ignis citywire berlin_nov11_final

DESCRIPTION

TRANSCRIPT

Ignis Absolute Return Government Bond Fund

Diversified returns from global government bonds and currencies

This presentation is intended for professional clients and investment professionals only and should not be relied upon by retail investors.

Introduction

Ignis fixed income capabilities

Investment process

Fund summary

Appendix

Agenda

November 11

1

Ignis Absolute Return Government Bond Fund

Introduction

Ignis Absolute Return Government Bond FundNovember 11

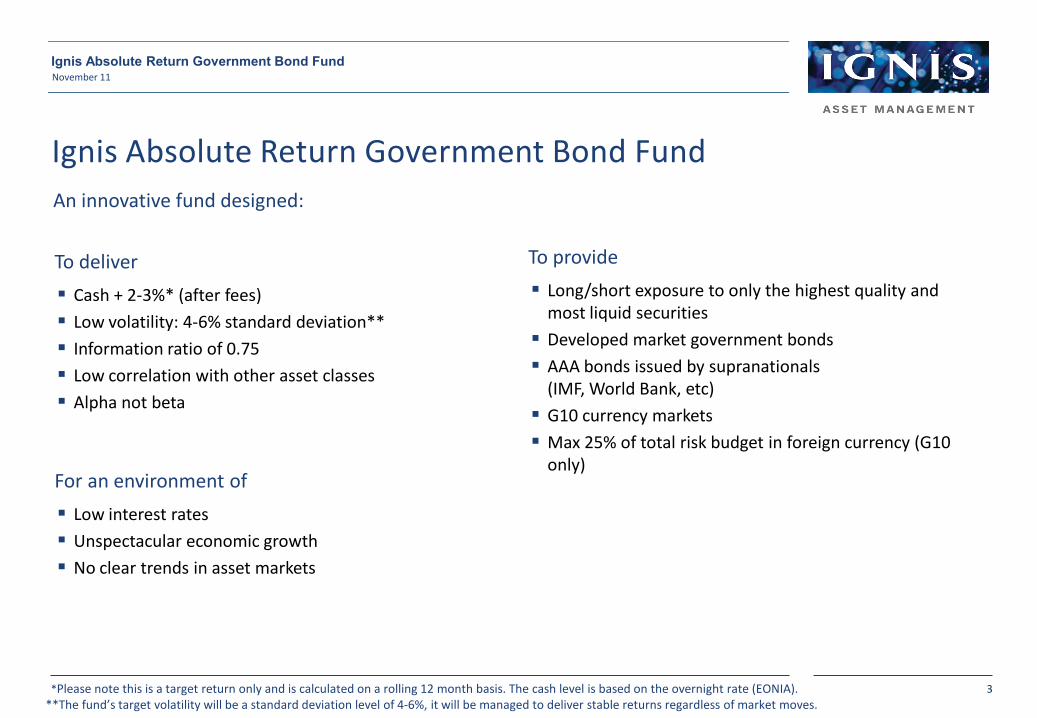

To deliver

Cash + 2-3%* (after fees)

Low volatility: 4-6% standard deviation**

Information ratio of 0.75

Low correlation with other asset classes

Alpha not beta

For an environment of

Low interest rates

Unspectacular economic growth

No clear trends in asset markets

Ignis Absolute Return Government Bond Fund

To provide

Long/short exposure to only the highest quality and most liquid securities

Developed market government bonds

AAA bonds issued by supranationals(IMF, World Bank, etc)

G10 currency markets

Max 25% of total risk budget in foreign currency (G10 only)

An innovative fund designed:

*Please note this is a target return only and is calculated on a rolling 12 month basis. The cash level is based on the overnight rate (EONIA).**The fund’s target volatility will be a standard deviation level of 4-6%, it will be managed to deliver stable returns regardless of market moves.

November 11

3

Ignis Absolute Return Government Bond Fund

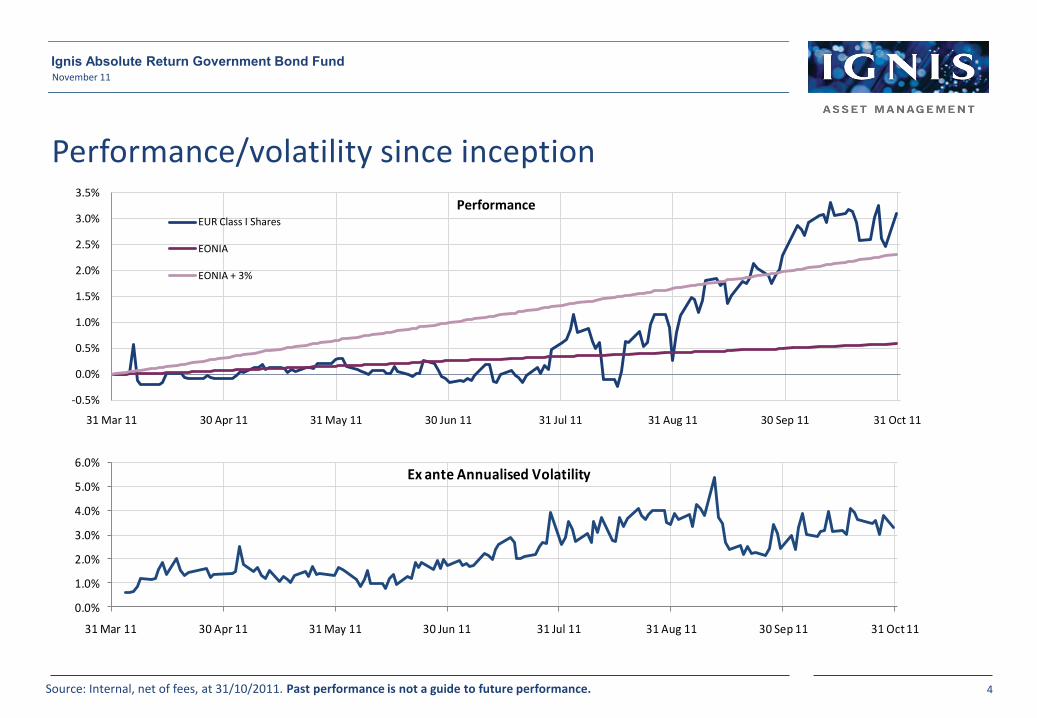

Performance/volatility since inception

Source: Internal, net of fees, at 31/10/2011. Past performance is not a guide to future performance.

November 11

4

Ignis Absolute Return Government Bond Fund

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

31 Mar 11 30 Apr 11 31 May 11 30 Jun 11 31 Jul 11 31 Aug 11 30 Sep 11 31 Oct 11

PerformanceEUR Class I Shares

EONIA

EONIA + 3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

31 Mar 11 30 Apr 11 31 May 11 30 Jun 11 31 Jul 11 31 Aug 11 30 Sep 11 31 Oct 11

Ex ante Annualised Volatility

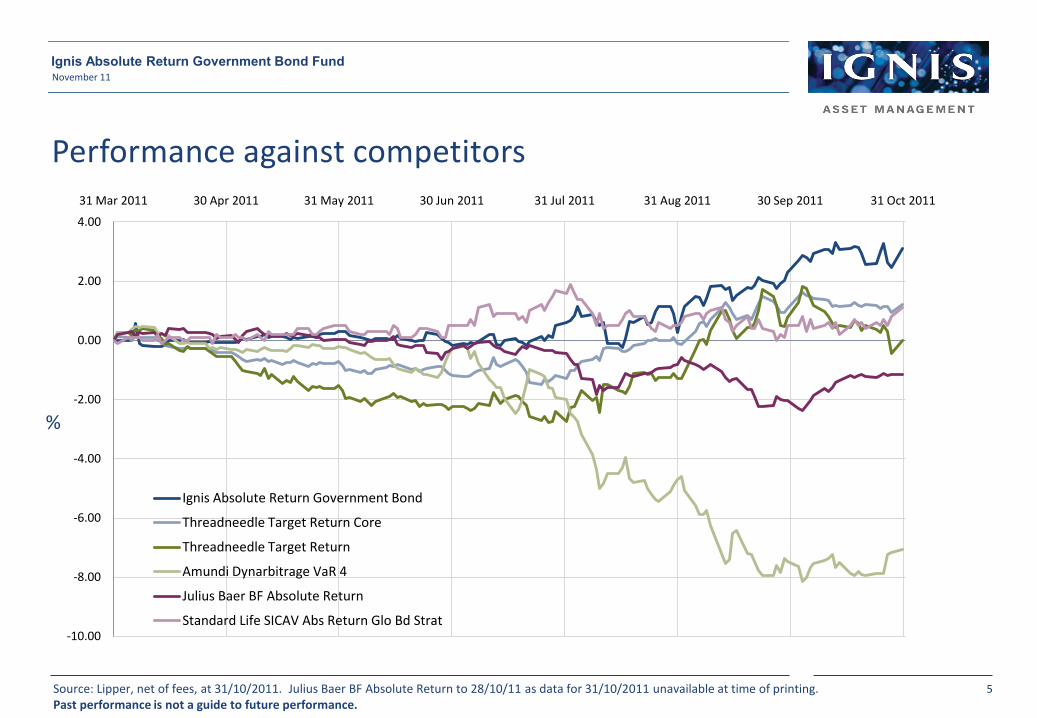

Performance against competitors

Source: Lipper, net of fees, at 31/10/2011. Julius Baer BF Absolute Return to 28/10/11 as data for 31/10/2011 unavailable at time of printing.Past performance is not a guide to future performance.

