iew politics take centre stage 18 october 2016...the house view, 18 october 2016 – politics take...

TRANSCRIPT

Resea

rch

D

euts

che B

ank

The

House V

iew

Politics take centre stage

DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI(P) 057/04/2016

18 October 2016

Distributed on: 18/10/2016 04:10:00 GMT

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Month in Review

2

Reuters, 1st October 2016

FX Street, 7th October 2016

MarketWatch, 6th October 2016

Daily Mail, 5th October 2016

Seeking Alpha, 5th October 2016

IMF, 4th October 2016

Bloomberg, 29th September 2016

Bloomberg, 7th October 2016 Bloomberg, 7th October 2016

WSJ, 7th October 2016

WSJ, 5th October 2016

CNN, 7th October 2016

FT, 9th October 2016

Fortune, 21st September 2016

The Guardian 2nd October 2016

WSJ, 5th October 2016

The Week, 13th October 2016

The Local, 12h October 2016

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

The political calendar is filled with risk events over the next year. The US elections in

a few weeks are likely to yield a Clinton win and continued gridlock. Spain continues

without a government, but an end to the impasse could be nearing. In Italy, however,

the risk is rising that December’s Senate referendum will be rejected. In this case,

new elections, though unlikely, cannot be ruled out. Anti-EU parties might also make

gains in next year’s German and French elections. In the UK, the government’s hard-

line rhetoric and an uncompromising EU stance are paving the way for a hard Brexit.

On the macro front, global growth remains sluggish, although there have been some

signs of improvement. US growth is expected to pick up slightly but the eurozone is

yet to feel the full impact of Brexit. Importantly, political headwinds prevent necessary

structural reforms and limit meaningful fiscal stimulus programmes.

Meanwhile, there has been a chorus of calls for such responses from central

bankers, as incremental monetary easing is increasingly seen as less effective and

even counterproductive. We expect the ECB to extend its QE programme this year,

but the Fed is eager to raise rates before year-end, and the BoJ has taken measures

to stem the decline in long-end yields.

The ongoing policy rethink informs our market views. The sell-off in rates should be

sustained, and possibly extended next year. In FX, we are bullish the yen and the

dollar post election, and bearish the euro and sterling. We are cautious on US and

European equities. EM assets have performed well on the back of material inflows,

but we expect a short-term pause in these dynamics ahead of key risk events.

David Folkerts-Landau, Group Chief Economist

3

The House View, 18 October 2016 – Politics take centre stage

The views in this publication are informed by Deutsche Bank’s Global Strategy Group, which advises management and

clients on broad market risks and global economic and financial developments. The views and forecasts of the group,

which consists of senior research staff, may occasionally differ from those disseminated by their research colleagues

Editors: Marcos Arana, Aditya Bhave,

Matthew Luzzetti, Rajni Thakur

Table of contents

Introduction 4-boxes

Total returns

Macro

update

Global growth

Outlook for US, Europe,

and China

Monetary

policy

A new framework?

Outlook for ECB, BoJ and

Fed

Politics

US election

Brexit

European political risk

Markets

Summary of market views

Recent market drivers

FX, rates, EM, credit and

equity views

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Fed: November hike almost fully ruled out; expect hike

in December, and very cautious cycle thereafter

ECB: easing bias. 9-12 month QE extension in Dec.;

further deposit rate cuts unlikely. Taper talk unfounded

BoJ: introduced 10Y yield target. Additional easing

could involve rate cuts, but substantial cuts unlikely

BoE: aggressive easing post-Brexit may be premature.

Expect further rate cut around year-end if data weaken

PBoC: return to easing in H1-2017

EM: easing bias in Asia, CEEMEA (ex- South Africa).

LatAm picture less uniform

Sluggish global growth outlook. 2016 at 3.0%, slowest

pace post-crisis, rising modestly into 2017 to 3.4%

US growth subdued and well below recent years’ trend.

2016 at 1.3%, half the rate in 2015. Growth should rise

moderately in coming quarters

Downbeat view on eurozone recovery. Growth resilient

in 2016 at 1.6%, but set to slow in 2017 as Brexit adds

to existing downside risks

EM outlook similarly subdued, but signs of bottoming

across several major economies. Expect some

acceleration next year in LatAm and CEEMEA

Politics: taking centre stage, political uncertainty high

over next 12 months. US election unlikely to have

substantial impact on macro or markets

Policy rethink: increasing recognition of reduced impact

of additional monetary easing, but little to expect from

fiscal stimulus, structural reforms

Brexit: hard Brexit increasingly likely given tough UK

rhetoric that makes finding a compromise difficult. If /

when economic pain rises, positions may soften

European banks: underlying issue remains unresolved,

continues to be a source of downside risk for growth

Views on key themes

Economic outlook Central bank watch

Key downside risks to our view

Notes: H / M / L indicates estimated probability of risk (High, Medium, Low).

(*) Sharp deceleration in growth, e.g., growth falling below 5%

(**) Non-performing loans

4

Negative spillover from banking stress / political risk

escalation in Europe that derails recovery

China hard landing: sharp contraction that drags down

global growth, possibly due to deflating property bubble

Market corrections / volatility episodes, e.g., unexpect-

ed shock from US election, reassessment of Fed hikes

Corporate credit crisis and wave of defaults; rising

dollar, US rates put pressure on EM corporates and US

HY, especially energy sector

Sharper US slowdown than our below-consensus view

M

M

M

L

L

Global growth remains sluggish and is expected to improve only modestly in 2017. Political risk to remain high in next 12 months

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

42

16 16 15 11

9 6

-2 -5 -5

-11 -12 -19

14 8 7 6

11

5 5

16

4 1

-1

-17

38

32

20 18

-20

-10

0

10

20

30

40

50

Bra

zil

Bovespa

Russia

Mic

ex

MS

CI E

M

UK

FT

SE

100

Turk

ey B

IST

India

Nifty

US

S&

P 5

00

Germ

an D

AX

30

Euro

pe S

toxx 6

00

Spain

IB

EX

35

Japan N

ikkei

Shanghai C

om

posite

Italy

Mila

n

US

HY

US

IG

EU

R H

Y

EU

R IG

UK

Germ

any

US

JP

Y

EM

FX

EU

R

Dolla

r In

dex

GB

P

Bre

nt O

il

Iron O

re

BB

G C

mdty

Index

Gold

Since Fed / BoJ meeting (21 Sept)

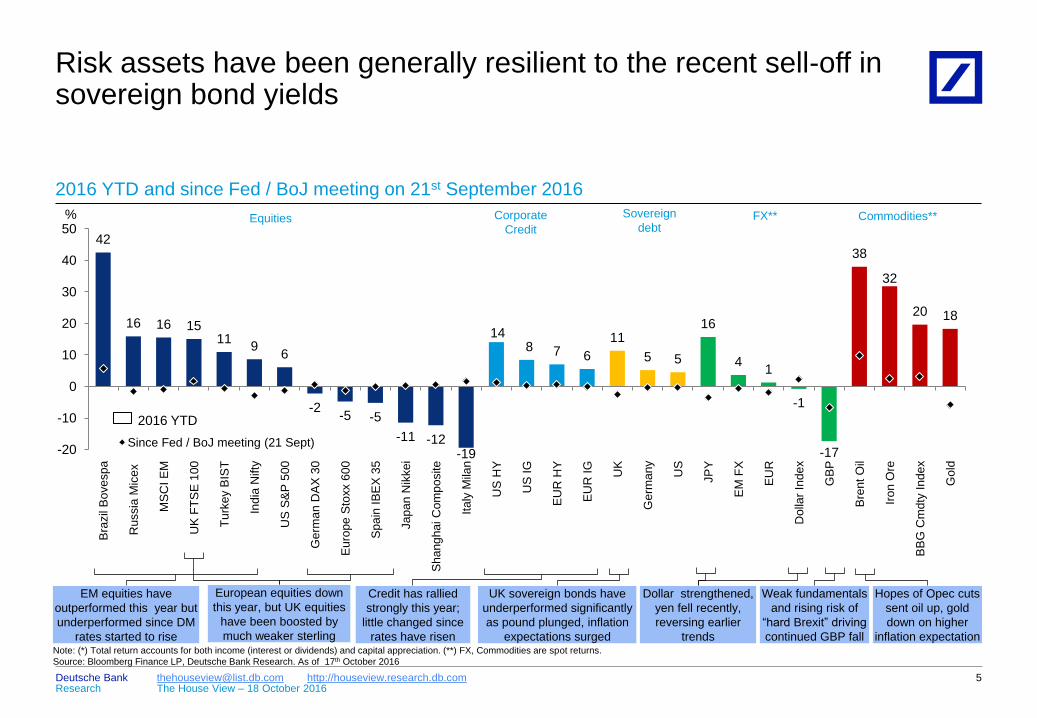

2016 YTD and since Fed / BoJ meeting on 21st September 2016

% Equities Commodities** FX** Sovereign

debt Corporate

Credit

2016 YTD

5

Note: (*) Total return accounts for both income (interest or dividends) and capital appreciation. (**) FX, Commodities are spot returns.

