international assignment servicesias.deloitte.com.au/downloads/ias_tax_issues_fn.pdfcommencement of...

TRANSCRIPT

Australian Taxation of Foreign Nationals

I N T E R N AT I O N A L A S S I G N M E N T S E R V I C E S

4

Table of Contents

Introduction 7

1. Will I have to pay tax in Australia during my assignment? 8

1.1 The Australian tax system 8

2. Will I be an Australian tax resident during my assignment? 9

2.1 Residence for Australian tax purposes 9

2.2 Dual residence 10

3. Taxation of residents 11

3.1 General principles 11

3.2 Calculation of taxable income 11

3.3 Assessable income 12

3.3.1 Employment income 12

3.3.2 Capital gains 13

3.3.3 Dividend income 15

3.3.4 Other income 16

3.3.5 Employee share plans 16

3.3.6 Attributable income of CFCs & FIFs 18

3.4 Allowable deductions 19

3.5 Foreign tax credit system 20

3.5.1 Rental income 21

3.5.2 Dividend income 22

3.5.3 Interest income 22

3.6 Offsets 23

3.6.1 Dependant offsets 23

3.6.2 Medical expenses offset 23

3.6.3 Parenting allowance 23

4. Taxation of non-residents 24

4.1 General principles 24

4.2 Calculation of taxable income 24

4.3 Assessable income 24

4.3.1 Employment income 24

4.3.2 Capital gains 25

4.3.3 Passive income 25

4.4 Allowable deductions 26

5. Lodgment and payment procedures 27

5.1 Will I have to lodge a return? 27

5.2 When will I have to lodge a return? 27

5.3 Assessment procedure 28

5.4 Collection of tax at source 28

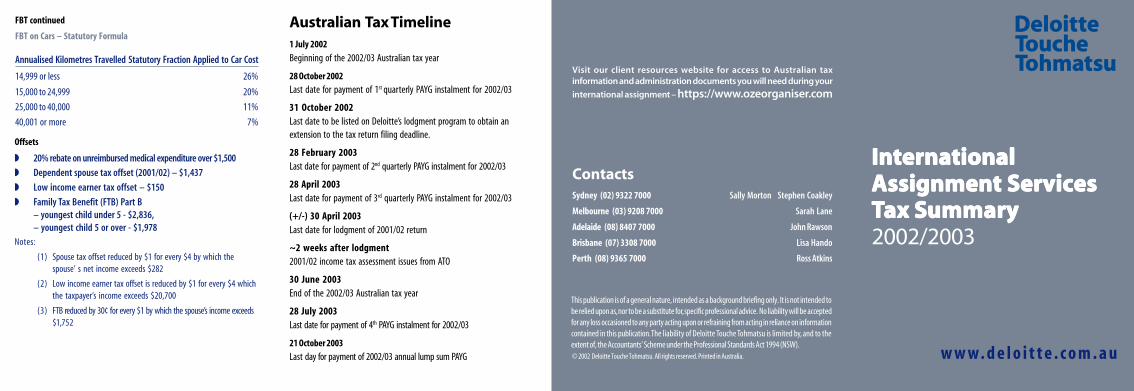

5.5 PAYG Instalments 28

5.6 Amendment and objection process 30

5.7 Private rulings 30

5.8 Tax file number 30

6. Procedures and tax consequences on departing Australia 31

6.1 General principles 31

6.2 Capital gains tax 31

6.3 Deferral of income and capital gains 32

7. Fringe Benefits Tax 33

7.1 Assessable income or fringe benefit 33

7.2 Rate of tax 33

7.3 FBT returns 34

7.4 Treatment of specific items of remuneration 34

8. Other taxes 37

8.1 Payroll tax 37

8.2 Property taxes 37

8.3 Stamp duty 37

8.4 Superannuation guarantee charge 37

8.5 Interest Withholding Tax (“IWT”) 38

8.6 Other taxes 38

9. Business visas and work permits 39

9.1 Short Stay Business Visas 39

(Subclass 456 and Electronic Travel Authorities)

9.2 Long Stay Business Visas (Subclass 457) 40

5

10. Social security and retirement benefits 41

10.1 Health system 41

10.2 Australian superannuation and termination benefits 42

10.2.1 Superannuation contributions 42

10.2.2 Withdrawal of benefits 44

10.3 Foreign superannuation and termination benefits 45

10.3.1 Payments relating to a period when you were 45

a non-resident of Australia

10.3.2 Transfer of benefit from an overseas fund 45

to another fund

10.4 Other social security benefits 46

11. Double tax treaties and tax havens 47

11.1 Basic principles of double tax treaties 47

11.2 Tax havens 47

12. Tax planning 48

12.1 Structure of remuneration package 48

12.2 Timing issues 48

12.3 Deferring certain actions until after departure 49

12.4 Other planning 49

13. Other considerations 50

13.1 Exchange control 50

13.2 Purchase of Australian real estate 50

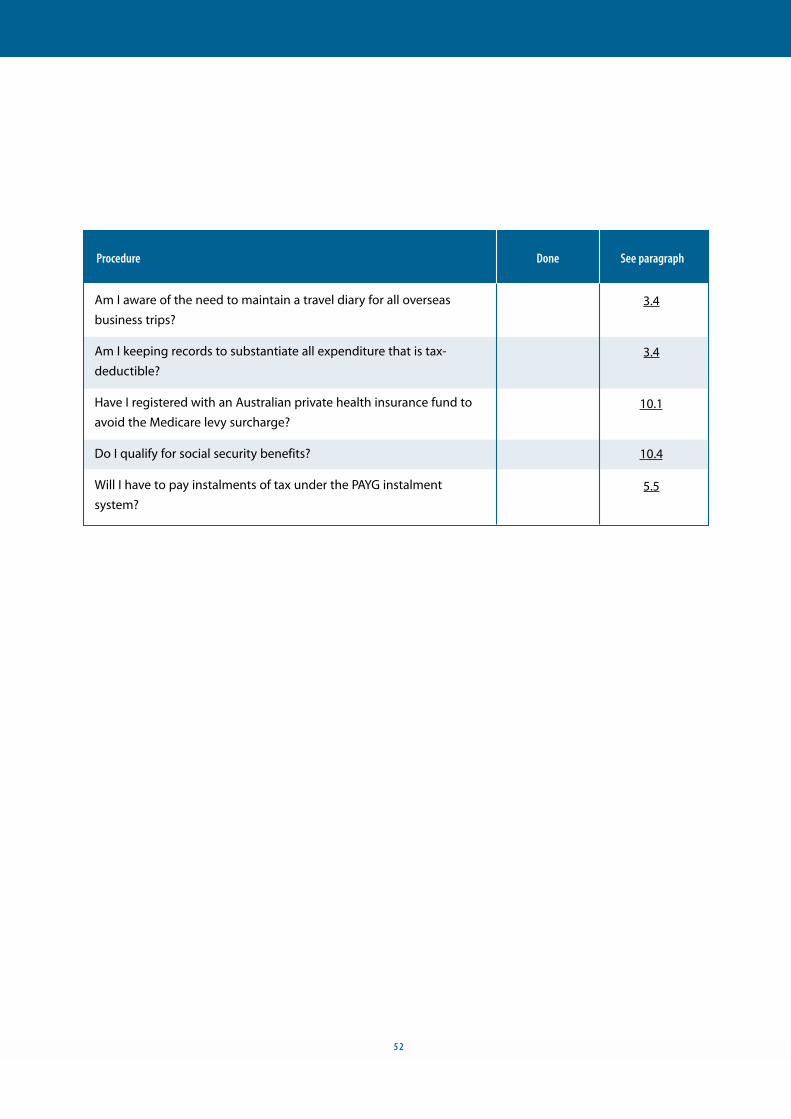

Appendix A 51

Checklist of procedures in year of arrival 51

6

Introduction

This booklet is designed to provide you with an understanding of the Australian

tax implications of undertaking employment in Australia. It combines a general

explanation of the law as at August 2002 with an overview of the tax issues that

you need to consider in preparing for, and during the course of, your Australian

assignment.

Note that all tax rates are contained in a separate brochure. Click on the links to

go directly to the relevant brochure.

We know that having relocated to Australia, you have many issues to consider.

This booklet cannot be an exhaustive tax analysis but serves as an introduction to

give non-tax experts quick access to the important tax considerations involved in

relocating to Australia.

Tax planning is critical to the success of any overseas assignment. It is important

to address the tax issues in both Australia and your home country prior to the

commencement of the assignment. With proper planning, you and your

employer can minimise your tax liabilities and avoid potential pitfalls.

Deloitte Touche Tohmatsu International Assignment Services tax specialists can

assist with assignment tax planning. With tax specialists in our offices

throughout the world we can advise you on both Australian and foreign tax

issues. In addition, we can assist you with projections of the total remuneration,

tax and relocation costs for your Australian assignment.

