independent petroleum association of america...

TRANSCRIPT

Independent Petroleum Association of America (IPAA) Oil & Gas Investment Symposium (OGIS) Toronto

Investor Presentation

June 5, 2014

NYSE: PVA

Forward-Looking Statements / Oil and Gas Reserves and Definitions

1

Forward-Looking Statements Certain statements contained herein that are not descriptions of historical facts are “forward-looking” statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from those expressed or implied by such forward-looking statements. These risks, uncertainties and contingencies include, but are not limited to, the following: the volatility of commodity prices for oil, natural gas liquids and natural gas; our ability to develop, explore for, acquire and replace oil and gas reserves and sustain production; our ability to generate profits or achieve targeted reserves in our development and exploratory drilling and well operations; any impairments, write-downs or write-offs of our reserves or assets; the projected demand for and supply of oil, natural gas liquids and natural gas; reductions in the borrowing base under our revolving credit facility; our ability to contract for drilling rigs, supplies and services at reasonable costs; our ability to obtain adequate pipeline transportation capacity for our oil and gas production at reasonable cost and to sell the production at, or at reasonable discounts to, market prices; the uncertainties inherent in projecting future rates of production for our wells and the extent to which actual production differs from estimated proved oil and gas reserves; drilling and operating risks; our ability to compete effectively against oil and gas companies; our ability to successfully monetize select assets and repay our debt; leasehold terms expiring before production can be established; environmental liabilities that are not covered by an effective indemnity or insurance; the timing of receipt of necessary regulatory permits; the effect of commodity and financial derivative arrangements; our ability to maintain adequate financial liquidity and to access adequate levels of capital on reasonable terms; the occurrence of unusual weather or operating conditions, including force majeure events; our ability to retain or attract senior management and key technical employees; counterparty risk related to their ability to meet their future obligations; changes in governmental regulations or enforcement practices, especially with respect to environmental, health and safety matters; uncertainties relating to general domestic and international economic and political conditions; and other risks set forth in our filings with the Securities and Exchange Commission (SEC). Additional information concerning these and other factors can be found in our press releases and public periodic filings with the SEC. Many of the factors that will determine our future results are beyond the ability of management to control or predict. Readers should not place undue reliance on forward-looking statements, which reflect management’s views only as of the date hereof. We undertake no obligation to revise or update any forward-looking statements, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise. Oil and Gas Reserves Effective January 1, 2010, the SEC permits oil and gas companies, in their filings with the SEC, to disclose not only “proved” reserves, but also “probable” reserves and “possible” reserves. As noted above, statements of reserves are only estimates and may not correspond to the ultimate quantities of oil and gas recovered. Investors are urged to consider closely the disclosure in PVA’s Annual Report on Form 10-K for the fiscal year ended December 31, 2013, which is available from PVA at Four Radnor Corporate Center, Suite 200, Radnor, PA 19087 (Attn: Investor Relations). You can also obtain this report from the SEC by calling 1-800-SEC-0330 or from the SEC’s website at www.sec.gov. Definitions Proved reserves are those quantities of oil and gas which, by analysis of geosciences and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward, from known reservoirs, and under existing economic conditions, operating methods and government regulation before the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether the estimate is a deterministic estimate or probabilistic estimate. Probable reserves are those additional reserves that are less certain to be recovered than proved reserves, but which are as likely than not to be recoverable (there should be at least a 50% probability that the quantities actually recovered will equal or exceed the proved plus probable reserve estimates). Possible reserves are those additional reserves that are less certain to be recoverable than probable reserves (there should be at least a 10% probability that the total quantities actually recovered will equal or exceed the proved plus probable plus possible reserve estimates). “3P” reserves refer to the sum of proved, probable and possible reserves. Estimated ultimate recovery (EUR) is the sum of reserves remaining as of a given date and cumulative production as of that date. EUR is a measure that by its nature is more speculative than estimates of reserves prepared in accordance with SEC definitions and guidelines and accordingly is less certain.

Penn Virginia Today

2

• Contiguous and high‐quality acreage position in the Eagle Ford Shale

• Approximately 86,800 net acres with over 1,500 remaining drilling locations; nearly a 15-year drilling inventory

• Continue to high-grade and increase acreage footprint

• Recent operational success

• Recent Upper Eagle Ford results has confirmed stacked potential

• Currently drilling premium acreage in the “Beer Quad” area

• Significant oil focus – current 2014E oil production growth guidance of greater than 65%

• Operational excellence and decreasing well costs

• Pad drilling and “zipper fracs” have increased efficiencies and improved well results

• Experienced team manages aggressive growth strategy

• Portfolio optimization focusing on Eagle Ford growth

• Recently announced Selma Chalk divestiture for approximately $73 MM

Eagle Ford Shale Will Drive Continued Growth

Operating Areas

3

Granite Wash/Mid-Continent YE13 proved reserves: 10.6 MMBOE

80% Developed 1Q14 Production: 1.9 MBOEPD

Eagle Ford Shale/South Texas YE13 proved reserves: 75.6 MMBOE

29% Developed 1Q14 Production: 15.2 MBOEPD

Selma Chalk/Mississippi YE13 proved reserves: 14.2 MMBOE

69% Developed 1Q14 Production: 2.0 MBOEPD

East Texas YE13 proved reserves: 35.9 MMBOE

30% Developed 1Q14 Production: 2.0 MBOEPD

As of and for the Quarter Ended March 31, 2014

Assets targeted for sale (Selma Chalk closing expected July 2014)

Total Company

• YE 2013 Reserves

• 136.3 MMBOE

• 40% Developed

• 45% Oil, 61% Liquids

• 1Q 2014 Production

• 21.1 MBOEPD

• 57% Oil, 69% Liquids

• 5% growth over 4Q13

• Eagle Ford Acreage & Locations

• ~126,500 gross (~86,800 net)

• Over 1,500 gross drilling locations remaining

• 6 rigs running

Strategy

4

Focused on

Operational Execution

and Further

Expansion in the

Eagle Ford

• Six drilling rigs, drilling 98 (53.3 net) wells in 2014

• Goal: increase acreage to a minimum of 100,000 net acres in our Eagle Ford backyard

• Delivering high levels of production, reserve and EBITDAX growth

Focused on Improving

Liquidity

• Availability under our revolver with its growing borrowing base and asset sales will fund

our anticipated development program through 2014

• Eagle Ford gas gathering / gas lift assets – closed January 2014 for $94 MM gross

• Selma Chalk assets – closing expected by July 2014 for approximately $73 MM

• Currently marketing Granite Wash assets, as well as the option to build an oil

gathering system in the Eagle Ford Shale

Focused on

Generating New

Opportunities

• Delineating Upper Eagle Ford (Marl) Shale

• Continuing to evaluate new oil resource play opportunities that have early entry

possibilities

0

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014E 2015E

BO

EPD

Eagle Ford Shale Mid-Continent Cotton Valley

Haynesville Shale Mississippi

5

PVA is an Eagle Ford Shale Oil Growth Story

Note: Excludes divested assets with the exception of recently announced Selma Chalk asset sale.

