interim financial report fourth quarter 2014 investor...

TRANSCRIPT

Interim financial report fourth quarter 2014 Investor presentation Koen Van Gerven, CEO Pierre Winand, CFO

Brussels – March, 17th 2015

2

Investor presentation - Interim financial report 4Q14

Disclaimer This presentation is based on information published by bpost in its Fourth Quarter 2014 Interim Financial Report and Financial Report 2014, made available on March, 16th at 5.45pm CET on www.bpost.be/ir . This information forms regulated information as defined in the Royal Decree of 14 November 2007. The information in this document may include forward-looking statements1, which are based on current expectations and projections of management about future events. By their nature, forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties, assumptions and other factors because they relate to events and depend on circumstances that will occur in the future whether or not outside the control of the Company. Such factors may cause actual results, performance or developments to differ materially from those expressed or implied by such forward-looking statements. Accordingly, no assurance is given that such forward-looking statements will prove to have been correct. They speak only as at the date of the Presentation and the Company undertakes no obligation to update these forward-looking statements contained herein to reflect actual results, changes in assumptions or changes in factors affecting these statements. This material is not intended as and does not constitute an offer to sell any securities or a solicitation of any offer to purchase any securities.

More on www.bpost.be/ir

06.05.2015 (17:45 CET) Quarterly results 1Q15

13.05.2015 Ordinary General Meeting of Shareholders

18.05.2015 Ex-dividend date

20.05.2015 Payment date of the dividend

Financial Calendar

1 as defined among others under the U.S. Private Securities Litigation Reform Act of 1995

08.12.2015 Ex-dividend date (interim dividend)

10.12.2015 Payment date of the interim dividend

06.08.2015 (17:45 CET) Quarterly results 2Q15

05.11.2015 (17:45 CET) Quarterly results 3Q15

03.12.2015 (17:45 CET) Results first 10 months 2015

3

Highlights of 4Q14 – Expectations exceeded

4Q14

Volume decline of domestic mail better than previous 3 quarters • improved advertising and transactional mail, but still impacted by

e-substitution and cost cutting

Cost savings well on track • costs (excl. one-offs, phasing and transport) down organically • average FTE reduction of 664 for the quarter and 974 for the full year

Strong growth in parcels • solid domestic parcels volume growth helped by particularly strong

December month at +15.6%; but negative mix effect of -2.2% for the first time

• organic international parcels growth in line with 3Q14, shipments to China slowing down

-3.7%

+7.1%

+ € 10.9m

- € 9.9m

EBITDA significantly up (€ +9.5m) € 131.0m

€ 1.26 gross

Proposed total dividend per share up 11.5% € 1.04 already paid in December 2014 and € 0.22 to be proposed at Annual General Meeting

Revenues up 2.2% (+1.7% organically) • partially helped by higher building sales (EUR +3.8m)

€ 655.3m

4

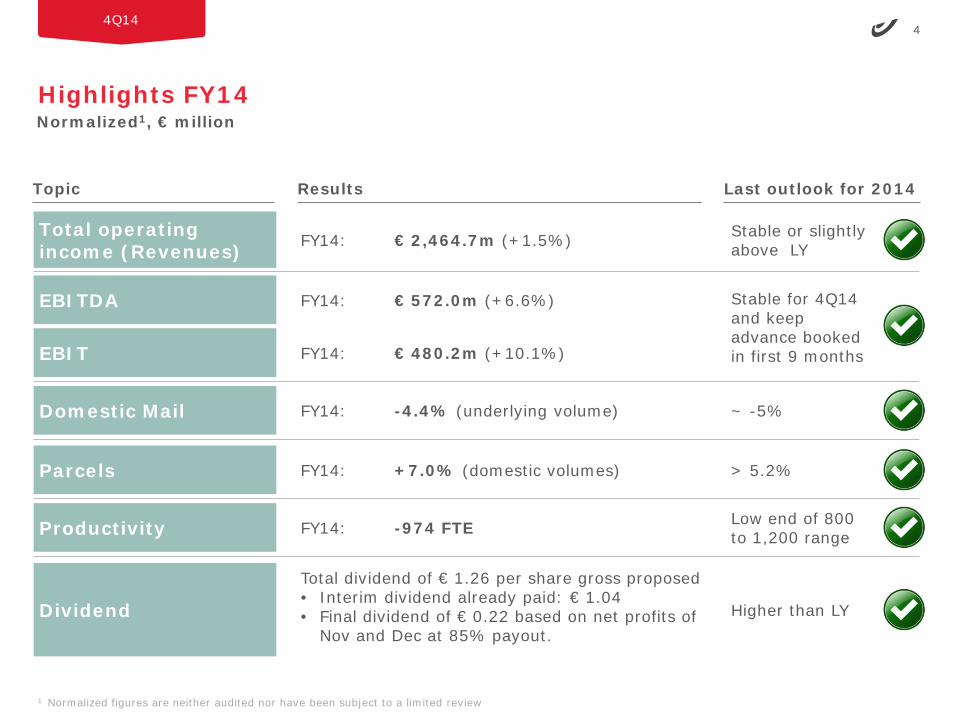

Highlights FY14

4Q14

Total operating income (Revenues) FY14: € 2,464.7m (+1.5%)

