internship report on js bank by labeeda farid

TRANSCRIPT

1

INTERNSHIP REPORTON

JAHANGIR SIDDIQUI BANK LIMITED

Specialization: Human Resource Management

Submitted to: ChairmanDepartment of Business Administration

Submitted By: Labeeda FaridRoll #: MBHF14M023

UNIVERSITY OF SARGODHA

2

DEDICATION

I would like to dedicate this accomplishment to my beloved and caring parents and to my teachers with the support of whom I am standing at this step of my life.

3

ACKNOWLEDGEMENT

In the name of ALLAH, the most kind and most merciful.

First of all I’m grateful to ALLAH ALMIGHTY, who bestowed me with health, abilities and guidance to complete the project in a successful manner, and without HIS help I was unable to perform this task.

I would also like to thank Branch Manager and Area manager Malik Lut Ful Manan Khan, Mr. Azmat Bashir Tarar (Branch Operations Manager) and Ms. Asma Farrukh (Customer Service Officer) for providing me with the opportunity to have an excellent learning experience during my internship.

4

TABLE OF CONTENTS

Serial # Title Page #1 Title page 22 Dedication 33 Acknowledgement 44 Table of contents 55 Executive Summary 66 Vision and Mission 77 About JS Bank 88 Banking 119 Awards 1710 Products and Services 1811 Investment Opportunities in Government Securities 4112 Loans and Running Finance 4413 Wealth Management 4614 Takaful Solutions 6215 Cheque and its Types 6516 Crossing of Cheque 6717 E-Banking 6818 Job Description of Employees 6919 Employee Benefits 8520 Branch Standard Checklist 8721 Work done by Internee 9422 SWOT Analysis 9923 Conclusion 10324 References 104

5

EXECUTIVE SUMMARY

JS Bank Limited is a majority-owned subsidiary of Jahangir Siddiqui & Co. Ltd. and

incorporated in 2007. JS Bank operates in commercial banking sector. The activities of

JS Bank are categorized into five business units. They are Retail Banking, Wealth

Management, Corporate Banking, Investment Banking and Treasury.

This report is an upshot of my ten weeks internship in JS Bank of Pakistan. The main

purpose of internship is to learn, by working in practical environment and to apply the

knowledge acquired, during the studies, in a real world scenario in order to tackle the

problems. In this report the detailed analysis of the organization has been done and all

the technical, managerial and strategic aspects have been evaluated to analyze the

current position of the organization. Along with it SWOT analysis of bank has been done

and the recommendations & suggestions for the improvement have been made

wherever required. During my ten weeks internship program, I mainly worked with the

following departments:

CUSTOMER DEALING, OPERATIONS.

I successfully completed the tasks that were assigned to me.

6

VISION AND MISSION

VISION STATEMENT:To provide quality and innovative range of banking services and products to our

customers through a highly motivated team of professionals, while maintaining high

ethical and regulatory standards, thereby generating sustainable returns to our

shareholders.

MISSION STATEMENT:

To be a preferred partner of our customers by providing complete financial solutions

exceeding service expectations, and to do so through a single relationship via

convenient distribution channels, both conventional and non-conventional.

7

ABOUT JS BANK LIMITED

JS Bank Limited was formed in 2006 by the merger of Jahangir Sidiqqui Investment Bank Ltd. and the commercial banking operations of American Express Bank (Pakistan) Ltd. JS Bank Limited also possesses a Primary Dealer License for Government Securities from the State Bank of Pakistan. JS Bank is one of the fastest growing banks in Pakistan in terms of deposit growth. JS bank Ltd. key activities can be divided into four business units namely: retail and consumer banking, treasury, corporate and commercial banking and investment banking. From 100 branches in 2009, JS Bank has grown rapidly to 238 branches in 122 cities in Pakistan.

JS Bank Limited in four years has more than doubled its top line revenues and bottom line profits. That is despite the tough economic conditions that prevailed for most of the four year period. The remarkable profit growth makes it one of the fastest growing commercial banks in the country, which is a clear achievement. JS Bank has done what the big players have i.e. to cash on Government securities . The bank's investment to deposit ratio stands at 62% as at September end, having touched the highest of 73% by March 2014. The ADR has remained in the mid 40s. It would be unfair to say that all focus has been on Government securities, as the ADR has jumped from 33% a year ago to a healthy 45% now. But most of the deposit growth has been parked in Government papers, because that is where the returns have been of late, and risk free one at that. The focus has been lately on Pakistan Investment Bonds as the returns have skyrocketed. There has been some signs of JS Bank's openness about private sector lending. Banking sector spreads have been sluggish for quite some times. The deposit growth has been nothing sort of exemplary, having crossed Rs. 100 Billion mark recently. JS Bank's Current Account and Saving Account (CASA) has been hovering at 60% and has decrease of late. Most bigger banks have shifted their focus towards zero growth in deposits while improving CASA. The cost to income ratio could still be improved , but one has to bear in mind that JS Bank is growing its network, which can result in comparatively higher cost to income ratio, than more settled banks.

JS Bank has the honor of being the first bank in Pakistan to implement one of the most sophisticated and advanced core banking systems Temenos T24. This is a shift from the previous SBS system and it will allow the bank to launch new products and provide improved services to its customers.

8

JS Bank has earned a 9 month profit before tax of Rs. 610.55 million till September 30th , 2014. The bank is positioned as a robust mid-sized bank with strong liquidity and sound capital base of Rs. 10.92 billion. During past nine months JS Bank deposits have increased by 26%, with almost Rs. 21 billion in growth since December 2013. This is a direct result of customer's trust and confidence also strength of relationship between the Bank and its customers. Some of the key numbers are presented below:

JS BANK LIMITED(ALL AMOUNTS IN

RS MILLION)SEP 2014 DEC 2013 DEC 2006

DEPOSITS 101,936 80,916 7,198

ADVANCES 45,637 33,763 1,693

EQUITY 11,050 9,139 3,004

TOTAL ASSETS 130,264 112,770 12,545

PROFIT BEFORE TAX 611 501 0.406

ADR 45% 42% 24%

NO. OF BRANCHES 212 211 4

SOCIAL CORPORATE RESPONSIBILITY:

JS Group has always strived to benefit this country and its citizens through various green initiatives leading to an environmentally sustainable planet. It was one of the pioneers in converting its bank branches to solar, including in various philanthropic activities through its charitable arm to support tree plantations. Its JS Bank's principal understanding that they must contribute back to the country.

1. In September 25, 2013 JS Bank promote and finance Solar System solution in Pakistan as part of JS Bank's business strategy and corporate social responsibility. JS Bank conducts its social corporate responsibility through its own initiatives and also in collaboration with the Mahvash & Jahangir Siddiqui Foundation. JS Bank has initiated a Go Green drive converting the Dhoraji

9

Branch karachi to solar power. That means all computers, servers, ATM and teller stations are now powered with solar energy.

2. In July 09, 2013 JS Bank has launched a tree plantation campaign at Jinnah International Airport Karachi in collaboration with World Wide Fund (WWF) to bring additional shade and relief for its passengers and visitors. It is JS Bank's belief that trees are our national asset and must be protected at all costs as they play a vital role in maintaining ecological balance, keeping the environment clean and induce rainfall.

3. In April 17, 2013 Bachelors program for deaf. JS Academy for deaf is a project of Mahvash & Jahangir Siddiqui Foundation and Noor-e-Ali trust. It is one of the best charity institutions imparting education to Deaf children in the country with a unique concept of having an open door policy, allowing all the deaf children to avail higher education without any age restriction.

4. In April 27, 2013 donation of Ambulance to Al-Azeem public school system in tehsil Kahuta.

5. Wheelchair distribution by JS Bank to the flood affected. 300 customized wheelchairs were distributed.

6. Mahvash & Jahangir Siddiqui Foundation and JS Bank responded to the severe flooding by providing assistance to thousands of people whose livelihoods, homes and belongings have been destroyed or severely damaged by the floodwaters. In the second phase of flood relief operation, the primary area of focus was to provide medical services to all those suffering from infectious diseases. Medically treated 22,134 patients.

10

BANKING

Retail Banking:

Retail banking is the provision of services by a bank to individual consumers, rather

than to companies, corporations or other banks. Also known as consumer banking or

personal banking, retail banking is the visible face of banking to the general public, with

bank branches located in abundance in most major cities. Services offered

include savings and transactional accounts, mortgages, personal loans, debit cards,

and credit cards. The term is generally used to distinguish these banking services

from investment banking, commercial banking or wholesale banking. It may also be

used to refer to a division or department of a bank dealing with retail customers.

Customer deposits garnered by retail banking represent an extremely important source

of funding for most banks. Retail banking is perhaps one area of banking that has been

most impacted by technology, thanks to the proliferation of ATMs and the popularity of

online and telephone banking.

Typical products offered by a retail bank include:

Current Accounts

Saving Accounts

Debit Card – banks charge some fee annually.

Credit Card – the high interest rates charged on most credit cards makes this a

lucrative source of interest income and fees for banks.

Traveler's cheques

Mortgages on residential and investment properties – because of their size,

mortgages account for both a substantial part of retail banking profits, as well as

the biggest chunk of a bank’s exposure to its retail client base.

11

Home Equity loans

Personal loans

Certificate of Deposit/Term Deposit - these are the most popular investment

products with conservative investors, and an important funding source for banks

since the funds in these products are available to them for defined periods of

time.

Foreign currency and remittance services – the increase in cross-border banking

transactions by retail clients, and the higher spreads on currencies paid by them,

makes these services a profitable offering for retail banking.

Automobile financing – banks offer loans for new and used vehicles, as well as

refinancing for existing car loans.

Retail banking clients may also be offered the following services, generally through

another division or affiliate of the bank:

Stock brokerage (discount and full-service)

Insurance

Private banking

Wealth Management

The level of personalized retail banking services offered to a client depends on his or

her income level and the extent of the individual’s dealings with the bank. While a client

of modest means would generally be served by a teller or customer service

representative, a high net worth individual who has an extensive relationship with the

bank would typically have his or her banking requirements handled by an Account

manager or Manager.

With 238 branches in 112 cities, Retail Banking at JS Bank constantly endeavors to

provide with best banking services at all times. The innovative range of banking

services is designed to exceed customer's service expectations. Retail Banking offers a

complete range of deposit & loan products, wealth management, trade finance and

12

transactional services to a growing base of individual and institutional customers across

Pakistan.

Corporate Banking:

Corporate banking, also known as business banking, refers to the aspect of banking

that deals with corporate customers. Financial services specifically offered

to corporations, such as cash management, financing, underwriting,

and issuing of stocks, bonds, or other instruments. Financial institutions often maintain

specific divisions for handling the needs of corporate clients, separate

from consumer or retail banking activities for individual accounts.

Products and services by Corporate banking are:

Loans and other credit products – this is typically the biggest area of business

within corporate banking, and as noted earlier, one of the biggest sources of

profit and risk for a bank.

Treasury and cash management services – used by companies for managing

their working capital and currency conversion requirements.

Equipment lending – commercial banks structure customized loans and leases

for a range of equipment used by companies in diverse sectors such as

manufacturing, transportation and information technology.

Trade finance – involves letters of credit, bill collection.

Employer services – services such as payroll and group retirement plans are

typically offered by specialized affiliates of a bank.

Through their investment banking arms, commercial banks also offer related

services to their corporate clients, such as asset management and securities

underwriters.

Corporate Banking division at JS Bank offers financial solutions to meet the needs of

every type of business.