At the time of publication of this booklet, the Australian Government is

contemplating substantial income taxation changes as a result of the Review of

Business Taxation undertaken in July 1999. Some of the RBT recommendations

specifically address the taxation of foreign nationals working temporarily in

Australia.

Legislation was introduced into parliament earlier this year which sought to

reduce the tax burden on temporary residents by removing tax on most sources

of foreign income and capital gains, as of 1 July 2002. Although the bill was

rejected by the opposition parties, the government has indicated that it plans to

push ahead with these tax reforms. Please refer to our website for articles and

updates in relation to tax reform and other issues.

Please note, the information and analysis in this booklet are not a substitute for

competent professional advice. While every effort has been made to ensure that

the text is correct, we cannot assume any legal responsibility for the accuracy of

any particular statement. No action should be initiated without consulting your

professional advisors. If you require further information regarding the matters

dealt with in this booklet, please contact any of our offices. A list, with telephone

numbers is on a the back cover of this publication.

7

1. Will I have to pay tax in Australia during my

assignment?

1.1 The Australian tax system

Generally speaking, you are taxed on your income in the year that you

receive it. You will be taxed differently depending on whether you are

a resident or a non-resident for tax purposes. The Australian tax year

for individuals ends on 30 June and each individual liable to tax must

file a separate tax return.

Residents of Australia (refer 2.1) are subject to tax on gross income

from worldwide sources. However, if foreign tax is payable on income

derived overseas, the Australian tax payable will generally be reduced

by a credit for the foreign tax paid (refer 3.5).

Non-residents of Australia are taxable only on Australian source

income, excluding interest, royalties and dividends which are subject

to withholding tax at source.

8

2. Will I be an Australian tax resident during my

assignment?

2.1 Residence for Australian tax purposes

Your residence for immigration purposes does not determine and is

not affected by your residence for tax purposes. For Australian

taxation purposes, you are a resident of Australia if you:

• reside in Australia; or

• have an Australian domicile (see below), unless the Commissioner

of Taxation is satisfied that your permanent place of abode is

outside Australia; or

• have been physically present in Australia for more than 183 days of

any income year (an Australian tax year begins 1 July and ends 30

June), unless the Commissioner is satisfied that your usual place of

abode is outside Australia and that you have no intention of taking

up residence in Australia.

A non-resident is defined as being a person who is not a resident of

Australia, that is, a person who does not meet any of the criteria for

residency set out above.

In the Commissioner’s view, “residency” is determined having regard

to whether an individual establishes and maintains a routine or

“mode of life” that is relatively similar to the life enjoyed before

entering Australia. The following factors will be relevant:

• purpose of your presence in Australia;

• your family and employment ties;

• maintenance and location of your assets; and

• your social and living arrangements.

Where your day-to-day behaviour over a period of six months is

similar to that before arriving in Australia, you will generally be

regarded as residing in Australia from the date of arrival.

Most individuals coming to Australia on an assignment expected to

last more than 6 months will be regarded as tax residents of Australia.

Your residency status must be determined for each year of income.

If you are a resident of Australia for only part of the year, you are

taxable as a resident for that part-year.

9

The concept of domicile is more permanent than residency. You have

a domicile of origin in the country in which you were born. You may,

at a later stage, acquire a domicile of choice in a different country if

you regard that country as “home”. Most foreign nationals working

temporarily in Australia are unlikely to have an Australian domicile.

2.2 Dual residence

In some situations you may be a tax resident and subject to tax in

both Australia and your home country under the domestic law of each

country.

Australia has concluded a number of treaties with other countries to

avoid double taxation in these circumstances. These double tax

treaties override Australian tax laws in the event of conflicting

provisions. “Tie breaker” clauses set out criteria to determine the

country in which you will be treated as a resident for the purposes of

determining which country has first taxing rights on income covered

by the treaty, in the event that you are a resident of both countries

under their respective tax laws.

These “tie-breaker” clauses vary from treaty to treaty (and the relevant

treaty must therefore be referred to) but usually include some or all of

the following factors:

• the country in which you have a permanent home available;

• the country in which you have a habitual abode;

• the country with which you have closer personal and economic

relations; and

• your country of citizenship.

The relevant Australian treaty must be reviewed to conclude your

residency for treaty purposes.

As a general rule, if you are not regarded as a resident of Australia for

treaty purposes (even though you are an Australian resident under

Australian domestic law) you will be subject to Australian tax only on

income from sources in Australia.

If you are an Australian tax resident you will want to read section 3

“Taxation of residents”. If you are not to be an Australian tax resident,

you may wish to turn directly to section 4 “Taxation of non-residents”.

1 0

3. Taxation of residents

3.1 General principles

As a resident taxpayer you are liable to tax on income from both

Australian and foreign sources.

You are also taxable on net capital gains from disposal of worldwide

assets acquired, or deemed to be acquired, after 19 September 1985.

Assets comprise any form of property and include intangible property.

If you are entitled to claim Medicare benefits you will be subject to the

Medicare Levy of 1.5% on your taxable income. If you are a higher

income earner and do not have private health insurance you may be

subject to a further 1% Medicare levy surcharge (refer 10.1).

A tax-free threshold on taxable income is available to you as a resident

(refer to “Personal Tax Rates” in the IAS Tax Summary). This

threshold may be decreased if you are a part-year resident.

As a resident you will be taxed at progressive rates which are detailed

in the “Personal Tax Rates” section in the IAS Tax Summary.

Where you have paid foreign tax on foreign sourced income, credit for

that tax is allowed against Australian tax payable on that income,

subject to certain limitations (refer 3.5).

Foreign sourced employment income derived from a continuous 91

day period of foreign service may be exempt from Australian tax (eg a

bonus in resect of previous overseas employment).

If you are a tax resident you may be eligible for certain personal

offsets which can reduce your Australian tax liability (refer 3.6).

3.2 Calculation of taxable income

As a resident individual you are taxable on your “taxable income” for

each year of income ending 30 June.

Taxable income is calculated by deducting from “assessable income”

all “allowable deductions” relating thereto for a particular year of

income. “Assessable income” does not include “exempt income”.

1 1

Resident tax rates are applied to taxable income to determine gross tax

payable from which any foreign tax credits and offsets are deducted to

determine the net tax payable.

3.3 Assessable income

Generally, your assessable income as a resident can be classified

under the following headings:

3.3.1 Employment income

Your gross income includes most cash remuneration arising from

your employment. Cash remuneration comprises salaries, wages,

commissions, bonuses and allowances.

Certain cash allowances, being living-away-from-home allowances

(“LAFHAs”), are subject to the fringe benefits tax (“FBT”) regime and

are therefore not income. An allowance is a LAFHA if it is provided to

you while you are living away from your usual place of residence to

compensate for additional expenses incurred and other disadvantages

suffered in order to fulfil employment duties.

Benefits-in-kind, such as accommodation, low-interest loans and

motor cars, provided to you or your associate by your employer are

not included in your assessable income. Instead, your employer is

liable to FBT on the taxable value of these benefits (refer chapter 7).

A lump sum payment that you receive as a consequence of

termination of employment or office is taxable on a concessional

basis. “Bona fide” redundancy payments are tax-free up to certain

limits (refer to “Superannuation and ETPs” in the IAS Tax Summary).

Termination payments are subject to a surcharge if your adjusted

taxable income exceeds the “Surcharge Threshold” (refer to

“Superannuation and ETPs” in the IAS Tax Summary). The surcharge

is levied only on the portion of the termination payment relating to

the period post 20 August 1996. Bona fide redundancy payments are

not subject to the surcharge.

Lump sums received on termination of employment can be rolled

over, i.e. deposited directly into an Australian superannuation fund,

approved deposit fund or other approved roll-over fund. Tax then

becomes payable by the fund on the contribution. You will be liable to

further tax when you withdraw an amount from the fund.

1 2

3.3.2 Capital gains

Capital gains on sale of assets acquired after 19 September 1985 are

assessable. Assets comprise any form of property and include

intangible assets such as options, rights under restrictive covenants,

etc., but exclude motor vehicles. The net capital gain is included in

your taxable income and subject to income tax, generally at your

marginal tax rate.

Capital losses may be used to offset your capital gains. Any excess

capital loss may be carried forward indefinitely to offset any gains

realised in future years.

Where you have held an asset for less than 12 months prior to

disposal, the entire capital gain is included in your taxable income.

Where you have held the asset for 12 months or more prior to

disposal, you can elect between two methods for calculating the

amount of capital gain to be included as assessable income. These

methods are the “Indexation Method” and the “Exemption Method”

(see below).

