india m&a trend report 2013

TRANSCRIPT

8/11/2019 India M&a Trend Report 2013

http://slidepdf.com/reader/full/india-ma-trend-report-2013 1/4

India M&A Trend Report: 2013

Overview

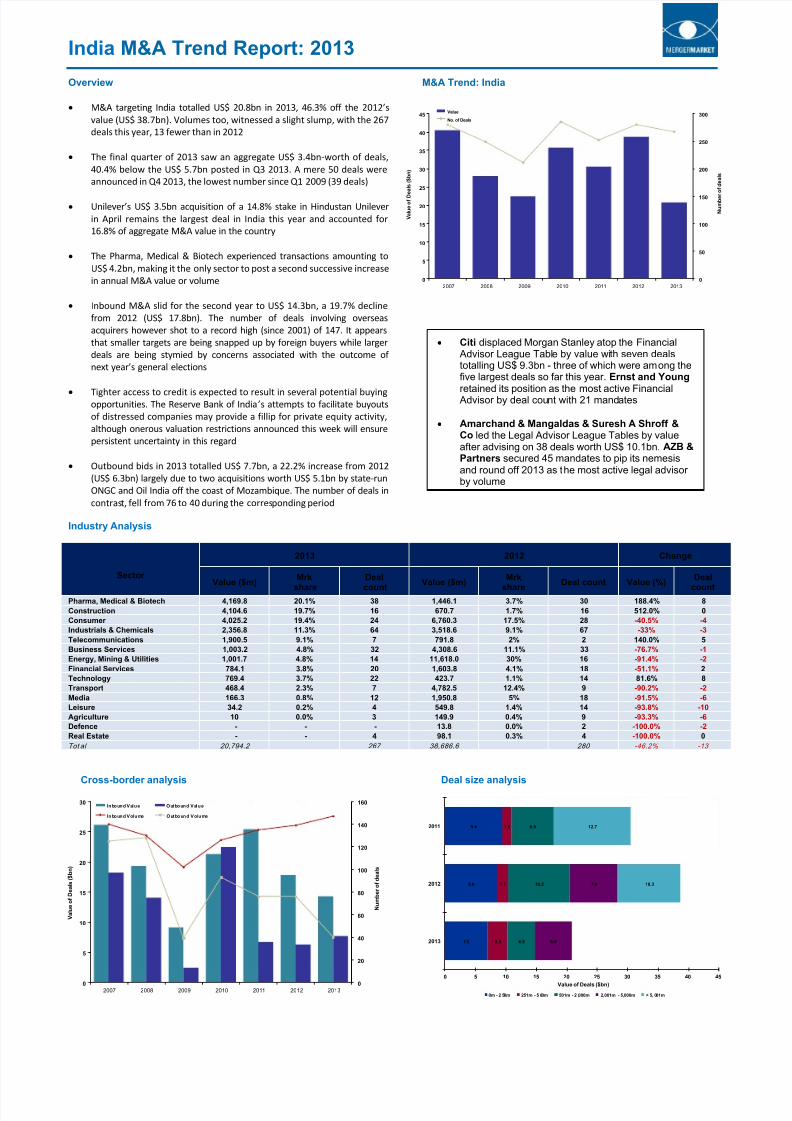

M&A targeting India totalled US$ 20.8bn in 2013, 46.3% off the 2012’s

value (US$ 38.7bn). Volumes too, witnessed a slight slump, with the 267

deals this year, 13 fewer than in 2012

The final quarter of 2013 saw an aggregate US$ 3.4bn-worth of deals,

40.4% below the US$ 5.7bn posted in Q3 2013. A mere 50 deals were

announced in Q4 2013, the lowest number since Q1 2009 (39 deals)

