investor presentation -...

TRANSCRIPT

Investor PresentationNovember 2014

Disclaimer

2

This presentation is not an offer to sell securities, nor is it a solicitation of an offer to buy securities, inany locality, state, country or other jurisdiction where such distribution, publication, availability or usewould be contrary to law or regulation or which would require any registration or licensing withinsuch jurisdiction.

Certain statements in this presentation and responses to various questions may constituteforward‐looking statements, including statements regarding the Company’s financial position,business strategy and plans and objectives of management for future operations. These statements,which in some cases contain words such as "believe,” “expect,” “anticipate,” “intends,” “estimate,”“forecast,” “project,” “will,” “may,” “should” and similar expressions, reflect the beliefs andexpectations of the Company and are subject to significant known and unknown risks, contingenciesand uncertainties, including those described under “Risk factors” in our most recent Annual Report onForm 20-F filed with the Securities and Exchange Commission or the SEC, which are difficult orimpossible to predict and beyond the company’s control, and which may cause actual results to differmaterially from those discussed in the forward-looking statement. These forward-looking statementsare made only as of the date hereof, and the Company undertakes no obligation to update or revisethe forward-looking statements, whether as a result of new information, future events or otherwise.

Throughout this presentation, we reference adjusted EBITDA, which is a non-GAAP financial measure.Please refer to the Appendix to this presentation, as well as to our most recent Annual Report on Form20-F, filed with the SEC on March 27, 2014, and our report of Foreign Private Issuer on Form 6-K,furnished to the SEC on November 12, 2014, for a discussion of adjusted EBITDA, reconciliation ofGAAP to Non-GAAP results, and a reconciliation of net income to adjusted EBITDA, the most directlycomparable financial measure required by, or presented in accordance with U.S. GAAP.

Presenting today

3

Tzipi Ozer-Armon | CEO

May 2012 - joined Lumenis

2009-2012 - TEVA Pharmaceuticals [NASDAQ: TEVA]; Last position, headed Japan activities with P&L responsibility ~$900m

2006-2008 - SanDisk [NASDAQ: SNDK]; Last position, Senior VP, Retail Sales & Marketing with sales responsibility ~$2.5B

2004-2006 – M-Systems [NASDAQ: FLSH]; VP General Manager, DiskOnKey Division with P&L responsibility ~$450m

1999-2004 – Comverse, VP Corporate Development

1991-1995 – Manager, AT Kearney, London

MBA and BA Economics Cum Laude, Tel Aviv University

Ophir Yakovian | CFO

February 2012 - joined Lumenis

2006-2012 - VP Finance, Verint Systems [NASDAQ: VRNT]

2001-2006 - Corporate controller, Metalink [NASDAQ:MTLK]

1998-2001 - Senior auditor, Deloitte

MA, Business Economics Suma Cum Laude and BA, Economics & Accounting Cum Laude, Bar-Ilan University

Who are we?

4

5

Investment highlights

Committed to delivering accelerating, sustainable and profitable growth

Total addressable market of $3.5b, growing at high single digitGrowth correlates with aging population2/3 reimbursed, 1/3 out of pocket

Large and growing markets

Innovative technology- better technology for better patient careGlobal reach, with strong presence in APACStrong brand- over 40 years of clinical outcomes

Strong management, proven execution track recordTwo largest business segments grew at an average of 10% in 2013GM expansion of 810 BPS over the last three years

Transformed-delivering accelerated profitable growth

Key product launches in 2014 Geographical expansionNew domains, leveraging technology / market reachExpanding margins

Solid plans: growth and margin expansion

Strong competitive assets

Accelerated growth on an LTM basis…

6

New management

Realigned organization

Revitalized R&D process and pipeline

Culture of accountability and success

Demonstrated financial results

LTM Revenues, $m

Q4Q3

284

261

257

Q3

265

Q2

251

Q2Q1 Q3

245

Q1Q4

247245

249

271

Q2

277

Q1

6.7%

2.4%

4.7%

5.3%

0.7%

2012 LTM 2013 LTM

7.9%

2014 LTM

8.0%

8.8%

X%LTM growth, YoY

Q3’14LTM

152

2013

142

113

123

2011 2012

…and significant improvement in profitability

7

Revenue growth acceleration

810bps gross margin improvement

Adjusted EBITDA margins1 doubled

1%

7%

10%

15%

$m$m$m

2011 2012

265

249

Q3’14LTM

284

2013

247

(1) Adjusted EBITDA represents net income before depreciation and amortization, stock-based compensation, legal settlements, net and other non-recurring expenses, financial expenses, net and taxes on income.

