investment 1

DESCRIPTION

Investments accounting INVESTMENTS 2 3 For strategic reasons 2. To generate earnings from investment income. 1. Corporation may have excess cash. 3. For strategic reasons. Temporary investments and the operating cycleoperatingcycle Are readily convertible to cash. S HORT -T ERM I NVESTMENTS (M ARKETABLE S HORT T ERM I NVESTMENTS (M ARKETABLE S ECURITIES ) 4 Debt Securitiesreflect creditor Debt Securitiesreflect creditor relationship (notes, bonds, etc.) I NVESTMENTS . . . 5TRANSCRIPT

Investments

accounting

INVESTMENTS

Short term i t tinvestment

Long term Long term investment

2

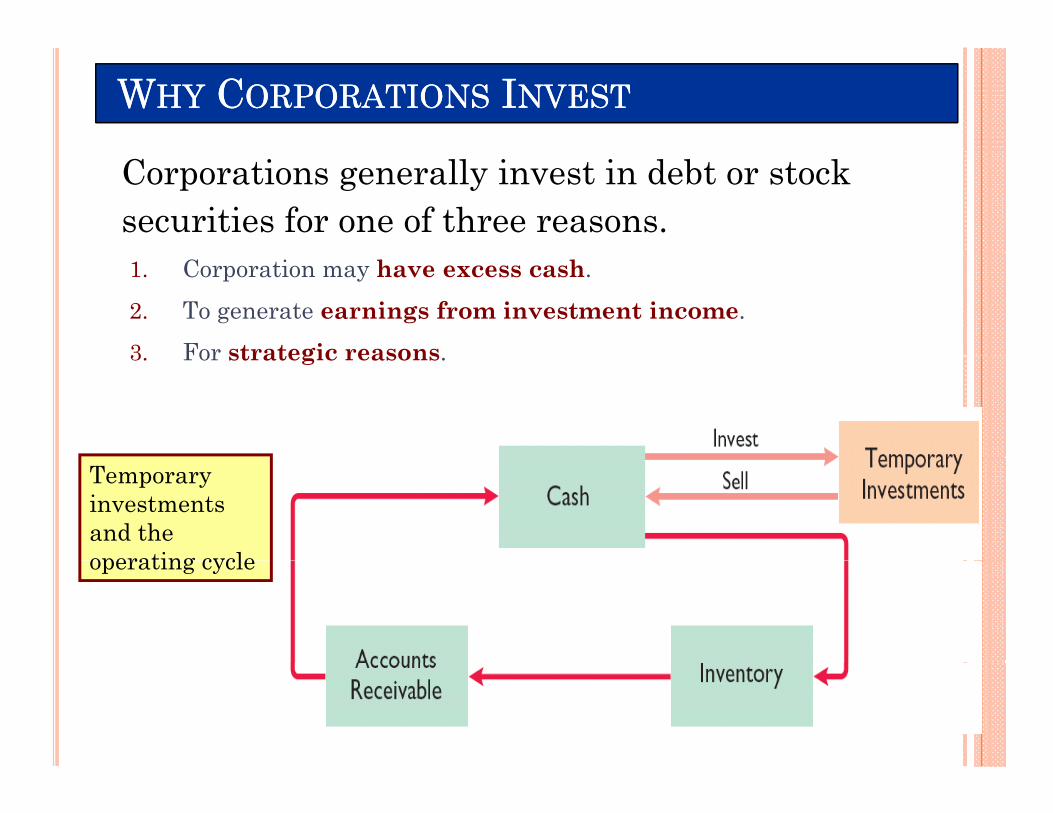

WWHYHY CCORPORATIONSORPORATIONS IINVESTNVEST

Corporations generally invest in debt or stock securities for one of three reasons.1. Corporation may have excess cash.2. To generate earnings from investment income.3 For strategic reasons3. For strategic reasons.

Temporary investments and the operating cycleoperating cycle

SHORT-TERM INVESTMENTS (MARKETABLESHORT TERM INVESTMENTS (MARKETABLESECURITIES)

Management intends to convert Management intends to convert to cash within one year or the

ti l hi h i operating cycle whichever is longer.

Are readily convertible to cash.

4

INVESTMENTS . . .

Debt Securities reflect creditor Debt Securities reflect creditor relationship (notes, bonds, etc.)

Equity Securities reflect owner relationship (stock)owner relationship (stock).

5

DEBT SECURITIES INVESTMENTS . . .

