international parity conditions: purchasing power parity 44 prices and policies second edition...

TRANSCRIPT

International Parity Conditions: Purchasing Power Parity

4

Prices and Policies

Second Edition ©2001

Richard M. Levich

International Financial Markets

McGraw Hill / Irwin

4 - 2

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

4 - 3

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

4 - 4

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

4 - 5

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

4 - 6

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Overview

The Usefulness of Parity Conditions in International Financial Markets An Overview of International Parity Conditions in a

Perfect Capital Market

Purchasing Power Parity in a Perfect Capital Market The Law of One Price Absolute Purchasing Power Parity Relative Purchasing Power Parity The Real Exchange Rate and Purchasing Power Parity

4 - 7

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Overview

Relaxing the Perfect Capital Market Assumptions Transaction Costs Taxes Uncertainty

4 - 8

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Overview

Empirical Evidence on Prices and Exchange Rates Empirical Methods, or How to Test a Parity Condition Evidence on the Law of One Price Relative PPP: Evidence from Recent Quarterly Data Relative PPP: Evidence from Hyperinflationary

Economies Relative PPP: Evidence from Long-Run Data Empirical Tests of PPP: Is the Real Exchange Rate

Constant? Empirical Tests of PPP: The Final Word

4 - 9

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Overview

Policy Matters - Private Enterprises The Role of Parity Conditions for Management

Decisions Purchasing Power Parity and Managerial Decisions Purchasing Power Parity and Product Pricing

Decisions

Policy Matters - Public Policymakers

4 - 10

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

Parity conditions can be thought of as international financial “benchmarks” or “break-even values”. They are the defining points where the decision-

maker is indifferent between the two strategies summarized by the two halves of the parity relation.

Because parity conditions rely heavily on arbitrage, a violation of parity often implies that a profit opportunity or cost advantage is available to the decision-maker.

4 - 11

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

We begin our analysis of international parity conditions by assuming a perfect capital market (PCM) setting: no transaction costs no taxes complete certainty

Based on the PCM assumptions, there are four principle parity conditions in international finance, of which only three are independent.

4 - 12

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

1a. Purchasing Power ParityAbsolute Version

The price of a market basket of U.S. goods equals the price of a market basket of foreign goods when

multiplied by the exchange rate.

SpotUKUS PP

Driven by arbitrage in goods.

4 - 13

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

1b. Purchasing Power ParityRelative Version

The percentage change in the exchange rate equals the percentage change in U.S. goods prices less the

percentage change in foreign goods prices.

UKUSSpot PP

Driven by arbitrage in goods.

4 - 14

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

2. Interest Rate Parity

The forward exchange rate premium equals (approximately) the U.S. interest rate minus the foreign

interest rate.

£iiSSF $

Driven by arbitrage between the spot and forward exchange rates, and money market interest rates.

4 - 15

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

3a. Fisher ParitiesFisher Effect (Fisher Closed)

For a single economy, the nominal interest rate equals the real interest rate plus the expected rate of inflation.

US$$

~PEri

Driven by desire to insulate the real interest against expected inflation,

and arbitrage between real and nominal assets.

4 - 16

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

3b. Fisher ParitiesInternational Fisher Effect (Fisher Open)

For two economies, the U.S. interest rate minus the foreign interest rate equals the expected percentage

change in the exchange rate.

potS£

~$ Eii

Driven by arbitrage in bonds denominatedin two currencies.

4 - 17

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

The Usefulness of Parity Conditionsin International Financial Markets

4. Forward Rate Unbiased

Today’s forward premium (for delivery in n days)equals the expected percentage change in the spot rate

(over the next n days).

ttntttt SSSESSF ~

Driving force: Market players monitor the difference between today’s forward rate (for delivery in n days)

and their expectation of the future spot rate (n days from today).

4 - 18

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

Purchasing power parity (PPP) is built on the notion of arbitrage across goods markets and the Law of One Price.

The Law of One Price is the principle that in a PCM setting, homogeneous goods will sell for the same price in two markets, taking into account the exchange rate.

£/$wheatUK,wheatUS, SPP

4 - 19

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

Let PUS and PUK represent the weighted average price level for goods in the U.S. and U.K. market baskets respectively.

