investment policy statement ppt northwest planned giving roundtable nov 13 2015 with notes

TRANSCRIPT

1

2

If the research is correct and many investors make decisions based on their feelings and not

what they know…It’s important to understand how are we currently feeling?

3

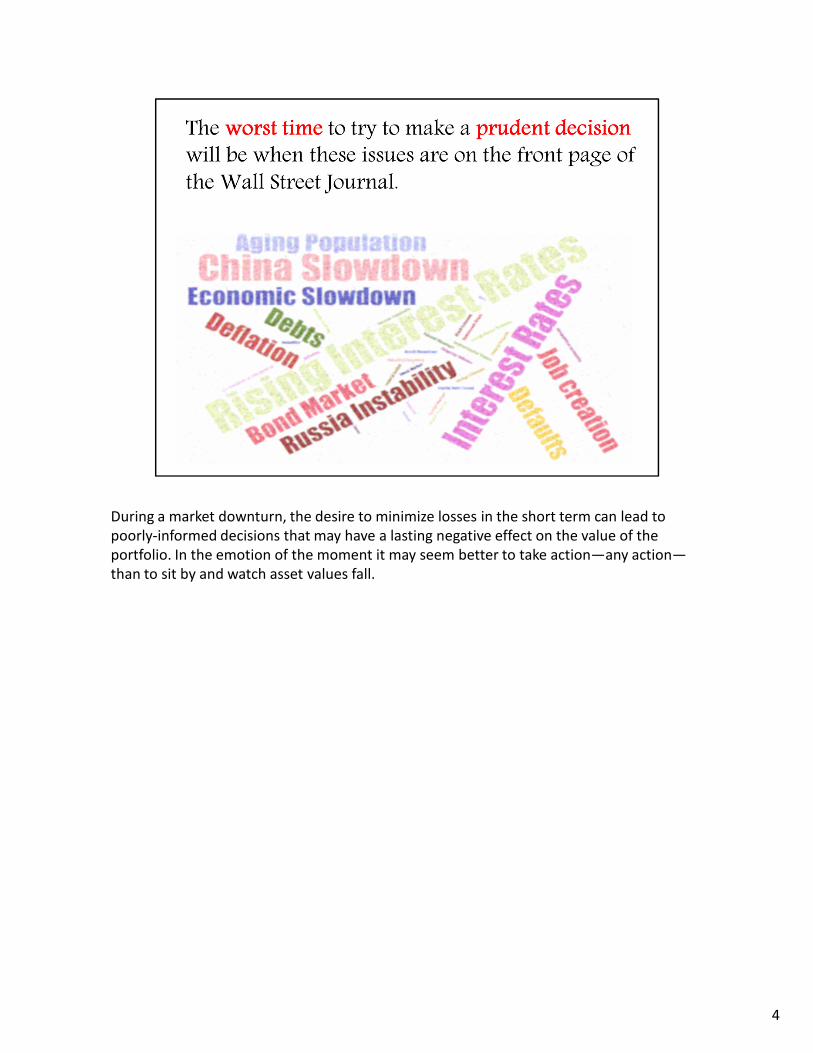

During a market downturn, the desire to minimize losses in the short term can lead to

poorly-informed decisions that may have a lasting negative effect on the value of the

portfolio. In the emotion of the moment it may seem better to take action—any action—

than to sit by and watch asset values fall.

4

A well written IPS along with prudent execution insulates your organization from making

decisions based on short-term events that lead to poor long-term outcomes.

5

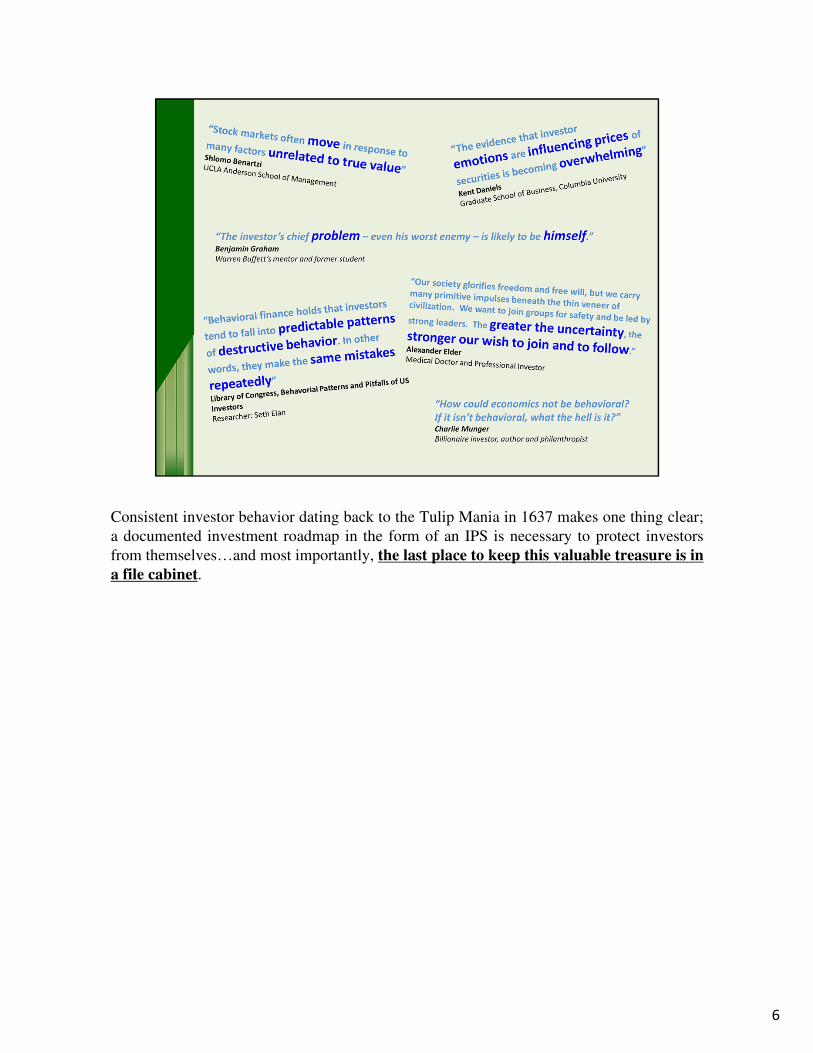

Consistent investor behavior dating back to the Tulip Mania in 1637 makes one thing clear;

a documented investment roadmap in the form of an IPS is necessary to protect investors

from themselves…and most importantly, the last place to keep this valuable treasure is in

a file cabinet.

