income from personal services and employment

DESCRIPTION

Income From Personal Services and EmploymentTRANSCRIPT

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 129

Chapter 6

Income from personal services and

employment

983209

2015 Thomson Reuters (Professional) ustralia td ll Rihts Reserved$onathan Teoh amponash niversity

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 229

Introduction

receipt from employment and providin personal servicesmay e suect to income ta+ or frine enefits ta+

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 329

rdinary income reard for services

Nexus connection or ne+us ith a receipt resultin from a ta+payer3spersonal service constitutes ordinary income

Courts have used a to4step approach to determine if an amountis ordinary income from personal services

1 Identification of the activity undertaen and

2 7eterminin hether the receipt is a reard for performinthat particular activity

enuine salary sacrifice has no ne+us under ordinaryconcepts

PoT 2015 pararaphs -620 8 -690 -660

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 429

rdinary income reard for services

Nexus clearly established e+us clearly estalished for common items of personale+ertion includin

8 alary and aes

8 Commissions

8 ltonuses

8 =ees chared for services rendered

8 ncillary payments that are an incident of laour

e+us not impacted y lump4sum or one4off receipts for the

performance of a specific tas

8 ee Brent v FCT (1971)

It is irrelevant ho pays or hen it is paid Kelly v FCT (1gt5)

PoT 2015 pararaphs -60 8 -650

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 529

rdinary income reard for services

Nexus uncertain - voluntary payments ne+pected or voluntary payments received as an incidenceof employment constitutes ordinary income =or e+ample

8 Christmas onuses paid to employees paid in the form of

redeemale ift vouchers Laidler v Perry (1gt65)

8 Tips received y a ta+i driver Calvert v Wainwright (1gtA)

8 ote possile to characterise as ordinary income ased on the

nature of payment (income characteristics) rather than ne+us

8 dditional periodic payments as a sustitute for aes that

ere relied upon y the ta+payer FCT v Dixon (1gt52)

PoT 2015 pararaphs -6A0 8 -60

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 629

rdinary income reard for services

Nexus uncertain - gifts Bifts

8 =or personal ualities is not rearded as ordinary income

8 risin from the ta+payer3s aility to or andDor the

employment contract is ordinary income

ecessary to distinuish eteen the aove here a ift is

made and there is an employment or commercial connection

8 Importance of a personal relationship eteen the parties

Sott v FCT (1gt66)

PoT 2015 pararaph -6gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 729

rdinary income reard for services

Nexus uncertain - gifts on4determinative factors to consider in orderline cases

8 E+pectation of the ift Sott v FCT (1gt66)

8 ump sum or reular payments FCT v Blae (1gt)

8 ampotive of the donor (note eiht placed on the nature of

receipt in the hands of the recipient) Sott v FCT (1gt66)

8 Fhether the recipient has een fully remunerated for

services provided Sott v FCT (1gt66) aye$ v FCT (1gt56)

8 Personal relationship Sott v FCT (1gt66) aye$ v FCT

(1gt56)

PoT 2015 pararaph -6100

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 829

rdinary income reard for services

Nexus uncertain - prizes PriGes and chance innins are non4assessale if the indfallain is derived y luc

8 Finnins of a casual participant on a TH sho Ca$e 7

(1gt66) Rulin IT 16A

lternatively ordinary income if derived y e+ercisin deree ofsill (personal e+ertion) that sufficiently outeihs luc

8 Professional sportin people Kelly v FCT (1gt5)

8 Irrelevant that payment does not arise from employer

PoT 2015 pararaph -6110

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 929

rdinary income reard for services

Nexus uncertain - prizes 7ifficulty ith determinin the sufficient deree of sill thatouteihs luc Consideration factors include

PoT 2015 pararaph -6120

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1029

rdinary income reard for services

Non-cash benefits Prereuisites of ordinary income

non4cash enefit may have a ne+us ith personal e+ertion

hoever if not convertile to cash3 it is not ordinary income

8 Redemption of freuent flyer points that ere accrued from

or4related travel Payne v FCT (1gtgt6)

ote may hoever e assessale under s 1542 ITgtA or

suect to frine enefits ta+

PoT 2015 pararaph -6190

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1129

rdinary income reard for servicesCapital receipt or personal exertion ecessary to distinuish eteen ordinary income receipts

and capital receipts (not ordinary income)

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1229

Capital receipt or personal e+ertionChanges to entitlements ain from a chane to entitlements under employment or

service contracts taes the character of hat it replaces

8 Relinuishin employment rihts (e rihts to control a

company as manain director) Bennett v FCT (1gtA)

8 oss of employee entitlements ampampT Ca$e 77

PoT 2015 pararaph -6150

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1329

Capital receipt or personal e+ertionRestrictive covenants Restrictive covenant or restraint of trade may e formed

rdinary income if connected ith the current employmentareement (ie payment of future services)

Capital characterisation

8 eparate areement to ive up valuale rihts igg$ v

livier (1gt52) FCT v Woite (1gt2) 8 o ne+us ith earnin activity (e payment made at end of

contract) e++le$ v FCT (1gtgt1)

8 ote capital ains ta+ may apply (CBT event 71)

PoT 2015 pararaphs -6160 8 -61A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1429

Capital receipt or personal e+ertionSign-on fees in4on (enticement) fees as part of normal practices of

attractin people into a ne employment contract

8 Characterised as a payment for future services (ordinary

income) Piord v FCT (1gtgt) Rulin TR 1gtgtgtD1A

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1529

tatutory incomeServices and employment (s 1- ltroad provision that rins the value of certain ains from

laour into assessale income includin non4cash enefits

that are not convertile to cash under ordinary concepts

8 Consider application of s 1542 only if s 645 does not apply

pplies hen the folloin three reuirements are satisfied

PoT 2015 pararaph -61gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1629

tatutory incomeServices and employment (s 1- irst re$uirement

There is an alloance ratuity compensation enefit onus

or premium

Reuirement has a ide scope and ould include

8 Cash cash convertile or non4cash convertile receipts

8 Holuntary receipts (e ratuities)

8 E+ternal arranements (e an accountin firm3s employee

receives free hotel accommodation from a client)

Second re$uirement

Ta+payer is reuired to receive the first reuirement (ie

provided to you)

PoT 2015 pararaphs -6200 8 -6210

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1729

tatutory incomeServices and employment (s 1- hird re$uirement

e+us must e estalished The ain must e

8 J in respect of or for or in relation directly or indirectly toany employment or services rendered y the ta+payer

Easier to estalish ne+us under s 1542 than ordinary income

8 mounts paid y an employer to its employee on completionof relevant tertiary suects S-ith v FCT (1gtA)

8 Reard money for helpin to prevent disaster FCT v

ol-e$ (1gtgt5) Insufficient ne+us for redemption of freuent flyer points that

ere accrued from or4related travel Payne v FCT (1gtgt6)

PoT 2015 pararaph -6220

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1829

tatutory incomeServices and employment (s 1- Relationship ampith other tax provisions

ection 1542 ill not apply under certain circumstances

Key e+clusions include

PoT 2015 pararaph -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1929

tatutory incomeReturn to ampor payments (s 1- Payments made to a ta+payer as an inducement to return to

or or to provide services constitutes statutory income

8 ame position under income from ordinary concepts

(ordinary income s 645)

PoT 2015 pararaph -6250

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2029

Payments upon termination of employment

pecific provisions prescriin ta+ation treatment of paymentsmade in connection to the termination of employment

ampain termination payments include

PoT 2015 pararaph -6260

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2129

Payments upon termination of employment)mployment termination payments To road su4types of ETPs

