intelligent cloning - the value firm

TRANSCRIPT

Copyright © 2021 by The Value Firm®. All rights reserved.

Intelligent Cloning The Spring 2021 Edition

All of those risk models… They are great, until complete

chaos happens. And then all the correlations break down

and can suck you into a false security.

In this Edition on Intelligent Cloning we’ll start with some

thoughts on the quote above. Then we’ll have a look at

the idea of Hyper Value Creators, by looking at the

Terry Smith Funds and the AAII Buffett Hagstrom

Screener, and finally some comments on a study entitled

“The Makings of a Multi-Bagger” by Alta Fox Capital

Management. Enjoy!

The quote above is from Stanley Druckenmiller,

Chairman and CEO of Duquesne Family Office. To put

this quote into perspective, let’s have a look at this

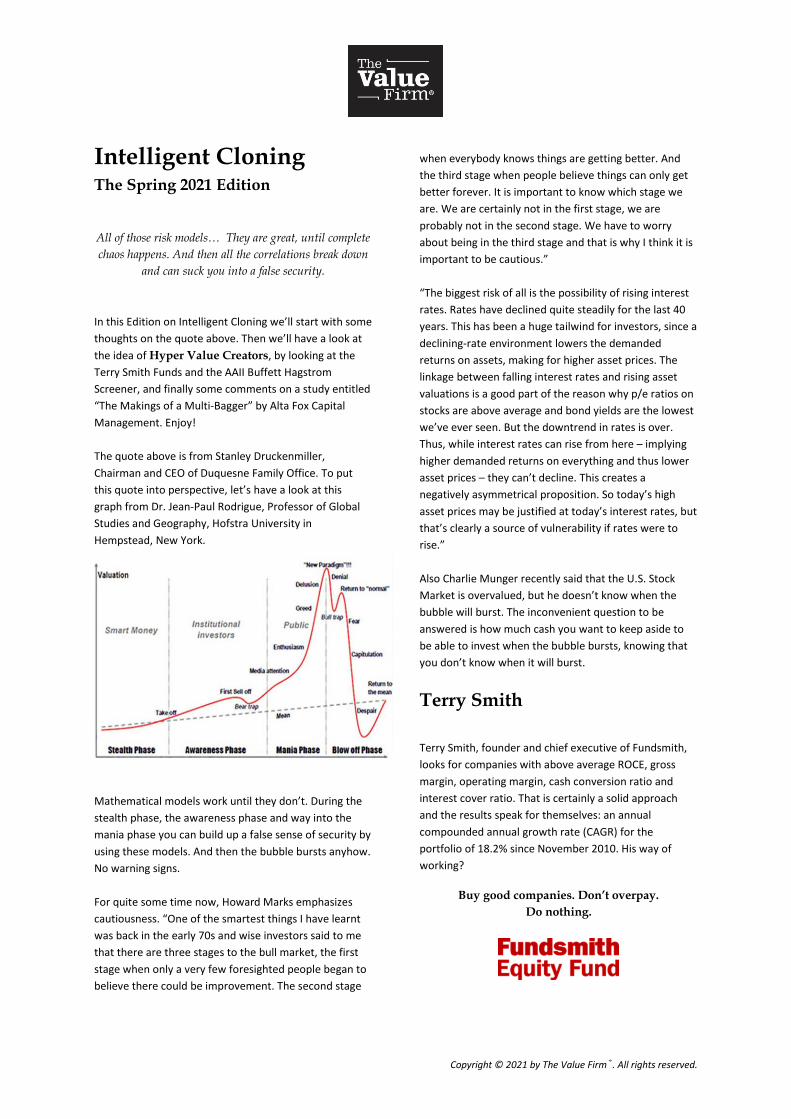

graph from Dr. Jean-Paul Rodrigue, Professor of Global

Studies and Geography, Hofstra University in

Hempstead, New York.

Mathematical models work until they don’t. During the

stealth phase, the awareness phase and way into the

mania phase you can build up a false sense of security by

using these models. And then the bubble bursts anyhow.

No warning signs.

For quite some time now, Howard Marks emphasizes

cautiousness. “One of the smartest things I have learnt

was back in the early 70s and wise investors said to me

that there are three stages to the bull market, the first

stage when only a very few foresighted people began to

believe there could be improvement. The second stage

when everybody knows things are getting better. And

the third stage when people believe things can only get

better forever. It is important to know which stage we

are. We are certainly not in the first stage, we are

probably not in the second stage. We have to worry

about being in the third stage and that is why I think it is

important to be cautious.”