6

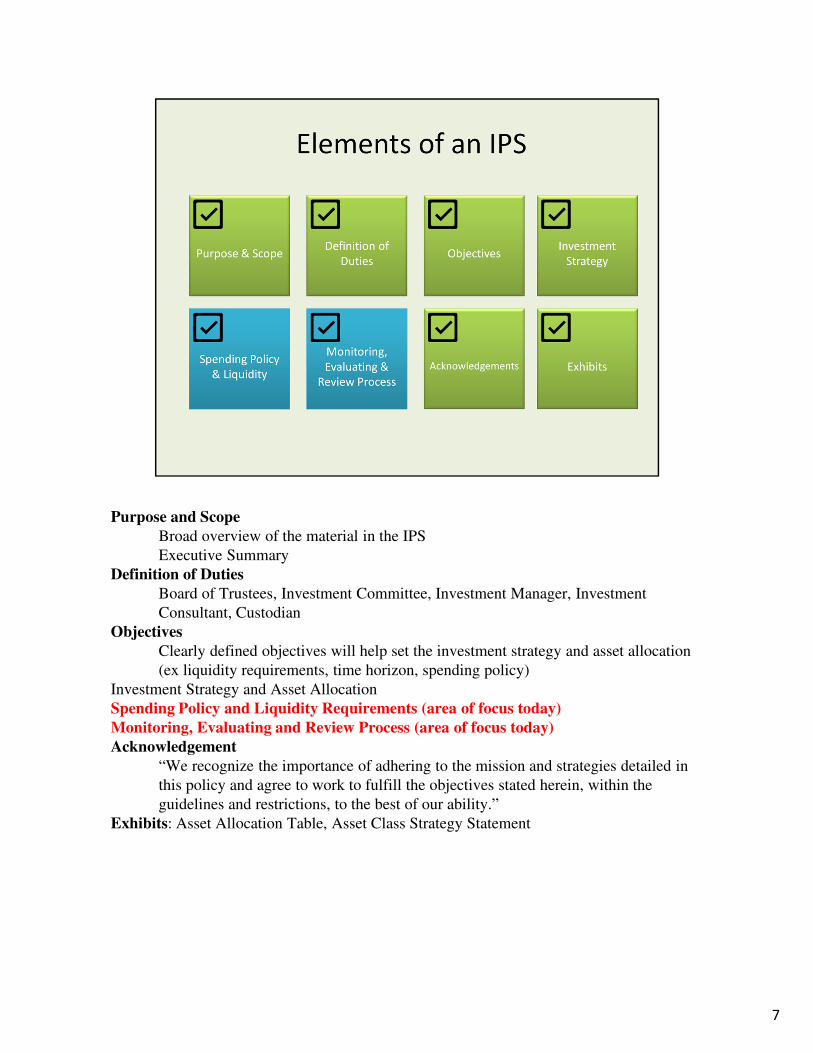

Purpose and Scope

Broad overview of the material in the IPS

Executive Summary

Definition of Duties

Board of Trustees, Investment Committee, Investment Manager, Investment

Consultant, Custodian

Objectives

Clearly defined objectives will help set the investment strategy and asset allocation

(ex liquidity requirements, time horizon, spending policy)

Investment Strategy and Asset Allocation

Spending Policy and Liquidity Requirements (area of focus today)

Monitoring, Evaluating and Review Process (area of focus today)

Acknowledgement

“We recognize the importance of adhering to the mission and strategies detailed in

this policy and agree to work to fulfill the objectives stated herein, within the

guidelines and restrictions, to the best of our ability.”

Exhibits: Asset Allocation Table, Asset Class Strategy Statement

7

The next three slides will paint a disappointing outlook for stock and bond returns on a go

forward basis. The most common asset allocation is around 60% equity 40% fixed income.

A ubiquitous 60/40 allocation typically has delivered over a full market cycle 6%-8.5%.

Let’s assume stocks return 8% and bonds 2.5% (due to the low entry yield) over the next

decade. The portfolio would deliver a total return of 5.8% (8%x.60 = 4.8% + 2.5%

x.4=1.0%=5.8%.

8

Interest rates have steadily declined since the early 1980s. This created a great 35+ year

secular bull market for bonds. Remember bond values are inverse related to bond yields.

So when bond yields decline the value of bonds rises. When/If interest rates rise in the

future investors will experience declining bond values and bond yields rise.

9

10

11

Both of these investment groups are incredibly smart, but investors need to scrutinize

forecasts about the financial markets.

GMO forecast is in real terms meaning they have adjusted returns for their inflation

expectations. William Blair’s are not adjusted for inflation. In the footnotes WB expects

inflation to run at 1.8% over the next 8 years.

GMO, LLC founded in 1977, is a privately held global investment management firm

servicing clients in the corporate, public, endowment, and foundation marketplaces. As

of September 30, 2015, we managed $104 billion* in client assets using a blend of

traditional judgments with innovative quantitative methods to find undervalued securities

and markets.

Our success in consistently providing value added performance across a broad range of

asset classes is founded on several key factors that include: discipline, value orientation,

investment research, and constant innovation (see GMO Qualities below). Our broad-based

value added over benchmarks has led many of our clients to request that we allocate assets

and advise them on a global scale.

William Blair & Company is privately held employee-owned financial services firm that

provides investment banking, equity research, brokerage, asset management and private

capital services. William Blair & Company, L.L.C. was founded in 1935. The firm has

approximately 920 employees and is based in Chicago with offices in London, San

Francisco, Tokyo, Liechtenstein and Zurich.