Held To Maturity SecuritiesHeld-To-Maturity Securities

Trading SecuritiesTrading Securities

Available For Sale SecuritiesAvailable-For-Sale Securities

6

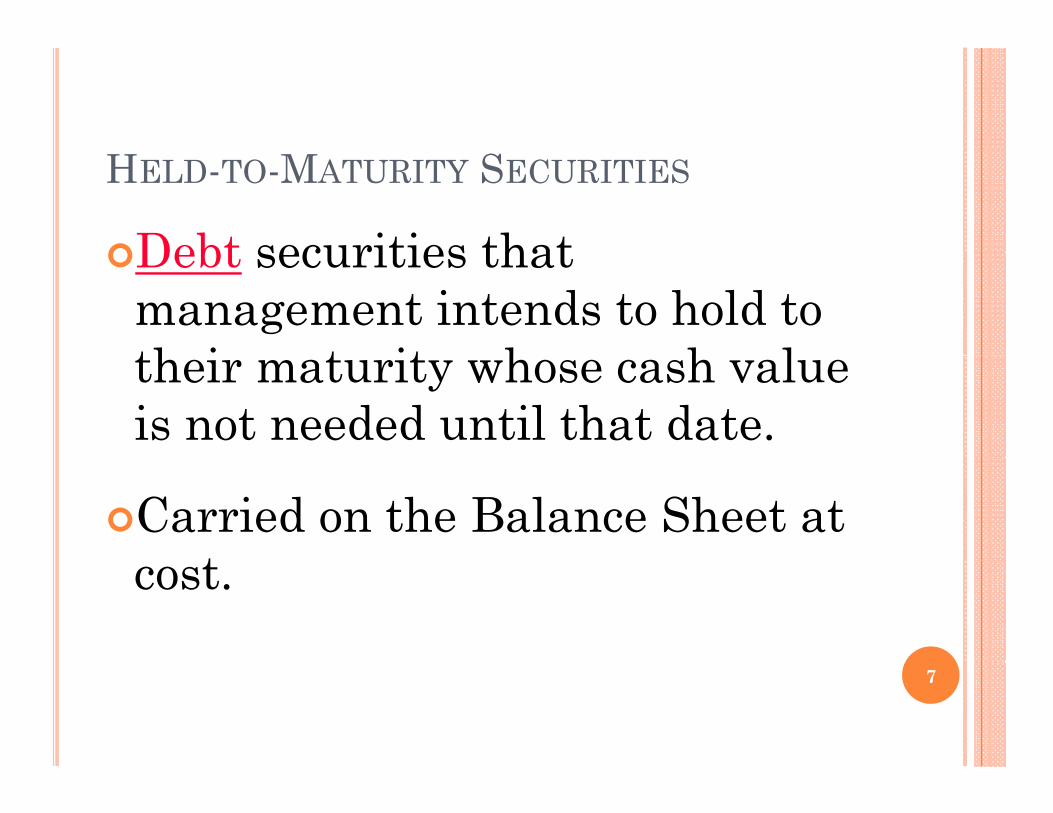

HELD-TO-MATURITY SECURITIES

Debt securities that Debt securities that management intends to hold to th i t it h h l their maturity whose cash value is not needed until that date.

Carried on the Balance Sheet at tcost.

7

TRADING SECURITIES

Debt securities that are bought and held principally for the and held principally for the purpose of being sold in the near termterm.

F e e tl bo ght a d old to Frequently bought and sold to generate profits on short-term h i h i ichanges in their prices. 8

TRADING SECURITIES

Entire portfolio of trading iti i t d t it securities is reported at its

market value with a “realizable value adjustment” from the cost of the portfolio.p

9

TRADING SECURITIES

Any unrealized gain (or loss)f h i th li bl from a change in the realizable value of the portfolio of trading securities during a period is reported on the income statement.p

10

AVAILABLE-FOR-SALE SECURITIES

Debt securities not classified as t di h ld t t it trading or held-to-maturity securities.

11

Accounting For Held g

to maturity debt

securities investmentsecurities investment

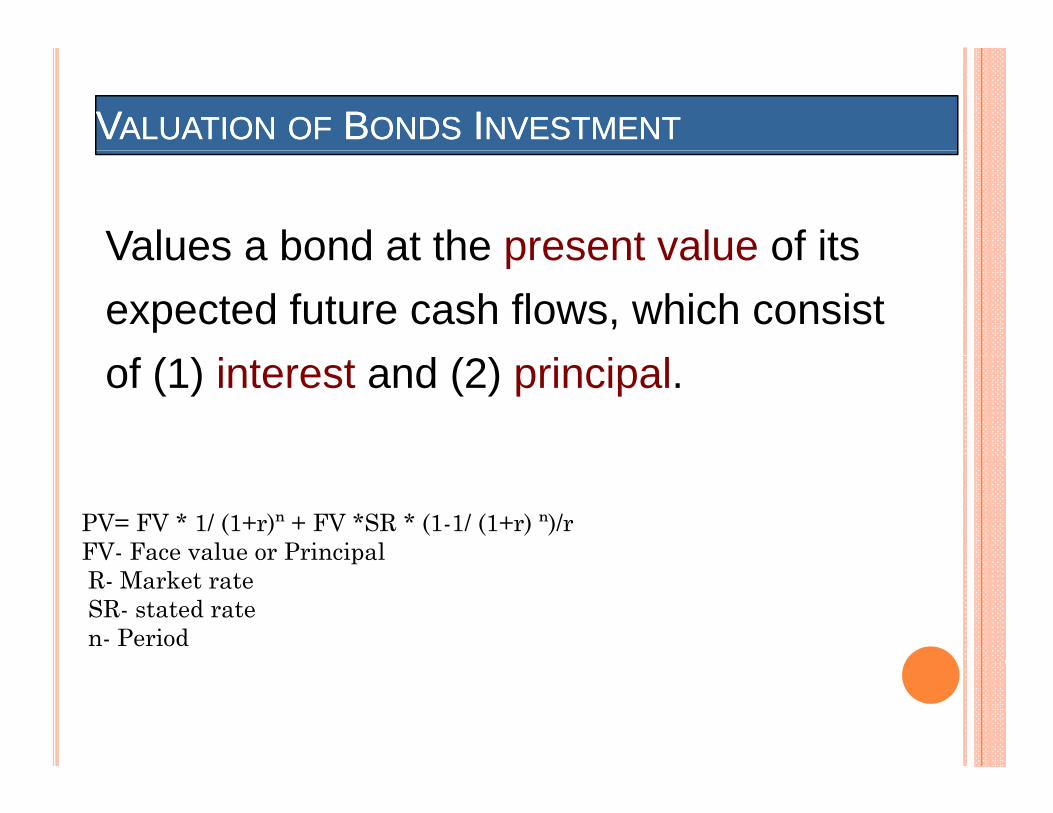

VVALUATIONALUATION OFOF BBONDSONDS IINVESTMENTNVESTMENT

Values a bond at the present value of itsValues a bond at the present value of its expected future cash flows, which consist of (1) interest and (2) principal.

PV= FV * 1/ (1+r)ⁿ + FV *SR * (1-1/ (1+r) ⁿ)/rFV- Face value or PrincipalpR- Market rateSR- stated raten- Period

INTEREST RATES AND BOND PRICES

Issued Market Rates Bonds Bought at:Issuedwhen:

8% Premium

Market Rates Bonds Bought at:

BOND

stated Face (Par)INTERESTRATE 10%

10% Face (Par)Value

12% Discount

BBONDSONDS IISSUEDSSUED ATAT AA FFACEACE VVALUEALUE

Journal entry on date of bought, Jan. 1, 2011.

