invesco trust company annual report - merrill

TRANSCRIPT

Invesco Trust Company

Annual ReportYear Ended December 31, 2017

Invesco Stable Value Retirement Trust

(This page intentionally left blank)

Financial Statements

01 Schedule of Investments02 Statement of Assets and Liabilities03 Statement of Operations04 Statement of Changes in Net Assets06 Financial Highlights07 Notes to Financial Statements14 Independent Auditor’s Report

Supplemental Information16 Supplemental Schedule of Securities Purchased, Sold, or Matured

1 Invesco Stable Value Retirement Trust

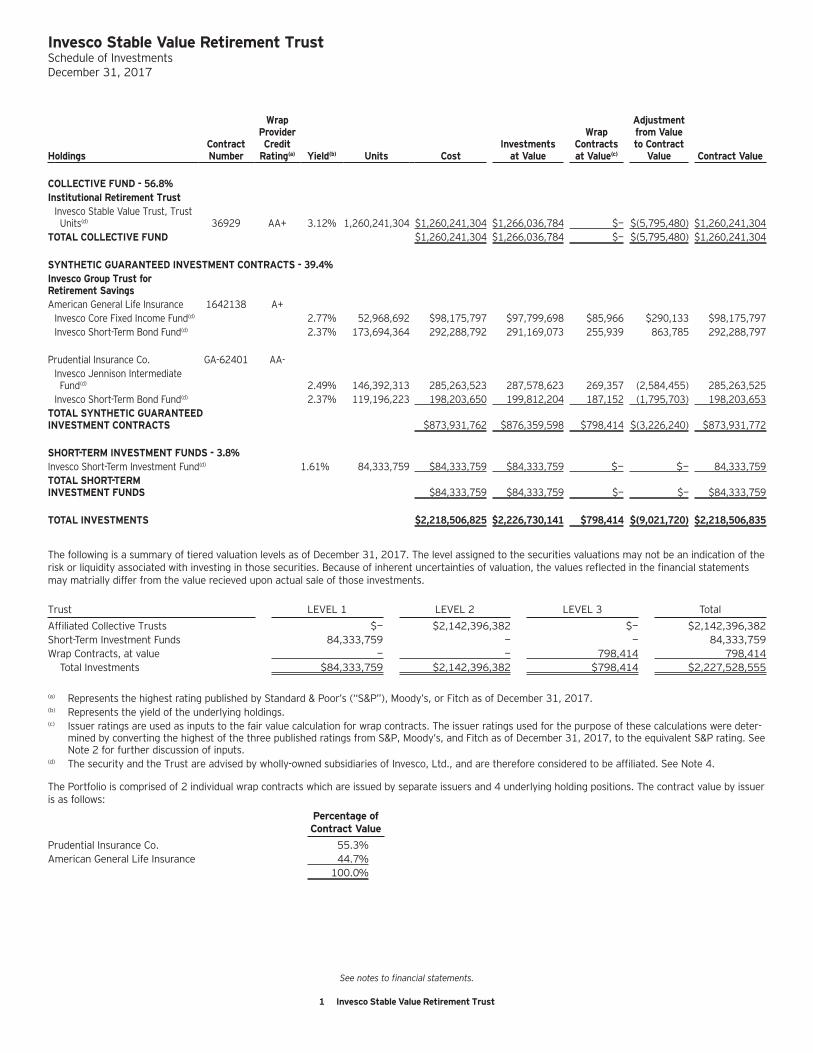

Invesco Stable Value Retirement TrustSchedule of InvestmentsDecember 31, 2017

See notes to financial statements.

HoldingsContract Number

Wrap Provider Credit

Rating(a) Yield(b) Units CostInvestments

at Value

Wrap Contractsat Value(c)

Adjustment from Value to Contract

Value Contract Value

COLLECTIVE FUND - 56.8%Institutional Retirement Trust

Invesco Stable Value Trust, Trust Units(d) 36929 AA+ 3.12%

1,260,241,304

$1,260,241,304

$1,266,036,784 $—

$(5,795,480)

$1,260,241,304

TOTAL COLLECTIVE FUND $1,260,241,304 $1,266,036,784 $— $(5,795,480) $1,260,241,304

SYNTHETIC GUARANTEED INVESTMENT CONTRACTS - 39.4%Invesco Group Trust for Retirement SavingsAmerican General Life Insurance 1642138 A+

Invesco Core Fixed Income Fund(d) 2.77% 52,968,692 $98,175,797 $97,799,698 $85,966 $290,133 $98,175,797 Invesco Short-Term Bond Fund(d) 2.37% 173,694,364 292,288,792 291,169,073 255,939 863,785 292,288,797

Prudential Insurance Co. GA-62401 AA-Invesco Jennison Intermediate Fund(d) 2.49% 146,392,313 285,263,523 287,578,623 269,357 (2,584,455) 285,263,525

Invesco Short-Term Bond Fund(d) 2.37% 119,196,223 198,203,650 199,812,204 187,152 (1,795,703) 198,203,653 TOTAL SYNTHETIC GUARANTEED INVESTMENT CONTRACTS $873,931,762 $876,359,598 $798,414

$(3,226,240) $873,931,772

SHORT-TERM INVESTMENT FUNDS - 3.8%Invesco Short-Term Investment Fund(d) 1.61% 84,333,759 $84,333,759 $84,333,759 $— $— 84,333,759 TOTAL SHORT-TERM INVESTMENT FUNDS $84,333,759 $84,333,759 $— $— $84,333,759

TOTAL INVESTMENTS $2,218,506,825 $2,226,730,141 $798,414 $(9,021,720) $2,218,506,835

The following is a summary of tiered valuation levels as of December 31, 2017. The level assigned to the securities valuations may not be an indication of the risk or liquidity associated with investing in those securities. Because of inherent uncertainties of valuation, the values reflected in the financial statements may matrially differ from the value recieved upon actual sale of those investments.

