industrial - us investment outlook - jll · pdf file12-month net absorption (as % of...

TRANSCRIPT

United States | H1 2017

Industrial Investment

A focus on value and risk shaping investor behavior

JLL Research

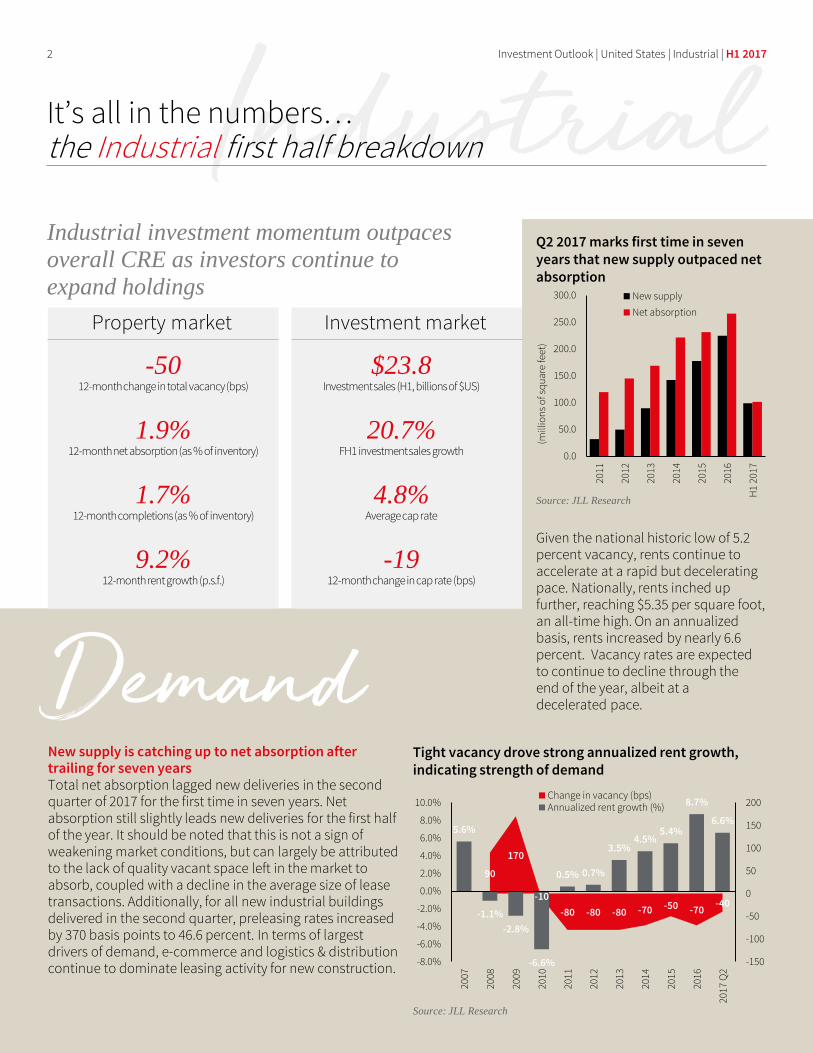

IndustrialProperty market

It’s all in the numbers… the Industrial first half breakdown

Investment Outlook | United States | Industrial | H1 20172

Industrial investment momentum outpaces

overall CRE as investors continue to

expand holdings

-5012-month change in total vacancy (bps)

Source: JLL Research

Tight vacancy drove strong annualized rent growth, indicating strength of demand

1.9%12-month net absorption (as % of inventory)

1.7%12-month completions (as % of inventory)

9.2%12-month rent growth (p.s.f.)