Reuirements for a payment to e an ETP under s 24190

8 Payment is in conseuence of the employment termination

8 There as in fact a enuine termination payment

8 The payment does not fall ithin an e+clusion esuperannuation payments pensions and annuities enuineredundancy payments or early retirement scheme payments

PoT 2015 pararaphs -62A0 8 -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2229

Payments upon termination of employment)mployment termination payments +n conse$uence of termination of employment

Employment termination needs to e one of the causes for the

ETP ut does not need e the dominant cause) e$e v FCT

(1gtA5) Le rand v FCT (2002)

=act that termination and payment occurs are similar times isinsufficient to estalish causation ltrennan $ in 0nto$h v FCT

(1gtAgt)

enuine termination

Termination includes cessation of employment due toretirement or death s 0410

8 =i+ed4term position made permanent not rearded as a

termination realy v FCT (1gtgt)

PoT 2015 pararaphs -62gt0 8 -6910

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2329

Payments upon termination of employment)mployment termination payments axation of )s

To components

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2429

Payments upon termination of employment)mployment termination payments Ta+ale component of a lie 2eneit ter-ination +ay-ent

ltroadly the threshold amount is the loer of (s 2410()) 8 L15000 (for 201D15) and

8 L10000 hole of income cap3 hich is reduced y anynon4ETP ta+ale income and suect to certain e+clusions

) taxablecomponentamount

axpayer is atpreservation age( years

axable is beloamppreservation age(0 years

0 8 threshold Ta+ed at normal marinal

rates ut capped at a rateof 15M plus 2M ampedicarelevy

Ta+ed at normal marinal

rates ut capped at a rateof 90M plus 2M ampedicareevy

mounts overthe threshold

Ta+ed at AM plus 2Mampedicare levy

Ta+ed at AM plus 2Mampedicare levy

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2529

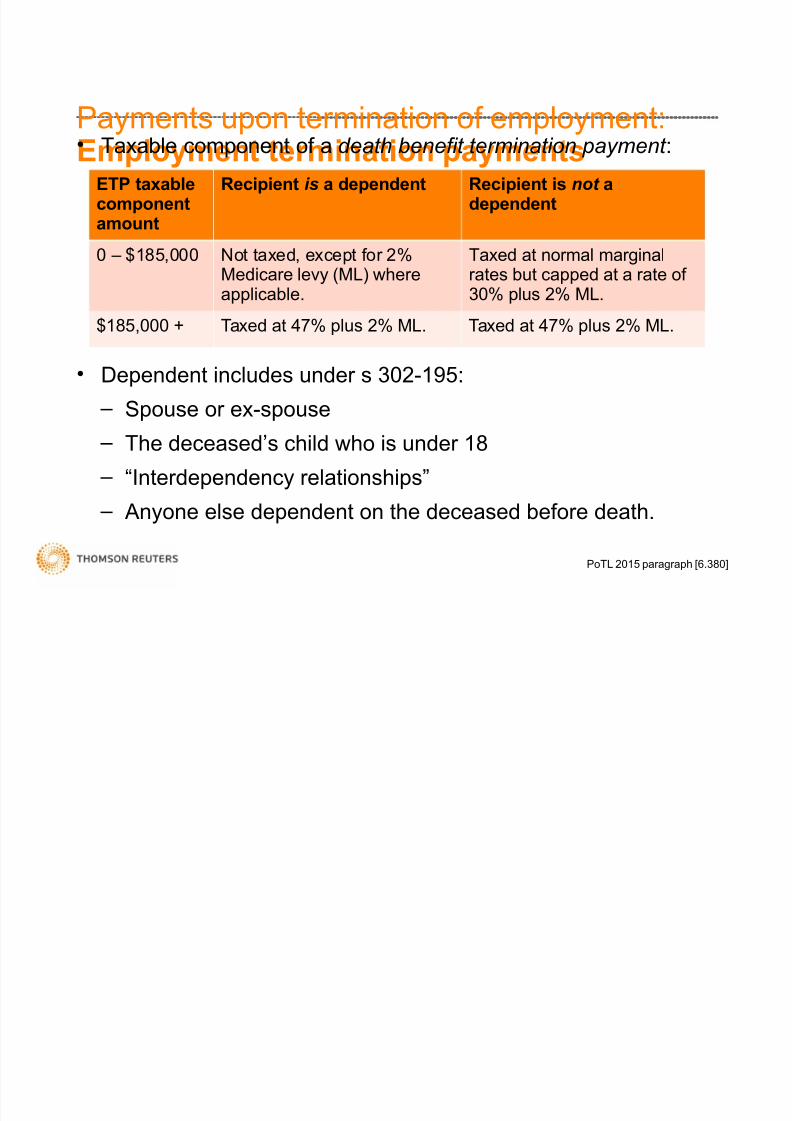

Payments upon termination of employment)mployment termination payments Ta+ale component of a death 2eneit ter-ination +ay-ent

7ependent includes under s 90241gt5

8 pouse or e+4spouse 8 The deceased3s child ho is under 1

8 Interdependency relationships

8 nyone else dependent on the deceased efore death

) taxablecomponentamount

Recipient is a dependent Recipient is not adependent

0 8 L15000 ot ta+ed e+cept for 2M

ampedicare levy (amp) hereapplicale

Ta+ed at normal marinal

rates ut capped at a rate of90M plus 2M amp

L15000 N Ta+ed at AM plus 2M amp Ta+ed at AM plus 2M amp

PoT 2015 pararaph -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2629

Payments upon termination of employmentenuine redundancy and early retirements Benuine redundancy payment is a payment made to an

employee hose position is enuinely made redundant

Early retirement scheme satisfies the folloin conditions

8 cheme is open to all eliile employees

8 Employer3s purpose of havin the scheme is to reoranise

the operations of the orplace and

8 The Commissioner has approved the scheme as an early

retirement scheme

PoT 2015 pararaphs -6920 8 -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2729

Payments upon termination of employmentenuine redundancy and early retirements =urther conditions e+ist in ss 941A5 and 9410 for payments