Trust LEVEL 1 LEVEL 2 LEVEL 3 Total

Affiliated Collective Trusts $— $2,142,396,382 $— $2,142,396,382 Short-Term Investment Funds 84,333,759 — — 84,333,759 Wrap Contracts, at value — — 798,414 798,414

Total Investments $84,333,759 $2,142,396,382 $798,414 $2,227,528,555

(a) Represents the highest rating published by Standard & Poor’s (“S&P”), Moody’s, or Fitch as of December 31, 2017.(b) Represents the yield of the underlying holdings.(c) Issuer ratings are used as inputs to the fair value calculation for wrap contracts. The issuer ratings used for the purpose of these calculations were deter-

mined by converting the highest of the three published ratings from S&P, Moody’s, and Fitch as of December 31, 2017, to the equivalent S&P rating. See Note 2 for further discussion of inputs.

(d) The security and the Trust are advised by wholly-owned subsidiaries of Invesco, Ltd., and are therefore considered to be affiliated. See Note 4.

The Portfolio is comprised of 2 individual wrap contracts which are issued by separate issuers and 4 underlying holding positions. The contract value by issuer is as follows:

Percentage of Contract Value

Prudential Insurance Co. 55.3%American General Life Insurance 44.7%

100.0%

2 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustStatement of Assets and LiabilitiesDecember 31, 2017

See notes to financial statements.

Assets:Investments:

Investments in affiliated securities, at value(1) $ 2,226,730,141Total investments, at value (Note 5) 2,226,730,141Wrap contracts, at value 798,414

Receivable for:Income from affiliated securities 2,479,197Total Assets 2,230,007,752

Liabilities:Payable for:

Management fees 457,832Accrued other operating expenses 85,580Total Liabilities 543,412

Net Assets (at value) $ 2,229,464,340Adjustment from Value to Contract Value (Note 5) (9,021,720)Net Assets (at contract value) (Note 5) $ 2,220,442,620Tier 1 Units:

Net Assets (at contract value) $ 881,074,222Units Outstanding (unlimited number of units authorized, no par value) 881,074,222Net Unit Value (at contract value) $ 1.00

Tier 2 Units:Net Assets (at contract value) $ 280,294,683Units Outstanding (unlimited number of units authorized, no par value) 280,294,683Net Unit Value (at contract value) $ 1.00

Tier 3 Units:Net Assets (at contract value) $ 416,347,480Units Outstanding (unlimited number of units authorized, no par value) 416,347,480Net Unit Value (at contract value) $ 1.00

Tier 4 Units:Net Assets (at contract value) $ 396,543,874Units Outstanding (unlimited number of units authorized, no par value) 396,543,874Net Unit Value (at contract value) $ 1.00

Tier 5 Units:Net Assets (at contract value) $ 246,182,361Units Outstanding (unlimited number of units authorized, no par value) 246,182,361Net Unit Value (at contract value) $ 1.00

(1) Investments in affiliated securities, at cost $ 2,218,506,825

3 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustStatement of OperationsFor the Year Ended December 31, 2017

See notes to financial statements.

Investment Income:Credit rate income on wrap contracts $ 18,599,370Income from affiliated securities 27,641,781

Total investment income 46,241,151Wrap fees (1,892,502)

Investment income after wrap fees 44,348,649Expenses:Management fees – Tier 1 Units 776,583Management fees – Tier 2 Units 422,483Management fees – Tier 3 Units 1,198,739Management fees – Tier 4 Units 1,656,588Management fees – Tier 5 Units 1,561,525Accounting fees 75,668Custodian fees 2,502Transfer agent fees 37,620Trustee fees 442,392Professional fees 29,645

Total expenses 6,203,745Net investment income $ 38,144,904

4 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustStatement of Changes in Net AssetsFor the Year Ended December 31, 2017

See notes to financial statements.

Operations:Net investment income $ 38,144,904

Distributions to Tier 1 Unitholders:From net investment income (14,642,028)

Distributions to Tier 2 Unitholders:From net investment income (5,158,722)

Distributions to Tier 3 Unitholders:From net investment income (8,233,622)

Distributions to Tier 4 Unitholders:From net investment income (6,531,963)

Distributions to Tier 5 Unitholders:From net investment income (3,578,569)

Net increase (decrease) in net assets from distributions to unitholders (38,144,904)Capital Transactions to Tier 1 Unitholders

Proceeds from units issued 487,145,498 Distributions reinvested 14,642,028 Cost of units redeemed (377,899,180)

Net increase in net assets from Tier 1 Units 123,888,346 Capital Transactions to Tier 2 Unitholders

Proceeds from units issued 98,256,675 Distributions reinvested 5,158,722 Cost of units redeemed (88,801,528)

Net increase in net assets from Tier 2 Units 14,613,869 Capital Transactions to Tier 3 Unitholders

Proceeds from units issued 187,987,146 Distributions reinvested 8,233,622 Cost of units redeemed (323,638,281)

Net increase (decrease) in net assets from Tier 3 Units (127,417,513)Capital Transactions to Tier 4 Unitholders

Proceeds from units issued 136,173,380 Distributions reinvested 6,531,963 Cost of units redeemed (176,484,834)

Net increase (decrease) in net assets from Tier 4 Units (33,779,491)Capital Transactions to Tier 5 Unitholders

Proceeds from units issued 79,203,588 Distributions reinvested 3,578,569 Cost of units redeemed (109,152,380)

Net increase (decrease) in net assets from Tier 5 Units (26,370,223)Net increase (decrease) in net assets resulting from capital transactions (49,065,012)Net increase (decrease) in net assets (49,065,012)Net Assets, Beginning of year $ 2,269,507,632 Net Assets, End of year $ 2,220,442,620

5 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustStatement of Changes in Net AssetsFor the Year Ended December 31, 2017

See notes to financial statements.

