ifc - promoting environmental and social risk management (esrm) in the financial sector of pakistan

TRANSCRIPT

PROMOTING ENVIRONMENTAL AND SOCIAL

RISK MANAGEMENT (ESRM) IN THE

FINANCIAL SECTOR OF PAKISTAN

OUTLINE

• The concept of ESRM

• Global ESRM programme

• Challenges faced by the bankers

• Why ESRM is important for clients

• Why ESRM is important for Banks

• Way forward

2

PAKISTAN SCENARIO

3

QUICK STATS

“Annual cost of environmental degradation in Pakistan is about 4.3 % of GDP (US $ 4.3 billion)”. ---SUPARCO

“Pakistan had needed to spend Rs82.5 billion on industrial environment management between 1997 and 2010, but actually spent only around Rs7.5 billion, leaving a deficit of Rs75 billion. If we continue polluting our ecosystem at the current rates, this deficit could climb to Rs140 billion by 2025.”--- Express Tribune, 2012

“741 cases registered against factory owners for not complying with the National Environmental Quality Standards (NEQS), 339 have been settled while remaining 402 cases are still under consideration of the Environmental Tribunals”.---The Nation, 2010

4

WHAT IS ENVIRONMENTAL & SOCIAL RISK

MANAGEMENT (ESRM) FOR FINANCIAL

INSTITUTIONS?

Sustainable finance (ESRM for FIs) can be defined as

the provision of financial capital and risk

management products and services in ways that

promote or do not harm economic prosperity, the

ecology and community well-being.

Sustainable Finance does not mean saving the

environment just for the sake of saving it.

Sustainable Finance means good business for FIs.

Scope of ESRMProject Finance Corporate Finance SME

WHY IS SUSTAINABILITY IMPORTANT

FOR CLIENTS?

6

Reputational Risk

Compliance

Access to New Markets

Cost saving

Loss reduction

Clients don’t care for the Environment because of the goodness of their

heart. Caring for the environment is a pure business decision.

Banks should also care about sustainability for pure business reasons

Why Banks should worry about Sustainability?

Campaigners gave out the mock newspaper, “The Daily Whale” to

employees outside each of the 3 banks, Standard Chartered, BNP

Paribas and Credit Suisse in London.

7

This is an example what the banks should avoid--- a reactive approach once

reputational harm has been done.

8

9

WHY IS SUSTAINABLE FINANCE

IMPORTANT FOR BANKS?

Litigation, shut down leading to increase in NPL

Decrease in the value of collateral and additional cost

of cleaning up.

Disruption of operation

Reputational risk

Pressure from investors, government

International Commitments: Equator Principle,

Climate Principles

10

The question is not “WHY” Banks should

consider ESRM. The Question is “HOW”

E&S RISK ASSESSMENT (ESRA) FRAMEWORK

11

POLICYESRM Guideline

E&S Capacity

Development•Roles and

responsibilities

•Training: E learning,

Webinar

PROCEDURE

E&S risk Assessment

Exclusion List

E&S Risk Assessment Tool

Risk rating

Escalation

Conditions/ Action Plan

REPORTING

• Annual

Sustainability

Review

Monitoring E&S risk

Annual review: monitor

performance

Managing non compliance

CHALLENGES FACED BY RMS AND CREDIT IN E&S DUE DILIGENCE

Perceptual Barrier

Not important

Climate Change is a myth

Institutional Barrier

Lack of valid data

Misalignment between RMs

target and E&S requirements

Policy and regulatory Barrier

Country laws not conducive

Skill, knowledge, information

barriers

Lack of proper understanding of

E&S issues

Lack of training

Lack of tools and processes

12

SUSTAINABILITY IS A SHARED

RESPONSIBILITY

13

Regulator/Government

- Policy

- Enforcement

- Tax/incentive

-Institutional strengthening

Business

-obtain social license to operate

-Ensure safety, efficiency

-Compliance

Banks

-Mission, vision

-Policies procedures

-skilled workforce

-Moving from only compliance to value addition to clients

Media

-Understand and sensitize the public

- Publish case studies

-Demystify technical issues

Sustainability

ENVIRONMENTAL & SOCIAL RISK

MANAGEMENT (ESRM) FOR FIS ADVISORY

SERVICES PROGRAM

Objectives:

Creating regulatory drivers through support for banking

regulators and associations with E&S risk management

guideline development

Market capacity development for trainer and consultant

networks to provide technical support for FIs

ESMS diagnostic and implementation support to FIs

Raising awareness through the Sustainable Banking

Network, developing business case studies and best practices

14

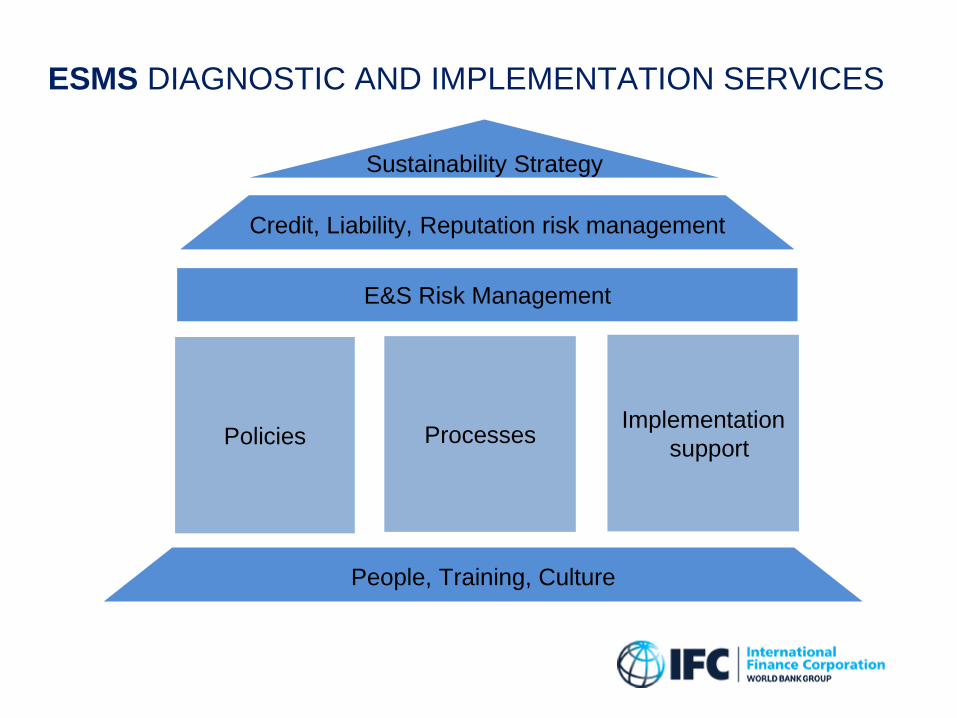

ESMS DIAGNOSTIC AND IMPLEMENTATION SERVICES

15

Policies ProcessesImplementation

support

People, Training, Culture

Sustainability Strategy

Credit, Liability, Reputation risk management

E&S Risk Management

IMPLEMENTATION SUPPORT

16

ESRM Framework

ESMS Core Module

ESMS Implementation

Support

Capacity Development &

Training

ESMS Data, Ratings and KPI development

External Communication

Support for Internal Audit

17

E&S Risk Management /

EP Implementation

• Built system, procedure

and tools

• Created dedicated team

and built capacity

• Actively communicated

with client and multi-

stakeholders

• Developed reporting

system

Sustainability Products

• First FI Green Bond (approved

by authority, to be launched in

2015 )

• Carbon finance

• Low carbon credit card

• First carbon assets backed

lending

• First emission rights backed

lending

• First IFC partner bank in China

for energy-efficiency lending to

support SMEs

Strong contributor to overall business:

• Strong business results: assets grow 15 times (2003 to 2014), ROE over 20% since 2006, NPL ratio <1%,

• Reputation and brand value: brand value of US$1.09 billion (by Interbrand, 2012), 50% increase over 2011;

won many top national and international awards

• Increased value to shareholders – 2013 Asia Best Shareholder Return Bank

• Better access to international capital and cooperation (IFC, ING, Citibank, etc.)