7%

45.6%

49.6%

53.6%53.7%

2011

26

12

2013

31

Q3’14LTM

2012

18

46%

4.9%

7.2%

9.8%

10.8%

47%

19%7%

Revenue growth acceleration

Key launches will support future growth

8

Completely shifted gear

1 1

1

1

1

2

11

11

2013

2Aesthetic

Surgical

Ophthalmic

20142011 201220102009

2

2008

4

2007

Number of product releases per year, 2007-2014

5 Launches

6 Launches

New products launched in the past 18 months generated over

15% of product revenues in Q3’14

Well-positioned across multiple attractive end markets

9

Q3’14 LTM: $284m

Ophthalmic - $59m -3% in LTM; 21% of total revenue Retina Glaucoma & Secondary

CataractAddressable market of ~$350m

Aesthetic - $116m +19% Growth in LTM; 41% of total revenue Skin rejuvenation Hair removalAddressable market of ~$1.5b

Surgical - $109m +6% Growth in LTM; 38% of total revenue BPH (Benign Prostatic

Hyperplasia) Lithotripsy ENT Micro-SurgeryAddressable market of ~$1.7b

Total addressable market of ~$3.5b

Global reach, scale and APAC strength

10

Asia Pacific business more than doubled within the past 5 years

Q3’14 LTM: $284m

>420 employees

across:

China

India

Australia

Hong Kong

Singapore

Americas32% - $92m

Japan14% - $40m

EMEA20% - $56m

APAC34% - $96m

$m

75

60

4739

201120102009 2013

$86m

2012 2014E

Growth of 16% in 2014 YTD

Surgical leader focused on improving patient outcomes

11

~$1.7b addressable market

BPH

The BPH solution - Enucleation Minimizes collateral damage Better symptomatic recovery Lowest re-intervention rate Shorter hospital stays

PowerSuite 100W Holmium

Lithotripsy

The stone dusting solution Minimally invasive urinary lithotripsy Self clearing stones Broad stone targeting

PowerSuite 60W Holmium

ENT

Advanced precision and guidance High-end, high-energy, short-pulse-duration CO2 laser Vaporization and excision Minimal collateral tissue damage Better patient outcomes

AcuPulse DUO

New Product Introduction -Lumenis Pulse 120H

12

“All in One” superior platform for laser Urology solutions: Enucleation, Vaporization, Flexible Ureteroscopy and PCNL

Addressing 5 most desired outcomes: safety, minimized procedure time, superior clinical outcome, ease of use, cost efficiency

Set of new supplemental tools: tools and fibers for comprehensive treatment

Received FDA clearance and CE mark in March 2014

First units shipped in Q2’14; sales expected to ramp up in 2015

Pioneer in the Ophthalmic laser market

13

~$350m addressable market

Retina

Upgradable, cost effective treatment Treats various retinal pathologies Better treatment of existing indications

Vision One

Array Laser Link

Glaucoma& Secondary Cataract

SLT1 inventor SLT, YAG photo-disruption and photo-coagulation Maximum space utilization Proven long term clinical efficacy Accounts for 50% of global SLT market

Selecta Trio

Continual innovation Array Laser Link pattern scanning device Reduces procedure time by 80% Received FDA and MHLW clearance in Q4’13 Expands the capability of Vision1 and Spectra

(1) Selective Laser Trabeculoplasty

New Product Introduction - Array - Scanning Laser Link

14

The benefits of pattern scanning laser with the familiarity of Lumenis laser for Retina treatments

Shorter duration for each spot creates less intense burns, less pain to the patient and greater predictability

Multiple spots allow shorter and fewer treatments

Reduced risk of retinal bleeding

Product differentiation

Touchpad allows the physician to maintain eyes-forward while performing titrate, power adjustments and pattern modifications

Heads up display - While changing the system’s parameters the physician gets a visual confirmation displayed on the Retina (power, status)

Received FDA, CE mark and Japanese MHLW

Premium brand in Aesthetics

15

~$1.5b addressable market

Skin Rejuvenation

Deep, single pulse penetration

Multi-application, modular, upgradable platform

Proven clinical efficacy and safety

ResurFx – “truly fractional” solution

Ability to address severe scarring

M22

UltraPulse

HairRemoval

The Gold standard in hair removal

Significantly more comfortable and less painful

Short treatment cycle

Fast treatment time

Superior efficacy

LightSheer

New Product Introduction - LightSheer Infinity & Desire

16

LightSheer Infinity LightSheer Desire

Compact, portable and upgradablelaser hair removal system with HIT1

technology and advanced user interface

Ability to treat all body areas and skin types

805nm wavelength diode, vacuum assist technology and contact cooling ChillTip

FDA and CE approved

Our cutting edge laser hair removal system with HIT1 and advanced user interface

Up to 75 percent faster than other currently available devices

All existing benefits plus Dual Wavelength – 805nm & 1060nm to treat dark and tanned skin, vacuum assist technology and contact cooling ChillTip

FDA and CE approved

(1) High-speed Integrated Technology for increased safety and efficacy and decreased pain and treatment time

Increase penetration in

existing territories

Expand and go direct in

emerging territories

Several key launches of new platforms in

2014…and more to come

Penetrate new domains with innovative

platforms

Our plan for accelerated profitable growth

17

3

Continue to improve

profitability

2Expand

geographic footprint

1Launch

innovative new

productsGross Margin

expansion

Operational excellence

Ophir Yakovian — Chief Financial Officer

Financial review

Growth expected to continue at high-single digit pace

Nine quarters of continuous revenue growth

19

YoY

3.7%(0.4%)