• We significantly increased oil production over the last few years and we expect that trend to continue

• Other plays, largely gassy, have been allowed to decline and will play a less strategic role

• Drilling program anticipated to provide oil production growth >65% in 2014 and ~30% in 2015

Historical and Anticipated Production Growth

0

10

20

30

40

50

60

70

80

Year-End 2011 Year-End 2012 Mid-Year 2013 Year-End 2013

MM

BO

E

Growth in Eagle Ford Shale Proved Reserves

Crude Oil NGLs Natural Gas

$0

$20

$40

$60

$80

$100

$120

$MM

Growth in Eagle Ford Shale Revenues

Crude Oil NGLs Natural Gas

0

2

4

6

8

10

12

14

MB

OEP

D

Growth in Eagle Ford Shale Production

Crude Oil NGLs Natural Gas

6

Growing Our Eagle Ford Shale Position

Increases in Production, Revenues and Reserves

0

20

40

60

80

100

120

140

160

180

200

Year-End 2011 Year-End 2012 Mid-Year 2013 Year-End 2013

MM

BO

E

Growth in Eagle Ford Shale Proved Reserves

Crude Oil NGLs Natural Gas

0

20

40

60

80

100

120

140

160

180

200

Year-End 2011 Year-End 2012 Mid-Year 2013 Year-End 2013

MM

BO

E

Growth in Eagle Ford Shale 3P Reserves

Proved Probable and Possible

Note: Some EFS operators off map. (1) Based on recent company presentations, as well as industry publications. Some industry publication information may be out of date.

Eastern Volatile Oil and Condensate Rich Gas Windows(1)

7

Overview of the Eagle Ford Shale

Victoria

Goliad

Bee

Live Oak McMullen

Wilson

Atascosa

Bexar

San Antonio

Texas

Volatile Oil

Higher GOR Oil

Gonzales

Lavaca

DeWitt

PVA

BHP

CHK

COG

COP

CRK

CRZO

DVN (new)

EOG

FST/Sabine

MRO

MUR

NFX

Oak Valley

PXD

PXP

Sabine/FST

SFY

SN

STO

TLM

EFS Operators

8

Overview of PVA’s Eagle Ford Shale Position

Emerging Presence in Leading U.S. Oil Shale Play

• 126,500 gross (86,800 net) acres in Gonzales and Lavaca Cos.

• Avg. IP/30-day rates of 1,469/869 BOEPD for the last 68/53 wells in the Peach Creek, Rock Creek Ranch and Shiner Fields(1)

• 15,000 net BOEPD March 2014 daily EF sales (89% liquids)

• Proved PV-10 at YE13 of $1,584MM ($754MM of PD value) (2)

Approximately 190 MMBOE of 3P reserves at YE13 (3)

• Greater than 1,500 remaining gross drilling locations

• Positive down-spacing results associated with pad drilling

• Additional upside potential in Upper Eagle Ford (Marl) and Austin Chalk

• Rigs and infrastructure in place

• Drilling plan includes 6 rigs; 53 net wells in 2014

• Contracts with two frac companies in place; looking to expand

(1) Since the beginning of 2Q13; excludes “shallow” wells. (2) Based on SEC proved reserve estimates as of 12/31/13. (3) 3P reserves based on internal estimates of probable and possible reserves as of 12/31/13.

PVA

BHP Billiton

ConocoPhillips

Devon (new)

EOG

Forest / Sabine

Nearby Operators

Marathon

Oak Valley

Pioneer

Plains

Sabine / Forest

Sanchez

Gonzales

Lavaca

DeWitt

PVA's Concentrated Position in the Eagle Ford Shale

Fayette

Lavaca

Gonzales

0 1 2 mi mi

0 5,280’ 10,560’

Peach Creek

Rock Creek / Bozka

Shiner

Additional PVA Leasehold

“Beer Quad”

Recent Operated Drilling Activity

Shiner

Rock Creek

9

Peach Creek

Wombat Unit 1H : IP 1,670 BOEPD 2H : IP 1,423 BOEPD

Leal Unit 3H : IP 1,365 BOEPD 4H : IP 1,641 BOEPD

Welhausen Unit A 2H (Marl) : IP 2,165 BOEPD

B 1H : IP 1,536 BOEPD

Zebra Hunter Unit 2H : IP 1,511 BOEPD 3H : IP 2,250 BOEPD

RCR Wyatt Unit 1H : IP 857 BOEPD

2H : IP 1,624 BOEPD 3H : IP 1,323 BOEPD 4H : IP 1,228 BOEPD

Amber Unit 1H : IP 2,217 BOEPD 2H : IP 1,919 BOEPD

Penn Virginia Continues to Produce Strong Well Results

Acreage and Current Activity

Bozka

Blonde Unit 1H : IP 2,521 BOEPD

Porter Unit 1H : IP 2,670 BOEPD

Kosmo Unit 1H : IP 2,168 BOEPD

10

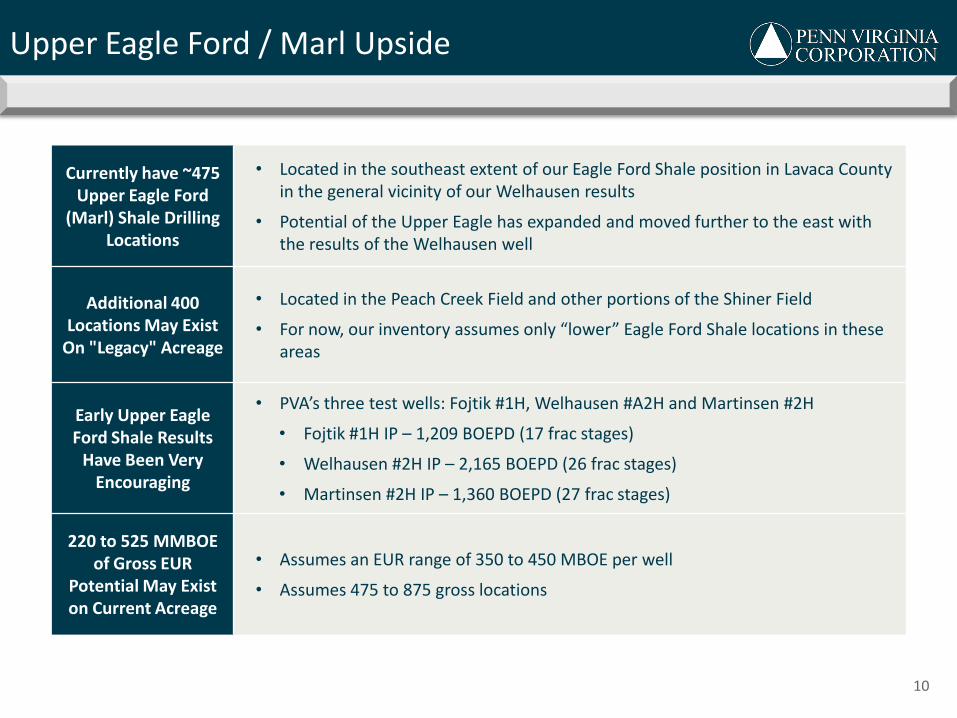

Currently have ~475 Upper Eagle Ford

(Marl) Shale Drilling Locations

• Located in the southeast extent of our Eagle Ford Shale position in Lavaca County in the general vicinity of our Welhausen results