Source: Bloomberg Finance LP, Deutsche Bank Research. As of 17th October 2016

Hopes of Opec cuts

sent oil up, gold

down on higher

inflation expectation

Credit has rallied

strongly this year;

little changed since

rates have risen

European equities down

this year, but UK equities

have been boosted by

much weaker sterling

Weak fundamentals

and rising risk of

“hard Brexit” driving

continued GBP fall

UK sovereign bonds have

underperformed significantly

as pound plunged, inflation

expectations surged

Dollar strengthened,

yen fell recently,

reversing earlier

trends

EM equities have

outperformed this year but

underperformed since DM

rates started to rise

Risk assets have been generally resilient to the recent sell-off in sovereign bond yields

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

After slowing sharply in 2015 and

early-2016, global growth mom-

entum has picked up recently,

though it remains subdued

− Acceleration more evident in

manufacturing than services

− Global manufacturing PMI

highest level since mid-2015

over past 3 months

The breadth of the improvement

has been impressive…

− Number of countries with dec-

lining PMIs lowest in 3 years

…With EM accelerating most

rapidly…

− EM composite PMI up two

points over past year

…But momentum has also picked

up modestly across DM

− Manufacturing trend moved

higher across US, Eurozone,

Japan and UK

50

51

52

53

2013 2014 2015 2016

Global manufacturing momentum has

improved in recent months

Global manufacturing PMI, 3m MA

48

50

52

54

56

58

2013 2014 2015 2016

Momentum has improved everywhere but EM

economies have accelerated more rapidly

Composite PMI, 3m MA

DM

EM

Global growth momentum picked up modestly in recent months but remains subdued

6

47

49

51

53

UK Euro- zone

US* China Japan

Avg. Jan-Jun Avg. Jul-Sep

Manufacturing PMIs have improved broadly

relative to H1 2016

Index

5

10

15

20

25

2013 2014 2015 2016

Breadth of improvement impressive, with

limited countries experiencing falling PMIs

# countries with declining

manufacturing PMIs, 2m MA

Number of declining

PMIs lowest since 2013

Note: (*) ISM. Source: Markit, ISM, Haver Analytics, Bloomberg Finance LP, Deutsche Bank Research

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

0

1

2

3

4

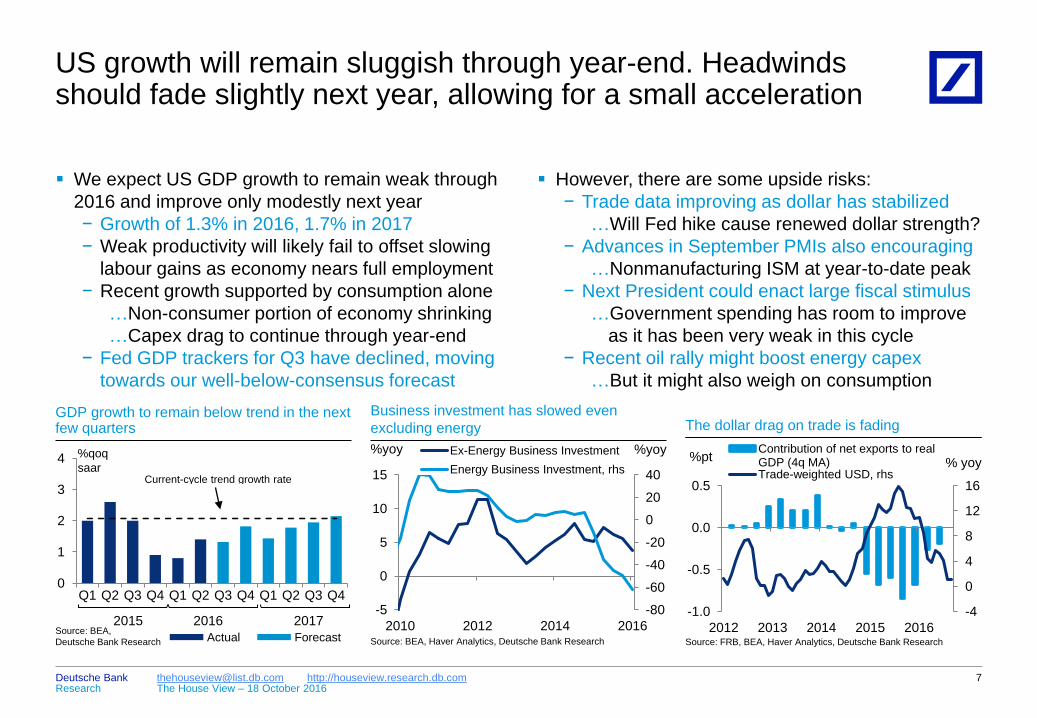

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Actual Forecast

%qoq

saar

2015 2016

GDP growth to remain below trend in the next few quarters

Source: BEA,

Deutsche Bank Research

Current-cycle trend growth rate

2017

US growth will remain sluggish through year-end. Headwinds should fade slightly next year, allowing for a small acceleration

-80

-60

-40

-20

0

20

40

-5

0

5

10

15

2010 2012 2014 2016

Ex-Energy Business Investment

Energy Business Investment, rhs

Business investment has slowed even

excluding energy

%yoy

Source: BEA, Haver Analytics, Deutsche Bank Research

%yoy

-4

0

4

8

12

16

-1.0

-0.5

0.0

0.5

2012 2013 2014 2015 2016

Contribution of net exports to real GDP (4q MA) Trade-weighted USD, rhs

Source: FRB, BEA, Haver Analytics, Deutsche Bank Research

%pt % yoy

The dollar drag on trade is fading

However, there are some upside risks:

− Trade data improving as dollar has stabilized

…Will Fed hike cause renewed dollar strength?

− Advances in September PMIs also encouraging

…Nonmanufacturing ISM at year-to-date peak

− Next President could enact large fiscal stimulus

…Government spending has room to improve

as it has been very weak in this cycle

− Recent oil rally might boost energy capex

…But it might also weigh on consumption

We expect US GDP growth to remain weak through

2016 and improve only modestly next year

− Growth of 1.3% in 2016, 1.7% in 2017

− Weak productivity will likely fail to offset slowing

labour gains as economy nears full employment

− Recent growth supported by consumption alone

…Non-consumer portion of economy shrinking

…Capex drag to continue through year-end

− Fed GDP trackers for Q3 have declined, moving

towards our well-below-consensus forecast

7

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Eurozone growth slow but stable at 1.2-1.5% over

the last couple of years despite many shocks...

− Latest data point to Q3 growth around this level

...But the recovery is vulnerable

− Cyclical picture weak – rising oil prices, euro not

depreciating as was expected, fiscal policy likely

to be less supportive in 2017

− Structural issues of high debt, low growth, low

competitiveness still unresolved

− Political event risk high in 5 largest economies

We forecast growth of just 1.1% in 2017, down from

1.6% this year – but risks tilted to the downside

− Persistent policy uncertainty (political, fiscal,

monetary) could weigh further on investment

and growth, and keep productivity low

− With banking sector issues unresolved, credit

growth could stall and hurt domestic demand

…Consensus growth forecasts need an

ambitious 3-4% credit growth in 2017

…Latest credit data suggest slower growth

− Brexit impact still to be felt

Our macro view on the eurozone remains unchanged: growth has been resilient, but risks are tilted to the downside

8

-10

-8

-6

-4

-2

0

2

4

6

2005 2007 2009 2011 2013 2015

Credit impulse, % of GDP

Private domestic demand, % yoy

Credit impulse still positive but slower, pointing to domestic demand

growth of 1.5% yoy by early 2017, down from 2% in recent quarters

Focus Europe-European Quarterly Update:30 September 2016

Euro PMIs: confirming slower momentum - 5 October 2016

-3

-2

-1

0

1

2

3

50 100 150 200 250 300

Persistent high uncertainty could weigh on investment spending

EU economic policy uncertainty index

Note: (*) 4q lag. Source: Eurostat, www.policyuncertainty.com, Deutsche Bank Research

Eu

rozone in

ve

stm

ent, %

qo

q*

Sovereign crisis Post-Lehman

Note: (*) Credit impulse: Deutsche Bank’s non-consensus view is that it is not credit growth but rather the

change in credit growth that is important for domestic demand growth. A slowdown in the pace of

deleveraging boosts spending growth, even if credit growth may still be negative

Source: ECB, Eurostat, Haver Analytics, Deutsche Bank Research

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

With China’s economy in the middle of a structural

growth slowdown, concerns about a credit-fuelled

property bubble have intensified

− Property prices are up sharply on ballooning

mortgage debt

− Developers could face steep losses if price rises

slow after paying high land auction premiums

Near-term, strong property sector should slightly

boost growth...