Unit Transactions to Tier 1 UnitholdersIssued 487,145,498 Reinvested 14,642,028 Redeemed (377,899,180)

Net increase in Tier 1 Units 123,888,346 Unit Transactions to Tier 2 Unitholders

Issued 98,256,675 Reinvested 5,158,722 Redeemed (88,801,528)

Net increase in Tier 2 Units 14,613,869 Unit Transactions to Tier 3 Unitholders

Issued 187,987,146 Reinvested 8,233,622 Redeemed (323,638,281)

Net increase (decrease) in Tier 3 Units (127,417,513)Unit Transactions to Tier 4 Unitholders

Issued 136,173,380 Reinvested 6,531,963 Redeemed (176,484,834)

Net increase (decrease) in Tier 4 Units (33,779,491)Unit Transactions to Tier 5 Unitholders

Issued 79,203,588 Reinvested 3,578,569 Redeemed (109,152,380)

Net increase (decrease) in Tier 5 Units (26,370,223)Total increase (decrease) in Units (49,065,012)

6 Invesco Stable Value Retirement Trust

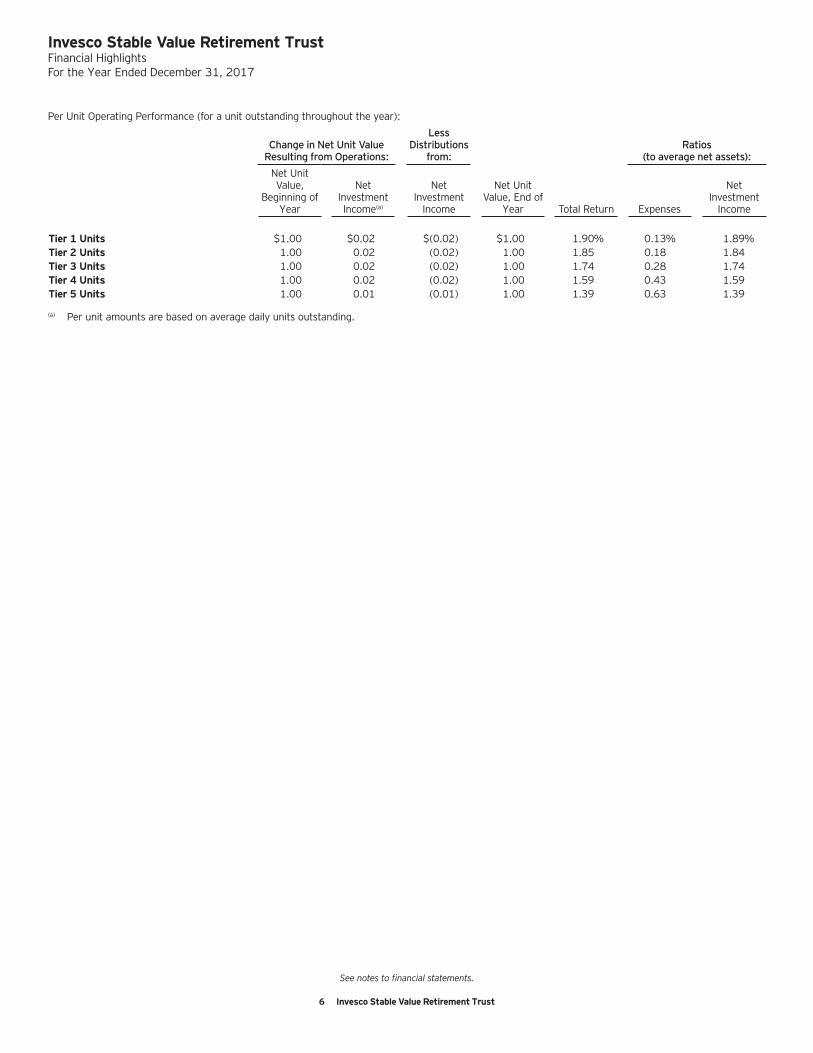

Invesco Stable Value Retirement TrustFinancial HighlightsFor the Year Ended December 31, 2017

See notes to financial statements.

Per Unit Operating Performance (for a unit outstanding throughout the year):

Change in Net Unit ValueResulting from Operations:

LessDistributions

from:Ratios

(to average net assets):

Net Unit Value,

Beginning of Year

Net Investment Income(a)

Net Investment

Income

Net Unit Value, End of

Year Total Return Expenses

Net Investment

Income

Tier 1 Units $1.00 $0.02 $(0.02) $1.00 1.90% 0.13% 1.89%Tier 2 Units 1.00 0.02 (0.02) 1.00 1.85 0.18 1.84Tier 3 Units 1.00 0.02 (0.02) 1.00 1.74 0.28 1.74Tier 4 Units 1.00 0.02 (0.02) 1.00 1.59 0.43 1.59Tier 5 Units 1.00 0.01 (0.01) 1.00 1.39 0.63 1.39

(a) Per unit amounts are based on average daily units outstanding.