“The biggest risk of all is the possibility of rising interest

rates. Rates have declined quite steadily for the last 40

years. This has been a huge tailwind for investors, since a

declining-rate environment lowers the demanded

returns on assets, making for higher asset prices. The

linkage between falling interest rates and rising asset

valuations is a good part of the reason why p/e ratios on

stocks are above average and bond yields are the lowest

we’ve ever seen. But the downtrend in rates is over.

Thus, while interest rates can rise from here – implying

higher demanded returns on everything and thus lower

asset prices – they can’t decline. This creates a

negatively asymmetrical proposition. So today’s high

asset prices may be justified at today’s interest rates, but

that’s clearly a source of vulnerability if rates were to

rise.”

Also Charlie Munger recently said that the U.S. Stock

Market is overvalued, but he doesn’t know when the

bubble will burst. The inconvenient question to be

answered is how much cash you want to keep aside to

be able to invest when the bubble bursts, knowing that

you don’t know when it will burst.

Terry Smith

Terry Smith, founder and chief executive of Fundsmith,

looks for companies with above average ROCE, gross

margin, operating margin, cash conversion ratio and

interest cover ratio. That is certainly a solid approach

and the results speak for themselves: an annual

compounded annual growth rate (CAGR) for the

portfolio of 18.2% since November 2010. His way of

working?

Buy good companies. Don’t overpay.

Do nothing.

Copyright © 2021 by The Value Firm®. All rights reserved.

Here are the Terry Smith 10 Golden Rules:

1. If you don’t fully understand it, don’t invest

2. Don’t try to time the market

3. Minimize fees

4. Deal as infrequently as possible

5. Don’t over diversify

6. Never invest just to avoid tax

7. Never invest in poor quality companies

8. Buy shares in a business which can be run by an idiot

9. Don’t engage in “greater fool theory”

10. If you don’t like what’s happening to your shares,

switch off the screen

The 10 year CAGR of 18.2% is exceptional. He would do

even better than that if he decided to just focus on

Hyper Value Creators (HVCs).

So what is a HVC? Well, the Oracle of Omaha Warren

Buffett once said that a good company is a company that

earns a high rate of return on tangible assets. And the

best ones are the ones that earn a high rate of return on

tangible assets and grow.

What I am looking for is the very best of the best, the

Hyper Value Creators (HVCs), and these are companies

with an exceptional high Value Creation Engine (VCE),

which is indeed a for growth adjusted Return on

Invested Capital (ROIC) measure. In the Terry Smith

portfolio there are quite some Hyper Value Creators:

Company TSR (%)

Microsoft Corp. 787

IDEXX Laboratories 1318

Facebook Inc. 583

Intuit Inc. 683

Philip Morris Intl. 37

Visa Inc. 103

Starbucks Corp. 542

Qualys Inc. 603

Fortinet Inc. 746

Verisign Inc. 452

Paycom Software Inc. 2469

Mercadolibre Inc. 2647

Zoetis Inc. 413

PayPal 665

MSCI Inc. 1063

The TSR (%) is the 10 year Total Stock Return as per 23

February 2021. On average, that is a 10 year gross CAGR

of 25.6%.

And if we look at the companies that did not make the

grade of a Hyper Value Creator, the 10 year gross CAGR

of this group of stocks was 17%, which is still great.

It makes a lot of sense to focus on the Hyper Value

Creators. Invest in the best, forget about the rest.

American Association of

Individual Investors

On March 10, the American Association of Individual

Investors (AAII) covered the stock-picking strategy of

Warren Buffett and gave us a list of 30 stocks that

passed their screen based on Robert Hagstrom’s

extensive writings about Buffett’s approach. You can find

the article HERE.

Here is the list of Hyper Value Creators found in the 30

stock list of the Buffett Hagstrom screener:

Company Market Cap P/S

Fortinet Inc 30263 11,7

Medifast Inc 2918 3,1

Chemed Corporation 7100 3,4

The Ensign Group, Inc. 4907 2,0

Accenture Plc 166575 3,8

ABIOMED, Inc. 13576 16,1

Qualys Inc 3977 11,0

National Beverage Corp. 5204 5,2

Logitech International SA (USA) 16225 5,5

Humana Inc 53604 0,7

WNS (Holdings) Limited (ADR) 3899 4,2

Facebook Inc 765031 8,9

Arista Networks Inc 21623 9,3

11 March 2021

The 10 year average Total Shareholder Return, TSR (%),

of the Hyper Value Creators is 760%.