Green Finance Expansion:

• Green finance about 12% of total lending, highest among the Chinese banks (national average is 8%)

• Climate benefits: reduced 68 mn tons of CO2, saved 255 mn tons of water. The energy conserved and

emission reduced is equivalent to shutting off 157 thermal power plants of 100 MW.

China Industrial Bank’s Green Banking Journey:

“From Green to Gold”

18

2006First Chinese

bank to sign

Energy

Efficiency

Finance

(CHUEEE) with

IFC, Beijing

2007

Runner-up of

FT Sustainable

Deal of the

Year;

Joining UNEP

Finance

Initiative

.

Stage I: Piloting Green

Lending Product

2008

Adopting Equator

Principles, Beijing,

becoming the first

EP bank in Asia

emerging market;Launched CHUEE

Ⅱ.

2009Establishment of

Sustainable

Finance Center;FT Emerging

Markets

Sustainable Bank

of the Year (Asia)

First Sustainability

Report in China

Banking sector;

“The Best Green

Bank”

&“Environmental

Information

Disclosure Award”

by 9 Chinese

NGOs.

Stage II: Adopting &

Implementing Equator

Principles

Stage III: Fully Integrated

Sustainable Finance Model

2012Establishment

of Sustainable

Finance

Department,

sets up regional

green finance

business units

across China

2010Launched the first

Low-carbon Credit

Card;Included in the

“Hang Seng (China

A) Corporate

Sustainability

Index ”&“Hang

Seng (Mainland

and HK) Corporate

Sustainability Index”

2011Promoting 8+1

green financial

products;Annual Most

Social

Responsible

Institutions

Award and Best

Green Finance

Award by the

China Banking

Association;

.

2013Green

finance

clients hit

2,472,

about 12

times vs.

2009; and

green

finance

based

financing

balance

reached

US$30

billion, 13

times

vs. 2009

IB’s 3-Stage Journey to be the Leading Green Bank in China and Asia

Bank of Philippine Island (BPI):

A Pioneer in Green Banking In the Philippines

• 1st phase largely focused on energy efficiency loans ($ 26.9 Million)

• 2nd phase included renewable energy loans ($110.1 Million)

• 3rd phase expanded to green mortgage, carbon finance and energy performance contracting ($216.1

Million)

• 4th phase included green buildings and continuous capacity building (ongoing, $130.1 Million)

• As of December 2014, $483 Million total loan volume IFC helped generate with SEF since 2008

• Over 1 Million metric tons of GHG emissions reduced

• RSF 1 signed in 2009 ($46 Million), expanded to ($114 Million) in 2012

• BPI has utilized 78% of the guarantee facility as of end 2014.

• BPI’s entry focused on sustainable energy finance for SMEs

• Recognized among 345 innovations submitted from 75 countries.

• International recognition for its SEF program

• USD 1.4 Million grant for market development and capacity building

Management system

Capacity building for bank loan officers

• Demonstration impact for other Philippine banks

• Consider to join the EPs

19

1st Philippine bank to partner with IFC on Sustainable Energy Finance in 2008

Risk Sharing Facility

Winner, G20 SME Finance Challenge in 2012

E&S risk management

EE INVESTMENT MATRIX FOR INDUSTRY IN PAKISTAN(SECTOR VS. TECHNOLOGY)

20

Technology

Estimated Investment (Million PKR)

Textile

Spinning

Textile

ProcessSugar Leather Paper Cement Fertilizer Other Sectors Total

Payback

Period (Yrs)

Co-generation 100,800 22,500 30,850 154,150 4-5

Compressor 6,000 5,300 165 880 3,100 15,445 1-3

Heat recovery 43,300 35,000 84 272 22 540 19,750 98,968 -

Heat transfer 4,000 15,600 25 58 4,950 24,633 2-3

Lights 2,800 400 800 4,000 1-2

Meters 4,600 4,300 60 2,200 11,160 -

Motors 16,000 9,200 840 110 440 6,700 33,290 1-2

Power Factor 350 100 110 140 700 1-4

Process 1,350 1,200 6,250 7,900 5,220 5,500 27,420 2-4

Process Control 14,350 420 275 22 100 3,800 18,967 1-2

Steam system 550 4,500 600 165 1,450 7,265 1-4

VFD 4,100 1,750 840 53 63 1,700 8,506 1-2

Total 82,700 90,750 104,809 1,145 7,777 30,623 5,760 80,940 404,504

• The overall investment potential for the Energy Efficiency (“EE”) measures

identified in the industrial sectors in Pakistan is in the order of PKR 400 billion…

