instructions for preparing 2017 form 500, virginia ... · page 2 instructions for preparing 2017...

TRANSCRIPT

Instructions for Preparing

2017 FORM 500Virginia Corporation Income Tax Return

2601005 Rev. 08/17

Commonwealth of VirginiaDepartment of Taxation

Richmond, Virginia

www.tax.virginia.gov

Contents

What’s New .....................................................................................................................................1 Advancement of Virginia’s Fixed Date Conformity with the Internal Revenue Code .................... 1 ModifiedMethodofApportionmentforTaxpayerswithEnterpriseDataCenterOperations ......... 1 New Administrative Fees .............................................................................................................. 1General Information ....................................................................................................................... 2 CorporationsRequiredtoFile ....................................................................................................... 2 ExemptCorporations .................................................................................................................... 2 Period to be Covered by Return ................................................................................................... 3 Accounting Methods ..................................................................................................................... 3 When to File .................................................................................................................................. 3 How to File .................................................................................................................................... 3 ElectronicFiling............................................................................................................................. 3 ExtensionofTimetoFile............................................................................................................... 4 Penalties and Interest .................................................................................................................. 4 Return Forms and Schedules ....................................................................................................... 5 Consolidated or Combined Returns .............................................................................................. 5 In-StateCorporations .................................................................................................................... 6 MultistateCorporations ................................................................................................................ 6 ReportofChangeinFederalTaxableIncome .............................................................................. 6 NetOperatingLossDeductions ................................................................................................... 7 EstimatedIncomeTax .................................................................................................................. 7 VirginiaTaxableIncome ............................................................................................................... 7Form 500 Line Instructions............................................................................................................ 7Instructions for Schedule 500ADJ .............................................................................................. 10 FixedDateConformityUpdatesfor2017.................................................................................... 10 SectionA-AdditionstoFederalTaxableIncome ........................................................................ 11 SectionB-SubtractionsfromFederalTaxableIncome .....................................................................12 Section C - Amended Return ...................................................................................................... 14 Section D - Schedule of VK-1 Withholding ................................................................................. 14Tax Credits ................................................................................................................................... 14

Page 1

What’s New

Advancement of Virginia’s Fixed Date Conformity with the Internal Revenue CodeVirginia’s date of conformity with the Internal Revenue Code (IRC) was advanced from December 31, 2015 to December 31,2016,withlimitedexceptions.Virginiawillcontinuetodeconformfromthebonusdepreciationallowedforcertainassetsunderfederallaw;thefive-yearcarrybackofcertainfederalnetoperatingloss(NOL)deductionsgeneratedinTaxableYear2008or2009;thefederalincometaxtreatmentofapplicablehighyielddiscountobligations;andthefederalincometaxtreatment of cancellation of debt income realized in connection with certain business debts.Atthetimetheseinstructionswenttoprint,theonlyrequiredfixeddateconformityadjustmentswerethosementionedabove.However,iflegislationisenactedthatresultsinchangestotheIRCforthe2017taxableyear,taxpayersmayneedtomakeadjustmentstotheirVirginiareturnsthatarenotdescribedintheseinstructions.InformationaboutanysuchadjustmentswillbepostedontheDepartment’swebsiteatwww.tax.virginia.gov.

Modified Method of Apportionment for Taxpayers with Enterprise Data Center OperationsAtaxpayerwithanenterprisedatacenteroperationthatentersintoamemorandumofunderstandingwiththeVirginiaEconomicDevelopmentPartnershipAuthority(“VEDP”)tomakeanewcapitalinvestmentofatleast$150millioninanenterprisedatacenterinVirginiaisrequiredtoapportionVirginiataxableincomeusingasinglesalesfactormethodofapportionment.Thismodifiedmethodofapportionmentisphasedinasfollows:

• From July 1, 2016 until July 1, 2017,qualifyingcorporationsarerequiredtouseaquadruple-weightedsalesfactor;and• From July 1, 2017 and thereafter, qualifying corporations are required to use the single sales factormethodof

apportionment.New Administrative Fees

Legislationenactedbythe2017GeneralAssemblyimposesadministrativefeesforeachrequestfor:• AnofferincompromisewithrespecttodoubtfulcollectibilityunderVa. Code § 58.1-105; • A letter ruling under Va. Code § 58.1-203; • AlocalbusinesstaxadvisoryopinionunderVa. Code §§ 58.1-3701 or 58.1-3983.1; and• AcorporateincometaxfilingstatuschangerequestunderVa. Code § 58.1-442.

ThefeesareeffectiveJuly1,2017andmustbepaidatthetimetherequestismade.Taxpayersmayrequestwaiversfromtheseadministrativefees.WaiverswillbegrantedonlyiftheTaxCommissionerfindsthatthefeecreatesanunreasonableburdenonthepersonmakingtherequest.Forfurtherinformation,seetheinstructionsontherelevantfeeform.AdditionalinformationisavailableontheDepartment’swebsiteatwww.tax.virginia.gov.

Assistancewww.tax.virginia.gov

TheDepartment’swebsitecontainsvaluableinformationtohelpyou.

• Online Services-Linktoonlineregistration,filing,payment,andotherelectronicservices.• Laws, Rules, & Decisions –AccesstheCodeofVirginia,TaxRegulations,LegislativeSummaries,RulingsbytheTax

Commissioner,TaxBulletins,andAttorneyGeneralOpinions.• Email Updates –Signupandstayinformed.Bysubscribing,youwillperiodicallyreceiveautomaticemailnotifications

regardinglegislativechanges,filingreminders,andotherrelevantinformation.

Customer Service Inquiries

DepartmentofTaxationP.O.Box1115

Richmond, Virginia 23218-1115

Phone: (804) 367-8037Fax:(804)254-6111

Forms Requests

DepartmentofTaxationP.O.Box1317

Richmond, Virginia 23218-1317

Phone: (804) 367-8037or visit www.tax.virginia.gov

Page 2

Instructions for Preparing 2017 Form 500, Virginia Corporation Income Tax Return

General Information

Corporations Required to FileEverycorporationorganizedunderthelawsofVirginia,everyforeigncorporationregisteredwiththeStateCorporationCommissionfortheprivilegeofdoingbusinessinVirginia,andeverycorporationhavingincomefromVirginiasources,asidefromcorporationsthatqualifyforanexception,must(with theexceptionsstated in these instructions) fileareturnthroughtheFederal/Statee-Fileprogram.Thereturnshouldbesubmittedandacceptedonorbeforethe15thdayofthe4thmonth(15thdayofthe6thmonthfornonprofitcorporations)followingthecloseofitstaxableyear.Receivers,trusteesindissolution,trusteesinbankruptcy,andassignees,operatingthepropertyorbusinessofcorporationsmustmakereturnsof incomeforsuchcorporations.Ifareceiver has full custody of and control over the business orpropertyofacorporation,heisdeemedtobeoperatingsuchbusinessorproperty,whetherheiscarryingonthebusinessforwhichthecorporationwasorganizedorisonlyinmarshaling,selling,ordisposingofitsassetsforpurposesofliquidation(Va. Code § 58.1-441).A Foreign Sales Corporation (FSC) and any incomeattributable to an FSC are exempt under Virginia law;however,itmaybenecessaryforanFSCtofileaninformationreturnifitmeetstheprovisionsofVa. Code § 58.1-441 and the regulations thereunder.Anyelectricsupplier,pipelinedistributioncompany,gasutility,orgassupplierthatissubjecttofederalincometaxisalsosubjecttotheVirginiacorporationincometaxandshouldfileaVirginiaCorporationIncomeTaxReturn,Form500.Electricsuppliersmaybesubjecttoaminimumtaxinsteadofthecorporatetaxforanytaxableyearthattheirminimumtaxliabilityisgreaterthantheircorporateincometaxliability.Schedule500ELisusedtocomputetheminimumtaxanddeterminewhichtaxapplies.ElectricCooperativesaresubject to taxonallmodifiednetincomederivedfromnonmembersalesandmustfileaForm500ECevenifnotaxisdue.Electriccooperativesmaybesubjecttoaminimumtaxinsteadofthemodifiednetincome tax if their minimum tax liability is greater than their modifiednetincometaxliability.SeeSchedule500MT.ACaptiveREITisrequiredtoaddbackanyfederaldeductionfordividendspaidtoitsshareholders.Itwillthenallocateandapportionincome,andpayVirginiaincometax,inthesamemannerasothercorporations.ACaptiveREITisdefinedasaREIT:(i) whosesharesarenotpubliclytraded,(ii) 50%ormoreofthesharesareownedbyacorporate

entity, and

(iii) morethan25%oftheincomeoftheREITconsistsofrentsfromrealproperty.

ExceptionsareprovidedtoensurethatanaffiliatedgroupofREITswillnotbeconsideredcaptiveREITsunlesstheultimateownershipofthegroupisbyasinglecorporateentity. Also, entities organized under the laws of Australia and otherforeigncountriesthataresimilartoREITswillnotbeconsideredacaptiveREIT,iftheyarewidelyheld.Inaddition,fortaxableyearsbeginningonorafterJanuary1,2016,anyvotingpowerorvalueofthebeneficialinterestsorsharesinaREITthatareheldinaseparateassetaccountofalifeinsurancecorporationareexcludedfromconsiderationforpurposesofdeterminingwhethertheREITisacaptiveREITforpurposesoftheaddition.Electingsmallbusinesscorporations,not taxableascorporationsunderVa. Code§58.1-400,arerequiredtofileForm502,Pass-ThroughEntityReturnofIncomeandReturnofNonresidentWithholdingTax.Exempt CorporationsCorporations not organized for pecuniary profit, whicharealsoexemptfromincometaxunderIRC§501(c),aretaxed only on their unrelated business taxable income and mustreportthatunrelatedbusinessincomeonForm500;otherwise,noreturnsarerequired.Publicservicecorporationsthatpayastatefranchisetaxorlicensetaxupongrossreceipts,insurancecompaniesthatpayastate licensetaxongrosspremiumsandreciprocalor inter-insurance exchanges that pay a premium tax tothe state are not required to file an income tax return.Additionally,stateandnationalbanks,bankingassociations,trustcompanies,andcreditunionsorganizedandconductedas banking institutions are not taxed on their incomebyVirginiaandarenot required tofilean income tax return.In addition, effective for taxable years beginning on or after January1,2014, Interest-ChargedDomestic InternationalSalesCorporations (IC-DISCs) are exempt fromVirginiaCorporationIncomeTaxandarenotrequiredtofileanincometax return (Va. Code § 58.1-401).Nonprofit Hospitals Nonprofit hospitalsarerequiredtoprovidetheDepartmentwithacopyofthehospital’sfederalForm990orForm990-EZ(orthesuccessorformtosuchform)thatwasfiledwiththeInternalRevenueService for the relevant year.Nonprofithospitalsarenot required tofileaForm500; therefore,apapercopyofthefederalForm990orForm990-EZmustbemaileddirectlytotheDepartment.ApapercopyoftheformmustbeprovidedtotheDepartmentwithin30daysfollowingthefilingofthefederalForm990orForm990-EZtaxformwiththeInternalRevenueService.Inaddition,suchhospitalmustprovidetheDepartmentacopyofanyinterimtaxform,