− Pressure on FX, capital controls, outflows could

be partly relieved by better near-term growth

…And lower likelihood of imminent policy easing

− Government has actually tightened credit supply

to developers to contain bubble

− Interest rate cut possible in Q2 2017 if property

sector begins to cool

A deflating property bubble poses material

downside risk to the economy

− Growth likely to slow to 6.2% in Q1 2017

− 2018 GDP growth forecast cut by 0.5pp to 6%

− Outflow pressures to intensify: FX reserves to

fall below $3tn; RMB weaken to 7.4 by end-17

0

20

40

60

15

20

25

30

2010 2011 2012 2013 2014 2015 2016

Broad credit growth (avg. of previous 2 Qs)

Land auction premium (avg. of current and next Q, rhs)

Surge in broad credit growth has fuelled property bubble

Source: CREIS, WIND, Deutsche Bank Research

%yoy

Correlation 0.86

%

In China, a rising property bubble could modestly boost near-term growth but raises risks into 2017 and 2018

9 China’s property bubble – 28-Sep-2016

17.8 24.7

19.5 16.2 25.3 22.8 26

34.8

71.2

0

20

40

60

80

2009 2010 2011 2012 2013 2014 2015 2016 H1

2016 Jul-Aug

Mortgage share of total new RMB loans

Mortgage share of total loans more than doubled in recent months

%

Source: WIND, Deutsche Bank Research

China’s property bubble II: Government tightens developers financing – 13-Oct-2016

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Years of ultra-loose monetary policy have failed to

reignite growth and raise inflation across DM

− Monetary policy can address cyclical issues but

not structural ones

− Easing was effective initially, when rates, risk

premia were high – but this is no longer the case

− Political constraints leaving central banks’ calls

for structural reform, fiscal stimulus unanswered

Additional material easing increasingly seen as

ineffective and even counterproductive...

− Inflation expectations have risen but remain low

− Euro, yen ‘not responding’ to additional easing

− Hunt for yield continues to distort asset prices

...with even ECB, BoJ taking a pause

− While defending policy to date, both CBs

acknowledged negative impact of their policies

(especially flat yield curves) on banks, insurers

Monetary policy to remain very accommodative, but

focus shifting away from rate cuts, flat yield curves

− Expect little in terms of fiscal easing

After years of extreme accommodation, we are going through a monetary policy rethink

10 The House View - Infographic: Change in the policy mix - 14 September 2016

0

10

20

30

40

50

50

60

70

80

90

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Germany

Japan (rhs)

Central banks increasingly wary of impact of monetary policy on

banks, insurers. Focus shifting away from flat yield curves

bps

Source: Bloomberg Finance LP, Deutsche Bank Research

bps

Steepening of

yield curves

BoJ meeting

“[T]he stimulus provided by lowering interest rates (...) would of course be

much weaker. (…) [E]xtended use of unconventional measures could

come with rising side effects, for instance on financial stability, financial

intermediation and international spillovers.”

Benoit Coeure, ECB board member, Jackson Hole speech, Aug-2016

“[T]he significant fall in lending rates [following the introduction of negative

interest rates] (…) has been achieved at the expense of financial

institutions' profits.”

Haruhiko Kuroda, Governor of the BoJ, Kisaragi-kai speech, Sep-2016

ECB, BoJ conscious of diminishing returns of policy easing, impact

on financial firms’ profitability

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

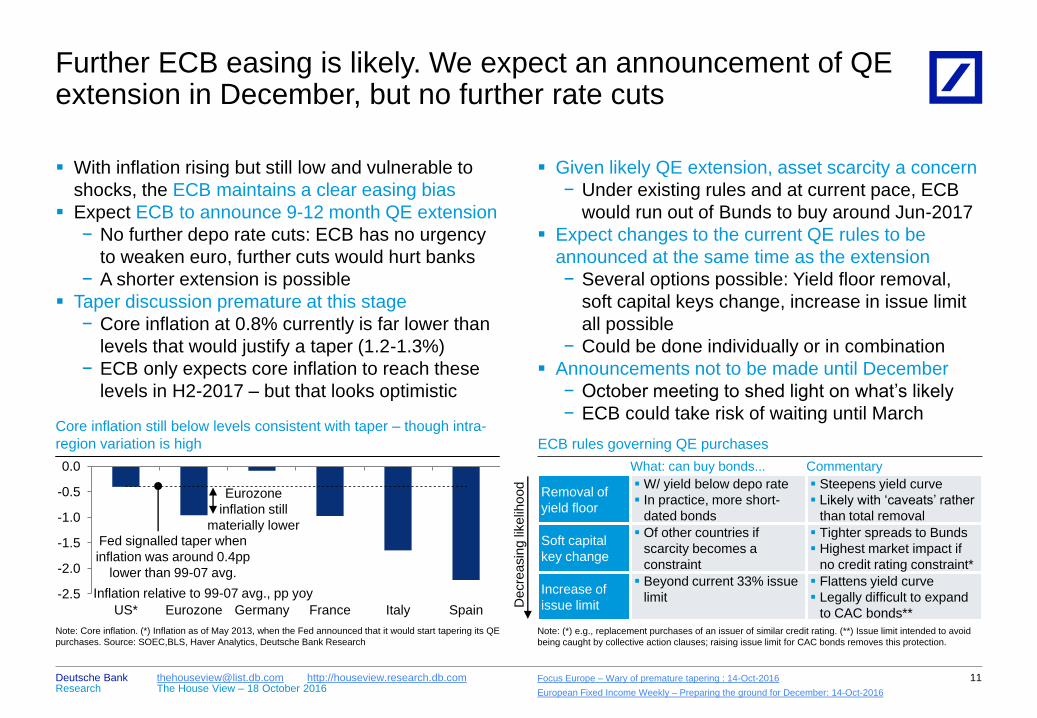

Given likely QE extension, asset scarcity a concern

− Under existing rules and at current pace, ECB

would run out of Bunds to buy around Jun-2017

Expect changes to the current QE rules to be

announced at the same time as the extension

− Several options possible: Yield floor removal,

soft capital keys change, increase in issue limit

all possible

− Could be done individually or in combination

Announcements not to be made until December

− October meeting to shed light on what’s likely

− ECB could take risk of waiting until March

Further ECB easing is likely. We expect an announcement of QE extension in December, but no further rate cuts

11 Focus Europe – Wary of premature tapering : 14-Oct-2016

European Fixed Income Weekly – Preparing the ground for December: 14-Oct-2016

With inflation rising but still low and vulnerable to

shocks, the ECB maintains a clear easing bias

Expect ECB to announce 9-12 month QE extension

− No further depo rate cuts: ECB has no urgency

to weaken euro, further cuts would hurt banks

− A shorter extension is possible

Taper discussion premature at this stage

− Core inflation at 0.8% currently is far lower than

levels that would justify a taper (1.2-1.3%)

− ECB only expects core inflation to reach these

levels in H2-2017 – but that looks optimistic

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

US* Eurozone Germany France Italy Spain

Note: Core inflation. (*) Inflation as of May 2013, when the Fed announced that it would start tapering its QE

purchases. Source: SOEC,BLS, Haver Analytics, Deutsche Bank Research

Core inflation still below levels consistent with taper – though intra-

region variation is high

Inflation relative to 99-07 avg., pp yoy

Fed signalled taper when

inflation was around 0.4pp

lower than 99-07 avg.

Eurozone

inflation still

materially lower

ECB rules governing QE purchases

What: can buy bonds... Commentary

Removal of

yield floor

W/ yield below depo rate

In practice, more short-

dated bonds

Steepens yield curve

Likely with ‘caveats’ rather

than total removal

Soft capital

key change

Of other countries if

scarcity becomes a

constraint

Tighter spreads to Bunds

Highest market impact if

no credit rating constraint*

Increase of

issue limit

Beyond current 33% issue

limit

Flattens yield curve

Legally difficult to expand

to CAC bonds**

Note: (*) e.g., replacement purchases of an issuer of similar credit rating. (**) Issue limit intended to avoid

being caught by collective action clauses; raising issue limit for CAC bonds removes this protection.

