ifrs institute webcast on consolidation 052913 institute webcast … · 5/29/2013 1 ifrs institute...

TRANSCRIPT

5/29/2013

1

IFRS Institute Webcast

New IFRS Requirements for Consolidation

May 29, 2013

Administrative

CPE regulations require online participants take part in online questions. Participants are required to respond to a minimum of four questions in order to be eligible for CPE credit.

Results will be reviewed in aggregate and may be published as a “pulse survey” of the marketplace in the aggregate. Please note that no responses will be tracked back to any individual or organization.

Send questions via the “Ask a Question” button.

Help Desk: 1-877-398-1471 or outside the United States at 1-954-969-3342

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

11

5/29/2013

2

Today’s presenters

Paul MunterU.S. IFRS Professional Practice Leader KPMG LLP New York

Mike HallAdvisory Partner KPMG LLP New York

John Nabial

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

2

John NabialVice President – Financial Reporting Sumitomo Corporation., U.S.

Learning objectives

By completing this module, you should beable to:

1) Understand the overall impact of the “new suite” of consolidation standards under IFRS

2) Explain the key principles including an understanding of selected application examples when applying the consolidation model under IFRS 10

3) Understand the transition provisions under IFRS 10

4) Understand key differences between U.S. GAAP and IFRS regarding consolidation.

5/29/2013

3

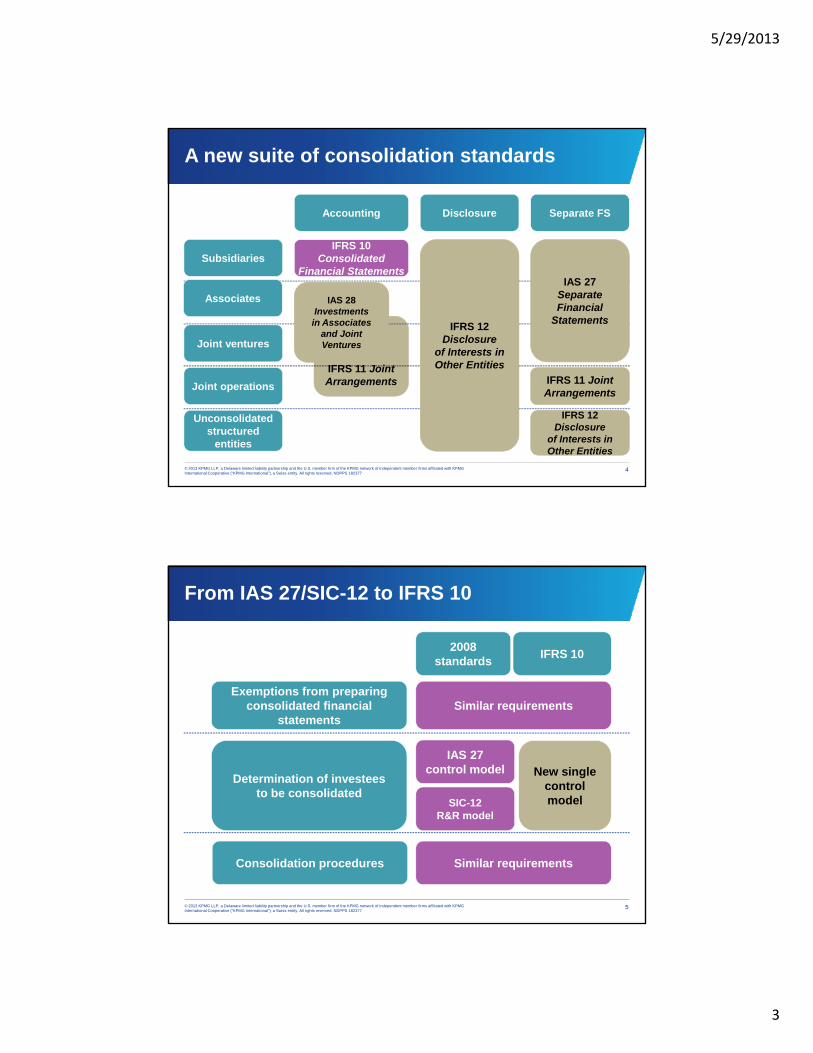

A new suite of consolidation standards

Accounting

IFRS 10

Disclosure Separate FS

IFRS 11 Joint

Associates

Joint ventures

SubsidiariesIFRS 10

Consolidated Financial Statements

IAS 28 Investments

in Associates and Joint Ventures

IFRS 12 Disclosure

of Interests in Other Entities

IAS 27 Separate Financial

Statements

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

4

IFRS 11 Joint ArrangementsJoint operations

Unconsolidated structured

entities

Other Entities

IFRS 11 Joint Arrangements

IFRS 12 Disclosure

of Interests in Other Entities

From IAS 27/SIC-12 to IFRS 10

2008 standards

IFRS 10

Exemptions from preparing consolidated financial

statementsSimilar requirements

Determination of investees to be consolidated

IAS 27 control model New single

control modelSIC-12

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

5

Consolidation procedures Similar requirements

SIC 12 R&R model

5/29/2013

4

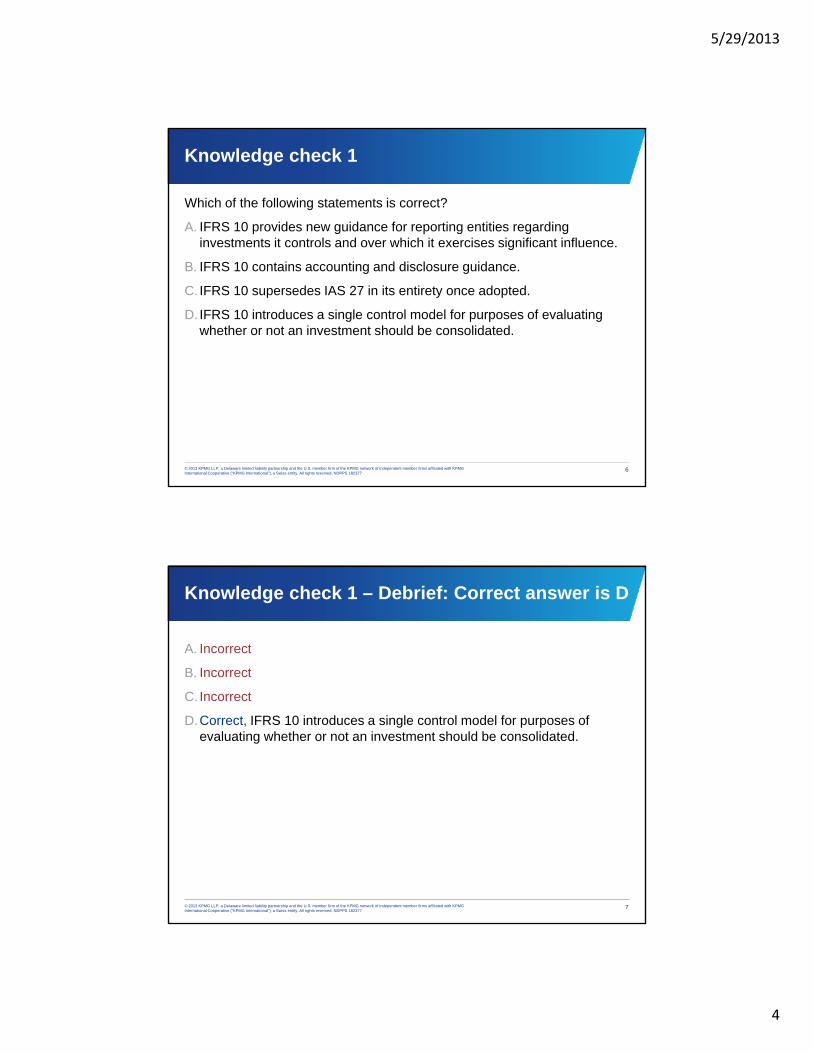

Knowledge check 1

Which of the following statements is correct?