• Under the “Indexation Method”, the capital gain is determined

after indexing the capital cost of the asset for the appropriate

inflation rate as published by the Australian Statistician. As part of

the transition to the new “Exemption Method”, indexation has been

frozen at 30 September 1999.

• Under the “Exemption Method”, you can elect to claim an

exemption of 50% of the nominal capital gain from the disposal of

each asset. In other words, this method allows you to report a

capital gain equal to 50% of the excess of the sales proceeds over

the unindexed cost base of the asset disposed. Indexation is not

applicable under this method.

On becoming an Australian resident, you are deemed to have

acquired at that time, for a consideration equal to their market value,

most post 19 September 1985 assets that you own. Assets which are

specifically excluded from the rules are assets having the “necessary

connection with Australia” and assets which are specifically exempt

from CGT (refer below).

1 3

Assets having the “necessary connection with Australia” are subject to

the capital gains tax (“CGT”) rules regardless of your residency status.

Assets which fall into this category are effectively located in Australia

and include:

• Australian real estate;

• shares in Australian private companies;

• interests in Australian partnerships and trust estates;

• assets used in Australian businesses;

• interests of 10% or more in Australian public companies and unit

trusts;

• options to acquire any of the above; and

• the benefits of certain “restrictive covenants” (eg non-compete

clause payments)

Your main residence is exempt from CGT provided that the property

has been your main place of residence at all times prior to the

disposal and has not been used for income producing purposes.

If you cease to occupy your main residence whilst on assignment in

Australia, you can elect that the property continue to be regarded as

your main residence for CGT purposes, until the earliest of the

following times:

• when the dwelling again becomes your main residence;

• when you dispose of the dwelling; or

• when the dwelling has been used for income producing purposes

for a total of six years.

The exemption from CGT is available even if the residence is used for

income producing purposes (ie rented out) during your absence and

you do not resume residence prior to disposal.

There is also an effective exemption for personal use assets such as

items of furniture and electrical appliances where the cost of the asset

was $10,000 or less. However, certain assets, such as works of art and

antiques, are subject to the CGT rules on disposal if the acquisition

cost is at least A$500.

The CGT implications upon departure from Australia are discussed in

detail in Chapter 6.

1 4

A capital gain arising from the sale of an asset may attract tax in the

country of source as well as in Australia. If a capital gain arising from

a foreign source is taxable both in the source country and in Australia,

you may claim a foreign tax credit for the foreign tax paid, up to the

amount of Australian tax payable on the gain (refer 3.5).

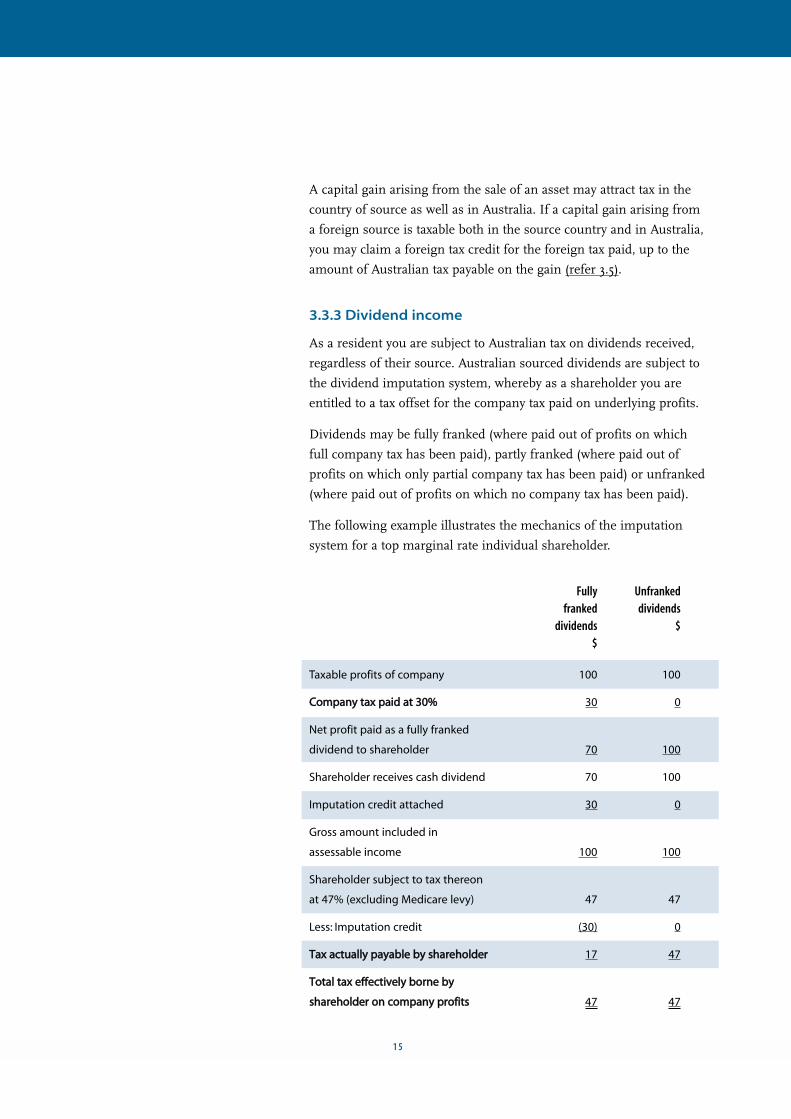

3.3.3 Dividend income

As a resident you are subject to Australian tax on dividends received,

regardless of their source. Australian sourced dividends are subject to

the dividend imputation system, whereby as a shareholder you are

entitled to a tax offset for the company tax paid on underlying profits.

Dividends may be fully franked (where paid out of profits on which

full company tax has been paid), partly franked (where paid out of

profits on which only partial company tax has been paid) or unfranked

(where paid out of profits on which no company tax has been paid).

The following example illustrates the mechanics of the imputation

system for a top marginal rate individual shareholder.

Fully Unfranked franked dividends

dividends $$

Taxable profits of company 100 100

CCoommppaannyy ttaaxx ppaaiidd aatt 3300%% 30 0

Net profit paid as a fully franked

dividend to shareholder 70 100

Shareholder receives cash dividend 70 100

Imputation credit attached 30 0

Gross amount included in

assessable income 100 100

Shareholder subject to tax thereon

at 47% (excluding Medicare levy) 47 47

Less: Imputation credit (30) 0

TTaaxx aaccttuuaallllyy ppaayyaabbllee bbyy sshhaarreehhoollddeerr 17 47

TToottaall ttaaxx eeffffeeccttiivveellyy bboorrnnee bbyy

sshhaarreehhoollddeerr oonn ccoommppaannyy pprrooffiittss 47 47

1 5

Your gross amount of foreign sourced dividends is fully taxable in

Australia (refer 3.5.2).

3.3.4 Other income

As a resident you are subject to tax on all other income (including

interest, rent, royalties, income from partnerships, trusts, pensions,

businesses and any other income from any activity derived from any

source, world-wide).

Your foreign losses cannot generally be offset against Australian

source income (refer 3.5)

Certain foreign investment earnings you derive within a tax

advantaged savings plan in your home country are likely to be subject

to Australian tax.

3.3.5 Employee share plans

The taxation of shares and options granted under employee share

plans depends upon whether you acquired the shares and options

before or after 28 March 1995.

Where you were granted the shares or options to acquire shares under

an employee share acquisition scheme (“ESAS”) before 28 March

1995, the rules governing their taxation are as follows:

• As a general rule, you are subject to tax at the time that

“unrestricted shares” are acquired under an ESAS. The assessable

benefit is the difference between the market value at that time and

the amount paid to acquire the shares.

• However, where you elected to bring forward the taxing point to

either the time when the options were granted or “restricted

shares” acquired, no gain is recognised at the time that the options

are exercised or restrictions on shares are lifted.

• On disposal of shares acquired under an ESAS, you will be subject

to capital gains tax (refer 3.3.2 for more details) on any further gain

arising on disposal.

1 6

Where you were granted the shares or options to acquire shares under

an ESAS on or after 28 March 1995 (subject to transitional rules

which allow some rights or shares acquired after 28 March 1995 but

before 1 July 1996 to be treated under the old rules), the rules

governing their taxation are as follows:

• Where an ESAS meets certain conditions, it will be “qualifying”,

and liability to tax can be deferred for up to 10 years from date of

grant. A “qualifying” ESAS must involve ordinary shares (or

options in respect thereof ) in either the employer company or

holding company of the employer. The shares or options will not be

“qualifying” when offered to employees with a shareholding of

more than 5% in the company. The shares (but not options) must

be offered to at least 75% of all permanent employees of the

employer.

• Where the conditions are not met an ESAS will be “non-

qualifying”, and you will be subject to tax on the value of the

discount inherent in the option or share at the date of original

grant, regardless of any restrictions on exercise or sale thereof.

