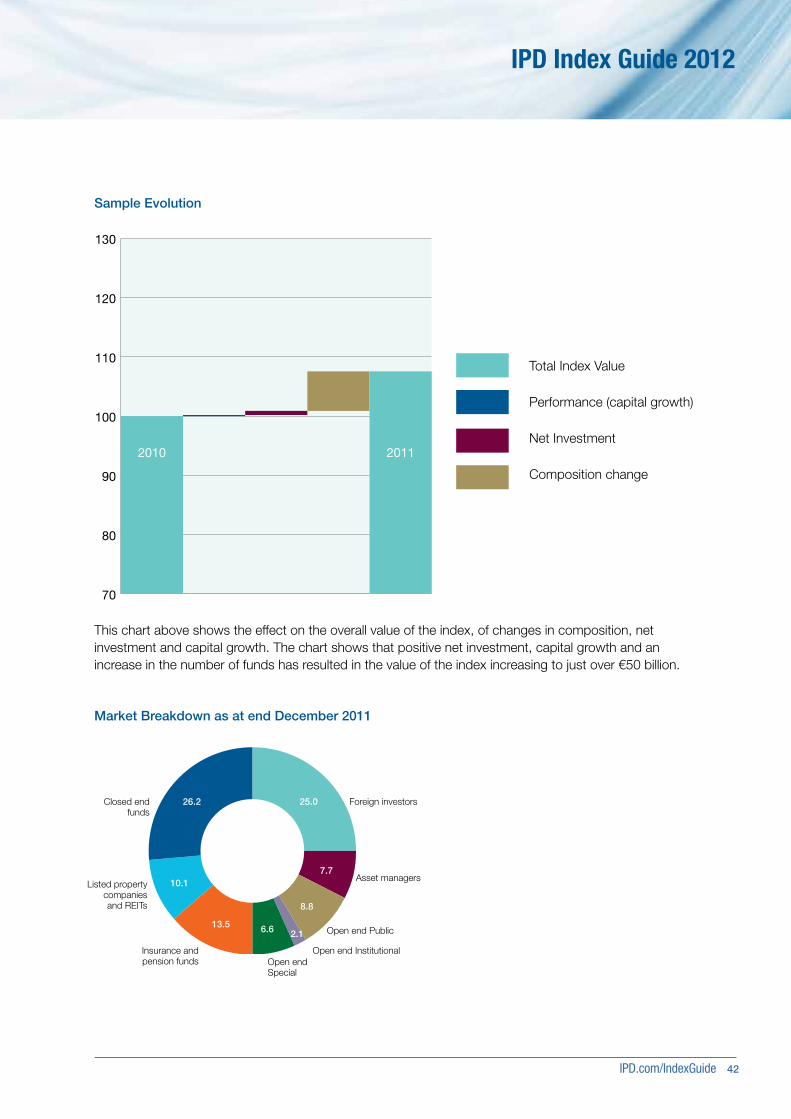

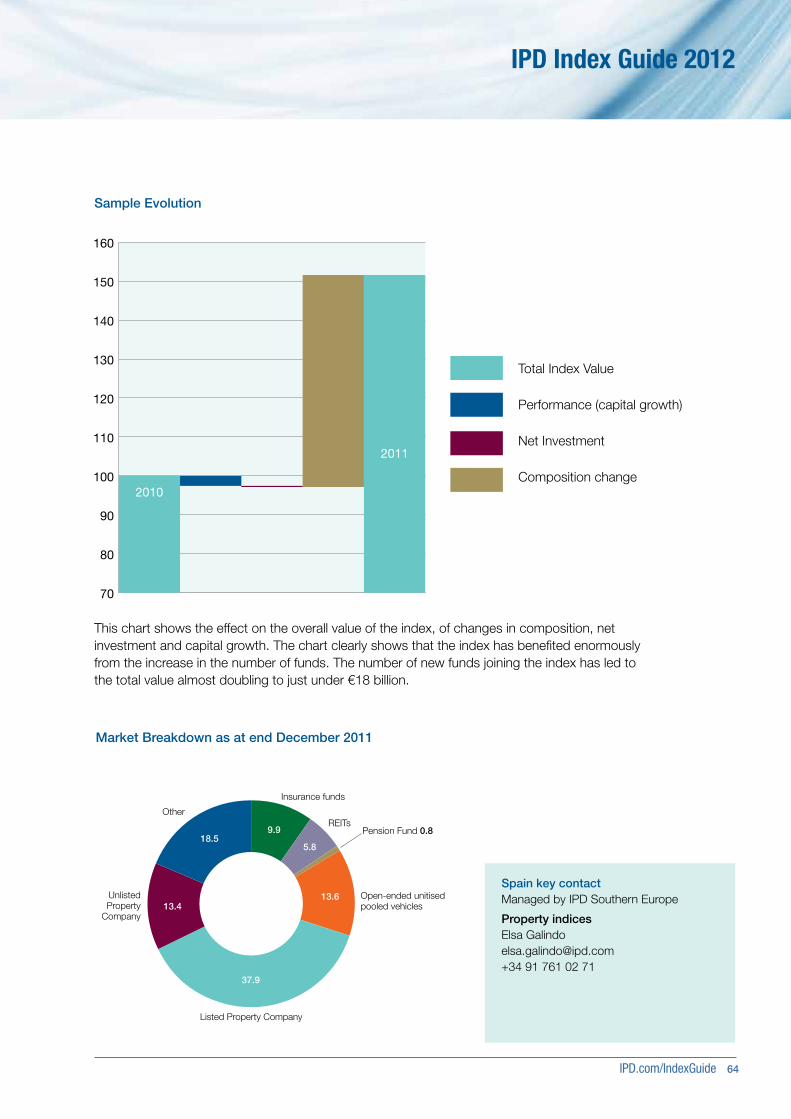

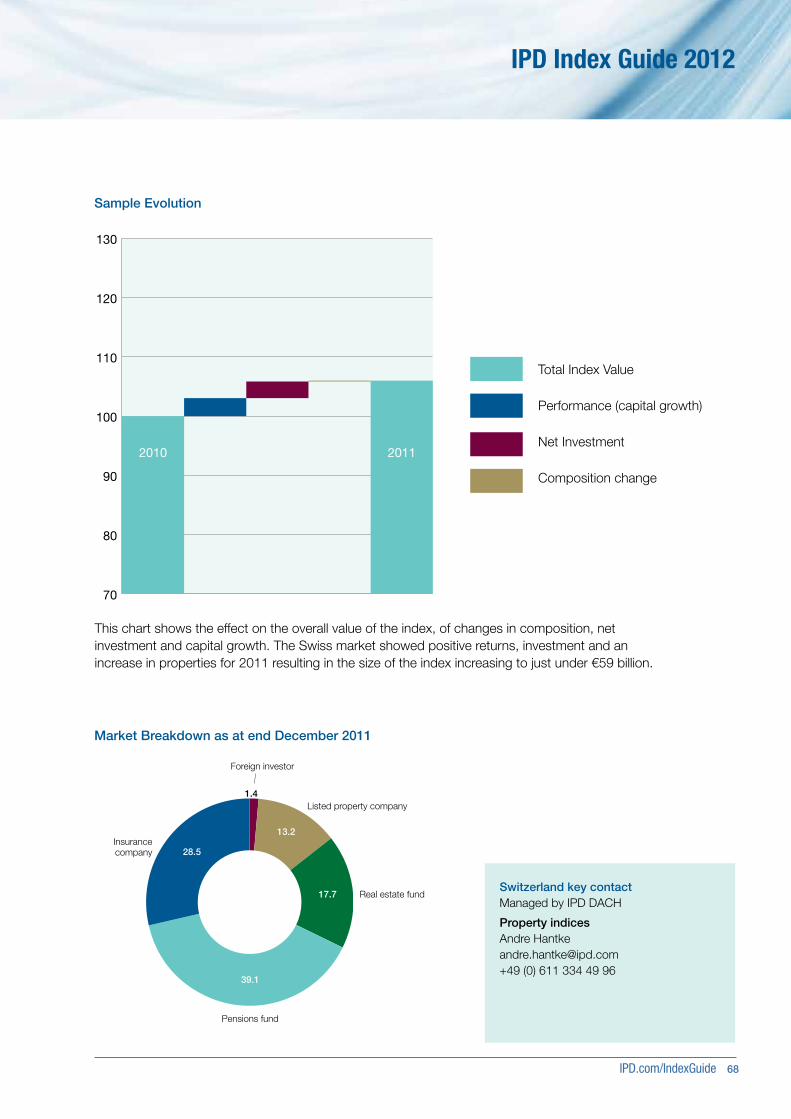

This chart above shows the effect on the overall value of the index, of changes in composition, net investment and capital growth. The chart shows that whilst there has been positive net investment in Australia and positive capital growth the reduction in the number of funds has reduced the size of the index to just under $135 billion.

Total Index Value

Performance (capital growth)

Net Investment

Composition change

25 IPD.com/IndexSchedule

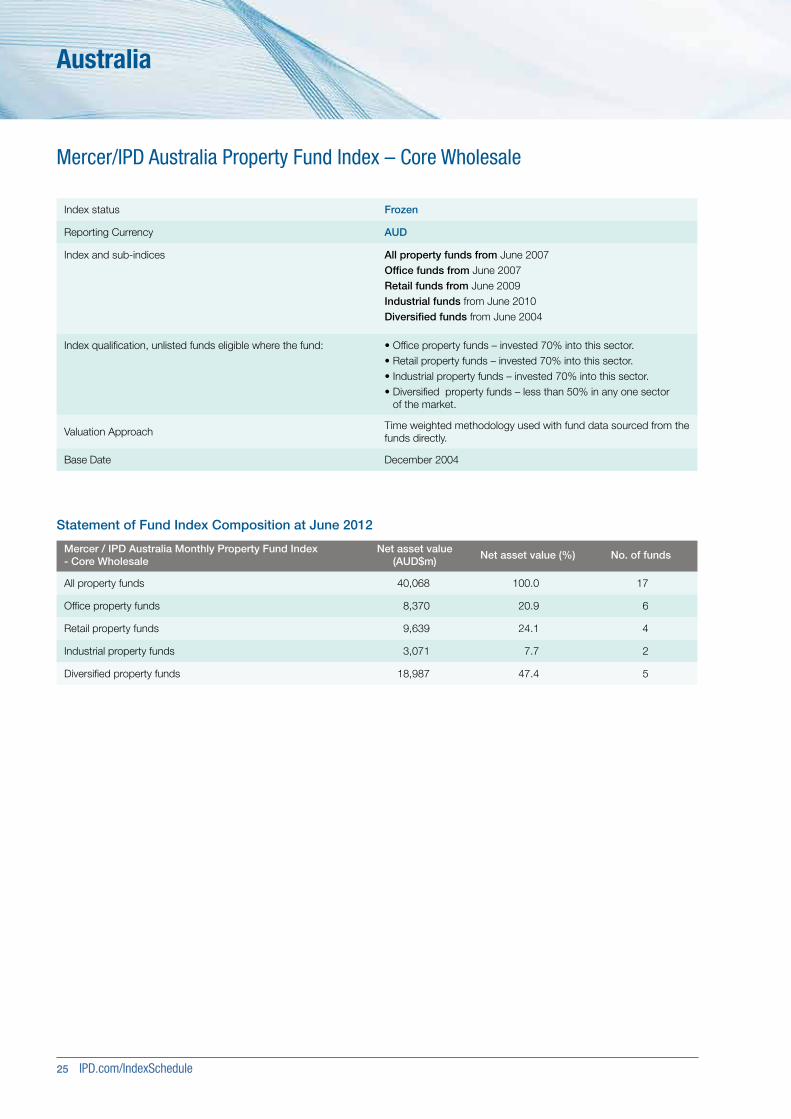

Australia

Mercer/IPD Australia Property Fund Index – Core Wholesale

Statement of Fund Index Composition at June 2012

Mercer / IPD Australia Monthly Property Fund Index - Core Wholesale

Net asset value (AUD$m)

Net asset value (%) No. of funds

All property funds 40,068 100.0 17

Office property funds 8,370 20.9 6

Retail property funds 9,639 24.1 4

Industrial property funds 3,071 7.7 2

Diversified property funds 18,987 47.4 5

Index status Frozen

Reporting Currency AUD

Index and sub-indices All property funds from June 2007Office funds from June 2007Retail funds from June 2009Industrial funds from June 2010Diversified funds from June 2004

Index qualification, unlisted funds eligible where the fund: • Office property funds – invested 70% into this sector.• Retail property funds – invested 70% into this sector.• Industrial property funds – invested 70% into this sector.• Diversified property funds – less than 50% in any one sector

of the market.

