international accounting standards board - thefsa.org · financial accounting standards board this...

TRANSCRIPT

Financial Accounting Standards Board

This presentation has been prepared by the staff of the FASB and the IASB. The views expressed in this presentation are those of the presenters, not necessarily those of the Financial Accounting Foundation (FAF), the FASB, the IASB or IFRS Foundation. Official positions of the FASB and the IASB are reached only after extensive due process and deliberations.

International Accounting Standards Board

Revenue from Contracts with Customers

Kristin Bauer, Deloitte & Touche LLP & FASB Practice Fellow Russell Hodge, General Electric

Agenda

• Project status and objective • Overview of the revised revenue proposals

– Summary of key steps in model – Key areas of potential judgment

• Q&A

2

Project status 3

2010 2013 2011

November 2011

Revised exposure draft

Re-exposure of Revenue from Contracts with Customers

March 2012

Comment letter deadline

April 2012

Roundtables May 2012

Redeliberations, substantially complete in 2012

June 2010

Exposure draft

Revenue from Contracts with Customers

Early 2013

Expected IFRS / ASU

Retrospective transition proposed, effective date no earlier than January 1, 2015

2012

Project objective

• The revenue standard aims to improve accounting for contracts with customers by:

– Providing a more robust framework for addressing revenue issues as they arise

– Increasing comparability across industries and capital markets

– Requiring better disclosure

Objective: To develop a single, principle-based revenue standard for US GAAP and IFRSs

4

Overview of revised proposals

1. Identify the contract(s) with the customer

2. Identify the separate performance obligations

3. Determine the transaction price

5. Recognise revenue when a performance obligation is satisfied

4. Allocate the transaction price

Recognise revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services

Steps to apply the core principle:

Core principle:

5

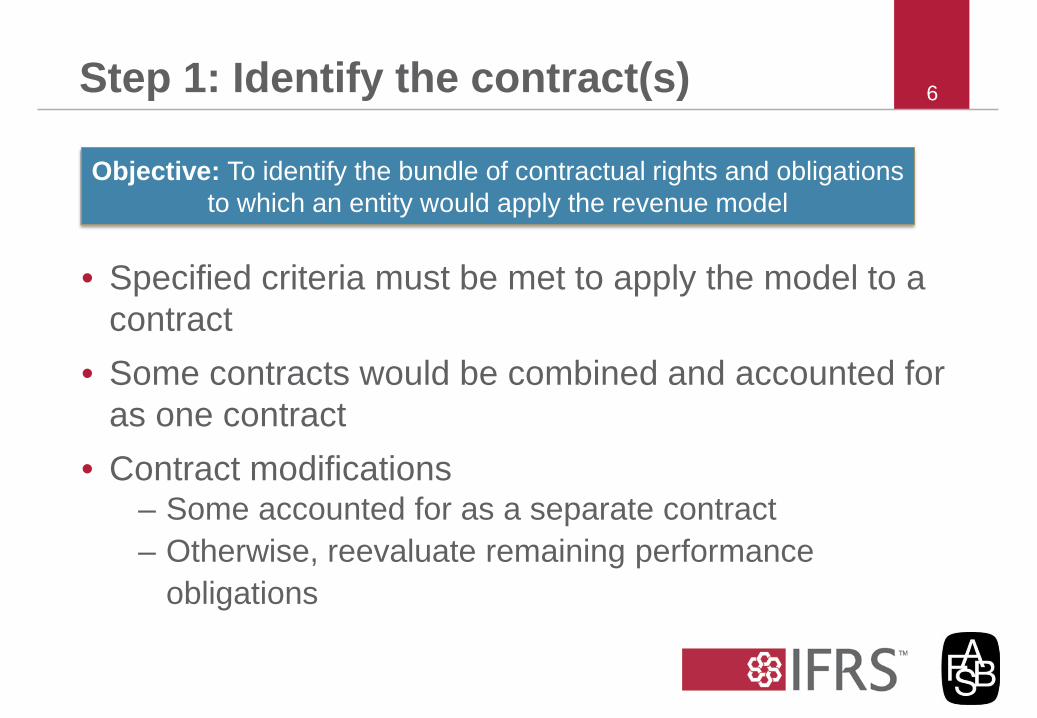

Step 1: Identify the contract(s)

• Specified criteria must be met to apply the model to a contract

• Some contracts would be combined and accounted for as one contract

• Contract modifications – Some accounted for as a separate contract – Otherwise, reevaluate remaining performance

obligations

Objective: To identify the bundle of contractual rights and obligations to which an entity would apply the revenue model

6

Step 1: Identify the contract(s)

• Assessment of the arrangement – Who is the customer?