EBITDA

EBIT

Domestic Mail

Parcels

Productivity

Dividend

Normalized1, € million

1 Normalized figures are neither audited nor have been subject to a limited review

FY14: € 572.0m (+6.6%)

FY14: € 480.2m (+10.1%)

FY14: -4.4% (underlying volume)

FY14: +7.0% (domestic volumes)

FY14: -974 FTE

Total dividend of € 1.26 per share gross proposed • Interim dividend already paid: € 1.04 • Final dividend of € 0.22 based on net profits of

Nov and Dec at 85% payout.

Topic Results Last outlook for 2014

Stable or slightly above LY

Stable for 4Q14 and keep advance booked in first 9 months

~ -5%

> 5.2%

Low end of 800 to 1,200 range

Higher than LY

5

4Q14 EBITDA grew solidly thanks to Parcels, domestic mail volume decline better than previous quarters at -3.7% and costs under control taking into account growth of transport costs

4Q14

+3.7

+0.8

+11.7

Domestic Mail

-5.1

Scope

+0.4

EBITDA 4Q13

+121.6

+131.0

Parcels EBITDA 4Q14

Costs

-2.0

Corporate Additional sources of revenues

100% acquisition of Gout, BEurope, Ecom and Starbase by Landmark Global Inc.

Total operating income (revenues)

1 Normalized figures are neither audited nor have been subject to a limited review

€ +9.1m / +7.5%

Normalized1, € million

Of which building sales € +3.8m.

Including increase of one-offs and phasing by € 0.9m and transport costs by € 11.1m

6

Scope elements affecting results: small bolt-on acquisitions relating to international parcels activities

4Q14

Acquisition of Gout

InternationalBV and

BEurope

Acquisition of Ecom

Acquisition of Starbase

Topic Description High-level impact

Ch

ang

es in

sco

pe

• Additional operating income of € 2.1m and additional operating expenses of € 1.9m in 4Q14, bringing FY contributions to € 7.1m and € 6.0m respectively.

• Additional operating income of € 0.8m and additional operating expenses of € 0.7m in 4Q14, bringing FY contributions to € 2.1m and € 2.4m respectively.

• Additional operating income of € 0.3m and additional operating expenses of € 0.3m in 4Q14, bringing FY contributions to € 1.1m and € 1.1m respectively.

• In Jan. 2014, Landmark Global Inc. acquired 100% of the shares of Gout and BEurope both based in the Netherlands

• Both companies offer import services for customers looking to sell their products in Europe. This includes customs clearance services, warehousing, pick & pack and last mile delivery

• Landmark Global Inc. acquired 100% of the shares of Ecom Ltd in February 2014

• Import services for goods in UK

• Landmark Global Inc. acquired 100% of the shares of Starbase in February 2014 (based in US)

• Import services for goods in the US

7

Summary of key financials 4Q14

4Q14

1 Normalized figures are neither audited nor have been subject to a limited review

€ million

4Q13 4Q14 4Q13 4Q14 % ∆Total operating income (revenues) 640.9 655.3 640.9 655.3 2.2%Operating expenses 519.4 524.3 519.4 524.3 0.9%EBITDA 121.6 131.0 121.6 131.0 7.8%Margin (%) 19.0% 20.0% 19.0% 20.0%EBIT 86.8 102.8 86.8 102.8 18.4%Margin (%) 13.5% 15.7% 13.5% 15.7%Profit before tax 85.5 85.3 85.5 85.3 -0.2%Income tax expense 32.8 34.7 32.8 34.7 Net profit 52.7 50.7 52.7 50.7 -3.8%FCF 12.6 48.4 12.5 48.4 286.8%bpost S.A./N.V. net profit (BGAAP) 72.7 78.8 72.7 78.8 8.5%Net Debt/ (Net cash), at 31 December (360.7) (486.2) (360.7) (486.2) 34.8%

Reported Normalized1

8

Total operating income (revenues) of € 655.3m in 4Q14, increase of € 11.1m on an organic basis

4Q14

1 Normalized figures are neither audited nor have been subject to a limited review ² Scope including Gout International BV, BEurope, Ecom and Starbase ³ Defined as domestic and Belgian in- and outbound

Normalized1, € million

4Q13 Scope2 Organic 4Q14 % Org

Transactional mail 259.6 - -0.4 259.2 -0.2%Advertising mail 74.0 - -2.4 71.5 -3.3%Press 80.7 - -2.3 78.5 -2.8%