Valuation ApproachTime weighted methodology used with fund data sourced from the funds directly.

Base Date December 2004

IPD.com/IndexGuide 26

IPD Index Guide 2012

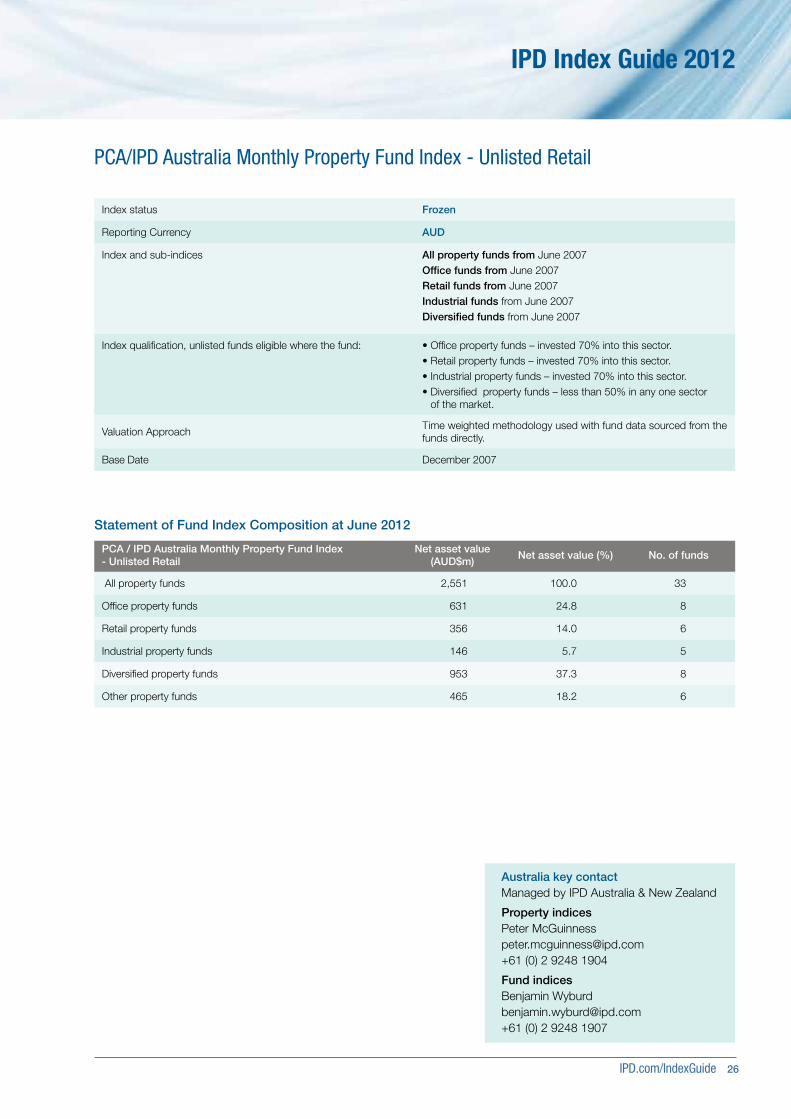

PCA/IPD Australia Monthly Property Fund Index - Unlisted Retail

Statement of Fund Index Composition at June 2012

PCA / IPD Australia Monthly Property Fund Index - Unlisted Retail

Net asset value (AUD$m)

Net asset value (%) No. of funds

All property funds 2,551 100.0 33

Office property funds 631 24.8 8

Retail property funds 356 14.0 6

Industrial property funds 146 5.7 5

Diversified property funds 953 37.3 8

Other property funds 465 18.2 6

Index status Frozen

Reporting Currency AUD

Index and sub-indices All property funds from June 2007Office funds from June 2007Retail funds from June 2007Industrial funds from June 2007Diversified funds from June 2007

Index qualification, unlisted funds eligible where the fund: • Office property funds – invested 70% into this sector.• Retail property funds – invested 70% into this sector.• Industrial property funds – invested 70% into this sector.• Diversified property funds – less than 50% in any one sector

of the market.

Valuation ApproachTime weighted methodology used with fund data sourced from the funds directly.