Investment market

$23.8Investment sales (H1, billions of $US)

20.7%FH1 investment sales growth

4.8%Average cap rate

-1912-month change in cap rate (bps)

Given the national historic low of 5.2 percent vacancy, rents continue to accelerate at a rapid but decelerating pace. Nationally, rents inched up further, reaching $5.35 per square foot, an all-time high. On an annualized basis, rents increased by nearly 6.6 percent. Vacancy rates are expected to continue to decline through the end of the year, albeit at a decelerated pace. Demand

New supply is catching up to net absorption after trailing for seven yearsTotal net absorption lagged new deliveries in the second quarter of 2017 for the first time in seven years. Net absorption still slightly leads new deliveries for the first half of the year. It should be noted that this is not a sign of weakening market conditions, but can largely be attributed to the lack of quality vacant space left in the market to absorb, coupled with a decline in the average size of lease transactions. Additionally, for all new industrial buildings delivered in the second quarter, preleasing rates increased by 370 basis points to 46.6 percent. In terms of largest drivers of demand, e-commerce and logistics & distribution continue to dominate leasing activity for new construction.

90

170

-10

-80 -80 -80 -70 -50 -70-40

5.6%

-1.1%

-2.8%

-6.6%

0.5% 0.7%

3.5%4.5%

5.4%

8.7%

6.6%

-150

-100

-50

0

50

100

150

200

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Q2

Change in vacancy (bps)Annualized rent growth (%)

Source: JLL Research

Q2 2017 marks first time in seven years that new supply outpaced net absorption

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2011

2012

2013

2014

2015

2016

H1

2017

(mill

ion

s o

f sq

uar

e fe

et)

New supply

Net absorption

The first half of 2017 recorded robust industrial investment volumes, closing with the second-largest first-half tally since 2007 and year-over-year growth of over 20.0 percent. First-half total volume amounted to nearly $24.0 billion, as 245.0 million square feet of industrial assets traded hands, setting expectations that the year is positioned to exceed the $47.8 billion 2016 total and make 2017 second only to 2015 in terms of overall historic activity. Single-asset transactions led sales velocity in the first half, representing 62.5 percent of all activity. However, the second half of the year is expected to experience a resurgence of large-scale portfolio activity after being largely sidelined in 2016.

Large-scale portfolios (transactions over $250.0 million) have already exceeded $3.5 billion in 2017, capped by the $1.07 billion sale of a Cabot industrial portfolio to DRA Advisors, the mixed-asset portfolio sale by TA Realty to Brookfield ($629.4 million) and ElmTree Funds’ 95.0 percent recapitalization by China Life. A new third GLP industrial fund launched in December,and is expected to have a $1.5 billion investment capacity, with a $400.0 million U.S. industrial asset deployment mandate, setting the tone for continued competition as portfolios do come to market.

The second half of 2017 will likely be the most active period in the industrial sector’s history, as +$12.5 billion of large-scale portfolio activity is set to close before the end of the year, not including the estimated $11.6 billion buyout bid for GLP and its U.S. assets led by Hopu Investment Management, Vanke Group and Hillhouse Capital.

TransactionsTop transactions – what’s happening and where

Investment Outlook | United States | Industrial | H1 20173

Another wave of large-scale

industrial portfolio transactions will

lead second-half activity

Notable industrial park transactions, Q2 2017Market Property Buyer Seller Price ($) Size (s.f.) Price (p.s.f.)

Inland Empire Safari Business Center (16 bldgs)

Rexford Industrial REIT

American Realty Advisors / SBCERA

$141,200,000 1,140,000 $124

Philadelphia-C. PA

Capital Business Center (6 bldgs.)

Dermody Properties Woodmont Properties / AEW Capital Management

$76,100,000 1,531,880 $50

Denver The Campus at Longmont (27 bldgs.)

Gibralt Capital Corporation

Goff Capital Partners $69,600,000 1,130,000 $62

Louisville Dixie Industry and Commerce Park (6 bldgs.)

UPS Dixie Real Properties $33,000,000 913,000 $36

Oakland-East Bay

Fremont Business Center (4 bldgs.)

TA Realty Deutsche $32,900,000 192,397 $171

Notable single asset transactions, Q2 2017Market Property Buyer Seller Price ($) Size (s.f.) Price (p.s.f.)