12

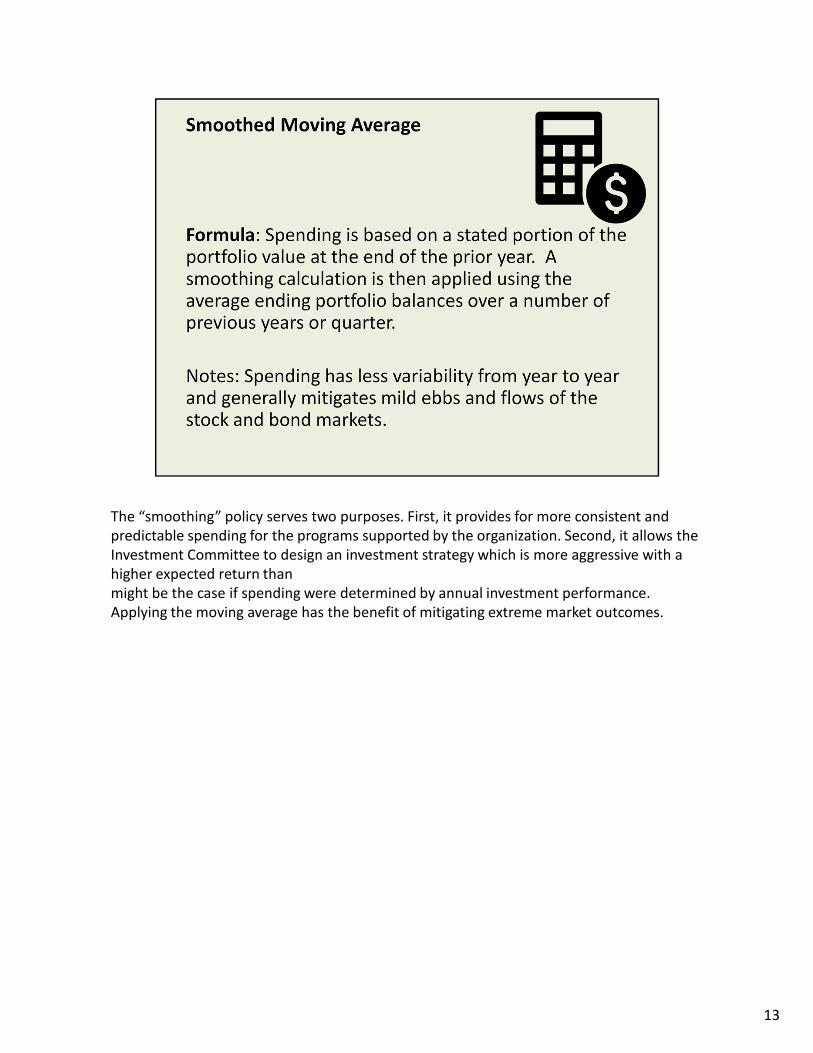

The “smoothing” policy serves two purposes. First, it provides for more consistent and

predictable spending for the programs supported by the organization. Second, it allows the

Investment Committee to design an investment strategy which is more aggressive with a

higher expected return than

might be the case if spending were determined by annual investment performance.

Applying the moving average has the benefit of mitigating extreme market outcomes.

13

Spending Language Example:

The College employs a total return Endowment spending policy that establishes the

amount of investment return made available for spending. The Board of Trustees

determines and implements the spending policy based on investment returns and the

needs of the College. Investment staff provides input to the Board of Trustees Finance

Committee regarding expected return of the Portfolio, a critical variable in the spending

policy.

Spending Language Example:

The Investment Committee will attempt to balance the Endowment’s shorter-term

distributions with its goal to provide for distributions in perpetuity and therefore design

a spending policy which is flexible. It is currently anticipated that contributions to the

Endowment will be greater than draws from it for a number of years, and that net draws

of 5% or more are not anticipated until FY 20XX, if not later. However, contributions and

distributions are expected to be inconsistent, and a target of at least $[X] million should

be maintained in cash equivalents in the Endowment.

Source: hallcapital.com “A Roadmap for the Roadmap, 2012

14

Hybrid Approach Example:

Under the Endowment spending policy, the payout is set as a dollar amount and

increased by the rate of inflation each year within a band. The increase each year is the

greater of 2% or the actual rate of inflation based on the most recent CPI, with a

maximum annual increase of 5%. In addition, the annual draw from the Endowment

shall be no less than 4% and no greater than 7% based on the prior year-end market

value of the Portfolio.

