international builders show january 13, 2010 builders show january 13, ... •quarterly survey of...

TRANSCRIPT

55+ Economic & Market Forecast

International Builders Show

January 13, 2010

• Paul Emrath

• VP-Survey and Housing Policy Research

Outline

• NAHB 55+ HMI & other survey results

• Financing 55+ housing

• NAHB housing/house price forecast

• 55+ housing forecast

55+ Housing Market Index (HMI) Survey

• Quarterly survey of 55+ builders

• Patterned after survey for the NAHB/Wells Fargo HMI, successfully conducted since the mid-1980s

• Asks builders to rate markets as “good”, “fair” or “poor”

• Results used to create summary indexes

– Scale of 0 to 100

– 50 means “GOOD” = “POOR”

– Can includes special questions (e.g., on sales incentives )

NAHB 55+ HMI Survey:

New 55+ Single Family Home Sales

Source: 55+ Housing Market Index, 4th Qtr. 2010 and

Builders’ Economic Council (BEC) survey, Nov 2010, NAHB EcHp.

Note: Only numbers from the BEC survey (the last column) are seasonally adjusted

55+ HMI Survey Survey of

all SF

Builders

Dec 2010

2009 2010

Q4 Q1 Q2 Q3 Q4 (P)

55+ Single-Family HMI 17 19 12 15 14 16

Components:

Present Sales 17 17 12 15 14 16

Expected Next 6 Months 29 30 17 24 24 25

Traffic 12 18 12 11 10 11

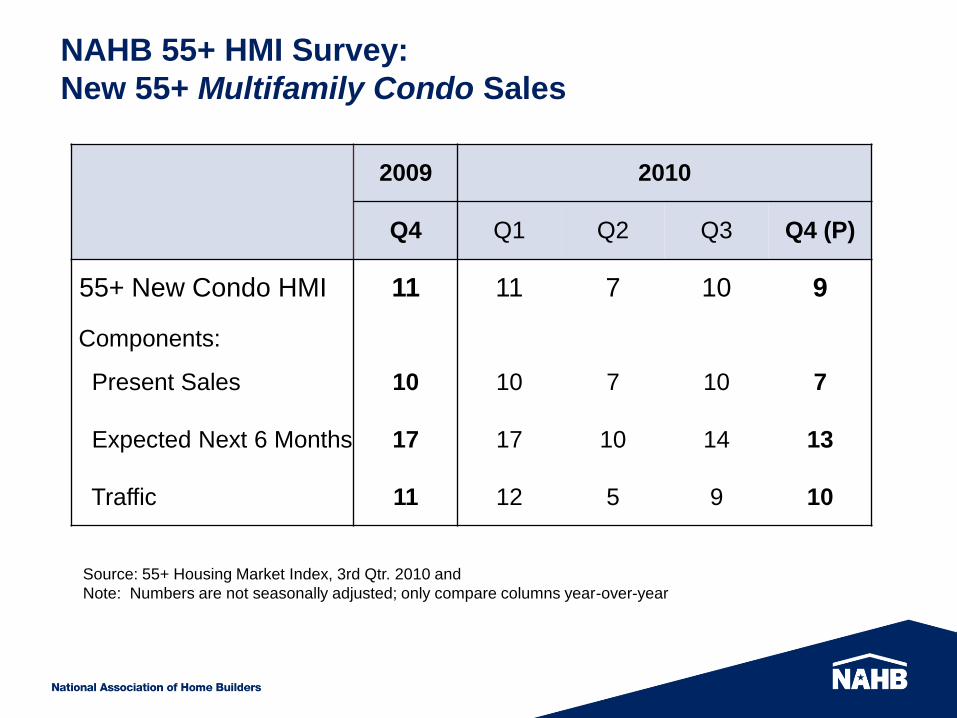

NAHB 55+ HMI Survey:

New 55+ Multifamily Condo Sales

Source: 55+ Housing Market Index, 3rd Qtr. 2010 and

Note: Numbers are not seasonally adjusted; only compare columns year-over-year

2009 2010

Q4 Q1 Q2 Q3 Q4 (P)

55+ New Condo HMI 11 11 7 10 9

Components:

Present Sales 10 10 7 10 7

Expected Next 6 Months 17 17 10 14 13

Traffic 11 12 5 9 10

NAHB 55+ HMI Survey:

Multifamily Rental Apartments

Source: 55+ Housing Market Index, 3rd Qtr. 2010 and

Note: Numbers are not seasonally adjusted; only compare columns year-over-year

2009 2010

Q4 Q1 Q2 Q3 Q4(P)

Production of New 55+ Rental Apartments:

Present Production 16 13 15 14 17

Expected Next 6 Months 18 19 16 16 23

Demand for Existing 55+ Rental Apartments:

Present Demand 26 28 31 28 28

Expected Next 6 Months 30 34 30 32 32

Sales incentives/premiums used to promote

55+ housing developments

Source: 55+ Housing Market Index Special Questions, 3rd Qtr. 2009, NAHB EcHp.

33%

15%

3%

5%

15%

34%

49%

None of the above

Other

Trips

Discounts on outside services

Prepaid homeowner fee (e.g. one year)

A free option package (e.g. 3rd bathroom)

Free upgrades package (e.g. premium carpeting, upgraded appliances)

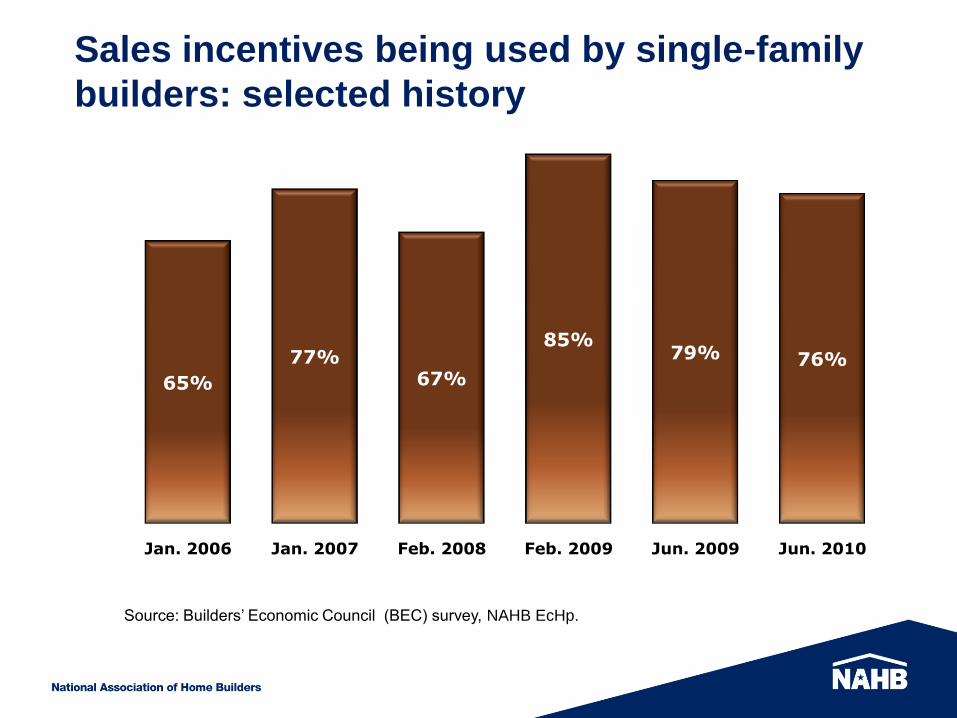

Sales incentives being used by single-family

builders: selected history

Source: Builders’ Economic Council (BEC) survey, NAHB EcHp.

