insight cee going forward - ing wholesale … · cee going forward long-term commitment ing guide...

TRANSCRIPT

INSIGHT CENTRAL & EASTERN EUROPE

BUSINESS AS USUAL

CEE GOING FORWARD

LONG-TERM COMMITMENT

ING GUIDE TO COMMERCIAL BANKING IN CEE

BUILDING DEEPER RELATIONSHIPS

9 5 717

8 Czech Republic 16 Romania 20 Russia 26 Slovakia 34 Bulgaria

CONTENTS

Introducing CEE

Long-term commitment to the regionThe fact that we have been in Central & Eastern Europe for virtually 25 years gives us a lot of knowledge of the region. Our history is one of our strengths.

Business as usual

Sector view The economic uncertainty of recent years has highlighted CEE’s strengths in many of the world’s most important sectors.

4 Foreword by Alexander Pisaruk, Regional Head Commercial Banking CEE 10 Bracing for the climb: macro-economic outlook on Central & Eastern Europe 70 ING Commercial Banking in Central & Eastern Europe

6 Long-term commitment to the region

40 Kazakhstan 44 Hungary 56 Poland 62 Ukraine 68 Turkey

36 Combining CEE knowledge and structured finance strength 38 Developments in metals and mining 42 Finding directions in CEE – infrastructure developments 46 Connecting CEE to the rest of the world – telecom, media and technology 48 Syndicated lending and financing projects 50 Time to harvest – agricultural finance 58 Source of opportunities – energy and utilities

INSIGHT CEE - edition 2014 ING Commercial Banking, Central & Eastern Europe

Developments in financing18 Building a deeper relationship 22 Evolution in CEE lending market 28 Increasing focus on cash management in CEE 64 FX hedging to the fore 66 Commodity derivatives 67 Securities finance

Cover world map ING Commercial Banking

Thanks to: Laurence Neville, Anna Lvova, Pieternel Boogaard, Julia Chekrygina, Tibor Bodor, Stefan Verhoeven, Andre Rijs, Michiel de Haan, Michael Dinham, Pieter Puijpe, Ali Miraj, Alexander Alting von Geusau, Rodolphe Olard, Arek Szperna, Jens Vrolijk, Jason Cade, Richard Pryce.

For more information please contact Vincent Verhoeff manager marketing & communications ING Commercial Banking Central & Eastern Europe at [email protected].

Client cases32 Grupa Żywiec 54 Kernel 72 Client cases - overview

contents

Welcome to Insight CEE, ING’s guide to Central & Eastern Europe (CEE) We hope this guide will help you understand the trends that will shape CEE in the coming years. In here we assess the economic outlook, highlighting both the risks and opportunities across the region. We also look at some of the most important markets, such as infrastructure finance, project finance, syndicated lending and derivatives, as well as sectors including, telecom, media and technology, metals and mining, energy, infrastructure and agriculture.

CEE weathered the financial crisis well and is now enjoying a solid, albeit slow, recovery. As economic growth gathers pace in the European Union – by far CEE’s largest trading partner – companies in the region will benefit. Meanwhile, the economic fundamentals of most CEE countries are broadly positive. While many emerging markets have been destabilised by capital inflows spurred by the Federal Reserve’s quantitative easing, inflows to CEE have been modest. Consequently, outflows driven by impending tapering should also be modest.

ING serves companies across all sectors with a range of products and services that are carefully tailored to each client and market. ING was one of the first banks to arrive in CEE in 1991 and unlike many interna-tional banks ING has demonstrated a consistent commitment, also during years of crisis and uncertainty such as 2008 and 2009. ING has continued to invest and reap the rewards as CEE has bounced back quicker than Western Europe. Clients appreciate ING’s commitment to the region and its approach to service.

In view of the nature of CEE, lending, cash management and FX are central to ING’s relationship with companies in the region. ING has a comprehensive track record of meeting its clients’ needs in these areas and leveraging its operations across the region to make it easier for clients to gain assistance wherever they need it. The bank’s longstanding presence in the region makes integration and control straightfor-ward and secure. In transaction services, including payments and cash management (PCM), ING has a world-class offering in the most important markets in CEE. We act as both a local and an international bank, combining the benefits of flexibility and standardisation of documentation and customer support internationally. Similarly, in FX we combine global emerging markets FX desks in Amsterdam, Brussels and London with our local knowledge, execution and research across CEE.

In order to ensure that its capital is targeted at the most appropriate clients, ING focuses on client relationships that are complementary for both parties. ING continues to have the capacity and a willing-ness to lend and provide cash management and FX services. In return we expect clients to recognise ING’s expertise – both within CEE and internationally – across a wide variety of products, including capital markets and M&A advisory.

ING does not expect a client to select anything other than the best provider. That said, clients can be confident in the knowledge that working with ING means gaining access to world-class products and services. Our in-depth knowledge of local market conditions enables us to take a proactive approach to the challenges our clients face whether they are related to financial markets services such as foreign exchange, commodity and interest rate hedging, or project and infrastructure financing. We expect to be on a client’s shortlist in the many areas where ING offers competitive solutions.

CEE is at the heart of ING’s vision for the future. We understand that our success in the region depends on meeting our clients’ expectations. As CEE’s economic recovery strengthens in the coming months we are ready to help our clients take advantage of emerging opportunities and achieve their strategic goals. We hope this guide provides useful insights and prompts thoughts and ideas about the opportunities in CEE. We would be delighted to hear from you if you would like to learn more.

Alexander PisarukRegional Head ING Commercial Banking Central & Eastern Europe

5introduction

First account for Russian client at Barings Established in London in 1762, Barings (part of ING) rapidly emerged as the world’s leading merchant bank. The firm undertook prestigious transactions worldwide and the first account of a Russian client was opened in 1775. From the eighteenth century Barings also financed Russian trade. As merchants, the firm traded in a wide variety of Russian goods through the ports of St Petersburg and Rostov. Timber was of special importance but hemp, tallow, flax, hides, linseed and grain also figured.

LONG-TERM COMMITMENT TO THE REGION“Our history is one of our strengths. The fact that we have been in Central & Eastern Europe for virtually 25 years gives us a wealth of knowledge of the region. The fact that we have been building this presence carefully, and mostly organically, means we know what we are doing in the region. This has helped us to stay here throughout the business cycles — even during the recent turmoil we remained committed because we have always known what we are doing and where we are going.” - Alexander Pisaruk

Bank Śląski and ING start cooperation Bank Śląski was established in 1988 as a result of a spin-off from the National Bank of Poland. In 1991 it was transformed from a state bank into a limited company and in 1994 it debuted on the Warsaw Stock Exchange. ING Group has been the bank’s majority shareholder since 1996.

In 2001 Bank Śląski merged with the Warsaw branch of ING Bank N.V. and the bank has been operating since under the name ING Bank Śląski.

ING opens offices in Romania, Bulgaria & Ukraine

20xx

ING sets foot in Turkey

Poland and Ukraine successfully host EURO 2012

Virtually 25 years of continuous presence in CEE Today ING is highly regarded for its expertise in emerging markets in Central & Eastern Europe. With offices in Russia, Bulgaria, Czech Republic, Hungary, Kazakhstan, Poland, Romania, Slovakia, Turkey and Ukraine, the bank offers a wide range of financial services mainly focused on cash manage-ment, financial markets, lending and structured finance.

6

1775

1991

1992

End of the eighties - new opportunities The 1990s marked the start of a new era with the fall of the Berlin Wall. Not only for the countries in Eastern Europe, but also in the banking business. ING continued as a single entity in 1990 when the legal restrictions on mergers between insurers and banks were lifted in the Netherlands. This prompted insurance company Nationale-Nederlanden and banking company NMB Postbank Groep to enter into negotiations and eventually merge into Internationale Nederlanden Groep (ING) in 1991.

ING expands into CEE Leveraging on the new opportunities, ING developed into a strong multinational bank through a combination of organic growth and various acquisitions. ING opened its own office in Hungary in 1991, followed by branches in Czech Republic and Slovakia in 1992.