7 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

NOTE 1 - ORGANIZATION AND DESCRIPTION OF THE TRUST

Invesco Stable Value Retirement Trust (the “Trust”) is a Collective Trust of Invesco Trust Company (the “Company” or the “Trustee”), a Texas state trust company. The Trust was established for the purposes of the investment and reinvestment of funds contributed by the Company in its capacity as a fiduciary for pension and profit sharing trusts. The Trust is authorized by the Amended and Restated Declaration of Trust (“Trust Agreement”) dated as of April 1, 2017. Citi Fund Services Ohio, Inc. is the service provider to the Trust, providing fund accounting and financial reporting services. State Street Bank and Trust Company provides custodial services. The Trust is an investment company and follows the accounting and reporting guidance in the Financial Accounting Standards Board (“FASB”) accounting standards codification 946, Financial Services - Investment Companies. The Trust’s primary investment objectives are to seek preservation of principal and provide interest income reasonably obtained under prevailing market conditions and rates, consistent with seeking to maintain required liquidity. The Trust offers five classes of Units. The investment objectives of the Trust are identical among each class of Units. The classes, Tier 1, Tier 2, Tier 3, Tier 4 and Tier 5 units each declare income dividends daily and thereby maintain a net asset value of $1.00 per unit. NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Trust in preparation of its financial statements. In accordance with Accounting Standards Codification (“ASC”) 946-210-45 through 946-210-55, Reporting of Fully Benefit-Responsive Investment Contracts, investments held by the Trust are required to be reported at fair value, which is generally determined as the amount that could reasonably be expected to realize from an orderly disposition of securities and other financial instruments over a reasonable period of time. However, contract value is the relevant measurement attribute for that portion of the net assets of the Trust attributable to fully benefit responsive investment contracts because contract value is the amount unitholders would receive if they were to initiate permitted transactions under the terms of the underlying defined contribution plans. The accompanying Schedule of Investments reflects both the fair value as well as the adjustment to contract value for each investment contract deemed fully benefit-responsive. The Statement of Assets and Liabilities presents the fair value of the investment contracts as well as the adjustment of the fully benefit-responsive investment contracts from fair value to contract value. The Statement of Operations and Statement of Changes in Net Assets are prepared on a contract value basis. A. Security Valuation Securities are valued according to the following policy. The Trust may invest in bank, insurance company and other financial institution investment contracts (“GICs”). The Trust holds synthetic guaranteed investment contracts (“synthetic GICs”). Synthetic GICs are portfolios of securities (debt securities or units of collective trusts) owned by the Trust with wrap contracts associated with the portfolios. The Trust’s investment contracts are carried at contract value which is equal to principal balance plus accrued interest plus deposits and less withdrawals. An investment contract is generally permitted to be valued at contract value, rather than fair value, to the extent it is fully benefit-responsive and held by a trust offered only to qualified employer-sponsored defined-contribution plans. Investment contracts that do not meet the criteria for valuation at contract value will be valued at fair value as determined by the Trustee, and such value may be more or less than contract value. Investment contracts have elements of risk due to lack of a secondary market and resale restrictions resulting in the inability of the Trust to sell a contract. In addition, investment contracts may be subject to credit risk based on the ability of the wrapper providers to meet their obligations under the terms of the contract (see Note 5). The Trust may also invest in traditional guaranteed investment contracts (“traditional GICs”). Traditional GICs are backed by the general account of the issuer. The Trust deposits a lump sum with the issuer and receives a guaranteed interest rate for a specified time. Interest is accrued on either a simple interest or fully compounded basis and is paid either periodically or at the end of the contract term. The issuer guarantees that all qualified participant withdrawals, as defined, will occur at contract value (principal plus accrued interest). Traditional GICs generally do not permit issuers to terminate the agreement prior to the scheduled maturity date. The fair value of traditional GICs is determined using an income approach where the individual contract cash flows are discounted at the prevailing interpolated swap rate as of year-end. Short-term securities are stated at amortized cost (which approximates market value) if maturity is 60 days or less at the time of purchase, or at market value if maturity is greater than 60 days. Investments in open-end and closed-end registered investment companies and collective trust funds that do not trade on an exchange are valued at the end of day net asset value per share. Investments in open-end and closed-end registered investment companies that trade on an exchange are valued at the last sales price or official closing price as of the close of the customary trading session on the exchange where the security is principally traded.

8 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

Debt obligations (including convertible securities) and unlisted equities are fair valued using an evaluated quote provided by an independent pricing service. Evaluated quotes provided by the pricing service may be determined without exclusive reliance on quoted prices, and may reflect appropriate factors such as institution-size trading in similar groups of securities, developments related to specific securities, dividend rate (for unlisted equities), yield (for debt obligations), quality, type of issue, coupon rate (for debt obligations), maturity (for debt obligations), individual trading characteristics and other market data. Pricing services generally value debt obligations assuming orderly transactions of institutional round lot size, but a trust may hold or transact in the same securities in small, odd lot sizes. Odd lots often trade at lower prices than institutional round lots. Debt obligations are subject to interest rate and credit risks. In addition, all debt obligations involve some risk of default with respect to interest and/or principal payments. The fair value of the separate account insurance contracts is based on the net asset value of an insurance company separate account on which the crediting rate is based. The underlying fixed income securities of the separate accounts are valued on the basis of valuation furnished by approved independent pricing services. These services determine valuations for normal institutional-size trading units of such securities using model or matrix pricing. Securities for which market prices are not provided by any of the above methods may be valued based upon quotes furnished by independent sources. The last bid price may be used to value equity securities. The mean between the last bid and asked prices is used to value debt obligations, including corporate loans. Securities for which market quotations are not readily available or became unreliable are valued at fair value as determined in good faith by or under the supervision of the Trust’s officers following procedures approved by the Board of Trustees. Issuer specific events, market trends, bid/ask quotes of brokers and information providers and other market data may be reviewed in the course of making a good faith determination of a security’s fair value. The Trust may invest in securities that are subject to interest rate risk, meaning the risk that the prices will generally fall as interest rates rise and, conversely, the prices will generally rise as interest rates fall. Specific securities differ in their sensitivity to changes in interest rates depending on their individual characteristics. Changes in interest rates may result in increased market volatility, which may affect the value and/or liquidity of certain of the Trust’s investments. Valuations change in response to many factors including the historical and prospective earnings of the issuer, the value of the issuer’s assets, general economic conditions, interest rates, investor perceptions and market liquidity. Because of the inherent uncertainties of valuation, the values reflected in the financial statements may materially differ from the value received upon actual sale of those investments. B. Investment Transactions and Investment Income Investment transactions are accounted for on a trade date basis. Realized gains or losses on sales are computed on the basis of specific identification on the securities sold. Interest income (net of withholding tax, if any) is recorded on the accrual basis from settlement. Bond premiums and discounts are amortized and/or accreted over the lives of the respective securities. Distributions from ordinary income from underlying funds, if any, are recorded as dividend income on ex-dividend date. Distributions from gains from underlying funds, if any, are recorded as realized gains on ex-dividend date. Income from investment contracts is recorded at the contract rate, which in the case of synthetic investment contracts is referred to as the crediting rate. Crediting rates on synthetic contracts are net of fees to the issuer of the wrap contract and custody fees on underlying assets. For fully benefit-responsive synthetic investment contracts, earnings on the underlying assets are factored in the next computation of the crediting rate re-set. The Trust may periodically participate in litigation related to the Trust’s investments. As such, the Trust may receive proceeds from litigation settlements. Any proceeds received are included in the Statement of Operations as realized gain (loss) for investments no longer held and as unrealized gain (loss) for investments still held. The Trusts allocates investment income, to a unit class, if applicable, based on the relative net assets of each unit class. C. Distributions Distributions of net investment income are declared daily and paid monthly. Such distributions are reinvested in the month-end net unit value. D. Income Taxes No provision for federal income taxes has been recorded since the Trust is exempt under Section 501(a) of the Internal Revenue Code. The Trust recognizes the tax benefits of uncertain tax positions only when the position is more likely than not to be sustained. Management has analyzed the Trust’s uncertain tax positions and concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions. Management is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months.