65%

77%67%

85%79% 76%

Jan. 2006 Jan. 2007 Feb. 2008 Feb. 2009 Jun. 2009 Jun. 2010

Incentives marketed as a substitute for the

Expired Home Buyers Tax Credit?(Of those who report using incentives)

Source: Builders’ Economic Council (BEC) survey, June 2010, NAHB EcHp.

Yes

19%No

81%

Reasons for Not Using Special Sales Incentives

19%

6%

18%

41%

50%

Other

Market now strong enough, incentives not needed

Don't think incentives work in my market area

Have tried incentives, but they were ineffective

Cannot afford to offer incentives due to rising

construction costs

Source: Builders’ Economic Council (BEC) survey, June 2010, NAHB EcHp.

Financing of 55+ Housing

• New construction: financing for acquisition, development & construction

– Many challenges, need to be innovative

– 55+ similar to other markets

• Sales of existing homes: mortgages

– Problems of financial turmoil, declining prices

– 55+ markets may be different

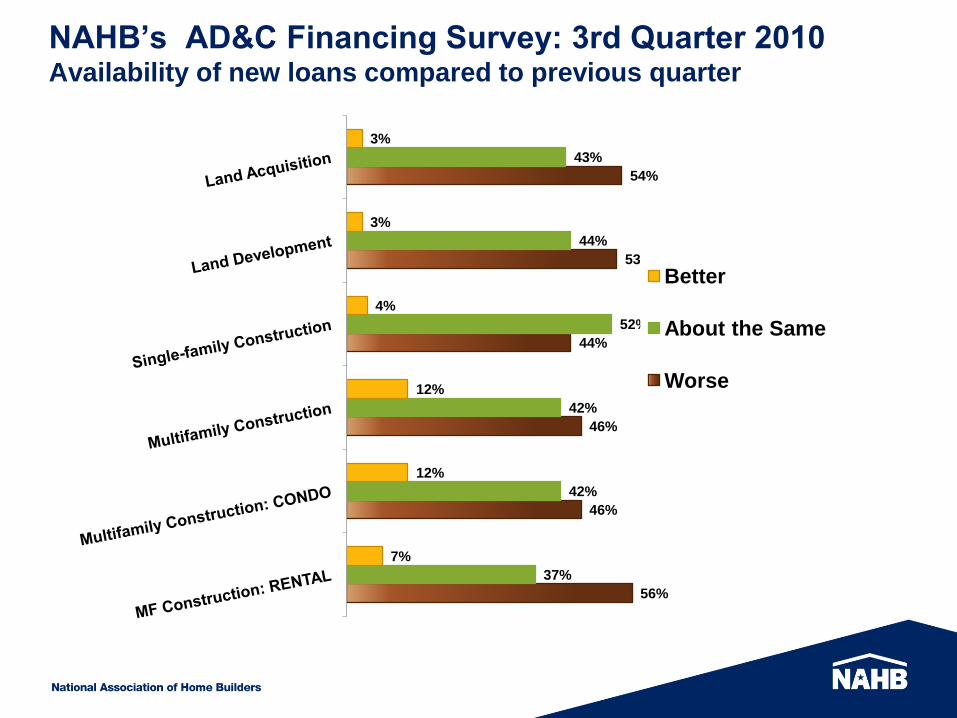

NAHB’s AD&C Financing Survey: 3rd Quarter 2010Availability of new loans compared to previous quarter