Domestic parcels3 39.0 - 1.9 40.9 4.9%International parcels 32.9 2.4 10.9 46.3 33.0%Special logistics 4.1 - -1.1 2.9 -27.3%

International mail 55.2 - 0.2 55.3 0.3%Value added services 22.9 - 0.8 23.7 3.6%Banking and financial 52.8 - -0.2 52.6 -0.5%Others 25.6 0.8 0.1 26.5 0.4%

Corporate -5.8 - 3.7 -2.1 -63.5%

640.9 3.2 11.1 655.3 1.7%

Domestic mail

Parcels

Additional sources of revenues

TOTAL

9

Domestic Mail underlying volume decline at -3.7% as a result of lower volume decline both in transactional mail and advertising mail

4Q14

6.9

409.2

-5.1

4Q14

Price/Mix

Volume -12.8

Working day impact 0.9

4Q13 414.3

Normalized1 total operating income (revenues), € million

1 Normalized figures are neither audited nor have been subject to a limited review 2 2Q14 was impacted by elections. In 3Q14 we had 1 business working day less and in 4Q14 we had 1 business working day more compared to 2013. In terms of

working days for 2015, 1Q15, 2Q15 and 4Q15 will be equal to same quarters of 2014. In 3Q15 we will have 1 business working day more.

• 1 business working day more. • Underlying volume decline at -3.7% from both lower

volume decline in Transactional and Advertising mail. • Transactional mail remained affected by e-substitution

and cost reduction measures although no new aggressive measures were implemented by customers.

• Advertising mail trend improved in part as a result of stronger performance from some food retailers and slower decline of catalogue sellers.

1Q14 2Q14 3Q14 4Q14 YTD14 1Q14 2Q14 3Q14 4Q14 YTD14Transactional mail -5.3% -5.2% -5.1% -3.1% -4.7% -5.3% -5.9% -4.7% -4.2% -5.0%Advertising mail -2.7% 2.0% -3.7% -3.4% -1.9% -2.7% -3.6% -3.7% -2.1% -3.0%Press -3.2% -2.9% -2.5% -2.6% -2.8% -3.2% -2.9% -2.5% -2.6% -2.8%Domestic Mail -4.6% -3.6% -4.6% -3.1% -3.9% -4.6% -5.1% -4.3% -3.7% -4.4%

Reported Underlying²

10

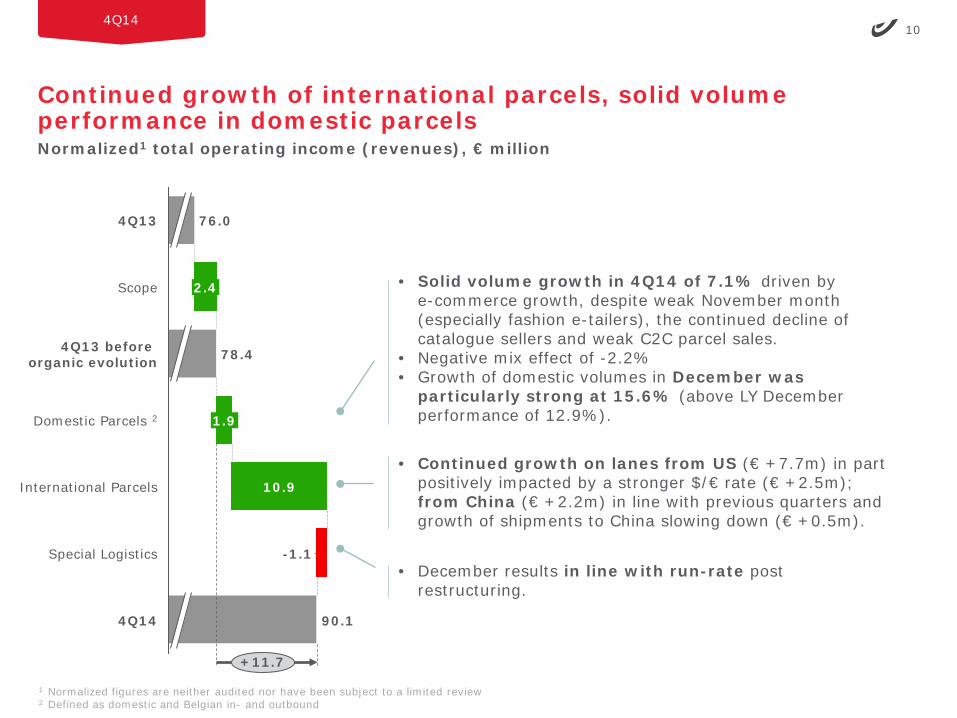

Continued growth of international parcels, solid volume performance in domestic parcels

4Q14

Normalized1 total operating income (revenues), € million

1 Normalized figures are neither audited nor have been subject to a limited review 2 Defined as domestic and Belgian in- and outbound

90.1

+11.7

4Q14

Special Logistics -1.1

International Parcels 10.9

Domestic Parcels 2 1.9

4Q13 before organic evolution 78.4

76.0 4Q13

2.4 Scope • Solid volume growth in 4Q14 of 7.1% driven by e-commerce growth, despite weak November month (especially fashion e-tailers), the continued decline of catalogue sellers and weak C2C parcel sales.

