immigrant entrepreneurship - harvard business school

TRANSCRIPT

Immigrant Entrepreneurship

Sari Pekkala Kerr William R. Kerr

Working Paper 17-011

Working Paper 17-011

Copyright © 2016 by Sari Pekkala Kerr and William R. Kerr

Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author.

Immigrant Entrepreneurship Sari Pekkala Kerr Wellesley College

William R. Kerr Harvard Business School

Immigrant Entrepreneurship

Sari Pekkala KerrWellesley College

William R. KerrHarvard Business School

June 2016∗

Abstract

We examine immigrant entrepreneurship and the survival and growth of immigrant-founded businesses over time relative to native-founded companies. Our work quantifiesimmigrant contributions to new firm creation in a wide variety of fields and using multipledefinitions. While significant research effort has gone into understanding the economic im-pact of immigration into the United States, comprehensive data for quantifying immigrantentrepreneurship are diffi cult to assemble. We combine several restricted-access U.S. Cen-sus Bureau data sets to create a unique longitudinal data platform that covers 1992-2008and many states. We describe differences in the types of businesses initially formed byimmigrants and their medium-term growth patterns. We also consider the relationship ofthese outcomes to the immigrants’age at arrival to the United States.

JEL Classification: F22, J15, J44, J61, L26, M13, O31, O32, O33.

Keywords: immigration, entrepreneurship, entry, firm survival and growth, venturecapital, high-tech.

∗Author contact information: [email protected], [email protected]. Sari Pekkala Kerr is a senior researchscientist at the Wellesley Centers for Women (Wellesley College). William Kerr is a professor at Harvard BusinessSchool and a Research Associate at the National Bureau of Economic Research (NBER) and Bank of Finland.This is a revised version of a paper prepared for the Conference on Research in Income and Wealth (CRIW)NBER meeting on December 16-17, 2014, in Washington DC and a draft chapter for the CRIW-NBER volumeMeasuring Entrepreneurial Business: Current Knowledge and Challenges, edited by John Haltiwanger, ErikHurst, Javier Miranda and Antoinette Schoar. We thank our discussant Ethan Lewis, the editors, and CRIW-NBER participants for very helpful comments. We thank the Alfred P. Sloan Foundation, National ScienceFoundation, Harvard Business School, and the Ewing Marion Kauffman Foundation for financial support thatmade this research possible. The research in this paper was conducted while the authors were Special SwornStatus researchers of the U.S. Census Bureau at the Boston Census Research Data Center. Research results andconclusions expressed are the authors’own and do not necessarily reflect the views of the Census Bureau or theNSF. This paper has been screened to ensure that no confidential data are revealed.

1

1 Introduction

Immigrant entrepreneurship is of central policy interest and a frequent hot point in the popularpress. Many policy makers believe that immigrant founders are an important and under-utilizedlever for the revival of U.S. job growth and continued recovery from the Great Recession. Severallocal and national policy initiatives have been launched to attract immigrant entrepreneurs (e.g.,the Thrive competition in New York City, the Offi ce of New Americans in Chicago, and theWhiteHouse Startup America initiative). Some of the policy initiatives focus on specific issues thathave been found to limit immigrant entrepreneurs from starting or growing their businesses (e.g.,language barriers, diffi culty navigating the legal steps to start a company, or lack of capital topilot projects), while others are generally focused on attracting more new businesses into thecountry. Policies vary in the immigrant group that they target, ranging from a specific focuson high-skilled immigrant entrepreneurship with venture capital (VC) backing to broad-basedmeasures that potentially touch many diverse immigrant communities.Academic research, unfortunately, possesses only a small voice in this debate or policy de-

sign. For example, advocates of greater immigrant entrepreneurship mainly cite a few extremeexamples of success such as Sergey Brin, one of the founders of Google, and extrapolate informa-tion from some exceptionally influential case studies regarding Silicon Valley and large high-techcompanies (e.g., Saxenian, 1999; Wadhwa et al., 2007). While each of these supporting pieces hasits merits and liabilities discussed below, it is important for rigorous trends and statistics to alsoinform this debate. For example, even with respect to Silicon Valley and high-tech companies,it is not immediately clear what the oft-cited statistics mean– it is likely true that more thanhalf of the entrepreneurs in Silicon Valley are of immigrant origin, as the surveys suggest, butthe exact same could be said of the undergraduate student populations at most schools in theSan Francisco area. Second, given the substantial heterogeneity in immigrant entrepreneurship,which comes in just as many flavours as native entrepreneurship, it is unsatisfying to focus onsuch a narrow population of high-tech entrepreneurs for contemplating possible initiatives.For economists to be able to aid the policy process, and ultimately improve economic perfor-

mance in this arena, we need better-grounded estimates on the importance of immigrant groupsfor the creation of new firms, the business activities and growth profiles of created firms, and soon. This study constructs a data platform using Census Bureau administrative data to assistin this process. The purpose of this chapter is to detail the platform’s components and providesome early views of the trends for immigrant entrepreneurs and the patterns in their behavior.We have several audiences in mind. First, we are able to offer some new facts to the discussionof immigrant entrepreneurship that can be useful for policy discussions, although we do notexamine any specific policy actions or recommendations about encouraging immigrant entrepre-neurship in this study. Second, we hope that others find this discussion encouraging for makingprogress on this front and that they too seek access to these data through the Census Bureau.

1

Ideally, our paper can provide them a one-stop-shop for what is feasible in the data and how tobuild the platform, and this chapter goes into greater depth than is normal for academic paperson how the platform is built and its traits. Finally, we speak to future efforts to enhance thesedata. In terms of representative statistics, this platform is likely as good as it gets with today’sdata collection. We describe below a wish list for future data development efforts.Section 2 provides a brief review of the previous empirical literature on immigrant entrepre-

neurs and their traits. Fairlie and Lofstrom (2014) provide a comprehensive recent review ofthis literature strand and statistics from the 2007 Survey of Business Owners (SBO). In thischapter, relative to prior academic work, we make three contributions. First, our data platformprovides consistent estimates of immigrant entrepreneurship over a long time period (1995-2008)and across skill levels (e.g., all entrepreneurs, VC-backed firms). Existing work, even when usingrepresentative national samples, tends to be cross-sectional at a given point in time and focusedon a specific skill population, whereas for most purposes the comparisons across time and groupswould be very important. Second, we study the different dynamics of employment and growthamong immigrant-led businesses compared to those founded by natives. Fairlie and Lofstrom(2014) conclude that a central research goal for immigrant entrepreneurship is to identify the dy-namics of employment growth among these firms, and our constructed platform makes progressin this domain. Third and related, we provide a first breakdown of these growth dynamics by theage of immigration to the United States. This last analysis is preliminary and mostly undertakento show the potential of the data for observing differences along traits identifiable from the 2000Census match, but striking nonetheless.Section 3 details the construction of our data platform. The strength of our study lies in

the ability to use and combine several restricted-access U.S. Census Bureau data sets to createa unique longitudinal data platform with millions of observations. Indeed, a key purpose of thischapter is to report on the potential of these data and describe their traits for research pur-poses. The backbone for our work is the employer-employee data in the Longitudinal Employer-Household Dynamics (LEHD) database. The LEHD provides firm-worker information collectedfrom unemployment insurance records. From this information, one can observe the birth of newfirms and their employee composition, including immigration status. We also utilize other data:[1] the Longitudinal Business Database (LBD) to assess the employment growth dynamics ofnew firms, [2] the long-form records of the 2000 Decennial Census to collect additional person-and household-level traits (e.g., year of arrival to the United States), and [3] external data setsto identify companies that have VC backing or achieve an initial public offering (IPO). Theresulting data platform can describe many forms of entrepreneurship, ranging from general pat-terns to "growth entrepreneurs" described in the VC literature. These detailed new data allowus to study person- and firm-level patterns in a way that has not been possible to date, andthis section also depicts the variations and limits on the definitions of entrepreneurship in the