Absolute PPP predicts that these two price measures will be equal after adjusting for the exchange rate: PUS = S$/£ PUK

Absolute PPP requires that the consumption baskets are identical across the two countries.

4 - 20

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

Suppose absolute PPP is violated. Introduce K so that:

PUS, t +1 = K S$/£, t +1 PUK, t +1 (a)

PUS, t = K S$/£, t PUK, t (b)

pUS = s + pUK + s pUK

t

tt

t

tt

t

tt

P

PPp

P

PPp

S

SSs

UK,

UK,1 UK,UK

US,

US,1 US,US

$/£,

$/£,1 $/£, , , where

For small % changes, or when continuous rates are used, the cross-product term s pUK can be ignored.

% exchange rate = % U.S.prices – % U.K.prices

4 - 21

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

Often, we are interested in the level of the exchange rate that satisfies PPP.

The PPP spot rate reestablishes PPP relative to a base period. It is the exchange rate that would just offset the relative inflation between a pair of countries since the base period.

tt

ttttPPP PP

PPSS

(b)

(a)

UK,1 UK,

US,1 US, £,/$1,

4 - 22

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

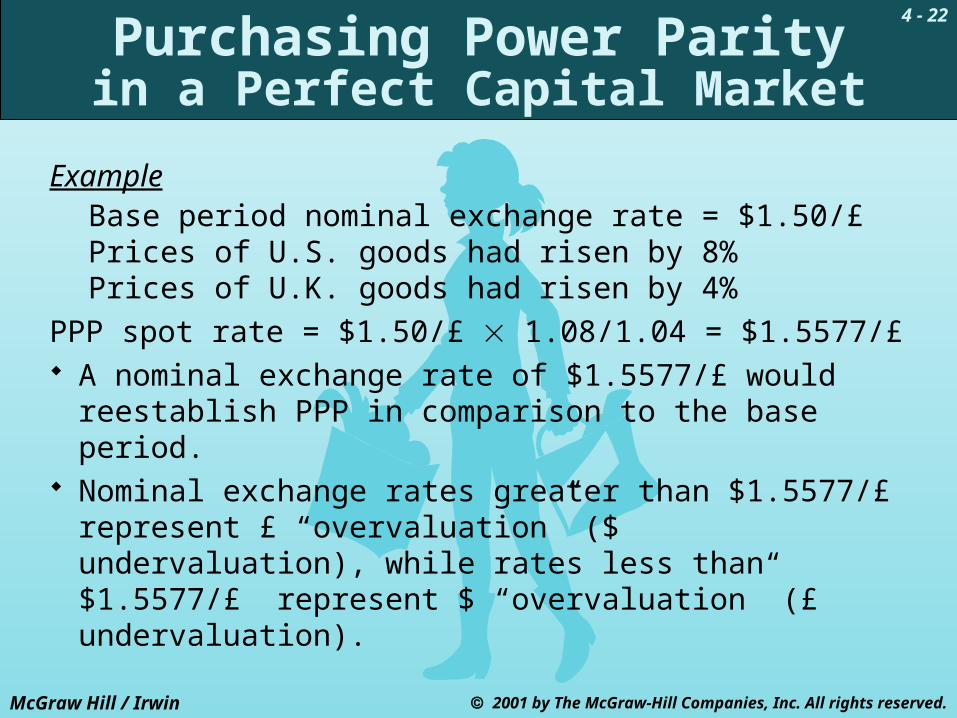

ExampleBase period nominal exchange rate = $1.50/£Prices of U.S. goods had risen by 8%Prices of U.K. goods had risen by 4%

PPP spot rate = $1.50/£ 1.08/1.04 = $1.5577/£ A nominal exchange rate of $1.5577/£ would

reestablish PPP in comparison to the base period. Nominal exchange rates greater than $1.5577/£

represent £ “overvaluation” ($ undervaluation), while rates less than $1.5577/£ represent $ “overvaluation” (£ undervaluation).

4 - 23

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

PPP conditions do not imply anything about causal linkages between prices and exchange rates or vice versa.

Both prices and exchange rates are jointly determined by other variables in the economy.