1993 ING opens Russian offices in Moscow & St Petersburg

1994

1997

Kazakhstan office opened

1997

2014

history 7

1989

2009

2012

Global services and operations hub opened in Bratislava to serve clients more efficiently

Business as usualPRAGUE, CZECH REPUBLIC 10.15 AM

CZECH REPUBLIC

GDP change %

Private consumption% change

Investment % change

CA balance in % GDP

Fiscal balance in %

CPI average % YoY

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

czech republic

Source: ING

estimated average growth 2014/ 2015

9

More information on ING CB in Czech Republic visitingcb.com/czechrepublic or view the introduction video [click here]

BRACING FOR THE CLIMB macro-economics

by Rob Rühl, Head of Business Economics ING Economics Department Global Markets Research and Mohammed Nassiri, Researcher ING Eco-nomics Department Global Markets Research

CEE economies are well-positioned compared to their 2008/2009 battering to show positive economic growth rates in coming years. Years of poor growth are starting to make way for improved external balances and financial stability. However, increas-ing political and policy risks in the region cannot be ignored as numerous elections are approaching. Moreover, while most CEE countries are recovering, they remain some way from the heights achieved in the pre-2008 period.

Recent performance Compared with other regions CEE enjoyed moderate economic growth rates during 2013 with central banks across the region trying to support growth by lowering offi-cial interest rates or, in countries with rela-tively high inflation, implementing liquidity support measures. Positives for the region included a clear recovery in other parts of the world, low foreign interest rates, ample global liquidity and stable commodity prices. However, the ongoing recession in the EU had a major impact on trade and financial flows in CEE. Output weakness in 2012/2013 can nevertheless be attributed to a lack of domestic demand rather than disappointing export performance.

Fixed investment slowly recovered in 2013. This reflects lower capital inflows as well as policy restraints. Other headwinds for the region include deleveraging pressures on banks and regulatory changes which are increasing the cost of capital allocated to CEE. In the aftermath of the financial crisis there was a surge in non-performing loans as growth slowed, unemployment rose and the housing boom ended. Bank lending fell as a consequence while households facing an uncertain future in terms of income cut spending and boosted savings.

Most governments in the region have succeeded in keeping government deficits below the magic 3% of GDP level (the so-called Maastricht criteria for the eurozone). Exceptions include Poland, the Slovak Republic and Romania. Similarly, govern-ment debt was kept below 60% of GDP everywhere except Hungary and, outside the EU, Russia. While oil and gas revenues supported government finances and its

international reserves position, the country nevertheless faces significant challenges. Insufficient investment, lagging structural reform and an adverse investment climate are constraints to potential growth.

One advantage of the slow growth in domestic demand across CEE is downward pressure on inflation and improved current account deficits in many countries. The latter reduces the reliance of CEE countries on foreign savings. However, Turkey and Ukraine still depend on large foreign capital inflows. As a consequence both countries’ currencies depreciated heavily against the dollar and the euro following the 22 May announcement by the US Fed-eral Reserve Bank that its loose monetary policy would be curtailed in future (a so-called tapering process starting in January 2014).

Prospects for 2014-2015With growth in the eurozone picking up, the outlook for CEE countries will improve in 2014-2015. The EU5 (Bulgaria, Czech Republic, Hungary, Poland and Romania) will benefit the most with Turkey profiting to a lesser extent. ING’s base forecast for most of the region is for a slow growth recovery. The large build-up of slack in recent years will act as a stabilising factor for short-term interest rates as it will delay any build-up of inflation.

Consumers across the region will gain confidence and start spending money on consumer durables. Similarly, companies should resume investments, especially those associated with replacing existing production facilities to improve produc-tivity and save energy. As a result imports

are likely to pick up, reversing the trend towards lower current account deficits.Governments are expected to support the revival of private domestic demand as the key adjustments required to ensure eco-nomic stability have already been made. Bulgaria, Romania and Hungary may have room for fiscal relaxation to stimulate domestic demand while pension reforms in Poland have made room for extra government spending ahead of the 2015 parliamentary elections.

The EU5 countries will benefit from the disbursement of funds under the EU 2014-2021 budget, as well as from a boost in infrastructure investments. Poland appears best-positioned to absorb these EU funds as the absorption capacity in the other four countries is still limited.

The downside risks to growth are most prominent in Hungary. Taxes on banks and schemes to convert foreign exchange-de-nominated mortgages into Hungarian forint will constrain bank lending. Mean-while Turkey will have to adapt to years of lower foreign capital inflows. As a conse-quence the country faces difficult decisions if it is to reduce its current account deficit. One option would be a depreciation of the currency to stimulate exports and reduce imports. However, that would jeopardise the policy goal of the Turkish central bank to keep inflation under control. The most likely outcome would appear to be for the central bank to raise interest rates in order to reduce domestic demand.

Unlocking potential growth in Russia will require investments in infrastructure and improvements in the ease of doing

11macro-economics

business. Neither objective looks likely to be achieved in the short run. The govern-ment is expected to stick to fiscal tight-ening in line with the 2014-2016 budget framework. So while Russia will remain financially stable – thanks to its oil and gas reserves – the outlook for economic growth will be constrained. Neighbour-ing Ukraine faces a period of important adjustments to reduce its fiscal and current account deficits: the country could suffer a severe loss of income and output and from a depreciation of the hryvnia. Support from Russia will mitigate the negative impact of developments in Ukraine. All in all the CEE & CIS region will profit (GDP growth 3.5%) from a moderate economic recovery in the European economies (1.3%) and domestic policy adjustments in 2014/2015. Increas-ing political pressure due to upcoming elections may have a negative impact.

CEE and Western Europe growing closer The CEE economic block is becoming a more open region with an increasingly important role as a global trading partner. CEE exports grew at a compound annual growth rate (CAGR) of 15% between 2002 and 2012 (figure 2). The merchandise trade ratio increased from 63% to 84% of GDP, showing that trade is becoming more important for the region’s economy. At the same time the region’s share of global trade increased by 1.2 percentage points to 5.0% of global exports. This is partly the result of a high growth rate of trade with the own region (so-called intra-regional trade). The euro area is still, however, the most important trade partner for the CEE countries, while emerging countries

outside the own region only play a minor role (figure 1).

The top three exporting countries in the CEE region in descending order are Poland, the Czech Republic and Turkey. The same countries are the main importers and are together responsible for 57% of the region’s foreign trade. Intra-regional trade increased between 2002 and 2012 from 16% to 22% of total exports, reflecting the growing interdependence between countries within the region. Poland (17%), Czech Republic (17%), Slovakia (15%) and Hungary (14%) are together respon-sible for 63% of this intra-regional trade. Growth in intra-regional trade is one of the quick wins for the region’s trade develop-ment and is mainly due to an increasing importance in the European supply chain.

This will continue in 2014/2015. Not only by trade ties between CEE and WEU ties became stronger. Foreign direct investment and bank lending from Western Europe-an banks helped to finance the transfer of production capacity to CEE countries, enabling CEE to link its industrial sectors to the successful European supply chains in the technological industries.

Trade within CEE and with CIS and the Middle East & North Africa (MENA) is gradually increasing. However, CEE exports continue to depend heavily on Western European markets, which accounted for 53% of exports in 2012 (the EU accounts for 43% of the total). Consequently, the outlook for CEE is closely linked to recovery in the EU. The nascent recovery in many eurozone countries therefore bodes well

for CEE in 2014/2015. 12% of CEE goods go to emerging countries in other regions such as Asia, Latin America (LATAM) and MENA. Excluding trade with the MENA region – which is dominated by Turkey with almost 75% of the total CEE trade – this share is even smaller (5%). Despite this low share CEE is well-positioned through its ties to the supply chains of countries like Germany to benefit indirectly from high growth rates in emerging countries. Nevertheless, exporting more to emerging countries directly could help CEE become more diversified and less susceptible to a possible economic slowdown in Europe.

