information and communications technology (ict ... · 4.4 ict and productivity at the industry...

TRANSCRIPT

Information and Communications Technology (ICT), Productivity and

Economic Growth in China

by

Chee Kong WONG

This thesis is presented for the degree of Doctor of Philosophy

of the University of Western Australia

Business School

December 2007

ABSTRACT

In the current literature on productivity and economic growth, many studies have

explored the relationship between information and communications technology (ICT)

and growth. In these studies, ICT capital stock is treated as an individual input in the

production process that contributes to output growth. In fact, ICT is found to be a key

driver of productivity growth in the developed economies. However, few empirical

studies deal with China which has in recent years become one of the world’s largest ICT

markets and production centres. The lack of empirical work in this field contrasts

sharply with the wealth of literature which presents background and descriptive studies

of China’s high technology sectors that include the telecommunications, the computer

and the Internet sectors.

This dissertation attempts to fill the void in the literature by examining the role of ICT

in China’s economy over the past two decades. It aims to develop a framework which

emphasizes ICT as a production factor and apply it to interpret China’s economic

growth. The dissertation contributes to the empirical literature by focusing on the

following core aspects underlying the linkage between ICT and economic growth. First,

it attempts to estimate the size of China’s ICT capital stock using the perpetual

inventory method. Second, based on such estimates, the dissertation measures the

contribution of ICT to China’s economic growth by means of a production function

model that segregates ICT from all other forms of capital. Third, the dissertation

examines the impact of ICT on technical efficiency in China’s regions by applying a

stochastic frontier model. Lastly, the dissertation looks at the demand aspect of the ICT

industry by estimating and projecting demand for ICT services, namely, the

telecommunications and computer markets in China.

According to this study, ICT capital is found to be a positive driver for the Chinese

economy, and is responsible for about 25% of the country’s economic growth, although

the percentage varies at different periods. ICT capital is also found to have a positive

and significant impact on technical efficiency in the Chinese regions. However, the

disparity between the coastal and inland regions in terms of technical efficiency scores

is found to be very wide, due to the bulk of ICT investment going into the municipal

cities and coastal provinces. It is also found that China may be facing the beginning of a

period of strong productivity growth driven by increased investment in ICT, especially

i

innovative investment. Furthermore, projections of demand show that the majority of

Chinese citizens will have access to a fixed-line telephone or the mobile phone in five

years from now, while about half of the Chinese population is expected to use the

computer by 2010.