2

LEHD.1

Section 4 provides our trend estimates. Most of our work focuses on 11 states present inthe LEHD since 1992, which include California and Florida. We estimate 24% of entrepreneursin these states from 1995-2008 are immigrants, which broadly corresponds with other studies.As important, this immigrant entrepreneurship share rises from 17% in 1995 to 27% in 2008.Our sample, by coincidence, draws from heavy immigration states. Looking at a sample of 28states present in the LEHD by 2000, we estimate these numbers may be 3% higher than thetotal population, with the growth trend being similar. Returning to our focal set of states,the immigrant share among entrepreneurs receiving VC financing is modestly higher, reaching30% in 2005 compared to 27% for all firms. In terms of entrepreneurship rates, roughly 2% ofimmigrants start a business over a three-year period; 0.1% start a firm backed by VC financing.These rates are higher than those we estimate for natives, which is reflected in the fact thatimmigrants constitute 19% of the LEHD workforce in our sample, less than the entrepreneurshipshares reported above.Section 5 documents basic patterns related to entry, survival, and growth of immigrant

versus native businesses. On the whole, the businesses started by immigrant entrepreneursperform better than native businesses with respect to employment growth over three- and six-yearhorizons. This is evident in the raw data and mostly persists when comparing immigrant- andnative-founded businesses started in the same city, industry, and year. By contrast, immigrant-founded businesses show no advantages with respect to payroll growth, and may in fact generatelower-wage job growth. Combining business survival with growth dynamics, immigrants tend tobe engaged in more volatile, up-or-out type dynamics, along the lines described by Haltiwangeret al. (2013) for young businesses and job creation. Most of this effect is captured by the city-industry-year choices made for businesses, versus variation in growth patterns within these cells.Breaking down these aggregate results, the strongest employment growth impacts for immigrantsare found in high-wage businesses and high-tech sectors. Conditional on receiving VC investment,however, we do not observe greater business survival, better employment outcomes, or higherlikelihood of going public for firms founded by immigrant entrepreneurs. Businesses founded byimmigrants who came the United States by age 18 have stronger growth patterns than thosefounded by immigrants migrating as adults.Section 6 concludes with a discussion of these findings in the larger context of immigration and

entrepreneurship policy. This section also describes enhancements to the platform that wouldenable better research efforts going forward. Immigration policy is designed and administered atthe national level, with few restrictions on the location choices of immigrants within the UnitedStates. A methodological conclusion from this study is that the LEHD-based platform canconsistently describe immigrant entrepreneurship across many industries, geographies, and skill

1In a broad review of the immigration literature, Lewis (2013a) raises immigrant entrepreneurship as one ofthe key areas requiring further study and notes the key ingredient of employer-employee data for this purpose.The LEHD is the source of this type of administrative information for the United States.

3

levels. This is an important ingredient for delivering systematic advice about how immigrantentrepreneurs impact the U.S. economy and where the effects of expansion in admission levelsmight be felt. We also find that the detail of the LEHD can aid more effective policy advicefor sub-groups of immigrants. The surveys most cited in the public discourse are actually quitecrude in this regard. For example, although Sergey Brin is often used as the showcase example forimmigration reform on high-skilled H-1B policies, he came to the United States as a child, whilethe H-1B program is focused on temporary admissions of adults with college-level education.Our disaggregation by the age at arrival for immigrants indicates this assembled platform canhelp begin to disentangle these important details. To be clear, our study stops well short ofmaking a direct input to immigration policy design on this or other dimensions, but we do findthat these data elements are of suffi cient strength and depth that they can serve as an effectivefoundation for future research efforts to inform the economic consequences of selection strategiesbased upon certain immigrant traits.On the other hand, we note that there are many places where the LEHD has limits, some

of which may be addressable. For example, here we define entrepreneurship status through ini-tial wage profiles of firm employees, which is certainly incomplete. Over short-term horizons,it would be useful to consider linking LEHD workers to SBO-type data to evaluate the accu-racy and bias of derived entrepreneurship definitions with greater detail. Similarly, we describehow links of LEHD workers to external data sources at the individual-level would be powerful(e.g., entrepreneurs/CEOs contained in the Venture Xpert data, inventors contained in UnitedStates patent data). More challenging, while we are able to make progress towards some of theimportant traits of immigrants, we miss completely with the LEHD the essential questions ofimmigration visa type (e.g., H-1B, green card), which is strongly emphasized by Hunt (2011) asa key predictor for choices by immigrants with respect to entrepreneurship. For the evaluationand design of effective policy, the inclusion of visa status and transitions over time must be atthe top of any wish list.

2 Previous Literature on Immigrant Entrepreneurs

This section provides some background for our study from the academic literature, with Fairlieand Lofstrom (2014) reviewing the immigrant entrepreneurship literature in a more compre-hensive manner. There is a large body of literature showing that general rates of businessownership are higher among the foreign-born than natives in many developed countries, includ-ing the United States, United Kingdom, Canada, and Australia.2 Fairlie (2012) and Fairlie andLofstrom (2014) also observe that trends in self-employment rates and new business formationare increasing among immigrants but decreasing among natives in the United States. In closely-related work to the current analysis, Hunt (2011, 2015) focuses on skilled immigrants and finds

2Studies include Borjas (1986); Lofstrom (2002); Clark and Drinkwater (2000, 2006); Schuetze and Antecol(2007); and Fairlie et al. (2010).

4

that they are more likely to start firms with more than 10 employees than comparable natives.Hunt uses the National Survey of College Graduates (NSCG), which provides a nationally rep-resentative sample of persons with a college degree and interesting information about the initialvisa status of immigrants. She finds that the probability of starting a firm was highest for thoseinitially arriving on a study visa or a work visa, versus family reunification. While the level ofdetail on the specific degrees and entry visas in the NSCG is impressive, the major issues forresearchers trying to describe national trends in immigrant-founded firms are the small samplesizes, the lack of longitudinal dimension, and the absence of firms as a data element.In parallel to these general patterns, a second research stream focuses specifically on immi-

grant entrepreneurship in the high-tech sector. Saxenian (1999, 2002) documents that up to aquarter of the high-tech firms in Silicon Valley in the 1980s and 1990s were founded or beingrun by immigrants. Wadhwa et al. (2007) extends this survey analysis to the rest of the countryand other industries to study firms founded in 1995-2005. They document similar shares ofimmigrant-founded companies across the country, although elements of their study are diffi cultto generalize.3 Table 1 provides a summary of several related studies on immigrant entrepre-neurs. These efforts connect into a broader line of work showing the over-representation of skilledimmigrants among certain extreme outcomes in U.S. science and engineering: for example, U.S.-based Nobel Prize winners (Peri, 2007), high-impact companies (Hart and Acs, 2011), patentapplications (Wadhwa et al., 2007), members of the National Academy of Sciences and the Na-tional Academy of Engineering (Stephan and Levin, 2001), and biotech companies undergoinginitial public offerings (Stephan and Levin, 2001). It is these kinds of factors that likely drive thecurrent policy enthusiasm towards immigrant entrepreneurs. On the other hand, with respect toimmigrant high-tech contributions, Hart and Acs (2011) suggest that although immigrants playan important role, "most previous studies have overstated the role of immigrants in high-techentrepreneurship."Statistics with respect to immigrant entrepreneurship among VC-backed firms are harder to

assemble. Fairlie (2012) calculates from the 2007 SBO that equally few native and immigrantbusiness owners rely on any VC funding; more generally, the study finds that immigrants areless likely to start a business with no capital and just as likely as natives to start a business withmore than $1 million of capital. Hegde and Tumlinson (2014) and Bengtsson and Hsu (2015)are recent examples of studies of immigrant entrepreneurship among VC-backed firms usingethnic names to distinguish the likelihood of a founder being an immigrant. In an advocacy

3The sample with responses covers 7% of the approximately 30,000 firms in the Dunn & Bradstreet data thatwere founded in 1995-2005, had sales greater than $1 million, and employed at least 50 persons. Despite theextensive efforts of their research team to reach a subset of companies listed in the Dunn & Bradstreet data,the study faces a lower response rate, selectivity in terms of which firms choose to respond, and perhaps limitsregarding the ability of the surveys to reach the right person to answer the questions related to the founders’origin (as an HR or a PR person might not know whether one of the founders moved to the United States as achild). Therefore, the researchers extrapolate from their sample to produce nationally representative numbers forrevenue and employment generation. Monti et al. (2007) provide related evidence from Massachusetts high-techfirms.