• Potential of the Upper Eagle has expanded and moved further to the east with the results of the Welhausen well

Additional 400 Locations May Exist

On "Legacy" Acreage

• Located in the Peach Creek Field and other portions of the Shiner Field

• For now, our inventory assumes only “lower” Eagle Ford Shale locations in these areas

Early Upper Eagle Ford Shale Results

Have Been Very Encouraging

• PVA’s three test wells: Fojtik #1H, Welhausen #A2H and Martinsen #2H

• Fojtik #1H IP – 1,209 BOEPD (17 frac stages)

• Welhausen #2H IP – 2,165 BOEPD (26 frac stages)

• Martinsen #2H IP – 1,360 BOEPD (27 frac stages)

220 to 525 MMBOE of Gross EUR

Potential May Exist on Current Acreage

• Assumes an EUR range of 350 to 450 MBOE per well

• Assumes 475 to 875 gross locations

Upper Eagle Ford / Marl Upside

Lavaca

Lavaca

Gonzales

Fayette

Lavaca

Gonzales

00

1

100

10

0

100

100

00

2

20

0

200

00

2

200

200

20 0 20

0

200

200

200

20

0

00

2

00

2

00

2

300

300

003

300

003

300

003

300

CANNONADE RANCH1

CANNONADE RANCH2

SCHRADER-THIEDE1

LAVENDER-THIEDE1

GONZO HUNTER1H

SOUTHERN HUNTER1H

GARDNER ET AL1H

GONZO NORTH1H

HAWN HOLT2H

HAWN HOLT1H

BOZKA1H

HAWN HOLT4H

HAWN HOLT6H

HAWN HOLT9H

HAWN HOLT10H

HAWN HOLT13H

HAWN HOLT7H

HAWN HOLT3H

HAWN HOLT5H

HAWN HOLT8H

HAWN HOLT12H

HAWN HOLT11H

MUNSON RANCH1H

MUNSON RANCH3H

MILLER1H

DICKSON-ALLEN1H

DICKSON-ALLEN2H

HAWN HOLT15H

GARDNER ET AL2H

CANNONADE RANCH NORTH1H

SOUTHERN HUNTER2H

SCHAEFER R L1H

SCHAEFER R L1H

GONZO NORTH2H

SCHAEFER R L3HST1

SCHAEFER R L3H

CANNONADE RANCH3H

SCHAEFER R L2H

MUNSON RANCH2H_PLT

MUNSON RANCH5H

MUNSON RANCH7H

MUNSON RANCH4H

MUNSON RANCH8H

HAWN DICKSON1H

MUNSON RANCH6H

MUNSON RANCH9H

ROCK CREEK 1H1H

ROCK CREEK2H

ROCK CREEK RANCH3H

ROCK CREEK RANCH4H

SHINER RANCH1H

FOREMAN D UNIT1H

HENNING UNIT1H

ROCK CREEK RANCH5H

ROCK CREEK RANCH6H

ROCK CREEK RANCH7H

ROCK CREEK RANCH8H

ROCK CREEK RANCH9H

ROCK CREEK RANCH10H

GEO HUNTER1H

FURRH1H

ORYX HUNTER1H

FURRH2H

SABLE HUNTER1H

KUDU HUNTER1H

SNIPE HUNTER1H

HAWG HUNTER1H

LEOPARD HUNTER1H

HIPPO HUNTER1H

KUDU HUNTER2H

LEOPARD HUNTER2H

ORYX HUNTER2H

EFFENBERGER1H

VANA UNIT1H

LEOPARD HUNTER3H

HIPPO HUNTER2H

SCHACHERL1H

MUNSON RANCH2H

SCHACHERL UNIT1H

VANA1H

SRALLA1H

MCCREARY1V

MOOSE HUNTER1H

SNIPE HUNTER2H

HENNING UNIT2H

ROCK CREEK RANCH11H

GARDNER ET AL1H

MCCREARY1H

MOOSE HUNTER2H

ELK HUNTER1H

ELK HUNTER2H

FURRH3H

ELK HUNTER3H

MOOSE HUNTER3H

PAVLICEK1H

TARGAC UNIT1H

FREYTAG1H

SMITH1H

NEUSE UNIT1H

LEAL1H

KLEIHEGE1H

TECHNIK1H

MATIAS1H

HILL1H

GARZA KODAK1H

MILLER UN 22H

MILLER UN 21H

PAVLICEK2H

PAVLICEK5H

DUBOSE2H

KLEIHEGE2H

DUBOSE UNIT 21H

CANNONADE RANCH17H

CANNONADE RANCH18H

CANNONADE RANCH19H

RCR-WYATT3H

RCR-WYATT1H

RCR-WYATT4H

JOSEPH SIMPER1H

DOUGLAS RAAB1H

HINZE1H

OTHOLD UNIT1H

MARTINSEN UNIT3H

VANA4H

VANA3H

SCHACHERL-VANA (A)1H

SCHACHERL2H

EFFENBERGER4H

EFFENBERGER-SCHACHERL (A)4H

BERGER-SIMPER2H

BERGER-SIMPER1H

TECHNIK7H

TECHNIK2H

KUSAK2H

BERTHA1H

ZEBRA HUNTER1H

RHINO HUNTER1H

ADDAX HUNTER1H

ADDAX HUNTER2H

ADDAX HUNTER3H

BARRAZA UNIT1H

KUSAK UNIT1H

ARLEDGE RANCH1H

WASHINGTON R UNIT1H

RAAB UNIT1H

BUFFALO HUNTER1H

GONZO SOUTH1H

MARTINSEN UNIT1H

FOJTIK UNIT1H

HEFE HUNTER1H

PILSNER HUNTER1H

NETARDUS UNIT1H

DUBOSE2HST1

PLATYPUS HUNTER1H

STAG HUNTER1H

GEO HUNTER1H

STAG HUNTER2H

EFFENBERGER5H

RCRS HINTON1H

RCRS HINTON3H

RCR-WYATT2H

SCHACHERL_ST12H

GONZO HUNTER2H

GONZO HUNTER3H

GONZO HUNTER4H

BONGO HUNTER1H

MOOSE HUNTER4H

BONGO NORTH1H

BONGO NORTH2H

J.BERGER UNIT1H

NETARDUS UNIT1H

FURRH1H

CANNONADE RANCH SOUTH18HST2