ii

TABLE OF CONTENTS

Abstract i

List of tables vii

List of figures x

Acknowledgements xii

1 INTRODUCTION 1

1.1 Background 2

1.2 Objectives and contributions 3

1.3 Outline of the chapters 4

2 DEVELOPMENT OF THE ICT SECTOR 7

2.1 Definitions of ICT 7

2.2 The telecommunications industry 8

2.2.1 The monopoly era (1949-1994) 9

2.2.2 Telecommunications reform and policies 10

2.2.3 Telecommunications developments after WTO 12

2.3 The computer industry 16

2.3.1 Development of the hardware industry 17

2.3.2 Software development 24

2.4 National science and technology programs 32

2.4.1 Brief overview of China’s science and technology (S&T) policy 32

2.4.2 S&T projects 33

2.4.3 High technology development zones 35

2.5 The ICT market in China 40

2.5.1 Rise of the ICT market 41

2.5.2 China’s ICT trade 49

2.6 Conclusion 50

Appendix to Chapter 2 56

iii

3 ICT, PRODUCTIVITY AND GROWTH: DEBATES AND 59 MEASURES

3.1 Introduction 59

3.2 Debates on the role of ICT 60

3.2.1 ICT and productivity growth: A microeconomic view 60

3.2.2 ICT and productivity growth: A macroeconomic view 62

3.2.3 The ICT productivity paradox 65

3.3 Measuring the contribution of ICT to productivity and economic growth 69

3.3.1 ICT contribution to GDP or output growth 70

3.3.2 ICT contribution to average labour productivity (ALP) growth 71

3.3.3 ICT contribution to TFP growth 73

3.4 Conclusion 75

4 ICT, PRODUCTIVITY AND GROWTH: EMPIRICAL STUDIES 76

4.1 Introduction 76

4.2 ICT contribution to economic growth 76

4.3 ICT and labour productivity growth 89

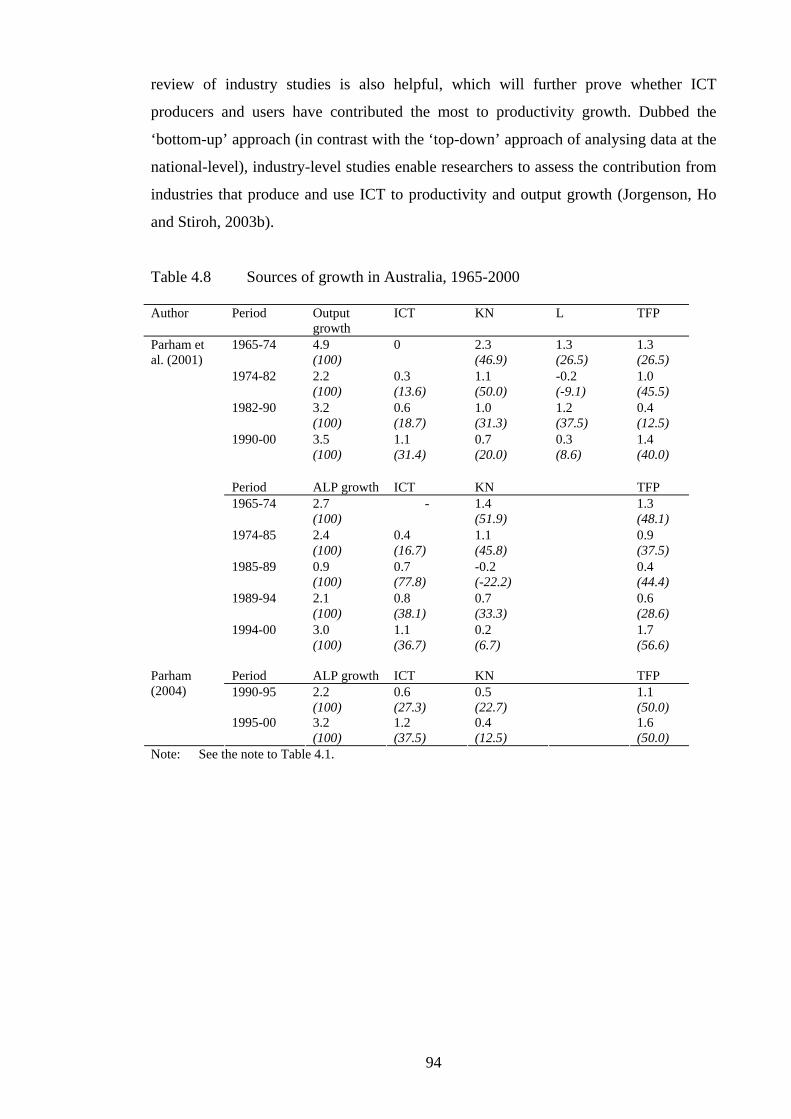

4.4 ICT and productivity at the industry level 93

4.4.1 ICT-producing vs ICT-using industries 96

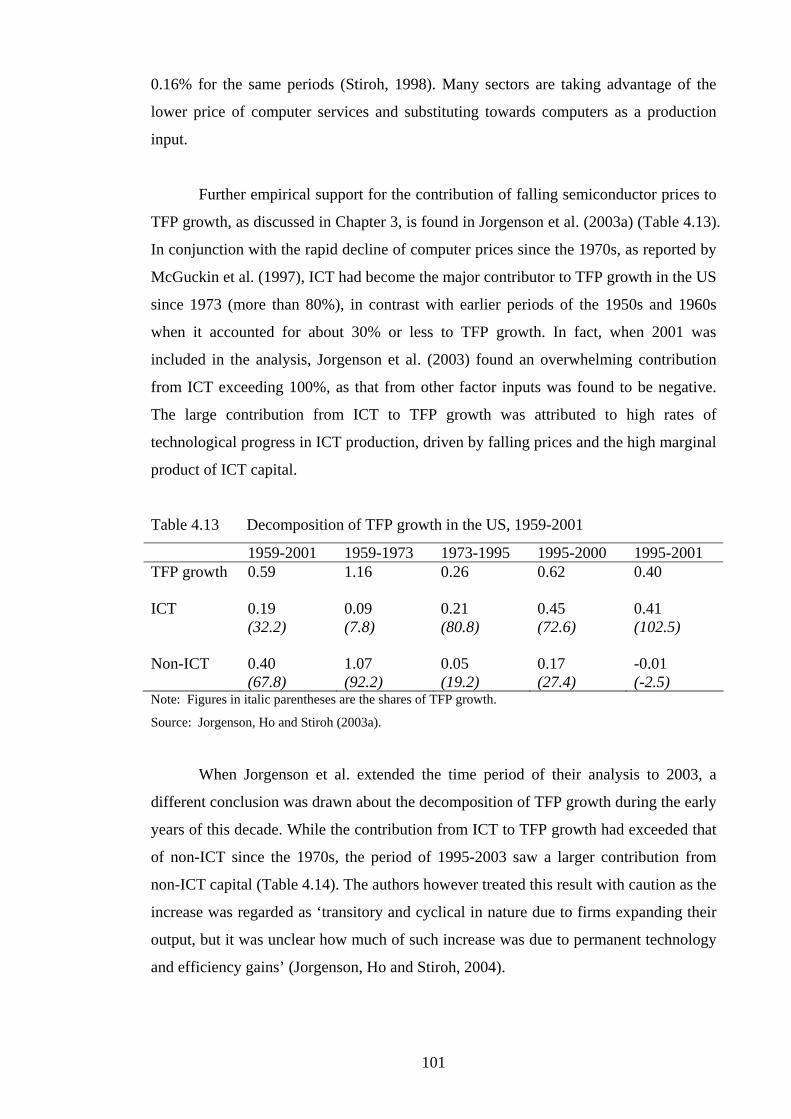

4.4.2 ICT contribution to TFP growth 100

4.5 China-related studies 103

4.6 Conclusion 105

5 ESTIMATIONS OF ICT CAPITAL STOCK 107

5.1 Introduction 107

5.2 ICT investment in China 108

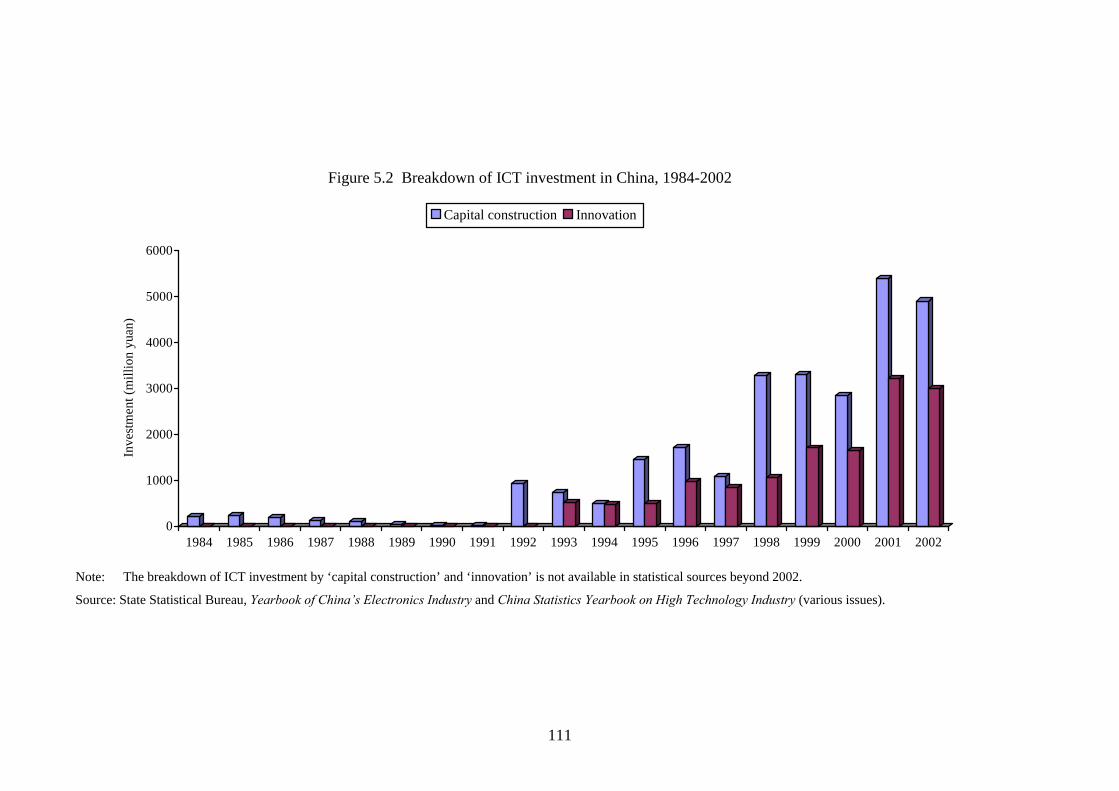

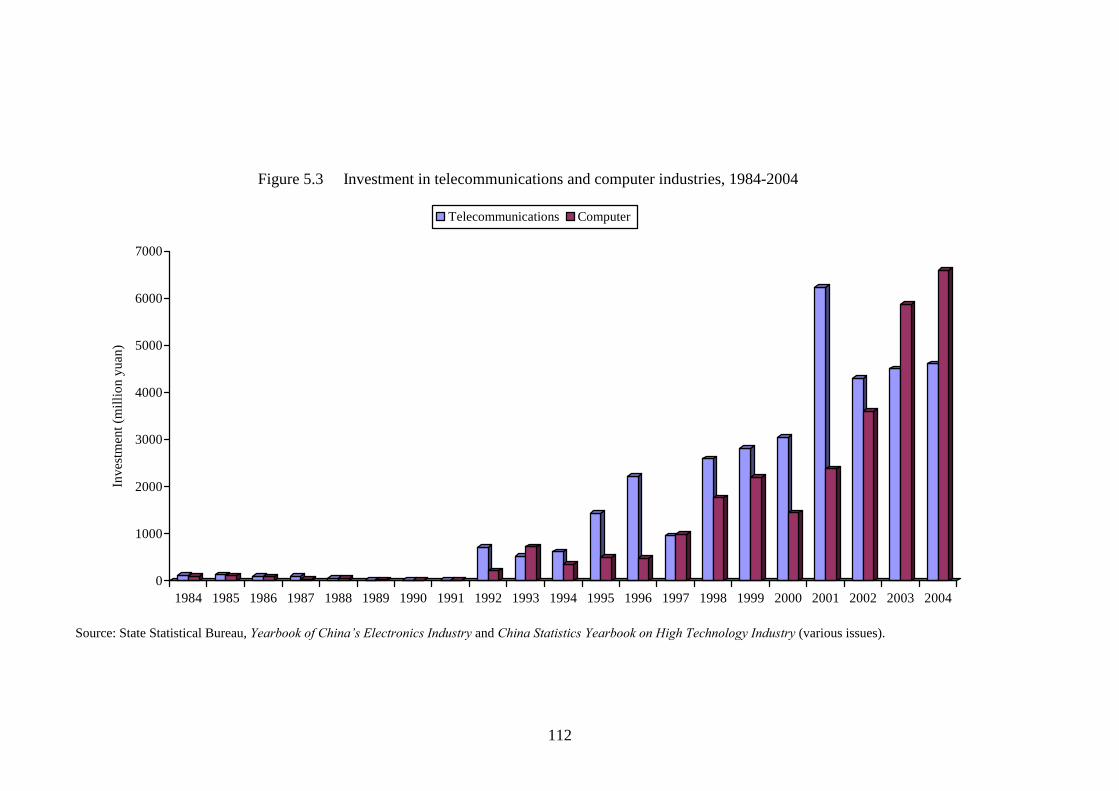

5.2.1 Patterns of ICT investment 108

5.2.2 Explaining the growth of ICT investment 114

5.3 Estimation of capital stock 118

5.3.1 A theoretical model 118

5.3.2 Depreciation of ICT capital 119

5.3.3 Measurement of China’s ICT capital stock 120

iv

5.4 Estimation and sensitivity analysis 124

5.5 Conclusion 126

Appendix to Chapter 5 131

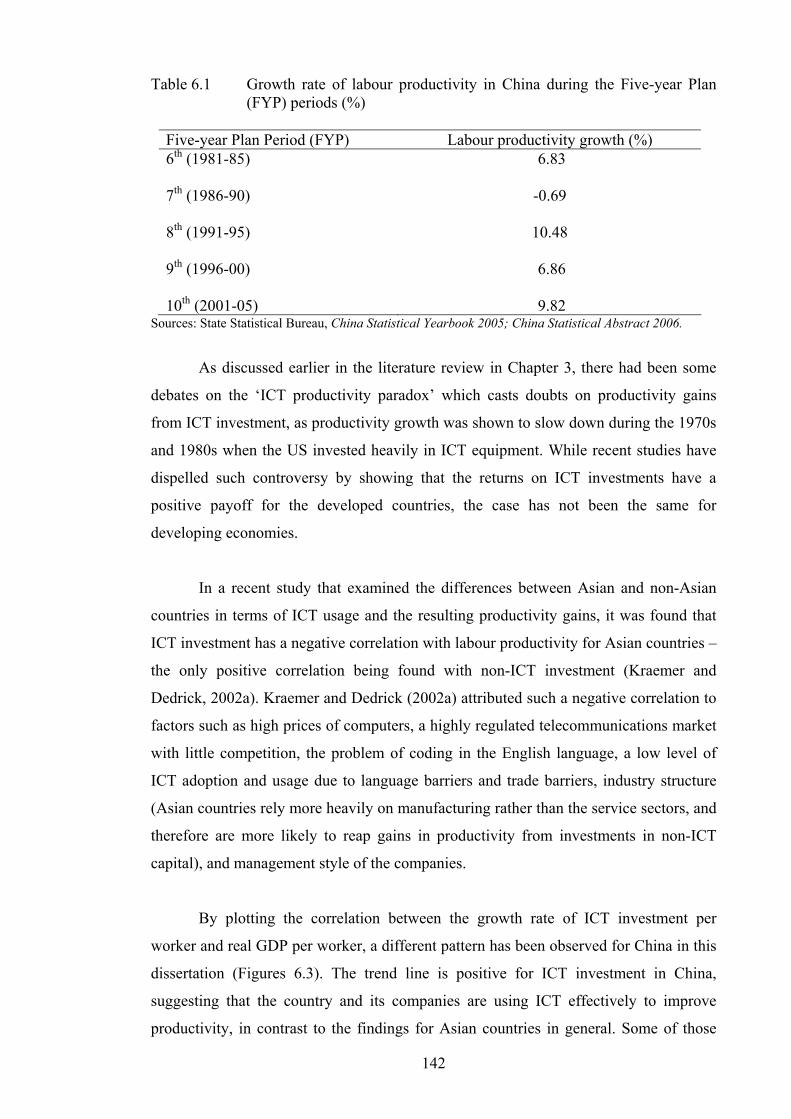

6 ICT AND ECONOMIC GROWTH: A NATIONWIDE STUDY 138

6.1 Introduction 138

6.2 ICT, productivity and the Chinese economy 138

6.3 Model specification 145

6.4 Description of data 146

6.5 Estimation results and interpretation 147

6.5.1 Estimation results 147

6.5.2 Decomposition of output growth 148

6.5.3 TFP growth in China 151

6.5.4 Sensitivity analysis 152

6.6 Conclusion 156

Appendix to Chapter 6 158

7 ICT AND EFFICIENCY IN CHINESE REGIONS 161

7.1 Introduction 161

7.2 ICT investment in Chinese regions 161

7.3 ICT and technical efficiency: a review 164

7.3.1 Conceptual issues 164

7.3.2 Efficiency measurement 164

7.3.3 ICT and technical efficiency 169

7.3.4 China-related studies 170

7.4 Modelling framework 171

7.5 Description of data 173

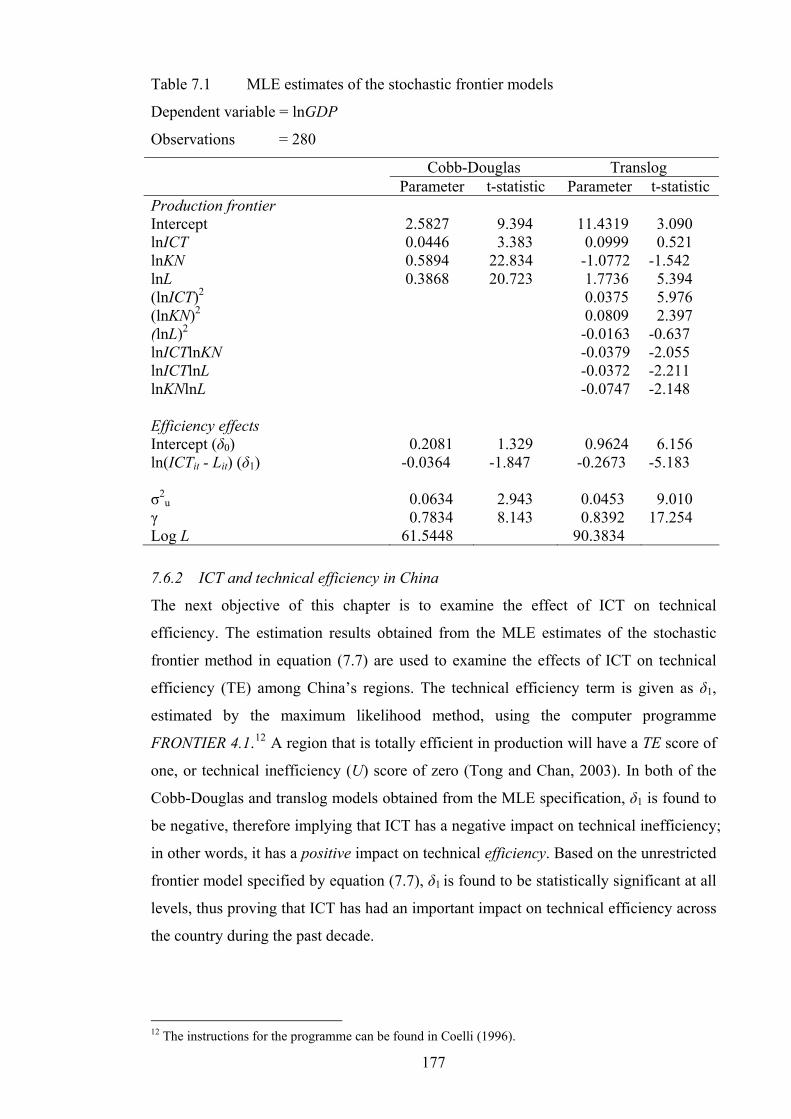

7.6 Estimation results and interpretation 175

7.6.1 Estimation results 175

7.6.2 ICT and technical efficiency in China 177