5

piece, Anderson and Platzer (2006) identify the higher immigrant entrepreneur share amongpublicly-listed VC-backed U.S. companies.Related to our focus on entrepreneurs and how immigration influences the supply of these in-

dividuals, prior studies show that more-educated business owners run more-successful businesses,generate more innovations, and grow their firms faster over time (e.g., Unger et al., 2011). Thereis an overall positive relationship between education and business ownership, although the ev-idence is somewhat mixed as highlighted in the meta-analysis of van der Sluis et al. (2008).Lofstrom et al. (2014) postulate that this may be due to sorting into industries based on entrybarriers. They find that educational credentials of highly educated potential entrepreneurs areassociated with lower probability of small-firm ownership in less-financially-rewarding industries,while they increase entry into higher-barrier industries offering higher returns.Immigrants can take a variety of paths into firm ownership in the United States. Many

skilled immigrants enter the United States for study or paid work and found their company afterseveral years in the country, while a smaller number enter for the specific purpose of openinga business. Kerr et al. (2015a,b) describe in greater detail how U.S. immigration law andcorporate sponsorship of visas contribute to this career trajectory. Akee et al. (2007) find thatpre-migration self-employment in home countries increases the probability of self-employmentby immigrants in the United States and boosts self-employment earnings. Lofstrom (2002)finds that self-employment probabilities and earnings for immigrants increase with time spent inthe United States, perhaps even reaching earnings parity with observationally similar U.S.-bornentrepreneurs after about 25 years in the country. The use of repeated cross-sections of Censuses,however, limits the degree to which the role of assimilation can be separated from selective out-migration. Blau and Kahn (2016) describe cultural factors influencing gender-based rates ofassimilation for work by immigrants.The spillover effects to native opportunities for opening a business have been examined by

several research teams. Fairlie and Meyer (2003) find some evidence that immigration maynegatively affect native self-employment probabilities using the 1980 and 1990 Census records.Other researchers suggest skilled immigrants generate positive spillover effects in local areas. Forexample, recent work points toward positive spillover effects for cities or states when measuredin terms of innovation, publications, and productivity (e.g., Kerr and Lincoln, 2010; Hunt andGauthier-Loiselle, 2010; Peri et al., 2015). Lewis and Peri (2015) provide a theoretical frameworkand review of literature on the effects of immigration on local areas. Evidence from morehistorical contexts are mixed (e.g., Borjas and Doran, 2012; Moser et al., 2014). Kerr (2013)provides an extended review of literature on skilled immigration and notes the particular gaparound the empirics of immigrant entrepreneurship specifically.Another line of work documents how immigrant entrepreneurs appear to specialize in a

narrower range of industries or occupations compared to native entrepreneurs. Very commonexamples from the United States include Korean entrepreneurs for dry cleaners, Vietnamese

6

entrepreneurs for nail care salons, Gujarati Indian entrepreneurs for the motel industry, andPunjabi Indian entrepreneurs for convenience stores. Chung and Kalnins (2006) provide a firstanalysis of this specialization for U.S. Indian entrepreneurs, and Patel and Vella (2013) documentpatterns more broadly and show earning consequences. Fairlie et al. (2010) provide cross-country comparisons for some groups. Kerr and Mandorff (2015) provide a theoretical modeland empirical evidence of how small group sizes and social isolation can provide comparativeadvantages for ethnicities in self-employed sectors where the entrepreneurs benefit from the tightnetworking of their social group.Compared to this earlier literature, the LEHD-based platform has the capacity to provide

critical and novel information for the enhanced understanding of immigrant entrepreneurshipand the effective calibration of immigration policy. Indeed, even though earlier work has tackledmany important issues, there remain unfortunate gaps in both the big-picture study of immigrantentrepreneurship and in the depth of insights feasible.Starting with the big picture, immigrant entrepreneurship is often greatly hyped in both

policy and media circles, and a number of newspaper and business press articles (e.g., Forbes,New York Times) tout immigrant founders as the solution to the sluggish recovery from theGreat Recession. Similarly, current local and national policy efforts seek to attract and supportnew firm formation by immigrants, as noted in the Introduction. Many of the studies in Table1 are limited by sample designs that are not broadly representative of the economy, or they arecross-sectional in nature if representative. This creates a credibility challenge for the work, evenwhen undertaken with the utmost objectivity; the gap gets extremely large with advocacy piecesor those concentrating only on the most prominent high-tech clusters. Building directly uponadministrative data, an LEHD-based platform can provide a substantially stronger foundationfor its covered states and the credibility necessary for grounding debates around common facts.The depth is also essential. Some studies, such as Fairlie (2008, 2012) and Fairlie et al.

(2015), provide attractive estimates from the Current Population Survey (CPS) that are thecurrent best practice for longitudinal series. The CPS is in many respects a solid platform,given its stable data collection and long series, and we compare some of our work to the CPSlater. The diffi culty with the CPS is the ultimate depth that it can provide. Its sample sizes ofabout 500 thousand adults are large enough to provide annual estimates for states or industries,but the cell counts become too small when attempting to jointly view these traits. Moreover,the CPS records cannot be linked to future growth trajectories of the firms, the use of venturecapital funding, and so on. The CPS relies on founders declaring themselves to be self-employedand yet also does not measure if other employment is being generated. Thus, while the CPS isan important and publicly-available resource, the development of an LEHD-based platform thatincludes every business in covered states will provide much deeper capacity for statistical andanalytical work. As we describe below, there is no question that the LEHD is far from perfectin terms of what it can do; on the other hand, if these limitations are acceptable, then the scope

7

of follow-on work becomes extraordinary. This depth is true in terms of potentially publishablestatistics of entry rates, and also in terms of more complex academic questions (e.g., how manyprior employers do immigrants typically have before starting a firm and how does this prior jobhistory impact entrant performance).Reading the anecdotal accounts and collected statistics regarding immigrants being very

involved in high-growth entrepreneurship, it seems natural from a policy perspective to wantto encourage this development. Encouraging immigrant entrepreneurs seems like an essentialprong of science policy, and its mandate reaches the highest levels of government. Yet, the earlierresearch has developed only partial data needed to effectively evaluate these policies or enhancetheir design. Research based upon case studies or small surveys may identify the trend, butthey fail to build the empirical foundation necessary for confidence in the design of proposedlegislation and the likely impact of reforms. The data platform introduced here makes significantheadway in that respect as it will utilize and combine universal and unique micro-data sets onindividuals and firms (LEHD, LBD, and the Decennial Censuses). In short, this provides aunique platform for the study of immigration and entrepreneurship.

3 Census Bureau Data and Measurement

3.1 Data Platform

The LEHD is the centerpiece of our platform, in combination with the LBD and a person-levelmatch to the 2000 Decennial Census of Population (Census). These datasets are confidential,housed by the U.S. Census Bureau, and accessible via Research Data Centers. Built from quar-terly worker-level filings by employers for the administration of state unemployment insurance(UI) benefit programs, the LEHD identifies the employees of each private-sector firm in theUnited States and their quarterly compensation. It is longitudinally linked at both the firm andemployee levels, allowing one to model how firm employment structures adjust over time, hownew entrepreneurial firms form, and how individuals transition from wage work into entrepre-neurship. This rich data source is currently available for 31 states for research purposes, and itwill eventually cover the whole country.The initial LEHD dates vary by state, and we focus on two samples in this paper. The first is

the 11 states that have LEHD records that begin by 1992 or earlier: California, Colorado, Florida,Idaho, Illinois, Louisiana, Maryland, North Carolina, Oregon, Washington, and Wisconsin. Ourdata extend through 2008, and the newest vintage of the LEHD continues coverage until 2011.Certain analyses are also conducted on a larger set of 28 states present in the LEHD by 2000as shown in Appendix Table 1 and Figure 1. The larger sample can only be followed over ashort time span, but it helps us understand the impact of state-level variation in immigrationand entrepreneurship rates for the trends presented in this paper, particularly the inclusion ofimmigrant-heavy California and Florida among our primary sample.

8

The LEHD Individual Characteristics File (ICF) contains basic information about individu-als, such as age, gender, race, place of birth, and citizenship status. Through the EmploymentHistory Files (EHF), one can also discern earnings and employment histories of each personjob-by-job and in aggregate. In addition, unique person identifiers (PIKs) afford matches of theLEHD to the individual-level records contained in the 2000 Census of Populations. PIKs areanonymous identifiers that match one-for-one with Social Security Numbers. The Census long-form responses cover 1/6 of the U.S. population, allowing us to link Census responses for roughly16% of our LEHD workers. From the 2000 Census, we extract individual-level characteristicsfrom the Person File and household and housing-unit characteristics from the Household File.Long-form responses contain very detailed person and household characteristics (e.g., year ofentry into the United States, level of education, occupation, marital status, family composition,household income by source, etc.). It is important to recognize that while the LEHD coversemployees from the early 1990s through 2008– including new immigrants at the end of the endof the sample period– the 2000 Census match requires individuals to be living in the UnitedStates by 2000.We build a tailored dataset for the analysis of immigrant status and entry into entrepreneur-

ship, first focusing on the dynamics over time. We take several steps to reduce the set of massivedata records into a manageable platform that properly represents the phenomenon of interest,and it is important to describe these steps as they have some bearing on our measurements. Webegin by retaining for each individual their main job during the year (i.e., the job from which theperson obtains the majority of their LEHD earnings). We also only retain persons for whom theaverage quarterly earnings from the main job are at least $2,000 per quarter. We further restrictour sample in each year to individuals aged 25 to 50. This age restriction is such that we stayreasonably far away from retirement decisions– and in particular, the formation of small-scalebusinesses as a form of semi-retirement– and concentrate on entrepreneurial activity in the peakemployment years of each person’s working life. Moreover, we require individuals be present inthe LEHD at least three quarters that span two calendar years.Immigrants are simply identified as those persons born outside of the United States. This

information is available for all LEHD individuals and is based on the Social Security Adminis-tration (SSA) Statistical Administrative Records System (i.e., StARS database). Some of theseimmigrants may have later been naturalized and become citizens, but that information is notutilized in this study. This is partly due to our focus and also due to uncertainty about theupdating procedures for this information. By defining immigration status through the ICF files,we can depict immigrant entrepreneurship consistently over the sample period, including new ar-rivals. We separately consider information from the match with the 2000 Census, which recordsthe year when the immigrant arrived into the United States.

