in-depth analysis evaluating the legal, political and ... - 3 a maitrot de la motte... · mining...

TRANSCRIPT

In-Depth Analysis evaluatingthe legal, political and

institutional framework onoffshore practices related to

tax evasion, money launderingand tax transparency in the

Overseas Countries andTerritories (OCT) of France, asdefined in Annex II (TFEU), and

the relations of France withthese OCTs

Pr. AlexandreMAITROT DE LA MOTTE

Brussel - 2 May 2017

Rédacteur2 May 2017 2

INTRODUCTION

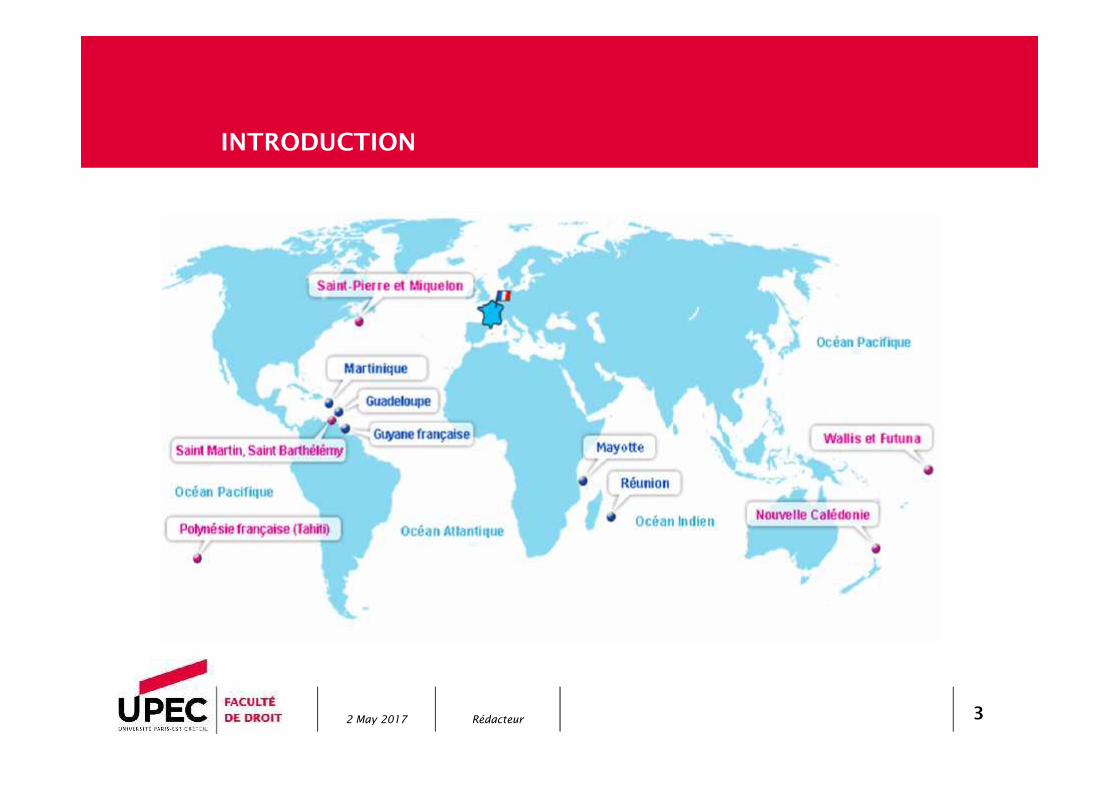

Under the law of the European Union, the French OCTs are:

• St. Barthelemy,

• Saint-Pierre-and-Miquelon,

• Wallis-and-Futuna Islands,

• French Polynesia,

• and the group constituted by the four territories of NewCaledonia (hereinafter ‘New Caledonia’).

Rédacteur2 May 2017 3

INTRODUCTION

Rédacteur2 May 2017 4

INTRODUCTION

DOM ROMDOMANDROM

COM Other UPR OCT

Guadeloupe C C C

Martinique C C

Guyana C C

Reunion C C C

Mayotte C C C

St. BarthelemyC/as.

C

Saint-MartinC/as.