7.7 Conclusion 180

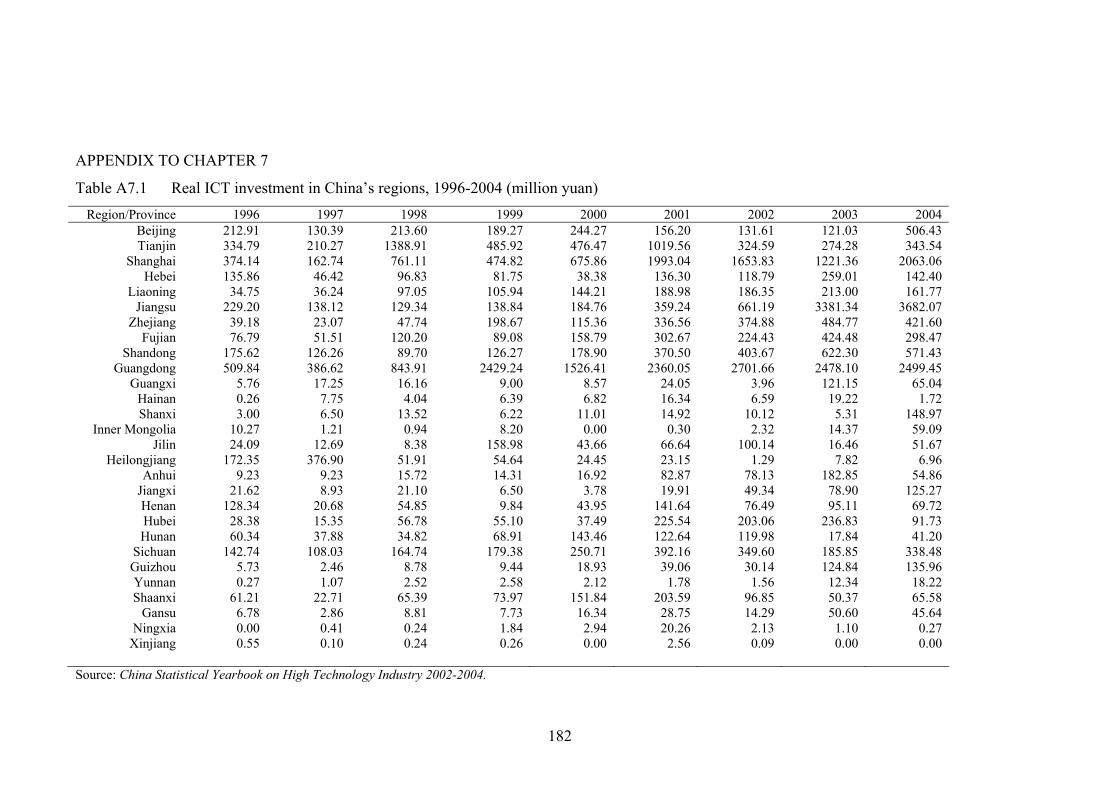

Appendix to Chapter 7 182

v

8 DEMAND FOR ICT SERVICES IN CHINA 184

8.1 Introduction 184

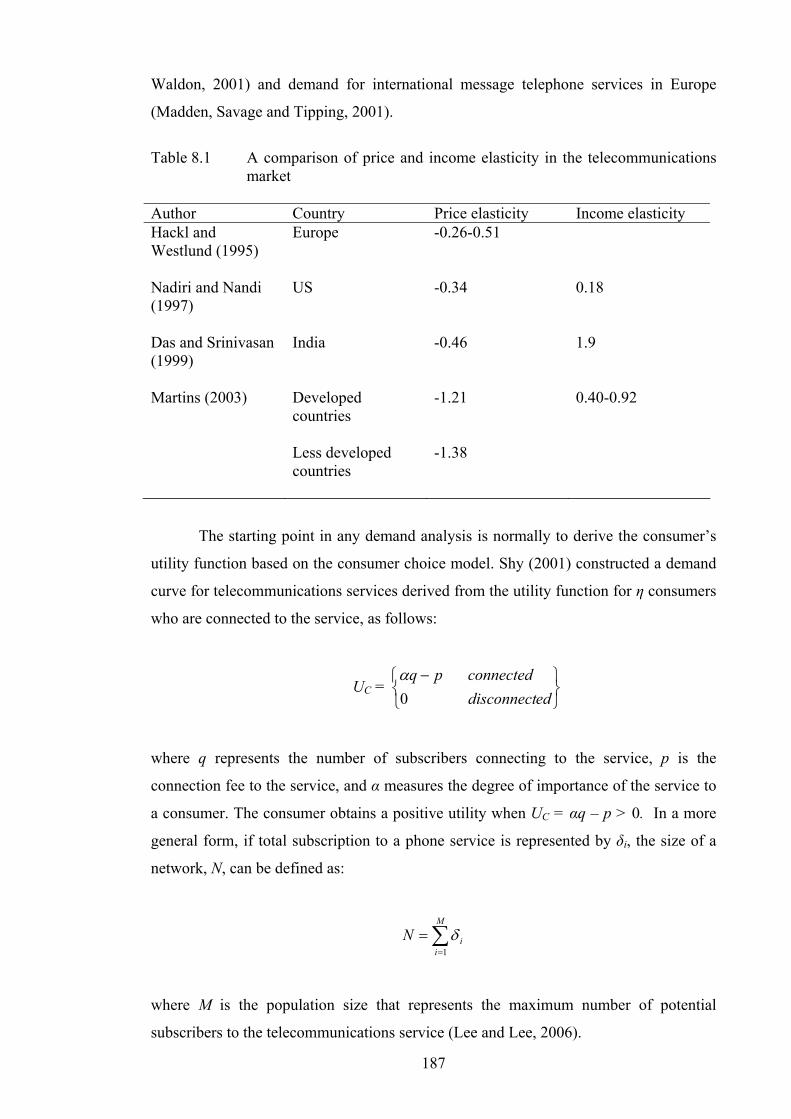

8.2 Literature review 185

8.2.1 Demand for telecommunications 185

8.2.2 Demand for computers 190

8.3 Modeling demand 191

8.3.1 Modeling demand for fixed-line telecommunications 191

8.3.2 Modeling demand for mobile telecommunications 193

8.3.3 Modeling demand for computers 194

8.4 Data issues 196

8.5 Estimation results 202

8.5.1 Estimation results for fixed-line telecommunications demand 202

8.5.2 Estimation results for mobile telecommunications demand 205

8.5.3 Estimation results for computer demand 209

8.6 Projection of ICT demand 210

8.6.1 Forecasting telecommunications demand 211

8.6.2 Forecasting computer demand 213

8.7 Conclusion and growth prospects 214

9 CONCLUSION 220

9.1 Summary of findings 220

9.2 Future directions of ICT in China 221

9.2.1 Prospects after WTO 221

9.2.2 Moving beyond the Earth: Development of satellite and space 223 technology

9.3 Epilogue 225

BIBLIOGRAPHY 227

vi

LIST OF TABLES

2.1 Market shares of China’s PCs (%) 19 2.2 China’s CPU market, 2001-2004 23 2.3 Market shares of China’s software (%) 27 2.4 Strategic choices for developing China’s software industry 31 2.5 China’s Golden Projects 36 2.6 Geographic distribution of HTDZs in China 37 2.7 Actual and projected output growth rate of computers and office 43

equipment in China and developed countries, 2004-2009 (% change y-o-y)

2.8 Breakdown of Internet usage by services in China, 2002-2006 49 (million users in June of the year)

A2.1 History of China’s computer history, 1956-2004 56 4.1 Sources of growth in GDP and ALP in the US, 1973-2001 79 4.2 Contribution of ICT to output growth in nine OECD countries, 80 1985-2000 4.3 Contribution of ICT to output growth in ten Asian countries, 82 1990-1999 4.4 Contributions to GDP growth 83 4.5 Sources of growth in non-farm output and ALP in the US, 90

1974-2001 4.6 Contribution of ICT to ALP growth in ten Asian economies, 92 1990-1999 4.7 Sources of growth in Canada, 1972-2001 93 4.8 Sources of growth in Australia, 1965-2000 94 4.9 Contributions of ALP growth: Single country study (Unit: %) 95 4.10 Contributions of ALP growth: Cross-country study, 1995-99 96 (Unit: %) 4.11 Decomposition of US labour productivity growth by industry, 98 1987-2000

vii

4.12 Decomposition of ALP growth in Canada, EU and US by industry, 98 1995-2000 4.13 Decomposition of TFP growth in the US, 1959-2001 101 4.14 Decomposition of TFP growth in the US, 1959-2003 102 4.15 Decomposition of TFP growth in Japan, 1975-2003 102 4.16 Contribution of ICT production to TFP growth in the EU and US, 104 1995-2001 4.17 Empirical studies of the contribution of ICT to China’s economic 104 and labour productivity growth 5.1 Growth indicators, 1986-2004 (%) 109 5.2 Depreciation rate of ICT equipment 121 A5.1 Real ICT investment in China, 1984-2004 (using CPI) 131 A5.2 ICT capital stock series in China, 1983-2004 (using CPI) 132 A5.3 Real ICT investment in China, 1984-2004 (using hedonic price indices) 134 A5.4 Alternative ICT capital stock series in China, 1983-2004 135 A5.5 Price deflators 137 6.1 Growth rate of labour productivity in China during the Five-year Plan 142