Unilever’s US$ 3.5bn acquisition of a 14.8% stake in Hindustan Unilever

in April remains the largest deal in India this year and accounted for

16.8% of aggregate M&A value in the country

The Pharma, Medical & Biotech experienced transactions amounting to

US$ 4.2bn, making it the only sector to post a second successive increase

in annual M&A value or volume

Inbound M&A slid for the second year to US$ 14.3bn, a 19.7% decline

from 2012 (US$ 17.8bn). The number of deals involving overseas

acquirers however shot to a record high (since 2001) of 147. It appears

that smaller targets are being snapped up by foreign buyers while larger

deals are being stymied by concerns associated with the outcome of

next year’s general elections

Tighter access to credit is expected to result in several potential buying

opportunities. The Reserve Bank of India’s attempts to facilitate buyouts

of distressed companies may provide a fillip for private equity activity,

although onerous valuation restrictions announced this week will ensure

persistent uncertainty in this regard

Outbound bids in 2013 totalled US$ 7.7bn, a 22.2% increase from 2012

(US$ 6.3bn) largely due to two acquisitions worth US$ 5.1bn by state-run

ONGC and Oil India off the coast of Mozambique. The number of deals in

contrast, fell from 76 to 40 during the corresponding period

M&A Trend: India

Industry Analysis

Sector

2013 2012 Change

Value ($m)Mrk

shareDealcount

Value ($m)Mrk

shareDeal count Value (%)

Dealcount

Pharma, Medical & Biotech 4,169.8 20.1% 38 1,446.1 3.7% 30 188.4% 8

Construction 4,104.6 19.7% 16 670.7 1.7% 16 512.0% 0

Consumer 4,025.2 19.4% 24 6,760.3 17.5% 28 -40.5% -4

Industrials & Chemicals 2,356.8 11.3% 64 3,518.6 9.1% 67 -33% -3

Telecommunications 1,900.5 9.1% 7 791.8 2% 2 140.0% 5

Business Services 1,003.2 4.8% 32 4,308.6 11.1% 33 -76.7% -1

Energy, Mining & Utilities 1,001.7 4.8% 14 11,618.0 30% 16 -91.4% -2

Financial Services 784.1 3.8% 20 1,603.8 4.1% 18 -51.1% 2

Technology 769.4 3.7% 22 423.7 1.1% 14 81.6% 8

Transport 468.4 2.3% 7 4,782.5 12.4% 9 -90.2% -2

Media 166.3 0.8% 12 1,950.8 5% 18 -91.5% -6

Leisure 34.2 0.2% 4 549.8 1.4% 14 -93.8% -10

Agriculture 10 0.0% 3 149.9 0.4% 9 -93.3% -6

Defence - - - 13.8 0.0% 2 -100.0% -2

Real Estate - - 4 98.1 0.3% 4 -100.0% 0

Tot al 20,794.2 267 38,686.6 280 -46.2% -13

Cross-border analysis Deal size analysis

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

40

45

2007 2008 2009 2010 2011 2012 2013

N u m b e r o f d e a l s

V a l u e o f D e a l s ( $ b n )

Value

No. of Deals

0

20

40

60

80

100

120

140

160

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013

N u m b e r o f d e a l s

V a l u e o f D e a l s ( $ b n )

Inbound Value Outbound Value

Inbound Volume Outbound Volume

7.0

8.6

9.4

3.3

1.7

1.6

4.5

10.2

6.9

6.0

7.9 10.3

12.7

0 5 10 15 20 25 30 35 40 45

2013

2012

2011

Value of Deals ($bn)

0m - 2 50m 251m - 5 00m 501m - 2 ,000m 2,001m - 5,000m > 5, 001m

Citi displaced Morgan Stanley atop the Financial Advisor League Table by value with seven dealstotalling US$ 9.3bn - three of which were among the

five largest deals so far this year. Ernst and Young retained its position as the most active Financial Advisor by deal count with 21 mandates

Amarchand & Mangaldas & Suresh A Shroff &Co led the Legal Advisor League Tables by valueafter advising on 38 deals worth US$ 10.1bn. AZB &Partners secured 45 mandates to pip its nemesisand round off 2013 as the most active legal advisorby volume

