interim condensed consolidated financial...

TRANSCRIPT

Interim condensed consolidated financial statements PJSC Sovcombank

for the six months ended 30 June 2015

with review report

Interim condensed consolidated financial statements PJSC Sovcombank

2

Contents

Page

Report on review of the interim condensed consolidated financial

statements 3 Interim condensed consolidated statement of comprehensive income 5 Interim condensed consolidated statement of financial position 6 Interim condensed consolidated statement of changes in net assets

attributable to participants 7 Interim condensed consolidated statement of cash flows 8 Notes to the interim condensed consolidated financial statements which

are its integral part Background 9 1. Basis of preparation 9 2. Business combinations 12 3. Reclassification 17 4. Allowance for loan impairment 17 5. Fee and commission income 18 6. Other operating income 18 7. Other impairment and provisions 18 8. Personnel expenses 18 9.

Other general and administrative expenses 19 10. Income tax expense 19 11. Cash and cash equivalents 19 12. Financial instruments at fair value through profit or loss 20 13. Loans to customers 20 14. Held-to-maturity investment securities 23 15. Current accounts and deposits from customers 24 16. Amounts due to the CBR 24 17. Deposits and balances from banks 24 18. Debt securities issued 24 19. Subordinated debt 24 20. Fair value of financial instruments 25 21. Share capital and other contributions to share capital 27 22. Taxation contingencies 28 23. Related party transactions 28 24. Share of investments in joint venture 30 25. Principal subsidiaries 31 26. Subsequent events 32 27.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

9

Background 1. Principal activities These consolidated financial statements include the financial statements of Public Joint-Stock Company Sovcombank (the "Bank" or "Sovcombank") and its subsidiaries (together referred to as the "Group" or "Sovcombank Group"). The list of principal consolidated subsidiaries included in these consolidated financial statements of Sovcombank Group is disclosed in Note 26. Sovcombank, the parent company of the Group, was originally established in the city of Kostroma as a limited liability company in 1990. The Bank’s registered legal address is Russia, 156000, Kostroma, prospekt Tekstilshchikov, 46. The Bank operates under general banking license No. 963 issued by the Central Bank of the Russian Federation (the "CBR"). The Bank also holds licenses for securities operations and custody services from the Federal Commission for the Securities Market (the "FSMC") issued on 7 February 2006. The Bank is a member of the deposit insurance system of the Russian Federation. The Bank accepts deposits from the public and extends credit, transfers payments in Russia and abroad, performs transactions with securities, exchanges currencies and provides other banking services to its retail and commercial customers. The main office of the Bank is in Kostroma. As at 30 June 2015, the Bank operates in 901 cities, towns and villages across 49 subjects of Russian Federation. The Bank had 7,728 employees as at 30 June 2015 (7,850 as at 31 December 2014). Participants As at 30 June 2015 and 31 December 2014, the Group's ownership was as follows:

Ownership, % Ownership, % 30 June 2015 31 December 2014

SovCo Capital Partners B.V. 100.00% 100.00% There is no single ultimate legal entity or individual that exercised control over the Group as at 30 June 2015 and 31 December 2014. SovCo Capital Partners B.V., a legal entity incorporated in the Netherlands, is the shareholder of the Group since 2003. SovCo Capital Partners B.V. is controlled by a group of Russian businessmen, including key members of Management. Operating environment Russia continues economic reforms and development of its legal, tax and regulatory frameworks as required by a market economy. The future stability of the Russian economy is largely dependent upon these reforms and developments and the effectiveness of economic, financial and monetary measures undertaken by the government of the Russian Federation. In 2015, a significant drop in crude oil prices and a significant devaluation of the Russian ruble, as well as sanctions imposed on Russia by several countries in 2014 continued to have an adverse effect on the Russian economy. The ruble interest rates remained high as a result of raising the key interest rate by the Central Bank of Russia in December 2014 with an incremental decrease in 2015. The combination of the above resulted in reduced access to capital, a higher cost of capital, increased inflation and uncertainty regarding economic growth, which may negatively affect the Group’s future financial position, results of operations and business prospects. Management believes that it is taking appropriate measures to support the sustainability of the Group's business in the current circumstances.

Basis of preparation 2. General These interim condensed consolidated financial statements for the six months ended 30 June 2015 have been prepared in accordance with International Accounting Standard (IAS) 34 Interim Financial Reporting. The interim condensed consolidated financial statements do not include all the information and disclosures required in the annual financial statements, and should be read in conjunction with the Group’s annual financial statements for the twelve months ended 31 December 2014.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

10

2. Basis of preparation (continued) Changes in accounting policies The nature and the effect of these changes are disclosed below. Although these new standards and amendments apply for the first time in 2015, they do not have a material effect on the annual consolidated financial statements or the interim condensed consolidated financial statements of the Group. The nature and the impact of each standard or amendment are described below: The accounting policies adopted in the preparation of the interim condensed consolidated financial statements are consistent with those followed in the preparation of the Group’s annual financial statements for the year ended 31 December 2014, except for the adoption of new standards as at 1 January 2015, noted below. The Group has not adopted early any other standard, interpretation or amendment that has been issued but is not yet effective. Amendments to IAS 19 Defined Benefit Plans: Employee Contributions IAS 19 requires an entity to consider contributions from employees or third parties when accounting for defined benefit plans. Where the contributions are linked to service, they should be attributed to periods of service as a negative benefit. These amendments clarify that, if the amount of the contributions is independent of the number of years of service, an entity is permitted to recognize such contributions as a reduction in the service cost in the period in which the service is rendered, instead of allocating the contributions to the periods of service. The amendments are effective for annual periods beginning on or after 1 July 2014. These amendments had no impact on the Group, since none of the entities within the Group has defined benefit plans with contributions from employees or third parties. Annual improvements 2010-2012 These improvements are effective from 1 July 2014 and the Group has applied these amendments for the first time in these interim condensed consolidated financial statements. They include: IFRS 2 Share-based Payment This improvement is applied prospectively and clarifies various issues relating to the definitions of performance and service conditions which are vesting conditions, including:

• A performance condition must contain a service condition.

• A performance target must be met while the counterparty is rendering service.

• A performance target may relate to the operations or activities of an entity, or to those of another entity in the same group.

• A performance condition may be a market or non-market condition.

• If the counterparty, regardless of the reason, ceases to provide service during the vesting period, the service condition is not satisfied.

The above approaches are the same as those used by the Group to define performance and service conditions that are vesting conditions. Thus, this amendment does not impact the accounting policy of the Group. IFRS 3 Business Combinations The amendment is applied prospectively and clarifies that all contingent consideration arrangements classified as liabilities (or assets) arising from a business combination should be subsequently measured at fair value through profit or loss whether or not they fall within the scope of IFRS 9 (or IAS 39, as applicable). These provisions are consistent with the Group's current accounting policies. Therefore, this amendment has no impact on the Group’s accounting policies. IFRS 8 Operating Segments Theese amendments are applied retrospectively and clarify that:

• An entity must disclose the judgments made by management in applying the aggregation criteria in paragraph 12 of IFRS 8, including a brief description of operating segments that have been aggregated and the economic characteristics (e.g., sales and gross margins) used to assess whether the segments are 'similar'.

• The reconciliation of segment assets to total assets is only required to be disclosed if the reconciliation is reported to the chief operating decision maker, similar to the required disclosure for segment liabilities.

The Group did not apply the aggregation criteria provided in paragraph 12 of IFRS 8.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

11

2. Basis of preparation (continued) Changes in accounting policies (continued) IFRS 13 Short-term Receivables and Payables – Amendments to IFRS 13 This amendment to IFRS 13 clarifies in the Basis for Conclusions that short-term receivables and payables with no stated interest rates can be measured at invoice amounts when the effect of discounting is immaterial. These provisions are consistent with the Group's current accounting policies, therefore, this amendment has no impact on the Group’s accounting policies. IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets The amendment is applied retrospectively and clarifies in IAS 16 and IAS 38 that the asset may be revalued by reference to observable data on either the gross or the net carrying amount. In addition, the accumulated depreciation or amortization is the difference between the gross and carrying amounts of the asset. The Group did not record any revaluation adjustments during the current interim period. IAS 24 Related Party Disclosures The amendment is applied retrospectively and clarifies that a management entity (an entity that provides key management personnel services) is a related party subject to the related party disclosures. In addition, an entity that uses a management entity is required to disclose the expenses incurred for management services. The amendment is not relevant for the Group as the Group does not receive any management services from other entities. Annual improvements 2011-2013 These improvements are effective from 1 July 2014 and the Group has applied these amendments for the first time in these interim condensed consolidated financial statements. They include: IFRS 3 Business Combinations The amendment is applied prospectively and clarifies for the scope exceptions within IFRS 3 that:

• Joint arrangements, not just joint ventures, are outside the scope of IFRS 3.