C

Saint-Pierre-and-Miquelon

C/as.C

Wallis-and-Futuna

C/sp.C

French PolynesiaC/sp.

C

New Caledonia C/sp. C

Rédacteur2 May 2017 5

INTRODUCTION

These French OCTs are not completelyindependent or even autonomous:

• They do not have sovereignty;

• Like all French local authorities, they are decentralisedand exercise the powers that the state gives them (andcan take over) within the framework of a unitary state.

French law is governed by a logic that is that ofdecentralisation: the French state remains a unitary statewhich has transferred powers and financial resources to

non-sovereign local authorities.

Rédacteur2 May 2017 6

INTRODUCTION

Territory Population Size GDPGDP percapita

Unemploymentrate

Key economicsectors

Frenchbudgetary aid

St. Barthelemy 9,131 (2012) 24 km²319 million

euros (2010)

35,700euros(2010)

4.3%

Tourism; Buildingsand Public Works;Non-financialmarket sector;trade

2 million euros

Saint-Pierre-and-Miquelon

6,081 242 km²172 million

euros28,327euros

8.7%

PublicAdministrationsand Merchantservices

77 million euros

Wallis-and-Futuna 12,200 142 km²150 million

euros10,100euros

8.8%

Agriculture ; NonMerchant services(education, Healthand publicservices) ; trade

106 million euros

French Polynesia 271,8004 167k

m²4,346 billioneuros (2012)

16,000euros(2012)

21.8% Services; Tourism.1,192 millioneuros

New Caledonia 268,00018 576

km²7,105 billioneuros (2010)

28,931euros(2010)

13.85% (2009)

Mining activities(nickel); trade ;construction ;tourism

1,217 millioneuros

Rédacteur2 May 2017 7

INTRODUCTION

Syllabus:

I / Tax evasion and French OCTs

II / Money laundering and French OCTs

III / Fiscal transparency and French OCTs

Rédacteur2 May 2017 8

I / Tax evasion and French OCTs

Rédacteur2 May 2017 9

I / Tax evasion and French OCTs

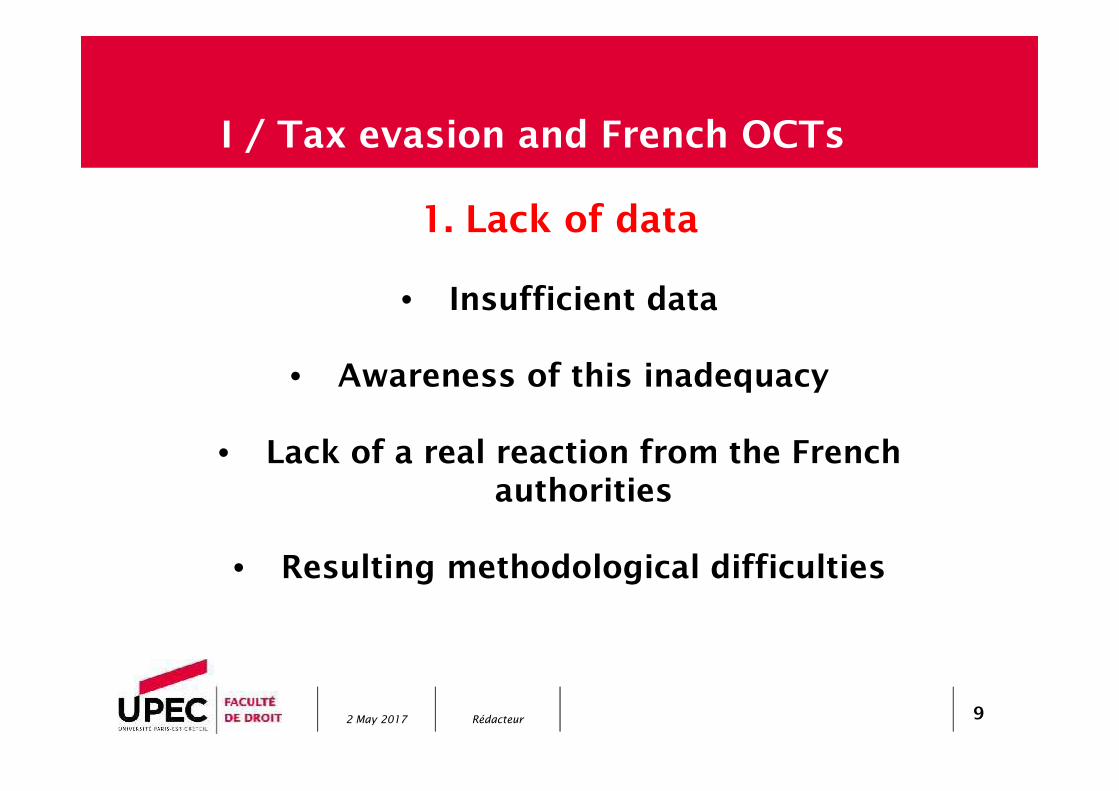

1. Lack of data

• Insufficient data

• Awareness of this inadequacy

• Lack of a real reaction from the Frenchauthorities

• Resulting methodological difficulties

Rédacteur2 May 2017 10

I / Tax evasion and French OCTs

2. Factors favouring tax evasion throughcertain French OCTs.

• The low level of direct taxes (St Barth & Wallis-and-Futuna)

• The lack of tax audits (all French OCTs, outsideof Saint-Pierre-and-Miquelon)

Rédacteur2 May 2017 11

I / Tax evasion and French OCTs

3. Factors putting into perspective therisks of tax evasion through French

OCTs

• The tax regimes applicable to non-residenttaxpayers in the French OCTs (double taxation)

• The geographical distances and the difficultiesof access

• The low level of development of localeconomies and banking systems

Rédacteur2 May 2017 12

II / Money laundering and FrenchOCTs

Rédacteur2 May 2017 13

II / Money laundering and French OCTs

1. The indirect application of Europeananti-money laundering rules in the

French OCTs

• Traditional extension to the French OCTs of EUsecondary legislation on the fight against

money laundering

• Extension to the French OCTs of the mostrecent provisions of European Union anti-

money laundering legislation (Regulation (EU)2015/847; and Directive (EU) 2015/849)

Rédacteur2 May 2017 14

II / Money laundering and French OCTs

2. Critical examination of the effectivenessof the rules applicable within the French

OCTs

• The insufficiency of the reporting ofsuspicions and of the controls

• The lack of data on money laundering in theFrench OCTs

Rédacteur2 May 2017 15

II / Money laundering and French OCTs

3. The need to put into perspective therisks of money-laundering via the French

OCTs

• With respect to banking systems and feasiblebanking operations, the risks are limited

• Given the number of bank accounts opened inthe French OCTs and the amount of bankassets, money laundering practices are

necessarily low

Rédacteur2 May 2017 16

III / Tax transparency and FrenchOCTs

Rédacteur2 May 2017 17

III / Tax transparency and French OCTs

1. A willingness to tax transparencyrespecting the highest standards

• Article L. 114 of the French Code of TaxProcedures: ‘The tax administration may exchange information with the

financial administrations of Saint-Pierre-and-Miquelon, New Caledonia, FrenchPolynesia, the Wallis-and-Futuna Islands and the French Southern and Antarctic

Territories and other local and regional authorities of the French Republicgoverned by a specific tax system, and with states which have concluded withFrance an administrative assistance agreement to combat the tax fraud and tax

evasion’

• Agreements between the French state and theFrench OCT with a view, inter alia, to

organising the exchange of tax information

Rédacteur2 May 2017 18

III / Tax transparency and French OCTs

1. A willingness to tax transparencyrespecting the highest standards

• In practice, the conventions binding the OCTsand the central state comply with OECD

standards

• Sometimes they go even beyond (by offering thepossibility for the state to monitor on-the-spot thereality of operations which have given right to tax

exemptions in metropolitan France; sometimes, the statemay itself impose the taxation of persons settled in St.