to e considered redundancy payments and early retirement

scheme payments

8 The employee must e dismissed efore heDshe reaches 65

years of ae 8 The payment must represent hat ould e payale under a

normal commercial arranement

8 There must e no arranement at the time of dismissal that

the employee e re4employed y the employer

PoT 2015 pararaph -6950

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2829

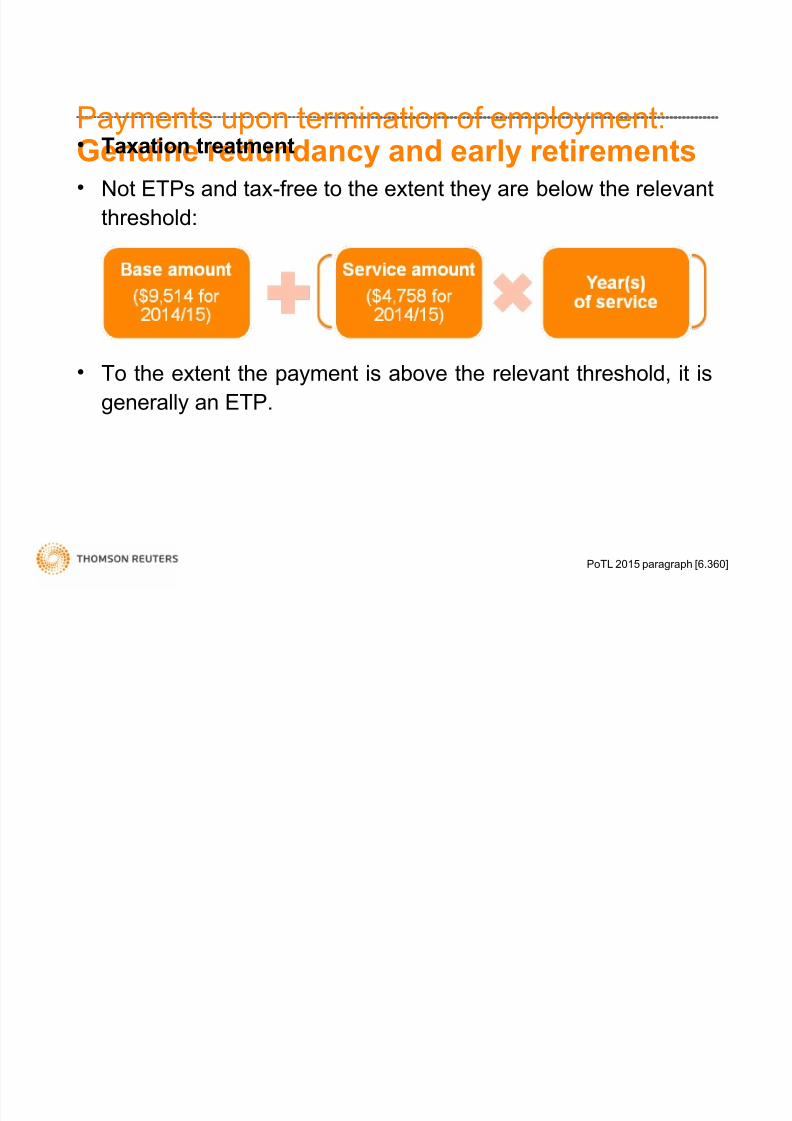

Payments upon termination of employmentenuine redundancy and early retirements axation treatment

ot ETPs and ta+4free to the e+tent they are elo the relevant

threshold

To the e+tent the payment is aove the relevant threshold it is

enerally an ETP

PoT 2015 pararaph -6960

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2929

Payments upon termination of employmentnused annual and long service leave nnual leave and lon service leave payments are enerally

ta+ed at normal marinal ta+ rates

Concessional treatment (capped at the rate of 90M plus

ampedicare levy) under certain circumstances includin

8 Payment due to leave accruals in respect of servicesperformed efore 1 uust 1gtgt9 or

8 Payment as in connection ith a payment that consists of

a enuine redundancy payment or early retirement scheme

payment or an invalidity sement of an ETP

PoT 2015 pararaph -69gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 229

Introduction

receipt from employment and providin personal servicesmay e suect to income ta+ or frine enefits ta+

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 329

rdinary income reard for services

Nexus connection or ne+us ith a receipt resultin from a ta+payer3spersonal service constitutes ordinary income

Courts have used a to4step approach to determine if an amountis ordinary income from personal services

1 Identification of the activity undertaen and

2 7eterminin hether the receipt is a reard for performinthat particular activity

enuine salary sacrifice has no ne+us under ordinaryconcepts

PoT 2015 pararaphs -620 8 -690 -660

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 429

rdinary income reard for services

Nexus clearly established e+us clearly estalished for common items of personale+ertion includin

8 alary and aes

8 Commissions

8 ltonuses

8 =ees chared for services rendered

8 ncillary payments that are an incident of laour

e+us not impacted y lump4sum or one4off receipts for the

performance of a specific tas

8 ee Brent v FCT (1971)

It is irrelevant ho pays or hen it is paid Kelly v FCT (1gt5)

PoT 2015 pararaphs -60 8 -650

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 529

rdinary income reard for services

Nexus uncertain - voluntary payments ne+pected or voluntary payments received as an incidenceof employment constitutes ordinary income =or e+ample

8 Christmas onuses paid to employees paid in the form of

redeemale ift vouchers Laidler v Perry (1gt65)

8 Tips received y a ta+i driver Calvert v Wainwright (1gtA)

8 ote possile to characterise as ordinary income ased on the

nature of payment (income characteristics) rather than ne+us

8 dditional periodic payments as a sustitute for aes that

ere relied upon y the ta+payer FCT v Dixon (1gt52)

PoT 2015 pararaphs -6A0 8 -60

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 629

rdinary income reard for services

Nexus uncertain - gifts Bifts

8 =or personal ualities is not rearded as ordinary income

8 risin from the ta+payer3s aility to or andDor the

employment contract is ordinary income

ecessary to distinuish eteen the aove here a ift is

made and there is an employment or commercial connection

8 Importance of a personal relationship eteen the parties

Sott v FCT (1gt66)

PoT 2015 pararaph -6gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 729

rdinary income reard for services

Nexus uncertain - gifts on4determinative factors to consider in orderline cases

8 E+pectation of the ift Sott v FCT (1gt66)

8 ump sum or reular payments FCT v Blae (1gt)

8 ampotive of the donor (note eiht placed on the nature of

receipt in the hands of the recipient) Sott v FCT (1gt66)

8 Fhether the recipient has een fully remunerated for

services provided Sott v FCT (1gt66) aye$ v FCT (1gt56)

8 Personal relationship Sott v FCT (1gt66) aye$ v FCT

(1gt56)

PoT 2015 pararaph -6100

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 829

rdinary income reard for services

Nexus uncertain - prizes PriGes and chance innins are non4assessale if the indfallain is derived y luc

8 Finnins of a casual participant on a TH sho Ca$e 7

(1gt66) Rulin IT 16A

lternatively ordinary income if derived y e+ercisin deree ofsill (personal e+ertion) that sufficiently outeihs luc

8 Professional sportin people Kelly v FCT (1gt5)

8 Irrelevant that payment does not arise from employer

PoT 2015 pararaph -6110

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 929

rdinary income reard for services

Nexus uncertain - prizes 7ifficulty ith determinin the sufficient deree of sill thatouteihs luc Consideration factors include

PoT 2015 pararaph -6120

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1029

rdinary income reard for services

Non-cash benefits Prereuisites of ordinary income

non4cash enefit may have a ne+us ith personal e+ertion

hoever if not convertile to cash3 it is not ordinary income

8 Redemption of freuent flyer points that ere accrued from

or4related travel Payne v FCT (1gtgt6)

ote may hoever e assessale under s 1542 ITgtA or

suect to frine enefits ta+

PoT 2015 pararaph -6190

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1129

rdinary income reard for servicesCapital receipt or personal exertion ecessary to distinuish eteen ordinary income receipts

and capital receipts (not ordinary income)

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1229

Capital receipt or personal e+ertionChanges to entitlements ain from a chane to entitlements under employment or

service contracts taes the character of hat it replaces

8 Relinuishin employment rihts (e rihts to control a

company as manain director) Bennett v FCT (1gtA)

8 oss of employee entitlements ampampT Ca$e 77

PoT 2015 pararaph -6150

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1329

Capital receipt or personal e+ertionRestrictive covenants Restrictive covenant or restraint of trade may e formed

rdinary income if connected ith the current employmentareement (ie payment of future services)

Capital characterisation

8 eparate areement to ive up valuale rihts igg$ v

livier (1gt52) FCT v Woite (1gt2) 8 o ne+us ith earnin activity (e payment made at end of

contract) e++le$ v FCT (1gtgt1)

8 ote capital ains ta+ may apply (CBT event 71)

PoT 2015 pararaphs -6160 8 -61A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1429

Capital receipt or personal e+ertionSign-on fees in4on (enticement) fees as part of normal practices of

attractin people into a ne employment contract

8 Characterised as a payment for future services (ordinary

income) Piord v FCT (1gtgt) Rulin TR 1gtgtgtD1A

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1529

tatutory incomeServices and employment (s 1- ltroad provision that rins the value of certain ains from

laour into assessale income includin non4cash enefits

that are not convertile to cash under ordinary concepts

8 Consider application of s 1542 only if s 645 does not apply

pplies hen the folloin three reuirements are satisfied

PoT 2015 pararaph -61gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1629

tatutory incomeServices and employment (s 1- irst re$uirement

There is an alloance ratuity compensation enefit onus

or premium

Reuirement has a ide scope and ould include

8 Cash cash convertile or non4cash convertile receipts

8 Holuntary receipts (e ratuities)

8 E+ternal arranements (e an accountin firm3s employee

receives free hotel accommodation from a client)