13

INVESTMENT BANKING:

An investment bank is a financial institution that assists individuals, corporations, and

governments in raising financial capital by underwriting or acting as the client's agent in

the issuance of securities (or both). An investment bank may also assist companies

involved in mergers and acquisitions (M&A) and provide ancillary services such

as market making, trading of derivatives and equity securities, and FICC services (fixed

income instruments, currencies, and commodities). Unlike commercial banks and retail

banks, investment banks do not take deposits.

JS Bank’s Investment Banking Group (IBG) has been the pioneer of numerous

landmark transactions brought to the domestic capital markets. JS Bank offers tailor-

made solutions for capital raising strategies. The products, advice / solutions offered to

clients are specifically designed to adapt to their financing / capital-raising or investment

requirements.

JS Bank’s IBG provides a comprehensive range of Corporate Finance Advisory

services in the Debt & Equity Capital Markets, including Mergers & Acquisitions,

Project Finance Advisory, Corporate Debt Originations & Syndications, Term

Finance Certificates (TFCs), Sukuks & Initial Public Offerings.

JS Bank provides assessments of capital markets and offers sound, substantial

recommendations, financial valuation and due diligence advice, either as an

independent body or as an integral part of a comprehensive Advisory and

Arrangement transaction. Given an impeccable track record of successfully

executing a wide array of large capital transactions, often under challenging

economic and time considerations, IBG has established itself as a top player in a

very elite group.

Managed by a dedicated team of professionals, IBG offers trustee / agency

services to various corporate debt offerings and plays an active role in structuring

and maintaining special purpose accounts.

14

With substantial underwriting capability, JS Bank’s IBG offers the ability to handle

large capital market offers, helping you through the Private Placement and Initial

Public Offers, i.e. pre-IPO and IPO stages. JS Bank takes pride in of bringing a

substantial number of valuable offerings to Pakistan.

JS Bank’s IBG acts as ‘Bankers to the Issue’ for Initial Public Offerings catering

to Equity as well as Debt Capital markets, Rights issues, Share Buybacks and all

other transactions where the appointment of Bankers are required by our

esteemed clientele.

Banks are middlemen between a company that wants to issue new securities

and the buying public.

In merger and acquisition, banks advise buyers and sellers on business

valuation, negotiation, pricing and structuring of transactions, as well as

procedure and implementation.

15

INSTITUTIONAL BANKING:

Institutional Banking is a specialized division in a bank that offers a comprehensive suite

of products and services for large institutions both locally and abroad. In particular they

can provide complex advisory and financing functions for corporate and Government

clients who may require tailored capital products. In addition, they may also advise on

surrounding debt equity and capital markets, risk management and transactional

banking.

Institutional banking incorporate services such as evaluating merger and acquisitions,

investment, managing treasuries etc. Also help client to create corporate strategies and

develop opportunities for growth on a national and global level. Institutional banks

provide clients with expertise, research analysis and research-based methodologies

that enable them to make sound financial decisions, suited to their business

environment.

Js bank caters to diverse needs and requirements of retail, commercial and corporate

clients’ global import and export needs in a timely, efficient, risk averse manner.

While having a continuously growing distribution network covering over 250 global

destinations via SWIFT at present.

Fund based relationships:

Discounting of Letters of Credit

Risk Participation

Trade Relationships:

Letters of Credit – Advising

Letters of Credit – Confirmation

Guarantees

JS Bank guarantees are acceptable with Government of Pakistan, its agencies and

major financial institutions.

16

AWARDS

JS Bank recognized for its Corporate Social Responsibility efforts by National Forum for Environment And Health (NFEH) at the CSR Business Excellence Awards 2013. JS Bank received its award in the category of Social Impact.

In July 13, 2009 JS Bank received an award for the "Best Communication Campaign by a Conventional Bank" as part of the Pakistan Banking Awards. The award was given by Khaleej Times which is one of the most prominent daily newspaper in UAE.

Brand of the Year Award 2013For the year 2013, JS Bank was awarded "Brand of the Year" in the category "Online Internet Banking" by the Brands Foundation.

Primary Dealer 2011-12The State Bank of Pakistan recently, 2nd year in a row has declared JS Bank as the Number 1 Primary Dealer of Government Securities for the year 2011-12. JS Bank is one of only 11 State Bank of Pakistan appointed Primary Dealers authorized to participate in the auctions of Government of Pakistan securities consisting of Treasury Bills (T-Bills) and Pakistan Investment Bonds (PIBs).

Primary Dealer 2010-11JS Bank Limited won the first award for the primary dealer for Financial Year 2010-11.

Entity Rating PACRAPACRA Upgrades Ratings of JS Bank Limited. The Pakistan Credit Rating Agency (PACRA) has upgraded the long-term entity rating of JS Bank Limited (JSBL) to ‘A+’ (Single A Plus). These ratings denote a low expectation of credit risk, while the capacity of timely payment of financial commitments is considered strong. It also reflects bank's strong financial profit emanating from improving profitability, strong liquidity and supporting capital adequacy.

17

PRODUCTS AND SERVICES

DEPOSIT PRODUCTS:

JS PLATINUM BUSINESS ACCOUNT:

It is current account for businessmen. Monthly average balance requirement of Rs.

150,000. It is non-remunerable account i.e. no profit earned on the account.

JS Platinum Business Account maybe opened by Individuals / Sole Proprietorship /

Partnership and Limited Company, primarily for business transactions.

Account holders can:

Conduct several transactions every month.

Use SMS Alerts to keep track of transactions.

Use Debit card for cash.

Use business financing for growing business.

Target Market

Well-educated Businessmen

Stakeholders of public and private companies

Small to medium sized business setups

Small merchants, traders and retailers

Transactional Benefits

Chequebooks:

18

Customers can write unlimited cheques for their business transactions. Even if average

balance falls below the requirement, one Chequebook of 50 leaves will be provided on

monthly basis free of charge.

Pay Orders:

Customers can issue as many pay orders as their business requires free of charge.

Charges will be applicable as per schedule of charges (SOC), Rs. 250/- against account

and Rs.2,500/- against cash, if average balance is not maintained.

Intercity Online Transaction:

Customers can conduct free intercity online transactions for business purposes,

regardless of average balance requirement. Normally intercity clearing charges are Rs.

300/- per cheque, but this service is provided free for this account holders.

Convenience Benefits

Platinum VISA Debit Card:

Issuance of platinum VISA Debit Card is free. Annual fee of Rs. 1800/- will be charged

if average balance is not met during the month.

SMS Alerts:

Customers can enjoy free SMS Alerts to keep them up-to-date with business

transactions. SMS Alerts charges of Rs. 1000/- per annum will be charged if average

balance is not met.

ATM Cash Withdrawal:

Customers can withdraw cash from any ATM ( 1-Link or M-Net) across Pakistan,

without any charge.

Security Benefits

19

Worry-free Cash Withdrawal:

JS Platinum Business Account provides security for cash withdrawals made anywhere

in Pakistan, through a JS Bank branch or any ATM in Pakistan. This coverage has been

designed to reimburse losses from a snatching or holdup upon cash withdrawal.

Customers are covered for cash withdrawals up to a total of Rs.50,000 per year, for up

to two instances per annum. Cash Withdrawal Insurance is valid as long as customer

inform the Bank within 30 minutes of the snatching, and is limited to 500 meters radius

of the branch or ATM where the withdrawal was made.

The branch staff will record the incidence particulars at the insurance portal and

dispatch copies of all requisite documents:

Claim Form - available at branch.

Police Report (Roznamcha) - Customer to provide.

CNIC copy - Customer to provide.

Bank Statement - To be extracted for customer account.

ATM Receipt - Customer to provide.

In case the insurance claim is approved, Insurer will make payment through cheque

favoring the beneficiary (with customer name and account number), which will be sent

to branch, for onward delivery to customer.

In case claim is declined, Insurer will inform via return email regarding reason for

declining the claim, for onward communication to the customer by the Branch.

Relationship Manager will inform the customer by calling him personally with the status

of claim.

20

JS Premium Current Account:It is current account. Monthly average balance requirement of Rs. 100,000. It is non-

remunerable account i.e. no profit earned on the account. It may be opened by

Individuals / Sole Proprietorship / Joint Accounts.

Customers can:

Frequently conduct ATM Transactions.

Have limited over-the-counter transactions.

Use deposit accounts for payment of bills and services.

Transactional Benefits

Chequebooks:

Customers can have first cheque book of 50 leaves free of charge.

Pay Orders:

Customers can issue four pay orders free of charge every month. Charges will be

applicable as per schedule of charges (SOC), Rs. 250/- against account and Rs.2,500/-

against cash, if average balance is not maintained.

Intercity Online Transaction:

Customers can conduct free intercity online transactions for business purposes,

regardless of average balance requirement. Normally intercity clearing charges are Rs.

300/- per cheque, but this service is provided free for this account holders.

Convenience Benefits

Gold VISA Debit Card:

Issuance of Gold VISA Debit Card is free. Annual fee of Rs. 1200/- will be charged if

average balance is not met during the month.

Small Locker:

21

Customers are offered with a small locker free of charge (subject to availability). The

related fees of Rs. 3000/- will be applicable as per Schedule of Charges, if the average

balance is not maintained for a full year.

ATM Cash Withdrawal:

Charges on cash withdrawals from any ATM ( 1-Link or M-Net) across Pakistan, will be

reversed into the customer's account on daily basis regardless of average balance

requirement.

Security Benefits

Worry-free Cash Withdrawal:

Customers are provided with security for cash withdrawals made anywhere in Pakistan,

through a JS bank branch counter or any ATM in Pakistan. Two snatching instances per

annum will be covered , and the aggregate coverage amount will be Rs. 50,000/- per

annum for ATM and over the counter withdrawals across Pakistan.

Mobile Snatching Insurance:

JS bank provide customers with free insurance coverage for mobile snatching.

Coverage of up to Rs. 20,000/- per annum and only one such instance per year will be

covered.

Wallet Snatching Insurance:

Coverage of Rs. 5000/- per annum and only one such instance per year will be covered.

Claim Filing:

Incidence of snatching must be reported within 30 minutes of incident through:

Phone Banking at 0800-01122

Any Js bank branch

22

The branch staff will record the incidence particulars at the insurance portal and

dispatch copies of all requisite documents:

Claim Form - available at branch.

Police Report (Roznamcha) - Customer to provide.

CNIC copy - Customer to provide.

Bank Statement - To be extracted for customer account.

ATM Receipt - Customer to provide.

In case the insurance claim is approved, Insurer will make payment through cheque

favoring the beneficiary (with customer name and account number), which will be

sent to branch, for onward delivery to customer.

In case claim is declined, Insurer will inform via return email regarding reason for

declining the claim, for onward communication to the customer by the Branch.

Relationship Manager will inform the customer by calling him personally with the

status of claim.

23

JS KAMIYAB BUSINESS ACCOUNT:The Kamiyab Business Account offers great value for businessmen, to make business

transactions smoother and faster. The following services are offered absolutely free of

charge:

Online inter-city fund transfer

Return Cheque (outward)

Demand Draft and Pay Order Issuance

Additionally, by maintaining an average monthly balance of only PKR 100,000 in the

Kamiyab Business Account, the following services can also be availed absolutely free of

charge:

Counter Cheques - Bank's book on which no account number is mentioned. When customer

needs urgent cheque and he neither has cheque book nor ATM card then bank issues that

cheque , the customer had to fill in the value of the cheque, Account number, the date, and

their signature. One counter cheque costs Rs. 100/- but it is free in this case.

Collection Cheque (Local) - is an item presented to a bank for deposit that the bank will not,

under its procedures, provisionally credit to the depositor's account or which the bank cannot

(due to provisions or law or regulation) provisionally credit to a depositor's account. Payment

must be received from the payor bank before the item may be credited to the depositor's

account.