Cars and machines in exchange for mineral fuelsMuch of CEE’s dependence on the EU as an export market stems from devel-opments in the 1990s when there was a considerable transfer of production capac-ity by original equipment manufacturers from Western Europe. From the mid-90s onwards CEE became a major exporter of machinery and transport equipment. The continued high share of intermediary prod-ucts in total exports shows the importance of the region’s role as a supplier for both the euro area and the region itself. The CAGR of machinery and transport equip-ment exports between 1995 and 2012 was

17%, making it by far the most important export sector. By 2012 machinery and transport equipment represented 39% of exports (with 61% of these exports shipped to Western Europe). Machinery and transport equipment is gen-erally characterised by its high added value, underlining the increasingly sophisticated export profile of CEE (figure 3). In Germany in particular (which accounts for 20% of CEE exports) CEE products are important input for the production of cars and ma-chines. Almost 50% of all foreign interme-diate products for motor vehicles and 30% of the machinery used by German sectors is produced in the CEE region. This makes

Source: UNCTAD, ING calculations

> 30 bn. USD 20 - 30 bn. USD 10 - 20 bn. USD 0 - 10 bn. USD

Figure 1 - CEE export growth by country 2002-2012

67%

21%3%9%

USD 213 bnRest of the world

MENA

Emerging Europe

Western Europe

RU 5%

CZ 3%

PL 3%

53%

30%

USD 873 bn

GE 20%

IT 6%

UK 5%

FR 5%

7%

9%

+15%

Major countries within the region% share total exports 2012

59%

23%

7%12%

USD 277 bnRest of the world

MENA

Emerging Europe

Western Europe

RU 11%

CZ 3%

PL 3%

46%

31%

USD 975 bn

GE 18%

IT 6%

NL 4%

FR 4%

11%

12%

+13%

Major countries within the region% share total imports 2012

CH 7%

2002 20122002 2012

Figure 2 - Development of exports and imports in Central & Eastern Europe by region 2002-2012, value USD billion

Source: UNCTAD, ING calculationsNote: Emerging Europe consists of CEE + CIS

13macro-economics

CEE well-positioned to benefit from the positive outlook for German sectors such as the transport and machinery sectors in coming years.

Despite the export success of CEE the trade deficit almost doubled in the last decade from USD 64 billion to USD 102 billion. The main contributors to the region’s trade deficit (60%) are Turkey and Romania (oil bill). Czech Republic, Slovakia and Hungary were able to turn their deficit into a surplus mainly by exporting more road vehicles, electrical machinery and telecommunica-tion appliances. More exports of cars and machines in exchange for mineral fuels will be the name of the game in CEE in the coming years. The expansion of the pro-duction capacity of high-tech goods and the continued strong market position in intermediary products will help to achieve this goal.

CEE technological sector continues to growThe CAGR of the production of invest-ment goods and consumer durables was between 8.6% and 8.8% from 1998 until 2012 – double the regional GDP growth rate. Globally CEE accounted for 7.6%

of worldwide durable consumer goods production and 4.8% of the production of investment goods in 2013. As shown in figure 4 we expect industries included in the production of technological goods (indicated by blue bulbs) to show the high-est growth rates in 2013-2018. Foreign direct investment made before the start of the global crisis and adjustments to in-vestment plans resulted in idle production capacity later. This capacity will be used in the coming years to increase production for domestic sales and exports. Europe-an producers will continue to allocate production to the CEE region. Some critical production processes for the European market can be transferred from Asia to countries in the CEE region. With sales prospects for Asian companies improving in Europe, more Asian companies are expected to step up foreign investments in CEE. Cost advantages of producing in CEE, direct access to the EU market and lower transport costs are the main drivers for Asian companies to establish themselves in the region. Foreign direct investment by companies in the automotive, comput-er and office equipment, and domestic appliances sectors have driven production growth: 65% of automotive production in the region was started by Western

European companies. The best-known examples of international firms that have established a significant presence in CEE are Volkswagen in Czech Republic and Renault in Romania. Asian companies have also established production facilities in the region, such as Kia in Slovakia and Toyota and Honda in Turkey.

Russia, Poland, Turkey and Czech Republic are the most important producers of tech-nological products. Although technological production attracts most of the attention, the production of intermediate products and food is still an important cornerstone for the CEE economies. Growth in the production of chemicals, wood products, coke and refined petro-leum products and basic metals will keep pace with GDP growth. Turkey will be the main source of growth in these sectors as investment activity in Turkey is highly focused on these sectors. Food, beverag-es and tobacco will continue to play an important role (7% of global production) with Turkey, Russia and Poland being the main food-producing countries in the re-gion. Turkey’s leading role is supported by its high agricultural share (3.5%) of global production.

Russia: global producer for domestic marketRussia’s economic performance is main-ly linked to the oil and gas industry. A lesser-known fact is that the country is by far the largest producer of investment goods with a global market share of 5.1% for the production of computers, for example. The country is also the largest producer of cars and other vehicles, with a global market share of 2.1%. The focus of Russian production is mainly on the domestic market and the markets of the countries of the Customs Union (Russia, Belarus and Kazakhstan). At the same time the Russian market is known as one of the most protected markets. Russia’s focus on the creation of a customs union and the protection of its own markets limits the Russian technological sector’s ability to play a more important role in global trade, thus preventing Russian industry from unlocking its potential.

105

343

343

167

Machinery and transport equipment

Manufactured goods

Miscellaneous manufactured articles

67 Chemicals and related products

65 Food and live animals

54 Mineral fuels

31

4

Crude materials, inedible

Other products29

9Beverages and tobacco

Animal and vegetable oils, fats, waxes

PRODUCT GROUP SHARE (%)1995

SHARE (%)2012

CAGR (%)1995 - 2012*

1 0.4 11

2 1 9

1 3 22

5 4 10

5 6 14

10 7 11

9 8 11

20 12 9

27 19 10

20 39 17

Figure 3 - Exports Central & Eastern Europe by product group, 2012

Source: UNCTAD, ING calculations

Figure 4 - Development sectors by output growth and share in global production (CEE and CIS)1

Food, beverages and tobacco

267 USD bn

Paper and printing

267 USD bn 67

% of global production 2012

FIGURE 5 Development sectors by output growths and share in global production (CEE and CIS)1

7.5%

7.0%

6.5%

6.0%

5.5%

5.0%

4.5%

4.0%

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0%

0 2 4 6 8 10 12

Transport equipment266 USD bn

High-tech goods141 USD bn

Chemicals and pharmaceuticals

168 USD bn

Mechanical engineering

92 USD bn

Basic metals

155 USD bn

Utilities177 USD bn

Extraction184 USD bn

Leather goods8 USD bn

Garments23 USD bn

Textiles44 USD bn

Agriculture, forestry and fisheriy

257 USD bn

Othermanufacturing38 USD bn

Furniture manufacturing27 USD bn

Metal products

87 USD bn

Electric machinery and apparatus

108 USD bn

Non-metallic minerals

83 USD bn

Rubber and plastics

110 USD bnWood and wood products34 USD bn

% a

vera

ge

gro

wth

201

3 -

2018

average growth all sectors

Source: Oxford Economics, ING calculations1. Total region consists of Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Russia, Slovak Republic, Slovenia, Turkey, Ukraine

* CAGR ‘95 - ‘12 of all products = 12%

macro-economics 15

Business as usualDANUBE, ROMANIA 3.58 PM

14

ROMANIA

GDP change %

Private consumption% change

Investment % change

CA balance in % GDP

Fiscal balance in %

CPI average % YoY

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

romania

Source: ING

estimated average growth 2014/ 2015

17

More information on ING CB in Romania visitingcb.com/romania

CFOs and treasurers in Central & Eastern Europe face challenging conditions for the foreseeable future, not unlike their peers elsewhere in the world. By working with their banks to improve liquidity management and de-risk their balance sheets, companies in emerging Europe are ensuring that they are well positioned for every eventuality - by Tibor Bodor, Head of Client Coverage CEE

The global economy and financial markets have created headwinds for corporate growth in emerging Europe. Many of the region’s exports go to the troubled eurozone, while regulatory reform and upheaval in the banking sector threaten to reduce companies’ access to capital. In response CFOs and treasurers in the region are focusing on two key priorities, according to research by ING.