9

3.2 Defining Firm Entry and Entrepreneurs

Our evaluation of entry into entrepreneurship also utilizes the LBD, a business registry that con-tains annual employment and payroll for all private-sector establishments in the United Statessince 1976. The LBD and the LEHD use several levels of establishment and firm identifiers:[1] State Employer Identification Numbers (SEIN), [2] federal Employer Identification Numbers(EIN), and [3] the overall company identifier (ALPHA) that the Census Bureau uses to link theestablishments of multi-unit companies together. Following Haltiwanger et al. (2013), we iden-tify for each establishment the first year during which the firm that the establishment belongs towas observed to be in operation within the LBD. We also create for each firm the number of em-ployees that the LBD reports were working for this firm in the initial year.4 Approaching entrantdefinition in this way accomplishes several things– it builds off of the national LBD databaseto avoid issues related to the partial LEHD state coverage, connects SEINs as appropriate intoparent firms, and ensures a consistent definition of entry with prior academic work using theCensus Bureau data. As two examples, this approach ensures our entrepreneurship definitiondoes not include the formation of a new SEIN by an existing multi-unit firm expanding into anLEHD state, or the development of new SEINs for tax purposes by existing businesses. Withrespect to the broader literature, our approach focuses on the formation of employer establish-ments, whereas the commencement of Schedule C self-employment activity is unmeasured andnot considered to be entrepreneurship in this sample.5

A very important issue, and the weakest link of these data for the study of entrepreneurship,is that the LEHD does not designate the founders or owners of firms. Similarly, compensationdata includes bonus pay but not equity ownership of individuals. We use the term "entrepreneur"to describe anyone present in the data who satisfies three criteria: [1] in an entering single-unitfirm per the Haltiwanger et al. (2013) definition, [2] present in the LEHD in the first year thatthe new firm entered, and [3] among the top three initial earners in the firm. With respectto the first condition, we require the new firm be a single-unit firm in its start year to ensurethat we have complete employment records from the LEHD. By itself, the second conditionfocuses on the initial employees of the firm and will in many cases include early hires. Thethird condition then associates entrepreneurship with the top initial earners in the firm. Thiswill clearly be inaccurate in some cases, and some entrepreneurs deliberately take low salariesor no compensation from their firms early on to conserve funds. On the other hand, as wedescribe below, most firms in our sample are small and are likely reasonably well modelled bythis approach. We also show results that drop the third condition and thereby provide statisticsrelated to all initial employees in the firm.Terms like "entrepreneurship" are also vague with respect to the time dimension. For exam-

4The data structure of the LEHD and LBD allow for establishments within each firm to have different industriesand locations. In rare cases where required in this study, we define the main industry and main location of amulti-unit firm through the facility with the largest number of employees.

5There is scope for further work on this regard using the Integrated LBD that contains non-employer firms.

10

ple, a strict application of our three-part definition would declare the founder of a new firm to bea wage worker starting in the second year of a firm’s life, yet many still consider Mark Zuckerbergto be an entrepreneur a decade after the founding of Facebook. For most of our trend statistics,we accordingly use a three-year window that declares an individual to be an entrepreneur iftheir firm was founded in the prior three years. We still require that the individual had beenpresent in the year of founding and a top initial earner, the second and third conditions. In fact,we do not require the individual remain necessarily associated with the firm, simply that thefirm and individual persist. We present results that alternatively use a strict one-year definition.Overall, an unfortunate trade-off exists in that longer windows for keeping track of entrepreneursresult in shorter sample durations, due to the greater number of pre-period years that must bedevoted to determining the initial values. Said differently, if we wanted to declare individualsto be entrepreneurs if they have founded a business over the prior ten years, the earliest startdate for the LEHD-based sample series is 2001, after the 1990s high-tech boom period that is sointeresting to study.

3.3 Benchmarks for Definitions

We can use the public-use Survey of Business Owners (SBO) data from 2007 to help benchmarkthese choices with respect to the top three earners and their limits. The file contains overtwo million observations on employer and non-employer firms, and the data contain detailedinformation about the firm and its owners. We focus on employer firms that mirror the LEHD-based sample built upon UI data, and we drop a small number of firms where the firm does notreport whether the first-listed owner is a native or immigrant or no ownership data are presentat all. Throughout, we use sample weights to provide population-level statistics.6

We first analyze the likelihood that the business represents the owner’s primary source ofpersonal income. For the full cross-section of single-owner businesses in 2007, this is true for81.8% of businesses with an immigrant owner and 81.4% of businesses with a native owner.Similarly, when incorporating businesses with multiple owners, at least one owner reports thebusiness as the primary income source in 81.9% of firms where an immigrant owner is present,very similar to the 81.3% rate in firms where no immigrant owner is present. When looking atthe most recent entrants (i.e., business founded in 2007), the overall fraction of businesses beingthe primary income source unsurprisingly declines due to transition issues, but remains at two-thirds. It also tilts modestly towards immigrants– across all 2007 entrants, 70.3% and 64.7%of immigrant- and native-owned entering businesses constitute the primary ownership source,respectively, and this difference is statistically significant (t-stat=4.03). Nonetheless, these gen-

6Data and descriptions are available at: https://www.census.gov/econ/sbo/pums.html. This is the first-ever SBO Public Use Microdata Sample and it allows researchers to create their own tabulations and analyseson entrepreneurial activity, including the relationships between firm characteristics such as sources of capital,number of owners, firm size, and firm age. Going forward, a main data objective is to unite our LEHD platformwith the confidential version of the SBO.

11

eral patterns are supportive of the use of LEHD records for identifying entrepreneurs, comparedto an environment where most owners only derived very modest sums from businesses (e.g.,businesses set up for tax purposes, hobby entrepreneurship, or to employ household workers).We next consider calculations that help evaluate our focus on up to three owners. The news

is again mostly supportive. Across all SBO firms in 2007, the average number of owners is 1.8,while for the newest 2007 entrants it is 1.7 owners. With our approach in the LEHD data, theaverage owner number is 2.16. This difference comes mostly from underestimating the shareof firms with a single founder, and in some cases we are including an extra person in some ofour assignments. On the other hand, a non-trivial share of SBO businesses report four or moreowners compared to our cap at three entrepreneurs. Without more information, we must drawthe line at some founder count, and we believe three founders provides the best balance.This trade-offsuggests that we need to examine closely how immigrant owners are distributed

over the owner count distribution to see if scope for bias exists. Focusing on the 2007 entrants,we find relatively uniform rates of an immigrant owner being present: 23.4%, 22.4%, 27.0%,and 27.3% for firms with 1, 2, 3, and 4+ owners, respectively. A rising share on this dimensionis to be expected, given our focus on any owner being an immigrant, and the differences arevery modest. This suggests a rather small scope for issues emerging with counting too few ormany owners with our three-person definition. This does not resolve the possibility of confusingemployees with owners, to which we return shortly. Among the largest ownership teams forentering firms, we do not find immigrants being substantially different in terms of order listed.For 4+ person teams, the immigrant shares are 20.3%, 14.4%, 13.8%, and 14.2% for the firstthrough fourth positions (max reported) of listed owners. These structures again do not suggestvery substantial issues likely to emerge with a three-person focus compared to using two- orfour-person cut-offs.7

As a final step, the SBO contains some employment information that we can compare againstthe owner counts. As advanced warning, however, two significant issues exist in the analysis tofollow. First, how each firm chooses to count owners towards employment is unclear. Second,the public-use SBO files intentionally introduce noise into the employment data to protect theidentify of firms. Thus, while we believe the following analysis is quite informative for whetherour definition creates a bias for immigrant vs. native businesses, we need to be cautious aboutthe exact figures reported. Our approach is simply to define an indicator variable for caseswhere we know we would have added an extra employee to our owner/entrepreneur definitionbecause the employment count exceeds the owner count and the owner count was less than threeowners; this is not comprehensive for all possible errors in our definition, but it is the mostworrisome. Among the 2007 SBO entrants, this condition is met in 39.4% cases. This numberseems high to us, but we also don’t know really how to evaluate it in light of the noisy data,

7In our regression sample, our mean immigrant entrepreneur share is 22.6%, with a 2005/1995 growth ratioof 1.31 (Column 2 of Table 3 that is discussed below). We find comparable means and very similar growth ratioswhen examining firms that start with one entrepreneur (23.6%, 1.32) or two entrepreneurs (21.4%, 1.29).