Base Date December 2007

Australia key contactManaged by IPD Australia & New Zealand

Property indicesPeter McGuinness [email protected] +61 (0) 2 9248 1904

Fund indices Benjamin Wyburd [email protected] +61 (0) 2 9248 1907

27 IPD.com/IndexSchedule

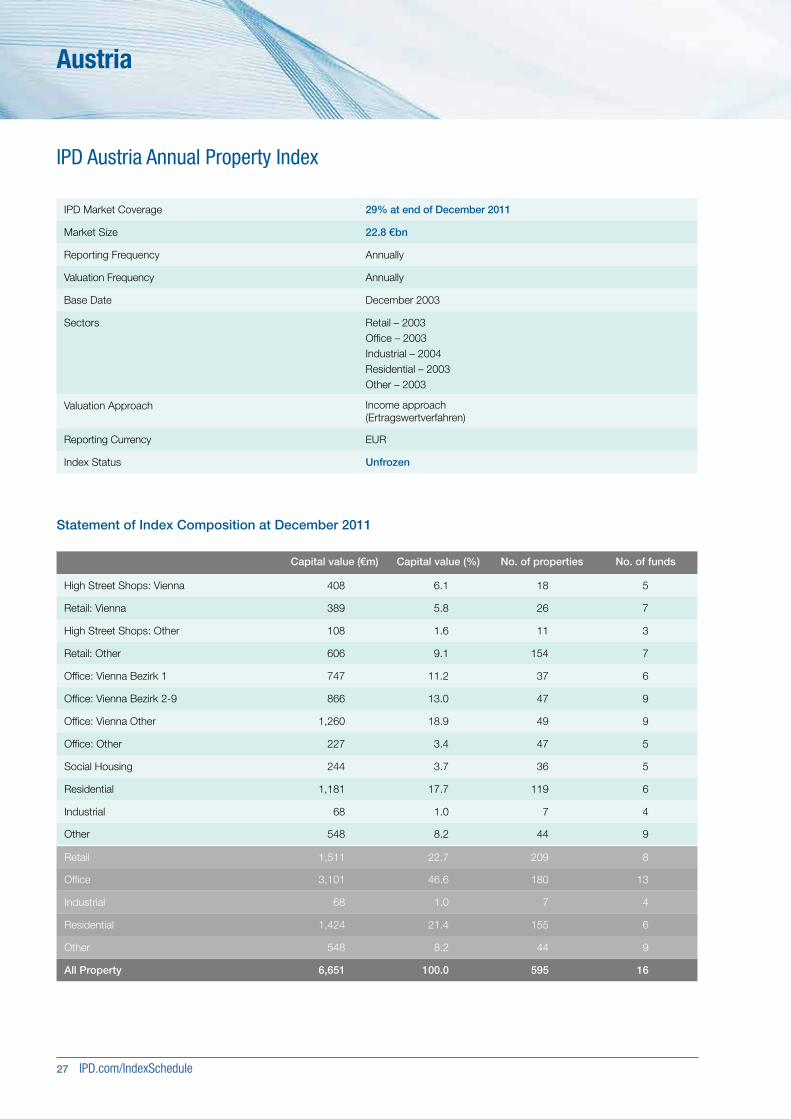

Austria

IPD Austria Annual Property Index

Capital value (€m) Capital value (%) No. of properties No. of funds

High Street Shops: Vienna 408 6.1 18 5

Retail: Vienna 389 5.8 26 7

High Street Shops: Other 108 1.6 11 3

Retail: Other 606 9.1 154 7

Office: Vienna Bezirk 1 747 11.2 37 6

Office: Vienna Bezirk 2-9 866 13.0 47 9

Office: Vienna Other 1,260 18.9 49 9

Office: Other 227 3.4 47 5

Social Housing 244 3.7 36 5

Residential 1,181 17.7 119 6

Industrial 68 1.0 7 4

Other 548 8.2 44 9

Retail 1,511 22.7 209 8

Office 3,101 46.6 180 13

Industrial 68 1.0 7 4

Residential 1,424 21.4 155 6

Other 548 8.2 44 9

All Property 6,651 100.0 595 16

Statement of Index Composition at December 2011

IPD Market Coverage 29% at end of December 2011

Market Size 22.8 €bn

Reporting Frequency Annually

Valuation Frequency Annually

Base Date December 2003

Sectors Retail – 2003Office – 2003Industrial – 2004Residential – 2003Other – 2003

Valuation Approach Income approach (Ertragswertverfahren)

