introducing the etheridge integrated agriculture project

TRANSCRIPT

Introducing the

Etheridge Integrated Agriculture Project

A Large‐scale, World‐class, Vertically Integrated,

Agribusiness Development

Page 1

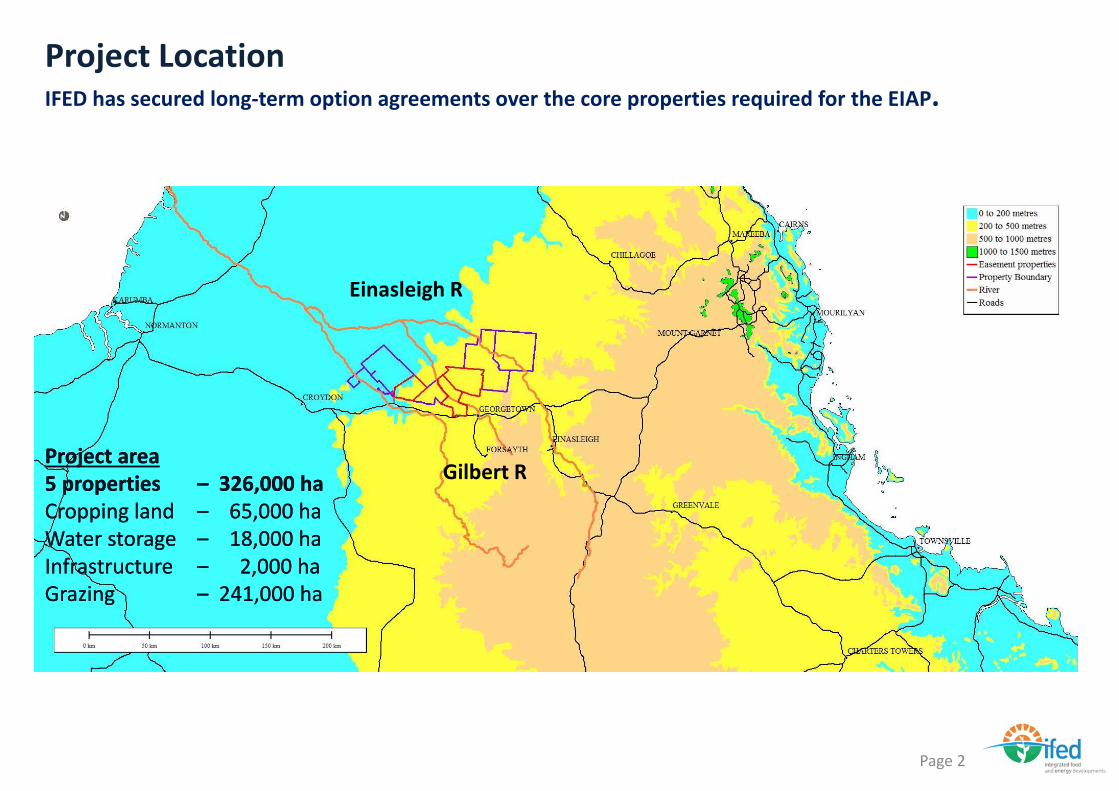

Project LocationIFED has secured long‐term option agreements over the core properties required for the EIAP.

Page 2

Project area5 properties – 326,000 haCropping land – 65,000 haWater storage – 18,000 haInfrastructure – 2,000 haGrazing – 241,000 ha

Project area5 properties – 326,000 haCropping land – 65,000 haWater storage – 18,000 haInfrastructure – 2,000 haGrazing – 241,000 ha

Einasleigh R

Gilbert R

Off‐ river water Storage ~2m/ML

The Project VisionA sustainable, world class, large scale, vertically integrated, farming and processing enterprise.