Held to maturity securities 1000Held to maturity securities 1000

Cash 1000

Journal entry to record accrued interest revenue at Sep. 30, 2011.

Interest receivable (1000 x 10%) 25

Bond interest revenue 25

Journal entry to record first receipt of interest on Jan. 1, 2012.

Cash 50Cas 50

Interest receivable 50LO 3

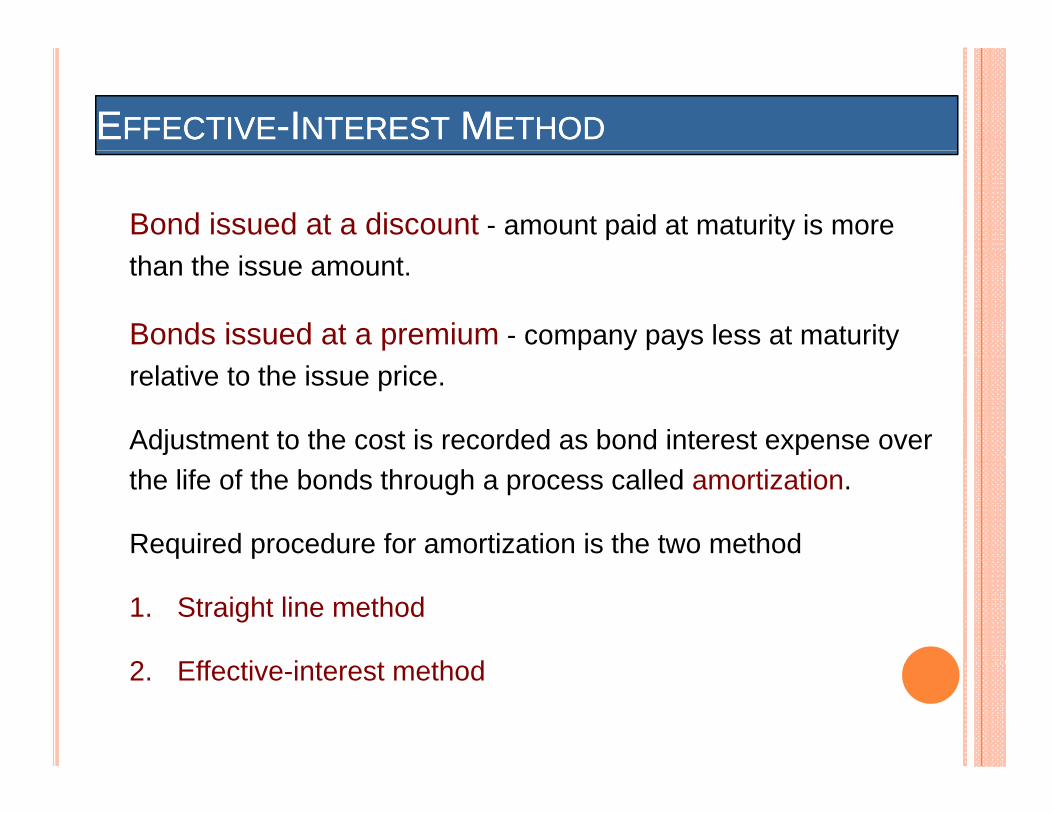

EEFFECTIVEFFECTIVE--IINTERESTNTEREST MMETHODETHOD

Bond issued at a discount - amount paid at maturity is more than the issue amount.

Bonds issued at a premium - company pays less at maturity relative to the issue price.

Adjustment to the cost is recorded as bond interest expense over the life of the bonds through a process called amortization.

Required procedure for amortization is the two method

1. Straight line method

2 Eff ti i t t th d2. Effective-interest method

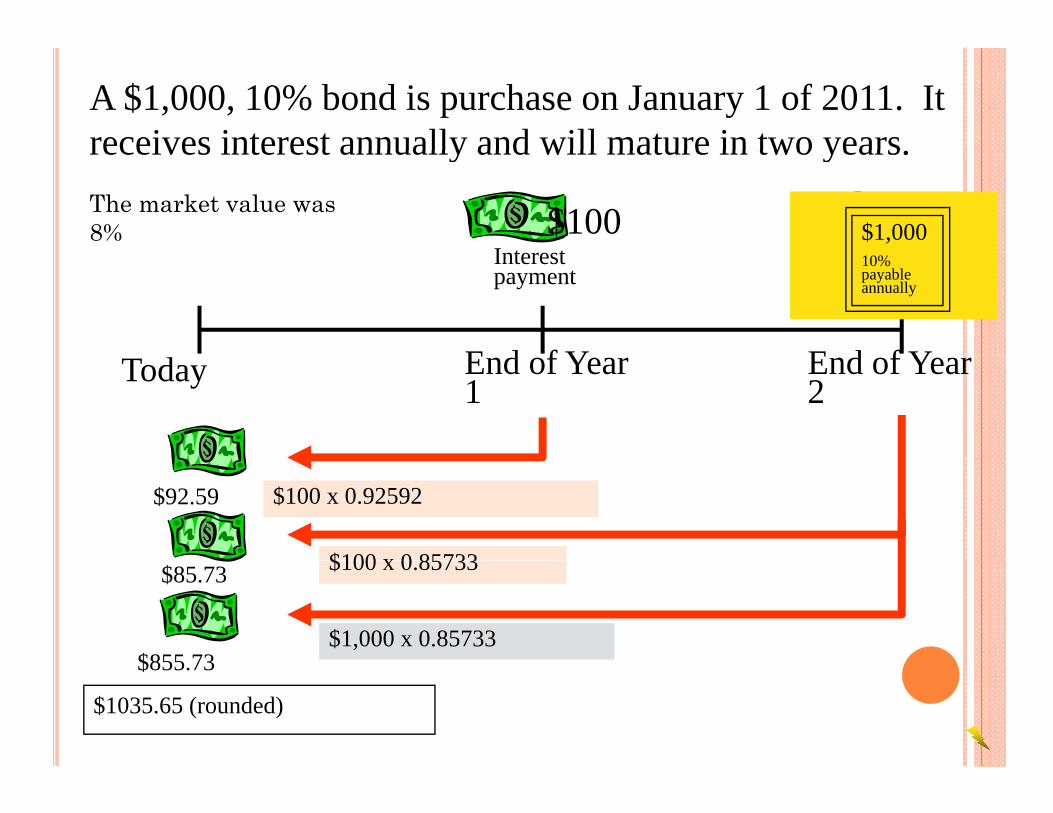

A $1,000, 10% bond is purchase on January 1 of 2011. It receives interest annually and will mature in two yearsreceives interest annually and will mature in two years.