PPP is an equilibrium condition that must be satisfied when the economy is at its long-term equilibrium.

4 - 24

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

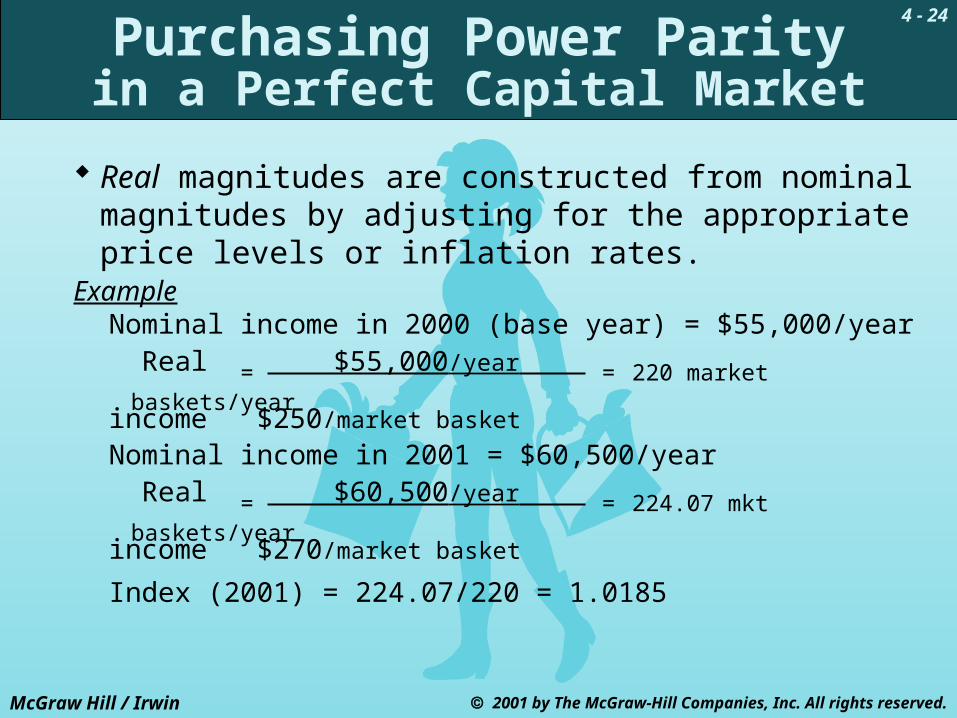

Real magnitudes are constructed from nominal magnitudes by adjusting for the appropriate price levels or inflation rates.

ExampleNominal income in 2000 (base year) = $55,000/year Real = $55,000/year = 220 market baskets/yearincome $250/market basket

Nominal income in 2001 = $60,500/year Real = $60,500/year = 224.07 mkt baskets/yearincome $270/market basket

Index (2001) = 224.07/220 = 1.0185

4 - 25

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

The real exchange rate is calculated by correcting the nominal exchange rate for the price levels in the two countries.

When absolute PPP holds:

$1.50/£ = $1,500/US good .

£ 1,000/British good LHS = 1 US good / British good RHS

When PPP holds, the real exchange rate is constant.

4 - 26

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchasing Power Parityin a Perfect Capital Market

An index of the real exchange rate is defined as:

Spot (Real, t) = Spot (Nominal, t) .

Spot (PPP, t)Example

Today’s spot exchange rate is $1.80/£PPP spot rate is $1.50/£Real exchange rate index = 1.80/1.50 = 1.20

At 1.20, the £ is “overvalued” on a PPP basis. 1.0 British good can be exchanged for 1.2 U.S. goods. So, sellers of British goods have “lost competitiveness” on international markets.

4 - 27

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Relaxing the Perfect Capital Market Assumptions

Transaction Costs Transport and menu costs lead to a neutral band

around the PPP line, within which it is not profitable to execute arbitrage transactions.

Taxes Tariffs have an effect similar to transaction costs.

Uncertainty Arbitrageurs will seek a greater profit to compensate

for risks, thus leading to a wider band around the PPP line before arbitrage becomes profitable.

4 - 28

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

A parity condition can be viewed as a 45° line passing through the origin with the LHS and RHS variables plotted on the x and y axes.