A. IFRS 10 provides new guidance for reporting entities regarding investments it controls and over which it exercises significant influence.g

B. IFRS 10 contains accounting and disclosure guidance.

C. IFRS 10 supersedes IAS 27 in its entirety once adopted.

D. IFRS 10 introduces a single control model for purposes of evaluating whether or not an investment should be consolidated.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

6

Knowledge check 1 – Debrief: Correct answer is D

A. Incorrect

B. Incorrect

C. Incorrect

D.Correct, IFRS 10 introduces a single control model for purposes of evaluating whether or not an investment should be consolidated.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

7

5/29/2013

5

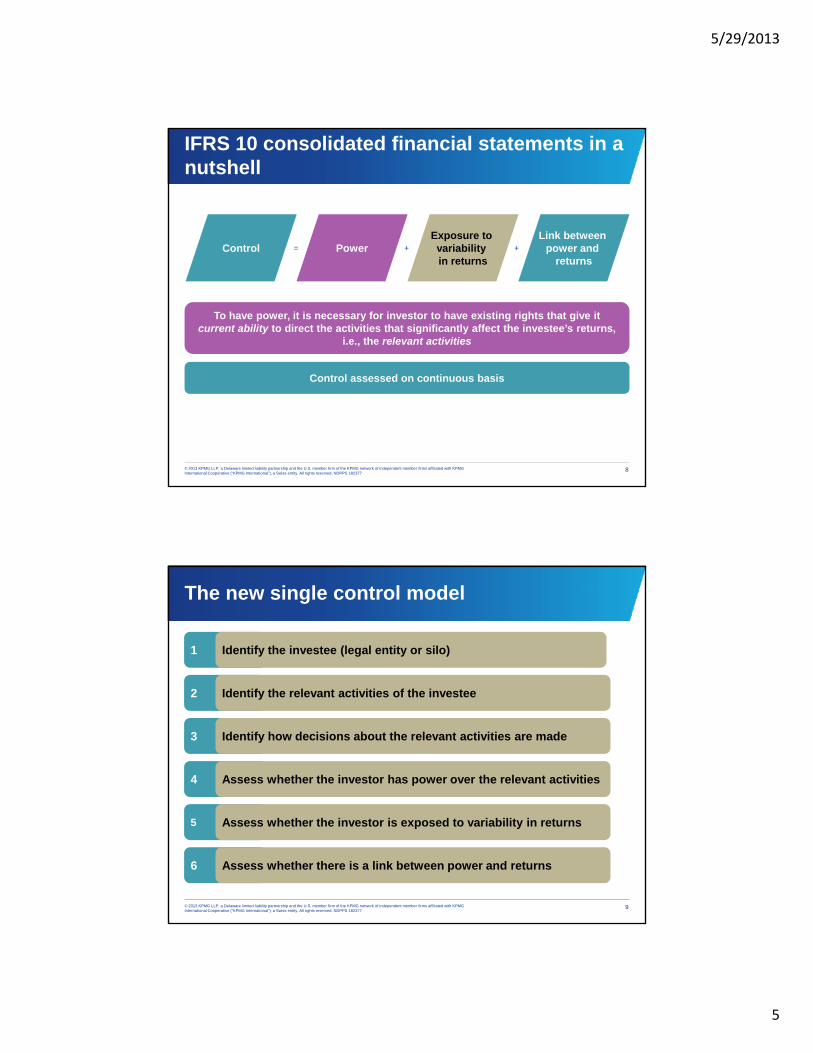

IFRS 10 consolidated financial statements in a nutshell

PowerExposure to variability

Link between power andControl + +=

To have power, it is necessary for investor to have existing rights that give it current ability to direct the activities that significantly affect the investee’s returns,

i.e., the relevant activities

Power variability in returns

power and returns

Control + +=

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

8

Control assessed on continuous basis

The new single control model

1 Identify the investee (legal entity or silo)

2 Identify the relevant activities of the investee

3 Identify how decisions about the relevant activities are made

4 Assess whether the investor has power over the relevant activities

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

9

5 Assess whether the investor is exposed to variability in returns

6 Assess whether there is a link between power and returns

5/29/2013

6

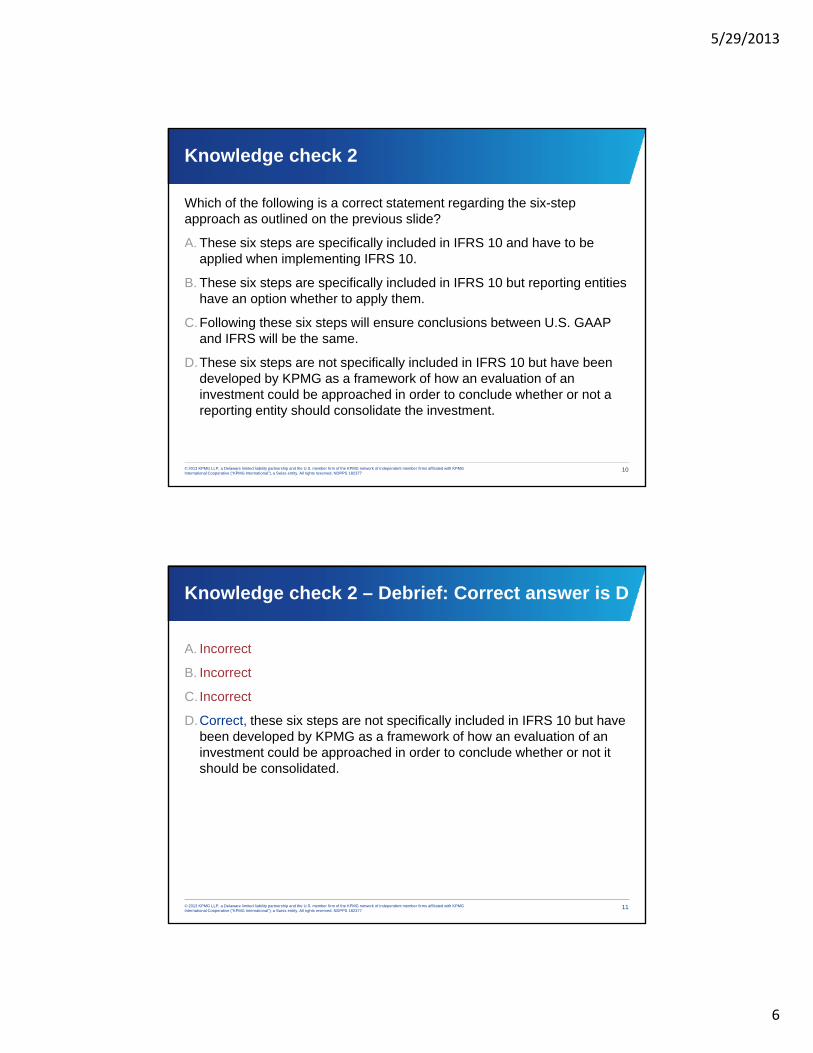

Knowledge check 2

Which of the following is a correct statement regarding the six-step approach as outlined on the previous slide?

A. These six steps are specifically included in IFRS 10 and have to be p p yapplied when implementing IFRS 10.

B. These six steps are specifically included in IFRS 10 but reporting entities have an option whether to apply them.

C.Following these six steps will ensure conclusions between U.S. GAAP and IFRS will be the same.

D.These six steps are not specifically included in IFRS 10 but have been

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

10

p p ydeveloped by KPMG as a framework of how an evaluation of an investment could be approached in order to conclude whether or not a reporting entity should consolidate the investment.

