ibisworld industry report j7100...

TRANSCRIPT

2 About this Industry2 Industry Definition

2 Main Activities

2 Similar Industries

2 Additional Resources

3 Industry at a Glance

4 Industry Performance4 Executive Summary

4 Key External Drivers

5 Current Performance

8 Industry Outlook

11 Industry Life Cycle

14 Products & Markets14 Supply Chain

14 Products & Services

16 Demand Determinants

17 Major Markets

18 International Trade

19 Business Locations

21 Competitive Landscape21 Market Share Concentration

21 Key Success Factors

22 Cost Structure Benchmarks

24 Basis of Competition

25 Barriers to Entry

26 Industry Globalisation

28 Major Companies28 Telstra Corporation Limited

31 SingTel Optus Pty Limited

32 Vodafone Hutchison Australia Pty Limited

37 Operating Conditions37 Capital Intensity

38 Technology & Systems

41 Revenue Volatility

42 Regulation & Policy

45 Industry Assistance

46 Key Statistics46 Industry Data

46 Annual Change

46 Key Ratios

47 Jargon & Glossary

IBISWorld Industry Report J7100Telecommunications Services in AustraliaMay 2012 Craig Shulman

Wired to wireless: Growth is expected as next generation networks are adopted

www.ibisworld.com.au | (03) 9655 3881 | [email protected]

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 2

Telecommunications companies provide telecommunication services to businesses and consumers using wire, cable, wireless and satellite infrastructure. Not all sector participants

own and operate telecommunications infrastructure. Telecommunications resellers purchase network capacity and then retail services to businesses and consumers.

The primary activities of this industry are

Wired telecommunication service provision

Mobile telecommunications service provision

Internet service provision

Satellite communication service provision (except mobile telephones)

Television relay station operation

Radio relay station operation

Industry definition

Main Activities

Similar Industries

Additional resources

The major products and services in this industry are

Fixed internet services

Mobile services

Resellers

Satellite, TV and radio relay

Wired services

About this Industry

E ConstructionCompanies in this industry lay cable, construct transmission lines or towers and install or repair telephone or telegraphic equipment.

P Cultural and recreational ServicesEnterprises in this industry operate radio or television broadcasting services.

L7800 business Services in AustraliaBusinesses in this industry operate telephone answering services or message delivery services.

X0016 Integrated Logistics in AustraliaFirms in this industry deliver freight items but not letters and mail-type articles.

For additional information on this industry

www.abs.gov.au Australian Bureau of Statistics

www.acma.gov.au Australian Communications and Media Authority

www.accc.gov.au Australian Competition and Consumer Commission

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 3

Market ShareTelstra Corporation Limited 52.5%

SingTel Optus Pty Limited 22.5%

Vodafone Hutchison Australia Pty Limited 11.1%

Key External driversreal household disposable incomeNumber of businessesInternet connectionsLegislative compliance requirements for communication servicesNumber of householdsdemand from free to air television services

Key Statistics Snapshot

Industry at a GlanceTelecommunications Services in 2011-12

revenue

$40.8bnProfit

$6.1bnwages

$4.7bnbusinesses

617

Annual Growth 12-17

3.0%Annual Growth 07-12

-0.9%

Industry Structure Life Cycle Stage Decline

Revenue Volatility Low

Capital Intensity High

Industry Assistance Medium

Concentration Level High

Regulation Level Heavy

Technology Change High

Barriers to Entry High

Industry Globalisation Medium

Competition Level Medium

FOR ADDITIOnAL STATISTICS AnD TIME SERIES SEE THE APPEnDIx On PAGE 46

% c

hang

e

10

−2

0

2

4

6

8

1604 06 08 10 12 14Year

Real household disposable income

SOURCE: WWW.IBISWORLD.COM.AU

% c

hang

e

6

−6

−4

−2

0

2

4

1804 06 08 10 12 14 16Year

Revenue Employment

Revenue vs. employment growth

Employment distribution

22,015NSW

865ACT

17,070VIC

865TAS

680NT

10,700QLD

5,810WA

3,835SA

SOURCE: WWW.IBISWORLD.COM.AU

p. 28

p. 4

SOURCE: WWW.IBISWORLD.COM.AU

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 4

Key External drivers Real household disposable incomeHouseholds’ consumption of telecommunications services depends in part on disposable income. This is particularly the case for spending on the sector’s latest services such as mobile internet, GPRS, IPTV and super fast fixed internet. Spending on the sector’s more traditional service offerings such as voice and messaging are relatively insensitive to disposable income changes.

Number of businessesBusinesses are an important market for telecommunication companies. Businesses depend on telecommunications services when

producing and distributing goods and services. An increase in the number of businesses in Australia will boost sector demand and revenue. Moreover, an increase in the output of businesses (i.e. GDP growth) will be in part dependent on higher telecommunications consumption. So an improvement in economic conditions will be accompanied by an expansion in businesses’ telecommunications use.

Internet connectionsDemand for internet services depends on the number of internet connections, which is influenced by computer and 3G mobile penetration rates. For ISPs,

Executive Summary

The explosion in connectivity has entrenched telecommunications as a vital part of the day-to-day functioning of Australian businesses and has changed the way Australians interact, with social networking moving online. Despite the increased demand to communicate over these pathways, IBISWorld forecasts that revenue for the Telecommunications Services sector will decline by 2.0% to $40.8 billion in 2011-12.

Industries within the Telecommunications Services sector have

experienced contrasting results. Overall sector revenue has remained stable, and is expected to record an annualised decline of just 0.9% in the five years through 2011-12. However, over the past five years there has been an increased demand and use of telecommunications services. Despite the increased demand, intense intra-industry and intra-sector competition has created a fiercely competitive environment. This has meant that growth in demand has been achieved at the expense of other, more profitable, telecommunications services. In

particular, the Mobile Telecommunication Carriers industry has been succeeding thanks to wired-to-wireless substitution and thus has made inroads into the internet service provider market, in addition to the voice market. The Wired Telecommunications Carriers industry has thus suffered a collapse in access lines and usage, and will continue to recede into the future.

The overriding factor driving this shift in demand has been price-based competition and as such the demand has shifted to lower priced services that benefit the consumer, which is occurring at the expense of overall sector revenue, as well as sector profitability. In an attempt to underpin margins, telecommunications companies (telcos) have looked to improve efficiency by reducing employee numbers. IBISWorld expects the sector labour force will have declined by 2.9% per annum over the five years through 2011-12 to 60,618 people, with wages exhibiting a similar fall.

IBISWorld forecasts that sector revenue will return to growth in the coming five years to increase by an average 3.0% per annum to $47.2 billion in 2016-17. Growth will be the result of advances in technology, expanding network coverage and network infrastructure upgrades.

Industry PerformanceExecutive Summary | Key External drivers | Current Performance Industry Outlook | Life Cycle Stage

The expansion and acceleration of a wired-to-wireless shift has pressured prices

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 5

Industry Performance

Current Performance

The appetite for constant connectivity and the blossoming of data are the two major stories of the past five years. Mobile network infrastructure in Australia advanced with third generation (3G) networks assuming dominance. The next generation of mobile technology enabled significant enhancements to the quality of service offered and, when combined with increased affordability, resulted in extra push behind the fixed-to-mobile substitution trend. This trend has resulted in mobile service revenue

usurping all fixed-line revenue (wired and ISP) for the first time ever in 2009-10, with mobile revenue expected to break the $20 billion barrier this year.

The preference for mobility is at the expense of wired services, which traditionally generate high margins. IBISWorld forecasts that fixed-line telecommunication services will contract by an annualised 8.6% over the five years through 2011-12 to $10.2 billion. However, this does not signal the death of wired infrastructure. The current

Key External driverscontinued

demand depends on the number of fixed-line connections while for mobile carriers it depends on mobile connections. The number of fixed connections has actually been declining as wireless internet as grown in popularity. Consumption on internet services also depends on connection speeds with faster connections facilitating more usage and revenue. Connection speeds are accelerating as users migrate to faster services.