Houston 4762 & 4830 Borusan Rd Pure Industrial REIT Clay Development $63,500,000 996,482 $64Philadelphia-C. PA

1 Ames Dr UPS Dermody Properties $55,000,000 595,000 $92

Atlanta 8095 McLarin Rd Clarion Partners USAA Real Estate $54,725,000 1,044,248 $52South Bay-Silicon Valley

587 Cinnabar St Trammell Crow Co. A & F Properties LLC $51,500,000 201,940 $255

Notable portfolio transactions, Q2 2017Market Property Buyer Seller Price ($) Size (s.f.) Price (p.s.f.)

National High Street Fund IV Portfolio Blackstone High Street $400,000,000 5,797,101 $69

NationalElmTree Net Lease Fund II Recap (56% Ind.; 29% Off.; 15% Health-Care)

China Life (95%) ElmTree Funds $950,000,000 5,500,000 $173

New Jersey Hampshire Companies NJ Infill Port.

AEW Capital Management Hampshire Companies

$146,850,000 1,218,164 $121

New York Estate Four Capital (Ind. & Land)

Sitex Group Estate Four $105,000,000 347,000 $160

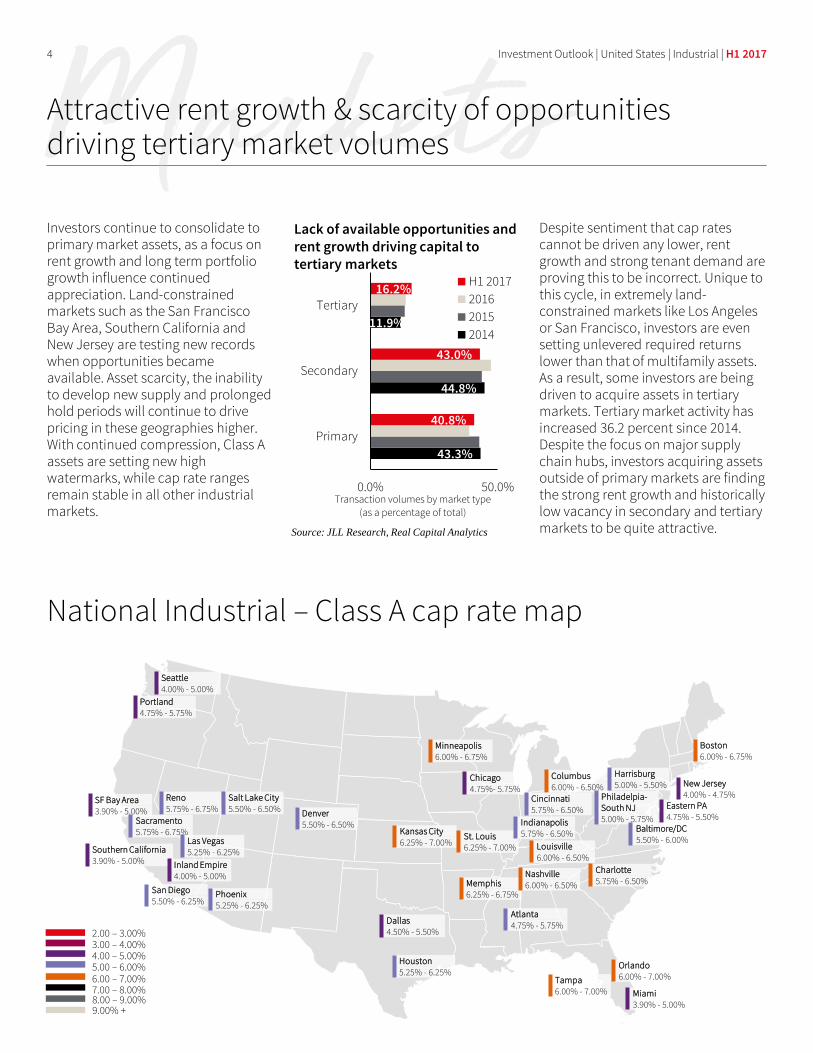

Investors continue to consolidate to primary market assets, as a focus on rent growth and long term portfolio growth influence continued appreciation. Land-constrained markets such as the San Francisco Bay Area, Southern California and New Jersey are testing new records when opportunities became available. Asset scarcity, the inability to develop new supply and prolonged hold periods will continue to drive pricing in these geographies higher. With continued compression, Class A assets are setting new high watermarks, while cap rate ranges remain stable in all other industrial markets.