• Negative mix effect of -2.2% • Growth of domestic volumes in December was

particularly strong at 15.6% (above LY December performance of 12.9%).

• Continued growth on lanes from US (€ +7.7m) in part positively impacted by a stronger $/€ rate (€ +2.5m); from China (€ +2.2m) in line with previous quarters and growth of shipments to China slowing down (€ +0.5m).

• December results in line with run-rate post restructuring.

11

Additional sources of revenues holding well

4Q14

Normalized1 total operating income (revenues), € million

1 Normalized figures are neither audited nor have been subject to a limited review

0.8

0.8

156.5

158.1

+0.8

4Q13

4Q14

Others 0.1

Banking & Financial -0.2

VAS

International Mail 0.2

4Q13 before organic evolution 157.3

Scope

• Excluding lower one-off settlements relating to last year (€ -0.7m) and positive FX impact (€ +1.8m), international mail sales were slightly down.

• Mainly less service fee (€ -0.4m) paid as a result of cost optimization of activities performed on behalf of bpost bank and lower volumes of financial transactions managed on behalf of the Belgian state while prepaid cards continued to grow (€ +0.3m).

• Higher assets under management offset by lower transformation margin and lower insurance production.

• Contribution of solutions thanks to European license plates.

12

Costs remained well under control and were down € 9.9m on an underlying basis (excl. one-offs, phasing and transport)

4Q14

Operating expenses excl. depreciation and amortization, Normalized1, € million

1 Normalized figures are neither audited nor have been subject to a limited review

3.5

524.3 -9.9

4Q14

Other costs -0.3

Other SG&A

Payroll & Interim -13.1

4Q13 excl. one-off, phasing & transport 534.2

Transport costs 11.1

One-off & phasing 0.9

4Q13 before organic evolution 522.2

Scope 2.9

4Q13 519.4

• Increase in consultancy costs, 3rd party costs, advertising costs (parcels) and other services, partly compensated by the decrease in maintenance costs and energy delivery.

• Total FTE reduction of 664 FTE (€-9.1m), partly supported by a hiring freeze since the start of the Alpha analysis (48 FTE).

• Positive mix impact of € -0.8m mainly thanks to the recruitment of auxiliary postmen as well as other factors accounting for € -3.2m.

• Increase in transport costs relating to the evolution of international activities, including FX impact (€ +3.3m)

• Terminal dues one-offs (€ +4.1m) and phasing impact (€ +2.7m) both relating to last year in transport costs.

• Phasing and one-off effects relating mainly to payroll restructuring charges (€ +6.3m) and employee benefits provision movements (€ -8.0m).

• Decrease in provisions (€ -4.2m) in other costs.

13

Operating free cash flow1 of € +48.4m in 4Q14

4Q14

• Lower capital expenditure in 4Q14 (€ +3.2m) • Higher proceeds sale of buildings in 4Q14 (€ +7.3m) due to the sale of a large

property

• Lower results of operating activities (€ -9.2m) mainly due to higher prepayment income taxes in 4Q14 (€ -10.0m)

• Positive evolution of the working capital vs. 4Q13 (€ +34.6m). Working capital was positively influenced by terminal dues mainly related to the earlier settlement of another postal operator (which will negatively impact 2015), and an access fee (€ +5.0m) paid by a partner in financial services

1 Operating free cash flow = cash flow from operating activities + cash flow from investing activities, excludes the impact of the 2013 repayment of prior compensation, following the 2012 EU ruling and deposits received from 3rd parties.

€ million

• Interim dividend payment is € -22.0m higher than last year

€ million 4Q13 4Q14 Delta

Cash flow from operating activities +46.4 +71.8 +25.4Cash flow from investing activities -33.9 -23.4 +10.5Operating free cash flow1 +12.5 +48.4 +35.9Financing activities -195.3 -217.7 -22.4Net cash movement -182.8 -169.3 +13.5