Interest$100

Interest$100$1,000

The market value was 8%

E d f Y E d f Y

Interest payment

Interest payment

10% payable annually

Today End of Year 1

End of Year 2

$92.59 $100 x 0.92592

$100 x 0 85733$85.73 $100 x 0.85733

$1,000 x 0.85733$855 73$855.73

$1035.65 (rounded)

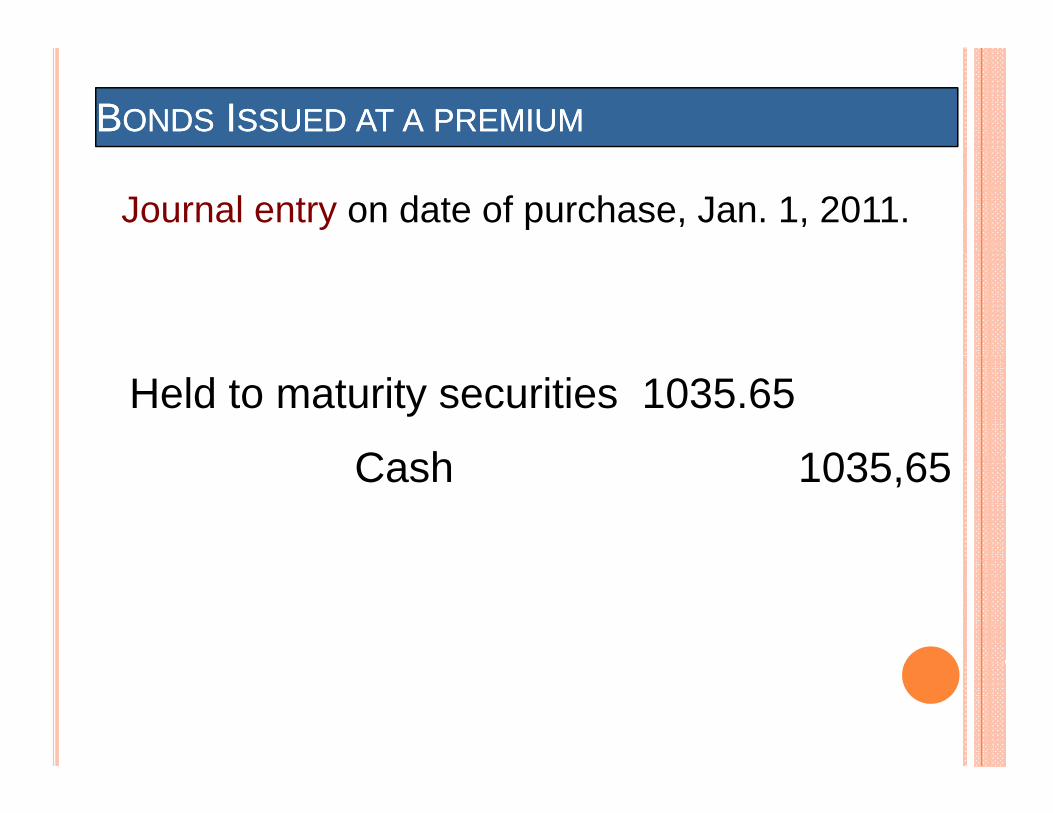

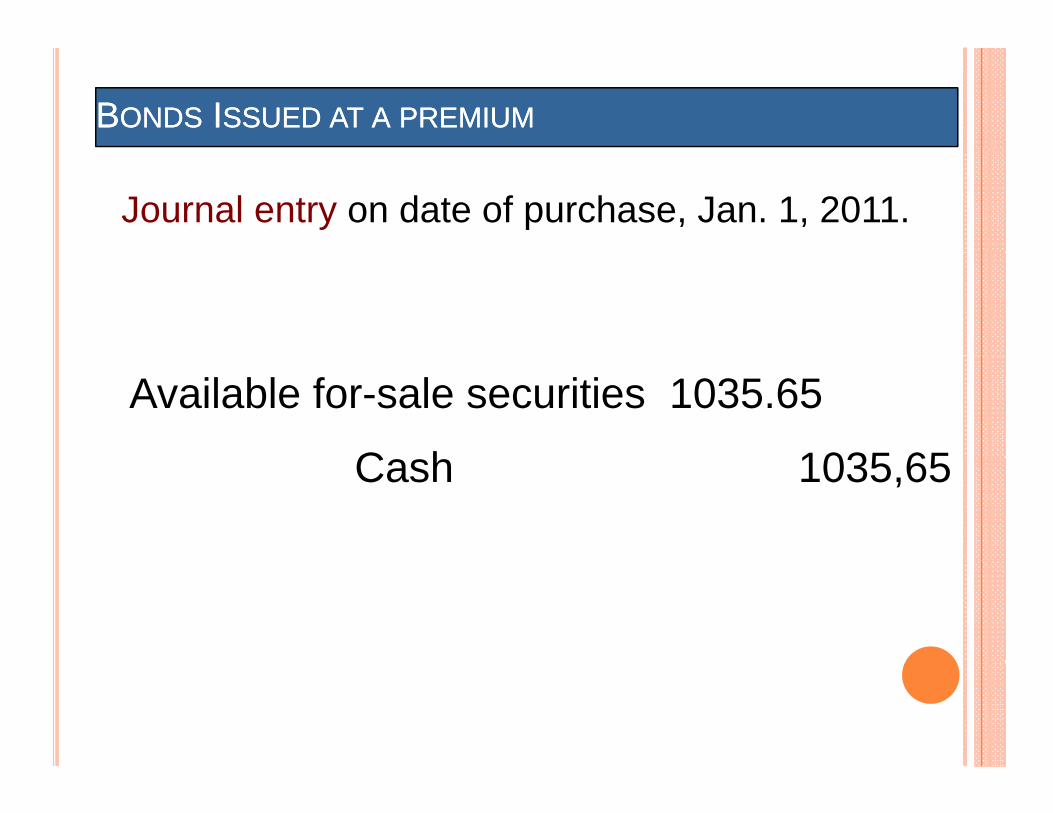

BBONDSONDS IISSUEDSSUED ATAT AA PREMIUMPREMIUM

Journal entry on date of purchase, Jan. 1, 2011.