(FYP) periods (%) 6.2 Regression results of China’s sources of economic growth, 1983-2004 148 6.3 Contributions to output growth in China, 1983-2004 149 6.4 Sensitivity tests using various depreciation rates of ICT capital stock 155 in China 6.5 Results of sensitivity analysis 156 A6.1 Regression results of China’s sources of economic growth, 1983-2004 158 A6.2 Contributions to output growth in China, 1983-2004 159 A6.3 Results of sensitivity analysis 160 7.1 MLE estimates of the stochastic frontier models 177 7.2 Average technical efficiency (TE) in China’s regions 178 A7.1 Real ICT investment in China’s regions, 1996-2004 (million yuan) 182

viii

A7.2 ICT capital stock in China’s regions, 1995-2004 (million yuan) 183 8.1 A comparison of price and income elasticity in the telecommunications 187 market 8.2 A comparison of price and income elasticity in the computer market 191 8.3 Estimation results: fixed-line telephone demand 203 8.4 Estimation results: mobile telephone demand 208 8.5 Estimation results: computer demand 209 8.6 Estimated price and income elasticity for China’s fixed-line telecom 212 demand 8.7 Estimated growth rate of price and income for China’s fixed-line 212 telecom demand 8.8 Estimated price and income elasticity for China’s mobile telecom 213 demand 8.9 Estimated growth rate of price and income for China’s mobile 213 telecom demand 8.10 Estimated price and income elasticity for China’s computer demand 214 8.11 Estimated growth rate of price and income for China’s computer 214

demand

ix

LIST OF FIGURES

2.1 Production of PCs in China, 1990-2005 18 2.2 Growth and forecasts of Chinese software sales, 2000-2009 26 2.3 Telecommunications network capacity in China, 1978-2006 44 2.4 Number of fixed line and mobile subscribers in China, 1986-2006 45 2.5 Fixed and mobile penetration rates in China, 1988-2006 46 2.6 Number of Internet users in China, 1994-2007 47 2.7 China’s trade in ICT products, 1984-2005 51 2.8 ICT and total trade in China, 1984-2005 52 2.9 Growth rate of ICT and total trade in China, 1985-2005 53 3.1 ICT and firm productivity 61 3.2 ICT, productivity and growth 64 5.1 Real ICT investment in China, 1984-2004 110 5.2 Breakdown of ICT investment in China, 1984-2002 111 5.3 Investment in telecommunications and computer industries, 1984-2004 112 5.4 Ratio of ICT investment to total fixed investment in China, 1984-2004 113 5.5 ICT capital stock in China, 1983-2004 127 5.6 Ratio of ICT to total capital stock and output in China, 1983-2004 128 5.7 Growth rate of ICT capital stock and real GDP in China, 1993-2004 129 6.1 China’s tertiary output, 1978-2005 (in 1978 constant prices) 140 6.2 Labour productivity in China, 1978-2005 141 6.3 ICT investment per worker and labour productivity in China, 144 1985-2004 6.4 Output and input indexes in China, 1984-2004 153 6.5 TFP growth in China, 1984-2004 154 7.1 Correlation between GDP per worker and ICT investment per worker 165 in China’s provinces, 2004

x

7.2 Total ICT investment in China’s regions, 1996-2004 166 7.3 Ratio of ICT investment to GDP in China’s regions, 1996-2004 167 7.4 ICT capital stock in China’s regions, 1995-2004 176

7.5 The effect of ICT on technical efficiency in China’s regions, 1995-2004 181 8.1 Growth rate of fixed line, mobile and GDP in China, 1979-2005 198 8.2 Log-linear relationship between fixed line subscribers and ICT price 199 index in China, 1978-2005 8.3 Log-linear relationship between mobile subscribers and ICT price index 200

in China, 1988-2005 8.4 Correlations between fixed-line subscription, mobile subscription, and 201 income per capita in China, 1978-2005 8.5 Forecast of China’s fixed-line telephone demand, 2005-2010 215 8.6 Forecast of China’s mobile telephone demand, 2005-2010 216 8.7 Forecast of China’s computer demand, 2005-2010 217

xi

ACKNOWLEDGEMENTS

I wish to thank my supervisor, Associate Professor Yanrui Wu, for his patience and

excellent supervision in providing guidance in the course of writing this dissertation. He

has contributed invaluable and constructive comments in all aspects of the dissertation,

covering the econometric exercises, thesis structure and checks for grammar errors.

I am eternally grateful to my parents for the emotional and financial support which

helped me see through periods of anxiety and distress. They have been my greatest

supporters, not only in ensuring that I meet my financial needs, but most importantly,

with the love that they showered unceasingly at all times. It is when I live away from

home that I could feel the strong bonding between us, and truly appreciate the sacrifices

my parents have made in bringing me up.

There are several persons who have become an important part of my life in Perth.

Firstly, I will always remember Mr and Mrs Ng who provided accommodation at

Ballajura during the first six months of my stay upon arrival in Perth, by offering a

room at very low cost and treating me like a part of their family. During these four years

of candidature, I am also fortunate to be acquainted with many local residents, including

Mr and Mrs Jeremy Koh, Paul, Elaine, Jivan, Alvin, Irene, ‘Uncle’ Steven and ‘Aunt’

Cecilia, who have helped me feel at home and adapt to the community life within the

shortest possible time span.

In times of financial difficulties, especially when I had to pay my tuition fees before a

semester, I would not have been able to foot some of the bills without the selfless

assistance from Mr P. C. Wong, Liang Fook, Bernard Peh and David Phan. The

dissertation was also completed with financial support from the C. A. Vargovic Bursary

of UWA Business School and a Completion Scholarship of the Graduate Research

School.

Last but not least, there are many others who have lent their encouragement and moral

support that helped me to persevere. Special thanks go to Ian Li, Martin Lim, Cindy

Chia, Eugene Koo, Kenneth Wu and Dawn Low, who have rendered their assistance

with my research work in one form or another, including data entry and proof-reading.

xii

Chapter 1

INTRODUCTION

China’s economy has been growing at an average rate of 8.7% annually in the past two

decades (1986-2005).1 Many studies attribute China’s rapid growth to various macro-

economic factors, such as economic reform, including fiscal reform and exchange rate

reform, the huge domestic market and active participation in globalisation, including

increased international trade and inflow of foreign direct investment. However, few

studies have paid attention to the role of information and communications technology

(ICT) as a potential and increasingly significant source of productivity and economic

growth for this economy. 2 This is surprising as there is an increasing amount of

literature which studies China’s high technology sectors, such as telecommunications,

the computer industry and Internet.

The aim of this dissertation is to examine the relationship between ICT and

China’s economic growth over the past two decades, and thus contribute to the literature.

Since the 1990s, China’s economy has been increasingly stimulated through

development in its ICT sector. Most significantly, China has in recent years become one

of the world’s largest ICT markets and production centres. ICT is therefore expected to

be a crucial driving force for China’s economic growth in the 21st century. In fact,

China today is even looked upon as ‘a leader in technology and innovation’, or a

‘telecommunications superpower’ as recognized by the International

Telecommunications Union (Conan, 2005; Low and Johnston, 2005). In a country

where ICT investment is growing at twice the rate of national output, it would be

interesting to look at the impact of ICT on China’s economy over the past two decades.

1 Based on gross domestic product (GDP) data obtained from China Statistical Abstract 2006. 2 The terms, ICT and IT (information technology), have been used interchangeably in the literature. In general, American scholars use IT in their literature. They include, among others, Brynjolfsson (2003), Dedrick, Gurbaxani and Kraemer (2003), Jorgenson, Ho and Stiroh (2003, 2005), Oliner and Sichel (2000, 2003), and Shao and Lin (2001, 2002); whereas European (and OECD) scholars tend to use ICT. Examples include Atzeni and Carboni (2006), Becchetti, Bedoya and Paganetto (2003), Colecchia and Schreyer (2002), Edquist (2005), Fabiani, Schivardi and Trento (2005), Inklaar, O’Mahony and Timmer (2003), Katsuno (2005), OECD (2004), Oulton and Srinivason (2005), Pohjola (2003) and Susiluoto (2003). Chinese scholars have used ‘ICT’ in recent literature, including Jing (2006), and Meng and Li (2002).

1

1.1 Background

The general impacts of ICT on the economy can be outlined as follows (OECD, 2004).

First, countries that have a strong ICT-production sector such as the US and Finland

tend to enjoy comparative advantage over those with a weaker ICT sector by generating

technological innovation and creating high demand in their economies. The same goes

for countries that have a strong ICT-using service sector as well. Second, ICT

investment contributes to increased ‘capital deepening’, that is, more capital input per

worker, which leads to improved productive efficiency and therefore increases

productivity. Third, the use of ICT produces networking externalities, meaning that the

resulting greater interaction between firms and their customers or other agents will

improve firm performance and increase total factor productivity (TFP) throughout the

economy. In this respect, ICT capital plays a very significant role in the production

process and should be treated as an individual factor input in growth accounting

methods.

The positive relationship between ICT and productivity in developed economies

is well documented, and this applies to developing countries as well.3 Indeed, there is a

consensus of ICT being a key driver of productivity growth. In particular, the revival of

productivity growth in the US since the mid-1990s has been attributed to the

acceleration in average labour productivity (ALP) and total factor productivity (TFP)

growth, driven by the semiconductor industry (Jorgenson, 2001). However, while the

explosive growth of ICT investment and its rising contribution to GDP and labour

productivity growth in the advanced economies has already been extensively

researched, there has been little research on China, despite the giant developing

economy having one of the world’s largest ICT markets and a rapidly growing ICT

infrastructure. OECD (2004) has also acknowledged that there is a lack of research on a

single developing country which can challenge the findings in the current literature that

‘the contribution of ICT to economic growth in developing countries has been minimal’.

My research therefore aims to develop a framework for interpreting China’s economic

growth by examining the neoclassical growth theories with a special emphasis on ICT

as a factor in economic growth.

3 A review of theoretical literature with respect to this issue is discussed in Chapter 3, while empirical evidence gathered in studies of various countries is discussed in Chapter 4.

2

1.2 Objectives and contributions

The main objective of my dissertation is to examine the role of ICT in China’s

productivity and economic growth. First, it aims to present a review of the existing

literature analysing the effect of ICT on productivity and economic growth. Second, it

applies the conventional growth accounting method to assess the impact of ICT on

China’s economy. Finally, the empirical results provide a comprehensive analysis of the

sources of China’s economic growth during a period of rapid ICT development.

The dissertation will make the following contributions to the existing literature.

Its contribution to academia involves mainly the findings generated from the method

applied. One major contribution of the dissertation is the estimation of an ICT capital

stock series for China from the mid-1980s to the first few years of this century, using

various methods of estimation and assumed rates of depreciation, which is not found

anywhere in the literature. The attempt to estimate the size of ICT capital stock in China

will be an addition to current literature. These estimates are based on a consistent set of

data that can be obtained from the statistical sources available.

Next, based on the ICT capital stock series derived from ICT investment, the

dissertation will adopt a production function that segregates the contribution of ICT

capital to economic growth from that of other forms of capital. The impact of ICT on

China’s economic growth will be analysed at two levels. First, the contribution of ICT

capital to economic growth is examined at the national level. The empirical results

obtained from this exercise are also compared with those found in current literature,

which is still very scant.4 Second, the effect of ICT on technical efficiency is examined

at the provincial/regional level by using a stochastic production frontier model.