8/11/2019 India M&a Trend Report 2013

http://slidepdf.com/reader/full/india-ma-trend-report-2013 2/4

India M&A Trend Report: 2013

Spotlight on Pharma, Medical & Biotech (PMB) M&A

Overview

Pharma, Medical & Biotech (PMB) dealmaking hit US$ 4.2bn (38 deals), a

staggering 188.4% increase from 2012 (US$ 1.4bn, 30 deals) with eight more

deal announcements. This represents a second consecutive annual rise by

both value and volume

The rest of the Asia-Pacific region too witnessed an increase in PMB M&A,

rising 12.1% from US$ 11.5bn in 2012 to US$ 14.4bn (163 deals). China and

Hong Kong were stellar performers, recording four successive years of

growth in deal values to US$ 6.8bn and US$ 1.3bn respectively

Private equity buyers acquired 19 firms in transactions totalling US$ 0.7bn in

2013, representing the most deals and the highest value on Mergermarket

record (since 2001) for this activity

Exits too saw the most targets sold for the highest value on Mergermarket

record. Deal value soared 383.9% from 2012 (US$ 0.1bn) to US$ 0.5bn in

2013 with seven deals, three more than the previous peak of four in 2010

Mylan’s US$ 1.6bn purchase of Agila Specialties marked the largest

transaction in the PMB space this year. GlaxoSmithKline Plc dished out US$

1bn to increase its stake in GlaxoSmithKline Pharmaceuticals Ltd to the

maximum permissible 75%, a trend slated to continue among MNCs in the

country

Pharma, Medical & Biotech trend

Asian TargetCountry

2013 2012 2011

Value($m)

DealCount

Value($m)

DealCount

Value($m)

DealCount

China 6,816 81 6,061 67 3,611 51

Japan 1,960 24 416 24 2,051 19Australia 1,787 28 2,081 21 2,112 23

Hong Kong 1,333 7 408 3 213 3

South Korea 951 19 1,327 13 1,143 13

Singapore 918 6 630 6 1,028 6

Taiwan 246 4 60 1 1

Indonesia 226 3 1

Vietnam 119 2 8 2 78 2

Malaysia 35 2 300 3 1,302 7

New Zealand 32 5 87 3 58 4

Thailand 14 2 100 1 116 1

Bangladesh 10 1

Kazakhstan 67 1

Pakistan

Philippines 1 6 1 41 2

Sri Lanka 32 1

Tot al 14,437 184 11,515 147 11,832 134

India PMB buyouts and exits analysis Pharma, Medical & Biotech projections

Both primary and secondary private equity buyouts are expected to increase

in 2013. Companies in the PMB space are seeking capital for expansion, which

should provide an ideal window of opportunity for private equity firms as

other exit options such as a strategic sale and IPOs are expected to remain

slow until the outcome of the 2014 general elections

An impasse between different government ministries regarding restrictions

on FDI in generic drug makers resulted in diminished strategic investor

interest. We expect foreign acquirers to remain wary of acquiring Indiantargets in spite of the government’s decision to retain the 100% FDI limit until

after the general elections

Indian pharmaceutical giants Cipla and Sun Pharmaceutical Industries are

known suitors and have reportedly been eyeing generic drug manufacturers

in Japan, Europe and the US. High interest rates and difficulties in raising

funds for deals will however continue to pose problems for Indian firms on

the acquisition warpath

Top Pharma, Medical & Biotech deals involving Indian targets

Ann. Date Bidder company Target company Seller company Bidder advisors Target/Seller advisors Deal Value(US$m)

27-Feb-13 Mylan Inc Agila Specialties PrivateLimited; and AgilaSpecialties Asia Pte Limited

Strides Arcolab Limited FA: Morgan Stanley

LA: Barbosa, Mussnich & Aragao;Morgan Lewis & Bockius; Osler,Hoskin & Harcourt; PlatinumPartners; Skadden Arps SlateMeagher & Flom; Slaughter andMay

FA: Jefferies; Moelis &Company

LA: Borden Ladner Gervais;DSK Legal; Haynes andBoone; Herbert SmithFreehills; Jones Day;Pinheiro Neto Advogados

1,600

16-Dec-13 GlaxoSmithKline Plc GlaxoSmithKlinePharmaceuticals Ltd(24.3% Stake)

FA: HSBC

LA: Slaughter & May

FA: -

LA: -

1,035

13-Dec-13 Torrent Pharmaceuticals Ltd Elder PharmaceuticalsLimited (Branded DomesticFormulation Business)

Elder PharmaceuticalsLimited

FA: Deloitte

LA: -

FA: Nomura Holdings

LA: Khaitan & Co

323

23-Nov-13 Pfizer Ltd Wyeth Ltd FA: Bank of America MerrillLynch

LA: AZB & Partners

FA: Citi

LA: Advis ing FA: Davis Polk& Wardwell

294

27-Nov-13 Kohlberg Kravis Roberts &Co LP

Gland Pharma Limited Evolvence India LifeSciences Fund

FA: Citi

LA: Amarchand & Mangaldas &Suresh A Shroff & Co; SimpsonThacher & Bartlett

FA: -

LA: AZB & Partners

200

0

10

20

30

40

50

60

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013

N u m b e r o f d e a l s

V a l u e o f D e a l s ( $ m )