• This scope exception applies only to the accounting in the financial statements of the joint arrangement itself. The amendment is not relevant to the Group and its subsidiaries as the Group is not a joint venture. IFRS 13 Fair Value Measurement The amendment is applied prospectively and clarifies that the portfolio exception in IFRS 13 can be applied not only to financial assets and financial liabilities, but also to other contracts within the scope of IFRS 9 (or IAS 39, as applicable). The Group does not apply the exception provided in IFRS 13 for companies holding a group of financial assets and liabilities (portfolio) and managing this group as a whole. IAS 40 Investment Property The description of ancillary services in IAS 40 differentiates between investment property and owner-occupied property (i.e., property, plant and equipment). The amendment is applied prospectively and clarifies that IFRS 3, and not the description of ancillary services in IAS 40, is used to determine if the transaction is the purchase of an asset or business combination. The Group relies on IFRS 3, not IAS 40, in determining whether the transaction is the purchase of an asset or a business combination. Thus, this amendment does not impact the accounting policy of the Group. Meaning of effective IFRSs – Amendments to IFRS 1 The amendment clarifies in the Basis for Conclusions that an entity may choose to apply either a current standard or a new standard that is not yet mandatory, but permits early application, provided that either standard is applied consistently throughout the periods presented in the entity's first IFRS financial statements. Since the Group prepares its financial accounts in accordance with IFRS, this standard is not relevant for the Group.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

12

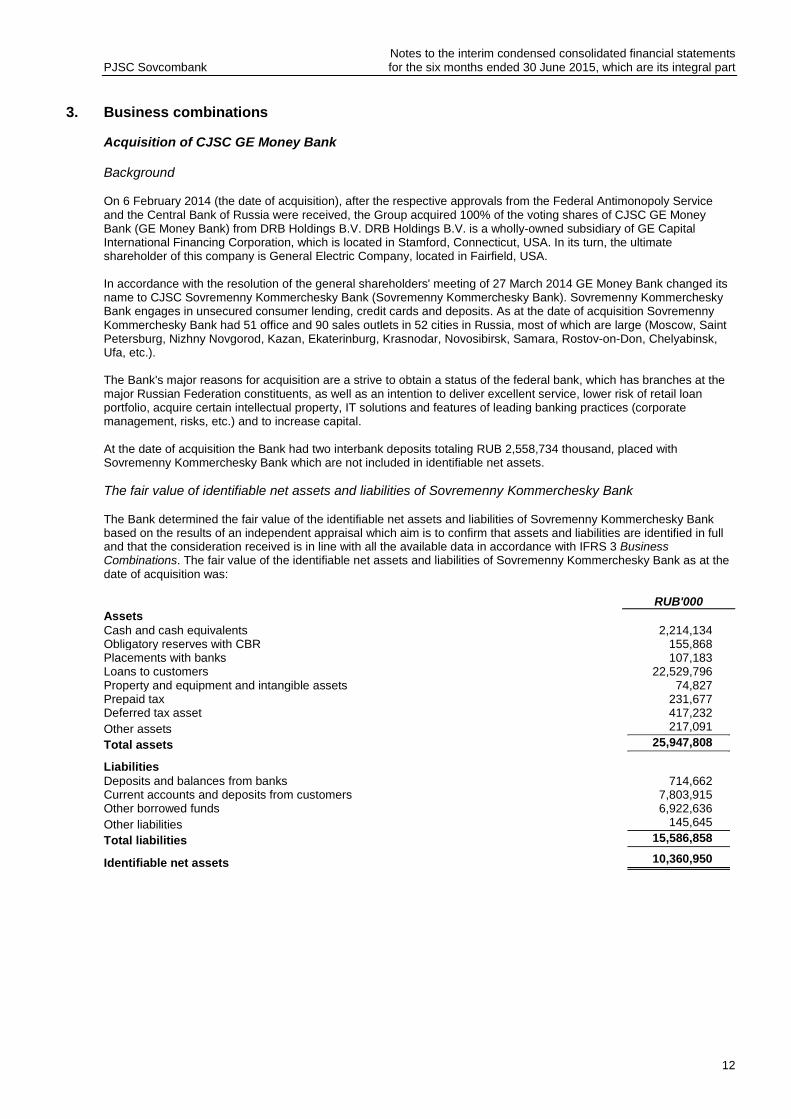

Business combinations 3. Acquisition of CJSC GE Money Bank Background On 6 February 2014 (the date of acquisition), after the respective approvals from the Federal Antimonopoly Service and the Central Bank of Russia were received, the Group acquired 100% of the voting shares of CJSC GE Money Bank (GE Money Bank) from DRB Holdings B.V. DRB Holdings B.V. is a wholly-owned subsidiary of GE Capital International Financing Corporation, which is located in Stamford, Connecticut, USA. In its turn, the ultimate shareholder of this company is General Electric Company, located in Fairfield, USA. In accordance with the resolution of the general shareholders' meeting of 27 March 2014 GE Money Bank changed its name to CJSC Sovremenny Kommerchesky Bank (Sovremenny Kommerchesky Bank). Sovremenny Kommerchesky Bank engages in unsecured consumer lending, credit cards and deposits. As at the date of acquisition Sovremenny Kommerchesky Bank had 51 office and 90 sales outlets in 52 cities in Russia, most of which are large (Moscow, Saint Petersburg, Nizhny Novgorod, Kazan, Ekaterinburg, Krasnodar, Novosibirsk, Samara, Rostov-on-Don, Chelyabinsk, Ufa, etc.). The Bank's major reasons for acquisition are a strive to obtain a status of the federal bank, which has branches at the major Russian Federation constituents, as well as an intention to deliver excellent service, lower risk of retail loan portfolio, acquire certain intellectual property, IT solutions and features of leading banking practices (corporate management, risks, etc.) and to increase capital. At the date of acquisition the Bank had two interbank deposits totaling RUB 2,558,734 thousand, placed with Sovremenny Kommerchesky Bank which are not included in identifiable net assets. The fair value of identifiable net assets and liabilities of Sovremenny Kommerchesky Bank The Bank determined the fair value of the identifiable net assets and liabilities of Sovremenny Kommerchesky Bank based on the results of an independent appraisal which aim is to confirm that assets and liabilities are identified in full and that the consideration received is in line with all the available data in accordance with IFRS 3 Business Combinations. The fair value of the identifiable net assets and liabilities of Sovremenny Kommerchesky Bank as at the date of acquisition was:

RUB'000

Assets Cash and cash equivalents 2,214,134

Obligatory reserves with CBR 155,868 Placements with banks 107,183 Loans to customers 22,529,796 Property and equipment and intangible assets 74,827 Prepaid tax 231,677 Deferred tax asset 417,232 Other assets 217,091 Total assets 25,947,808 Liabilities Deposits and balances from banks 714,662 Current accounts and deposits from customers 7,803,915 Other borrowed funds 6,922,636 Other liabilities 145,645 Total liabilities 15,586,858

Identifiable net assets 10,360,950

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

13

3. Business combinations (continued) Acquisition of CJSC GE Money Bank (continued) Gain on a bargain purchase Due to the fact that the fair value of identifiable net assets and liabilities of Sovremenny Kommerchesky Bank exceeded consideration transferred to DRB Holdings B.V. on acquisition, the Bank recorded gain on a bargain purchase within profit or loss in other operating income (Note 7). Gain on a bargain purchase of business as at the date of acquisition comprised:

RUB'000

Transferred consideration 5,294,909 Interbank deposits placed with Sovremenny Kommerchesky Bank 2,558,734 Fair value of the identifiable net assets of Sovremenny Kommerchesky Bank as at the date of

acquisition (10,360,950)

Gain on a bargain purchase (Note 7) (2,507,307) Consideration on acquisition was paid to DRB Holdings B.V. in cash. Profit and loss of Sovremenny Kommerchesky Bank for the six months ended 30 June 2014 Profit of Sovremenny Kommerchesky Bank from the date of acquisition to 30 June 2014 was RUB 2,864,325 thousand. This profit is included in the consolidated statement of comprehensive income of the group for the six months of 2014:

RUB'000

Interest income 3,295,663 Interest expense (458,844) Net interest income 2,836,819

Allowance for loan impairment 2,481,340 Net interest income after allowance for impairment of loans and other impairment

allowances 5,318,159

Fee and commission income 329,238 Fee and commission expense (31,958) Net fee and commission income 297,280

Net foreign exchange gain 607 Other impairment and provisions (10,512) Other operating income 12,872 Operating income 5,618,406

Personnel expenses (903,539) Other general and administrative expenses (903,915) Profit before income tax expense 3,810,952

Income tax expense (946,627)

Profit for the period 2,864,325 Cash outflow on acquisition of the subsidiary Net cash acquired with the subsidiary (included in cash flows from investing activities) 2,214,314 Cash paid (included in cash flows from investing activities) (5,294,909)

Net cash outflow (3,080,595)

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

14

3. Business combinations (continued) Acquisition of LLC ICICI Bank Eurasia Background On 17 March 2015, after the respective approvals from the Federal Antimonopoly Service and the Central Bank of Russia were received, the Group acquired 100% interest in LLC ICICI Bank Eurasia (LLC ICICI Bank) from LLC ICICI Bank Limited. ICICI Bank Limited is a company established under the laws of India, located at Landmark, Race Course Circle, Vadodara – 390 007, India, registered on 5 January 1994 under registration number 04-21012. In accordance with the decision of the Sole participant (shareholder) of LLC ICICI Bank Eurasia dated 29 April 2015 the Bank changed its name to Sovremenny Kommerchesky Ipotechny Bank ("SCIB"). SCIB engages mainly into issue and service mortgage loans and provision of bank guarantees in accordance with the Federal Law No. 44-FZ dated 5 April 2013 On the Contract System for the Procurement of Goods, Work and Services for State and Municipal Needs. SCIB engages into the following core activities:

• providing loans secured by property to individuals (mortgage);

• invest in debt securities of highly credible Russian issuers (state and corporate);

• providing to individuals money transfer services (mainly from Russia to the Republic of India);

• providing bank guarantees in accordance with the Federal Law No. 44-FZ dated 5 April 2013 On the Contract System for the Procurement of Goods, Work and Services for State and Municipal Needs.

At the date of the acquisition, SCIB had one branch in Saint Petersburg. The main reasons for acquisition for the Bank were bargain purchase price. Quality low risk mortgage portfolio and that in order to execute a planned transaction to acquire a share in JSC “Silhouette” (see below in Note 3),the Group had to acquire a separate bank holding a banking license. Taking into consideration the effectiveness of the Debt Collection function of the Bank the Group expects that the reversal of impairment allowance for the mortgage loan portfolio may be significant. Fair value of identifiable net assets and liabilities of Sovremenny Kommerchesky Ipotechny Bank The Bank determined the fair value of the net identifiable assets and liabilities of SCIB and Management of the Group believes that the consideration received is in line with all the available data in accordance with IFRS 3 Business Combinations. The fair value of the identifiable net assets and liabilities of SCIB as at the date of the acquisition was: RUB'000 Assets

Cash and cash equivalents 1,173,221 Obligatory reserves with CBR 17,861 Trading portfolio 295,331 Loans to customers 761,033 Property and equipment and intangible assets 14,884 Other assets 27,060 Total assets 2,289,390

Liabilities Deposits and balances from banks 236,069

Current accounts and deposits from customers 965,709 Securities issued 333 Other liabilities 3,327 Total liabilities 1,205,438

Identifiable net assets 1,083,952

RUB'000

Transferred consideration (1,083,952) Fair value of the identifiable net assets of SCIB at the date of acquisition 1,083,952

Total –

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

15

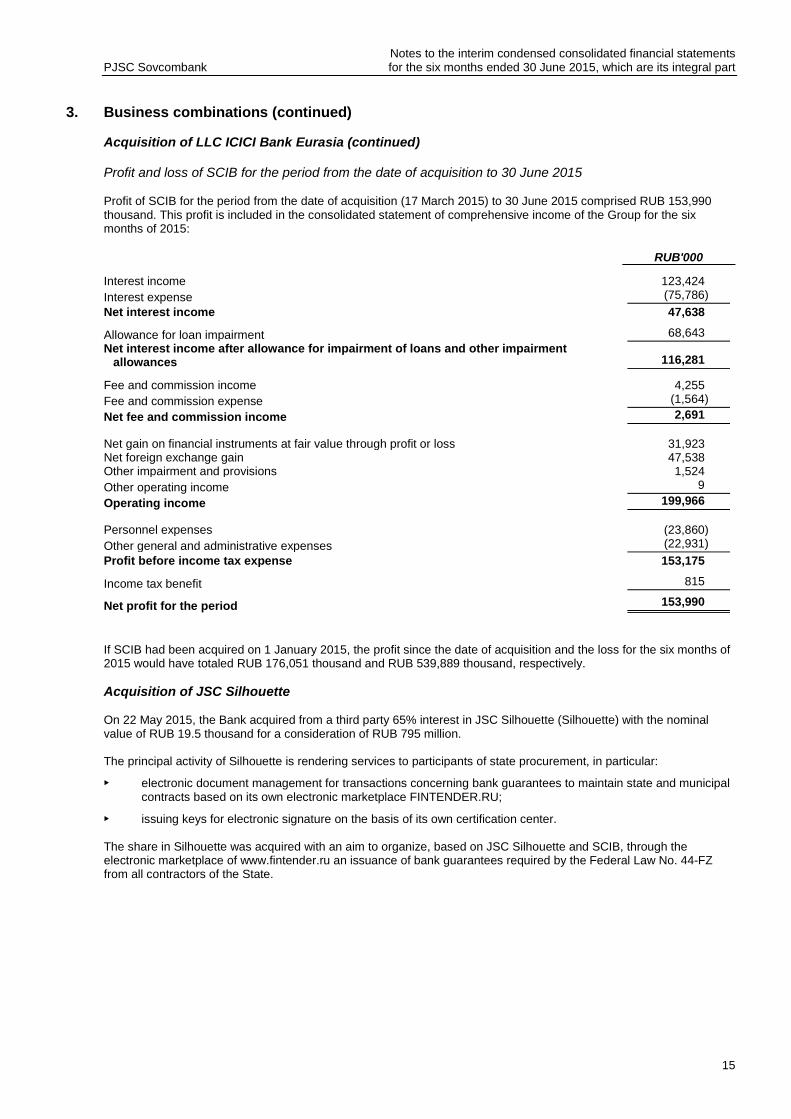

3. Business combinations (continued) Acquisition of LLC ICICI Bank Eurasia (continued) Profit and loss of SCIB for the period from the date of acquisition to 30 June 2015 Profit of SCIB for the period from the date of acquisition (17 March 2015) to 30 June 2015 comprised RUB 153,990 thousand. This profit is included in the consolidated statement of comprehensive income of the Group for the six months of 2015:

RUB'000

Interest income 123,424 Interest expense (75,786) Net interest income 47,638

Allowance for loan impairment 68,643 Net interest income after allowance for impairment of loans and other impairment

allowances 116,281

Fee and commission income 4,255 Fee and commission expense (1,564) Net fee and commission income 2,691

Net gain on financial instruments at fair value through profit or loss 31,923 Net foreign exchange gain 47,538 Other impairment and provisions 1,524 Other operating income 9 Operating income 199,966

Personnel expenses (23,860) Other general and administrative expenses (22,931) Profit before income tax expense 153,175