Legislative compliance requirements for communication servicesThis sensitivity represents the federal and state government policies and regulations for the telecommunications industries and new network user industries, such as online services, broadcasting (including pay-TV) multimedia and computing

industries. Changes to local government planning regulations with respect to the construction of new telecommunications infrastructure also apply. A decrease in the regulatory burden of this industry will increase competition, placing pressure on pricing and stimulating demand.

Number of householdsAn increase in the number of households represents an expansion in the potential market for wired telecommunications carriers, resellers and ISPs.

Demand from free to air television servicesDemand for free-to-air services influences demand for satellite and television relay operations.

% c

hang

e

7

2

3

4

5

6

1705 07 09 11 13 15Year

Number of businesses

SOURCE: WWW.IBISWORLD.COM.AU

% c

hang

e

10

−2

0

2

4

6

8

1604 06 08 10 12 14Year

Real household disposable income

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 6

Industry Performance

Current Performancecontinued

environment is conducive to mobile infrastructure, as the maturity of 3G technology is coinciding with the decline of copper and its associated internet access technologies. However, IBISWorld expects that fixed and mobile communication infrastructures will coexist in harmony in the future.

The overall outcome for the Telecommunications Services sector is one of treading water. The growth of mobile revenue is cancelled out by the decline in wired revenue, ultimately resulting in an annualised revenue decline of 0.9% in the past five years. The decline may seem astounding considering booming

telecommunications services consumption. However, the increased price-based competition and new technologies have resulted in sizeable price declines. IBISWorld estimates that telecommunications services prices have fallen by 4.9% per annum over the past five years, or 22.4% in total. Telcos have generally enacted price cuts by offering greater usage for the same plan payment. Importantly, the price decline represents the sector’s traditional services’ long-term shift toward a utility service, where the provision of data will eventually mirror electricity, gas and water utilities. Sector revenue is forecast to increase by 2.8% in 2012-13 to $41.9 billion.

rising competition Over the past five years, the industry has been largely defined by its three biggest players – Telstra, dominating half of the sector, Singtel Optus, holding around a quarter and Vodafone Hutchison Australia (VHA). While Telstra and Singtel Optus participate in all areas of the sector, VHA’s business is heavily focused on mobile telecommunications. Furthermore, the company was only formed via a merger in 2009, making it a relatively new major player.

Remaining sector participants operate on a much smaller scale, with the next-largest grouping classified as second-tier telcos. Second-tier telcos are characterised as having market share of 1.0% to 2.0% and tend to be pushing through the new technologies and products that are absorbing the traditional telecommunications revenue. The best example is iiNet. Through service innovation, pushing naked digital subscriber lines (DSL) and unique marketing, iiNet became Australia’s second-largest ISP in 2010-11.

Competition has been intensifying as mobile networks, a market in which Telstra faces the stiffest competition and has the least-dominant market share, become the dominant revenue generator.

This is extremely important in terms of industry dynamics, as Optus and VHA, own full coverage mobile networks. To encourage the migration to mobile, VHA’s predecessors and Optus instigated aggressive price competition. This began with the introduction of capped plans and has extended to larger handset subsidies. The fixed-line providers, carriers and resellers responded by slashing their prices, particularly for long-distance calls. The consumer has been the big winner, according to IBISWorld forecasts that telecommunications service prices have collapsed by 22.4% in the past five years.

The Internet Service Providers industry has exhibited similar price contractions, as access and price per bit have tumbled. This can be attributed to operators such as iiNet and TPG embarking on aggressive campaigns designed to win market share. However,

The wired-to-wireless trend is forecast to result in mobile service revenue usurping fixed-line revenue

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 7

Industry Performance

rising competitioncontinued

price has not been the sole competitive weapon employed; service innovation has also been critical. Naked DSL and VoIP are new services bringing benefits to

smaller operators and hurting the dominant infrastructure owners by absorbing existing revenue streams

The demand to communicate

The demand for communication services has grown strongly in the five years through 2011-12. The consumer has been the big winner of the intensifying sector competition, which is delivering considerable benefits to households and businesses. Lower prices are the most immediate benefits and have enabled much higher use of telecommunication services. This is particularly the case in the mobile and ISP spaces. The price declines have placed pressure on margins, which has caused telcos to introduce innovative value-added services, in addition to the traditional offerings, to encourage further usage and to protect margins. This is further embedding telecommunications into the daily lives of businesses and consumers as it makes telecommunication networks the backbone to an ever-growing number of services.

The changes in the mobile space over the past five years exemplify this trend. Mobile phones originally focused on mobile voice services but now provide voice, messaging, e-mail, internet browsing, mapping, GPS and modem services (via tethering). Such service

breadth is making household and business subscribers incredibly dependent on their mobiles. The all-encompassing product range is allowing a growing number of consumers, sole proprietors and small businesses to rely solely on wireless services for delivering all their communication needs. Such dependency is facilitating a boom in mobile usage.

Likewise, high-speed fixed-line broadband connections have enabled a growing selection of data-intensive services to flourish, such as social networking, content sharing, sophisticated online shopping, e-finance and video content. For businesses, a growing number of productivity boosting applications are internet dependent. Many of the latest applications are cloud-like solutions that depend on continuous connections and are therefore particularly data intensive. Usage is booming as fixed connections become an increasingly important service gateway. This, however, was attempted to be quashed by the media industry via the Australian Federation Against Copyright Theft (AFACT) who

Telecommunication subscribers

yearFixed lines

(’000)Mobile connections

(’000)Fixed internet

(’000)Mobile internet

(’000)

2004-05 11,460 18,423 5,984 502005-06 11,250 19,760 6,306 1502006-07 10,920 21,360 6,779 2202007-08 11,000 22,120 6,442 7852008-09 10,670 24,220 6,459 1,9612009-10 10,460 26,600 6,130 2,8002010-11 10,260 29,200 6,090 3,400

SOURCE: IBISWORLD

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 8

Industry Performance

The demand to communicatecontinued

sued iiNet for being responsible for their customer’s copyright theft. After many appeals, iiNet suceeded in winning the High Court judgment in April 2012,

avoiding the potential loss of customers and rise in operational costs that would have affected the whole industry.

Industry Outlook

The next five years will be an exciting period for the Telecommunications Services sector as Australia’s digital economy landscape begins to take shape. IBISWorld expects that sector revenue will return to growth, increasing at an average 3.0% per annum to be worth $47.2 billion in 2016-17. There will be further advancements in network infrastructure technologies, the rollout of advanced fibre-to-the-home (FTTH) services and 4G mobile networks will be of particular importance. As the advanced networks expand their coverage, new telecommunication-enabled smart applications for the utility, transport, health, education, commerce and retail sectors will be developed, creating new revenue streams for telcos. IBISWorld expects the most significant sector growth to occur after 2013, as this is when the next generation networks will

begin to be adopted by the masses. Advances in network infrastructure will enable the adoption of emerging services such as VoIP, naked DSL, IPTV (TV over the internet) and mobile tethering to become mainstream services.

Fixed-to-mobile substitution

The most significant trend in the past five years has been fixed-to-mobile substitution. The switch is being fuelled by rapid advances in mobile technology, which, in combination with a greater contraction in mobile prices in comparison to wired services, has created a value gap between mobile telephone services and wired services. An added incentive fuelling the substitution has been the increased demand for the constant connectivity that mobile services deliver. Mobile services have become so attractive that many households have hung up their traditional phone and disconnected their landline altogether. Telstra reports that access lines in service have fallen from over 10 million in 2005 to just 8.8 million in December 2009. Fixed-to-mobile substitution has served to weaken Telstra’s sector dominance, while

providing valuable gains for various competitors in growth segments of the telecommunications market. In particular, VHA’s sector market share increase by 4.5 percentage points since 2005.

The shift to mobile has been best exemplified by the divergent directions in subscriber numbers. Over the five years through 2010-11, IBISWorld estimates the number of mobile connections and mobile internet subscribers increased by an annualised 8.1% and 86.7% respectively. Meanwhile, fixed-line connections are estimated to have decreased by 1.8% annually, while fixed-line internet subscribers grew by an anaemic 0.5% per annum. Mobile revenue will exhibit an annualised increase of 6.2%, while wired revenue contracts by 7.7% per annum.