MILLER1H

BLONDE1H

KOSMO1H

PILSNER HUNTER2H

PILSNER HUNTER3H

PILSNER HUNTER4H

PILSNER HUNTER5H

ZEBRA HUNTER3H

RHINO HUNTER7H

RHINO HUNTER6H

AMBER2H

AMBER1H

WELHAUSEN BB1H

WELHAUSEN AA2H

RCRS HINTON2HST2

PORTER1HST2

KUSAK UNIT3HST1

LEAL3HST1

HILL2HST1

ZEBRA HUNTER2HST1

LEAL4HST1

MARTINSEN2HST1

KLEIHEGE3HST2(3)

EAGLE_FORD_REGIONAL - Eagle Ford Trend MAP

FEET

0 18,551

PETRA 5/30/2014 4:12:58 PM

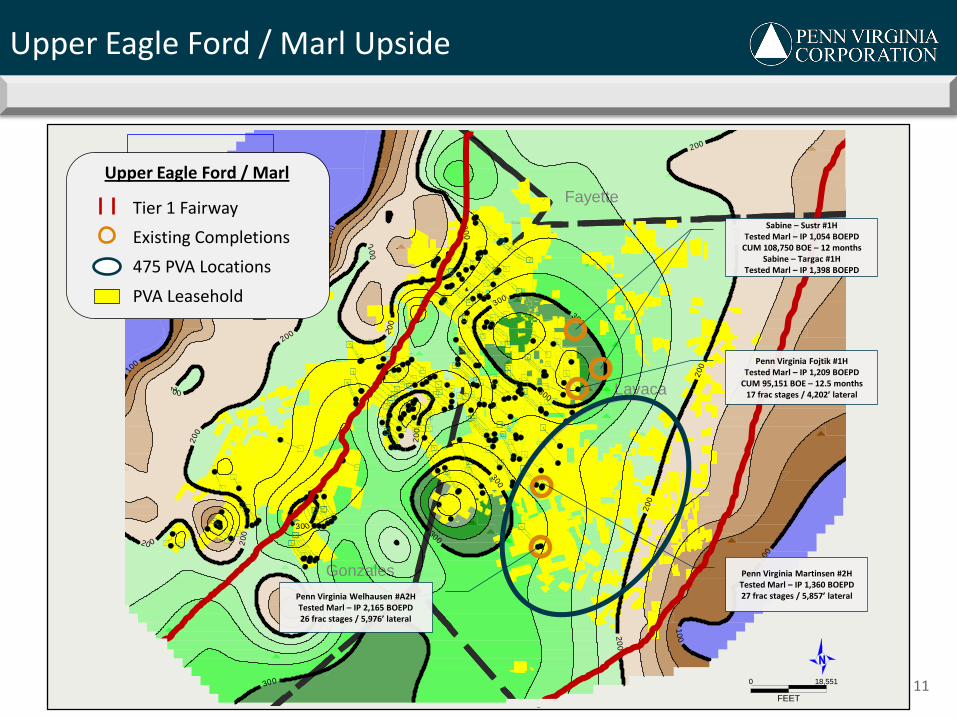

Upper Eagle Ford / Marl Upside

11

Tier 1 Fairway

Existing Completions

475 PVA Locations

PVA Leasehold

Upper Eagle Ford / Marl

Penn Virginia Martinsen #2H Tested Marl – IP 1,360 BOEPD 27 frac stages / 5,857’ lateral Penn Virginia Welhausen #A2H

Tested Marl – IP 2,165 BOEPD 26 frac stages / 5,976’ lateral

Penn Virginia Fojtik #1H Tested Marl – IP 1,209 BOEPD

CUM 95,151 BOE – 12.5 months 17 frac stages / 4,202’ lateral

Sabine – Sustr #1H Tested Marl – IP 1,054 BOEPD

CUM 108,750 BOE – 12 months Sabine – Targac #1H

Tested Marl – IP 1,398 BOEPD

• Due to acquisitions and leasing efforts, our acreage position has grown to now 126,500 gross (86,800 net) acres

• We now have ~15-year inventory of over 1,500 additional gross drilling locations • Three successful tests of Upper Eagle Ford (Marl) Shale thus far

• Successful down-spacing testing has added infill locations to our inventory

• Inventory will continue to increase with an ongoing active leasing program

12

Area Developed

Wells Remaining Locations(1)

Total Well Locations(1)

Gross Acreage

Net Acreage

Acres / Location(2)

Shiner(1) 46 939 985 58,401 46,518 59

Peach Creek 123 313 436 32,007 16,696 73

Rock Creek/Bozka 22 78 100 6,472 5,084 65

Shallow / Hunt 31 179 210 29,647 18,472 141

Totals 222 1,509 1,731 126,527 86,769 73

Note: Latest through 5/13/14 (1) Includes 474 undeveloped and 3 developed Upper Eagle Ford (Marl) Shale locations and wells in Shiner. (2) Represents gross acres per location. Actual location count depends upon lease configurations, lateral lengths and spacing between laterals.

Eagle Ford Shale Drilling Inventory

Inventory of Drilling Locations Increasing Due to Leasing and Downspacing

Gross Production Actuals vs. Type-Curve

Per Frac Stage Average Actual Monthly Production of Operated Wells vs. YE13 Type Curve

13

0

200

400

600

800

1,000

1,200

1,400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

BO

E/M

on

th/F

rac

Stag

e

Months

PEACH CREEKAverage Wellhead Performance per Frac Stage

Peach Creek Average per Frac Stage

YE13 PUD Type Curve per Frac Stage

0

200

400

600

800

1,000

1,200

1,400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

BO

E/M

on

th/F

rac

Stag

e

Months

SHINERAverage Wellhead Performance per Frac Stage

Shiner Average per Frac Stage

YE13 PUD Type Curve per Frac Stage

• Normalizing for production by frac stage, the past approximately 50 wells in Peach Creek and Shiner have a tight fit with the YE13 type curve per frac stage

• Recent enhancements, such as zipper fracs and increased frac intensity are not yet fully reflected in the actual or type curve data

Notes: (1) Based on YE13 type curve per outside reservoir engineering firm. Terminal declines of 12% in both Peach Creek and Shiner begin at 7.8 years and are higher than internal terminal decline estimates. (2) Gross EUR assumes 13.1 MBOE of EUR per frac stage in Peach Creek (11.3 thousand barrels of oil (MBO), 1.0 MBO of NGLs and 133 Mcf of gas) and 17.9 BOE per frac stage in Shiner (11.5 MBO, 3.4 MBO of NGLs and 489 Mcf of gas). (3) Assumes a flat $80 or $100 per barrel WTI oil price. (4) Capital cost plus before tax PV-10 divided by capital cost.