Barthelemy but taxed as residents of the state)

Rédacteur2 May 2017 19

III / Tax transparency and French OCTs

2. The regrettable lack of data on theimplementation of tax transparency in

the French OCTs

Rédacteur2 May 2017 20

III / Tax transparency and French OCTs

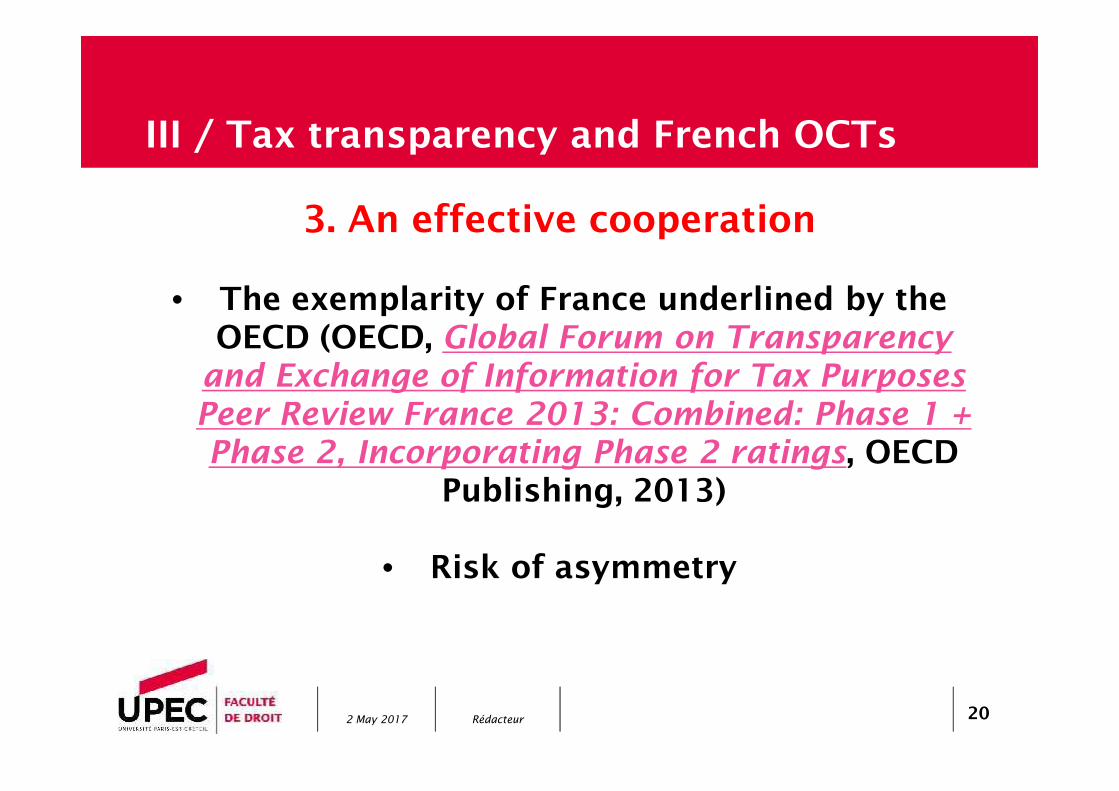

3. An effective cooperation

• The exemplarity of France underlined by theOECD (OECD, Global Forum on Transparency

and Exchange of Information for Tax PurposesPeer Review France 2013: Combined: Phase 1 +Phase 2, Incorporating Phase 2 ratings, OECD

Publishing, 2013)

• Risk of asymmetry

Rédacteur2 May 2017 21

CONCLUSION

The in-depth analysis of the French situation withregard to tax evasion, money laundering andtax transparency shows that the French OCTspresent little risk for the other Member States

of the European Union.