9 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

The Trust has analyzed its uncertain tax positions for all open tax years (generally the last three years) and has concluded that no provision for income taxes is required in its financial statements. E. Unit Classes and Expenses The Trust has multiple unit classes which have identical investment holdings and share expenses and investment income on a relative daily net asset basis. Accounting, Professional, Custodian and Transfer Agent Fees Expenses chargeable to the Trust include those relating to, without limitation, sub-advisory fees and expenses of vehicles in which the Trust invests, trustee fees and expenses of vehicles in which the Trust invests, portfolio accounting and performance monitoring, legal services, transfer agency, custody, stable value wrap contract or similar fees, annual report preparation and distribution, overdraft charges and compensation paid to agents for monitoring and evaluation of the quality of service provided and the reasonableness of fees charged by other independent outside service providers engaged on behalf of the Trust. Expenses shall be charged to the class of units in such equitable proportion as may be determined by the Trustee. Extraordinary transaction costs attributable to a participating trust’s contribution to or redemption from the Trust may be charged to such participating trust in accordance with applicable law. All taxes that may be levied upon or in respect of the Trust or liquidating account under existing or future laws shall be charged to the Trust or liquidating account with respect to which such taxes were levied or assessed. Wrap Fees Wrap fees associated with synthetic GICs are charged to the Trust by the applicable bank or insurance company at an annual rate of 0.22% to 0.23% of the respective contract value. The wrap fees are proportionately allocated across the unit classes based on relative net assets. Management Fees Management fees are charged by the Company based on the average daily net assets of that Tier. The following is a summary of the investment management fees for the year ended December 31, 2017:

Management FeeTier Annual RateTier 1 0.10%Tier 2 0.15%Tier 3 0.25%Tier 4 0.40%Tier 5 0.60% The Trust pays a trustee fee to the Company at an annual rate of 0.02% of average daily net assets. F. Unit Transactions Issuances and redemptions of participant units are made on each business day (“Valuation Date”). As permitted under the Trust Agreement, participant units are issued and redeemed based upon the net asset value per unit of the Trust at contract value, determined in accordance with the terms of the Trust Agreement, as of the Trust’s Valuation Date last preceding the date on which such orders to issue or redeem units are received. A participating trust is required to give the Trustee 24 months’ irrevocable written notice of intent to redeem all or a portion of its participation in the Trust. A participating trust may redeem units at any time upon 10 business days’ notice at the lesser of the market value or the book value of the redeemed units. G. Accounting Estimates The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period including estimates and assumptions related to taxation. Actual results could differ from those estimates by a significant amount. In addition, the Trust monitors for material events or transactions that may occur or become known after the period-end date and before the date the financial statements are released to print.

10 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

H. Indemnifications Under the Trust Agreement, the Company is indemnified against certain liabilities arising out of the performance of its duties to the Trust. Additionally, in the normal course of business, the Company as trustee for the Trust, enters into contracts with its vendors and others that contain a variety of indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust. The risk of material loss as a result of such indemnification claims is considered remote. I. Other Risks The Trust maintains investment contracts issued by insurance companies, banks and other financial institutions as required by the Declaration of Trust. The issuing institution’s ability to meet its contractual obligations under the respective contracts may be affected by future economic and regulatory developments in the insurance and banking industries. NOTE 3 - ADDITIONAL VALUATION INFORMATION

GAAP defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, under current market conditions. GAAP establishes a hierarchy that prioritizes the inputs to valuation methods, giving the highest priority to readily available unadjusted quoted prices in an active market for identical assets (Level 1) and the lowest priority to significant unobservable inputs (Level 3), generally when market prices are not readily available or are unreliable. Based on the valuation inputs, the securities or other investments are tiered into one of three levels. Changes in valuation methods may result in transfers in or out of an investment’s assigned level: Level 1 – Prices are determined using quoted prices in an active market for identical assets.Level 2 – Prices are determined using other significant observable inputs. Observable inputs are inputs that other market participants may

use in pricing a security. These may include quoted prices for similar securities, interest rates, prepayment speeds, credit risk, yield curves, loss severities, default rates, discount rates, volatilities and others.

Level 3 – Prices are determined using significant unobservable inputs. In situations where quoted prices or observable inputs are unavailable (for example, when there is little or no market activity for an investment at the end of the period), unobservable inputs may be used. Unobservable inputs reflect the Trust’s own assumptions about the factors market participants would use in determining fair value of the securities or instruments and would be based on the best available information.