• Define the contract arrangement – When does a contract exist? (wholly unperformed

contracts, paragraph 15)

• Contract modifications – assessment of distinct: – Prospectively adjusted, paragraph 22(a), – Retrospectively adjusted, paragraph 22(b), or – Combination of both, paragraph 22(c)

Key areas of potential judgment

7

Step 2: Identify the separate performance obligation(s)

•

• A good or service is distinct if either: – The entity regularly sells the good or service separately – The customer can benefit from the good or service on its own or

together with other readily available resources

• A good or service that is part of a bundle of goods or services is not distinct if both:

– The goods or services are highly interrelated and the contract requires the entity to provide a significant service to ‘integrate’ them into items for which the customer has contracted

– The bundle of goods or services is significantly modified or customised to fulfil the contract

Objective: To identify the promised goods or services that are distinct and, hence, that should be accounted for separately

8

Step 2: Identify the separate performance obligation(s)

•

• Key judgement – assessment will impact rest of the model (measurement and recognition of revenue)

• Paragraph 28 – ‘Regularly’ sold separately – Entity’s assessment if customer can benefit either (1) on its own or

(2) together with other readily available resources

• Paragraph 29 – Nothwithstanding 28, if a bundle, not distinct – (a) Assessment of ‘highly interrelated’ and ‘significant service to

‘integrate’ – (b) Assessment of significantly modified or customised

Key areas of potential judgment

9

Step 3: Determine transaction price

• Estimate variable consideration at expected value or most likely amount

– Use the method that is a better prediction of the amount of consideration to which the entity will be entitled

• Adjust for time value of money only if there is a financing component that is significant to the contract

• Customer credit risk accounted for under other standards and presented adjacent to revenue line on income statement

Objective: To determine amount of consideration that an entity expects to be entitled in exchange for promised goods or services

10

Step 3: Determine transaction price

• Estimation of contingent or variable consideration: – Expected value (probability-weighted assessment), used for a

large number of contracts with similar characteristics, or – Most likely amount (single most likely outcome), binary

outcomes, e.g. achieve a performance bonus or not

• Time Value of Money – assessment if a ‘significant’ financing component is present

• Customer credit risk – current constraint (collectibility is reasonably assured) is lowered

Key areas of potential judgment

11

Step 4: Allocate the transaction price

• Allocating on a relative standalone selling price basis will generally meet the objective

– Estimate selling prices if they are not observable – Residual estimation techniques may be appropriate

• Discounts and contingent amounts are allocated entirely to one performance obligation if specified criteria are met

Objective: To allocate to each separate performance obligation the amount to which the entity expects to be entitled

12

Step 4: Allocate the transaction price

• Estimating selling price – Identifying relevant observable evidence to

support stand-alone selling price – Amounts to use when not observable

(paragraph 73) – Allocating discounts (paragraph 75)

Key areas of potential judgment

13

Step 5: Recognise revenue Objective: To recognise revenue when (or as) the entity satisfies a performance obligation by transferring a promised good or service

14

Performance obligations

satisfied over time A performance obligation is satisfied over time if: • the entity’s performance creates or

enhances an asset (e.g. WIP) that the customer controls as the asset is created or enhanced; or

• the criteria in paragraph 35(b) are met (see following slides)

Revenue is recognised by measuring progress towards complete satisfaction of the performance obligation

Performance obligations satisfied at a point in time

All other performance obligations are satisfied at a point in time Revenue is recognised at the point in time when the customer obtains control of the promised asset. Indicators of control include: • a present right to payment • legal title • physical possession • risks and rewards of ownership • customer acceptance