Capex +37.2 +34.0 -3.2

14

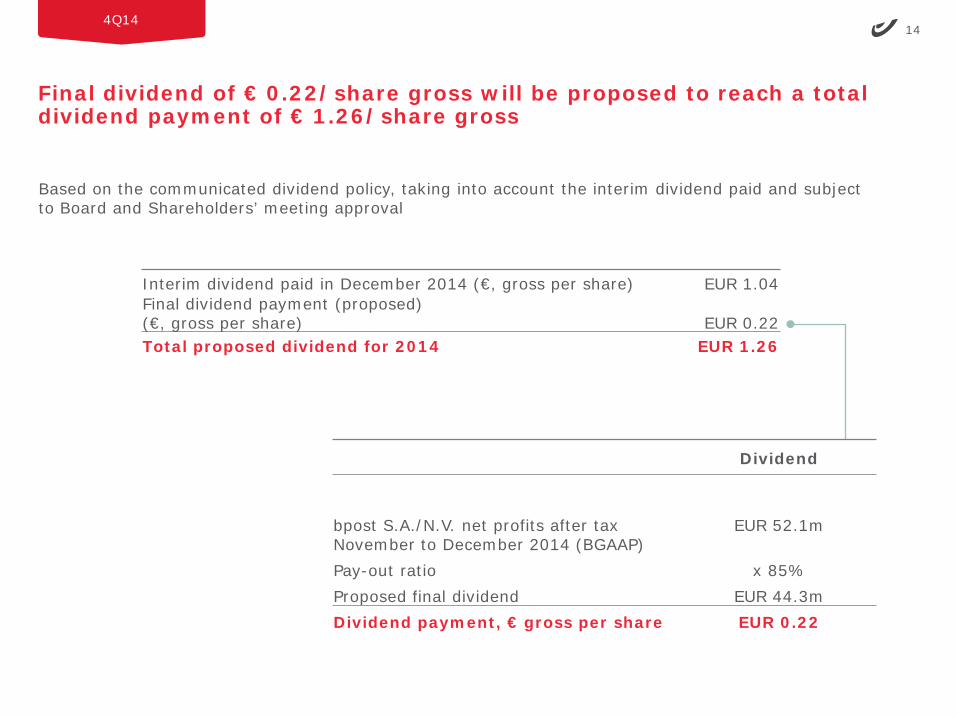

Final dividend of € 0.22/share gross will be proposed to reach a total dividend payment of € 1.26/share gross

4Q14

Based on the communicated dividend policy, taking into account the interim dividend paid and subject to Board and Shareholders’ meeting approval

Dividend

bpost S.A./N.V. net profits after tax November to December 2014 (BGAAP)

EUR 52.1m

Pay-out ratio x 85% Proposed final dividend EUR 44.3m Dividend payment, € gross per share EUR 0.22

Interim dividend paid in December 2014 (€, gross per share) EUR 1.04 Final dividend payment (proposed) (€, gross per share) EUR 0.22 Total proposed dividend for 2014 EUR 1.26

15

Strong balance sheet structure

4Q14

€ million

PPE & intangible assets

Inventories

Trade & other receivables

Investments in associates

Other assets

Cash & cash equivalents

Dec 31, 2014

2,121.8

655.2

12.5

400.8

416.5

74.4

562.3

Dec 31, 2013

1,929.2

659.2

9.2

402.4

341.3

68.7

448.2

86.9

Employee benefits

Total equity

Trade & other payables

Provisions

Interest-bearing loans & borrowings

Dec 31, 2014

2,121.8

681.4

368.6

931.4

64.8 75.6

Dec 31, 2013

1,929.2

576.9

345.1

857.7

62.6

Assets Equity and liabilities

16

Outlook for 2015

4Q14

• After a very strong 2014 which allowed us to report historically high numbers, we will be facing some headwind in 2015:

• We expect mail volumes to remain under substantial pressure from e-substitution. As a consequence we plan for mail a volume decline of over -5%. This has been confirmed by a relatively soft start of the year in mail.

• The compensation for the SGEI’s (management contract) will be € 16.5m lower than in 2014 as the government has decided to reduce the compensation above and beyond the already lower contractual cap.

• Parcels to China (milk powder) are no longer growing and could be declining.

• The planned productivity improvements as per the Vision 2020 planning are at the very low end of our 800 to 1,200 FTE/year range.

• On the positive side, we still expect mid single digit growth in domestic parcels in spite of the intensification of competition. We also expect continued growth in the US and Asia parcels segment.

• On balance, our ambition is to hold our recurring EBIT(DA) at the high level achieved in 2014 thanks to the partial effects of the Alpha plan and a continued focus on costs. Reported EBIT will be affected by the Alpha restructuring cost. Our ambition is to achieve the same level of dividend payment.

• Cash generation should follow normal seasonality and net capex is expected at around € 90m. Working capital will be negatively affected by the favorable phasing on terminal dues payment in 2014.

Appendix: Full year 2014 details

Brussels – March, 17th 2015

18

FY14 EBITDA grew solidly thanks to solid revenue growth both in parcels and additional sources of revenues along with continued cost savings

FY14

+8.6+8.0

+49.6

Domestic Mail

-28.3

Scope

+0.8

EBITDA FY13

+536.9

EBITDA FY14

+572.0

Costs Corporate

-3.5

Additional sources of revenues

Parcels

100% acquisition of Gout, BEurope, Ecom and Starbase by Landmark Global Inc.