15

16

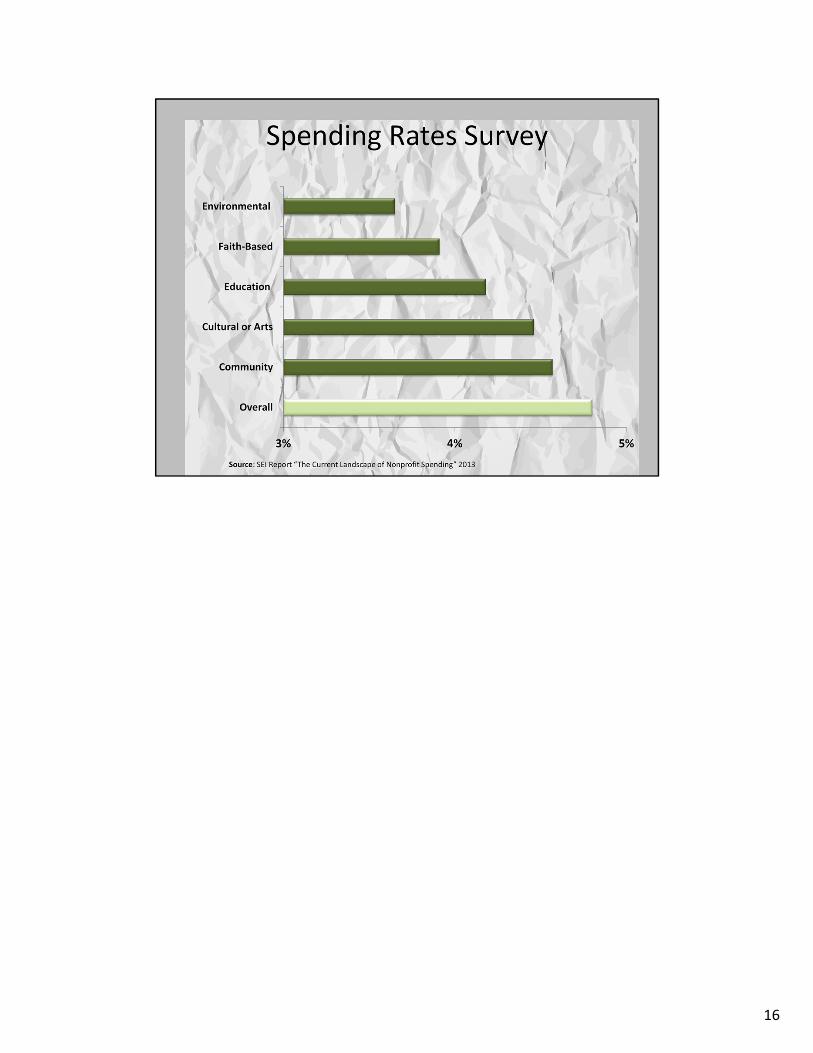

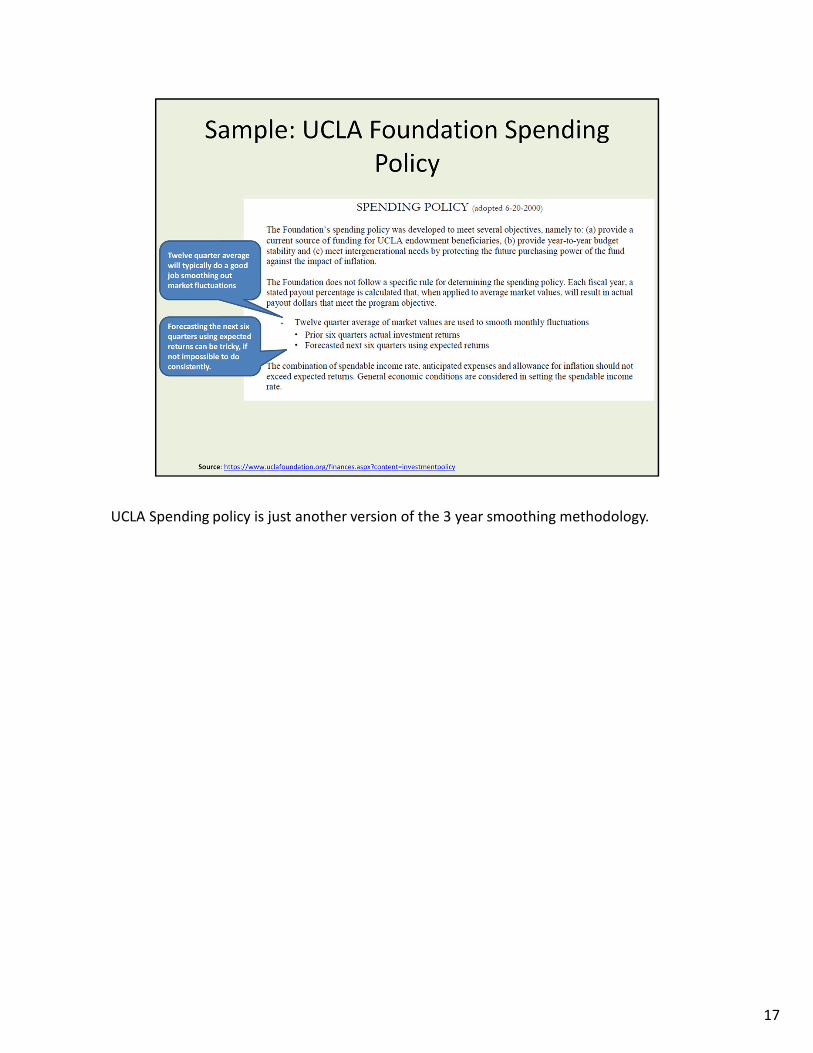

UCLA Spending policy is just another version of the 3 year smoothing methodology.

17

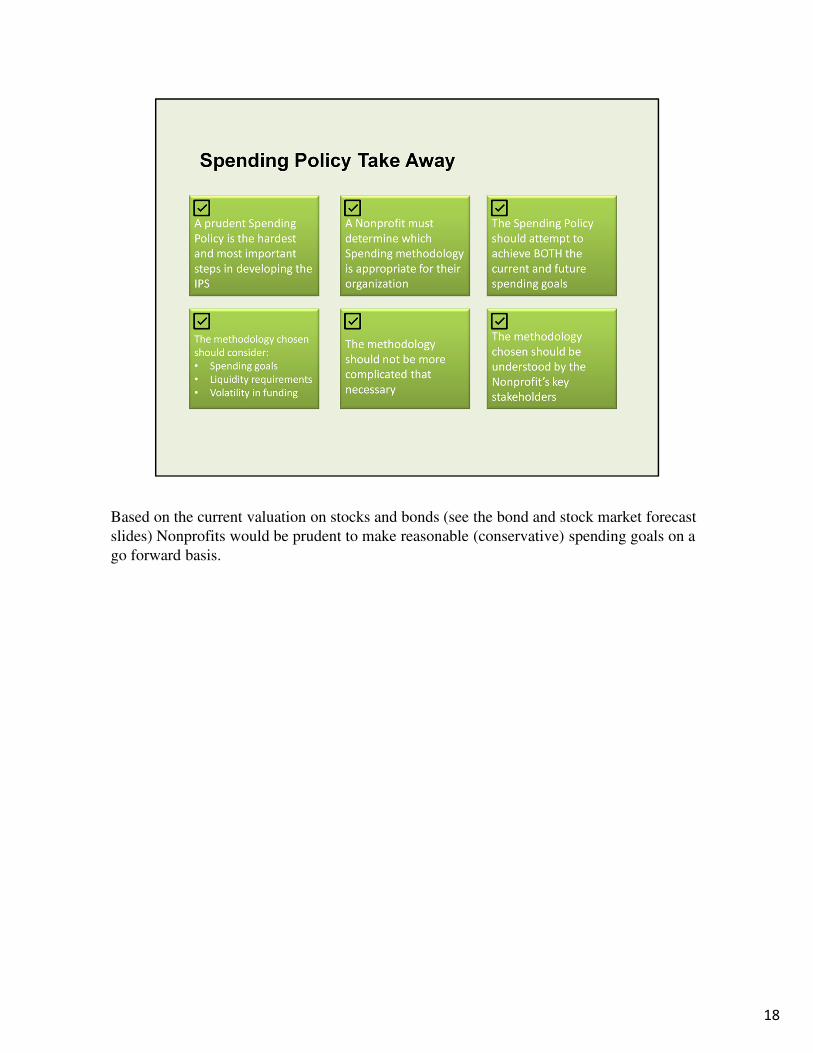

Based on the current valuation on stocks and bonds (see the bond and stock market forecast

slides) Nonprofits would be prudent to make reasonable (conservative) spending goals on a

go forward basis.

18

Long-term perpetual portfolios have a time frame longer than that of any other type of

investment program. Organizations should be mindful to make sure board members and

finance committees are always aware of the perpetual time horizon. It’s easy for individuals

to view the organization’s portfolio from their personal lens.

A good measure of success will be evaluated by the effectiveness of the investments in

producing a steady and growing stream of distributions that at least keeps pace with

inflation.

Inflation measures for nonprofit institutions are generally higher than those for consumers,

due in large measure to the comparatively labor-intensive nature of nonprofits’ activities.