Income tax benefit 815

Net profit for the period 153,990

If SCIB had been acquired on 1 January 2015, the profit since the date of acquisition and the loss for the six months of 2015 would have totaled RUB 176,051 thousand and RUB 539,889 thousand, respectively. Acquisition of JSC Silhouette On 22 May 2015, the Bank acquired from a third party 65% interest in JSC Silhouette (Silhouette) with the nominal value of RUB 19.5 thousand for a consideration of RUB 795 million. The principal activity of Silhouette is rendering services to participants of state procurement, in particular:

• electronic document management for transactions concerning bank guarantees to maintain state and municipal contracts based on its own electronic marketplace FINTENDER.RU;

• issuing keys for electronic signature on the basis of its own certification center. The share in Silhouette was acquired with an aim to organize, based on JSC Silhouette and SCIB, through the electronic marketplace of www.fintender.ru an issuance of bank guarantees required by the Federal Law No. 44-FZ from all contractors of the State.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

16

3. Business combinations (continued) Acquisition of JSC Silhouette (continued) The Bank determined the preliminary fair value of the identifiable net assets and liabilities of Silhouette and Management of the Group believes that the consideration received is in line with all the available data in accordance with IFRS 3 Business Combinations. The preliminary fair value of the identifiable net assets and liabilities of Silhouette as at the date of acquisition was: RUB'000 Assets Property and equipment 243 Computer software 127,536 Intangible assets 1,385,496 Total assets 1,513,275

Liabilities Deferred tax liability 301,285

Other liabilities 99,004 Total liabilities 400,289

Identifiable net assets 1,112,986

Transferred consideration 795,000 Non-controlling interests 389,545 Fair value of the acquiree's identifiable net assets (1,112,986)

Goodwill arising on acquisition 71,559 In May 2015, the Bank performed a transaction to sell 35% interest in SCIB to Silhouette owners for a consideration of RUB 315,000 thousand. The Group recognized the transaction to sell the interest in SCIB and the purchase of interest in Silhouette as related. Therefore the value of recognized goodwill was increased by RUB 64,383 thousand to RUB 135,942 thousand. Acquisition of LLC AeroPlaza On 29 May 2015, the Group acquired 100% of share capital in LLC AeroPlaza with a nominal value of RUB 10 thousand from a related party for RUB 4.1 bn. The main asset of LLC AeroPlaza is a hotel and office complex Aerostar, located at: bld. 9, 37 Leningradsky prospekt, Moscow (www.aerostar.ru). The Group does not consider LLC AeroPlaza as a strategic investment and Management is planning to sell LLC AeroPlaza by the end of 2015. On this basis, as at 30 June 2015, investments to LLC AeroPlaza were recognized as assets held for sale. According to the results of independent valuation of LLC AeroPlaza, the value of this investments was RUB 3.35 bn. The difference between the acquisition cost and value of LLC AeroPlaza in the of RUB 550 million was recognized as an impairment loss and recorded as a part of “Other impairment and provisions”.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

17

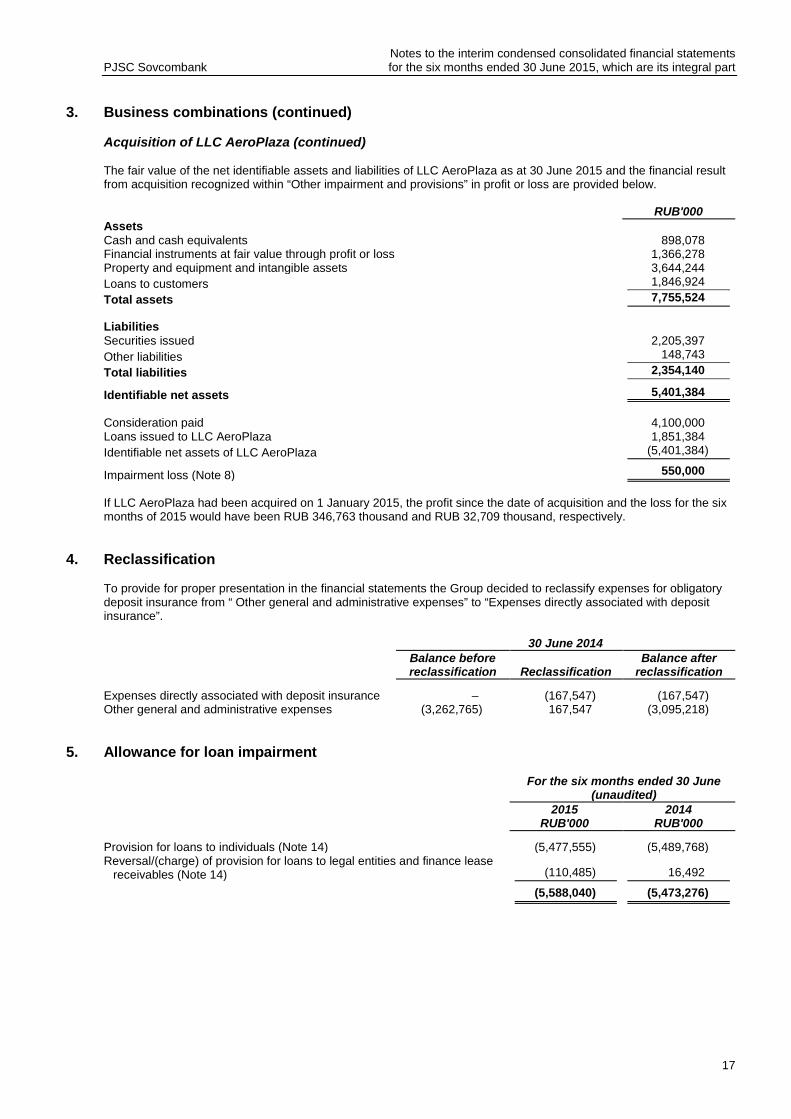

3. Business combinations (continued) Acquisition of LLC AeroPlaza (continued) The fair value of the net identifiable assets and liabilities of LLC AeroPlaza as at 30 June 2015 and the financial result from acquisition recognized within “Other impairment and provisions” in profit or loss are provided below. RUB'000 Assets Cash and cash equivalents 898,078 Financial instruments at fair value through profit or loss 1,366,278 Property and equipment and intangible assets 3,644,244 Loans to customers 1,846,924 Total assets 7,755,524

Liabilities Securities issued 2,205,397

Other liabilities 148,743 Total liabilities 2,354,140

Identifiable net assets 5,401,384

Consideration paid 4,100,000 Loans issued to LLC AeroPlaza 1,851,384 Identifiable net assets of LLC AeroPlaza (5,401,384)

Impairment loss (Note 8) 550,000 If LLC AeroPlaza had been acquired on 1 January 2015, the profit since the date of acquisition and the loss for the six months of 2015 would have been RUB 346,763 thousand and RUB 32,709 thousand, respectively.

Reclassification 4. To provide for proper presentation in the financial statements the Group decided to reclassify expenses for obligatory deposit insurance from “ Other general and administrative expenses” to “Expenses directly associated with deposit insurance”. 30 June 2014

Balance before reclassification Reclassification

Balance after reclassification

Expenses directly associated with deposit insurance – (167,547) (167,547) Other general and administrative expenses (3,262,765) 167,547 (3,095,218)

Allowance for loan impairment 5.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Provision for loans to individuals (Note 14) (5,477,555) (5,489,768) Reversal/(charge) of provision for loans to legal entities and finance lease

receivables (Note 14) (110,485) 16,492

(5,588,040) (5,473,276)

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

18

Fee and commission income 6.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Collective financial protection program membership fee 2,733,487 4,061,128 Credit card operations 744,536 511,046 Insurance agent’s commission 302,463 47,173 Guarantee issuance 261,290 10,898 Fees for cash transfer to pension funds 116,631 – Settlement operations 77,268 68,150 Cash operations 33,210 38,945 Currency operations 9,617 9,499 Securities operations 1,439 2,495 Cash transfers 1,329 1,392 Other 3,880 4,264

4,285,150 4,754,990

Other operating income 7.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Penalties received 31,901 – Disposal of foreclosed property 16,279 17,181 Income from operational sublease 5,227 7,543 Operating lease of investment property 2,687 2,266 Disposal of property and equipment 103 1,582 Gain on a bargain purchase (Note 3) – 2,507,307 Other 11,001 8,258

67,198 2,544,137

Other impairment and provisions 8.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Impairment of assets held for sale (Note 3) (550,000) – Litigations (95,511) (61,148) Other assets (60,072) (29,368) Reversal of provision for bonds issued by financial institutions and

previously recorded within placements with banks 19,779 –

(685,804) (90,516)

Personnel expenses 9.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Employee benefits, including bonuses (1,925,820) (2,661,026) Payroll related taxes (540,801) (662,996)

(2,466,621) (3,324,022)

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

19

Other general and administrative expenses 10.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Rent (642,118) (722,081) Professional and cash collection services (376,272) (410,168) Advertising and marketing (351,659) (575,327) Depreciation and amortization (203,121) (218,644) Telecommunications and information services (182,005) (239,397) IT expenses (143,726) (251,589) Maintenance (112,137) (174,273) Transport (86,282) (102,645) Security (79,092) (114,976) Office stationery (72,847) (130,516) Property insurance (41,218) (29,764) Taxes other than income tax (18,056) (60,275) Other (85,172) (65,563)

(2,393,705) (3,095,218)

Income tax expense 11.