The estimated value of the collective trust funds and insurance company separate accounts is net asset value, exclusive of the adjustment to contract value, and is considered Level 2. The use of net asset value as fair value is deemed appropriate as the collective trust funds and insurance company separate accounts do not have finite lives, unfunded commitments relating to these types of investments, or significant restrictions on redemptions. The Trust’s policy is to recognize transfers in and out of the valuation levels at the end of the reporting period. During the year ended December 31, 2017, there were no material transfers between valuation levels. A summary of valuation inputs can be found on the Schedule of Investments. NOTE 4 - TRANSACTIONS WITH AFFILIATES

Investment management services are provided to the Trust by the Company, an indirectly wholly-owned subsidiary of Invesco Ltd. The Company is compensated as described in Note 2E. The Company has employed, at its own expense, Invesco Fixed Income, a division of Invesco Advisers, Inc. (“Invesco”), as sub-adviser to the Trust. Invesco is an indirectly wholly-owned subsidiary of Invesco Ltd. Substantially all assets of the Trust are invested in affiliates: 56.8% in the Invesco Stable Value Trust of the Institutional Retirement Trust; 39.4% in Invesco Group Trust for Retirement Savings Collective Funds (“IGT Trusts”) and 3.8% in Invesco Short-Term Investment Fund (“Invesco STIF”). Withdrawals from the Invesco Stable Value Trust by the Trust may only be made upon 24 months’ advance written notice of intent to redeem. All funds are managed by the Company. Due to the significance of the investment in the Invesco Stable Value Trust of the Institutional Retirement Trust, those financial statements have been included within these financial statements. See the Schedule of Investments for the IGT Trusts’ cost and trust name, the percent of net assets that the IGT Trusts represent of the total net assets of the Trust, and the values of the investments in the IGT Trusts as of December 31, 2017. Redemptions of units in the IGT Trusts may be made daily.

11 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

The majority of the IGT Trusts are sub-advised by Invesco, which is an affiliate of the Company. Invesco does not charge any investment management fees on the IGT Trusts it sub-advises. Certain of the IGT Trusts in which the Trust invests are sub-advised by unaffiliated sub-advisers. These sub-advisers are paid investment management fees from the IGT Trusts they sub-advise. In addition, all IGT Trusts pay operating expenses including, but not limited to, portfolio accounting, audit, legal services, transfer agency, custody and annual report preparation and distribution. Further information regarding the fees paid to the unaffiliated sub-advisers and operating expenses for the IGT Trusts is available upon request. The Trust also invests in units of the Invesco STIF, a short-term investment vehicle managed by the Company. See the Schedule of Investments for the cost, the percent of net assets that the Invesco STIF represents of the total net assets of the Trust, and the value of the investment in the Invesco STIF as of December 31, 2017. Redemptions of units in the Invesco STIF may be made daily. Concentration of Ownership As of December 31, 2017, 100% of the Trust’s outstanding units were owned by 1 unitholder. NOTE 5 - ADDITIONAL INFORMATION REGARDING INVESTMENT CONTRACTS

Nature of Investment Contracts The Trust enters into wrapper agreements with wrap providers. A wrapper agreement is a derivative instrument that is designed to minimize the risk of investment losses and under most circumstances maintain a constant net asset value per share. Under normal circumstances, the value of the wrapper agreements is expected to vary inversely with the market value of the Trust’s assets covered (“covered assets”) by the wrapper agreement. If the market value of the covered assets is less than their book value, the wrapper agreements are assets of the Trust with a value equal to the difference which will generally result in future interest crediting rates that are lower than current market yields. Conversely, if the market value of the covered asset is more than their book value, this generally results in a deduction from market value to contract value and future crediting rates that are higher than current market yields. The book value of the wrapper agreement is equal to the purchase price of covered assets less the sale price of covered assets sold to cover share redemptions plus interest accrued at the crediting rate. To accomplish the primary objectives outlined in Note 1, the Trust enters into wrapper contracts (also known as synthetic GICs). In a synthetic GIC structure, the underlying investments are owned by the Trust for plan participants. The Trust enters into wrapper contracts from high-quality insurance companies or banks that serve to substantially offset the price fluctuations in the underlying investments caused by movements in interest rates. Each wrapper contract obligates the wrapper provider to maintain the “contract value” of the underlying investments. The contract value is generally equal to the principal amounts invested in the underlying investments, plus interest accrued at a crediting rate established under the contract, less any adjustments for withdrawals (as specified in the wrapper contract). Under the terms of the wrapper contract, the realized and unrealized gains and losses on the underlying investments are, in effect, amortized over the duration of the underlying investments through adjustments to the future contract interest crediting rate (which is the rate earned by participants in the Trust for the underlying investments). The wrapper contract provides that the adjustments to the interest crediting rate will not result in an interest crediting rate that is less than zero. This minimizes the risk of loss with respect to principal and interest. In general, if the contract value of the wrapper contract exceeds the market value of the underlying investments (including accrued interest), the wrapper provider becomes obligated to pay that difference to the Trust in the event that shareholder redemptions result in a total contract liquidation. In the event that there are partial shareholder redemptions that would otherwise cause the contract’s crediting rate to fall below zero percent, the wrapper provider is obligated to contribute to the Trust an amount necessary to maintain the contract’s crediting rate of at least zero percent. The circumstance under which payments are made and the timing of payments between the Trust and the wrapper provider may vary based on the terms of the wrapper contract. Calculating the Interest Crediting Rate in Wrapper Contracts The key factors that influence future interest crediting rates for a wrapper contract include: • The level of market interest rates • The amount and timing of participant contributions, transfers, and withdrawals into/out of the wrapper contract • The investment returns generated by the fixed income investments that back the wrapper contract • The duration of the underlying fixed income investments backing the wrapper contract