Payback times for the investments identified are generally below 5 years…

The opportunities are there for FIs to develop an entirely new business

Benefits for Pakistani Banks and their Clients

21

For Clients:

• Cost savings – Improved Productivity/Quality of Output –

Competitiveness

• Reasonable pay-back period – Investments recovered from energy cost

savings

• Reduced footprint – Sustainable access to global supply chains

For FIs:

• Expanded market through a new business line:

Innovative product- First mover advantage/differentiation

Sell on value to customer, not pricing

Monetize existing client base- Attract quality new clients

New marketing channels through vendor partnerships

• Improved risk profile of portfolio:

Cost efficient clients = Better performing clients

Energy cost savings as a part of cash-flow

• Positive social and environmental impacts:

Enhanced brand reputation, PR opportunities

IFC’S SUPPORT TO CLIMATE CHANGE MITIGATION

THROUGH SEF

Under Sustainable Energy Finance (SEF) product line, IFC

provides financial products and/or advisory services to FIs in

following areas:

• Energy Efficiency (EE): Investing into fixed asset to reduce energy

bill of end-users through increased efficiency of energy use

• Renewable Energy (RE): Investing into technologies generating

power or heat from renewable resources

• Resource Efficiency (Ref): Investing into technologies minimizing

water, raw material, waste and emissions from industrial

processes and maximizing product output

22

IFC’S COMPREHENSIVE APPROACH TO

OPTIMIZING SEF IMPACT

Financial products tailored to the needs of diverse

markets

Credit lines and senior loans (medium- to long- term)

Risk sharing products and partial guarantees

Trade guarantees

Mezzanine financing and subordinated debt

Risk capital

Mobilizing donor funding for concessional finance

Advisory to build a profitable SEF business

Market analysis and product development

Enabling the FI to build a pipeline of EE/RE sub-projects

Training for loan officers, credit risk managers, marketing personnel

Tools and resources to add value with low transaction cost

Work with contractors/energy service companies /vendors

23

About the Sustainable Banking Network (SBN)

SBN

• Launched in 2012

• A unique, knowledge-sharing

network of banking regulators

and banking associations

• Supports a level playing field

for E&S risk management by

financial institutions

• Promotes green and inclusive

lending

IFC

• Supporting development and

implementation of national

policies/guidelines

• Facilitating South-South learning and

cooperation

• Co-hosting SBN annual meetings

• Developing and disseminating tools and

knowledge resources

24

Facilitator and Technical Advisor

25 25

Sustainable Banking Network

The Network currently consists of banking regulators and banking associations

from16 countries

26

Heads of the interested

institutions confirm their

decision to join SBN.

IFC VP sends a formal invitation

letter

Interested institutions

contact SBN coordinator*

*contacts at the last slide

26

Sustainable Banking Network

How to become a member

27

Click the picture or here to watch the video of the

First International Green Credit Forum

Sustainable Banking Network Events

1st International Green Credit Forum in China

2nd Sustainable Banking Network Meeting In Nigeria

Click the picture or here to watch the video of SBN

Annual Forum in Lagos, Nigeria, Mar. 2014

27

28

Asia

BangladeshBangladesh

Bank-

Environmental

Risk

Management

(ERM) Policy

ChinaChina Banking

Regulatory

Commission

(CBRC) -

Green Credit

Guidelines

ChinaCBRC-M&E

mechanism

launched

IndonesiaOJK (financial regulator) --

Roadmap for Sustainable

Finance in Indonesia 2015-

2019

MongoliaMongolia Banking Association-

Mongolia Sustainable Finance

Principles and 4 Sector

Guidelines

ChinaCBRC-Green Credit Guidelines

KPIs Checklist launched

BangladeshBangladesh Bank-ESRM

Guidelines of

8 Sector Guidelines (planning)

Vietnam The State Bank of Vietnam-the

Directive on Promoting Green

Credit and Managing

Environmental and Social Risks

and 10-sector checklists

NepalThe Central

bank-

Sustainable

Banking Policy

(planning)