Some might think that “the algorithm” is “just” another

type of Buffett Munger screener. Yes and no. Of course I

use the well proven Buffett metrics like return on

invested capital (ROC/ROIC) , but there is much more to

it. I believe that “the algorithm” better balances risk,

growth and profitability than any other “screener” that I

know of and also has a better approach towards ranking

the stocks. But I am perfectly ready to be proven wrong.

Copyright © 2021 by The Value Firm®. All rights reserved.

Alta Fox Capital Management

Connor Haley founded Alta Fox Capital Management, LLC

in April 2018. It’s a long/short hedge fund based in Fort

Worth, Texas. They scour the world for the highest

quality businesses at the lowest possible prices

regardless of size. This often leads to unusual corners of

the market that the majority of institutional investors

cannot or do not consider.

Their prototypical investment is a high-quality business

that has not yet attracted significant institutional

coverage, is not included in major stock indices, and has

a multi-year profitable growth runway with high returns

on capital. It is their belief that these undiscovered

gems can produce attractive and often uncorrelated

results relative to the broader market.

The Alta Fox 2020 Summer Intern Class Project,

consisting of Owen Stimpson, Max Schieferdecker and

Elizabeth DeSouza, analyzed the highest performing

stocks over the last five years and identified their

common characteristics, trends, and catalysts to identify

strategies to find the next set of high performing stocks.

These interns did a fantastic job. It’s definitely worth

reading. You can find it on the Alta Fox website.

They researched the business of each company

individually using a standardized 6-page slide deck

format and compiled quantitative and qualitative data

from all companies, analyzed it, and then drew

conclusions based on it. Here are the 5 high-level

takeaways and a framework to screen for future multi-

baggers:

1. Look for businesses with advantageous positioning:

80% of businesses had moderate-to-high barriers to

entry and 91% had moderate-to-high competitive

advantages.

2. Spend time on financially healthy companies: 88% of

outperformers came from a position of financial

health in June 2015 and grew faster than the market

might have anticipated. Looking for financially

healthy companies, rather than turnarounds, is also

less risky.

3. Acquisitions can create value: While many

acquisitions fail to create value, the highest

performing stocks often leverage acquisitions to

bolster their returns. If you are looking for

phenomenal returns, finding companies that make

strong acquisitions will increase your odds of

success.

4. Don’t rely on multiples: While it is always better to

buy a great business at a low multiple rather than a

high one, many of the top performing stocks began

with already healthy multiples – those multiples

often expanded even further.

5. Be open to international companies.

The third one is an eye opener to me:

The highest performing stocks often

leverage acquisitions to bolster their returns.

Thank you, Elisabeth, Max and Owen. Let me return the

favor. What I would like to add to this list is: look for an

operator-owner with skin in the game and/or a family-

controlled business. Here is a chart that illustrates how

founder led companies outperform:

I mentioned before that “the algorithm” has this ability

to identify Hyper Value Creators early in their

competitive life cycle. The algorithm was designed with

something that’s known as “reinforcement learning” in

mind. Reinforcement learning, also known as “learning

by trial and error” is one of the basic building blocks of

the Artificial Intelligence programs used by DeepMind, to

develop software that’s able to play Atari Games very

well.

I studied stocks that did very well over the last 10 years,

like Amazon, Monster Beverage and Mercadolibre,

looking for commonalities is terms of balance sheet

strength, return on invested capital (ROIC) and growth. I

put these insights into code and ran “the algorithm” on

the financial data from 2005 to 2009 for all NYSE or

Copyright © 2021 by The Value Firm®. All rights reserved.

NASDAQ listed companies by then. The result was not

very compelling.

Then I studied these mediocre results, identified

improvements, put it into code and ran “the algorithm”.

Again not very compelling. So I studied the results,

etcetera, etcetera. And that’s what you repeat time after

time, until you come up with something that actually

works in terms of generating a list of 25 stocks with a

high degree of multi-baggers in it, based upon the 2005

to 2009 financial data.