• There are specific rules for determining the market value of

unlisted options, taking into account the share price, exercise price

and exercise period of the options and ignoring any restrictions

attached to the options. Under these rules most options will have a

value at grant date.

• If a qualifying ESAS satisfies certain additional conditions

including being offered on a non-discretionary basis with a 3 year

minimum disposal restriction, a $1,000 exemption of taxable value

per annum is available to you, if you elect to be taxed up front on

all ESAS benefits granted in a particular year.

• On disposal of shares acquired under an ESAS, you will be subject

to capital gains tax (refer 3.3.2 for more details) on any further gain

arising on disposal.

If you are subject to tax in your home country upon the acquisition of

the shares or options, a foreign tax credit may be claimed in respect of

the foreign tax paid on the gain (refer 3.5) in order to reduce the

Australian tax payable. Care must be taken in these situations to avoid

double tax on the gain, particularly since there are no clearly defined

Australian tax rules regarding the source of the gain.

1 7

Professional advice should be sought from Deloitte Touche Tohmatsu

on the application of these rules if you acquire shares or options or

exercise options acquired under an ESAS while on assignment in

Australia.

3.3.6 Attributable income of CFCs & FIFs

There are three different regimes which can operate to “attribute”

income to you as an Australian tax resident.

Attribution means that you are assessed on income you do not

actually receive, where that income is received by a foreign entity in

which you have an interest.

The Controlled Foreign Company (“CFC”) rules apply to attribute

income to you as an Australian resident shareholder in respect of

profits derived by a foreign company that is controlled by 5 or fewer

Australian residents.

The Foreign Investment Fund (“FIF”) regime can apply to assess you

on the annual increase in market value of your non-controlling

interests in foreign companies and trusts unless:

• you hold a temporary resident visa in Australia lasting no more

than 4 years and you have not applied for permanent residency; or

• the total value of your investments in FIFs does not exceed

A$50,000; or

• the investments are in foreign public listed companies which do

not engage in certain prohibited activities (such as funds

management and financial intermediation services); or

• the interest is held in a foreign employer sponsored

superannuation fund; or

• the interest is held in a US corporation or certain other US entities

subject to tax on worldwide income; or

• the interest is held in a US mutual fund.

The Foreign Life Assurance Policy (FLP) regime can apply to assess

you on the annual increase in surrender value of any FLPs in which

you have an interest.

1 8

The non-resident trust estate rules can attribute income to you as an

Australian resident if you have transferred property or services to a

non-resident trust or have received a distribution from a non-resident

trust.

The rules under which these regimes operate are complex and

professional advice should be sought on their potential application.

3.4 Allowable deductions

Generally, expenses and losses are deductible provided you incur

them in gaining or producing assessable income. However, expenses

of a private, domestic or capital nature are generally not deductible.

Commonly allowable deductions include:

• interest paid on funds you borrow to invest in income producing

assets;

• depreciation of assets used to produce your assessable income;

• donations to approved organisations;

• employment-related expenses such as the cost of tools of trade,

trade journals, business related seminars and regular subscriptions

to trade, professional and business associations;

• business related travel expenses but not cost of travel from home to

work;

• car expenses including all costs or outgoings that are incurred in

maintaining and operating a car for employment related (ie

business) purposes (allowable car expenses do not include the

expenses of operating an employer provided vehicle or the costs of

travel from home to work); and

• tax agent fees that you pay.

Refer to our flyer “Record keeping requirements” for details regarding

the evidentiary requirements that must be fulfilled in order to support

employment related deductions claimed in your income tax return.

1 9

There is no standard deduction and you must be able to comply with

specific substantiation rules where work-related claims exceed $300

in a year of income. When you make a claim for such expenses, you

must declare in your tax return that you have the necessary receipts

and other records (eg travel diaries for most overseas travel) to

substantiate the claim.

Contributions you make to your home country pension or tax

advantaged savings arrangements are not allowable as tax deductions

in Australia. Generally company contributions to such schemes would

not be considered assessable income to you, but the tax treatment

would depend on the terms of the individual scheme. Such

contributions may be subject to fringe benefits tax or may be non-

deductible to your employer.

3.5 Foreign tax credit system

The Foreign Tax Credit System (“FTCS”) provides a mechanism for

relief from double tax where you derive foreign income and foreign

tax has been paid on that income.

The source of an item of income is factual and is determined

separately in each case. While there are general rules regarding

different types of income, consideration must always be given to the

facts surrounding each case. In general terms, income is sourced as

follows:

IInnccoommee ttyyppee FFaaccttoorrss ddeetteerrmmiinniinngg ssoouurrccee

Employment Where the duties are performed

Dividend Where the profits, out of which the dividend is

paid, are earned

Interest Where the obligation to pay the interest arose

Rental Where the property is situated

Under the FTCS the Australian tax otherwise payable on foreign

income is reduced by the amount of foreign tax paid. The credit in

respect of any year is limited to the amount of Australian tax payable

on the particular class of foreign income or the actual amount of

foreign tax paid, whichever is less.

2 0

For this purpose there are two classes of income relevant to

individuals:

• passive income; and

• other foreign income

Passive income includes dividends, interest, annuities, rents, royalties,

capital gains, commodity gains and attributed income (refer 3.3.6).

Other foreign income includes employment and business income.

Where the foreign tax credit claimed is limited to the amount of

Australian tax on the particular class of foreign income, any excess

foreign tax paid can be carried forward for up to 5 years to be offset

against your Australian tax on foreign income of that class in a

subsequent year.

Where there is an overall foreign loss from a particular class of

foreign income, that loss may be offset only against future income

from that particular class (i.e. it is “quarantined”). For this purpose,

interest is a separate class of foreign income to other passive income.

Hence your foreign interest income cannot be offset against your

rental loss. Your foreign interest income is assessable and your

foreign rental loss may be used only to offset income of that class in

the same or a future year.

Capital losses are separately quarantined under the general capital

gains tax provisions (refer 3.3.2).

3.5.1 Rental income

You may rent out your home while you are on assignment in

Australia. The rental income is assessable, for Australian tax

purposes, and deductions may be claimed for expenses of

maintaining your home. If you are also subject to tax on this income

in your home country, a credit may be claimed for the foreign tax

paid.

As of 1 July 2001, interest and borrowing expenses incurred in

relation to a foreign rental property are fully deductible in your

income tax return. However where you have a net foreign rental loss

generated by other deductions, this loss is not deductible against your

Australian source income. It may only be offset against your other

foreign sourced income of the same class (see above).

2 1

If you pay mortgage interest to an overseas bank or financial

institution as a resident of Australia, you are generally required to

remit interest withholding tax equal to 10% of the mortgage interest

paid. You may not claim a deduction for the mortgage interest in your

tax return unless this tax has been paid (refer 8.5).

Our flyer “Common rental deductions” lists deductions that you can

claim against your rental income, including an outline of the main

rental property depreciation assets.

3.5.2 Dividend income

The gross amount of foreign sourced dividends you receive (after

grossing up for foreign withholding tax paid thereon) is taxable. You

will be allowed a credit for any foreign tax paid on the income.

Where you receive the dividends from a country with which Australia

has entered into a Double Tax Treaty, the credit is limited to the rate of

tax specified in the relevant treaty (refer to Australia's Double Taxation

Treaties), notwithstanding that foreign tax may have been deducted in

excess of this amount. A refund claim for the tax deducted in excess

of the treaty rate must be separately made to the relevant foreign tax

authority.

You are not entitled to a credit for any foreign underlying tax paid by

the foreign company on profits out of which the dividend is paid.

3.5.3 Interest income

As a resident you are subject to Australian tax on all interest derived

regardless of its source. You may claim a credit for foreign taxes you

pay on foreign sourced interest. In the case of interest received from

treaty countries, the foreign tax credit is limited to the rate of tax

specified in the relevant treaty (normally 10% but sometimes 15%).

Foreign tax may have been deducted in excess of this amount in

which case a refund claim for the tax deducted in excess of the treaty

rate must be made separately to the relevant foreign tax authority

(refer to Australia's Double Taxation Treaties).

2 2

3.6 Offsets

Details of the rates of personal offsets available to resident taxpayers

are contained in “Offsets” in the IAS Tax Summary.

3.6.1 Dependant offsets

As a resident taxpayer you may be entitled to claim an offset against

Australian taxes payable where you maintain your spouse or your

dependent parent or parent-in-law during the year.

3.6.2 Medical expenses offset

As a resident taxpayer you are allowed an offset for unreimbursed

medical expenses above a certain threshold incurred in obtaining

medical treatment for you or your dependants (refer to “Offsets” in

the IAS Tax Summary).

3.6.3 Parenting allowance

Dependent spouses with dependent children may directly receive a

tax-free parenting allowance in cash, on a fortnightly basis, from

Centrelink.