PhilippinesThe Central

bank-Roadmap

to Banking

Policy

(planning)

Latin

America

ColombiaBanking

Association

(Asobancaria) -

Green Protocol

BrazilCentral Bank’s Guidelines of

Social Responsibility Policy for

FIs

PeruPeru Superintendency of Banking

and Insurance (SBS) -Resolution

No. 1928-2015.

MexicoMexico Banking Association (ABM)

- Voluntary Green Protocol

(planning)

Africa

NigeriaCentral Bank of

Nigeria

-Nigerian

Sustainable

Banking Principles

& 3 Sector

Guidelines

KenyaThe Kenya Bankers Association

(KBA)-Sustainable Finance

Initiative (SFI)

SBN Members – Timeline of Initiatives

2011 2012 2013 2014 2015 2016

28

29 29

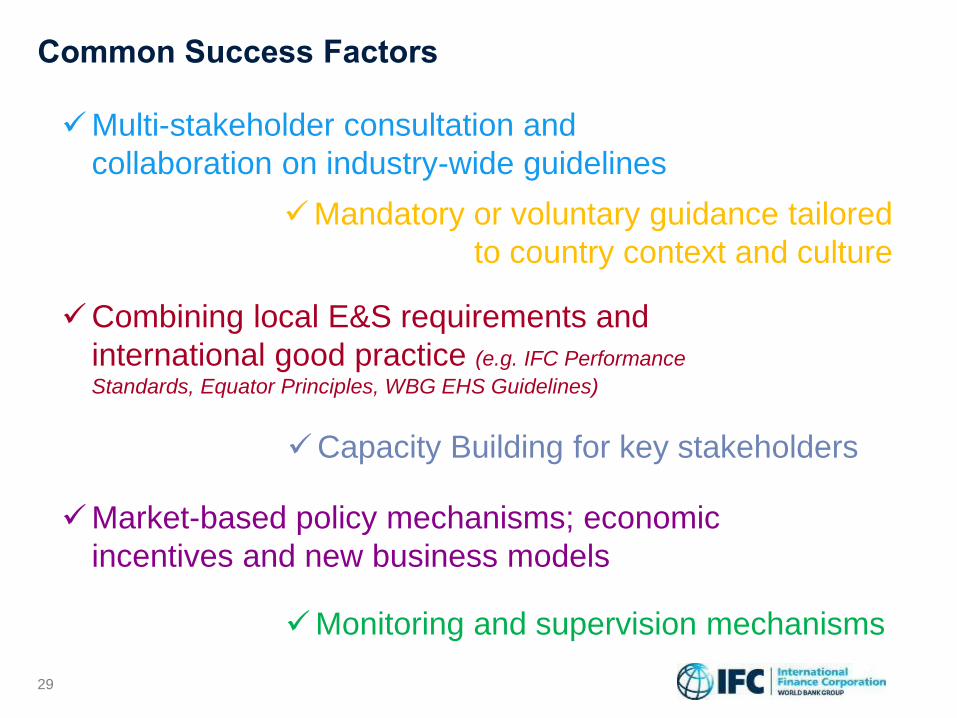

Common Success Factors

on industry-

wide

guidelines

guidance

based on

Multi-stakeholder consultation and

collaboration on industry-wide guidelines

Combining local E&S requirements and

international good practice (e.g. IFC Performance

Standards, Equator Principles, WBG EHS Guidelines)

Market-based policy mechanisms; economic

incentives and new business models

Mandatory or voluntary guidance tailored

to country context and culture

Capacity Building for key stakeholders

Monitoring and supervision mechanisms

30

Supports creation of a level playing field in line with international good practice