12

etc. What we do take great comfort in, however, is that this fraction is 40.3% for immigrant-owned businesses and 39.1% for native-owned businesses, with the differences not statisticallysignificant (t-stat=0.74). This suggests that we while we may modestly mismeasure levels (e.g.,identifying too many entrepreneurs), we are unlikely to have a bias by immigration status inthis regard.Overall, we take comfort in the SBO comparison. Any single rule like our three-person

definition will face liabilities, and these tabulations appear to say our calibration is reasonablybalanced. We also note one feature that helps isolate our technique from potential biases wherewe may identify an employee as an entrepreneur. Empirical studies of the hiring patterns byimmigrant owners emphasize the strong degree to which they hire from their own ethnic group(e.g., García-Pérez, 2012; Andersson et al., 2012, 2014; Åslund et al., 2014). Thus, our "falsepositive" for an immigrant-owned business is most likely to be an immigrant, and vice versafor a native-owned business. As an extreme example, our definition would be fully robust tounpaid owners or the inclusion of too many wage earners if the immigrant status of the employeesexactly mirrored that of the true owners. This extreme condition does not hold, of course, butthe quite high rates of concentration among small employers documented in Andersson et al.(2014) and similar studies are comforting for our design.A second point of comparison comes from individuals to whom we can link LEHD records to

their responses to the 2000 Census. The long-form collects whether or not an individual declaresthemselves to be primarily self-employed in an incorporated firm, primarily self-employed inan unincorporated firm, an employee in a private-for-profit firm, or other categories. Lookingat 2000 for individuals working in an SEIN created since 1995, we find that we label as anentrepreneur 66% of those declaring themselves to be self-employed in an incorporated firm. Bycontrast, we only label as an entrepreneur 29% of those declaring themselves to be self-employedin an unincorporated firm. Thus, our definition clearly tilts towards incorporated firms and thoseoriented towards employment and possibly growth, capturing a large portion of this group. Thelarger deviation, which is not surprising, is that about two-thirds of the overall set of peoplewe declare to be entrepreneurs are listing themselves as an employee in a private-for-profit firm.Specifically, the composition of our entrepreneurial pool breaks down as 68% saying they areemployed in private-for-profit firms, 28% self employed, and a small residual in other categories.In many of these new firms, no one is declaring themselves to be self-employed, which is alimitation of this approach to defining entrepreneurship. We thus find it diffi cult to benchmarkthis form of the metric compared to the self-employment breakdown.

3.4 Measuring Firm Dynamics

Our analyses consider the survival and growth of new businesses, which we measure exclusivelythrough the LBD. This choice, which was not obvious to us at the start of this project, isimportant. By measuring outcomes through the LBD, we capture the full employment and

13

payroll growth that the firm experiences (domestically in the United States). Alternative metricsbased upon SEINs alone can miss substantial firm adjustments that occur within LEHD stateswhen they open up new SEIN codes. Moreover, by definition, LEHD-based definitions of growthare subject to the state coverage limitations of the database. Thus, in combination with thediscussion above, our strategy can be summarized as follows– [1] find single-unit firm entrantsduring 1992-2008 in the LBD that are in a covered LEHD state, [2] collect the initial employmentrecords that are contained in the LEHD to describe the immigrant-native composition of initialemployees and founders, and [3] return to the LBD for subsequent growth outcomes. Thisstrategy allows us to retain all entrants and consistently measure growth; fortuitously, it alsolets us use the LBD outcome data to 2011 for growth dynamics even though our version of theLEHD ends in 2008. The only potential biases will relate to the specific set of states that weobserve and how they compare nationally. On the other hand, this strategy would not necessarilybe optimal in cases where one wanted to observe the employment composition of firm growth(e.g., the year-on-year subsequent hiring of immigrant or natives).Our platform describes immigrant entrepreneurship in general and across sub-populations.

We split the sample by low- and high-wage firms using the median quarterly earnings duringthe year of entry. We also define firms as high-tech if the majority of their employment is in athree-digit SIC code listed as a high-tech industry in Hecker (1999). Separate characterizationsare also provided by one-digit SIC codes. Given the specific academic interest and policy focuson VC-backed firms, we identify entrants that receive VC funding by 2005, as recorded in theVenture Xpert database, using name and geographical-location matching algorithms (Kerr et al.,2014). As we do not have matches beyond this point, we only study VC-backed entrepreneurshiprates through 2005. Finally, we provide some tentative notes about whether firms go public by2005. This information is collected by observing whether the new firm is later present in theCensus Bureau’s Compustat Bridge File, which was last updated for the 2005 public firm cohort.

3.5 Additional Discussion

A central goal of this project is the compilation of information and best practices necessaryfor using the LEHD for studies of immigrant entrepreneurship. To this end, a detailed dataappendix provides specific instructions and commentary for researchers regarding the LEHD,with a special focus on the firm-level dimensions and the longitudinal aspect of the LEHD data.This appendix information extends beyond the present study to also document issues noted inthe Kerr et al. (2015b) study of large firms. Additional restricted-access materials are availableupon request. The appendix also provides thoughts about other datasets that could improveupon the entrepreneurship definitions developed here.