56%

46%

46%

44%

53%

54%

37%

42%

42%

52%

44%

43%

7%

12%

12%

4%

3%

3%

Better

About the Same

Worse

AD&C Financing Survey: Availability of Loans Last 4 Quarters

Land Acquisition

Better 3% 2% 5% 4%

Worse 54% 55% 64% 66%

Land Development

Better 3% 4% 5% 4%

Worse 53% 61% 70% 62%

Single-family Construction

Better 4% 6% 5% 2%

Worse 44% 48% 48% 58%

Multifamily Construction

Better 12% 8% 12% 3%

Worse 46% 63% 65% 79%

Multifamily Construction: CONDO

Better 12% 8% 12% 3%

Worse 46% 63% 65% 79%

Multifamily Construction: RENTAL

Better 7% 7% 0% 8%

Worse 56% 45% 81% 64%

AD&C

Q110

AD&C

Q409

AD&C

Q210

AD&C

Q310

60%

67%

70%

71%

78%

Lenders are increasing documentation requirements

Lenders are requiring personal guarantees or collateral not related to

the project

Lenders are reducing amount willing to lend

Lenders are lowering the allowable LTV (or loan-to-cost) ratio

Lenders are not making new loans

AD&C Financing Survey: 3rd Quarter 2010 Nature of changes for the worse

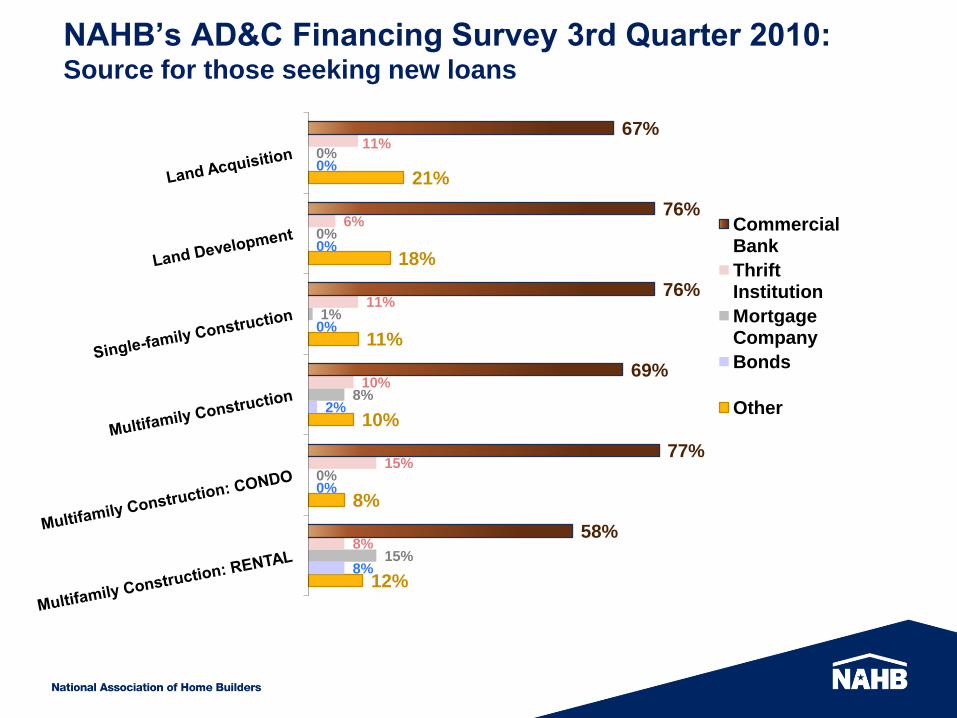

NAHB’s AD&C Financing Survey 3rd Quarter 2010:Source for those seeking new loans

12%

8%

10%

11%

18%

21%

8%

0%

2%

0%

0%

0%

15%

0%

8%

1%

0%

0%

8%

15%

10%

11%

6%

11%

58%

77%

69%

76%

76%

67%

Commercial Bank

Thrift Institution

Mortgage Company

Bonds

Other

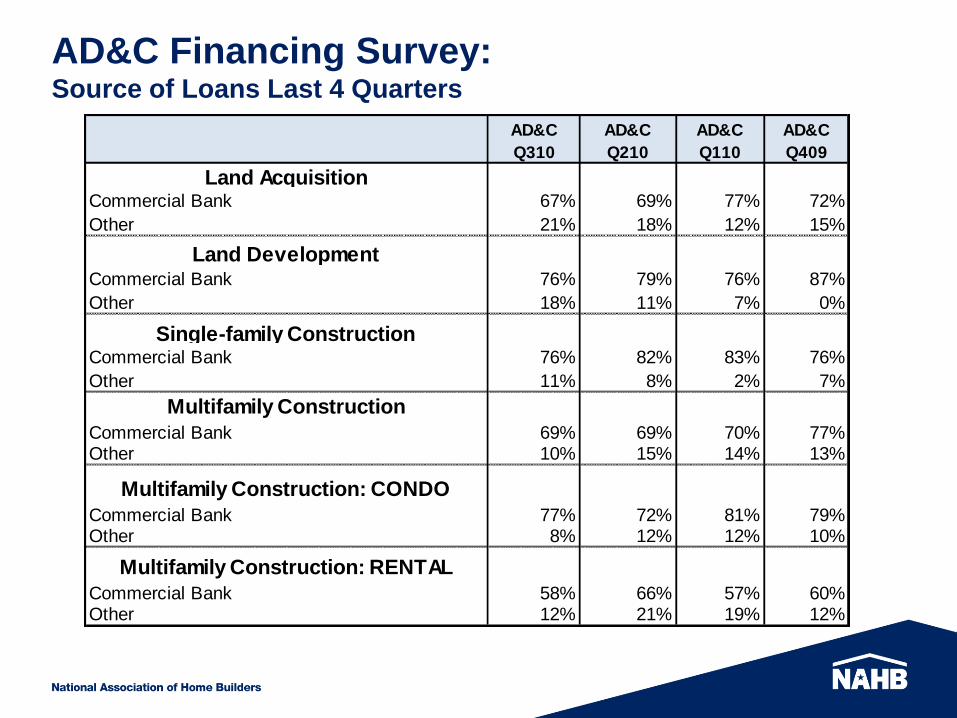

AD&C Financing Survey: Source of Loans Last 4 Quarters

Land AcquisitionCommercial Bank 67% 69% 77% 72%

Other 21% 18% 12% 15%

Land DevelopmentCommercial Bank 76% 79% 76% 87%

Other 18% 11% 7% 0%

Single-family ConstructionCommercial Bank 76% 82% 83% 76%

Other 11% 8% 2% 7%

Multifamily Construction

Commercial Bank 69% 69% 70% 77%Other 10% 15% 14% 13%

Multifamily Construction: CONDO

Commercial Bank 77% 72% 81% 79%Other 8% 12% 12% 10%

Multifamily Construction: RENTAL

Commercial Bank 58% 66% 57% 60%Other 12% 21% 19% 12%

AD&C

Q409

AD&C

Q310

AD&C

Q110

AD&C

Q210

AD&C Financing Sessions at 2011 IBS(All in Orange County Convention Center)

• Securing Investors and Lenders for Land Developers Friday, January 14, 3:30-5:00 pm West 304 C-D

• Age-Restricted Rental Housing: Obtaining Financing in Today's Market Saturday, January 15, 10:00 - 11:30 am West 314 B

• Surviving Lender Action Saturday, January 15, 10:00-11:30 am West 308 A-B

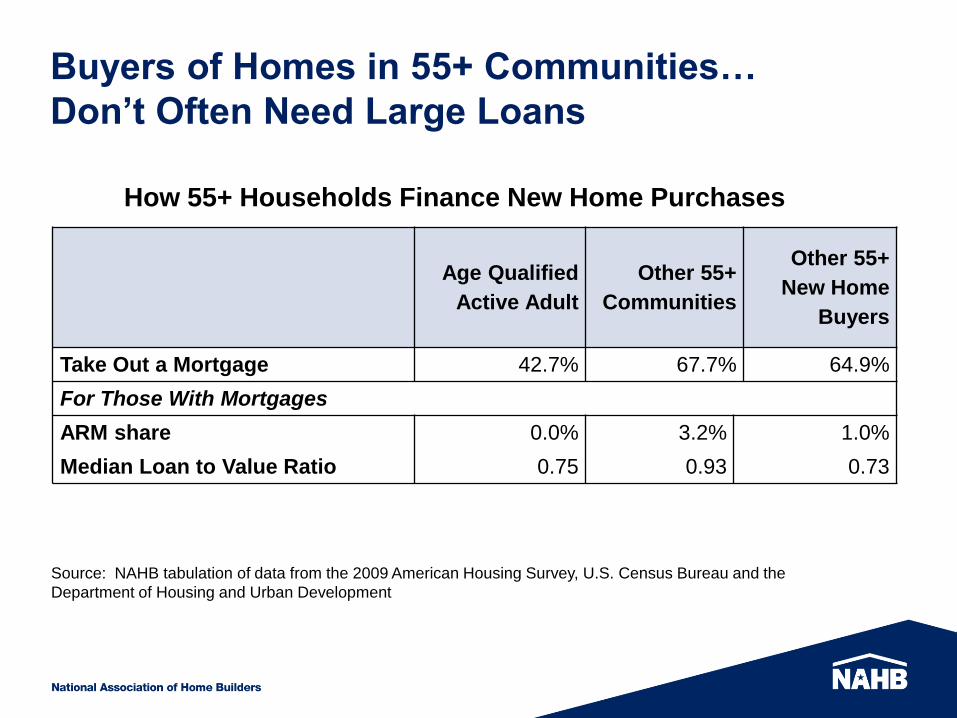

Buyers of Homes in 55+ Communities…

Don’t Often Need Large Loans

Age Qualified

Active Adult

Other 55+

Communities

Other 55+

New Home

Buyers

Take Out a Mortgage 42.7% 67.7% 64.9%

For Those With Mortgages

ARM share 0.0% 3.2% 1.0%

Median Loan to Value Ratio 0.75 0.93 0.73

How 55+ Households Finance New Home Purchases

Source: NAHB tabulation of data from the 2009 American Housing Survey, U.S. Census Bureau and the