What you look for is something that worked very well in

the past and what you hope for is that it will work very

well from now on and way into the future. The Value

Creation Engine (VCE), a for growth adjusted return on

capital (ROIC) measure, is based upon the results of this

reinforcement learning approach that I applied to the

historical financial data of superior multi-baggers. Is this

a winning formula? I just don’t know. But given its back

test results, which you can find in the Winter 2021

Edition on Intelligent Cloning, it would be a fantastic act

of omission not to give it a go.

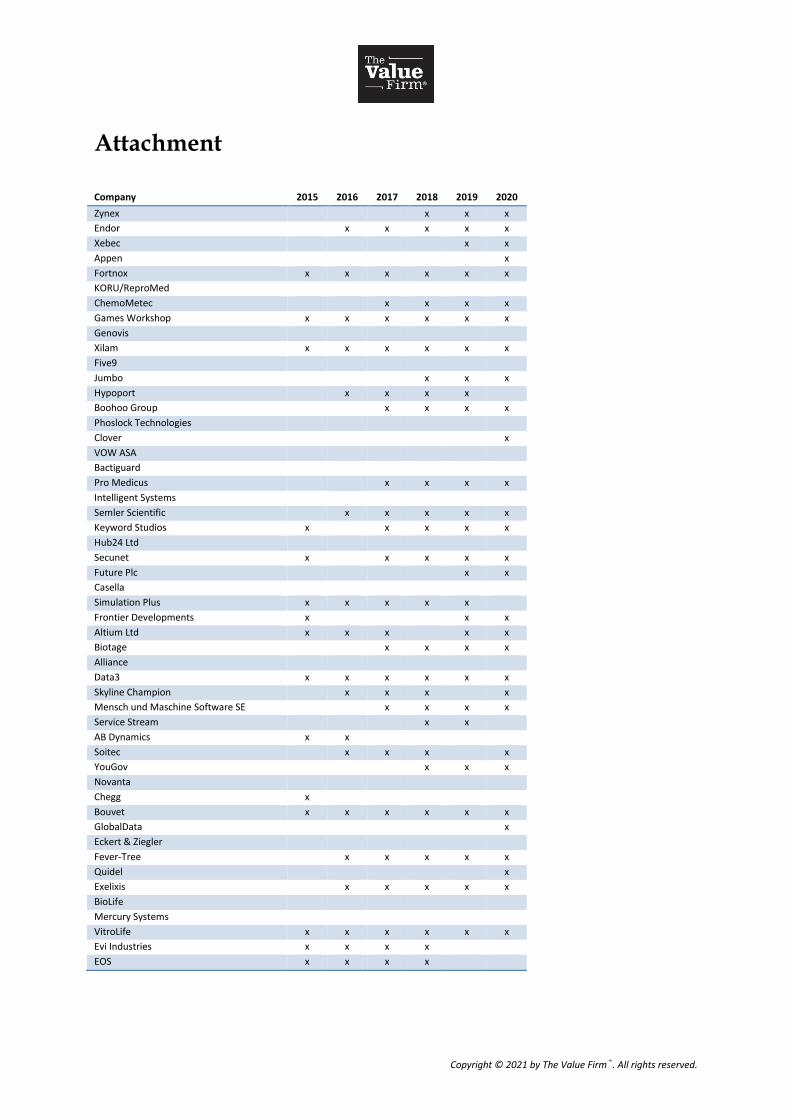

I ran the algorithm on the 104 Alta Fox multi-baggers to

find out if “the algorithm” was able to identify these

companies as a Hyper Value Creator. Please find the

results in the attachment.

For instance, Zynex, the first company on the list, was

identified by the algorithm as a Hyper Value Creator in

2018, based upon the financial data from 2013 to 2017.

The algorithm was able to identify 25% of these multi-

baggers in 2015. And since you only have to find a few

ideas a year, I am more than happy with the result.

As you know, most of the todays great companies once

started as a small one. And there comes a time when

such a company, early in its competitive life cycle,

catches up steam and steps on the path of “robust

profitable growth”, or “profitable compounding” if you

will. The algorithm surely helps to identify that moment

in time.

So here we are

If I had to set up a new fund today, it would have almost

the same characteristics as the Brown Capital

Management International Small Company (BCSVX).

That’s actually the fund where I “cloned” my latest

investment in XPEL from.

Finding tomorrow’s star growth stocks today is not easy.

What to look for are “exceptional growth companies”,

with four qualities: solid revenue growth, a competitive,

sustainable position in its industry, executives with a

vision of the future and an ability to make it happen, and

profitability to fuel and sustain earnings growth. That’s

how Brown Capital defines it and I agree.