Reporting Currency EUR

Index Status Unfrozen

IPD.com/IndexGuide 28

IPD Index Guide 2012

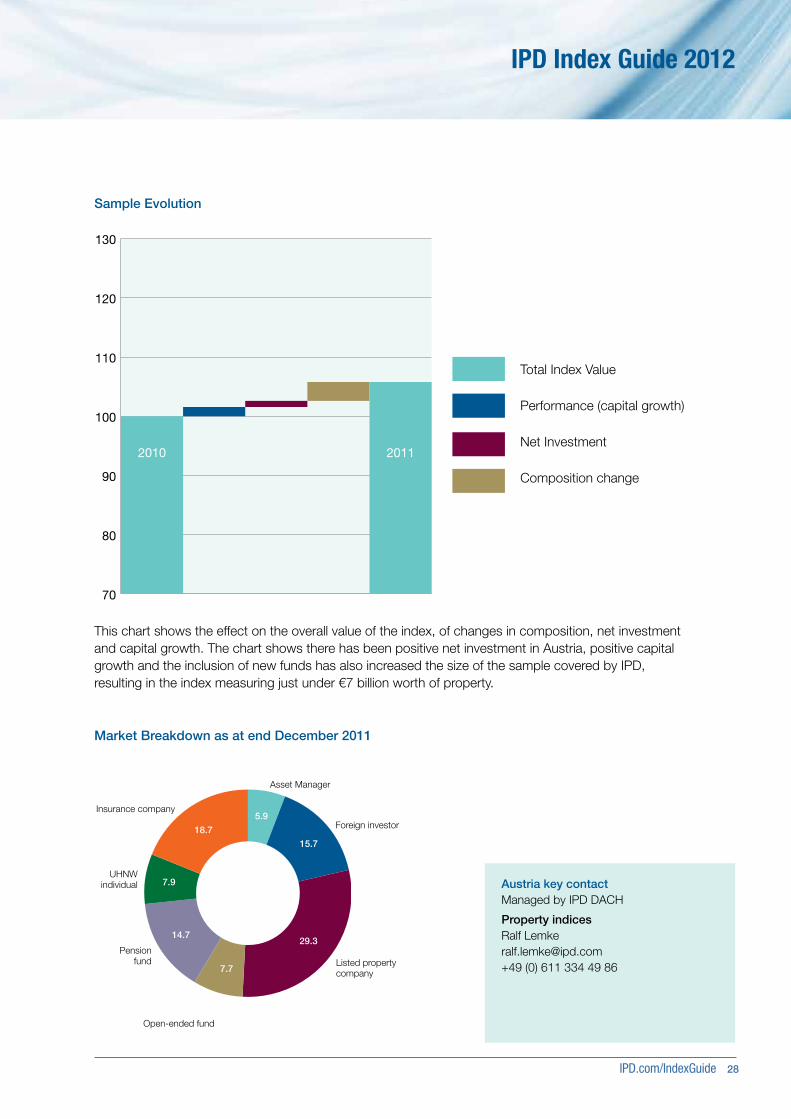

Market Breakdown as at end December 2011

Asset Manager

5.9

15.7

29.314.7

7.9

18.7

7.7

Open-ended fund

Pension fund

UHNW individual

Insurance company

Foreign investor

Listed property company

70

80

90

100

110

120

130

2010 2011

Sample Evolution

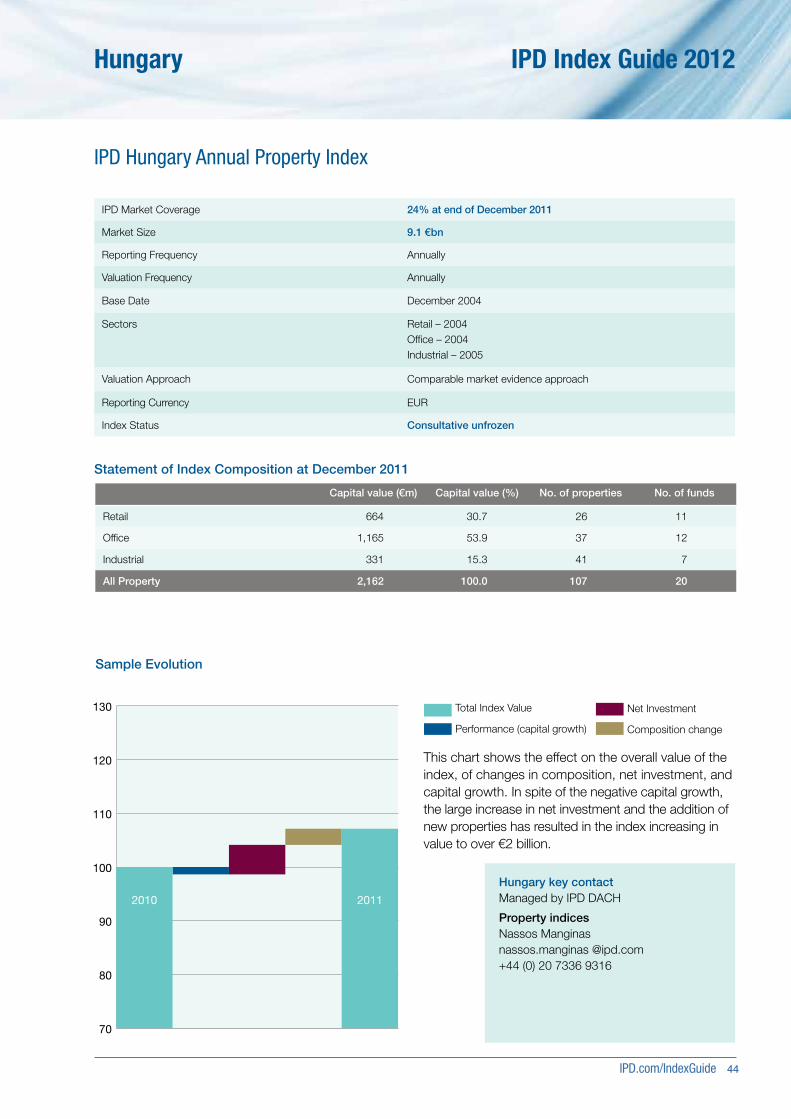

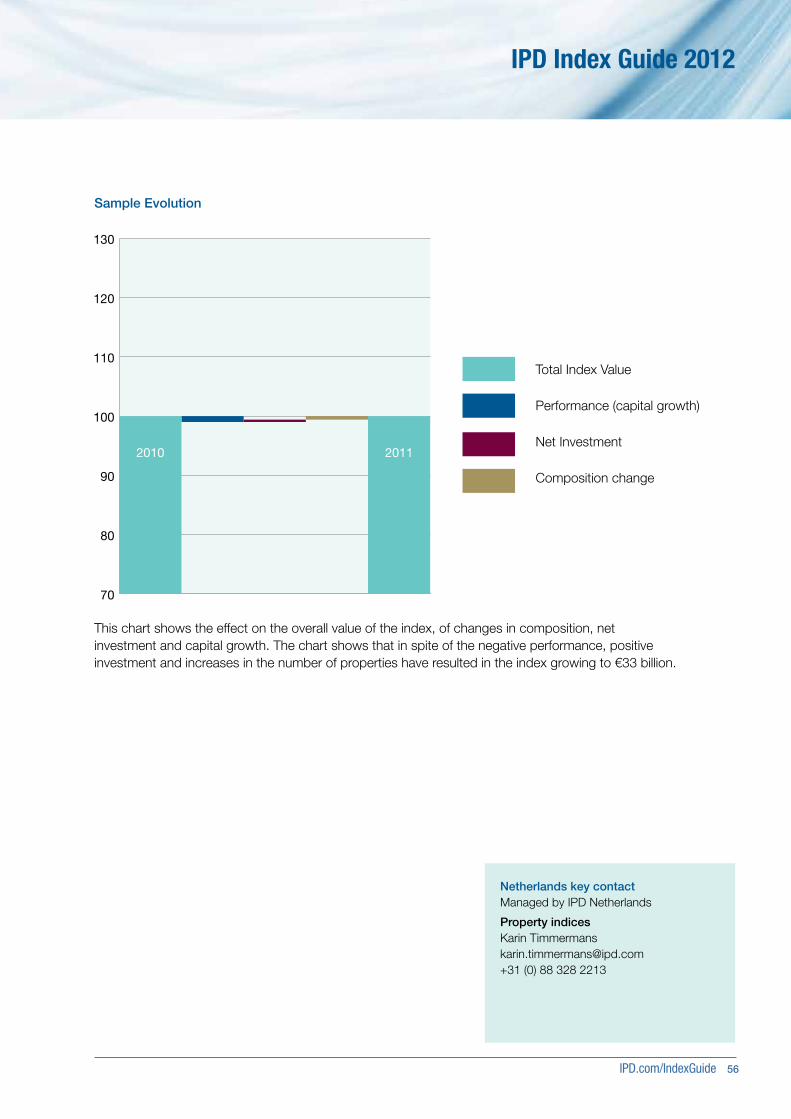

This chart shows the effect on the overall value of the index, of changes in composition, net investment and capital growth. The chart shows there has been positive net investment in Austria, positive capital growth and the inclusion of new funds has also increased the size of the sample covered by IPD, resulting in the index measuring just under €7 billion worth of property.