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Current income tax Current income tax (164,659) (744,172)

(164,659) (744,172)

Deferred income tax Origination of temporary differences (2,071,073) 787,662

Total income tax expense (2,235,732) 43,490 Current income tax rate is 20%.

Cash and cash equivalents 12.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000

Cash on hand 3,725,085 9,941,744 Nostro accounts with Russian banks 4,935,995 6,683,533 Accounts with the CBR 7,355,751 6,345,591 Nostro accounts with OECD banks 124,695 1,960,338 Short-term deposits and reverse repurchase transactions less than 90 days

with Russian banks – 495,068

16,141,526 25,426,274

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

20

Financial instruments at fair value through profit or loss 13.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000 Held by the Group

Corporate bonds 6,596,803 5,655,222 Bonds of companies with the State participation 4,794,504 3,447,845 State and municipal bonds 868,005 – Total financial instruments at fair value through profit or loss held by

the Group 12,259,312 9,103,067 Pledged under repurchase agreements Bonds of companies with the State participation 66,855,882 14,916,294 Corporate Eurobonds 42,046,208 14,063,252 State and municipal bonds 5,550,015 – Total financial instruments at fair value through profit or loss pledged

under repurchase agreements 114,452,105 28,979,546

Total financial instruments at fair value through profit or loss 126,711,417 38,082,613 All the bonds recorded on the Bank's balance sheet are National Settlement Depository CJSC, which provides settlement and custodial services to participants in financial markets in the Russian Federation.

Loans to customers 14.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000 Loans to individuals

Consumer loans 66,332,293 76,298,895 Credit cards 8,638,603 9,687,076 Mortgage loans 1,336,501 406,386 Total loans to individuals 76,307,397 86,392,357 Loans to corporate customers and finance lease receivables Loans to corporate customers 10,892,250 9,111,701 Loans to small entities and other loans to customers 637,530 472,010 Loans to entities of the Russian Federation and constituent entities 11,302,457 – State and municipal bonds 20,537,586 22,530,163 Corporate bonds 7,278,297 9,338,029 Total loans to corporate customers and finance lease receivables 50,648,120 41,451,903 Gross loans to customers 126,955,517 127,844,260

Less: allowance for loan impairment (11,520,661) (11,079,501)

Loans to customers, net 115,434,856 116,764,759 All the bonds recorded on the Bank's balance sheet are held only with National Settlement Depository CJSC, which provides settlement and custodial services to participants in financial markets in the Russian Federation.

30 June 2015 (unaudited) 2014

Due to the CBR RUB'000

Current accounts and deposits from

customers RUB'000

Due to the CBR RUB'000

Loans to customers pledged under repurchase agreements

Corporate bonds 7,045,764 − 8,424,402 State and municipal bonds 17,317,434 740,222 21,181,947

Total carrying amount 24,363,198 740,222 29,606,349

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

21

14. Loans to customers (continued) Changes in allowance for loan impairment for the six months ended 30 June 2015 and 30 June 2014 are as follows:

Loans to corporate customers

Loans to entities of the

Russian Federation and

constituent entities SME loans

Consumer lending Credit cards

Mortgage loans Total

At 1 January 2015 (312,670) – (15,762) (9,092,180) (1,614,037) (44,852) (11,079,501) (Charge)/reversal for

the year (2,793) (56,512) (51,180) (4,614,149) (785,493) (77,913) (5,588,040) Reversal of amounts

previously written off – – (3,360) (5,376) – (66,819) (75,555)

Loans written off as uncollectible 428 – 52,384 4,316,268 853,356 (1) 5,222,435

At 30 June 2015 (315,035) (56,512) (17,918) (9,395,437) (1,546,174) (189,585) (11,520,661)

At 1 January 2014 (81,620) – (71,140) (5,572,181) (659,122) (4,253) (6,388,316) (Charge)/reversal for

the year 20,404 – (3,912) (4,615,511) (856,283) (17,974) (5,473,276) Reversal of amounts

previously written off – – (5,027) (21) – (2,871) (7,919)

Loans written off as uncollectible 76 – 29,275 2,678,631 292,239 751 3,000,972

At 30 June 2014 (61,140) – (50,804) (7,509,082) (1,223,166) (24,347) (8,868,539) Credit quality of loans to individuals The credit quality of loans to individuals is assessed and managed by the Group based on the number of days overdue. The tables below show the credit quality of loans to individuals based on the number of days overdue as at 30 June 2015 and 31 December 2014. As at 30 June 2015:

Gross loans Impairment Net loans

Impairment to gross loans

RUB'000 RUB'000 RUB'000 %

Consumer loans - Not past due 50,773,686 (561,701) 50,211,985 1.11%

- Overdue less than 30 days 4,233,524 (656,791) 3,576,733 15.51% - Overdue from 30 to 89 days 2,497,003 (1,316,735) 1,180,268 52.73% - Overdue from 90 to 179 days 3,272,289 (2,308,173) 964,116 70.54% - Overdue from 180 to 360 days 5,555,791 (4,552,037) 1,003,754 81.93% Total consumer loans 66,332,293 (9,395,437) 56,936,856 14.16%

Credit cards - Not past due 6,380,279 (91,863) 6,288,416 1.44% - Overdue less than 30 days 573,029 (116,470) 456,559 20.33% - Overdue from 30 to 89 days 339,945 (194,662) 145,283 57.26% - Overdue from 90 to 179 days 482,886 (372,108) 110,778 77.06% - Overdue from 180 to 360 days 862,464 (771,071) 91,393 89.40% Total credit cards 8,638,603 (1,546,174) 7,092,429 17.90%

Mortgage loans - Not past due 716,355 (9,726) 706,629 1.36% - Overdue less than 30 days 91,638 (5,794) 85,844 6.32% - Overdue from 30 to 89 days 67,487 (9,802) 57,685 14.52% - Overdue from 90 to 179 days 195,481 (53,080) 142,401 27.15% - Overdue from 180 to 360 days 195,539 (69,345) 126,194 35.46% Overdue more than 360 days 70,001 (41,838) 28,163 59.77% Total mortgage loans 1,336,501 (189,585) 1,146,916 14.19%

Total other loans to individuals 76,307,397 (11,131,196) 65,176,201 14.59%

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

22

14. Loans to customers (continued) Credit quality of loans to individuals (continued) As at 31 December 2014:

Gross loans Impairment Net loans

Impairment to gross loans

RUB'000 RUB'000 RUB'000 %

Consumer loans - Not past due 61,420,162 (632,071) 60,788,091 1.03%

- Overdue less than 30 days 3,792,573 (718,194) 3,074,379 18.94% - Overdue from 30 to 89 days 2,556,292 (1,348,137) 1,208,155 52.74% - Overdue from 90 to 179 days 3,038,510 (2,094,710) 943,800 68.94% - Overdue from 180 to 360 days 5,491,358 (4,299,068) 1,192,290 78.29% Total consumer loans 76,298,895 (9,092,180) 67,206,715 11.92% Credit cards - Not past due 7,358,608 (97,553) 7,261,055 1.33% - Overdue less than 30 days 539,122 (110,637) 428,485 20.52% - Overdue from 30 to 89 days 396,645 (220,168) 176,477 55.51% - Overdue from 90 to 179 days 483,754 (368,883) 114,871 76.25% - Overdue from 180 to 360 days 908,947 (816,796) 92,151 89.86% Total credit cards 9,687,076 (1,614,037) 8,073,039 16.66% Mortgage loans - Not past due 198,137 (1,982) 196,155 1.00% - Overdue less than 30 days 66,513 (3,326) 63,187 5.00% - Overdue from 30 to 89 days 54,777 (5,478) 49,299 10.00% - Overdue from 90 to 179 days 20,481 (4,096) 16,385 20.00% - Overdue from 180 to 360 days 16,341 (4,902) 11,439 30.00% - Overdue more than 360 days 50,137 (25,068) 25,069 50.00% Total mortgage loans 406,386 (44,852) 361,534 11.04%