Eligibility for the allowance depends upon the immigration residency

status and the income of the dependent spouse, as determined for

Social Security purposes. It is unlikely that a spouse holding a

temporary resident visa will be eligible for these allowances.

2 3

4. Taxation of non-residents

4.1 General principles

As a non-resident you are subject to Australian tax only on your

Australian sourced income.

As a non-resident you are subject to tax on gains derived from the

disposal of certain assets having a necessary connection with Australia

(refer 4.3.2).

As a non-resident no Medicare Levy is payable (refer 10.1).

No tax-free threshold is available and tax is payable at progressive

rates (refer to “Personal Tax Rates” in the IAS Tax Summary).

No concessional offsets are available to you as a non-resident.

You are liable to withholding tax at the rate of 10% on Australian

interest, 30% (reduced by most treaties to 15%) on the unfranked part

of any Australian dividend income and 30% (reduced treaty rate of

10%) on Australian royalties (refer to Australia's Double Taxation

Treaties). You will not be subject to Australian tax on franked

dividends you receive.

4.2 Calculation of taxable income

Your taxable income is calculated by deducting from “assessable

income” all “allowable deductions” relating thereto for a particular

year of income.

However, as a non-resident you are taxable only on Australian sourced

income, and may claim allowable deductions only for expenditure that

relates to that income.

4.3 Assessable income

4.3.1 Employment income

Generally employment income is sourced where the services are

performed. Accordingly, as a non-resident you are not subject to

Australian tax on your earnings for services performed outside

Australia.

2 4

Where you perform services both in and out of Australia, it is usually

necessary for you to keep detailed records of all workdays to enable an

appropriate apportionment between Australian and foreign source

earnings, based on time spent in and out of Australia.

In certain circumstances employment income for services in Australia

may be exempt from Australian tax through the operation of a double

tax treaty (refer 11.1).

4.3.2 Capital gains

The capital gains tax (“CGT”) regime is described at 3.3.2.

As a non-resident, you are subject to tax only on capital gains derived

from the disposal of assets having the necessary connection with

Australia acquired after 19 September 1985. These assets are

described at 3.3.2.

4.3.3 Passive income

Australian source interest you derive as a non-resident is subject to

withholding tax at source (i.e. withheld and remitted by the payer) at

the rate of 10% of the gross amount of the interest. This represents a

final tax liability on such income and the income need not be

included in your Australian tax return. It is your responsibility to

advise the payer of your non-resident status.

Australian source unfranked dividends that you receive while non-

resident are subject to withholding tax at source at the rate of 30% of

the gross dividend, unless Australia has concluded a double tax treaty

with your country of residence (refer to Australia's Double Taxation

Treaties), in which case a 15% (in most cases) withholding tax rate will

apply.

The withholding tax is a final tax liability on such income and the

income need not be included in your Australian tax return.

Australian source franked dividends that you receive while non-

resident are not subject to withholding tax or to any further Australian

tax in your hands and are not required to be included in your

Australian tax return.

2 5

Australian source rental income is taxed on an assessment basis and

is not generally subject to tax withholding at source. It is therefore

required to be included in your tax return.

Australian source royalty income is subject to withholding tax at

source at the rate of 30% of the gross royalty, unless Australia has

concluded a treaty with your country of residence (refer to Australia's

Double Taxation Treaties), in which case a 10% (in most cases)

withholding tax rate will apply. The withholding tax is a final tax

liability on such income and the income need not be included in your

tax return.

4.4 Allowable deductions

Generally, expenses and losses are deductible only to the extent to

which they are incurred in gaining or producing Australian source

assessable income.

Expenses of a private, domestic or capital nature are generally not

deductible. Refer to section 3.4 for a list of the most common

deductions.

As with resident individuals, no standard deduction applies and you

must retain proper documentary evidence to substantiate any

deductions claimed.

Expenses incurred in earning Australian sourced interest and

dividends are not allowable deductions.

2 6

5. Lodgment and payment procedures

5.1 Will I have to lodge a return?

If you are a resident of Australia you must lodge a separate tax return

if your taxable income exceeds the tax free threshold for the year (refer

to “Personal Tax Rates” in the IAS Tax Summary). You may also need

to lodge a return if your income is below the threshold but you have

had tax deducted from income at source (e.g. tax instalment

deductions from salary).

If you are a non-resident and you derive any Australian source

assessable income you must lodge a return. Assessable income does

not include dividend, interest or royalty income that is subject to the

withholding tax provisions.

Where you and your partner receive income jointly, you must each

include your share of the income in your own return (for example net

rental income from a jointly owned property).

5.2 When will I have to lodge a return?

The Australian tax year ends on 30 June and income tax returns must

normally be lodged by the following 31 October, although this can be

varied each year by the Commissioner of Taxation (“Commissioner”).

If your return is prepared by a registered tax agent, such as Deloitte

Touche Tohmatsu, lodgment may be deferred provided you are

registered on the tax agent's program by the date set for that purpose

by the Commissioner.

Tax agents are required to progressively lodge returns on their

program and ensure that all returns are lodged by the due dates

determined annually by the Commissioner. The due date is

determined by the amount of tax that you paid in the previous year,

and whether your prior year return was lodged by its due date and can

vary from the end of October to mid-May of the following year.

2 7

5.3 Assessment procedure

Shortly after lodgment of your tax return the Commissioner issues an

assessment notice specifying the taxable income, tax assessed, credits

allowed for foreign taxes, tax already paid and offsets. There is either a

net refund, in which case a cheque is attached to the assessment

notice, or a balance due for payment no earlier than 21 days from the

issue date of the assessment. You may elect to have a tax refund

deposited directly into a nominated bank account. A tax liability may

be paid by direct debit on request.

The assessment is usually based on information contained in the

return, although the Commissioner is not obliged to rely solely on

this information.

A default assessment may be issued if you fail to lodge a return or a

return is found to be unsatisfactory.

5.4 Collection of tax at source

Tax on your employment income is withheld by way of the Pay As You

Go (“PAYG”) Withholding system.

Technically, the use of an offshore payroll does not avoid the PAYG

withholding system. We recommend that you seek professional advice

from Deloitte if you are paid by an overseas employer and PAYG

withholding is not being deducted from your salary.

Tax on your investment income may be withheld at source, either by

non-resident withholding tax or at the top marginal rate of tax if you

do not provide your tax file number to the investment body (refer 5.8).

5.5 PAYG Instalments

If you had business or investment income on your last income tax

return in excess of $1,000 and you had a tax liability of more than

$250, you are generally liable to make tax payments under the Pay As

You Go (PAYG) Instalment system.

If you are liable to pay PAYG instalments, you will be notified by the

ATO. You will receive an Instalment Activity Statement which will

contain an instalment rate calculated by the ATO based on your latest

assessed income tax return.

2 8

Most PAYG instalment payers will calculate their instalments by

multiplying the instalment rate by their instalment income.

Instalment income includes:

• fees received for services;

• employee share plan income;

• interest;

• rent; and

• dividends.

Salary and wages are excluded.

Instalment income does not include capital gains.

PAYG instalments will usually be made quarterly. You have the option

of making an annual payment where the following criteria are

satisfied:

• your most recent notional tax (as advised by the ATO, usually

corresponding to business and non CGT investment income from

the previous year) was less than $8,000; and

• you (or a partnership in which you are a partner) are not registered

or required to be registered for GST.

Quarterly payments will be due no earlier than 21 days after the end

of each quarter. Instalments for most taxpayers will therefore be due

on 21 October, 21 January, 21 April and 21 July. Note that the ATO can

extend these deadlines. The date for annual payments will be no

earlier than 21 October following the tax year-end.

You are able to vary the amount of each instalment in line with

variations in your income. This can be done by applying to the ATO to

vary the instalment rate.

If your notional tax is in excess of $8,000 or if you are registered for

GST purposes or are in a partnership registered for GST purposes

you can choose to pay an amount notified by the Commissioner or

you can calculate actual income subject to PAYG.

2 9

5.6 Amendment and objection process

You can request an amended assessment to correct an error made

when preparing the original return. This request should be made

within four years of the issue of the assessment notice.

You have four years in which to object to an assessment. Objections

must be lodged in writing and state fully the grounds upon which

they are based.

The Commissioner must provide a written decision on the objection.

You can appeal against an objection decision if still dissatisfied.

5.7 Private rulings

You may request a private ruling to obtain the Commissioner's view

on the application of a particular tax law.

A private ruling issued by the Commissioner in respect of an

arrangement which commenced after 30 June 1992 is generally

binding on the Commissioner, but can be overridden by a subsequent

Public Ruling in its prospective application.

5.8 Tax file number

Every person liable to taxation in Australia must obtain a tax file

number (“TFN”).