Despite sentiment that cap rates cannot be driven any lower, rent growth and strong tenant demand are proving this to be incorrect. Unique to this cycle, in extremely land-constrained markets like Los Angeles or San Francisco, investors are even setting unlevered required returns lower than that of multifamily assets. As a result, some investors are being driven to acquire assets in tertiary markets. Tertiary market activity has increased 36.2 percent since 2014. Despite the focus on major supply chain hubs, investors acquiring assets outside of primary markets are finding the strong rent growth and historically low vacancy in secondary and tertiary markets to be quite attractive.

MarketsAttractive rent growth & scarcity of opportunitiesdriving tertiary market volumes

Investment Outlook | United States | Industrial | H1 20174

Source: JLL Research, Real Capital Analytics

Lack of available opportunities and rent growth driving capital to tertiary markets

NJ

CT

MA

NH

NC

VA

WA

VT

AL

AZ

AR

CACO

FL

GA

ID

IL IN

IA

KSKY

LA

ME

MI

MN

MS

MO

MT

NE

NV

NM

NY

ND

OH

OK

OR

PA

SC

SD

TN

TX

UTWV

WI

WY

Seattle4.00% - 5.00%

43.3%

44.8%

11.9%

40.8%

43.0%

16.2%

0.0% 50.0%

Primary

Secondary

Tertiary

Transaction volumes by market type (as a percentage of total)