Second re$uirement

Ta+payer is reuired to receive the first reuirement (ie

provided to you)

PoT 2015 pararaphs -6200 8 -6210

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1729

tatutory incomeServices and employment (s 1- hird re$uirement

e+us must e estalished The ain must e

8 J in respect of or for or in relation directly or indirectly toany employment or services rendered y the ta+payer

Easier to estalish ne+us under s 1542 than ordinary income

8 mounts paid y an employer to its employee on completionof relevant tertiary suects S-ith v FCT (1gtA)

8 Reard money for helpin to prevent disaster FCT v

ol-e$ (1gtgt5) Insufficient ne+us for redemption of freuent flyer points that

ere accrued from or4related travel Payne v FCT (1gtgt6)

PoT 2015 pararaph -6220

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1829

tatutory incomeServices and employment (s 1- Relationship ampith other tax provisions

ection 1542 ill not apply under certain circumstances

Key e+clusions include

PoT 2015 pararaph -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1929

tatutory incomeReturn to ampor payments (s 1- Payments made to a ta+payer as an inducement to return to

or or to provide services constitutes statutory income

8 ame position under income from ordinary concepts

(ordinary income s 645)

PoT 2015 pararaph -6250

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2029

Payments upon termination of employment

pecific provisions prescriin ta+ation treatment of paymentsmade in connection to the termination of employment

ampain termination payments include

PoT 2015 pararaph -6260

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2129

Payments upon termination of employment)mployment termination payments To road su4types of ETPs

Reuirements for a payment to e an ETP under s 24190

8 Payment is in conseuence of the employment termination

8 There as in fact a enuine termination payment

8 The payment does not fall ithin an e+clusion esuperannuation payments pensions and annuities enuineredundancy payments or early retirement scheme payments

PoT 2015 pararaphs -62A0 8 -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2229

Payments upon termination of employment)mployment termination payments +n conse$uence of termination of employment

Employment termination needs to e one of the causes for the

ETP ut does not need e the dominant cause) e$e v FCT

(1gtA5) Le rand v FCT (2002)

=act that termination and payment occurs are similar times isinsufficient to estalish causation ltrennan $ in 0nto$h v FCT

(1gtAgt)

enuine termination

Termination includes cessation of employment due toretirement or death s 0410

8 =i+ed4term position made permanent not rearded as a

termination realy v FCT (1gtgt)

PoT 2015 pararaphs -62gt0 8 -6910

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2329

Payments upon termination of employment)mployment termination payments axation of )s

To components

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2429

Payments upon termination of employment)mployment termination payments Ta+ale component of a lie 2eneit ter-ination +ay-ent

ltroadly the threshold amount is the loer of (s 2410()) 8 L15000 (for 201D15) and

8 L10000 hole of income cap3 hich is reduced y anynon4ETP ta+ale income and suect to certain e+clusions

) taxablecomponentamount

axpayer is atpreservation age( years

axable is beloamppreservation age(0 years

0 8 threshold Ta+ed at normal marinal

rates ut capped at a rateof 15M plus 2M ampedicarelevy

Ta+ed at normal marinal

rates ut capped at a rateof 90M plus 2M ampedicareevy

mounts overthe threshold

Ta+ed at AM plus 2Mampedicare levy

Ta+ed at AM plus 2Mampedicare levy

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2529

Payments upon termination of employment)mployment termination payments Ta+ale component of a death 2eneit ter-ination +ay-ent

7ependent includes under s 90241gt5

8 pouse or e+4spouse 8 The deceased3s child ho is under 1

8 Interdependency relationships

8 nyone else dependent on the deceased efore death

) taxablecomponentamount

Recipient is a dependent Recipient is not adependent

0 8 L15000 ot ta+ed e+cept for 2M

ampedicare levy (amp) hereapplicale

Ta+ed at normal marinal

rates ut capped at a rate of90M plus 2M amp

L15000 N Ta+ed at AM plus 2M amp Ta+ed at AM plus 2M amp

PoT 2015 pararaph -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2629

Payments upon termination of employmentenuine redundancy and early retirements Benuine redundancy payment is a payment made to an

employee hose position is enuinely made redundant

Early retirement scheme satisfies the folloin conditions

8 cheme is open to all eliile employees

8 Employer3s purpose of havin the scheme is to reoranise

the operations of the orplace and

8 The Commissioner has approved the scheme as an early

retirement scheme

PoT 2015 pararaphs -6920 8 -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2729

Payments upon termination of employmentenuine redundancy and early retirements =urther conditions e+ist in ss 941A5 and 9410 for payments

to e considered redundancy payments and early retirement

scheme payments

8 The employee must e dismissed efore heDshe reaches 65

years of ae 8 The payment must represent hat ould e payale under a

normal commercial arranement

8 There must e no arranement at the time of dismissal that

the employee e re4employed y the employer

PoT 2015 pararaph -6950

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2829

Payments upon termination of employmentenuine redundancy and early retirements axation treatment

ot ETPs and ta+4free to the e+tent they are elo the relevant

threshold

To the e+tent the payment is aove the relevant threshold it is

enerally an ETP

PoT 2015 pararaph -6960

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2929

Payments upon termination of employmentnused annual and long service leave nnual leave and lon service leave payments are enerally

ta+ed at normal marinal ta+ rates

Concessional treatment (capped at the rate of 90M plus

ampedicare levy) under certain circumstances includin

8 Payment due to leave accruals in respect of servicesperformed efore 1 uust 1gtgt9 or

8 Payment as in connection ith a payment that consists of

a enuine redundancy payment or early retirement scheme

payment or an invalidity sement of an ETP

PoT 2015 pararaph -69gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 329

rdinary income reard for services

Nexus connection or ne+us ith a receipt resultin from a ta+payer3spersonal service constitutes ordinary income

Courts have used a to4step approach to determine if an amountis ordinary income from personal services

1 Identification of the activity undertaen and

2 7eterminin hether the receipt is a reard for performinthat particular activity

enuine salary sacrifice has no ne+us under ordinaryconcepts

PoT 2015 pararaphs -620 8 -690 -660

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 429

rdinary income reard for services

Nexus clearly established e+us clearly estalished for common items of personale+ertion includin

8 alary and aes

8 Commissions

8 ltonuses

8 =ees chared for services rendered

8 ncillary payments that are an incident of laour

e+us not impacted y lump4sum or one4off receipts for the

performance of a specific tas

8 ee Brent v FCT (1971)

It is irrelevant ho pays or hen it is paid Kelly v FCT (1gt5)

PoT 2015 pararaphs -60 8 -650

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 529

rdinary income reard for services

Nexus uncertain - voluntary payments ne+pected or voluntary payments received as an incidenceof employment constitutes ordinary income =or e+ample

8 Christmas onuses paid to employees paid in the form of

redeemale ift vouchers Laidler v Perry (1gt65)

8 Tips received y a ta+i driver Calvert v Wainwright (1gtA)

8 ote possile to characterise as ordinary income ased on the

nature of payment (income characteristics) rather than ne+us

8 dditional periodic payments as a sustitute for aes that

ere relied upon y the ta+payer FCT v Dixon (1gt52)