Total other loans to individuals 86,392,357 (10,751,069) 75,641,288 12.44% Credit quality of loans to corporate customers The following table provides information on the credit quality of loans to legal entities and finance lease receivables as at 30 June 2015:

Gross loans Impairment Net loans

Impairment to gross loans

RUB'000 RUB'000 RUB'000 %

Loans to corporate customers and finance lease receivables

Unimpaired loans and finance lease receivables 50,358,748 (333,959) 50,024,789 0.66% Impaired loans and finance lease receivables - Overdue less than 90 days 22,662 (727) 21,935 3.21% - Overdue more than 90 days and less than 1 year 258,594 (46,954) 211,640 18.16% - Overdue more than 1 year 8,116 (7,825) 291 96.41% Total impaired loans and finance lease

receivables 289,372 (55,506) 233,866 19.18%

Individual impairment 223,010 (43,574) 179,436 19.54% Collective impairment 66,362 (11,932) 54,430 17.98% Total loans to legal entities and finance lease

receivables 50,648,120 (389,465) 50,258,655 0.77%

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

23

14. Loans to customers (continued) Credit quality of loans to corporate customers (continued) The following table provides information on the credit quality of loans to legal entities and finance lease receivables as at 31 December 2014:

Gross loans Impairment Net loans Impairment to gross loans

RUB'000 RUB'000 RUB'000 % Loans to corporate customers and finance

lease receivables Unimpaired loans and finance lease receivables 41,045,590 (277,157) 40,768,433 0.68% Impaired loans and finance lease receivables - Overdue less than 90 days 16,760 (637) 16,123 3.80% - Overdue more than 90 days and less than 1 year 382,965 (44,418) 338,547 11.60% - Overdue more than 1 year 6,588 (6,220) 368 94.41% Total impaired loans and finance lease

receivables 406,313 (51,275) 355,038 12.62%

Individual impairment 352,493 (42,316) 310,177 12.00% Collective impairment 53,820 (8,959) 44,861 16.65% Total loans to corporate customers and

finance lease receivables 41,451,903 (328,432) 41,123,471 0.79% As at 30 June 2015, gross loans to individuals included fair value of loans acquired through business combination with Sovremenny Kommerchesky Bank. As at 30 June 2015, the gross amount of NPL (non-performing loans – overdue more than 90 days), the respective total impairment and the NPL coverage ratio of consumer loans and credit cards were as follows:

NPL gross amount Total impairment NPL coverage ratio

Consumer loans 8,828,080 (9,395,437) 106.4% Credit cards 1,345,350 (1,546,174) 114.9% Had the Group not applied IFRS 3 as at 30 June 2015, the gross amount of NPL, total impairment and the NPL coverage ratio of consumer loans and credit cards would have been as follows:

NPL gross amount Total impairment NPL coverage ratio

Consumer loans 8,951,815 (10,132,008) 113.2% Credit cards 1,345,351 (1,546,174) 114.9%

Held-to-maturity investment securities 15. On 27 April 2015, the State Corporation Deposit Insurance Agency (the "DIA") entered into subordinated loan agreements with the Bank to increase Bank’s capitalization. At the same time, the Bank received Russian State bonds (“OFZ”) from five issues (No. 29006RMFS, No. 29007RMFS, No. 29008RMFS, No. 29009RMFS, No. 29010RMFS) with a total nominal value of RUB 6,272,750 thousand. The Group recognizes these OFZ as held-to-maturity investment securities. All the bonds recorded on the Bank's balance sheet are held only with National Settlement Depository CJSC, which provides settlement and custodial services to participants in financial markets in the Russian Federation. Pursuant to the agreements with the DIA, the Bank has the right to pledge these OFZ under repurchase agreements with the CBR.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

24

Current accounts and deposits from customers 16.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000 Individuals

Current accounts and demand deposits 2,985,669 2,516,784 Term deposits 95,875,850 98,666,591 Legal entities Current accounts and demand deposits 5,502,096 12,651,223 Term deposits 6,270,407 3,679,490

110,634,022 117,514,088

Amounts due to the CBR 17.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000

Repurchase agreements 133,038,658 62,515,620 Loans secured by guarantees 1,841,504 –

134,880,162 62,515,620

Deposits and balances from banks 18.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000

Repurchase agreements 3,129,936 – Loro accounts 365,172 606,871 Deposits 200,000 24,273

3,695,108 631,144

Debt securities issued 19.

30 June 2015 RUB'000

(unaudited) 31 December 2014

RUB'000

Promissory notes 2,153,371 2,562,097 Domestic bonds issued 789,981 177,925

2,943,352 2,740,022

Subordinated debt 20. Additional capitalization of the Bank by the DIA In 2015, the DIA chose Sovcombank along with other 26 Russian banks to participate in the Plan of Priority Measures to Ensure Sustainable Development of the Economy and Social Stability in 2015 approved by Regulation No. 98-r dated 27 January 2015 (the "Anti-crisis plan"). The list of banks participating in the crisis plan was approved by the Board of Directors of the DIA on 23 January 2015 and the Russian Government on 2 February 2015.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

25

20. Subordinated debt (continued) Additional capitalization of the Bank by the DIA (continued) On 27 April 2015, the DIA provided the Group with five subordinated loans of RUB 6,272,750 thousand and in a form of Russian State bonds (OFZ) which are issued by the Russian Ministry of Finance. These subordinated loans shall be repaid within 12 to 19 years. The key terms and conditions of these agreements are as follows:

• interest rates on subordinated loans are equal to rates applicable to coupon income on the related OFZ bonds increased by 1% p.a.;

• in case the arbitration court declares the Bank insolvent (bankrupt), the DIA's claims of the subordinated loan will be settled after settling the claims of all other creditors but taking into consideration a priority of claims regarding a subordinated debt;

• if subsequent to the provision of the subordinated loan, the information is posted on the official CBR web-site regarding the Bank and claiming that one of the following occurs:

1) core capital adequacy ratio (N1.1), calculated in accordance with the Instruction of the Bank of Russia No. 139-I of 3 December 2012 Concerning Mandatory Bank Ratios, drops below the level stated in the Regulation for Subordinated Loan Exchange, which was 2% for the period defined by the Regulation as at the date of the subordinated agreements; or

2) the Committee on Banking Supervision of the CBR approves the plan of the DIA's participation in measures to prevent the Bank's bankruptcy. This plan provides that the DIA will deliver financial support pursuant to the Federal Law On Insolvency (Bankruptcy),

the DIA's requirements under the subordinated loan agreement are changed to the Bank's ordinary shares.

The CBR confirmed that these subordinated loans may be included the Bank capital (Note 22). The list of the subordinated loans received by the Bank and their key terms are provided below.