74.272.5

65.871.1

67.866.360.1

66.363.960.9

57.6

Q3’12 Q2’13Q1’13Q4’12Q2’12Q1’12 Q3’14Q2’14Q1’14Q3’13 Q4’13

(2.8%) 1.9% 4.4% 9.0% 6.2% 7.3% 9.5%

Revenues, $m

9.3% 9.4%

Proven track record of margin expansion

2020

Gross margin expanding 810 BPS since 2011Adjusted EBITDA margin expanding 590 BPS ($18.5m) since 2011

Drivers of margin expansion: Tight inventory management

Improved manufacturing efficiency

Product quality

Cost reduction across platforms

Scale

Q2’13 Q4’13

9.8%

26.0

10.1%

27.3

Q1’14

29.2

10.5%

$30.6m

Q2’14Q3’13

9.4%

24.5

Q1’13 Q3’14

10.8%

22.1

8.6%

13.2

Q4’12

17.8

4.2%

7.7%

12.1

7.2%

19.2

Q3’12Q1’12 Q2’12

15.710.4

Q4’11

4.9% 5.4%6.3%

Q3’12

48.5%

Q2’12

51.5%

Q1’13Q4’12

50.5%

Q2’14Q1’14

53.9%

Q4’13

54.0%

Q3’13

53.5%

Q2’13

52.6%

49.8%

53.7%

45.6% 45.9%

Q4’11

47.2%

Q1’12 Q3’14

% of revenue

$mx

Q3’14 Non-GAAP results

21

$ in millionActual Q3’13

Actual Q3’14

Variance Q3’13-Q3’14

Revenues 67.8 74.2 6.4

YoY growth (%) 9.4%

Gross profit 37.2 39.7 2.5

Gross margin, % 54.8% 53.5% -1.3%

Adjusted EBITDA 8.7 10.2 1.4

EBITDA margin, % 12.9% 13.7% 0.8%

YoY growth (%) 16.4%

Net income 5.7 6.0 0.2

Net margin, % 8.4% 8.0% -0.4%

YoY growth (%) 4.2%

Fully diluted EPS ($) 0.19 0.17 -0.02

2014 Annual guidance

22

For the full year ended December 31, 2014, we expect to report on a non-GAAP basis:

Revenue in a range of $285 and $287 million, representing an

increase of 7% - 8% year-over-year

Adjusted EBITDA in a range of $29.6 to $30.6 million,

representing an increase of 14% - 18% year-over-year

Non-GAAP Net Income in a range of $18.1 to $19.6 million

reflecting an Non-GAAP EPS of $0.51 - $0.55

Thank You

www.lumenis.com

APPENDIX

24

Q3’14 vs. Q3’13 Reconciliation of GAAP to Non-GAAP

25

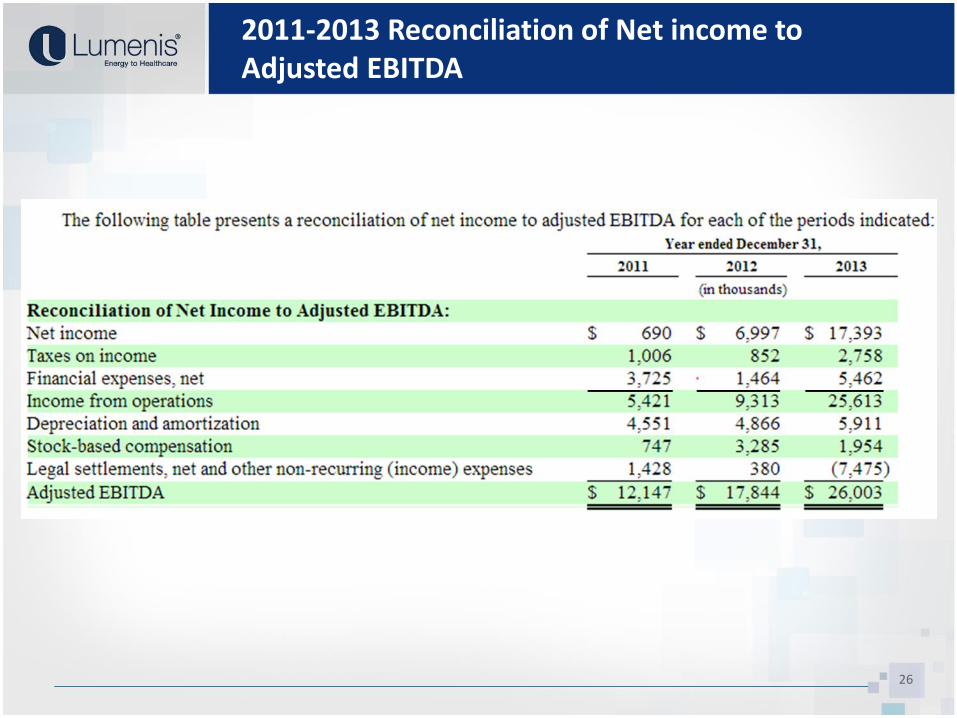

2011-2013 Reconciliation of Net income to Adjusted EBITDA

26