Knowledge check 2 – Debrief: Correct answer is D

A. Incorrect

B. Incorrect

C. Incorrect

D.Correct, these six steps are not specifically included in IFRS 10 but have been developed by KPMG as a framework of how an evaluation of an investment could be approached in order to conclude whether or not it should be consolidated.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

11

5/29/2013

7

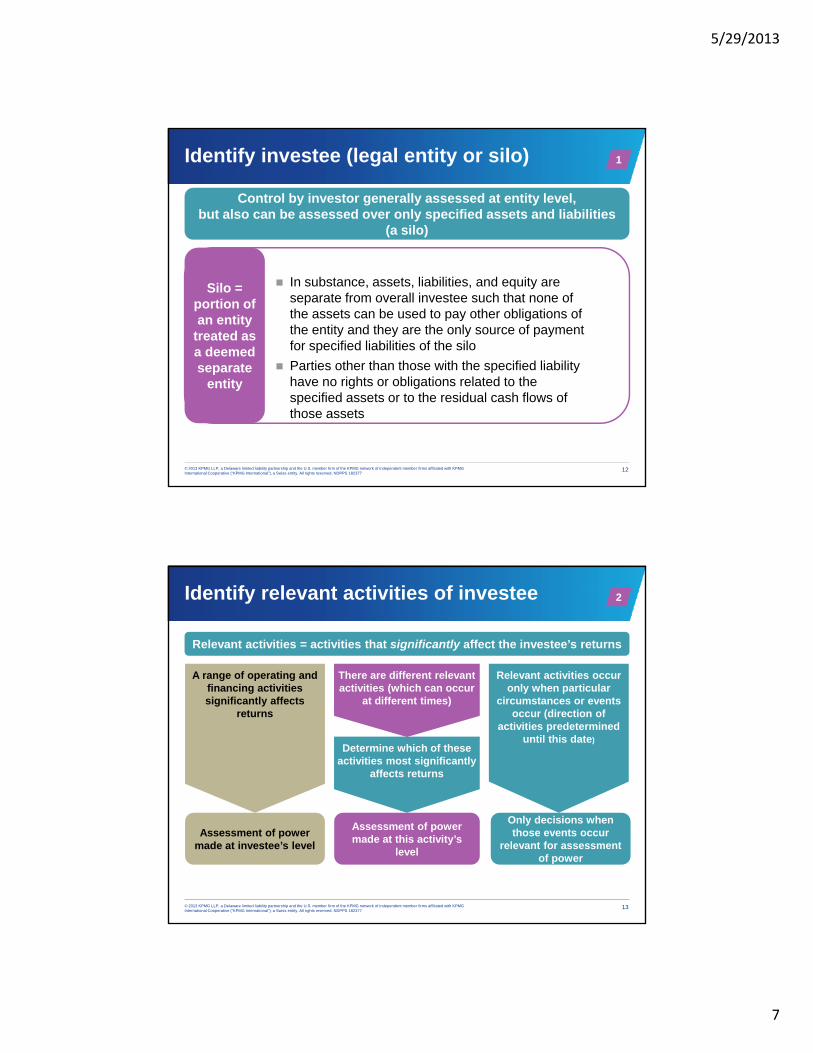

Identify investee (legal entity or silo)

Control by investor generally assessed at entity level, but also can be assessed over only specified assets and liabilities

(a silo)

1

Silo = portion of an entity

treated as a deemed separate

In substance, assets, liabilities, and equity are separate from overall investee such that none of the assets can be used to pay other obligations of the entity and they are the only source of payment for specified liabilities of the silo

Parties other than those with the specified liability

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

12

separate entity

Parties other than those with the specified liability have no rights or obligations related to the specified assets or to the residual cash flows of those assets

Identify relevant activities of investee 2

Relevant activities = activities that significantly affect the investee’s returns

A range of operating and fi i ti iti

There are different relevantti iti ( hi h

Relevant activities occur l h ti lfinancing activities

significantly affects returns

Determine which of these activities most significantly

affects returns

activities (which can occur at different times)

only when particular circumstances or events

occur (direction of activities predetermined

until this date)

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

13

Assessment of power made at investee’s level

Assessment of power made at this activity’s

level

Only decisions when those events occur

relevant for assessment of power

5/29/2013

8

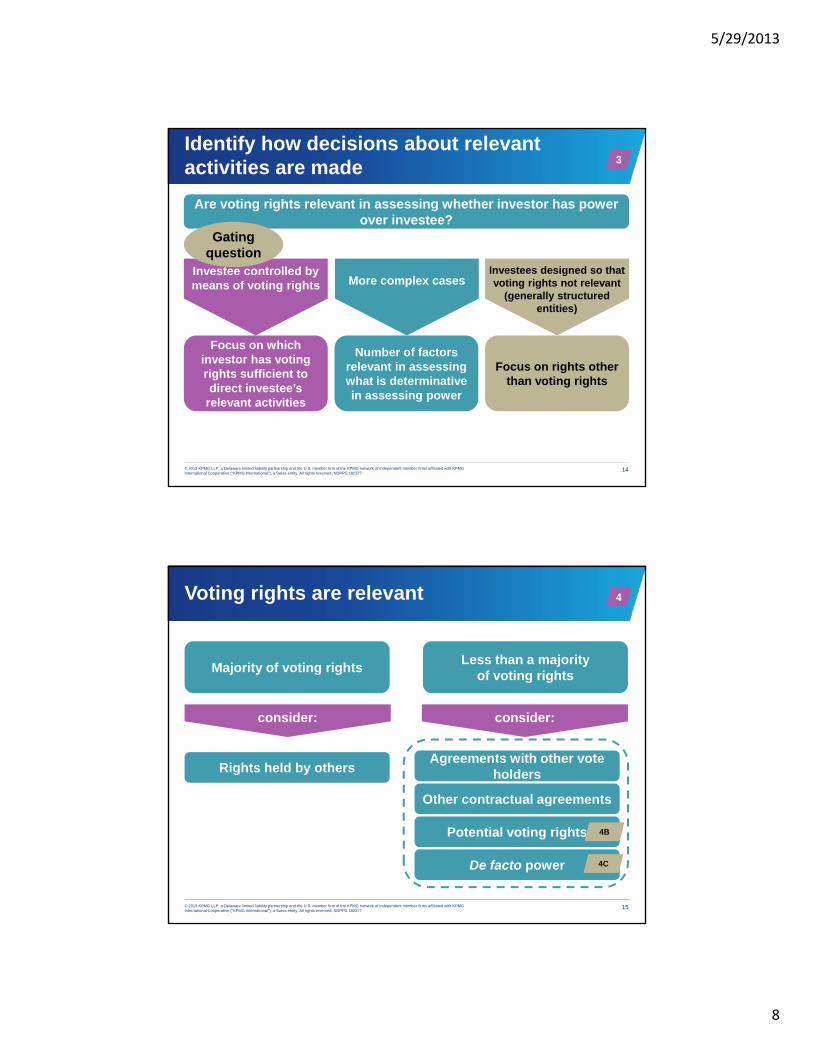

Identify how decisions about relevant activities are made 3

Are voting rights relevant in assessing whether investor has power over investee?

Gating

Focus on which investor has voting

Investee controlled by means of voting rights

question

Number of factors relevant in assessing

More complex cases

Focus on rights other

Investees designed so that voting rights not relevant

(generally structured entities)

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

14

rights sufficient to direct investee’s

relevant activities

relevant in assessing what is determinative in assessing power

Focus on rights other than voting rights

Voting rights are relevant 4

Less than a majority of voting rights

Majority of voting rights

Rights held by others

consider: consider:

Agreements with other vote holders

Other contractual agreements

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

15

g

Potential voting rights 4B

De facto power 4C

5/29/2013

9

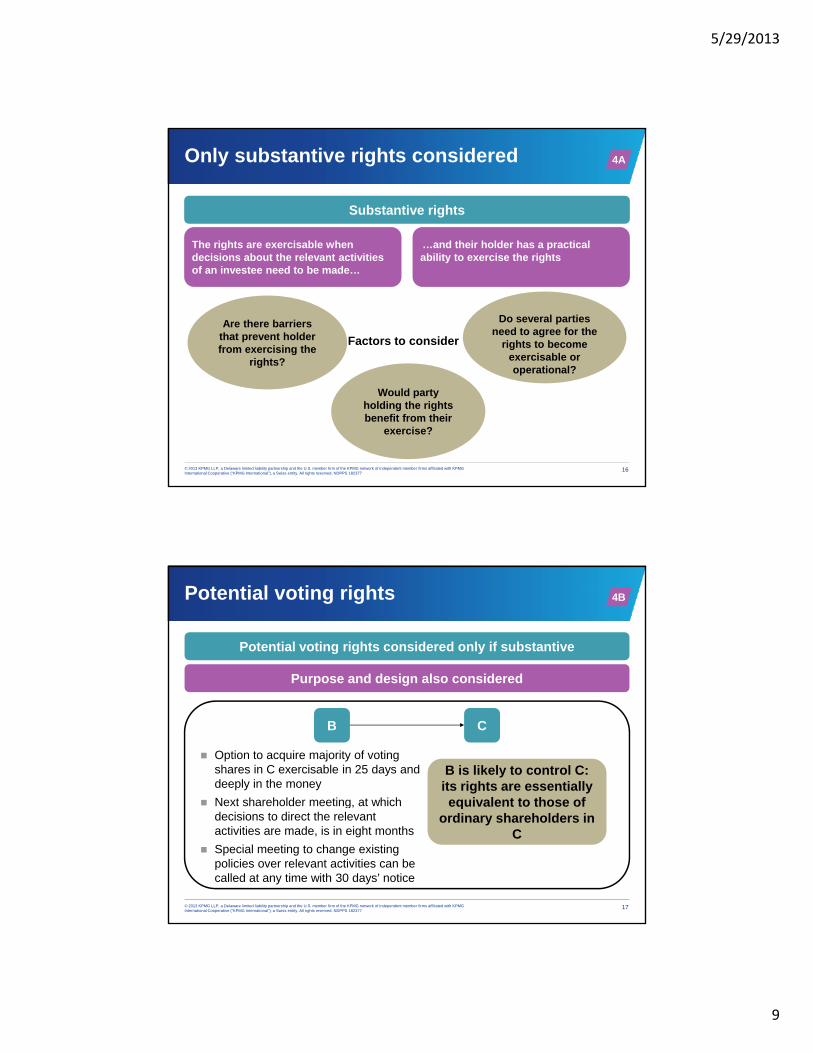

Only substantive rights considered

Substantive rights

…and their holder has a practicalThe rights are exercisable when

4A

Factors to consider

…and their holder has a practical ability to exercise the rights

The rights are exercisable when decisions about the relevant activities of an investee need to be made…

Are there barriers that prevent holder from exercising the

rights?

Do several parties need to agree for the

rights to become exercisable or

ti l?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

16

g

Would party holding the rights benefit from their

exercise?

operational?

Potential voting rights

Potential voting rights considered only if substantive

Purpose and design also considered

4B

p g

B C

Option to acquire majority of voting shares in C exercisable in 25 days and deeply in the money

Next shareholder meeting at which

B is likely to control C: its rights are essentially equivalent to those of

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

17

Next shareholder meeting, at which decisions to direct the relevant activities are made, is in eight months

Special meeting to change existing policies over relevant activities can be called at any time with 30 days’ notice

equivalent to those of ordinary shareholders in

C

5/29/2013

10

Knowledge check 3

Which of the following statements is correct with regard to potential voting rights?

A. Consideration of potential voting rights is a new principle introduced in p g g p pIFRS 10 for the first time.

B. Consideration of potential voting rights is not a new principle introduced in IFRS 10 for the first time, but its consideration differs from that under IAS 27.

C.The consideration of potential voting rights in IFRS 10 results in convergence between IFRS and U.S. GAAP.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

18

D.The consideration of potential voting rights only is applicable for the evaluation of investees which are special purpose vehicles.

Knowledge check 3 – Debrief: Correct answer is B

A. Incorrect

B. Correct, consideration of potential voting rights is not a new principle i t d d i IFRS 10 f th fi t ti b t it id ti diff fintroduced in IFRS 10 for the first time, but its consideration differs from IAS 27.

C. Incorrect

D. Incorrect

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

19

5/29/2013

11

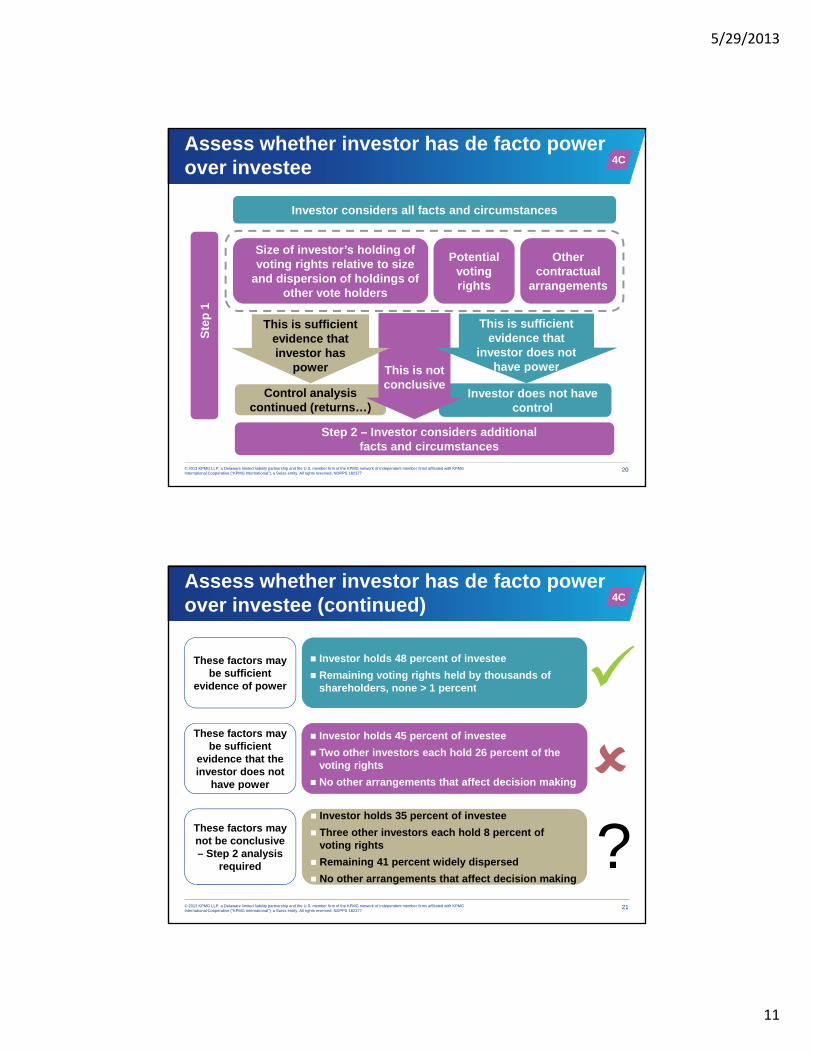

Assess whether investor has de facto power over investee

Investor considers all facts and circumstances

Size of investor’s holding of

4C

Ste

p 1

Size of investor’s holding of voting rights relative to size

and dispersion of holdings of other vote holders

Potential voting rights

Other contractual

arrangements

Thi i t

This is sufficient evidence that investor has

power

This is sufficient evidence that

investor does not have power

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

20

Step 2 – Investor considers additional facts and circumstances

Control analysis continued (returns…)

Investor does not have control

This is not conclusive

power have power

Assess whether investor has de facto power over investee (continued)

These factors may be sufficient

evidence of power

Investor holds 48 percent of investee

Remaining voting rights held by thousands of h h ld > 1 t

4C

These factors may be sufficient

evidence that the investor does not

have power

Investor holds 45 percent of investee

Two other investors each hold 26 percent of the voting rights

No other arrangements that affect decision making

evidence of power shareholders, none > 1 percent

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

21

These factors may not be conclusive – Step 2 analysis

required

Investor holds 35 percent of investee

Three other investors each hold 8 percent of voting rights

Remaining 41 percent widely dispersed

No other arrangements that affect decision making?