Department of Housing and Urban Development

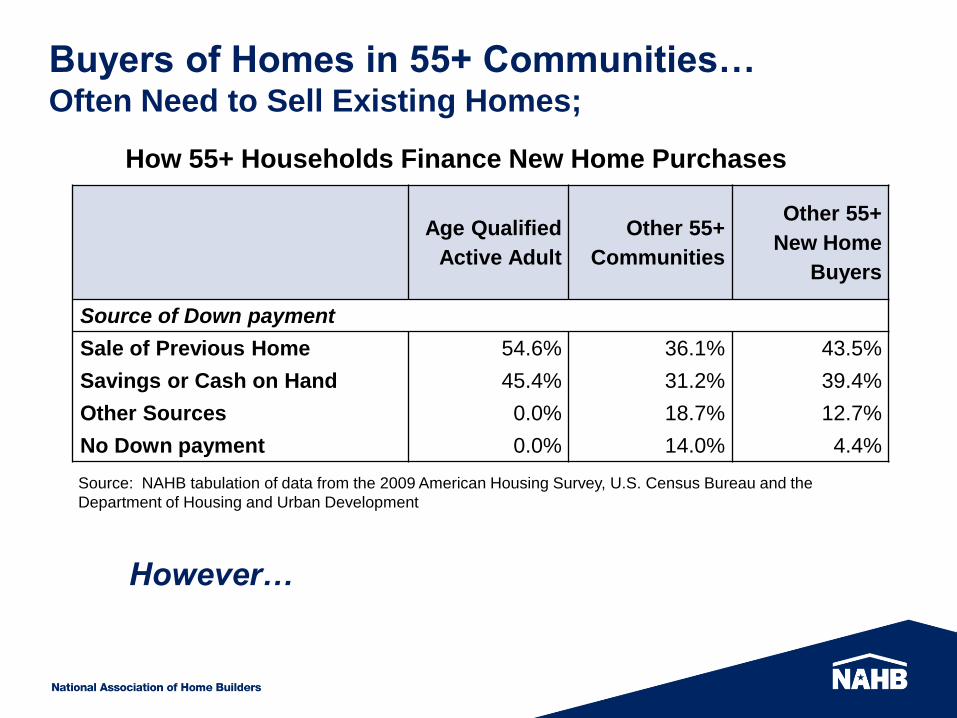

Buyers of Homes in 55+ Communities…Often Need to Sell Existing Homes;

Age Qualified

Active Adult

Other 55+

Communities

Other 55+

New Home

Buyers

Source of Down payment

Sale of Previous Home 54.6% 36.1% 43.5%

Savings or Cash on Hand 45.4% 31.2% 39.4%

Other Sources 0.0% 18.7% 12.7%

No Down payment 0.0% 14.0% 4.4%

How 55+ Households Finance New Home Purchases

Source: NAHB tabulation of data from the 2009 American Housing Survey, U.S. Census Bureau and the

Department of Housing and Urban Development

However…

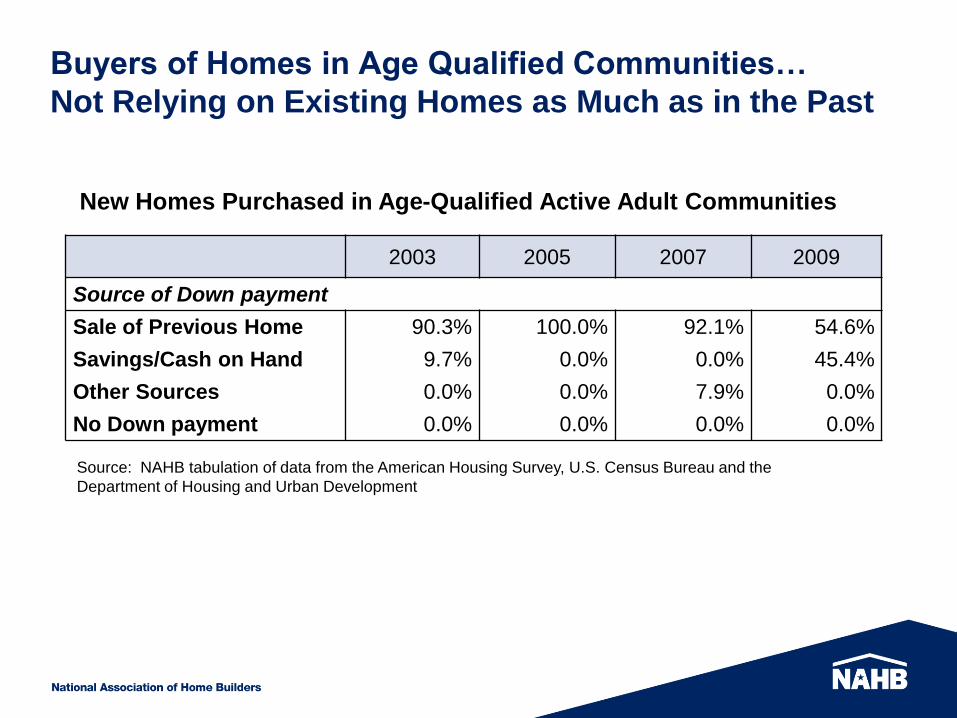

Buyers of Homes in Age Qualified Communities…

Not Relying on Existing Homes as Much as in the Past

2003 2005 2007 2009

Source of Down payment

Sale of Previous Home 90.3% 100.0% 92.1% 54.6%

Savings/Cash on Hand 9.7% 0.0% 0.0% 45.4%

Other Sources 0.0% 0.0% 7.9% 0.0%

No Down payment 0.0% 0.0% 0.0% 0.0%

New Homes Purchased in Age-Qualified Active Adult Communities

Source: NAHB tabulation of data from the American Housing Survey, U.S. Census Bureau and the