Buyouts Value

Exits Value

No. of Buyouts

No. of Exits

8/11/2019 India M&a Trend Report 2013

http://slidepdf.com/reader/full/india-ma-trend-report-2013 3/4

India M&A Trend Report: 2013

Top Deals

Ann. Date Bidder company Target Company Seller company Buy-side Advisory Sell-side Advisory Deal Value ($m)

30-Apr-13 Unilever NV Hindustan Unilever Limited(14.8% Stake)

FA: HSBC; UBS Investment Bank

LA: Linklaters; Talwar Thakore &Associates

FA: Citi

LA: Advis ing FA : Davis Polk& Wardwell

3,549

25-Aug-13 ONGC Videsh Limited Rovuma Offshore Area 1Block (10% Stake)

Anadarko PetroleumCorporation

FA: Bank of America MerrillLynch

LA: Simmons & Simmons

FA: Citi

LA: -

2,640

25-Jun-13 ONGC Videsh Limited; andOil India Limited

Rovuma Offshore Area 1Block (10% Stake)

Videocon Mauritius EnergyLimited

FA: Bank of America MerrillLynch; Morgan Stanley

LA: Kochhar & Co; PLMJ -Sociedade de Advogados;Simmons & Simmons

FA: Credit Suisse; StandardChartered; UBS InvestmentBank

LA: Amarchand &Mangaldas & Suresh AShroff & Co

2,475

24-Jul-13 Ambuja Cements Limited ACC Limited (50.01% Stake) Holcim Ltd FA: Axis Capital

LA: Amarchand & Mangaldas &Suresh A Shroff & Co

FA: Citi

LA: Homburger

2,433

27-Feb-13 Mylan Inc Agila Specialties PrivateLimited; and AgilaSpecialties Asia Pte Limited

Strides Arcolab Limited FA: Morgan Stanley

LA: Barbosa, Mussnich & Aragao;

Morgan Lewis & Bockius; Osler,Hoskin & Harcourt; PlatinumPartners; Skadden Arps SlateMeagher & Flom; Slaughter andMay

FA: Jefferies; Moelis &Company

LA: Borden Ladner Gervais;

DSK Legal; Haynes andBoone; Herbert SmithFreehills; Jones Day;Pinheiro Neto Advogados