Held to maturity securities 1035.65

C h 1035 65Cash 1035,65

SSTRAIGHTTRAIGHT LINELINE METHODMETHOD

Amortization amount= Bonds investment premium/ n=35 65/ 2=17 825/4= 4456 2535.65/ 2=17.825/4= 4456.25

Journal entry to record accrued interest at sep. 30, 2011.

Interest receivable 25

Held to maturity securities 4.456

Interest revenue 20.544

Journal entry to record first receipt of revenue on Jan. 1, 2012.

Cash 50Cas 50

Interest receivable 50

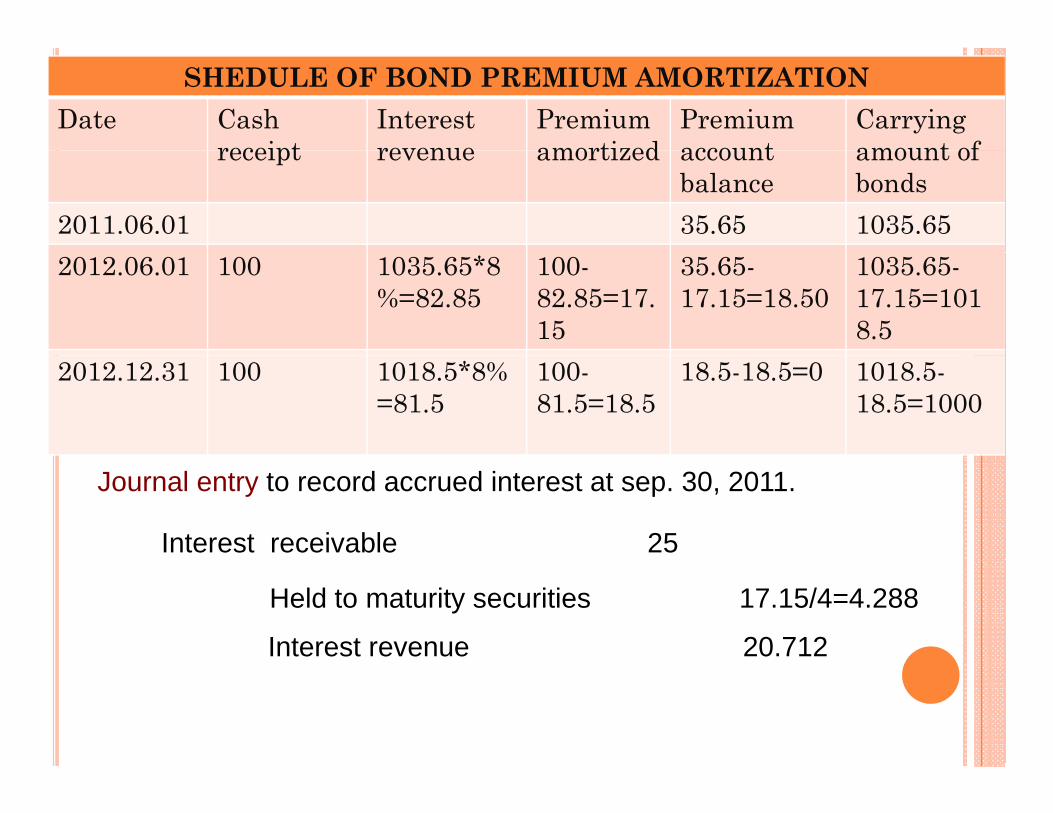

SHEDULE OF BOND PREMIUM AMORTIZATIONDate Cash

receiptInterest revenue

Premiumamortized

Premium account

Carrying amount of receipt revenue amortized account

balanceamount of bonds

2011.06.01 35.65 1035.652012.06.01 100 1035.65*8

%=82.85100-82.85=17.15

35.65-17.15=18.50

1035.65-17.15=1018.5

2012.12.31 100 1018.5*8%=81.5

100-81.5=18.5

18.5-18.5=0 1018.5-18.5=1000

Journal entry to record accrued interest at sep. 30, 2011.

Interest receivable 25

Held to maturity securities 17.15/4=4.288

Interest revenue 20.712

Accounting For g

Trading debt

securities investmentsecurities investment

Focus Co. purchases short-term investments in trading securities investments in trading securities on July 01, 2011. Interest payment each 3 monthpayment each 3 month.

Face value 12 000₮ 10% 100 units Face value 12,000₮, 10%- 100 units purchased for 1160,000₮. Paid brokers fee 20 000₮ brokers fee 20,000₮.

At December 31 2011 these At December 31, 2011, these securities had a market value of a 11 000₮ B 13000₮a.11,000₮ B. 13000₮

Trading Securities

Let’s record the purchase.

07/01 T din s iti s 1180 00007/01 Trading securities 1180,000Cash 1180,000

P h f T d Purchase of Trading Securities

Trading Securities

Let’s record the receipt of interest.