Stop Payment - If customer looses a filled out cheque, then on customer's request bank

stops the payment of the cheque. Charges are Rs 300/- per cheque and Rs. 500/- per series,

but this is free in this case.

Chequebook Issuance (25 leaves)

Small Locker*

ATM Card Issuance**

ATM Card Annual Fee

Telex / Postage - Postage charges on cheques or bills are Rs. 100/- which in this case is

free.

Statement Issuance - It contain all the account details, deposit and withdrawals of the time.

Balance Certificate - It contain only the name of customer, his account number and closing

balance. Its charges are Rs. 200/- but it is free in this case.

24

*Subject to availability of vacant lockers at the branch.

**Applicable for individuals, sole proprietorships and partnership accounts.

25

JS RUPEE PLUS ACCOUNT:A high performing product, JS Bank’s Rupee-Plus savings account calculates profits on

a daily basis, giving maximum returns with the greatest flexibility. Profit is given on

monthly basis. Profit rate is 4.5%. Average balance of Rs

. 50,000/- should be maintained in this account otherwise (Rs. 50/- + Tax) account

maintenance charges will be cut from the account monthly.

By maintaining an average monthly balance of PKR 250,000 in the Rupee-Plus

Account, you can avail the following additional services absolutely free of charge:

Counter Cheques

Collection Cheque (Local)

Stop Payment

Chequebook Issuance (25 leaves)

Small Locker*

ATM Card Issuance**

ATM Card Annual Fee

Telex / Postage

Statement Issuance

Balance Certificate

*Subject to availability of vacant lockers at the branch.

**Applicable for individuals, sole proprietorships and partnership accounts

Calculations of monthly profit:Balance in Account × 4.5% / 365 × 30

(Subtract 10% Government charge from answer amount and then monthly profit is

calculated.)

26

JS RUPEE CURRENT ACCOUNT:The Rupee Current Account primarily targets individuals and companies that have a

high turnover of cheques. Ideal for volume based businesses, Rupee Current Account

has no initial balance requirement.

Non-profit based account and no minimum balance is required. There are no online

charges.

In addition, if an average monthly balance of PKR 100,000 is maintained in the Rupee

Current Account, the following services would be absolutely free of charge:

Online Inter-city Funds Transfer

Return Cheque (outward)

Demand Draft and Pay Order Issuance

Counter Cheques

Collection Cheque (Local)

Stop Payment

Chequebook Issuance (25 leaves)

Small Locker*

ATM Card Issuance**

ATM Card Annual Fee Waiver

Telex / Postage

Statement Issuance

Balance Certificate

*Subject to availability of vacant lockers at the branch.

**Applicable for individuals, sole proprietorships and partnership accounts

27

JS PLS RUPEE SAVING ACCOUNT:

The JS Bank PLS Saving Account is a Profit and Loss sharing account that offers

competitive returns on your savings with security and convenience. No account

maintenance charges of Rs. 50/- Profit is calculated monthly but given after every six

months. A PLS Rupee Saving Account holder gets the following services absolutely free

of charge:

Online Inter-city Funds Transfer

Return Cheque (outward)

Demand Draft and Pay Order Issuance

In addition to this, by maintaining an average monthly balance of PKR 250,000 in the

PLS Saving Account, the following additional services can also be availed absolutely

free of charge:

Counter Cheques

Collection Cheque (Local)

Retained Mail

Stop Payment

Cheque-book Issuance (25 leaves)

Small Locker*

ATM Card Issuance**

ATM Card Annual Fee Waiver

Telex / Postage

Statement Issuance

Balance Certificate

*Subject to availability of vacant lockers at the branch.

**Applicable for individuals, sole proprietorships and partnership accounts

Calculations of six months profit:Balance in Account × 4.5% / 365 × 30 ×6

(Subtract 10% Government charge from answer amount and then six months profit is

calculated.)

28

JS RUPEE BASIC BANKING ACCOUNT:

This is a Rupee account that can be operated keeping a balance as low as Rs 1,000/-.

Ideal for salaried individuals and persons with low transaction turnover, Rupee Basic

Banking Account has the following salient features:

No transactional charges up to 2 deposit transactions and 2 checking withdrawals per

month.

Not for profit account.

No minimum balance requirements.

No charges to maintain the account.

Country wide banking facility.

In case, balance of a BBA account remains nil continuously for six months then bank

closes that account.

Account statement is issued only once per year.

JS FOREIGN CURRENCY ACCOUNT:Current and Savings accounts in US$, Pound Sterling and Euros.

Money has to be deposited in the same currency as the account. On withdrawal of

money convert the money in Pakistani rupees at the rate of that day on which money is

to be withdrawn i.e. same day exchange rates apply. Withdrawal of money in foreign

currency depends upon availability of foreign currency in the bank branch.

JS FOREIGN CURRENCY PLUS SAVING ACCOUNT:

This is a new product offered from August 2015. It is a saving account with great profits

on higher deposits. The account offers option to save in US Dollars, Pound Sterling and

Euros.

Profit on this account is payable on quarterly basis, and is calculated on daily basis.

That means you get the highest returns on the savings with frequent profit payments.

29

This account allows great flexibility for all the withdrawals and deposits. Financing in

Pak Rupees up to 90% of JS Foreign currency Plus Savings Account deposit. First

chequebook is free of charge upon opening this account.

Minimum average balance requirement is:

Pounds 300

Euro 400

Dollars 500

If the minimum average balance is not maintained, an amount in prevailing currency

equivalent to Rs. 50 is applicable on monthly basis as charges.

PROFIT RATES:

JS Foreign Currency Plus Savings Account Pound Euro USD

For balance less than 4,999.99 0.10% 0.10% 0.10%

For balance between 5,000 up to 24,999.99 0.25% 0.25% 0.25%

For balances between 25,000 up to 49,999.99 0.50% 0.50% 0.50%

For balances between 50,000 up to 99,999.99 0.75% 0.75% 0.75%

For balances of 100,000 and above 1.00% 1.00% 1.00%

Profit rates of JS Foreign Currency Plus Savings Account are subject to change on

monthly basis.

30

MUHIB-E-WATAN ACCOUNT:

It’s never easy when loved ones are living abroad. Now with the JS Bank Muhib-e-

Watan Account, you have peace of mind in knowing that you can get the best return on

your funds even when your loved ones are miles away. Designed specifically for the

needs of foreign remittance beneficiaries, the JS Bank Muhib-e-Watan Account gives

you great benefits and a high rate of return so that you can enjoy the very best of life.

Great profits, paid every month

Account tailored specially for remittance customers

Fast processing for Muhib-e-Watan account holders

Easy and secure account opening.

Convenience of withdrawing funds from more than 100 JS Bank branches all over the

country

24-hour convenience of withdrawing funds with your ATM card

Account opening with just PKR 5. No limit on amount kept in account. Therefore, the

higher the amount, the bigger the profit

In accordance with the State Bank of Pakistan’s PRI program, funds from anywhere in

the world may be received in Muhib-e-Watan account*

The facility of transferring funds from any bank to your account. Submission of deposit

receipt is mandatory. The receipt should not be older than 3 working days.

In addition, avail the following and numerous other benefits, free of charge:

On-line Banking

Issuance of Cheque Book (25 leaves)

Issuance of ATM Card

Annual Fee Waiver on ATM Card

Pay Order and Demand Draft

Telebanking

31

JS GLOBAL ONLINE TRADING ACCOUNT:JS Global online trading account provides an investor direct access to Karachi Stock

Exchange through a software application. Minimum account opening is Rs. 25000.

JS Global provides two types of accounts:

A Basic Account where the investor likes to trade on his own without any

financial advisor.

A Premium Account where a dedicated trader (Financial Advisor) is assigned in

addition to the access to software application.

Through the software solution, investors can access the Ready Market against 100%

cash.

Process flow for customers inquiring about the product:1. The Branch Manager are requested to directly connect the customer to JS Global

at 021-111-574-111 or e-mail at [email protected] for any information /

queries. This process will help the customer connect directly with JS Global for

future references.

2. Any customer requiring any Relationship Manager about JS Global Online

Trading should be referred to contact the Branch Manager directly.

3. In case the customer does not have any account at JS bank, the customer

should be presented with an option of opening an account or the customer is

requires to get their signatures verified from their respective bank.

4. When finalizing the account opening form, the Branch manager should inform the

customer of attending two verification calls (one from JS bank and second from

JS Global). The account opening process will take 72 hours post these calls.

5. Branches with no Standees/Brochures of JS Global Online Trading should

coordinate with Nomita Talha (JS Global). Branches are required to display the

standees and brochures.

Account Opening Form (AOF) instructions:

32

1. Account opening form duly filled and signed (17 signatures in total) along with the

bank verification.

2. CNIC/Passport copy of account holder and Nominee. Make sure the photocopy

shows the signatures clearly.

3. Cheque in favor of JS Global Capital limited-Online Trading or Bank transfer to

JS Global Online Account # 130612. Minimum Rs. 25,000/- for basic account,

Rs. 100,000/- for premium account and Rs. 10,000/- for Student account.

4. Student ID card in case of student account.

5. Zakat Declaration Form - if applicable (True copy or attested).

6. Dispatch the documents to Muhammad Rehan Wealth Management Operations,

JS bank, 1st floor, Shaheen Commercial Complex for future processing.

Commission Structure For JS Bank Relationship Manager: The relationship manager will earn 25% of commission earned in the first year referred

through any JS Bank branch. The application form should be forwarded mentioning the

Relationship Manager code clearly on top of the form to the Wealth Management.

JS SHANDAR MUNAFA TERM DEPOSIT ACCOUNT:

This is a new product that started in August 2015. JS Shandar Munafa provides

maximum profit on a monthly basis with a seamless banking experience. It is a three

year term deposit account with monthly payout. JS Shandar Munafa Term Deposit

Account of Rs.1,00,000 up to maximum of Rs. 10 Million.

JS Shandar Munafa can be used to avail financing up to 90% of Term Deposit amount.

First cheque book is free. Also VISA Debit Classic Card is also free.

33

JS RUPEE TRAVELLERS CHEQUE:It is an easy to use cheque instrument designed to facilitate transactions in a secure

and smart way, allowing customers great flexibility in conducting transactions on the

move. For customers who travel alot within cities of Pakistan.

JS Rupee travellers cheque is very useful for individuals, particularly for customers who

need cash while travelling within Pakistan to conduct transactions, make payments and

keep their payments safe with them.

Targeted towards:

Individual travellers

Businessmen

General public

JS Rupee Travellers Cheque is available in denominations of Rs. 5000/- and Rs.

10,000/- strengthened by as many as 9 unique security features. Security features have

been added in order to make it impossible to replicate, making Travelling Cheque the

most secure in Pakistan. These security features include:

PSPC (Pakistan Security Printing Corporation) watermark on all cheques.

Unique Red Fluorescent numbering on all cheques.

Linographic Tint on background of the cheque.

Unique black MICR (Magnetic Ink Character Recognition) coding at the bottom of

the cheque.

2-color invisible Hilits at the bottom of the cheque.

State-of-the-art DP Border around cheque.

Guilloche in the center of the cheque.

JS Rupee Travellers Cheque can be en-cashed at any of JS bank branch or any bank

all over Pakistan. RTC issuance charge Rs 25 per instrument (Upto 1000 per

purchased) + 16% FED and can be waived by Regional Head and Business Head

recommendation RTC refund charges Rs 750 per instrument + 16% FED RTC

replacement charges Rs 500 per instrument + 16% FED.

34

Eligibility: JS Rupee Travellers Cheque can be issued to a literate individual and it is

mandatory to be a JS bank account holder.

RTCs can be issued individual who has firm signature.

Ineligibility:

RTCs cannot be issued against thumb impression.