Removes impediments and strengthens the business case for sustainable

banking

Supports country-level frameworks

For Financial Institutions

SBN – Key Benefits

Access to global trends, knowledge, practical experiences and lessons learned

Support from IFC and other members when developing and implementing

effective E&S risk management standards and sustainable banking guidance

Platform for collaboration on a shared vision for sustainable banking

For Banking Regulators / Banking Associations

Supports capacity building of local service providers, such as training and

technical institutions, to assist FIs on E&S risk management

Encourages consideration of E&S regulations in financial sector due diligence

Supports national climate change and green growth agendas

For Local Markets

31

IFC Advisory Services ESRM for FIs Program

Policy/regulatory support to

develop E&S risk

management guidance

Awareness raising and

promotion

Direct technical support for

FIs through training and

consultancy services

Regulatory & market

environment

Training Partners

Consultants

Banking Associations

ESMS diagnostic reports

ESMS development

Individual FIs

IFC ESRM

Advisory

Service

Program

Regulatory and

Market Drivers

Market

Capacity

FIs Capacity

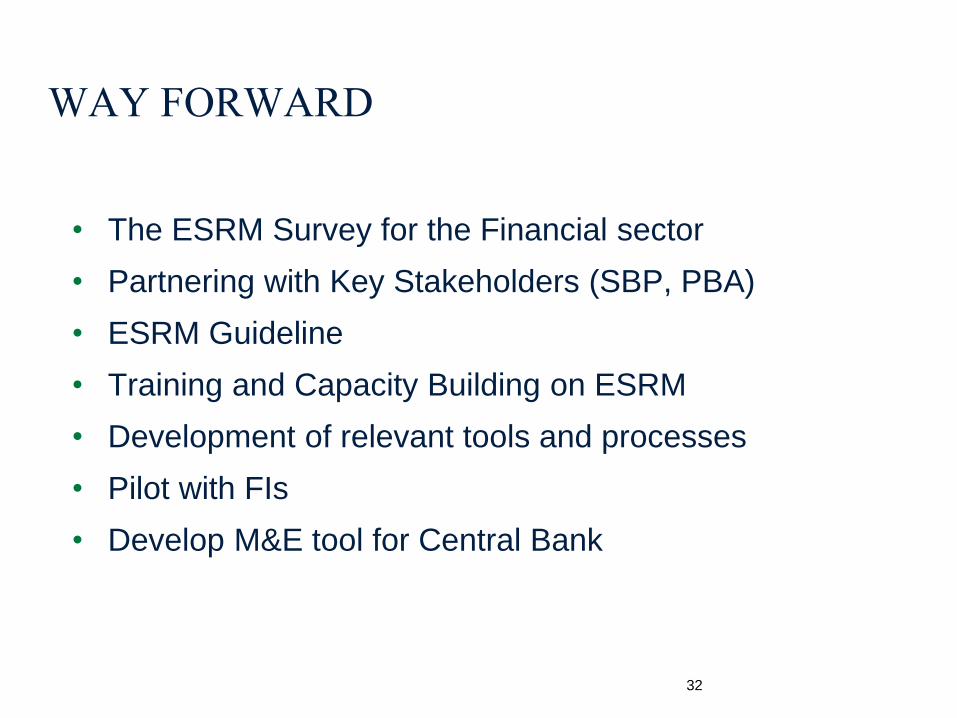

WAY FORWARD

• The ESRM Survey for the Financial sector

• Partnering with Key Stakeholders (SBP, PBA)

• ESRM Guideline

• Training and Capacity Building on ESRM

• Development of relevant tools and processes

• Pilot with FIs

• Develop M&E tool for Central Bank

32

More resources

SBN Website: http://firstforsustainability.org/sustainable-banking-network/

IFC Sustainability Framework and Advisory Services www.ifc.org/sustainability

CONTACTS

Name Title E-mail

Rong Zhang SBN Global Coordinator [email protected]

Atiyah Curmally ESRM AS Program Global Product Specialist [email protected]

Quyen Nguyen ESRM AS Program Manager [email protected]

Afifa Raihana Regional Specialist [email protected]

33