Principal, thousand

units Currency Counterparty Interest

rate Issue date Maturity date 30 June 2015

31 December 2014

RUB'000 RUB'000

94,470 USD Sovco Capital Partners B.V. 14.0% 16 December

2013 16 December

2073 5,300,428 5,370,536

1,254,550 RUB State Corporation Deposits

Insurance Agency 15.2% 27 April 2015 24 February

2027 1,288,013 –

1,254,550 RUB State Corporation Deposits

Insurance Agency 17.1% 24 February

2027 29 November

2034 1,280,837 –

1,254,550 RUB State Corporation Deposits

Insurance Agency 16.5% 27 April 2015 26 September

2029 1,290,911 –

1,254,550 RUB State Corporation Deposits

Insurance Agency 13.7% 27 April 2015 22 January

2025 1,284,588 –

1,254,550 RUB State Corporation Deposits

Insurance Agency 17.4% 27 April 2015 28 April 2032 1,274,889 –

11,719,666 5,370,536

Fair value of financial instruments 21. The following disclosure of the estimated fair value of financial instruments is made in accordance with the requirements of IFRS 7 Financial Instruments: Disclosures. Fair value is defined as the amount at which the instrument could be exchanged in a current transaction between knowledgeable willing parties in an arm’s length transaction other than in forced sale or liquidation. As no readily available market exists for a large part of the Group’s financial instruments (specifically extended loans) at which such financial assets would be traded on a regular basis judgment is necessary in arriving at fair value based on current economic conditions and the specific risks attributable to a given instrument. The estimates presented herein are not necessarily indicative of the amounts the Group could realize in a market exchange from the sale of its full holdings of a particular instrument.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

26

21. Fair value of financial instruments (continued) The Group uses the following hierarchy for determining and disclosing the fair value of financial instruments by valuation technique:

• Level 1: quoted (unadjusted) prices in active markets for identical assets or liabilities

• Level 2: techniques for which all inputs which have a significant effect on the recorded fair value are observable, either directly or indirectly; and

• Level 3: techniques which use inputs which have a significant effect on the recorded fair value that are not based on observable market data.

The following table shows an analysis of financial instruments recorded at fair value by level of the fair value hierarchy:

Fair value measurement using

At 30 June 2015 (unaudited)

Quoted prices in active markets

(Level 1)

Significant observable

inputs (Level 2)

Significant unobservable

inputs (Level 3) Total

Assets measured at fair value Financial instruments at fair value through profit or

loss 20,096,399 106,615,018 – 126,711,417 Assets for which fair values are disclosed Cash and cash equivalents 16,141,526 – – 16,141,526 Obligatory reserves with the CBR – – 1,132,491 1,132,491 Placements with banks and other financial

institutions – 9,642,927 476,428 10,119,355 Loans to customers – 27,815,883 86,217,171 114,033,054 Other assets – – 1,700,053 1,700,053 Liabilities for which fair values are disclosed Amounts due to the CBR – – 134,880,162 134,880,162 Deposits and balances from banks – – 3,695,108 3,695,108 Current accounts and deposits from customers – 109,527,000 109,527,000 Debt securities issued 744,162 – 2,153,371 2,897,533 Subordinated debt – – 11,719,666 11,719,666 Other liabilities – – 1,539,501 1,539,501

Fair value measurement using

31 December 2014

Quoted prices in active markets

(Level 1)

Significant observable

inputs (Level 2)

Significant unobservable

inputs (Level 3) Total

Assets measured at fair value Financial instruments at fair value through profit or

loss 1,535,749 36,546,864 – 38,082,613 Assets for which fair values are disclosed Cash and cash equivalents 25,426,274 – – 25,426,274 Obligatory reserves with the CBR – – 1,072,389 1,072,389 Placements with banks and other financial

institutions – 14,198,829 387,810 14,586,639 Loans to customers – 30,104,617 85,002,457 115,107,074 Other assets – – 1,776,891 1,776,891 Liabilities for which fair values are disclosed Amounts due to the CBR – – 62,515,620 62,515,620 Deposits and balances from banks – – 631,144 631,144 Current accounts and deposits from customers – – 110,599,761 110,599,761 Debt securities issued 188,571 – 2,562,097 2,750,668 Subordinated debt – – 5,370,536 5,370,536 Other liabilities – – 1,389,484 1,389,484

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

27

21. Fair value of financial instruments (continued) Financial instruments recorded at fair value The following is a description of the determination of fair value for financial instruments which are recorded at fair value using valuation techniques. These incorporate the Bank’s estimate of assumptions that a market participant would make when valuing the instruments. Financial assets at fair value through profit or loss Trading securities valued using a valuation technique or pricing models primarily consist of unquoted equity and debt securities. These securities are valued using models which sometimes only incorporate data observable in the market and at other times use both observable and non-observable data. The non-observable inputs to the models include assumptions regarding the future financial performance of the investee, its risk profile, and economic assumptions regarding the industry and geographical jurisdiction in which the investee operates. Fair values of financial assets and liabilities not carried at fair value Set out below is a comparison by class of the carrying amounts and fair values of the Group's financial instruments that are not carried at fair value in the consolidated statement of financial position. The table does not include the fair values of non-financial assets and non-financial liabilities.

30 June 2015

RUB'000

30 June 2015

RUB'000

30 June 2015

RUB'000

31 December 2014

RUB'000

31 December 2014

RUB'000

31 December 2014

RUB'000

Carrying amount

Fair value

Unrecognized gain/(loss)

Carrying amount

Fair value

Unrecognized gain/(loss)

Assets Cash and cash

equivalents 16,141,526 16,141,526 – 25,426,274 25,426,274 – Obligatory reserves with

the CBR 1,132,491 1,132,491 – 1,072,389 1,072,389 – Placements with banks

and other financial institutions 10,182,186 10,119,355 (62,831) 14,864,749 14,586,639 (278,110)

Loans to customers 115,434,856 114,033,054 (1,401,802) 116,764,759 115,107,074 (1,657,685) Other assets 1,700,053 1,700,053 – 1,776,891 1,776,891 – Liabilities

Amounts due to the CBR 134,880,162 134,880,162 – 62,515,620 62,515,620 –

Deposits and balances from banks 3,695,108 3,695,108 – 631,144 631,144 –

Current accounts and deposits from customers 110,634,022 109,527,000 1,107,022 117,514,088 110,599,761 6,914,327

Debt securities issued 2,943,352 2,897,533 45,819 2,740,022 2,750,668 (10,646) Subordinated debt 11,719,666 11,719,666 – 5,370,536 5,370,536 – Other liabilities 1,539,501 1,539,501 – 1,389,484 1,389,484 –

(311,792) 4,967,886

Share capital and other contributions to share capital 22. As at 30 June 2015 and 31 December 2014, the share capital was RUB 1,906,004 thousand. As at 30 June 2015, the number of declared ordinary shares with the nominal value of RUB 0.1 each totals 19,060,040,773. The share capital of the Bank has been contributed by shareholders in Russian rubles. Shareholders are entitled to dividends and any capital distribution in Russian rubles. On April 2015, the Bank received subordinated loans from the DIA totaling RUB 6,272,750 thousand (Note 20). After reviewing set of the supporting documents, the CBR confirmed by a letter No. 66-6-39/5546 dated 29 April 2015 that provided to the Bank by DIA funds may be included into the Bank capital.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

28

Tax contingencies 23. Russian tax, currency and customs legislation as currently in effect is subject to varying interpretations, selective and inconsistent application and changes, which may occur frequently, at short notice and may apply retrospectively. Management interpretation of such legislation as applied to the transactions and activity of the Group may be challenged by the relevant regional and federal authorities. Recent events within the Russian Federation suggest that the tax authorities may be taking a more assertive position in their interpretation and application of this legislation and assessments. It is therefore possible that transactions and activities of the Group that have not been challenged in the past may be challenged at any time in the future. As a result, significant additional taxes, penalties and interest may be assessed by the relevant authorities. Fiscal periods remain open and subject to review for a period of three calendar years immediately preceding the year in which the decision to conduct a tax review is taken. Under certain circumstances, tax reviews may cover longer periods. As at 30 June 2015, Group Management believes that its interpretation of the relevant legislation is appropriate and that the Group’s tax, currency and customs positions will be sustained.