% c

hang

e

6

−6

−4

−2

0

2

4

1804 06 08 10 12 14 16Year

Industry revenue

SOURCE: WWW.IBISWORLD.COM.AU

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 9

Industry Performance

Industry Outlookcontinued

IBISWorld expects the heightened merger and acquisition activity will continue as the second-tier telcos look to boost competitiveness, which is obtained through greater scale. The recent announcement that NBN Co, the company created to administer the national broadband network (NBN), will look at acquiring telcos as part of the network expansion. This will add another dimension to the merger and acquisition activity. External competitive threats will

also emerge from other fields and beyond Australia’s borders as the convergence trend in media and communications continues. IBISWorld expects that once the NBN rollout occurs there will be a spate of new retail service providers looking to enter the market, which will ensure that sector enterprise numbers return to expansion, with a forecast 0.3% per annum increase in sector enterprises for the five years through 2016-17.

Capacity constraints Mobile networks have prospered recently because of the constant connectivity advantage in comparison to the traditional wired carrier market. The mobile networks have been able to cope with the demand that the initial

applications have placed on the network. However, the increasing penetration of data-hungry and internet enabled devices will create challenges for mobile networks and will place incredible capacity constraints on the mobile

National broadband Network

The most significant development faced by the Telecommunications Services sector in the near term and throughout the next five years will be the Federal Government’s $43 billion FTTH NBN initiative. This project is the modern-day equivalent of the Snowy Mountains River scheme. As the NBN is interconnected with an already established 4G rollout, the Australian economy will be ushered into the digital age. Wired and mobile connectivity of 100+ megabits per second (Mbps) will facilitate mass-market adoption of VoIP and IPTV, smart grids, true e-health and e-learning, innovative online shopping and many other applications. The establishment of 4G

networks and the NBN will increase consumer and business reliance on telecommunications services.

In April 2009, the Federal Government outlined a plan to build a $43 billion, 100+ megabits per second (Mbps) FTTH broadband network to cover 93% of the Australian population. The remaining 7.0% of citizens are to get at least 12 Mbps connectivity using a combination of mobile and satellite technology. The plan involves the establishment of a company, NBN Co., legislated to be at least 51% government owned until at least five years before the completion of the build, to act as the wholesale entity.

Telecommunication subscriber forecast

yearFixed lines

(‘000)Mobile connections

(‘000)Fixed internet

(‘000)Mobile internet

(‘000)

2011-12 10,140 29,400 6,160 3,7602012-13 9,990 30,200 6,380 4,0602013-14 9,840 31,300 6,915 4,2502014-05 9,760 32,400 7,530 4,6002015-16 9,420 33,300 8,100 5,500

SOURCE: IBISWORLD

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 10

Industry Performance

Capacity constraintscontinued

networks. As a result, the later part of the coming five-year period is expected to yield resurgent growth in the number of fixed internet connections. This move will be further encouraged by the recent hybrid fibre-coaxial (HFC) upgrades to DOCSIS 3.0 technology, combined with the move to FTTH, will deliver super high-speed connectivity and will re-establish the utility of fixed connections.

As the penetration of high-speed connections further advances, the prices per byte will begin to erode, but the explosion in usage will ensure a return to

double-digit revenue growth for the Internet Service Providers industry. By 2016-17, IBISWorld expects that fixed internet access services will comprise 22% of sector revenue. Strong growth in the mobile and ISP markets will offset continued revenue decay in the Wired Telecommunications Carriers industry and anaemic growth from the Satellite, Television and Radio Relay Operations industry. The latter industry will face some difficulties in the final years of the period as analogue TV services are switched off.

Competition Assuming a smooth NBN rollout, towards the end of next five years the 4G-FTTH world will be a land of opportunity for the Telecommunications Services sector. Given that the future of communication will become more data-centric, the distinction between ISP and telecommunications carriers will eventually disappear as the services become one and the same. In addition, the global trend is that companies that previously operated in non-telecommunication industries such as cable operators, mobile-TV technology providers, content owners and search providers will look to move into the Telecommunications Services sector. To gain greater control over the supply chain and a larger portion of the spoils, major market participants will want to fully integrate and operate across key distribution channels. This will necessitate that the wired and mobile markets coexist within the media, IT and communications sectors.

Ultimately, it will be important for telcos to diversify their operations from traditional telecommunications provision. The wireless segment’s

traditional product offering (voice and messaging) is becoming a commodity business with high volumes and low profits, reflected by falling average revenue per user. If the segment doesn’t evolve, it will trend further towards becoming a low-margin commodity type segment, where operators become dumb pipe providers that deliver data (i.e. content) from producers to consumers.

One way that industry players can differentiate themselves is through service integration and cross-selling, marketing and service innovation. Cross-selling is already gaining greater emphasis, with product bundling becoming more prominent through its ability to cross sell and retain customer commitment for longer periods of time. Cost control will also be important in ensuring competitive pricing, but the future of internet access will be low margin, so cost control will simply be a competitive necessity. Furthermore, a greater focus on digital service provision is gaining greater attention as Optus’ parent company Singtel restructures its entire operations towards pursuing this revenue stream.

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 11

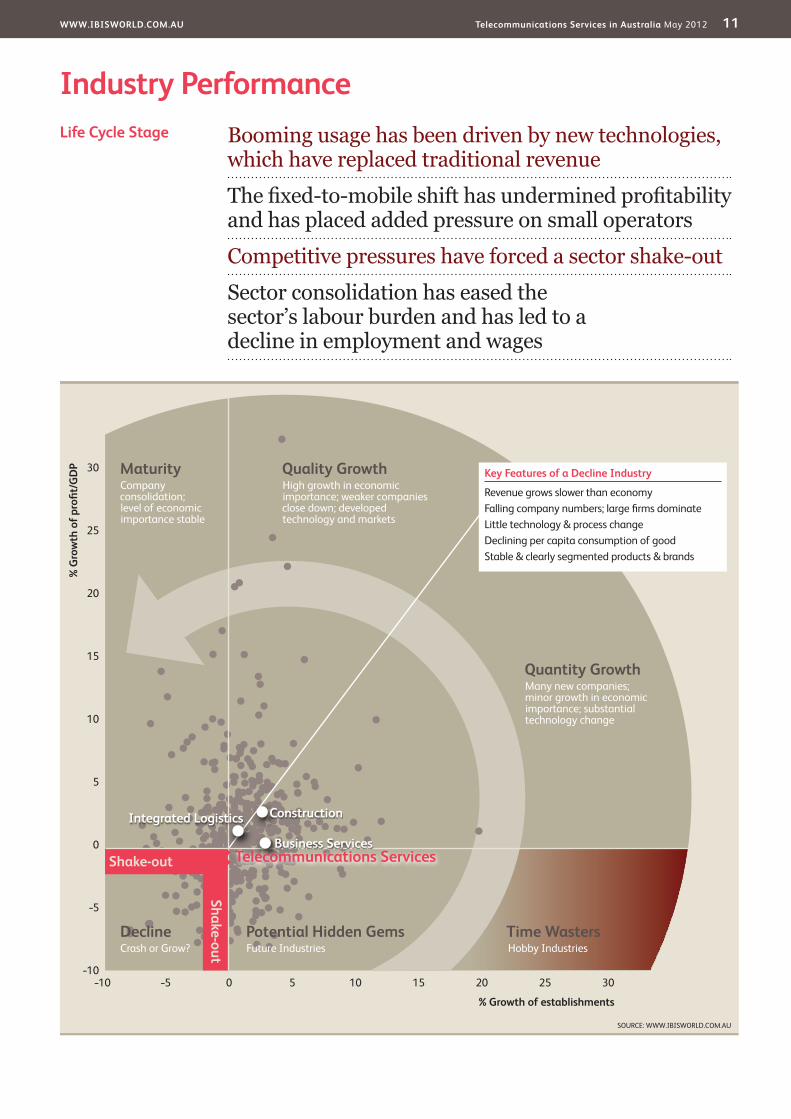

Industry PerformanceBooming usage has been driven by new technologies, which have replaced traditional revenue

The fixed-to-mobile shift has undermined profitability and has placed added pressure on small operators

Competitive pressures have forced a sector shake-out

Sector consolidation has eased the sector’s labour burden and has led to a decline in employment and wages

Life Cycle Stage

SOURCE: WWW.IBISWORLD.COM.AU

30

25

20

15

10

5

0

–5

–10–10 100 20–5 155 25 30

% G

row

th o

f pro

fi t/G

dP

% Growth of establishments

declineCrash or Grow?