PoT 2015 pararaphs -6A0 8 -60

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 629

rdinary income reard for services

Nexus uncertain - gifts Bifts

8 =or personal ualities is not rearded as ordinary income

8 risin from the ta+payer3s aility to or andDor the

employment contract is ordinary income

ecessary to distinuish eteen the aove here a ift is

made and there is an employment or commercial connection

8 Importance of a personal relationship eteen the parties

Sott v FCT (1gt66)

PoT 2015 pararaph -6gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 729

rdinary income reard for services

Nexus uncertain - gifts on4determinative factors to consider in orderline cases

8 E+pectation of the ift Sott v FCT (1gt66)

8 ump sum or reular payments FCT v Blae (1gt)

8 ampotive of the donor (note eiht placed on the nature of

receipt in the hands of the recipient) Sott v FCT (1gt66)

8 Fhether the recipient has een fully remunerated for

services provided Sott v FCT (1gt66) aye$ v FCT (1gt56)

8 Personal relationship Sott v FCT (1gt66) aye$ v FCT

(1gt56)

PoT 2015 pararaph -6100

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 829

rdinary income reard for services

Nexus uncertain - prizes PriGes and chance innins are non4assessale if the indfallain is derived y luc

8 Finnins of a casual participant on a TH sho Ca$e 7

(1gt66) Rulin IT 16A

lternatively ordinary income if derived y e+ercisin deree ofsill (personal e+ertion) that sufficiently outeihs luc

8 Professional sportin people Kelly v FCT (1gt5)

8 Irrelevant that payment does not arise from employer

PoT 2015 pararaph -6110

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 929

rdinary income reard for services

Nexus uncertain - prizes 7ifficulty ith determinin the sufficient deree of sill thatouteihs luc Consideration factors include

PoT 2015 pararaph -6120

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1029

rdinary income reard for services

Non-cash benefits Prereuisites of ordinary income

non4cash enefit may have a ne+us ith personal e+ertion

hoever if not convertile to cash3 it is not ordinary income

8 Redemption of freuent flyer points that ere accrued from

or4related travel Payne v FCT (1gtgt6)

ote may hoever e assessale under s 1542 ITgtA or

suect to frine enefits ta+

PoT 2015 pararaph -6190

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1129

rdinary income reard for servicesCapital receipt or personal exertion ecessary to distinuish eteen ordinary income receipts

and capital receipts (not ordinary income)

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1229

Capital receipt or personal e+ertionChanges to entitlements ain from a chane to entitlements under employment or

service contracts taes the character of hat it replaces

8 Relinuishin employment rihts (e rihts to control a

company as manain director) Bennett v FCT (1gtA)

8 oss of employee entitlements ampampT Ca$e 77

PoT 2015 pararaph -6150

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1329

Capital receipt or personal e+ertionRestrictive covenants Restrictive covenant or restraint of trade may e formed

rdinary income if connected ith the current employmentareement (ie payment of future services)

Capital characterisation

8 eparate areement to ive up valuale rihts igg$ v

livier (1gt52) FCT v Woite (1gt2) 8 o ne+us ith earnin activity (e payment made at end of

contract) e++le$ v FCT (1gtgt1)

8 ote capital ains ta+ may apply (CBT event 71)

PoT 2015 pararaphs -6160 8 -61A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1429

Capital receipt or personal e+ertionSign-on fees in4on (enticement) fees as part of normal practices of

attractin people into a ne employment contract

8 Characterised as a payment for future services (ordinary

income) Piord v FCT (1gtgt) Rulin TR 1gtgtgtD1A

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1529

tatutory incomeServices and employment (s 1- ltroad provision that rins the value of certain ains from

laour into assessale income includin non4cash enefits

that are not convertile to cash under ordinary concepts

8 Consider application of s 1542 only if s 645 does not apply

pplies hen the folloin three reuirements are satisfied

PoT 2015 pararaph -61gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1629

tatutory incomeServices and employment (s 1- irst re$uirement

There is an alloance ratuity compensation enefit onus

or premium

Reuirement has a ide scope and ould include

8 Cash cash convertile or non4cash convertile receipts

8 Holuntary receipts (e ratuities)

8 E+ternal arranements (e an accountin firm3s employee

receives free hotel accommodation from a client)

Second re$uirement

Ta+payer is reuired to receive the first reuirement (ie

provided to you)

PoT 2015 pararaphs -6200 8 -6210

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1729

tatutory incomeServices and employment (s 1- hird re$uirement

e+us must e estalished The ain must e

8 J in respect of or for or in relation directly or indirectly toany employment or services rendered y the ta+payer

Easier to estalish ne+us under s 1542 than ordinary income

8 mounts paid y an employer to its employee on completionof relevant tertiary suects S-ith v FCT (1gtA)

8 Reard money for helpin to prevent disaster FCT v

ol-e$ (1gtgt5) Insufficient ne+us for redemption of freuent flyer points that

ere accrued from or4related travel Payne v FCT (1gtgt6)

PoT 2015 pararaph -6220

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1829

tatutory incomeServices and employment (s 1- Relationship ampith other tax provisions

ection 1542 ill not apply under certain circumstances

Key e+clusions include

PoT 2015 pararaph -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1929

tatutory incomeReturn to ampor payments (s 1- Payments made to a ta+payer as an inducement to return to

or or to provide services constitutes statutory income

8 ame position under income from ordinary concepts

(ordinary income s 645)

PoT 2015 pararaph -6250

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2029

Payments upon termination of employment

pecific provisions prescriin ta+ation treatment of paymentsmade in connection to the termination of employment

ampain termination payments include

PoT 2015 pararaph -6260

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2129

Payments upon termination of employment)mployment termination payments To road su4types of ETPs

Reuirements for a payment to e an ETP under s 24190

8 Payment is in conseuence of the employment termination

8 There as in fact a enuine termination payment

8 The payment does not fall ithin an e+clusion esuperannuation payments pensions and annuities enuineredundancy payments or early retirement scheme payments

PoT 2015 pararaphs -62A0 8 -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2229

Payments upon termination of employment)mployment termination payments +n conse$uence of termination of employment

Employment termination needs to e one of the causes for the

ETP ut does not need e the dominant cause) e$e v FCT

(1gtA5) Le rand v FCT (2002)

=act that termination and payment occurs are similar times isinsufficient to estalish causation ltrennan $ in 0nto$h v FCT

(1gtAgt)

enuine termination

Termination includes cessation of employment due toretirement or death s 0410

8 =i+ed4term position made permanent not rearded as a

termination realy v FCT (1gtgt)

PoT 2015 pararaphs -62gt0 8 -6910

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2329

Payments upon termination of employment)mployment termination payments axation of )s

To components

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2429

Payments upon termination of employment)mployment termination payments Ta+ale component of a lie 2eneit ter-ination +ay-ent

ltroadly the threshold amount is the loer of (s 2410()) 8 L15000 (for 201D15) and

8 L10000 hole of income cap3 hich is reduced y anynon4ETP ta+ale income and suect to certain e+clusions

) taxablecomponentamount

axpayer is atpreservation age( years

axable is beloamppreservation age(0 years

0 8 threshold Ta+ed at normal marinal

rates ut capped at a rateof 15M plus 2M ampedicarelevy

Ta+ed at normal marinal

rates ut capped at a rateof 90M plus 2M ampedicareevy

mounts overthe threshold

Ta+ed at AM plus 2Mampedicare levy

Ta+ed at AM plus 2Mampedicare levy

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2529

Payments upon termination of employment)mployment termination payments Ta+ale component of a death 2eneit ter-ination +ay-ent