Of which building sales € -2.3m.

Total operating income (revenues)

1 Normalized figures are neither audited nor have been subject to a limited review

€ +34.4m / +6.4%

Normalized1, € million

Including increase of transport costs by € 38.2m

19

Summary of key financials FY14

FY14

1 Normalized figures are neither audited nor have been subject to a limited review

€ million

FY13 FY14 FY13 FY14 % ∆Total operating income (revenues) 2,443.2 2,464.7 2,428.6 2,464.7 1.5%Operating expenses 1,891.7 1,892.6 1,891.7 1,892.6 0.0%EBITDA 551.4 572.0 536.9 572.0 6.6%Margin (%) 22.6% 23.2% 22.1% 23.2%EBIT 450.7 480.2 436.1 480.2 10.1%Margin (%) 18.4% 19.5% 18.0% 19.5%Profit before tax 456.8 454.1 442.2 454.1 2.7%Income tax expense 168.9 158.6 168.9 158.6 Net profit 287.9 295.5 273.3 295.5 8.1%FCF 125.9 373.3 249.0 373.5 50.0%bpost S.A./N.V. net profit (BGAAP) 248.2 296.9 248.2 296.9 19.6%Net Debt/ (Net cash), at 31 Dec. (360.7) (486.2) (360.7) (486.2) 34.8%

Reported Normalized1

2013: gain of € 14.6m from sale of Certipost divisions

20

Total operating income (revenues) of € 2,464.7m in FY14, increase of € 25.8m on an organic basis

FY14

1 Normalized figures are neither audited nor have been subject to a limited review ² Scope including Gout International BV, BEurope, Ecom and Starbase ³ Defined as domestic and Belgian in- and outbound

Normalized1, € million

FY13 Scope2 Organic FY14 % Org

Transactional mail 961.3 - -18.0 943.2 -1.9%Advertising mail 275.9 - -4.5 271.4 -1.6%Press 314.1 - -5.8 308.4 -1.8%

Domestic parcels3 141.9 - 9.4 151.3 6.7%International parcels 91.5 8.1 43.7 143.3 47.7%Special logistics 16.2 - -3.6 12.6 -22.0%

International mail 199.3 0.0 4.4 203.7 2.2%Value added services 89.4 - 6.0 95.4 6.7%Banking and financial 209.2 - -1.8 207.5 -0.8%Others 104.4 2.3 -0.6 106.0 -0.6%

Corporate 25.5 - -3.5 21.9 -13.9%

2,428.6 10.3 25.8 2,464.7 1.1%

Domestic mail

Parcels

Additional sources of revenues

TOTAL

21

Domestic mail underlying volume decline at -4.4%

FY14

26.7Price/Mix

-28.3

FY14 1,523.0

Volume -59.5

Elections & working day 4.6

FY13 1,551.3

Normalized1 total operating income (revenues), € million

1 Normalized figures are neither audited nor have been subject to a limited review 2 2Q14 was impacted by elections. In 3Q14 we had 1 business working day less and in 4Q14 we had 1 business working day more compared to 2013. In terms of

working days for 2015, 1Q15, 2Q15 and 4Q15 will be equal to same quarters of 2014. In 3Q15 we will have 1 business working day more.

• In 2014, elections’ contribution amounted to € +4.6m. • Underlying volume decline at -4.4%. • Transactional mail affected by e-substitution (with some

large customers implementing aggressive measures) and cost cutting. Some one-off mailings and specific actions from customers impacted the 2H volume trend positively.

• Advertising mail benefiting from food retailers despite continued decline of catalogue sellers.

1Q14 2Q14 3Q14 4Q14 YTD14 1Q14 2Q14 3Q14 4Q14 YTD14Transactional mail -5.3% -5.2% -5.1% -3.1% -4.7% -5.3% -5.9% -4.7% -4.2% -5.0%Advertising mail -2.7% 2.0% -3.7% -3.4% -1.9% -2.7% -3.6% -3.7% -2.1% -3.0%Press -3.2% -2.9% -2.5% -2.6% -2.8% -3.2% -2.9% -2.5% -2.6% -2.8%Domestic Mail -4.6% -3.6% -4.6% -3.1% -3.9% -4.6% -5.1% -4.3% -3.7% -4.4%

Reported Underlying²

22

Continued solid growth of domestic and international parcels

FY14

Normalized1 total operating income (revenues), € million

1 Normalized figures are neither audited nor have been subject to a limited review 2 Defined as domestic and Belgian in- and outbound

43.7

9.4

307.2

FY13 before organic evolution 257.7

Scope 8.1

FY13 249.6

International Parcels

-3.6 Special Logistics

FY14

+49.6

Domestic Parcels 2 • Continued solid volume growth of domestic parcels

reaching 7.0% despite a continued decline of catalogue sellers and weak C2C parcel sales.