Department of Housing and Urban Development

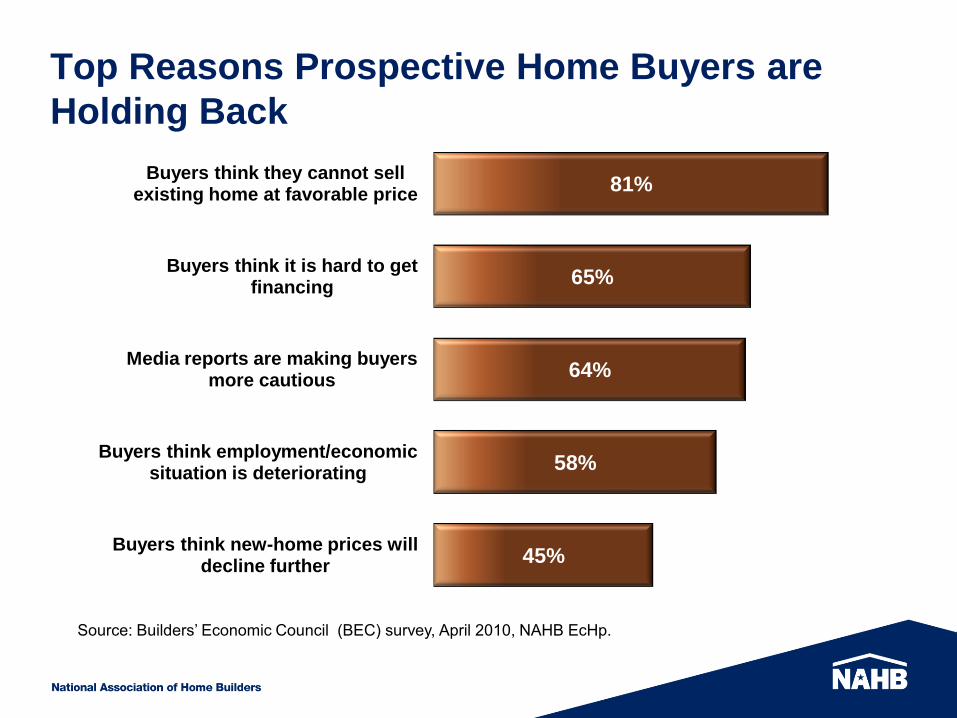

Top Reasons Prospective Home Buyers are

Holding Back

45%

58%

64%

65%

81%

Buyers think new-home prices will decline further

Buyers think employment/economic situation is deteriorating

Media reports are making buyers more cautious

Buyers think it is hard to get financing

Buyers think they cannot sell existing home at favorable price

Source: Builders’ Economic Council (BEC) survey, April 2010, NAHB EcHp.

NAHB Forecast

• GDP Growth

• Employment

• House Prices

• Sales & Starts

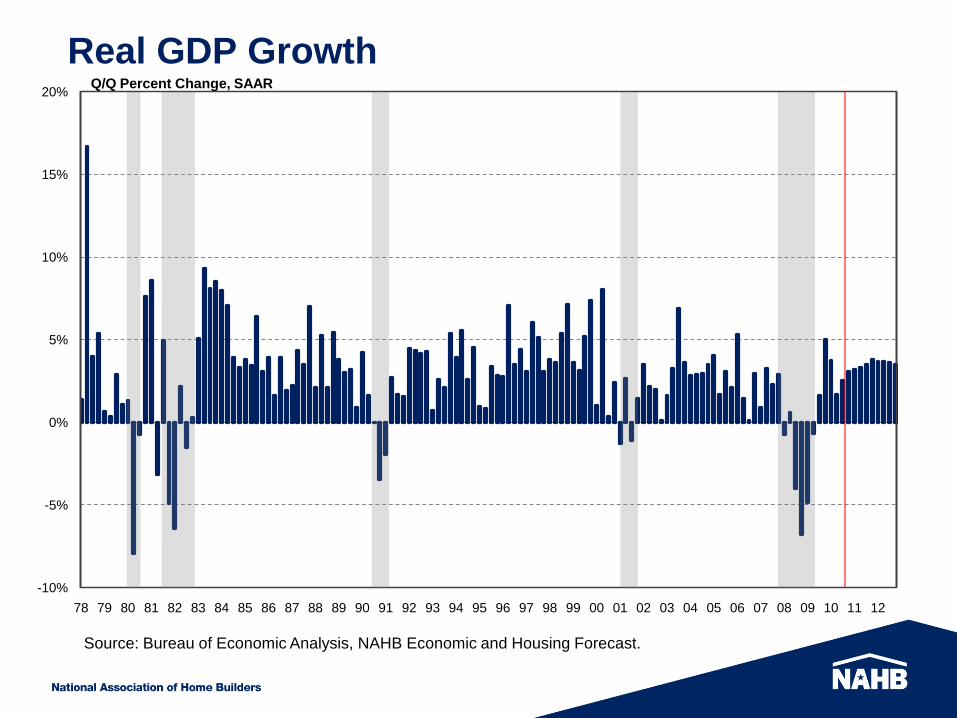

Real GDP Growth

-10%

-5%

0%

5%

10%

15%

20%

78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Q/Q Percent Change, SAAR

Source: Bureau of Economic Analysis, NAHB Economic and Housing Forecast.

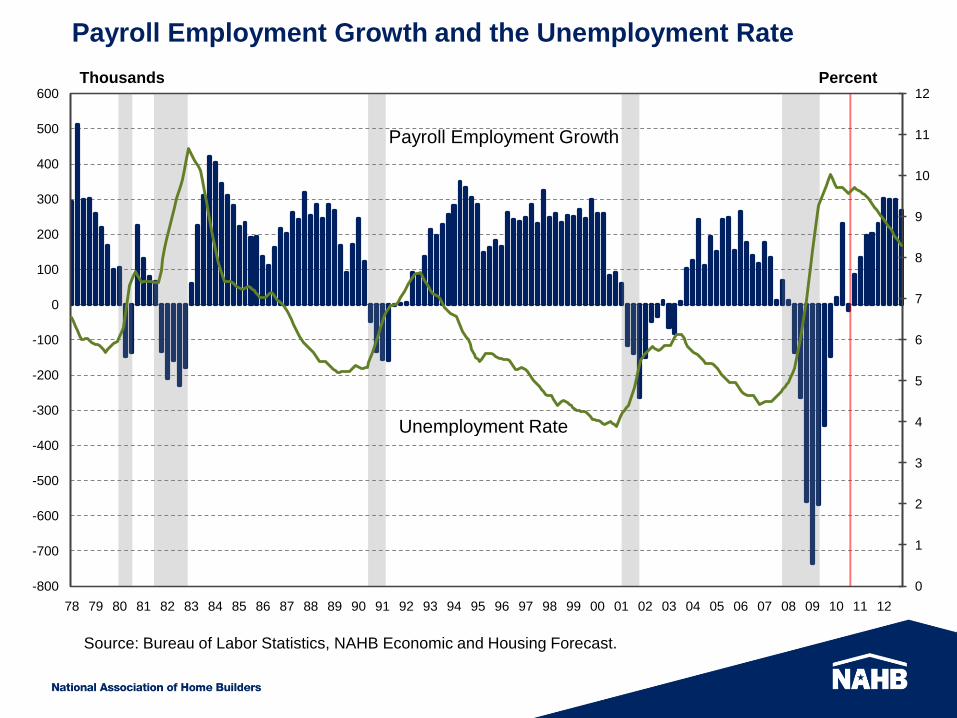

Payroll Employment Growth and the Unemployment Rate

0

1

2

3

4

5

6

7

8

9

10

11

12

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

500

600

78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Payroll Employment Growth

Unemployment Rate

PercentThousands

Source: Bureau of Labor Statistics, NAHB Economic and Housing Forecast.