RTCs cannot be issued to minor or insane person.

RTCs cannot be issued in name of any firm/company, shops or joint names.

Salient Benefits:

Readily available with minimum formality.

Sense of security with peace of mind.

Hassel free en-cashable process.

Easily refundable.

Most secured.

validity until en-cashed.

Minimum penalty in case of lost or stolen.

RTCs are available at 80 designated branch of JS bank.

Requirement for Issuance or Rupee Travellers Cheque :For JS account holders: Valid CNIC / Passport, Sale form RTC-10 completed and signed by customer along with

RTC request form. Issuance charges are Rs 25 per instrument, up to maximum Rs.

1000/- per purchase (to be waived if Rs. 100,000/- maintained in current account).

For walk in customers:Attested copy of CNIC, in case of a walk in customer/ non-account holder if the amount

of sale is up to PKR 10,000.

Lost RTCs:The customer can contact any JS bank branch and provide FIR (First Investigation

Report)/CNIC (attested photocopy)/ copy of purchase form/ indemnity form/ refund form.

35

Cancellation/ Reissuance of lost RTC charge is Rs. 500/- per instrument. Refund in lieu

of lost RTC charge is Rs. 750/- per instrument.

CARD PRODUCTS: VISA DEBIT CARD:

JS Bank Visa Debit Card gives you the convenience and freedom of using your card for

shopping directly wherever you see Visa sign in addition to cash withdrawal facility from

ATM at any time. No more worrying about carrying excess cash, your money is safe

and always reachable. Exclusive benefits of Visa Debit Card are:

Withdraw cash from over 4,800 ATMs in Pakistan on 1-Link or MNET network.

Withdraw cash from over 1 million Visa Network ATMs globally.

Accepted at over 55,000 and 27 Million retailers in Pakistan and Internationally for

shopping respectively

Easy activation through JS Phone Banking 24 hours a days.

Manage your funds, spend only as much as you have in your account.

Safer than carrying cash and in case your card is stolen or lost card you are protected

against fraudulent transactions made on your card after you report the incident.

Fees and Charges will be levied according to prevailing JS Bank Schedule of Charges.

1. ATM Cash withdrawal charges is free on JS Bank ATMs and Rs. 15 on other

bank ATMs.

2. Inter-bank fund transfer, through ATM is Rs. 60 per transaction, through mobile

and internet banking Rs. 50 per transaction.

3. Chip maintenance charges Rs. 500 per annum.

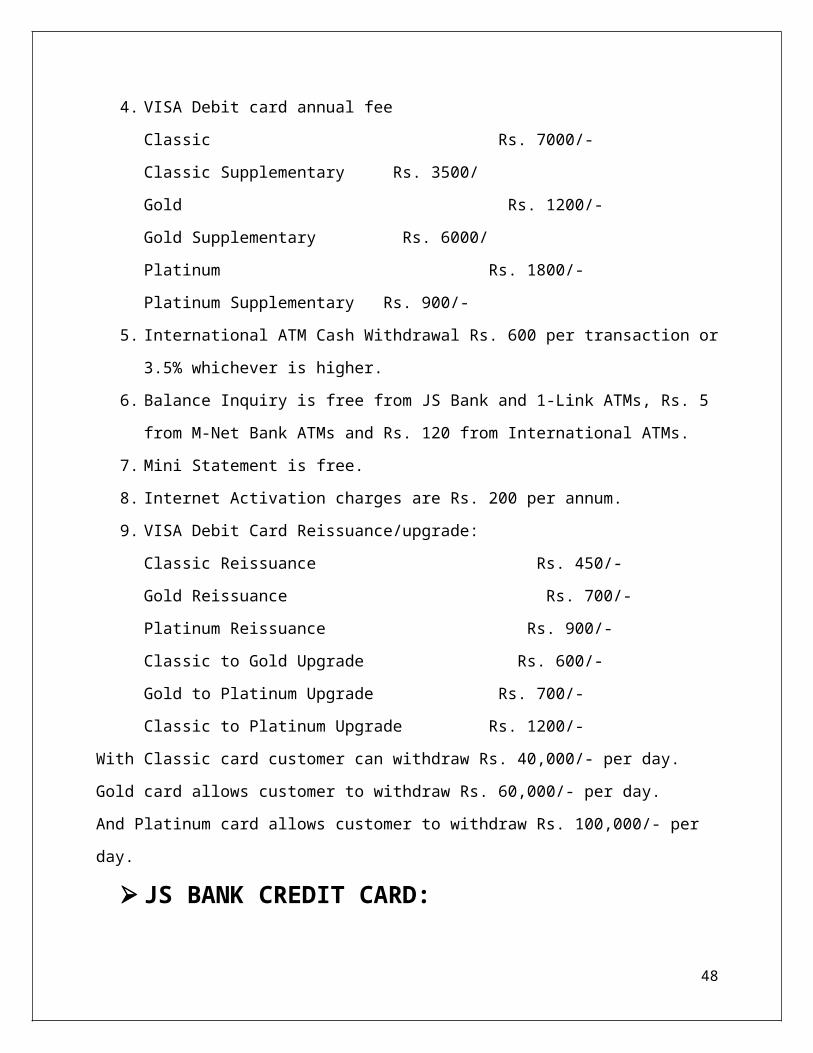

4. VISA Debit card annual fee

Classic Rs. 7000/-

Classic Supplementary Rs. 3500/

Gold Rs. 1200/-

Gold Supplementary Rs. 6000/

36

Platinum Rs. 1800/-

Platinum Supplementary Rs. 900/-

5. International ATM Cash Withdrawal Rs. 600 per transaction or 3.5% whichever is

higher.

6. Balance Inquiry is free from JS Bank and 1-Link ATMs, Rs. 5 from M-Net Bank

ATMs and Rs. 120 from International ATMs.

7. Mini Statement is free.

8. Internet Activation charges are Rs. 200 per annum.

9. VISA Debit Card Reissuance/upgrade:

Classic Reissuance Rs. 450/-

Gold Reissuance Rs. 700/-

Platinum Reissuance Rs. 900/-

Classic to Gold Upgrade Rs. 600/-

Gold to Platinum Upgrade Rs. 700/-

Classic to Platinum Upgrade Rs. 1200/-

With Classic card customer can withdraw Rs. 40,000/- per day.

Gold card allows customer to withdraw Rs. 60,000/- per day.

And Platinum card allows customer to withdraw Rs. 100,000/- per day.

JS BANK CREDIT CARD:JS Bank offers you a Credit Card which empowers you to shop at millions of locations

worldwide facilitated with amazing discounts offered globally at different outlets. JS

Bank VISA Credit Card offers all services and many more advantages which would fulfill

your credit, spending and lifestyle needs. Your card is accepted at any VISA-accepting

outlets in Pakistan and throughout the world.

JS Bank Credit Protector gives you and your family peace of mind and protection you

need. It gives you 100% coverage against your outstanding and an additional 100% to

your family, in case of death or accident. This insurance is underwritten by EFU Life

Assurance Limited, and is charged at only 0.48% of your monthly outstanding balance.

JS Bank Credit Cards will be at your service 24 hours a day 7 days a week. The VISA

sign on your Credit Card is your gateway to spending at thousands of outlets nationwide

37

and millions of locations worldwide. Your JS Bank Credit Card now lets you avail

boundless opportunities at home and abroad.

REPAYMENT PROCESS:Simply fill out the deposit slip at any JS Bank branch and deposit the cheque/cash at

the teller counter or drop it in the JS Bank Credit Card payment drop box in the branch.

Please ensure you mention your JS Bank Credit Card number on the slip. Please allow

up to three working days for same city clearance and seven working days for out of city

clearance.

SUPPLEMENTARY CARDS:Now you can have up to 6 supplementary Credit Cards issued for your family & friends,

and you can specify the credit limit for each card.

REMITTANCE SERVICES:Home Remittance facility available to JS and non-JS Bank customers. In order to

facilitate the flow of home remittance from non-resident Pakistani living abroad to their

families and loved ones in Pakistan, Home Remittance has established partners across

the globe, where the non-resident Pakistanis can remit funds to their loved ones through

the partner correspondents/Exchange Companies. This service is targeted towards

everyone, students, individuals, salaried people, sole proprietorship, partnerships or

private limited companies. Receive Remittance as high as PKR 500,000.

HOW TO RECEIVE CASH IN PAKISTAN:To receive cash payment over the counter from any nearest JS Bank branch, customer

needs to furnish the following information:

Unique Reference number i.e. MTCN/PIN

Valid photo ID (CNIC/Passport/Driving License)

CASH OVER COUNTER (COC):Customers can receive cash from 238 branches across 122 cities in Pakistan. In

addition, they may walk into any MCB or Allied Bank Limited to withdraw their cash

through a special arrangement with MCB and Allied Bank Limited respectively.

Valid Information of the Beneficiary

38

Valid photo ID (CNIC/Passport/Driving License)

TRANSFER OF FUNDS TO BENEFICIARY'S ACCOUNT WITH JS BANK:Customers can remit funds to the beneficiary's acccount maintained with any JS Bank

Branch through our partner exchange companies, having their presence nearby you by

providing the following details:

Account number

Title of account of the beneficiary

TRANSFER OF FUND TO BENEFICIARY'S ACCOUNT WITH ANY OTHER BANK IN PAKISTAN:Customers can transfer funds to beneficiary's account with any other bank in Pakistan.

Funds transfer to beneficiary account at any other bank takes place in following two

ways:

Inter Bank Funds Transfer IBFT

Real Time Gross Settlement RTGS

Inter Bank Funds Transfer:It can be done only through ATM. Funds can be transferred from any JS branch to other

bank or from any other bank to any JS Bank branch.

Real Time Gross Settlement:If fund has to be transferred from JS branch to Alfalah branch, for example, then JS

branch scans that document and sends to their head office. JS head Office sends that

to Alfalah Head Office which sends to Alfalah Branch in which the customer has

account. That branch transfers the fund to that customer's account. No withholding tax

is applied because this is bank's transaction for customers. Tax is only for customers

and not for bank.

Remittance services offered by JS bank are as follows:

WESTERN UNION SERVICE:It is dependent on 10 digits Money Transfer Control Number MTCN. CNIC Original is

needed/Passport/Driving License.

RIA INTERNATIONAL SERVICE:

39

It has 11 digits MTCN. It starts from 1211. Requirement is same as above.

EXPRESS MONEY:It has 16 digits. This service belongs to Dubai. Requirement is same as above.

AFTAB CURRENCY EXCHANGE (ACE):It has 13 digits number. requirement is same as above. For foreigners only passport is

required, no need for Computerized National Identity Card.

DEX INTERNATIONAL:It has 9 digits Money Transfer Control Number MTCN. CNIC Original is

needed/Passport/Driving License.

SPEED REMIT:It has 12 digits Money Transfer Control Number MTCN. CNIC Original is

needed/Passport/Driving License.

INSTANT CASH:It has 9 digits Money Transfer Control Number MTCN. CNIC Original is

needed/Passport/Driving License.

ALI CO:It has 8 digits Money Transfer Control Number MTCN. CNIC Original is

needed/Passport/Driving License.

40

INVESTMENT OPPORTUNITIES IN GOVERNMENT SECURITIES

The State Bank of Pakistan has allowed Banks to offer Investor Portfolio Securities (IPS) Account to all their customers for broadening the investor base of Government Securities. The product types which fall under the IPS category are Treasury Bills, Pakistan Investors Bonds and Ijarah Sukuks and any other securities that may be issued by the State bank of Pakistan on behalf of the Government of Pakistan.Previously, these products were only made available by the bank to its corporate customers and the sale was directly handled by the Bank's Treasury Department. Now branches will also be able to participate in offering this product to their retail customers.JS Bank as a primary dealer for Government Securities is permitted to act as custodian on behalf of its customers for holding their Treasury Bills, Pakistan Investment Bonds and Ijarah Sukuk Bonds in scrip-less/electronic form in these accounts. The ultimate custodian of such securities is with the Public Debt Office of the State Bank.JS bank offers financing up to 90% against T-bills, PIBs and Ijarah Sukuks.