09/30 C sh 30 00009/30 Cash 30,000Interest revenue 30,000

R d f Record receipt of interest

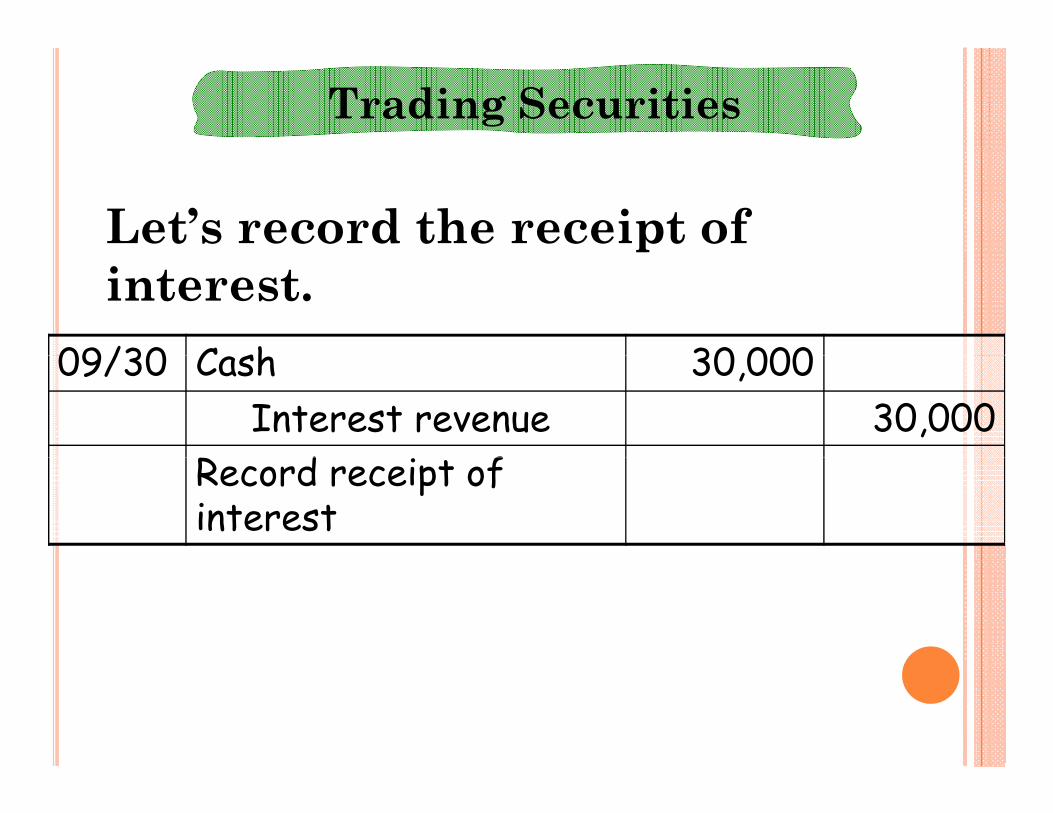

Trading Securities

Let’s record the receipt of interest.

12/31 C sh 30 00012/31 Cash 30,000Interest revenue 30,000

R d f Record receipt of interest

Trading Securities

1. Prepare the 12/31/11 year-end adjusting entry for the trading securities’ portfolio. (Year-end value = 11,000₮)

12/31 Unrealized loss 100,000l l l dRealizable value adj. 100,000

To record realizable value dj t tadjustment.

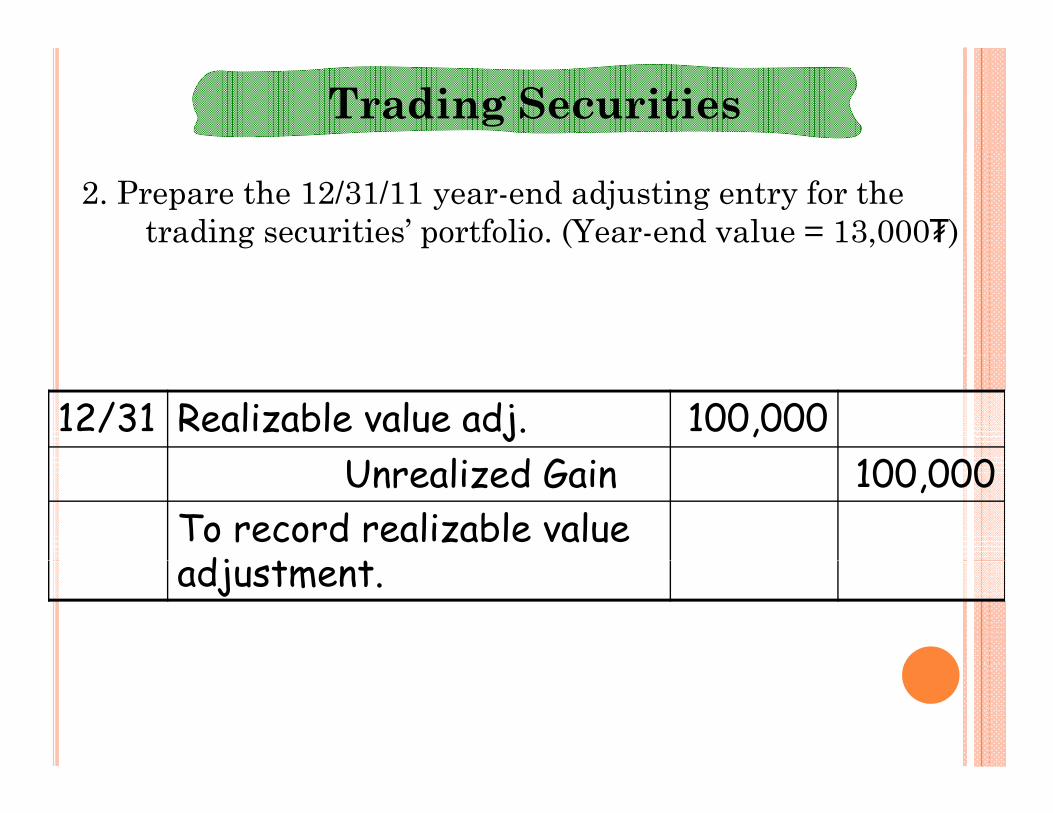

Trading Securities

2. Prepare the 12/31/11 year-end adjusting entry for the trading securities’ portfolio. (Year-end value = 13,000₮)

12/31 Realizable value adj. 100,000l d Unrealized Gain 100,000

To record realizable value dj t tadjustment.