Measures of House Prices

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

0

20

40

60

80

100

120

140

160

180

200

Case-Shiller

FHFA

NAR

Flow of Funds

2000Q1 = 100

Sources: National Association of Realtors, Federal, Reserve Board, S&P Case-Shiller, FHFA

NAHB Economic and Housing Forecast.

US Housing Market Conditions

Prices and Income – Current and Trend

0

50

100

150

200

250

300

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0Median House Price / Median Income Income and Prices, Thousands

House Price

Price / Income

Income

3.2

4.7

Source: US Census Bureau, National Association of Realtors

House Prices and Income – Trend, Peak and Current

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

220%

240%

U

S

M

I

U

T

W

Y

N

V

A

L

G

A

O

H

S

D

I

D

I

N

A

R

M

T

N

H

I

L

A

Z

C

T

N

M

A

K

C

O

K

S

K

Y

M

O

V

T

N

E

M

N

C

A

T

X

T

N

F

L

W

V

I

A

P

A

M

S

O

K

N

D

R

I

W

I

O

R

M

E

V

A

M

A

N

C

S

C

W

A

N

Y

D

C

D

E

L

A

N

J

H

I

M

D

Percentage of Historical Trend

Source: US Census Bureau, National Association of Realtors

FLCANV

AZ

Median Value of New Homes Purchased by

55+ Buyers

2005 2007 200905-07

change

In Age-Qualified Active Adult

Communities $320,000 $300,000 $300,000 -6.3%

In Other Communities Occupied

Mostly by 55+ Residents$300,000 $274,000 $255,000 -15.0%

In Ordinary (Non-55+)

Communities$258,000 $280,000 $239,000 -7.4%

S&P/Case-Shiller® U.S. National

Home Price Index166 135 134 -19.4%

Source: NAHB tabulation of data from the American Housing Survey, U.S. Census Bureau and the

Department of Housing and Urban Development; Standard & Poor’s

0

1

2

3

4

5

6

7

8

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

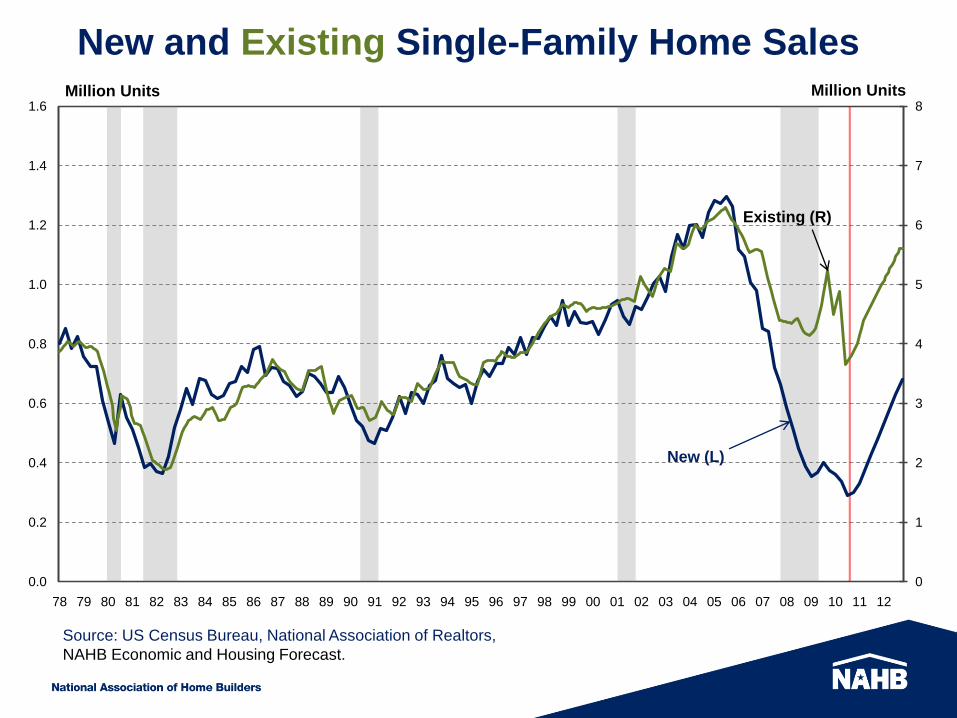

78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Million Units

Existing (R)

New (L)

Million Units

New and Existing Single-Family Home Sales

Source: US Census Bureau, National Association of Realtors,

NAHB Economic and Housing Forecast.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Million Units, SAAR

Single-Family Housing Starts

Source: US Census Bureau, NAHB Economic and Housing Forecast.

0

50

100

150

200

250

300

350

400

450

500

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Thousands of Units, SAAR

Multifamily Housing Starts

Source: US Census Bureau, NAHB Economic and Housing Forecast.

55+ Housing Projections

Based on….

• Historic market shares (from HUD/Census

American Housing Survey)