7ependent includes under s 90241gt5

8 pouse or e+4spouse 8 The deceased3s child ho is under 1

8 Interdependency relationships

8 nyone else dependent on the deceased efore death

) taxablecomponentamount

Recipient is a dependent Recipient is not adependent

0 8 L15000 ot ta+ed e+cept for 2M

ampedicare levy (amp) hereapplicale

Ta+ed at normal marinal

rates ut capped at a rate of90M plus 2M amp

L15000 N Ta+ed at AM plus 2M amp Ta+ed at AM plus 2M amp

PoT 2015 pararaph -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2629

Payments upon termination of employmentenuine redundancy and early retirements Benuine redundancy payment is a payment made to an

employee hose position is enuinely made redundant

Early retirement scheme satisfies the folloin conditions

8 cheme is open to all eliile employees

8 Employer3s purpose of havin the scheme is to reoranise

the operations of the orplace and

8 The Commissioner has approved the scheme as an early

retirement scheme

PoT 2015 pararaphs -6920 8 -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2729

Payments upon termination of employmentenuine redundancy and early retirements =urther conditions e+ist in ss 941A5 and 9410 for payments

to e considered redundancy payments and early retirement

scheme payments

8 The employee must e dismissed efore heDshe reaches 65

years of ae 8 The payment must represent hat ould e payale under a

normal commercial arranement

8 There must e no arranement at the time of dismissal that

the employee e re4employed y the employer

PoT 2015 pararaph -6950

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2829

Payments upon termination of employmentenuine redundancy and early retirements axation treatment

ot ETPs and ta+4free to the e+tent they are elo the relevant

threshold

To the e+tent the payment is aove the relevant threshold it is

enerally an ETP

PoT 2015 pararaph -6960

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2929

Payments upon termination of employmentnused annual and long service leave nnual leave and lon service leave payments are enerally

ta+ed at normal marinal ta+ rates

Concessional treatment (capped at the rate of 90M plus

ampedicare levy) under certain circumstances includin

8 Payment due to leave accruals in respect of servicesperformed efore 1 uust 1gtgt9 or

8 Payment as in connection ith a payment that consists of

a enuine redundancy payment or early retirement scheme

payment or an invalidity sement of an ETP

PoT 2015 pararaph -69gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 429

rdinary income reard for services

Nexus clearly established e+us clearly estalished for common items of personale+ertion includin

8 alary and aes

8 Commissions

8 ltonuses

8 =ees chared for services rendered

8 ncillary payments that are an incident of laour

e+us not impacted y lump4sum or one4off receipts for the

performance of a specific tas

8 ee Brent v FCT (1971)

It is irrelevant ho pays or hen it is paid Kelly v FCT (1gt5)

PoT 2015 pararaphs -60 8 -650

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 529

rdinary income reard for services

Nexus uncertain - voluntary payments ne+pected or voluntary payments received as an incidenceof employment constitutes ordinary income =or e+ample

8 Christmas onuses paid to employees paid in the form of

redeemale ift vouchers Laidler v Perry (1gt65)

8 Tips received y a ta+i driver Calvert v Wainwright (1gtA)

8 ote possile to characterise as ordinary income ased on the

nature of payment (income characteristics) rather than ne+us

8 dditional periodic payments as a sustitute for aes that

ere relied upon y the ta+payer FCT v Dixon (1gt52)

PoT 2015 pararaphs -6A0 8 -60

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 629

rdinary income reard for services

Nexus uncertain - gifts Bifts

8 =or personal ualities is not rearded as ordinary income

8 risin from the ta+payer3s aility to or andDor the

employment contract is ordinary income

ecessary to distinuish eteen the aove here a ift is

made and there is an employment or commercial connection

8 Importance of a personal relationship eteen the parties

Sott v FCT (1gt66)

PoT 2015 pararaph -6gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 729

rdinary income reard for services

Nexus uncertain - gifts on4determinative factors to consider in orderline cases

8 E+pectation of the ift Sott v FCT (1gt66)

8 ump sum or reular payments FCT v Blae (1gt)

8 ampotive of the donor (note eiht placed on the nature of

receipt in the hands of the recipient) Sott v FCT (1gt66)

8 Fhether the recipient has een fully remunerated for

services provided Sott v FCT (1gt66) aye$ v FCT (1gt56)

8 Personal relationship Sott v FCT (1gt66) aye$ v FCT

(1gt56)

PoT 2015 pararaph -6100

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 829

rdinary income reard for services

Nexus uncertain - prizes PriGes and chance innins are non4assessale if the indfallain is derived y luc

8 Finnins of a casual participant on a TH sho Ca$e 7

(1gt66) Rulin IT 16A

lternatively ordinary income if derived y e+ercisin deree ofsill (personal e+ertion) that sufficiently outeihs luc

8 Professional sportin people Kelly v FCT (1gt5)

8 Irrelevant that payment does not arise from employer

PoT 2015 pararaph -6110

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 929

rdinary income reard for services

Nexus uncertain - prizes 7ifficulty ith determinin the sufficient deree of sill thatouteihs luc Consideration factors include

PoT 2015 pararaph -6120

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1029

rdinary income reard for services

Non-cash benefits Prereuisites of ordinary income

non4cash enefit may have a ne+us ith personal e+ertion

hoever if not convertile to cash3 it is not ordinary income

8 Redemption of freuent flyer points that ere accrued from

or4related travel Payne v FCT (1gtgt6)

ote may hoever e assessale under s 1542 ITgtA or

suect to frine enefits ta+

PoT 2015 pararaph -6190

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1129

rdinary income reard for servicesCapital receipt or personal exertion ecessary to distinuish eteen ordinary income receipts

and capital receipts (not ordinary income)

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1229

Capital receipt or personal e+ertionChanges to entitlements ain from a chane to entitlements under employment or

service contracts taes the character of hat it replaces

8 Relinuishin employment rihts (e rihts to control a

company as manain director) Bennett v FCT (1gtA)

8 oss of employee entitlements ampampT Ca$e 77

PoT 2015 pararaph -6150

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1329

Capital receipt or personal e+ertionRestrictive covenants Restrictive covenant or restraint of trade may e formed

rdinary income if connected ith the current employmentareement (ie payment of future services)

Capital characterisation

8 eparate areement to ive up valuale rihts igg$ v

livier (1gt52) FCT v Woite (1gt2) 8 o ne+us ith earnin activity (e payment made at end of

contract) e++le$ v FCT (1gtgt1)

8 ote capital ains ta+ may apply (CBT event 71)

PoT 2015 pararaphs -6160 8 -61A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1429

Capital receipt or personal e+ertionSign-on fees in4on (enticement) fees as part of normal practices of

attractin people into a ne employment contract

8 Characterised as a payment for future services (ordinary

income) Piord v FCT (1gtgt) Rulin TR 1gtgtgtD1A

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1529

tatutory incomeServices and employment (s 1- ltroad provision that rins the value of certain ains from

laour into assessale income includin non4cash enefits

that are not convertile to cash under ordinary concepts

8 Consider application of s 1542 only if s 645 does not apply

pplies hen the folloin three reuirements are satisfied

PoT 2015 pararaph -61gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1629

tatutory incomeServices and employment (s 1- irst re$uirement

There is an alloance ratuity compensation enefit onus

or premium

Reuirement has a ide scope and ould include

8 Cash cash convertile or non4cash convertile receipts

8 Holuntary receipts (e ratuities)

8 E+ternal arranements (e an accountin firm3s employee

receives free hotel accommodation from a client)

Second re$uirement

Ta+payer is reuired to receive the first reuirement (ie

provided to you)

PoT 2015 pararaphs -6200 8 -6210

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1729

tatutory incomeServices and employment (s 1- hird re$uirement

e+us must e estalished The ain must e

8 J in respect of or for or in relation directly or indirectly toany employment or services rendered y the ta+payer

Easier to estalish ne+us under s 1542 than ordinary income

8 mounts paid y an employer to its employee on completionof relevant tertiary suects S-ith v FCT (1gtA)