You must complete an application form and present at least two types

of original approved identity documents (eg passport, birth certificate)

with the application to the Australian Taxation Office ("ATO”).

You must provide your TFN to your employer within 28 days of

commencing employment. Failure to do so creates an obligation on

the employer to deduct tax instalments from your salary at the top

marginal rate (currently 48.5%).

If you are an Australian resident you should provide your TFN to your

relevant financial institutions to avoid tax being withheld from

income at the top marginal rate.

If you are a non-resident you should advise your Australian financial

institutions to deduct withholding tax at source from investment

income.

3 0

6. Procedures and tax consequences on

departing Australia

There are a number of matters that you will need to address shortly

before departing Australia. These matters generally apply only if you

cease to be a resident of Australia when you depart.

6.1 General principles

As a foreign national leaving Australia permanently, you will not be

subject to any special administrative requirements other than to

ensure normal tax return ruling requirements are competed (either

before or after departure).

No tax clearance certificate or notification to the ATO is required prior

to departure from Australia.

If you depart Australia during a tax year it will often be necessary to

vary your PAYG instalments based on your estimated income for that

year, if this is less than the income on which PAYG instalments have

been determined.

6.2 Capital gains tax

Upon ceasing to be an Australian resident, you are deemed to have

disposed of all assets then held, to which the CGT provisions apply, at

their market value at that date. Certain assets excluded from these

rules include:

• assets acquired before 20 September 1985;

• assets having the necessary connection with Australia (refer 3.3.2);

and

• assets held at the date that residence commenced, or acquired by

inheritance, provided you were not a resident in Australia for more

than 5 years in the last 10 years prior to ceasing residence.

You may therefore be subject to tax on unrealised gains, including

exchange rate variances in respect of assets held overseas.

However, you may elect to treat all assets otherwise deemed to be

disposed of as assets having the necessary connection with Australia.

The effect of the election is that no gain is recognised at the time of

departure from Australia and the actual capital gain on ultimate

disposal will be subject to Australian tax. If appropriate, the election

should be made for the tax year that you cease Australian residency.

3 1

The Protocol to the US/Australia Double Tax Agreement is expected to

take effect from 1 July 2003 and offers protection against double

taxation of capital gains for US citizens working in Australia as it has

detailed rules allocating taxing rights in respect of capital gains.

Under the Protocol, US Citizens who elect to defer the Australian

CGT will, if they ultimately sell the assets after returning to the US,

pay tax on the whole gain only in the US. If the gain is realised when

the individual has a tax-home in a third country, the individual will

have to pay Australian capital gains tax, but US domestic law provides

a mechanism for allowing a credit for the Australian tax in such

circumstances.

If an individual departing Australia chooses to recognise the deemed

disposal in Australia at departure, such disposal may, if so elected by

the individual, also be recognised for US tax purposes. In this case,

the individual will be considered to have sold and immediately

reacquired the asset for US purposes at its fair market value at that

time. This will ensure that US citizens may claim a credit for the

Australian tax paid against their US tax liability.

6.3 Deferral of income and capital gains

In order to not trigger an Australian tax liability before departing

Australia, you should consider deferring the exercise of any options

and the disposal of any assets to which the CGT or ordinary income

tax provisions apply, until after departure from Australia.

3 2

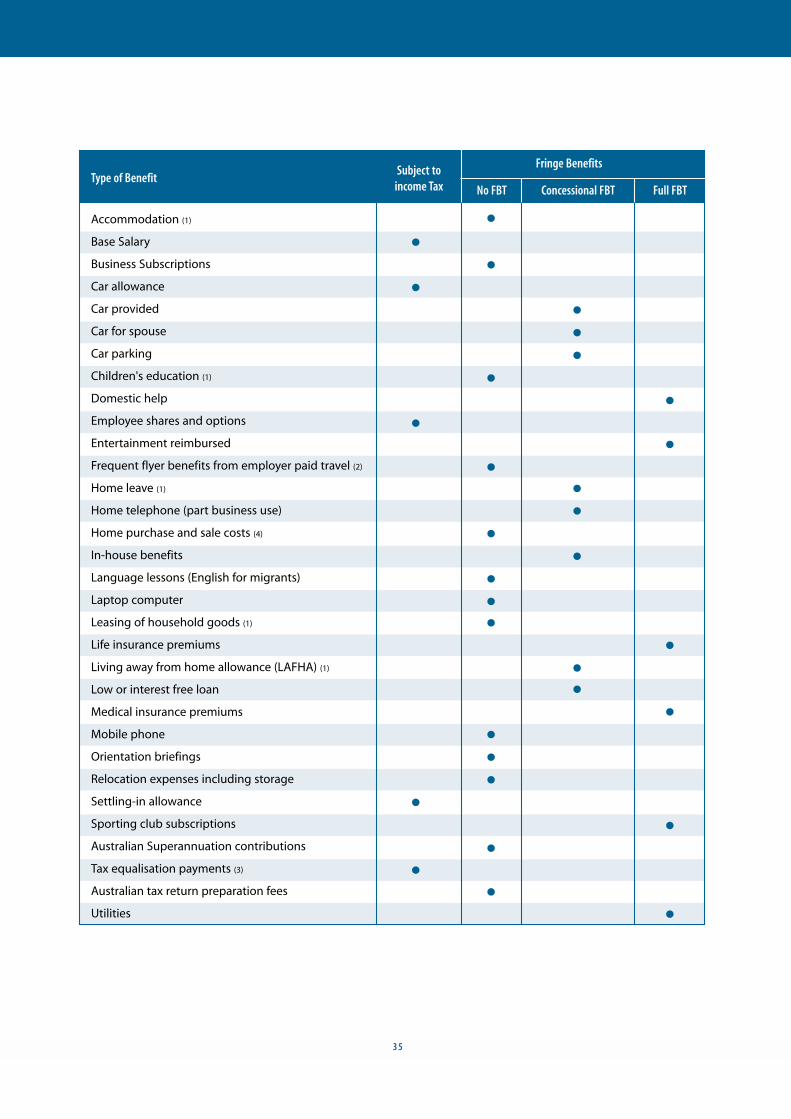

7. Fringe Benefits Tax

7.1 Assessable income or fringe benefit

It is necessary to distinguish between the items included in a

remuneration package which are assessable income to you, upon

which you are subject to income tax, and items which are fringe

benefits, upon which your employer is subject to fringe benefits tax

(“FBT”). The chart at 7.4 summarises the standard tax treatment of

most commonly provided remuneration items.

Where a benefit is subject to the FBT regime it is exempt from

income tax in your hands.

Whether an employer seeks to recover any FBT costs against your

gross remuneration package is a matter of contract between you and

your employer.

Your employer must report the grossed-up value of all fringe benefits

provided to you for any FBT year, on your annual payment summary.

An exemption is provided where the taxable value (i.e. before the

gross-up) is less than $1,000. You must report the amount on your tax

return and it is taken into account for the purpose of computing

certain charges, including the superannuation surcharge (refer 10.2.1).

7.2 Rate of tax

FBT is levied on the grossed up taxable value of all fringe benefits.

The gross-up factor depends on whether or not your employer can

claim an input tax credit under the Goods and Services Tax (“GST”)

for the benefit year (refer to “Fringe Benefits Tax” in the IAS Tax

Summary). The purpose of the gross-up is to equate the cost of

providing a fully taxable fringe benefit with the cost of providing an

equivalent benefit as salary for a top marginal rate taxpayer.

FBT is a tax-deductible expense to the employer.

3 3

7.3 FBT returns

The FBT year ends on 31 March and employers are required to lodge

an annual return to report the taxable value of all benefits provided,

ascertained in accordance with specific valuation rules.

The taxable value of fringe benefits can be reduced by:

• any contribution made by you towards the provision of the benefit

(eg running costs paid by you on an employer provided car); and

• the amount for which you could have claimed an income tax

deduction if you had personally incurred the expense (eg the

business use of a home telephone paid for by your employer).

Certain benefits, such as Australian superannuation, are exempt from

FBT and are not required to be included in an FBT return.

7.4 Treatment of specific items of remuneration

As a general rule cash remuneration, including most allowances to

cover estimated expenses, is income to you while benefits in kind and

reimbursements of actual expenditures incurred by you are fringe

benefits.

Typical benefits included in an expatriate's remuneration package and

their usual treatment for FBT purposes are shown in the following

table. The actual tax treatment will depend upon your individual

circumstances.