TREAUREY BILLS (T-BILS): Zero coupon instruments issued by the Government of Pakistan. 3 months, 6 months and 1 year tenor Instruments are sold at a discount and mature at face value Sold through Primary Dealer Banks by the State Bank of Pakistan via bi-monthly

auctions Highly marketable and reserve eligible securities for Financial Institutions. Minimum denomination is Rs. 100,000.

PAKISTAN INVESTMENT BONDS (PIBs): Long term instruments issued by the Government of Pakistan. 3 years, 5 years, 10 years and 20 years tenors. Sold through Primary Dealer Banks by State Bank via monthly auctions. Fixed semi-annual coupons and repayment of principal at maturity. Highly marketable and reverse eligible securities for Financial Institutions. The minimum denominations is 100,000.

IJARAH SUKUK: Long term Islamic instruments issued by Government of Pakistan. 3 years tenor. Sold through Islamic Bank by State Bank via periodic auctions.

41

Highly marketable and reverse eligible securities for Islamic Financial Institutions. Floating and semi-annual coupon payment and repayment of principal at

maturity. Highly marketable and reverse eligible securities for Financial Institutions. Minimum denomination is Rs. 100,000.

HOW TO INVEST IN GOVERNMENT SECURITIES

Open a PKR account with any JS Bank branch

Open an IPS account linked to your PKR account.

Contact Branch for various transactions.

Finalize the transaction and receive confirmation.

Provide cheque or debit instructions for Purchase/ Sale amount.

Profit/maturity/sale amount will be credited to PKR account.

PROCESS FOR IPS ACCOUNT OPENING: Customers wanting to purchase Government Securities must sign an IPS

Account Opening Form which is available on JS Bank website. Customers other than individuals account must provide a resolution for opening

the IPS account passed by the board of directors/governing body. Upon receipt of IPS account opening form and supporting documents (if

required), Treasury office staff will scrutinize the same for completeness and issue an IPS Account number to the customer.

The IPS account statement shall be sent to customers on a quarterly basis.WITHHOLDING TAX:10% Withholding Tax is applicable from the profit/mark-up amount. Customers exempted from Withholding Tax must produce an exemption certificate issued by

42

Federal Board of Revenue (FBR) while opening the IPS Account with JS Bank. Copy of this certificate will be provided to State Bank of Pakistan by Treasury Bank office.

BENEFITS:Guaranteed Repayment:The repayment of face value at maturity and periodic coupon payments are guaranteed by the Government of Pakistan.Higher Returns:These securities provide higher returns to the investor, as compared to most bank deposits.Investment for medium term to long term:These securities offer investors with maturity periods from 3 years to 20 years.Liquidity:Highly liquid and tradable in the secondary market.Easy Process of Investment:Local and foreign investors can easily invest in the PIBs by opening an IPS Account in any Bank offering these services.

43

LOANS AND RUNNING FINANCE

JS GOLD FINANCE:JS Bank offers its customers to convert their gold ornaments into working capital for their business or investment needs, through JS Gold Finance, a unique financing facility that offers term or revolving loan against gold ornaments. It is available to JS Bank Deposit customers including individuals, sole proprietors, partnerships or private limited companies. Simply pledge the gold ornaments and avail financing through a term loan (3 years) or revolving facility , up to 70% of assessed gold value.GOLD VALUATION:JS Gold Finance offers financing against gold ornaments to the extent of net gold contents of the required fineness, as determined by Bank's designated valuator (Goldsmith). JS Bank accepts gold of at least 21 karat purity. Valuation of ornaments will only include net gold contents and will not take into account any wax, strings, fastenings, precious and semi-precious stones.FINANCING FACILITY AND TENURE:JS Bank offers financing against gold, as a running finance facility, as well as, term finance.Running Finance is offered for a tenure of one year and can be renewed after expiry of the initial term.Term Finance is offered in tenures of one, two and three years. Repayments are made in quarterly installments.WITHDRAWAL PROCESS:Gold will remain safe and insured with JS Bank for the duration of the facility, and will be returned if the customer no longer require the financing facility. Once the customer has paid off the facility, he may request the return of the Gold Ornaments from the Branch.Markup as low as at a rate of 3M KIBOR + 6% floating rate. One of the lowest rates available in the market. Prompt Payment bonus of 2% will not apply in case customer do not make payment by due date, and their markup will be 3M KIBOR + 8%.FINANCING UP TO RS 2.5 MILLION:JS Gold finance offers financing between RS. 100,000 and RS. 2.5 Million depending upon the amount of gold pledge and the amount of financing facility.

JS CAR AAMAD (AUTO FINANCING):JS Car Aamad is an installment-based loan for purchase of new, used and improved vehicles up to 9 years old from the date of manufacture.

44

BENEFITS AND FEATURES: Quickest and hassle-free processing. Lowest down payment as low as 10%. Flexible tenure 1-7 years. First year insurance financing. Insurance through reputable insurance partner-EFU at lowest rates. Financing based on fixed rate of 1 Year KIBOR + 7%. Co-borrower facility. No hidden charges. Financing from Rs. 300,000 to Rs. 5,000,000. No down payment or processing fee payments before approval.

WEALTH MANAGEMENT45

BANCASSURANCE:

ROSHAN KAL:1. THE PLAN:Roshan Kal is a regular premium Unit Linked Whole of Life Endowment Plan where the

benefits are largely linked to the value of a Growth Fund in which a portion of the

premium is invested.

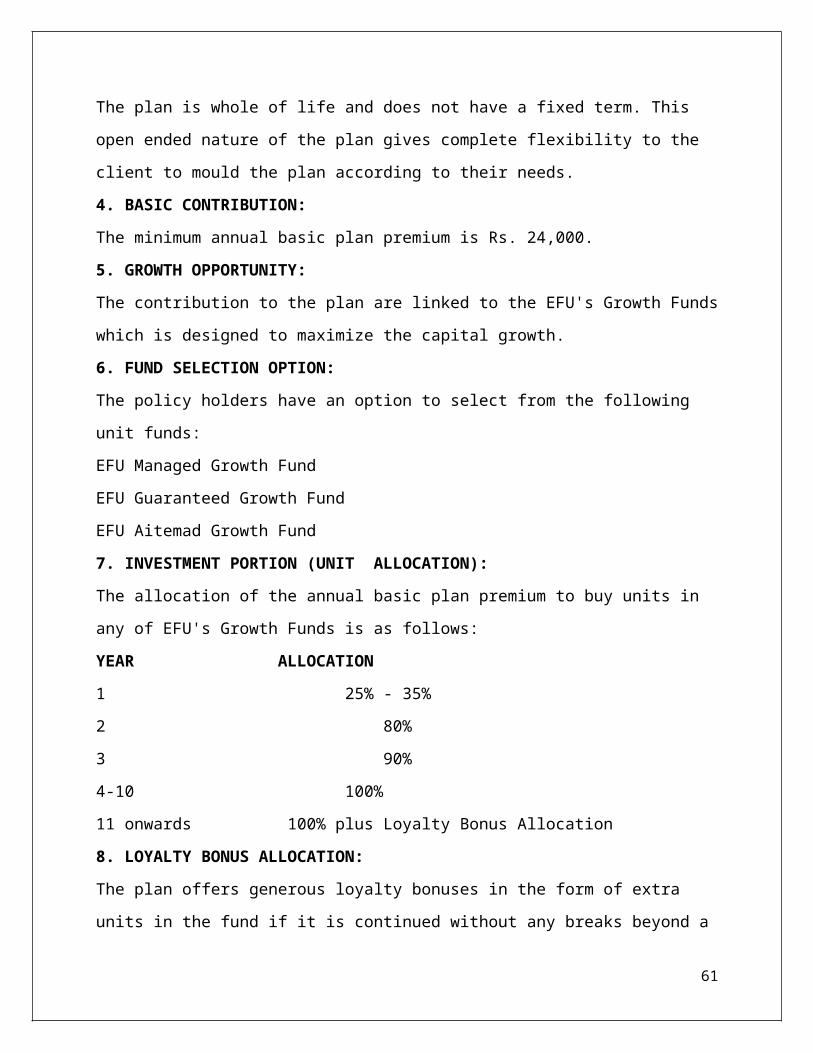

2. ELIGIBILITY AGE:Anyone between the ages of 18 years and 60 years.

3. WHOLE OF LIFE (NO FIXED TERM):The plan is whole of life and does not have a fixed term. This open ended nature of the

plan gives complete flexibility to the client to mould the plan according to their needs.

4. BASIC CONTRIBUTION:The minimum annual basic plan premium is Rs. 24,000.

5. GROWTH OPPORTUNITY:The contribution to the plan are linked to the EFU's Growth Funds which is designed to

maximize the capital growth.

6. FUND SELECTION OPTION:The policy holders have an option to select from the following unit funds:

EFU Managed Growth Fund

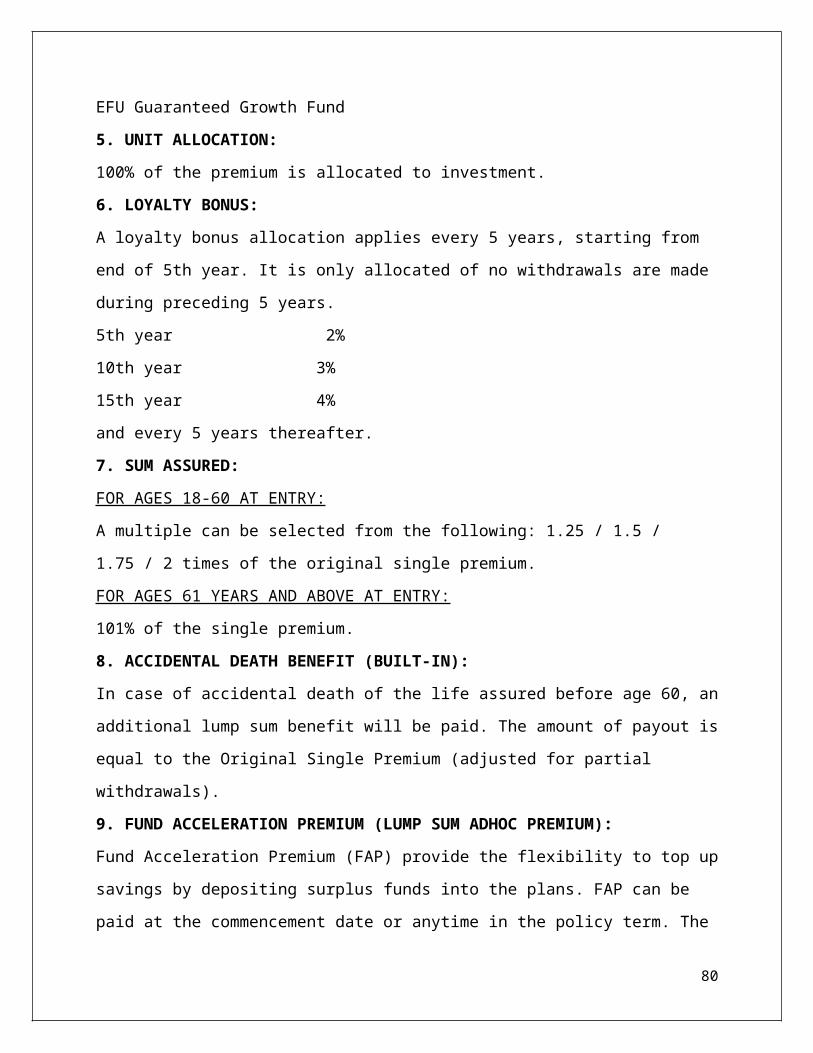

EFU Guaranteed Growth Fund

EFU Aitemad Growth Fund

7. INVESTMENT PORTION (UNIT ALLOCATION):The allocation of the annual basic plan premium to buy units in any of EFU's Growth

Funds is as follows:

YEAR ALLOCATION1 25% - 35%

2 80%

3 90%

46

4-10 100%

11 onwards 100% plus Loyalty Bonus Allocation

8. LOYALTY BONUS ALLOCATION:The plan offers generous loyalty bonuses in the form of extra units in the fund if it is

continued without any breaks beyond a period of 10 years. The bonus is allocated to the

plan every five years. The longer the plan is continued, the higher the rewards will be.