De

cre

asin

g li

ke

liho

od

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

The BoJ announced a new monetary policy

framework at its September meeting

− Introduced target 10-year JGB yield around 0%,

in part to keep yield curve steeper

− Abandoned monetary base growth target

− Kept short-term policy rate unchanged at -0.1%

Re-think comes as BoJ struggles to raise inflation

While details of the new regime are still uncertain, it

will likely lead to a de facto tapering of QE

− Higher long yields require a reduction in duration

of purchases (i.e. shift from long- to short-term

bonds) or slower balance sheet growth

Policy risks being pro-cyclical: positive shocks that

raise long-term yields would require more BoJ

purchases to hit yield target (and vice versa)

Looking ahead, further near-term easing is unlikely,

as BoJ gauges impact of new framework

− Significant exogenous shock (e.g., sharp yen

appreciation) likely required for new action

If it occurs, additional easing would likely take form

of cuts to the policy rate and 10-year yield target

-0.4

-0.2

0.0

0.2

0.4

Oct-15 Jan-16 Apr-16 Jul-16 Oct-16

JGB 10 year yield

Bank of Japan’s 0% target for 10-year yields is above current levels

%

Source: Bloomberg Finance LP, Deutsche Bank Research

The BoJ’s new yield curve targeting framework is likely to lead to a de facto tapering; further easing is unlikely near-term

12

0 10 20 30 40 50

Japan US Eurozone

BoJ holds greater share of outstanding government debt than peers

% of central government debt held by central bank

Source: ECB, BOJ, FRB, Treasury, Haver Analytics, Deutsche Bank Research

0%

target

revealed

Japan Monetary Policy Watch- Effect of BoJ's JGB purchasing: Stock view vs. flow view : 5 October 2016

Japan Monetary Policy Watch - Can the Bank of Japan control the yield curve? : 19 September 2016

-1

0

1

2

2012 2013 2014 2015 2016 2017 2018

CPI Core CPI Core Core

Inflation in Japan is expected to remain stuck well below target over

at least the next several years

%yoy

Note: Core inflation excludes fresh food. Core-core inflation excludes food, beverages and energy.

Source: Cabinet Office of Japan, MIC, Haver Analytics, Deutsche Bank Research

Inflation target

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

We maintain our long-held view that the next rate

increase will be in December

− The markets are pricing a ~65% chance of a

rate hike by yearend

Markets expecting about 2 cumulative hikes

through 2018, likely due to recession risk

− In addition to a December rate increase, we

forecast 2 hikes each in 2017 and 2018

− However, some inflation metrics suggest the

Fed might have to hike at a faster pace

Most FOMC participants want to raise rates in 2016

− Only 3 of 17 participants want to remain on hold

until next year

November rate hike not expected

− Markets pricing only ~20% rate-hike probability:

with meeting only six days before US Election,

risk of severe market reaction is elevated

− Data not so strong as to force Fed’s hand

− Instead, November statement likely to strongly

signal a December move

As for the Fed, a November hike is almost completely ruled out, while a December hike is “just right”

13

0

1

2

3

4 FOMC projections

Median projections

OIS

The Fed is looking to hike once this year and then at a much faster

pace than the market is pricing

%

Source: FRB, Bloomberg Finance LP, Deutsche Bank Research

2016 2017 2018 2019 Longer run 0.5

1.0

1.5

2.0

2.5

3.0

3.5

2006 2008 2010 2012 2014 2016

Atlanta Fed core Sticky CPI FRB Cleveland Median CPI Core CPI Core PCE

While the core PCE is subdued, other metrics suggest a more robust

increase in inflation

%yoy

Source: BEA, BLS, FRBCLE, FRBATL, Haver Analytics, Deutsche Bank Research

US inflation rising across several

metrics

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Possible government outcomes: a divided government most likely

Senate

White House

Democrat Republican

Divided

government

Narrow Senate

control

Divided

government

No Senate control

Unlikely: Trump

win only if strong

Republican vote

Most likely chance

of unified

government

Most forecasts show a widening lead for Clinton in

the presidential race – likelihood higher than 4 to 1

− Note that lead in popular vote is only around 5pp

Both candidates promise higher fiscal spending – a

marginal positive for growth, but no game changer

Beyond agreement on headline fiscal stimulus, the

policy platforms are starkly opposed

The race for the Senate is less clear-cut, but

likelihood also favour the Democrats

With the Republicans favoured to retain the House,

another divided government is most likely – pointing

to continued political gridlock

A Clinton win appears increasingly likely in the US. Base case is a divided government, but a Democratic sweep is possible

14

The House View Special: US election: Policy continuity or paradigm shift – 4-Oct-2016

But a Democratic sweep cannot be excluded

− Likelihood of Democrats winning both Senate

and House have risen

This scenario or a Trump win are not priced and

would have significant market repercussions

− Trump win signals policy change

− Democratic sweep means most extreme Clinton

policy measures, e.g., on tax, become likely

− Higher volatility across asset classes

Weakest Administration Strongest Administration

Increasing

likelihood

Note: Scenarios sorted anti-clockwise by increasing order of likelihood, from bottom left (least likely).

Source: Wikipedia, Deutsche Bank

0

25

50

75

100

June July August September October November Notes: Net Clinton lead = probability of Clinton win minus probability of Trump win

Source: FiveThirtyEight Polls plus forecast, Iowa Electronic Markets, Deutsche Bank Research

Clinton’s lead has widened materially over the last month. Likelihood

of Democrats winning both Senate and House have also risen

% Election Day

8-November

Net Clinton

lead

Democrat

Congress

Presidential

debates

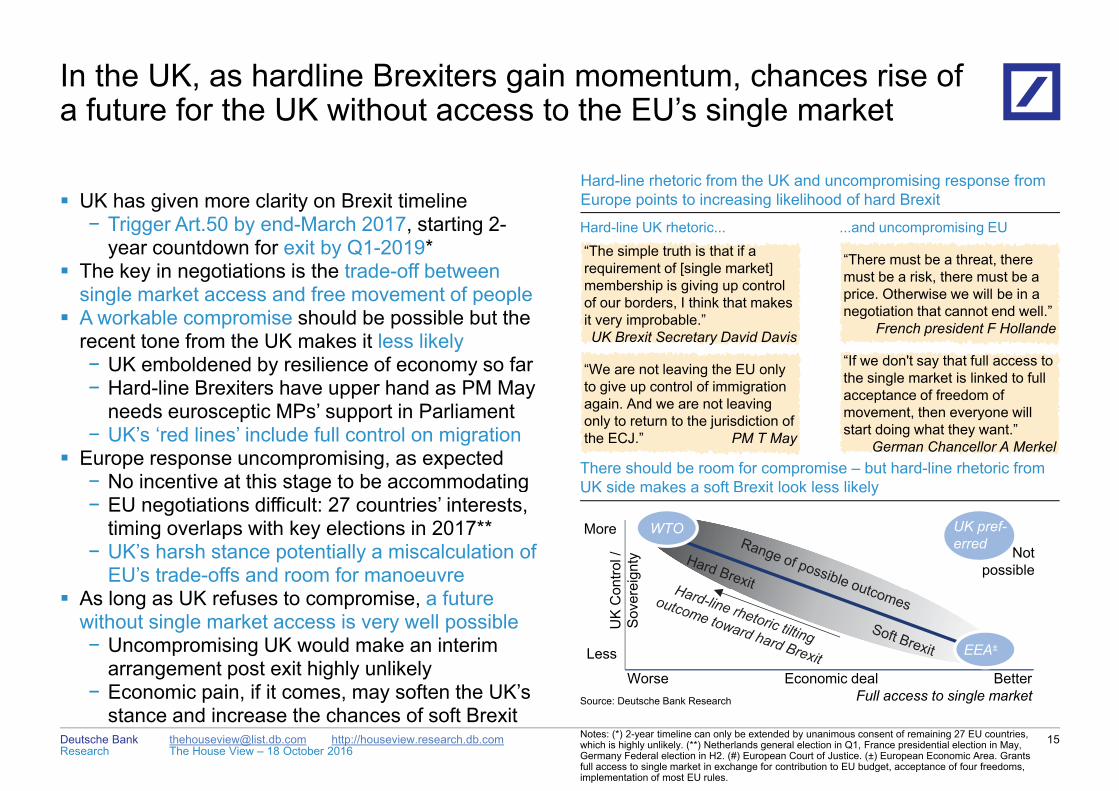

In the UK, as hardline Brexiters gain momentum, chances rise of a future for the UK without access to the EU’s single market

UK has given more clarity on Brexit timeline

a future for the UK without access to the EU’s single market

Hard-line rhetoric from the UK and uncompromising response from Europe points to increasing likelihood of hard Brexit UK has given more clarity on Brexit timeline

− Trigger Art.50 by end-March 2017, starting 2-year countdown for exit by Q1-2019*

The key in negotiations is the trade-off between single market access and free movement of people

“There must be a threat, there must be a risk, there must be a price. Otherwise we will be in a

“The simple truth is that if a requirement of [single market] membership is giving up control f b d I thi k th t k

Europe points to increasing likelihood of hard Brexit

Hard-line UK rhetoric... ...and uncompromising EU

single market access and free movement of people A workable compromise should be possible but the

recent tone from the UK makes it less likely− UK emboldened by resilience of economy so far− Hard-line Brexiters have upper hand as PM May

“We are not leaving the EU only to give up control of immigration

price. Otherwise we will be in a negotiation that cannot end well.”

French president F Hollande

of our borders, I think that makes it very improbable.”UK Brexit Secretary David Davis

“If we don't say that full access to the single market is linked to full acceptance of freedom ofpp y

needs eurosceptic MPs’ support in Parliament− UK’s ‘red lines’ include full control on migration

Europe response uncompromising, as expected− No incentive at this stage to be accommodating

again. And we are not leaving only to return to the jurisdiction of the ECJ.” PM T May

There should be room for compromise – but hard-line rhetoric from UK side makes a soft Brexit look less likely

acceptance of freedom of movement, then everyone will start doing what they want.”