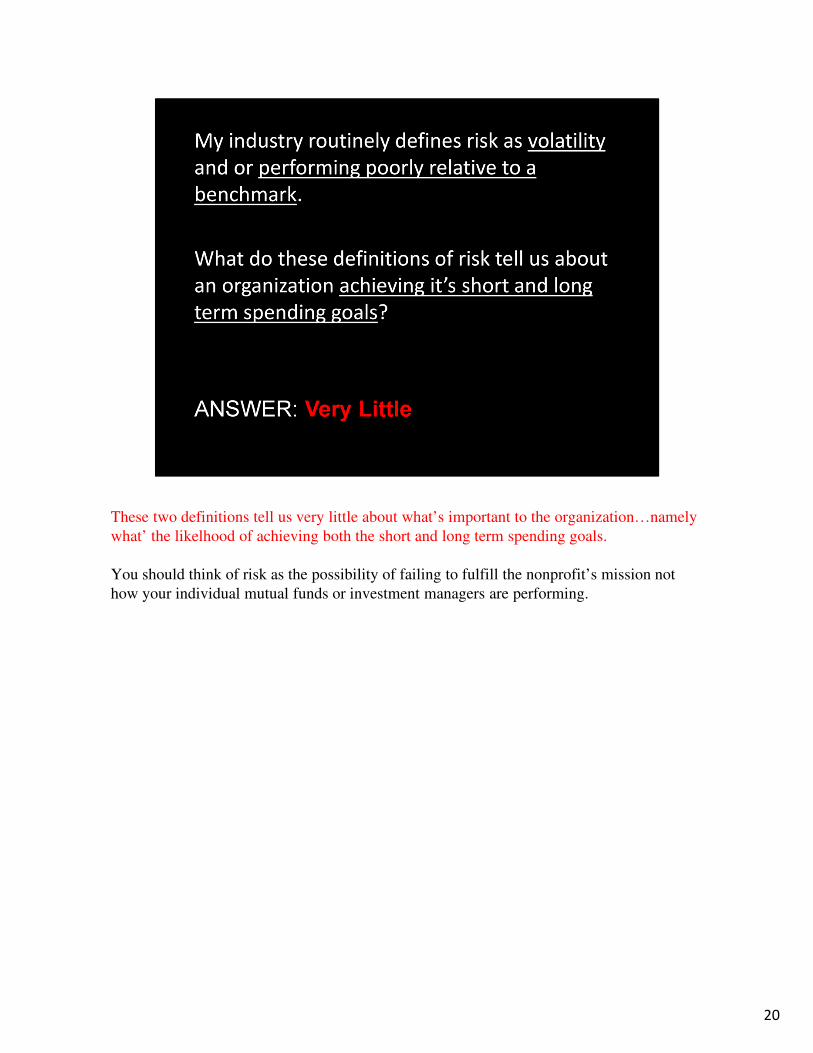

These two definitions tell us very little about what’s important to the organization…namely

what’ the likelhood of achieving both the short and long term spending goals.

You should think of risk as the possibility of failing to fulfill the nonprofit’s mission not

how your individual mutual funds or investment managers are performing.

20

These two definitions tell us very little about what’s important to the organization…namely

what’ the likelhood of achieving both the short and long term spending goals.

You should think of risk as the possibility of failing to fulfill the nonprofit’s mission not

how your individual mutual funds or investment managers are performing.

21

22

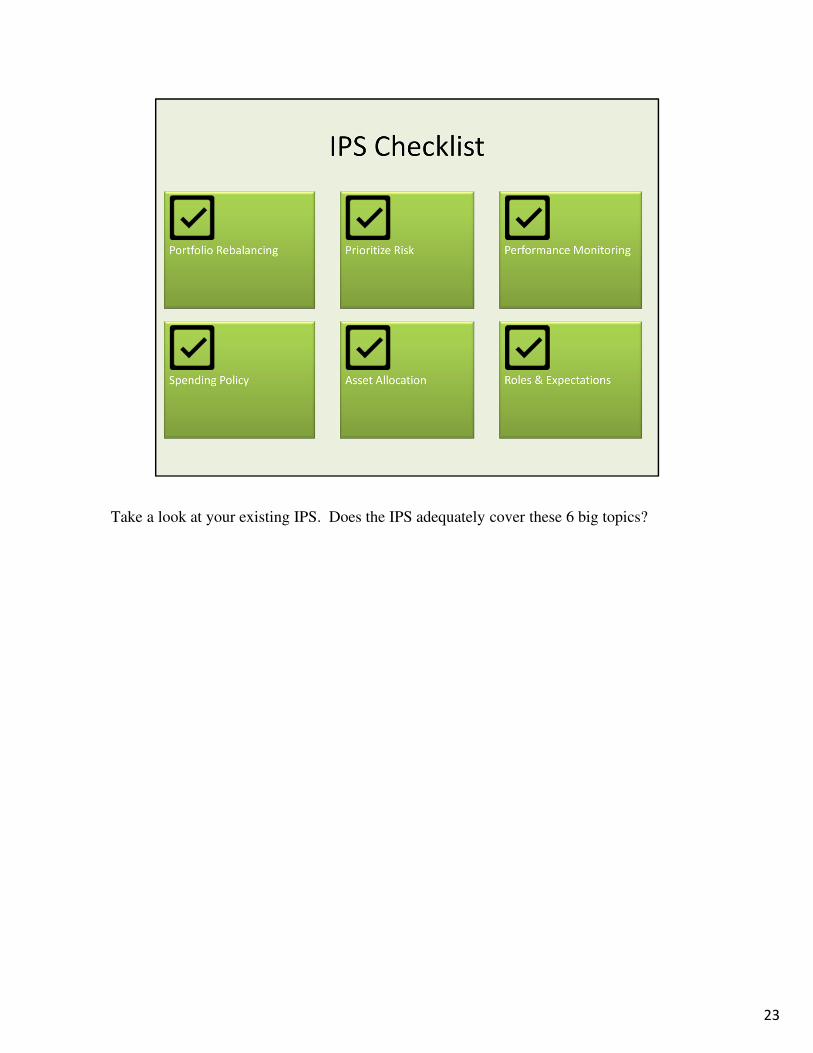

Take a look at your existing IPS. Does the IPS adequately cover these 6 big topics?