November 11

5

Ignis Absolute Return Government Bond Fund

%

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

31 Mar 2011 30 Apr 2011 31 May 2011 30 Jun 2011 31 Jul 2011 31 Aug 2011 30 Sep 2011 31 Oct 2011

Ignis Absolute Return Government Bond

Threadneedle Target Return Core

Threadneedle Target Return

Amundi Dynarbitrage VaR 4

Julius Baer BF Absolute Return

Standard Life SICAV Abs Return Glo Bd Strat

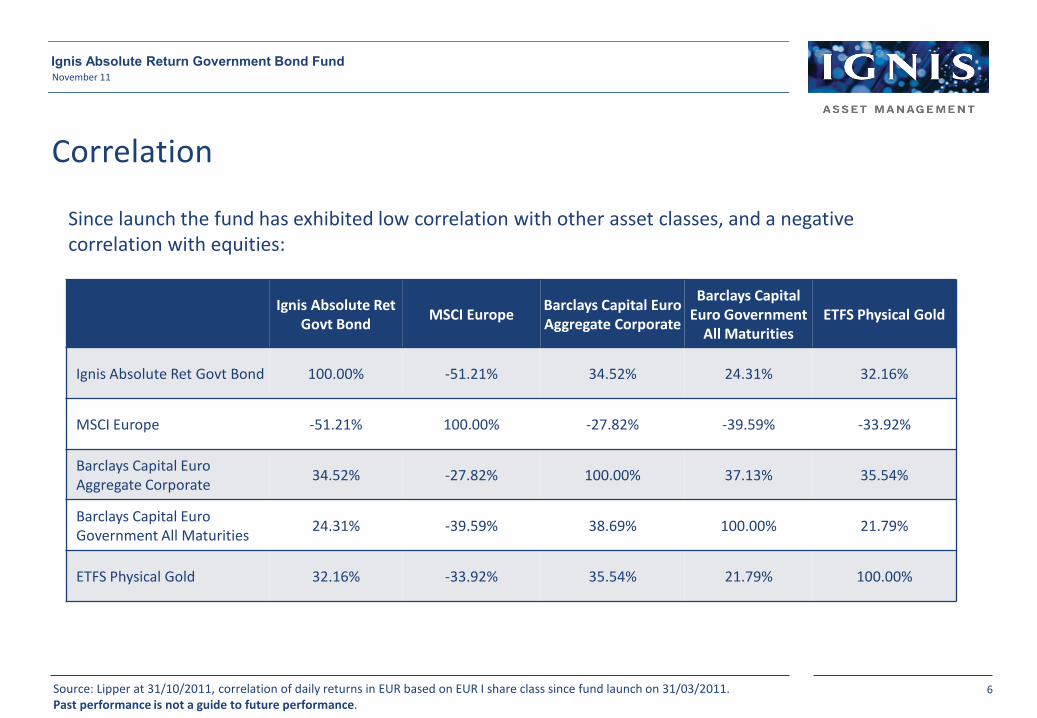

Correlation

Source: Lipper at 31/10/2011, correlation of daily returns in EUR based on EUR I share class since fund launch on 31/03/2011. Past performance is not a guide to future performance.

Since launch the fund has exhibited low correlation with other asset classes, and a negative correlation with equities:

Ignis Absolute Ret Govt Bond

MSCI Europe Barclays Capital Euro Aggregate Corporate

Barclays Capital Euro Government

All Maturities ETFS Physical Gold

Ignis Absolute Ret Govt Bond 100.00% -51.21% 34.52% 24.31% 32.16%

MSCI Europe -51.21% 100.00% -27.82% -39.59% -33.92%

Barclays Capital Euro Aggregate Corporate

34.52% -27.82% 100.00% 37.13% 35.54%

Barclays Capital Euro Government All Maturities

24.31% -39.59% 38.69% 100.00% 21.79%

ETFS Physical Gold 32.16% -33.92% 35.54% 21.79% 100.00%

November 11

6

Ignis Absolute Return Government Bond Fund

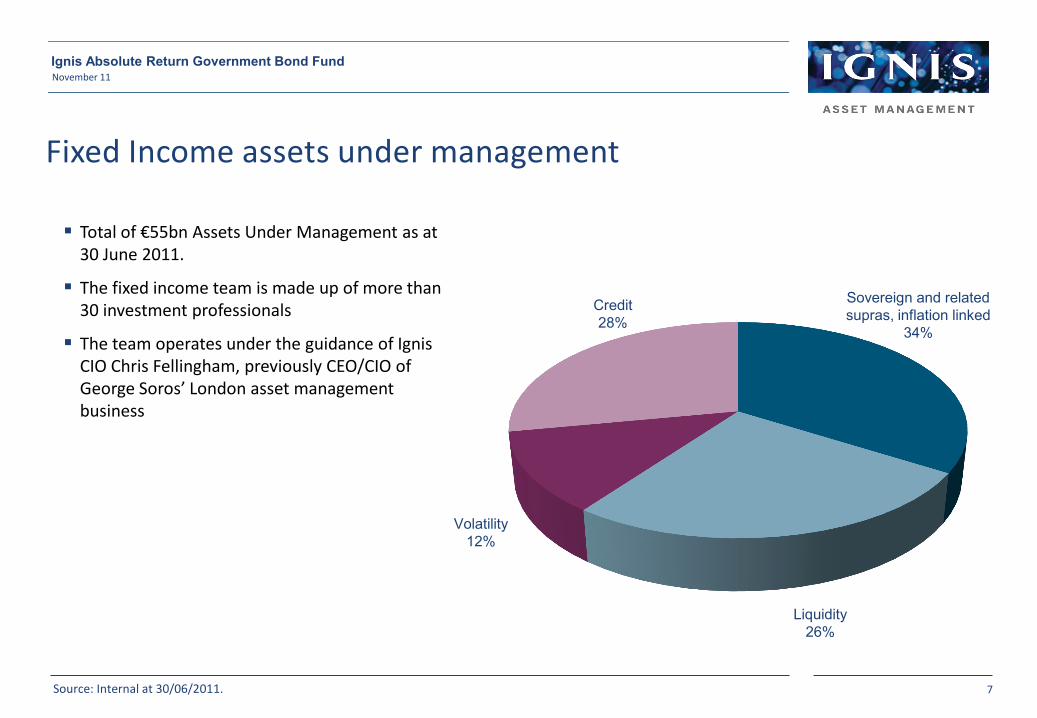

Fixed Income assets under management

Total of €55bn Assets Under Management as at 30 June 2011.

The fixed income team is made up of more than 30 investment professionals

The team operates under the guidance of Ignis CIO Chris Fellingham, previously CEO/CIO of George Soros’ London asset management business

Source: Internal at 30/06/2011.

November 11

7

Ignis Absolute Return Government Bond Fund

Sovereign and related supras, inflation linked

34%

Liquidity 26%

Credit 28%

Volatility 12%

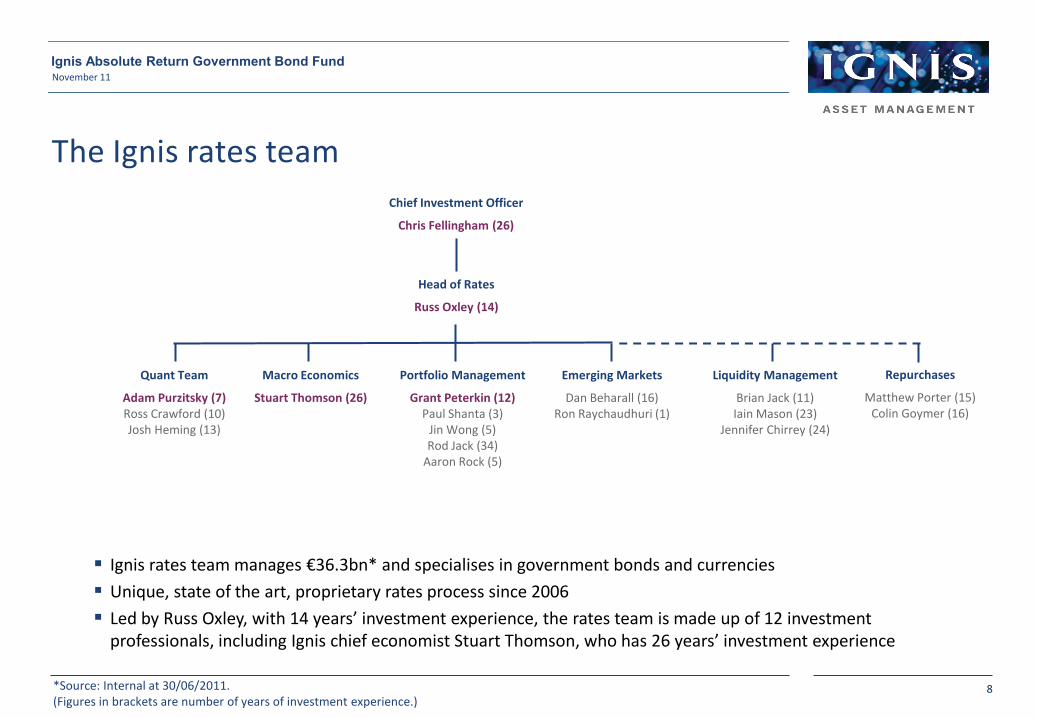

Ignis rates team manages €36.3bn* and specialises in government bonds and currencies

Unique, state of the art, proprietary rates process since 2006

Led by Russ Oxley, with 14 years’ investment experience, the rates team is made up of 12 investment professionals, including Ignis chief economist Stuart Thomson, who has 26 years’ investment experience

The Ignis rates team

Head of Rates

Russ Oxley (14)

Quant Team

Adam Purzitsky (7)Ross Crawford (10)Josh Heming (13)

Macro Economics

Stuart Thomson (26)

Portfolio Management

Grant Peterkin (12)Paul Shanta (3)

Jin Wong (5)Rod Jack (34)

Aaron Rock (5)

Emerging Markets

Dan Beharall (16)Ron Raychaudhuri (1)

Liquidity Management

Brian Jack (11)Iain Mason (23)

Jennifer Chirrey (24)

Repurchases

Matthew Porter (15)Colin Goymer (16)

November 11

8

Ignis Absolute Return Government Bond Fund

*Source: Internal at 30/06/2011. (Figures in brackets are number of years of investment experience.)