0

10

20

30

40

50

60

70

80

90

100

40 50 60 70 80 90 100 110 120

Rat

e o

f R

etu

rn B

FIT

-%

WTI Oil Price (Flat) - $/Bbl

SHINER FIELDPre-Tax Rate of Return Sensitivities; Assumes $9.2MM D&C Cost

$9.2MM EUR: 484 MBOE

$4.00/MMBtu HH Gas Price (Flat)

0

10

20

30

40

50

60

70

80

90

100

40 50 60 70 80 90 100 110 120

Rat

e o

f R

etu

rn B

FIT

-%

WTI Oil Price (Flat) - $/Bbl

PEACH CREEK FIELDPre-Tax Rate of Return Sensitivities; Assumes $8.4MM D&C Cost

$8.4MM EUR: 367 MBOE

$4.00/MMBtu HH Gas Price (Flat)

Eagle Ford Well Economics

Pretax IRR Sensitivities – Excellent Returns in Peach Creek and Shiner

14

Peach Creek Field

• Assumes 28 frac stages • 367 MBOE EUR type curve (1); 86% oil, 8% NGLs (2)

• Drilling and completion costs of $8.4MM ($301K/stage) • Reserves reflect 29% EUR reduction from internal estimates

and is modeled with a higher terminal decline rate

Shiner Field

• Assumes 27 frac stages • 484 MBOE EUR type curve (1); 65% oil, 19% NGLs (2)

• Drilling and completion costs of $9.2MM ($342K/stage) • Reserves reflect 29% EUR reduction from internal estimates

and is modeled with a higher terminal decline rate

Key Takeaways $80 WTI Price $100 WTI Price

IRR (3) 40% 72%

BTAX PV-10 (3) ($MM) $4.7 $8.0

PV/I (4) 1.51 1.87

Key Takeaways $80 WTI Price $100 WTI Price

IRR (3) 45% 83%

BTAX PV-10 (3) ($MM) $4.7 $7.9

PV/I (4) 1.55 1.94

PV-10 Breakeven PV-10 Breakeven

15

Maintain at Least $150 MM of

Financial Liquidity

• Liquidity of $295 MM at March 31, 2014

• Non-core asset sales underway to continue to boost liquidity and reduce indebtedness – Expected sale of MS assets for approximately $73 MM in July 2014

Target Debt-to-Adjusted EBITDAX

< 2.5x

• 1Q 2014 net leverage ratio of 3.6x (3.7x at YE13)

• Anticipate achieving goal by 2017 without additional asset sales

• Non-core asset sales accelerate this goal

Protect Cash Flows with Hedges

• ~70% of 2014 and ~50% of 2015 oil production is hedged

• Target 70% of production while leverage is higher than 3.0x

• Protect minimum $85 WTI oil price along with some upside

Continue to Invest in High Return

Development Projects

• 90%+ of capital investment is in Eagle Ford development

• Targeted rates of return of 50% – 60% at $90 WTI price (70% – 80% at $100 WTI)

• Operational flexibility to high-grade drilling strategy

Financial Strategy

Focus on a Strong Balance Sheet and Value Creation

Capitalization and Credit Stats

16 (1) Excludes impact of announced Selma Chalk divestiture for approximately $73 MM of gross proceeds. Anticipate borrowing base reduction of $37.5 MM. (2) Share price of $16.36 as of 5/30/14.

Capitalization ($ millions) 12/31/13 3/31/14

Cash 23$ 10$

Debt

Credit Facility 206$ 190$

7.25% senior notes due 2019 300$ 300$

8.50% senior notes due 2020 775$ 775$

Total debt 1,281$ 1,265$

6% convertible preferred (PVAYL: $115mm principal) 205$ 325$

Market cap 616$ 996$

Enterprise value 2,102$ 2,586$

Proved Reserves 136 136

PV-10 1,717$ 1,717$

Credit Statistics 12/31/13 3/31/14

Net Debt /

Proved reserves ($/BOE) 9.22$ 9.21$

LTM Ajdusted EBITDAX 3.7x 3.6x

PV-10 / Net Debt 1.4x 1.4x

Net Debt / Enterprise Value 60% 49%

Liquidity 242$ 295$

Company Highlights

17

Premier Eagle Ford Position

• ~86,800 acres in the Eagle Ford with ~15 years of drilling inventory, or ~12 years with accelerated drilling

• Continued acreage growth through organic leasing and bolt-on acquisitions

Operational Excellence

• Beginning to delineate Upper Eagle Ford, generating over 475 gross locations

• Efficient pad drilling and “zipper fracs” enhancing drilling returns

• Focused development program has generated substantial production growth in the Eagle Ford, increasing from 2.3 MBOE/D in 2011 to 15.2 MBOE/D in 1Q 2014

• Initial production rates continue to increase and well costs decline

Liquidity

• Planned asset sales increase liquidity

• Anticipate closing Selma Chalk divestiture in July 2014 for ~$72.7 MM

• Assets currently in the market include Granite Wash assets, and option to construct an oil gathering system

Highly Experienced Management Team

• Proven stewards of capital - increased stock price by ~215% (1) over the past year

• Average experience of ~24 years

(1) Market data as of 5/30/14.