Finally, the dissertation attempts to estimate the demand functions for ICT usage

(namely, demand for telecommunications services and computers) and project the

growth of the ICT market in China for the next five years. Just like the literature

examining ICT contributions to growth, very few studies have attempted to estimate the

demand for telecommunications and computer markets in China. The dissertation will

4 As will be noted in chapter 4, there are currently only two empirical papers that examined the contribution of ICT capital to China’s economic growth.

3

estimate the elasticity of demand for ICT with respect to price and income, which can

be compared with findings using data from other parts of the world.

1.3 Outline of the chapters

The dissertation is broadly divided into three major sections, dealing with descriptive,

theoretical and empirical discussions. The descriptive section provides an introductory

background of the concept of ICT and an overview of ICT development in China

(Chapters 1 and 2). The theoretical section embarks on a review of current and recent

literature presenting debates concerning the relationship between ICT and economic

growth, as well as empirical evidence from various countries or regions around the

world (Chapters 3 and 4). The empirical section is focused mainly on analysis of the

role of ICT in China’s economy using data obtained from Chinese statistical sources

(Chapters 5 to 8). Finally, the thesis rounds up with a concluding chapter that

summarises the empirical findings and discusses growth prospects for the Chinese ICT

sector in the near future.

Chapter 2 provides an account of the development of the ICT industry in China

and a review of the science and technology (S&T) programs that have been

implemented to promote the development of this sector. It first defines what the term

‘ICT’ encompasses, and provides an overview of the ICT market in China. Next, the

chapter outlines the development of the telecommunications industry in China, followed

by a background review of the computer industry, which is made up of the hardware

and software sectors. Finally, the chapter provides an account and review of the major

policies that have been implemented to promote the development of science and

technology (S&T) in China.

Chapter 3 presents a review of the conceptual debates and measurement issues

associated with ICT, productivity and economic growth. The chapter will explore how

investment in ICT affects productivity at the firm, industry and country level. It begins

with an outline of evidence that shows how increasing ICT investment, especially in the

US and other developed countries has resulted in the recent revival of productivity

growth in these countries. Besides those supporting the positive link between ICT and

productivity, there are studies that question the real impact of ICT on productivity. This

is followed by a discussion of the theoretical frameworks used to measure the

4

contribution of ICT to labour productivity and economic growth, where ICT capital is

distinguished from other factor inputs in the growth accounting exercises.

Chapter 4 continues to review the empirical literature on the contribution of ICT

to economic growth. While current literature focuses mainly on empirical survey in the

developed countries, there is only a handful of research work that examines the

developing countries, including China. The empirical results for various countries are

then presented to illustrate the differing contribution of ICT capital among the

economies.

Chapter 5 is the starting point for empirical exercises in the dissertation. It aims

to estimate the ICT capital stock series in China using the perpetual inventory method.

The estimates are based on data of investment in telecommunications and computer

equipment for the period of 1983 to 2004. This will involve, first, estimating the initial

value of ICT capital stock in 1983, and second, estimating the capital stock series

assuming certain rates of depreciation throughout the entire period. The chapter will

conclude with a sensitivity analysis of capital stock estimation using different rates of

depreciation. The ICT capital stock series generated will be used for empirical exercises

in the subsequent chapters.

Chapter 6 focuses on assessing the contribution of ICT capital as a production

factor to economic growth in China. This chapter will add to the literature by focusing

on China, using the estimates of ICT capital stock series obtained in Chapter 5. This

chapter comprises three main parts. First, it describes the relationship between ICT,

productivity and economic growth in China by comparing the pattern of growth in ICT

capital and labour productivity during the past twenty years or so. Second, the chapter

attempts to specify an appropriate model to examine the contribution of ICT and other

factor inputs to economic growth in China. Finally, the chapter will test the robustness

of the model by comparing empirical results based on different estimates of the ICT

capital stock. Conclusions will then be drawn about the role of ICT in China’s economic

growth over the past two decades.

Chapter 7 seeks to estimate the regional ICT capital stock and to examine the

impact of ICT capital on technical efficiency in China’s regions. It contributes to the

literature by looking at the pattern of disparity in ICT investments in China. It will

5

provide a background review of how the pattern of regional disparity in China has

changed as far as ICT investment is concerned. The chapter attempts to look at the

impact of ICT on regional growth and technical efficiency in China. No previous work

in this area has been reported.

Chapter 8 looks at the demand side of the ICT industry by estimating demand

functions for ICT services in China. Specifically, this chapter attempts to estimate a

demand function for the telecommunications and computer markets in China,

respectively. It has two main objectives: first, to estimate the demand elasticity of ICT

services and compare them with those of other countries; second, to project demand for

ICT services in the near future till 2010. It contributes to current literature that has

largely focused on the supply-side growth accounting and hence the contribution of ICT

capital/investment to economic and labour productivity growth.

Finally, the dissertation concludes with a discussion of outlook and growth

prospects for the Chinese ICT industry in the near future. The chapter first summarises

the empirical findings from the previous chapters. It will next discuss the direction of

growth for the ICT sector after the first few years of accession into WTO whereby

China is expected to fulfil its entry commitments, and conclude by highlighting some

important areas where growth will be focused on.

6

Chapter 2

DEVELOPMENT OF THE ICT SECTOR

This chapter provides an overview of the development of the information and

communications technology (ICT) sector in China. It outlines the historical

development as well as government policies introduced to encourage and promote

development of this sector. The chapter begins by looking at various definitions of the

term ‘ICT’ used in current literature and provides an assessment of the ICT market in

China. This is followed by an outline of the development of the telecommunications

industry in China and a background review of the computer industry, which is made up

of the hardware and software sectors. Finally, the chapter presents a review of the major

policies that have been implemented to promote the development of science and

technology (S&T) in China. The latter is vital to the development of the ICT sector.

2.1 Definitions of ICT

In most literature, the term ICT is used interchangeably with information technology

(IT) although slight variations exist. ICT is broadly defined in the literature to include

the telecommunications, computer hardware and software sectors. According to the

Information Technology Agreement (ITA) of the World Trade Organization (WTO), IT

includes telecommunications equipment, computers and semiconductors. 1 The ICT

sector was defined by the OECD in 1998 as ‘the combination of manufacturing and

service industries that capture, transmit, and display data and information electronically’

(Jing, 2006). Similarly, ICT is divided into three broad categories according to its use,

namely, computing, communication as well as the transmission of data and

communication via Internet (Quibria et al., 2003).

In the empirical literature, the term ‘IT’ investment generally covers ‘computer

hardware, software and communications equipment’ (Shinjo and Zhang, 2003;

Miyagawa et al., 2004; Timmer and van Ark, 2005). Miyagawa et al. (2004) included a

range of communications and electronic equipment in their definition of ‘IT capital

goods’, such as telecommunications systems, radio, consumer electronic equipment as 1 Following the conclusion of the Ministerial Declaration on Trade in Information Technology Products at the Singapore Ministerial Conference in December 1996, the ITA entered into force with the first stage of reduction in tariffs for IT products that took place on 1 July 1997. See WTO website, http://www.wto.org/English/tratop_e/inftec_e/itaintro_e.htm.

7

well as electrical and optical instruments. In another study of the Japanese economy,

Jorgenson and Motohashi (2005) defined ‘IT investment’ in accordance to the Japanese

national accounts, which consists of computer equipment (including computer

peripherals), and communications equipment (including television and radio, video, and

cable and wireless communications devices). However, Timmer and van Ark (2005)

used the term ‘ICT investment’ to include computers, communications equipment

(which comprises radio, TV, telecommunications and photocopiers) and software. In

examining the role of ICT in Australia’s economy, Diewert and Lawrence (2005)

defined ICT capital to consist of computers, software and electrical machinery.

In China, the ICT industries defined above are encompassed in the term

‘electronic industry’, used by the Ministry of Information Industry (MII) and in official

statistical publications, which also includes electronic consumer goods such as

televisions and radio. Time series data that is available from statistical sources

published by MII are investment in the ICT manufacturing sector. As listed in Katsuno

(2005), the ICT sector covers the following category of products – telecommunications

equipment, broadcasting equipment, computer equipment and software, household

electronics, electronic measuring instruments, electronic devices, electronic parts and

equipment, and other materials used for the production of electronics. The computer

sector is further comprised of personal computers (PCs), PC peripherals (such as disk

drives and printer), PC parts (such as motherboard, memory card, power supply units

and other parts), as well as software (consists of operating system, intermediate and

application software). Based on the data available from Chinese statistical sources, the

ICT sector to be discussed in this dissertation covers the telecommunications (excluding

broadcasting equipment and household electronics) and computer sectors (including

software).

2.2 The telecommunications industry

This section provides an overview of development of telecommunications policy in

China by examining how telecommunications policies have changed since the

beginning of economic reform to meet changes in market demand and the need to open

up the telecommunications market to foreign competition. The main focus of this

section is on developments in the Chinese telecommunications industry after entry into

the WTO, as current literature covering developments during the reform period is

8

already substantial (Loo, 2004; Lu, 2000a; Lu and Wong, 2003; Mueller and Tan, 1997;

Wong, 2002). Finally, the section rounds up with an overview of the growth of the

telecommunications market in China, using the most recent statistical data available.

2.2.1 The monopoly era (1949-1994)

The historical development and changing policies of the telecommunications industry in

China have been evaluated by several authors in the recent literature. An account of the

achievements up to the late 1990s is covered in detail by Lu (2000a) and Wong (2002).

These studies began with the formation of the Ministry of Posts and

Telecommunications (MPT) on 27 September 1949, stretching through the Cultural

Revolution (1966-76) and beginning of reform till the end of the 1990s. Other authors

have examined the evolution of China’s telecommunications policy in response to

changing market demands, bureaucratic reform and negotiations for entry into the WTO

(Mueller and Tan, 1997; Lu and Wong, 2003). As such, this dissertation will only

provide a brief outline of changes in China’s telecommunications policy with materials

drawn from the more recent studies.2

Loo (2004) analysed the changing telecommunications policies in China since

the opening by breaking the period of study into four stages – pre-1994, 1994-97, 1998-

99 and 2000 onwards, each period reflecting the change in the way different forces were

influencing telecommunications development. During the 1980s, the primary goal of the

MPT was the provision of universal service of fixed line telephones to the population at

large (Loo, 2004). The MPT enjoyed an almost exclusive monopoly of the public

telecommunications network, with other private and independent networks maintained

by some powerful governmental bodies, such as the Ministry of Railway (MOR), the

Chinese Academy of Sciences (CAS) and the State Education Commission (SEC).

Telecommunications was made a strategic priority during the Seventh Five-Year Plan

(1986-2000) when China placed emphasis on high technology as a means to speed up

telecom development. It was in 1987 that the mobile phone first came into use when

China began its utilization of cellular technology with the analogue TACS (Total

Access Communications System) (Wong, 2002).

2 The main focus will be on the recent developments related to new technologies in the few years after accession into WTO (in section 2.2.3 of this dissertation).