Potential Hidden GemsFuture Industries

Quality GrowthHigh growth in economic importance; weaker companies close down; developed technology and markets

Time wastersHobby Industries

MaturityCompany consolidation;level of economic importance stable

Shake-out

Shake-out

Quantity GrowthMany new companies; minor growth in economic importance; substantial technology change

Key Features of a decline Industry

Revenue grows slower than economyFalling company numbers; large fi rms dominateLittle technology & process changeDeclining per capita consumption of goodStable & clearly segmented products & brands

Construction

business Services

Integrated Logistics

Telecommunications Services

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 12

Industry Performance

Industry Life Cycle The initial perception of Australia’s Telecommunications Services sector is one of growth, as information and communication services are becoming increasingly important in the day-to-day lives of business and consumer. However, the initial perception does not reveal the whole truth and by looking a little closer it is clear that the Telecommunications Services sector is actually in the decline stage of its economic life cycle.

The last few years have been marked by some landmark events in the Telecommunications Services sector. In 2007-08, for the first time in its history, the Internet Service Providers industry witnessed a decline in the number of fixed-line internet connections. This mirrors the decline in fixed voice telecommunications, where overall decline in fixed networks has been a result of improvements in mobile network speeds and affordability, have made mobile internet connectivity a viable option for a growing number of businesses and consumers. As a result, the 2009-10 year was predicted to be the first time the sector earns more revenue from mobile infrastructure than fixed, with proportions forecast at 46% and 45.3% respectively. Such a development ultimately represents another step closer to the end for the dominant fixed-line technology, copper. For much of the early 2000s, the life cycle of copper was prolonged by internet services. However, with advanced HFC, 4G and then FTTH networks on their way, the revenue decline for this piece of ageing infrastructure is set to accelerate.

Technology advances, service introductions and price declines have made it convenient and cost effective for consumers to disconnect their land lines to rely solely on their mobiles. As more users and traffic have moved onto mobile networks, further price cuts have become possible. This has ensured the fixed-to-mobile shift has meant a net revenue loss to the sector. In addition to the substitution threat posed by wireless services, fixed revenue has been undermined by service innovations such

as naked DSL and VoIP. These new services deliver internet access and fixed voice at a much lower cost to users, in effect absorbing operator revenue. The new technologies have been pioneered by small telcos who are yet to have an established subscriber base and have developed business models around the new technology. Dominant providers are remiss to offer new technology as they greatly reduce the life cycle of traditional, high margin, telecommunications services. Industry blended ARPU has declined over the last five years, as the price of services across all infrastructures has reduced as operators compete to retain subscriber share.

The sizable declines in pricing have placed pressure on margins. To ease the load, many companies have engaged in merger and acquisition activity to build scale and realise efficiencies. Infrastructure owners have purchased wholesale clients, Vodafone and Hutchison merged and some resellers have bought infrastructure owners. Alternatively, many small operators have exited the sector as margin pressures have taken their toll. In all, the sector has been through a significant shakeout that has improved its productiveness. A larger number of medium-to-large operators eased the sector’s labour burden. By the end of 2010-11, sector employment is expected to be down 15.2% on 2005-06, which has dropped the total wage cost 18.4% lower.

Telcos have continued their investment in additional and upgraded infrastructure over the past five years. However, the majority of investment was undertaken early in the period, prior to the economic downturn. Infrastructure upgrades have included investment in DSLAMs, 3G technology and fixed-network builds. While Telstra has just finished upgrading its HFC network with Optus to follow, the bulk of depreciation charges will be felt from 2010-11. Ultimately, a marginal slowdown in investment in recent years caused depreciation as a percentage of revenue contract by 0.6 percentage points to

This industry is declining

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 13

Industry Performance

Industry Life Cyclecontinued

16.2% over the five years.With profit, wages and depreciation

all on the slide, the sector’s economic contribution will have contracted over the five-year period. IBISWorld expects the decline in sector value added will average 1.0% per annum. This will compare with annualised GDP growth of 2.9% and will see the sector’s share of the economy slide to 1.39% in 2010-11. The divergent direction in sector value added and GDP is indicative of a sector in decline.

Over the coming five years, the Telecommunications Services sector will

shift back into growth. Sector revenue gains will increase as demand booms with the arrival of the latest network technologies – 4G and FTTH. Skyrocketing demand will necessitate an increase in sector employment and wages. Greater infrastructure investment will yield higher depreciation as a share of revenue. While margins from traditional services will decline, absolute profit will increase and there will be a multitude of new value-added services, which will give many telcos the opportunity to reinvent their business model to improve margins.

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 14

Products & Services Mobile carriers usurped wired carriers as the dominant industry within the Telecommunications Services sector in 2007. Since that time, mobile services have continued to assert their dominance in the overall sector, forecast to account for 46.6% of total revenue in 2011-12. The mobile market has benefited from the changing behaviour and preference of consumers as they have shifted consumption from wired to mobile voice. This trend has been driven by the greater convenience of mobility and rapid declines in prices for mobile voice. It has become cheaper for many consumers to disconnect their landlines and rely solely on their mobiles for voice services. The fixed-to-mobile substitution trend that has accelerated the decline of the Wired Telecommunications Carriers industry is also being felt in the internet space. Since 2007-08, the number of fixed internet connections has declined as mobile internet surged and stole some of the market.

Despite the continual decline in

demand for wired voice services, the wired services segment still accounts for a sizeable portion of telecommunications consumption. For 2011-12, the wired services will account for 29.6% of sector revenue, a 14 percentage point drop from the 44% proportion in 2005. This is because this service segment includes line access and fixed data services. Line access still generates a lot of revenue, forecast to account for 36% of wired revenue, because the majority of fixed internet connections depend on a wired access line. However, line access revenue is set to crash over the next few years as naked internet connections become more common. Fixed data services are becoming an increasingly important part of the wired services segment as businesses become more dependent on data networks for running their daily operations.

The provision of fixed internet services is the next-largest service segment in the Telecommunications Services sector. The fixed internet services market enjoyed

KEy buyING INduSTrIES

G5000 Consumer Goods retail in Australia Retailers are becoming more reliant on telecommunication services in running both brick-and-mortar and online channels.

K7300 Finance in Australia Finance companies are big consumers of telecommunication services. This is demonstrated by the sizable contracts signed by the big banks (e.g. $100 million per annum).

L7800 business Services in Australia The property and business service industries are a key user of services provided by the various components of the Telecommunications sector.

N Education Australia’s education institutions are becoming increasing dependant on telecommunications in delivering services.

O8600 Health Services in Australia Currently, health providers are only small consumers of telecommunications services. However, the establishment of next generation networks will unlock a plethora of e-health applications.

X0016 Integrated Logistics in Australia Logistics operators use telecommunications services in performing a number of functions including fleet management and load tracking.

KEy SELLING INduSTrIES

J7100 Telecommunications Services in Australia Industry participants are heavily dependent upon the infrastructure and services provided by other participants.

Products & MarketsSupply Chain | Products & Services | demand determinants Major Markets | International Trade | business Locations

Supply Chain

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 15

Products & Markets

Products & Servicescontinued

rapid growth in the decade through 2007-08; its revenue proportion increased from just 2.0% in 1998 to 14.5% of total sector revenue in 2008. However, toward the end of the five years through 2010-11, revenue growth slowed, improving by just 0.6 percentage points to 15.1% of total revenue in 2011-12. The subdued revenue growth is a result of the increased substitution threat from advanced 3G wireless internet. In 2007-08 and 2008-09, the number of wireless subscribers jumped 3.7% and 2.4% respectively. Meanwhile, the number of fixed connections contracted 0.8% and 4.0% in these years. Big improvements in wireless network speeds have made it possible for many consumers and small businesses to rely on a mobile internet connection. Mobile connections are much more convenient than fixed connections, as not only do they enable mobility but they are portable (i.e. when a consumer moves house they do not have to move the connection).