German Chancellor A Merkel

g g− EU negotiations difficult: 27 countries’ interests,

timing overlaps with key elections in 2017**− UK’s harsh stance potentially a miscalculation of

EU’s trade-offs and room for manoeuvre

U s de a es a so t e t oo ess e y

More

ontro

l /

eign

ty

WTO UK pref-erred Not

possible

As long as UK refuses to compromise, a future without single market access is very well possible− Uncompromising UK would make an interim

arrangement post exit highly unlikelyE i i if it ft th UK’

Economic dealWorse

Less

UK

Co

Sov

ere

EEA±

Better

ResearchDeutsche Bank

The House View – 18 October [email protected] http://houseview.research.db.com

− Economic pain, if it comes, may soften the UK’s stance and increase the chances of soft Brexit

15Notes: (*) 2-year timeline can only be extended by unanimous consent of remaining 27 EU countries, which is highly unlikely. (**) Netherlands general election in Q1, France presidential election in May, Germany Federal election in H2. (#) European Court of Justice. (±) European Economic Area. Grants full access to single market in exchange for contribution to EU budget, acceptance of four freedoms, implementation of most EU rules.

Source: Deutsche Bank Research Full access to single market

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Italy’s Senate referendum on 4-Dec intended to improve governability*

Vote now partly about PM Renzi Approval of Senate reform is best

case scenario, but it is no panacea Rejection negative but not neces-

sarily means new election – even if tail risk would weigh on sentiment

Outcome of vote too close to call but risk of rejection rising

Overall risk exacerbated by fact that key challenges of low growth, bank concerns will remain

Spain has been under a caretaker

government since Dec-2015

− Two elections have not yielded

a workable Parliament majority

Deadline for new government is 31-

Oct, otherwise election triggered

But chance of ending deadlock

− Interim PM Rajoy of PP # needs

to win a confidence vote

− Resignation of PSOE # leader

opens door for party to abstain

from confidence vote – allowing

a minority PP government

− Polls suggest PSOE has little to

gain from a third election

New election not necessarily a bad

outcome

− Polls point to potential PP,

Citizens centre-right majority

− Alternative is continued gridlock

– but risk of anti-establishment

or eurosceptic government low

21-Oct DBRS rating review could

cost Portugal IG rating, making it

ineligible for ECB QE purchases

− Portugal already rated junk by

S&P, Moody’s, Fitch

− Base case is no downgrade

Political situation less unstable, but

outlook for fiscal consolidation,

reform remains weak

Aid programme reviews, fund dis-

bursements delayed and likely to

drag well into 2017

Debt relief negotiations not

advanced, and election calendar

makes negotiations difficult

Risk that IMF exits programme

− IMF participation, a must for

Germany, conditional on debt

relief, fiscal sustainability

Political risk in Europe remains high and could derail the recovery – especially in Italy

16

Tail risk of credit downgrade Possible end to deadlock Senate referendum tail risk

IMF participation at risk

Note: (*) Proposal to narrow Senate’s role in favour of Lower House, reducing chance of political gridlock. (**) Euro-

sceptic, anti-establishment 5 Star Movement. (±) Binding referendum not allowed by law, but could hold a consultative,

non-binding referendum. (#) PP is centre-right incumbent Partido Popular; PSOE is main opposition socialist party

Italy: Key recent developments – 29-Sep-2016

Range of outcomes in Italy

Approved Rejected,

new gvmt.

Rejected,

new election

Govm’t. Renzi

continues

Interim,

maybe Renzi

Risk of

5SM**

Govm’t.

scope As is

Limited to

electoral law As is

Next

election Q2-2018 Mid-2017 Q1-2017

Reform

outlook

No major

new reform

Electoral law

only

Reform

reversal risk

EU /

euro n/a n/a

Risk of euro

referendum± Decreasing market

friendliness

Spain: Decision time – 2-Oct-2016

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com 17

Summary of market views

Asset View Rationale

Markets Cautious on risk

assets Overall cautious stance on risk assets, even though benign backdrop can

last a little longer with DM central bank policy remaining accommodative

Equities

Cautious stance

US, Europe: no

upside into year-end

US: risk of pullback; index within 3% of historic high despite macro and

political uncertainty, weak earnings outlook

Europe: downside into year-end on macro, political risks and bank concerns

Rates

DM sell-off likely

sustainable

Neutral on Bunds,

USTs into year-end

Increase in inflation expectations makes DM rates sell-off more sustainable

as it is bullish risk assets

Shift by BoJ, ECB to lift US long-end further in 2017 via higher term premia

Bunds little changed: QE extension could affect slope of yield curve

FX

Near-term neutral

USD Uncertainty ahead of election limits near-term strength

Dollar strength should then resume as market prices Fed hikes

Bearish sterling Rising risks of “hard” Brexit add to already-weak fundamentals

Bearish euro Weaker on persistent outflows but near-term risk of remaining range-bound

Bullish yen BoJ 10Y target risks stronger yen if financial conditions tighten

Credit

US: wider spreads Wider spreads into year-end. HY looks relatively rich; IG to outperform

Europe: slightly less

supportive technicals Technicals supportive but have become slightly less so. Expect financials to

non-financials differential to compress

EM

Strong inflows vs.

little improvement in

fundamentals

EM has benefited from substantial relocation of capital away from core

markets, even though EM macro outlook has not improved materially

More cautious stance into November as inflows could slow ahead of risk

events (e.g., US election). Positive trend to resume as uncertainty eases

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

The bond market sell-off on the back of the oil rally, a hawkish Fed have driven markets. Hard Brexit fears sent pound tumbling

18

20

30

40

50

60

Oct-15 Jan-16 Apr-16 Jul-16 Oct-16

Sharp rally in oil to highest level in a year...

Brent crude price, $ / barrel

Sharp rally in oil on

OPEC freeze talks

OPEC freeze

0%

5%

10%

15%

20%

0%

20%

40%

60%

80%

100%

Jun-16 Aug-16 Oct-16

Oil price factor* QE factor* (rs)

...making oil again the key driver for markets

Note: (*) Data show % of variation in 14 total returns series explained by a given factor. (**) Derived from 5y5y inflation swaps. Source: Bloomberg Finance LP, Deutsche Bank Research

92

94

96

98

100 25

30

35

40

45

50

55

60

Jan-16 Mar-16 May-16 Jul-16 Sep-16

Brent Oil

Trade weighted Dollar (inverted, rhs)

Dollar- oil price relationship shifting

$/bbl

1.20

1.25

1.30

1.35 2.75

3.00

3.25

3.50

3.75

Jun-16 Aug-16 Oct-16

Inflation expectations** GBPUSD (rs, inverted)

Hard Brexit sent pound tumbling, UK inflation

expectations soaring

%yoy

0

20

40

60

80

Jun-16 Aug-16 Oct-16

Hawkish Fed signals raised likelihood of Dec

hike

Prob. of Fed rate hike by Dec-2016 (%)