Constraint – reasonably assured

Step 5: Recognise revenue

• An entity is reasonably assured only if: – The entity has experience with (or has other evidence about)

similar types of performance obligations, and – The entity’s experience (or other evidence) is predictive of the

amount of consideration to which the entity will be entitled

• Various factors might indicate that the entity’s experience is not predictive

Constraint: When the consideration is variable, the cumulative amount of revenue recognised is limited to the amount to which an

entity is reasonably assured to be entitled

15

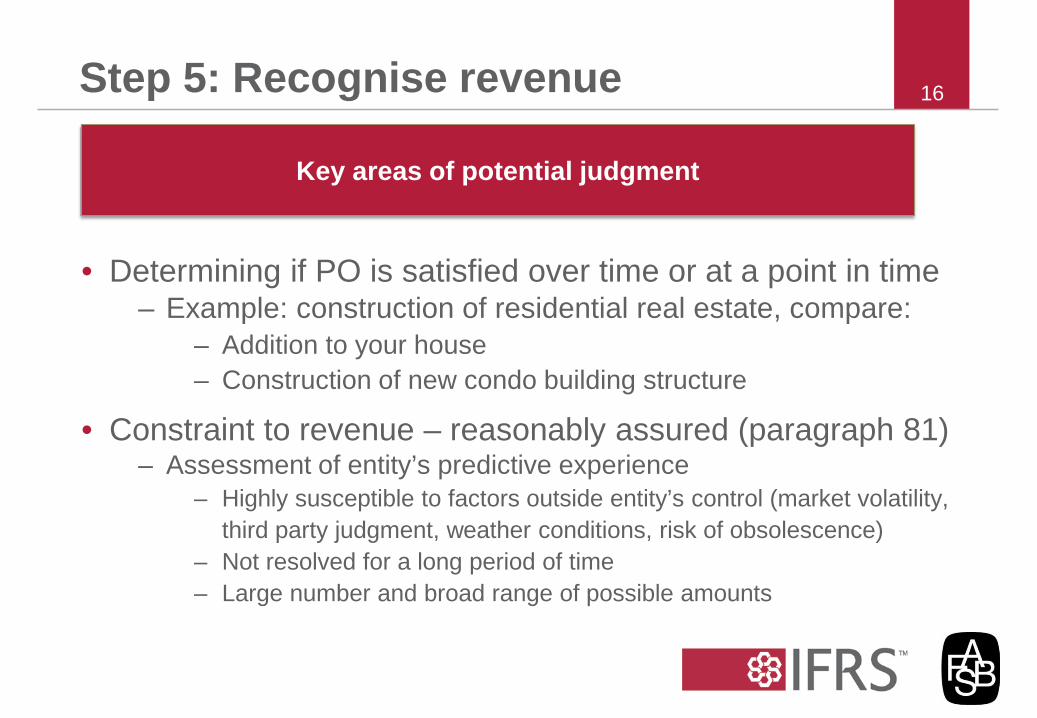

Step 5: Recognise revenue

Key areas of potential judgment

16

• Determining if PO is satisfied over time or at a point in time – Example: construction of residential real estate, compare:

– Addition to your house – Construction of new condo building structure

• Constraint to revenue – reasonably assured (paragraph 81) – Assessment of entity’s predictive experience

– Highly susceptible to factors outside entity’s control (market volatility, third party judgment, weather conditions, risk of obsolescence)

– Not resolved for a long period of time – Large number and broad range of possible amounts

Disclosure Objective: To enable users of financial statements to understand the

nature, amount, timing and uncertainty of revenue and cash flows arising from contracts with customers

17

Some disclosures required for

interim reporting

Note disclosures

Information about

contracts with

customers

Information about

judgements used

Reconciliation of contract balances

Information about long-

term contracts

Disaggregation of revenue

Overall Feedback to date

• Generally supportive of clarifications & simplifications • Clarify and refine further

– Criteria for identifying separate performance obligations – Criteria for determining revenue over time

• Difficulties in practically applying proposals – Time value of money – Retrospective transition

• Disagreement – Disclosure requirements – Onerous performance obligations

18

More information

Additional information about the revised proposals and the revenue recognition project is available at www.ifrs.org and www.fasb.org. Kristin Bauer, FASB Practice Fellow & Deloitte & Touche LLP [email protected] (203) 956-3469

19

Questions or comments?

Expressions of individual views by members of the FASB & IASB and its staff are encouraged. The views expressed in this presentation are those of the presenter. Official positions of the FASB & IASB on accounting matters are determined only after extensive due process and deliberation.

20