Chief Investment Officer

Chris Fellingham (26)

9

November 11Ignis Absolute Return Government Bond Fund

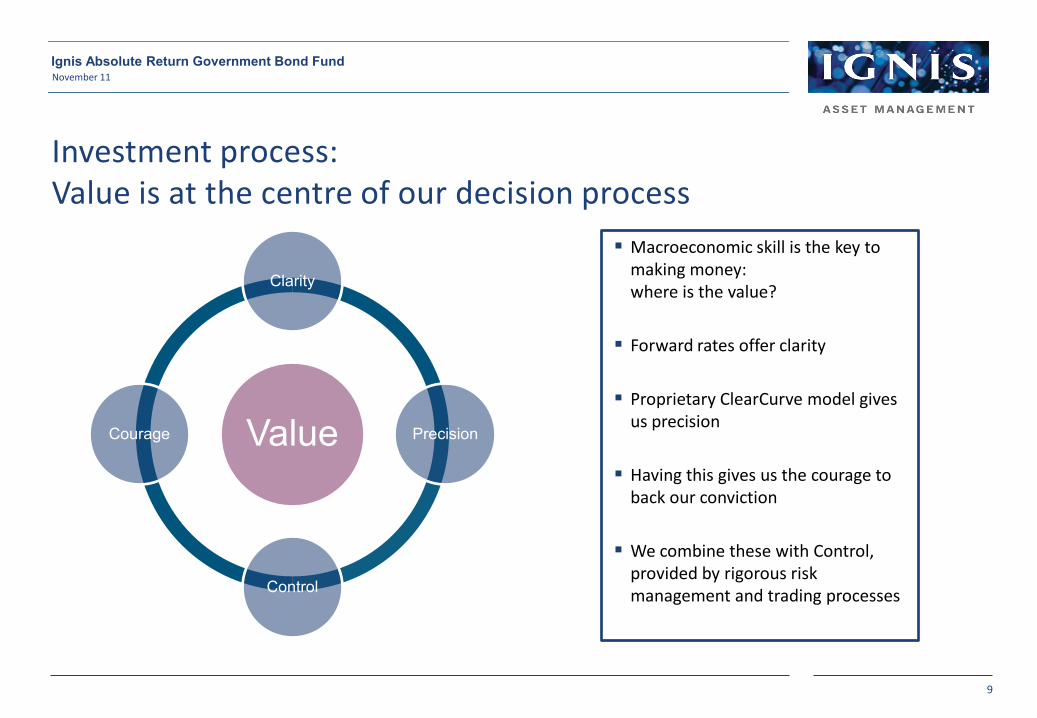

Investment process: Value is at the centre of our decision process

Macroeconomic skill is the key to making money: where is the value?

Forward rates offer clarity

Proprietary ClearCurve model gives us precision

Having this gives us the courage to back our conviction

We combine these with Control, provided by rigorous risk management and trading processes

Value

Clarity

Precision

Control

Courage

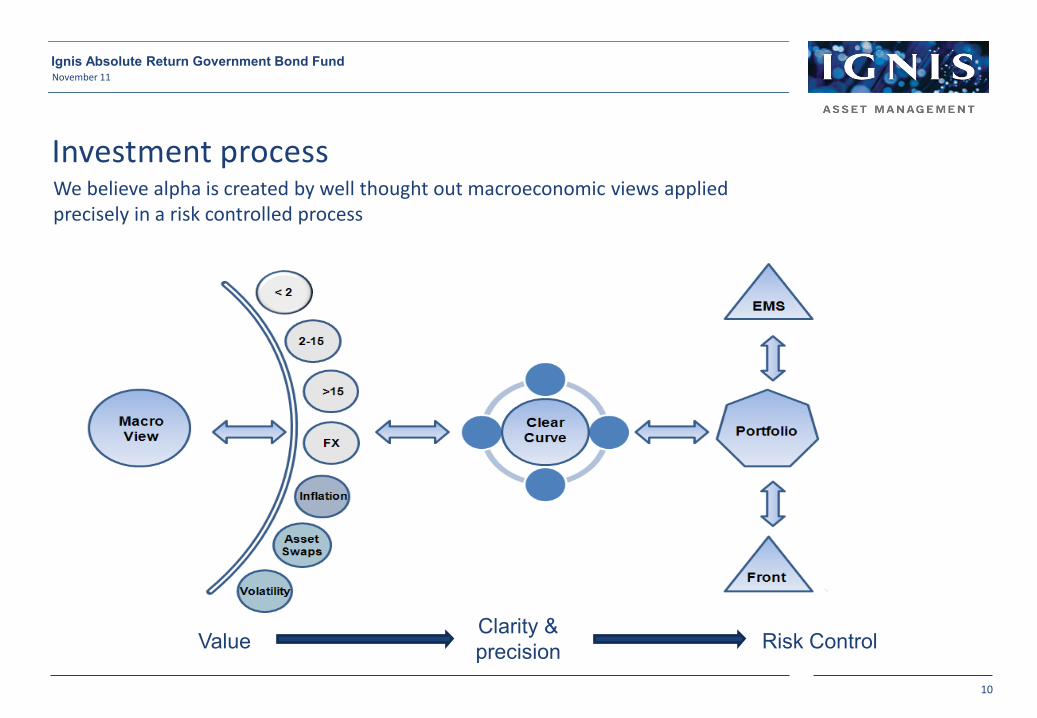

Investment processWe believe alpha is created by well thought out macroeconomic views applied precisely in a risk controlled process

ValueClarity & precision Risk Control

November 11

10

Ignis Absolute Return Government Bond Fund

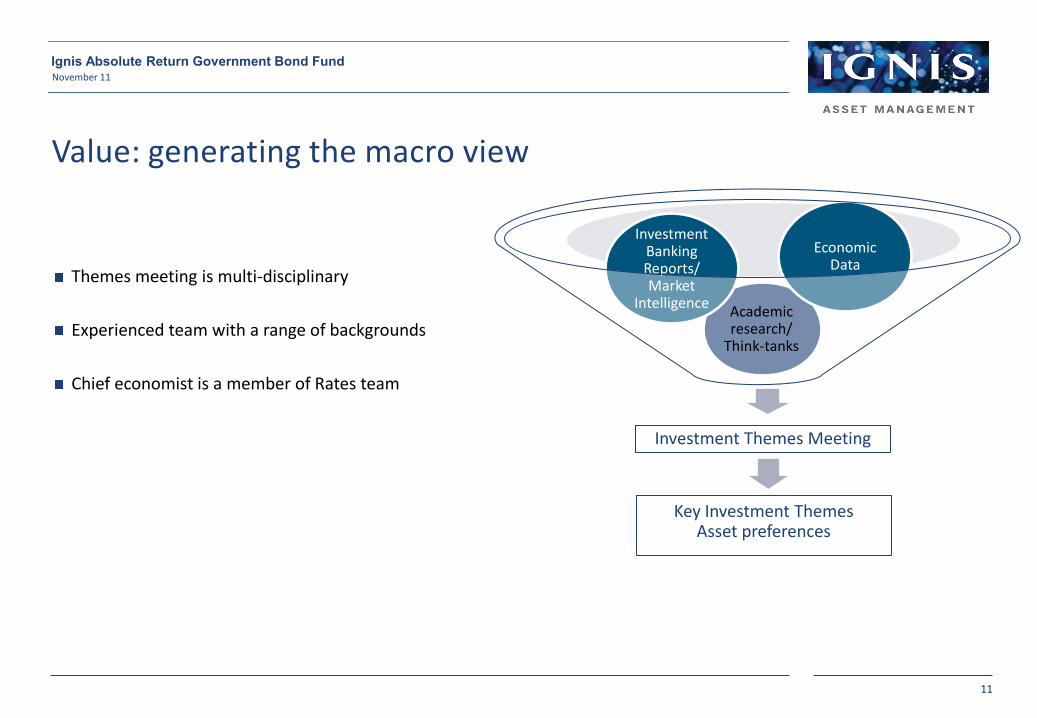

Investment Themes Meeting

Academic research/

Think-tanks

Investment Banking Reports/Market

Intelligence

Economic Data

Themes meeting is multi-disciplinary

Experienced team with a range of backgrounds

Chief economist is a member of Rates team

Value: generating the macro view

Key Investment ThemesAsset preferences

November 11

11

Ignis Absolute Return Government Bond Fund

Academic research/

Think-tanks

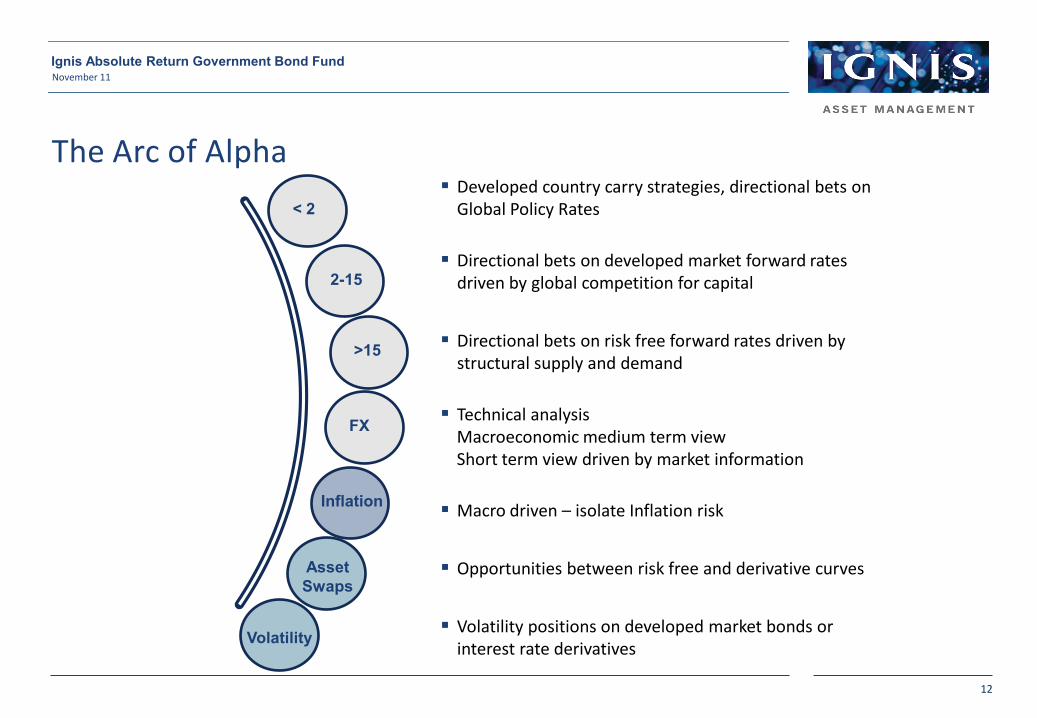

Developed country carry strategies, directional bets on Global Policy Rates

Directional bets on developed market forward rates driven by global competition for capital

Directional bets on risk free forward rates driven by structural supply and demand

Technical analysisMacroeconomic medium term viewShort term view driven by market information