0.00

0.05

0.10

0.15

0.20

US Eurozone

Inflation expectations**

10y yields

Higher oil led to a rise in inflation

expectations, and nominal bond yields

pp change

since OPEC

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

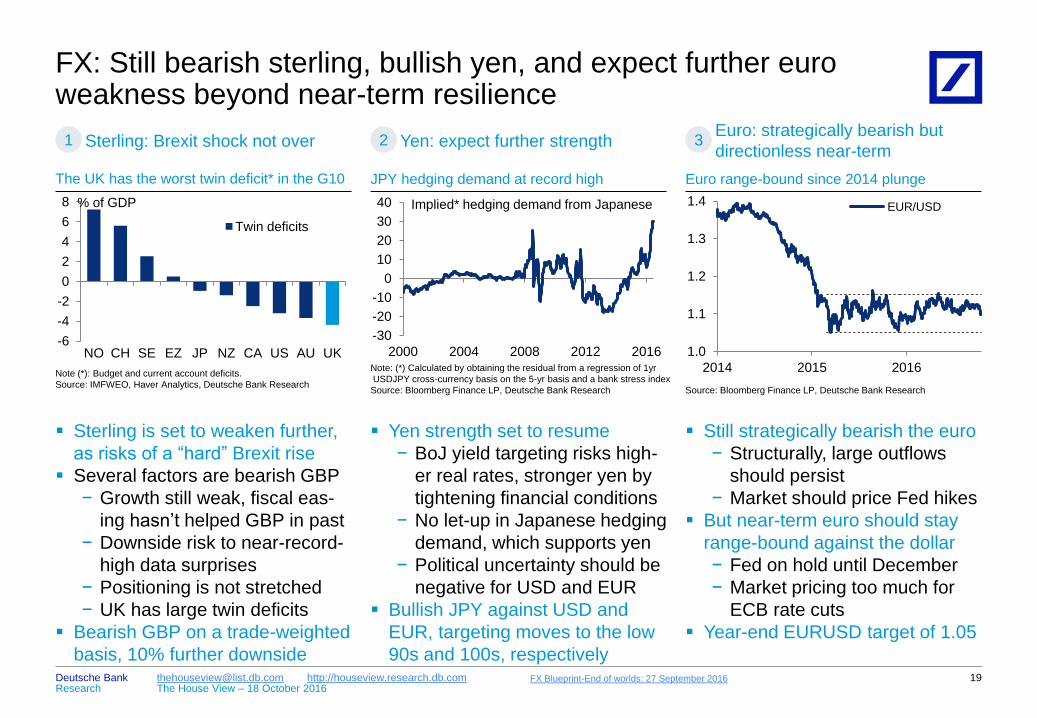

Sterling is set to weaken further,

as risks of a “hard” Brexit rise

Several factors are bearish GBP

− Growth still weak, fiscal eas-

ing hasn’t helped GBP in past

− Downside risk to near-record-

high data surprises

− Positioning is not stretched

− UK has large twin deficits

Bearish GBP on a trade-weighted

basis, 10% further downside

Still strategically bearish the euro

− Structurally, large outflows

should persist

− Market should price Fed hikes

But near-term euro should stay

range-bound against the dollar

− Fed on hold until December

− Market pricing too much for

ECB rate cuts

Year-end EURUSD target of 1.05

FX: Still bearish sterling, bullish yen, and expect further euro weakness beyond near-term resilience

19

Yen strength set to resume

− BoJ yield targeting risks high-

er real rates, stronger yen by

tightening financial conditions

− No let-up in Japanese hedging

demand, which supports yen

− Political uncertainty should be

negative for USD and EUR

Bullish JPY against USD and

EUR, targeting moves to the low

90s and 100s, respectively

-6

-4

-2

0

2

4

6

8

NO CH SE EZ JP NZ CA US AU UK

Twin deficits

The UK has the worst twin deficit* in the G10

% of GDP

Note (*): Budget and current account deficits.

Source: IMFWEO, Haver Analytics, Deutsche Bank Research

1.0

1.1

1.2

1.3

1.4

2014 2015 2016

EUR/USD

Source: Bloomberg Finance LP, Deutsche Bank Research

Euro range-bound since 2014 plunge

1 Sterling: Brexit shock not over 2 Yen: expect further strength 3 Euro: strategically bearish but

directionless near-term

-30

-20

-10

0

10

20

30

40

2000 2004 2008 2012 2016 Note: (*) Calculated by obtaining the residual from a regression of 1yr

USDJPY cross-currency basis on the 5-yr basis and a bank stress index

Source: Bloomberg Finance LP, Deutsche Bank Research

JPY hedging demand at record high

Implied* hedging demand from Japanese

FX Blueprint-End of worlds: 27 September 2016

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

DM long-end rates have sold off substantially since

late September, with curves steepening

− E.g., since September 28, 10Y Treasury yield up

19 bps and 10Y Bund yield up 20 bps

− ECB, BoJ moves have mitigated hunt for yield

− As a result, downward pressure on US term

premium has eased

− US short-end also up due to expected Fed hike

Sell-off in Treasuries, Bunds due in roughly equal

parts to real rates and breakevens – increase in

latter more sustainable as it is bullish for risk assets

We have raised our US yield forecasts:

− 10Y yield to remain near current levels through

year-end, rise to 2.0% next year

We are roughly neutral on Bund yields for this year

− 10Y yield to increase to 0.25% by year-end 2017

UK yields have increased even more dramatically

− Real yields up slightly this month after collapsing

post-Brexit

− Breakevens have soared due to GBP weakness

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

2.0

2.2

2.4

2.6

2.8

3.0

3.2

Jan-16 Apr-16 Jul-16 Oct-16

10y breakeven inflation 10Y real yield

UK breakeven inflation has spiked; real yields plummeted post

Brexit but are little changed in recent months

%

Source: Bloomberg Finance LP, Deutsche Bank Research

Rates: DM yields expected to hold steady in 2016, sell-off moderately further in 2017

20

12 11

7 9

0

2

4

6

8

10

12

14

16

US Germany

10y breakeven inflation 10y real yield

The rise in breakeven inflation makes the DM rates sell-off more

sustainable

bps, change since 28th Sep

Source: Bloomberg Finance LP, Deutsche Bank Research

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Expect short-term pause in inflows as key risk

events approach (US election, Fed meeting)

But trend should resume afterwards as uncertainty

dissipates

− Material policy shift in DM unlikely (e.g., fiscal

easing and monetary tightening) – search for

yield to continue

− EM growth outlook to improve marginally as low

inflation allows for easier EM monetary policy

4.2

4.7

3

4

5

6

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16

2016 2017

Source: Deutsche Bank Research

…Despite no improvement to EM macro outlook

DB Real GDP growth forecast for EM, %yoy

If anything, growth forecasts are

lower than a few months ago

Material inflows into EM assets in recent months...

− Pick-up particularly large post-Brexit vote

− At the expense of Europe / other risky assets

...Despite no significant improvement in EM macro

outlook

− Despite marginal rise recently our EM growth

forecasts remain lower than a few months ago

Relocation of capital underpinned by search for

yield on the back of still dovish monetary policy

− No Fed hike, dovish tone from ECB and BoJ

-10%

-5%

0%

5%

10%

15%

Jan-16 Mar-16 May-16 Jul-16 Sep-16

Source: EPFR, Haver Analytics, Deutsche Bank Research

EM has received material inflows since mid-year…

Cumulative flows ytd

(% of AUM) EM bonds

EU equities

US HY

US IG

US treasuries

EM assets have benefited from inflows despite no improvement in fundamentals; expect pause in inflows but only short-term

21 EM Monthly: Re-Inflating EM – 6-Oct-2016

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

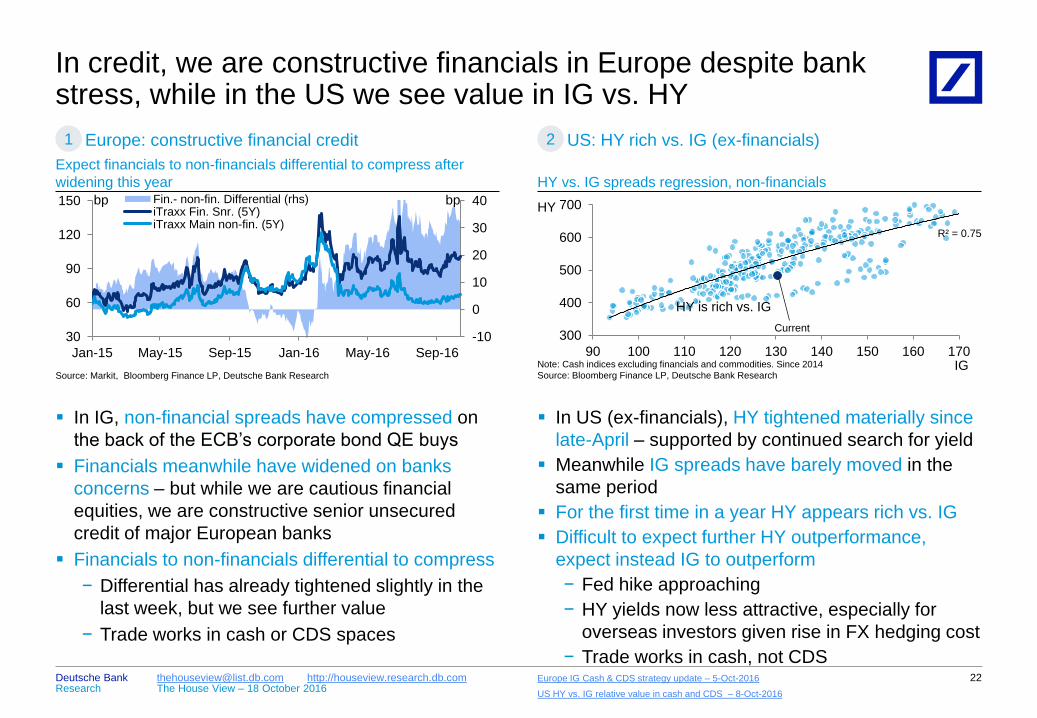

In US (ex-financials), HY tightened materially since

late-April – supported by continued search for yield

Meanwhile IG spreads have barely moved in the

same period

For the first time in a year HY appears rich vs. IG

Difficult to expect further HY outperformance,

expect instead IG to outperform

− Fed hike approaching

− HY yields now less attractive, especially for

overseas investors given rise in FX hedging cost

− Trade works in cash, not CDS

-10

0

10

20

30

40

30

60

90

120

150

Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16

Fin.- non-fin. Differential (rhs) iTraxx Fin. Snr. (5Y) iTraxx Main non-fin. (5Y)