5/29/2013

12

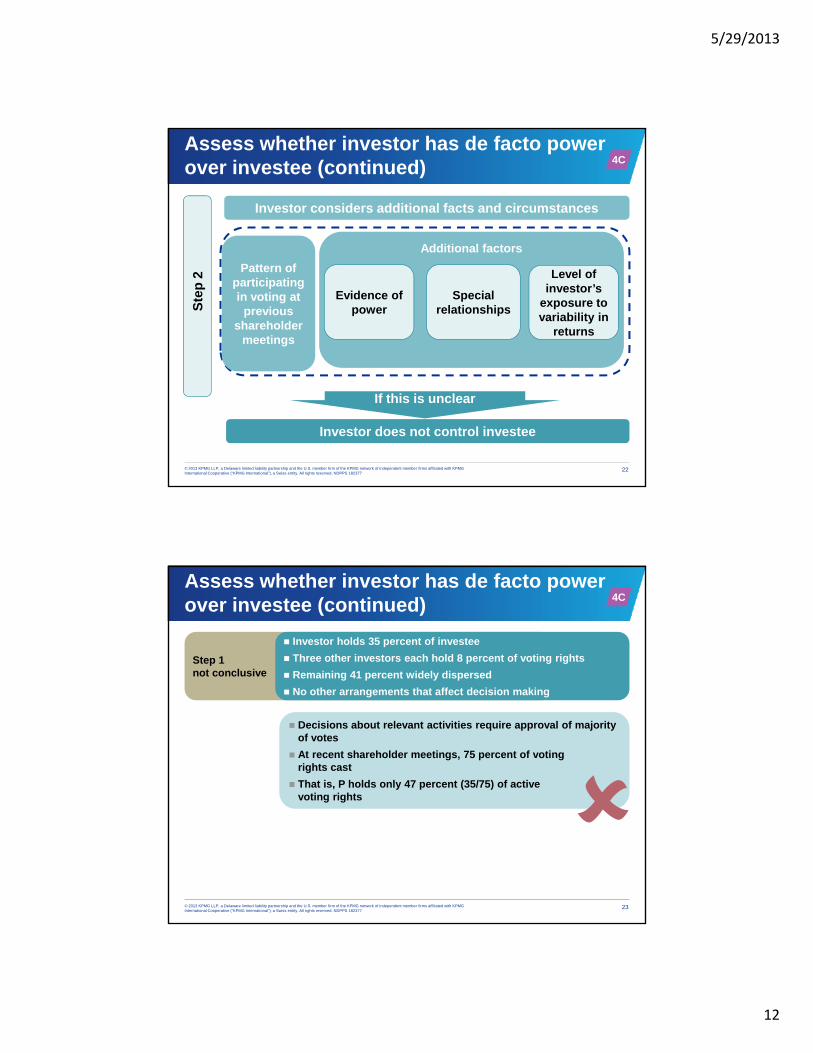

Assess whether investor has de facto power over investee (continued)

Investor considers additional facts and circumstances

Additional factors

4C

Pattern of participating in voting at

previous shareholder

meetings

Additional factors

Evidence of power

Special relationships

Level of investor’s

exposure to variability in

returns

Ste

p 2

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

22

If this is unclear

Investor does not control investee

Assess whether investor has de facto power over investee (continued)

Step 1 not conclusive

Investor holds 35 percent of investee

Three other investors each hold 8 percent of voting rights

Remaining 41 percent widely dispersed

4C

No other arrangements that affect decision making

Decisions about relevant activities require approval of majority of votes

At recent shareholder meetings, 75 percent of voting rights cast

That is, P holds only 47 percent (35/75) of active voting rights

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

23

5/29/2013

13

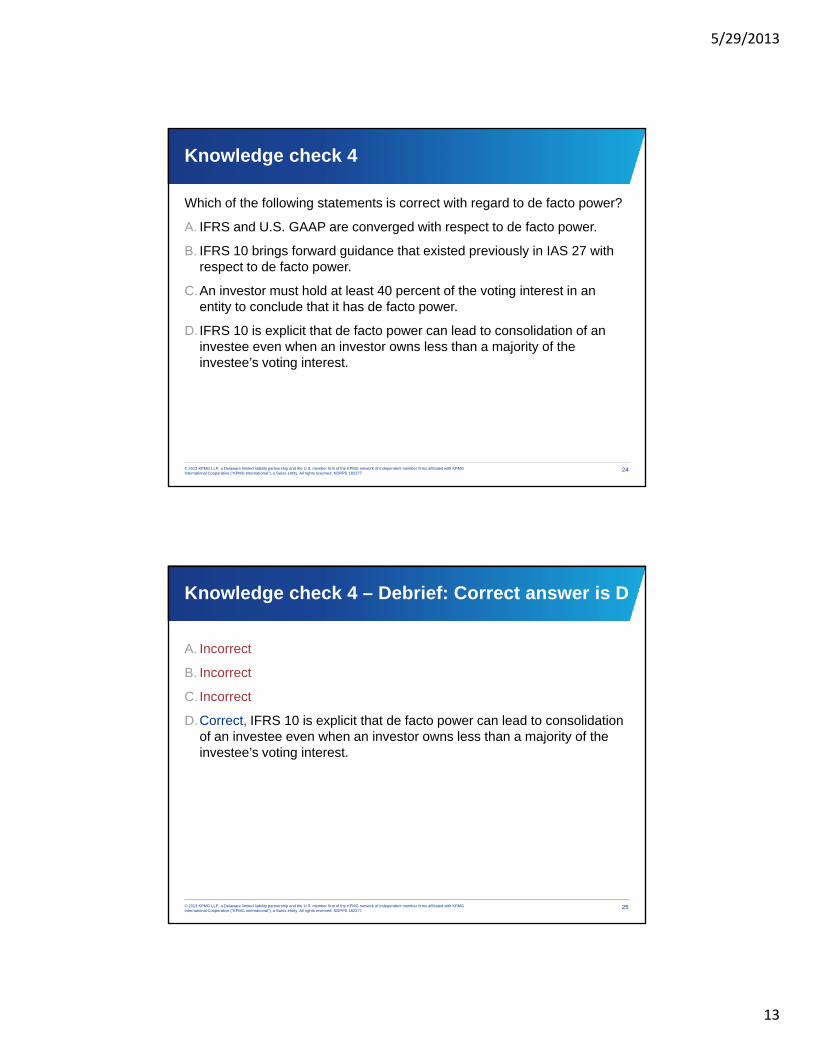

Knowledge check 4

Which of the following statements is correct with regard to de facto power?

A. IFRS and U.S. GAAP are converged with respect to de facto power.

B IFRS 10 b i f d id th t i t d i l i IAS 27 ithB. IFRS 10 brings forward guidance that existed previously in IAS 27 with respect to de facto power.

C.An investor must hold at least 40 percent of the voting interest in an entity to conclude that it has de facto power.

D. IFRS 10 is explicit that de facto power can lead to consolidation of an investee even when an investor owns less than a majority of the investee’s voting interest.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

24

g

Knowledge check 4 – Debrief: Correct answer is D

A. Incorrect

B. Incorrect

C. Incorrect

D.Correct, IFRS 10 is explicit that de facto power can lead to consolidation of an investee even when an investor owns less than a majority of the investee’s voting interest.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