Macro driven – isolate Inflation risk

Opportunities between risk free and derivative curves

Volatility positions on developed market bonds or interest rate derivatives

The Arc of Alpha

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

November 11

12

Ignis Absolute Return Government Bond Fund

0.00

1.00

2.00

3.00

4.00

5.00

Forward rate curveForward - 02/11/2011Forward - 04/01/2011

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

1y0y

1y1y

1y2y

1y3y

1y4y

1y5y

1y6y

1y7y

1y8y

1y9y

1y10

y

1y11

y

1y12

y

1y13

y

1y14

y

1y15

y

1y16

y

1y17

y

1y18

y

1y19

y

1y20

y

1y21

y

1y22

y

1y23

y

1y24

y

1y25

y

1y26

y

1y27

y

1y28

y

1y29

y

%

November 11Ignis Absolute Return Government Bond Fund

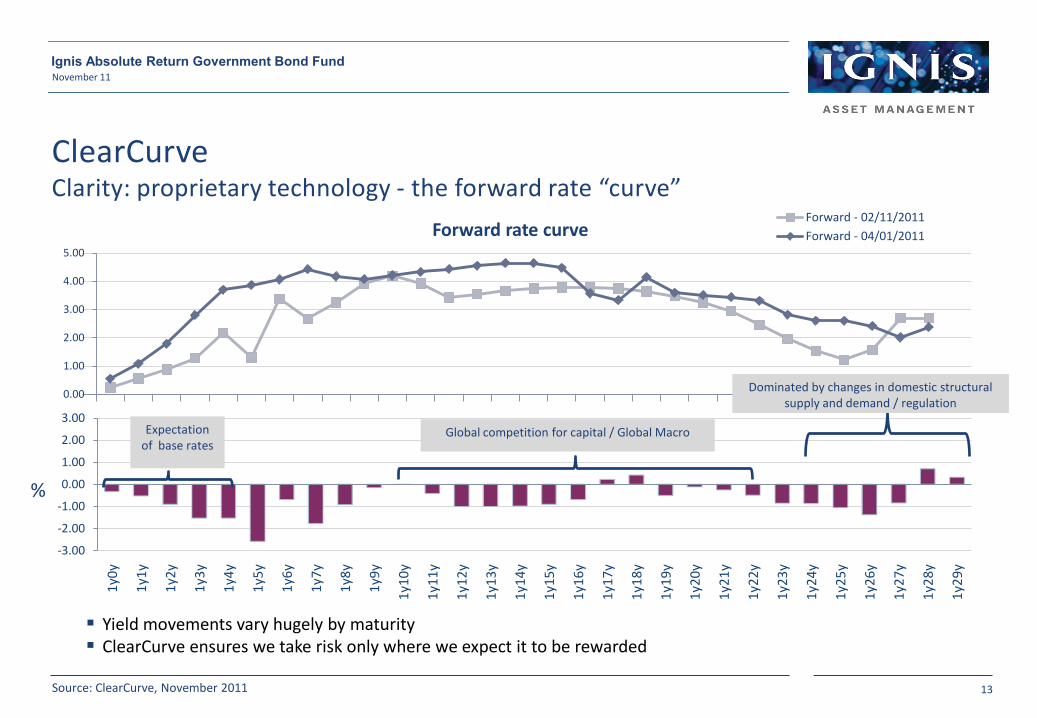

ClearCurveClarity: proprietary technology - the forward rate “curve”

Yield movements vary hugely by maturity ClearCurve ensures we take risk only where we expect it to be rewarded

Dominated by changes in domestic structural supply and demand / regulation

Global competition for capital / Global MacroExpectation of base rates

Source: ClearCurve, November 2011 13

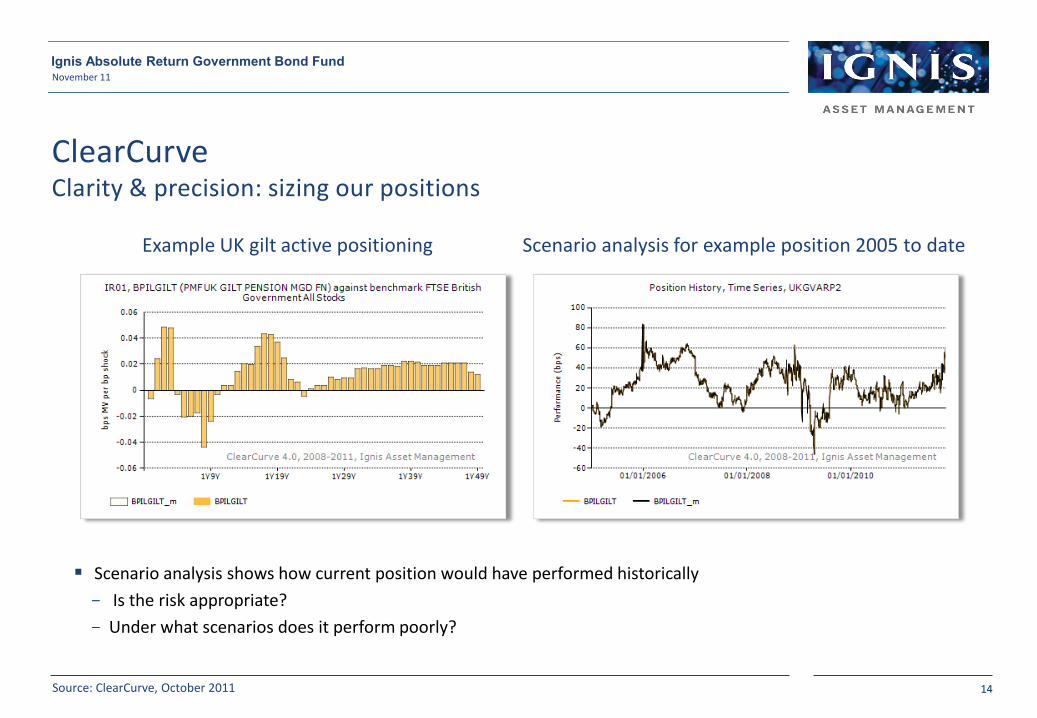

Scenario analysis shows how current position would have performed historically

Is the risk appropriate?

Under what scenarios does it perform poorly?

ClearCurveClarity & precision: sizing our positions

14

Example UK gilt active positioning Scenario analysis for example position 2005 to date

Source: ClearCurve, October 2011

November 11Ignis Absolute Return Government Bond Fund

November 11Ignis Absolute Return Government Bond Fund

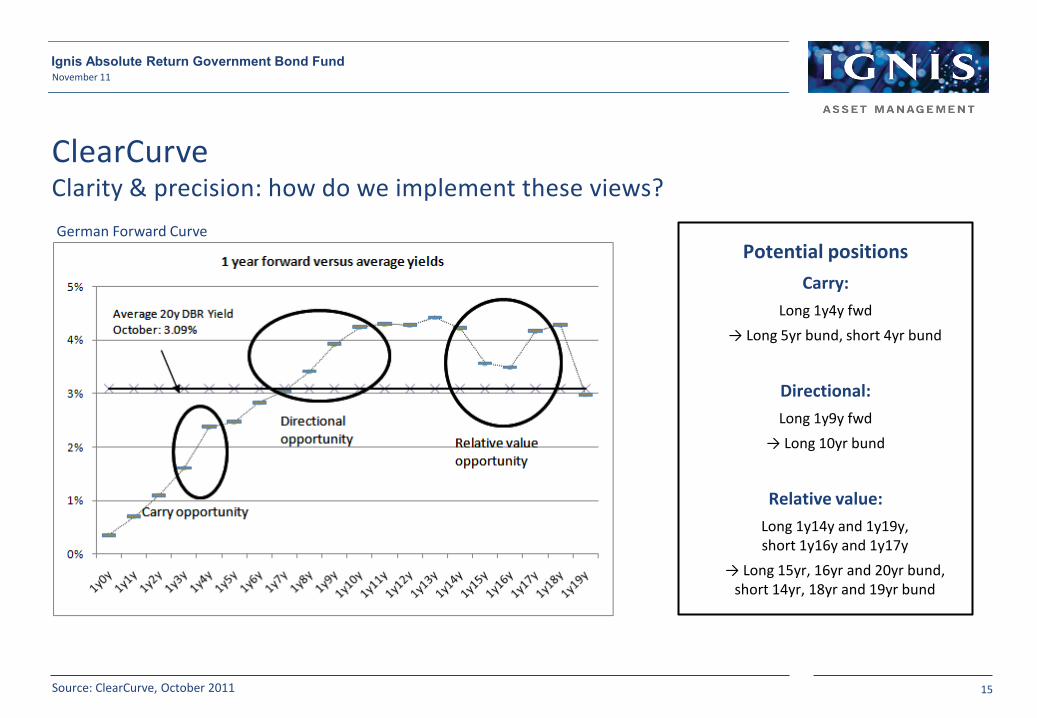

ClearCurveClarity & precision: how do we implement these views?

German Forward CurvePotential positions

Carry:Long 1y4y fwd

→ Long 5yr bund, short 4yr bund

Directional:Long 1y9y fwd

→ Long 10yr bund

Relative value:Long 1y14y and 1y19y,short 1y16y and 1y17y

→ Long 15yr, 16yr and 20yr bund, short 14yr, 18yr and 19yr bund

Source: ClearCurve, October 2011 15

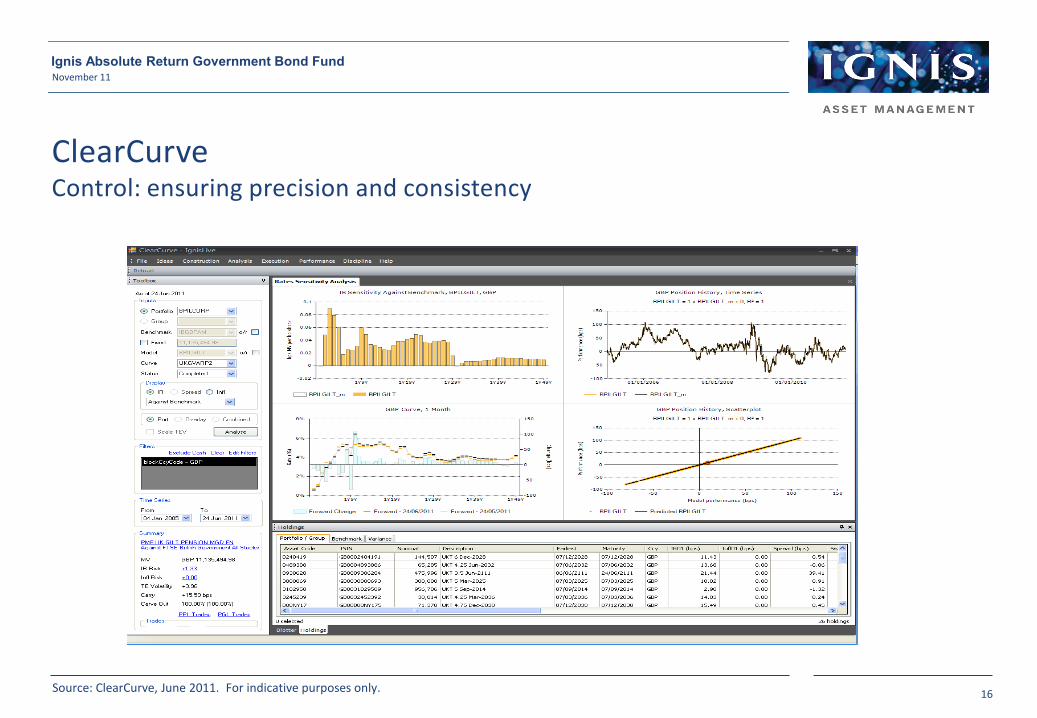

ClearCurveControl: ensuring precision and consistency

November 11

16

Ignis Absolute Return Government Bond Fund

Source: ClearCurve, June 2011. For indicative purposes only.