23

24

25

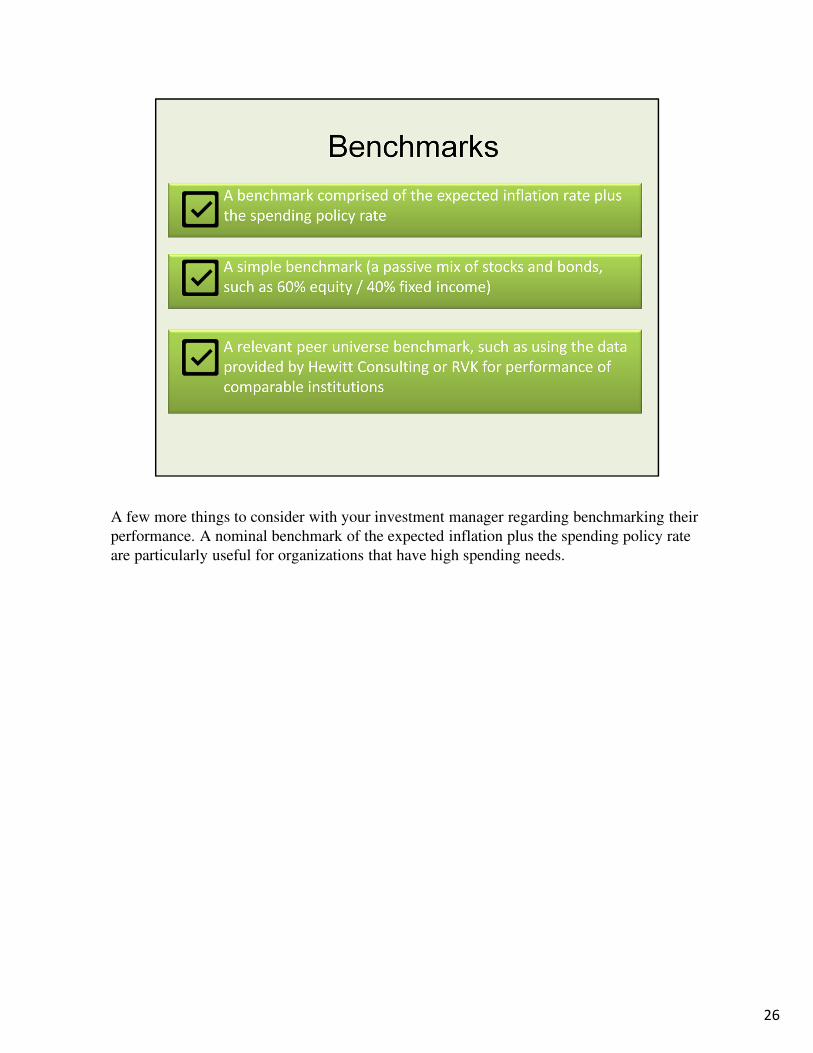

A few more things to consider with your investment manager regarding benchmarking their

performance. A nominal benchmark of the expected inflation plus the spending policy rate

are particularly useful for organizations that have high spending needs.

26

Where is the discussion of your organizations financial goals? Is the market conditions

likely to impact your short-term spending goals? What future expected return will the

portfolio have to produce to achieve your organization’s long-term goals? These questions

are usually absent during these reviews.

27

28

Stock Gifts: I suggest the organization have a standard default policy that stock gifts by

donor be received and sold in a timely way. Typically the organization isn’t in a position to

determine when to sell these assets. The investment manager depending on their investment

style, resources and capabilities may not properly monitor and track the stock gift or have

the expertise advice you when to sell. It’s typically best to default towards a policy of sell

in a timely way.

Fee Agreement: The nonprofit can negotiate with the investment manager for a lower fee

structure. If the nonprofit is a large and/or strategic client of the investment manager the

nonprofits can request (and in the right situation will get) a contractually agreement they

will be lowest cost client the investment had and in the event the investment manager makes

arrangements with a new or existing client for a more favorable fee structure your nonprofit

to get the same deal.

Avoid Back Tested Strategies: An investment manager will typically not show a client or

potential client a back-tested investment strategy that doesn’t have a wonderful past track

record. Why show a strategy or investment product that does performance extremely well.

The problem is many of these back tested strategies are “data mined” there is no guarantee

that just because a strategy worked in the past it will work in the future. Caveat Emptor

when it comes to investment folks pitching “back-tested” strategies.

Sample Request for Proposal

Proposal Requirements

29

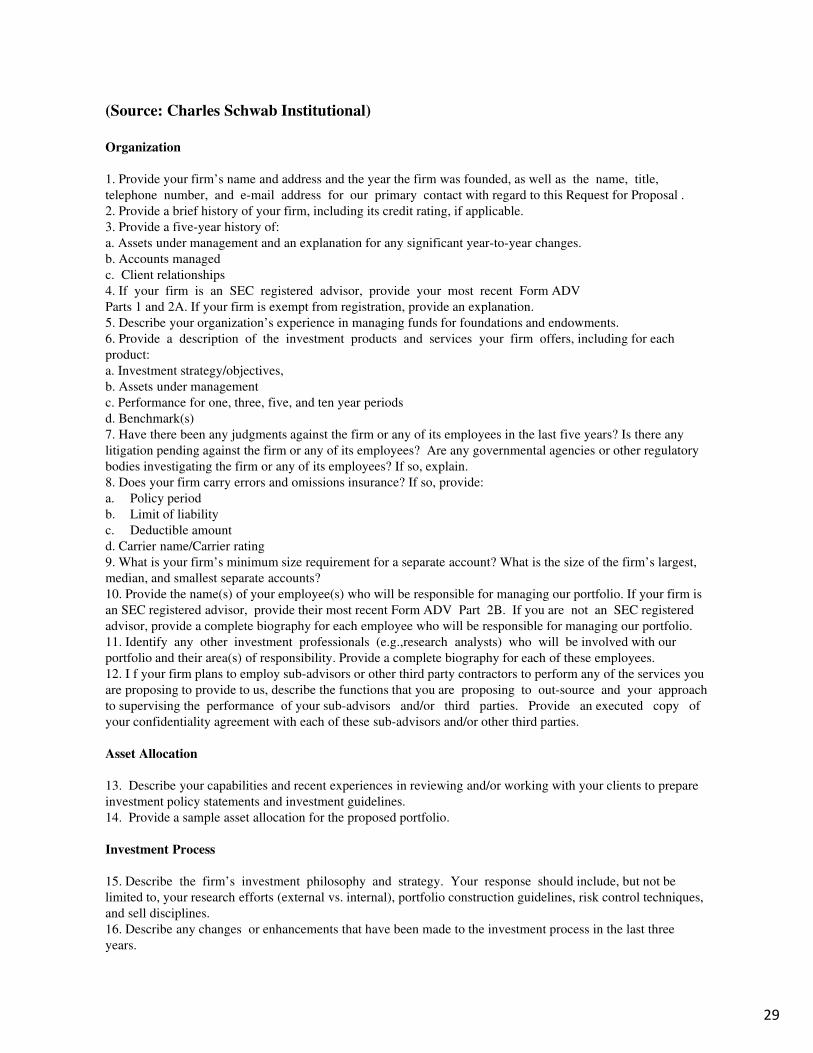

(Source: Charles Schwab Institutional)

Organization

1. Provide your firm’s name and address and the year the firm was founded, as well as the name, title,

telephone number, and e-mail address for our primary contact with regard to this Request for Proposal .