9

China entered the Information Age only in 1994 following a breakthrough in

Sino-American talks concerning the connection of the Chinese network with the

Internet in April of that year (Loo, 2004). Prior to this development, the first computer

networking activities in China took place when CAnet (China Academic Network) was

successfully established on September 20, 1987 between the Institute for Computer

Applications (ICA) in Beijing and Karlsruhe University in Germany.3 Subsequently,

Internet access was extended to the research community from CAS and the universities

in Beijing, Chengdu, Shijiazhuang, Shanghai and Nanjing, following the completion of

the China Research Network (CRN) in May 1989 (Tan, Mueller and Foster, 1997; Loo,

2004). The implementation of the Golden Bridge Project in March 1993 was a further

step initiated by the central government to develop an advanced telecommunications

infrastructure throughout China.4 It can thus be seen that up till the mid-1990s, the

development of the Chinese telecommunications industry was largely led by state

initiatives.

2.2.2 Telecommunications reform and policies

During the second half of the 1990s, the evolution of China’s telecommunications

reform and policies could be seen as a result of the interplay between foreign pressure,

market forces brought about by increased demand and the ‘power tussle’ between

various ministries and government bodies. The Chinese central government hopped

onto the bandwagon of worldwide liberalization of the telecommunications industry by

breaking the monopoly of the MPT and establishing new players in their domestic field.

A major milestone in the history of Chinese telecommunications took place in July 1994

when the MPT was renamed as China Telecommunications Corporation (China

Telecom) and at the same time, a new firm, China United Telecommunications (China

Unicom) was set up to bring in competition to the incumbent monopoly.5 However,

competition did not truly exist as China Telecom still owned the only fixed line network

in China, while China Unicom had a restricted share of the mobile services – less than

5% at the end of 1999 (Wong, 2002). Nevertheless, this was a sign of mounting foreign

3 China Internet Network Information Center (CNNIC), http://www.cnnic.net.cn/en/index/0O/ index.htm. For more details of the origin of China’s Internet connection, refer to “How China was Connected to the International Computer Networks”, Willkommen, http://www-ks.hpi.uni-potsdam.de/ index.php?id=76. 4 The Golden Bridge Project is the first of several “Golden Projects” that have been implemented to modernize the ICT infrastructure in China. Refer to section 2.4 of this chapter for further details. 5 China Unicom was established as a joint venture between the Ministry of Electronics Industry (MEI), the Ministry of Electrical Power (MEP), the Ministry of Railway (MOR) and thirteen autonomous state-owned enterprises (Lu and Wong, 2003).

10

pressure together with surging domestic demand to open up the monopolistic Chinese

telecommunications industry to competition.

Rising market demand has also prompted a rapid expansion of the Internet

infrastructure, which consisted of: the China Science and Technology Network

(CSTNet) which began construction in 1989 and was connected to the global Internet

network in 1994; the ChinaNet which is the primary nationwide commercial network

run by China Telecom and was completed in January 1996; the China Education and

Research Network (CERNet) which provided network connection to academic

institutions in China by October 1994; and the Golden Bridge Network (GBNet) which

was operated by Jitong Communications and completed in 1996.6

The influence of foreign pressure became more visible towards the end of the

1990s as China sought entry into the WTO. As it became apparent that membership into

the world body would not be realised unless the telecommunications industry was

unlocked to foreign investment, the Chinese government took the first step towards

opening up through ministerial restructuring in March 1998 by merging the MPT and

Ministry of Electronic Industry (MEI) to form the Ministry of Information Industry

(MII), which became the ‘super-authority’ overseeing the ICT industry in China.

The following three years (1999-2001) saw an influx of new competitors,

although only in small numbers. First, China Netcom (CNC) was established in April

1999 as the fourth telecommunications operator in China, for the construction of a

broadband Internet Protocol (IP) network (CNCNet). A major restructuring of China

Telecom took place when its code division multiple access (CDMA) Great Wall

Network and Guoxin Paging branch were merged with China Unicom, in which the

incumbent still retained the local fixed line network. The next player to enter the

telecommunications field was China Railway Telecommunications Corporation (China

Railcom) in June 1999. China Railcom had its own exclusive communications network,

6 Other networks include the China Uninet (launched by China Unicom in July 2000), the CNCnet (launched by China Netcom in December 2005), the China International Economy and Trade Net (CIETNet), the CMNet (provided by China Mobile), the China Great Wall Net (Cgwnet), the China Satellite Net (CSNet) and the China Next Generation Internet (CNGI) which is a five-year plan initiated for the implementation of IPv6 (Internet Protocol version 6), scheduled for showcase at the 2008 Olympic Games in Beijing. See China Internet Network Information Center (CNNIC), 10th - 18th Statistical Survey Report on the Internet Development in China (July 2002 - July 2006), http://www.cnnic.net.cn/en/index/0O/index.htm.

11

and was subsequently granted a license to provide the fixed line, Internet and IP

telephony services in 2001 (Lu and Wong, 2003).

Further restructuring of the Chinese telecommunications industry occurred with

the ‘second divestiture’ (a term coined by Lu and Wong, 2003) of China Telecom in

December 2001, almost immediately after the entry of China into the WTO. China

Telecom was restructured geographically when it was to operate only the network of 21

provinces in south China and the western autonomous regions, with the remaining 10

provinces in north China to be taken over by the merger of China Netcom and Jitong

Communications. Finally, the most recent player to join the ‘telecom league’, China

Satellite Communications Corporation (China Satcom), was formed in December 2001,

through the merger of satellite-based telecommunications companies such as China

Telecommunications Broadcast Satellite Corporation, China Orient Telecom, China

Space Mobile Satellite and ChinaSat of China Telecom (Hong Kong) (Lu and Wong,

2003).

Despite rising demand for further deregulation and calls for foreign competition,

the telecommunications field in China still remain almost ‘exclusively Chinese’, over

which the State has majority ownership and control. As of 2006, there are six telecom

operators in China, namely, China Telecom and China Netcom (operating the fixed-line

network), China Mobile and China Unicom (mobile network), China Railcom and

China Satcom.

2.2.3 Telecommunications developments after WTO

This final section examines how further developments in the telecommunications

industry in China after entry into WTO are driven by new technologies. The most recent

developments in the Chinese telecom field are mainly related to the deployment of 3G

(third generation) mobile standards. Currently, among the four leading

telecommunications network operators in China, the mobile carriers, namely China

Mobile and China Unicom, are providing 2G (second generation) and 2.5G mobile

services (i.e. GSM and CDMA) respectively; whereas the fixed-line carriers, China

Telecom and China Netcom, are providing an alternative form of wireless service

known as Xiaolingtong (meaning ‘little smart’ in Mandarin) with limited geographical

12

coverage (Yuan et al., 2006).7 As convergence between the telecommunications and

traditional information technology industries takes shape, the Chinese government and

enterprises alike now recognise the increasingly significant role of 3G technologies in

the race to boost competitiveness.

One of the major breakthroughs in the history of China’s telecommunications

industry occurred when a leading Chinese telecom equipment manufacturer, Datang

Technology8, together with Siemens of Germany, developed the Chinese 3G standard

known as Time Division-Synchronous Code Division Multiple Access (TD-SCDMA),

which was approved by the International Telecommunications Union (ITU) in May

2000 as one of the internationally-accepted 3G mobile communications standards,

rivalling W-CDMA (Wideband CDMA) adopted by Europe and CDMA2000 used in

the US, Japan and Korea. 9 However, it was only in October 2002 that Datang

Technologies obtained support from the Chinese government when the MII announced

an allocation of 155MHz of Time Division Duplex (TDD) resource to TD-SCDMA;

and at the following week, seven telecommunications equipment manufactures –

namely, Datang Technology, Huawei Technology, Huali Group, Southern Hitech,

Shenzhen Zhongxin Technology (ZTE), China Electronics Group and China PuTian

Group, formed the ‘TD-SCDMA Industrial Alliance’ with support from three

government agencies – the State Planning Commission, the MII and the National

Science and Technology Department (Fan, 2006).10

Another significant milestone in Chinese telecommunications development is

exemplified in the achievements of another domestic telecom equipment manufacturer,

Huawei Technology which was established in 1988. After launching its first GSM

7 ‘GSM’ stands for ‘Global System for Mobile Communications’ and ‘CDMA’ stands for ‘Code Division Multiple Access’. Xiaolingtong is based on the Personal Handy Phone System (PHS) technology which originated in Japan in 1995. For more details on a description of the Xiaolingtong technology, refer to Yuan et al. (2006). 8 Datang Telecom Technology Corporation (DTT) was established in the Haidian district of Beijing on September 21, 1998. It is a leading communications equipment manufacturer and provider of a wide range of telecommunications services in China. See DTT website, http://www.datang.com/. 9 “PacificNet Announces 3G Strategy at ITU Telecom World 2006”, TMCnet (December 6, 2006), http://www.tmcnet.com/usubmit/2006/12/06/2148540.htm. 10 The delay in announcement of support from MII was attributed to the fact that TD-SCDMA had less support and R&D investment compared with the other standards, WCDMA and CDMA2000 which are favoured by China Mobile and China Unicom respectively. WCDMA is also supported by major multinational companies such as NTT DoCoMo of Japan, and Ericsson and Nokia of Europe; while CDMA2000 is mainly supported by North American and Korean companies, including Qualcomm, Nortel Networks, Motorola and Samsung. Leading Chinese companies such as Huawei and ZTE have invested in WCDMA and CDMA2000 respectively. For more details, see Fan (2006).

13

equipment in 1997, the company started R&D investment in 3G, i.e. WCDMA in 1998.

In 2002, Huawei established the first 3G Open Lab with NEC in China and introduced

WCDMA core network equipment based on soft switches at ITU (Fan, 2006). Two

years later, Huawei established a joint venture with Siemens to develop the TD-

SCDMA mobile communications technology to serve the Chinese market.11 Adding

further glory to its record of achievements to date, the company obtained three awards

at the 2006 Frost & Sullivan Asia Pacific ICT Awards – namely, ‘2006 Vendor of the

Year’, ‘2006 Optical Vendor of the Year’ and ‘2006 Broadband Equipment Vendor of

the Year’.12

In anticipation of such a trend towards greater application of 3G technology in

the future, nine leading Chinese telecom institutions, namely, the telecom operators –

China Telecom, China Mobile, China Unicom and China Netcom; equipment providers

– Huawei Technologies, ZTE Corporation, Putian Corporation and Vimicro Corporation;

and a research institute – the China Academy of Telecommunication Research of the

MII, formed a mobile multimedia technology alliance (MMTA) in October 2004. The

MMTA alliance will serve to ‘boost technical innovation and development of standards

and applications in the booming mobile multimedia industry, and thereby boosting the

competitiveness of Chinese enterprises in applying upcoming 3G technologies’ (Xiao,

2004).

The key lies in greater co-operation among the Chinese enterprises if they are to

grab a larger market share facing tense competition with international rivals. The mobile

communication multimedia represented by 3G service is expected to attract newcomers

into the industry, with an increasingly wider range of services coming onto the scene,

including the mobile game services, mobile photo services, mobile colour message

services, mobile short message services as well as other existing services (Xiao, 2004).