25

5/29/2013

14

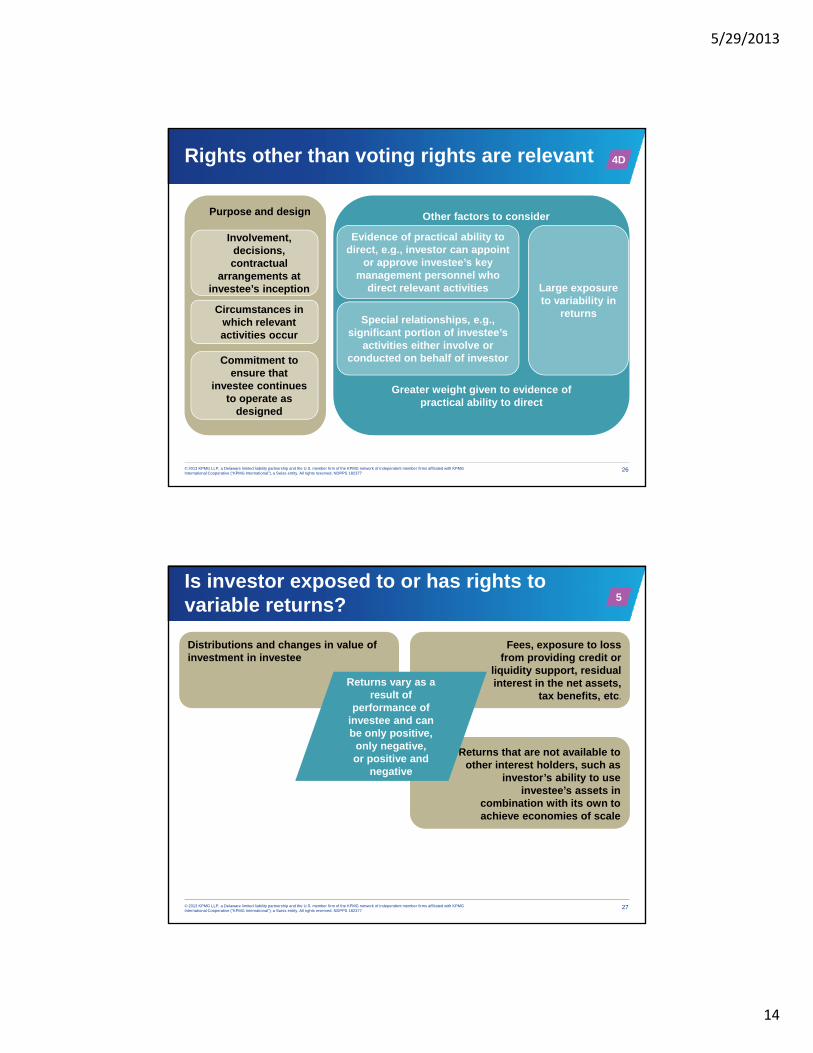

Rights other than voting rights are relevant

Other factors to considerPurpose and design

Evidence of practical ability to direct e g in estor can appoint

Involvement, d i i

4D

Special relationships, e.g., significant portion of investee’s

activities either involve or conducted on behalf of investor

Large exposure to variability in

returns

direct, e.g., investor can appoint or approve investee’s key

management personnel who direct relevant activities

decisions, contractual

arrangements at investee’s inception

Circumstances in which relevant activities occur

Commitment to

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

26

Greater weight given to evidence of practical ability to direct

ensure that investee continues

to operate as designed

Is investor exposed to or has rights to variable returns?

Distributions and changes in value of investment in investee

Fees, exposure to loss from providing credit or

liquidity support, residual interest in the net assetsReturns vary as a

5

interest in the net assets, tax benefits, etc.

Returns that are not available to other interest holders, such as

investor’s ability to use investee’s assets in

combination with its own to

Returns vary as a result of

performance of investee and can be only positive,

only negative, or positive and

negative

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

27

combination with its own to achieve economies of scale

5/29/2013

15

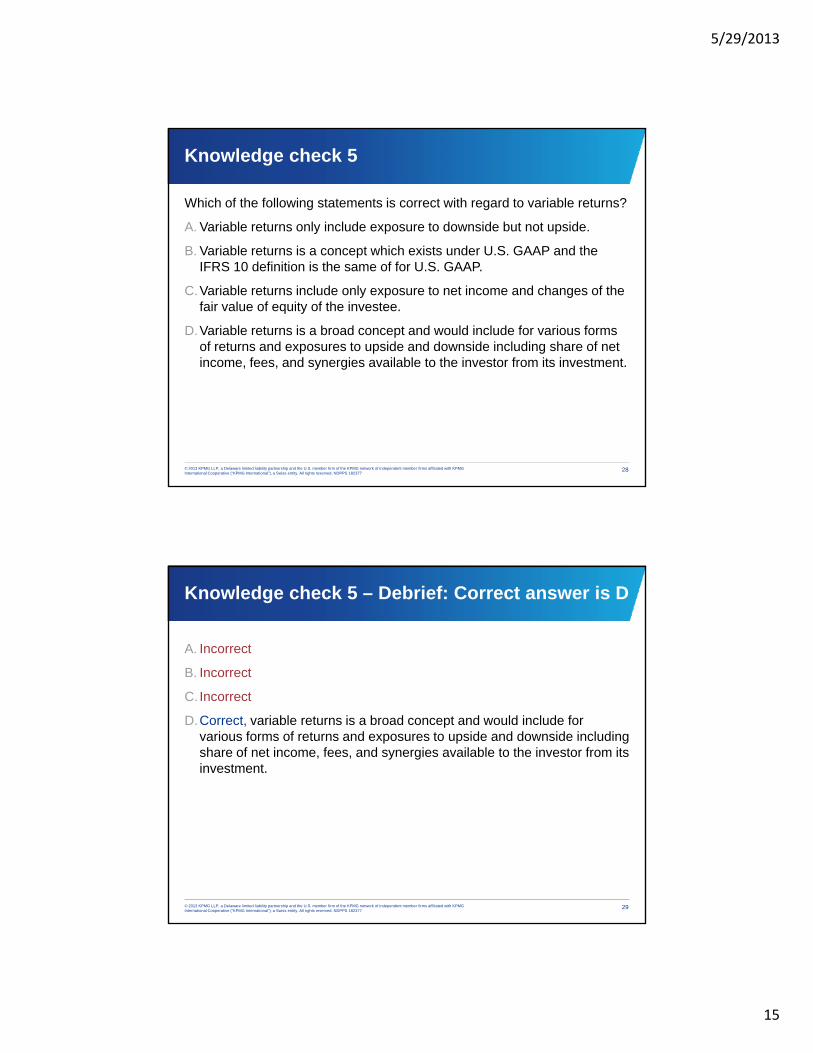

Knowledge check 5

Which of the following statements is correct with regard to variable returns?

A. Variable returns only include exposure to downside but not upside.

B V i bl t i t hi h i t d U S GAAP d thB. Variable returns is a concept which exists under U.S. GAAP and the IFRS 10 definition is the same of for U.S. GAAP.

C.Variable returns include only exposure to net income and changes of the fair value of equity of the investee.

D.Variable returns is a broad concept and would include for various forms of returns and exposures to upside and downside including share of net income, fees, and synergies available to the investor from its investment.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

28

, , y g

Knowledge check 5 – Debrief: Correct answer is D

A. Incorrect

B. Incorrect

C. Incorrect

D.Correct, variable returns is a broad concept and would include for various forms of returns and exposures to upside and downside including share of net income, fees, and synergies available to the investor from its investment.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

29

5/29/2013

16

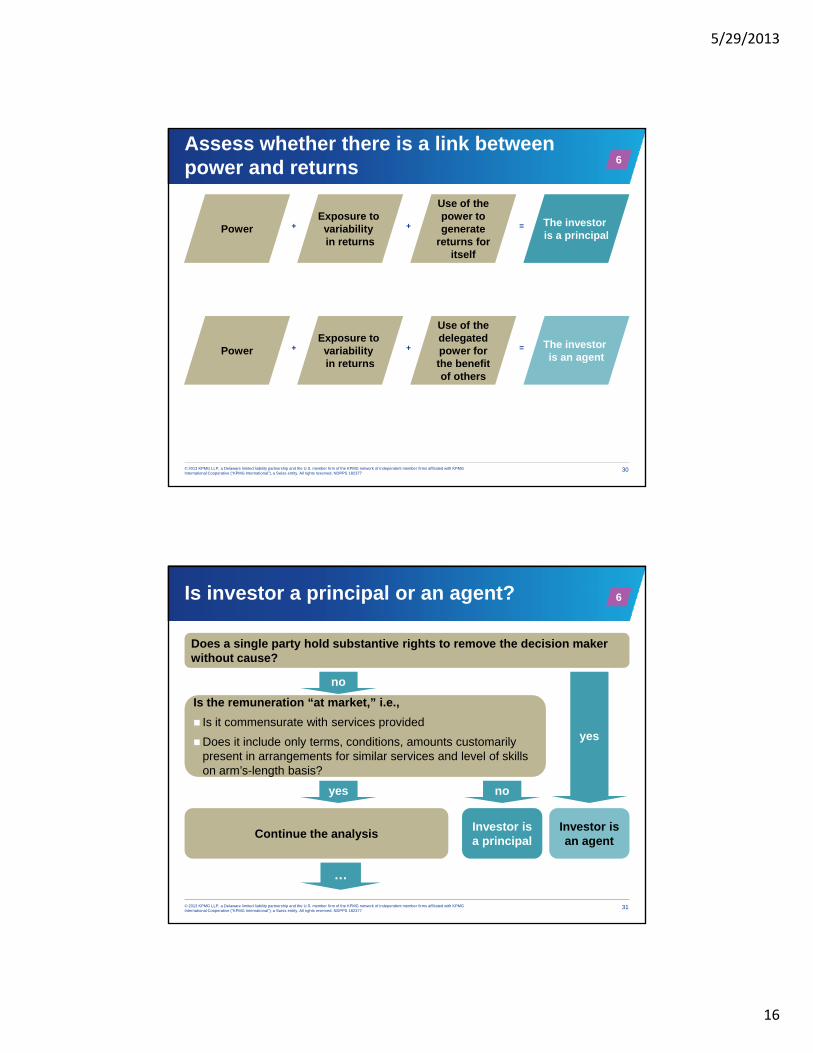

Assess whether there is a link between power and returns

=PowerExposure to variability in returns

The investor is a principal

++

Use of the power to generate

returns for

6

itself

=++PowerExposure to variability in returns

The investor is an agent

Use of the delegated power for the benefit

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

30

of others

Is investor a principal or an agent?