• Turnaround of activities implemented: revenues decreased as a result of discontinuing the activities in distribution & warehousing.

• Continued growth from US (€ +22.7m), from China (€ +8.6m) and shipments to China (€ +8.3m).

23

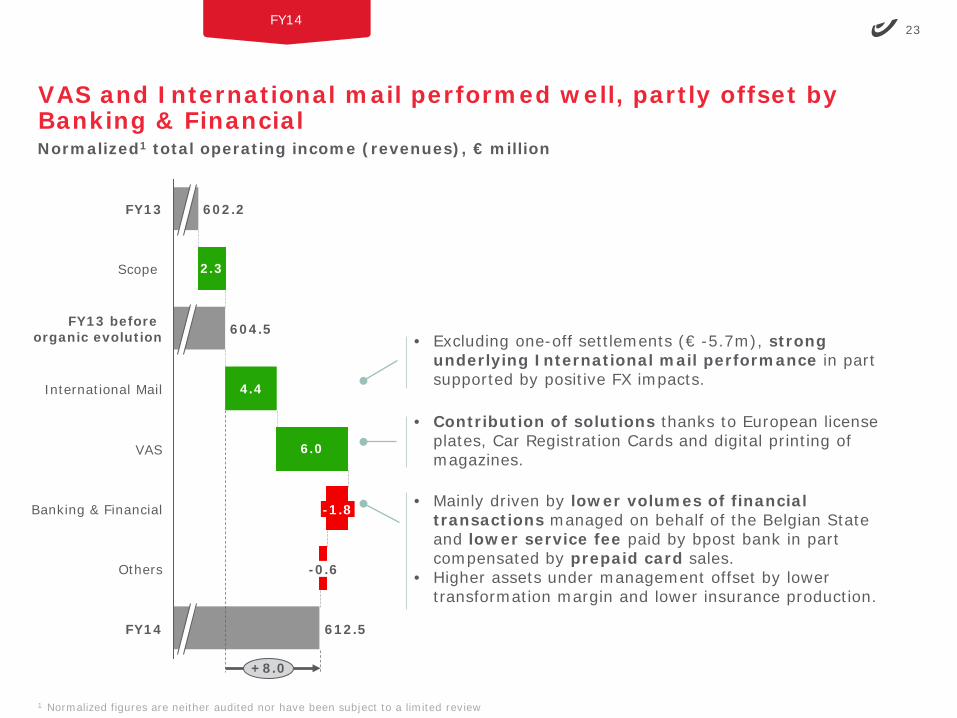

VAS and International mail performed well, partly offset by Banking & Financial

FY14

Normalized1 total operating income (revenues), € million

1 Normalized figures are neither audited nor have been subject to a limited review

4.4

6.0

2.3

Banking & Financial

-0.6 Others

FY14

+8.0

612.5

-1.8

VAS

International Mail

FY13 before organic evolution 604.5

Scope

FY13 602.2

• Excluding one-off settlements (€ -5.7m), strong underlying International mail performance in part supported by positive FX impacts.

• Mainly driven by lower volumes of financial transactions managed on behalf of the Belgian State and lower service fee paid by bpost bank in part compensated by prepaid card sales.

• Higher assets under management offset by lower transformation margin and lower insurance production.

• Contribution of solutions thanks to European license plates, Car Registration Cards and digital printing of magazines.