2. Provide a brief history of your firm, including its credit rating, if applicable.

3. Provide a five-year history of:

a. Assets under management and an explanation for any significant year-to-year changes.

b. Accounts managed

c. Client relationships

4. If your firm is an SEC registered advisor, provide your most recent Form ADV

Parts 1 and 2A. If your firm is exempt from registration, provide an explanation.

5. Describe your organization’s experience in managing funds for foundations and endowments.

6. Provide a description of the investment products and services your firm offers, including for each

product:

a. Investment strategy/objectives,

b. Assets under management

c. Performance for one, three, five, and ten year periods

d. Benchmark(s)

7. Have there been any judgments against the firm or any of its employees in the last five years? Is there any

litigation pending against the firm or any of its employees? Are any governmental agencies or other regulatory

bodies investigating the firm or any of its employees? If so, explain.

8. Does your firm carry errors and omissions insurance? If so, provide:

a. Policy period

b. Limit of liability

c. Deductible amount

d. Carrier name/Carrier rating

9. What is your firm’s minimum size requirement for a separate account? What is the size of the firm’s largest,

median, and smallest separate accounts?

10. Provide the name(s) of your employee(s) who will be responsible for managing our portfolio. If your firm is

an SEC registered advisor, provide their most recent Form ADV Part 2B. If you are not an SEC registered

advisor, provide a complete biography for each employee who will be responsible for managing our portfolio.

11. Identify any other investment professionals (e.g.,research analysts) who will be involved with our

portfolio and their area(s) of responsibility. Provide a complete biography for each of these employees.

12. I f your firm plans to employ sub-advisors or other third party contractors to perform any of the services you

are proposing to provide to us, describe the functions that you are proposing to out-source and your approach

to supervising the performance of your sub-advisors and/or third parties. Provide an executed copy of

your confidentiality agreement with each of these sub-advisors and/or other third parties.

Asset Allocation

13. Describe your capabilities and recent experiences in reviewing and/or working with your clients to prepare

investment policy statements and investment guidelines.

14. Provide a sample asset allocation for the proposed portfolio.

Investment Process

15. Describe the firm’s investment philosophy and strategy. Your response should include, but not be

limited to, your research efforts (external vs. internal), portfolio construction guidelines, risk control techniques,

and sell disciplines.

16. Describe any changes or enhancements that have been made to the investment process in the last three

years.

29

17. Describe how your portfolio managers interact with your research analysts.

18. Describe how an investment idea is originated, vetted, and approved.

19. Describe how Investments Are Select ed for a portfolio (for example, model portfolio approach, approved

firm buy list, other).

20. Describe how research is organized and any changes in the last three years.

21. Detail the policies and procedures you have established to insure compliance with your clients’ investment

policy statements and guidelines and to assure quality control of the portfolio management process.

29

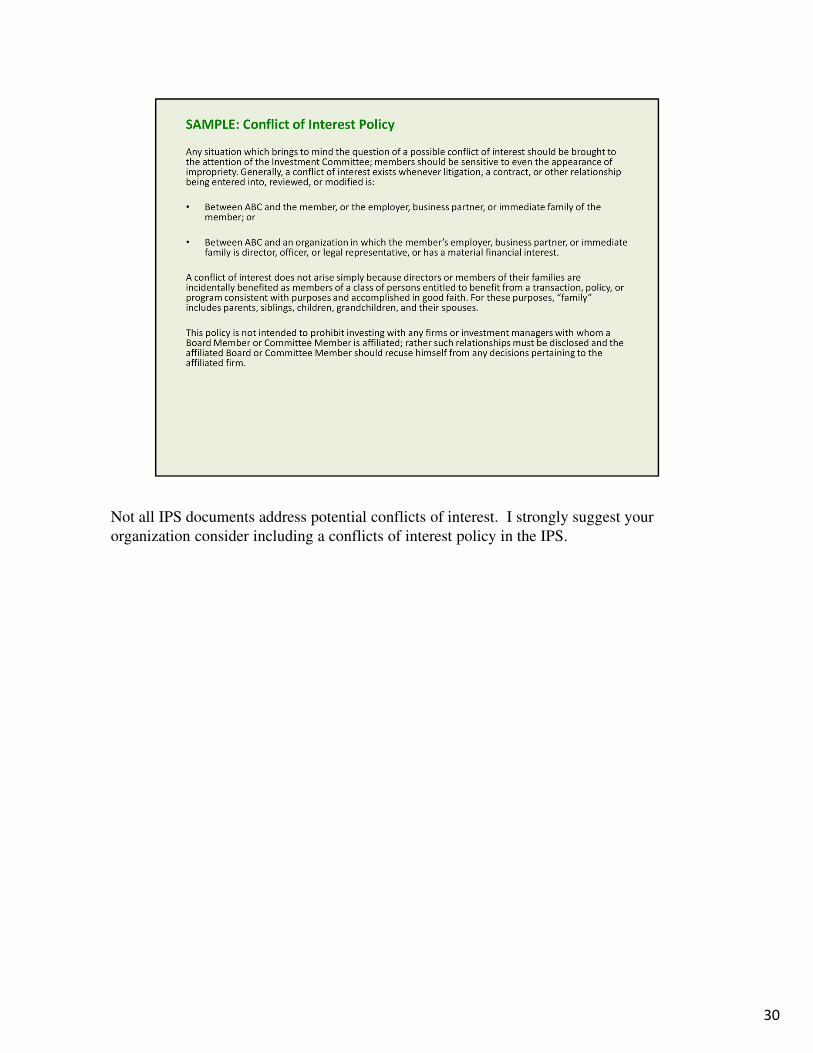

Not all IPS documents address potential conflicts of interest. I strongly suggest your

organization consider including a conflicts of interest policy in the IPS.