3 4

3 5

Accommodation (1)

Base Salary

Business Subscriptions

Car allowance

Car provided

Car for spouse

Car parking

Children's education (1)

Domestic help

Employee shares and options

Entertainment reimbursed

Frequent flyer benefits from employer paid travel (2)

Home leave (1)

Home telephone (part business use)

Home purchase and sale costs (4)

In-house benefits

Language lessons (English for migrants)

Laptop computer

Leasing of household goods (1)

Life insurance premiums

Living away from home allowance (LAFHA) (1)

Low or interest free loan

Medical insurance premiums

Mobile phone

Orientation briefings

Relocation expenses including storage

Settling-in allowance

Sporting club subscriptions

Australian Superannuation contributions

Tax equalisation payments (3)

Australian tax return preparation fees

Utilities

Type of BenefitSubject to

income Tax No FBT Concessional FBT

Fringe Benefits

Full FBT

The following notes should be read in conjunction with the table:

1. You must be living away from home in order for the benefit to be

either exempt from, or subject to, concessional FBT. As a general rule,

you will be considered to be living away from home if you are

working in Australia on an assignment of a finite duration with a

definite intention to return to your home country to live at the

completion of the assignment.

2. Where you pay for the membership into a frequent flyer scheme, the

value of benefits obtained from the use of frequent flyer points

accumulated from employer paid travel are generally non-assessable

income to you and also exempt from FBT, unless the membership of

the scheme was obtained by arrangement between the employer and

an airline. Where an employer pays your membership fee for use of

an airport lounge, the fee itself is specifically exempt from fringe

benefits tax.

3. The tax treatment of tax equalisation payments depends upon the tax

equalisation arrangements in place. However, tax equalisation

settlements are usually treated as part of your assessable income.

4. You must have changed your usual place of residence and sold a

house at the former location within a certain time period for the

benefits to be exempt from FBT.

3 6

8. Other taxes

There are a number of indirect taxes levied by State governments and

municipal authorities, which are relevant to foreign nationals working

in Australia. The more commonly encountered taxes are briefly

described below.

8.1 Payroll tax

Payroll tax is levied by each State government on the gross payrolls of

employers operating in that State. Most States exempt employer

groups with a total payroll of under $500,000 from the tax and adopt

a maximum rate of tax of 6.85%. The tax is payable by the employer.

8.2 Property taxes

There are two types of property tax:

• Rates levied by local authorities on all properties to cover the cost of

community services; and

• Land tax levied by State governments at varying rates on the

unimproved value of land. In most states, it is not applicable to the

average home but may apply to investment properties.

8.3 Stamp duty

Stamp duty is a tax imposed by State governments on certain

documents including contracts for the purchase of houses and cars.

Bank debits tax is payable on withdrawals from bank accounts in

some states of Australia.

8.4 Superannuation guarantee charge

A non tax-deductible charge is imposed on employers for failing to

provide a minimum level of superannuation contributions for each of

their full-time, part-time and casual employees.

The required employer contribution level is determined based on a

percentage of ordinary time earnings (refer to “Superannuation and

ETPs” in the IAS Tax Summary).

3 7

The charge is equal to any shortfall in contribution plus a penalty for

failure to comply.

At present there are certain limited classes of employees for whom

contributions are not required, including:

• “prescribed employees” (refer 10.2.1);

• employees that are exempt under a totalisation agreement

(refer 10.2.1);

• employees aged 70 and over; and

• employees receiving salary and wages of less than $450 a month.

8.5 Interest Withholding Tax (“IWT”)

All residents of Australia, who pay interest to a non-resident of

Australia, are required to withhold and remit to the ATO, a tax equal

to 10% of the gross interest paid. An exception is provided where the

interest is incurred as an expense of carrying on a business overseas.

You are liable to interest withholding tax if you are a tax resident and

pay mortgage interest to a bank in your home country, regardless of

whether your residence is used for income producing purposes. This

interest withholding tax should be remitted via an Instalment Activity

Statement (refer 5.5) although you will need to complete an additional

form to have this information added to your quarterly statement.

US citizens will be exempt from IWT once the Protocol to the Double

Tax Agreement between Australia and the US takes effect. The

Protocol is expected to take effect from 1 July 2003.

8.6 Other taxes

There are no death, estate, gift or wealth taxes in Australia. Sales tax is

a Federal tax, which is generally imposed on the last wholesale sale of

new goods imported into or manufactured and consumed in

Australia.

Goods and Services Tax (GST) is levied on most goods and services at

a rate of 10%.

The Tourist Refund Scheme is a GST recovery mechanism which

permits an outbound traveller from Australia to recover GST paid on

goods which are being exported as accompanied baggage. The refund

will be paid on goods costing $300 (GST inclusive) or more, bought

from the same store, no more than 30 days before you leave.

3 8

9. Business visas and work permits

All nationals, excluding Australian and New Zealand citizens, require

a valid visa to enter and remain in Australia. The appropriate type of

visa will depend on an individual's intended length and purpose of

stay. The time involved in securing a visa is usually greater the longer

the period of stay required.

The following visa classes may be suitable for persons seeking to

enter Australia for business or employment purposes.

9.1 Short Stay Business Visas (Subclass 456 and Electronic Travel Authorities)

Individuals intending to visit Australia for business purposes such as

negotiations, speaking at or attending conferences, or fulfilling

contractual obligations for an overseas employer may apply for a

Short Stay Business visa if they are not required to remain in

Australia for more than three months.

These visas accommodate most business/work activities that will not

have adverse consequences for employment or training opportunities,

or conditions of employment, for Australian citizens or Australian

permanent residents.

However, applicants for Short Stay Business visas must not intend to

undertake any business-related employment or training activity in

Australia as this is not a work visa and persons seeking to engage in

paid employment in Australia should apply for the Long Stay

Business visa (Subclass 457).

For nationals of certain countries, the Short Stay Business visa is

available as an Electronic Travel Authority (ETA), an electronically

stored visa which can be obtained from travel agencies, airlines or

over the internet.

Individuals who are not eligible for an ETA, can make an application

for a Subclass 456 Temporary Business (Short Stay) visa at the nearest

Australian diplomatic mission or, in some countries, certain local

travel agents, through agency arrangements.

It is not possible to apply for a subclass 456 or ETA visa in Australia.

3 9

9.2 Long Stay Business Visas (Subclass 457)

Subclass 457 visas provide for long-term stay and employment in

Australia for periods of more than three months and up to four years

for expatriate personnel in the following categories:

• employees of Australian based companies;

• personnel from offshore companies seeking to establish a branch

of the company in Australia, participate in joint ventures or

undertake employment in relation to a contract awarded to an

offshore company;

• independent executives seeking to establish new businesses or join

existing businesses in Australia; certain services sellers; and

• certain persons accorded diplomatic-type privileges and immunities

To seek a Subclass 457 visa for an expatriate to work for an

organisation in Australia, there are generally three processing steps

administered by immigration as follows;

• the employer must be approved as sponsor;

• the employer must then lodge a business nomination which

describes the activity (vacancy/position) to be undertaken by the

expatriate and that nomination must be approved; and

• a vviissaa aapppplliiccaattiioonn must be made by the applicant.

Subclass 457 visas are granted with multiple entries for a specific

period of time (up to 4 years). The primary or main applicant is only

entitled to work in Australia for the sponsoring organisation in the

nominated occupation approved by immigration. Provisions exist in

Australian immigration law for Subclass 457 visa holders to change

employer or occupation in Australia.

The sponsorship, nomination and visa application can be lodged with

a local or overseas Australian immigration office. Subclass 457 visa

applications may include the primary applicant's spouse and

dependent children.

Provisions exist in Australian immigration law for Subclass 457 visas

to be extended from within Australia for a further temporary stay or

permanent residence.

4 0

10. Social security and retirement benefits

10.1 Health system

The Medicare levy is a compulsory form of health insurance

administered by the Australian Government.

If you are a tax resident of Australia you are generally subject to the

Medicare levy, collected as part of the tax system. No levy is payable if

your taxable income is below a certain level and phasing-in provisions

apply to low income earners. If you are liable to the Medicare levy, you

must pay an additional 1% surcharge if you are a high income earner

and you do not have private hospital insurance with an Australian

registered health fund (refer to “Medicare levy” in the IAS Tax

Summary).

If you are a non-resident of Australia, you are not subject to the

Medicare levy or surcharge.

Part year residents are entitled to a proportionate reduction in the levy

for the period of non-residence.

If your earnings are below the relevant thresholds you will receive a

tax offset if you have private health insurance.

As an incentive to take out private health insurance with a health fund

registered in Australia, you may be able to receive a reduction in the

cost of private health insurance in the form of an offset. The offset

can be claimed either as a direct reduction in the insurance premium,

a cash or cheque rebate from Medicare or as an income tax offset.

Most expatriates working in Australia on temporary resident visas are

ineligible for Medicare benefits. However contributors to government

health schemes in the United Kingdom, Finland, Malta, Italy, Sweden,

New Zealand and the Netherlands are entitled to receive limited

reciprocal rights under Medicare.