Balance sheet Balance sheetBalance sheet.Current assets:Trading securities

Balance sheet.Current assets:Trading securities

1180,000Realizable value

Trading securities 1180,000

R li bl l adjustment (100,000) 1080,000Realizable value

Realizable value adjustment

100 0001280,000Realizable value

100,000

28

Trading Securities

Sold 40 units for 12500₮ to each securities on feb.01.2012.

02/01 Cash 500,000

d 4 2 000Trading securitiesRealized gain

472,00028,000

To record sell of trading securities.

Adjusting available-for-

sale debt securitiessale debt securities

to market.

A $1,000, 10% bond is purchase on January 1 of 2011. It receives interest annually and will mature in two yearsreceives interest annually and will mature in two years.

Interest$100

Interest$100$1,000

The market value was 8%

E d f Y E d f Y

Interest payment

Interest payment

10% payable annually

Today End of Year 1

End of Year 2

$92.59 $100 x 0.92592

$100 x 0 85733$85.73 $100 x 0.85733

$1,000 x 0.85733$855 73$855.73

$1035.65 (rounded)

BBONDSONDS IISSUEDSSUED ATAT AA PREMIUMPREMIUM

Journal entry on date of purchase, Jan. 1, 2011.

Available for-sale securities 1035.65

C h 1035 65Cash 1035,65

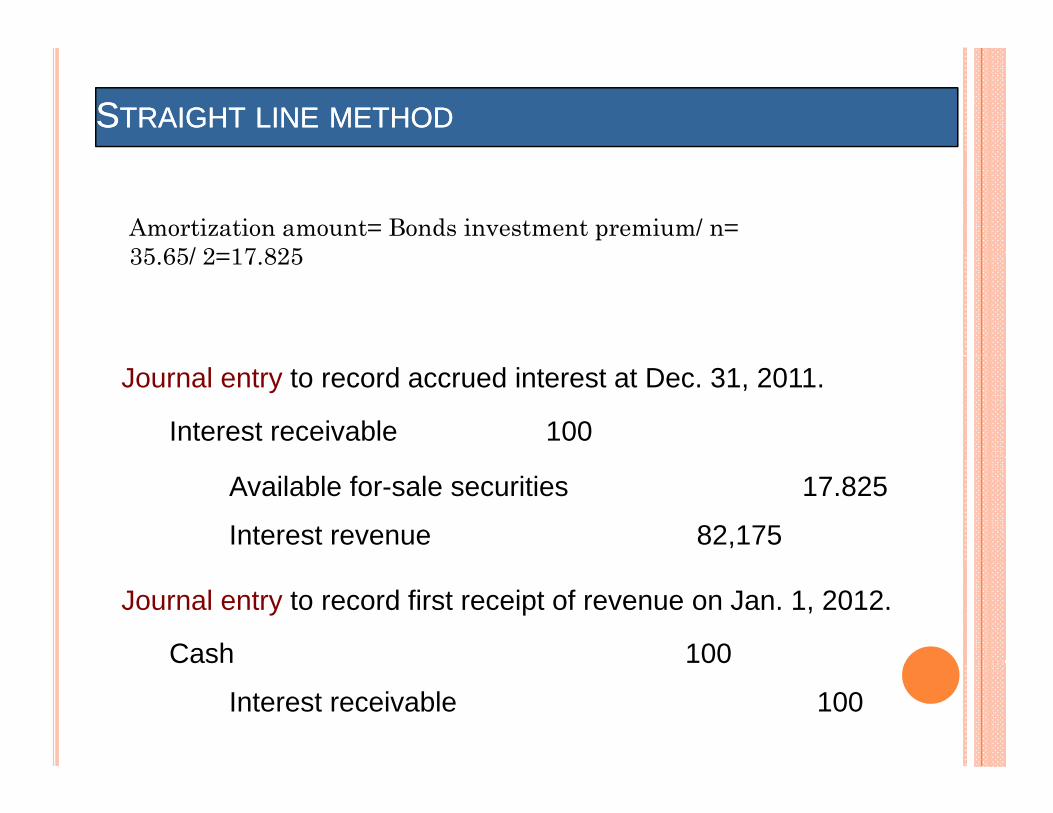

SSTRAIGHTTRAIGHT LINELINE METHODMETHOD

Amortization amount= Bonds investment premium/ n=35 65/ 2=17 82535.65/ 2=17.825

Journal entry to record accrued interest at Dec. 31, 2011.

Interest receivable 100

Available for-sale securities 17.825

Interest revenue 82,175

Journal entry to record first receipt of revenue on Jan. 1, 2012.

Cash 100Cas 00

Interest receivable 100

SHEDULE OF BOND PREMIUM AMORTIZATIONDate Cash

receiptInterest revenue

Premiumamortized

Premium account

Carrying amount of receipt revenue amortized account

balanceamount of bonds

2011.01.01 35.65 1035.652011.12.31 100 1035.65*8

%=82.85100-82.85=17.15

35.65-17.15=18.50

1035.65-17.15=1018.5

2012.12.31 100 1018.5*8%=81.5

100-81.5=18.5

18.5-18.5=0 1018.5-18.5=1000

Journal entry to record accrued interest at Dec. 31, 2011.