30

31

32

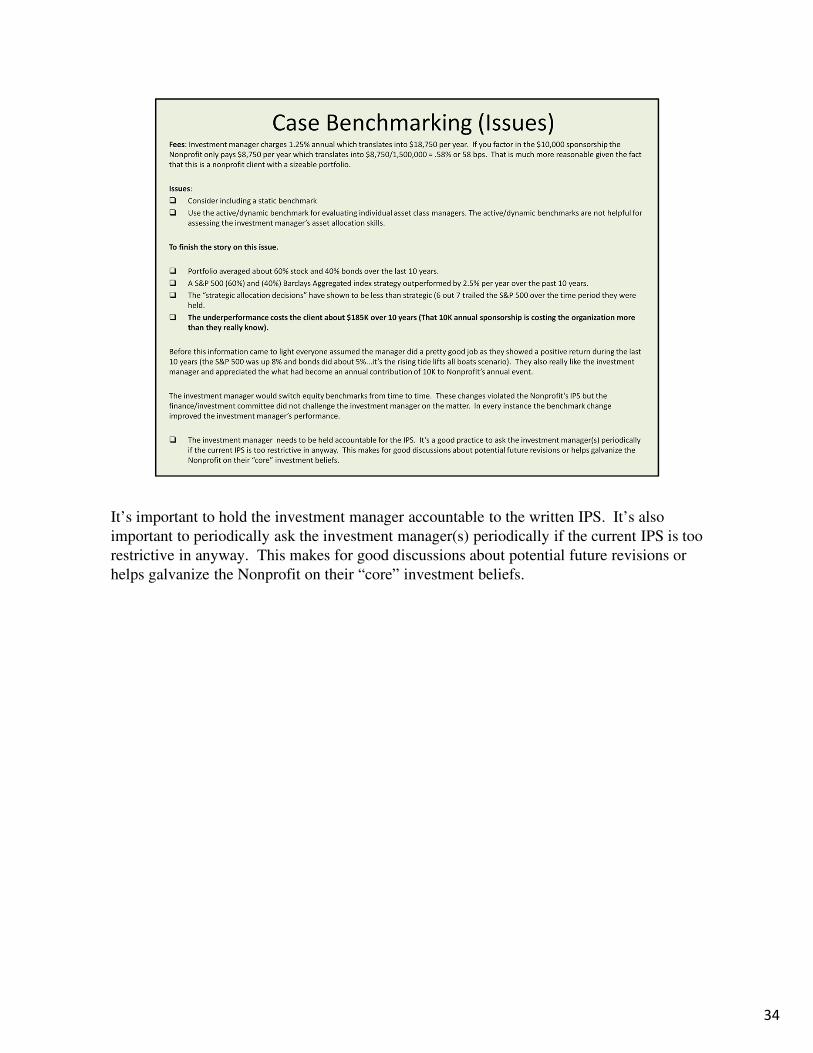

Investment manager charges 1.25% annual which translates into $18,750 per year. If you

factor in the $10,000 sponsorship the Nonprofit only pays $8,750 per year which translates

into $8,750/1,500,000 = .58% or 58 bps. That is much more reasonable given the fact that

this is a nonprofit client with a sizeable portfolio.

Issues:

The investment manager does not show a static benchmark (example 60% S&P 500 and

40% Barclays Bond Aggregate). The dynamic benchmarking does show how the

investment manager’s mutual fund/etf etc. has performed in the specific asset subclass

(examples: gold, commodities, international small cap stocks etc.) but fails to show whether

it was a prudent decision to allocate capital to that asset subclass in the first place. For

example, in this case the investment manager allocated aggressively to gold which

insignificantly underperformed over the last several years. So during the period of time the

investment manager held those assets they were benchmarked against a commodity index

which was appropriate, but once the asset subclass (gold) was sold it is difficult to see how

the past gold exposure impacted the overall performance. This investment manager has a

history of poor allocation decisions (they invested in gold at the top, energy near the top of

the cycle, treasury inflation protect bonds (TIPs) that have materially declined). Since they

don’t report against a static benchmark, once these asset subclasses are sold it’s hard for the

Nonprofit to see how poorly these decisions were. THE FIX: Dynamic benchmarking is

fine to review how the asset subclass managers are performing relative to their benchmarks,

but without a portfolio showing a static benchmark (Example 60% S&P 500, 10% MSCI

EAFE and 30% Barclays Bond Index) it’s difficult to determine how skilled the investment

33

manager is at asset allocation decisions. Incorporate both a static and dynamic benchmarking

if you have an active investment manager that is rotating in and out of asset subclasses

routinely.

To finish the story on this issue. I went back and determined the investment manager

averaged about 60% stock and 40% bonds over the last 10 years. I went back and determined

that a very simple portfolio of S&P 500 (60%) and (40%) Barclays Aggregated index

outperformed this manager by about 2.5% per year. It’s pretty clear that this manager had a

lousy 10 year track record of asset allocation decisions. The investment manager did just

have one or two significantly bad allocation decisions as they made what they called

“strategic allocation decisions” to 6 out 7 trailed the S&P 500 over the time period they held

them. The underperformance costs the client about $185K over 10 years (That 10K

annual sponsorship is costing the organization more than they really know).

Before this information came to light assumed the manager did a pretty good job as they

showed a positive return during the last 10 years (the S&P 500 was up 8% and bonds did

about 5%...it’s the rising tide lifts all boats scenario). They also really like the investment

manager and appreciated the what had become an annual contribution of 10K to Nonprofit’s

annual event.

Lastly, the investment manager would switch equity benchmarks from time to time. These

changes violated the Nonprofit’s IPS but the finance/investment committee did not challenge

the investment manager on the matter. In every instance the benchmark change improved the

investment manager’s performance. The FIX: hold the investment manager accountable for

the IPS. It’s a good practice to ask the investment manager(s) periodically if the current IPS

is too restrictive in anyway. This makes for good discussions about potential future revisions

or helps galvanize the Nonprofit on their “core” investment beliefs.

33

It’s important to hold the investment manager accountable to the written IPS. It’s also

important to periodically ask the investment manager(s) periodically if the current IPS is too

restrictive in anyway. This makes for good discussions about potential future revisions or

helps galvanize the Nonprofit on their “core” investment beliefs.

34