Source: Markit, Bloomberg Finance LP, Deutsche Bank Research

bp

Expect financials to non-financials differential to compress after

widening this year

bp

In IG, non-financial spreads have compressed on

the back of the ECB’s corporate bond QE buys

Financials meanwhile have widened on banks

concerns – but while we are cautious financial

equities, we are constructive senior unsecured

credit of major European banks

Financials to non-financials differential to compress

− Differential has already tightened slightly in the

last week, but we see further value

− Trade works in cash or CDS spaces

In credit, we are constructive financials in Europe despite bank stress, while in the US we see value in IG vs. HY

22 Europe IG Cash & CDS strategy update – 5-Oct-2016

1 Europe: constructive financial credit 2 US: HY rich vs. IG (ex-financials)

US HY vs. IG relative value in cash and CDS – 8-Oct-2016

300

400

500

600

700

90 100 110 120 130 140 150 160 170

HY vs. IG spreads regression, non-financials

R² = 0.75

Note: Cash indices excluding financials and commodities. Since 2014

Source: Bloomberg Finance LP, Deutsche Bank Research IG

HY

Current

HY is rich vs. IG

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

1,700

1,800

1,900

2,000

2,100

2,200

2,300

Jan-15 Jul-15 Jan-16 Jul-16 Note: Columns denote previous instances of 5%+ corrections

Source: Bloomberg Finance LP, Deutsche Bank Research

S&P500: Risk of 5-10% correction with index within 3% of record

high

S&P500

5-10% correc-

tion range

Brexit vote China fears

post Fed hike China fears

~1,920

~2,025

S&P500 overdue a 5-10% correction...

− Index within 3% of historic high despite macro

and political uncertainty, weak earnings outlook

Several potential triggers...

− US election uncertainty – though this has

diminished in recent weeks

− Dollar strength as Fed hike approaches

− Scope for disappointment on Q3 earnings

...But no near-term bear market – S&P500 more

likely to reach 2,500 before 20%+ decline

70

75

80

85

90

95 100

110

120

130

140

150

160

170

2013 2014 2015 2016

UK exporters vs. domestic, rel. performance

GBP TWI (rhs, inverted)

A FTSE100 exporters vs. domestic basket is our cleanest short

sterling play

Source: Bloomberg Finance LP, Deutsche Bank Research

Implied upside from

5% GBP TWI

depreciation

We introduced several Brexit trades that benefit

when sterling depreciates

− Long FTSE100 vs. FTSE250

− Long FTSE100 vs. Stoxx600

− Long UK exporters vs. domestics

Very strong performance to date – but expectation

of further sterling weakness suggest further upside

Exporters vs. domestics trade has highest FX

sensitivity – 8% return for every 5% GBP TWI fall

Bloomberg baskets: DBCTBXEP Index (exporters),

DBCTBXDP Index (domestic)

In equities we see further scope for outperformance in our Brexit trades in Europe, while we remain cautious on the S&P500

23

1 Europe: maintain Brexit trades*

Don’t exit Brexit trades – 12-Oct-2016

2 US: cautious S&P500, risk of a correction

Note: (*) The key risk to our Brexit trades is a bout of sterling strength.

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Keep informed with our regular The House View publications at houseview.research.db.com

The House View

range

The House View Infographic Special Snapshot Macro Forecasts

Monthly report

Summarises key financial

and economic

developments

Provides context on

Deutsche Bank’s forecasts

and outlook for economic

growth, monetary policy

and financial markets

A one-pager that tackles a

current topic in a few

charts and visuals

Ad-hoc in depth reports on

major underlying topics

affecting global economic

growth and markets

A handy two-page

summary of Deutsche

Bank Research macro and

markets views

A summary of Deutsche

Bank Markets Research

macroeconomic, fixed

income, foreign

exchange and

commodities forecasts

24

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

DB forecasts

Source: Deutsche Bank Research

25

ASIA: China, HK, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Sri Lanka, Taiwan,

Thailand, Vietnam

DM: Australia, Canada, Denmark , Eurozone, Japan, New Zealand, Norway, Sweden,

Switzerland, UK, US

* CPI (%) forecasts are period averages

CEEMEA: Czech Rep., Israel, Egypt, Hungary, Kazakhstan, Nigeria, Poland, Romania, Russia, Saudi

Arabia, South Africa, Turkey, UAE and Ukraine

LATAM: Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela

GDP growth (%) 2014 2015 2016F 2017F CPI inflation, YoY* (%) 2014 2015 2016F 2017F

Global 3.4 3.2 3.0 3.4 US 1.6 0.1 1.3 2.1

US 2.4 2.6 1.3 1.7 Eurozone 0.4 0.0 0.2 1.3

Eurozone 1.1 1.9 1.6 1.1 Japan 2.7 0.8 -0.2 0.5

Germany 1.6 1.7 1.9 1.0 UK 1.5 0.0 0.7 2.2

France 0.7 1.2 1.4 1.4 China 2.0 1.4 1.9 1.8

Italy 0.1 0.7 0.7 0.4

Spain 1.4 3.2 3.0 2.0 Central Bank policy rate (%) Current Q4-16F Q2-17F Q4-17F

Japan -0.1 0.6 0.6 0.9 US 0.375 0.625 0.875 1.125

UK 3.1 2.2 1.9 0.9 Eurozone 0.00 0.00 0.00 0.00

China 7.3 6.9 6.6 6.5 Japan -0.10 -0.10 -0.10 -0.10

India 7.0 7.2 7.5 7.6 UK 0.25 0.10 0.10 0.10

EM Asia 6.4 6.1 6.0 6.0 China 1.50 1.50 1.25 1.25

EM CEEMEA 2.3 1.0 1.9 2.6

EM LatAm 0.6 -0.3 -0.9 1.9 Key market metrics Current Q4-16F Q2-17F Q4-17F

EM 4.6 4.0 4.2 4.7 US 10Y yield (%) 1.76 1.75 2.00 2.00

DM 1.7 2.1 1.4 1.4 EUR 10Y yield (%) 0.05 0.00 0.15 0.25

EUR/USD 1.100 1.05 1.00 0.95

USD/JPY 104 94 94 94

S&P 500 2,133 2,150 #N/A 2,350

Stoxx 600 340 325 #N/A 345

Oil WTI (USD/bbl) 50.3 48.0 51.0 55.0

Oil Brent (USD/bbl) 51.6 50.0 53.0 57.0

Current prices as of 14-Oct-2016

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com

Analyst Certification

This report covers more than one security and was contributed to by more than one analyst. The views expressed in this report accurately reflect the

views of each contributor to this compendium report. In addition, each contributor has not and will not receive any compensation for providing a specific

recommendation or view in this compendium report. Marcos Arana / Matthew Luzzetti / Aditya Bhave / Rajni Thakur

Attribution

The authors wish to acknowledge the contributions made by Shakun Guleria in the preparation of this report.

*Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg

and other vendors . Other information is sourced from Deutsche Bank, subject companies, and other sources. For disclosures pertaining to recommendations

or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global

disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr

26

Appendix 1 Important Disclosures *Other information available upon request

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com 27

Additional Information The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively "Deutsche Bank"). Though the information herein is believed to be reliable and has been obtained from public sources believed to be reliable, Deutsche Bank makes no representation as to its accuracy or completeness. If you use the services of Deutsche Bank in connection with a purchase or sale of a security that is discussed in this report, or is included or discussed in another communication (oral or written) from a Deutsche Bank analyst, Deutsche Bank may act as principal for its own account or as agent for another person. Deutsche Bank may consider this report in deciding to trade as principal. It may also engage in transactions, for its own account or with customers, in a manner inconsistent with the views taken in this research report. Others within Deutsche Bank, including strategists, sales staff and other analysts, may take views that are inconsistent with those taken in this research report. Deutsche Bank issues a variety of research products, including fundamental analysis, equity-linked analysis, quantitative analysis and trade ideas. Recommendations contained in one type of communication may differ from recommendations contained in others, whether as a result of differing time horizons, methodologies or otherwise. Deutsche Bank and/or its affiliates may also be holding debt or equity securities of the issuers it writes on. Analysts are paid in part based on the profitability of Deutsche Bank AG and its affiliates, which includes investment banking, trading and principal trading revenues. Opinions, estimates and projections constitute the current judgment of the author as of the date of this report. They do not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank provides liquidity for buyers and sellers of securities issued by the companies it covers. Deutsche Bank research analysts sometimes have shorter-term trade ideas that are consistent or inconsistent with Deutsche Bank's existing longer term ratings. Trade ideas for equities can be found at the SOLAR link at http://gm.db.com. A SOLAR idea represents a high conviction belief by an analyst that a stock will outperform or underperform the market and/or sector delineated over a time frame of no less than two weeks. In addition to SOLAR ideas, the analysts named in this report may from time to time discuss with our clients, Deutsche Bank salespersons and Deutsche Bank traders, trading strategies or ideas that reference catalysts or events that may have a near-term or medium-term impact on the market price of the securities discussed in this report, which impact may be directionally counter to the analysts' current 12-month view of total return or investment return as described herein. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof if any opinion, forecast or estimate contained herein changes or subsequently becomes inaccurate. Coverage and the frequency of changes in market conditions and in both general and company specific economic prospects make it difficult to update research at defined intervals. Updates are at the sole discretion of the coverage analyst concerned or of the Research Department Management and as such the majority of reports are published at irregular intervals. This report is provided for informational purposes only and does not take into account the particular investment objectives, financial situations, or needs of individual clients. It is not an offer or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are inherently imprecise and a product of the analyst’s judgment. The financial instruments discussed in this report may not be suitable for all investors and investors must make their own informed investment decisions. Prices and availability of financial instruments are subject to change without notice and investment transactions can lead to losses as a result of price fluctuations and other factors. If a financial instrument is denominated in a currency other than an investor's currency, a change in exchange rates may adversely affect the investment. Past performance is not necessarily indicative of future results. Unless otherwise indicated, prices are current as of the end of the previous trading session, and are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank, subject companies, and in some cases, other parties. The Deutsche Bank Research Department is independent of other business areas divisions of the Bank. Details regarding our organizational arrangements and information barriers we have to prevent and avoid conflicts of interest with respect to our research is available on our website under Disclaimer found on the Legal tab.

Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promise to pay fixed or variable interest rates. For an investor who is long fixed rate instruments (thus receiving these cash flows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thus cause a loss. The longer the maturity of a certain cash flow and the higher the move in the discount factor, the higher will be the loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are among the most common adverse macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, client segmentation, regulation (including changes in assets holding limits for different types of investors), changes in tax policies, currency convertibility (which may constrain currency conversion, repatriation of profits and/or the liquidation of positions), and settlement issues related to local clearing houses are also important risk factors to be considered. The sensitivity of fixed income instruments to macroeconomic shocks may be mitigated by indexing the contracted cash flows to inflation, to FX depreciation, or to specified interest rates – these are common in emerging markets. It is important to note that the index fixings may -- by construction -- lag or mis-measure the actual move in the underlying variables they are intended to track. The choice of the proper fixing (or metric) is particularly important in swaps markets, where floating coupon rates (i.e., coupons indexed to a typically short-dated interest rate reference index) are exchanged for fixed coupons. It is also important to acknowledge that funding in a currency that differs from the currency in which coupons are denominated carries FX risk. Naturally, options on swaps (swaptions) also bear the risks typical to options in addition to the risks related to rates movements.

Derivative transactions involve numerous risks including, among others, market, counterparty default and illiquidity risk. The appropriateness or otherwise of these products for use by investors is dependent on the investors' own circumstances including their tax position, their regulatory environment and the nature of their other assets and liabilities, and as such, investors should take expert legal and financial advice before entering into any transaction similar to or inspired by the contents of this publication. The risk of loss in futures trading and options, foreign or domestic, can be substantial. As a result of the high degree of leverage obtainable in futures and options trading, losses may be incurred that are greater than the amount of funds initially deposited. Trading in options involves risk and is not suitable for all investors. Prior to buying or selling an option investors must review the "Characteristics and Risks of Standardized Options”, at http://www.optionsclearing.com/about/publications/character-risks.jsp. If you are unable to access the website please contact your Deutsche Bank representative for a copy of this important document.

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com 28

Participants in foreign exchange transactions may incur risks arising from several factors, including the following: ( i) exchange rates can be volatile and are subject to large fluctuations; ( ii) the value of currencies may be affected by numerous market factors, including world and national economic, political and regulatory events, events in equity and debt markets and changes in interest rates; and (iii) currencies may be subject to devaluation or government imposed exchange controls which could affect the value of the currency. Investors in securities such as ADRs, whose values are affected by the currency of an underlying security, effectively assume currency risk.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor's home jurisdiction. Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the "Disclosures Lookup" and "Legal" tabs. Investors are strongly encouraged to review this information before investing.

United States: Approved and/or distributed by Deutsche Bank Securities Incorporated, a member of FINRA, NFA and SIPC. Analysts located outside of the United States are employed by non-US affiliates that are not subject to FINRA regulations. Germany: Approved and/or distributed by Deutsche Bank AG, a joint stock corporation with limited liability incorporated in the Federal Republic of Germany with its principal office in Frankfurt am Main. Deutsche Bank AG is authorized under German Banking Law and is subject to supervision by the European Central Bank and by BaFin, Germany’s Federal Financial Supervisory Authority. United Kingdom: Approved and/or distributed by Deutsche Bank AG acting through its London Branch at Winchester House, 1 Great Winchester Street, London EC2N 2DB. Deutsche Bank AG in the United Kingdom is authorised by the Prudential Regulation Authority and is subject to limited regulation by the Prudential Regulation Authority and Financial Conduct Authority. Details about the extent of our authorisation and regulation are available on request.

Hong Kong: Distributed by Deutsche Bank AG, Hong Kong Branch.

India: Prepared by Deutsche Equities India Pvt Ltd, which is registered by the Securities and Exchange Board of India (SEBI) as a stock broker. Research Analyst SEBI Registration Number is INH000001741. DEIPL may have received administrative warnings from the SEBI for breaches of Indian regulations. Japan: Approved and/or distributed by Deutsche Securities Inc.(DSI). Registration number - Registered as a financial instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, Type II Financial Instruments Firms Association and The Financial Futures Association of Japan. Commissions and risks involved in stock transactions - for stock transactions, we charge stock commissions and consumption tax by multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional losses stemming from foreign exchange fluctuations. We may also charge commissions and fees for certain categories of investment advice, products and services. Recommended investment strategies, products and services carry the risk of losses to principal and other losses as a result of changes in market and/or economic trends, and/or fluctuations in market value. Before deciding on the purchase of financial products and/or services, customers should carefully read the relevant disclosures, prospectuses and other documentation. "Moody's", "Standard & Poor's", and "Fitch" mentioned in this report are not registered credit rating agencies in Japan unless Japan or "Nippon" is specifically designated in the name of the entity. Reports on Japanese listed companies not written by analysts of DSI are written by Deutsche Bank Group's analysts with the coverage companies specified by DSI. Some of the foreign securities stated on this report are not disclosed according to the Financial Instruments and Exchange Law of Japan. Korea: Distributed by Deutsche Securities Korea Co. South Africa: Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register Number in South Africa: 1998/003298/10).

Singapore: by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch (One Raffles Quay #18-00 South Tower Singapore 048583, +65 6423 8001), which may be contacted in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and regulations), they accept legal responsibility to such person for its contents. Taiwan: Information on securities/investments that trade in Taiwan is for your reference only. Readers should independently evaluate investment risks and are solely responsible for their investment decisions. Deutsche Bank research may not be distributed to the Taiwan public media or quoted or used by the Taiwan public media without written consent. Information on securities/instruments that do not trade in Taiwan is for informational purposes only and is not to be construed as a recommendation to trade in such securities/instruments. Deutsche Securities Asia Limited, Taipei Branch may not execute transactions for clients in these securities/instruments.

Qatar: Deutsche Bank AG in the Qatar Financial Centre (registered no. 00032) is regulated by the Qatar Financial Centre Regulatory Authority. Deutsche Bank AG - QFC Branch may only undertake the financial services activities that fall within the scope of its existing QFCRA license. Principal place of business in the QFC: Qatar Financial Centre, Tower, West Bay, Level 5, PO Box 14928, Doha, Qatar. This information has been distributed by Deutsche Bank AG. Related financial products or services are only available to Business Customers, as defined by the Qatar Financial Centre Regulatory Authority.

Research Deutsche Bank

The House View – 18 October 2016 [email protected] http://houseview.research.db.com 29

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute, any appraisal or evaluation activity requiring a license in the Russian Federation.

Kingdom of Saudi Arabia: Deutsche Securities Saudi Arabia LLC Company, (registered no. 07073-37) is regulated by the Capital Market Authority. Deutsche Securities Saudi Arabia may only undertake the financial services activities that fall within the scope of its existing CMA license. Principal place of business in Saudi Arabia: King Fahad Road, Al Olaya District, P.O. Box 301809, Faisaliah Tower - 17th Floor, 11372 Riyadh, Saudi Arabia.

United Arab Emirates: Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulated by the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may only undertake the financial services activities that fall within the scope of its existing DFSA license. Principal place of business in the DIFC: Dubai International Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has been distributed by Deutsche Bank AG. Related financial products or services are only available to Professional Clients, as defined by the Dubai Financial Services Authority. Australia: Retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. Please refer to Australian specific research disclosures and related information at https://australia.db.com/australia/content/research-information.html

Australia and New Zealand: This research is intended only for "wholesale clients" within the meaning of the Australian Corporations Act and New Zealand Financial Advisors Act respectively. Additional information relative to securities, other financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published without Deutsche Bank's prior written consent.

Copyright © 2016 Deutsche Bank AG