The latest sign of the ambition by Chinese companies to expand their influence into the

international telecommunications field took place in May 2006, with China Mobile

signing a US$5.3 billion deal to acquire (its first ever overseas acquisition) Millicom

International Cellular SA of Luxembourg, which operates mobile services in 16

countries (Singer and Dean, 2006). 11 Huawei website, http://www.huawei.com/. 12 Frost & Sullivan is a global consulting company for emerging high technology and industrial markets. Huawei had also been awarded “Vendor of the Year” in 2005 based on its strong performance such as revenue growth, new customer wins and innovative strategy. See “Huawei Technologies Bags Three Awards at the 2006 Frost & Sullivan Asia Pacific ICT Awards”, M2 Presswire (Coventry: June 19, 2006).

14

Yet, despite the hype about the competitive advantages that 3G will bring, it

took almost six years since the recognition by ITU in 2000 for an official announcement

from the Chinese authorities concerning the long-awaited issue of 3G licences to the

leading telecommunications operators in the country. On January 20, 2006, the MII

formally announced TD-SCDMA to be the country’s standard of 3G mobile

communications.13 The Chinese government has taken a cautious approach to this issue

as it has invested heavily in developing TD-SCDMA technology, spending about 55

billion yuan (US$6.63 billion) in 2005. It is estimated that more than one trillion yuan

would have to be spent on building the 3G network alone if all the four leading Chinese

telecommunications operators were to be awarded with 3G licenses (Yuan et al., 2006).

Nevertheless, it was a significant development when the nation’s two largest

fixed-line operators, China Telecom and China Netcom, were licensed by the MII in

May 2006 to obtain the number segment prefixed with 188 and 189 respectively in their

test 3G networks in the northern city of Baoding and eastern city of Qingdao. In

addition, China Mobile and China Unicom have already been permitted to use numbers

prefixed with 159 and 153 respectively in the southwestern municipality of Chongqing,

beginning in June 2006.14

The ‘big news’ eventually came when MII Minister, Wang Xudong, seizing the

opportunity at the ITU Telecom World 200615, announced that China would issue 3G

licenses ‘very soon’, and assured that it would be on time for operators to ‘offer 3G

services during the 2008 Olympic Games in Beijing’.16 The 3G licenses are expected to

be issued no later than the first quarter of 2007 to ensure 3G networks to be operational

before the Games begin (Perez, 2006). China Mobile has been reported to be planning

the operation of the TD-SCDMA network in Beijing and Qingdao, before implementing

it in the provincial capitals of the coastal areas and finally in the inland provincial

capitals.17

13 “PacificNet Announces 3G Strategy at ITU Telecom World 2006”, TMCnet (December 6, 2006), http://www.tmcnet.com/usubmit/2006/12/06/2148540.htm. 14 “China Telecom, China Netcom obtain 3G number segment”, SinoCast China Business Daily News (London: May 10, 2006).

15 Held on 4-8 December, 2006, at AsiaWorld-Expo, Hong Kong, China, http://www.itu.int/WORLD2006/ 16 “PacificNet Announces 3G Strategy at ITU Telecom World 2006”, TMCnet (December 6, 2006), http://www.tmcnet.com/usubmit/2006/12/06/2148540.htm. 17 “China Mobile prepares for TD-SCDMA”, SinoCast China Business Daily News (London: January 2, 2007).

15

Finally, the growth of China’s telecommunications can be further boosted by

tapping on the resources of foreign companies. In this respect, the Chinese government

has taken a proactive approach when the National Development and Reform

Commission (NDRC) signed a deal with SK Telecom, the leading provider of mobile

communications services in Korea, in August 2006, to develop the TD-SCDMA for 3G

mobile telecom by setting up a joint centre for research in China. The agreement was

followed up with the joint construction of a TD laboratory between the Korean

company and Datang Technology, with the possibility of ZTE Corporation joining the

partnership to build the first trial TD-SCDMA network in the first quarter of 2007.18

The Chinese telecommunications market received an added boost with news of a

merger between Lucent Technologies of the US and Alcatel of France on November 30,

2006, both of which have strong ties to Datang Technology.19 The former had signed a

deal for TD-SCDMA in November 2005, while the latter had signed a Memorandum of

Understanding (MOU) with the Chinese company in November 2006 (before the

merger) which will reinforce its commitment to invest in the development of TD-

SCDMA in China.20

2.3 The computer industry

This section traces the development of computer hardware and software in China. In

particular, it explores the various government-led policies implemented to foster

development in the computer industry as well as the shift in the focus of policies in

18 “SK Telecom, Chinese government sign 3G services deal”, Asia Pacific Telecom 10 (10), October 2006; “Datang to build 1st TD network in South Korea”, USITO website, http://www.usito.org/news_dl.php?id=76. 19 Based in Paris, Alcatel-Lucent will have the combined revenue of approximately Euro €21.3 billion (US$28 billion) with 79,000 employees in more than 130 countries. With the merger, the company has a global leading position in a wide spectrum of ICT services, such as Internet Protocol (IP) television, broadband access, carrier IP and 3G technologies, including CDMA2000, WCDMA and TD-SCDMA. See Alcatel-Lucent website, http://www.alcatel-lucent.com/. 20 Alcatel and Datang first signed an agreement to invest in TD-SCDMA two years earlier, in November 2004. It is also estimated that the former Lucent had invested a total of US$2.9 billion in China between 1995 and 2005, while the former Alcatel invested more than US$1 billion in the mainland in 2005 alone. See “Lucent Takes IMS (IP Multimedia Subsystem) to China”, Light Reading (November 16, 2005), http://www.lightreading.com/document.asp?doc_id=84416; “Alcatel and Datang Group to advance TD-SCDMA development”, Premium mobile technologies (November 30, 2006), http://premium-mobile.com/content/alcatel-and-datang-group-to-advance-td-scdma-development/. “Alcatel-Lucent to boost mainland investment: Communications giant will concentrate on the enterprise market in China”, South China Morning Post (Hong Kong: December 5, 2006).

16

17

recent years in adaptation to changing consumer demands and the competitive

environment.

2.3.1 Development of the hardware industry

China is now the world’s second largest PC (personal computer) maker and is expected

to become the world’s largest by 2010 (Kshetri, 2005). The production of PC in China

has jumped almost 100 times since 1995, from less than one million units in that year to

80 million in 2005 (Figure 2.1). This is an amazing achievement, considering the fact

that China had only 500,000 PCs for more than 1.2 billion people in 1990 (Kraemer and

Dedrick, 2002b). The sales of Chinese PC (including desktops and laptops) grew

annually by about 15% between 2002 and 2004.21 In 2004, the desktop and laptop PCs

accounted for 88% and 12% of the Chinese PC market respectively. The market was

dominated by the largest domestic firm, Lenovo Group Ltd, holding 25% of the market

share. The largest shares held by foreign companies were Dell Inc. and IBM

Corporation, holding about 7% and 5% respectively (Table 2.1).

There has been less discussion on the history of the computer hardware industry

in China compared with that of the telecoms industry. The development of the computer

industry had been a priority in the agenda of the science and technology development

policies since 1955. An overview of the historical development of computers in China

has been discussed in Witzell and Smith (1989). The history of China’s computer

industry could be said to begin with the founding of its first national computer research

institution, the Institute of Computing Technology within the Chinese Academy of

Sciences (CAS) in 1956.22 With assistance from the Soviet Union, in August 1958, the

CAS Institute built the first generation of computers in China, known as Model 103.23

Such assistance was however ended in 1960 which rendered China with only the ‘self

reliance’ path (Lu, 2000b).

The Cultural Revolution of 1966-76 disrupted the development of the national

economy as well as the computer industry. Yet surprisingly, China seemingly was

closing the gap in computer achievements with the Soviet Union. For instance, by 1977,

the CAS Institute developed the model 013, ‘a third generation computer capable of 2

21 “China PCs 2005”, Snapshots International, March 2005. 22 The Institute of Computing Technology will be referred hereafter as ‘CAS Institute’. 23 Institute of Computing Technology website, http://www.ict.ac.cn/.

0

10

20

30

40

50

60

70

80

90

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Mill

ion

units

-40

-20

0

20

40

60

80

100

120

140

%

PC (million)Growth rate (%)

Figure 2.1 Production of PCs in China, 1990-2005

18

Source: State Statistical Bureau, China Statistical Abstract 2006, Beijing.

million ops compared with the 1976 RIAD 1060 of the Soviet Union which was only

capable of 1.5 million ops’, the reason being that the Soviet Union ‘chose to concentrate

on producing R&D computers for military use’ (Witzell and Smith, 1989: 37). Yet, in

spite of the disruptions caused by the Cultural Revolution, the computer industry

seemed to overcome the economic turmoil with impressive achievements, as reported

by Witzell and Smith (1989: 41) and listed in Appendix 2.1.

Table 2.1 Market shares of China’s PCs (%) Company 2004 Lenovo Group Ltd Founder Electronics Co. Tsinghua Dongfang Co. Ltd Dell Inc. IBM Corporation Hewlett-Packard Co. Others Total

25.1 9.9 7.8 7.2 5.1 4.8 40.1 100

Source: “China PCs 2005”, Snapshots International, March 2005.

During the pre-reform era, computers in China were not produced for

commercial use until 1973. Computer models developed by various ministries and

universities were used mainly for military and scientific purposes such as developing

the atomic bomb, satellites and weather-forecasting models (Lu, 2000b). As China

sought to revive its economy from the shocks of the Cultural Revolution, the Chinese

government laid out the ‘Four Modernizations’ – Agriculture, Defence, Industry, and

Science and Technology, as the pillars of national economic revival and development.

Consequently, a National Plan for the Development of Science and Technology (1978-

85) emerged at the National Science Conference on March 18, 1978, where Fang Yi (a

member of the Central Committee of the Chinese Communist Party) spoke: ‘The eight-

year outline plan draft gives prominence to the comprehensive science and technology

spheres … agriculture, energy, materials, electronic computers, lasers, space, high

energy physics and genetic engineering.’ Going on further, Fang Yi emphasized that

‘China must make a big new advantage in computer science and technology, and should

lose no time in solving the scientific and technical problems in the production of large

scale integrated circuits (ICs), and make a breakthrough in the technology of ultra-large

scale ICs….. We aim to acquire, by 1985, a comparatively advanced force in research in

computer science and build a fair size modern computer industry… A number of key

19

enterprises will use computers to control the major processes of production and

management’ (Witzell and Smith, 1989: 39).

As economic reform steered the whole country towards a more open and market-

oriented economy, a similar fashion was occurring in the reform of Chinese science and

technology policies that helped further expansion of the computer industry. There was

evident recognition by Chinese leaders from national to local levels of a larger role of

foreign investment and multinational corporations in the development of high

technology in China, thus paving the way for less dependence on government-led

planning initiatives and more on individual innovation and entrepreneurship. China’s

drive to commercialise its computer industry formally began in 1986 with an ambitious

effort to create an electronics industry which was listed as a ‘pillar industry’ for

developing the national economy in accordance with the Seventh Five-Year Plan

(Kraemer and Dedrick, 2002b).