If you are not entitled to Medicare benefits you may apply to the

Minister of Health for a certificate of ineligibility to Medicare benefits

which will relieve you of liability to the Medicare levy and surcharge.

This application is generally filed at the end of an income year and

cannot be filed for a future period.

4 1

The benefits available under Medicare cover only certain treatment by

doctors, so private medical insurance cover is common and

recommended.

None of the agreements that Australia has entered into with other

countries regarding social security benefits (totalisation agreements)

limit the liability to the Medicare levy.

Under “Lifetime Health Cover”, health funds are required to increase

premiums over a base rate depending on the age when a member

first takes out hospital cover with a registered health fund. If you join

after the age of 30, you will pay a 2% premium loading for each year

you delay joining. The loading is capped at a maximum of 70% above

the premium payable by a person who joins at the age of 30.

10.2 Australian superannuation and termination benefits

10.2.1 Superannuation contributions

Your employer is required to make a minimum annual contribution

to superannuation on your behalf, calculated as a percentage of salary

up to a maximum income threshold. Failure to contribute the

required amount will result in a non-deductible superannuation

guarantee charge being imposed on your employer (refer 8.4).

Any superannuation contributions made by an Australian employer to

an Australian complying superannuation fund are deductible to the

employer provided they are within the deductible limits (refer to

“Superannuation and ETPs” in the IAS Tax Summary).

Superannuation contributions made by your employer as well as fund

earnings are assessable to the superannuation fund (at the rate of only

15% for a “complying” resident fund which satisfies various prudential

requirements).

A surcharge is imposed on the fund in respect of deductible

contributions made on behalf of employees and by self employed

individuals where the individual's “total income”, broadly defined as

taxable income plus deductible superannuation support, exceeds a

certain threshold. If your total income exceeds the threshold a 15%

surcharge will be imposed on the fund (refer to “Superannuation and

ETPs” in the IAS Tax Summary).

4 2

Employees cannot generally claim a tax deduction for their own

contributions to superannuation, although this may be effective in

certain limited circumstances.

EExxeemmppttiioonn ffrroomm ssuuppeerraannnnuuaattiioonn

Your employer may not need to make superannuation contributions

on you behalf if:

• You meet the criteria for exemption from superannuation as a

“prescribed employee”:

you hold a subclass 456 or 457 temporary resident visa or ETA

equivalent (956 and 957); and either

a) Have been appointed as the company's national (or deputy

national) managing executive, or state manager; or

b) i) Are a senior executive, or are otherwise establishing a business

activity in Australia on behalf of the company; and

ii) Your position carries substantial executive responsibility; and

iii) You have the appropriate qualifications; and

iv) Your role is a full time position; or

• You meet the criteria for exemption from superannuation under a

totalisation agreement:

a) You are from a country with which Australia has a totalisation

agreement which provides relief from superannuation, and

b) You would otherwise be covered by the social security / compulsory

pension laws of both countries; and

c) Your assignment period (both expected and actual) is within the

prescribed limits; and

d) Your employer obtains a Certificate of Coverage from the relevant

home country authority.

Australia has negotiated social security agreements that include relief

from dual social security/superannuation obligations with the

following countries:

• USA

• Portugal

• Netherlands.

4 3

The agreements with the USA and Portugal took effect from

1 October 2002 and the agreement with the Netherlands is expected

to take effect from 1 April 2003.

10.2.2 Withdrawal of benefits

You can generally only withdraw benefits from an Australian

superannuation fund on:

• death;

• permanent disability; or

• ermanent retirement from the work force.

As of 1 July 2002, accumulated superannuation benefits may be

refunded to certain foreign nationals who have permanently departed

Australia. Access to accumulated benefits will be granted where:

• You entered Australia on an eligible temporary resident visa; and

• Your visa has expired or been cancelled; and

• You have permanently departed Australia.

There is an administrative requirement to satisfy the Superannuation

Trustee that the funds may be released.

The refund of accumulated superannuation entitlements will be

subject to a final withholding tax at a rate dependent on the type of

contributions made into the fund. For compulsory superannuation

guarantee charge contributions the rate is 30% (if you are less than

age 55). This tax is a final tax and you are not required to report the

payment in your Australian tax return.

Certain components of lump sum termination benefits that you

receive (including payments of pensions and annuities which do not

comply with certain standards) which do not in total exceed a

“reasonable benefit limit” (RBL) are taxed at concessional maximum

rates. For the current rates and RBL, refer to “Superannuation and

ETPs” in the IAS Tax Summary.

Any benefit in excess of your RBL which you take as a lump sum is

taxed at the top marginal tax rate of 47% plus the Medicare levy (if

applicable).

4 4

Lump sum benefits from an Australian fund cannot be rolled over to

a foreign superannuation fund without incurring a tax liability,

although tax deferral may be available upon rollover to another

complying Australian fund.

10.3 Foreign superannuation and termination benefits

10.3.1 Payments relating to a period when you were a non-resident of Australia

((ii)) FFoorreeiiggnn ssuuppeerraannnnuuaattiioonn ppaayymmeennttss

Generally, if the foreign fund benefit was accumulated while you were

a non-resident of Australia and is paid out within 6 months of you

becoming an Australian resident, it will be exempt from Australian

tax.

However, if the benefit is received outside the 6 month period, a part

thereof will be assessable. The amount subject to tax will (with certain

exclusions) be the excess received over your accumulated entitlement

in the foreign fund on the day you became a resident plus additional

contributions thereafter. You may claim a foreign tax credit for foreign

tax paid on the amount that is assessable in Australia.

((iiii)) FFoorreeiiggnn tteerrmmiinnaattiioonn ppaayymmeennttss

In most cases, any other lump sum payment made solely in

consequence of termination of a period of foreign employment is

exempt from Australian tax, even if received after you again become

an Australian tax resident.

10.3.2 Transfer of benefit from an overseas fund to another fund

If you transfer a benefit from an overseas fund to another fund it is

treated in the same way as a benefit payment and is subject to tax at

the time of the transfer. The amount you transfer will be a “member

undeducted contribution” to the recipient fund and can thus be

subsequently withdrawn free of Australian tax, e.g. certain UK

pensions can be transferred in a tax effective manner to certain

approved Australian funds.

4 5

10.4 Other social security benefits

While Australia operates a social security system which provides

pension, health, unemployment and a range of other benefits to low

income earners, no special contributions have to be made to this

system, either by employer or employee, other than the Medicare levy.

Family allowances are paid to families supporting children under 18

years of age and certain full-time dependent students. In addition a

non-working spouse may be eligible for the parenting allowance

(refer 3.6.3). On arrival in Australia you should contact your local

Centrelink office to ascertain eligibility for such benefits.

Australia has entered into a number of totalisation agreements with

other countries for the provision of social security benefits. These

agreements provide a definition of residency for social security

purposes and determine an individual's entitlement to welfare

payments such as unemployment, age and widow pensions.

4 6

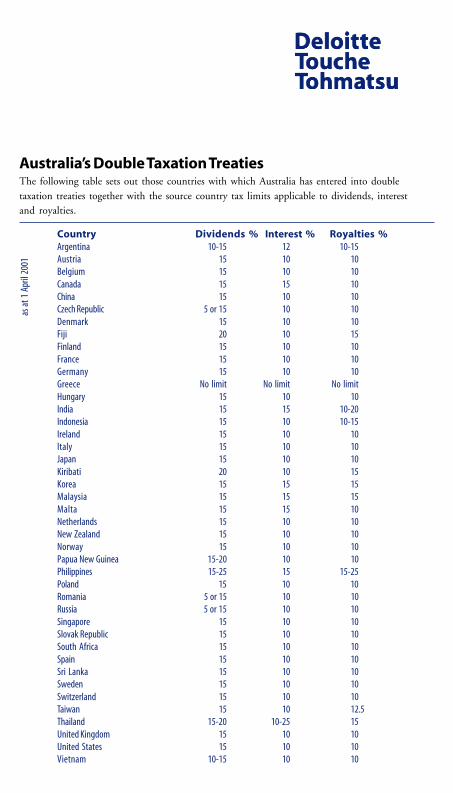

11. Double tax treaties and tax havens

11.1 Basic principles of double tax treaties

Australia has entered into a number of double tax treaties (refer to

Australia's Double Taxation Treaties). Australia's tax treaties generally

follow the OECD model and are designed to minimise the likelihood

that you are subject to double tax on the same income in two different

countries.

Common provisions found in most of the treaties include:

• exemption from Australian tax on income derived (when you are a

resident of another country) from employment in Australia which

is not attributed to a fixed base of the employer in Australia,

provided you are present in Australia for less than 183 days in the

tax year and, as a general rule, are subject to tax on the

employment income in your country of residence;

• dividends received when you are a resident of one country from a

company resident in the other country subject to tax at no more

than 15% in the country of source;