12 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

Wrapper contracts’ interest crediting rates are typically reset on a monthly or quarterly basis according to each contract. While there may be slight variations from one contract to another, most wrapper contracts use a formula that is based on the characteristics of the underlying fixed income portfolio: CR = [(1+YTM) x (MV/CV)1/Dur -1] – F Where: CR = Contract interest crediting rate YTM = Yield to maturity of underlying investments MV = Market value of underlying investments CV = Contract value (principal plus accrued crediting rate interest) Dur = Duration of the underlying investments F = Wrapper contract fees Over time, the crediting rate formula amortizes the Trust’s realized and unrealized market value gains and losses over the duration of the underlying investments. Because changes in market interest rates affect the yield to maturity and the market value of the underlying investments, they can have a material impact on the wrapper contract’s interest crediting rate. In addition, participant withdrawals and transfers from the Trust are paid at contract value but funded through the market value liquidation of the underlying investments, which also impacts the interest crediting rate. The resulting difference between the market value of the underlying investments relative to the wrapper contract value is presented on the Trust’s Schedule of Investments and Statement of Assets and Liabilities as the “Adjustment from Value to Contract Value”. If the Adjustment from Value to Contract Value is positive for a given contract, this indicates that the wrapper contract value is greater than the market value of the underlying investments. The embedded market value losses will be amortized in the future through a lower interest crediting rate. If the Adjustment from Value to Contract Value is negative, this indicates that the wrapper contract value is less than the market value of the underlying investments. The amortization of the embedded market value gains will cause the future interest crediting rate to be higher. Events That Limit the Ability of the Trust to Transact at Contract Value Investment contracts are valued at contract value principally because unitholders are able to transact at contract value when initiating benefit-responsive withdrawals, taking loans or making investment option transfers permitted by the participating plan. A benefit-responsive withdrawal includes a payment to a unitholder arising from retirement, termination of employment, disability or death. In the normal course, unitholder events are predictable (for unitholders as a group) such that the economic integrity of investment contracts is largely unaffected by unitholder withdrawals. Employer initiated events, if material, may affect the underlying economics of investment contracts. These events include plant closings, layoffs, plan termination, bankruptcy or reorganization, merger, early retirement incentive programs, tax disqualification of a trust or other events. The occurrence of one or more employer initiated events could limit the Trust’s ability to transact at contract value with plan unitholders. For example, retirement benefit payments which occur because an employer has offered a subsidized early retirement program will not transact at contract value unless the scope of the program is not material or the investment contract includes a “contract value corridor”. Whether an employer initiated event is probable is foremost within the knowledge of the employer, but in the normal course may be communicated to the investment manager of the Trust. While the investment manager may take action to minimize or eliminate the impact of the employer initiated event, there is no assurance that the issuer will continue to transact at contract value once the corridor is used. In that case, the Trust would be unable to maintain the ability to transact at contract value. As of December 31, 2017, the Trust’s management believes the occurrence of an event that would limit the ability of the Trust to transact at contract value with the unitholders in the Trust is not probable. Issuer-Initiated Contract Termination Examples of events that would permit a wrapper contract issuer to terminate a wrapper contract upon short notice include the plan’s loss of its qualified status, material breaches of responsibilities that are not cured, or material and adverse changes to the provisions of the plan. If one of these events was to occur, the wrapper contract issuer could terminate the wrapper contract at the market value of the underlying investments (or in the case of a traditional GIC, at the hypothetical market value based upon a contractual formula).

13 Invesco Stable Value Retirement Trust

Invesco Stable Value Retirement TrustNotes to Financial StatementsDecember 31, 2017

Addendum to the December 31, 2017 Statement of Assets and Liabilities

Adjustment from value to contract value at 12/31/2016: $ (8,001,877)Change in the difference between value and contract value of all fully benefit-responsive investment contracts (1,019,843)Change in the fully benefit-responsive status of the investment contracts —Adjustment from value to contract value at 12/31/2017: $ (9,021,720)

Ratio of year end market value yield to investments (at value) 2.302%Ratio of year end crediting rate to investments (at value) 2.181%Ratio of year end market value to book value 100.37%

Sensitivity Analysis

The following tables are presented to show the impact hypothetical changes in market interest rates would have on the crediting interest rates for synthetic GICs assuming constant duration of the underlying investments.

Projected Average Interest Crediting Rate (at the end of blended rate periods):

Average Portfolio Duration: 3.02 yearsAverage Portfolio Crediting Rate: 2.18%Average Portfolio Yield: 2.30%

Participant Cash Flows: 0.0%Market Rate Shock: -50% -25% No change 25% 50%Market Rate Scenario: 1.15% 1.73% 2.30% 2.88% 3.45%

Immediate: December 31, 2017 1.38% 1.51% 1.65% 1.76% 1.88%Period End: Q1 March 31, 2018 2.01% 2.06% 2.10% 2.13% 2.15%

Q2 June 30, 2018 1.92% 2.02% 2.10% 2.18% 2.24%Q3 September 30, 2018 1.84% 1.98% 2.10% 2.22% 2.32%Q4 December 31, 2018 1.77% 1.94% 2.10% 2.25% 2.40%

Participant Cash Flows: -10.0%

Market Rate Shock: -50% -25% No change 25% 50%Market Rate Scenario: 1.15% 1.73% 2.30% 2.88% 3.45%

Immediate: December 31, 2017 1.46% 1.55% 1.64% 1.73% 1.80%Period End: Q1 March 31, 2018 2.13% 2.12% 2.11% 2.08% 2.03%

Q2 June 30, 2018 2.03% 2.07% 2.11% 2.12% 2.13%Q3 September 30, 2018 1.94% 2.03% 2.10% 2.17% 2.22%Q4 December 31, 2018 1.86% 1.99% 2.10% 2.21% 2.30%

NOTE 6 - SUBSEQUENT EVENTS

On February 2, 2018, the Invesco Trust Company Board of Directors (the “Board”) approved proposed changes to the Amended and Restated Declaration of Trust for Invesco Stable Value Retirement Trust. The Board changed the withdrawal notice provision from the current 24 months to 12 months. The effective date of this change is April 30, 2018.