Calculates forward curves for all instruments

Assists in benchmark construction and portfolio implementation

Monitors portfolio risk

Scales active positions according to risk budget

17

ClearCurveA key proprietary tool

November 11Ignis Absolute Return Government Bond Fund

Source: ClearCurve, June 2011. For indicative purposes only.

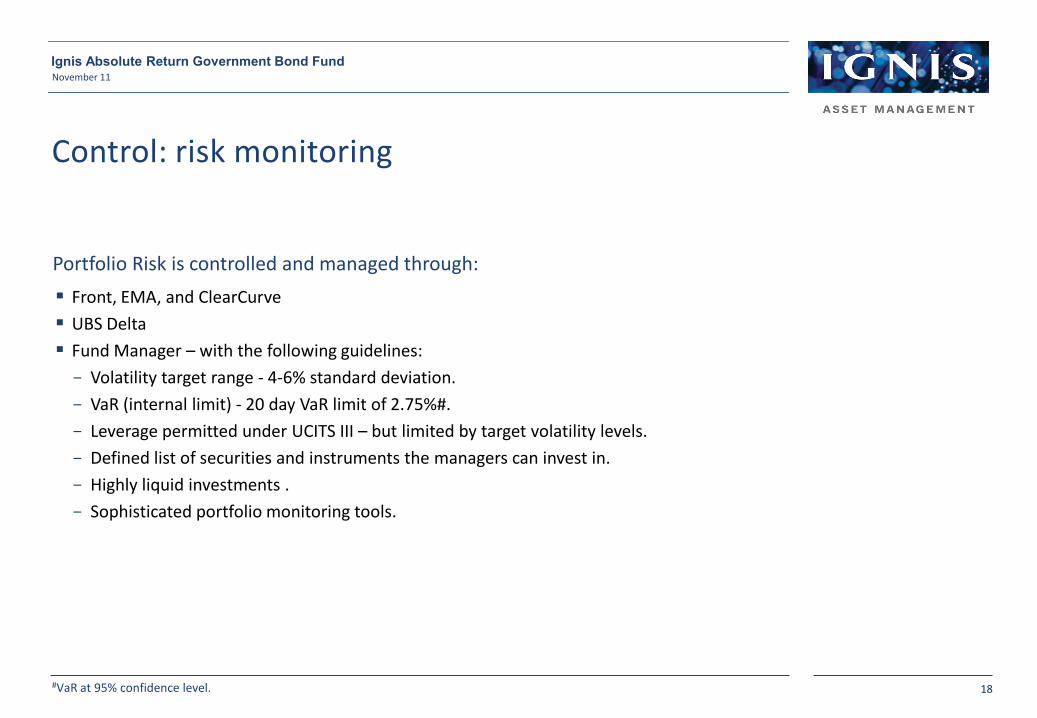

Portfolio Risk is controlled and managed through:

Front, EMA, and ClearCurve

UBS Delta

Fund Manager – with the following guidelines:

Volatility target range - 4-6% standard deviation.

VaR (internal limit) - 20 day VaR limit of 2.75%#.

Leverage permitted under UCITS III – but limited by target volatility levels.

Defined list of securities and instruments the managers can invest in.

Highly liquid investments .

Sophisticated portfolio monitoring tools.

Control: risk monitoring

November 11

18

Ignis Absolute Return Government Bond Fund

#VaR at 95% confidence level.

19

November 11Ignis Absolute Return Government Bond Fund

Ex-ante Tracking Error: diversified strategies have helped in a volatile environment

Source: UBS Delta, data as at 31/10/2011. The fund takes risk by implementing different strategies. If each strategy was well correlated, the total risk of the fund would be a sum of the parts. In fact, the strategies are lowly correlated. This creates a diversification benefit, reducing the fund’s total volatility.

-4

-3

-2

-1

0

1

2

3

4

TOTAL Rates < 2yr Rates 2-15yr Rates 15yr+ FX Global Inflation

Asset Swap Volatility Strategies

Diversification

%

Why a fund like this? Low risk*

Lowly correlated with other asset classes

Designed to deliver performance in volatile/low growth conditions

Alpha not beta

Why Ignis for a fund like this?

Stable, experienced team

Innovative process

Proprietary technology

Performance

Ignis Absolute Return Government Bond Fund

*The fund’s target volatility is a standard deviation level of maximum 6%, it is managed to deliver positive returns regardless of market moves.

November 11

20

Ignis Absolute Return Government Bond Fund

Appendix

Ignis Absolute Return Government Bond FundNovember 11

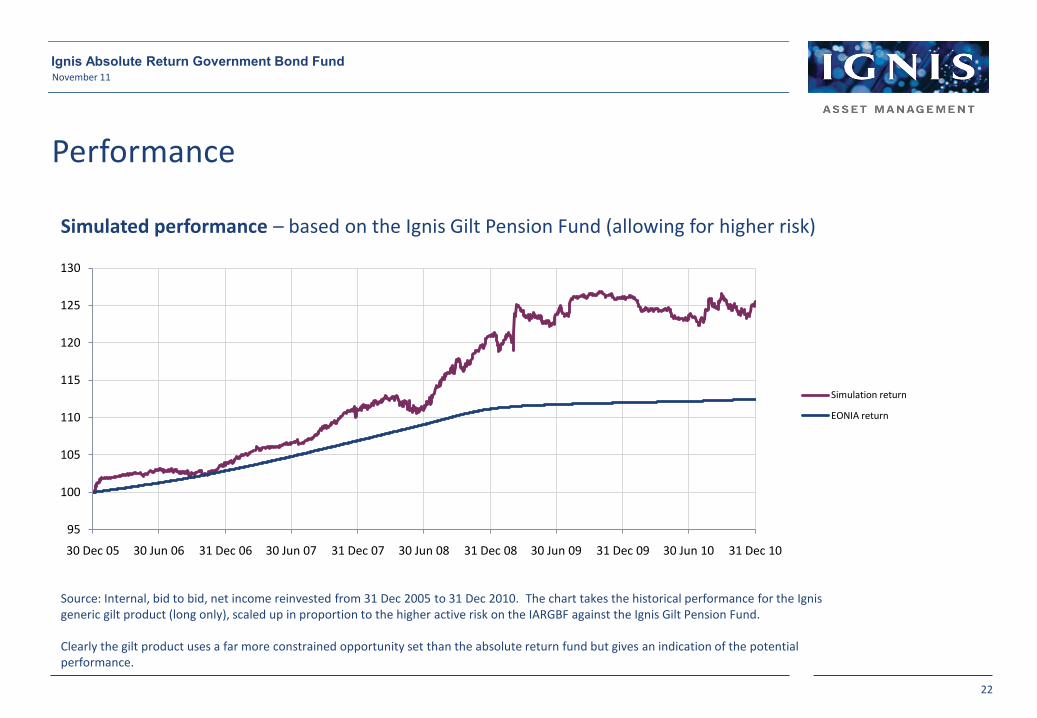

Performance

Source: Internal, bid to bid, net income reinvested from 31 Dec 2005 to 31 Dec 2010. The chart takes the historical performance for the Ignis generic gilt product (long only), scaled up in proportion to the higher active risk on the IARGBF against the Ignis Gilt Pension Fund.

Clearly the gilt product uses a far more constrained opportunity set than the absolute return fund but gives an indication of the potential performance.

Simulated performance – based on the Ignis Gilt Pension Fund (allowing for higher risk)

95

100

105

110

115

120

125

130

30 Dec 05 30 Jun 06 31 Dec 06 30 Jun 07 31 Dec 07 30 Jun 08 31 Dec 08 30 Jun 09 31 Dec 09 30 Jun 10 31 Dec 10

Simulation return

EONIA return

November 11

22

Ignis Absolute Return Government Bond Fund

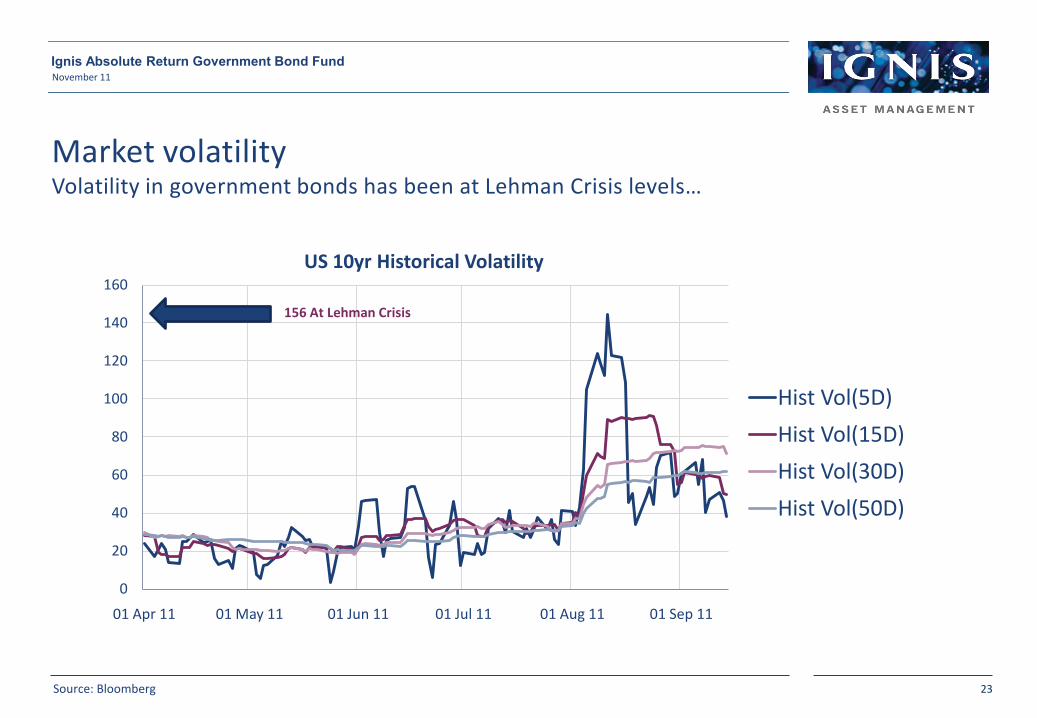

Market volatilityVolatility in government bonds has been at Lehman Crisis levels…

Source: Bloomberg

0

20

40

60

80

100

120

140

160

01 Apr 11 01 May 11 01 Jun 11 01 Jul 11 01 Aug 11 01 Sep 11

US 10yr Historical Volatility

Hist Vol(5D)

Hist Vol(15D)

Hist Vol(30D)

Hist Vol(50D)

156 At Lehman Crisis

November 11

23

Ignis Absolute Return Government Bond Fund

Example trade strategies

Ignis Absolute Return Government Bond FundNovember 11

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

Short European 2y Swap Rate

Following the ECB rate hike at the start of April the 2y swap rate sold off as the markets were less convinced there would be immediate rate hikes to follow.