Thus, parity conditions can be tested by running the simple linear regression: LHSt = + RHSt + t

Parity holds when the data cannot reject a null hypothesis where = 0, = 1, and the error terms have classical properties.

4 - 29

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

In reality, seemingly “homogeneous” goods may differ in a number of important respects which undermine tests of the Law of One Price.

One test of the Law of One Price is the Big Mac index, which has been published annually in The Economist since 1986. It was devised as a light-hearted

guide to whether currencies are at their “correct” level, based on PPP.

4 - 30

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Isra

el

Den

mar

k

Japa

n

Swed

en

Uni

ted

Stat

es

Chi

le

Ger

man

y

Mex

ico

Spai

n

Sing

apor

e

New

Zea

land

Aus

tral

ia

Cze

ch R

ep

Sout

h A

fric

a

Pola

nd

Chi

na

Source: The Economist, April 29, 2000

Sw

itze

rlan

d

Bri

tain

Sou

th K

orea

Fra

nce

Arg

enti

na

Eur

o A

rea

Tai

wan

Ital

y

Can

ada

Indo

nesi

a

Bra

zil

Tha

ilan

d

Hon

g K

ong

Rus

sia

Hun

gary

Mal

aysi

a

Ratio of Big Mac Prices in US$ Relative to U.S. PriceU.S. Price is $2.51/Big Mac

4 - 31

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

With the rise of e-commerce, investigating the Law of One Price becomes easier and violations more puzzling. A recent Wall Street Journal article highlighted the

case of a popular book that sold for $16.20 at Amazon.com (U.S.), for $13.52 at Amazon.co.uk (Britain), and for $27.00 at Amazon.de (Germany).

4 - 32

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

To examine the relative PPP condition, we can compare the exchange rate change to the contemporaneous inflation differential:

st = + (p$ – pDM)t + t

It seems that PPP is a poor explanation of exchange-rate changes on a period-by-period basis.

However, there is a tendency for PPP to reassert itself as time passes (mean reversion).

4 - 33

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Quarterly Deviations from Relative PPPCPI: Germany and the United States, 1973-1999

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999

(US-German)Inflation

Spot Rate Changes

= 0.003 = 0.15 R2 = 0.003 N = 107 (0.007) (0.83) D–W = 1.83

% D

evia

tion

s

AverageInflation

Difference

4 - 34

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

During a hyperinflation period, even the demanding regression-style test tends to support PPP. This is due in some degree to dollarization.

Long-run data indicated that the real exchange rate did not evolve as a random walk, but demonstrated a clear tendency to revert back to its central value.

4 - 35

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

Note that the real exchange rate itself may not be constant. It may change on a permanent basis if a real shock

affected one country but not its trading partners. The Balassa-Samuelson hypothesis states that

countries that have experienced high productivity gains, higher real income growth and higher real incomes should have appreciating real exchange rates.

4 - 36

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Empirical Evidence onPrices and Exchange Rates

Empirical tests confirm that ... PPP is a poor descriptor of exchange rate behavior

in the short run, where the rates are quite volatile and domestic prices are somewhat sticky.

But in longer-run analysis, it appears that PPP offers a reasonably good guide.

4 - 37

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Policy Matters - Private Enterprises

If managers can identify the deviations from parity that are growing larger or likely to persist, then profit-maximizing decisions can be made.

Knowing that deviations from parity occur, managers may adopt strategies that reduce their exposure to the risks of such deviations.

4 - 38

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

4 - 39

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

4 - 40

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Policy Matters - Private Enterprises

In a number of instances, international price differentials in some commodities have been both large and persistent.

More interesting perhaps are the international price differentials across “branded goods” like McDonald’s Big Mac and The Economist, whose prices are set by brand managers rather than by market forces.

4 - 41

McGraw Hill / Irwin 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Policy Matters - Public Policymakers

Deviations from PPP, by definition, measure changes in a country’s international competitiveness, and reveal whether a currency is overvalued or undervalued relative to a simple standard.

However, there are limitations on the usefulness of PPP in policy decisions, as real macroeconomic disturbances call for a change in the real exchange rate.