1,600

League Tables to M&A Activity Involving India

Financial advisor league table by value – 2013

Legal advisor league table by value – 2013

Rank2012 2013

House Value ($m)Deal

count% Value change

2 1 Citi 9,277 7 -49.7%

9 2 UBS Investment Bank 6,024 2 57.3%

3 3 Bank of America Merrill Lynch 5,327 5 -61%16 4 HSBC 4,993 4 234%

1 5 Morgan Stanley 4,168 8 -79.5%

10 6 Standard Chartered 3,762 4 12.2%

11 7 Axis Capital 3,508 9 20.1%

5 8 Credit Suisse 3,240 3 -69.3%

- 9 Moelis & Company 2,129 3 -

6 10 Goldman Sachs 2,056 5 -79.7%

32 11 Jefferies 1,600 1 306.1%

15 12 Barclays 1,551 5 -0.5%

12 13 Kotak Investment Banking 1,072 10 -52.6%

13 14 Rothschild 1,062 8 -43.3%

- 15 Macquarie Group 1,043 3 -

Rank2012 2013

House Value ($m)Deal

count% Value change

1 1Amarchand & Mangaldas &Suresh A Shroff & Co 10,149 38 -51.2%

25 2 Simmons & Simmons 5,115 2 411.5%

16 3 Jones Day 4,009 4 248.3%

46 4 Davis Polk & Wardwell 3,886 4 1,070.5%

39 5 Linklaters 3,648 3 825.9%

134 6 Talwar Thakore & Associates 3,601 5 -

7 7 Slaughter and May 3,350 5 -31.4%

89 8 White & Case 3,333 5 9,158.3%

6 9 AZB & Partners 3,305 45 -36.4%

- 10PLMJ - Sociedade deAdvogados 2,475 1 -

122 11 Bowman Gilfillan Africa Group 2,436 2 -

- 12 Homburger 2,433 1 -

- 13= CMS 2,331 1 -

- 13= Sullivan & Cromwell 2,331 1 -

10 15 Khaitan & Co 2,246 27 -37.5%

Financial advisor league table by deal count – 2013

Legal advisor league table by deal count – 2013

Rank2012 2013

House Value ($m)Deal

countCount change

1 1 EY 534 21 4

19 2 PwC 656 11 6

7 3 Kotak Investment Banking 1,072 10 011 4 ICICI Securities 809 10 1

2 5 KPMG 555 10 -2

3 6 BMR Advisors 208 10 -1

13 7 Axis Capital 3,508 9 1

5 8 Morgan Stanley 4,168 8 -2

17 9 Rothschild 1,062 8 3

65 10 o3 Capital Advisors 99 8 7

9 11 Citi 9,277 7 -2

62 12 Translink 84 6 5

28 13 Bank of America Merrill Lynch 5,327 5 3

16 14 Goldman Sachs 2,056 5 0

20 15 Barclays 1,551 5 1

Rank

2012 2013

House Value ($m)Deal

count

Count change

4 1 AZB & Partners 3,305 45 15

1 2Amarchand & Mangaldas &Suresh A Shroff & Co 10,149 38 -6

3 3 Khaitan & Co 2,246 27 -10

2 4 Desai & Diwanji 617 24 -16

5 5 Trilegal 697 22 2

7 6 J Sagar Associates 693 17 2

19 7 DLA Piper 1,573 13 8

9 8 Tatva Legal 219 13 2

10 9 Nishith Desai Associates 115 8 -2

11 10 Rajani, Singhania & Partners 298 7 -3

6 11 DSK Legal 1,674 6 -11

26 12 Vaish Associates 627 6 2

16 13 Luthra & Luthra Law Offices 325 6 1

134 14 Talwar Thakore & Associates 3,601 5 4

28 15 Slaughter and May 3,350 5 2

8/11/2019 India M&a Trend Report 2013

http://slidepdf.com/reader/full/india-ma-trend-report-2013 4/4

India M&A Trend Report: 2013

Notes

All data is based on announced transactions over US$ 5m. Deals with undisclosed deal values are included where the target’s turnover exceedsUS$ 10m. Deals where the stake acquired is less than 10% will only be included if their value is greater than US$ 100m. Activities excluded includeproperty transactions and restructurings where the ultimate shareholders’ interests are not changed. All data excludes minority stake deals (10% -30%) where the dominant target geography is Asia-Pacific and the deal value is less than US$ 100m

M&A Trend: Based on the dominant geography of the target company being India. Excludes lapsed and withdrawn bids

Cross-border M&A: Inbound refers to cross-border M&A where the dominant geography of the target company is India. Outbound refersto cross-border M&A where the dominant geography of the bidder company is India. Excludes lapsed and withdrawn bids

Top Announced Deals: Based on the dominant geography of the target, bidder or seller company being India. Excludes lapsed andwithdrawn bids. FA refers to Financial Advisor and LA refers to Legal Advisor

Industry Analysis: Based on the dominant geography of the target company being India. Industry sectors represent the primary industrysector of the target company only. Excludes lapsed and withdrawn bids. The Buyout Sector breakdown includes Other which refers toBusiness Services, Leisure, Agriculture, Defence and Real Estate and. The Exit sector breakdown includes Other which refers to. Buyoutand Exit sector breakdown include TMT which refers to Technology, Media & Telecommunications

League Tables for Total India M&A: Based on the dominant geography of the target, bidder or seller company being India. The Financial Advisor tables exclude lapsed and withdrawn bids, and the legal advisor tables include lapsed and withdrawn bids

League Tables for Indian M&A Advisors: Based on the dominant geography of the target, bidder or seller company being India and the

advisor being an entity which is headquartered in India. The Financial Advisor tables exclude lapsed and withdrawn bids, and the legaladvisor tables include lapsed and withdrawn bids

All values are in US$

All data correct as of 09 January 2014

Criteria

PR contacts

Europe Flora Wilke +44 207 010 6438

Americas Chrissy Carney +1 646 378 3118

Asia Flora Wilke +44 207 010 6438

Commercial contacts

Europe Ben Rumble +44 207 010 6100

Americas Lauren Peterson +1 212 500 7537

Asia Ajay Narang +852 2158 9764

Research contacts

Editor Kirsty Wilson +44 207 010 6271

Analyst Raza Hussain +852 2158 9726

Deal submission contacts

Europe EMEA

Nancy Honsinger

CEE

Zaynab Dost

+44 207 010 6227

+44 207 010 6129

Americas Raquel Mozzer +1 212 574 7866

Asia Asia-Pacific

Miran Lim

Japan

Sophie Kim

+852 2158 9709

+81 3 3597 2055