The fixed versus mobile internet battle is set to heat up over the next five years as the availability of mobile tethering increases. The upside of tethering is that it gives consumers and small businesses the opportunity to access all

telecommunications services via one contract and device. The outcomes are greater convenience and cost savings. Once 4G services arrive, consumers and small businesses will get access to super-fast connectivity, making mobile internet a more attractive offering to a larger portion of the market. The one problem with mobile internet is the capacity constraints faced by the network. This means the usage prices for mobile connections increase much faster than fixed. Thus, for heavy internet users, a fixed connection will always be more cost effective.

The remainder of sector revenue is derived from telco resellers and satellite, TV and radio relay providers. Both segments are becoming niche players in the overall Telecommunications Services sector. Resellers have seen their sector revenue share deteriorate as infrastructure owners have focussed on increasing their own subscriber bases, where previously they had been happy to resell a higher proportion of unprofitable consumers. This has resulted in resellers’ market share contracting by 2.7 percentage points, forecast to account for just 6.9% of total telecommunications revenue in 2011-12.

Products and services segmentation (2011-12)

Total $40.8bn

46.6%Mobile services

29.6%Wired services

15.1%Fixed internet services

6.9%Resellers

1.8%Satellite, TV and radio relay

SOURCE: WWW.IBISWORLD.COM.AU

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 16

Products & Markets

demanddeterminants

Demand determinants outline the various factors that stimulate or reduce the demand for services supplied by this sector.

Each industry within the Telecommunications Services sector has its demand influenced by the over-riding economic conditions. Consumer demand is largely a function of employment levels, household disposable incomes, taxes and interest rates. An increase in household disposable income is likely to result in an increase in household consumption for telecommunications services, with mobile telecommunications carriers and internet service providers having the greatest capacity to absorb an increase in demand given that consumers can move to higher and more expensive usage plans. The overall consumer demand for telecommunications services is relatively resistant to the economic conditions, but it is the service mix of the demand that is influenced. The correlation of higher income to increased demand in other telecommunication industries, such as wired telecommunications, is not as high.

Business demand is largely a function of economic activity, the state and health of the industry in which the company operates in and company profitability. A general increase in economic activity tends to correlate with increased demand for telecommunications services. A company that is performing well is also more likely to invest in more advanced telecommunications such as dedicated high-speed internet services, IP-based digital phone systems and in some cases, satellite telecommunications, which offer ubiquitous coverage as opposed to terrestrially based networks.

Perceived valuePrice is a key demand determinant for household users of telecommunications services. Lower, or falling, prices lead to an increase in consumer demand and are the key reason in the increased Australian mobile penetration over the last five years. A new service is initially priced at premium rates but as the

service gains subscribers the price contracts until a critical point is reached that fosters mass adoption amongst consumers. Similarly, with entry level broadband prices having fallen considerably over the past five years there has been rapid substitution from dial-up to broadband services within the existing subscriber market as well as the uptake of broadband internet by new customers. Overall this has seen strong internet subscriber growth over the last five years.

Business customers are less sensitive to price reductions, though it is important, particularly for those companies that have a large workforce. Business customers favour the level and quality of service as opposed to price, the inferior quality of initial VoIP offerings in comparison with traditional voice mediums has been the major factor in businesses not adopting the cheaper VoIP product.

Advanced technologyTechnological advances enable the introduction of new, or advancements in existing services. The continual improvement to services flows through to increase demand across all key market segments. The introduction of ADSL2+ services, which offer broadband internet speeds of up to 24 Mbps, has resulted in an increase in demand in the Internet Service Providers industry, whilst the Mobile Telecommunications Carriers industry growth has been re-invigorated by the introduction of 3G services. The Mobile Telecommunications Carriers industry is heavily marketing advanced 3G services, whilst the once dominant second generation technology is somewhat forgotten and will be phased out in the future. Enhancements of

Demand is affected by the introduction of new services and enhancement of existing services

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 17

Products & Markets

existing services and technologies such as moving from PABX phone systems to digitally-based services and video conferencing as opposed to telephone hook-ups will also result in increased demand for sector services. The Satellite, Television and Radio Relay Operations industry has benefited from the concurrent transmission of digital and analogue services; however the ideal environment will come to an end in 2013 when analogue TV transmission ceases.

Availability of servicesDemand for telecommunications services is also a function of supply. Presently, not all Australians have access to broadband internet services and a smaller proportion of the population are not covered by any of the terrestrially-based mobile telecommunications networks. Although availability of services may depend on investment principles or government assistant, an increase in coverage will increase demand.

demanddeterminantscontinued

Major Markets Households are estimated to account for 67.7% of the total market for telecommunication services. The overall market share accounted for by households varies considerably between industries. Households are the major market in the wired, mobile and ISP industries. In contrast, households are reported to account for only a small proportion of the market for telecommunication resellers and satellite, TV and radio relay operators.

Corporate clients are expected to account for 27.5% of sector revenue. This largely includes demand for services from a broad range of divisions such as Finance and Insurance, Manufacturing, Retail Trade, Wholesale Trade and

Property and Business Services. Analysis suggests that satellite, TV and radio relay operators rely heaviest on the corporate market. This is because their industry is upstream from telecommunication carriers and broadcasters and therefore gains a large proportion of its revenue from businesses.

Government is expected to account for 4.8% of the demand for services provided by this sector. Satellite, TV and radio relay operators depend on the government market for a sizeable share of their revenue. Their industry provides services to the ABC and SBS in particular. The government segment is usually fairly stable.

Major market segmentation (2011-12)

Total $40.8bn

67.7%Households

27.5%Corporate clients

4.8%Government

SOURCE: WWW.IBISWORLD.COM.AU

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 18

Products & Markets

International Trade Domestic and international markets examine the import source and export destination for services supplied by this sector. For the Telecommunications Services sector, it represents the value of termination fees incurred by domestic carriers overseas and foreign carriers domestically. Increased competitiveness has put downward pressure on prices. So while international traffic volumes have

increased, the value of exports and imports is believed to have changed little over the past decade. IBISWorld anticipates that the current trend of low trade levels for services provided by this sector will persist over the next five years. Ultimately, the Telecommunications Services sector provides services to the Australian economy so international trade is not a focus of operators.

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 19

Products & Markets

SOURCE: WWW.IBISWORLD.COM.AU

TAS1.4

wA9.4

QLd17.3

VIC27.6

NSw35.6

NT1.1

SA6.2

ACT1.4

Employment (%)

Cold Zone (<10) <25 <50 Hot Zone (<100) Not applicable

business Locations 2011-12

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 20

Products & Markets

business Locations The geographic distribution of the Telecommunications Services sector is relatively consistent with the population distribution of the nation, although there are some notable contrasts. The biggest divergence between employment share and population share is in New South Wales. It is expected that New South Wales is to account for about 35.6% of total sector employment compared to a population share of 32.4%, implying higher employment on a per capita basis. Employment share in New South Wales has been declining due to higher sector employment in Queensland and Western Australia. Despite this, sector employment in these states will still be lower than their respective population shares. This is because the head offices of telecommunications companies tend to be in Victoria and New South Wales.

A greater concentration of head offices means Victoria and New South Wales exhibit a disproportionately high share of wages. This is because higher earning roles such as senior management and executives are located at head offices. So a higher average wage means a greater overall share of wages. IBISWorld

believes Western Australia has the lowest average wage. This is particularly notable given that state had the lowest unemployment level in the country, which generally puts upward pressure on wages. Ultimately, it suggests the majority of employment within Western Australia is focused on customer service, sales and administration functions instead of head-office tasks.