18

Appendix

Casing Oil

Oil Gas Equiv % Choke Pressure Gravity

Location (BOPD) (MCFD) (BOEPD) Rank Oil GOR (64ths") (psi) API‐60˚

Shiner - "Beer Quad" (Mod. GOR) 1,554 1,879 1,867 74.5 1 84% 1,152 24.3 2,848 50.0

Shiner - Upper Eagle Ford (Marl) 899 4,073 1,578 68.3 2 59% 4,425 22.0 4,500 55.0

Peach Creek 1,165 662 1,275 65.6 3 92% 556 23.1 2,016 44.8

Shiner - Moderate GOR 1,050 1,256 1,259 61.6 4 84% 1,135 20.0 2,935 46.8

Rock Creek Ranch / Bozka 889 691 1,004 56.2 5 89% 771 21.1 2,261 45.6

Shiner - High GOR 836 1,863 1,147 55.3 6 74% 2,198 19.8 3,506 49.2

Shiner - Low GOR 925 759 1,052 52.8 7 87% 926 17.3 3,622 47.7

Totals and Averages 1,080 1,047 1,254 62.4 87% 1,021 21.6 2,727 47.1

Oil Gas Equiv %

Location (BOPD) (MCFD) (BOEPD) Rank 30-Day/IP Oil GOR

Shiner - "Beer Quad" (Mod. GOR) 925 1,216 1,128 43.5 2 58% 82% 1,310

Shiner - Upper Eagle Ford (Marl) 497 1,121 684 40.2 4 59% 73% 2,256

Peach Creek 692 434 764 39.4 5 60% 91% 611

Shiner - Moderate GOR 596 747 720 35.7 6 58% 83% 1,239

Rock Creek Ranch / Bozka 583 450 658 44.3 1 79% 88% 786

Shiner - High GOR 515 1,154 708 34.7 7 63% 74% 2,168

Shiner - Low GOR 692 636 798 41.8 3 79% 87% 879

Totals and Averages 661 635 766 39.3 63% 87% 983

BOEPD/

Stage

Initial Potential

BOEPD/

Stage

30-Day Average

BOEPD/

Stage

BOEPD/

Stage

BOEPD/

Stage

Detailed Analysis of EFS Wells by Location

19

Excludes Non-Operated and “Shallow” Wells

Notes - “Beer Quad” wells are moderate GOR wells, with beer types in their names, located primarily in Lavaca County to the northwest of the town of Shiner. - “Shiner - Moderate GOR” wells are located to the east and northeast of the “Beer Quad.” - Excluded shallow wells are wells with less than 10,500’ of vertical depth (defined as measured depth less lateral length). - Sorted by ranking of IP BOEPD / frac stage. - In the “Shiner - Upper Eagle Ford (Marl)” location, the 30-day information pertains to one well. The other two wells have not yet had 30 days of production information.

Detailed Analysis of EFS Wells by Location

20

Excludes Non-Operated and “Shallow” Wells

Gross Net WI

Location Wells Wells (%)

Shiner - "Beer Quad" (Mod. GOR) 11 5.5 50%

Shiner - Upper Eagle Ford (Marl) 3 2.8 94%

Peach Creek 78 48.7 62%

Shiner - Moderate GOR 12 9.1 76%

Rock Creek Ranch / Bozka 18 12.1 67%

Shiner - High GOR 22 20.0 91%

Shiner - Low GOR 10 6.6 66%

Totals and Averages 155 105.8 68%

No. of Lateral Lat. Length Actual

Frac Proppant Length per Stage VD

Location Stages (lbs) (ft) (ft/stage) (lbs) Rank (lbs) Rank (ft)

Shiner - "Beer Quad" (Mod. GOR) 25.0 7,835,782 5,736 225 306,988 2 1,368 2 12,505

Shiner - Upper Eagle Ford (Marl) 23.3 8,026,312 5,345 231 332,022 1 1,452 1 12,955

Peach Creek 20.1 4,799,045 4,821 242 234,615 7 974 7 11,334

Shiner - Moderate GOR 20.2 5,317,600 4,857 242 264,542 5 1,100 6 12,368

Rock Creek Ranch / Bozka 18.7 5,221,373 4,412 240 262,611 6 1,109 5 11,191

Shiner - High GOR 21.0 5,595,461 4,888 234 266,540 3 1,148 3 12,746

Shiner - Low GOR 20.1 5,423,609 4,753 240 264,737 4 1,128 4 12,128

Totals and Averages 20.5 5,327,049 4,854 239 253,997 1,074 11,774

Proppant

per Foot

Proppant

per Stage

Proppant

per Stage

Drilling and Completion Information

Proppant

per Foot

0

15

30

45

60

75

90

105

120

135

150

40 50 60 70 80 90 100 110 120

Rat

e o

f R

etu

rn B

FIT

-%

WTI Oil Price (Flat) - $/Bbl

SHINER FIELDPre-Tax Rate of Return Sensitivities; Assumes $9.2MM D&C Cost

$9.2MM EUR: 680 MBOE

$4.00/MMBtu HH Gas Price (Flat)

0

15

30

45

60

75

90

105

120

135

150

40 50 60 70 80 90 100 110 120

Rat

e o

f R

etu

rn B

FIT

-%

WTI Oil Price (Flat) - $/Bbl

PEACH CREEK FIELDPre-Tax Rate of Return Sensitivities; Assumes $8.4MM D&C Cost

$8.4MM EUR: 520 MBOE

$4.00/MMBtu HH Gas Price (Flat)$4.00/MMBtu HH Gas Price (Flat)

21

Internal Well Economics

Notes: (1) Based on latest internal type curve. Terminal declines of 5% in both Peach Creek and Shiner, as opposed to 12% terminal decline per outside reservoir engineering report. Internal type curves represent management's best estimates of type curves and may differ from those of our third-party reserve engineers. Financial reporting reserves are based on the type curves of our third-party reserve engineers. Both the internal type curves and those of our third-party reserve engineers are estimates based on limited data. There can be no assurance that actual production will conform with either set of type curves. (2) Gross EUR assumes 18.5 MBOE of EUR per frac stage in Peach Creek (15.9 MBO of oil, 1.4 MBO of NGLs and 188 Mcf of gas) and 25.2 BOE per frac stage in Shiner (16.2 MBO, 4.8 MBO of NGLs and 687 Mcf of gas). (3) Assumes a flat $80 or $100 per barrel WTI oil price. (4) Capital cost plus before tax PV-10 divided by capital cost.

Pretax IRR Sensitivities – Superior Returns in Peach Creek and Shiner

Peach Creek Field

• Assumes 28 frac stages • 520 MBOE EUR type curve (1); 86% oil, 8% NGLs (2)

• Drilling and completion costs of $8.4MM ($301K/stage) • Internal reserves 40% higher than YE13 third-party reserves

Shiner Field

• Assumes 27 frac stages • 680 MBOE EUR type curve (1); 65% oil, 19% NGLs (2)

• Drilling and completion costs of $9.2MM ($342K/stage) • Internal reserves 40% higher than YE13 third-party reserves

Key Takeaways $80 WTI Price $100 WTI Price

IRR (3) 61% 118%

BTAX PV-10 (3) ($MM) $7.7 $11.7

PV/I (4) 1.83 2.27

Key Takeaways $80 WTI Price $100 WTI Price

IRR (3) 69% 136%

BTAX PV-10 (3) ($MM) $7.5 $11.4

PV/I (4) 1.88 2.35

PV-10 Breakeven PV-10 Breakeven

Full-Year 2014 Guidance Table

22 (a) Assumes average benchmark prices of $90.00 per barrel for crude oil and $4.50 per MMBtu for natural gas in the final three quarters of 2014, prior to any premium or discount for quality, basin

differentials, the impact of hedges and other adjustments. NGL realized pricing is assumed to be $29.06 per barrel in the final three quarters of 2014.. (b) Adjusted EBITDAX is not a measure of financial performance under GAAP and should not be considered as a measure of liquidity or as an alternative to net income. (c) Seismic expenditures are also reported as a component of exploration expense and as a component of net cash provided by operating activities.