Our view was that aggressive action from Trichet was not fully priced into the market.

We paid the European 2y Swap rate 2.353% on 21 April. The rate rallied aggressively to 2.48% before the May ECB meeting. We closed this position here capturing the 13bps yield move and 7bps of performance for the fund.

25

EUR – short dated

2.20

2.25

2.30

2.35

2.40

2.45

2.50

05 Apr 11 12 Apr 11 19 Apr 11 26 Apr 11 03 May 11 10 May 11 17 May 11

Opened at 2.353%

Closed close to the Intraday high at 2.48%

Source: Bloomberg, May 2011

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

November 11Ignis Absolute Return Government Bond Fund

%

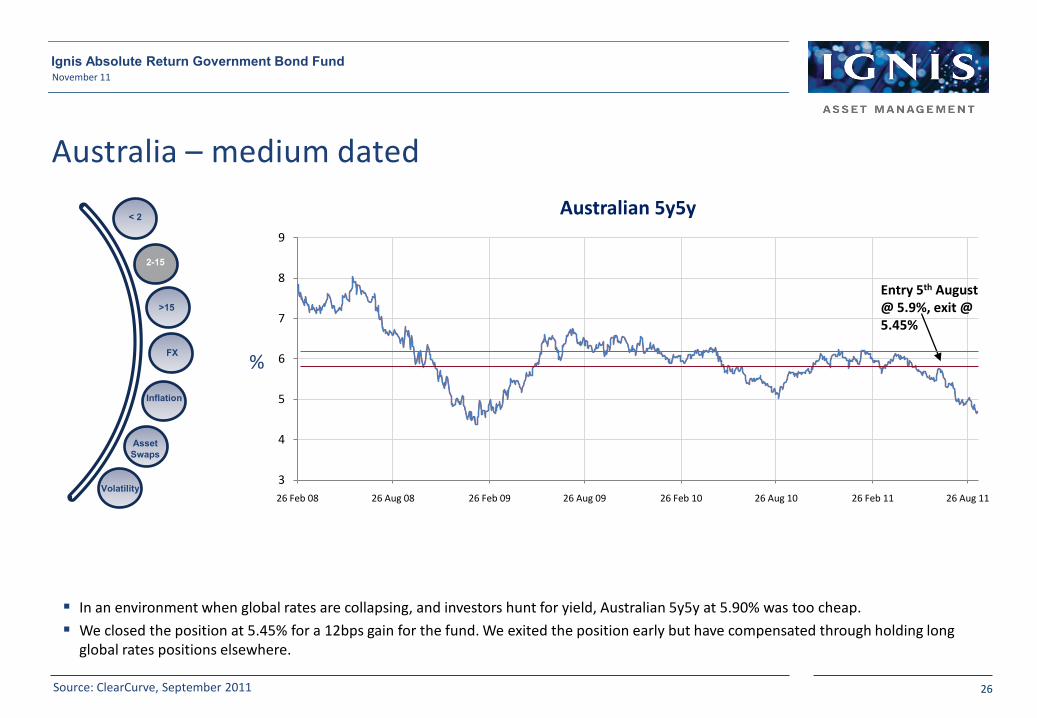

In an environment when global rates are collapsing, and investors hunt for yield, Australian 5y5y at 5.90% was too cheap.

We closed the position at 5.45% for a 12bps gain for the fund. We exited the position early but have compensated through holding long global rates positions elsewhere.

26

Australia – medium dated

Target3

4

5

6

7

8

9

26 Feb 08 26 Aug 08 26 Feb 09 26 Aug 09 26 Feb 10 26 Aug 10 26 Feb 11 26 Aug 11

Australian 5y5y

Entry 5th August @ 5.9%, exit @ 5.45%

%

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

Source: ClearCurve, September 2011

November 11Ignis Absolute Return Government Bond Fund

3.0

3.5

4.0

4.5

5.0

5.5

6.0

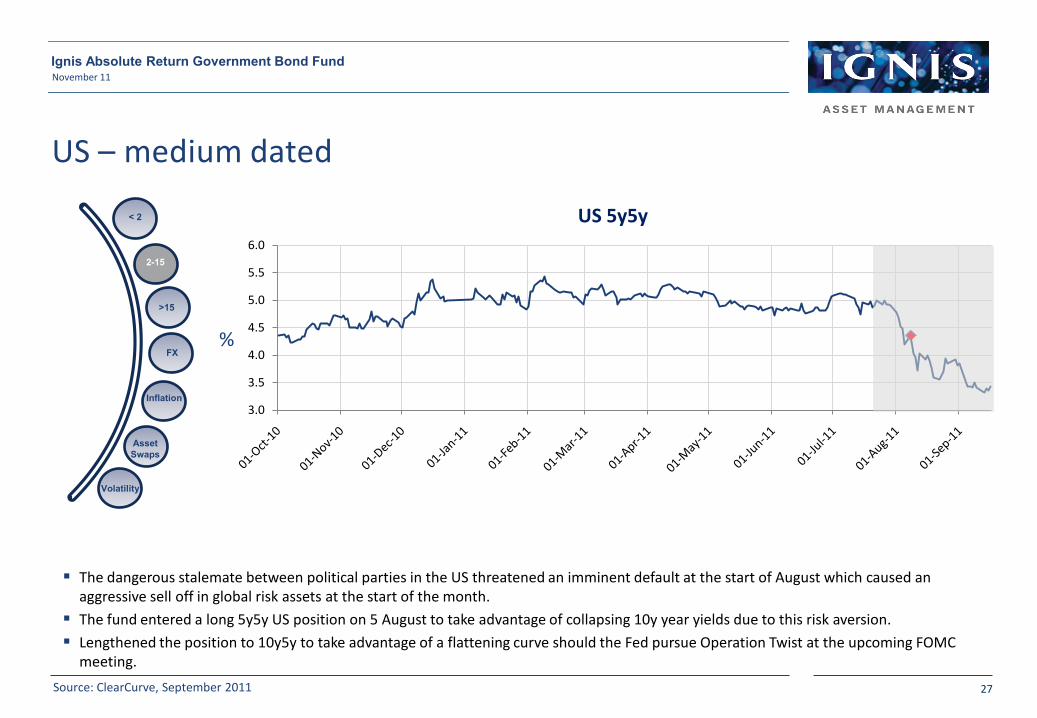

US 5y5y

The dangerous stalemate between political parties in the US threatened an imminent default at the start of August which caused an aggressive sell off in global risk assets at the start of the month.

The fund entered a long 5y5y US position on 5 August to take advantage of collapsing 10y year yields due to this risk aversion.

Lengthened the position to 10y5y to take advantage of a flattening curve should the Fed pursue Operation Twist at the upcoming FOMC meeting.

27

US – medium dated

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

Source: ClearCurve, September 2011

November 11Ignis Absolute Return Government Bond Fund

%

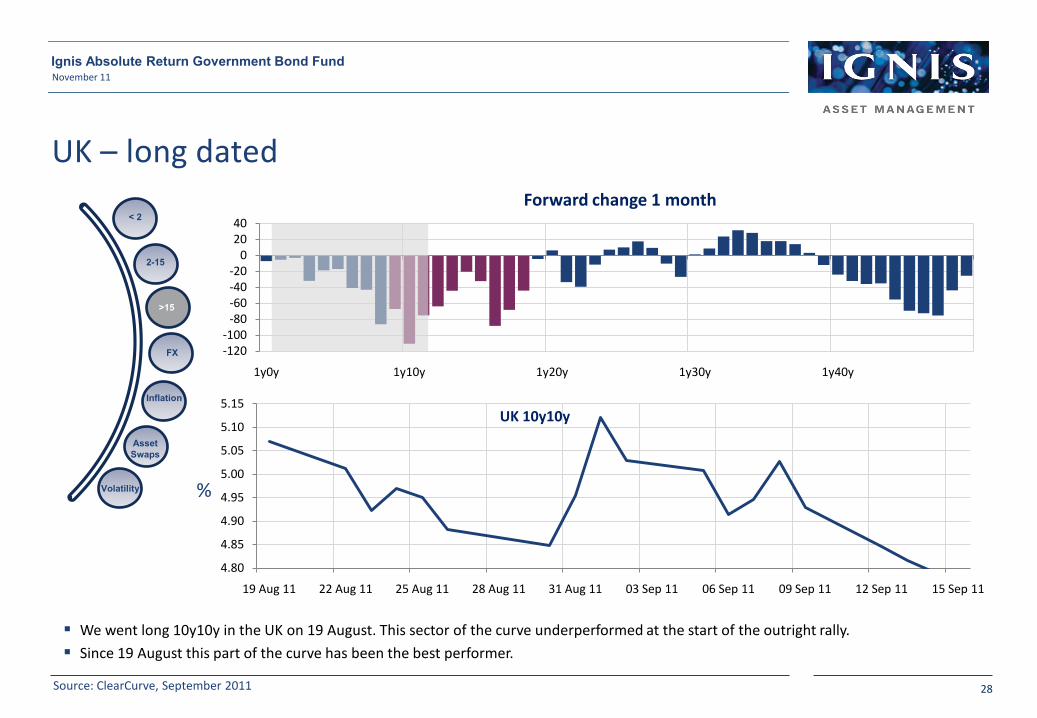

We went long 10y10y in the UK on 19 August. This sector of the curve underperformed at the start of the outright rally.