8 Reard money for helpin to prevent disaster FCT v

ol-e$ (1gtgt5) Insufficient ne+us for redemption of freuent flyer points that

ere accrued from or4related travel Payne v FCT (1gtgt6)

PoT 2015 pararaph -6220

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1829

tatutory incomeServices and employment (s 1- Relationship ampith other tax provisions

ection 1542 ill not apply under certain circumstances

Key e+clusions include

PoT 2015 pararaph -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1929

tatutory incomeReturn to ampor payments (s 1- Payments made to a ta+payer as an inducement to return to

or or to provide services constitutes statutory income

8 ame position under income from ordinary concepts

(ordinary income s 645)

PoT 2015 pararaph -6250

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2029

Payments upon termination of employment

pecific provisions prescriin ta+ation treatment of paymentsmade in connection to the termination of employment

ampain termination payments include

PoT 2015 pararaph -6260

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2129

Payments upon termination of employment)mployment termination payments To road su4types of ETPs

Reuirements for a payment to e an ETP under s 24190

8 Payment is in conseuence of the employment termination

8 There as in fact a enuine termination payment

8 The payment does not fall ithin an e+clusion esuperannuation payments pensions and annuities enuineredundancy payments or early retirement scheme payments

PoT 2015 pararaphs -62A0 8 -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2229

Payments upon termination of employment)mployment termination payments +n conse$uence of termination of employment

Employment termination needs to e one of the causes for the

ETP ut does not need e the dominant cause) e$e v FCT

(1gtA5) Le rand v FCT (2002)

=act that termination and payment occurs are similar times isinsufficient to estalish causation ltrennan $ in 0nto$h v FCT

(1gtAgt)

enuine termination

Termination includes cessation of employment due toretirement or death s 0410

8 =i+ed4term position made permanent not rearded as a

termination realy v FCT (1gtgt)

PoT 2015 pararaphs -62gt0 8 -6910

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2329

Payments upon termination of employment)mployment termination payments axation of )s

To components

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2429

Payments upon termination of employment)mployment termination payments Ta+ale component of a lie 2eneit ter-ination +ay-ent

ltroadly the threshold amount is the loer of (s 2410()) 8 L15000 (for 201D15) and

8 L10000 hole of income cap3 hich is reduced y anynon4ETP ta+ale income and suect to certain e+clusions

) taxablecomponentamount

axpayer is atpreservation age( years

axable is beloamppreservation age(0 years

0 8 threshold Ta+ed at normal marinal

rates ut capped at a rateof 15M plus 2M ampedicarelevy

Ta+ed at normal marinal

rates ut capped at a rateof 90M plus 2M ampedicareevy

mounts overthe threshold

Ta+ed at AM plus 2Mampedicare levy

Ta+ed at AM plus 2Mampedicare levy

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2529

Payments upon termination of employment)mployment termination payments Ta+ale component of a death 2eneit ter-ination +ay-ent

7ependent includes under s 90241gt5

8 pouse or e+4spouse 8 The deceased3s child ho is under 1

8 Interdependency relationships

8 nyone else dependent on the deceased efore death

) taxablecomponentamount

Recipient is a dependent Recipient is not adependent

0 8 L15000 ot ta+ed e+cept for 2M

ampedicare levy (amp) hereapplicale

Ta+ed at normal marinal

rates ut capped at a rate of90M plus 2M amp

L15000 N Ta+ed at AM plus 2M amp Ta+ed at AM plus 2M amp

PoT 2015 pararaph -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2629

Payments upon termination of employmentenuine redundancy and early retirements Benuine redundancy payment is a payment made to an

employee hose position is enuinely made redundant

Early retirement scheme satisfies the folloin conditions

8 cheme is open to all eliile employees

8 Employer3s purpose of havin the scheme is to reoranise

the operations of the orplace and

8 The Commissioner has approved the scheme as an early

retirement scheme

PoT 2015 pararaphs -6920 8 -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2729

Payments upon termination of employmentenuine redundancy and early retirements =urther conditions e+ist in ss 941A5 and 9410 for payments

to e considered redundancy payments and early retirement

scheme payments

8 The employee must e dismissed efore heDshe reaches 65

years of ae 8 The payment must represent hat ould e payale under a

normal commercial arranement

8 There must e no arranement at the time of dismissal that

the employee e re4employed y the employer

PoT 2015 pararaph -6950

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2829

Payments upon termination of employmentenuine redundancy and early retirements axation treatment

ot ETPs and ta+4free to the e+tent they are elo the relevant

threshold

To the e+tent the payment is aove the relevant threshold it is

enerally an ETP

PoT 2015 pararaph -6960

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2929

Payments upon termination of employmentnused annual and long service leave nnual leave and lon service leave payments are enerally

ta+ed at normal marinal ta+ rates

Concessional treatment (capped at the rate of 90M plus

ampedicare levy) under certain circumstances includin

8 Payment due to leave accruals in respect of servicesperformed efore 1 uust 1gtgt9 or

8 Payment as in connection ith a payment that consists of

a enuine redundancy payment or early retirement scheme

payment or an invalidity sement of an ETP

PoT 2015 pararaph -69gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 529

rdinary income reard for services

Nexus uncertain - voluntary payments ne+pected or voluntary payments received as an incidenceof employment constitutes ordinary income =or e+ample

8 Christmas onuses paid to employees paid in the form of

redeemale ift vouchers Laidler v Perry (1gt65)

8 Tips received y a ta+i driver Calvert v Wainwright (1gtA)

8 ote possile to characterise as ordinary income ased on the

nature of payment (income characteristics) rather than ne+us

8 dditional periodic payments as a sustitute for aes that

ere relied upon y the ta+payer FCT v Dixon (1gt52)

PoT 2015 pararaphs -6A0 8 -60

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 629

rdinary income reard for services

Nexus uncertain - gifts Bifts

8 =or personal ualities is not rearded as ordinary income

8 risin from the ta+payer3s aility to or andDor the

employment contract is ordinary income

ecessary to distinuish eteen the aove here a ift is

made and there is an employment or commercial connection

8 Importance of a personal relationship eteen the parties

Sott v FCT (1gt66)

PoT 2015 pararaph -6gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 729

rdinary income reard for services

Nexus uncertain - gifts on4determinative factors to consider in orderline cases

8 E+pectation of the ift Sott v FCT (1gt66)

8 ump sum or reular payments FCT v Blae (1gt)

8 ampotive of the donor (note eiht placed on the nature of

receipt in the hands of the recipient) Sott v FCT (1gt66)

8 Fhether the recipient has een fully remunerated for

services provided Sott v FCT (1gt66) aye$ v FCT (1gt56)

8 Personal relationship Sott v FCT (1gt66) aye$ v FCT

(1gt56)

PoT 2015 pararaph -6100

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 829

rdinary income reard for services

Nexus uncertain - prizes PriGes and chance innins are non4assessale if the indfallain is derived y luc

8 Finnins of a casual participant on a TH sho Ca$e 7

(1gt66) Rulin IT 16A

lternatively ordinary income if derived y e+ercisin deree ofsill (personal e+ertion) that sufficiently outeihs luc

8 Professional sportin people Kelly v FCT (1gt5)

8 Irrelevant that payment does not arise from employer

PoT 2015 pararaph -6110

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 929

rdinary income reard for services

Nexus uncertain - prizes 7ifficulty ith determinin the sufficient deree of sill thatouteihs luc Consideration factors include