14

4 Entrepreneurship Trends

4.1 LEHD Statistics

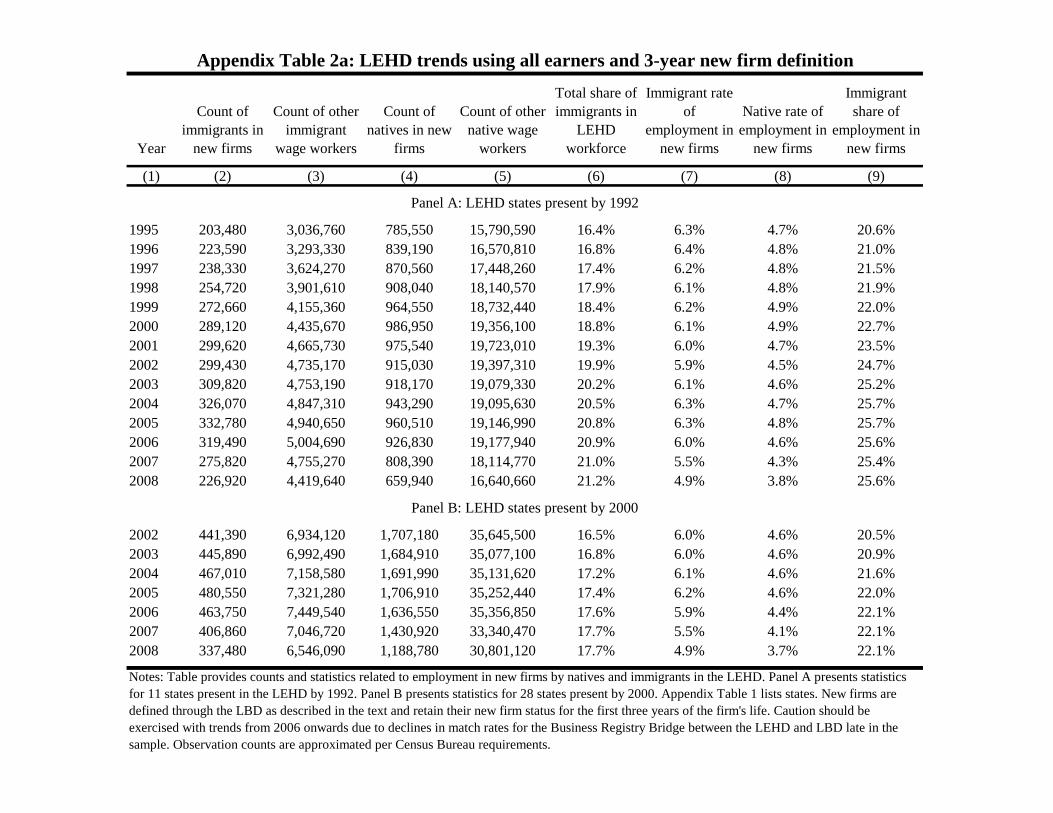

Table 2a presents our core trends using all LEHD workers and a three-year definition for en-trepreneurship. For these initial tabulations that regard all workers, we do not impose thesingle-unit firm restrictions or similar, keeping a very broad set of data. Column 2 considers im-migrant participation rates in new firms relative to the total immigrant workforce in the LEHD.Approximately 6.0% of immigrants in the LEHD are working in new firms born over the priorthree years, with some evidence for a decline in the rate over time. Appendix Table 2a providesthe observation counts that underlie these estimates, which cover 3.2 and 4.6 million immigrantsin 1995 and 2008, respectively. Throughout this paper, observation counts are approximate androunded per Census Bureau disclosure requirements. This appendix table also shows that immi-grants constitute 19.3% of the LEHD sample during 1995-2008, growing from 16.4% to 21.2%,and the native rate of employment in new firms averages 4.6% (versus 6.0% for immigrants).The native rate is similarly declining after 2005.8

Column 3 documents that 2.2% of immigrants are among the top earners in a new businessand thus declared to be an entrepreneur by our definition. Parallel to Fairlie and Lofstrom (2014)and in contrast to Column 2, this share grows substantially to 2005, before declining some.Features of the data initialization process for identifying entrepreneurship are more diffi cultfor 1995 and 1996 for some states, and we are required to use some minor extrapolation forthese initial years for Column 3 in Tables 2a and 2b. These initialization challenges impactentrepreneurial rate calculations mostly, with upcoming share-based calculations in Columns4-10 being substantially less sensitive and unadjusted. Similarly, we report the trend statisticsthrough 2008, but we hesitate to make too much of the declines observed after 2005. Through2005, the entry rates are overall stable, and we believe some, if not all, of the decline after 2005can be traced to declines in match rates of new firms in the Business Registry Bridge betweenthe LEHD and LBD. That said, to the extent that the trends are real, they would match thebroad secular decline in employment in young U.S. firms documented by Decker et al. (2014).Most of our focus is on the share of entrepreneurs who are immigrants, which is not materiallyinfluenced by these issues.Columns 4-10 consider immigrant shares of activities relative to natives. Columns 4 and 5

repeat the previous two analyses on a relative basis. We estimate immigrants account for about24% of entrepreneurs and the new employees of firms in our sample. The immigrant share of newentrepreneurs rises dramatically in our sample from 16.7% in 1995 to 27.1% in 2008, while thetrend for immigrant shares of initial employees is more modest. Figure 2 graphs these trends. In

8While the 11 states are present in the LEHD by 1992, the statistics begin in 1995 to allow full initiation ofall of our data and definitions. For example, while we can identify from the LBD the full set of young firms in1992 (i.e., those born in 1989-1992), we do not know the immigration status of all of their top earners in the firstyear of the firm’s life.

15

Column 6, we isolate the top quartile of the initial earnings distribution of start-ups (measuredas quarterly averages). Immigrants tend to create firms with lower initial earnings, and theupward trend in immigrant shares for this top quartile is a bit weaker. Some of this patternresurfaces below when looking at payroll growth regressions.A number of studies report the share of firms with at least one immigrant founder. This often

appears motivated by a desire to have the highest share possible for advocacy pieces, but it mayalso stem from a genuine desire to capture the number of businesses touched in some way byimmigrant entrepreneurship. By contrast, our baseline estimates are implicitly allowing fractionimmigrant entrepreneurship in firms with several starting employees and weighting larger initialteams more (up to three employees). Columns 7 and 8 show that about 35% of entering SEINsor LBD firms have an initial immigrant employee, with Column 7 also implicitly showing thatour LEHD-LBD match is not introducing a bias. Columns 9 and 10 show patterns defined overlarger LBD samples. While the results vary somewhat depending on these definitions used, themain message from Table 2a is that the overall time-series pattern of our findings remains largelyunchanged– immigrants are accounting for roughly a quarter of entrepreneurs and their shareis increasing with time.Appendix Table 2a provides complementary statistics for the 28 states present in the LEHD

by 2000. The wider state panel allows us to assess the potential impact of focusing on just 11states, including two of the nation’s most immigrant-heavy states, California and Florida. Con-sidering the overlapping 2002-2008 period, our longer panel has an average immigrant workershare of 20.6% compared to 17.3% in the wider sample; likewise the immigrant share of entrepre-neurship is 25.4% versus 21.6%. Thus, our "levels" statistics are on the order of 3% higher. Onthe other hand, rates of immigrant and native entry are extremely close (5.9% vs. 5.8%, 4.5%vs. 4.4%), and all of the 2002-2008 trends are very close to each or even stronger in the widersample. We thus conclude that our longer state sample may overstate national levels slightlybut are otherwise quite representative. This is due in part to the larger average state sizes in thelonger panel (despite the addition of Texas in the larger set of 28 states), with the 11 baselinestates constituting 57% of the employment in the 28 states during 2002-2008.Appendix Table 2b shows that the results are robust to defining new firm employment through

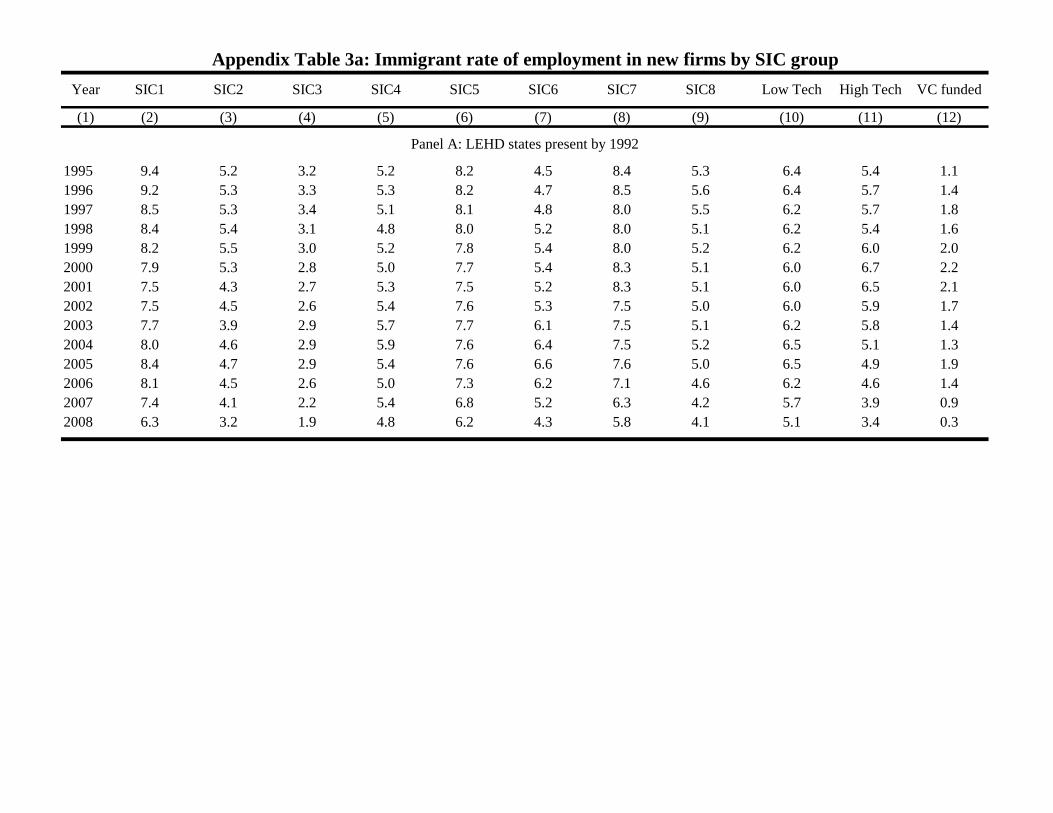

the first year of business entry only. This narrower definition essentially cuts the rate of firm entryby two-thirds. The one-year employment rate in new firms for immigrants is now 2.0%, comparedto 1.5% for natives, a sizeable differential remaining. The immigrant share of employment innew firms grows from 17.6% in 1992 to 24.9% in 2008, parallel to our baseline results in Table2a.Appendix Tables 3a and 3b report results for one-digit industries. Rates of immigrant entry

are highest in mining & construction (SIC1), wholesale & retail trade (SIC5), and services (SIC7).Splitting industries at the three-digit level, entry rates tend to be higher for low-tech sectors, butthis pattern is inverted around 2000 during the high-tech boom. A similar pattern is evident for

16

VC-backed entry. Some of these patterns reflect inherent differences in entry rates across sectorsand over time, common to immigrants and natives. In terms of share of initial employment,immigrants have higher relative representation in manufacturing (SIC2-3), wholesale & retailtrade (SIC5), and services (SIC7).Table 2b repeats Table 2a for the part of our sample of firms that are backed by VC investors.