(References are to the Code of Virginia, unless otherwise noted)

Page 3

report,orreturnthatthehospitalfiledwithorprovidedtotheInternalRevenueServicefortherelevantyearpursuanttoTitle26oftheUnitedStatesCodeortherulesandregulationsthereunder.Thecopyoftheinterimtaxform,report,orreturnmustbeprovidedtotheDepartmentwithin30daysfollowingthefilingofthesamewith,ortheprovidingofthesameto,the Internal Revenue Service.Period to be Covered by ReturnAcorporation’staxableyearisthesameasitstaxableyearforfederalincometaxpurposes.Ifacorporation’staxableyearischangedforfederalincometaxpurposes,itstaxableyearalsochangesforstateincometaxpurposes(Va. Code § 58.1-440).Accounting MethodsAcorporation’smethodofaccountingisthesameasitsmethodofaccountingforfederalincometaxpurposes.Inthe absence of any method of accounting for federal income taxpurposes,Virginiataxableincomemustbecomputedusing the accounting method that is regularly used in the corporation’sbookkeeping,providedsuchmethodclearlyreflects income in theopinionof theDepartment. Ifacorporation’saccountingmethodchangesforfederalincometaxpurposes,italsochangesforstateincometaxpurposes(Va. Code § 58.1-440).Standard Apportionment Method for Corporations A double-weighted sales factor is used for corporateapportionment. Under this formula, the sales factoris weighted 50% and payroll and property are bothweighted25%indeterminingtheoverallcorporateincomeapportionmentfactor.Apportionment for Manufacturers - Alternative ElectionQualifyingmanufacturingcorporationsmayelecttodeterminetheir Virginia taxable income by using a single sales factor methodofapportionmentbasedonsales.Forpurposesofthiselection,amanufacturingcorporationisdefinedasadomesticorforeigncorporationprimarilyengagedinactivitiesthatinaccordancewiththeNorthAmericanIndustryClassificationSystem (NAICS), United States Manual, United States OfficeofManagementandBudget,1997Edition,wouldbeincluded in Sector 11, 31, 32, or 33. See the instructions for Schedule500Afordetailsonhowtocomputeapportionmentfactors. Apportionment for Retail CompaniesRetailcompaniesarerequiredtouseasinglesalesfactormethodofapportionment.Forpurposesofthisrequirement,aretailcompanyisdefinedasadomesticorforeigncorporationprimarilyengagedinactivities that, in accordance with the North American Industry ClassificationSystem(NAICS),UnitedStatesManual,UnitedStatesOfficeofManagementandBudget,1997Edition,would be included in Sectors 44-45.See the instructions for Schedule 500A for details on how to computeapportionmentfactors.

Apportionment for Certain Enterprise Data Center OperationsA taxpayerwith an enterprise data center operation thatenters into a memorandum of understanding with the Virginia EconomicDevelopmentPartnershipAuthority (“VEDP”) tomakeanewcapital investmentofat least$150million inanenterprisedatacenterinVirginiaisrequiredtoapportionVirginia taxable income using a single sales factor method ofapportionment.Thismodifiedmethodofapportionmentisphasedinasfollows:

• FromJuly1,2016toJuly1,2017qualifyingcorporationsarerequiredtouseaquadruple-weightedsalesfactor;and

• FromJuly1,2017andthereafter,qualifyingcorporationsarerequiredtousethesinglesalesfactormethodofapportionment.

When to FileEverycorporationincometaxreturnmustbesubmittedonor before the 15th day of the 4th month (15th day of the 6thmonthfornonprofitcorporations)followingthecloseofacorporation’staxableyear(Va. Code § 58.1-441).How to FileThe Department requires that corporation income taxreturns and payments be submitted electronically.Therearetwooptionsavailable.ReturnsmaybefiledthroughtheFederal/Statee-Fileprogram,orcertainVirginiacorporationsmay qualify to file a Form 500EZ using eForms on theDepartment’swebsite.Seebelowformoreinformation.Electronic FilingThee-File system is supportedbynumerous commercialsoftwareprograms.e-Filesoftwarewillautomaticallycheckfor completeness, correct errors, generate theapplicablecorporationincometaxschedules,andelectronicallytransmitthereturnandpaymenttotheFederal/Statee-Fileprocessingsystems.AlistofapprovedcommercialsoftwareisavailableontheDepartment’swebsite.Ifataxpaymentisrequired,thepaymentcanbemade throughe-FileoreFormsasadirectdebit,orthecorporationmaypaywithanACHcreditestablished through the corporation’s bank. The e-Fileprogramprovidesmanybenefitstocorporations:

• Thefederalandstatereturnsmaybefiledelectronicallyat the same time.

• The federal return is automatically provided to thestate electronically.

• Consolidatedandcombinedreturnsaresupported.• Portable Document Format (PDF) files of required

documents may be attached.• Choice of approved e-File software programs.

Corporationsmayfindtheircurrentsoftwarealreadysupportse-Filing.

• Theabilitytoschedulepaymentofataxduethroughdirect debit for a future datewhen filing before thedue date.

• e-Fileprioryearreturnsforupto2taxyears.

Page 4

Inordertosuccessfullye-File,thecorporationmust:• Useanapprovedcommerciale-Filesoftwareproduct.

Approvede-Filesoftwarevendorswillbelistedonourwebsite.

• Beable tocreatea readablePDF.Thismeansyoumust either have a scanner that allows you to scan documents into aPDF file, or software that allowsyou to savedocuments asaPDF.This featurewillallowyoutoe-fileyourstatereturniftheIRSdoesnotsupport the federal returnand/orschedules throughthee-Filesystem.YoucanattachunsupportedfederalreturnsandschedulesasPDFfilestotheelectronictransmission of the state return.

• TheVirginia e-File programhas been designed toaccept transmissionof the federal and state returntogetherorseparately.Thisisoftenreferredtoasastate-only transmission which can be used when the federalreturnbeingfiledisnotsupportedbythefederale-Filesystem.Thisallowsthestatereturntobee-Filedbyitself.Mostsoftwarevendorssupporttheelectronictransmission of the federal and state returns together orseparately.

• Large corporationsmust decidewhether to useanElectronicReturnOriginator(ERO)toelectronicallyfilethereturnorprepareande-Filethereturnthemselves.If a corporation chooses to prepare and e-File thereturnthemselves,theymayhavetoregisterandapplywiththeIRStoobtainanElectronicFilingIdentificationNumber(EFIN)andpossiblyanElectronicTransmitterIdentificationNumber (ETIN) depending upon thee-File option chosen.See ourwebsite for detailedinformation.

• Smallcorporationsshoulduseanonlineprovider toavoidhavingtoregisterwiththeIRSforanElectronicFilingIdentificationNumber(EFIN).

eForms (Forms 500EZ, 500CP, 500V, and 500ES)An online return, Form 500EZ, is available through theeFormsapplicationontheDepartment’swebsite.Thisreturnis a shorter version of the existing Form 500, and is designed tosimplifythefilingprocess.Youcanalsosubmitcorporationincome taxpaymentselectronically througheForms.Thisincludesreturnpayments(Form500V),estimatedpayments(Form500ES)andextensionpayments(Form500CP).UsingeFormsisafastandfreewaytofileandpaystatetaxes.To be eligible to file Form 500EZ, you must meet all of the criteria below:

• 100%ofthecorporation’sbusinessisinVirginia.• The total additions to federal taxable income are

$1,000orless.• Thetotalsubtractionsfromfederaltaxableincomeare

$1,000orless.• ThecorporationmaynotclaimtheSavingsandLoan

Association Bad Debt Deduction.• Thecorporation isnot included inaconsolidatedor

combinedfilingofanotherentity.

• The corporation claims no tax credits other thantentativetaxpaymentsorestimatedtaxpayments.

• The corporation is not required to pay federalAlternativeMinimumTax.

• ThetaxpayerisnotaTelecommunicationsCorporationrequiredtofileForm500ToranElectricCooperativerequiredtofileSchedule500EL.

• ThecorporationwillnotclaimaNetOperatingLossDeductionfortheyearbeingfiled.

• TheCorporationisnotaPass-ThroughEntity.• TheFederalTaxableIncomeoftheCorporationmay

notexceed$40,000forthetaxableyearofthisform.• The Corporation may not have any Fixed-Date

ConformityAdjustmentsorModifications.Ifthecorporationmeetstheaboveconditions,completeandfileForm500EZontheDepartment’swebsiteundereFormsat www.tax.virginia.gov.Waiver RequestIf you are unable to file and pay electronically, youmayrequestawaiver.Allrequestsforwaiversmustbesubmittedto the Department in writing using the CorporationIncomeTaxElectronicFilingWaiverRequest formon theDepartment’swebsiteatwww.tax.virginia.gov. Extension of Time to FileYouareallowedanautomatic7-monthextensionoftime(6monthsfornonprofitcorporationsandentitiesotherthanCcorporations)tofileyourcorporationincometaxreturn.Thisprovisiondoesnotextendtheduedateforpaymentoftaxes;andyoumustpayatleast90%ofyourtaxduebytheoriginalduedateforfilingthereturn.IfForm500isfiledwithintheautomaticextensionperiod,butlessthan90%ofthetaxliabilitywaspaidbytheoriginalduedate,anextensionpenaltywillapply.Theextensionpenaltyisimposedattherateof2%permonthorfractionthereof from the original due date through the date of full paymentortheextendedreturnduedate,whicheveroccursfirst,toamaximumof14%(12%fornonprofitcorporationsandentitiesotherthanCcorporations).Ifanadditionaltaxpaymentisneededtoensurethatthetaxliabilityhasbeenpaid,theextensionpaymentmustbemadeelectronically.TheDepartmentprovidestwosecureonlineoptionsforsubmittingextensionpayments,eForms(usingForm500CP)andBusinessiFile.CorporationscanalsopayusinganACHcredittransaction.Electriccooperativesarerequiredtomakesufficientpaymentsbasedontheirestimatedmodifiednetincome tax liability. If the return is filed after the extended due date, a 30% late filing penalty will apply on the balance of tax due with the return. The minimum penalty for failure to file timely is $100. If any amount of the tax is underestimated, interest accrues attheunderpaymentratesetinIRC§6621,plus2%.Penalties and Interest Ifthereturnisfiledwithinthe7-monthextension(6monthsfornonprofitcorporationsandentitiesotherthanCcorporations),