Since 19 August this part of the curve has been the best performer.

28

UK – long dated

-120-100

-80-60-40-20

02040

1y0y 1y10y 1y20y 1y30y 1y40y

Forward change 1 month

4.80

4.85

4.90

4.95

5.00

5.05

5.10

5.15

19 Aug 11 22 Aug 11 25 Aug 11 28 Aug 11 31 Aug 11 03 Sep 11 06 Sep 11 09 Sep 11 12 Sep 11 15 Sep 11

UK 10y10y

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

Source: ClearCurve, September 2011

November 11Ignis Absolute Return Government Bond Fund

%

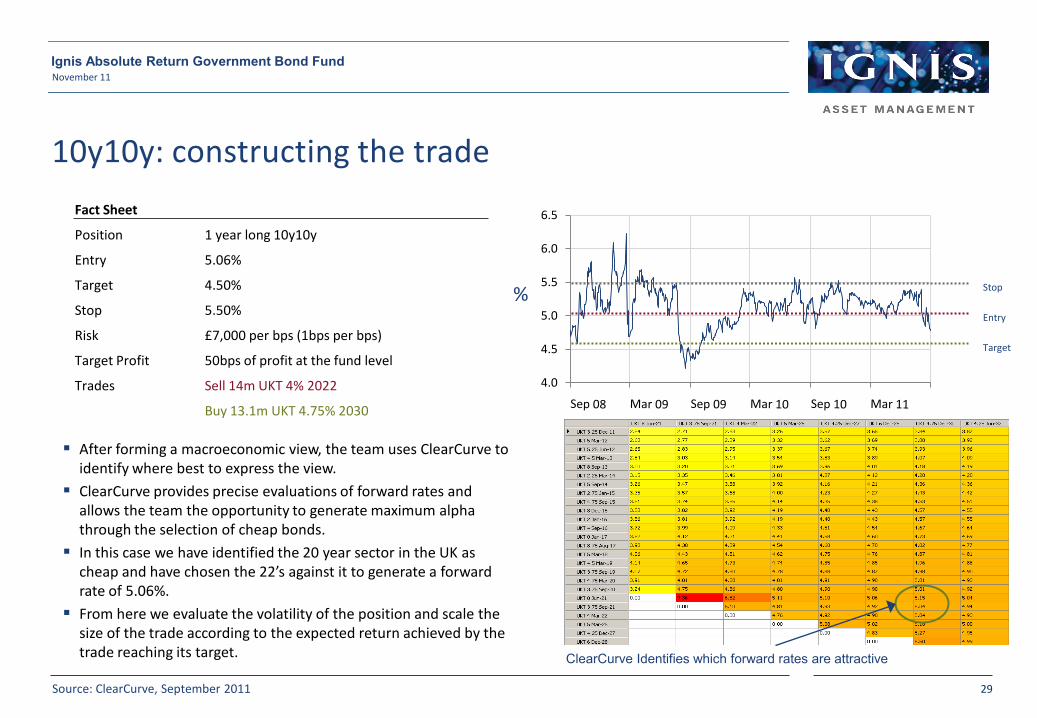

After forming a macroeconomic view, the team uses ClearCurve to identify where best to express the view.

ClearCurve provides precise evaluations of forward rates and allows the team the opportunity to generate maximum alpha through the selection of cheap bonds.

In this case we have identified the 20 year sector in the UK as cheap and have chosen the 22’s against it to generate a forward rate of 5.06%.

From here we evaluate the volatility of the position and scale the size of the trade according to the expected return achieved by the trade reaching its target.

10y10y: constructing the trade

29

ClearCurve Identifies which forward rates are attractive

Fact Sheet

Position 1 year long 10y10y

Entry 5.06%

Target 4.50%

Stop 5.50%

Risk £7,000 per bps (1bps per bps)

Target Profit 50bps of profit at the fund level

Trades Sell 14m UKT 4% 2022

Buy 13.1m UKT 4.75% 2030

4.0

4.5

5.0

5.5

6.0

6.5

Entry

Target

Stop

Source: ClearCurve, September 2011

November 11Ignis Absolute Return Government Bond Fund

%

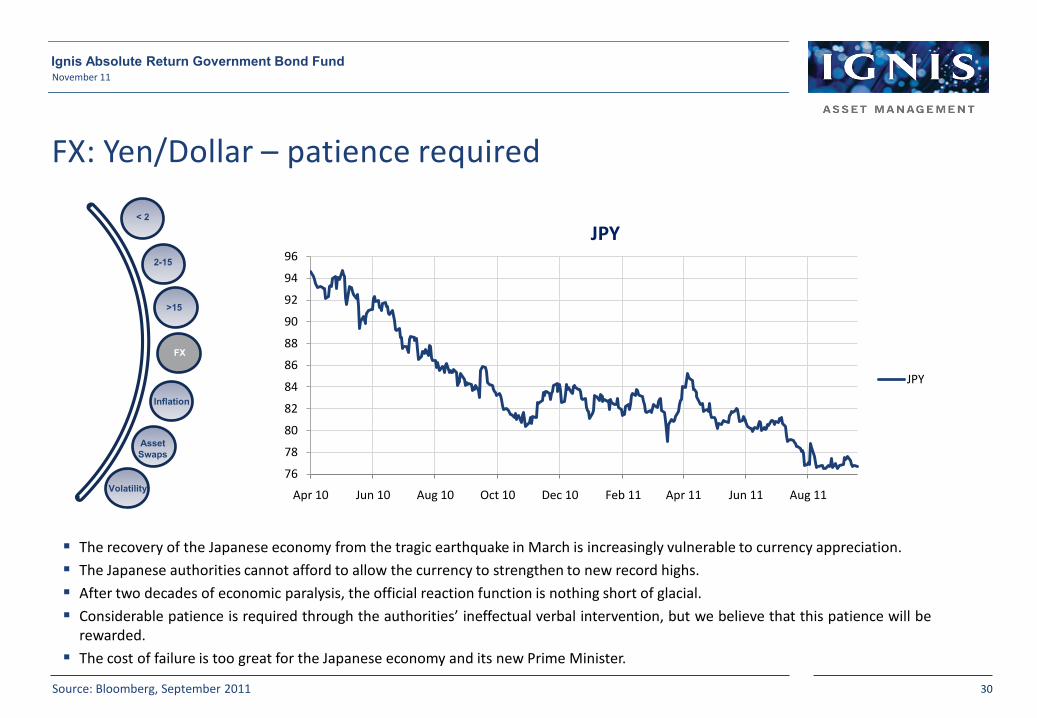

The recovery of the Japanese economy from the tragic earthquake in March is increasingly vulnerable to currency appreciation.

The Japanese authorities cannot afford to allow the currency to strengthen to new record highs.

After two decades of economic paralysis, the official reaction function is nothing short of glacial.

Considerable patience is required through the authorities’ ineffectual verbal intervention, but we believe that this patience will berewarded.

The cost of failure is too great for the Japanese economy and its new Prime Minister.

FX: Yen/Dollar – patience required

76

78

80

82

84

86

88

90

92

94

96

Apr 10 Jun 10 Aug 10 Oct 10 Dec 10 Feb 11 Apr 11 Jun 11 Aug 11

JPY

JPY

< 2

2-15

>15

FX

Inflation

AssetSwaps

Volatility

Source: Bloomberg, September 2011

November 11

30

Ignis Absolute Return Government Bond Fund

Uses the unique Ignis forward rates process:

- Process moves beyond the traditional approach based on duration and sensitivity

- Combination of numerous lower risk uncorrelated trades rather than one directional call = higher alpha potential from the same or lower risk

- Flexible implementation of investment views targeting specific parts of the yield curve (through analysis of forward rates)

- Efficient portfolio construction - ClearCurve proprietary model allows the team to implement, on a risk adjusted basis, its investment views

Generates alpha from fundamental views and the analysis of various forward government bond rate curves

Only invests in a market if the team have a strong fundamental view and an efficient way of taking advantage of that opportunity

Benefits of the forward rates process: Why is this fund different?

November 11

31

Ignis Absolute Return Government Bond Fund

Bond Futures

Interest Rate Swaps

OTC Options (on rates and currencies)

Swaptions

Currency Forwards

Inflation Swaps and Options

Examples of derivatives used to implement alpha strategies:

November 11

32

Ignis Absolute Return Government Bond Fund

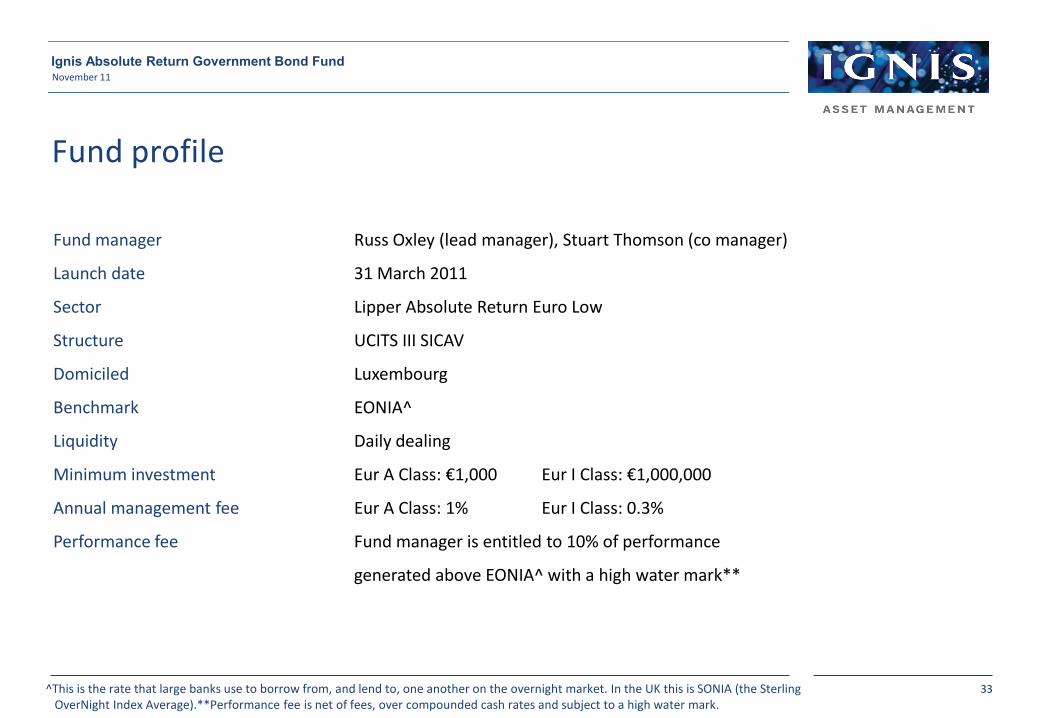

^This is the rate that large banks use to borrow from, and lend to, one another on the overnight market. In the UK this is SONIA (the Sterling OverNight Index Average).**Performance fee is net of fees, over compounded cash rates and subject to a high water mark.