H1 2017

2016

2015

2014

Portland4.75% - 5.75%

Reno5.75% - 6.75%

SF Bay Area3.90% - 5.00%

Southern California3.90% - 5.00%

Sacramento5.75% - 6.75%

Inland Empire4.00% - 5.00%

San Diego5.50% - 6.25%

Salt Lake City5.50% - 6.50%

Las Vegas5.25% - 6.25%

Phoenix5.25% - 6.25%

Denver5.50% - 6.50%

Minneapolis6.00% - 6.75%

Chicago4.75%- 5.75%

Kansas City6.25% - 7.00%

St. Louis6.25% - 7.00%

Memphis6.25% - 6.75%

Dallas4.50% - 5.50%

Houston5.25% - 6.25%

Columbus6.00% - 6.50%

Cincinnati5.75% - 6.50%

Louisville6.00% - 6.50%

Nashville6.00% - 6.50%

Atlanta4.75% - 5.75%

Boston6.00% - 6.75%

Eastern PA4.75% - 5.50%

Philadelpia-South NJ5.00% - 5.75%

Harrisburg5.00% - 5.50%

Baltimore/DC 5.50% - 6.00%

Charlotte5.75% - 6.50%

Orlando6.00% - 7.00%Tampa

6.00% - 7.00% Miami3.90% - 5.00%

4.00 – 5.00%5.00 – 6.00%6.00 – 7.00%7.00 – 8.00%

3.00 – 4.00%2.00 – 3.00%

8.00 – 9.00%9.00% +

National Industrial – Class A cap rate map

Indianapolis5.75% - 6.50%

New Jersey4.00% - 4.75%

capitalSources of

Investment Outlook | United States | Industrial | H1 20175

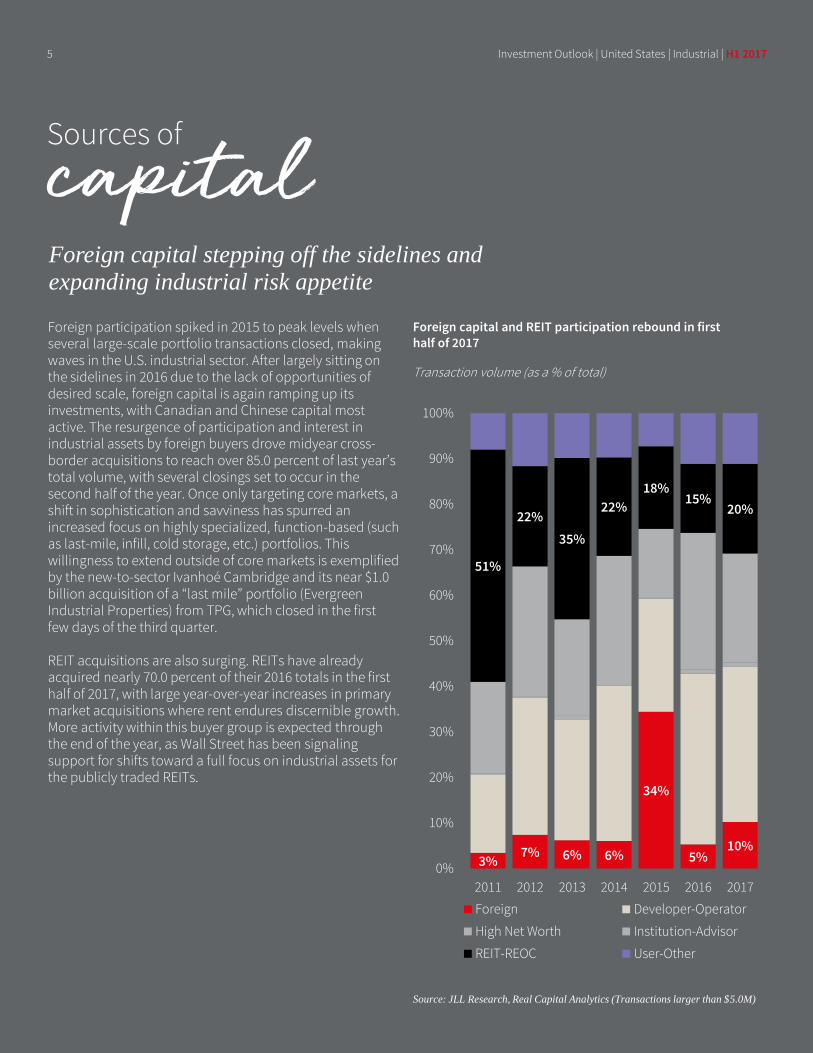

Foreign capital stepping off the sidelines and

expanding industrial risk appetite

Foreign participation spiked in 2015 to peak levels when several large-scale portfolio transactions closed, making waves in the U.S. industrial sector. After largely sitting on the sidelines in 2016 due to the lack of opportunities of desired scale, foreign capital is again ramping up its investments, with Canadian and Chinese capital most active. The resurgence of participation and interest in industrial assets by foreign buyers drove midyear cross-border acquisitions to reach over 85.0 percent of last year’s total volume, with several closings set to occur in the second half of the year. Once only targeting core markets, a shift in sophistication and savviness has spurred an increased focus on highly specialized, function-based (such as last-mile, infill, cold storage, etc.) portfolios. This willingness to extend outside of core markets is exemplified by the new-to-sector Ivanhoé Cambridge and its near $1.0 billion acquisition of a “last mile” portfolio (Evergreen Industrial Properties) from TPG, which closed in the first few days of the third quarter.

REIT acquisitions are also surging. REITs have already acquired nearly 70.0 percent of their 2016 totals in the first half of 2017, with large year-over-year increases in primary market acquisitions where rent endures discernible growth. More activity within this buyer group is expected through the end of the year, as Wall Street has been signaling support for shifts toward a full focus on industrial assets for the publicly traded REITs.