If ‘government involvement’ was the key characteristic defining the

development process during the reform period of the 1980s and early 1990s, then

‘learning’ and ‘innovation’ have been the driving forces behind the rapid growth of the

Chinese computer industry since the 1990s.24 In his study of how indigenous Chinese

computer companies were catching up in the high technology sector, Lu (2000b) noted

that the traditional model of technology transfer which has been used to describe the

export-led technology learning in the East Asian Newly Industrialized Economies

(NIEs) could not explain China’s rapid catch-up in high technology sectors such as

telecommunications equipment and computers. While technology transfer normally

follows a ‘bottom-up’ linear sequence in four stages – cheap labour assembly of

imported kits, original equipment manufacturing (OEM) or the localization of parts and

components, original design manufacturing (ODM) or product redesign, and original

brand manufacturing (OBM) or product design, “learning” assumes ‘top-down’

approach as it could start off at any stage such as product design or redesign.25 Such a

mode of technology learning is also known as “innovation” by definition (Lu, 2000b).

A comparison of China’s experience in developing its computer industry reveals

some similarities as well as differences between them and other developing countries. 24 ‘Learning’ is defined as a process of acquiring the capability to develop technological resources and converting them to commercial uses (Lu, 2000b: 3). 25 The terms ‘OEM’, ‘ODM’ and ‘OBM’ originated from Hobday (1995).

20

China’s policies are said to resemble the developmental approach of Japan and the East

Asian NIEs such as Korea, Taiwan and Singapore with strong support from the

government which combines the promotion of exports to achieve global

competitiveness with strong efforts to develop indigenous technological capabilities

such as building an information infrastructure as well as providing financial and

technical aid to domestic companies (Kraemer and Dedrick, 2002b). In fact, China’s

export-oriented policy turned it into a net computer export for the first time in 1994

when it established export-processing zones and offered tax incentives to attract foreign

investment (Kraemer and Dedrick, 2002b).

However, China’s developmental path differs from other developing countries in

certain ways. First, unlike the East Asian NIEs which rely primarily on export markets,

China enjoys the benefit of having a huge domestic market which ‘provided a stimulus

for indigenous technological innovations for processing Chinese characters in computer

systems’ (Lu, 2000b). China is also different from many developing countries in the fact

that it had established an extensive S&T infrastructure during the central planning era.

The latter enables Chinese companies to tap on both domestic as well as foreign sources

of technology. Finally, and perhaps most importantly, China has been able to attract

foreign investment on terms favourable to the host country – a strategy which is less

successful in many other developing countries. With the lure of their huge market size,

China ‘could exchange market access for foreign technology, by requiring foreign

multinationals to develop joint ventures with domestic companies and allowing

Taiwanese companies to set up production networks in the mainland to support

domestic companies’ (Kraemer and Dedrick, 2002b).

For instance, IBM was unable to penetrate the Chinese PC market until it set up

a joint venture with a domestic company, Great Wall, in 1994 which allowed the latter

access to IBM technology and manufacturing know-how in return for access to local

distribution channels. Other foreign multinationals which have set up joint ventures

include Compaq (with Stone Group), Hewlett-Packard (with Lenovo), Toshiba (with

Tontru) and LG Electronics (with Tontru) (Kraemer and Dedrick, 2002b).

China’s policy to nurture its computer industry is further embodied in the ninth

Five-Year Plan (1996-2000) which emphasized the implementation of several ‘Golden

21

Projects’26 to support the development of ICT and encourage computer use throughout

the country (Kraemer and Dedrick, 2002b). The Plan laid out the following goals:27

• Increase the percentage of domestic components in Chinese-assembled computers and increase

the nation’s capacity to produce peripherals such as monitors, printers, disk drives, add-on cards,

and high-definition displays;

• Achieve a per capita national computer penetration of 1%, and 20% among urban families;

• Develop two to three domestic PC manufacturers into enterprises with an annual production

capacity of more than US$1 billion;

• Apply computer technologies to the renovation of traditional industries;

• Develop uniform PC standards via a production licensing system to answer complaints about

lack of service and intellectual property protection on clone PCs.

Indeed, it was the strategy which focuses on home-grown innovation that

culminated in one of the most astonishing news that rattled across the globe. In

December 2004, for the first time in Chinese and global history of the computer

industry, China’s computer giant Lenovo Group bought over the PC division of IBM for

US$1.25 billion, effectively acquiring the latter’s entire global desktop and laptop

computer R&D and manufacturing business. It was a deal that would turn the Chinese

company into the world’s third largest PC maker with annual revenue exceeding US$10

billion, and accounting for 8% of the world market share.28 On the other hand, IBM will

gradually withdraw from the PC market and focus on the game machine business in

China.29

The turning point for the Chinese computer industry came in September 2002,

when the Institute of Computing Technology (CAS Institute) developed the first ever

Chinese-made CPUs (central processing unit) known as ‘Godson-I’.30 However, the

new developments did not fundamentally alter the structure of the Chinese CPU market

which was still largely dominated by foreign manufacturers. The introduction of

Godson-I did not make any impact in the Chinese market due to limited demand and its

26 See Table 2.5 in this chapter for the list of Golden Projects implemented in China. 27 These points are extracted from Kraemer and Dedrick (2002b). 28 “China’s Lenovo Group acquires IBM’s PC business”, People’s Daily (Beijing: December 8, 2004). 29 “IBM to fade from PC market, quit China PC business”, People’s Daily (Beijing: December 6, 2004). 30 It was designed by Professor Hu Weiwu, a researcher of the CAS Institute who graduated from the University of Science and Technology of China (USTC) in 1991. See “The Chief Designer of the CPU ‘Godson I’ Made his Presentation at His Alma Mater”, USTC website, http://www.ustc.edu.cn/ en/ article/56/42ff2484/.

22

clock speed of 266 MHz failed to meet the minimum requirement of 400 MHz for

procurement by the Beijing government (USITO, 2005).

A new breakthrough occurred a year later with an announcement of Godson-II,

China’s first 64-bit high performance processor which supports the Linux operating

system and X-window system, and it’s the equivalent of Pentium III.31 Compared to the

earlier Godson-I, it has ‘an improved frequency scaling, true 64-bit instruction support,

and significantly reduced power consumption at less than 5 watts for the 500 MHz

model (Richmond, 2003). The introduction of Godson-II increased the market share of

home-grown processors from zero to 1% in 2003 (Table 2.2).

Table 2.2 China’s CPU market, 2001-2004 Market share (%)

Company 2001 2002 2003 2004Intel AMD Via Tech Chinese processors Others

90.05.02.00.03.0

84.0 8.0 3.0 0.0 5.0

83.0 9.5 3.5 1.0 3.0

74.018.0

4.01.03.0

Source: USITO (May 13, 2005).

The story of Chinese processors has not ended though. It was reported in early

2006 that a new type of CPU, the ‘Godson-III’, the equivalent of Pentium IV, was being

developed by a research team at CAS Institute known as the ‘Super Dragon’.32 It did

not take too long for one of the greatest achievements to materialise when the CAS

Institute developed the first Chinese low-cost computer, Longmeng (meaning ‘Dragon

Dream’ in Chinese), having the size of a notebook, which costs only 1,000 yuan

(US$125) which was announced by Zhang Fuxin, a researcher at the institute.33 Using

Red Flag Linux as its operating system, and equipped with a DVD drive and a video

game player, Longmeng is ‘equivalent to a 1G Pentium III desktop’.34 The computer is

marketed for users from low income groups and students in rural areas by the Menglan

Group from Changshu in Jiangsu province. However, it will take a few years to assess

whether there is any impact of the new Chinese processors on their market share

compared to those of major foreign competitors like Intel and AMD.

31 “Chinese-made CPU Chip Equivalent to Pentium III”, China Education and Research Network (Beijing: April 20, 2005), http://www.edu.cn/20050420/3134777.shtml. 32 “Future Super Dragon Super Server”, Zhongguo Wang (China Net) (Beijing: March 4, 2006), http://www.china.org.cn/english/scitech/160125.htm. 33 “China to produce low-cost computers of its own”, China Economic Net (Beijing: March 15, 2006). 34 Ibid.

23

Meanwhile, China has taken great strides in developing its own models of

supercomputers. China had developed the 10-teraflop Dawning 4000A in June 2004 on

its own.35 Later on, when IBM announced its success in developing the 100-teraflop

supercomputer at the end of 2004, the National Research Centre for Intelligent

Computing Systems (NCIC) and the Dawning Company responded with similar

research and had expected to put their 100-teraflop ‘Dawning-5000’ supercomputer

model into use in 2008. 36 Finally, China was also reported to have commenced on a

preliminary research to develop the 1,000-teraflop supercomputers during the 11th Five-

Year Plan (2006-2010), headed by Lenovo Group.37 The key objective of this project,

which started in July 2005, was to develop a supercomputer without dependence from

foreign countries.

2.3.2 Software development

The software market is broadly defined to cover the application and systems software,

as well as the intermediate link software. Presently, it is dominated by the segment of

application software (about 65%), which consists of accounting software, word-

processing packages, anti-virus software and publishing software; followed by platform

software (29%), which includes the operating system (OS) and Linux-based operating

software; and intermediate software (6%).38

In 2005, the Chinese software industry increased its world market share to 3.5%,

exceeding those of India and South Korea.39 Chinese software sales grew annually by

almost 19% between 2000 and 2004. It had increased about six times within a decade

from US$1.1 billion in 1996 to almost US$6 billion in 2004 (Figure 2.2). According to

CCID Consulting, China’s software market is estimated to have reached US$6.8 billion

(56.5 billion yuan) in 2005, climbing to almost US$8 billion (66.1 billion yuan) in mid-

2006, and it’s further forecast to hit more than US$13 billion (110 billion yuan) in 2009,

growing annually at about 18%.40 In 2003, the Chinese software market was dominated

by Microsoft and Ufsoft Co. which had 21% and 17% of the market share respectively.

35 It means the supercomputer system calculates 10 teraflops per second. 36 “China begins preliminary research on 1,000 teraflops supercomputer”, People’s Daily (Beijing: July 22, 2005). 37 Ibid. The US has planned to develop the 1000-teraflop supercomputer in 2010. 38 “China Software 2005”, Snapshots International, March 2005. 39 “China’s Software Industry Sales to reach 1.3 trillion yuan in 2010”, SinoCast China Business Daily News (June 29, 2006). 40 “China Software Industry’s Development Trend and Feature”, China ComputerWorld Research (July 2006), http://www.ccwresearch.com.cn/en/; “China’s Software Industry Sales to reach 1.3 trillion yuan in 2010”, SinoCast China Business Daily News (June 29, 2006).

24

25

The largest shares held by domestic companies were Langchao Group and Beida

Fangzheng Co., at about 15% and 7% respectively (Table 2.3).

Yet, in comparison with its counterpart in India, there are indications that

China's software industry is still at a premature stage in many aspects. Although China