YEAR ALLOCATION11 30%

16 45%

21 60%

26 75%

31 90%

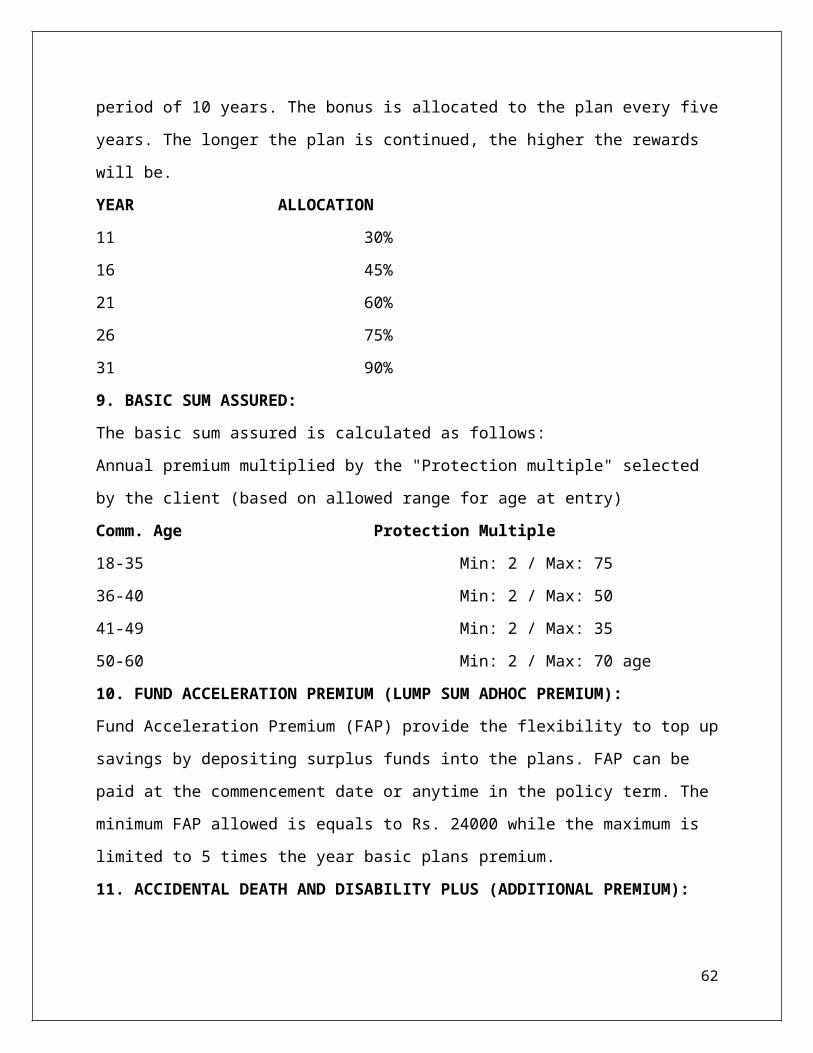

9. BASIC SUM ASSURED:The basic sum assured is calculated as follows:

Annual premium multiplied by the "Protection multiple" selected by the client (based on

allowed range for age at entry)

Comm. Age Protection Multiple 18-35 Min: 2 / Max: 75

36-40 Min: 2 / Max: 50

41-49 Min: 2 / Max: 35

50-60 Min: 2 / Max: 70 age

10. FUND ACCELERATION PREMIUM (LUMP SUM ADHOC PREMIUM):Fund Acceleration Premium (FAP) provide the flexibility to top up savings by depositing

surplus funds into the plans. FAP can be paid at the commencement date or anytime in

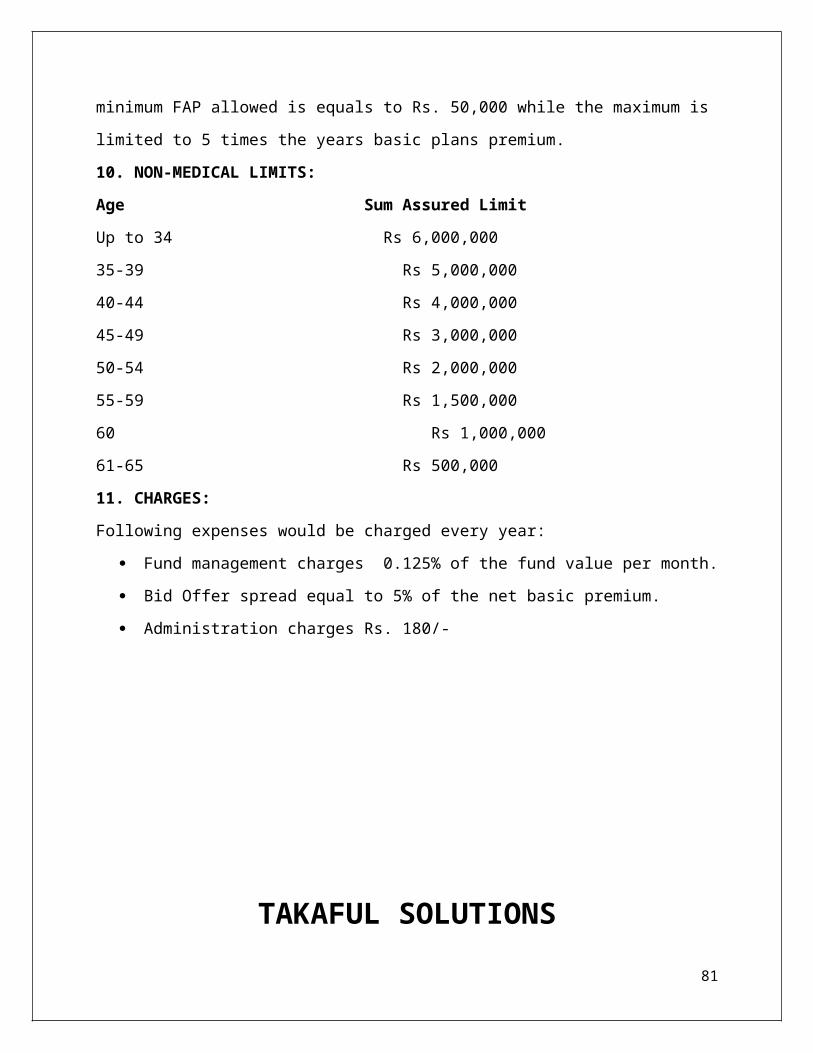

the policy term. The minimum FAP allowed is equals to Rs. 24000 while the maximum

is limited to 5 times the year basic plans premium.

11. ACCIDENTAL DEATH AND DISABILITY PLUS (ADDITIONAL PREMIUM):If death results due to an accident, an extra sum equals to 50% to 200% of the basic

sum assured would be payable. Alternately if a disability results due to an accident the

benefit would be 50% to 100% of the calculated amount. Maximum payout up to 10

Million.

47

12. WAIVER OF PREMIUM (ADDITIONAL BENEFIT):In case of partial or permanent total disability of the insured to continue any occupation

the premium is waived. However the benefit of the plan continues.

13. FAMILY INCOME BENEFIT (ADDITIONAL BENEFIT):A monthly income is paid to the family in case of the unfortunate death of the assured.

This amount is equal to 1% of the sum assured. The income can be used to pay for

continuing the educational expenses of the child. This income may also be used to

support the family.

14. LIFE CARE BENEFIT PLUS (ADDITIONAL BENEFIT):Specific sum amount is payable in the event of a range of 16 illnesses. Maximum up to

1.5 Million.

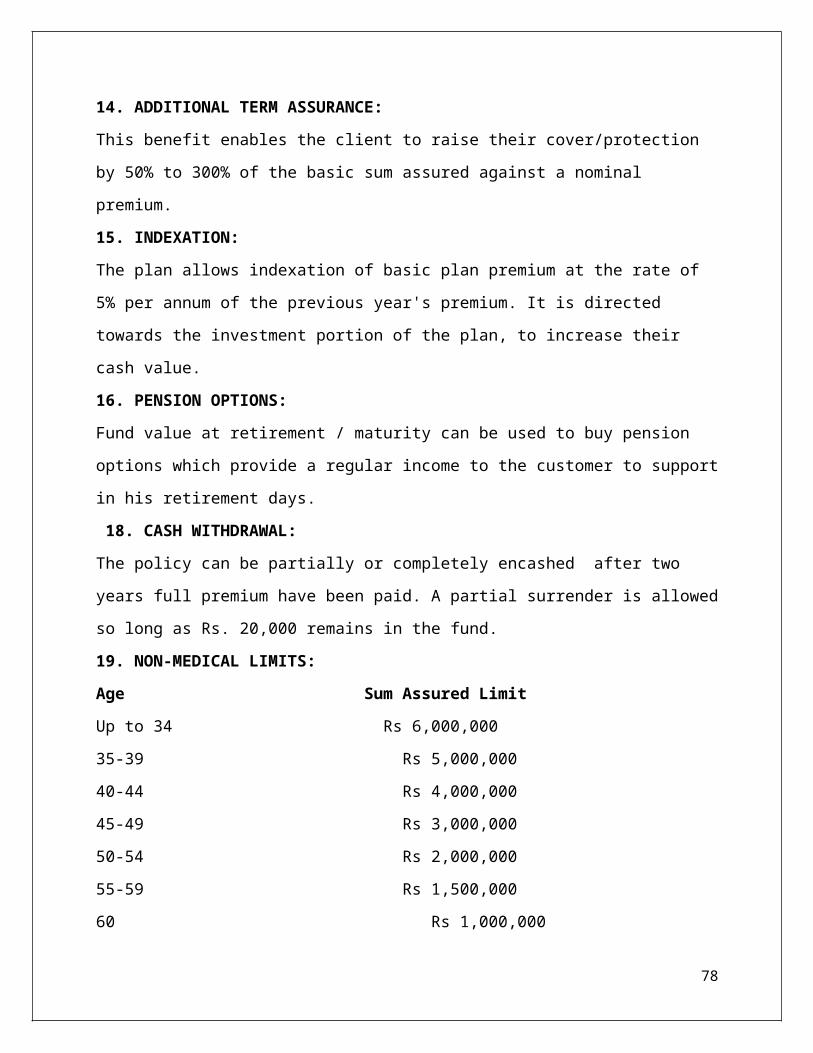

15. ADDITIONAL TERM ASSURANCE:This benefit enables the client to raise their cover / protection by 50% to 200% of the

basic sum assured against a nominal premium.

16. CHARGES: Following expenses would be charged every year:

Fund management charges 0.125% of the fund value per month.

Bid Offer spread equal to 5% of the net basic premium.