24

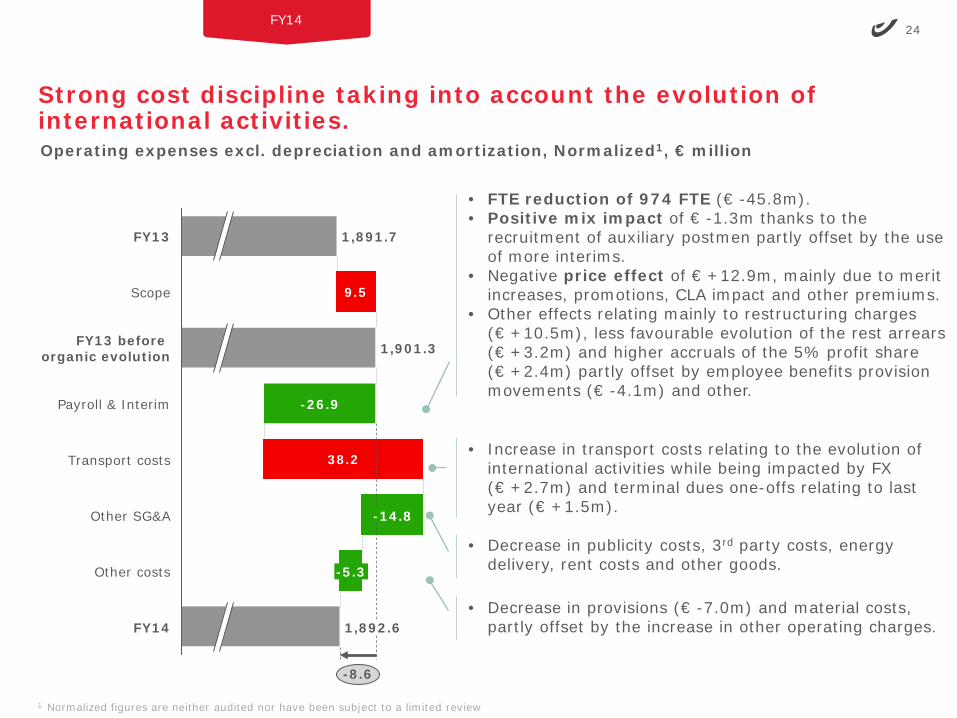

Strong cost discipline taking into account the evolution of international activities.

FY14

Operating expenses excl. depreciation and amortization, Normalized1, € million

1 Normalized figures are neither audited nor have been subject to a limited review

38.2

9.5

FY14

-5.3 Other costs

1,892.6

Other SG&A

Scope

1,891.7 FY13

1,901.3 FY13 before organic evolution

-26.9 Payroll & Interim

Transport costs

-14.8

-8.6

• FTE reduction of 974 FTE (€ -45.8m). • Positive mix impact of € -1.3m thanks to the

recruitment of auxiliary postmen partly offset by the use of more interims.

• Negative price effect of € +12.9m, mainly due to merit increases, promotions, CLA impact and other premiums.

• Other effects relating mainly to restructuring charges (€ +10.5m), less favourable evolution of the rest arrears (€ +3.2m) and higher accruals of the 5% profit share (€ +2.4m) partly offset by employee benefits provision movements (€ -4.1m) and other.

• Increase in transport costs relating to the evolution of international activities while being impacted by FX (€ +2.7m) and terminal dues one-offs relating to last year (€ +1.5m).

• Decrease in publicity costs, 3rd party costs, energy

delivery, rent costs and other goods.

• Decrease in provisions (€ -7.0m) and material costs, partly offset by the increase in other operating charges.

25

Operating free cash flow1 of € +373.5m in 2014

FY14

• Higher capital expenditure in 2014 (€ -11.8m) mainly related to extensions of the sorting centres and the installation of new sorting machines

• Lower proceeds sale of buildings (€ -5.5m) • Newly acquired subsidiaries in 2014 (€ -9.1m) while LY was impacted by capital increase bpost

bank (€ +37.5m), sale of Certipost (€-15.1m) and purchase MSI shares (€ +6.8m)

• Improved results of operating activities (€ +35.1m) • Positive evolution of the working capital vs. LY (€ +86.8m). Besides LY payment related to the

competition claim fine (€ +37.4m), working capital was positively influenced by terminal dues (€ +18.4m), mainly related to the earlier settlement of another postal operator, improvement in payments by State entities (€ +14.2m), the access fee paid by a partner in financial services (€ +5.0m) and LY advance for Gout acquisition which was utilized this year (net impact € 6.0m)

1 Operating free cash flow = cash flow from operating activities + cash flow from investing activities, excludes the impact of the 2013 repayment of prior compensation, following the 2012 EU ruling and deposits received from 3rd parties.

2 Financing activities includes the impact of the 2013 repayment of prior compensation and deposits received from 3rd parties.

€ million

• LY repayment of SGEI overcompensation (€ +123.1m) and decapitalisation/exceptional dividends (€ +198.0m)

• In 2014, higher dividend pay-out (€ -60.7m – impact of interim dividend, dividend to shareholders and minority interests together)

• Higher payments related to borrowings and financing lease liabilities in 2014 (€ -5.8m)

€ million FY13 FY14 Delta

Cash flow from operating activities +329.7 +451.7 +122.0Cash flow from investing activities -80.7 -78.2 +2.5Operating free cash flow1 +249.0 +373.5 +124.5Financing activities2 -513.8 -259.5 +254.3Net cash movement -264.7 +114.0 +378.7

Capex +79.2 +90.9 +11.8

26

Key contacts

Pierre Winand

CFO, Service Operations and ICT

• Email: [email protected] • Direct: + 32 (0)2 276 22 35 • Mobile: +32 (0) 494 566 348 • Address: bpost, Centre Monnaie, 1000 Brussels, Belgium

Paul Vanwambeke

Director Investor Relations

• Email: [email protected] • Direct: + 32 (0)2 276 28 22 • Mobile: +32 (0) 497 591 335 • Address: bpost, Centre Monnaie, 1000 Brussels, Belgium

Saskia Dheedene

Manager Investor Relations

• Email: [email protected] • Direct: + 32 (0)2 276 76 43 • Mobile: +32 (0) 477 922 343 • Address: bpost, Centre Monnaie, 1000 Brussels, Belgium