Total Index Value

Performance (capital growth)

Net Investment

Composition change

Austria key contactManaged by IPD DACH

Property indicesRalf Lemke [email protected] +49 (0) 611 334 49 86

29 IPD.com/IndexSchedule

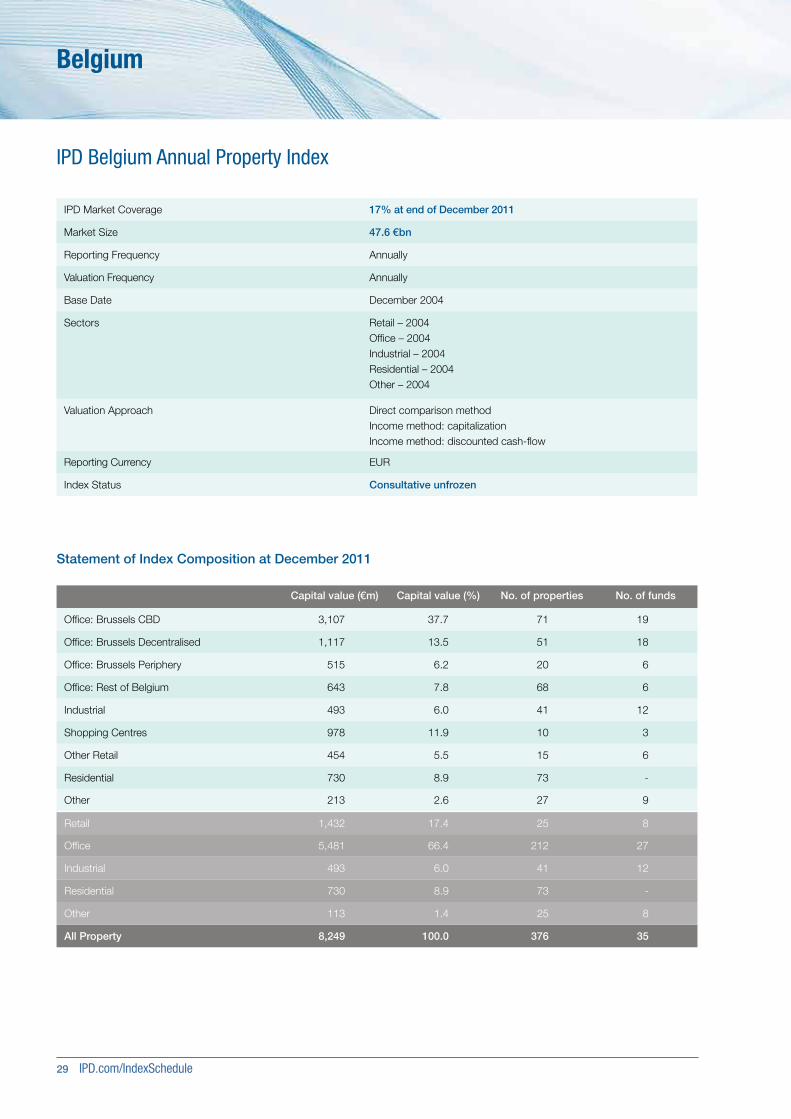

Belgium

IPD Belgium Annual Property Index

Capital value (€m) Capital value (%) No. of properties No. of funds

Office: Brussels CBD 3,107 37.7 71 19

Office: Brussels Decentralised 1,117 13.5 51 18

Office: Brussels Periphery 515 6.2 20 6

Office: Rest of Belgium 643 7.8 68 6

Industrial 493 6.0 41 12

Shopping Centres 978 11.9 10 3

Other Retail 454 5.5 15 6

Residential 730 8.9 73 -

Other 213 2.6 27 9

Retail 1,432 17.4 25 8

Office 5,481 66.4 212 27

Industrial 493 6.0 41 12

Residential 730 8.9 73 -

Other 113 1.4 25 8

All Property 8,249 100.0 376 35

Statement of Index Composition at December 2011

IPD Market Coverage 17% at end of December 2011

Market Size 47.6 €bn

Reporting Frequency Annually

Valuation Frequency Annually

Base Date December 2004

Sectors Retail – 2004Office – 2004Industrial – 2004Residential – 2004Other – 2004

Valuation Approach Direct comparison methodIncome method: capitalizationIncome method: discounted cash-flow

Reporting Currency EUR

Index Status Consultative unfrozen

IPD.com/IndexGuide 30

IPD Index Guide 2012

Market Breakdown as at end December 2011

Closed Ended Funds

Other

Fund Manager 0.3

Pension Fund 0.1

14.7

19.6

20.5

12.8

15.8

5.26.2

SICAFI

Open Ended Funds 2.9

Private Funds

Non-ListedManagement Company

REIT

Insurance Funds

70

80

90

100

110

120

130

2010 2011

Sample Evolution

This chart shows the effect on the overall value of the index, of changes in composition, net investment and capital growth. The chart shows that in spite of the negative investment and poor performance, the sample covered by IPD has increased significantly, resulting in the index measuring over €8 billion worth of property.