Perc

enta

ge

40

0

10

20

30

WA

ACT

NSW N

T

QLD SA TA

S

VIC

EmploymentPopulation

Distribution of employment vs. population

SOURCE: WWW.IBISWORLD.COM.AU

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 21

Key Success Factors Having an extensive distribution/collection networkAn exhaustive distribution network (or access to it), via an extensive infrastructure network, is a key factor to the success of the organisation.

Development of new productsDeveloping value-added products beyond the traditional market is critical in retaining and growing market share.

Ability to raise revenue from additional sourcesThe traditional products and markets are entering decline, so large telcos will need to reinvent themselves and look to new revenue streams.

Understanding government policies and their implicationsRegulations and government policies relating to the industry have changed and are changing significantly. This

affects many variables, including competition and pricing.

Economies of scaleFor industry participants, gaining economies of scale helps to reduce the cost of doing business, which contributes to higher profit margins.

Having contacts within key marketsThe development of strategic alliances with major end user industries, such as pay-TV, electronic commerce providers and other online service providers, is important.

Undertaking technical research and developmentBusinesses need to undertake research and development to ensure the organisation meets world best practice in operational efficiency and delivering the service.

Market Share Concentration

The Telecommunications Services sector has a high level of concentration with the top three major companies accounting for over 80% of revenue. The sector previously had four major players, but the third and fourth largest players, Vodafone and Hutchison, merged operations in 2009. There is a large gulf between the next level of second tier telcos. The high level of concentration can largely be attributed to Telstra, which has held onto around 50% of the market over the last five years. The challenger, Optus, has market share less than half of Telstra’s.

Telstra’s sector dominance ultimately lies in the company’s incumbency. Being an integrated service provider with ownership over the PSTN has placed the telco at considerable advantage. This is why Telstra’s share of the sector has remained virtually unchanged over the past five years, despite the best efforts of a host of competitors.

While the sector as a whole is regarded as highly concentrated, levels do vary between various industries. For example, the Telecommunications Resellers industry has a low level of concentration, especially as Optus gradually exits the industry. Alternatively, the Mobile Telecommunications Carriers industry has an extremely high level of concentration, with the top three players accounting for over 99% of revenue.

Competitive LandscapeMarket Share Concentration | Key Success Factors | Cost Structure benchmarks basis of Competition | barriers to Entry | Industry Globalisation

Concentration by industry

IndustryTop four share

(%)Concentration

(index)

Wired 93.7 HighMobile 99.6 HighResellers 31.5 LowISPs 63.4 MediumSatellite & other 88.8 High

SOURCE: IBISWORLD

Level Concentration in this industry is High

IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 22

Competitive Landscape

Cost Structure benchmarks

The Telecommunications Services sector cost structure largely reflects that of the infrastructure owners. The industries are dominated by the infrastructure owners and as such the overall sector mirrors the infrastructure performance, in that the sector achieves a high profit margin and incurs considerable depreciation and interest expense. The only industry in the sector that does not own and operate infrastructure is the relatively small Telecommunications Resellers industry. Resellers purchase wholesale capacity on the networks of other industries to then resell services to businesses and consumers. So for resellers, depreciation, interest and profit tend to represent a small share of revenue.

ProfitabilityTelecommunications companies require, and have been able to achieve, impressive profit margins due to the significant risk that they take on via the substantial initial, and the ongoing, investment in building, operating, maintaining and upgrading network infrastructure. Such investment comes with a high level of risk not only because the sums invested, but also the long return timeliness. This substantial investment risk then attracts a relatively high weighted average cost of capital (WACC), which necessitates sizeable profit margins. This year, IBISWorld expects the Telecommunications Services sector to achieve a profit margin of 14.9%, with a tax bill of 4.2% of revenue. The profit margin will be down 0.25 percentage points on the previous year and will reflect profit erosion in both wired and mobile services. In line with its low capital investment, the Telecommunications Resellers industry tends to generate the lowest margins at about 5.0%.

Access chargesThe largest expense for Telecommunications Services sector participants is the cost of services. This cost represents access charges, interconnection fees, USO fees and termination charges. This year, this is

expected to account for 31.4% of sector revenue. Resellers spend the most on the cost of services because they have to purchase network capacity. ISPs also spend heavily on this item as they must pay for using a carrier’s network (e.g. the PSTN and internet backbone). This is important considering that 95% of ISPs do not own infrastructure.

DepreciationThe sector’s heavy investment in infrastructure means it incurs large depreciation costs. Network investment is ongoing because operators must upgrade their networks with the latest technology developments. This is particularly the case in the mobile and internet services markets where there has been rapid technology innovation. Over the past decade, telcos have also invested in IT systems to automate a large number of administrative and processing functions. IBISWorld expects depreciation charges to account for 16.5% of revenue. Over the next decade, the sector’s proportional depreciation expense is expected to increase in line with the NBN roll out, expected 4G network builds and ongoing HFC investments.

Finance costsThe substantial costs associated with network builds are generally facilitated by debt. This means the sector has considerable costs allocated to the financing of said debt. This year, the sector’s interest expense will decrease by 0.4 percentage points to an expected 3.1% of revenue as major players benefit from the reduced interest rates and halt in investment that occurred as a result of the economic downturn. The biggest spenders on financing are the satellite and radio relay operators. These companies are particularly dependant on debt for financing their investment activities. Alternatively, resellers spend the least on interest because they only have small investment requirements.

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 23

Competitive Landscape

Cost Structure benchmarkscontinued

Labour forceDespite being capital intensive, success in the Telecommunications Services sector relies on a large labour force and as such labour remains a key cost to the sector. Critical functions such as sales, marketing, customer service, accountant administration and network maintenance depend on labour. However, over the past decade the labour intensiveness of a number of these functions (e.g. accounts and customer service) has fallen due to investment in automation technology. Moreover, ongoing merger and acquisition activity has facilitated more productive use of labour. Consequently, sector employment has declined and this

has seen the sector’s proportional wage expense fall.

Other expensesAdvertising expenses vary between competitors and varies from 1.0% to 4.0% of revenue. Big spenders on marketing include iiNet, SP Telemedia (owner of Soul and TPG), VHA, Telstra and Optus. While Telstra and Optus spend the most, these companies get to spread this spending over a much larger revenue base. Other operating expenses that are significant include purchase costs, repairs and maintenance, legal expenses, bad debts, leasing expenses, vehicle and travelling expenses and tax.

Sector vs. Industry Costs

■ Profi t■ rent■ utilities■ depreciation■ Other■ wages■ Purchases

Average costs of all industries in

sector (2011-12)Industry costs

(2011-12)

0

20

40

60

Perc

enta

ge o

f rev

enue

80

100

12.2

9.2

15.0

47.3

14.40.51.4

14.9

6.611.6

46.6

16.51.52.3

SOURCE: WWW.IBISWORLD.COM.AU

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 24

Competitive Landscape

basis of Competition Over the past five years, competition within the Telecommunications Services sector has greatly intensified. The commoditisation of key industry services has lead to price being the major competition basis. Because competition is primarily price-based, it has become increasingly important for companies in the sector to have large-scale operations in order to remain profitable. This was the catalyst for a spate of merger and acquisition activity within the Internet Service Providers industry that has seen the number of second-tier players expand with the emergence of SP Telemedia and iiNet. The merger and acquisition activity and creation of a number of larger players with more scale has further fuelled competition in the growing ISP market. Meanwhile, the Vodafone-Hutchison (VHA) merger in the Mobile Telecommunications Carriers industry means that the top three carriers will be able to compete due to their large scale of operations. The Wired Telecommunications Carriers industry, historically dominated by Telstra’s PSTN will also face increased competition once the National Broadband Network arrives; competition in wired will be transformed.

The major basis in which telecommunication companies compete is on the basis of price. The fixed-to-mobile substitution shift has been primarily driven by improved pricing position offered by mobile carriers. However, service quality in the form of coverage and product innovation in the form of value-added services has become increasingly important. Price is the critical factor because it is often difficult to differentiate between services that are becoming commoditised. The most common form of pricing strategy, initially implemented by mobile carriers but later adopted across the board, is the cap (or bucket) plan. These plans offer users a defined usage limit for a particular monthly fee. In the past five years, the value of the caps has increased to attract additional subscribers. So pricing changes can be a change in the cap service value or in the cap price.