Administration charges Rs. 180/-

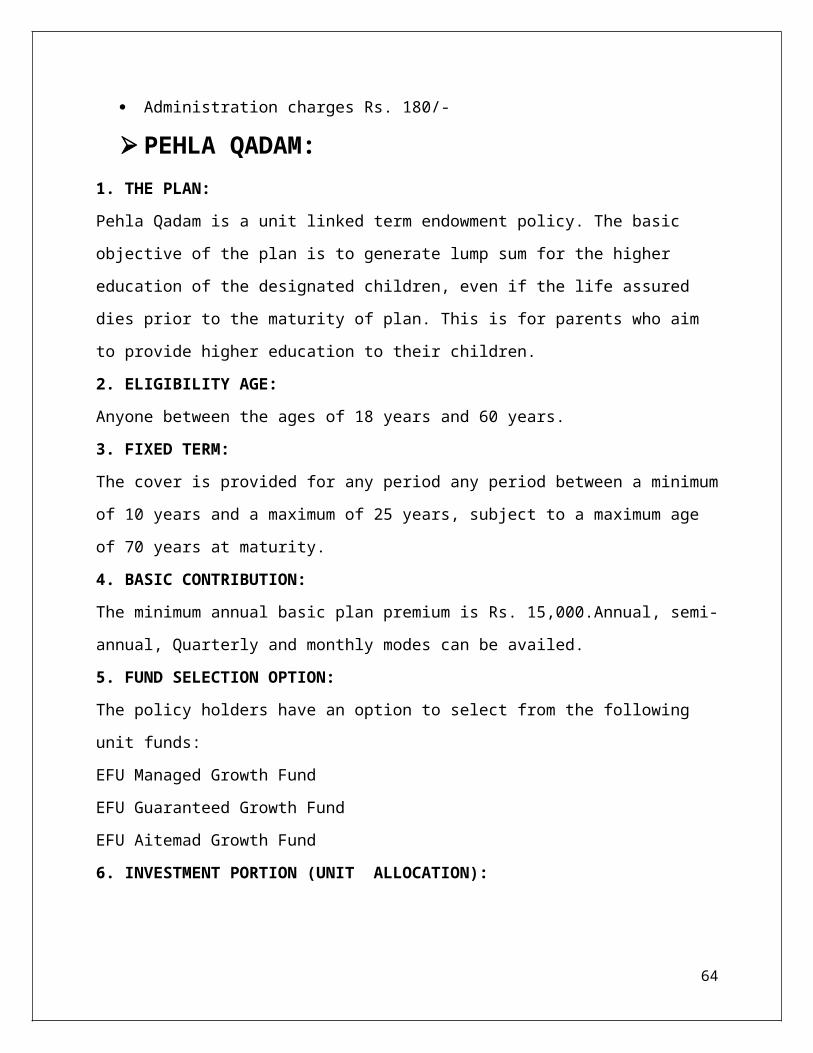

PEHLA QADAM:1. THE PLAN:Pehla Qadam is a unit linked term endowment policy. The basic objective of the plan is

to generate lump sum for the higher education of the designated children, even if the life

assured dies prior to the maturity of plan. This is for parents who aim to provide higher

education to their children.

2. ELIGIBILITY AGE:Anyone between the ages of 18 years and 60 years.

3. FIXED TERM:The cover is provided for any period any period between a minimum of 10 years and a

maximum of 25 years, subject to a maximum age of 70 years at maturity.

48

4. BASIC CONTRIBUTION:The minimum annual basic plan premium is Rs. 15,000.Annual, semi-annual, Quarterly

and monthly modes can be availed.

5. FUND SELECTION OPTION:The policy holders have an option to select from the following unit funds:

EFU Managed Growth Fund

EFU Guaranteed Growth Fund

EFU Aitemad Growth Fund

6. INVESTMENT PORTION (UNIT ALLOCATION):The allocation of the annual basic plan premium to buy units in any of EFU's Growth

Funds is as follows:

YEAR ALLOCATION1 25% - 35%

2 80%

3 onward 100%

11 onwards 105%

7. CONTINUATION BENEFIT (BUILT- IN):This is a built-in benefit. It ensures that all the future contributions will be paid by EFU

LIFE following the death of the Life Assured until the maturity date of the plan.

8. FUND ACCELERATION PREMIUM (LUMP SUM ADHOC PREMIUM):Fund Acceleration Premium (FAP) provide the flexibility to top up savings by depositing

surplus funds into the plans. FAP can be paid at the commencement date or anytime in

the policy term. The minimum FAP allowed is equals to Rs. 15,000 while the maximum

is limited to 5 times the year basic plans premium.

9. WAIVER OF PREMIUM (ADDITIONAL BENEFIT):In case of partial or permanent total disability of the insured to continue any occupation

the premium is waived. However the benefit of the plan continues.

10. INCOME BENEFIT (ADDITIONAL BENEFIT):A quarterly income is paid to the family in case of the unfortunate death of the assured.

This amount is equal to 25% of the basic plan premium. The income can be used to pay

49

for the continuing education expenses of the child. This income may also be used to

support the family.

11. ACCIDENTAL DEATH AND DISABILITY BENEFIT (ADDITIONAL BENEFIT):If death results due to an accident, an extra sum equals to 10 multiples of basic annual

premium is paid. Alternately in case of disability 50% to 100% of the calculated amount

will be paid. Maximum payout is limited to PKR 10 Million.

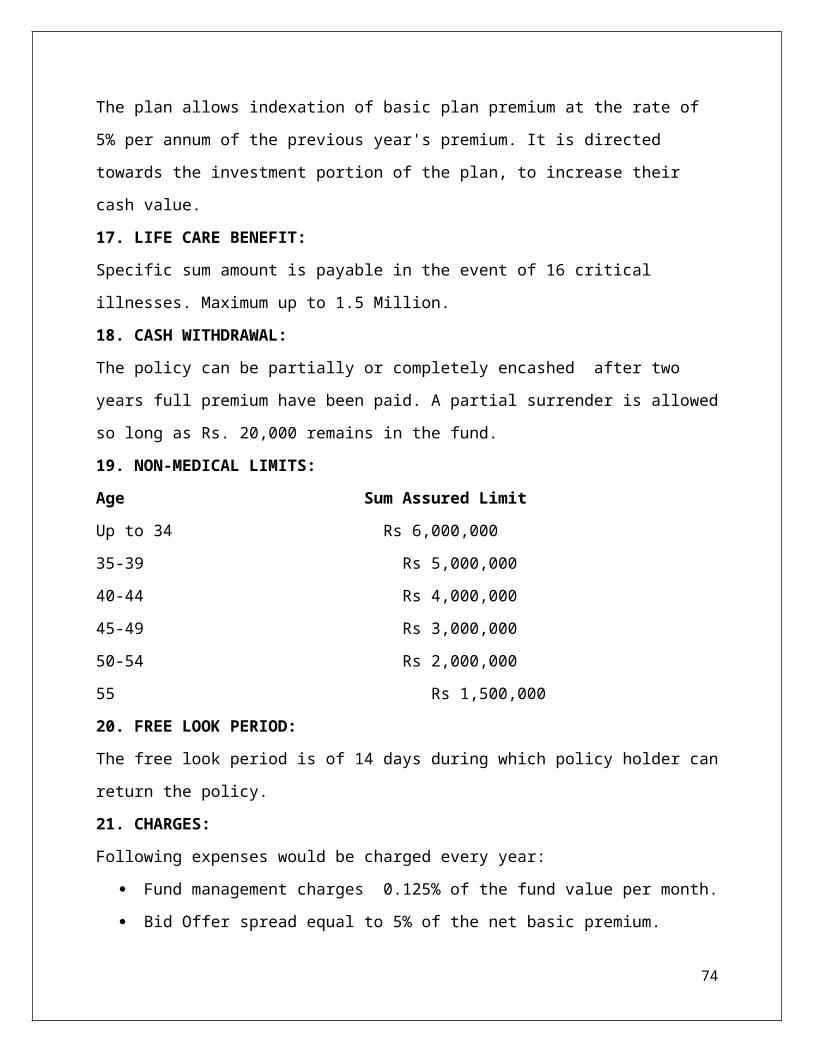

12. INDEXATION:The plan allows indexation of basic plan premium at the rate of 5% per annum of the

previous year's premium. It is directed towards the investment portion of the plan, to

increase their cash value.

13. CASH WITHDRAWAL:The policy can be partially or completely encashed after two years full premium have

been paid. A partial surrender is allowed so long as Rs. 20,000 remains in the fund.

14. NON-MEDICAL LIMITS:Age Sum Assured LimitUp to 34 Rs 6,000,000

35-39 Rs 5,000,000

40-44 Rs 4,000,000

45-49 Rs 3,000,000

50-54 Rs 2,000,000

55-59 Rs 1,500,000

60 Rs 1,000,000

15. FREE LOOK PERIOD:The free look period is of 14 days during which policy holder can return the policy.

16. CHARGES: Following expenses would be charged every year:

Fund management charges 0.125% of the fund value per month.

Bid Offer spread equal to 5% of the net basic premium.

Administration charges Rs. 180/-

HAMSAFAR:

50

1. THE PLAN:Hamsafar is a unit linked term endowment policy. The basic objective of the plan is to

generate lump sum for the higher marriage of the designated child, even if the life

assured dies prior to the maturity of plan. This is for parents who are planning a

handsome saving amount for the marriage of their children in upcoming future.

2. ELIGIBILITY AGE:Anyone between the ages of 18 years and 60 years.

3. FIXED TERM:The cover is provided for any period any period between a minimum of 10 years and a

maximum of 25 years, subject to a maximum age of 70 years at maturity.

4. BASIC CONTRIBUTION:The minimum annual basic plan premium is Rs. 24,000.Annual, semi-annual, Quarterly

and monthly modes can be availed.

5. FUND SELECTION OPTION:The policy holders have an option to select from the following unit funds:

EFU Managed Growth Fund

EFU Guaranteed Growth Fund

EFU Aitemad Growth Fund

6. INVESTMENT PORTION (UNIT ALLOCATION):The allocation of the annual basic plan premium to buy units in any of EFU's Growth

Funds is as follows:

YEAR ALLOCATION1 25% - 35%

2 80%

3 onward 100%

7. MARRIAGE SUPPORT BONUS:The plan offers generous loyalty bonuses in the form of extra units in the fund if it is

continued without any breaks beyond a period of 10 years. The bonus is allocated to the

plan every 5 years. The longer the plan is continued, the higher the rewards shall be.

11th year 100% + 20%

51

16th year 100% + 30%

21st year 100% + 50%

8. CONTINUATION BENEFIT (BUILT- IN):This is a built-in benefit. It ensures that all the future contributions will be paid by EFU

LIFE following the death of the Life Assured until the maturity date of the plan.

9. FUND ACCELERATION PREMIUM (LUMP SUM ADHOC PREMIUM):Fund Acceleration Premium (FAP) provide the flexibility to top up savings by depositing

surplus funds into the plans. FAP can be paid at the commencement date or anytime in

the policy term. The minimum FAP allowed is equals to Rs. 24000 while the maximum

is limited to 5 times the year basic plans premium.

10. WAIVER OF PREMIUM (ADDITIONAL BENEFIT):In case of partial or permanent total disability of the insured to continue any occupation

the premium is waived. However the benefit of the plan continues.

11. INCOME BENEFIT (ADDITIONAL BENEFIT):A quarterly income is paid to the family in case of the unfortunate death of the assured.

This amount is equal to 25% of the basic plan premium. The income can be used to pay

for the continuing education expenses of the child. This income may also be used to

support the family.

12. INDEXATION:The plan allows indexation of basic plan premium at the rate of 5% per annum of the

previous year's premium. It is directed towards the investment portion of the plan, to

increase their cash value.