Total Index Value

Performance (capital growth)

Net Investment

Composition change

Belgium key contactManaged by IPD Southern Europe

Property indicesSebastien [email protected]+49 (0) 611 334 49 986

31 IPD.com/IndexSchedule

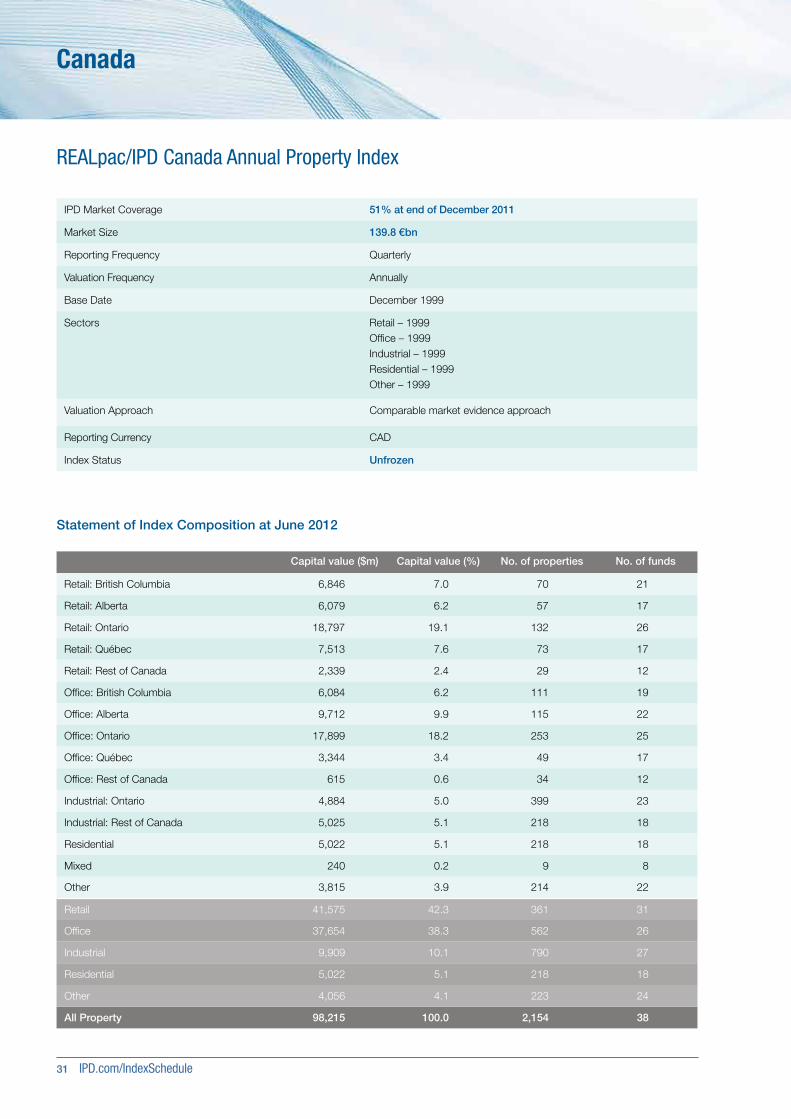

Canada

REALpac/IPD Canada Annual Property Index

Capital value ($m) Capital value (%) No. of properties No. of funds

Retail: British Columbia 6,846 7.0 70 21

Retail: Alberta 6,079 6.2 57 17

Retail: Ontario 18,797 19.1 132 26

Retail: Québec 7,513 7.6 73 17

Retail: Rest of Canada 2,339 2.4 29 12

Office: British Columbia 6,084 6.2 111 19

Office: Alberta 9,712 9.9 115 22

Office: Ontario 17,899 18.2 253 25

Office: Québec 3,344 3.4 49 17

Office: Rest of Canada 615 0.6 34 12

Industrial: Ontario 4,884 5.0 399 23

Industrial: Rest of Canada 5,025 5.1 218 18

Residential 5,022 5.1 218 18

Mixed 240 0.2 9 8

Other 3,815 3.9 214 22

Retail 41,575 42.3 361 31

Office 37,654 38.3 562 26

Industrial 9,909 10.1 790 27

Residential 5,022 5.1 218 18

Other 4,056 4.1 223 24

All Property 98,215 100.0 2,154 38

Statement of Index Composition at June 2012

IPD Market Coverage 51% at end of December 2011

Market Size 139.8 €bn

Reporting Frequency Quarterly

Valuation Frequency Annually

Base Date December 1999

Sectors Retail – 1999Office – 1999Industrial – 1999Residential – 1999Other – 1999