Page 5

but the corporation failed to pay 90%of the tax due bythe original due date, then the corporation is subject toan extension penalty of 2% permonth or fraction of amonth thereof from the original due date to the filing ofthecorporation incometaxreturn to thedateofpayment.Thepenalty isapplied to thebalanceof taxduewith thereturnfromtheoriginalduedatethroughthedateoffiling.Themaximumextensionpenaltyis14%(12%fornonprofitcorporationsandentitiesotherthanCcorporations)ofthetaxdue. If the return isfiledafter theextendedduedate,theextensionprovisionsdonotapplyandthecorporationissubjecttothelatefilingpenalty(Va. Code § 58.1-455). In nocasewillthepenaltyforfailuretofiletimelybelessthan$100,andthisminimum$100penaltyapplieswhetherornottaxisduefortheperiodcoveredbythereturn.IfForm500isfiledwithintheextensionperiodandthetotalamountdueisnotincludedwiththereturn,thelatepaymentpenaltywillbeassessedattherateof6%permonthfromthedateoffilingthroughthedateofpayment,uptoamaximumof30%ofthetaxdue.Civilandcriminalpenaltiesmaybeimposedforfilingafraudulentreturn.Thecriminalpenaltyforfilingafraudulentreturn is a Class 6 felony (Va. Code § 58.1-451 and Va. Code §58.1-452).InterestontheunpaidbalanceofanytaxandpenaltyischargedattheunderpaymentrateestablishedbyIRC§6621,plus2%,fromtheduedateuntilpaid.Penalty for Returned Check or EFT Nonpayment.IfyourbankdoesnothonoryourpaymenttotheDepartment,theDepartmentmayimposeapenaltyof$35,asauthorizedby Va. Code§2.2-614.1.Thispenaltywillbeassessedinadditiontootherpenaltiesdue.Return Forms and SchedulesListed below are the available forms and schedules tosubmit through the Federal/State e-File Program.• Form 500 – Corporation Income Tax Return. Used

tocomputeacorporation’sincometaxliabilityandtodetermine the amount of tax due or the amount of the refund.

• Schedule 500ADJ – Schedule of Adjustments. Used toreportadditionstoortoclaimsubtractionsfromFederalTaxableIncomeandtoclaimwithholdingreportedtoacorporationbyaPass-ThroughEntityonVirginiaScheduleVK-1.Also,usedtocomputethecorrectedtaxliability for an amended Form 500.

• Schedule 500CR – Schedule of Credits. Used to claim both nonrefundable and refundable credits.

• Schedule 500FED – Schedule of Federal Line Items. Usedtoreportspecificlineitemsfromthecorporation’sfederal income tax return.

• Schedule 500A – Multistate Corporation. Used to allocateandapportion incomebycorporations thattransactorconductpartoftheirbusinesswithinVirginiaandpartoftheirbusinessoutsideVirginia.

• Schedule 500AB – Schedule of Related Entity Add Backs and Exceptions.Usedto:(i)addbackcertaindeductionsthatmaybetakenbyacorporationonitsfederalreturnforinterest,royalties,andotherexpenses

relatedtointangiblepropertysuchastrademarksandpatents;(ii)reportpayments;and(iii)identifyexceptions.

• Schedule 500AC – Schedule of Affiliated Corporations. CorporationsfilingasCombinedorConsolidatedarerequiredtosubmitaSchedule500ACforeachmember,includingtheparentcompany,thatisdoingbusinessinVirginia,orthathasVirginiasourceincome,andispartofthegroupincludedinthistaxreturn.ThenumberofSchedules500ACenclosedwiththereturnmustequalthenumberofaffiliatesreportedonForm500,Page1.

• Form 500C – Underpayment of Estimated Tax. Used to determine if an addition to tax charge is owed for failure bythecorporationtopaysufficientestimatedtaxduringthe taxable year.

• Form 500T – Telecommunication Companies Minimum Tax.EverytelecommunicationscompanyasdefinedbystatuteandcertifiedbytheStateCorporationCommissionmustcompleteandsubmitForm500T.

• Schedule 500EL – Electric Suppliers Corporation Minimum Tax and Credit Schedule.EveryelectricsupplierasdefinedbystatuteandcertifiedbytheStateCorporationCommissionmustcompleteandsubmitSchedule500EL.

You must also enclose a copy of the federal return.ThecorporationmustsubmitacopyoftheincometaxreturnthatitfiledwiththeIRStotheDepartment.Not all federal income tax returns are available to electronically file. If the federal incometaxreturn isnotavailable tofileelectronically, then the federal return can be attached as a PDFfiletotheVirginiaelectronicreturn.Consolidated or Combined ReturnsAffiliatedcorporationsthataresubjecttoVirginiaincometaxeshavetheoptiontofileaconsolidatedorcombinedreturninsteadoffilingseparatereturns.Twoormorecorporationsareaffiliatedwhenonecorporationowns80%ormoreoftheoutstandingvotingstockofanothercorporation(s),or80%ormoreoftheoutstandingvotingstockoftwoormorecorporationsisownedbythesameinterest.AconsolidatedreturnisasinglereturnforanaffiliatedgroupofcorporationspreparedinaccordancewiththeprinciplesofIRC § 1502 and the regulations thereunder;Acombinedreturnisasinglereturnforanaffiliatedgroupofcorporationsinwhichincomeorlossisseparatelydeterminedinaccordancewiththefollowing:

a. Virginiataxableincomeorlossiscomputedseparatelyforeachcorporation;

b. Allocable income is allocated to the state of commercial domicileseparatelyforeachcorporation;

c. Apportionable income or loss is computed usingseparateapportionmentfactorsforeachcorporation;and

d. Incomeor loss computed in accordancewith itemsathroughcaboveiscombinedandreportedonasinglereturnfortheaffiliatedgroup.

Page 6

Ifacorporationelectstofileonaseparate,consolidated,orcombinedbasis,allreturnsthereaftermustbefiledonthesamebasis,unlesstheDepartmentgrantspermissionto change the election (Va. Code § 58.1-442). A binding electionismadeinthefirstyearinwhichagroupofaffiliatedcorporationsiseligibletofileaconsolidatedorcombinedreturn in Virginia. Prior elections continue in effect and can be changed only if permission is granted by the Department.ReturnsfiledonaconsolidatedorcombinedbasismustenclosewiththegroupreturnacompletedScheduleofAffiliatedCorporations,Schedule500AC,foreachmemberincludedin the combined or consolidated Virginia return, including allaffiliatesandtheparentcompany.Allsupplementaryandsupportingschedules filedwithaconsolidatedorcombinedreturnshouldbepreparedincolumnarform,onecolumnbeingprovidedforeachcorporationincludedintheconsolidatedorcombinedreturn.Supportingschedulesforconsolidated returns should also include a column for totals oflikeitemsbeforeadjustmentsaremade,acolumnforintercompanyeliminationsandadjustments,andacolumnfortotalsoflikeitemsaftergivingeffecttotheeliminationsandadjustments.Theitemsincludedinthecolumnsforeliminations should be symbolized to readily identify contra itemsaffected,andsuitableexplanationsshouldbeaddedif necessary.Prohibition of worldwide consolidation or combination.TheDepartmentshallnotrequire,andnocorporationmayelect,thataconsolidationorcombinationofanaffiliatedgroupincludeanycontrolledforeigncorporation,theincomeofwhich is derived from sources outside of the United States (Va. Code § 58.1- 443).Change in Filing Status.Anyrequesttoswitchfromonefilingmethodtoanothermustbesubmittedbefore the due date forthefirstreturntousetherequestedfilingmethod.Therequestsshouldbemailedto:Virginia Department of Taxation, P.O. Box 27203, Richmond, VA 23218-7203.EffectiveJuly1,2017,a$100administrativefee,theFormFilingStatus-Fee,andacopyofthefederalForm851mustaccompanyallrequests.TheDepartmentwillgenerallygrantrequeststochangeafilingstatusfromseparatetocombinedorfromcombinedtoseparate.Requeststochangeafilingstatusfromseparateorcombinedtoconsolidated,orfromconsolidatedtoseparateorcombinedwillgenerallybedenied.HoweveragroupofaffiliatedcorporationsthathasfiledVirginiaincometaxreturnsonthesamebasisforatleastthepreceding20yearswillbegrantedpermissiontochangeitsfilingstatusfromconsolidatedtoseparateorfromseparatetocombinedorconsolidatedif:(1) thetaxcomputedundertheaffiliatedgroup’srequested

returnbasiswouldbeequaltoorgreaterthanthetaxfortheprecedingtaxableyear;and

(2) theaffiliatedgroupagreestocomputeitstaxliabilityunderboththenewfilingstatusandtheformerfilingstatusandpaythegreaterofthetwoamountsforthefirst2taxableyearsinwhichthenewfilingstatusiseffective.

In-State CorporationsIf theentirebusinessofthecorporationistransactedorconductedwithinVirginia,thetaxiscomputedupontheentireVirginiataxableincomeofthecorporationforeachtaxableyear.Theentirebusinessofthecorporationwillbeconsideredto have been transacted or conducted within this state if the corporationisnotsubjecttoanetincometax,afranchisetaxmeasuredbynetincomeorafranchisetaxfortheprivilegeof doing business in another state (Va. Code § 58.1-405).Multistate Corporations Acorporationhavingincomefrombusinessactivitythatistaxable both within and without Virginia must allocate and apportionitsnetincomeasprovidedinVa. Code § 58.1-406 through Va. Code§58.1-421.SuchacorporationmustcompleteandencloseSchedule500Awiththereturn.Acorporationisnottaxableinanotherstateif thatstateisprohibitedfromimposinganincometaxonthecorporationbecause its business activity in the state does not exceed theminimumstandardsset forth inPublicLaw86-272.(15 U.S.C.A. §§ 381 - 384).Report of Change in Federal Taxable IncomeIftheamountofacorporation’sfederaltaxableincomeasreportedonitsfederal incometaxreturnforanytaxableyearischangedorcorrectedbytheIRS(orothercompetentauthority), or is changed as the result of a renegotiation of a contractorsubcontractwiththeUnitedStates,thetaxpayermustreportthischangetotheDepartmentwithin one year. Anytaxpayerfilinganamendedfederalreturnmustalsofileanamendedstatereturnandmustpayanyadditionaltaxandinterestdue,ifapplicable.Refund of Virginia TaxAcorporationmayfileanamendedreturntoclaimarefundwithinthelaterof:(1) 3 years from the due date of the return or extended due

date (whichever is later);(2) 1year fromthefinaldeterminationofanychangeor

correctionintheliabilityofthetaxpayerforanyfederaltaxuponwhichthestatetaxisbased,providedthattherefund does not exceed the amount of the decrease in Virginia tax attributable to such federal change or correction;

(3) 2yearsfromthefilingofanamendedVirginiareturnresultinginthepaymentofadditionaltax,providedthatthe amended return raises issues relating only to the prioramendedreturnandtherefunddoesnotexceedthe amount of the tax paymentmadewith the prioramended return; or

(4) 2yearsfromthepaymentofanassessment,providedthat the amended return raises issues relating only to thepriorassessmentandtherefunddoesnotexceedtheamountoftaxpaidonthepriorassessment.