Rédacteur2 May 2017 22

CONCLUSION

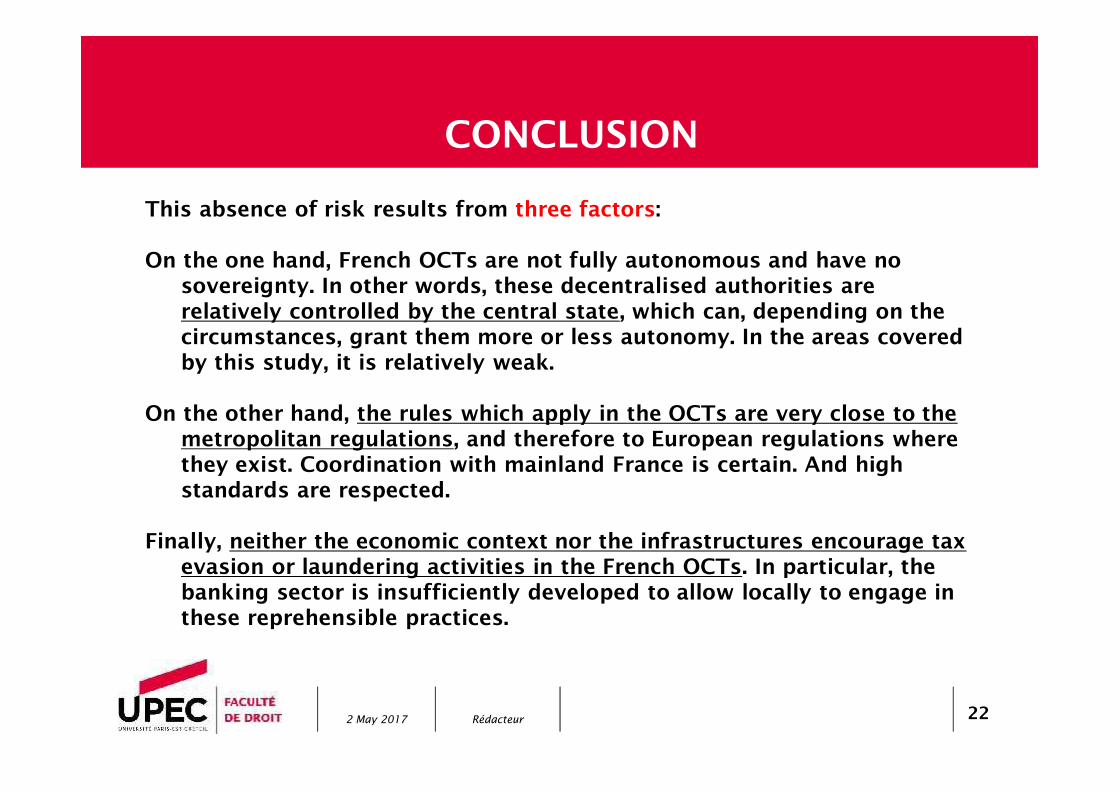

This absence of risk results from three factors:

On the one hand, French OCTs are not fully autonomous and have nosovereignty. In other words, these decentralised authorities arerelatively controlled by the central state, which can, depending on thecircumstances, grant them more or less autonomy. In the areas coveredby this study, it is relatively weak.

On the other hand, the rules which apply in the OCTs are very close to themetropolitan regulations, and therefore to European regulations wherethey exist. Coordination with mainland France is certain. And highstandards are respected.

Finally, neither the economic context nor the infrastructures encourage taxevasion or laundering activities in the French OCTs. In particular, thebanking sector is insufficiently developed to allow locally to engage inthese reprehensible practices.

Rédacteur2 May 2017 23

CONCLUSION

Of course, improvements could be made tocombat tax evasion and money laundering in

the French OCTs:

• In particular, the administrative departmentsresponsible for carrying out control operationscould benefit from more resources. This would

allow for more controls and more data.

• At the same time, local professionals could bemore aware of risks.

Rédacteur2 May 2017 24

CONCLUSION

It follows that the French OCTs can serve as amodel for the OCTs of the other Member States.

If the idea is not to question the competenceand autonomy of the latter, it would perhaps berelevant that, like the French OCTs, regulations

close to European regulations and Europeanstandards apply there in the field of the fight

against money laundering and of administrativecooperation.

Alexandre MAITROT DE LA MOTTE

Professor at Paris-Est Créteil UniversityAssociate Vice President, in charge of legal

affairs & communicationVice Dean of the Law Faculty

Head of the Public Law departmentDirector of the Research Center Marchés,

Institutions, Libertés (EA 7382)Director of the Master program Droit Fiscal,

spécialité fiscalité appliquée

61, avenue du Général de Gaulle94010 Créteil Cedex

Faculté de droit