The primary means for differentiating services is on quality: speed, coverage and reliability. Speed is increasing in importance as the sector transitions towards a digital data-based network. Subscribers have changed the product preference and now prefer to access more sophisticated web content and services such as video, IPTV, social networking, online gaming and innovative e-commerce. These applications require greater downlink speeds to attain usability, but at the same time they place a much larger strain on the overall network performance. Telcos are set to place even greater emphasis on speed (and network capacity) over the next five years as more services become IP based. High speed, high capacity networks will be necessary for enabling the multitude of innovative, web-based services that are being developed for businesses.

Advancements in network and device technology are enabling rapid product and service innovation. For telcos, being first to market with innovation can represent a significant competitive advantage. Optus’ iPhone play exemplifies this dynamic where it was able to leverage the success of the iPhone as a means of increasing its mobile market share. Also, iiNet is attempting to win with a first to market product-service innovation bundle in the ISP market with the release of ‘BoB’ (i.e. broadband in a box). The building of the NBN and eventual move to 4G will further intensify internal competition as the boundaries between historically distinct services are removed. The Telecommunications Services is trending toward a utility type service, high volume but low margin, which will see service innovation become the key to differentiation and to the ability of a participant to maintain strong margins.

Novel marketing and service packaging

Level & Trend Competition in this industry is Medium and the trend is Increasing

Competition between service providers is primarily based on price

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 25

Competitive Landscape

basis of Competitioncontinued

is also becoming an increasingly significant competitive point as players offer integrated combinations of the latest products and services to encourage customers to become multi-product users. Marketing strategies that focus on cross selling products can enable players to make the most of their subscriber base. A number of players have also cited the

importance of branding as a means of achieving differentiation. For example, Optus, an established telecommunications player, has invested substantial resources into developing the Optus brand, believing it to be a significant variable in customer acquisition and retention across most customer segments.

barriers to Entry Barriers to entry outline the factors that limit a company from entering the market. Key barriers to entry to the Telecommunications Services sector include economies of scale, capital intensity, service differentiation, distribution networks and licences. The barriers to entry in the Telecommunications Services sector are high, despite extensive deregulation of the past 15 years.

Despite the radical changes that have occurred in the regulatory backdrop of the Telecommunications Services sector, there still exists a number of barriers to entry that are inherent characteristics of the telecommunications market. For example, a network operator must build, upgrade and maintain network infrastructure. Doing so is very capital intensive and involves an extremely high level of sunk costs. The potential for new network operators is limited to well capitalised firms.

Other barriers revolve around the established position of the previous statutory monopoly. As has been found in a number of other countries that have recently liberalised their telecommunication sectors, these incumbents still maintain a large market share in many facets of the sector despite the regulatory changes that have occurred. For example, incumbents enjoy considerable cost advantages arising from economies of scale and scope. They also in effect still maintain control of essential or bottleneck facilities. Telstra and Singtel Optus are still thought to account for over 90% of fixed-line service revenue and more than 70% of the

mobile market. The issue of access rights and declared services for new entrants is of paramount importance.

Barriers to entry will vary between the various segments of the Telecommunications Services sector. For example, barriers to entry for switched service providers in the IDD (international direct dialling) market segment are lower than the local call market as a result of lower interconnection costs and more concentrated call patterns. There has also been a creation of new niches in the reseller market.

A significant issue determining the ease of entry into mobile markets is the availability of spectrum. Importantly, spectrum availability determines the number of carriers that can be licensed. With the merging of Vodafone and Hutchison, there are now just three network operators that account for over 99% of the Mobile Telecommunications Carriers industry. The potential for new entrants within the industry is limited to niche satellite services. The scarcity of available spectrum is flowing through as an increased barrier to the Telecommunications Resellers industry. Previously, network operators had wholesaled excess spectrum to resellers who would be able to better service particular markets, but as bandwidth use intensifies mobile operators are buying out mobile virtual network operators and amalgamating the subscriber base onto their own networks.

Entry into the Internet Service Protocol industry was historically relatively easy, evidenced the

Level & Trend Barriers to Entry in this industry are High and Steady

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 26

Competitive Landscape

Industry Globalisation

Globalisation measures the extent to which this sector operates on a global scale. IBISWorld classifies the Telecommunications Services sector as operating at a medium level of globalisation. This is mainly because foreign operators are heavily involved within the domestic telecommunications market.

Foreign ownership concentration has increased over the past decade. Of the top ten players, five are foreign owned: Optus, VHA, TCNZ (AAPT), Primus and Broadcast Australia. The first three of these companies represent the three largest operators in the Telecommunications Services sector behind Telstra. Combined, these telcos are expected to account for 36.2% of sector revenue.

Telstra remains the dominant telecommunications provider. Telstra is majority Australian owned and the

government still holds a sizable stake via the Future Fund. Telstra will remain Australian given that there are foreign ownership restrictions in place. Many of the smaller sector enterprises are domestically owned and operated.

A number of industries in this sector support Australian owned operators that earn the majority of their sales from domestic activity. The dominant telecommunication provider in Australia, Telstra, has operations in New Zealand and some Asian countries. However, revenue derived from these businesses account for less than 10% of Telstra’s

barriers to Entrycontinued

comparatively low level of industry concentration and high number of small ISPs operating in the market. However, becoming a financial success and winning subscribers from well-established players such as Telstra and Optus is difficult. As competition intensifies in this industry, the need for innovative marketing and pricing campaigns to win subscribers is increasing. Effective marketing can be resource intensive and the success of material price cuts ultimately depends on providing quality customer service in order to reduce subscriber churn (i.e. to retain won customers). There are significant scale economies that can be realised in the provision of customer service, which gives large ISPs a significant advantage and this has resulted in the level of competition within the industry increase. Smaller players are merging operations to give themselves a fighting chance of competing with the major ISPs.

With convergence being a major characteristic of the

Telecommunications Services sector in general, there is a growing need for business alliances and strategic partnerships to take advantage of convergence trends. To attract partners to deliver inter-connected information and communication services, telcos must be provide the partner with access to a large enough group of profitable customers that the investment in the partnership is worthwhile. Again this favours the larger telcos, many of which have already established alliances and strategic partnerships with information and communication companies.

barriers to Entry checklist Level

Competition MediumConcentration HighLife cycle stage DeclineCapital intensity HighTechnology change HighRegulation and policy HeavyIndustry assistance Medium

SOURCE: WWW.IBISWORLD.COM.AU

Most operators derive little revenue in foreign markets, but three of the four biggest telcos are foreign-owned

Level & Trend Globalisation in this industry is Medium and the trend is Increasing

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 27

Competitive Landscape

Industry Globalisationcontinued

total company revenue. Other players also have operations in foreign countries, however, these business also account for only a small portion of company revenue.

In analysing the level of globalisation in the Telecommunications Services sector, it is important to note the worldwide trend towards cross-border

investments in global telecommunications. In accordance with the WTO’s General Agreement in Trade in Services, a number of countries have liberalised markets and investment in telecommunications. In the short term, IBISWorld anticipates the level of sector globalisation will continue to rise.