EncloseacopyoffederalForms1120Xor1139,theRevenueAgent’sReport,StatementofAdjustmenttoYourAccount,orother forms or statements showing the nature of any federal changeandthedatethatitbecamefinal.ForanElectric

Page 7

Cooperativesubject to themodifiednet incometax,anamendedreturnmaybefiledonForm500EC.TheFederal/Statee-Fileprogramonlysupportsamendedreturns for the current taxable year and the 2 precedingtaxableyears.Amendedreturnsforpriortaxableyearsmustbefiledbypaper.AmendedForms500ECwillalsoneedtobefiledbypaper.Fortheabove-mentionedtypesofamendedreturns, write to:Virginia Department of Taxation, P.O. Box 1500, Richmond, Virginia 23218-1500.Net Operating Loss DeductionsVirginia tax law generally conforms to the IRC as it existed onDecember31,2016.ThereisnospecificVirginiastatutoryprovisionallowingnetoperatinglossdeductions,carrybacksorcarryforwards.However,because thestartingpoint(Form500,Line1)forcomputingVirginiataxableincomeisfederaltaxableincome,taxpayersaregenerallypermittedtoclaimnetoperatinglossdeductions,carrybacks,andcarryforwardsforVirginiataxpurposestotheextentthatsuch losses were included in federal taxable income. Since federalincomemustbemodifiedforVirginiaadditionsandsubtractions, the additions and subtractions of the loss year followthefederallosstotheyearthelossisused.Thus,ifthefederalnetoperatinglossisfullyusedinacarrybackorcarryover year, the net amount of additions and subtractions willbeappliedinthesameratiototheapplicableyear.Thefederalnetoperatinglossdeductionmaybeusedonlytoreducefederaltaxableincome,andafederalnetoperatingloss deduction cannot create or increase a federal net operatingloss.Also,due to the reduced tax liability incarrybackandcarryforwardyears,anycreditspreviouslyclaimedinthoseyearsmayneedtobeadjustedaswellasthecreditcarryoveramounts.AnamendedForm500shouldbefiledindicatingthe change in the amount of credits claimed and the corrected carryoveramounts.EnclosearevisedSchedule500CRwiththeamendedreturnsfiledtoreportthechangestothecredit(s) claimed or carryover amount resulting from the net operatinglosscarryback.Inmostcases,thecarrybackperiodfornetoperatinglosseswillbethesameforfederalandVirginiapurposes.However,under IRC§172(b)(1)(H),taxpayersmaycarrybacknetoperatinglossdeductionsgeneratedintaxableyears2008and2009for5yearsforfederalpurposes.VirginiadoesnotconformtothatprovisionoftheIRCandsuchlossesmayonlybecarriedbackfor2yearsforVirginiapurposes.Consequently,totheextentthatfederalandVirginianetoperatinglosscarrybacksandcarryforwardsdiffer,separateaccountingwillberequired.Note:DonotfileForm500 tocarrybackanetoperatingloss. Use Form 500NOLD, Corporation Application forRefundCarryback ofNetOperating Loss. Be sure to filethe correct form. Using the incorrect form will delay the processingofyourreturnandmayresultinhavingyourtaxreturnsentbacktoyou.FileForm500NOLDbypaper-theformisnotsupportedbytheFederal/Statee-FileProgram.For a copy of the Virginia regulations, visit www.tax.virginia.gov. For more information, call (804) 367-8037 or

write to Virginia Department of Taxation, P.O. Box 1115, Richmond, VA 23218-1115. Estimated Income Tax Corporationestimatedincometaxes(Form500ES)mustbefiledandpaidelectronically.Visitwww.tax.virginia.gov for detailsonelectronicpaymentoptionswhichincludee-Forms,BusinessiFile,andACHcreditEFT.Incaseofanyunderpaymentofestimatedtaxbyacorporation,Va. Code§58.1-504requiresthatanadditiontotaxbemadeattheestablishedinterestrateforunderpaymentsunlessoneoftheexceptionsinthatsectionapplies.UseForm 500C tocomputethisadditiontothetaxand/ortoindicatethatanexceptionapplies.Calendar Year FilersEverycorporationsubjecttoVirginiaincometaxthatusesacalendaryearaccountingperiodisrequiredtomakeadeclaration of estimated tax for the calendar year if its Virginia incometaxfor thatperiodcanreasonablybeexpectedtoexceed$1,000.PaymentoftheestimatedtaxmustbemadetotheDepartmentasfollows:25%byApril15,25%byJune15,25%bySeptember15,and25%byDecember15.Fiscal Year FilersIfacorporation’saccountingperiod isafiscalyear, thecorporationisrequiredtomakeadeclarationofestimatedincometaxandpay25%oftheamountduetotheDepartmentby the 15th day of the 4th month following the beginning of itsfiscalyear.Subsequentinstallmentswillbepayablebythe 15th day of the 6th month, the 15th day of the 9th month, and the 15th day of the 12th month following the beginning of itsfiscalyear(Va. Code § 58.1-500 - Va. Code § 58.1-504).Virginia Taxable IncomeVirginia taxable income for a taxable year means the federaltaxableincomeforsuchyearofacorporation(orthe“investmentcompanytaxable income”of regulatedinvestmentcompanies,orthe“realestateinvestmenttrusttaxableincome”ofrealestateinvestmenttrusts,towhichshallbeaddedineachcaseanyamountofcapitalgainstaxabletothecorporationunderfederallaw)ortheunrelatedbusinesstaxableincomeoforganizationsexemptfromincometaxunderIRC§501(c),adjustedasprovidedunderVa. Code §58.1-402;exceptacorporationsubjecttotheprovisionsofVa. Code § 58.1-403.

Form 500 Instructions

Fiscal Year Filers or Short Year Filers: Complete thisline only if your taxable year is not from January 1 toDecember31.Youmustuse thesame taxableperiodonyour Virginia return as on your federal return.Check if:

• Initial Filer –ThisisyourfirsttimefilinginVirginia.• Name Change –Yournamehaschangedsinceyour

lastfiling.• Mailing Address Change –Yourmailingaddresshas

changedsinceyourlastfiling.

Page 8

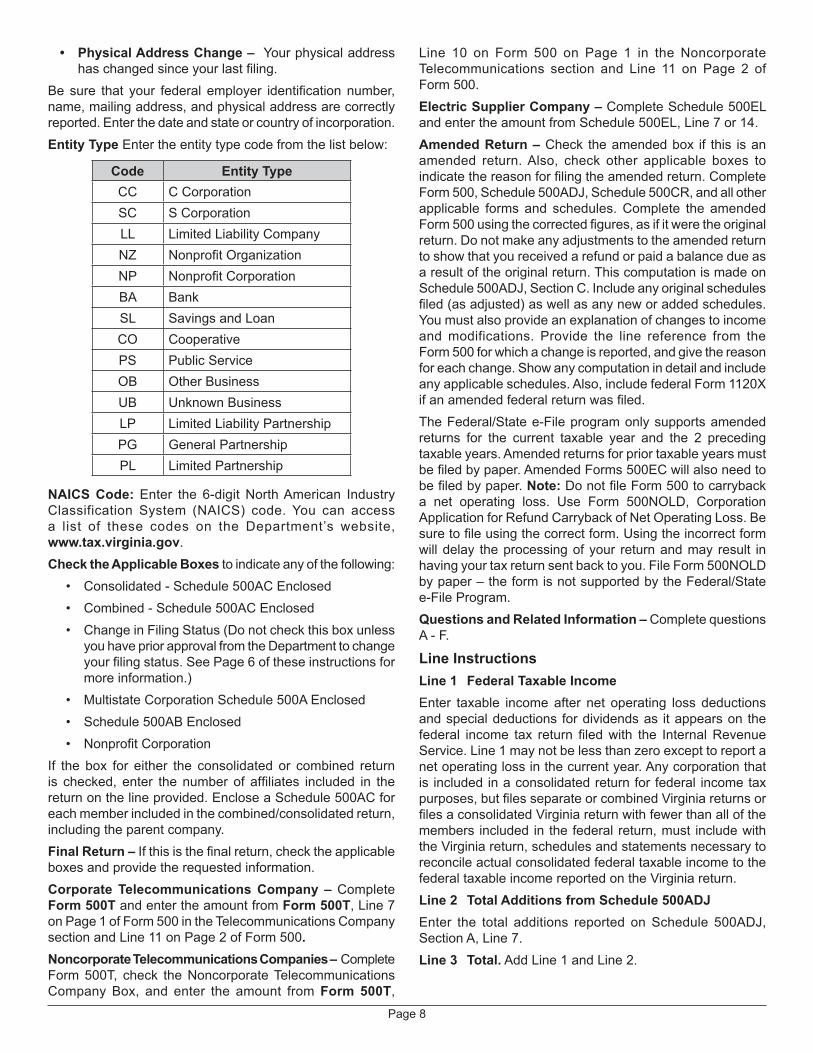

• Physical Address Change –Yourphysicaladdresshaschangedsinceyourlastfiling.

Be sure that your federal employer identification number,name,mailingaddress,andphysicaladdressarecorrectlyreported.Enterthedateandstateorcountryofincorporation.Entity TypeEntertheentitytypecodefromthelistbelow:

Code Entity TypeCC CCorporationSC SCorporationLL LimitedLiabilityCompanyNZ NonprofitOrganizationNP NonprofitCorporationBA BankSL SavingsandLoanCO CooperativePS Public ServiceOB OtherBusinessUB UnknownBusinessLP LimitedLiabilityPartnershipPG GeneralPartnershipPL LimitedPartnership

NAICS Code: Enter the 6-digitNorthAmerican IndustryClassification System (NAICS) code. You can accessa list of these codes on the Department’s website,www.tax.virginia.gov. Check the Applicable Boxestoindicateanyofthefollowing:

• Consolidated-Schedule500ACEnclosed• Combined-Schedule500ACEnclosed• ChangeinFilingStatus(Donotcheckthisboxunless

youhavepriorapprovalfromtheDepartmenttochangeyourfilingstatus.SeePage6oftheseinstructionsformore information.)