PoT 2015 pararaph -6120

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1029

rdinary income reard for services

Non-cash benefits Prereuisites of ordinary income

non4cash enefit may have a ne+us ith personal e+ertion

hoever if not convertile to cash3 it is not ordinary income

8 Redemption of freuent flyer points that ere accrued from

or4related travel Payne v FCT (1gtgt6)

ote may hoever e assessale under s 1542 ITgtA or

suect to frine enefits ta+

PoT 2015 pararaph -6190

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1129

rdinary income reard for servicesCapital receipt or personal exertion ecessary to distinuish eteen ordinary income receipts

and capital receipts (not ordinary income)

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1229

Capital receipt or personal e+ertionChanges to entitlements ain from a chane to entitlements under employment or

service contracts taes the character of hat it replaces

8 Relinuishin employment rihts (e rihts to control a

company as manain director) Bennett v FCT (1gtA)

8 oss of employee entitlements ampampT Ca$e 77

PoT 2015 pararaph -6150

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1329

Capital receipt or personal e+ertionRestrictive covenants Restrictive covenant or restraint of trade may e formed

rdinary income if connected ith the current employmentareement (ie payment of future services)

Capital characterisation

8 eparate areement to ive up valuale rihts igg$ v

livier (1gt52) FCT v Woite (1gt2) 8 o ne+us ith earnin activity (e payment made at end of

contract) e++le$ v FCT (1gtgt1)

8 ote capital ains ta+ may apply (CBT event 71)

PoT 2015 pararaphs -6160 8 -61A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1429

Capital receipt or personal e+ertionSign-on fees in4on (enticement) fees as part of normal practices of

attractin people into a ne employment contract

8 Characterised as a payment for future services (ordinary

income) Piord v FCT (1gtgt) Rulin TR 1gtgtgtD1A

PoT 2015 pararaph -610

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1529

tatutory incomeServices and employment (s 1- ltroad provision that rins the value of certain ains from

laour into assessale income includin non4cash enefits

that are not convertile to cash under ordinary concepts

8 Consider application of s 1542 only if s 645 does not apply

pplies hen the folloin three reuirements are satisfied

PoT 2015 pararaph -61gt0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1629

tatutory incomeServices and employment (s 1- irst re$uirement

There is an alloance ratuity compensation enefit onus

or premium

Reuirement has a ide scope and ould include

8 Cash cash convertile or non4cash convertile receipts

8 Holuntary receipts (e ratuities)

8 E+ternal arranements (e an accountin firm3s employee

receives free hotel accommodation from a client)

Second re$uirement

Ta+payer is reuired to receive the first reuirement (ie

provided to you)

PoT 2015 pararaphs -6200 8 -6210

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1729

tatutory incomeServices and employment (s 1- hird re$uirement

e+us must e estalished The ain must e

8 J in respect of or for or in relation directly or indirectly toany employment or services rendered y the ta+payer

Easier to estalish ne+us under s 1542 than ordinary income

8 mounts paid y an employer to its employee on completionof relevant tertiary suects S-ith v FCT (1gtA)

8 Reard money for helpin to prevent disaster FCT v

ol-e$ (1gtgt5) Insufficient ne+us for redemption of freuent flyer points that

ere accrued from or4related travel Payne v FCT (1gtgt6)

PoT 2015 pararaph -6220

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1829

tatutory incomeServices and employment (s 1- Relationship ampith other tax provisions

ection 1542 ill not apply under certain circumstances

Key e+clusions include

PoT 2015 pararaph -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 1929

tatutory incomeReturn to ampor payments (s 1- Payments made to a ta+payer as an inducement to return to

or or to provide services constitutes statutory income

8 ame position under income from ordinary concepts

(ordinary income s 645)

PoT 2015 pararaph -6250

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2029

Payments upon termination of employment

pecific provisions prescriin ta+ation treatment of paymentsmade in connection to the termination of employment

ampain termination payments include

PoT 2015 pararaph -6260

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2129

Payments upon termination of employment)mployment termination payments To road su4types of ETPs

Reuirements for a payment to e an ETP under s 24190

8 Payment is in conseuence of the employment termination

8 There as in fact a enuine termination payment

8 The payment does not fall ithin an e+clusion esuperannuation payments pensions and annuities enuineredundancy payments or early retirement scheme payments

PoT 2015 pararaphs -62A0 8 -620

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2229

Payments upon termination of employment)mployment termination payments +n conse$uence of termination of employment

Employment termination needs to e one of the causes for the

ETP ut does not need e the dominant cause) e$e v FCT

(1gtA5) Le rand v FCT (2002)

=act that termination and payment occurs are similar times isinsufficient to estalish causation ltrennan $ in 0nto$h v FCT

(1gtAgt)

enuine termination

Termination includes cessation of employment due toretirement or death s 0410

8 =i+ed4term position made permanent not rearded as a

termination realy v FCT (1gtgt)

PoT 2015 pararaphs -62gt0 8 -6910

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2329

Payments upon termination of employment)mployment termination payments axation of )s

To components

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2429

Payments upon termination of employment)mployment termination payments Ta+ale component of a lie 2eneit ter-ination +ay-ent

ltroadly the threshold amount is the loer of (s 2410()) 8 L15000 (for 201D15) and

8 L10000 hole of income cap3 hich is reduced y anynon4ETP ta+ale income and suect to certain e+clusions

) taxablecomponentamount

axpayer is atpreservation age( years

axable is beloamppreservation age(0 years

0 8 threshold Ta+ed at normal marinal

rates ut capped at a rateof 15M plus 2M ampedicarelevy

Ta+ed at normal marinal

rates ut capped at a rateof 90M plus 2M ampedicareevy

mounts overthe threshold

Ta+ed at AM plus 2Mampedicare levy

Ta+ed at AM plus 2Mampedicare levy

PoT 2015 pararaph -69A0

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2529

Payments upon termination of employment)mployment termination payments Ta+ale component of a death 2eneit ter-ination +ay-ent

7ependent includes under s 90241gt5

8 pouse or e+4spouse 8 The deceased3s child ho is under 1

8 Interdependency relationships

8 nyone else dependent on the deceased efore death

) taxablecomponentamount

Recipient is a dependent Recipient is not adependent

0 8 L15000 ot ta+ed e+cept for 2M

ampedicare levy (amp) hereapplicale

Ta+ed at normal marinal

rates ut capped at a rate of90M plus 2M amp

L15000 N Ta+ed at AM plus 2M amp Ta+ed at AM plus 2M amp

PoT 2015 pararaph -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2629

Payments upon termination of employmentenuine redundancy and early retirements Benuine redundancy payment is a payment made to an

employee hose position is enuinely made redundant

Early retirement scheme satisfies the folloin conditions

8 cheme is open to all eliile employees

8 Employer3s purpose of havin the scheme is to reoranise

the operations of the orplace and

8 The Commissioner has approved the scheme as an early

retirement scheme

PoT 2015 pararaphs -6920 8 -690

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2729

Payments upon termination of employmentenuine redundancy and early retirements =urther conditions e+ist in ss 941A5 and 9410 for payments

to e considered redundancy payments and early retirement

scheme payments

8 The employee must e dismissed efore heDshe reaches 65

years of ae 8 The payment must represent hat ould e payale under a

normal commercial arranement

8 There must e no arranement at the time of dismissal that

the employee e re4employed y the employer

PoT 2015 pararaph -6950

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2829

Payments upon termination of employmentenuine redundancy and early retirements axation treatment

ot ETPs and ta+4free to the e+tent they are elo the relevant

threshold

To the e+tent the payment is aove the relevant threshold it is

enerally an ETP

PoT 2015 pararaph -6960

7182019 Income From Personal Services and Employment

httpslidepdfcomreaderfullincome-from-personal-services-and-employment 2929

Payments upon termination of employmentnused annual and long service leave nnual leave and lon service leave payments are enerally

ta+ed at normal marinal ta+ rates

Concessional treatment (capped at the rate of 90M plus

ampedicare levy) under certain circumstances includin