The first is to improve liquidity manage-ment and working capital. The second is to identify opportunities for improved efficiency and to reduce risks, both operationally and on corporate balance sheets. In terms of liquidity management, many firms initially focused on rationalis-ing their inventory before seeking to extend payment terms with suppliers. There has also been a drive to improve receivables management. Recently there has been an increase in interest for more sophisticated working capital and trade finance solutions, including supply chain finance and factoring. Solutions such as these have been popular in other emerg-ing markets, most notably in Asia, for many years. However, their adoption in emerging Europe has been delayed for a number of reasons. The fragmented regional banking market serves as one explanation. State-owned banks have continued to make their balance sheets available, regardless of market conditions.

Similarly, a number of banks competing in the region are not subject to Basel requirements, enabling them to make funds available at a lower cost than banks headquartered in Western Europe, for example. Secondly, many corporates have, until recently, been unfamiliar with more sophisticated financing solutions. For example, it takes time to understand why the internal reorganisation required for factoring is worthwhile. A high degree of customisation is necessary to accom-modate local legal structures and requirements, even for banks that offer supply chain finance or factoring in markets outside of emerging Europe. Not all banks have been willing to make these investments.

De-risking corporatesChief financial officers’ second most important priority is de-risking their balance sheets. Treasurers and CFOs alike are scrutinising the banks they work with. Over the past year some international banks have exited the region while others have scaled down lending and retrenched capital. Since many companies in the region have sound balance sheets, few financial executives have found them-selves facing an immediate problem. However, there are genuine concerns about which banks will continue to provide funding and services in the coming years. Fast-growing companies in

BUILDING A DEEPER RELATIONSHIP

particular are worried about continued access to capital. The topic of bank lending is especially pertinent because the majority of corporates in the region are reliant on bank debt. Moreover, most large enterprises receive the largest portion of their funding from international banks, making them vulnerable to further retrenchment. Such companies are now considering alternative funding sources.

The syndicated loan market has largely dried up and international capital markets are currently accessible only to the largest firms in the region. However, some anticipate that international investors will view sovereign and corporate debt in CEE as an opportunity to seek the higher yields available there. While banks may have little appetite for 10-year lending, pension funds and other investors have long-term liabilities that must be matched.

Furthermore, pressure to generate yields is likely to spur a revision of investment policies. This change is being driven by the realisation that many countries in the region that are rated below investment grade might offer greater risk-adjusted returns than, for example, investment grade Spain. CEE’s weighted average debt-to-GDP ratio is 47% compared to 83% for Western Europe.

As a result, a number of emerging European corporates are now preparing IFRS accounts in order to access private placement and money market fund investors for the first time. ING has used its Eurobond platform to enable borrow-ers from Turkey, Poland and elsewhere to bring new issuances to the market. A recent beneficiary is Czech railway operator Ceské Dráhy, which raised EUR 300 million at 4.125% in July 2012. De-risking balance sheets also means identifying opportunities to unlock cash. For example, corporates are increasingly considering sale and leaseback arrange-ments to unlock real estate assets.ČSimilarly, there is increasing interest in identifying risks that were previously ignored, such as pension liabilities, and hedging volatile commodities like grain, oil and diesel. In order to respond to the needs of financial executives, some banks that are active in emerging Europe are changing how they serve the region. ING has adopted a new client-focused approach that complements its strategy in the rest of Europe. For banks willing to commit to a long-term future in emerging Europe, there is a need for more than just lending. They must adopt a relation-ship-focused approach that showcases

their capabilities, knowledge and people in order to win more business. Historically, banks in the region have taken a product-oriented approach that has failed to deliver cohesive solutions and has resulted in treasurers and CFOs spending disproportionate amounts of time on managing meetings with banks.

An alternative approach tasks bank product teams from a variety of areas with explaining the advantages and disadvan-tages of various options to finance chiefs in an unbiased way. This approach to relationships can prompt banks to focus on clients that are the best fit for their capabilities. Both banks and corporates stand to gain if banks re-evaluate how they serve clients in emerging Europe. For banks, understanding clients’ needs and business models helps them win addition-al business and create a more sustainable business model. For corporates, an increased understanding of their business means they receive better service while no longer having to meet with multiple product specialists. Perhaps most importantly, such an approach can enable the region’s companies to access the sophisticated solutions they require as they expand both regionally and internationally.

19

It’s about having a deeper understanding of what really drives our clients

clients

Business as usualMOSCOW, RUSSIA 6.21 PM

18

RUSSIA

GDP change %

Private consumption % change

Investment % change

CA balance in % GDP

Fiscal balance in %

CPI average % YoY

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

russia

Source: ING

estimated average growth 2014/ 2015

21

More information on ING CB in Russia visitingcb.com/russia

EVOLUTION IN CEE LENDING MARKET corporate lending

The corporate lending market in Central & Eastern Europe is experi-encing a cautious recovery. Stefan Verhoeven, head of Corporate and FI Lending for Central & Eastern Europe at ING Commercial Banking, explains how the market is chang-ing and why relationship lending is set to become more important for corporates.

As the storm clouds over Central & Eastern Europe (CEE) begin to recede, the region is enjoying an increase in confidence in both the corporate world and the bank lending market. However, with recovery in the European Union – CEE’s largest export market – still under-whelming, the borrowing appetite of corporates remains relatively low compared to the period before the start of the financial crisis.

lending services 23

This low level of activity also reflects changes in the behaviour of corporates. Companies in CEE have become resilient by necessity: having been through multiple crises in the past they are adaptable and have learned to handle external shocks well. Companies that had high capital ex-penditure and high leverage and that relied on short-term financing before the crisis have now changed their ways.

Many corporates subsequently de-lever-aged while others successfully refinanced in 2010 and early 2011, when a number of banks were trying to boost their market share by offering lending at attractive rates. In addition, the experience of cor-porates during the crisis in 2008 and 2009 encouraged them to become more pru-dent and depend more on internal sources of funding, reducing demand for lending.At the same time some borrowers, par-ticularly higher quality names (many of which are from Russia), have turned to the bond market as an alternative source of funds, reducing their dependence on bank lending.

It should, however, be noted that CEE – which implies the CEE lending market – is far from homogenous. Each national market has different dynamics with Turkey and Russia experiencing the strongest loan growth in the region on the back of rising GDP. At the same time, the dynamics of each market vary. Corporate lending in Russia and Ukraine tends to be dol-lar-based, for example. Most other markets in the region are focused on local currency lending although there is also appetite for euro-denominated loans, both in eurozone and non-eurozone countries.

Changes to lendingAs the patterns of demand for borrowing change, so too is the supply of funding. CEE lending remains dominated by banks with foreign owners and the nature of many banks is changing. Pressure by regulators to retain capital in-country, for example, is prompting international banks to become more local in their approach.

Similarly, while historically there has been a relatively low level of deposits to fund as-sets in the majority of CEE countries – with Czech Republic the most notable exception – dependence on cross-border funding of loan assets is now being reduced. This reduction is partly the result of regulatory restrictions on the movement of liquidity between markets and an increased reg-ulatory focus on the deployment of local deposits. However, in many countries (such as Poland) local deposits have grown signif-icantly as consumer savings have increased in the wake of the crisis and banks are simply putting these local currency deposits to work in the local market.

Given relatively weak demand – and mul-tiple alternative sources of supply – com-petition among banks to lend is strong. Despite concerns of a knock-on effect from the crisis, most banks remained in CEE. Moreover some bank have expanded their presence in corporate lending, most nota-bly Russian state-owned banks: last year one leading Russian bank bought the CEE operations of a Western European bank. Russian banks are generally increasingly lending, not only in Russia and Ukraine but also elsewhere in Central Europe.

lending services

borrower wants to borrow only in dollars, a bank may offer a club loan with euro and dollar tranches with different lenders par-ticipating in each of those tranches. That means that the freedom to borrow in any currency of choice with no impact in terms of cost is a thing of the past.

Banks are generally becoming more careful about the options they offer borrowers, also in their approach to liquidity back-up lines. This is largely prompted by the impending introduction of Basel III, which will raise capital requirements for banks and introduce a leverage ratio and stricter liquidity and funding requirements. There is also less emphasis on asset-based lend-ing and more focus on cash flow-based lending.