Does a single party hold substantive rights to remove the decision maker without cause?

no

6

Is the remuneration “at market,” i.e.,

Is it commensurate with services provided

Does it include only terms, conditions, amounts customarily present in arrangements for similar services and level of skills on arm’s-length basis?

yes

no

yes no

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

31

Investor is a principal

Investor is an agent

Continue the analysis

…

5/29/2013

17

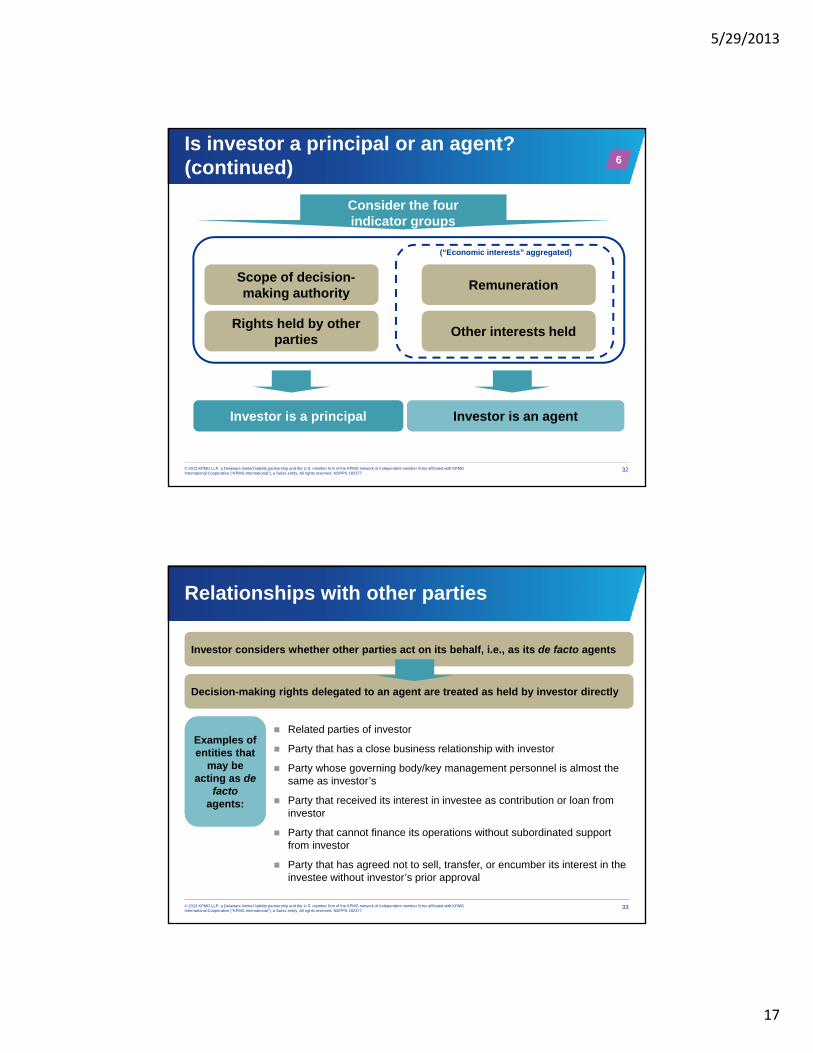

Is investor a principal or an agent? (continued)

Consider the four indicator groups

6

Scope of decision-making authority

Remuneration

Rights held by other parties

Other interests held

(“Economic interests” aggregated)

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

32

Investor is an agentInvestor is a principal

Relationships with other parties

Investor considers whether other parties act on its behalf, i.e., as its de facto agents

Decision-making rights delegated to an agent are treated as held by investor directly

Examples of entities that

may be acting as de

factoagents:

Related parties of investor

Party that has a close business relationship with investor

Party whose governing body/key management personnel is almost the same as investor’s

Party that received its interest in investee as contribution or loan from

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

33

agents: yinvestor

Party that cannot finance its operations without subordinated support from investor

Party that has agreed not to sell, transfer, or encumber its interest in the investee without investor’s prior approval

5/29/2013

18

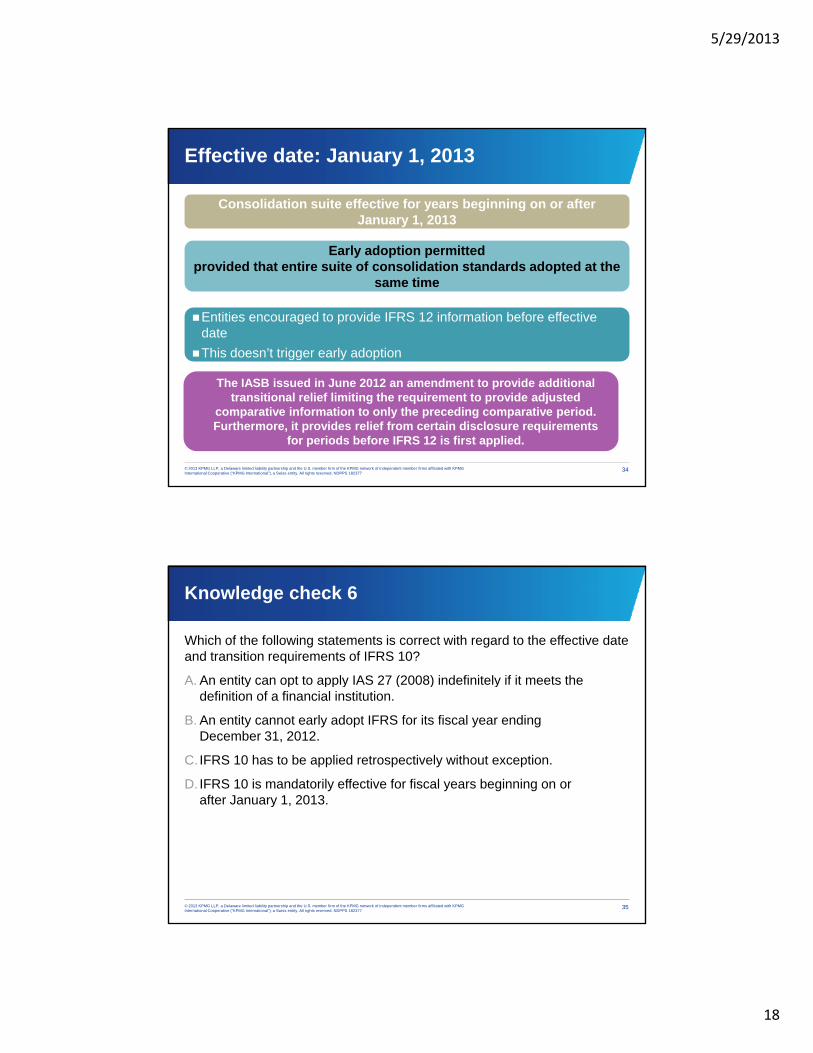

Effective date: January 1, 2013

Consolidation suite effective for years beginning on or after January 1, 2013

E l d ti itt dEarly adoption permitted provided that entire suite of consolidation standards adopted at the

same time

Entities encouraged to provide IFRS 12 information before effective date

This doesn’t trigger early adoption

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

34

The IASB issued in June 2012 an amendment to provide additional transitional relief limiting the requirement to provide adjusted

comparative information to only the preceding comparative period.Furthermore, it provides relief from certain disclosure requirements

for periods before IFRS 12 is first applied.