13. ENGAGEMENT BONUS:At the end of 15 years EFU LIFE will add an engagement bonus to the plan equal to

15% of the average basic plan premium paid.

14. MATURITY OPTION:At maturity if the funds are left with EFU LIFE for one year, EFU will pay the

accumulated fund value and a "Maturity Investment Bonus" of 20% of annual average

premium.

15. CASH WITHDRAWAL:

52

The policy can be partially or completely encashed after two years full premium have

been paid. A partial surrender is allowed so long as Rs. 20,000 remains in the fund.

16. NON-MEDICAL LIMITS:Age Sum Assured LimitUp to 34 Rs 6,000,000

35-39 Rs 5,000,000

40-44 Rs 4,000,000

45-49 Rs 3,000,000

50-54 Rs 2,000,000

55-59 Rs 1,500,000

60 Rs 1,000,000

17. FREE LOOK PERIOD:The free look period is of 14 days during which policy holder can return the policy.

18. CHARGES: Following expenses would be charged every year:

Fund management charges 0.125% of the fund value per month.

Bid Offer spread equal to 5% of the net basic premium.

Administration charges Rs. 180/-

WOMEN'S SAVING PLAN:1. THE PLAN:This is a regular unit linked protection and saving plan suitable for working females as

well as housewives. The plan helps accumulate a substantial fund which can be used to

finance future financial needs.

2. ELIGIBILITY AGE:Anyone between the ages of 18 years and 60 years.

3. TERM:The minimum term of plan is 10 years and a maximum of 25 years, subject to a

maximum age of 70 years at maturity.

4. BASIC CONTRIBUTION:

53

The minimum annual basic plan premium is Rs. 24,000.Annual, semi-annual, Quarterly

and monthly modes can be availed.

5. GROWTH OPPORTUNITY:The contribution to the plans are linked to the EFU Funds which is designed to

maximize the capital growth.

6. FUND SELECTION OPTION:The policy holders have an option to select from the following unit funds:

EFU Managed Growth Fund

EFU Guaranteed Growth Fund

EFU Aitemad Growth Fund

7. INVESTMENT PORTION (UNIT ALLOCATION):The allocation of the annual basic plan premium to buy units in any of EFU's Growth

Funds is as follows:

YEAR ALLOCATION1 35%

2 80%

3 90%

4 to 5 100%

6 to 10 103%

11 onwards 105%

8. BASIC SUM ASSURED FOR WORKING WOMEN:The basic sum assured is calculated as follows:

Annual premium multiplied by the "Protection multiple" selected by the client (based on

allowed range for age at entry)

Comm. Age Protection Multiple 18-35 Min: 2 / Max: 75

36-40 Min: 2 / Max: 50

41-49 Min: 2 / Max: 35

50-60 Min: 2 / Max: 70 age

9. BASIC SUM ASSURED FOR HOUSEWIVES:

54

For housewives the basic sum assured is 15 times Basic Annual Premium, subject to a

maximum amount of PKR 500,000.

10. FUND ACCELERATION PREMIUM (LUMP SUM ADHOC PREMIUM):Fund Acceleration Premium (FAP) provide the flexibility to top up savings by depositing

surplus funds into the plans. FAP can be paid at the commencement date or anytime in

the policy term. The minimum FAP allowed is equals to Rs. 24,000 while the maximum

is limited to 5 times the years basic plans premium.

11. FAMILY INCOME BENEFIT (BUILT-IN):A monthly income is paid to the family in case of the unfortunate death of the assured.

This amount is equal to 1% of the sum assured. The income can be used to pay for

continuing the educational expenses of the child. This income may also be used to

support the family.

For Housewives, in case of the death of the life assured, a fixed monthly income of PKR

5,000 is payable for the remaining term.

12. ACCIDENTAL DEATH AND DISABILITY BENEFIT (ONLY FOR WORKING WOMEN):If death results due to an accident, an extra sum equals to 10 multiples of basic plan

premium is paid. Alternately in case of disability 50% to 100% of the calculated amount

will be paid. Maximum payout is limited to PKR 10 Million.

13. WAIVER OF PREMIUM (ONLY FOR WORKING WOMEN):In case of partial or permanent total disability of the insured to continue any occupation

the premium is waived. However the benefit of the plan continues.

14. MEDICAL RECOVERY BENEFIT:This covers 379 diseases/illnesses. This is only for working women.

15. ADDITIONAL TERM ASSURANCE:This benefit enables the client to raise their cover/protection by 50% to 300% of the

basic sum assured against a nominal premium. This is only for working women.

16. INDEXATION:The plan allows indexation of basic plan premium at the rate of 5% per annum of the

previous year's premium. It is directed towards the investment portion of the plan, to

increase their cash value.

55

17. LIFE CARE BENEFIT:Specific sum amount is payable in the event of 16 critical illnesses. Maximum up to 1.5

Million.

18. CASH WITHDRAWAL:The policy can be partially or completely encashed after two years full premium have

been paid. A partial surrender is allowed so long as Rs. 20,000 remains in the fund.

19. NON-MEDICAL LIMITS:Age Sum Assured LimitUp to 34 Rs 6,000,000

35-39 Rs 5,000,000

40-44 Rs 4,000,000

45-49 Rs 3,000,000

50-54 Rs 2,000,000

55 Rs 1,500,000

20. FREE LOOK PERIOD:The free look period is of 14 days during which policy holder can return the policy.

21. CHARGES: Following expenses would be charged every year:

Fund management charges 0.125% of the fund value per month.

Bid Offer spread equal to 5% of the net basic premium.

Administration charges Rs. 180/-

RETIREMENT PLAN:1. THE PLAN:This is a regular premium Unit Linked Term Endowment Plan. The contribution in this

plan are invested in accumulation investment funds to build up substantial capital. At

retirement or anytime after age of 50 years, the accumulated fund can be converted into

a regular stream of pension.

2. ELIGIBILITY AGE:Anyone between the ages of 18 years and 60 years.

56

3. TERM:The minimum term of plan is 10 years and a maximum of 45 years, subject to a

maximum age of 70 years at maturity.

4. BASIC CONTRIBUTION:The minimum annual basic plan premium is Rs. 24,000. Annual, semi-annual, Quarterly

and monthly modes can be availed.

5. GROWTH OPPORTUNITY:The contribution to the plans are linked to the EFU Funds which is designed to

maximize the capital growth.

6. FUND SELECTION OPTION:The policy holders have an option to select from the following unit funds:

EFU Managed Growth Fund

EFU Guaranteed Growth Fund

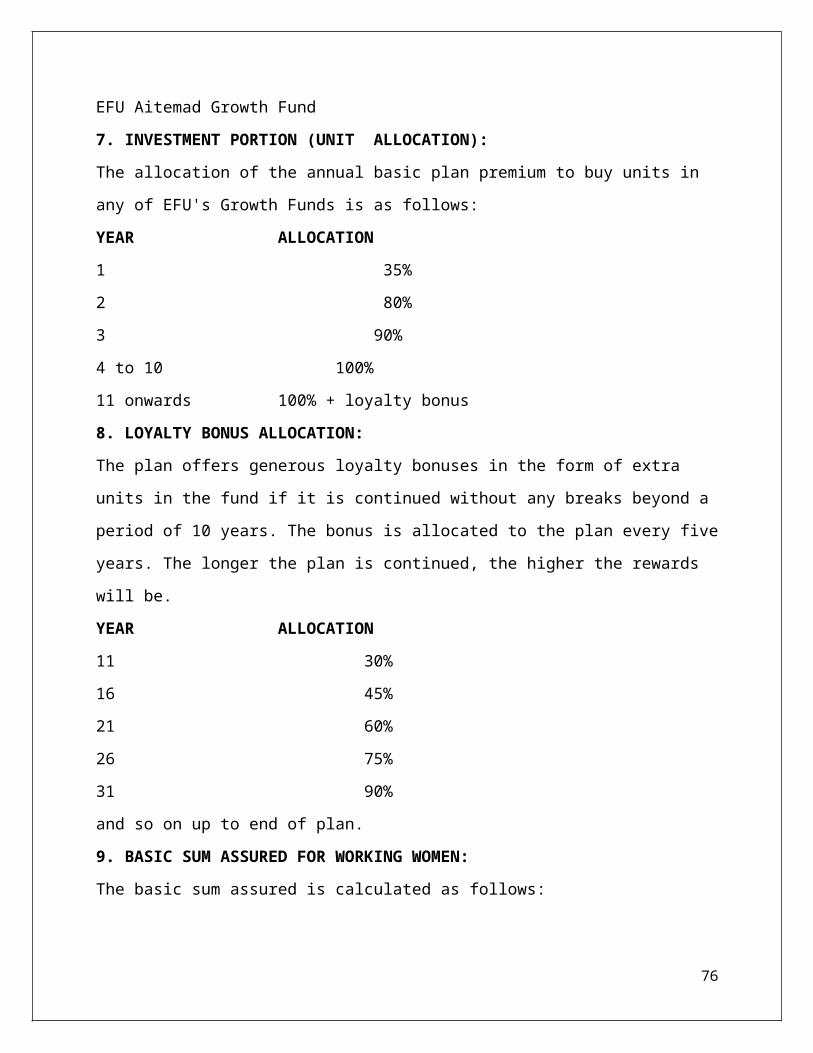

EFU Aitemad Growth Fund

7. INVESTMENT PORTION (UNIT ALLOCATION):The allocation of the annual basic plan premium to buy units in any of EFU's Growth

Funds is as follows:

YEAR ALLOCATION1 35%

2 80%

3 90%

4 to 10 100%

11 onwards 100% + loyalty bonus

8. LOYALTY BONUS ALLOCATION:The plan offers generous loyalty bonuses in the form of extra units in the fund if it is

continued without any breaks beyond a period of 10 years. The bonus is allocated to the

plan every five years. The longer the plan is continued, the higher the rewards will be.

YEAR ALLOCATION11 30%

16 45%

21 60%

57

26 75%

31 90%

and so on up to end of plan.

9. BASIC SUM ASSURED FOR WORKING WOMEN:The basic sum assured is calculated as follows:

Annual premium multiplied by the "Protection multiple" selected by the client (based on

allowed range for age at entry)

Comm. Age Protection Multiple 18-49 Min: 2 / Max: 35

50-60 Min: 2 / Max: 70 age

10. FUND ACCELERATION PREMIUM (LUMP SUM ADHOC PREMIUM):Fund Acceleration Premium (FAP) provide the flexibility to top up savings by depositing

surplus funds into the plans. FAP can be paid at the commencement date or anytime in

the policy term. The minimum FAP allowed is equals to Rs. 24,000 while the maximum

is limited to 5 times the years basic plans premium.

11. ACCIDENTAL DEATH AND DISABILITY PLUS (BUILT-IN):If death results due to an accident, an extra sum equals to 10 times of basic annual

premium is paid. Alternately in case of disability 50% to 100% of the calculated amount

will be paid. Maximum payout is limited to PKR 5 Million.

12. WAIVER OF PREMIUM:In case of partial or permanent total disability of the insured to continue any occupation

the premium is waived. However the benefit of the plan continues.

13. FAMILY INCOME BENEFIT:A monthly income is paid to the family in case of the unfortunate death of the assured.

This amount is equal to 1% of the sum assured. The income can be used to pay for

continuing the educational expenses of the child. This income may also be used to

support the family.

14. ADDITIONAL TERM ASSURANCE:This benefit enables the client to raise their cover/protection by 50% to 300% of the

basic sum assured against a nominal premium.

15. INDEXATION:

58

The plan allows indexation of basic plan premium at the rate of 5% per annum of the

previous year's premium. It is directed towards the investment portion of the plan, to

increase their cash value.