About 0.11% of immigrants are starting top earners in VC-backed firms during 1995-2005. Thisshare is naturally substantially less than the 2.2% in Table 2a due to the relatively small numberof ventures receiving VC investment. Reflecting the VC bubble that peaked in 2000, this rateis hump-shaped over time with a peak in 2000. Immigrants constitute about 28% of VC-backedfounders, with this fraction increasing over time. The substantial majority of entering VC-backedfirms have at least one initial immigrant employee, with the more-similar results regarding overallfractions of founders coming from the fact that VC-backed firms tend to have larger countsof initial employees and larger founding teams. On the whole, immigrant entrepreneurship issomewhat stronger for VC-backed firms than generally, with 30% of the former being immigrantscompared to 27% overall in 2005.Our data platform allows us to compare initial immigrant and native employees by [1] their

LEHD characteristics for the full sample and [2] the Census long-form responses for the matchedsample. Appendix Tables 4 and 5 provide these results that we quickly summarize here. Onaverage, immigrant employees in new firms tend to be slightly older and more likely to be male,with lower average LEHD quarterly earnings before, during, and after the founding of the firm.By contrast, the average quarterly earnings for immigrants before, during, and after the foundingof VC-backed firms tends to be higher than their native peers. Looking at respondents matchedto the 2000 Census, immigrants employed in young firms are more likely to be older, male,married, and have more children. While less likely to own a home, immigrants are more likelyto own a higher-priced home and rent more-expensive properties. This is partially connected toimmigrants being more likely to live in high-priced gateway cities. The average year of arrivalfor our 2000 cross-section is 1984, so that the average tenure in the United States in 2000 is 16years. These statistics are reasonable and comforting for our match, although we focus mostof our analytical attention elsewhere. We return later to the year of arrival when consideringdifferences between adult arrivals and those migrating as children.Fairlie (2013) documents from the 2007 SBO that immigrant-owned businesses represent

13.2% of all businesses in the United States, with $434,000 in average annual sales (compared tonon-immigrant-owned firm sales of $609,000). Only 28% of immigrant-owned businesses in theSBO hire outside employees, while the share is even smaller (26%) among the non-immigrant-owned businesses. For those that do hire employees, the average number of employees is 8 inthe immigrant-owned businesses and 12 in the native-owned businesses. Among our sample, theaverage initial employment for firms founded by immigrants exclusively is 4.4 workers, comparedto 7.0 workers for firms launched exclusively by natives. When both types of founders are present,

17

the average is 16.9 workers. Thus, in general, our data appears to match the broad levels andpatterns of the employer firms in the SBO sample, as well as differences in the typical sizesbetween immigrants and natives. Our overall numbers are naturally lower given the focus onthe initial year of the firm (versus a cross-section of employment patterns in existing firms).

4.2 CPS Comparison

To check our LEHD-based approach against publicly available survey data, we derive entrepre-neurship trends using the Current Population Survey (CPS) Merged Outgoing Rotation Group(MORG) data from the NBER.9 The data include details about the respondent’s place of birthstarting in 1994, and also reports the class of worker where one of the categories is "self-employedin an incorporated business". We prepare a CPS sample that matches the traits of our LEHDwork, starting with individuals aged 25 to 50 who live in one of our core 11 states and work inthe private sector. We further limit the data to those persons who are in the labor force andhave a known level of education and potential labor market experience of at least one year. Tostay consistent with the LEHD, we include as immigrants all those who are born outside of theUnited States.Figure 3a first compares the immigrant workforce shares evident in the two data sources. The

levels are very comparable, and the trends quite similar, with the CPS trend being modestlysharper. Figure 3b next compares the immigrant share of the entrepreneurial groups. TheCPS trend includes as new entrepreneurs those who are newly self-employed in an incorporatedbusiness. The levels are more different here, with the LEHD being consistently at least 3%-4%higher. Perhaps more important, while both are upwardly sloping, the timings are different. TheLEHD shows stronger growth during the 1990s, while the CPS picks up more in mid to late 2000s.We do not have a strong hypothesis regarding the source of these differences, although some of itmay connect to the CPS redesign in 2002-2003. Unreported tabulations include unincorporatedself-employed workers into the CPS entrepreneurial definitions, finding that the resulting trendsits in-between the two series shown in Figure 3b, with the augmented CPS series retaining itstrend differences from the LEHD.Figure 3c finally compares various metrics regarding rates of entrepreneurship for immigrants.

Relative to the immigrant entrepreneurial shares shown in Figure 3b, entrepreneurial rate cal-culations are substantially more sensitive to definitional decisions that can have large impacton their levels (regardless of data source). From the CPS, we provide at the top of Figure 3c ameasure of the incorporated self-employment rate for immigrants in the sample. This includesself-employed owners who have held their business for many years, and thus provides a higherestimate of about 3.5% for the years; this share would exceed 10% if including unincorporatedself-employment. At the bottom of Figure 3c is the Kauffman Foundation Index that is derived

9Data available at: http://www.nber.org/data/morg.html. We thank Ethan Lewis for his guidance on thiswork.

18

from the CPS through entry into self-employment (Fairlie et al., 2015); due to its focus on en-trepreneurial transitions, the rate is much smaller at about 0.4%. For the LEHD, we show ourcore measure, where we use a three-year window for counting entrepreneurs, and the one-yearversion that is most comparable to the Kauffman Foundation Index. It is clear that our metricsfall in between the extremes of CPS-based approaches. We tend to see comparable stability,and both data sources speak to a growing rate for immigrants compared to natives in terms ofentrepreneurial transitions (which is mostly implied by Figure 3b).10

5 Analysis of Firm Survival and Growth

We next consider differences in the performance of firms founded by immigrants versus natives.Table 3 first provides descriptive statistics for the sample of firms used for analytical workcomparable to Tables 2a and 2b. The analytical sample includes firms founded 1992-2005 ina Primary Metropolitan Statistical Area (PMSA) within a state present in the LEHD since1992. Relative to Tables 2a and 2b, several data preparation steps are undertaken to excludeentrants that are multi-unit LBD entering firms and entrants lacking complete information for theconsidered LBD and LEHDmetrics (e.g., reported payroll). The metrics focus on the immigrant-native composition of the top three initial earners. The sample ends with 2005 entrants to allowobservation of LBD outcomes until 2011 and to circumvent any issues with the LEHD-LBDmatch (Business Registry Bridge) in later years.Table 4a shows a basic tabulation of the data over a three-year growth horizon. We include in

this analysis all entering cohorts of firms during the 1992-2005 period, with outcomes measuredafter three years for each entrant (e.g., 2004 employment for a 2001 entrant). In Panel A, eachrow represents a separate starting size category in terms of employment. We then tabulatethe share of entrants for each starting size category that grow to the level indicated by columnheaders by the third year, with rows summing to 100%. Thus, Column 2 shows that over one-third of firms close across this time span, while Column 7 shows that very few firms reach orexceed 100 employees, especially when starting from the smallest size category. The cells in boldrepresent the least moment from initial employment levels, which is the most likely outcomeother than business closure.11

Panel B provides for each cell the average initial immigrant entrepreneurship share for thefirms in that group. Entrepreneur definitions use the top three initial earners, independent ofwhether these individuals remain top earners in the firm across the three years. The Total rows

10The one-year rolling definition of entrepreneurship in the LEHD provides an entry rate that is about two-thirds of the three-year basis in Figure 3c. This limited gap is due to the high rate of business failure in the firstthree years of operation. By contrast, employment in new ventures shows a greater difference, as described abovefor Appendix Table 2b. This is because employment counts capture the growth and scaling of surviving venturesthrough their first three years, in addition to business failure effects. As our identification of entrepreneurs isfixed from the first year of each venture and with a maximum of three founders, this latter effect is not presentand the differences based upon windows is smaller in Figure 3c.11The majority of closed businesses are failed companies, but closures also include acquired companies should

the LBD identifiers change, some of which may be quite successful outcomes.