Source: JLL Research, Real Capital Analytics (Transactions larger than $5.0M)

Foreign capital and REIT participation rebound in first half of 2017

Transaction volume (as a % of total)

3%7% 6% 6%

34%

5%10%

51%

22%

35%

22%

18%15%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 2017

Foreign Developer-Operator

High Net Worth Institution-Advisor

REIT-REOC User-Other

irisk

Investment Outlook | United States | Industrial | H1 20176

Current discourse within the investment community remains focused on the prolific performance of the industrial sector since the financial crisis, almost always coupled with anxieties over how mature into the cycle the sector is. A focus on certain elements of the current market conditions are becoming more vocalized, with particular attention being given to the following risk factors:

Oversupply apprehensions. Broadly, as new supply exceeded net absorption nationally for the first time in seven years in the second quarter, investors will keep a sharp eye on market fundamentals in the latter half of the year. Worries that supply outpacing net absorption could tip the market will be weighed against the lack of quality vacant space remaining in the market, as well as the recent reduction in the average lease transaction size.

Persistent troubles by retailers and the industrial requirements of these users. Further bankruptcies, store closings and mergers/acquisitions could pose residual effects on industrial fundamentals, presenting risks to planned tenant expansions and renewals. While this does present a risk, these industrial facilities typically are last to be liquidated, solace for investors with retail-tenanted assets.

Current scarcity of industrial assets. Scarcity will be further amplified as consolidation continues in the sector with large-scale portfolio activity. This is already impacting the competitive landscape for assets that do become available, affecting underwriting and asset pricing. From a transactional point of view, we are currently observing an increase in capital evaluating highly specialized assets (multistory mezzanine facilities, food processing facilities, cold/freezer storage, urban infill warehouses, etc.), reflective of a shift out on the risk curve given the risks associated with these assets. This could potentially leave investors more susceptible to downside risk if a downturn in demand does materialize in the geographies of these facilities.

Sources of

Concentrated competition driving investment

further out the risk curve

Source: JLL Research, NCREIF, Board of Governors of Federal Reserve System

Primary market spreads over risk-frees remain comparatively healthyScarcity of opportunities, strength of rent growth both major drivers of modest & sustained cap rate compression throughout primary markets

2.3%

4.7%

5.2%

0.0%

5.0%

10.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

H1

2017

10-year Treasury yield (%)Average primary market industrial cap rate (%)Average secondary market industrial cap rate (%)

ContactsInvestor Research:

Sean CoghlanDirector, Investor Research+1 215 988 [email protected]

Sean KaneManager, Investor Research+1 213 239 [email protected]

Office:

David Hoebbel+1 312 228 [email protected]

Retail:

Arielle Einhorn+1 312 228 [email protected]

Industrial:

Peter Kroner+1 312 228 [email protected]

Net Lease:

Sean Coghlan+1 215 988 [email protected]

Multifamily:

Michael Morrone+1 312 228 [email protected]

Debt & Equity:

Ronak Sheth+1 312 228 [email protected]

Investment Outlook | United States | Industrial | H1 20177

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. A Fortune 500 company, JLL helps real estate owners, occupiers and investors achieve their business ambitions. In 2016, JLL had revenue of $6.8 billion and fee revenue of $5.8 billion and, on behalf of clients, managed 4.4 billion square feet, or 409 million square meters, and completed sales acquisitions and finance transactions of approximately $145 billion. At the end of the second quarter of 2017, JLL had nearly 300 corporate offices, operations in over 80 countries and a global workforce of nearly 80,000. As of June 30, 2017, LaSalle Investment Management had $57.6 billion of real estate under asset management. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit ir.jll.com.

About JLL Research

JLL’s research team delivers intelligence, analysis and insight through market-leading reports and services that illuminate today’s commercial real estate dynamics and identify tomorrow’s challenges and opportunities. Our more than 400 global research professionals track and analyze economic and property trends and forecast future conditions in over 60 countries, producing unrivalled local and global perspectives. Our research and expertise, fueled by real-time information and innovative thinking around the world, creates a competitive advantage for our clients and drives successful strategies and optimal real estate decisions.

© 2017 Jones Lang LaSalle IP, Inc.

All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.