Page 3

Existingcattle

operations

Existingcattle

operations

Cogen – 90MWBagasse/biogas

Gum Plant

Sugar MillSugar, bagasse

Farm – 65,000haSugar ‐ 40,000 haGuar ‐ 25,000 ha

Feed Mill400 kt/y

Hull and germ 65 kt/y

Cane Tops

Raw sugar – 698 kt/y

Steam andElectricity ‐ 43MW

Guar gum ‐ 32 kt/y

Meat Processing

Plant

ngcattle

operations

Existingcattle

operations

Existingcattle

operations

From external local cattle producers

Cattle – 200,000Purchased from Others

Meat products 50 kt/yHides and offal

Molasses and bagasse from the sugar mill

Molasses and bagasse from the sugar mill

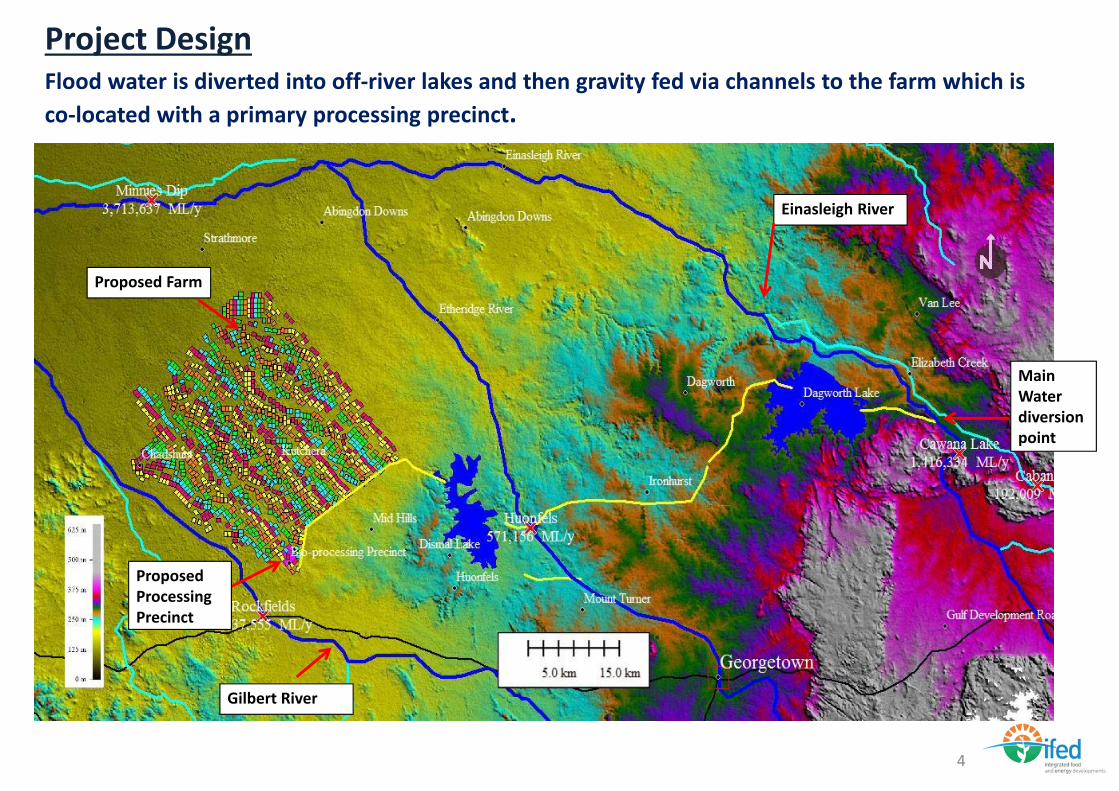

Flood water is diverted into off‐river lakes and then gravity fed via channels to the farm which is co‐located with a primary processing precinct.

4

Project Design

Main Water diversion point

Proposed Processing Precinct

Proposed Farm

Einasleigh River

Gilbert River

Project Cost Estimate Construction costs are estimated at A$1.989B and construction will take approximately 36 months.

Item Cost

Estimate $AUDm

Water diversion, storage and supply 484

Land preparation and irrigation 520

Farming and farm equipment 100

Sugar mill 515

Guar mill 52

Stock feed 36

Power station 161

Meat processing 64

Infrastructure 55

Overheads 2

Capital expenditure 1,989

Page 5

Rivers flowing into the Gulf of CarpentariaDiversion from the Gilbert River reduces flows into the Gulf of Carpentaria by 0.55 of 1% from 90,050 to 89,560 megalitres per year.

Gilbert River excl diversionDiversion from the Gilbert RiverOther Rivers discharging into the Gulf

93.8%

Source: Australia's Tropical Rivers ‐ Data Audit by NGIS Australia

5.65% 0.55 of 1%

Page 6

Water ReliabilitySimulation using government models (IQQM) combining climate, river and forecast water usage demonstrated 100% “Historical No Failure” at mean annual diversion of only 8.8%.