•NAHB’s overall housing forecast

•Adjust for factors specific to 55+ market

55+ Households as a Share of

the Total Housing Market

Total

In Age-

Qualified

Communities

In Other

Communities

Occupied

Mostly by 55+

All Recent Movers 14.0% 2.1% 2.6%

Movers into Rental Units 11.9% 2.3% 1.9%

Home Buyers: 18.5% 1.5% 4.1%

Existing Home Buyers 18.0% 1.4% 4.5%

New Home Buyers: 21.3% 2.3% 2.2%

New For-sale Home Buyers 20.1% 2.8% 1.9%

New Custom Home Buyers 24.4% 0.7% 3.0%

Source: NAHB tabulation of data from the 2009 American Housing Survey,

U.S. Census Bureau and the Department of Housing and Urban Development

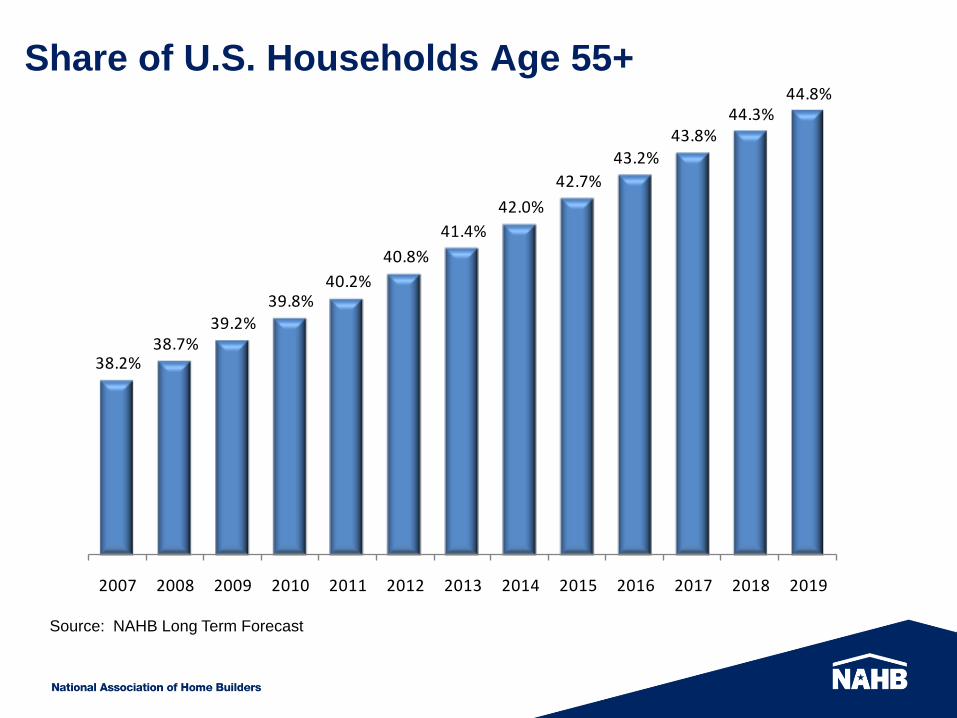

38.2%38.7%

39.2%39.8%

40.2%

40.8%

41.4%

42.0%

42.7%

43.2%43.8%

44.3%44.8%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Share of U.S. Households Age 55+

Source: NAHB Long Term Forecast

Homeownership Rate by Age

16.3%

44.7%

64.7%

73.7%77.9% 80.2% 81.3% 78.9%

68.7%

15-24 25-34 35-44 45-54 55-59 60-64 65-74 75-84 85+

Source: NAHB tabulation of data from the 2008 American Community Survey, U.S. Census Bureau.

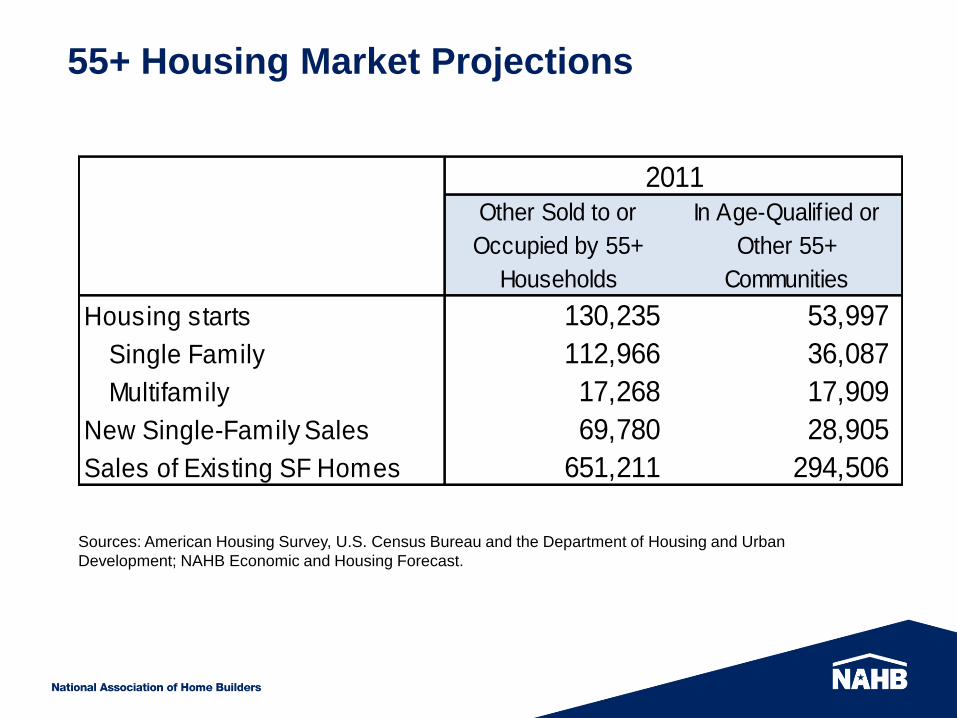

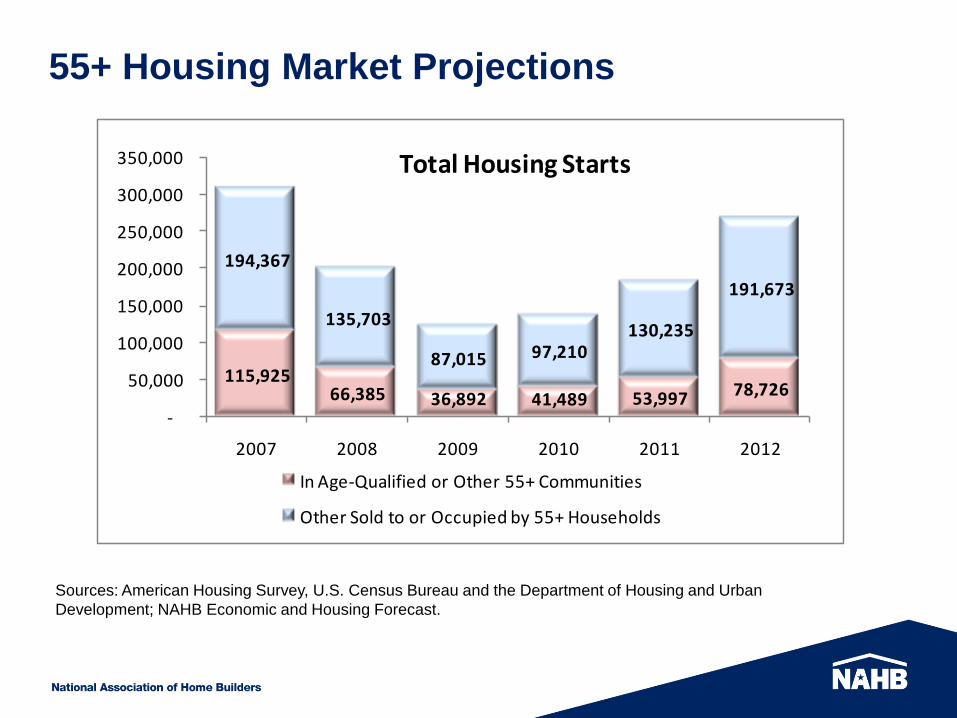

55+ Housing Market Projections

Sources: American Housing Survey, U.S. Census Bureau and the Department of Housing and Urban

Development; NAHB Economic and Housing Forecast.

Other Sold to or

Occupied by 55+

Households

In Age-Qualif ied or

Other 55+

Communities

Housing starts 130,235 53,997

Single Family 112,966 36,087

Multifamily 17,268 17,909

New Single-Family Sales 69,780 28,905

Sales of Existing SF Homes 651,211 294,506

2011

55+ Housing Market Projections

Sources: American Housing Survey, U.S. Census Bureau and the Department of Housing and Urban

Development; NAHB Economic and Housing Forecast.