• MultistateCorporationSchedule500AEnclosed• Schedule500ABEnclosed• NonprofitCorporation

If the box for either the consolidated or combined return is checked, enter the number of affiliates included in thereturnonthelineprovided.EncloseaSchedule500ACforeach member included in the combined/consolidated return, includingtheparentcompany.Final Return –Ifthisisthefinalreturn,checktheapplicableboxesandprovidetherequestedinformation.Corporate Telecommunications Company –CompleteForm 500T and enter the amount from Form 500T,Line7on Page 1 of Form 500 intheTelecommunicationsCompanysectionandLine11onPage2ofForm500. Noncorporate Telecommunications Companies – CompleteForm500T, check theNoncorporateTelecommunicationsCompanyBox, and enter the amount fromForm 500T,

Line 10 on Form 500 on Page 1 in the NoncorporateTelecommunications section and Line 11 on Page 2 ofForm 500.Electric Supplier Company –CompleteSchedule500ELandentertheamountfromSchedule500EL,Line7or14.Amended Return –Check theamendedbox if this isanamended return.Also, check other applicable boxes toindicatethereasonforfilingtheamendedreturn.CompleteForm500,Schedule500ADJ,Schedule500CR,andallotherapplicable formsand schedules.Complete the amendedForm500usingthecorrectedfigures,asifitweretheoriginalreturn.Donotmakeanyadjustmentstotheamendedreturntoshowthatyoureceivedarefundorpaidabalancedueasaresultoftheoriginalreturn.ThiscomputationismadeonSchedule500ADJ,SectionC.Includeanyoriginalschedulesfiled(asadjusted)aswellasanyneworaddedschedules.Youmustalsoprovideanexplanationofchangestoincomeand modifications. Provide the line reference from the Form500forwhichachangeisreported,andgivethereasonforeachchange.Showanycomputationindetailandincludeanyapplicableschedules.Also,includefederalForm1120Xifanamendedfederalreturnwasfiled.TheFederal/Statee-Fileprogramonlysupportsamendedreturns for the current taxable year and the 2 precedingtaxableyears.Amendedreturnsforpriortaxableyearsmustbefiledbypaper.AmendedForms500ECwillalsoneedtobefiledbypaper.Note:DonotfileForm500tocarrybacka net operating loss. Use Form 500NOLD, CorporationApplicationforRefundCarrybackofNetOperatingLoss.Besuretofileusingthecorrectform.Usingtheincorrectformwilldelay theprocessingofyour returnandmay result inhavingyourtaxreturnsentbacktoyou.FileForm500NOLDbypaper–theformisnotsupportedbytheFederal/Statee-File Program.Questions and Related Information – CompletequestionsA - F.

Line InstructionsLine 1 Federal Taxable IncomeEnter taxable incomeafter net operating loss deductionsandspecialdeductions fordividendsas itappearson thefederal income tax return filedwith the InternalRevenueService.Line1maynotbelessthanzeroexcepttoreportanetoperatinglossinthecurrentyear.Anycorporationthatis included in a consolidated return for federal income tax purposes,butfilesseparateorcombinedVirginiareturnsorfilesaconsolidatedVirginiareturnwithfewerthanallofthemembers included in the federal return, must include with the Virginia return, schedules and statements necessary to reconcile actual consolidated federal taxable income to the federaltaxableincomereportedontheVirginiareturn.Line 2 Total Additions from Schedule 500ADJEnter the total additions reported onSchedule 500ADJ,SectionA,Line7.Line 3 Total.AddLine1andLine2.

Page 9

Theseadjustments are only available to thosemultistatecorporationsthatfileaVirginiaSchedule500A toapportionand allocate their income, and provide clear and cogentevidence that the asset producing the income servesaninvestmentfunctionthatisunrelatedtooperationalfunctions.Thedenominatoroftherelevantapportionmentfactorsmustalsobeadjustedtoexcludeitemsrelatedtotheinvestmentassets.Any taxpayerwho qualifies for an alternativemethod ofallocation and apportionment for this type of income isrequired toaddbackany loss included in federal taxableincome that is attributable to the acquisition, ownership,management,stewardship,saleorexchangeofinvestmentassets that are unrelated to the taxpayer’s operationalfunctiononLine8(d).Ifthetaxpayerhaspreviouslyclaimedasubtractionfornonapportionableinvestmentfunctionincomewithrespecttoanyinvestmentassets,theadditionisrequiredforanysubsequentlossesgeneratedbysuchassets.Burden of Proof:Asaprerequisite to theability toclaiman adjustment on Lines 8(c) and 8(d) (which effectivelyallocates incomeother thandividends) the taxpayermustbeabletodemonstratethattheapplicationofVirginialawtotheirparticularfactswillbeunconstitutional.Theburdenis on the taxpayer to provide clear and cogent evidencethat thecapital investmentwascompletely separate fromitsoperations,andthatthetaxpayer’sinvestmentfunctionwas located outside ofVirginia.The taxpayermust alsodemonstratethattheclassificationofthecapitalassetanditsincomeforVirginiapurposesisconsistentwiththemannerinwhich the incomehasbeenallocatedandapportionedwithotherstatetaxauthorities.Thetaxpayerwillbeunderaparticularlyheavyburdenofproofincaseswheretheassetwasclearlyoperationalatanytime.Objectiveevidence isrequired;anunsubstantiatedstatementastothetaxpayer’sintent,purpose,orstateofmindwillbeinsufficienttomeetthe burden.Taxpayers claiming an adjustment for nonapportionableincomeonthe2017corporatetaxreturnsmustencloseastatementwiththereturnstatingthenatureoftheadjustmentandthebasis for thepositionthatrelief isprovidedundertheConstitution.Supplementalevidenceshouldbeclearlyreferencedandincludedwiththereturn.Thetaxpayershouldsubmit all evidence considered necessary to support thetaxpayer’sposition.Foradditionalinformation,seeVirginiaTaxBulletin93-4(4/6/93).Line 9 Income TaxMultiplytheincome(Line7orLine8(a),whicheverapplies)by 6%. Line 10 Nonrefundable Tax CreditsEnterthetotalnonrefundablecreditamountallowablethisyearfromSchedule500CR,Section2,Line1B.Line 11 Adjusted Corporate TaxSubtractLine10fromLine9.TelecommunicationCompaniesshouldrefertoForm500T.ElectricSupplierCompaniesshouldrefertoSchedule500EL.

Line 4 Total Subtractions from Schedule 500ADJEnterthetotalsubtractionsreportedonSchedule500ADJ,SectionB,Line10.Line 5 Balance.SubtractLine4fromLine3.Line 6 Savings and Loan Bad Debt DeductionIfaSavingsandLoanAssociationusedthepercentageofincomemethod to compute its federal deduction for baddebts, then it must add the federal bad debt deduction and recomputethebaddebtdeductionforVirginiapurposesbymultiplyingtheamountonLine5by40%.IftheSavingsandLoanAssociationusedthepercentageofloansmethodortheexperiencemethod,entertheamountclaimedforadditionCode13onSchedule500ADJ(Va. Code § 58.1-403).Line 7 Virginia Taxable Income Subtract Line6 fromLine5.This is yourVirginia taxableincomeiftheentirebusinessofthecorporationistransactedor conducted within Virginia. Corporations other thanmultistatecorporations,skiptoLine9.Line 8 Multistate Corporations OnlyMultistatecorporationswithnoVirginiaincomemustenterzeroesin8(a)and8(b).Otherwise,followtheinstructionsforLines8(a)through8(d)below.Line 8(a) Income Subject to Virginia TaxAcorporationwithincomefrombusinessactivitythatistaxableboth within and without Virginia should enter its multistate incomethatissubjecttoVirginiataxfromSchedule500A,SectionB,Line3(j).Line 8(b) Apportionment FactorEntertheapportionmentfactorfromtheappropriatelinefromSchedule500A,SectionB,Line1or2(g).Line 8(c) and 8(d) Nonapportionable InvestmentNonapportionableInvestmentFunctionNetIncomeandLoss(applicableonlytomultistatecorporations):Virginialawdoesnotprovideforanadditionorsubtractionofthisincome,nordoesthelawprovidefortheallocationofanyincomeotherthandividends.Lines8(c)and8(d)ontheForm500recognize thatsometaxpayersmaybeentitledto analternativemethodof allocation andapportionmentif they can demonstrate that the application ofVirginia’sapportionmentlawtotheirparticularfactsforthetaxableyearwouldbecontrarytotheprinciplessetforthinAllied Signal, Inc. v. Director, Div. of Taxation, 504 U.S. 768 (1992).In Allied Signal, Inc., theCourt reaffirmed the continuedvalidityofapportionmentofanyincomereceiveddirectlybythetaxpayer, including investment incomesuchascapitalgains,unlessthecapitaltransactionservesaninvestmentfunction that is completely unrelated to any operationalactivitiescarriedoninthestate.TheCourtalsoreinforcedthe principle that investment incomemay be included inapportionableincomeifthereisaunitaryrelationshipbetweenthetaxpayerandtheentityinwhichthetaxpayerhasinvested.However, the Court made it clear that the absence of a unitary relationshipdoesnotnecessarilyprecludeapportionment.

Page 10

Line 12 Estimated Income Tax Credits Enterthetotalamountpaidasestimatedincometax.Includetheamountofoverpaymentforthetaxableyear2016,electedas a credit against 2017 estimated tax.Line 13 Extension PaymentsEntertheamountofanyextensionpayments.Line 14 Total Refundable Tax Credits EntertheamountfromSchedule500CR,Section4,Line1A.I f f i l ing a combined or consolidated return with a telecommunicationscompany,donotenterrefundablecreditsincludedonForm500T.Line 15 Pass-Through Entity Withholding from Schedule 500ADJ EnterthetotalamountofVirginiaincometaxwithheldfromSchedule500ADJ,Page2,SectionD.Line 16 Total Payments and Credits AddLines12through15.Line 17 Tax OwedIfLine11isgreaterthanLine16,subtractLine16fromLine11.Line 18 Penalty for Return Filed After the Original Due Date With or Without Payment of Amount Due(a)Iffiledwithintheextensionperiodandthebalanceoftax

dueexceeds10%oftheactualtaxliability(Line9),enter2%permonthorfractionthereofofthebalance(Line17).Themaximumextensionpenaltyis14%ofthetaxdue(12%fornonprofitcorporationsandentitiesotherthanCcorporations).Inaddition,ifthetaxisnotpaidinfullwhenthereturnisfiled,alatepaymentpenaltywillbeassessedontheamountoftaxdue(Line17)attherateof6%permonthorpartofamonthfromthedatethereturnisfiledthroughthedatethetaxispaid,uptoamaximumof30%.Ifthereturnisfiledduringtheextensionperiod,butthetaxdueisnotpaidwhenthereturnisfiled,boththeextensionpenaltyandthelatepaymentpenaltymayapply.Theextensionpenaltywillapplyfromtheduedateofthereturnthroughthedatethereturnisfiled,andthelatepaymentpenaltywillapplyfromthedatethereturnisfiledthroughthedateofpayment.Toavoidpayingthelatepaymentpenaltyduringtheextensionperiod,thetaxowedmustbepaidwhenthereturnisfiled.OR

(b)Iffiledaftertheextendedduedate,enter30%ofLine17or$100,whicheverisgreater.