At the same time borrowers are also becoming more sophisticated in how they access funding. In the past, many companies simply looked at borrowing on a country-by-country basis. However, companies in CEE are increasingly expand-ing cross-border and are seeking to take a broader view of their overall borrowing requirements. Banks that operate across CEE can play a helpful role as companies adopt such strategies.

Relationships to the foreAs some new players have entered the CEE loan market, the changing characteristics of the market have elevated the impor-tance of relationship lending. For banks, lending to longstanding clients makes sense: the bank understands the client’s business and credit profile and has the ability to cross-sell, which is increasingly important for allocating scarcer capital and returns on such capital. Relationship

lending is also attractive for borrowers. It makes banks more willing to lend at times of uncertainty or credit scarcity. As a result, it provides greater predictability and stability in terms of certainty of funds. The period of post-crisis uncertainty – for both banks and corporates – has meant that many recent syndicated corporate deals have involved predominantly bank clubs composed of relationship banks.

ING is committed to CEE: it has extensive operations, a willingness and capacity to lend along with a strong track record and history of capital investment in the region. The bank is strengthening its core client relationships and seizing opportunities in the market. ING expects lending to be mu-tually beneficial: in return for dependable lending, it wants to be part of a long-term cooperation that includes non-lending business.

When ING commits to lend to a client, over time it expects to become a core bank and reciprocates by taking the time to really un-derstand the client and its sector so that it can become a trusted partner and advisor. ING is also eager to leverage its interna-tional network in CEE, Western Europe and globally to support clients as they become increasingly regional or global in nature. ING offers a common approach to banking relationships across multiple markets and provides guidance as they seek to broaden their sources of funding, for example by accessing the bond markets.

Meanwhile some European banks have been forced to scale back their lending ac-tivity due to capital constraints, impending regulatory change and the need to delever-age. However, the impact of deleveraging by European banks has generally been low-er than expected following ECB liquidity programmes and the postponement of the Basle III liquidity ratio. Moreover, greater competition from Russian banks – as well as some US and Japanese banks – has more than filled the gap in the current low demand environment.

Changed lending dynamicsThe resilience of most existing banks and the entry of new banks into the CEE lending market have ensured that credit remains available for many companies. Moreover, given strong competition – both between banks and between bank lending and the bond market – pricing has fallen sharply in many markets (with the largest drops in markets that have enjoyed strong liquidity, such as Poland). However, there is an important caveat as attractive terms and less restrictive covenants are only available for the best quality names.

Given the constraints in funding markets, banks are now more careful regarding the currencies of the loans they grant in CEE and also differentiate more clearly be-tween currencies in terms of costs. When a

25

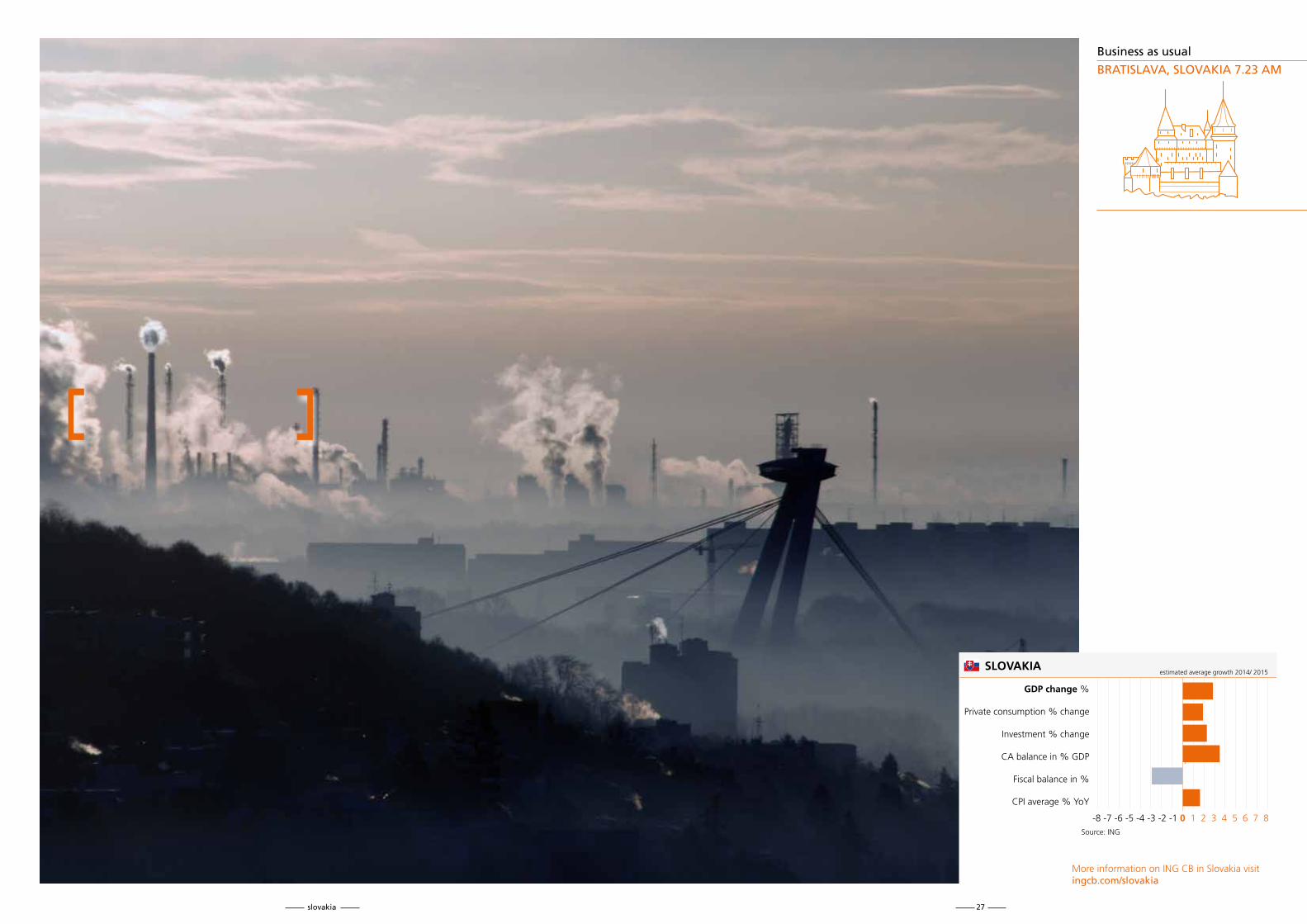

slovakia

SLOVAKIA

GDP change %

Private consumption % change

Investment % change

CA balance in % GDP

Fiscal balance in %

CPI average % YoY

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

Business as usual

BRATISLAVA, SLOVAKIA 7.23 AM

27

Source: ING

estimated average growth 2014/ 2015

More information on ING CB in Slovakia visitingcb.com/slovakia

INCREASING FOCUS ON CASH MANAGEMENT IN CEEtransaction services

Multinational companies usually di-vide the world into distinct regions for payments and cash management in order to maximise efficiency and minimise costs. These regions are determined not just by geography but to some extent also by shared characteristics. As a result, CEE is of-ten treated as a separate region to Western Europe. The irony is that CEE is an incredibly diverse region - by Andre Rijs, Head of TS Sales CEE at ING Commercial Banking

Unlike much of Western Europe, most CEE countries use national cur-rencies rather than the euro. Moreover, countries in CEE have starkly different regulatory regimes and controls regarding the movement of currency and capital.

One thing that many countries in CEE have in common is that inter-national perceptions of their currency and country risk have changed dramatically in recent years. Where political instability and macro-eco-nomic volatility were once the hallmark of many CEE countries, they now look impressively stable compared to many countries in the eurozone.

CEE has weathered the financial and economic crises since 2008 better than its Western European neighbours and has significantly lower levels of government debt. Given weak growth in much of the developed world, multinationals are seeking new growth opportu-nities and markets with growing demand and high margins. Many countries in CEE – most notably Turkey with its rapid growth rate and strong demographics – fit that description perfectly.