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 28

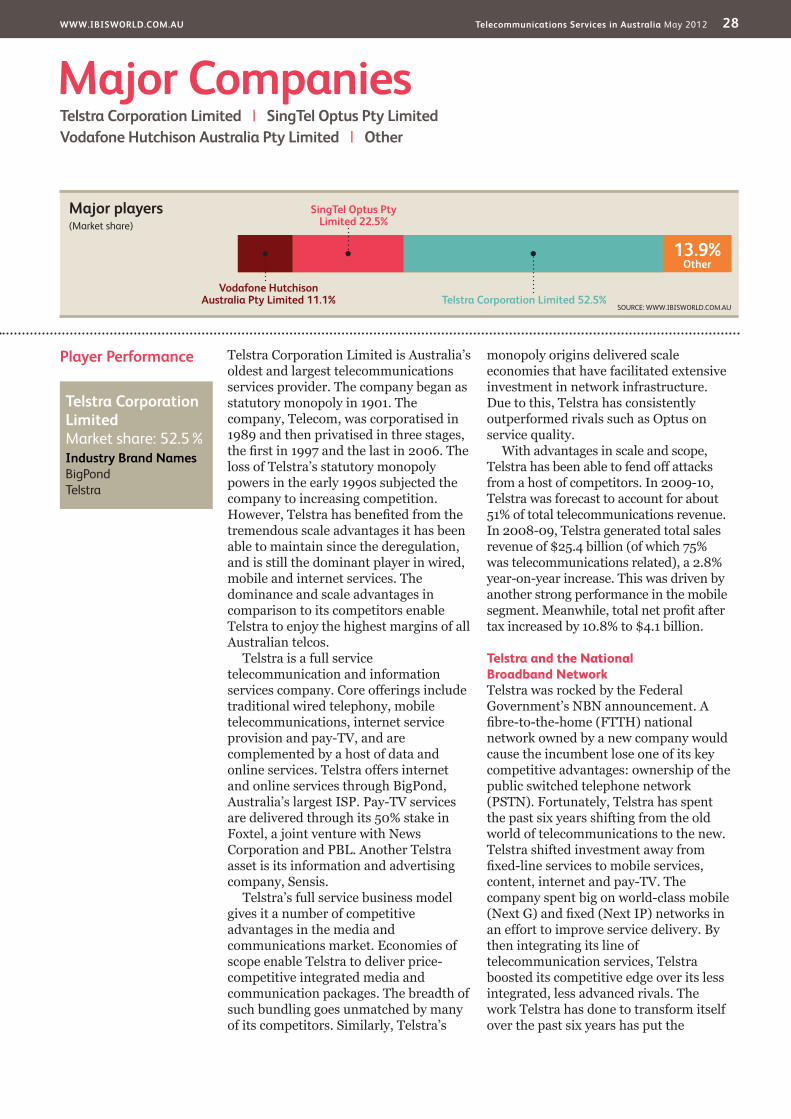

Player Performance Telstra Corporation Limited is Australia’s oldest and largest telecommunications services provider. The company began as statutory monopoly in 1901. The company, Telecom, was corporatised in 1989 and then privatised in three stages, the first in 1997 and the last in 2006. The loss of Telstra’s statutory monopoly powers in the early 1990s subjected the company to increasing competition. However, Telstra has benefited from the tremendous scale advantages it has been able to maintain since the deregulation, and is still the dominant player in wired, mobile and internet services. The dominance and scale advantages in comparison to its competitors enable Telstra to enjoy the highest margins of all Australian telcos.

Telstra is a full service telecommunication and information services company. Core offerings include traditional wired telephony, mobile telecommunications, internet service provision and pay-TV, and are complemented by a host of data and online services. Telstra offers internet and online services through BigPond, Australia’s largest ISP. Pay-TV services are delivered through its 50% stake in Foxtel, a joint venture with News Corporation and PBL. Another Telstra asset is its information and advertising company, Sensis.

Telstra’s full service business model gives it a number of competitive advantages in the media and communications market. Economies of scope enable Telstra to deliver price-competitive integrated media and communication packages. The breadth of such bundling goes unmatched by many of its competitors. Similarly, Telstra’s

monopoly origins delivered scale economies that have facilitated extensive investment in network infrastructure. Due to this, Telstra has consistently outperformed rivals such as Optus on service quality.

With advantages in scale and scope, Telstra has been able to fend off attacks from a host of competitors. In 2009-10, Telstra was forecast to account for about 51% of total telecommunications revenue. In 2008-09, Telstra generated total sales revenue of $25.4 billion (of which 75% was telecommunications related), a 2.8% year-on-year increase. This was driven by another strong performance in the mobile segment. Meanwhile, total net profit after tax increased by 10.8% to $4.1 billion.

Telstra and the National Broadband NetworkTelstra was rocked by the Federal Government’s NBN announcement. A fibre-to-the-home (FTTH) national network owned by a new company would cause the incumbent lose one of its key competitive advantages: ownership of the public switched telephone network (PSTN). Fortunately, Telstra has spent the past six years shifting from the old world of telecommunications to the new. Telstra shifted investment away from fixed-line services to mobile services, content, internet and pay-TV. The company spent big on world-class mobile (Next G) and fixed (Next IP) networks in an effort to improve service delivery. By then integrating its line of telecommunication services, Telstra boosted its competitive edge over its less integrated, less advanced rivals. The work Telstra has done to transform itself over the past six years has put the

Major CompaniesTelstra Corporation Limited | SingTel Optus Pty LimitedVodafone Hutchison Australia Pty Limited | Other

Major players(Market share)

13.9%Other

Telstra Corporation Limited 52.5%

SingTel Optus Pty Limited 22.5%

Vodafone Hutchison Australia Pty Limited 11.1%

SOURCE: WWW.IBISWORLD.COM.AU

Telstra Corporation Limited Market share: 52.5% Industry brand Names BigPond Telstra

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 29

Major Companies

Player Performancecontinued

company in the best position to deal with arrival of the NBN.

The announcement of the NBN forced Telstra to change its adversarial tact. The new CEO, David Thodey, has outlined Telstra’s intention to engage constructively with the government and the new NBN Co. in finding a solution that is in the best interests of the nation, while maintaining value for Telstra shareholders. Telstra and NBN Co. have released statements that show that the two organisations are in agreement that the PSTN will be phased out over time and replaced by the fibre network. This presents an interesting dilemma for Telstra because it will end up with only retail access to the NBN. With the finer details of the separation currently being worked out, David Thodey has shifted the focus to a fight about the value of the Telstra network rather than a fight about the structure of the company.

The NBN process has affected Telstra’s fixed-line investment strategy. In March 2009, Telstra announced it would spend $300 million over the year to upgrade its entire hybrid fibre-coaxial (HFC) network to deliver speeds of up to 100 Mbps. This followed the news the company had been excluded from the original NBN process. Importantly, 100 Mbps connectivity will match that of the NBN, with scope to accelerate speeds with further upgrades to 200 Mbps. Because such an investment could jeopardise the viability of the NBN, the Federal Government

considered coercing Telstra into divesting its HFC network and Foxtel. This would be a bold move as it would affect Telstra’s standing as an integrated telecommunications provider. Telstra then announced in October 2009 that it would no longer invest in ADSL2+ technology. This followed the 1,856th exchange upgrade to ADSL2+, extending these services to the majority of the population.

Fixed internet servicesTelstra BigPond is Australia’s largest ISP, with total fixed internet subscribers of 4.3 million in December 2009. Telstra’s fixed internet subscribers are dominated by broadband subscribers, 2.2 million out of its 4 million broadband subscribers are Telstra retail clients, with the remainder wholesaled to other ISPs.

Telstra’s average revenue per user (ARPU) for broadband services has been increasing since 2006-07, despite declining connection costs. To enjoy new web content and services, consumers have been migrating to premium high-speed ADSL2+ or super-fast cable plans with larger download limits.

The NBN will eventually erode Telstra’s speed and coverage advantages. There is the possibility that Telstra will cease to be an infrastructure owner altogether if the government forces it to sell its HFC assets. Telstra’s integrated retail business and significant telecommunications expertise would still

Telstra Corporation Limited (Australian telecommunication services segments) – fi nancial performance

yearrevenue ($ billion) (% change)

Operating Profi t ($ billion) (% change)

2006-07 20.4 n/C 4.9 n/C

2007-08 21.5 5.4 5.1 4.1

2008-09 21.8 1.4 5.5 7.8

2009-10 21.2 -2.8 5.4 -1.8

2010-11 21.8 2.8 4.8 -11.1

SOURCE: AnnUAL REPORT AnD IBISWORLD

www.IbISwOrLd.COM.Au Telecommunications Services in Australia May 2012 30

Major Companies

Player Performancecontinued

give the telco a broad-based competitive advantage. However, the playing field from an operational perspective would be levelled.