Line 19 InterestEntertheamountdueattheunderpaymentrateestablishedbyIRC§6621,plus2%,fromtheduedateofthereturnuntilpayment.Thisunderpaymentrateissubjecttoquarterlyadjustment.Whenpenaltyisenteredunder18(a)above,interestisaddedfromtheduedatetothedateofpayment.

Line 20 Additional ChargeEnter theamount fromLine17,Form500C.EncloseForm 500C.Line 21 Total DueEnterthetotalofLines17,18,19,and20.Thisisthetotalamountdue.Thefollowingpaymentoptionsareavailable:

• Direct debit through the e-File system, or• ACH credit transaction.

Ifyouchoosedirectdebit,youcanscheduletopayyourtaxdueforafuturedate,whenfilingbeforetheduedate.Inaddition,paymentmaybemadeusingeForms(Form500V).Line 22 OverpaymentIfLine16isgreaterthanLine11,subtractLine11fromLine16.Line 23 Amount to be Credited to 2018Entertheamountofoverpaymentthatyouwantcreditedtoyour 2018 estimated tax, if any.Line 24 Amount to be RefundedSubtractLine23fromLine22andentertheamounttoberefunded.

Instructions for Schedule 500ADJ

FIXED DATE CONFORMITY UPDATE FOR 2017Virginia’s date of conformity with the Internal Revenue Code (IRC) was advanced from December 31, 2015 to December31,2016,withlimitedexceptions.Bonus Depreciation: Virginia will continue to disallow any bonus depreciation claimed for certain assets underIRC § 168(k) duringTaxableYear 2001 and thereafter.Virginiawill also continue to disallowbonus depreciationclaimedunder IRC§§168(l),168(m),1400L,and1400N.Totheextentthatsuchbonusdepreciationwasclaimedforfederalincometaxpurposes,thedepreciationdeductionmustberecomputedforVirginiaincometaxpurposes.FortaxableyearswhentherecomputedVirginiadepreciationdeductionislessthanthefederaldeduction,thetaxpayermustclaimaVirginiaadditionequaltothedifference.FortaxableyearswhentherecomputedVirginiadepreciationdeductionismorethanthefederaldeduction,thetaxpayermayclaimaVirginiasubtractionequaltothedifference.Applicable High Yield Discount Obligations: Virginia will continue to deconform from IRC § 163(e)(5)(F), which suspendstheapplicationof theapplicablehighyielddebtobligation(“AHYDO”)rulesforcertaindebtsissuedbetweenSeptember30,2008,andDecember31,2009.Forfederalpurposes, special rules generally apply to computing theinterestdeductionthatappliestocertainhigh-yieldoriginalissue discount obligations. Because Virginia will continue todeconformfromthefederalprovisionthatsuspendstheAHYDOrules,suchruleswillcontinuetoapplyforVirginiaincometaxpurposes.AnyresultingdifferenceinthefederalandVirginiadeductionshouldbeclaimedasamodificationon your Virginia return.

Page 11

and17-1whichareavailableontheDepartment’swebsite:www.tax.virginia.gov or call (804) 367-8037. Otherchangesnotlisted–VisittheDepartment’swebsite,www.tax.virginia.gov, for information on any other additions thatarenecessaryduetofederaltaxlegislationpassedaftertheprintingdeadlinefortheseinstructions.TheDepartment’swebsitewillalsoreflectanyactionbytheVirginiaGeneralAssembly to advance the date of conformity to the IRC that maytakeplacebeforetheduedateforyourreturn.Includeanyadjustmentsdescribedonthewebsite.Also,encloseascheduleandexplanationofsuchadditions.Line 3 EntertheamountonSchedule500AB,Line10,asthetaxableamountofpaymentstoarelatedentityinconnectionwith trademarks, patents and similar intangible property.EncloseSchedule500AB.SeeVa. Code § 58.1-402 B.8 and Va. Code § 58.1-402 B.9.Line 4 Net income taxes and other taxes, including franchise and excise taxes, which are based on, measured by, or computedwith reference to net income, imposedby this state or anyother taxing jurisdiction to theextentdeducted in determining federal taxable income (Va. Code § 58.1-402 B.4).Line 5 Interest, less related expenses to the extentnot deducted in determining federal taxable income, on obligationsofanystateotherthanVirginiaorofapoliticalsubdivision of any state other than Virginia unless it was createdbyacompactoragreementtowhichthisstateisaparty(Va. Code § 58.1-402 B.1).Line 6 Other Additions to Federal Taxable Income.OnLines6a-6c,enterthe2-digitcode,listedbelow,intheboxesfollowedbytheamountoftheaddition.Ifyouarefilingelectronically and have more than 3 additions, do not enter “00” in thefirstboxand theamountsinceall theadditioncodes and amounts can be entered. If Code 99 is claimed, provide a detailed explanation in the applicable spaceprovided,bythesoftwareprogram.If you are filing by paper and have more than 3 of theadditionslistedbelow,enter“00”andtheamountofthetotalotheradditionsinthefirstboxandencloseanexplanationof each other addition claimed, including the applicablecode. IfCode99 is claimed, enclose an explanation andsupportingdocumentation,ifapplicable.Code Description

01 Agas supplier, pipeline distribution company, orgas utility must add to federal taxable income any amount that was deducted in determining taxable incomeasanetoperatinglosscarryoverfromanytaxable year beginning on or before December 31, 2000 (Va. Code § 58.1-403 8).

02 A gas supplier, pipeline distribution company orgas utility must add to federal taxable income any amount that was actually deducted in determining taxableincomeasanetoperatinglosscarryoverornetcapitallosscarryoverwhichwouldhavebeenanallowabledeductionasanetoperatingornetcapital

Cancellation of Debt Income:UnderIRC§108(i),taxpayerswere permitted to defer the income realized upon thereacquisitionofcertainbusinessdebtduring2009and2010,and instead report such income inTaxableYears 2014through 2018. VirginiadeconformedfromthisfederalprovisionandrequiredtaxpayerstoclaimaVirginiaadditionequaltotheamountofthefederalexclusion.However,fortransactionscompletedonor beforeApril 21, 2010, taxpayerswere permitted topartiallydefersuchincomebyclaimingtheVirginiaadditionover 3 taxable years.AtaxpayerwhopreviouslyclaimedtheVirginiacancellationofdebtadditionmayclaimasubtractiononhisorherTaxableYear 2017Virginia income tax return, to the extent suchincomewasreportedonhisorher2017federalincometaxreturn.Atthetimetheseinstructionswerepublished,theonlyrequiredadjustmentsfor“fixeddateconformity”werethosementionedabove. However, if federal legislation is enacted that results in changestotheIRCforthe2017taxableyear,taxpayerswillberequiredtomakeadjustmentstotheirVirginiareturnsthatarenotdescribedintheinstructionbooklet.Informationaboutanysuchadjustmentswillbepostedon theDepartment’swebsite at www.tax.virginia.gov.Section A - Additions to Federal Taxable IncomeLine 1 Fixed Date Conformity Addition – Depreciation. Enter theamount thatshouldbeaddedtofederal taxableincome based upon the recomputation of allowabledepreciation.Ifdepreciationwasincludedinthecomputationof your FederalTaxable Incomeand one ormore of thedepreciableassetsreceivedthespecial30%or50%bonusdepreciationdeductionforfederalpurposesinanyyearfrom2001through2017,thendepreciationmustberecomputedforVirginiapurposesasifsuchassetsdidnotreceivethespecial 30% or 50% bonus depreciation deduction forfederalpurposesinanyyearfrom2001through2017.Ifthetotal 2017Virginia depreciation is less than2017 federaldepreciation,thenthedifferencemustberecognizedasanadditiononLine1.Forfurtherinstructions,seeVirginiaTaxBulletins 10-8, 11-1, 12-1, 13-3, 14-1, 15-1, 16-1, and 17-1 at www.tax.virginia.gov or call (804) 367-8037. Line 2 Fixed Date Conformity Addition – Other.DisposedAsset – If an asset was disposed of in 2017and suchasset received the special 30%or 50%bonusdepreciationdeductionforfederalpurposesinanyyearfrom2001 through 2017, and a gain or loss was recognized for federalpurposes,thenthegainorlossmustberecomputedas if suchasset did not receive the special 30%or 50%bonusdepreciationdeduction for federalpurposes inanyyear from2001 through2017.Theadjustmentwillbe thedifference in the federal and Virginia basis of the asset when sold. If the federal basis of the asset is greater than the Virginiabasis,(resultinginalowergainreportedforfederalpurposes), then the difference between the bases is anaddition on the Virginia return. For further instructions, see VirginiaTaxBulletins10-8,11-1,12-1,13-3,14-1,15-1,16-1,

Page 12

loss carryover in computing taxable income for ayear beginning afterDecember 31, 2000, exceptthatsuchlosshadbeencarriedbackforataxableyearbeginningpriortoJanuary1,2001(Va. Code § 58.1-403 9).

03 Unrelatedbusiness taxable incomeasdefinedbyIRC § 512, to the extent excluded from Form 500, Line1(Va. Code § 58.1-402 B.5).

05 Theamountrequiredtobeincludedin incomeforthe purpose of computing the partial tax on anaccumulation distribution under IRC § 667 (Va. Code § 58.1-402 B.7).

10 Interestordividends,lessrelatedexpensestotheextent not deducted in determining federal taxable income, on obligations or securities of any authority, commission or instrumentality of the United States, which the lawsof theUnitedStatesexempt fromfederal income tax, but not from state income taxes (Va. Code § 58.1-402 B.2).

13 Thedeductionforbaddebtsallowedincomputingfederal taxable income for a state or federal savings and loan association (Va. Code § 58.1-403 1).

14 Enter the amount of dividends deductible underIRC§ 561 and IRC§ 857 by aREIT (Va. Code § 58.1-402 B.10).

16 Income from Dealer Disposition of Property Enter the amount thatwould be reported underthe installmentmethod from certain dispositionsof property. If, in a prior year, the taxpayerwasallowed a subtraction for certain income from dealer dispositions of propertymade on or afterJanuary1,2009,intheyearsfollowingtheyearofdisposition, the taxpayer is required to add backtheamount thatwouldhavebeen reportedunderthe installmentmethod.Eachdispositionmustbetrackedseparatelyforpurposesofthisadjustment(Va. Code § 58.1-402 F).

18 Telework Expenses - Thisadditionisnotapplicablefor the 2017 taxable year. Corporations that claim the Virginia TeleworkExpensesTaxCredit are not allowed to excludethose expenses fromVirginia taxable income.Tothe extent excluded from federal taxable income, anyexpensesincurredbyataxpayerthatareusedtoclaimtheTeleworkExpensesTaxCreditmustbeadded to the Virginia return.