Fund manager Russ Oxley (lead manager), Stuart Thomson (co manager)

Launch date 31 March 2011

Sector Lipper Absolute Return Euro Low

Structure UCITS III SICAV

Domiciled Luxembourg

Benchmark EONIA^

Liquidity Daily dealing

Minimum investment Eur A Class: €1,000 Eur I Class: €1,000,000

Annual management fee Eur A Class: 1% Eur I Class: 0.3%

Performance fee Fund manager is entitled to 10% of performance

generated above EONIA^ with a high water mark**

Fund profile

November 11

33

Ignis Absolute Return Government Bond Fund

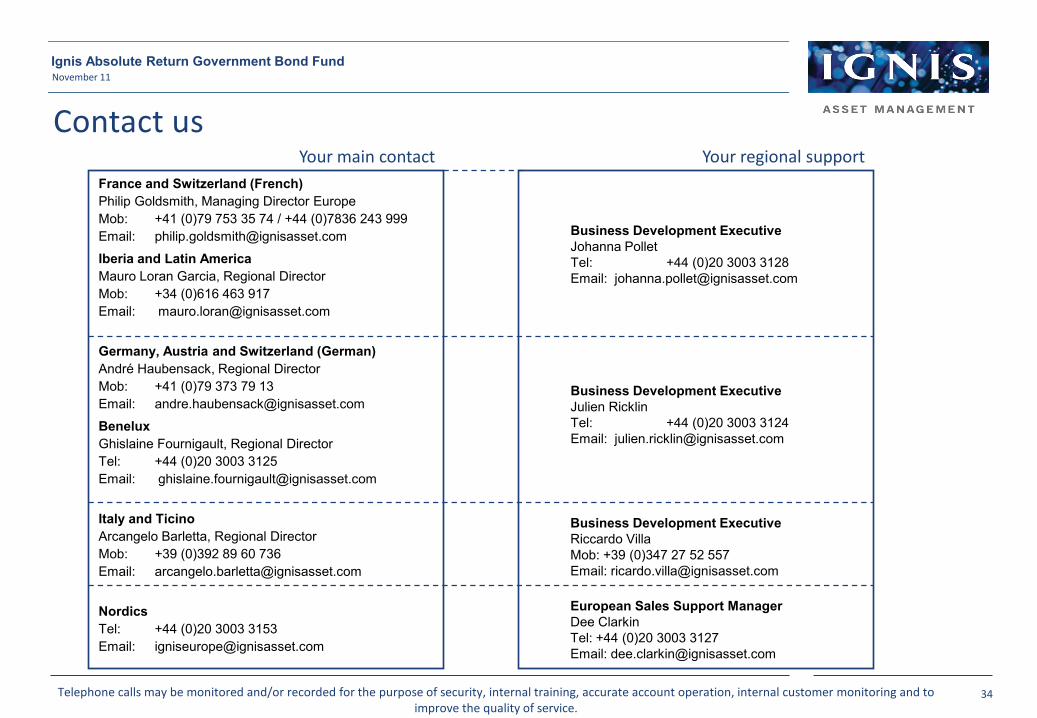

Contact us

France and Switzerland (French)Philip Goldsmith, Managing Director EuropeMob: +41 (0)79 753 35 74 / +44 (0)7836 243 999Email: [email protected]

Iberia and Latin AmericaMauro Loran Garcia, Regional DirectorMob: +34 (0)616 463 917Email: [email protected]

Germany, Austria and Switzerland (German)André Haubensack, Regional DirectorMob: +41 (0)79 373 79 13Email: [email protected]

BeneluxGhislaine Fournigault, Regional DirectorTel: +44 (0)20 3003 3125Email: [email protected]

Italy and TicinoArcangelo Barletta, Regional DirectorMob: +39 (0)392 89 60 736Email: [email protected]

NordicsTel: +44 (0)20 3003 3153Email: [email protected]

Telephone calls may be monitored and/or recorded for the purpose of security, internal training, accurate account operation, internal customer monitoring and to improve the quality of service.

Your main contact Your regional support

European Sales Support ManagerDee ClarkinTel: +44 (0)20 3003 3127Email: [email protected]

Business Development ExecutiveRiccardo VillaMob: +39 (0)347 27 52 557Email: [email protected]

Business Development ExecutiveJulien RicklinTel: +44 (0)20 3003 3124Email: [email protected]

Business Development ExecutiveJohanna PolletTel: +44 (0)20 3003 3128 Email: [email protected]

November 11

34

Ignis Absolute Return Government Bond Fund

35

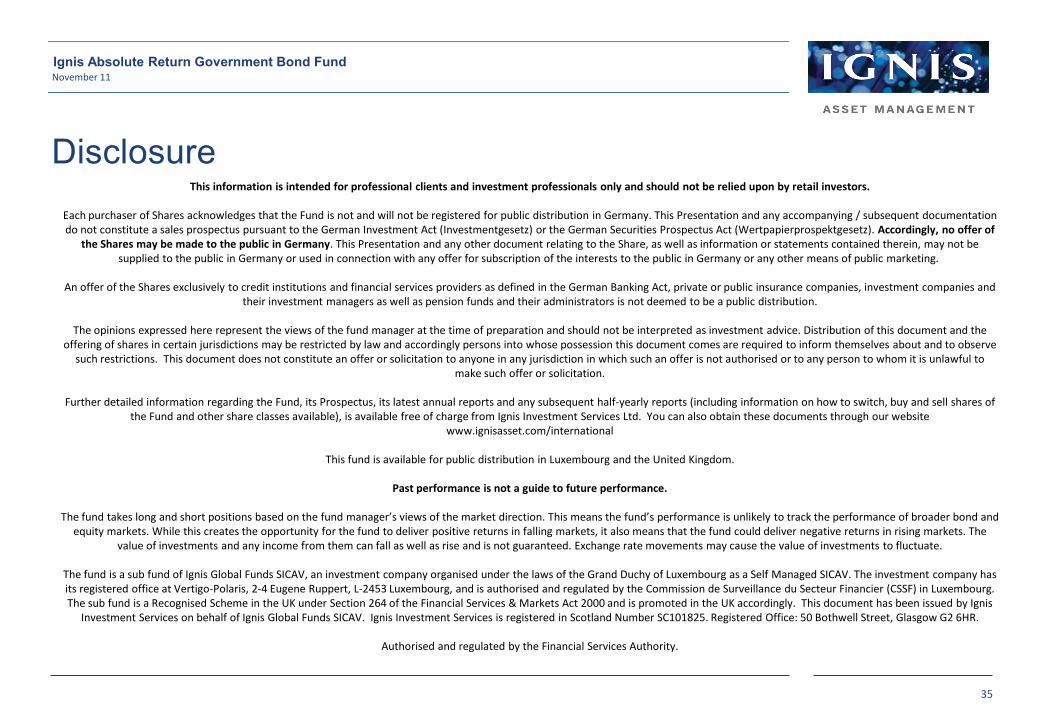

DisclosureThis information is intended for professional clients and investment professionals only and should not be relied upon by retail investors.

Each purchaser of Shares acknowledges that the Fund is not and will not be registered for public distribution in Germany. This Presentation and any accompanying / subsequent documentation do not constitute a sales prospectus pursuant to the German Investment Act (Investmentgesetz) or the German Securities Prospectus Act (Wertpapierprospektgesetz). Accordingly, no offer of

the Shares may be made to the public in Germany. This Presentation and any other document relating to the Share, as well as information or statements contained therein, may not be supplied to the public in Germany or used in connection with any offer for subscription of the interests to the public in Germany or any other means of public marketing.

An offer of the Shares exclusively to credit institutions and financial services providers as defined in the German Banking Act, private or public insurance companies, investment companies and their investment managers as well as pension funds and their administrators is not deemed to be a public distribution.

The opinions expressed here represent the views of the fund manager at the time of preparation and should not be interpreted as investment advice. Distribution of this document and the offering of shares in certain jurisdictions may be restricted by law and accordingly persons into whose possession this document comes are required to inform themselves about and to observe

such restrictions. This document does not constitute an offer or solicitation to anyone in any jurisdiction in which such an offer is not authorised or to any person to whom it is unlawful to make such offer or solicitation.

Further detailed information regarding the Fund, its Prospectus, its latest annual reports and any subsequent half-yearly reports (including information on how to switch, buy and sell shares of the Fund and other share classes available), is available free of charge from Ignis Investment Services Ltd. You can also obtain these documents through our website

www.ignisasset.com/international

This fund is available for public distribution in Luxembourg and the United Kingdom.

Past performance is not a guide to future performance.

The fund takes long and short positions based on the fund manager’s views of the market direction. This means the fund’s performance is unlikely to track the performance of broader bond and equity markets. While this creates the opportunity for the fund to deliver positive returns in falling markets, it also means that the fund could deliver negative returns in rising markets. The

value of investments and any income from them can fall as well as rise and is not guaranteed. Exchange rate movements may cause the value of investments to fluctuate.

The fund is a sub fund of Ignis Global Funds SICAV, an investment company organised under the laws of the Grand Duchy of Luxembourg as a Self Managed SICAV. The investment company has its registered office at Vertigo-Polaris, 2-4 Eugene Ruppert, L-2453 Luxembourg, and is authorised and regulated by the Commission de Surveillance du Secteur Financier (CSSF) in Luxembourg. The sub fund is a Recognised Scheme in the UK under Section 264 of the Financial Services & Markets Act 2000 and is promoted in the UK accordingly. This document has been issued by Ignis

Investment Services on behalf of Ignis Global Funds SICAV. Ignis Investment Services is registered in Scotland Number SC101825. Registered Office: 50 Bothwell Street, Glasgow G2 6HR.

Authorised and regulated by the Financial Services Authority.

November 11Ignis Absolute Return Government Bond Fund