Full Year 2014 Guidance

4Q13 1Q14

Production:

Crude oil (MBbls) 1,024 1,076 5,700 - 6,100

NGLs (MBbls) 234 227 1,075 - 1,175

Natural gas (MMcf) 3,502 3,593 14,000 - 15,000

Equivalent production (MBOE) 1,842 1,902 9,108 - 9,775

Equivalent daily production (BOEPD) 20,020 21,133 24,954 - 26,781

Percent crude oil and NGLs 68.3% 68.5% 69.3% - 79.9%

Production revenues (a):

Crude oil $96.9 $105.6 $500.0 - $535.0

NGLs 8.1 9.4 32.0 - 35.0

Natural gas 12.1 18.2 55.0 - 60.0

Total product revenues $117.1 $133.2 $587.0 - $630.0

Total product revenues ($ per BOE) $63.58 $70.01 $60.05 - $69.17

Percent crude oil and NGLs 89.7% 86.3% 84.4% - 97.1%

Operating expenses:

Lease operating ($ per BOE) $5.74 $5.47 $5.80 - $6.40

Gathering, processing and trans. costs ($ per BOE) $1.76 $1.56 $1.70 - $1.90

Production and ad valorem taxes (% of oil and gas revenues) 2.5% 5.5% 6.5% - 7.5%

General and administrative:

Recurring general and administrative $10.9 $9.9 $40.0 - $43.0

Share-based and liability-based compensation 3.6 6.8 12.0 - 15.0

Acquisition transaction expenses 0.2 --- 0.0 - 0.0

Total reported G&A $14.7 $16.7 $52.0 - $58.0

Exploration:

Total reported exploration $2.9 $8.6 $23.0 - $25.0

Unproved property amortization 3.4 3.3 12.5 - 13.0

Depreciation, depletion and amortization ($ per BOE) $36.50 $37.95 $35.00 - $36.00

Adjusted EBITDAX (b) $84.4 $93.8 $440.0 - $485.0

Capital expenditures:

Drilling and completion $103.5 $135.5 $510.0 - $540.0

Lease acquisitions 39.6 36.9 60.0 - 83.0

Seismic (c) 0.0 4.5 10.0 - 12.0

Pipeline, gathering, facilities and other 6.4 5.6 15.0 - 18.0

Total oil and gas capital expenditures $149.5 $182.4 $595.0 - $653.0

End of period debt outstanding $1,281.0 $1,265.0 $1,390.0 - $1,450.0

Interest expense:

Total reported interest expense $22.3 $22.5 $97.0 - $100.0

Cash interest expense $21.3 $21.5 $93.0 - $96.0

Preferred stock dividends paid $1.7 $1.7 $6.9 - $6.9

Income tax benefit rate 47.4% 42.6% 35.5% - 37.5%

2014 Guidance

$4.10 $4.10

$4.50 $4.50

$0.00

$1.50

$3.00

$4.50

$6.00

0

5

10

15

20

2Q14 3Q14 4Q14 1Q15

MM

Btu

pe

r D

ay (

00

0s)

We

ighte

d A

vg. Floo

rs and

Swap

s ($/M

MB

tu)

Weighted Swap Price by Quarter

$93.54 $92.67 $92.92 $90.11 $90.11 $89.19 $89.19

$95.24 $93.39 $93.58 $92.50 $92.50 $91.88 $91.88

$30

$40

$50

$60

$70

$80

$90

$100

$110

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Bar

rels

pe

r D

ay

We

ighte

d A

vg. Floo

rs and

Swap

s ($/B

bl.)

Weighted Average Floor /Swap Price by Quarter

Weighted Average Ceiling /Swap Price by Quarter

Crude Oil Hedges (Swaps and Collars)(1) Natural Gas Hedges (Swaps and Collars)(1)

• Maintain an active hedging program to help support capital spending program and ensure strong coverage metrics

• Hedges in place to protect cash flow

• Latest oil hedges:

– 12,000 BOPD (68% of est. vol.) is hedged for 2014 at an average floor price of $93.03

– 10,500 BOPD (~50% of est. vol.) is hedged for 2015 at an average floor price of $89.71

• Latest natural gas hedges:

– 12,700 MMBtu/d (~30% of est. vol.) is hedged for 2014 at an average floor price of $4.16

23

(1) As of 5/27/14.

Protect Cash Flow

Hedging Strategy

Current Derivative Positions as of 5/27/14

Notes: (a) All or a portion of these derivatives include "lower" puts sold at a strike price of $70 per barrel. If the price of WTI oil goes below $70 per barrel, the cash receipts on the derivatives will be limited to the difference between the swap / floor price and $70 per barrel. (b) This swaption contract gives our counterparties the option to enter into a fixed price swap with us at a future date. If the forward commodity price for calendar year 2015 is higher than or equal to $88.00 per barrel on December 31, 2014, the counterparty will exercise its option to enter into a fixed price swap at $88.00 per barrel for calendar year 2015, at which point the contract functions as a fixed price swap. If the forward commodity price for calendar year 2015 is lower than $88.00 per barrel on December 31, 2014, the option expires and no fixed price swap is in effect. We estimate that as of March 31, 2014, excluding the derivative positions described above, for every $10.00 per barrel increase or decrease in the crude oil price, operating income for 2014 would increase or decrease by approximately $41.0 million. In addition, we estimate that, excluding the derivative positions described above, for every $1.00 per MMBtu increase or decrease in the natural gas price, operating income for 2014 would increase or decrease by approximately $10.6 million. This assumes that crude oil prices, natural gas prices and inlet volumes remain constant at anticipated levels. These estimated changes in operating income exclude potential cash receipts or payments in settling these derivative positions. 24