19 Food Crop Donation - To the extent a credit isallowedforgrowingfoodcropsintheCommonwealthanddonatingsuchcropstoanonprofitfoodbankanadditiontothetaxpayer’sfederaltaxableincomeisrequiredforanyamountclaimedbythetaxpayerasa federal income tax deduction for such donation.

99 Other-Entertheamountofanyotherincomenotincluded in federal taxable income, which is taxable inVirginia.Ifyouarefilingelectronically,provideadetailedexplanation in thespaceprovidedby the

softwareprogram.Ifyouarefilingbypaper,enclosean explanation and supporting documentation, ifapplicable.

Line 7 Total AdditionsEnterthetotalofLines1-5andallamountsforLine6(a)-(c)hereandonForm500,Line2.Section B - Subtractions from Federal Taxable IncomeEnter theamount bywhich anyof the following changesincreased your federal taxable income.Line 1 Fixed Date Conformity Subtraction – Depreciation. Enter the amount that should be subtracted from federaltaxableincomebasedupontherecomputationofallowabledepreciation.Ifdepreciationwasincludedinthecomputationof your federal taxable income and one or more of the depreciableassetsreceivedthespecial30%or50%bonusdepreciationdeductionforfederalpurposesinanyyearfrom2001through2017,thendepreciationmustberecomputedforVirginiapurposesasifsuchassetsdidnotreceivethespecial 30% or 50% bonus depreciation deduction forfederalpurposesinanyyearfrom2001through2017.Ifthetotal2017Virginiadepreciation ismorethan2017federaldepreciation,thenthedifferencemustberecognizedasasubtractiononLine1.Forfurtherinstructions,seeVirginiaTaxBulletins10-8,11-1,12-1,13-3,14-1,15-1,16-1,and17-1 at www.tax.virginia.gov or call (804) 367-8037. Line 2 Fixed Date Conformity Subtraction – Other.DisposedAsset - If an asset was disposed of in 2017and such asset received the special 30%or 50%bonusdepreciation deduction for federal purposes in any ofthe years 2001 through 2017, and a gain or loss was recognizedforfederalpurposes,thenthegainorlossmustberecomputedasifsuchassetdidnotreceivethespecial30% or 50% bonus depreciation deduction for federalpurposes in any of the years 2001 through 2017. TheadjustmentwillbethedifferenceinthefederalandVirginiabasis of the asset when sold. If the federal basis of the asset is lower than the Virginia basis (resulting in a greater gain forfederalpurposes),thenthedifferencebetweenthetwobases is included as a subtraction on the Virginia return. For further instructions, seeVirginiaTaxBulletins 10-8, 11-1,12-1,13-3,14-1,15-1,16-1,and17-1ontheDepartment’swebsite, www.tax.virginia.gov, or call (804) 367-8037. Otherchangesnotlisted–VisittheDepartment’swebsite,www.tax.virginia.gov for information on any other subtractionsduetofederaltaxlegislationpassedaftertheprintingdeadline for these instructions.TheDepartment’swebsitewill also reflect any action byVirginia’sGeneralAssembly to advance the date of conformity to the IRC that maytakeplacebeforetheduedateforyourreturn.Includeanyadjustmentsdescribedonthewebsite.Also,encloseascheduleandexplanationofsuchsubtractions.Line 3 Enter the amount of income (interest, dividends,and gain) derived from obligations or the sale or exchange of obligations of the United States and on obligations or securities of any authority, commission or instrumentality of the United States to the extent included in federal taxable

Page 13

income,butexemptfromstateincometaxesunderthelawsoftheUnitedStates.Thisincludes,butisnotlimitedto,stocks,bonds, treasury bills, and treasury notes. It does not include interest on refundsof federal taxes, equipment purchasecontracts, or normal business transactions. See Va. Code § 58.1-402 C.1.Line 4 Any amounts included under the provisions ofIRC § 78 (Va. Code § 58.1-402 C.5).Line 5 Theamountofanyrefundorcreditforoverpaymentof incometaxesimposedbythisstateoranyothertaxingjurisdiction(Va. Code § 58.1-402 C.4).Line 6 Anyamount included thereinby theoperationofIRC§951(subpartFincome).(Va. Code § 58.1-402 C.7.)Line 7 Any amount included in federal taxable income which isforeignsourceincomeanddefinedasfollows:

1. Interest other than interest derived from sources within the United States;

2. Dividends other than dividends derived from sources within the United States;

3. Rents, royalties, license, and technical fees from property located or services performedwithout theUnitedStates or fromany interest in suchproperty,including rents, royalties, or fees for the use of or the privilegeofusingwithouttheUnitedStatesanypatents,copyrights, secret processesand formulas, goodwill,trademarks, trade brands, franchises, and other likeproperties;and

4. Gains,profits,orotherincomefromthesaleofintangibleor real property locatedwithout theUnited States(Va. Code § 58.1-402 C.8).

Line 8 The amount of any dividends received fromcorporations in which the taxpaying corporation owns50%ormore of the voting stock, to the extent they areincluded in federal taxable income and to the extent not otherwise subtracted from federal taxable income (Va. Code § 58.1-402 C.10).Line 9 Other Subtractions from Federal Taxable Income. OnLines9a-9c,enterthe2-digitcode,listedbelow,intheboxes followed by the amount of the subtraction. If you are filingelectronicallyandhavemorethan3subtractions,donotenter“00”inthefirstboxwiththetotalamountsinceallofthe subtraction Codes and amounts can be entered. If Code 99isclaimed,provideanexplanationintheapplicablespaceprovided,bythesoftwareprogram.If you are filing by paper and havemore than 3 of thesubtractions listed below, enter “00” and the amount ofthetotalothersubtractionsinthefirstbox.Ifyouarefilingelectronically,provideadetailedexplanation in thespaceprovidedbythesoftwareprogram.Ifyouarefilingbypaper,enclosean explanationand supportingdocumentation, ifapplicable.Code Description

50 The amount of wages and salaries eligible forthe federalWorkOpportunityTaxCredit that are

not deducted for federal tax purposes (Va. Code § 58.1-402 C.6).

54 The amount contributed to the Virginia PublicSchool ConstructionGrants Program and Fundthat has not been claimed as a deduction on the corporation’s federal income tax return (Va. Code § 58.1-402 C.15).

55 There shall be subtracted from federal taxableincome, by a gas supplier, pipeline distributioncompanyor gasutility company, theamount thatcouldhavebeendeductedasanetoperatinglosscarryoverornet capital loss inarrivingat taxableincomeexceptthatsuchlossorportionthereofhadbeencarriedbackforfederalpurposes(Va. Code § 58.1-403 9).

56 Asubtractionforgassuppliers,pipelinedistributioncompanies, gas utility companies, and electricsuppliers,exceptcooperatives,fortheamortizationof the Virginia tax basis of assets that are recoverable forfinancialaccountingand/orincometaxpurposesplacedinservicepriortothefirstdayofthetaxableyearthatthecompanybecamesubjecttoVirginiacorporate income tax (adjustment date). “Virginiataxbasis”meanstheaggregateadjustedbookbasislesstheaggregateadjustedtaxbasisofsuchassetsas recordedon thecompany’sbooksofaccountsas of the last day of the taxable year immediately precedingtheadjustmentdate.TheamortizationoftheVirginiataxbasisshallbecomputedusingthestraight-linemethodover a periodof thirty years,beginning on the adjustment date.Gain or lossonthedispositionorretirementofanysuchassetshall be computed using its adjusted federal taxbasis, and the amortization of the Virginia tax basis shall continue thereafterwithout adjustment.SeeVa. Code § 58.1-440.1.

57 A subtraction for intangible expenses and costsadded to the federal taxable income of a related member as shown on the Schedule 500AB enclosed withtheVirginiareturnfiledbysuchrelatedmember(Va. Code § 58.1-402 C. 21).

58 For taxableyearsbeginningonandafterJanuary1, 2006, there shall be subtracted from federal taxable income contract payments to a producerof quota tobacco or a tobacco quota holder asprovided under theAmerican JobsCreationActof2004(P.L.108-357).Ifthepaymentisreceivedin installmentpayments, thentherecognizedgainmay be subtracted in the taxable year immediately followingtheyearinwhichtheinstallmentpaymentis received. If thepayment is received inasinglepayment,then10%oftherecognizedgainmaybesubtracted in the taxable year immediately following theyear inwhich thesinglepayment is received.The taxpayermay then deduct an equal amountin each of the 9 succeeding taxable years. See Va. Code § 58.1-402 D. For more information, visit www.tax.virginia.gov.

Page 14

59 Income from Dealer Disposition of Property – Anadjustmentisavailableforcertainincomefromdealer dispositions of propertymade on or afterJanuary 1, 2009. In the year of disposition theadjustmentwillbeasubtractionforgainattributabletoinstallmentpaymentstobemadeinfuturetaxableyears provided that (i) the gain arises from aninstallmentsaleforwhichfederallawdoesnotpermitthedealertoelectinstallmentreportingofincome,and (ii) the dealer elects installment treatment of the incomeforVirginiapurposesonorbefore theduedateprescribedbylawforfilingthetaxpayer’sincometaxreturn.Insubsequenttaxableyears,theadjustmentwillbeanadditionforgainattributabletoanypaymentsmadeduringthetaxableyearwithrespecttothedisposition.Eachdispositionmustbetrackedseparatelyforpurposesofthisadjustment.See Va. Code § 58.1-402 F.

60 Gains from Land Preservation Tax – Enter theamount of federal gain or income recognized as a resultofthesaleofLandPreservationTaxCredits.See Va. Code § 58.1-513 D.

61 Certain Long-Term Capital Gains – Provided the long-term capital gain or investment servicespartnership qualified income is attributable to aninvestment ina “qualifiedbusiness”asdefined inVa. Code § 58.1-339.4 or any other technology businessapprovedbytheSecretaryofTechnology,it may be allowed as a subtraction. For taxable years beginningonor after January 1, 2011, enter anyqualifiedincometaxedasalong-termcapitalgainforfederalincometaxpurposes,oranyincometaxedasinvestmentservicespartnershipinterestincome(otherwiseknownasinvestmentpartnershipcarriedinterest income) for federal income taxpurposes.Toqualifyforthissubtraction,theincomemustbeattributabletoaninvestmentina“qualifiedbusiness,”asdefinedinVa. Code § 58.1-339.4, or in any other technology business approved by theSecretaryofTechnology, provided that thebusinesshas itsprincipalofficeorfacilityintheCommonwealthandlessthan$3millioninannualrevenuesinthefiscalyearpriortotheinvestment.Theinvestmentmustbemadebetween thedatesofApril1,2010,andJune30,2020.Notaxpayerthathasclaimedataxcredit for an investment in a “qualified business”under Va. Code § 58.1-339.4 shall be eligible for the subtraction under this subdivision for an investment in the same business. See Va. Code § 58.1-402 C.24.