Interest receivable 100

Available for-sale securities 17.15

Interest revenue 82,85

Trading Securities

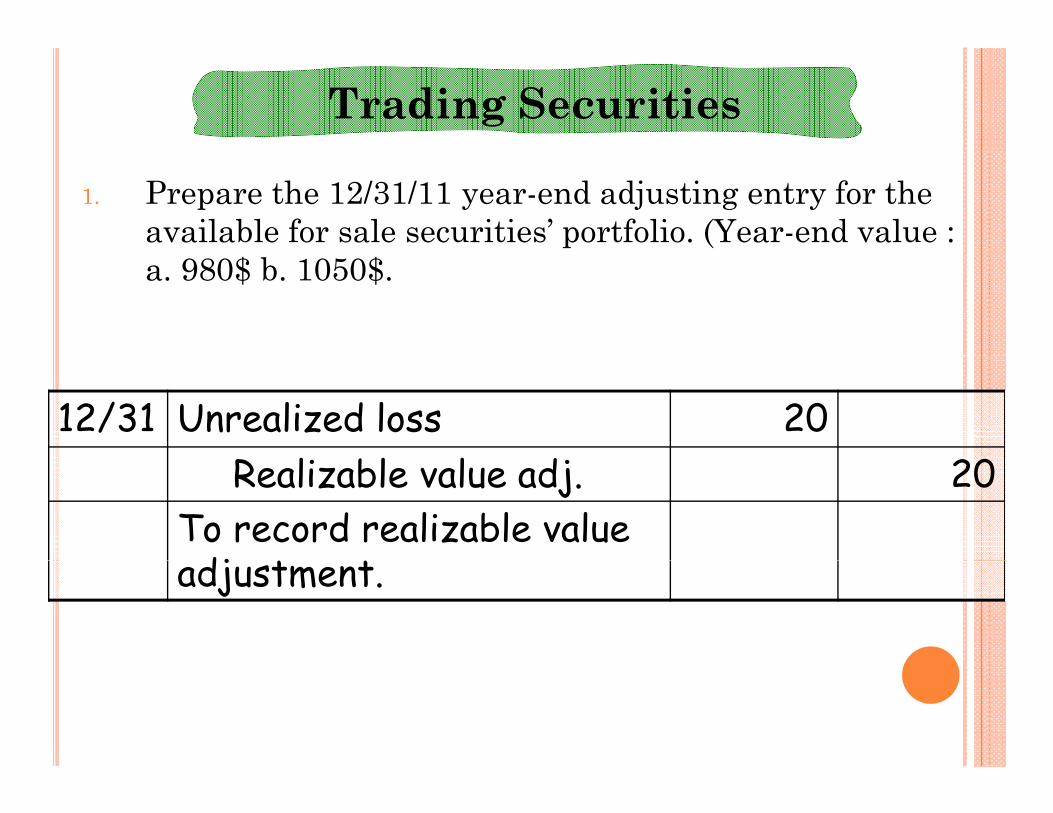

1. Prepare the 12/31/11 year-end adjusting entry for the available for sale securities’ portfolio. (Year-end value : a. 980$ b. 1050$.

12/31 Unrealized loss 20l l l dRealizable value adj. 20

To record realizable value dj t tadjustment.

Trading Securities

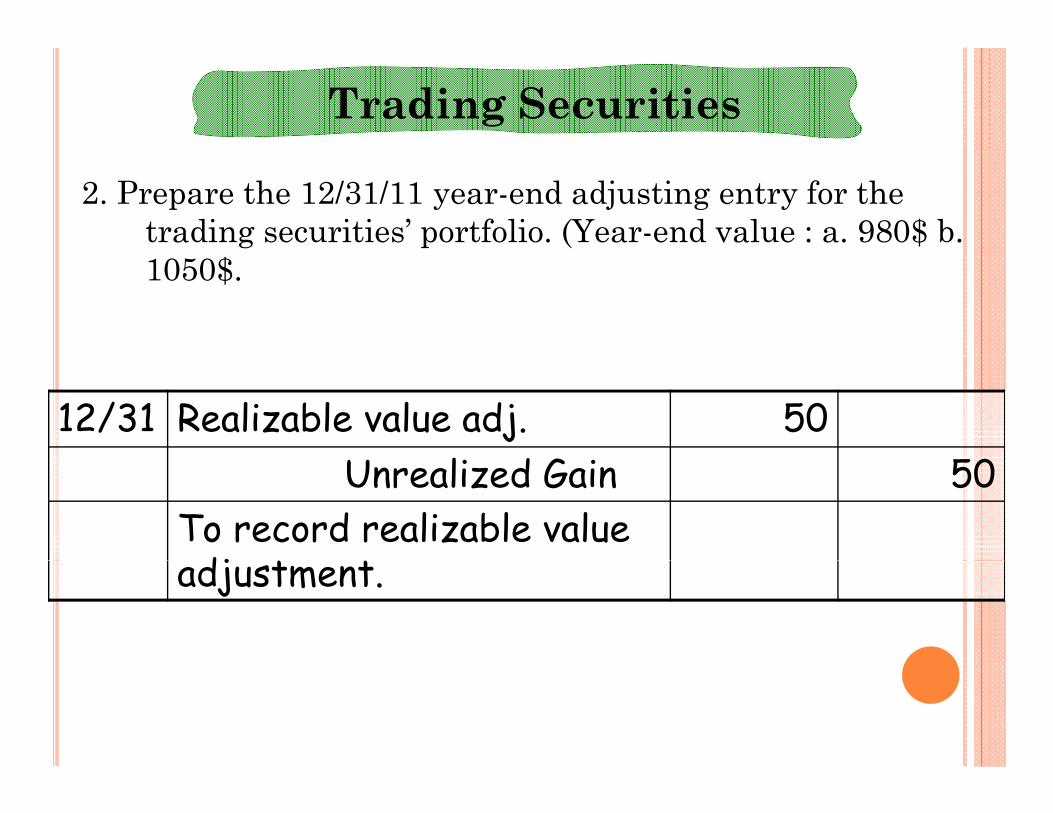

2. Prepare the 12/31/11 year-end adjusting entry for the trading securities’ portfolio. (Year-end value : a. 980$ b. 1050$.

12/31 Realizable value adj. 50l d Unrealized Gain 50

To record realizable value dj t tadjustment.

Exh. 7.17

DEBT SECURITIES INVESTMENT

Held To T di Available forHeld To Maturity Trading Available for

Sale

Debt securities notDebt securities held to maturity.

Debt securities actively traded.

Debt securities not in the other two

categories.

Cost. Realizable value.* Realizable value.**

*Unrealized gains/losses reported on the income statement.**Unrealized gains/losses reported in the equity section of the balance sheet.