Derivatives

Weighted Average Price Instrument Type Average Volume Per Day Floor/ Swap Ceiling Natural gas: (MMBtu) ($ / MMBtu) ($ / MMBtu) Second quarter 2014 Swaps 15,000 4.10 Third quarter 2014 Swaps 15,000 4.10 Fourth quarter 2014 Swaps 5,000 4.50 First quarter 2015 Swaps 5,000 4.50 Crude oil: (barrels) ($ / barrel) ($ / barrel) Second quarter 2014 Collars 2,500 92.00 99.46 Third quarter 2014 Collars 2,000 90.00 94.33 Fourth quarter 2014 Collars 2,000 90.00 94.33 First quarter 2015 Collars (a) 4,000 87.50 94.66 Second quarter 2015 Collars (a) 4,000 87.50 94.66 Third quarter 2015 Collars (a) 3,000 86.67 94.73 Fourth quarter 2015 Collars (a) 3,000 86.67 94.73 Second quarter 2014 Swaps 8,500 94.00 Third quarter 2014 Swaps (a) 10,000 93.21 Fourth quarter 2014 Swaps (a) 11,000 93.45 First quarter 2015 Swaps (a) 8,000 91.42 Second quarter 2015 Swaps (a) 8,000 91.42 Third quarter 2015 Swaps (a) 6,000 90.45 Fourth quarter 2015 Swaps (a) 6,000 90.45 First quarter 2015 Swaption (b) 1,000 88.00 Second quarter 2015 Swaption (b) 1,000 88.00 Third quarter 2015 Swaption (b) 1,000 88.00 Fourth quarter 2015 Swaption (b) 1,000 88.00

Non-GAAP Reconciliation

25

Adjusted EBITDAX Reconciliation

Note Pro forma to include 2013 Adjusted EBITDAX from the MHR Eagle Ford Shale acquisition which was generated prior to the acquisition in April 2013.

2009 2010 2011 2012 2013

Adjusted EBITDAX

Net income (loss) from continuing operations $ (130.9) $ (65.3) $ (132.9) $ (104.6) $ (143.1) $ (107.5)

Add: Income tax expense (benefit) (85.9) (42.9) (88.2) (68.7) (77.7) (54.6)

Add: Interest expense 44.2 53.7 56.2 59.3 78.8 86.9

Add: Depreciation, depletion and amortization 154.4 134.7 162.5 206.3 245.6 266.2

Add: Exploration 57.8 49.6 78.9 34.1 21.0 23.3

Add: Share-based compensation expense 9.1 7.8 7.4 6.3 5.8 5.5

Add/Less: Derivatives (income) expense included in net income (31.6) (41.9) (15.7) (36.2) 20.9 28.8

Add/Less: Cash receipts (payments) to settle derivatives 58.1 32.8 27.4 29.7 (1.0) (7.7)

Add/Less: Loss on firm transportation commitment - - - 17.3 - -

Add: Impairments 106.4 46.0 104.7 104.5 132.2 132.2

Add/Less: Net loss (gain) on sale of assets, other (2.0) (1.2) 22.0 (0.6) 33.7 (23.5)

Adjusted EBITDAX $ 179.7 $ 173.3 $ 222.5 $ 247.6 $ 316.2 $ 349.6

Pro Forma Adjusted EBITDAX $ 342.4 $ 353.3

dollars in millions

Year ended December 31, LTM

1Q14

26

Adjusted Net Loss Reconciliation

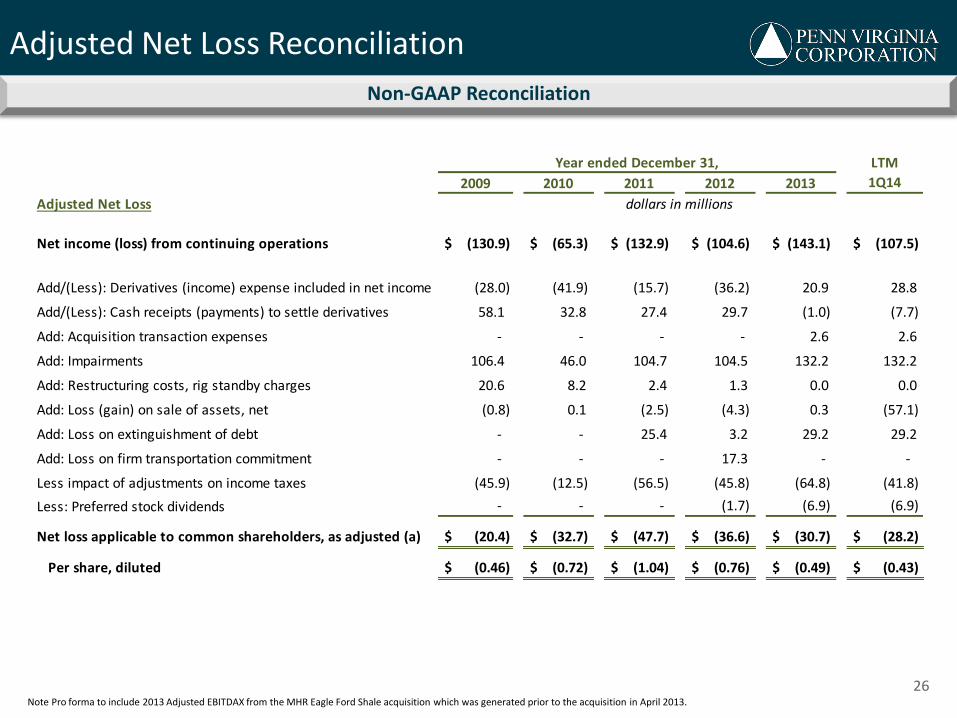

Non-GAAP Reconciliation

Note Pro forma to include 2013 Adjusted EBITDAX from the MHR Eagle Ford Shale acquisition which was generated prior to the acquisition in April 2013.

2009 2010 2011 2012 2013

Adjusted Net Loss

Net income (loss) from continuing operations $ (130.9) $ (65.3) $ (132.9) $ (104.6) $ (143.1) $ (107.5)

Add/(Less): Derivatives (income) expense included in net income (28.0) (41.9) (15.7) (36.2) 20.9 28.8

Add/(Less): Cash receipts (payments) to settle derivatives 58.1 32.8 27.4 29.7 (1.0) (7.7)

Add: Acquisition transaction expenses - - - - 2.6 2.6

Add: Impairments 106.4 46.0 104.7 104.5 132.2 132.2

Add: Restructuring costs, rig standby charges 20.6 8.2 2.4 1.3 0.0 0.0

Add: Loss (gain) on sale of assets, net (0.8) 0.1 (2.5) (4.3) 0.3 (57.1)

Add: Loss on extinguishment of debt - - 25.4 3.2 29.2 29.2

Add: Loss on firm transportation commitment - - - 17.3 - -

Less impact of adjustments on income taxes (45.9) (12.5) (56.5) (45.8) (64.8) (41.8)

Less: Preferred stock dividends - - - (1.7) (6.9) (6.9)

Net loss applicable to common shareholders, as adjusted (a) $ (20.4) $ (32.7) $ (47.7) $ (36.6) $ (30.7) $ (28.2)

Per share, diluted $ (0.46) $ (0.72) $ (1.04) $ (0.76) $ (0.49) $ (0.43)

dollars in millions

Year ended December 31, LTM

1Q14