62 Historic Rehabilitation – To the extent includedin federal taxable income, any amount of gain or incomerecognizedbyataxpayerinconnectionwiththeHistoricRehabilitationTaxCreditisallowedasasubtraction on the Virginia return.

99 Other – Enter the amount of any other incomeincluded in federal taxable income, which is not taxable inVirginia. If you are filing electronically,provide a detailed explanation in the applicable

space provided by the software program. If youare filing by paper, enclose an explanation andsupportingdocumentation,ifapplicable.

Line 10 Total Subtractions.AddLines1-8and9a-9c.EnterhereandonForm500,Line4.Section C – Amended ReturnIfyouarefilinganamendedreturn,completeanewreturnusingthecorrectedfigures,asifitweretheoriginalreturn.Donotmakeanyadjustmentstotheamendedreturntoshowthatyoureceivedarefundorpaidabalancedueastheresultoftheoriginalreturn.BesuretofillintheAmendedReturnsection on Form 500, Page 1.IncaseswhereaForm500NOLDisfiledtocarrybackorcarryforwardanetoperatingloss,anamendedForm500shouldbefiledindicatingthechangeintheamountofcreditsclaimedandthecorrectedcarryoveramounts.EnclosearevisedSchedule500CRwiththeamendedreturnsfiledtoreportthechangestothecredit(s)claimedorcarryoveramountresultingfromtheNOLcarryback.TheFederal/Statee-Fileprogramonlysupportsamendedreturns for the current taxable year and the 2 precedingtaxableyears.Amendedreturnsforpriortaxableyearsmustbefiledbypaper.AmendedForms500ECwillalsoneedtobefiledbypaper.Section D – Schedule of VK-1 WithholdingIf you are claimingwithholding on Form 500, Line 15,completeSchedule500ADJ,Page2.

Tax Credits

EncloseSchedule500CRwithyourreturnwhenclaiminga credit(s). See the instructions below for additional requirements.Whenclaimingacredit(s) that requiresdocumentation, you will need to attach a PDF of such documentationwhenfilingelectronically.Ifyouarefilingbypaperandclaimingacredit(s)thatrequiresdocumentation,the information must be enclosed. Missing enclosures may causedelaysinprocessingthereturnandmaycauseacreditto be disallowed.The following rulesapplywhen claiming credits onSchedule 500CR.

• Nonrefundablecreditswithoutacarryoverprovisionareclaimedfirst.

• Carryover credits must be fully used before any 2017 credits (current year credits) are allowed.

• Tomaximizeallowablecredit,carryovercreditsmaybeclaimedintheirorderofexpiration,regardlessofthe order shown on Schedule 500CR.

Many of the credits discussed below may not be claimed on yourreturnuntilafteryouhavesubmittedanapplicationandhavebeennotifiedinwritingthatyouareallowedtoclaimthe credit. If your return is due and you have not yet been notified,youhavetheoptiontoeither:

Page 15

• Pay at least 90% of your tax liability by the return due dateandfileyourreturnonextensionafterreceivingsuchnotification,or

• File your return by the due date without claiming the credit, and file an amended return after you havereceivedsuchnotification.

Neighborhood Assistance Act Tax Credit TheVirginiaNeighborhoodAssistanceTaxAct providestax credits to businesses that donatemoney,marketablesecurities, property, limited professional services, andcontractingservicesdirectlytopre-approvedNeighborhoodAssistanceProgramorganizationswhoseprimaryfunctionistoprovideeducationalorotherqualifiedservicesforthebenefitoflowincomefamilies.Licensedveterinarians,physicians,dentists,nurses,nursepractitioners,physicianassistants,optometrists, dental hygienists, professional counselors,clinical social workers, clinical psychologists,marriageand family therapists, physical therapists, chiropractors,pharmacists, and physician specialists ormediatorswhodonatetheirservicesforanapprovedorganizationmaybeeligiblefortaxcredits.Inaddition,atrustorafiduciaryfora trust, may receive a tax credit for a donation made to an approvedorganization.TheamountofcreditattributabletoapartnershiporScorporationmustbeallocatedtothepartnersandshareholdersinproportiontotheirownershiporinterestinthepartnershiporScorporation.Anyunusedtaxcreditsmay be carried forward for the next 5 taxable years. For a list ofapprovedorganizationsoradditionalinformation,writeto:Virginia Department of Social Services, Neighborhood Assistance Program, 801 E. Main Street, Richmond, VA 23219-3301 or the Virginia Department of Education, 21st Floor, P.O. Box 2120, Richmond, VA 23218-2120, Division of Finance and Operations, ATTN: Neighborhood Assistance Tax Credit Program for Education.

Enterprise Zone Act CreditBusinesseslocatedwithinanEnterpriseZonethathaveinitiatedtheuseoftheEnterpriseZoneGeneralIncomeTaxCredit or have a signed agreement with the Commonwealth regardingtheuseofsuchcreditsinplacebyJuly1,2005,maybeeligiblebasedonjobcreationtotakeacreditagainstthetaxdueonzonetaxableincomeinanamountequalto80%ofthetaxdueforthefirstyearand60%ofthetaxdueforthesecondthroughthetenthyears.Excessgeneraltaxcredit, if any, may not be carried forward. Such credits are authorizedthroughfiscalyear2019.Inaddition,businesseslocatedwithinanEnterpriseZonethathave initiated theuseof theZoneInvestmentTaxCredit or have a signed agreement with the Commonwealth regardingtheuseofsuchcreditsinplacebyJuly1,2005,may be eligible for a credit against zone taxable income. Theinvestmentcreditcanbecarriedforwarduntilthefullamountisused.Suchcreditsareauthorizedthroughfiscalyear2019.Iftheannualtaxcreditrequestedexceedstheannualappropriation,theVirginiaDepartmentofHousingandCommunityDevelopment (DHCD)willissueaproportionateamounttoeachqualifiedbusinessfirmrequestingthecredits.

ToclaimtheEnterpriseZoneCredits,businessesqualifiedbyDHCDmust complete Enterprise ZoneCreditForm 301, and transfer thecomputedamount to theapplicableline(s) on Schedule 500CR. Enclose Form 301, andSchedule 500CRwith your return. For application formsandspecificinformation,writeto:Virginia Department of Housing and Community Development, Community Revitalization Office, Main Street Centre, 600 East Main Street, Suite 300, Richmond, VA 23219, call (804) 371-7030 or visit www.dhcd.virginia.gov.

Conservation Tillage Equipment CreditAcorporationpurchasingandusingconservationtillageequipmentforthepurposeofagriculturalproductionmaytakeataxcreditequaling25%ofconservationtillageequipmentexpenditures(butnottoexceed$4,000orthetotalamountoftaxowed,whicheverisless)intheyearofpurchase.Theterm“conservationtillageequipment”meansaplanter,drill,orotherequipmentusedtoreducesoilcompactionincludingguidancesystemstocontroltrafficpatternsthataredesignedtominimizedisturbanceofthesoilinplantingcrops,includingplanters,drillsorotherequipmentdesignedtoreducesoilcompactionwhichmaybeattachedtoequipmentalreadyownedbythetaxpayer.Iftheamountofsuchcreditexceedsthetaxpayer’sliabilityforthetaxableyear,theamountthatexceeds the tax liability may be carried over to the next 5taxableyears.ThecreditmustbeallocatedtoindividualpartnersandshareholdersinproportiontotheirownershiporinterestinthepartnershiporScorporation.Encloseastatementwithyourreturnshowingtheconservationtillageequipmentpurchasedate,adescriptionof theequipment,andthecreditcomputationwhenclaimingthiscredit.

Biodiesel and Green Diesel Fuels Tax CreditBeginningonJanuary1,2008,acreditisavailableforVirginiabiodieselandgreendieselfuelproducerswhoproduceupto2milliongallonsoffuelperyear.Thiscreditisonlyavailableduringthefirst3yearsofproduction.Taxpayersmayclaima nonrefundable credit against their tax liability for the productionofthesefuels.Toclaimthetaxcredit,encloseacopyofthecertificatefromtheDepartment.Form BFCisusedtoapplytotheDepartmentforaBiodieselFuels Credit after the Department of Mines, MineralsandEnergyhascertified thatyouhavesatisfiedallof therequirementsof Va. Code §58.1-439.12:02.Theamountofthecreditis$0.01pergallon,nottoexceed$5,000annually.Anycreditnotusedforthetaxableyearmaybecarriedovertothenext3taxableyears.Theamountofthecredit allowed cannot exceed the tax liability for the taxable year in which the credit is being claimed.The creditmay be transferred to another taxpayer.Thetransferofthecreditmustbecompletedbeforetheendofataxable year in order to use the credit for that taxable year. Formore information,write to:Virginia Department of Taxation, Tax Credit Unit, P.O. Box 715, Richmond, VA 23218-0715, or call (804) 786-2992.

Page 16

Precision Fertilizer and Pesticide Application Equipment Credit

AnycorporationengagedinagriculturalproductionformarketthathasinplaceanutrientmanagementplanapprovedbythelocalSoilandWaterConservationDistrictbytherequiredtaxreturnfilingdatemayclaimataxcreditequaling25%ofallexpendituresmadebysuchcorporationforthepurchaseofequipment.Theamountofthetaxcreditcannotexceed$3,750orthetotalamountofthetaximposedbythischapter,whicheverisless,intheyearofpurchase.Iftheamountofsuchcreditexceedsthetaxpayer’staxliabilityforsuchtaxable year, the amount which exceeds the tax liability may be carried over for credit against the income taxes of such individual in the next 5 taxable years until the total amount ofthetaxcredithasbeentaken.Theequipmentisdividedintothefollowingcategories:

1. Sprayersforpesticidesandliquidfertilizers;2. Pneumaticfertilizerapplicators;3. Monitors,computerregulators,andheightadjustable

boomsforsprayersandliquidfertilizerapplicators;4. Manureapplicators;5. Tramlineadapters;and6. Starterfertilizerbandingattachmentsforplanters.

The amount of any credit attributable to the purchaseof equipment certified by the Virginia Soil andWaterConservationBoard as providingmore precise pesticideandfertilizerapplicationbyapartnershiporelectingsmallbusinesscorporation (Scorporation)mustbeallocated totheindividualpartnersorshareholdersinproportiontotheirownershiporinterestinthepartnershiporScorporation.Encloseastatementwithyourreturnshowingpurchasedate,descriptionandcreditcomputationwhenclaimingthiscredit.

Recyclable Materials Processing Equipment Tax Credit