Knowledge check 6

Which of the following statements is correct with regard to the effective date and transition requirements of IFRS 10?

A. An entity can opt to apply IAS 27 (2008) indefinitely if it meets the y p pp y ( ) ydefinition of a financial institution.

B. An entity cannot early adopt IFRS for its fiscal year ending December 31, 2012.

C. IFRS 10 has to be applied retrospectively without exception.

D. IFRS 10 is mandatorily effective for fiscal years beginning on or after January 1, 2013.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

35

y ,

5/29/2013

19

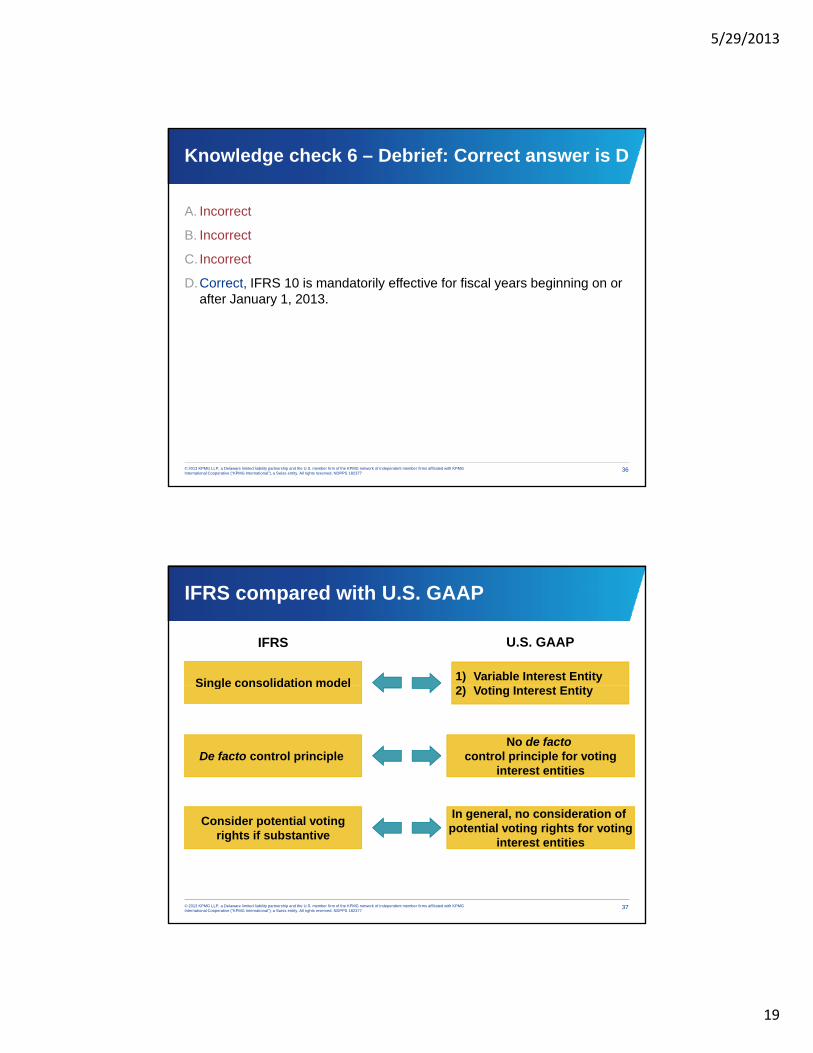

Knowledge check 6 – Debrief: Correct answer is D

A. Incorrect

B. Incorrect

C. Incorrect

D.Correct, IFRS 10 is mandatorily effective for fiscal years beginning on or after January 1, 2013.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

36

IFRS compared with U.S. GAAP

Single consolidation model1) Variable Interest Entity

IFRS U.S. GAAP

Single consolidation model2) Voting Interest Entity

De facto control principle No de facto

control principle for votinginterest entities

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

37

Consider potential votingrights if substantive

In general, no consideration of potential voting rights for voting

interest entities

5/29/2013

20

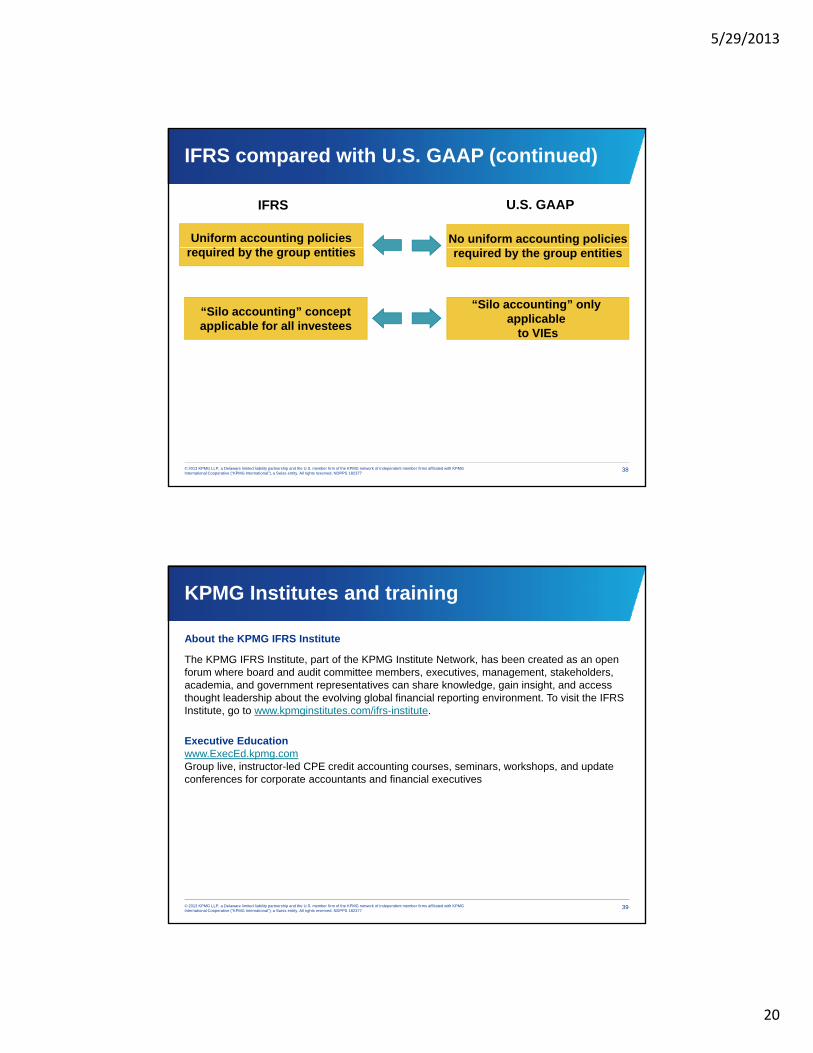

IFRS compared with U.S. GAAP (continued)

Uniform accounting policies No uniform accounting policies

IFRS U.S. GAAP

required by the group entities required by the group entities

“Silo accounting” conceptapplicable for all investees

“Silo accounting” only applicable

to VIEs

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

38

KPMG Institutes and training

About the KPMG IFRS Institute

The KPMG IFRS Institute, part of the KPMG Institute Network, has been created as an open forum where board and audit committee members, executives, management, stakeholders, academia and government representatives can share knowledge gain insight and accessacademia, and government representatives can share knowledge, gain insight, and access thought leadership about the evolving global financial reporting environment. To visit the IFRS Institute, go to www.kpmginstitutes.com/ifrs-institute.

Executive Educationwww.ExecEd.kpmg.comGroup live, instructor-led CPE credit accounting courses, seminars, workshops, and update conferences for corporate accountants and financial executives

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

39

5/29/2013

21

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future No one should act uponcontinue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 182377

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.