Many of the BCSVX holdings tilt toward e-commerce,

electronic payments, smart logistics, cloud adoption and

innovative health care solutions. German health care

firms Evotec and Stratec and Canadian logistics company

Kinaxis are amongst the fund’s top holdings.

The new fund I am thinking of would look for these type

of Hyper Value Creators (HVCs) early in their competitive

life cycle, when they are still small. The fund would be a

stocks only fund. No leverage, no derivatives, no shorts,

no bull shit.

Actually, I am looking for one or more entrepreneur(s) or

strategic partner(s) with the courage to give it a go and

who provide a critical mass of capital in exchange for

economic participation in the fund. I am open to discuss

a seed model based upon revenue sharing.

There is an Investor Presentation available. Let’s set up a

ZOOM meeting to discuss it in a 10 minute presentation.

Just send me an email: [email protected]. For

professional investors only.

Stay safe!

All of those risk models…

They are great, until complete chaos happens.

Peter

Peter Coenen

Founder & CEO

The Value Firm®

28 March 2021

Copyright © 2021 by The Value Firm®. All rights reserved.

This presentation and the information contained herein are for

educational and informational purposes only and do not

constitute, and should not be construed as, an offer to sell, or a

solicitation of an offer to buy, any securities or related financial

instruments. Responses to any inquiry that may involve the

rendering of personalized investment advice or effecting or

attempting to effect transactions in securities will not be made

absent compliance with applicable laws or regulations

(including broker dealer, investment adviser or applicable agent

or representative registration requirements), or applicable

exemptions or exclusions therefrom. The Value Firm® makes no

representation, and it should not be assumed, that past

investment performance is an indication of future results.

Moreover, wherever there is the potential for profit there is also

the possibility of loss.

Everybody makes mistakes now and then. If you find any, let me

know: [email protected]. Always do your own research!

Copyright © 2021 by The Value Firm®. All rights reserved.

Attachment

Company 2015 2016 2017 2018 2019 2020

Zynex x x x

Endor x x x x x

Xebec x x

Appen x

Fortnox x x x x x x

KORU/ReproMed ChemoMetec x x x x

Games Workshop x x x x x x

Genovis Xilam x x x x x x

Five9 Jumbo x x x

Hypoport x x x x

Boohoo Group x x x x

Phoslock Technologies Clover x

VOW ASA Bactiguard Pro Medicus x x x x

Intelligent Systems Semler Scientific x x x x x

Keyword Studios x x x x x

Hub24 Ltd Secunet x x x x x

Future Plc x x

Casella Simulation Plus x x x x x

Frontier Developments x x x

Altium Ltd x x x x x

Biotage x x x x

Alliance Data3 x x x x x x

Skyline Champion x x x x

Mensch und Maschine Software SE x x x x

Service Stream x x

AB Dynamics x x Soitec x x x x

YouGov x x x

Novanta Chegg x Bouvet x x x x x x

GlobalData x

Eckert & Ziegler Fever-Tree x x x x x

Quidel x

Exelixis x x x x x

BioLife Mercury Systems VitroLife x x x x x x

Evi Industries x x x x EOS x x x x

Copyright © 2021 by The Value Firm®. All rights reserved.

Company 2015 2016 2017 2018 2019 2020

BioVentix x x x x x x

Tristel x x MedCap x

Enlabs Solutions 30 LUNA Medistim ASA AMBU B Learning Technologies Group x x x x x

Note x Dicker Data x x x

Aphria CargoJet Kitron x XPEL x x x x x x

JD Sports Fashion x x x x Invisio x x x x x

Kinaksis x x

RWS Group Eldorado Resorts FOX Factory x x

Beijer Ref x

Bachem ETSY x x x

Biotelemetry x x x

Hexatronic x x Arrowhead Medios AG Amedisys x x x

Design Group Ideagen x x

Sectra x x x x

Tomra ATOSS Software x x x x x x

Esker x x x x x

Bechtle LGI Homes x x x x

Globalscape Datagroup x City Chic Collective x

Gamma x x x x x

National Research Corporation x x x x x x

Troax x Neogenomics S&T AG x x Salmar x x x x x x

Vitec IVU Traffic Technologies x x

Inphi x x x Entegris x x Norway Royal Salmon x x x

Also x