7

Transport LogisticsHigh capacity road trains deliver raw sugar to the Port of Townsville or Karumba to minimise inland transport costs.

Page 8

Port Distance,km Cost,$/tonneTownsville 630 35Karumba 320 18

___ Road Train___ B double

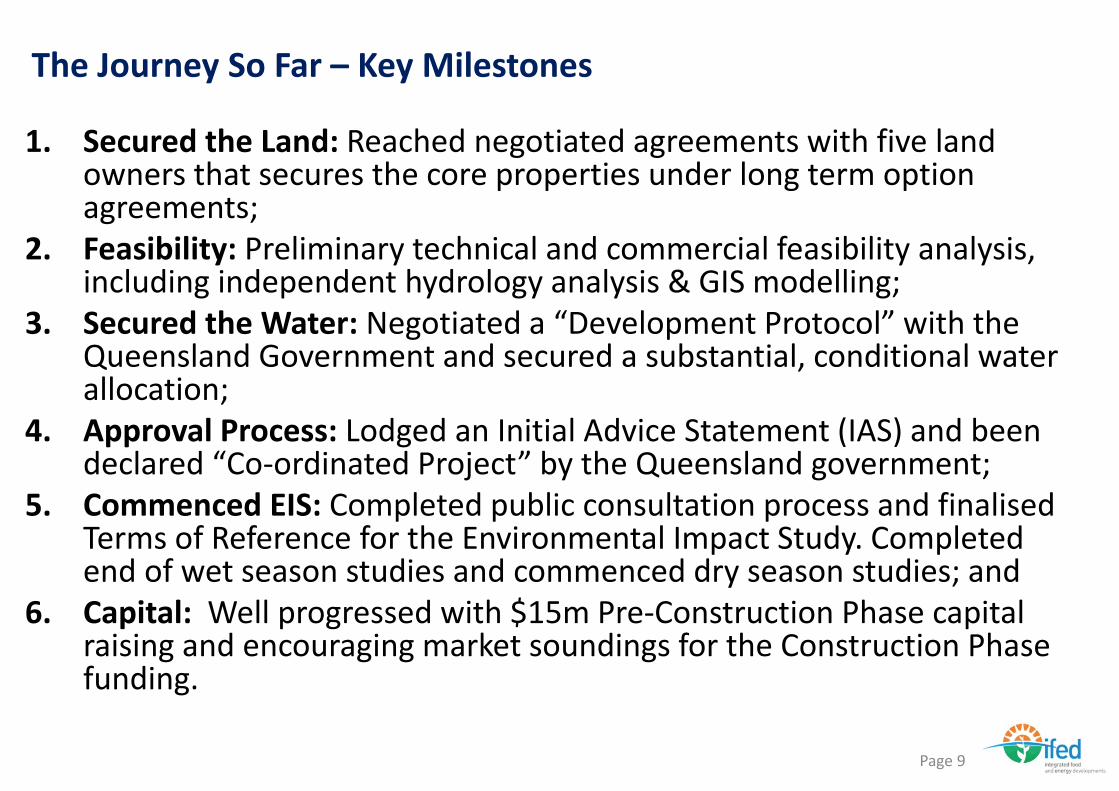

1. Secured the Land: Reached negotiated agreements with five land owners that secures the core properties under long term option agreements;

2. Feasibility: Preliminary technical and commercial feasibility analysis, including independent hydrology analysis & GIS modelling;

3. Secured the Water: Negotiated a “Development Protocol” with the Queensland Government and secured a substantial, conditional water allocation;

4. Approval Process: Lodged an Initial Advice Statement (IAS) and been declared “Co‐ordinated Project” by the Queensland government;

5. Commenced EIS: Completed public consultation process and finalised Terms of Reference for the Environmental Impact Study. Completed end of wet season studies and commenced dry season studies; and

6. Capital: Well progressed with $15m Pre‐Construction Phase capital raising and encouraging market soundings for the Construction Phase funding.

Page 9

The Journey So Far – Key Milestones

Page 10

The Wold Sugar Market

June 2014

11

Source: QSL – 22/10/14

Source: ABARES Outlook 2014

Source: ISO World Sugar Balance May 2014, updated Aug 2014

Sugar Price Indicators

12

13

Page 14

Thank You

June 2014