Valuation Approach Comparable market evidence approach

Reporting Currency CAD

Index Status Unfrozen

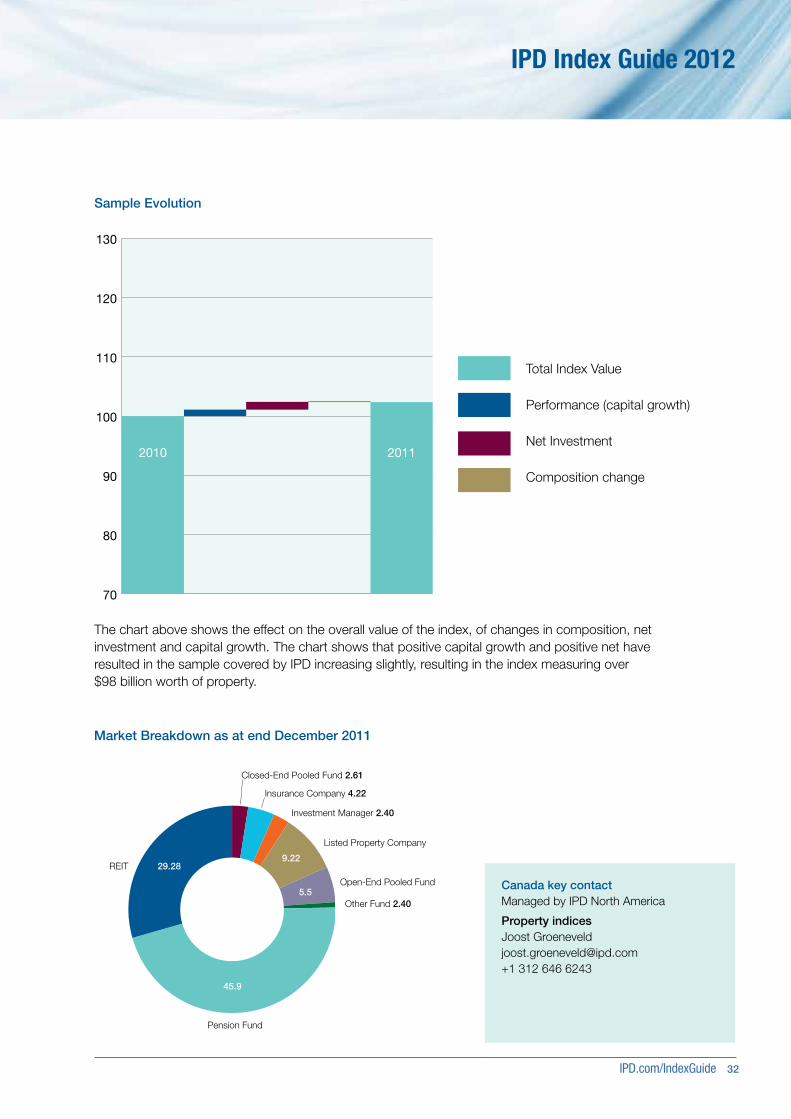

IPD.com/IndexGuide 32

IPD Index Guide 2012

Market Breakdown as at end December 2011

70

80

90

100

110

120

130

2010 2011

Sample Evolution

Closed-End Pooled Fund 2.61

Insurance Company 4.22

Investment Manager 2.40

Other Fund 2.40

Pension Fund

REIT

Listed Property Company

Open-End Pooled Fund

9.22

5.5

45.9

29.28

The chart above shows the effect on the overall value of the index, of changes in composition, net investment and capital growth. The chart shows that positive capital growth and positive net have resulted in the sample covered by IPD increasing slightly, resulting in the index measuring over $98 billion worth of property.

Total Index Value

Performance (capital growth)

Net Investment

Composition change

Canada key contactManaged by IPD North America

Property indicesJoost [email protected] +1 312 646 6243

33 IPD.com/IndexSchedule

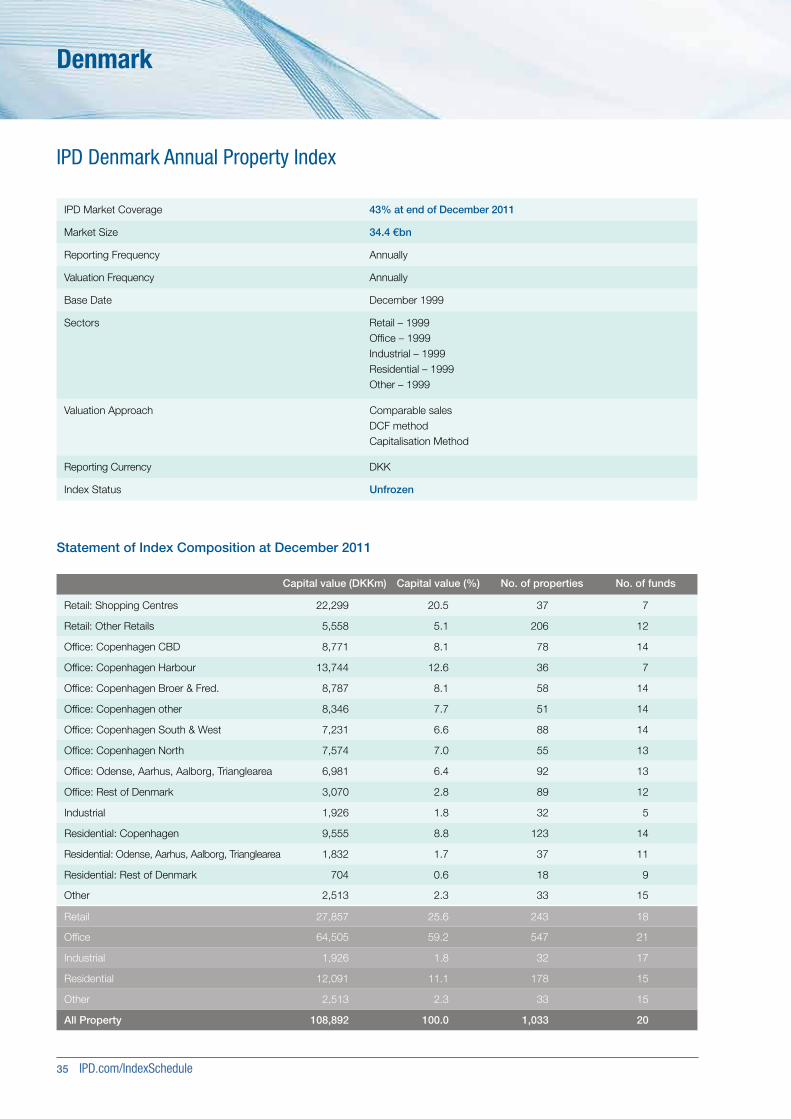

Czech Republic

IPD Czech Republic Annual Property Index

Capital value (€m) Capital value (%) No. of properties No. of funds

Retail 761 26.4 40 9

Office 1,578 54.8 42 12

Industrial 540 18.8 37 11

All Property 2,888 100.0 120 22

Statement of Index Composition at June 2012

IPD Market Coverage 26% at end of December 2011

Market Size 11.2 €bn

Reporting Frequency Annually

Valuation Frequency Annually

Base Date December 2004

Sectors Retail – 2004Office – 2004Industrial – 2005

Valuation Approach Comparable market evidence approach

Reporting Currency EUR

Index Status Consultative unfrozen

70

80

90

100

110

120

130

2010 2011

Sample Evolution

This chart shows the effect on the overall value of the index, of changes in composition, net investment and capital growth. Positive capital growth, net investment and the introduction of new properties into the index has resulted in it increasing in value to just under €3 billion.

Czech Republic key contactManaged by IPD DACH

Property indicesNassos Manginas nassos.manginas @ipd.com+44 (0) 20 7336 9316

Total Index Value

Performance (capital growth)

Net Investment

Composition change

IPD.com/IndexGuide 34

IPD Index Guide 2012