Related party transactions 24. Parties are considered to be related if one party has the ability to control the other party or exercise significant influence over the other party in making financial or operational decisions as defined by IAS 24 Related Party Disclosures. In considering each possible related party relationship, attention is directed to the substance of the relationship, not merely the legal form. Total remuneration included in employee compensation (Note 9) may be presented as follows:

30 June 2015,

RUB'000 30 June 2014,

RUB'000

Members of the Board of Directors 44,527 15,321 Key management 100,850 69,032

145,377 84,353 The outstanding balances with related parties as at 30 June 2015 (unaudited) are as follows:

Participants of Parent Group Joint venture*

Key management

personnel Other related

parties Total

RUB'000 RUB'000 RUB'000 RUB'000 RUB'000

Loans outstanding at 1 January – 141,379 271,572 5,408,681 5,821,632 Loans issued during the period 968,690 932,052 679,129 227,135 2,807,006 Loans repayments during the

period (968,690) (604,039) (413,451) (200,883) (2,187,063) Other movements – – (269,292) (4,644,130) (4,913,422) Loans outstanding at 30 June,

gross – 469,392 267,958 790,803 1,528,153 Less: allowance for impairment at

30 June – 5,633 3,402 5,190 14,225 Loans outstanding at 30 June,

net – 475,025 271,360 795,993 1,542,378 Deposits at 1 January 615,252 – 73,594 174,748 863,594 Deposits received during the period – – 1,998,240 713,137 2,711,377 Deposits repaid during the period (799,109) – (1,739,207) (611,987) (3,150,303) Other movements 183,912 – 225,696 (146,821) 262,787 Deposits at 30 June 55 – 558,323 129,077 687,455

Current accounts at 30 June 125,486 4,073 169,316 275,336 574,211 Subordinated debt at 1 January 5,370,536 – – – 5,370,536 Subordinated debt received during

the period – – – – – Subordinated debt repaid during

the period 6,613 – – – 6,613 Other movements (76,721) – – – (76,721)

Subordinated debt at 30 June 5,300,428 – – – 5,300,428 Guarantees received – 327,868 60,245 1,185,000 1,573,113 * Joint venture is a contractual arrangement whereby the Group and LLC Sollers undertake an economic activity which is under

joint control with LLC Sollers-Finance (Note 25). ** Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities

of the Group. Key management personnel of the Group are members of the Management Board and the Board of Directors.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

29

24. Related party transactions (continued) The outstanding balances with related parties as at 31 December 2014 were as follows:

Participants of Parent Group Joint venture*

Key management personnel**

Other related parties Total

RUB'000 RUB'000 RUB'000 RUB'000 RUB'000 Loans outstanding at 1 January,

gross – 13,856 65,896 725,234 804,986 Loans issued during the year – 1,002,219 300,343 5,265,212 6,567,774 Loan repayments during the year – (874,055) (32,438) (504,486) (1,410,979) Other movements – (641) (62,229) (77,279) (140,149) Loans outstanding at

31 December – 141,379 271,572 5,408,681 5,821,632 Less: allowance for impairment at

31 December – (1,697) 3,146 6,050 7,499 Loans outstanding at

31 December, net – 139,682 274,718 5,414,731 5,829,131 Deposits at 1 January – – 257,342 385,402 642,744 Deposits received during the year 8,911,925 – 105,968 174,718 9,192,611 Deposits repaid during the year (7,611,744) – (320,048) (199,251) (8,131,043) Other movements (684,929) – 30,332 (186,121) (840,718)

Deposits at December 31 615,252 – 73,594 174,748 863,594 Financial instruments at fair

value through profit or loss at 1 January 8,264 – – – 8,264

Acquired financial instruments at fair value through profit or loss – – – – –

Sold financial instruments at fair value through profit or loss – – – – –

Other movements (8,264) – – – (8,264) Financial instruments at fair

value through profit or loss at 31 December – – – – –

Current accounts at

31 December 4,969,088 2,076 74,665 114,460 5,160,289 Subordinated debt at 1 January 734,119 – – – 734,119 Subordinated debt received during

the year 2,484,061 – – – 2,484,061 Subordinated debt repaid during

the year – – – – – Other movements 2,152,356 – – – 2,152,356 Subordinated debt at

31 December 5,370,536 – – – 5,370,536 Guarantees received – – 151,016 1,255,000 1,406,016

* Joint venture is a contractual arrangement whereby the Group and LLC Sollers undertake an economic activity which is under joint control with LLC Sollers-Finance (Note 25).

** Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the Group. Key management personnel of the Group are members of the Management Board and the Board of Directors.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

30

24. Related party transactions (continued) The amounts recognized as transactions with related parties were included in the consolidated statement of profit or loss for the six months ended 30 June 2015 (unaudited) and are presented in the table below:

Participants of Parent Group Joint venture*

Key management

personnel Other related

parties Total

RUB'000 RUB'000 RUB'000 RUB'000 RUB'000

Interest income 1,112 17,327 22,633 53,621 94,693 Interest expense on deposits (2,514) – (9,544) (34,528) (46,586) Interest expense on subordinated

debt (382,284) – – – (382,284) Allowance for loan impairment – (1,911) 5 (12,601) (14,507) Fee and commission income 330 39 660 737 1,766 Other income – – 1,284 277 1,561 General and administrative

expenses – – (1,450) (162) (1,612) * Joint venture is a contractual arrangement whereby the Group and LLC Sollers undertake an economic activity which is under

joint control with LLC Sollers-Finance (Note 25).

** Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the Group. Key management personnel of the Group are members of the Management Board and the Board of Directors.

The amounts recognized as transactions with related parties were included in the consolidated statement of profit or loss for the six months ended 30 June 2014 (unaudited) and are presented in the table below:

Participants of Parent Group Joint venture*

Key management

personnel Other related

parties Total

RUB'000 RUB'000 RUB'000 RUB'000 RUB'000

Interest income – 3,144 5,150 45,847 54,141 Interest expense on deposits (221) – (7,611) (8,983) (16,815) Interest expense on subordinated

debt (122,164) – – – (122,164) Allowance for loan impairment – (21,943) 322 9,153 (12,468) Fee and commission income 245 46 827 446 1,564 Other income 6,276 – 177 3,893 10,346 General and administrative

expenses – – (899) – (899)

Share of investments in joint venture 25. The Group has a 50% interest in LLC Sollers-Finance which provides car leasing services for legal entities in the Russian Federation. Under IAS 31 Investments in Joint Ventures (prior to transition to IFRS 11), the Group’s interest in LLC Sollers-Finance was classified as interest in a jointly controlled entity and the Group’s share of the assets, liabilities, revenue, income and expenses were included in the consolidated financial statements on a pro rata basis. Upon adoption of IFRS 11, the Group determined its interest to be a joint venture and it is required to be accounted for using the equity method.

Notes to the interim condensed consolidated financial statements PJSC Sovcombank for the six months ended 30 June 2015, which are its integral part

31

25. Share of investments in joint venture (continued) The summarized financial information of LLC Sollers-Finance is presented below:

As at 30 June 2015

As at 31 December 2014

RUB'000 RUB'000

Cash and cash equivalents 14,310 8,086 Loans to customers 1,692,560 1,938,797 Property and equipment 56,735 47,957 Other assets 162,062 214,851 Total assets 1,925,667 2,209,691

Amounts due to credit institutions 1,000,336 1,260,829 Amounts due to customers – − Other liabilities 157,810 131,627 Total liabilities 1,158,146 1,392,456

Net assets 767,521 817,235

Group’s share in net assets 383,761 408,618 Goоdwill included in the carrying amount of investments 43,109 43,109

Carrying amount of investments in car leasing joint venture 426,870 451,727

For the six months ended 30 June (unaudited)

2015 2014

RUB'000 RUB'000

Interest income 276,488 278,349 Interest expense (73,354) (71,845) Allowance for loan impairment (26,640) (67,076) Non-interest income 69,507 34,449 Non-interest expense (164,827) (118,601)

Profit 81,174 55,276 Dividends received from the car leasing joint venture during the period 65,444 37,833

Principal subsidiaries 26. Included in the table below is the list of the principal consolidated subsidiaries, associates and joint ventures of the Group, as at 30 June 2015 and 31 December 2014.

Relationship Voting rights

30 June 2015 31 December 2014

LLC Regionalnaya Lisingovaya Compania Subsidiary 100.00% 100.00% LLC Sovremenny Kommerchesky Ipotechny

Bank Subsidiary 65.00% – CJSC Silhouette Subsidiary 65.00% – LLC Sollers-Finance Joint venture 50.00% 50.00% LLC Avtozaim Subsidiary 100.00% 100.00% LLC Shatalet Associate 49.00% –