19

and columns provide the weighted average immigrant entrepreneurship rates for their groups.The shares in Column 8 decline across starting levels reflective of the lower sample averageinitial employment for immigrant-started businesses noted above. Panel C similarly provides theaverage initial immigrant employment share for grouped firms independent of initial earnings.The intriguing initial pattern in the data points to a greater volatility of immigrant entre-

preneur outcomes. The immigrant shares are frequently lowest among the bolded cells thatrepresent static employment levels. In all cases, immigrants are more represented among closedfirms in Column 2 compared to the bolded cells. Moreover, among the firms that begin with5-9 or 10+ employees, immigrant shares are lowest in the bolded cells compared to any othermovement. In the smallest category, which Panel A shows is the most stagnant of the initial sizecategories, immigrant shares among those firms remaining at 1-4 employees closely mirrors theoverall share. Table 4b similarly considers a six-year growth horizon for cohorts, which uses theLBD data up to 2011 for our 2005 entrants. Over half of entrants fail by year six, which reflectstypical start-up life expectancies. The patterns are mostly repeated here, especially in Panel C.In Panel B, there is less evidence of upside growth outcomes.While intriguing, these tabulations do not account for general differences in when immigrant

versus native firms are founded or their other measurable attributes. To address these issuesTable 5a considers regressions of the three-year outcomes that take the form,

Yf,t+3 = ηt + βImmigrantEntrepreneurSharef,t + γXf,t + εf,t,

where f and t index firms and entering cohorts. We include a vector of cohort fixed effects ηtand control for the initial attributes of the firms (Xf,t) in terms of their starting log employmentand log payroll. Regressions are unweighted and report robust standard errors. Panel A presentsthe summary statistics for outcome variables. Panel B provides the baseline regression, with thelast row giving the relative effect of increasing the immigrant entrepreneur share from zero toone compared to the sample mean.Column 1 considers firm survival until the third year. On average, 64% of firms survive

this long, with immigrant-founded firms being 0.3% less likely to survive compared to similarfirms with only native founders. Columns 2-7 consider traits of firms conditional on survivingto their third year. We first look at employment growth, measuring changes relative to thefirm’s average in two periods following Davis et al. (1996): [Yf,t+3 − Yf,t]/[(Yf,t+3 + Yf,t)/2].

This measure is bounded by [-2, 2], prevents outliers, and symmetrically treats positive andnegative shifts. Conditional on survival, firms founded by immigrants show greater growth.Columns 3 and 4, by contrast, show no difference in terms of growth of payroll or establishmentcounts. The lower payroll growth may indicate lower wage growth, additional jobs being lowerwage, or that partial employment is in greater use. Column 5 alternatively models employmentgrowth through indicator variables for the firm achieving more workers than its initial level,while Columns 6 and 7 are similarly defined for the firm reaching 100 workers or being among

20

the top 10% of firms in terms of employment in its specific industry. These approaches confirmthe employment growth observed in Column 2. The final regression shows immigrant-startedfirms are much more likely to receive VC financing.Panel C takes a more-stringent approach that controls for cohort-PMSA-industry fixed ef-

fects, with industry being defined at the two-digit level of the SIC classification. This approachremoves any differences between immigrants and natives to found firms in certain cities or sec-tors, which can be important for outcomes, and instead compares immigrant outcomes to nativeswithin these narrow cells. We do not view either approach as an inherently better way to describethe data, as differences in the choices of locations and industries are as relevant as differencesin within-cell outcomes (e.g., due to different management practices). In some cases, this choicehas material impacts, while in other cases the results are robust across the variation employedin the estimates.12

In Panel C, we see that immigrant entrepreneurs are more likely to survive for three yearscompared to their closest native peers. The baseline employment growth is substantially dimin-ished in Column 2 compared to Panel A, while some of the binary employment growth outcomesin Columns 5-7 retain more strength. The most robust outcome is achieving the top decile ofindustry employment, which already has a degree of industry-level benchmarking built into it.Payroll growth is now significantly less than native peers, while establishment count growth isagain flat.Table 5b repeats Table 5a for the six-year outcomes. The relationships in Panel B are quite

comparable to the three-year outcomes, with payroll and establishment count growth now moreevident. Payroll growth is again noticeably smaller than employment growth. In general, there isgreater statistical precision for the results with six-year outcomes, and the relative magnitudesare larger in size compared to the U.S. average outcomes than earlier. The introduction ofcohort-PMSA-industry fixed effects in Panel C of Table 5b has a similar effect to what it didfor the three-year outcomes. Appendix Tables 6a and 6b repeat these outcomes using simplythe initial immigrant employee share as the explanatory variable, finding comparable results.Perhaps the key difference is that the employment growth outcomes are now more robust to theinclusion of the cohort-PMSA-industry fixed effects.On the whole, the data paint some interesting differences, albeit tentative and non-causal,

between firms founded by immigrants versus natives. When incorporating industry and citychoice into the variation, immigrant founders have a greater volatility that somewhat mimics theup-or-out dynamics of young firm growth described in Haltiwanger et al. (2013). They fail morefrequently, but generate greater employment growth if they manage to stay in business. Over asix-year horizon they become more associated with higher payroll and establishment counts, but

12Our analysis uses the geocoding for the initial PMSA for the business. In a separate context, Kerr et al.(2015) describe the geographic information in much greater detail for the LEHD and the LEHD-Decennial match.There is capacity within the LEHD to observe movements over cities for all individuals; for those matched to theDecennial Census, there is further power to look very closely at the locations of residence versus business. Thesedimensions would be very interesting to consider in the immigrant context.

21

these are second-order to employment outcomes. However, much of this action appears to comethrough the way in which immigrant entrepreneurs chose locations and industries. Conditionalon these features, they are more likely to survive than their native peers and modestly morelikely to experience employment growth, with payroll growth under-performing comparable firmsfounded by natives.Unreported estimations consider whether the industry or geography controls are more impor-

tant for the differences observed across panels in Tables 5a and 5b. The intriguing answer is thatgeography plays the central role– and especially one state. This can be expressed in two ways.First, where a reversal of coeffi cient direction occurs across panels, the same pattern usuallyoccurs when just introducing state fixed effects, while this is not true when introducing industryfixed effects. Second, adjustments in sample composition around the one state’s inclusion orexclusion can achieve similar shifts as well. We are not able to show these tabulations directlyor name the state due to the requirement that LEHD samples (or differences across two relatedsamples) contain three or more states. Our internal files record the state breakout. Thus, insome respect, the unconditional results evident in Panel B are the perspective taken when oneallows for much of immigrant entrepreneurship to be in one location. This can include possiblyendogenous flows of immigrants for opportunities, and it may reflect how immigrant entrepre-neurship impacts the state’s economic dynamics. By contrast, the patterns in Panel C of thesetwo tables are observations that control for these overall regional differences. Both perspectivesare quite important to consider.To look a little further behind these results, we also conduct several sample splits in Tables

6a and 6b for estimations with and without conditioning on cohort-PMSA-industry fixed effects.Each coeffi cient in the tables is from a separate regression. The top row repeats the baselinespecification, followed by splits between low- and high-wage firms, low- and high-tech sectors,and then VC backing (non-VC-backed results are not reported since they are so close to thebaseline outcomes). We most focus on Table 6b, where several intriguing differences are present.First, variation among low-wage and low-tech groups is generally responsible for our conditionalsurvival relationship. Second, employment growth is generally associated with high-wage andhigh-tech sectors. Third, payroll growth compared to natives is never present. Fourth, whileimmigrant-founded ventures are more likely to access VC financing, they do not display strongeroutcomes conditional on this financing. This is in many respects a parallel finding to our ob-servation that city-industry choice accounts for much of the observed differences in the generalsample. Finally, where employment growth occurs, it is usually about achieving any employ-ment expansion relative to the initial level or reaching the top deciles of an industry, rather thansurpassing the threshold of 100 employees (a benchmark that few newly started firms make).This is true for the general and VC-backed samples, suggesting that employment effects due toimmigrant entrepreneurship are more likely to come from accumulated contributions of manyfirms compared to the extreme outcomes of a few high-growth entities that are often emphasized

22

in the popular debate.In unreported estimations, we also look at the probability of achieving an IPO by 2005, both

in the whole sample and among firms backed by VC investors. We do not observe differencesfor immigrant entrepreneurs in this regard, but we also hesitate to emphasize this result giventhe early end date of the Compustat Bridge File for our sample.While this study does not identify why immigrants might choose riskier city-industry cells,