From a payments and cash management perspective, conditions continue to improve in CEE. Some countries, such as Poland, have reached a stage in their development where they are largely indistin-guishable from Western European countries in terms of their finan-cial market infrastructure and operating environment. Nevertheless, there are still challenging markets in the region. Broadly speaking the further east one travels, the more complex payments and cash management becomes. An example is Ukraine where interest rates are extremely volatile and the regulatory environment is closed.

Consequently, international companies seeking to operate in CEE must be flexible in the way they approach this diverse region which spans open economies that use the euro and closed economies with currency controls. It is therefore essential for corporates that operate in multiple CEE markets to work with a bank that has on-the-ground knowledge and expertise of market and regulatory conditions.

29transaction services

What clients needRegardless of the complexity of the regu-latory environment, the number of banks they work with, the range of currencies in use or the number of individual markets in which they operate, corporates want visibility of their cash. To some extent, the complexity of CEE cannot be overcome. It is a fact that CEE countries use many dif-ferent currencies and ING can help clients to rationalise their account structures and banking relationships so that they have the most efficient and effective payments and cash management structure possible in the region.

Dealing with the risk presented by multiple currencies is also a priority for multination-als that operate in CEE. There are effec-tively two strategies at their disposal. They can either retain local currencies or, for currencies of countries perceived to be at particular risk, convert them to lower risk currencies. Any decision about currencies must also take into account the use of funds and whether cash balances can go to a pool elsewhere or alternatively can be used to fund local operations.

Cash pooling in CEE is inevitably more complex than in Western Europe as not all currencies are freely convertible. However, contrary to many multinationals’ expec-tations, cash balances in currencies such as the Polish zloty, Hungarian forint and Russian rouble can now be maintained in countries including the Netherlands. Often used as a treasury location by multina-tionals, the Netherlands has tax treaties with most CEE countries to avoid double taxation.

Despite advances, challenges with pooling remain. For example it is still challenging to bring positions from Romania, Bulgaria and Turkey into a cash pool. However, while currency controls cannot be avoided some of the more onerous requirements

associated with them can still be over-come. ING has a branch in St Petersburg in Russia – where many auto part suppliers are based – that can complete much of the paperwork associated with moving funds, thus helping to reduce the adminis-trative burden on clients. ING can insource other activities for clients and also provide clear regulatory and tax advice on the implications of moving positions between countries.

Within CEE, clients can either physically move cash using zero-balancing account structures or adopt notional pooling struc-tures. In some circumstances, physical cash concentration using a zero-balancing struc-ture can be advantageous for corporates. For example, by pooling euros it might be possible to get a better return at the centre than in a particular CEE country. In some countries, concerns about the likelihood of regulatory change might encourage companies to physically take funds out of a country.

Another reason to adopt a zero-balancing structure is that corporates may need the funds elsewhere in the group or want to sweep funds back to a European hub in or-der to repatriate them to head office more easily. A further reason is that companies may not want to allow local operating companies to retain control over cash (as they would do under a notional pooling arrangement).

However, in most circumstances ING advises the use of notional pooling because it does not entail a change in ownership of funds or require potentially complex intercompany lending arrange-ments. The pooling account is in the name of the CEE entity but the central treasury has access to, and control of, the cash that can then be used to fund manufactur-ing in one country, for example by using sales proceeds from other CEE countries.

Regardless of the strategy adopted, ING’s depth in CEE enables it to deliver stand-ardised processes and services across the region in order to improve visibility, control and efficiency.

Meanwhile companies are increasingly creating regional payment hubs in coun-tries such as Poland and Hungary. By being close to the markets they serve, such hubs can reflect the diversity of the region more accurately. They offer a level of skills and language capabilities similar to Western Europe but at a significantly lower cost. ING is capable of offering full support for CEE-based payment hubs as well as for accounts payables and receivables.

Risks and challenges remainCEE continues to be a dynamic region. For example, the decision in November 2012 by Hungary to effectively double the tax on financial transactions has significant implications for corporates that operate in the country. ING is working with its clients to assess whether transactions should con-tinue to be made onshore or if they should be moved offshore in order to lower costs. Regulatory initiatives are also impacting payments and cash management in the region. Many international companies assume that the Single Euro Payment Area (SEPA) and the EU’s Payment Services Directive (PSD) are focused solely on West-ern European countries in the eurozone. However, both initiatives have significant implications for CEE and corporate interest, and the impact of SEPA and the PSD in CEE is growing rapidly, particularly in Slova-kia and Romania. SEPA and the PSD will enable corporates to increase the standard-isation of payments and lower costs. Given the multiplicity of regulatory and other changes in the region it is essential that companies seek advice and expertise on a pan-regional basis.

transaction services

Why ING is differentING has been an integral part of the banking industry in CEE since the late 1980s. As a leading bank it contributed to the founding of many clearing systems across the region and played a ma-jor role in helping to develop the regulatory landscape. The bank’s relationships with regulators, which it mobilises for the benefit of clients, and its insight into how the landscape is evolving, are second to none.

Moreover, ING has repeatedly shown its commitment to CEE. While many international banks have proved a fair-weather friend to CEE, ING is committed to the region and its clients through every stage of the CEE’s development – including in times of crisis. Finding a banking partner in times of prosperity is easy but ING has demonstrated that it is also prepared to stand by its clients in tough times.

ING is active in the nine most important markets in CEE. Its presence in each country extends not only to payments and cash management but also to a full-service commercial banking operation. In Poland, for example, ING operates a full network with 300 branches. This depth of knowledge about local market conditions enables ING to take a proactive approach to the challenges facing its clients, for example by rapidly informing its clients about the implications of the imposition of Hungary’s transaction tax.

In every market in which it operates ING behaves and acts as both a local and an international bank, combining the benefits of flexibility and standardisation. For example, ING can provide all local products and services, including domestic payment instruments. ING offers all of its products and services with standard international terms and conditions, making it easy for mul-tinational companies to manage their relationship with ING. It also offers service and customer support in an internationally consistent way to give clients the control and visibility they need across multiple countries. ING can also connect its solutions in CEE to any global solution in Asia, the US or anywhere else a multinational does business.

The strength of ING’s offering in CEE was recently recognised by TMI magazine for the second consecutive year with an award based on a readers’ poll. The award acknowledges ING’s history of innovation – the bank has invested heavily in solutions including electronic cash vaults that al-low cash collections to be posted to companies’ accounts on the day of collection (before being physically delivered to the bank) by installing deposit machines on the client’s premises. ING has also introduced virtual accounts that allow companies to create virtual accounts for their custom-ers so that payments are easy to reconcile. In July 2013 ING changed the way it provides trans-action services to better reflect how its clients operate. Instead of individual product teams, ING now meets client needs holistically through transactional banking consultants who can address multiple product areas and find the most appropriate solutions. The integration of payments and cash management with working capital solutions and trade finance services (which includes supply chain finance, traditional trade finance products such as letters of credit and the ability to access independent trade finance platforms) is not only aligned with how corporate treasur-ies are organised but also ensures that solutions are structured to optimise efficiency, maximise benefits, reduce risks and lower costs.

31

client case GRUPA ŻYWIECAs a result of a largely cash-driven payments culture in Poland, Grupa Żywiec collects part of its revenues in cash from thousands of customers across Poland. As cash collection can often be expensive and subject to a variety of risks, it was very important for Grupa Żywiec to have an efficient, cost-effective and risk-averse means of collecting, posting and reconciling cash. This article outlines how the company embarked on this transformation and the outcome it has achieved so far.By Karolina Tarnawska, Treasury & Credit Risk Director, Grupa Żywiec

Business modelGrupa Żywiec is a related entity to Heineken group. Of the c.a. 25 beers we offer on the market, the most famous brand is Żywiec which is one of the leading premium beer brands in the country. We also sell a number of other alcoholic and soft drink brands. We are Poland’s largest employer in the alcohol industry, with around 4,500 staff across the country. We have five breweries, with sales and distribution model, covering all group of clients: from small shops to large stores. We sell our products to around 60,000 customers across Poland, ranging from small shops to large stores. There are a variety of reasons why we have adopted this distribution model. One is that we are able to maintain a closer relationship with our customers than we could through a ‘reseller’ model. In addition, rather than channeling our business through a few wholesale partners which might create substantial business and credit risk, a direct sales model enables us to diversify our credit risk more widely.