115,925 66,385 36,892 41,489 53,997 78,726

194,367

135,703

87,015 97,210 130,235

191,673

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2007 2008 2009 2010 2011 2012

In Age-Qualified or Other 55+ Communities

Other Sold to or Occupied by 55+ Households

Total Housing Starts

55+ Housing Market Projections

Sources: American Housing Survey, U.S. Census Bureau and the Department of Housing and Urban

Development; NAHB Economic and Housing Forecast.

78,613 33,097 23,749 26,409 36,087 53,442

157,330

103,606

74,342 82,670

112,966

167,294

-

50,000

100,000

150,000

200,000

250,000

2007 2008 2009 2010 2011 2012

Single-Family Housing Starts

In Age-Qualified or Other 55+ Communities

Other Sold to or Occupied by 55+ Households

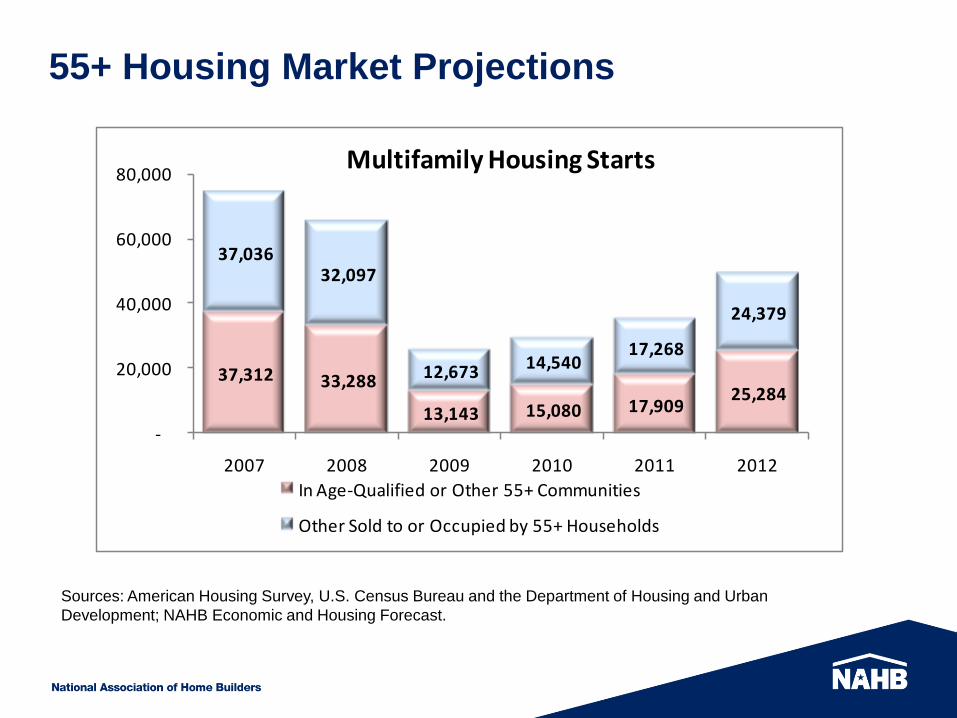

55+ Housing Market Projections

Sources: American Housing Survey, U.S. Census Bureau and the Department of Housing and Urban

Development; NAHB Economic and Housing Forecast.

37,312 33,288

13,143 15,080 17,909 25,284

37,036 32,097

12,673 14,540 17,268

24,379

-

20,000

40,000

60,000

80,000

2007 2008 2009 2010 2011 2012

Multifamily Housing Starts

In Age-Qualified or Other 55+ Communities

Other Sold to or Occupied by 55+ Households

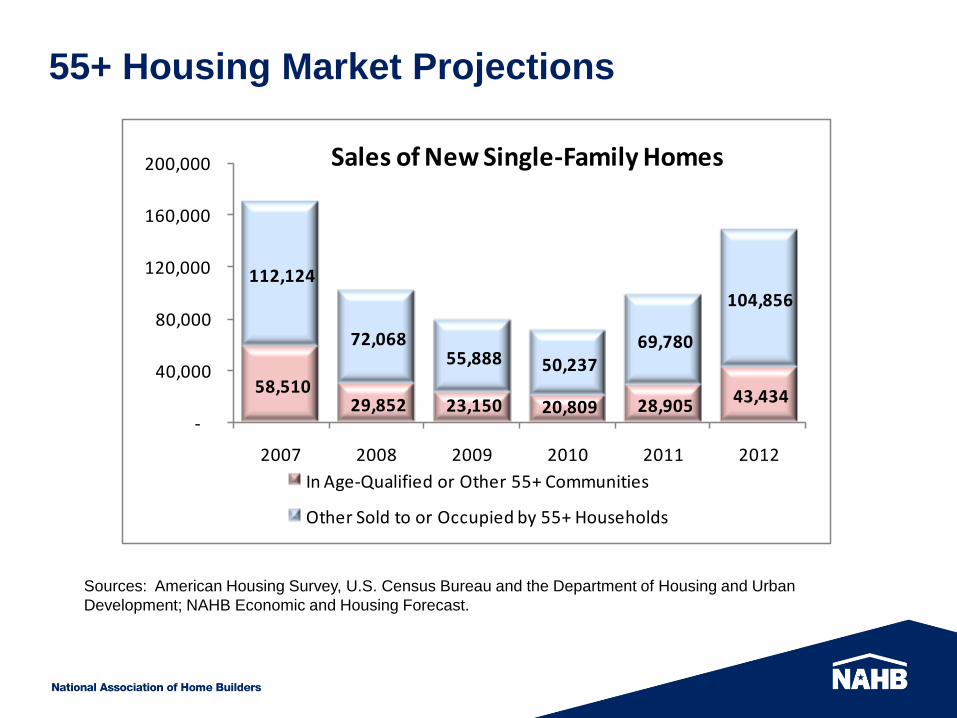

55+ Housing Market Projections

Sources: American Housing Survey, U.S. Census Bureau and the Department of Housing and Urban

Development; NAHB Economic and Housing Forecast.

58,510 29,852 23,150 20,809 28,905 43,434

112,124

72,068 55,888 50,237

69,780

104,856

-

40,000

80,000

120,000

160,000

200,000

2007 2008 2009 2010 2011 2012

Sales of New Single-Family Homes

In Age-Qualified or Other 55+ Communities

Other Sold to or Occupied by 55+ Households

55+ Housing Market Projections

Sources: American Housing Survey, U.S. Census Bureau and the Department of Housing and Urban

Development; NAHB Economic and Housing Forecast.

267 244 256 247 295 346

631 539 567 545

651 764

-

200

400

600

800

1,000

1,200

2007 2008 2009 2010 2011 2012

Tho

usa

nd

s

Sales of Existing Single-Family Homes

In Age-Qualified or Other 55+ Communities

Other Sold to or Occupied by 55+ Households

This presentation is available on the internet:

www.buildersshow.com/education

Contact

Paul Emrath

VP-Survey and Housing Policy Research

NAHB Economics and Housing Policy Group

1-800-368-5242 x8449

Thank You