Subsequent events have been evaluated for recognition and disclosure through March 29, 2018, the date the financial statements were available to be issued.

PricewaterhouseCoopers LLP, 101 Seaport Boulevard, Suite 500, Boston, MA 02210 T: (617) 530 5000, F: (617) 530 5001, www.pwc.com/us

Report of Independent Auditors To the Board of Directors of Invesco Trust Company We have audited the accompanying financial statements of Invesco Stable Value Retirement Trust (the “Trust”), which comprise the statement of assets and liabilities, including the schedule of investments, as of December 31, 2017 and the related statements of operations, of changes in net assets and the financial highlights for the year then ended. These financial statements and financial highlights are hereafter collectively referred to as "financial statements". Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on the financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the Trust’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Invesco Stable Value Retirement Trust as of December 31, 2017, and the results of their operations, changes in their net assets, and the financial highlights for the year then ended, in accordance with accounting principles generally accepted in the United States of America. Other Matter Our audit was conducted for the purpose of forming an opinion on the financial statements taken as a whole. The Supplemental Schedules of Securities Purchased, Sold, or Matured is presented for purposes of additional analysis and is not a required part of the financial statements. The information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other

PricewaterhouseCoopers LLP, 101 Seaport Boulevard, Suite 500, Boston, MA 02210 T: (617) 530 5000, F: (617) 530 5001, www.pwc.com/us

records used to prepare the financial statements or to the financial statements themselves and other additional procedures, in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the financial statements taken as a whole.

Boston, MA March 29, 2018

2

Other Matter Our audit was conducted for the purpose of forming an opinion on the financial statements taken as a whole. The Supplemental Schedules of Securities Purchased, Sold, or Matured is presented for purposes of additional analysis and is not a required part of the financial statements. The information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves and other additional procedures, in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the financial statements taken as a whole.

Boston, MA March 29, 2018

16 Invesco Stable Value Retirement Trust

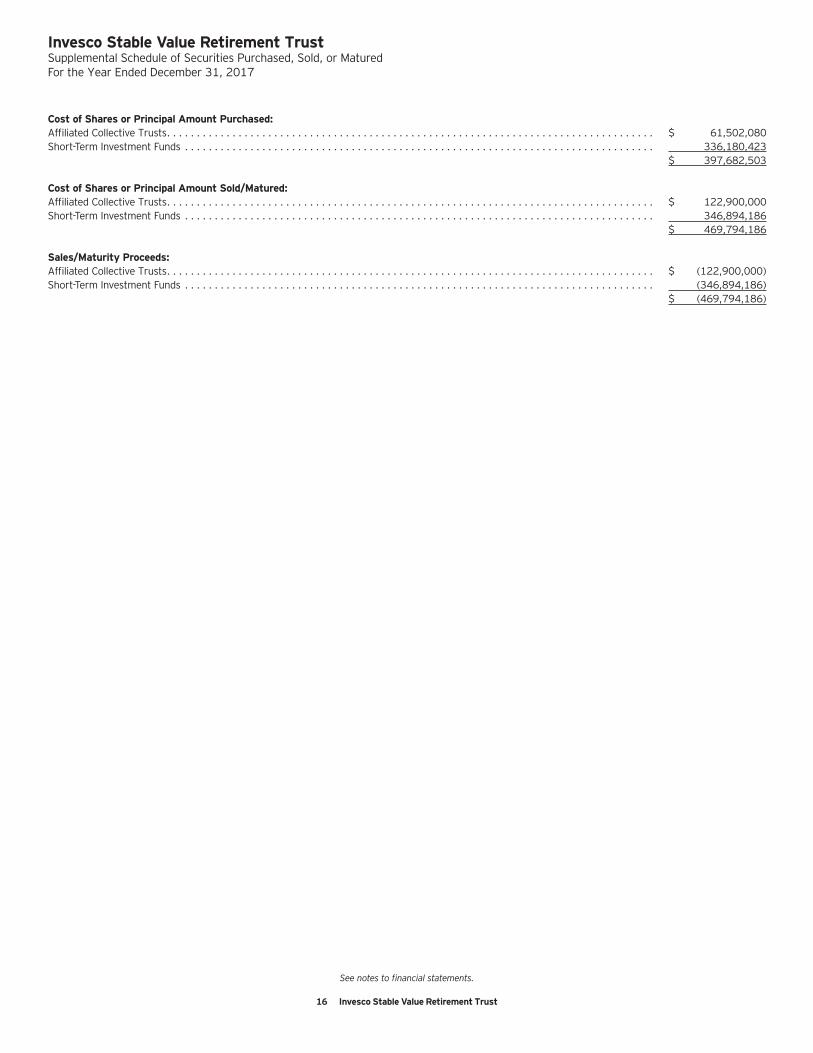

Invesco Stable Value Retirement TrustSupplemental Schedule of Securities Purchased, Sold, or MaturedFor the Year Ended December 31, 2017

See notes to financial statements.

Cost of Shares or Principal Amount Purchased:Affiliated Collective Trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 61,502,080 Short-Term Investment Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 336,180,423

$ 397,682,503

Cost of Shares or Principal Amount Sold/Matured:Affiliated Collective Trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 122,900,000 Short-Term Investment Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 346,894,186

$ 469,794,186

Sales/Maturity Proceeds:Affiliated Collective Trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ (122,900,000)Short-Term Investment Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (346,894,186)

$ (469,794,186)