Importance of cashOur direct sales approach influences every aspect of our business. We have a total of around 2,000 sales representatives and drivers who deliver goods and collect cash. These people are linked to one of 50 de-pots across the country and visit customers at least once a week. Larger customers, particularly wholesalers, generally pay through bank transfers. We do not use a direct debit scheme as this is not support-ed by law in Poland, which means that collection can be unpredictable. Smaller customers, such as retailers, typically pay in cash, both under cash-on-delivery arrange-ments and when credit terms are offered. Cash is the primary method used for retail payments, partly as widespread familiarity with or confidence in banking services is still lagging and the use of cards is not prevalent in many parts of the country. Amongst those customers with bank accounts, the use of electronic banking (particularly in more rural communities) is still rare, especially as internet access may be poor. Furthermore, paying cash into a bank branch is expensive due to high cash counting fees. Consequently, most business owners, who themselves receive payments in cash, prefer to pay cash to their suppliers to avoid additional costs.

Legacy cash collection processIn the past, the cash collection process was managed by sales representatives, who then went back to the depot and passed the cash on to the cashier. The cashier then counted and reconciled the amounts against the customer’s outstanding receivables. Cash was held in a safe box at the depot and then transported to the bank via secure courier to be booked on our account. This process had numerous disadvantages. Sales representatives were spending too much time on the cash col-lection process, which meant that they had less time for sales when visiting customers. They then had to wait a long time at the depot for the cash to be counted, often late in the day. Furthermore, once cash had been received at the depot, it could take another two days until it was posted on our bank account.

Seeking an alternative solutionAs a company, we are committed to the highest standards of customer service, financial integrity and efficiency. We therefore recognised the need to enhance our cash-collection processes as part of a wider initiative to update our business infrastructure and business processes. For example, we set up a central customer services division to ensure a consistently high-quality experience for customers and participated in a Heineken-wide project to implement a single ERP system across the business. Having discussed our cash collection challenges with other parts of the Heineken group, we identified a variety

of objectives for a revised process. Two of the most important objectives were: firstly, we wanted cash to be counted and booked on our account before being physically delivered to the bank. This included ensuring that the bank would be responsible for the cash as soon as it had been entered into the system, without the need to buy depositary machines for which we would be responsible. Secondly, we wanted to be able to post and rec-oncile the amount paid by the customer immediately to avoid the risk of theft or misrepresentation by the individual receiv-ing the cash. We approached our banking partners to discuss our requirements. This took a great deal of time because in many cases our banks did not understand or could not support what we were trying to achieve. We requested proposals from five banks but the quality of the respons-es we received was unsatisfactory, even from the largest banks. However, we found that ING was far more responsive and flexible, and committed time and resources to exploring our needs and devising an appropriate solution. Conse-quently, we were pleased to extend our relationship with ING into collections.

A new cash collection modelThe first deposit machine was installed in our depot in February 2012 and the last one in June 2012. Sales representa-tives are no longer responsible for cash collection, which is now undertaken only by drivers. This made it easier to roll out, particularly as our ERP system provides strong functionality for drivers. Drivers no longer have to wait at the depot for cash counting and any errors or inconsistencies can be identified more quickly thanks to barcoded envelopes used in the process of remote posting and reconciliation. . We have been able to book cash two days earlier, whilst also requiring fewer resources, enabling us to appoint former cashiers to other responsibilities. Our credit risk has been reduced and we are able to post and reconcile collections against credit lines very quickly, improving the service we provide to customers and enhancing our cash management and forecasting efficiency.

Business impactThe new cash collection process has been received very positively by the sales team, drivers and depot managers alike. As there is often a natural disinclination to change, we spent time on working out the best way of communicating on the new processes across the team with the strong support of senior management. In addition, we received advice and assis-tance from ING. Our business divisions typically operate quite independently of each other, so this project was an oppor-tunity for Treasury to work more closely

with our colleagues in Distribution and Sales. We involved them in decision-making which in turn encouraged broader-based support and ensured that the implementa-tion, which was undertaken by local teams, was consistent. As a result of this upfront effort and collaboration the new cash collection process has received widespread support.

Moving forwardAlthough our depots now operate using the new cash collection process, there are still enhancements we make. We need to ensure that we have sound contingency arrange-ments in place as maximising the security of our people and the cash machines is a priority. Another potential improvement is to reduce the number of exceptions between declared and deposited amounts. For example, there may be an input or round-ing error which would prevent automatic reconciliation. Our control mechanisms allow to identify any attempt of fraud or theft immediately but we are still trying to counteract the risk through such measures as scanning rather than manual inputting the collection amount.

This has been a pioneering project in Poland leveraging technology to enhance efficien-cy, risk management and customer service, whilst respecting the way in which our customers wish to operate. The initiative has also been very valuable in demonstrating the benefit of collaboration across different parts of the business to create a more inte-grated solution. We have been very fortu-nate to be able to leverage ING’s experience, expertise and innovative know-how, and the project would not have been possible without the flexible, ‘can do’ attitude that sets the bank apart from others that we approached. We look forward to contin-uing to enhance our cash collections and other financial processes, in the future, as part of our commitment to leading industry practices.

33grupa żywiec

Business as usualSofia, BULGARIA 9.12 AM

BULGARIA

GDP change %

Private consumption % change

Investment % change

CA balance in % GDP

Fiscal balance in %

CPI average % YoY

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

35

Source: ING

estimated average growth 2014/ 2015

bulgaria

More information on ING CB in Bulgaria visitingcb.com/bulgaria

The economic uncertainty of recent years has highlighted CEE’s strengths in many of the world’s most important sectors. Metals and mining companies and energy firms from CEE are not just regional powerhouses but crucial global players now. Few regions match the agricultural poten-tial of CEE. As companies consolidate and become more efficient, CEE will become ever more central to the world’s ability to feed itself. Elsewhere, in sectors such as infrastructure and in particular telecommunications, media and technology, the dynamics that became associated with CEE in the late 1980s is resurgent.

What these diverse sectors have in common is a need for finance. Given the nature of CEE and the changing needs of companies in the region, structured finance – which uses cash flow or asset-based financing structures – continues to play a crucial funding role alongside the ever-de-veloping debt capital markets. Effective structured finance requires wide-ranging and extensive connections with other financial institutions. It also demands structuring expertise, which comes from a combination of commitment to innovation and longstanding experience. At the same time in-depth knowledge of sectors and regions is equally important to structured finance.

The structured finance business is changing as the capacity of many banks to lend is curtailed by regulatory reform such as Basel III, which requires them to hold more capital. At ING we have re-affirmed our commitment to global structured finance as we remain a top 10 player, and to CEE where we have a 20-year track record and are consistently a top 3 supplier of structured finance solutions to our ever-growing client base. As arranger and underwriter we continue to play an active role in domestic and international deals in the club and syndicated loan market. We also offer advisory services that leverage our structured finance expertise and sector knowledge to give clients the edge when it comes to financing projects and acquisitions, or optimising their capital structures.

COMBINING CEE KNOWLEDGE AND STRUCTURED FINANCE STRENGTHstructured finance

ING combines its deep understanding of CEE and the region’s leading business sectors with its acclaimed capabilities in structured finance to give its clients world-class service and sup-port, according to Michiel de Haan, Head of Structured Finance for ING in CEE.

37structured finance

While most CEE companies restored their investment programmes cautiously following the 2008 and 2009 financial crisis, their plans were nevertheless predicated on a continuing commodity boom. In particular, there was an assumption that growth in China, which had fuelled the commodity boom, would continue and it would seek an ever-larg-er quantity of metals and mining products for its growing manufacturing sector.

In reality, China’s growth has slowed and it is now trying to shift to a consump-tion-based economy – there is no immediate prospect of metals and mining demand meeting previous expectations. Falling prices and lower than expected demand mean that companies have been forced to reconsid-er their capital expenditure given over-production. Planned projects are being put on hold or scaled down, inefficient capacity is being closed and non-core assets are being sold.

In the pre-2008 period (and also in 2010 and 2011 when there was a brief recovery), there was significant M&A activity in the metals and mining sector: many companies assumed that prices would continue to rise and achieving scale and raising volumes would be critical to future success. Falling prices and demand mean companies are now concentrating on low-cost producing assets and divesting assets rather than acquiring new ones (while also focusing on controlling expenses and decreasing their working capital requirements).For example, Mechel, the leading Russian coking coal producer, bought assets in the US, Ukraine and Kazakhstan during the M&A boom. Now, struggling with its pre-2008 debt burden, the company has sold off Romanian plants and some assets in Russia and Kazakhstan.

Crucially, the buyers of these assets are not global metals and mining groups. In Turkey, for example, Mechel sold several ferroalloys assets to Turkish diversified

industrial group Yildirim. Similarly, assets in Romania have been sold to domestic buyers.

Strong liquidityFinancing conditions for high quality metals and mining companies have improved markedly as the eurozone crisis, which severely affected some European banks’ ability to serve the sector, has subsided. Actions by the Federal Reserve and European Central Bank have provided banks with plentiful liquidity. Moreover, contrary to some expectations banks’ preparation for Basel III, which will increase the amount of capital they must hold for certain risk assets, has not decreased banks’ appetite for good quality metals and mining assets.

Pricing has fallen for high quality metals and mining companies and terms have become more attractive to borrowers. Indeed, for the first time leading companies in the sector have been able

Companies in the metals and mining sector in CEE, which is dominated by Russia but with major production in Ukraine, Kazakhstan and elsewhere, are global players. Consequently, they are affected by trends at a global level. The dominant issue in the post-2008 period has been a significant de-crease in prices for many hard commodities and over-capacity in metals and mining - by Julia Chekrygina, Head of Metals, Structured Metals and Energy Finance

DEVELOPMENTS IN METALS AND MINING

metals & mining

to access unsecured funding (previously competition was solely on price).For example, in September Magnitogorsk Iron and Steel Works, which is non-invest-ment grade, was able to borrow $500 million over four-years on an unsecured basis from a group of five banks, including ING. Similarly, Russian nickel and palladium giant Norilsk Nickel was able to borrow $2.35 billion over five-years on an unsecured basis from 16 banks, including ING.

While the best pricing and terms are only available to the strongest companies, buoyant liquidity conditions have allowed companies facing challenges to restructure their debt. For example, ING was a coordinator (together with Unicredit) for a $500 million three and five-year loan that refinanced Ukrainian steelmaker Donetsk-steel – Iron and Steel Works’ debt following a restructuring that began in 2008. The success of the deal despite the difficult backdrop – including the rating downgrade of Ukraine – highlights the strength of bank liquidity.

Currently, the only restriction on bank lending to high quality metals and mining companies is banks’ country limits, which – in some instances – have been filled by huge deals such as $22.5 billion raised by Rosneft through several syndicated facilities to finance its TNK-BP acquisition.

During the first half of 2013, metals and mining companies also enjoyed strong conditions in the bond market. ING acted as joint lead manager and bookrunner for a $1 billion seven-year eurobond offering from Russia’s large steelmaker Evraz in April. However, conditions in the bond market have become weaker since the Federal Reserve indicated that it would begin to taper its asset purchases and supply has dried up. Consequently, metals and mining companies have sought funds from their relationship banks instead.

ING’s metals and mining strengthING has a well-deserved reputation in the metals and mining sector in CEE having supported many of the leading companies from the region since their inception in the early 1990s: few banks can claim 20 years of experience in structured metals financing in CEE. As a result, ING has a deep understanding of the operating models of the region’s companies and their needs.

Moreover, throughout its long history of activity in CEE, ING has built up knowl-edge of the sector and created capabilities that rival any bank in the world. Using its network of local offices, ING offers comprehensive relationship coverage on the ground. This is combined with teams offering global capabilities in equity capital markets, debt capital markets and mergers and acquisitions advisory, which have an excellent track record in serving the metals and mining sector.ING’s strength across lending, structured

finance and corporate finance in metals and mining in CEE fits perfectly with the bank’s approach to working with clients on a relationship basis – taking a holistic view of their needs – rather than focusing on individual product offerings. ING’s event finance team, based in Amsterdam, coordinates all product activity so clients get the right solution for their specific requirements. This approach also better reflects the changing needs of the sector, following widespread restructurings in recent years.

ING’s long track record serving companies in the metals and mining sector in CEE is different to its competitors because the bank stands by its clients throughout the cycle – regardless of commodity price volatility or liquidity problems in the banking sector. ING provides not just products and services but also guidance and advice on balance sheet structuring and hedging that are only possible as a result of a deep and long-term relation-ship.

39

kazakhstan

Business as usualKAZAKHSTAN 2.13 PM

KAZAKHSTAN

GDP change %

Private consumption % change

Investment % change

CA balance in % GDP

Fiscal balance in %

CPI average % YoY

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

41

Source: ING

estimated average growth 2014/ 2015

More information on ING CB in Kazakhstan visitingcb.com/kazakhstan

FINDING DIRECTIONS IN CEE

The need for infrastructure development in CEE is significant. Despite huge investment in the region since 1989, utilities, road, rail and air infrastructure as well as other public and social infrastruc-ture continues to suffer from a legacy of historic underinvestment over many decades. Much ground still needs to be made up to raise infrastructure fully to EU standards - by Michael Dinham, Head of Infrastructure Finance for ING

Partly because of this inherent demand, infrastructure spending in CEE has remained impressively consistent over the past five years despite the financial crisis and the economic downturn that followed. The commitment of CEE governments to infrastructure has stayed strong while bank interest in infrastructure projects has been steady – the underlying potential for growth of much of CEE has ensured that it is a priority for banks involved in infrastructure finance.

Moreover, while CEE has not escaped the turbulent conditions of the past five years, its economies have performed significantly better than southern Europe, for example. Generally, most CEE economies recovered quicker than those in southern Europe – in-deed Poland was the only country in Europe not to suffer a recession – while banks in CEE did not require public bailouts. Investors are also reassured by CEE’s low public debt compared to much of the rest of Europe.

A diverse marketCEE is a diverse region that is often viewed as three distinct country groups rather than a single market. The first group includes EU members such as Poland, Czech Republic, Hungary, Slovakia and the Baltics that are perceived to be broadly economically successful with functioning legal and financial systems. The second group comprises weaker EU member states such as Bulgaria and Romania that have experienced economic or political problems in recent years that have undermined investor confidence. The third group includes Turkey and Russia which are seen as being distinct from the rest of the region given their size, location and characteristics.

Accordingly, these three groups of countries attract different levels of bank interest in terms of infrastructure finance. Their relative attraction has changed little in the post-fi-nancial crisis period. The first group of EU member states has always received strong

infrastructure finance

infrastructure investment while the weaker members have been less favoured. However, one notable change in recent years is that Russia and Turkey have become more attractive infrastructure investment destina-tions given their above-average growth potential.

The three groups of CEE countries – success-ful EU states, less-successful EU states and Turkey and Russia – have starkly different track records of involving private investors in infrastructure projects.

Predictably, the first group of EU countries has successfully adopted public private partnerships (PPP) as well as directly selling infrastructure assets to private entities, in line with EU guidelines. While attempts have been made by the second group of countries to use PPP and to even privatise assets, little progress has been made in both areas because of weak institutions, a lack of transparency and an insufficiently robust legal environment.

Turkey and Russia share some characteristics with Bulgaria and Romania in terms of uncertainty over some aspects of their legal and political environment. However, their scale – and the scale of funds available to spend on infrastructure within the countries – means they have attracted greater interest from international investors for PPP projects (although they have a patchy track record of privatising state-owned infrastructure assets).

Developments in financingFinancing structures for PPP have remained broadly similar in recent years: debt (provid-ed primarily by banks) typically makes up 80%-90% of a project’s finance and the remaining 10-20% is equity (provided by construction companies, infrastructure funds or other investors).

One change is that debt costs have risen compared to the period before 2008. However, the change has been relatively slight (with the exception of Hungary where political risk has made funding expensive). Another change in the post-crisis period is

that bank appetite for long-term risk (over 20 years) has diminished although there is still plenty of appetite to go to 15 years.